investors’ meeting -...

TRANSCRIPT

© 2006 Express Scripts, Inc.All Rights Reserved

INVESTORS’ MEETINGTempe, AZ

April 7, 2006

Our Pathways to Patients: Alignment in Action

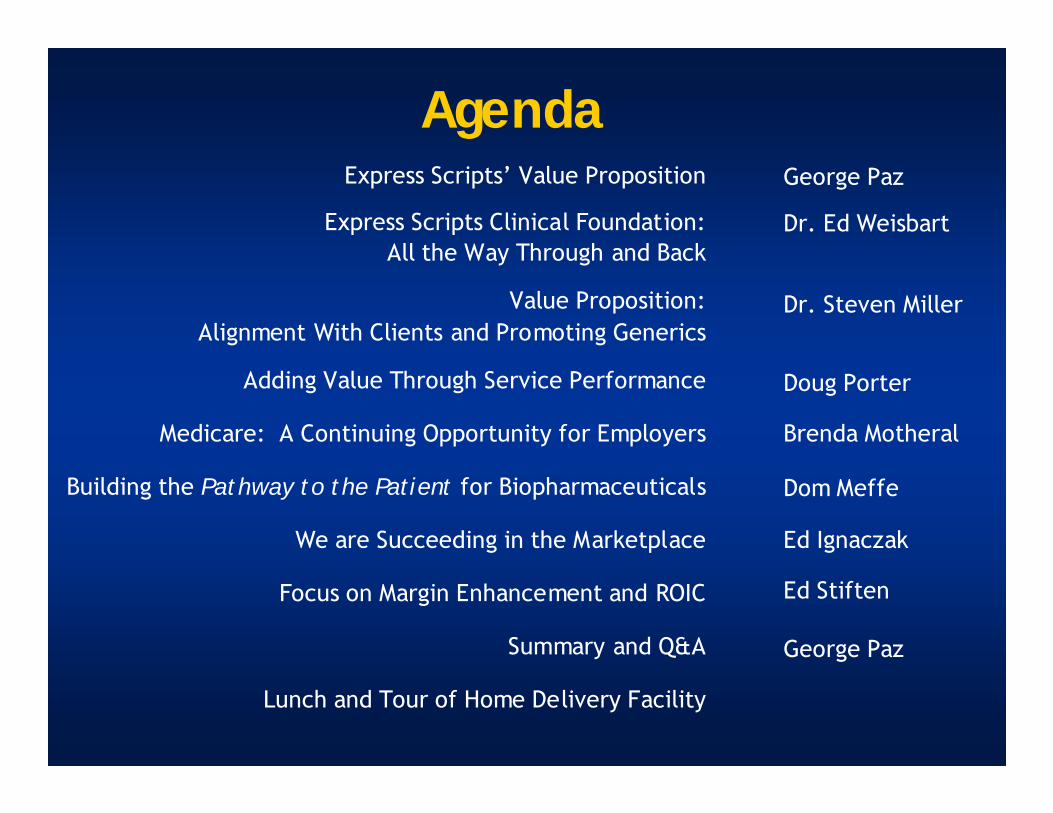

AgendaExpress Scripts’ Value Proposition

Express Scripts Clinical Foundation:All the Way Through and Back

Value Proposition:Alignment With Clients and Promoting Generics

Adding Value Through Service Performance

Medicare: A Continuing Opportunity for Employers

Building the Pathway to the Patient for Biopharmaceuticals

We are Succeeding in the Marketplace

Focus on Margin Enhancement and ROIC

Summary and Q&A

Lunch and Tour of Home Delivery Facility

George Paz

Dr. Ed Weisbart

Dr. Steven Miller

Doug Porter

Brenda Motheral

Dom Meffe

Ed Ignaczak

Ed Stiften

George Paz

© 2006 Express Scripts, Inc.All Rights Reserved 3

Statements included in this presentation or in the oral comments made as part of this presentation may contain forward-looking statements, including but not limited to statements of the Company’s plans, objectives, expectations or intentions, that involve risk and uncertainties.

The Company’s actual results may differ significantly from those projected or suggested in any forward-looking statement due to a variety of factors, which are discussed in detail in the Company’s filings with the Securities and Exchange Commission.

Forward-Looking Statements

© 2006 Express Scripts, Inc.All Rights Reserved

George PazPresident and CEO

Express Scripts’Value Proposition

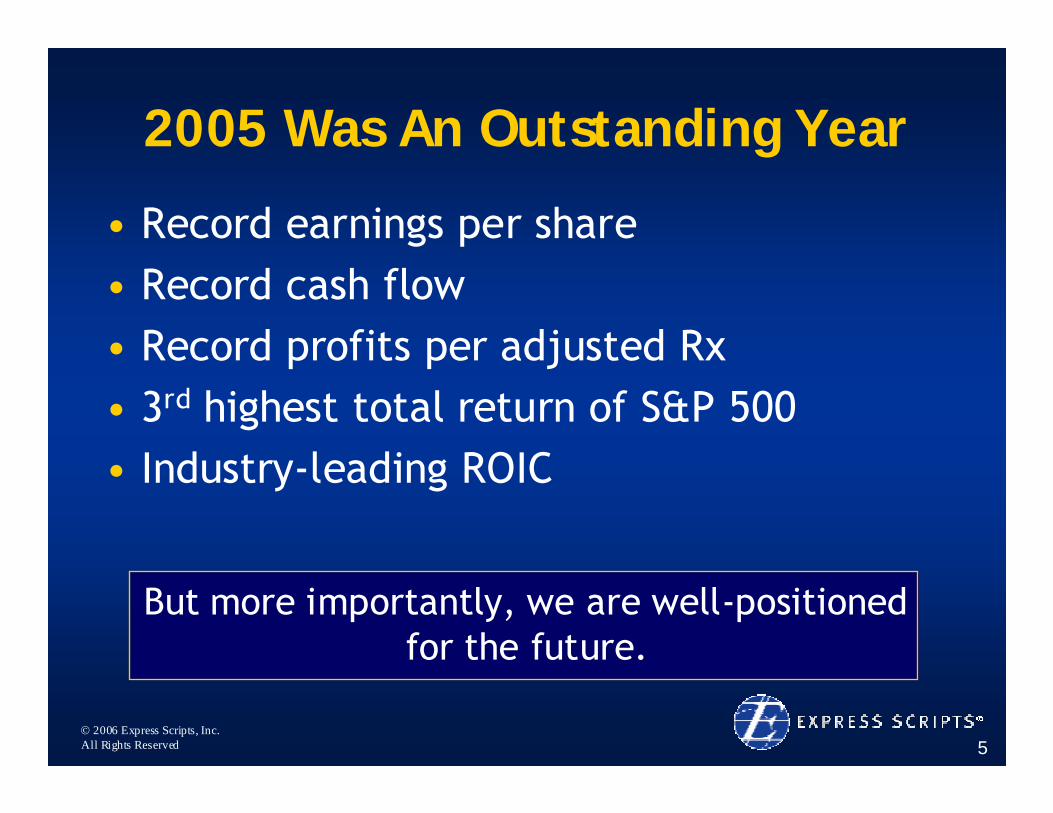

© 2006 Express Scripts, Inc.All Rights Reserved 5

2005 Was An Outstanding Year

• Record earnings per share• Record cash flow• Record profits per adjusted Rx• 3rd highest total return of S&P 500• Industry-leading ROIC

But more importantly, we are well-positioned for the future.

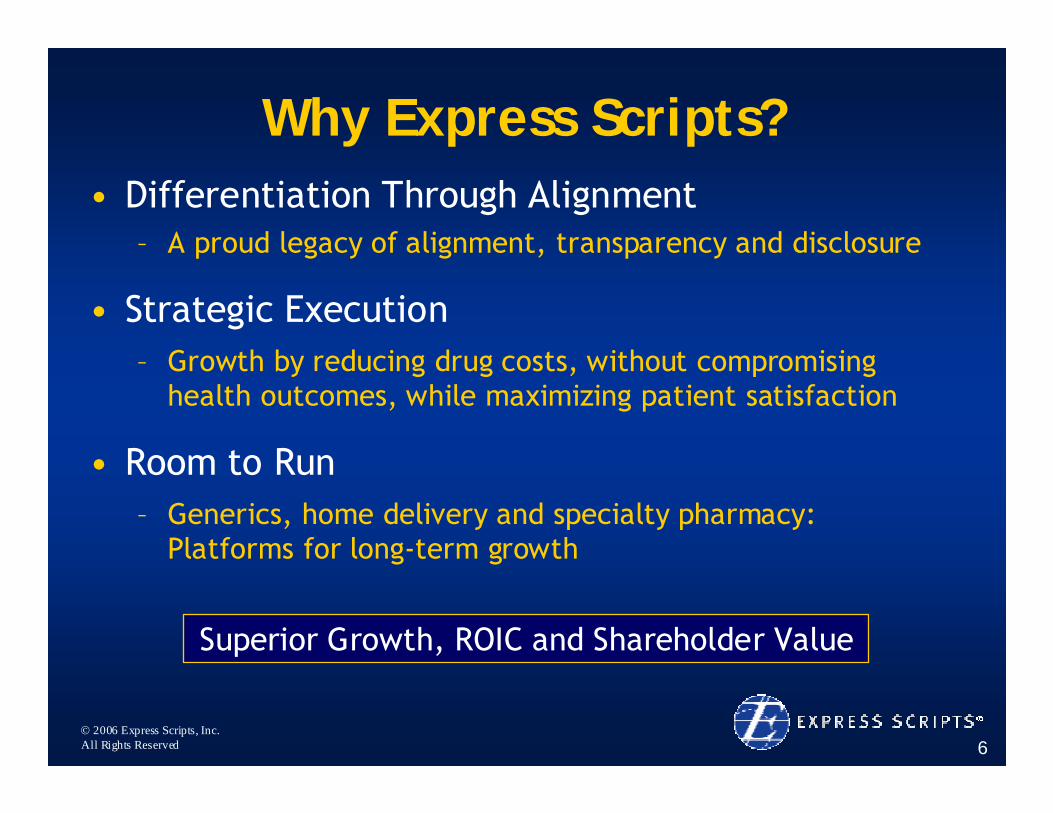

© 2006 Express Scripts, Inc.All Rights Reserved 6

Why Express Scripts?• Differentiation Through Alignment

– A proud legacy of alignment, transparency and disclosure

• Strategic Execution– Growth by reducing drug costs, without compromising

health outcomes, while maximizing patient satisfaction

• Room to Run– Generics, home delivery and specialty pharmacy:

Platforms for long-term growth

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved 7

Why Our Model Works?Alignment

Retail Non-Preferred Brand

Retail Preferred

Brand

GenericsHome Delivery

Increased SavingsOpportunities:

Client

Member

Increased

Profit

Opportunities:

Express Scripts

Moving to preferred brands, mail and generics

Moving to preferred brands, mail and generics

Moving to preferred brands, mail and generics

As We Save Our Clients Money, Our Performance Improves

© 2006 Express Scripts, Inc.All Rights Reserved 8

First and Foremost: Execution

• Record sales and retention

• Record patient and client satisfaction

• Record industry-leading generic use

• Industry-leading specialty platform

• Superior trend management

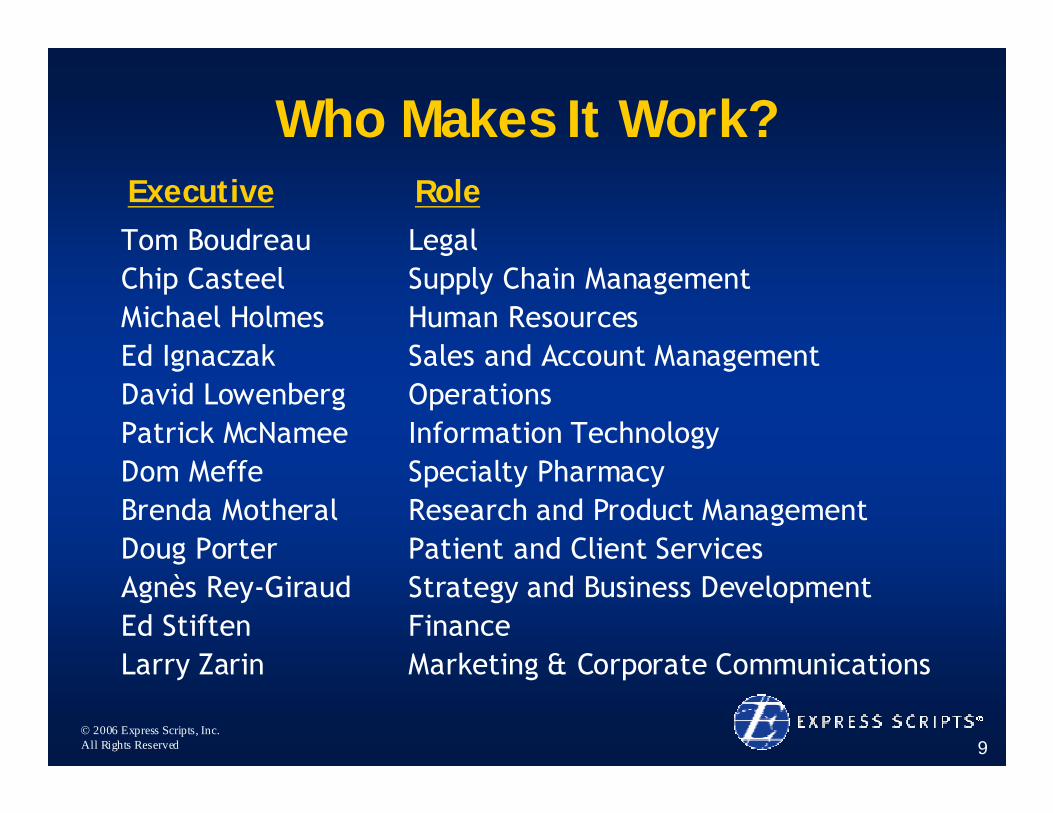

© 2006 Express Scripts, Inc.All Rights Reserved 9

Tom BoudreauChip CasteelMichael HolmesEd IgnaczakDavid LowenbergPatrick McNameeDom MeffeBrenda MotheralDoug PorterAgnès Rey-GiraudEd StiftenLarry Zarin

LegalSupply Chain ManagementHuman ResourcesSales and Account ManagementOperationsInformation TechnologySpecialty PharmacyResearch and Product ManagementPatient and Client ServicesStrategy and Business DevelopmentFinanceMarketing & Corporate Communications

Executive Role

Who Makes It Work?

© 2006 Express Scripts, Inc.All Rights Reserved 10

Today’s Discussion Topics

• Formulary management strategy

• Excellence in client and patient services

• Preparing for emerging markets

• Building the Pathway to the Patient for

biopharmaceuticals

• Sales and marketing success

• Enhancing margins and delivering superior ROIC andshareholder value

© 2006 Express Scripts, Inc.All Rights Reserved

Express Scripts Clinical Foundation: All The Way Through And Back

Ed Weisbart, MDChief Medical Officer

© 2006 Express Scripts, Inc.All Rights Reserved 12

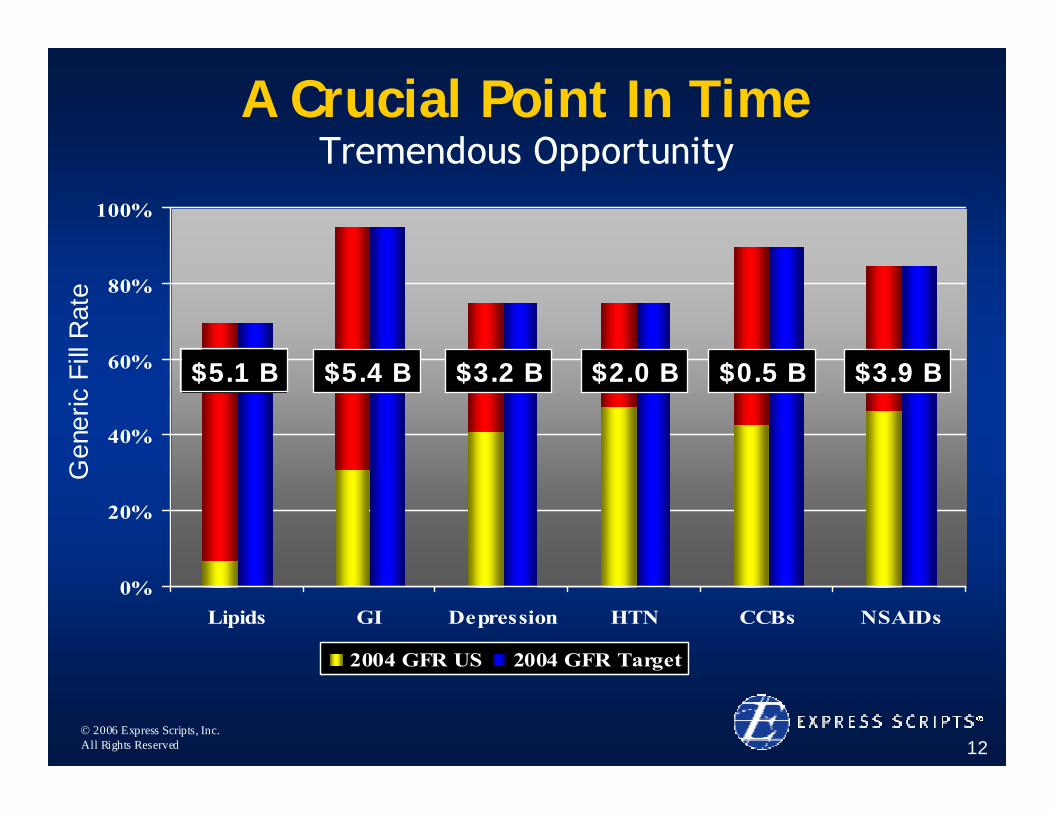

0%

20%

40%

60%

80%

100%

Lipids GI Depression HTN CCBs NSAIDs

2004 GFR US 2004 GFR Target

Gen

eric

Fill

Rat

eA Crucial Point In Time

Tremendous Opportunity

$5.1 B$5.1 B $5.4 B$5.4 B $3.2 B$3.2 B $2.0 B$2.0 B $0.5 B$0.5 B $3.9 B$3.9 B

© 2006 Express Scripts, Inc.All Rights Reserved 13

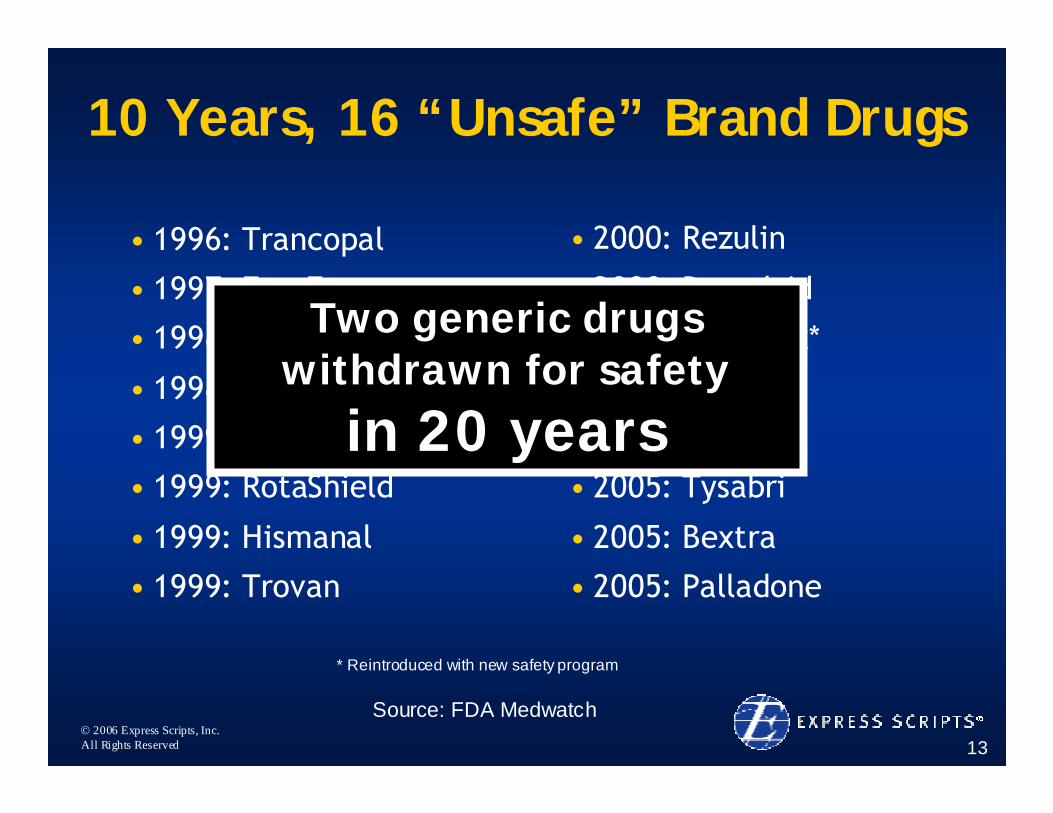

10 Years, 16 “Unsafe” Brand Drugs

• 1996: Trancopal

• 1997: Fen-Fen

• 1998: Duract

• 1998: Posicor

• 1999: Raxar

• 1999: RotaShield

• 1999: Hismanal

• 1999: Trovan

• 2000: Rezulin

• 2000: Propulsid

• 2000: Lotronex*

• 2001: Baycol

• 2004: Vioxx

• 2005: Tysabri

• 2005: Bextra

• 2005: Palladone

* Reintroduced with new safety program

Two generic drugs withdrawn for safety

in 20 years

Source: FDA Medwatch

© 2006 Express Scripts, Inc.All Rights Reserved 14

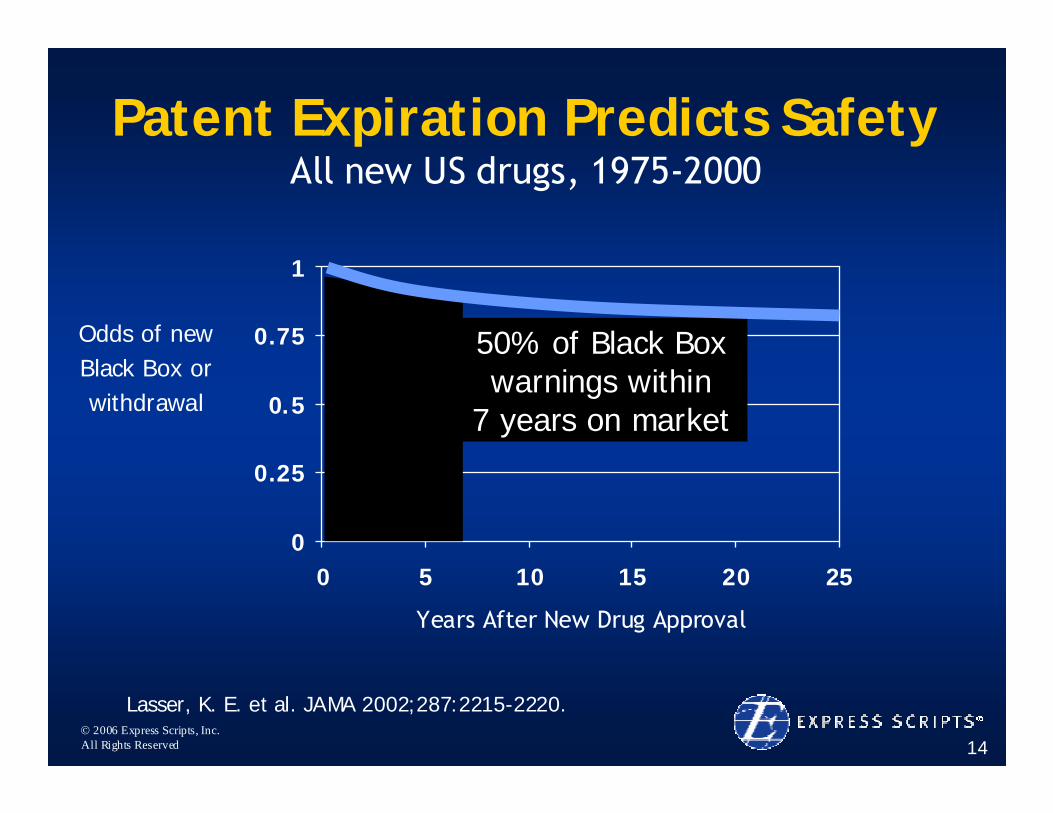

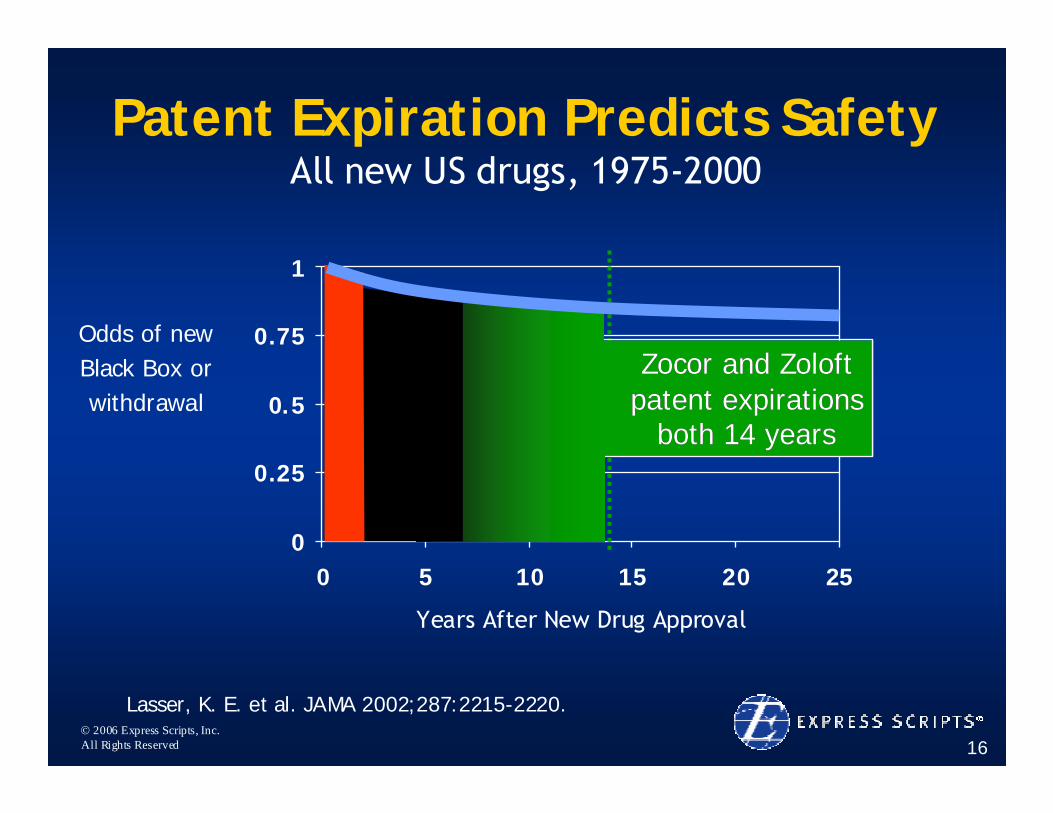

Patent Expiration Predicts Safety

Lasser, K. E. et al. JAMA 2002;287:2215-2220.

All new US drugs, 1975-2000

Odds of new Black Box or withdrawal

0

0.25

0.5

0.75

1

0 5 10 15 20 25

Years After New Drug Approval

50% of Black Box warnings within

7 years on market

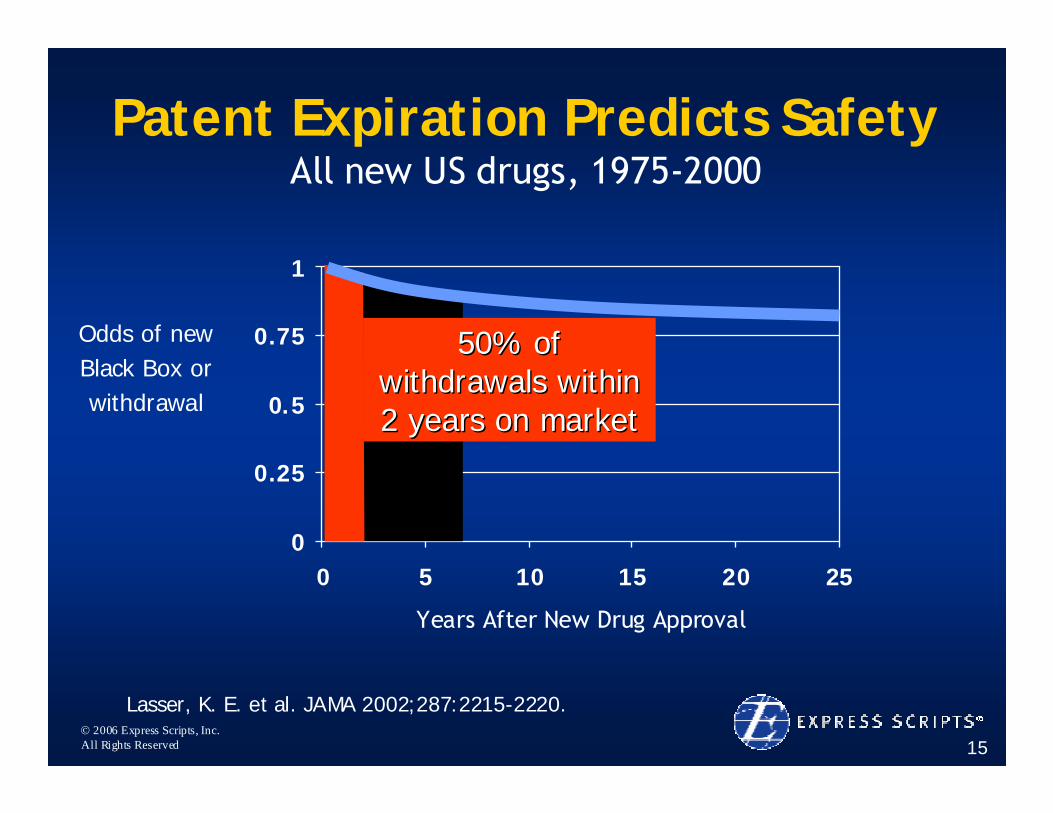

© 2006 Express Scripts, Inc.All Rights Reserved 15

0

0.25

0.5

0.75

1

0 5 10 15 20 25

Years After New Drug Approval

50% of 50% of withdrawals within withdrawals within 2 years on market2 years on market

Lasser, K. E. et al. JAMA 2002;287:2215-2220.

Odds of new Black Box or withdrawal

All new US drugs, 1975-2000Patent Expiration Predicts Safety

© 2006 Express Scripts, Inc.All Rights Reserved 16

0

0.25

0.5

0.75

1

0 5 10 15 20 25

Years After New Drug Approval

Zocor and Zoloft Zocor and Zoloft patent expirations patent expirations

both 14 yearsboth 14 years

Lasser, K. E. et al. JAMA 2002;287:2215-2220.

Odds of new Black Box or withdrawal

All new US drugs, 1975-2000Patent Expiration Predicts Safety

© 2006 Express Scripts, Inc.All Rights Reserved 17

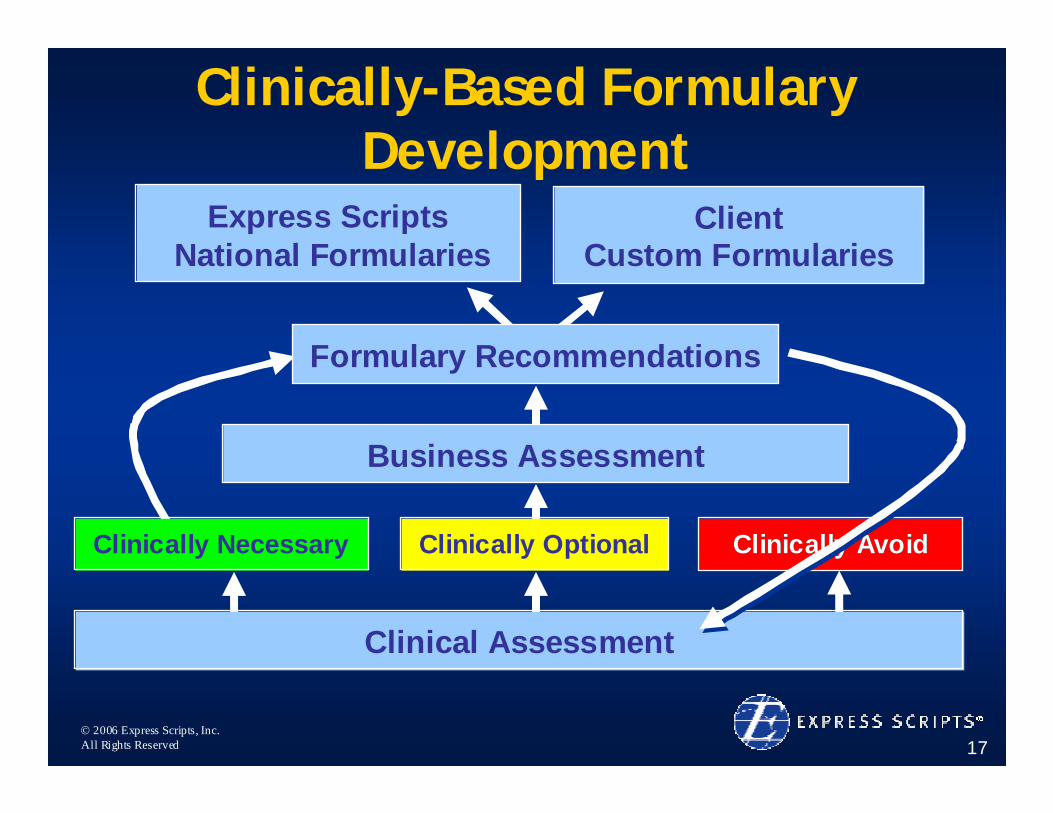

Client Custom Formularies

Express ScriptsNational Formularies

Business Assessment

Clinically-Based Formulary Development

Clinically AvoidClinically AvoidClinically Necessary Clinically Optional

Clinical Assessment

Formulary Recommendations

© 2006 Express Scripts, Inc.All Rights Reserved 18

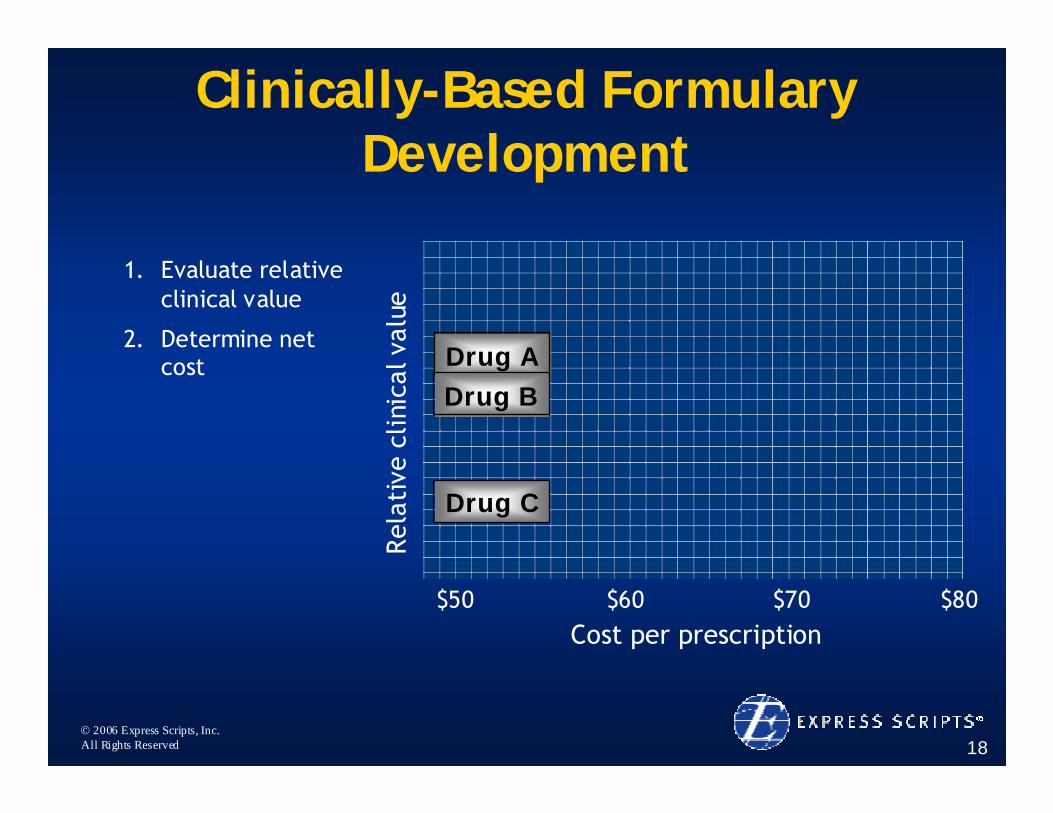

1. Evaluate relative clinical value

2. Determine net cost

Cost per prescription

Clinically-Based Formulary Development

Drug ADrug ADrug BDrug B

Drug CDrug C

$60$50 $70 $80

Rela

tive

clin

ical

val

ue

© 2006 Express Scripts, Inc.All Rights Reserved 19

Cost per prescription

Drug A

Drug B

Drug C

Most cost effective

Rela

tive

clin

ical

val

ue

$50 $60 $70 $80

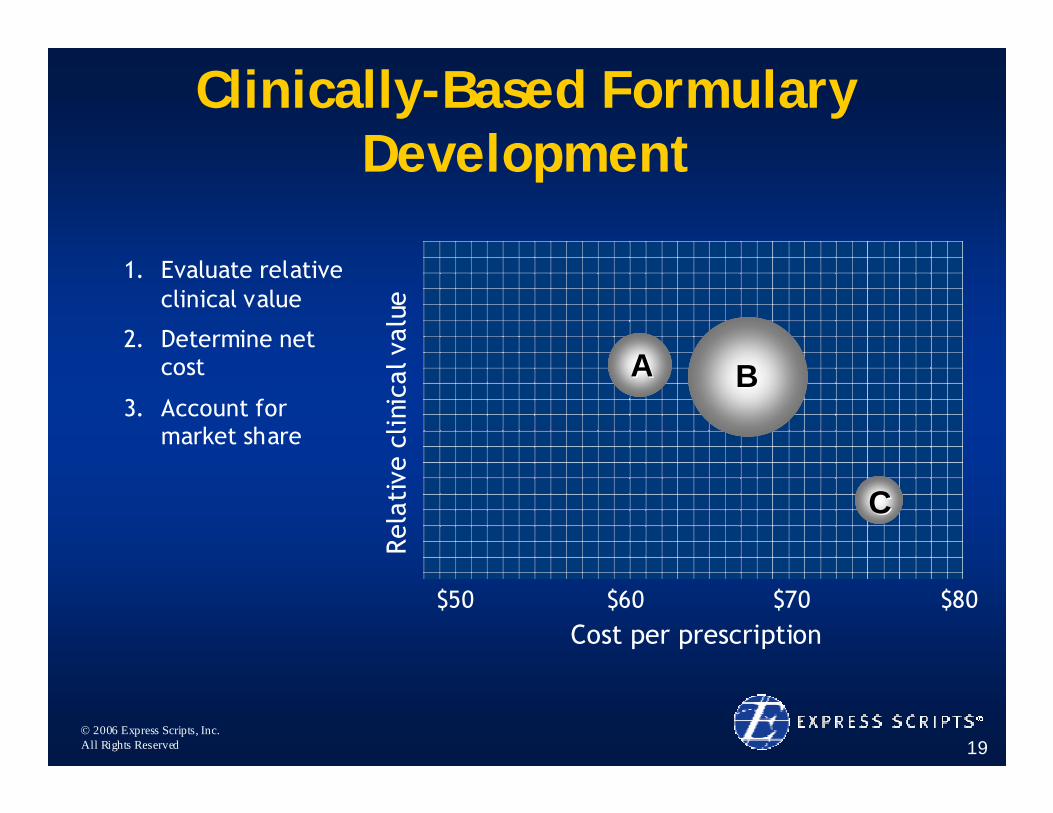

1. Evaluate relative clinical value

2. Determine net cost

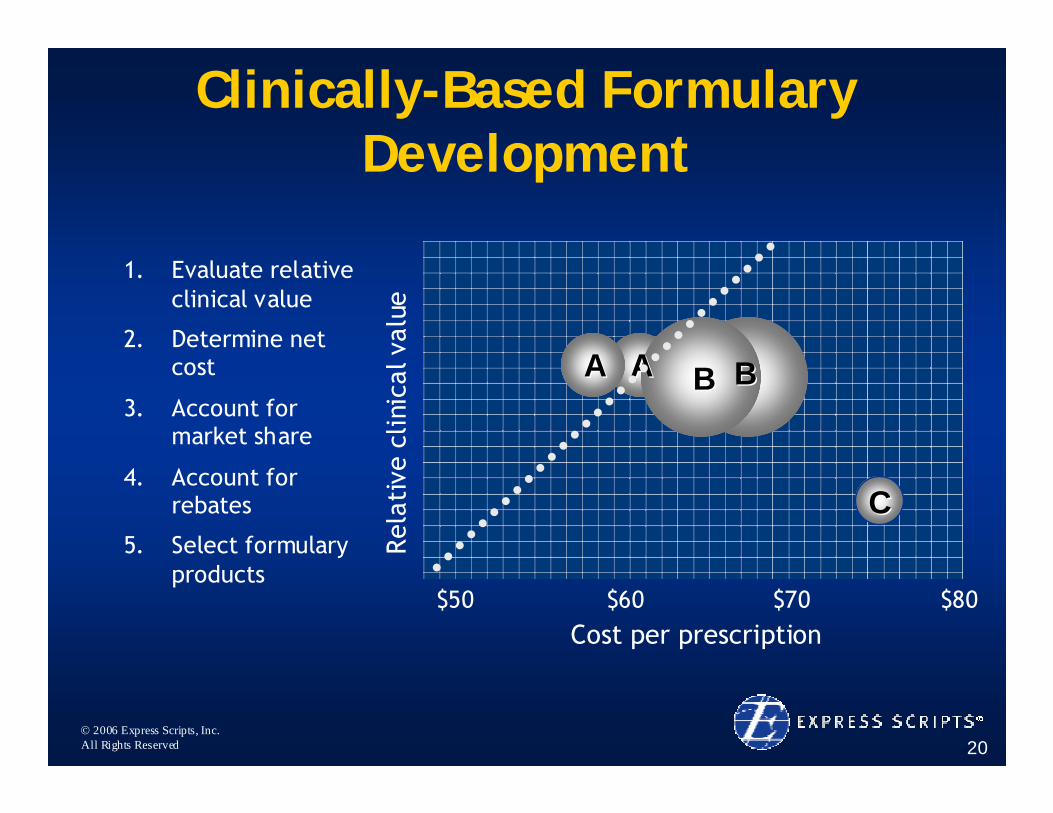

3. Account for market share

AA BB

CC

Clinically-Based Formulary Development

© 2006 Express Scripts, Inc.All Rights Reserved 20

1. Evaluate relative clinical value

2. Determine net cost

3. Account for market share

4. Account for rebates

5. Select formulary products

Cost per prescription

Rela

tive

clin

ical

val

ue

$50 $60 $70 $80

Drug A

Drug B

Drug C

Most cost effective

AA BB

CC

AA BB

Clinically-Based Formulary Development

© 2006 Express Scripts, Inc.All Rights Reserved 21

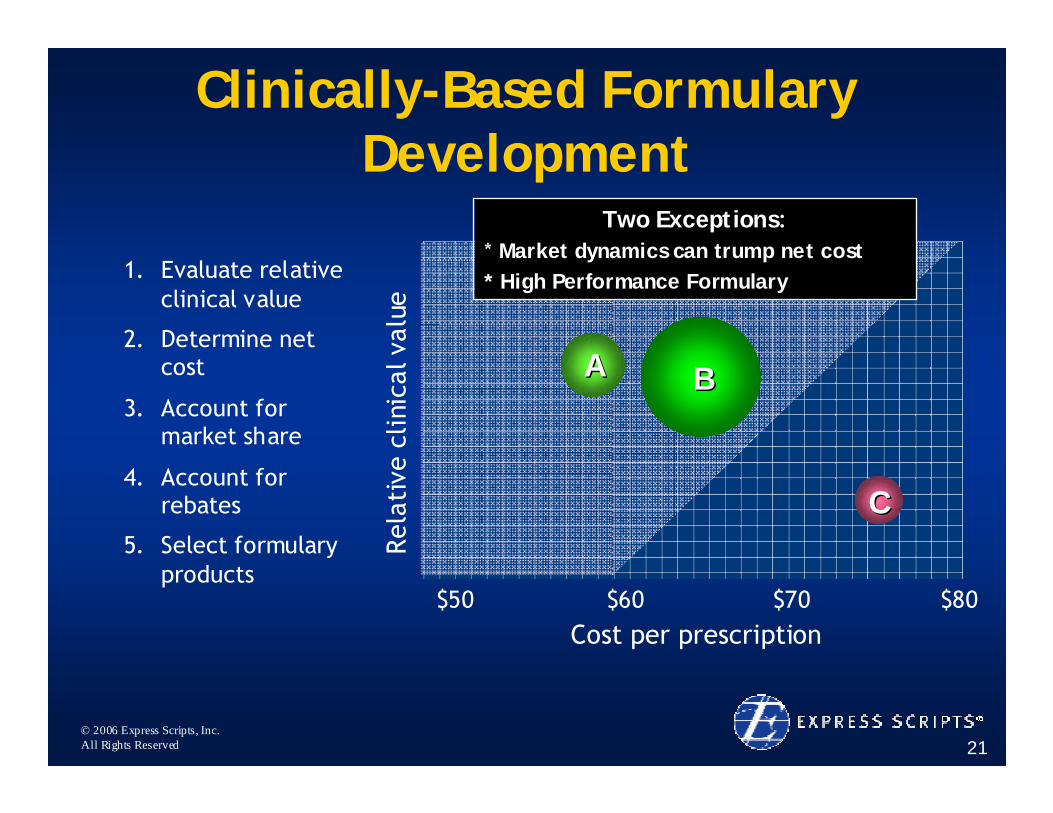

1. Evaluate relative clinical value

2. Determine net cost

3. Account for market share

4. Account for rebates

5. Select formulary products

Cost per prescription

Rela

tive

clin

ical

val

ue

$50 $60 $70 $80

Drug A

Drug B

Drug C

Most cost effective

Two Exceptions: * Market dynamics can trump net cost* High Performance Formulary

AA BB

CC

Clinically-Based Formulary Development

© 2006 Express Scripts, Inc.All Rights Reserved 22

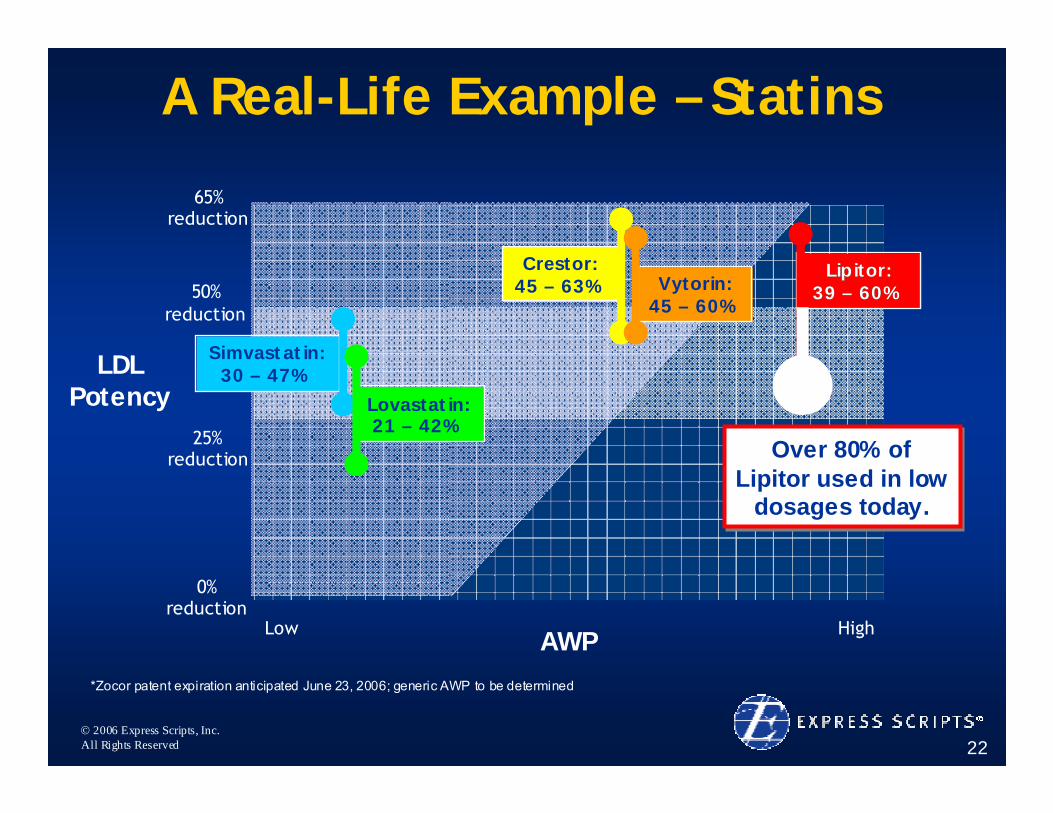

LDL Potency

AWP

A Real-Life Example – Statins

Low High

*Zocor patent expiration anticipated June 23, 2006; generic AWP to be determined

50% reduction

65% reduction

25% reduction

0% reduction

Crestor:45 – 63%

Lipitor:Lipitor:39 39 –– 60%60%Vytorin:

45 – 60%

Simvastatin:30 – 47%

Lovastatin: 21 – 42%

Over 80% of Lipitor used in low

dosages today.

Over 80% of Lipitor used in low

dosages today.

© 2006 Express Scripts, Inc.All Rights Reserved 23

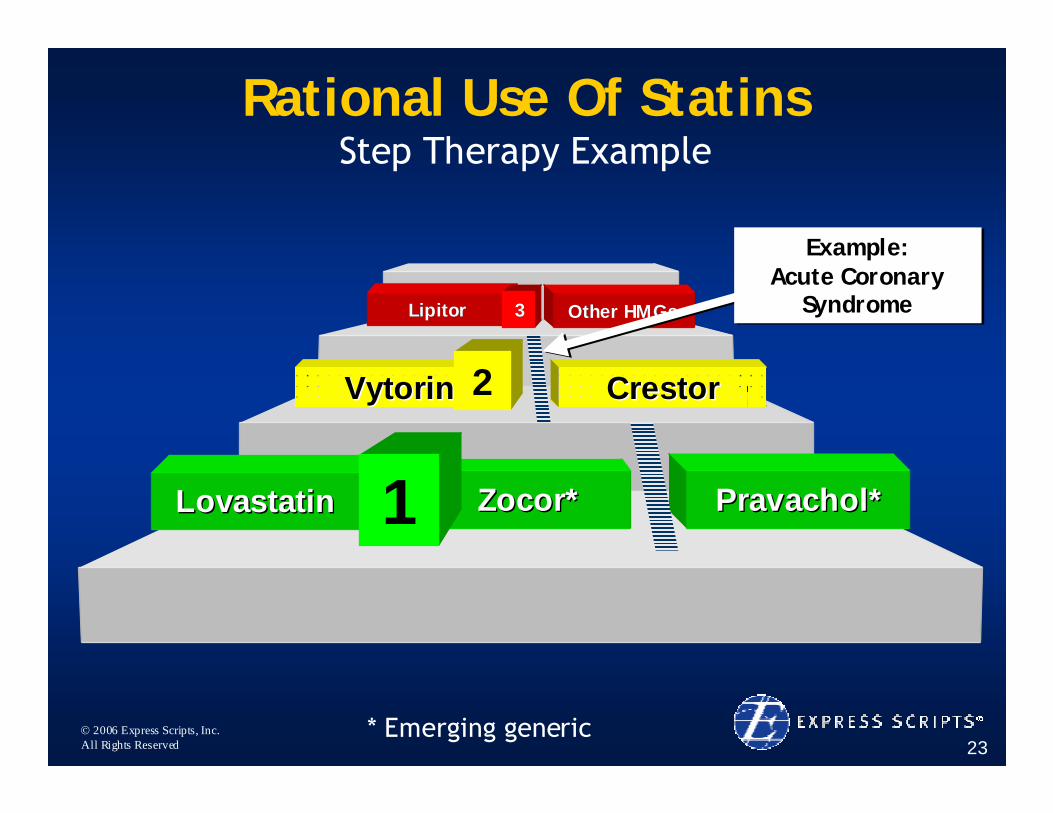

Rational Use Of StatinsStep Therapy Example

Zocor*Zocor*LovastatinLovastatin Pravachol*Pravachol*

LipitorLipitor Other HMGs Other HMGs

VytorinVytorin CrestorCrestor

1

2

33

* Emerging generic

Example: Acute Coronary

Syndrome

Example: Acute Coronary

Syndrome

© 2006 Express Scripts, Inc.All Rights Reserved 24

Why Express Scripts?• Differentiation Through Alignment

– Formulary strategy promotes generics and low-cost brands

• Strategic Execution– Rock-solid clinical foundation– Clinical and business solutions aligned

• Room to Run– Tremendous emerging generic opportunities

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

The Express Scripts Business Model:Alignment With Clients And

Promoting Generics

Steve Miller, MDVice President, Research and Clinical

Development

© 2006 Express Scripts, Inc.All Rights Reserved 26

What’s Driving Drug Trend?2003 : 2004

3%

27%

70%

0%

20%

40%

60%

80%

New Drugs Utilization Cost/Rx

DTR 2004 : ESI clients with funded integrated benefits

© 2006 Express Scripts, Inc.All Rights Reserved 27

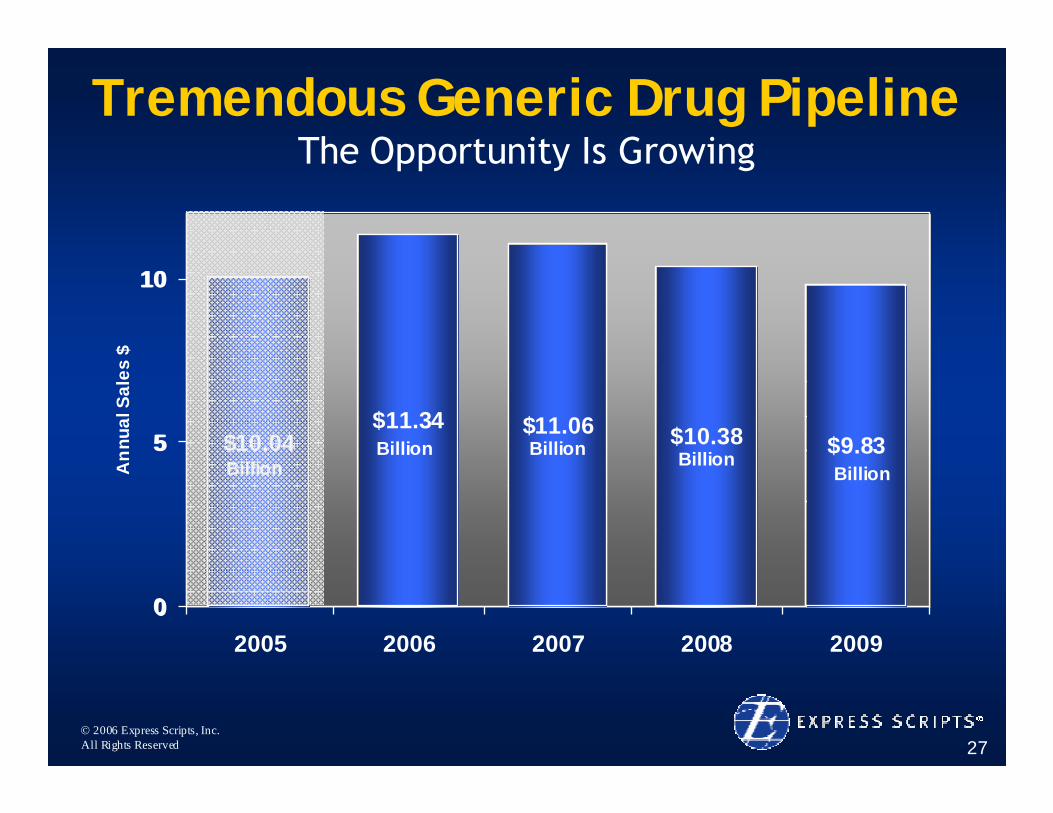

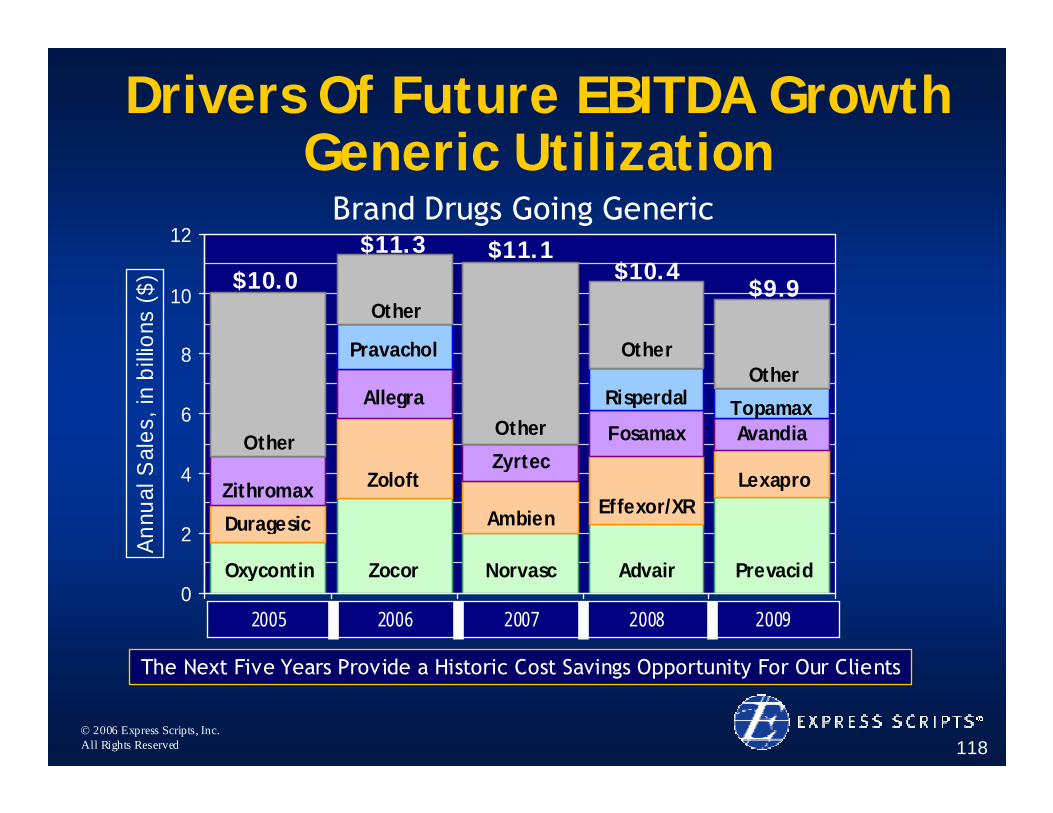

Tremendous Generic Drug PipelineThe Opportunity Is Growing

0

5

10

2005 2006 2007 2008 2009

Ann

ual S

ales

$

Oxycontin

Duragesic

Zithromax

Other

Zocor

Zoloft

Allegra

Pravachol

Other

Norvasc

Ambien

Zyrtec

Other

Advair

Effexor/XR

Fosamax

Risperdal

Other

Prevacid

Lexapro

Avandia

Topamax

Other

$10.04$11.34 $11.06 $10.38 $9.83

0

5

10

BillionBillion

Billion BillionBillion

© 2006 Express Scripts, Inc.All Rights Reserved 28

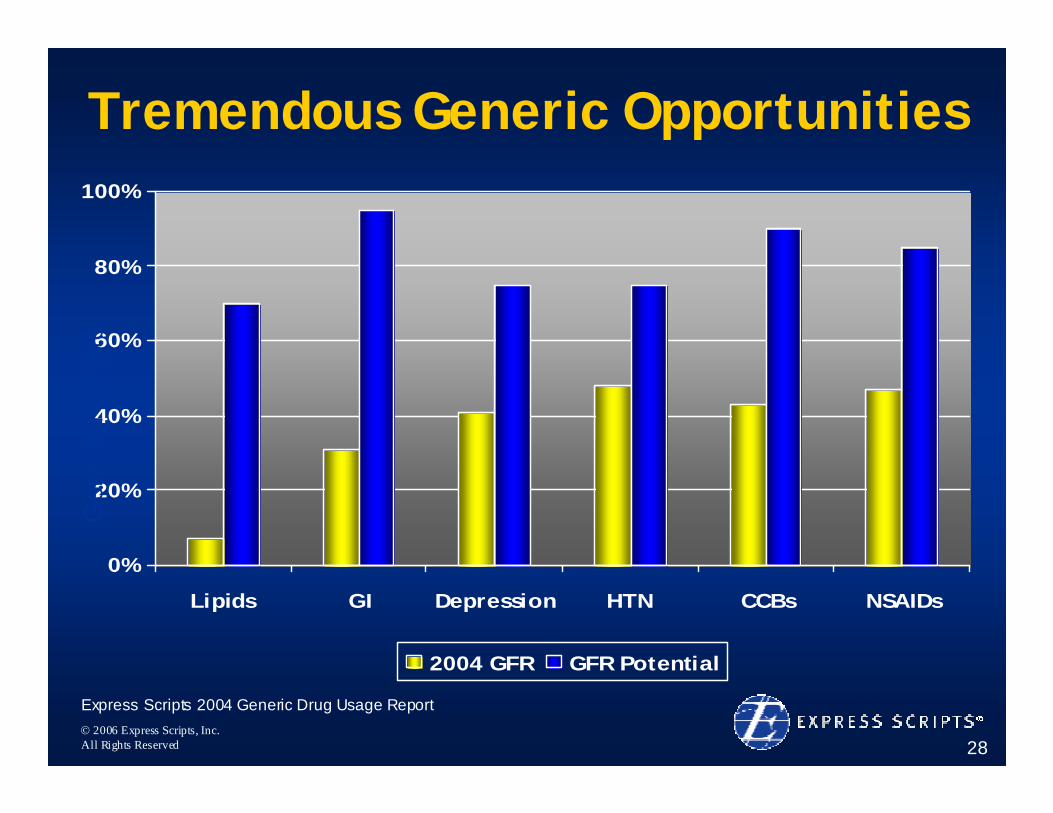

Tremendous Generic Opportunities

0%

20%

40%

60%

80%

100%

Lipids GI Depression HTN CCBs NSAIDs

2004 GFR GFR Potential

Gen

eric

Fill

Rat

e

Express Scripts 2004 Generic Drug Usage Report

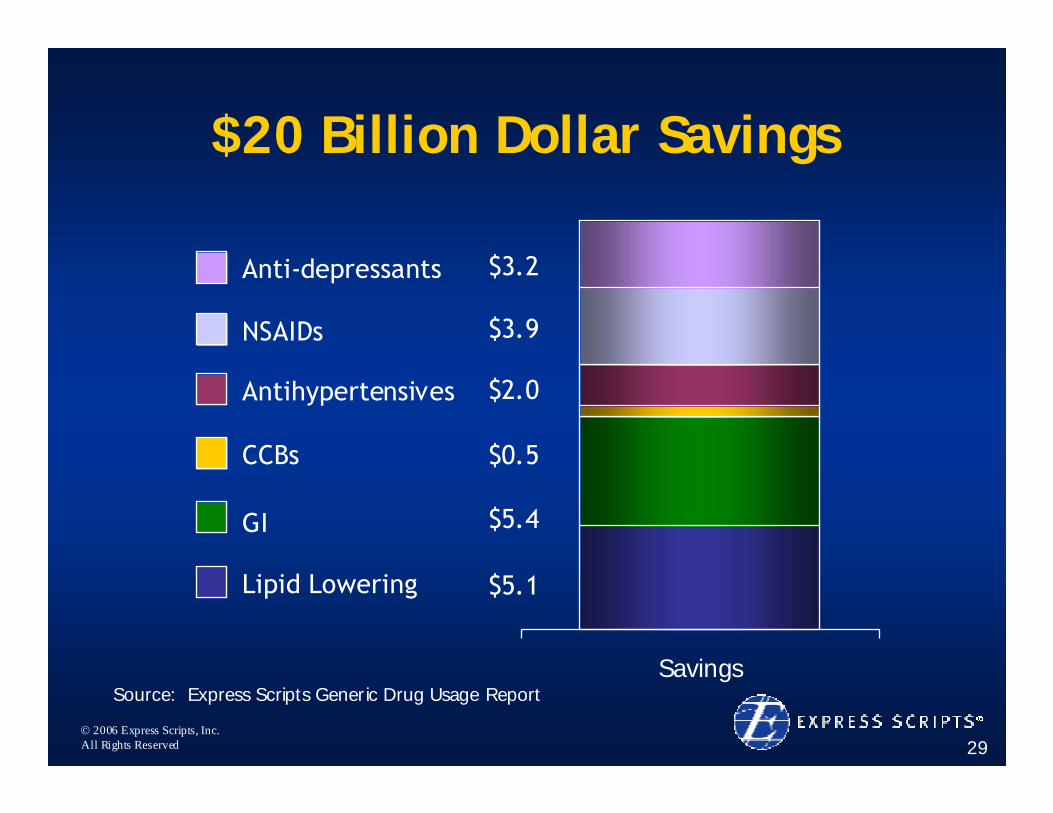

© 2006 Express Scripts, Inc.All Rights Reserved 29

$20 Billion Dollar Savings

SavingsSource: Express Scripts Generic Drug Usage Report

$5.1

$5.4

$0.5

$2.0

$3.9

$3.2Anti-depressants

NSAIDs

Antihypertensives

CCBs

GI

Lipid Lowering

© 2006 Express Scripts, Inc.All Rights Reserved 30

© 2006 Express Scripts, Inc.All Rights Reserved 31

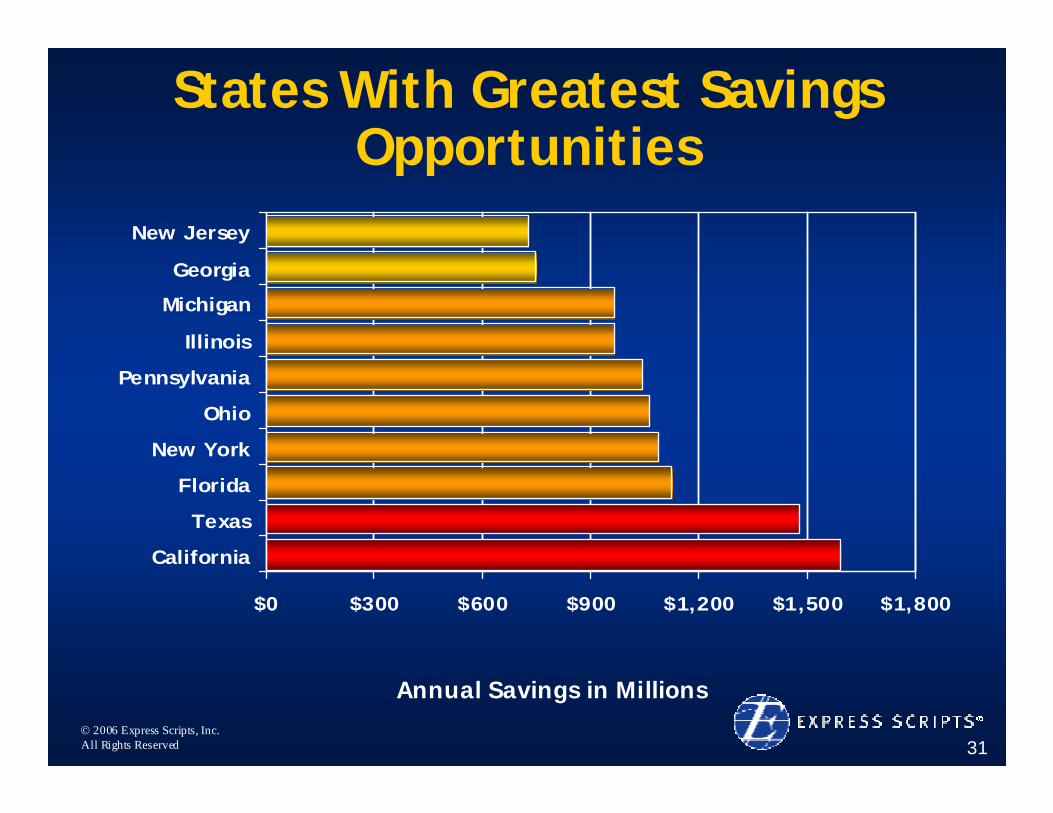

States With Greatest Savings Opportunities

$0 $300 $600 $900 $1,200 $1,500 $1,800

California

Texas

Florida

New York

Ohio

Pennsylvania

Illinois

Michigan

Georgia

New Jersey

Annual Savings in Millions

© 2006 Express Scripts, Inc.All Rights Reserved 32

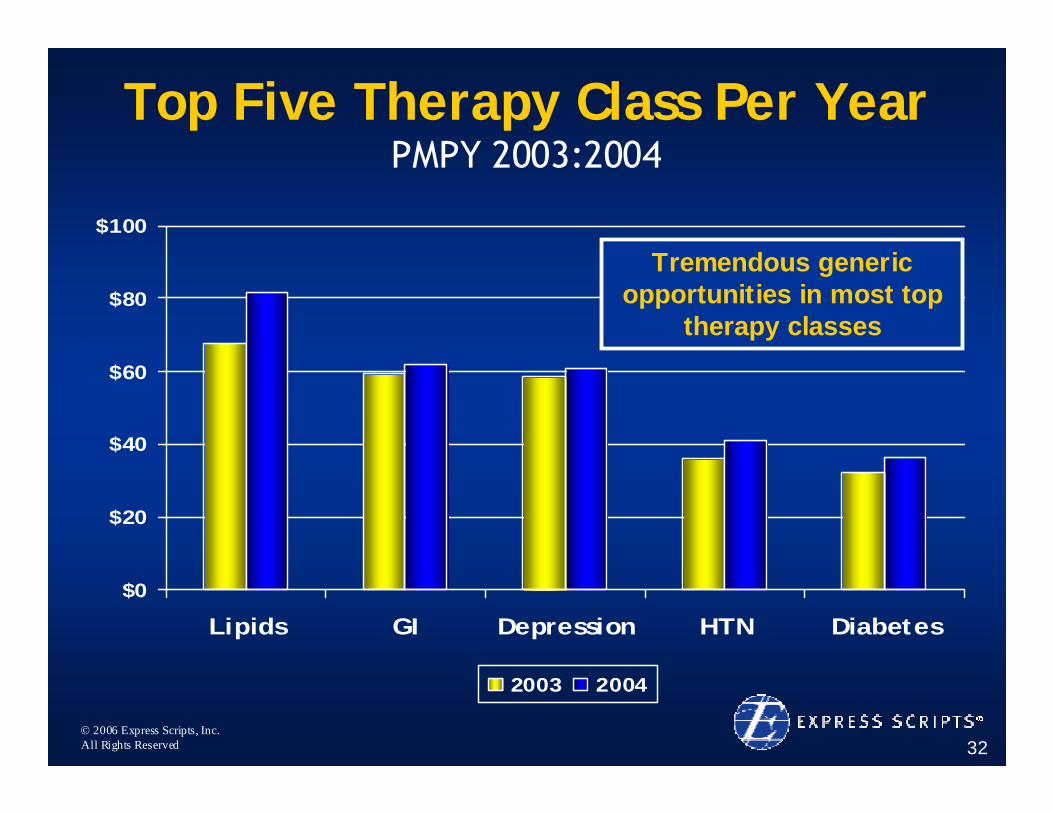

Top Five Therapy Class Per YearPMPY 2003:2004

$0

$20

$40

$60

$80

$100

Lipids GI Depression HTN Diabetes

2003 2004

PMPY

Tremendous generic opportunities in most top

therapy classes

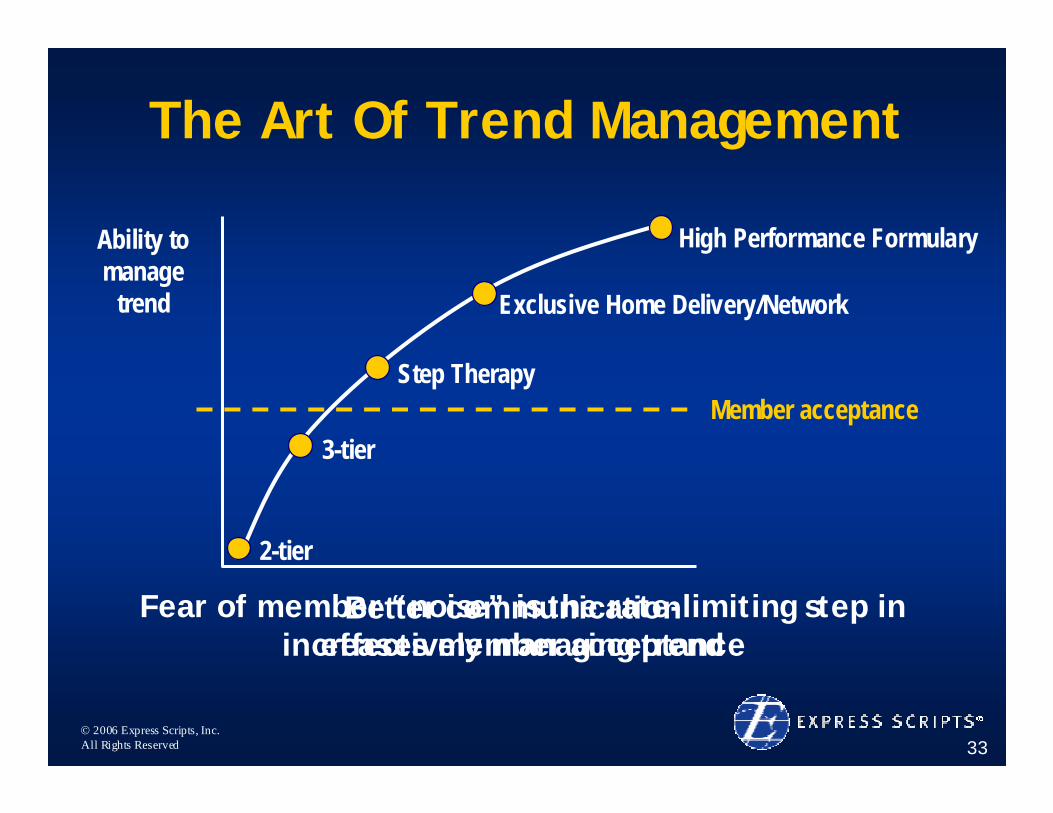

© 2006 Express Scripts, Inc.All Rights Reserved 33

Ability to manage

trend

2-tier

3-tier

Step Therapy

Exclusive Home Delivery/Network

The Art Of Trend Management

Member acceptance

High Performance Formulary

Fear of member “noise” is the rate-limiting step in effectively managing trend

Better communication increases member acceptance

© 2006 Express Scripts, Inc.All Rights Reserved 34

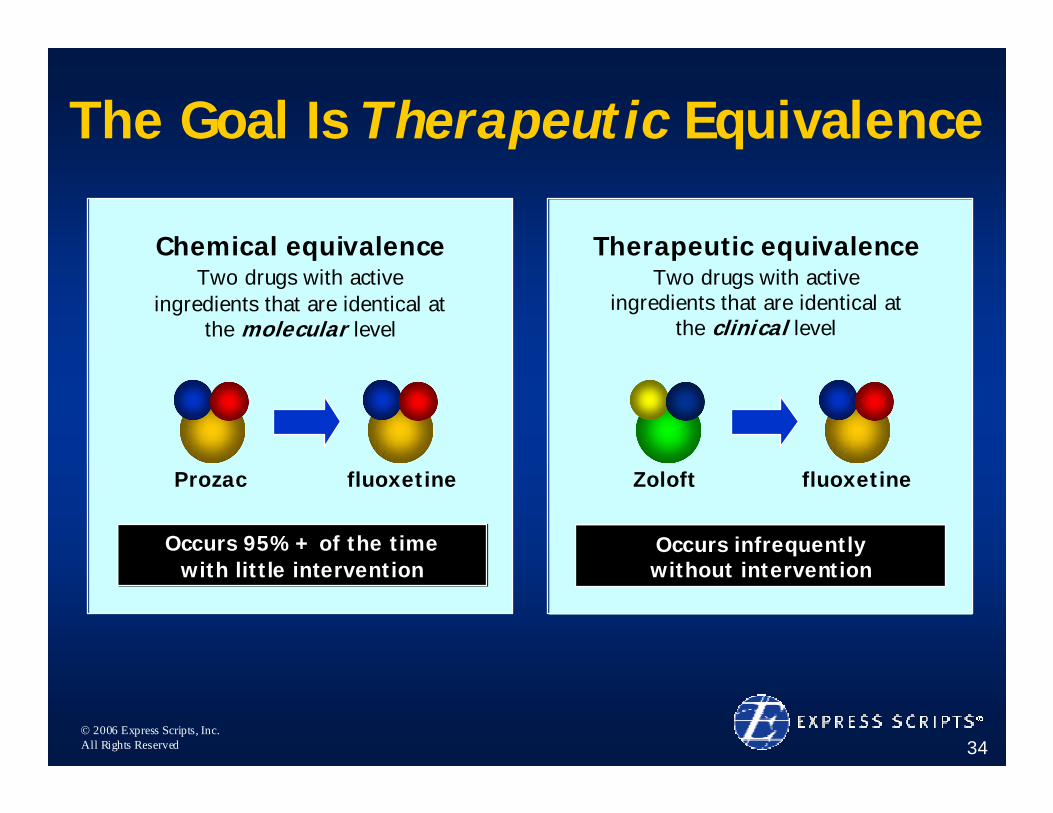

The Goal Is Therapeutic Equivalence

Chemical equivalenceTwo drugs with active

ingredients that are identical at the molecular level

Prozac fluoxetine

Occurs 95%+ of the time with little intervention

Therapeutic equivalenceTwo drugs with active

ingredients that are identical at the clinical level

Zoloft fluoxetine

Occurs infrequently without intervention

© 2006 Express Scripts, Inc.All Rights Reserved 35

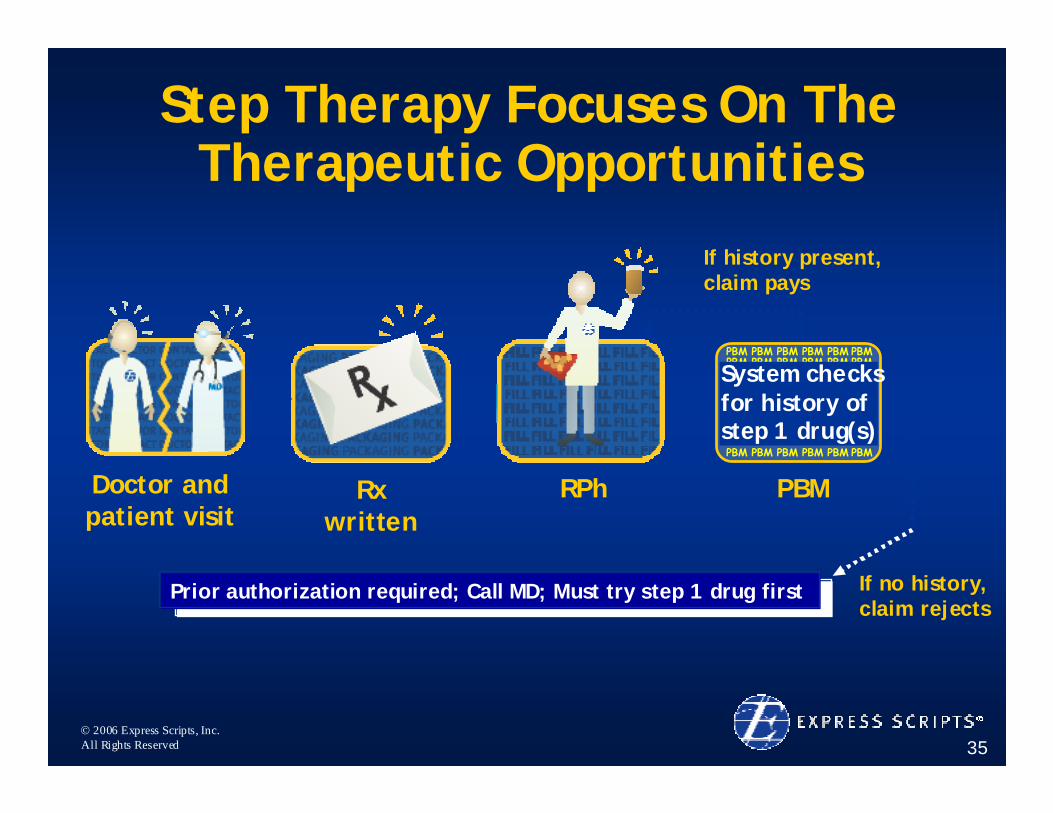

Step Therapy Focuses On The Therapeutic Opportunities

PBM

Prior authorization required; Call MD; Must try step 1 drug first

If history present, claim pays

If no history, claim rejects

Doctor and patient visit

Rx written

PBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBMPBM PBM PBM PBM PBM PBM

System checks for history of step 1 drug(s)

RPh

© 2006 Express Scripts, Inc.All Rights Reserved 36

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

Mar-02 Jul-02 Nov-02 Mar-03

Step Therapy Client All Non-Step Clients

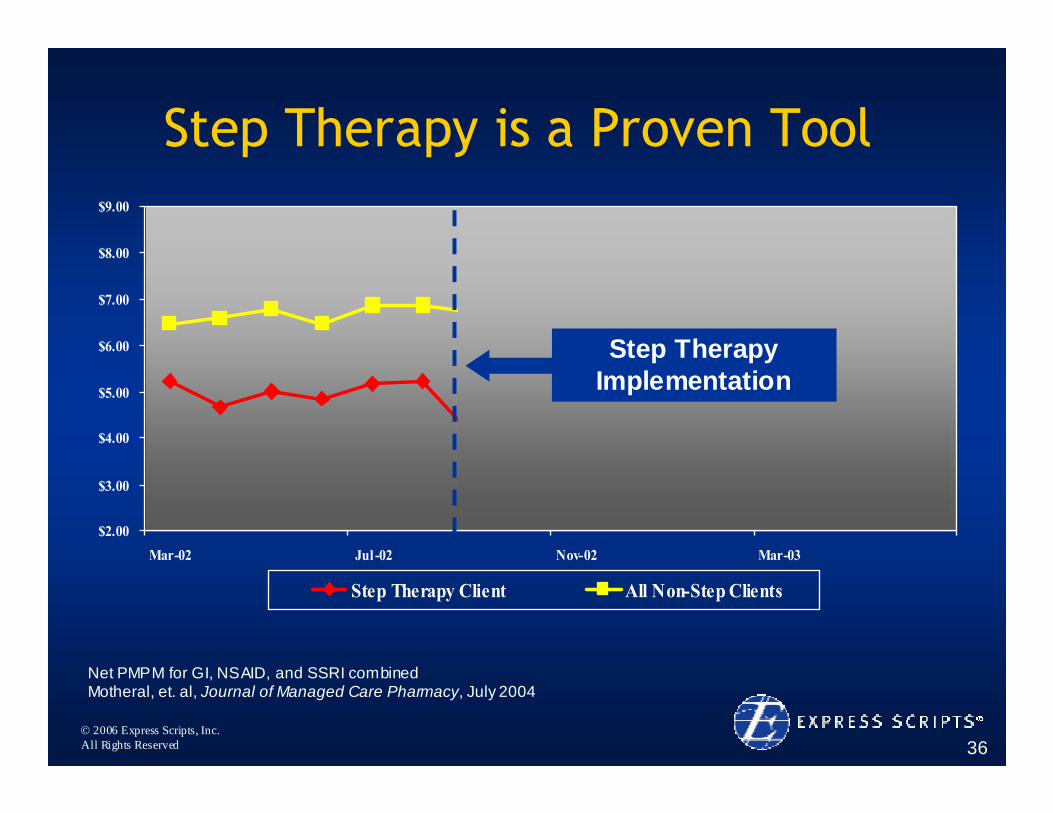

Step Therapy is a Proven Tool

Net PMPM for GI, NSAID, and SSRI combinedMotheral, et. al, Journal of Managed Care Pharmacy, July 2004

Step Therapy Implementation

© 2006 Express Scripts, Inc.All Rights Reserved 37

Home Delivery Pharmacy

• Convenience

• Cost

• Confidential

• 24 x 7 service

• Safety

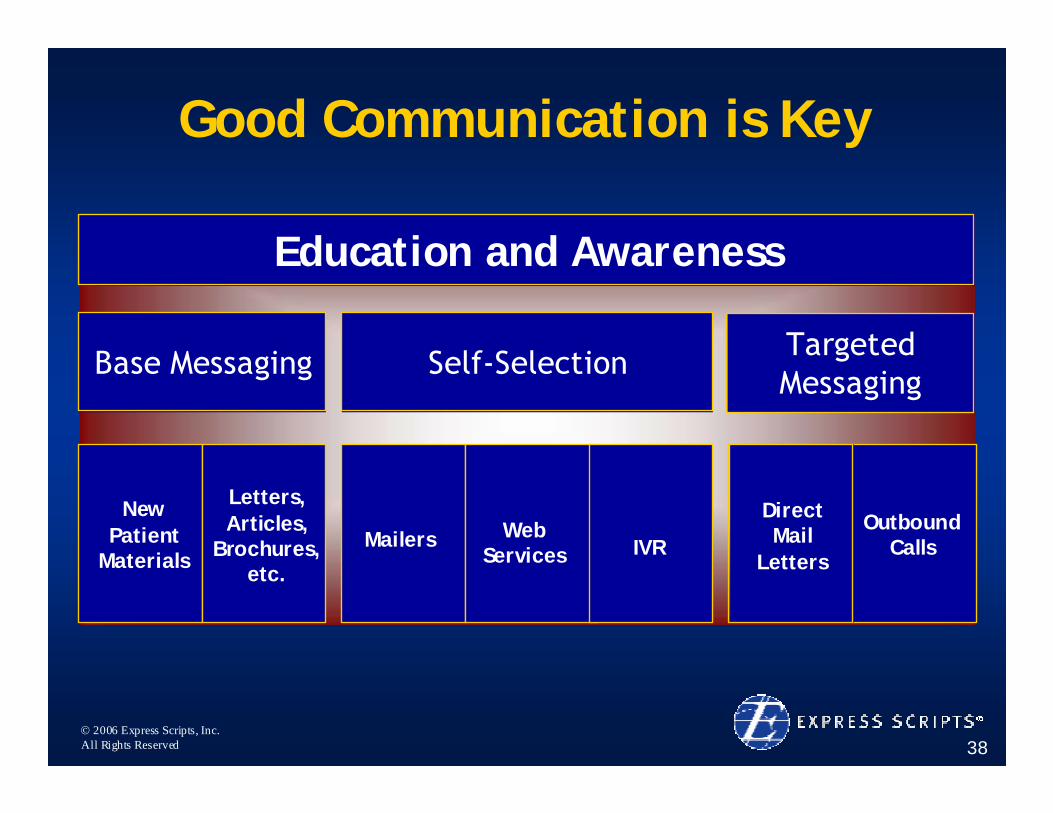

© 2006 Express Scripts, Inc.All Rights Reserved 38

New Patient

Materials

Letters, Articles,

Brochures, etc.

Mailers Web Services IVR

Direct Mail

Letters

Outbound Calls

Base Messaging Self-Selection TargetedMessaging

Education and Awareness

Good Communication is Key

© 2006 Express Scripts, Inc.All Rights Reserved 39

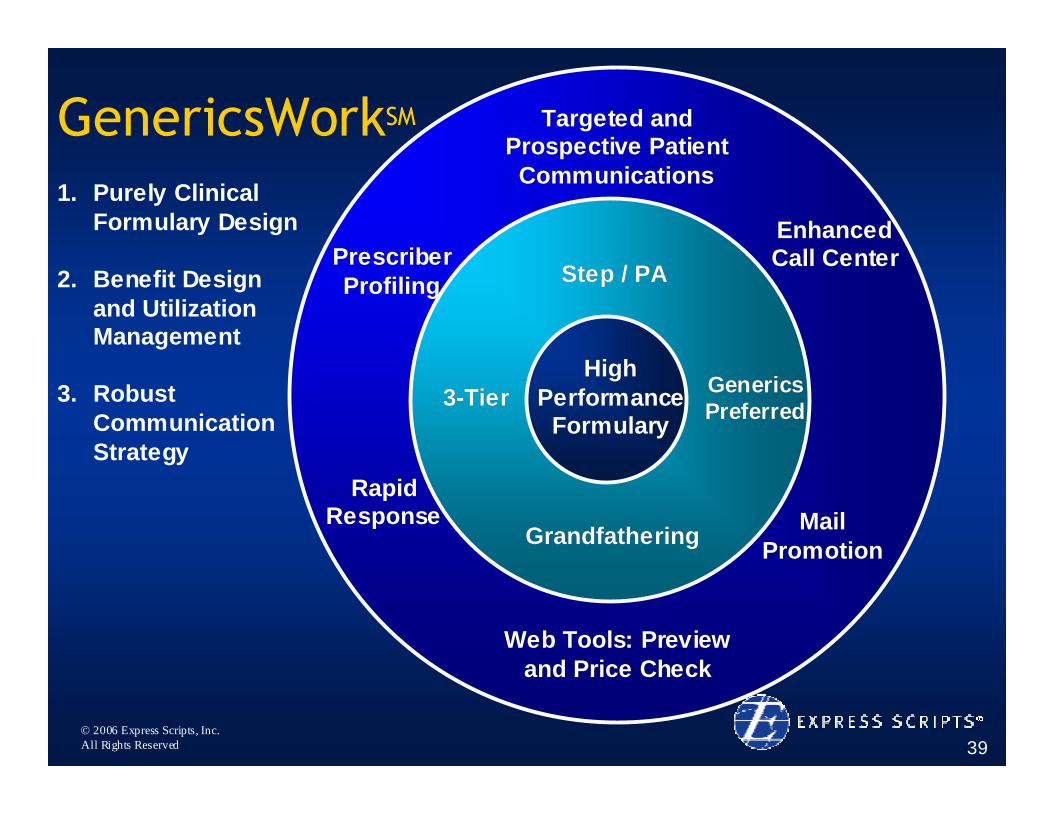

GenericsWorkSM Targeted and Targeted and Prospective Patient Prospective Patient CommunicationsCommunications

Web Tools: Preview Web Tools: Preview and Price Checkand Price Check

Prescriber Prescriber ProfilingProfiling

Enhanced Enhanced Call CenterCall Center

Mail Mail PromotionPromotion

Rapid Rapid ResponseResponse

GrandfatheringGrandfathering

Step / PAStep / PA

33--TierTier Generics Generics PreferredPreferred

High High Performance Performance

FormularyFormulary

1. Purely Clinical Formulary Design

2. Benefit Design and Utilization Management

3. Robust Communication Strategy

© 2006 Express Scripts, Inc.All Rights Reserved 40

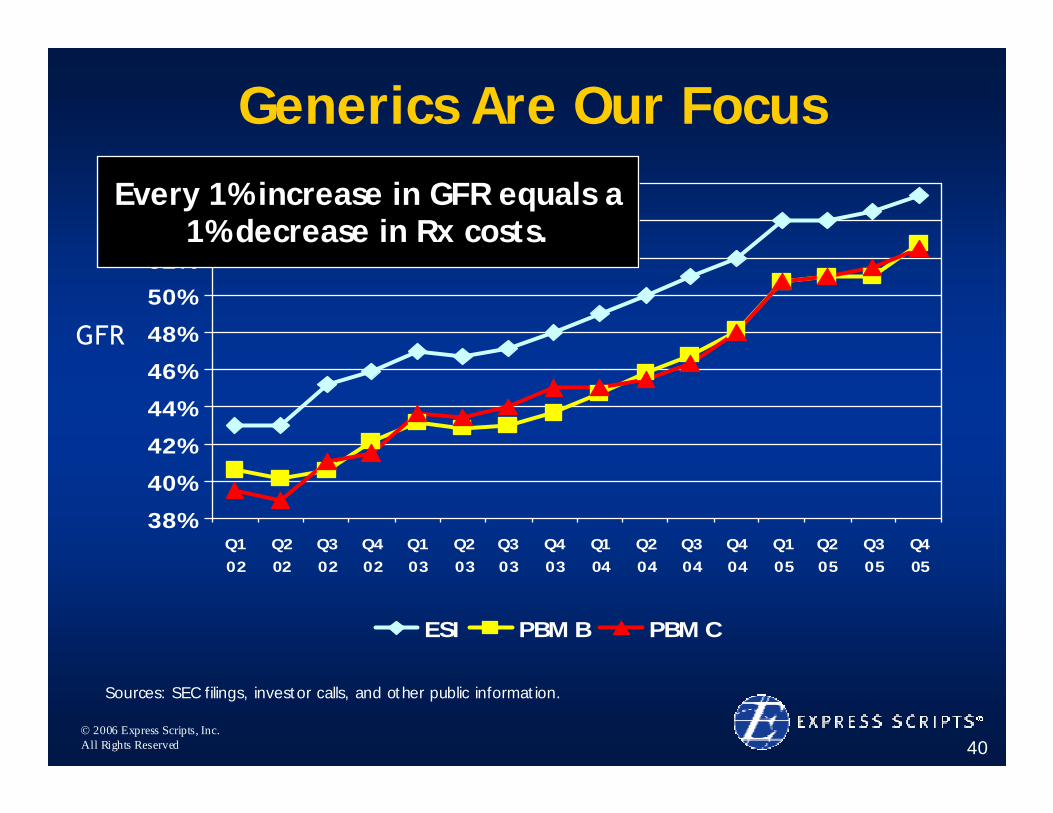

Generics Are Our Focus

Sources: SEC filings, investor calls, and other public information.

38%

40%

42%

44%

46%

48%

50%

52%

54%

56%

Q102

Q202

Q302

Q402

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

ESI PBM B PBM C

GFR

Every 1% increase in GFR equals a 1% decrease in Rx costs.

© 2006 Express Scripts, Inc.All Rights Reserved 41

Why Express Scripts?• Differentiation Through Alignment

– Business model drives out waste in healthcare

• Strategic Execution– Comprehensive programs with industry-leading success

• Room to Run– Generics, Home Delivery and Formulary Management:

Platforms for long-term growth

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

Adding Value Through Service Performance

Doug PorterSenior Vice President

Client and Patient Services

© 2006 Express Scripts, Inc.All Rights Reserved 43

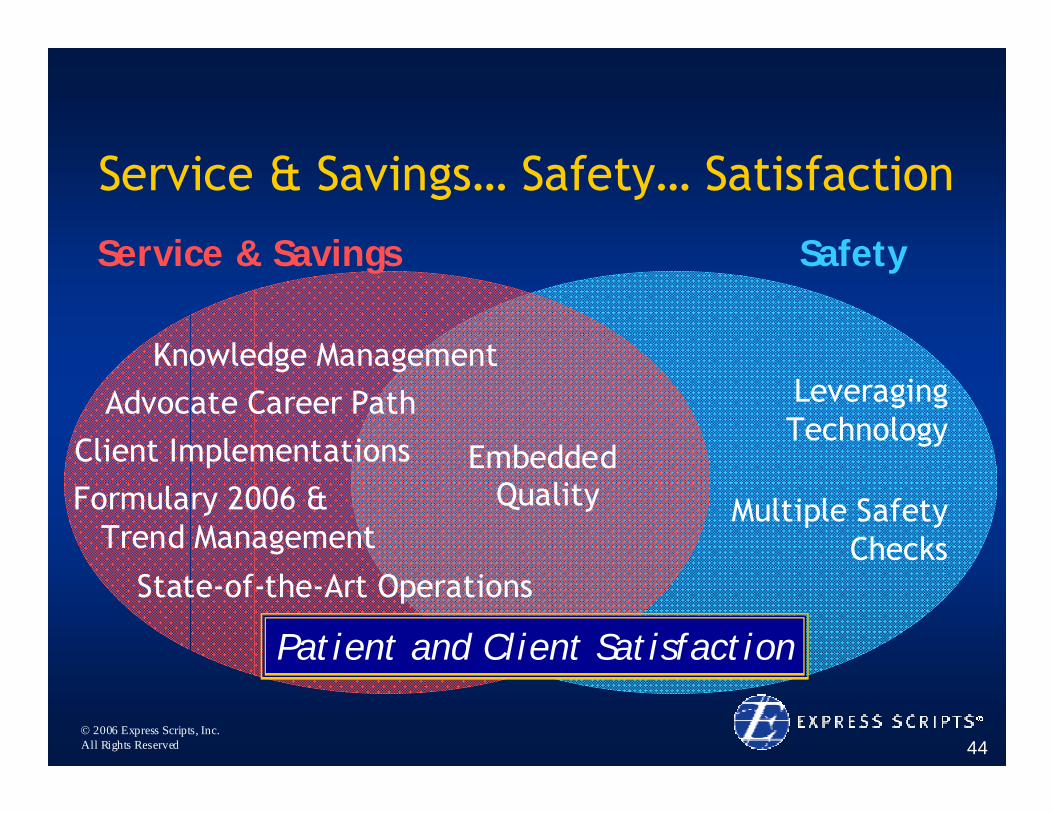

The Heart of Service Means…

Service & Savings… Safety… Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 44

Service & Savings… Safety… Satisfaction

Service & Savings Safety

Knowledge ManagementAdvocate Career Path

Client ImplementationsFormulary 2006 &

Trend Management

State-of-the-Art Operations

Leveraging Technology

Multiple Safety Checks

Embedded Quality

Patient and Client Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 45

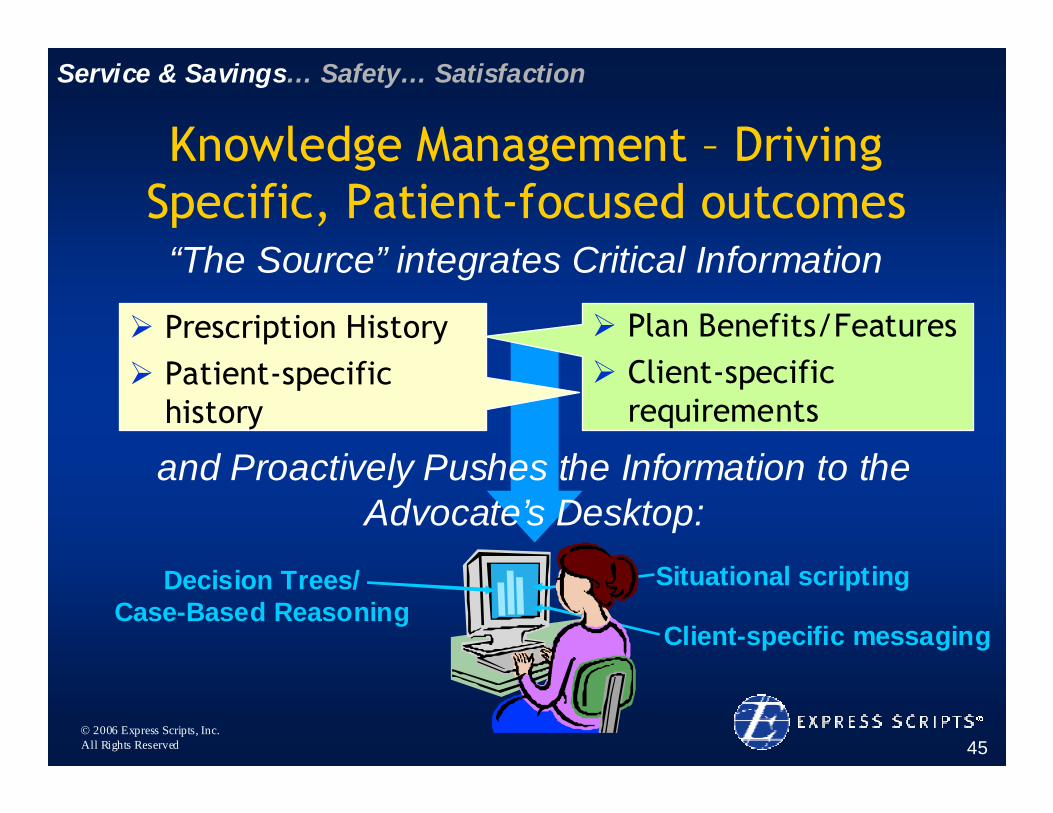

and Proactively Pushes the Information to the Advocate’s Desktop:

Situational scriptingDecision Trees/Case-Based Reasoning

Client-specific messaging

Knowledge Management – Driving Specific, Patient-focused outcomes

“The Source” integrates Critical Information

Prescription HistoryPatient-specific history

Plan Benefits/FeaturesClient-specific requirements

Service & Savings… Safety… Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 46

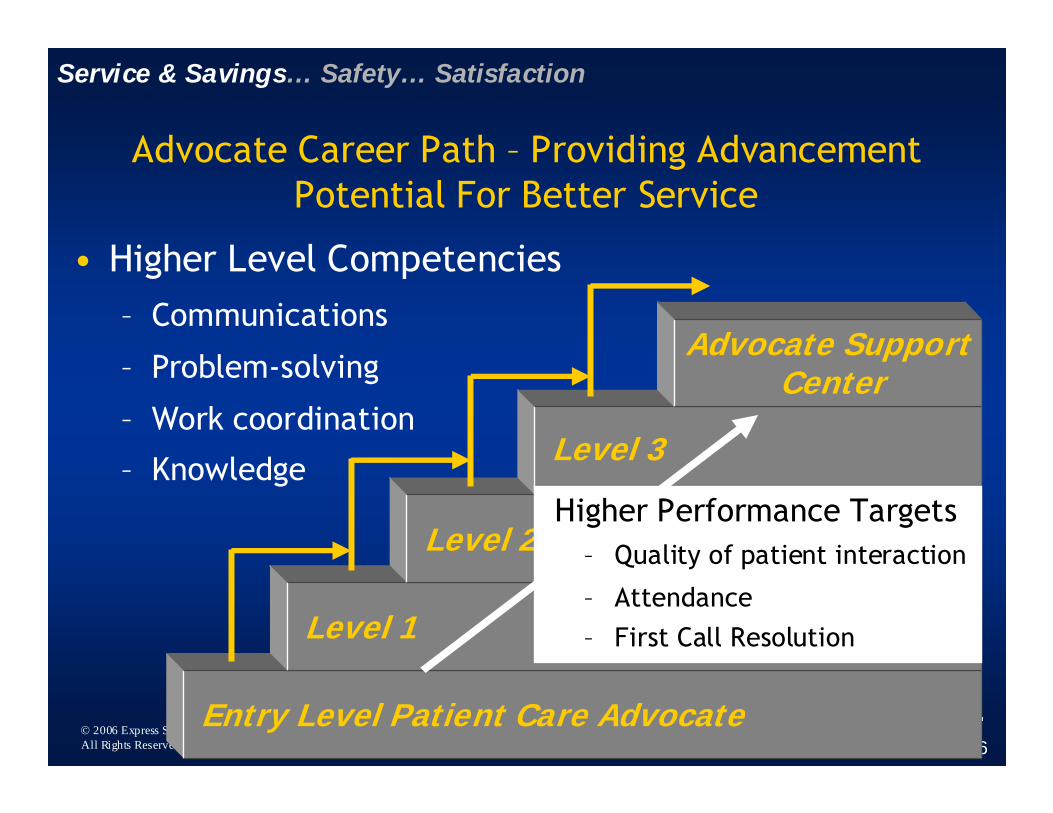

Advocate Career Path – Providing Advancement Potential For Better Service

Entry Level Patient Care Advocate

Level 1

Level 2

Level 3

Advocate Support Center

• Higher Level Competencies– Communications

– Problem-solving

– Work coordination

– KnowledgeHigher Performance Targets

– Quality of patient interaction

– Attendance– First Call Resolution

Service & Savings… Safety… Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 47

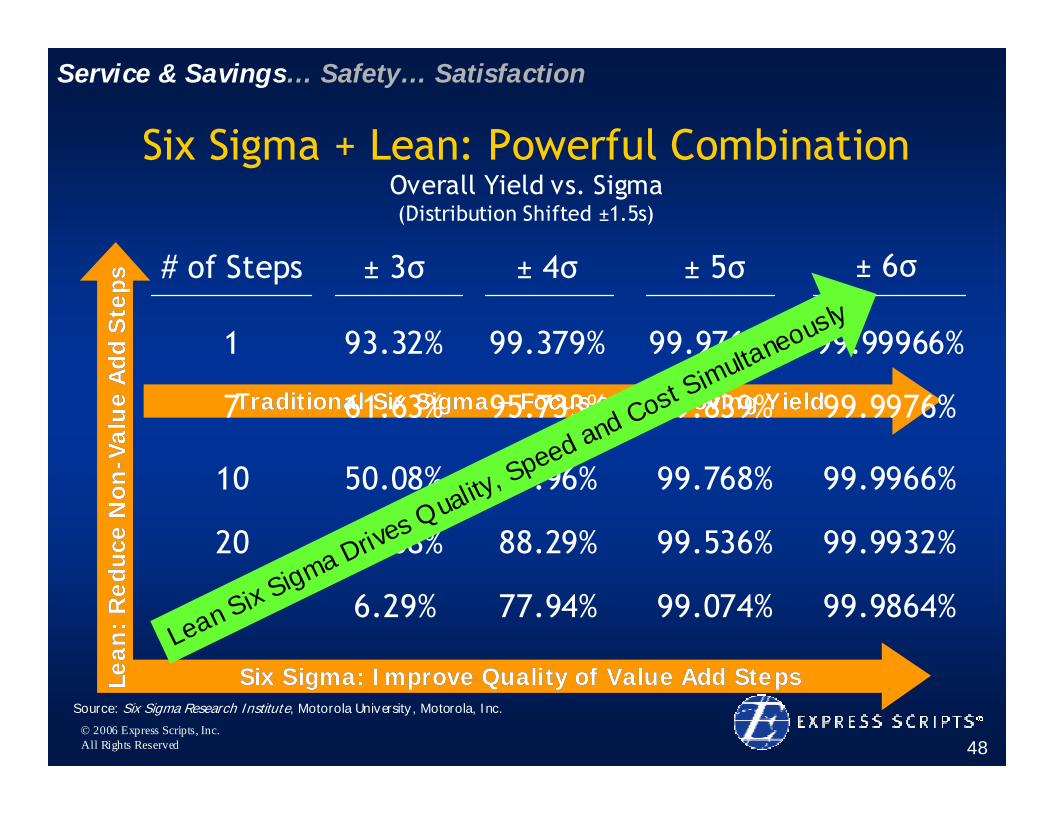

The Next Level: “Embedded Quality”

• Approach: Lean + Six Sigma

LEAN• Reduce Waste• Increase Speed• Bias for Action

SIX SIGMA• Voice of the Customer• Eliminate Variation• Rigorous Approach

LEAN SIX SIGMA

Service & Savings… Safety… Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 48

Six Sigma + Lean: Powerful CombinationOverall Yield vs. Sigma(Distribution Shifted ±1.5s)

Service & Savings… Safety… Satisfaction

Six Sigma: Improve Quality of Value Add StepsSix Sigma: Improve Quality of Value Add StepsSource: Six Sigma Research Institute, Motorola University, Motorola, Inc.

Lean

: R

educ

e N

onLe

an:

Red

uce

Non

--Val

ue

Add

Ste

psVa

lue

Add

Ste

ps

# of Steps ± 3σ ± 4σ ± 5σ ± 6σ

1 93.32% 99.379% 99.9767% 99.99966%

Traditional Six Sigma Traditional Six Sigma –– Focus on Improving YieldFocus on Improving Yield7 61.63%

10 50.08%

20 25.08%

40 6.29%

95.733% 99.839% 99.9976%

93.96% 99.768% 99.9966%

88.29% 99.536% 99.9932%

77.94% 99.074% 99.9864%Lean Six S

igma Drives Quality, Speed and Cost Simultaneously

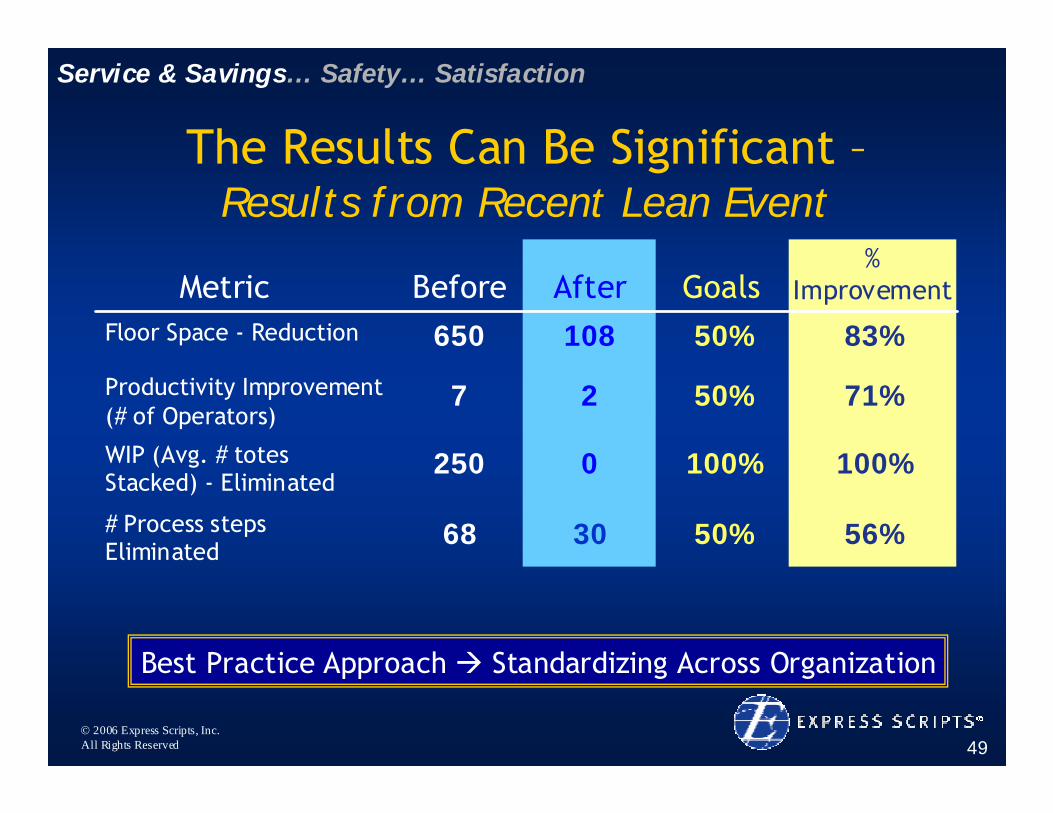

© 2006 Express Scripts, Inc.All Rights Reserved 49

56%

83%

The Results Can Be Significant –Results from Recent Lean Event

50%3068# Process steps Eliminated

100%0250WIP (Avg. # totes Stacked) - Eliminated

50%27Productivity Improvement(# of Operators)

50%108650Floor Space - Reduction

GoalsAfter BeforeMetric

100%

71%

% Improvement

Service & Savings… Safety… Satisfaction

Best Practice Approach Standardizing Across Organization

© 2006 Express Scripts, Inc.All Rights Reserved 50

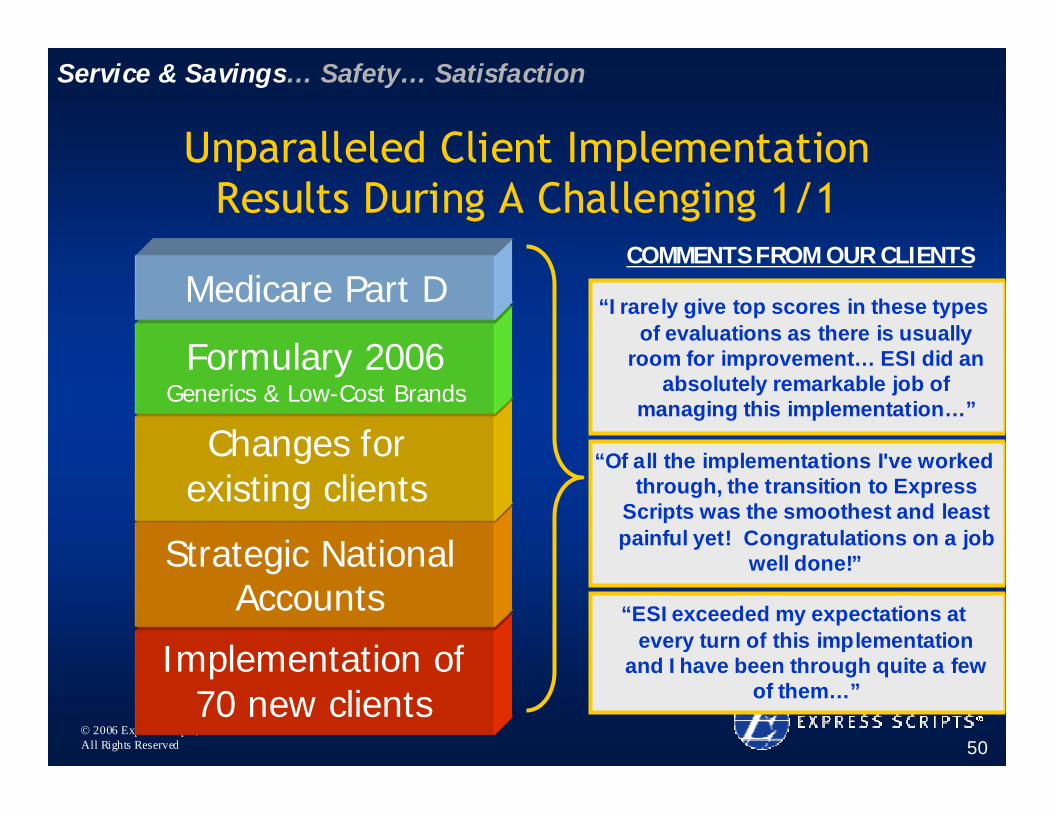

Unparalleled Client Implementation Results During A Challenging 1/1

“I rarely give top scores in these types of evaluations as there is usually

room for improvement… ESI did an absolutely remarkable job of

managing this implementation…”

“Of all the implementations I've worked through, the transition to Express

Scripts was the smoothest and least painful yet! Congratulations on a job

well done!”

“ESI exceeded my expectations at every turn of this implementation

and I have been through quite a few of them…”

COMMENTS FROM OUR CLIENTS

Implementation of 70 new clients

Strategic National Accounts

Changes for existing clients

Formulary 2006Generics & Low-Cost Brands

Medicare Part D

Service & Savings… Safety… Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 51

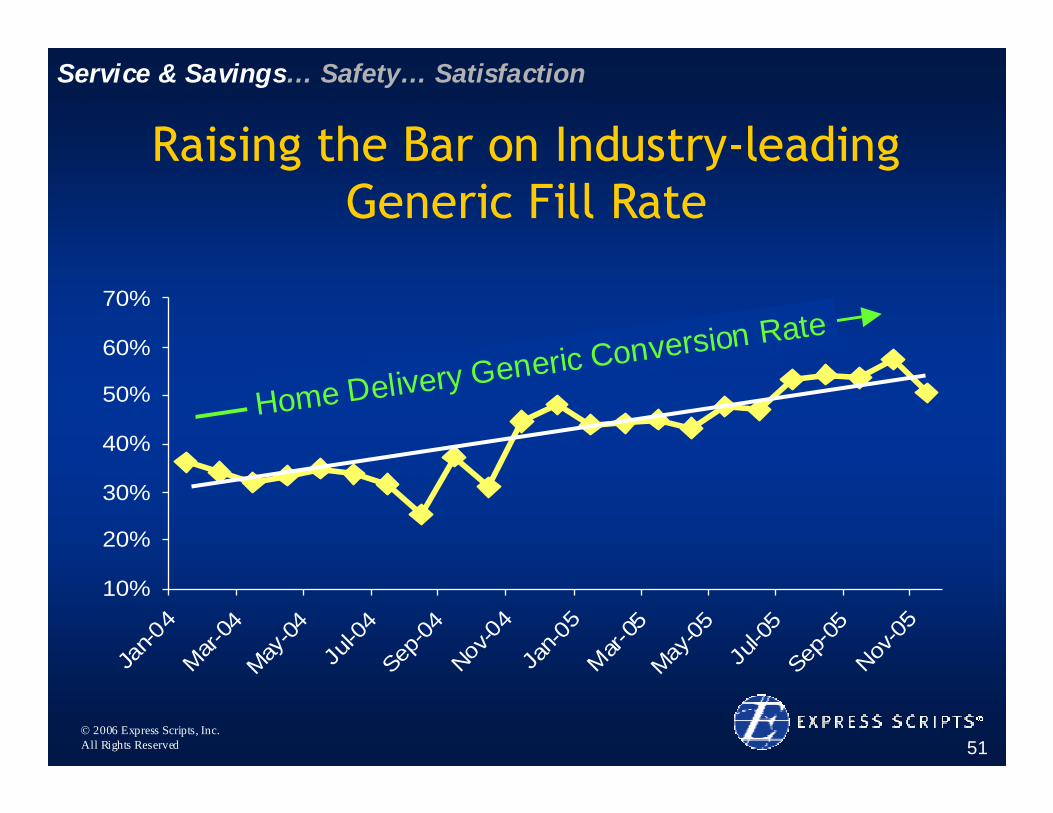

Raising the Bar on Industry-leading Generic Fill Rate

Service & Savings… Safety… Satisfaction

10%

20%

30%

40%

50%

60%

70%

Jan-0

4M

ar-04

May-0

4Ju

l-04

Sep-0

4Nov-0

4Ja

n-05

Mar-

05May

-05

Jul-0

5Sep

-05

Nov-0

5

Home Delivery Generic Conversion Rate

© 2006 Express Scripts, Inc.All Rights Reserved 52

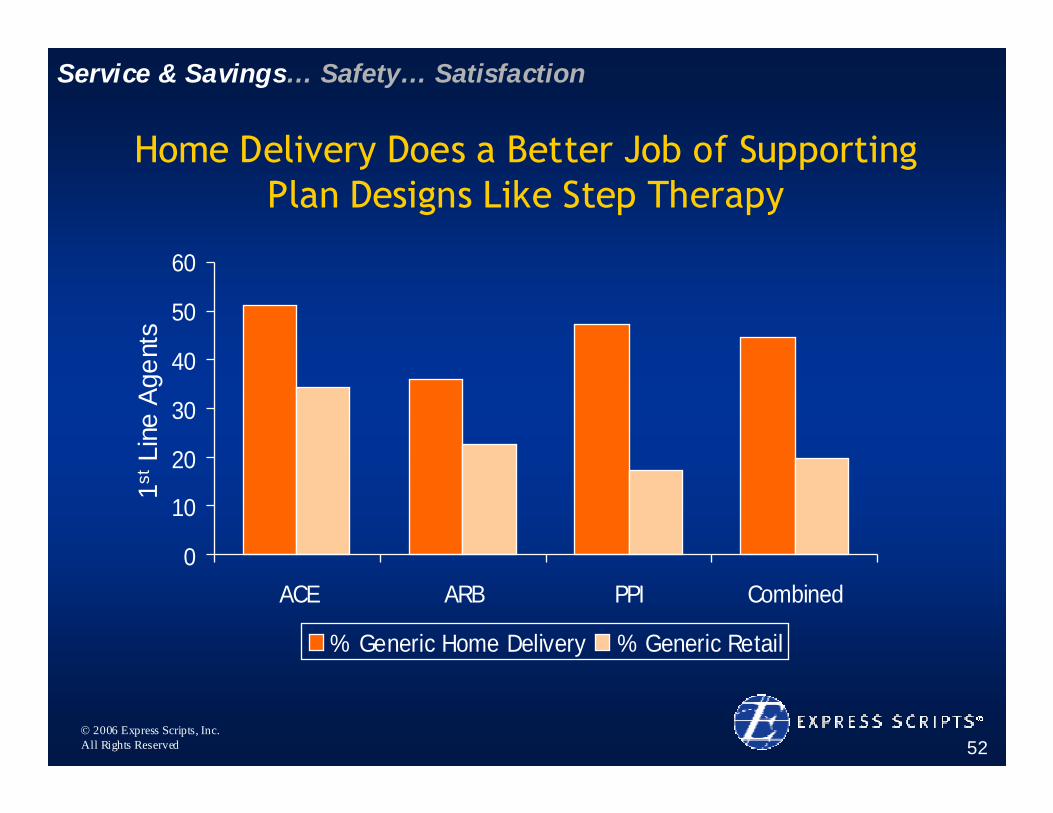

Home Delivery Does a Better Job of Supporting Plan Designs Like Step Therapy

0

10

20

30

40

50

60

ACE ARB PPI Combined

% Generic Home Delivery % Generic Retail

1stLi

ne A

gent

s

Service & Savings… Safety… Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 53

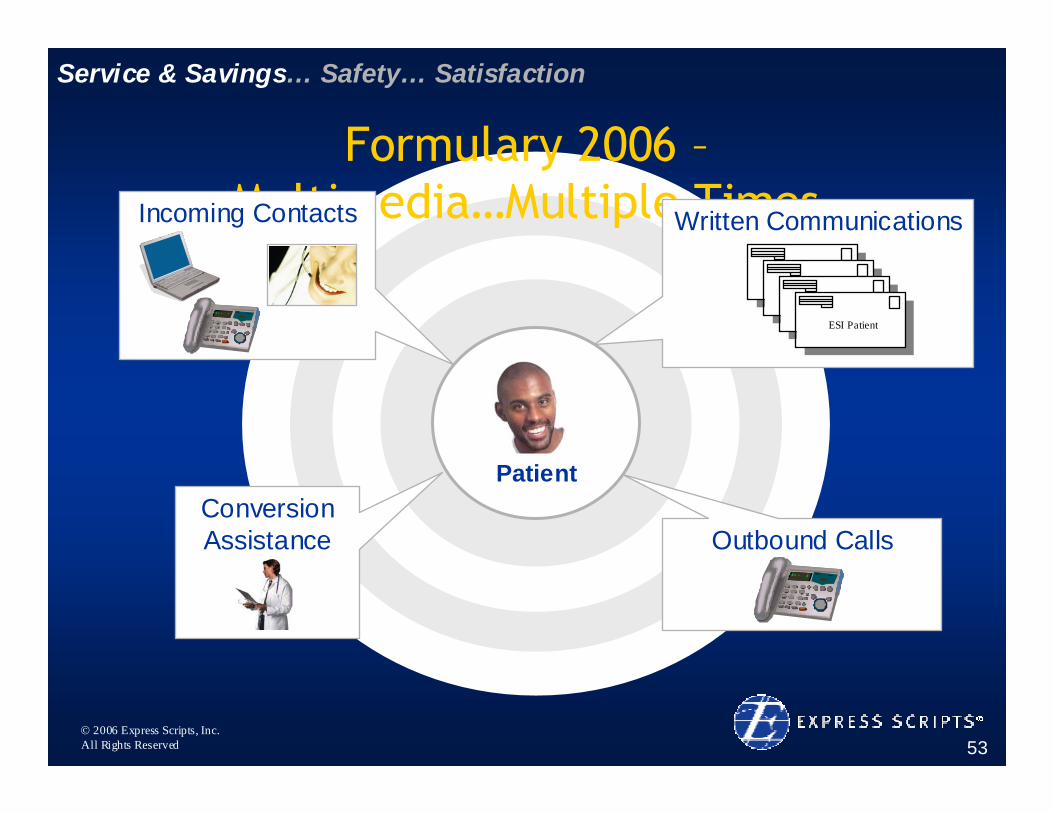

Service & Savings… Safety… Satisfaction

Patient

Formulary 2006 –Multimedia…Multiple TimesWritten CommunicationsIncoming Contacts

Conversion Assistance Outbound Calls

ESI Patient

© 2006 Express Scripts, Inc.All Rights Reserved 54

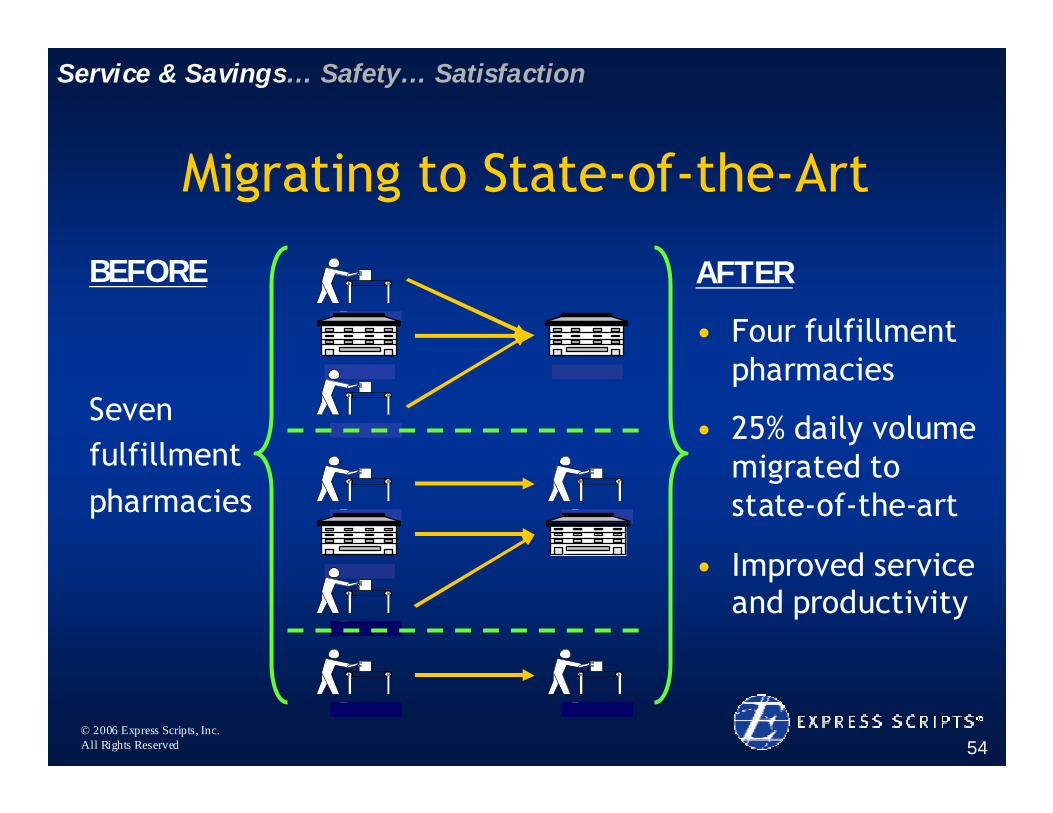

Migrating to State-of-the-Art

Service & Savings… Safety… Satisfaction

BEFORE

Seven fulfillment pharmacies

AFTER

• Four fulfillment pharmacies

• 25% daily volume migrated to state-of-the-art

• Improved service and productivity

© 2006 Express Scripts, Inc.All Rights Reserved 55

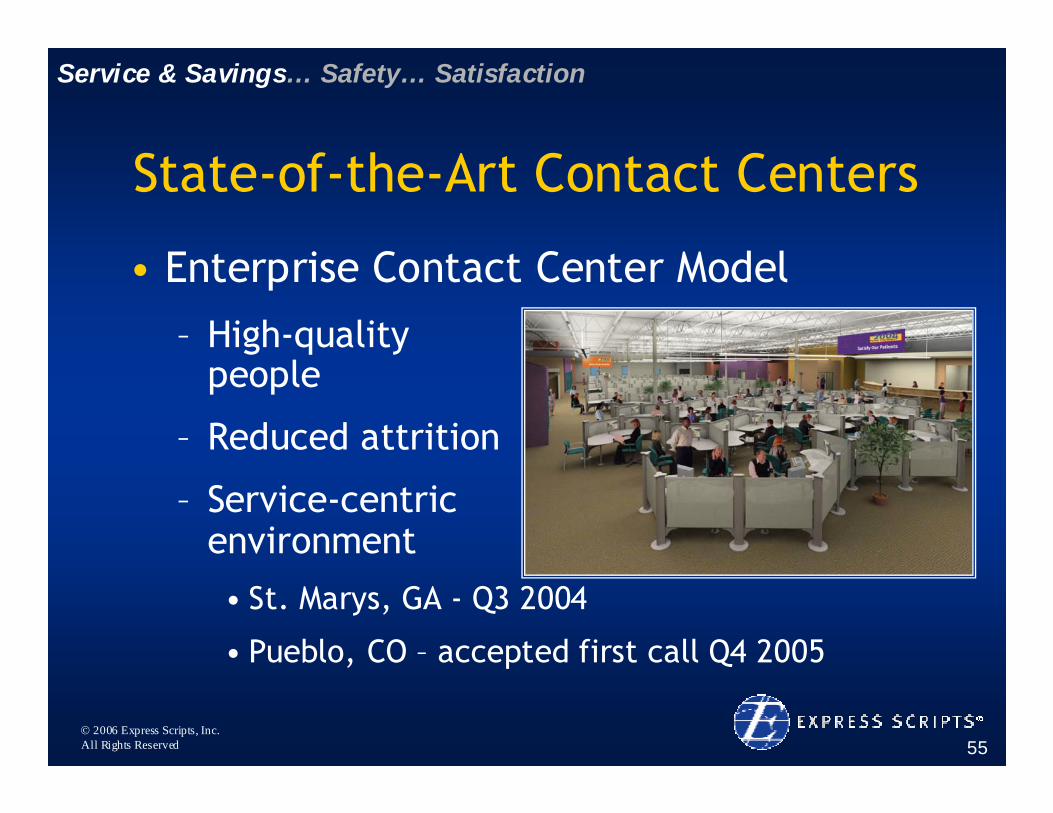

State-of-the-Art Contact Centers

• Enterprise Contact Center Model

– High-quality people

– Reduced attrition

– Service-centric environment • St. Marys, GA - Q3 2004

• Pueblo, CO – accepted first call Q4 2005

Service & Savings… Safety… Satisfaction

© 2006 Express Scripts, Inc.All Rights Reserved 56

Safety: Value Proposition Exceeds Retail

• Leveraging technology– Home Delivery quality 60 times better

than retail1

– Auto-Pack Technology

• Multiple safety checks inherent in process– Integrated on-line DUR– Sound-alike drugs

Service & Savings… Safety… Satisfaction

1 Dispensing Error Rate in a Highly Automated Mail-Service Pharmacy Practice, Pharmacotherapy 2005, 25(11): 1629-1635

© 2006 Express Scripts, Inc.All Rights Reserved 57

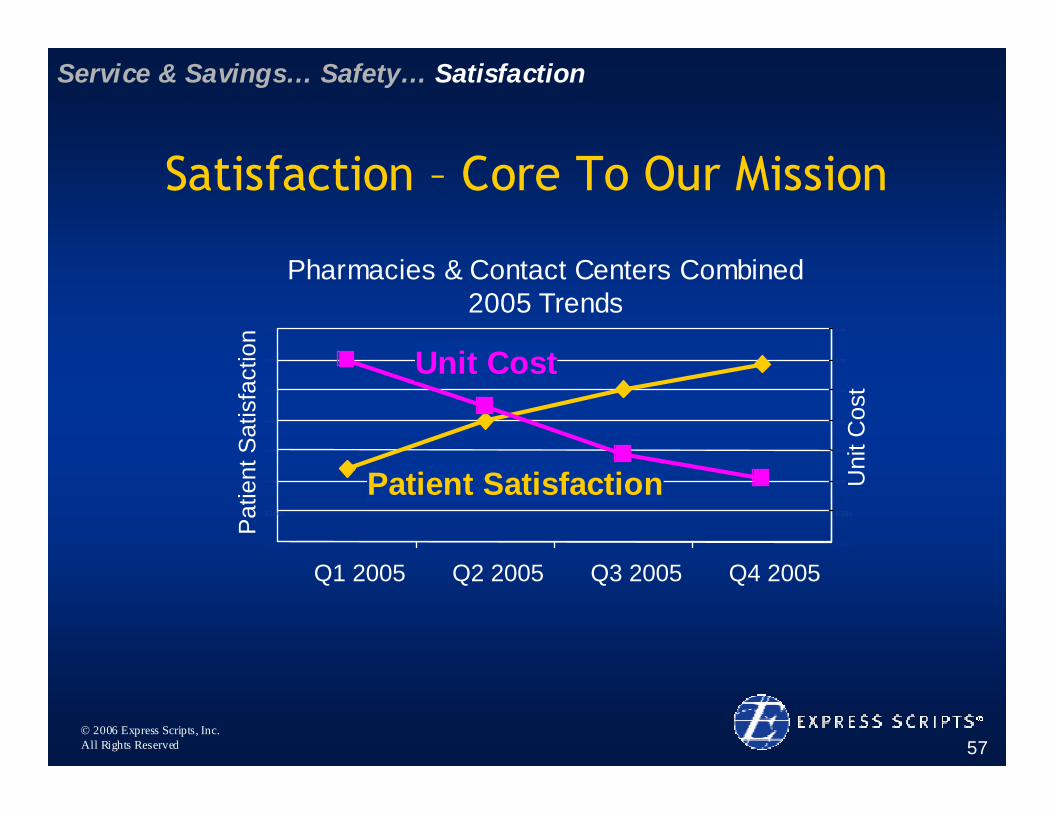

Satisfaction – Core To Our Mission

Service & Savings… Safety… Satisfaction

Pharmacies & Contact Centers Combined2005 Trends

60.0%

62.0%

64.0%

66.0%

68.0%

70.0%

72.0%

74.0%

Q1 2005 Q2 2005 Q3 2005 Q4 2005

Pat

ient

Sat

isfa

ctio

n

2.450

2.500

2.550

2.600

2.650

2.700

2.750

2.800

Uni

t Cos

t

Patient Satisfaction

Unit Cost

© 2006 Express Scripts, Inc.All Rights Reserved 58

Why Express Scripts?• Differentiation Through Alignment

– Service + Safety + Quality = Satisfaction

• Strategic Execution– Investments in people, infrastructure,

quality

• Room to Run– Generics and home delivery: Platforms for

long-term growth

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

Medicare: A Continuing Opportunity For Employers

Brenda MotheralSenior Vice President

Research and Product Management

© 2006 Express Scripts, Inc.All Rights Reserved 60

• Grow with our clients by becoming the most trusted Part D advisor for both employers and health plans

― Full suite of services

― Best-in-class modeling and consulting

― Flawless execution

Medicare Part D 2006 Strategy

© 2006 Express Scripts, Inc.All Rights Reserved 61

• Managed care: 32 MA-PDs and 14 PDPs, representing more than 600,000 lives

• Two direct PDPs

• More than 300 subsidy clients, representing more than 1 million lives

• Excellent execution in all operational areas

Our Approach Worked

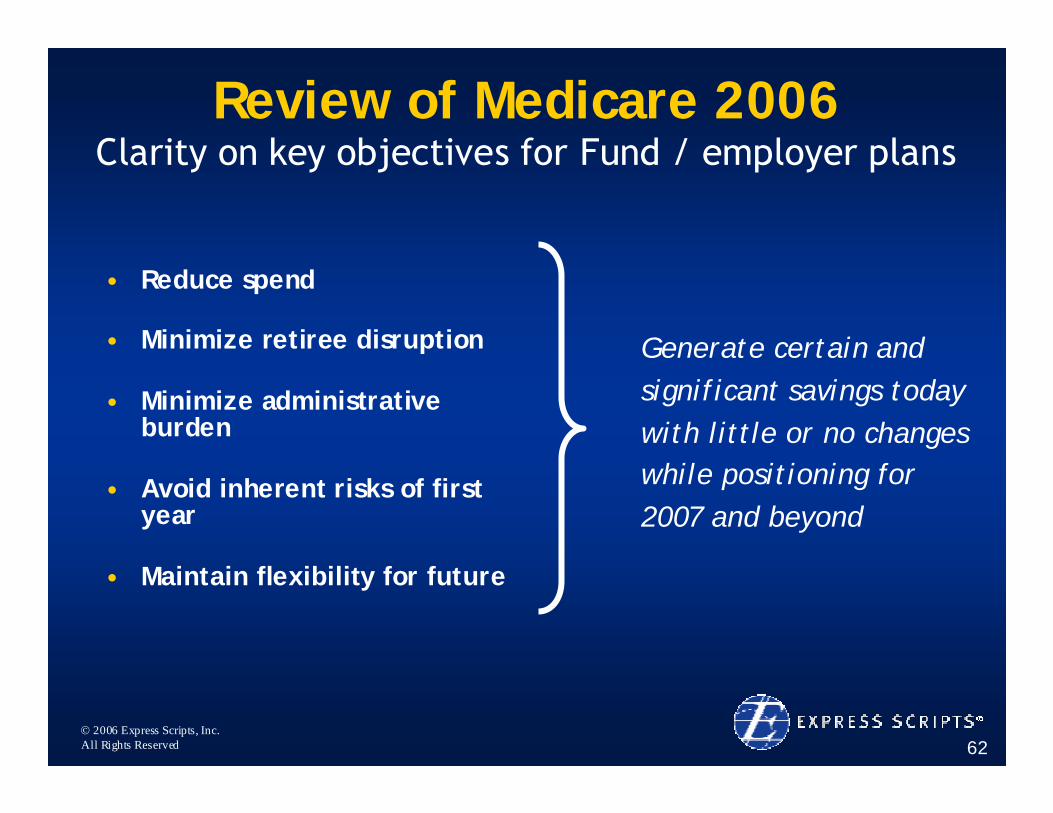

© 2006 Express Scripts, Inc.All Rights Reserved 62

Generate certain and significant savings today with little or no changes while positioning for 2007 and beyond

Review of Medicare 2006Clarity on key objectives for Fund / employer plans

• Reduce spend

• Minimize retiree disruption

• Minimize administrative burden

• Avoid inherent risks of first year

• Maintain flexibility for future

© 2006 Express Scripts, Inc.All Rights Reserved 63

Select option that balances savings and retiree impact subject to administrative resources

Looking to Medicare 2007Clarity on key objectives for Fund / employer plans

• Reduce spend

• Minimize retiree disruption

• Minimize administrative burden

© 2006 Express Scripts, Inc.All Rights Reserved 64

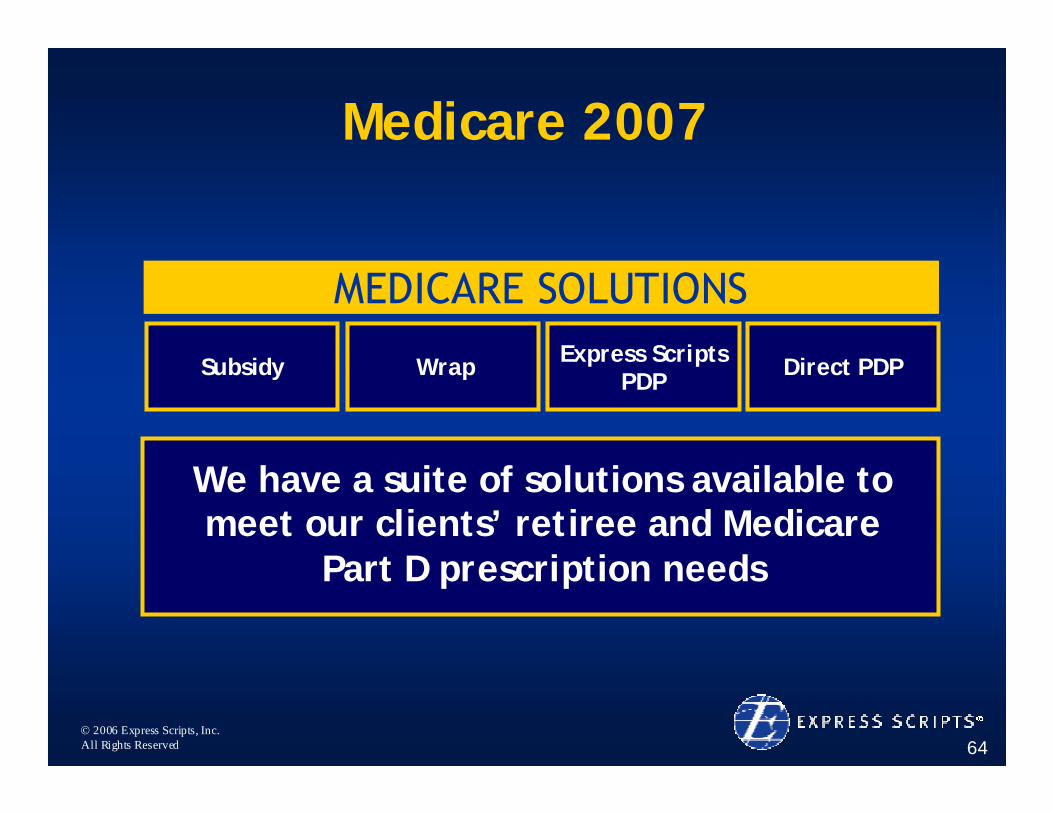

Medicare 2007

MEDICARE SOLUTIONS

WrapSubsidy Express Scripts PDP Direct PDP

We have a suite of solutions available to meet our clients’ retiree and Medicare

Part D prescription needs

© 2006 Express Scripts, Inc.All Rights Reserved 65

Medicare 2007

Express Scripts PDP

MEDICARE SOLUTIONS

Wrap Direct PDPSubsidy

• Designed to support employers will not market to consumers• Plan sponsor contracts with Express Scripts to provide a Part D

benefit unique to their own retirees• Provides the sponsor an opportunity for additional savings• Waives the sponsor from some Part D requirements• Will support existing benefit design• Will have Medicare compliant formularies that mimic Commercial

© 2006 Express Scripts, Inc.All Rights Reserved 66

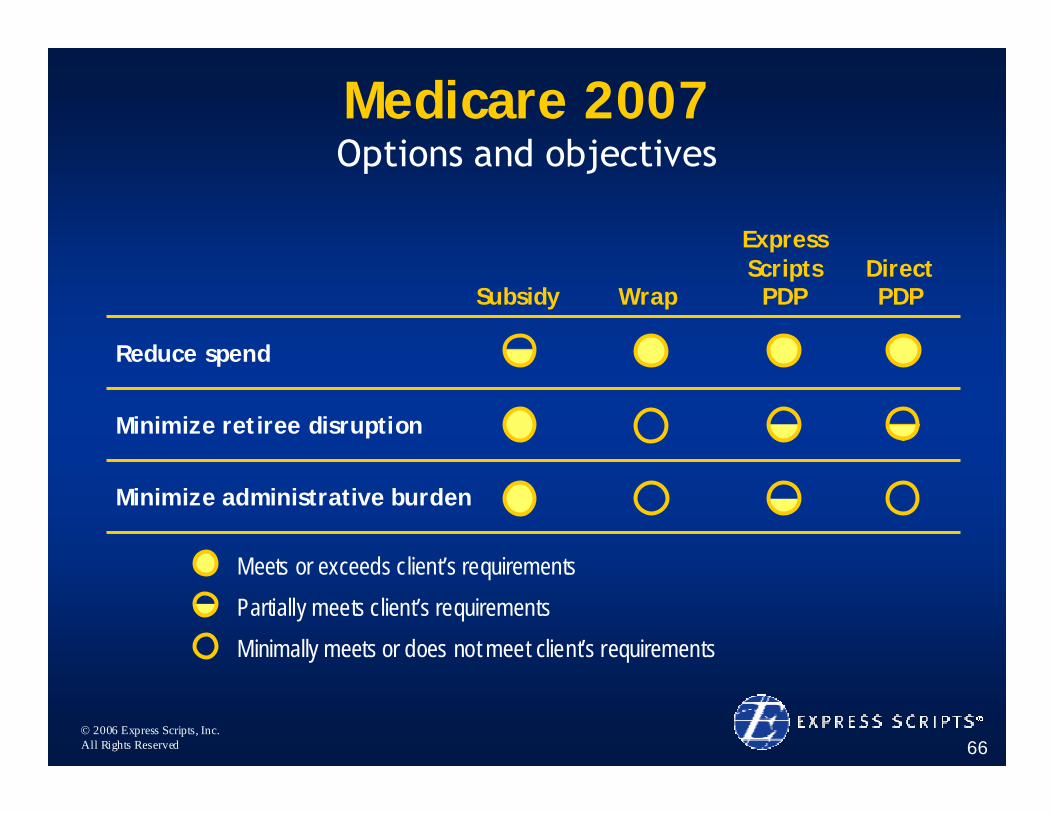

Medicare 2007Options and objectives

Minimize administrative burden

Minimize retiree disruption

Reduce spend

WrapSubsidy

Express Scripts

PDPDirect PDP

Meets or exceeds client’s requirementsPartially meets client’s requirementsMinimally meets or does not meet client’s requirements

© 2006 Express Scripts, Inc.All Rights Reserved 67

• Ongoing changes to meet new CMS requirements for our Part D and subsidy clients

• PDP application and bid

• New capabilities for enrollment and premium collection for the PDP

Preparing For 2007

© 2006 Express Scripts, Inc.All Rights Reserved 68

Why Express Scripts?

• Differentiation Through Alignment– Will not compete with our health plan clients for Medicare

Part D

• Strategic Execution– Best-in-class Medicare operational delivery on 1/1/06

• Room to Run– Offering a PDP to support our employer and labor clients in

2007

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

BREAK

© 2006 Express Scripts, Inc.All Rights Reserved

Building thePathway to the Patientfor Biopharmaceuticals

Dom MeffeSenior Vice President, Specialty Pharmacy

© 2006 Express Scripts, Inc.All Rights Reserved 71

Strategic Drivers

• We’re playing in a high growth market• ESI is aggressively investing in this segment• We bought Priority Healthcare to

– achieve scale and realize synergies– broaden our delivery platform– leverage our upselling success

• All built on a foundation of extraordinary patient care, which no one does better

© 2006 Express Scripts, Inc.All Rights Reserved 72

What Are Specialty Medications?

Specialty drugs are high-cost injectable, infused, oral or inhaled drugs that generally require close supervision and monitoring of the patient’s drug therapy

© 2006 Express Scripts, Inc.All Rights Reserved 73

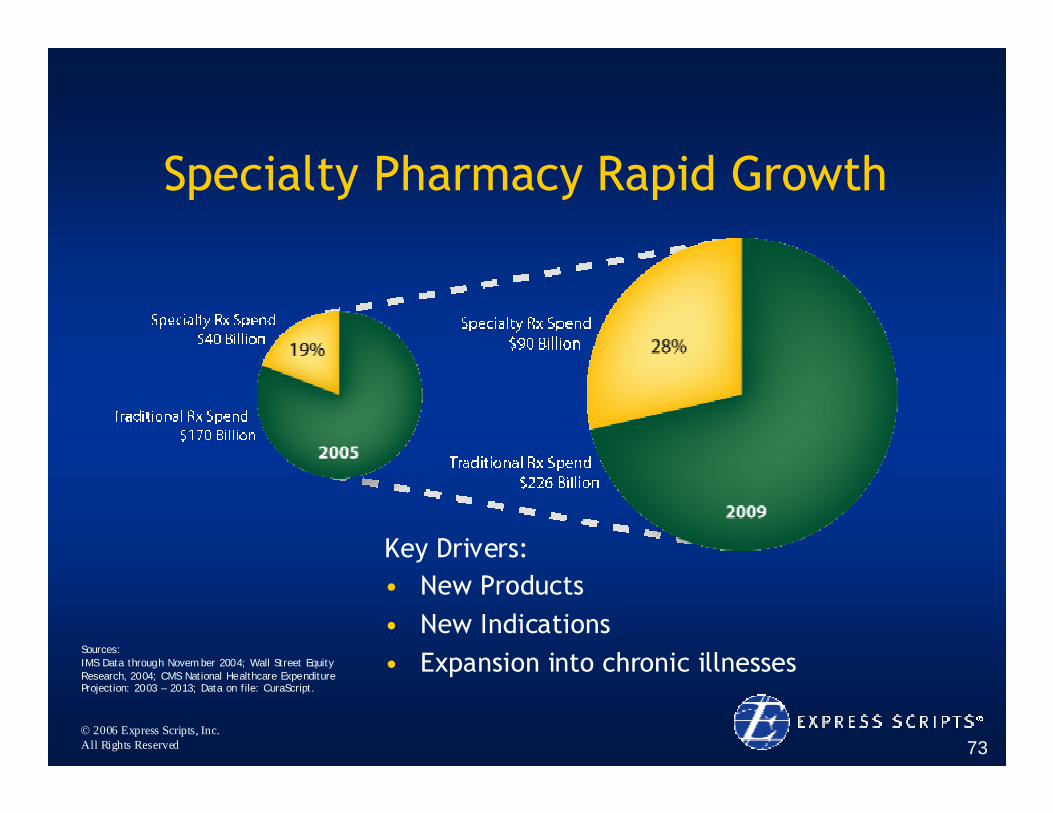

Specialty Pharmacy Rapid Growth

Key Drivers:• New Products• New Indications• Expansion into chronic illnesses

Sources:IMS Data through Novem ber 2004; Wall Street Equity Research, 2004; CMS National Healthcare Expenditure Projection: 2003 – 2013; Data on file: CuraScript.

© 2006 Express Scripts, Inc.All Rights Reserved 74

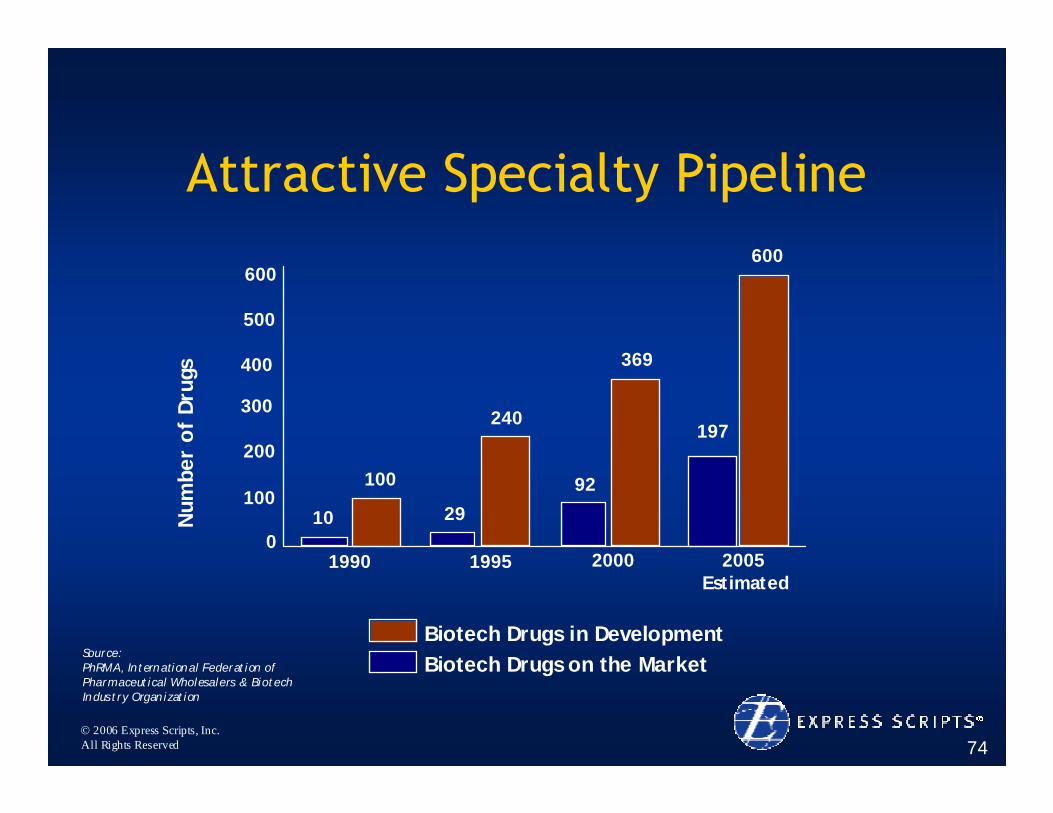

Attractive Specialty Pipeline

Source:PhRMA, International Federation of Pharmaceutical Wholesalers & Biotech Indus try Organization

Biotech Drugs in DevelopmentBiotech Drugs on the Market

2005Estimated

200019951990

600

500

400

300

200

100

0

600

197

369

92

240

29

100

10Num

ber

of

Dru

gs

© 2006 Express Scripts, Inc.All Rights Reserved 75

Why Acquire Priority Healthcare?

• Scale and Synergies

• Breadth of Distribution Platform

• Leverage Proven Upsell Capabilities

© 2006 Express Scripts, Inc.All Rights Reserved 76

Scale and Synergies

© 2006 Express Scripts, Inc.All Rights Reserved 77

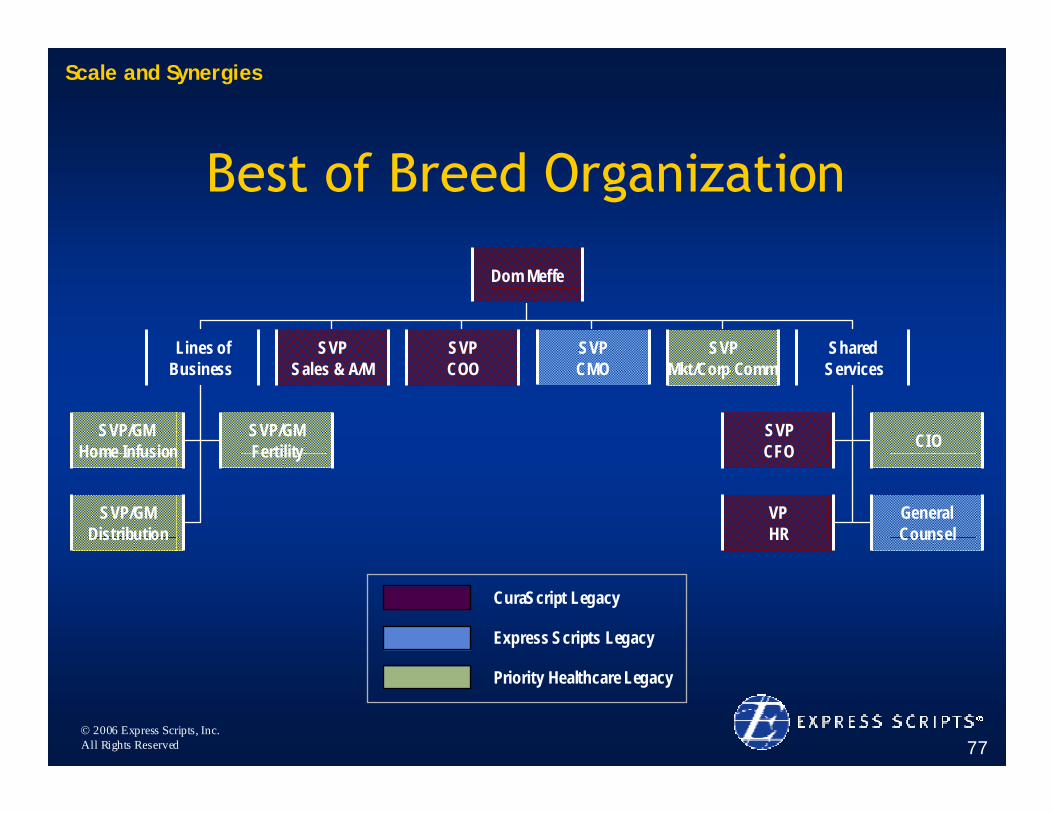

Best of Breed Organization

Dom Meffe

Lines ofBusiness

GeneralCounsel

SVPSales & A/M

SVPCOO

SVPCMO

SVPMkt/Corp Comm

SVPCFO CIO

VPHR

SharedServices

SVP/GM Home Infusion

SVP/GMFertility

SVP/GMDistribution

CuraScript Legacy

Express Scripts Legacy

Priority Healthcare Legacy

Scale and Synergies

© 2006 Express Scripts, Inc.All Rights Reserved 78

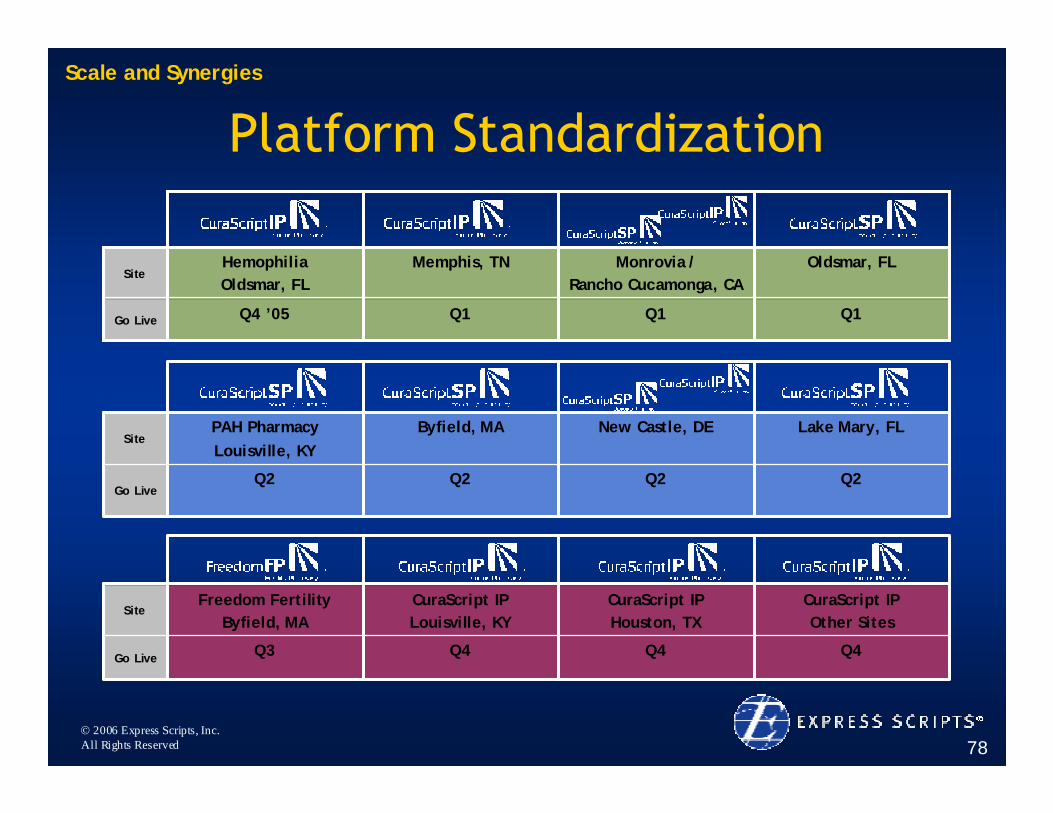

Platform Standardization

Q1

Monrovia / Rancho Cucamonga, CA

Q1

Memphis, TN

Q4 ’05

HemophiliaOldsmar, FL

Q1

Oldsmar, FL

Go Live

Site

Q2Q2Q2Q2Go Live

Lake Mary, FLNew Castle, DEByfield, MAPAH PharmacyLouisville, KY

Site

Q4Q4Q4Q3Go Live

CuraScript IPOther Sites

CuraScript IPHouston, TX

CuraScript IPLouisville, KY

Freedom FertilityByfield, MA

Site

Scale and Synergies

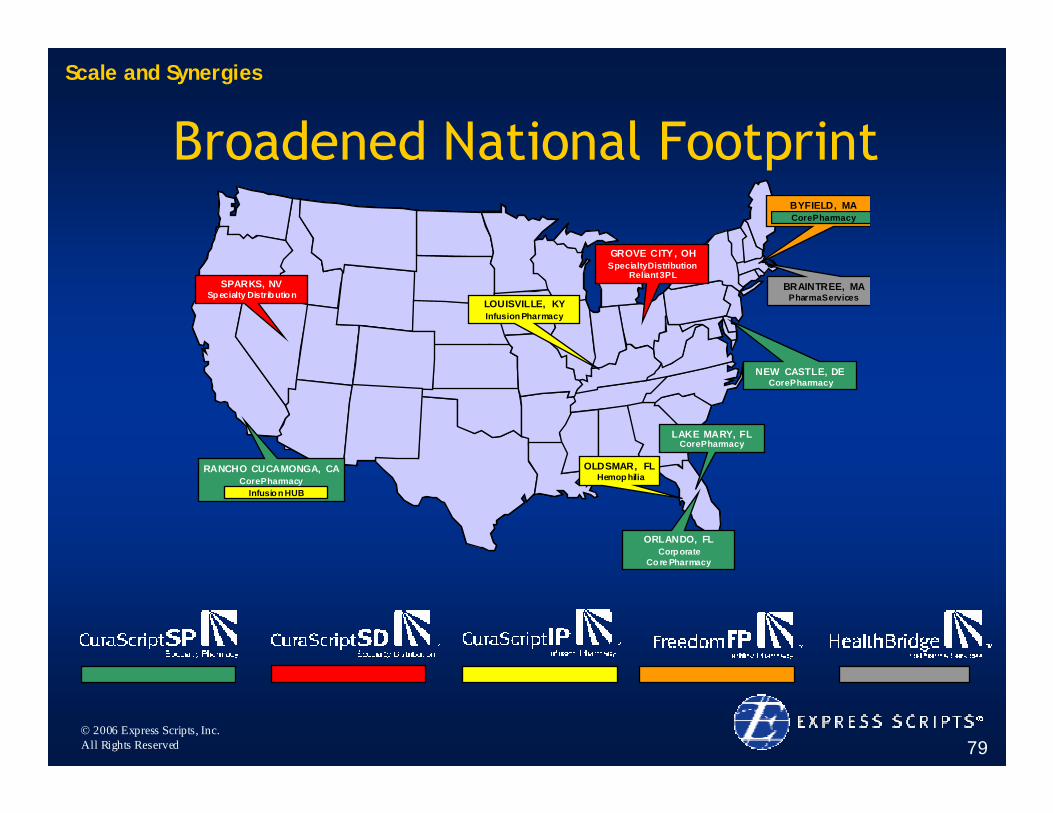

© 2006 Express Scripts, Inc.All Rights Reserved 79

EASTERN

REG ION

CENTRAL

REG ION

W ESTERN

REGION

LOUISVILLE, KYInfusion Pharmacy

LAKE MARY, FLCore Pharmacy

GROVE CITY , OHSpecialty Distribution

Reliant 3PL

OLDSMAR, FLHemop hilia

SPARKS, NVSp ecialty Distrib utio n

BYFIELD, MACore Pharmacy

NEW CASTLE, DECore Pharmacy

RANCHO CUCAMONGA, CACore Pharmacy

Infusio n HUB

ORLANDO, FLCorp orate

Co re Pharmacy

BRAINTREE, MAPharma Services

Broadened National FootprintScale and Synergies

© 2006 Express Scripts, Inc.All Rights Reserved 80

Enhanced Purchasing Power

Scale and Synergies

© 2006 Express Scripts, Inc.All Rights Reserved 81

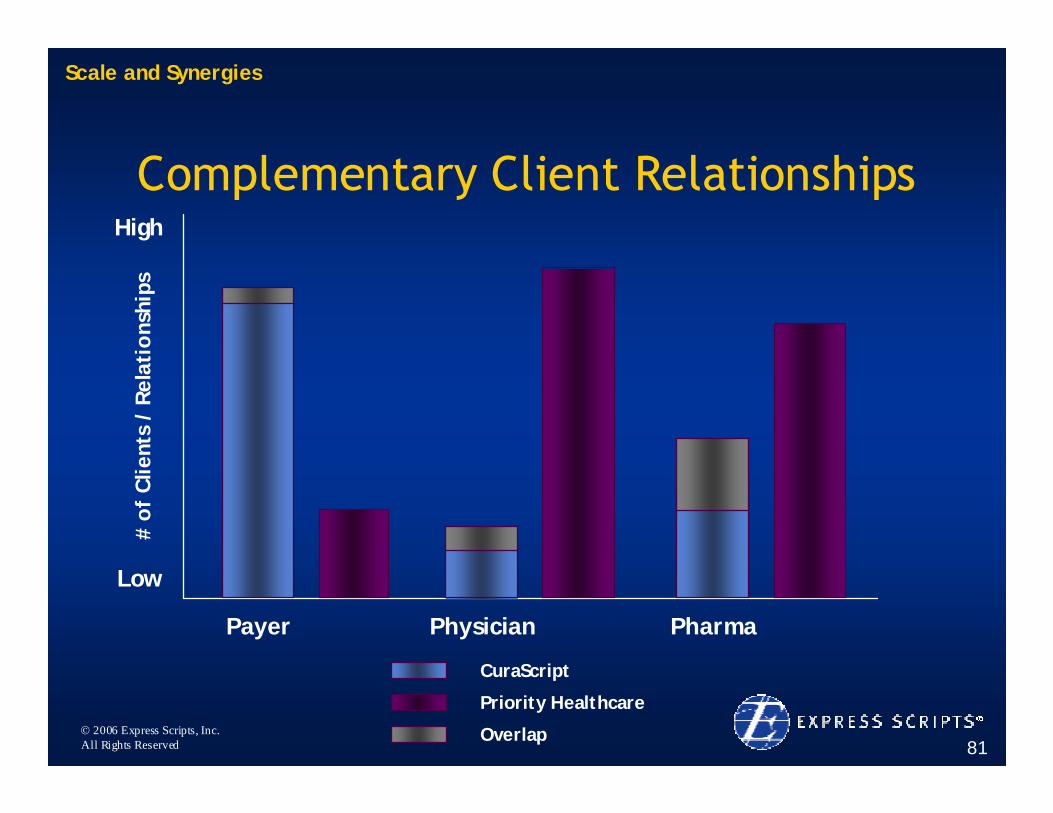

Complementary Client Relationships

Scale and Synergies

CuraScript

Priority Healthcare

Overlap

Payer Physician Pharma

Low

High

# o

f C

lient

s /

Rela

tio

nshi

ps

© 2006 Express Scripts, Inc.All Rights Reserved 82

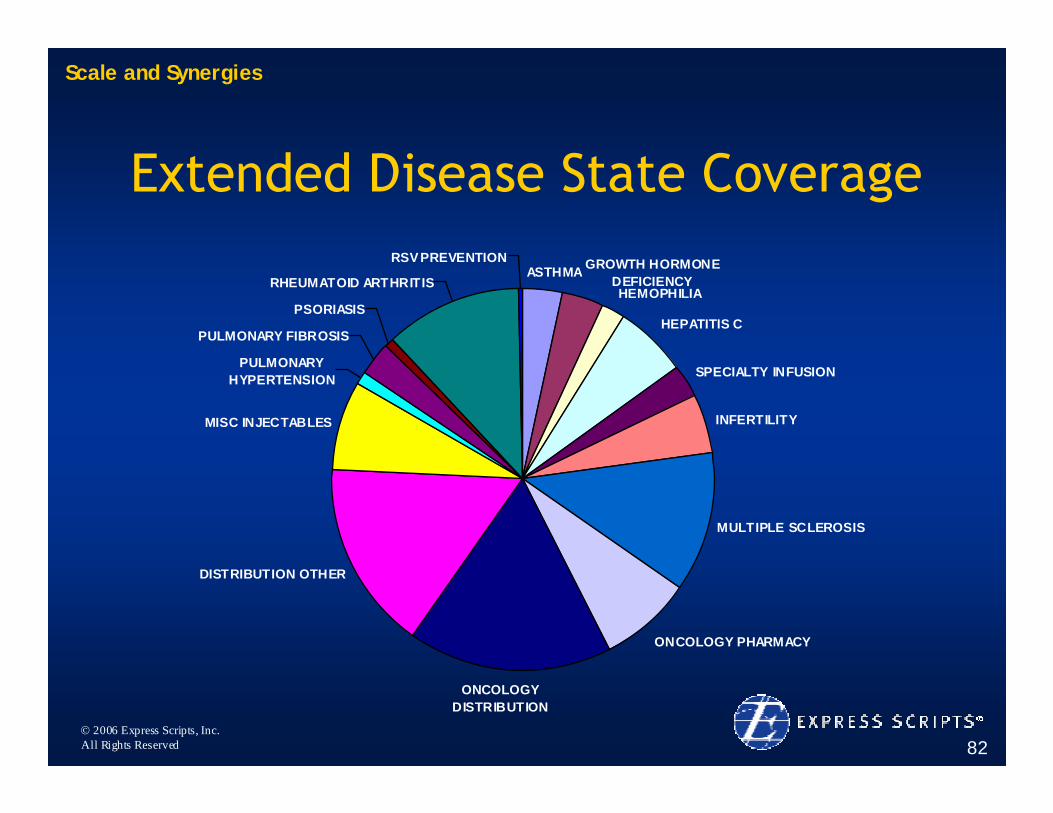

Extended Disease State Coverage

ASTHMA GROWTH HORMONE DEFICIENCYHEMOPHILIA

HEPATITIS C

SPECIALTY INFUSION

INFERTILITY

MULTIPLE SCLEROSIS

ONCOLOGY PHARMACY

ONCOLOGY DISTRIBUTION

DISTRIBUTION OTHER

MISC INJECTABLES

PULMONARY HYPERTENSION

PULMONARY FIBROSIS

PSORIASIS

RHEUMATOID ARTHRITIS

RSV PREVENTION

Scale and Synergies

© 2006 Express Scripts, Inc.All Rights Reserved 83

Breadth of Distribution Platform

© 2006 Express Scripts, Inc.All Rights Reserved 84

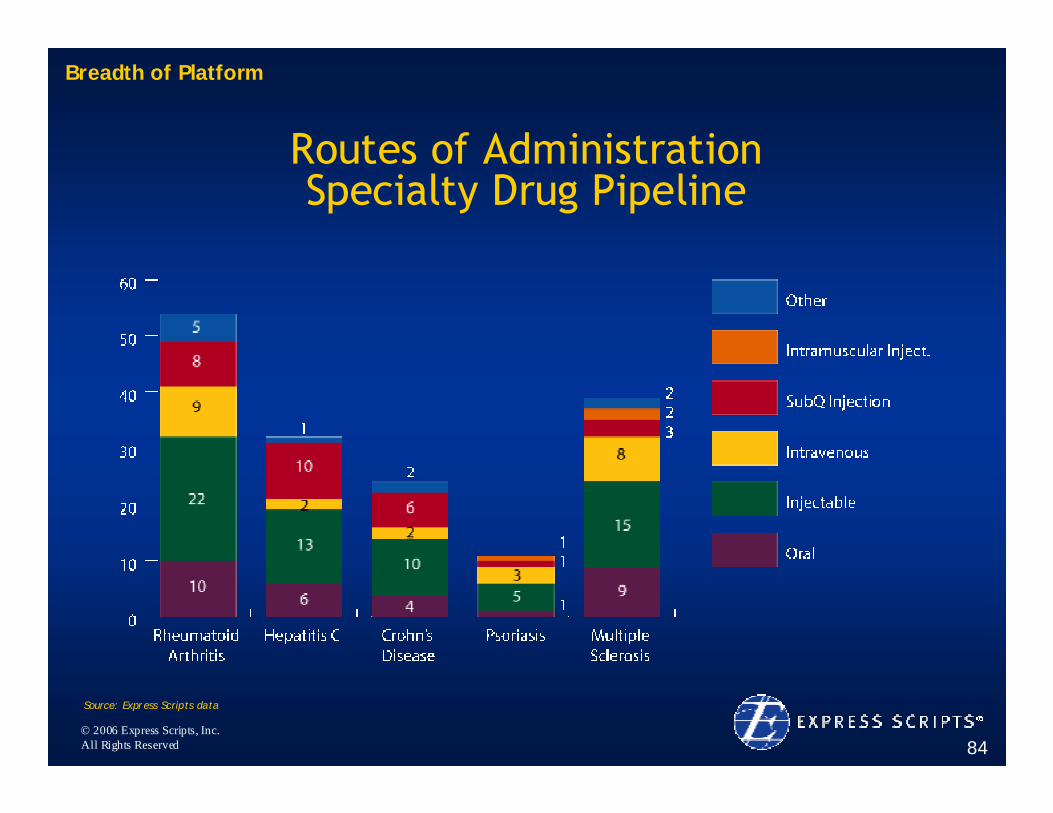

Routes of AdministrationSpecialty Drug Pipeline

Source: Express Scripts data

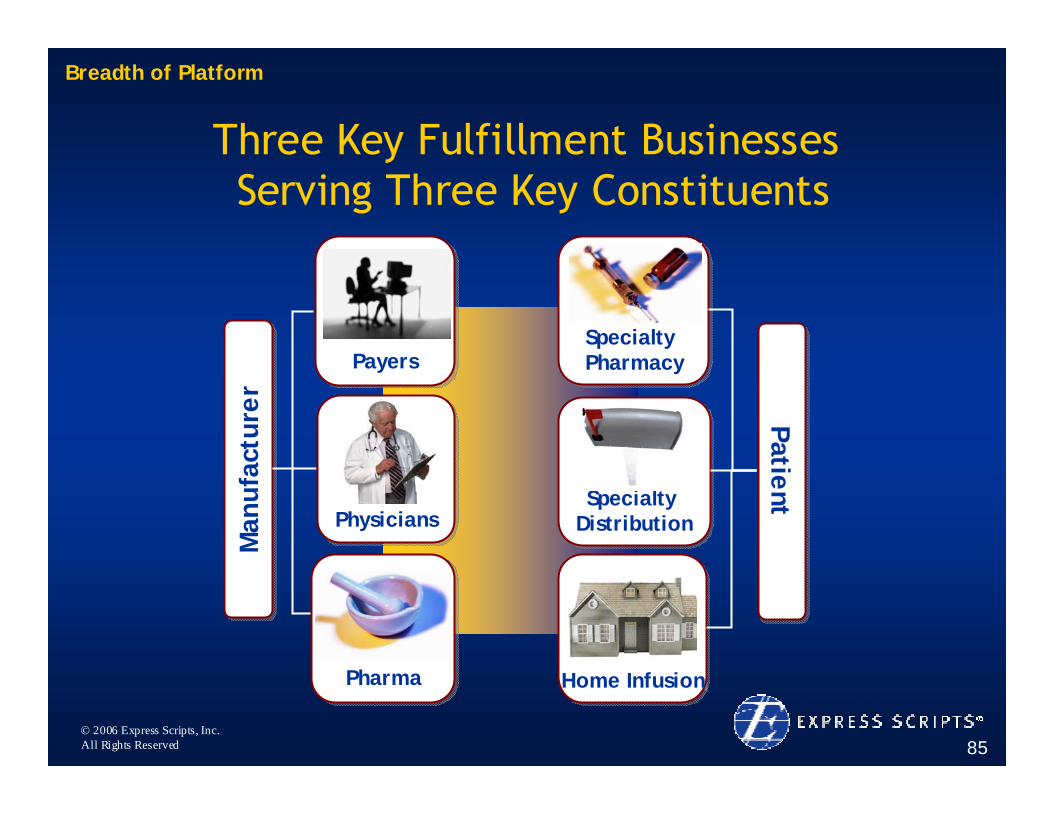

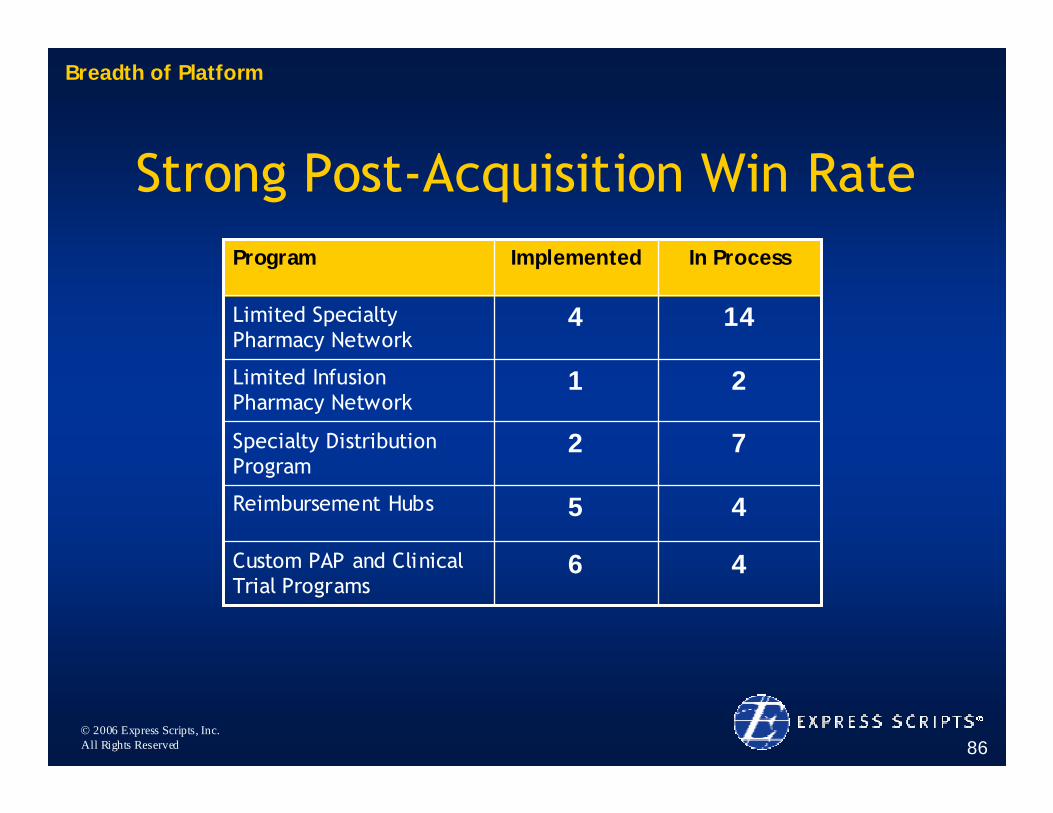

Breadth of Platform

© 2006 Express Scripts, Inc.All Rights Reserved 85

Three Key Fulfillment BusinessesServing Three Key Constituents

Man

ufac

ture

rM

anuf

actu

rer

PhysiciansPhysicians

PharmaPharma

PayersPayers

Home InfusionHome Infusion

Specialty DistributionSpecialty

Distribution

Specialty PharmacySpecialty Pharmacy

PatientPatient

Breadth of Platform

© 2006 Express Scripts, Inc.All Rights Reserved 86

Strong Post-Acquisition Win Rate

46Custom PAP and Clinical Trial Programs

45Reimbursement Hubs

72Specialty Distribution Program

21Limited Infusion Pharmacy Network

144Limited Specialty Pharmacy Network

In ProcessImplementedProgram

Breadth of Platform

© 2006 Express Scripts, Inc.All Rights Reserved 87

Significant Upsell Opportunity

© 2006 Express Scripts, Inc.All Rights Reserved 88

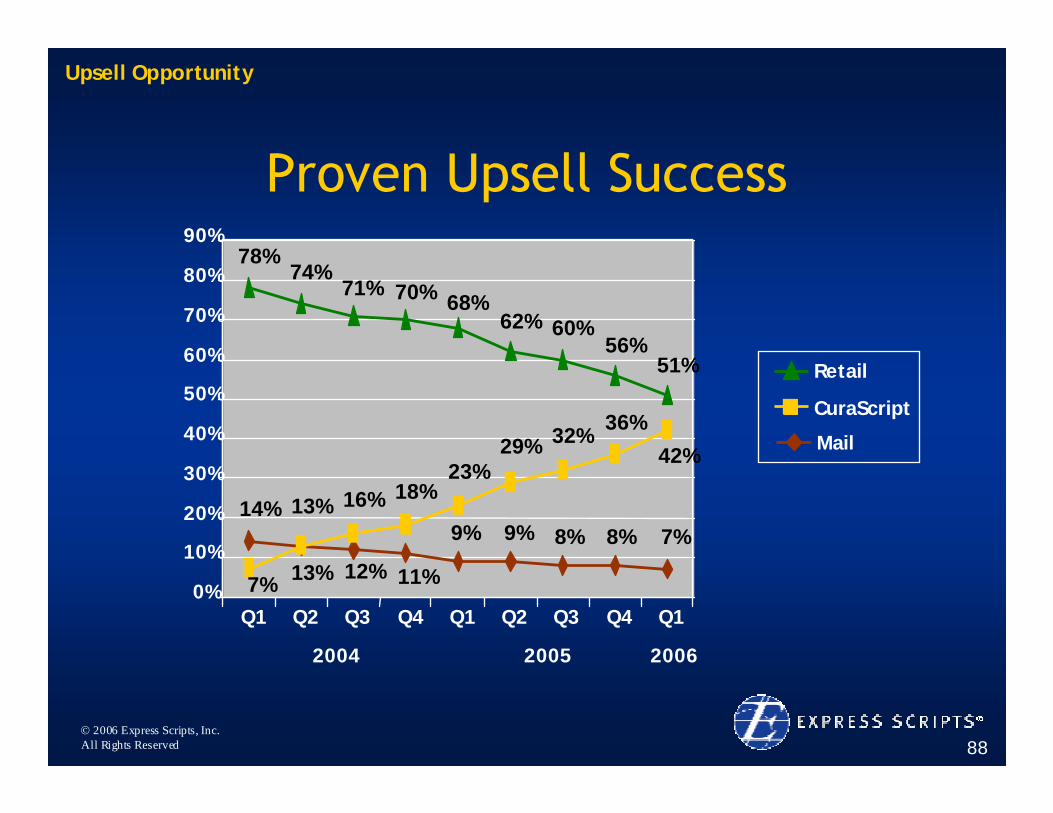

Proven Upsell Success

Upsell Opportunity

7%8%8%9%9%

12%13% 11%

14%

42%36%32%29%

23%18%

13% 16%

7%

71%78%

74%70% 68%

62% 60%56%

51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q1 Q2

2004

Q3 Q4 Q1

2005

Q2 Q3 Q4 Q1

2006

CuraScript

Retail

© 2006 Express Scripts, Inc.All Rights Reserved 89

Impressive New Client Growth

• 813 new clients in 24 months since acquisition

• Exclusive mix growing

Upsell Opportunity

34%Exclusive

66%Preferred

© 2006 Express Scripts, Inc.All Rights Reserved 90

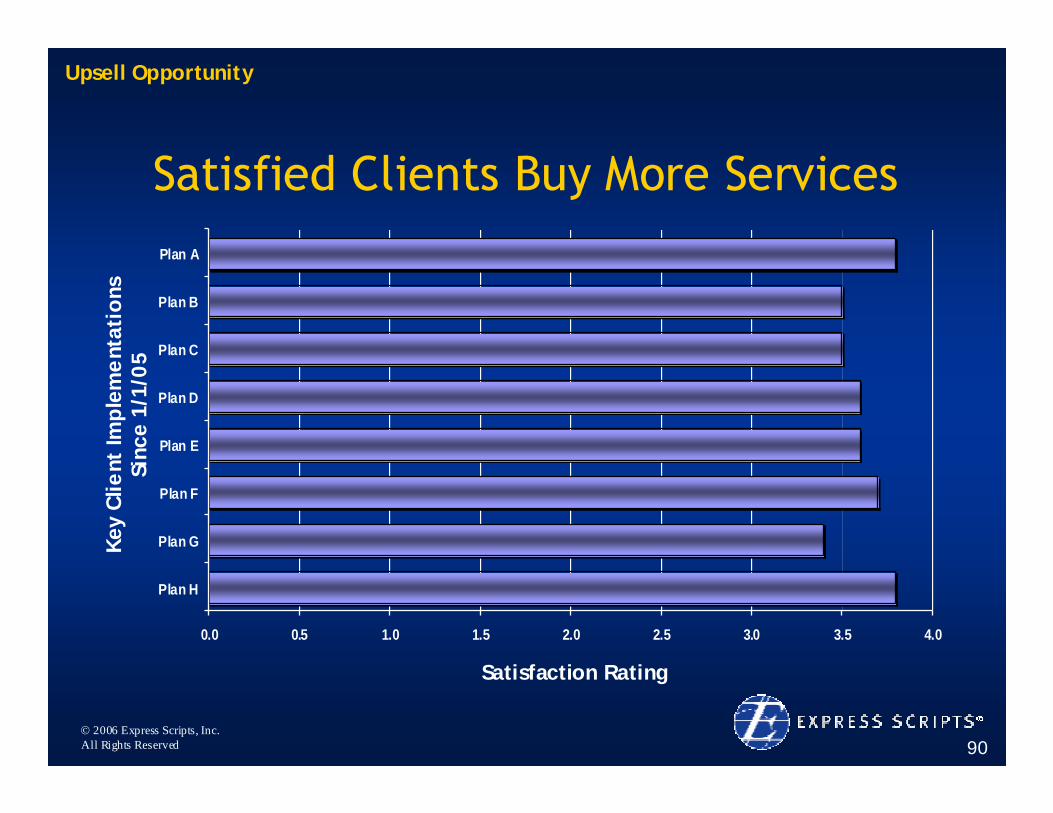

Satisfied Clients Buy More Services

Upsell Opportunity

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

Plan H

Plan G

Plan F

Plan E

Plan D

Plan C

Plan B

Plan A

Satisfaction Rating

Key

Clie

nt Im

ple

me

ntat

ions

Sinc

e 1/

1/0

5

© 2006 Express Scripts, Inc.All Rights Reserved 91

Future Upsell Product Offerings

PulmonaryArterialHypertensionProgram

Fertility Program

Home Infusion Program

Upsell Opportunity

© 2006 Express Scripts, Inc.All Rights Reserved 92

Why Express Scripts?• Differentiation Through Alignment

– A proud legacy of plan sponsor alignment

• Strategic Execution– Growth by managing biologic drug costs, without

compromising health outcomes, while maximizing patient satisfaction

• Room to Run– Specialty pharmacy, specialty infusion, specialty

distribution: Platforms for long-term growth

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

We Are Succeeding In The Marketplace

Ed IgnaczakSenior Vice President

Sales and Account Management

© 2006 Express Scripts, Inc.All Rights Reserved 94

Multiple Factors Being Leveraged To Drive Client/Shareholder Value

We can move the market…….

$ Value to ESI / $ Value to Clients

Satisfaction Satisfaction

Home Delivery

Satisfaction

Home Delivery

Generics

Satisfaction

Home Delivery

Generics

Specialty

Satisfaction

Home Delivery

Generics

Specialty

Pipeline

Satisfaction

Home Delivery

Generics

Specialty

Pipeline

New Sales

# of Leveraged Factors

ESI and Client Values are Aligned

© 2006 Express Scripts, Inc.All Rights Reserved 95

Specialized, Experienced Sales Organization Aligned To Support

Our Client Base

• 500+ Sales Professionals• 80% of employees supporting and maximizing opportunity

with existing clients • Average tenure over 5 years

Ed IgnaczakSVP Sales/

AM

Commercial LaborManaged

CarePublic Sector

Product Sales

Support/Medicare

Analytics / Benefits

ConsultingMarketing

StrategicBusiness

Development

WorkersComp.

Front Line Sales Sales/Client Support

© 2006 Express Scripts, Inc.All Rights Reserved 96

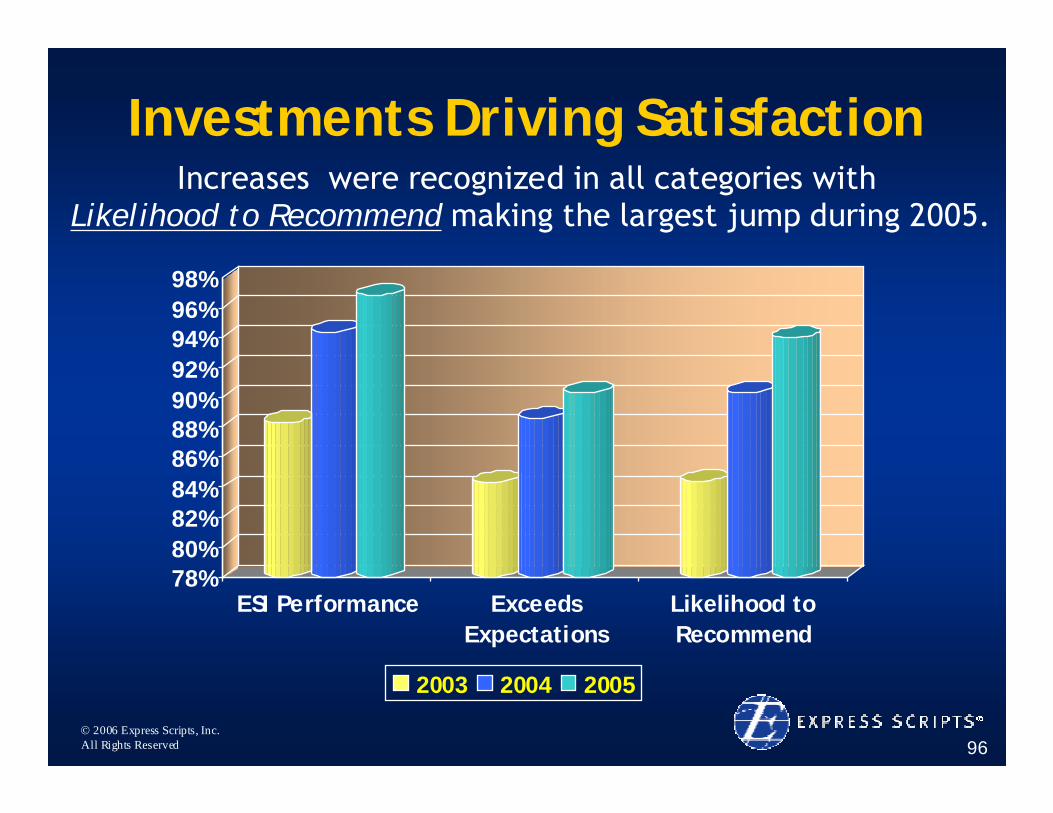

Investments Driving SatisfactionIncreases were recognized in all categories with

Likelihood to Recommend making the largest jump during 2005.

78%80%82%84%86%88%90%92%94%96%98%

ESI Performance ExceedsExpectations

Likelihood toRecommend

2003 2004 2005

© 2006 Express Scripts, Inc.All Rights Reserved 97

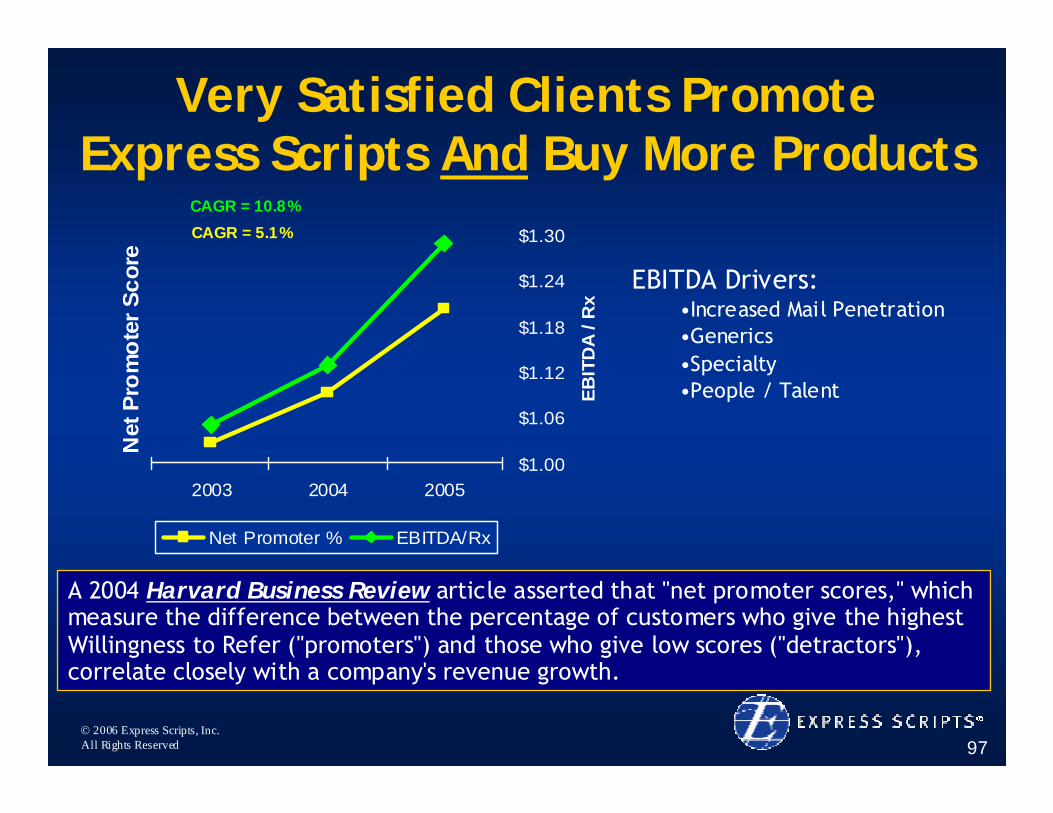

Very Satisfied Clients Promote Express Scripts And Buy More Products

A 2004 Harvard Business Review article asserted that "net promoter scores," which measure the difference between the percentage of customers who give the highest Willingness to Refer ("promoters") and those who give low scores ("detractors"), correlate closely with a company's revenue growth.

2003 2004 2005

Net

Pro

mot

er S

core

$1.00

$1.06

$1.12

$1.18

$1.24

$1.30

EBIT

DA

/ Rx

Net Promoter % EBITDA/Rx

CAGR = 5.1%CAGR = 10.8%

EBITDA Drivers:•Increased Mail Penetration•Generics•Specialty•People / Talent

© 2006 Express Scripts, Inc.All Rights Reserved 98

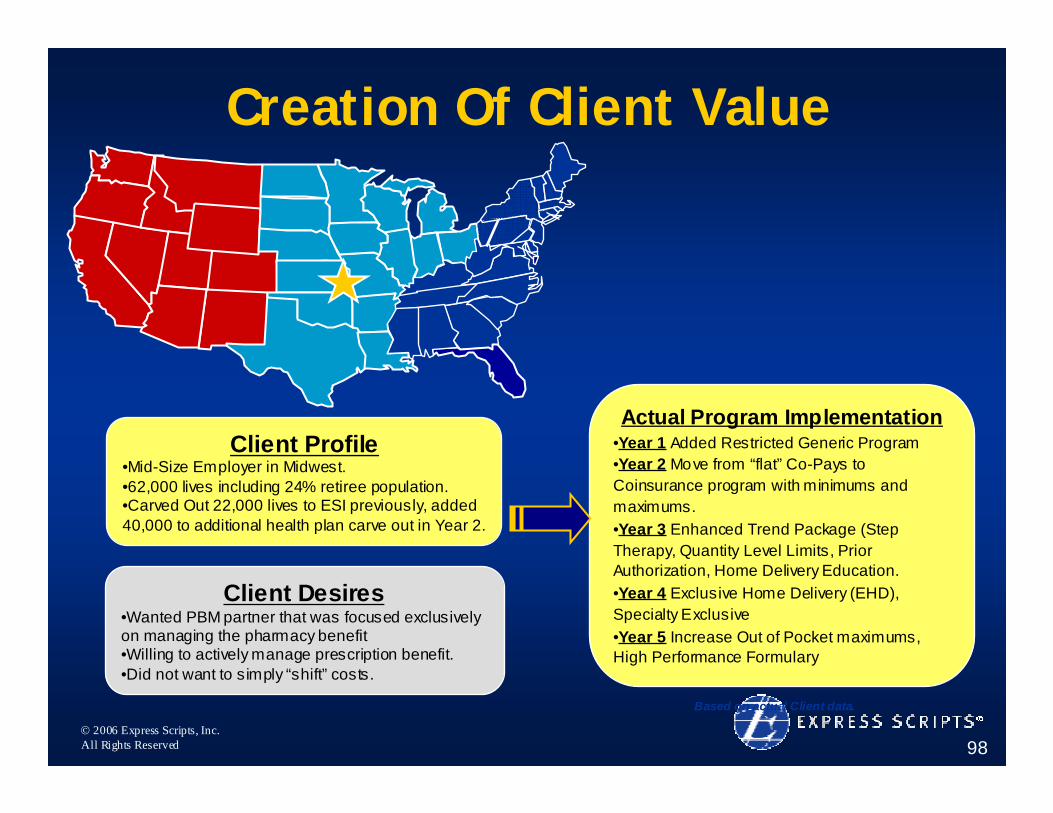

Creation Of Client Value

Client Profile•Mid-Size Employer in Midwest.•62,000 lives including 24% retiree population.•Carved Out 22,000 lives to ESI previously, added 40,000 to additional health plan carve out in Year 2.

Client Desires•Wanted PBM partner that was focused exclusively on managing the pharmacy benefit•Willing to actively manage prescription benefit.•Did not want to simply “shift” costs.

Actual Program Implementation•Year 1 Added Restricted Generic Program•Year 2 Move from “flat” Co-Pays to Coinsurance program with minimums and maximums.•Year 3 Enhanced Trend Package (Step Therapy, Quantity Level Limits, Prior Authorization, Home Delivery Education.•Year 4 Exclusive Home Delivery (EHD), Specialty Exclusive•Year 5 Increase Out of Pocket maximums, High Performance Formulary

Based on actual Client data.

© 2006 Express Scripts, Inc.All Rights Reserved 99

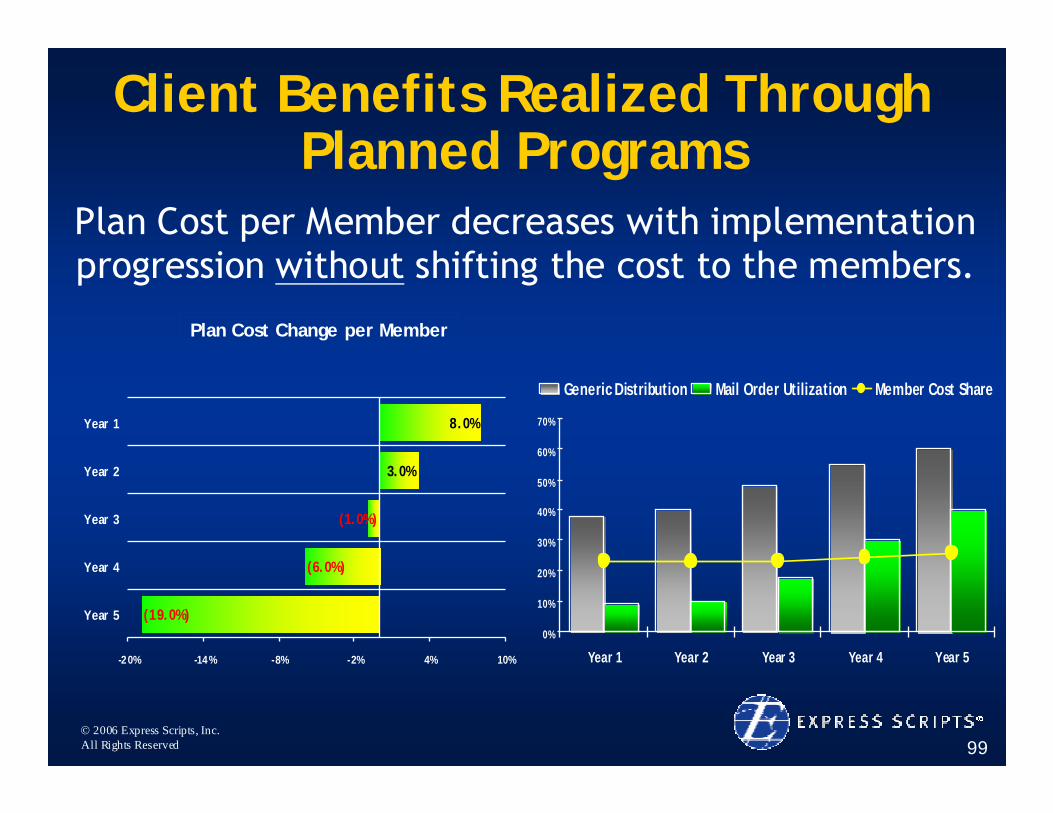

Client Benefits Realized Through Planned Programs

(19.0%)

(6.0%)

(1.0%)

3.0%

8.0%

-20% -14% -8% -2% 4% 10%

Year 5

Year 4

Year 3

Year 2

Year 1

Plan Cost Change per Member

0%

10%

20%

30%

40%

50%

60%

70%

Year 1 Year 2 Year 3 Year 4 Year 5

Generic Distribution Mail Order Utilization Member Cost Share

Plan Cost per Member decreases with implementation progression without shifting the cost to the members.

© 2006 Express Scripts, Inc.All Rights Reserved 100

Multiple Factors Driving New Sales Success. Why WE Win!

0% 100%

People

Specialty

Home Delivery

Medicare Support

Business Model Alignment

Sold!

Coverage/Quality

Strategic Acquisitions

Invest. in Sites/ Tech

Expert Consultation

Lowest Net Cost

When a large Employer changed PBM’s in 2005, they selected Express Scripts 72% of the time!

© 2006 Express Scripts, Inc.All Rights Reserved 101

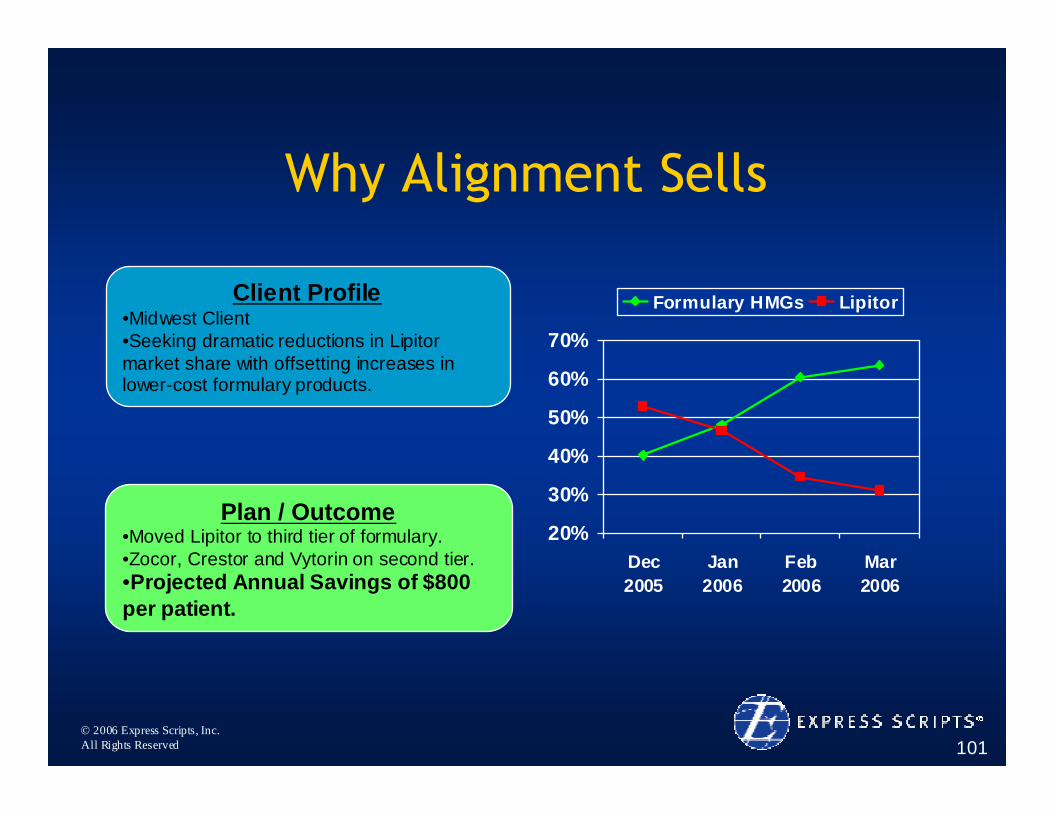

Why Alignment Sells

20%

30%

40%

50%

60%

70%

Dec2005

Jan2006

Feb2006

Mar2006

Formulary HMGs LipitorClient Profile•Midwest Client•Seeking dramatic reductions in Lipitor market share with offsetting increases in lower-cost formulary products.

Plan / Outcome•Moved Lipitor to third tier of formulary.•Zocor, Crestor and Vytorin on second tier.•Projected Annual Savings of $800 per patient.

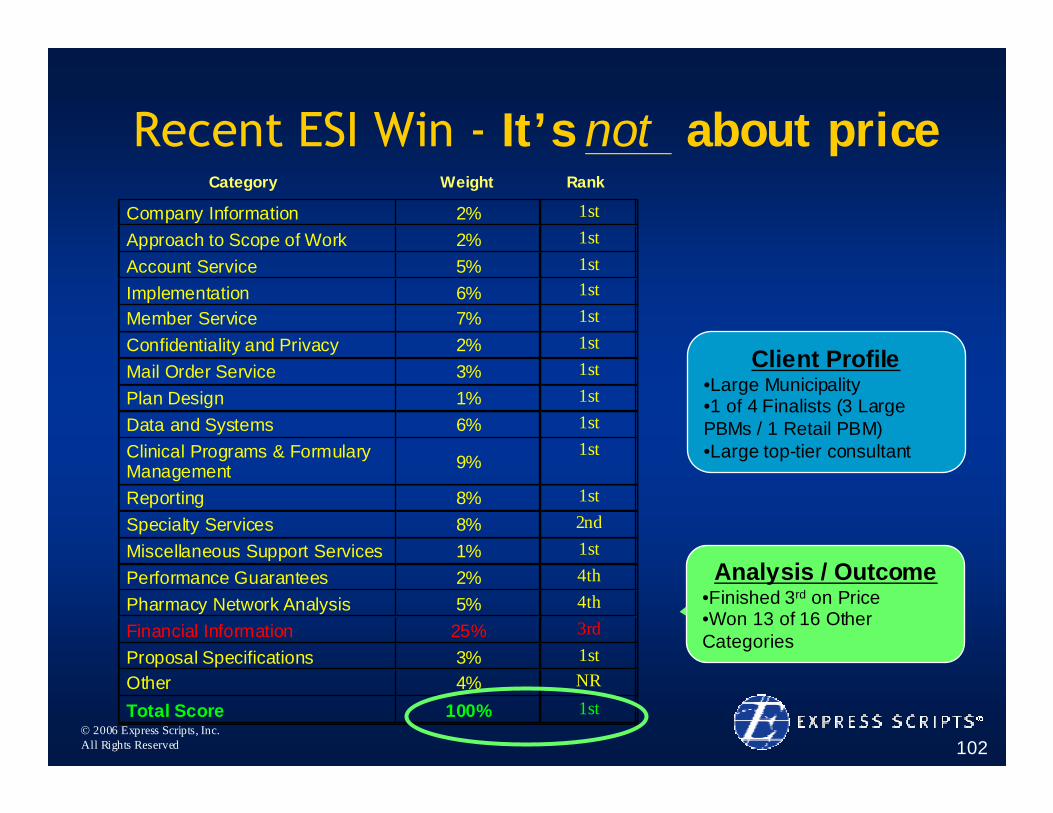

© 2006 Express Scripts, Inc.All Rights Reserved 102

Recent ESI Win - It’s not about priceCompany Information 2% 1st Approach to Scope of Work 2% 1st Account Service 5% 1st Implementation 6% 1st Member Service 7% 1st Confidentiality and Privacy 2% 1st Mail Order Service 3% 1st Plan Design 1% 1st Data and Systems 6% 1st Clinical Programs & Formulary Management 9%

1st

Reporting 8% 1st Specialty Services 8% 2nd Miscellaneous Support Services 1% 1st Performance Guarantees 2% 4th Pharmacy Network Analysis 5% 4th Financial Information 25% 3rd Proposal Specifications 3% 1st Other 4% NR

Total Score 100% 1st

Client Profile•Large Municipality •1 of 4 Finalists (3 Large PBMs / 1 Retail PBM)•Large top-tier consultant

Analysis / Outcome•Finished 3rd on Price•Won 13 of 16 Other Categories

Category Weight Rank

© 2006 Express Scripts, Inc.All Rights Reserved 103

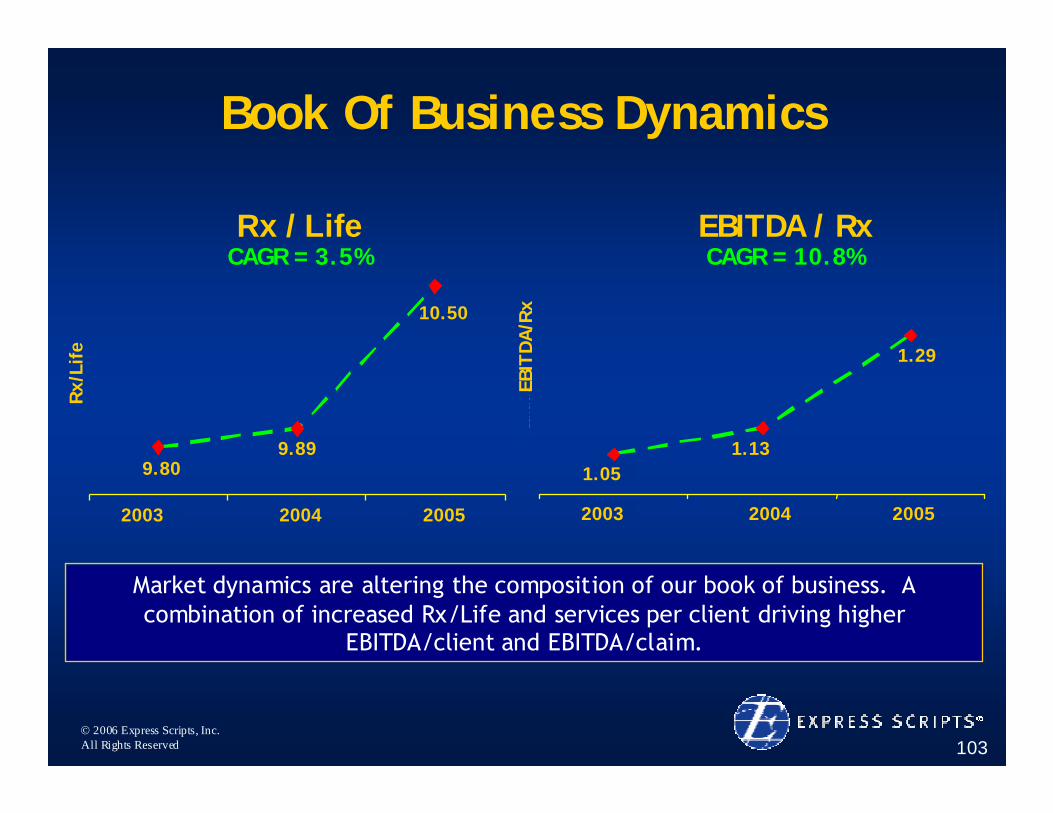

Market dynamics are altering the composition of our book of business. A combination of increased Rx/Life and services per client driving higher

EBITDA/client and EBITDA/claim.

Book Of Business Dynamics

1.05

1.13

1.29

2003 2004 2005

EBIT

DA/R

x

Rx / Life

9.809.89

10.50

2003 2004 2005

Rx /

Life

CAGR = 3.5%

10.50

9.89

200520042003

9.80

Rx/

Life

EBITDA / RxCAGR = 10.8%

1.29

1.131.05

200520042003EB

ITD

A/R

x

© 2006 Express Scripts, Inc.All Rights Reserved 104

Why Express Scripts?• Differentiation Through Alignment

– Alignment sells in the marketplace

• Strategic Execution– Investments in human capital and service

initiatives

• Room to Run– Significant upsell opportunities and targeted

organic growth

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

Focus On Margin Enhancement And ROIC

Ed StiftenCFO

© 2006 Express Scripts, Inc.All Rights Reserved 106

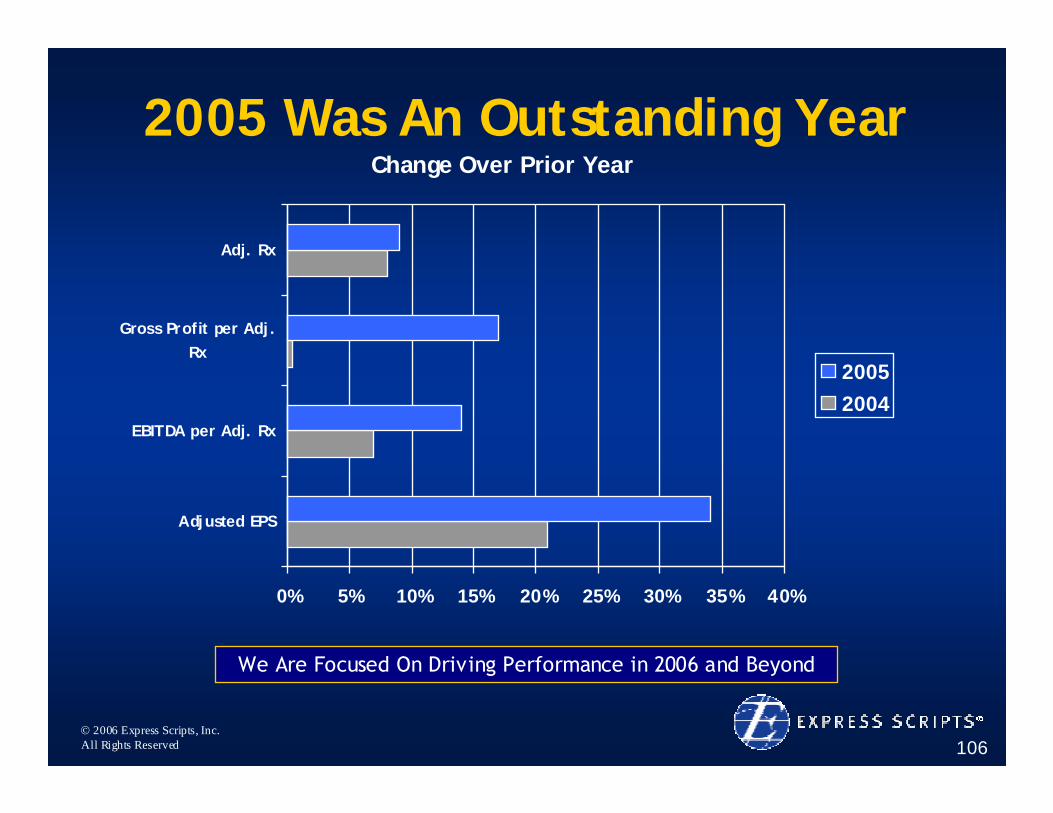

Change Over Prior Year

0% 5% 10% 15% 20% 25% 30% 35% 40%

Adjusted EPS

EBITDA per Adj. Rx

Gross Profit per Adj.Rx

Adj. Rx

20052004

2005 Was An Outstanding Year

We Are Focused On Driving Performance in 2006 and Beyond

© 2006 Express Scripts, Inc.All Rights Reserved 107

Changing Paradigm For Growth

We have positioned Express Scripts to produce

superior earnings growth and shareholder value

in an environment of claims growth that is lower than we have

experienced historically

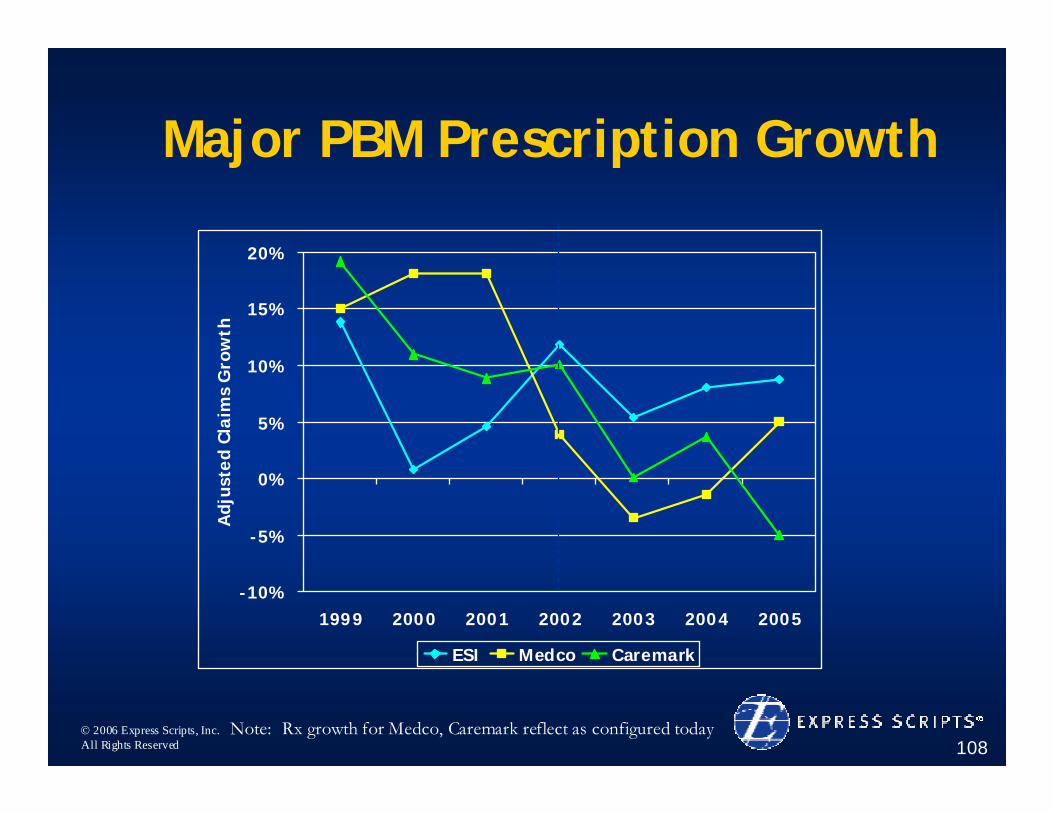

© 2006 Express Scripts, Inc.All Rights Reserved 108

-10%

-5%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005

Adj

uste

d Cl

aim

s G

row

th

ESI Medco Caremark

Major PBM Prescription Growth

Note: Rx growth for Medco, Caremark reflect as configured today

© 2006 Express Scripts, Inc.All Rights Reserved 109

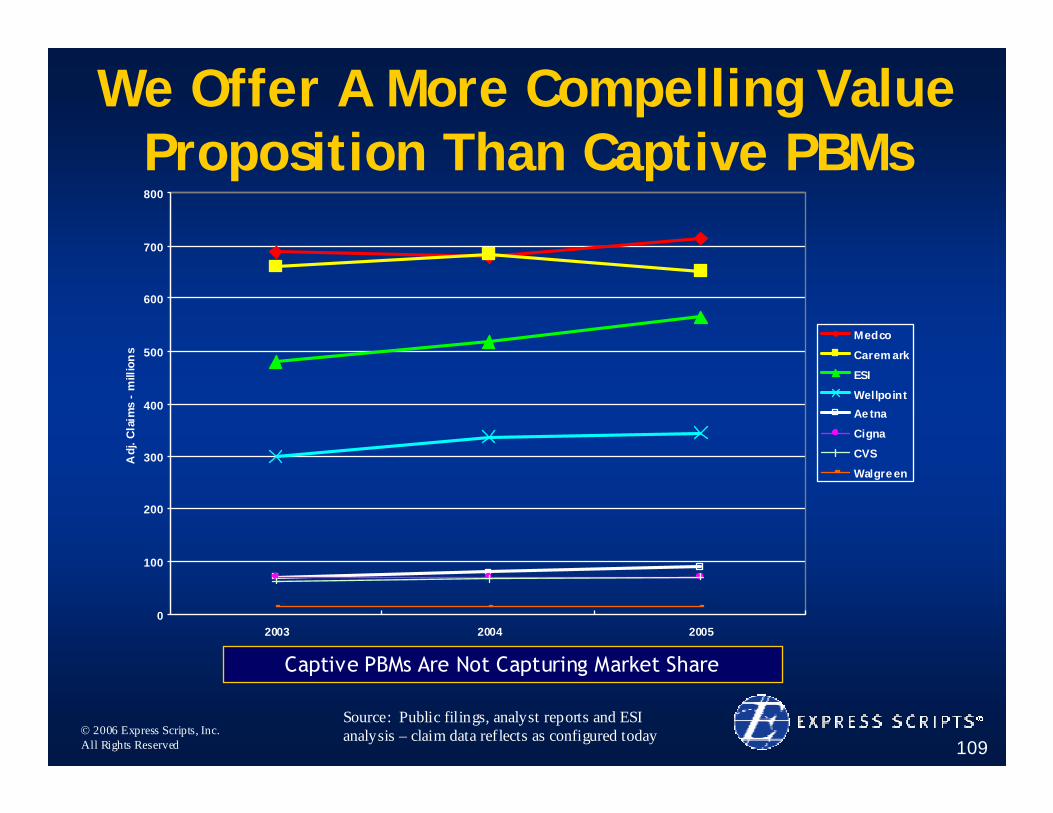

We Offer A More Compelling Value Proposition Than Captive PBMs

0

100

200

300

400

500

600

700

800

2003 2004 2005

Adj

. Cla

ims

- m

illio

ns

Medco

Carem ark

ESI

WellpointAe tna

Cigna

CVS

Walgre en

Source: Public filings, analyst reports and ESI analysis – claim data reflects as configured today

Captive PBMs Are Not Capturing Market Share

© 2006 Express Scripts, Inc.All Rights Reserved 110

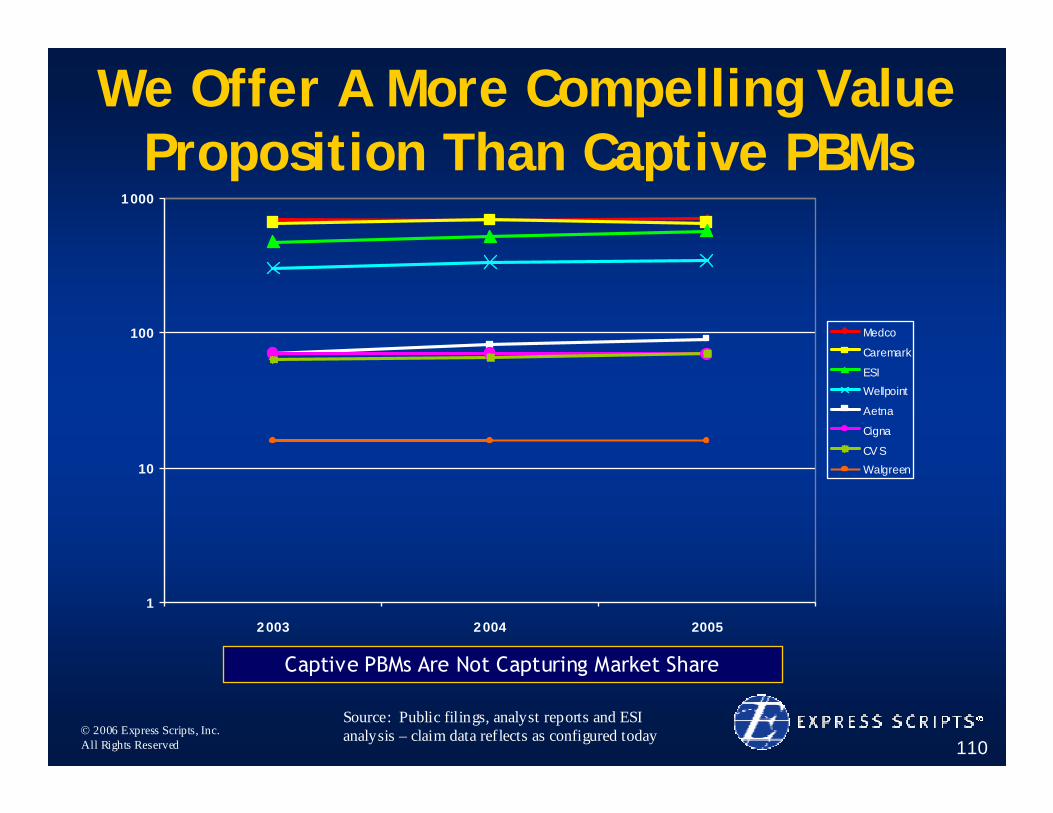

We Offer A More Compelling Value Proposition Than Captive PBMs

1

10

100

1000

2003 2004 2005

Medco

Caremark

ESIWellpoint

Aetna

Cigna

CV SWalgreen

Source: Public filings, analyst reports and ESI analysis – claim data reflects as configured today

Captive PBMs Are Not Capturing Market Share

© 2006 Express Scripts, Inc.All Rights Reserved 111

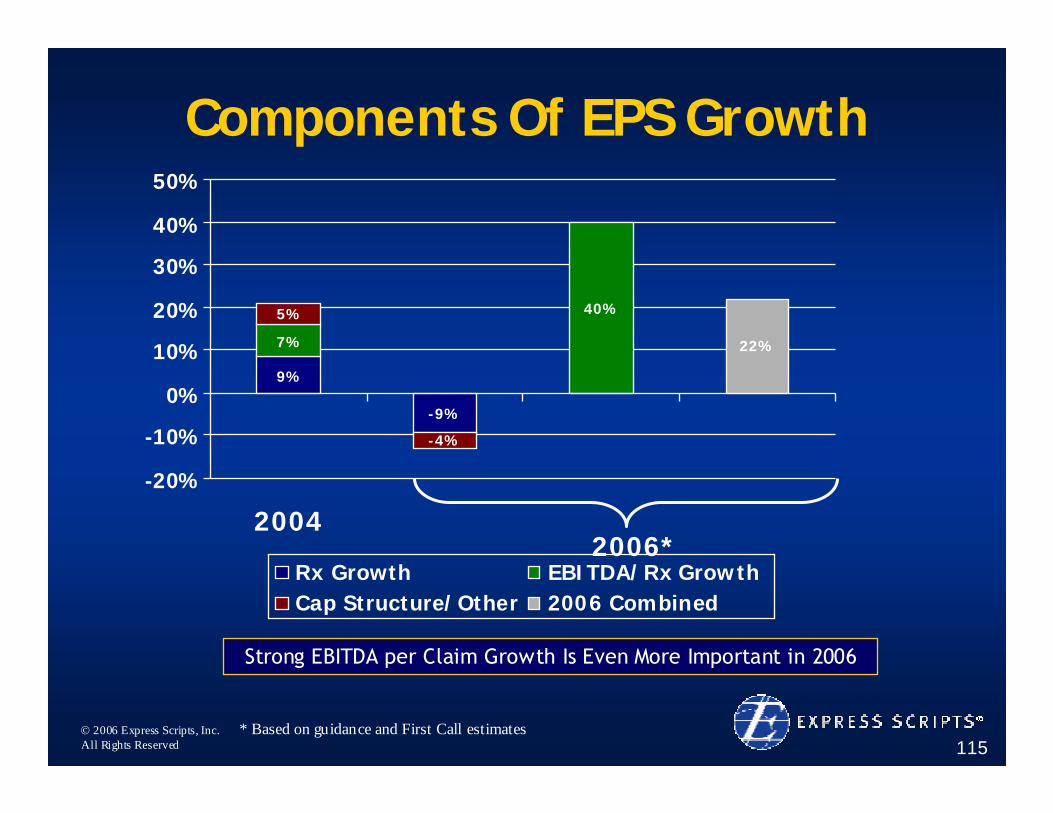

Components Of EPS Growth

9%

7%

5%

0%

5%

10%

15%

20%

25%

2004

Rx Growth EBITDA/Rx Growth Cap Structure/Other

Higher Claims Growth in the Past Required Less EBITDA per Claim Growth

© 2006 Express Scripts, Inc.All Rights Reserved 112

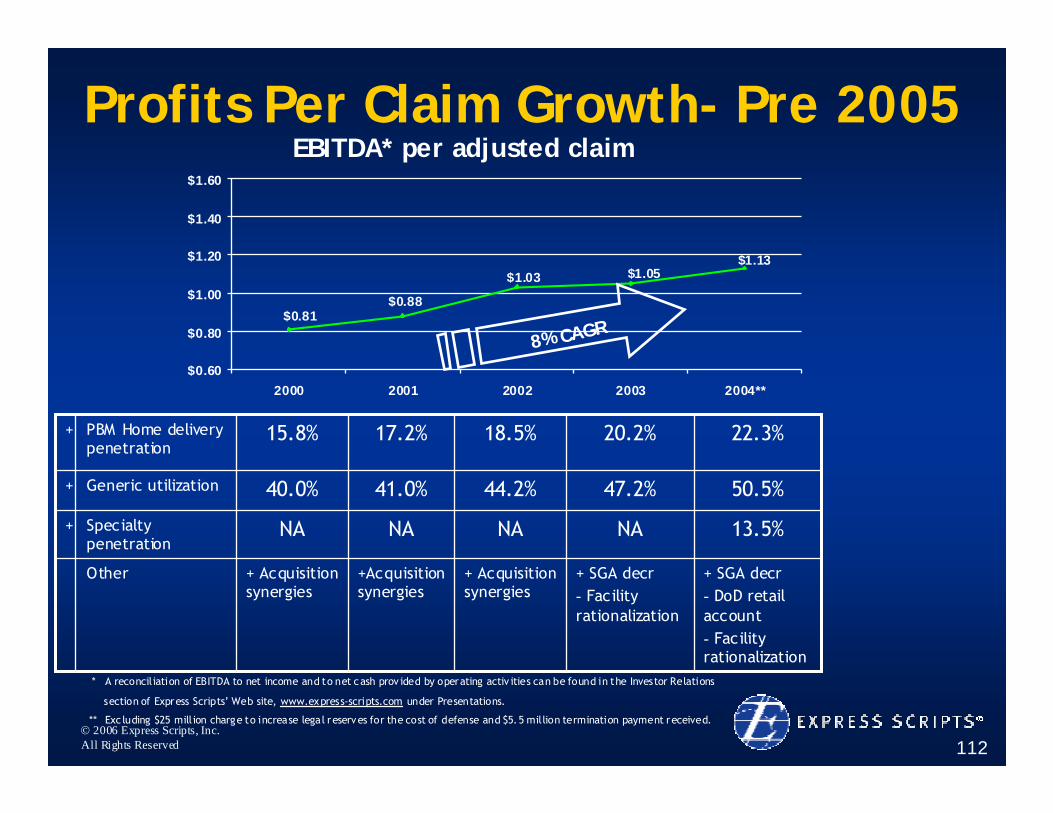

Profits Per Claim Growth- Pre 2005

$1.13$1.05$1.03

$0.88$0.81

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

2000 2001 2002 2003 2004**

EBITDA* per adjusted claim

* A reconciliation of EBITDA to net income and to net cash prov ided by operating activ ities can be found in the Investor Relations

section of Express Scripts’ Web site, www.express-scripts.com under Presentations.

** Exc luding $25 million charge to increase legal reserves for the cost of defense and $5.5 million termination payment received.

8% CAGR

+

+

+

+ SGA decr- DoD retail account- Facility rationalization

+ SGA decr- Facility rationalization

+ Acquisition synergies

+Acquisition synergies

+ Acquisition synergies

Other

13.5%NANANANASpecialty penetration

50.5%47.2%44.2%41.0%40.0%Generic utilization

22.3%20.2%18.5%17.2%15.8%PBM Home delivery penetration

© 2006 Express Scripts, Inc.All Rights Reserved 113

Drivers Of EBITDA/Rx Growth - 2005

• Lower home delivery and retail drug purchasing costs

• Specialty pharmacy

• Generic utilization

• Home delivery

• Productivity improvements – pharmacy and call centerMore Moderate Claims Growth Requires More EBITDA per Claim Growth

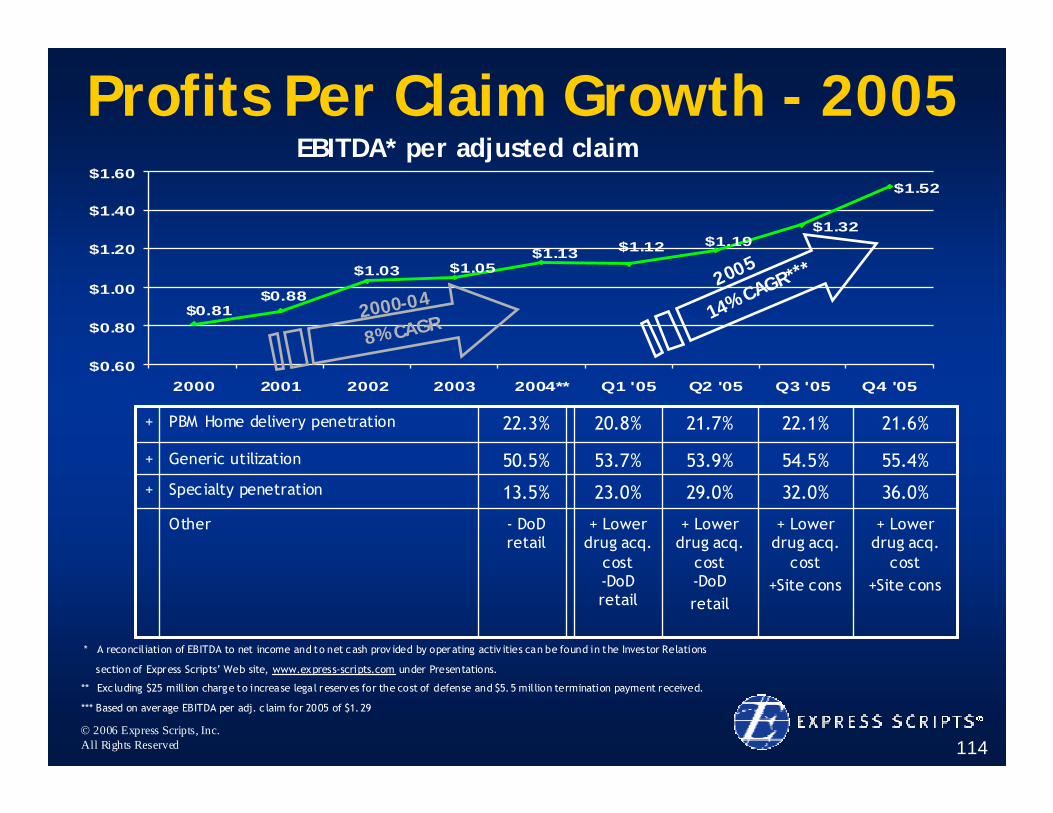

© 2006 Express Scripts, Inc.All Rights Reserved 114

Profits Per Claim Growth - 2005

$1.32

$1.52

$1.13 $1.12$1.05$1.03

$0.88$0.81

$1.19

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

2000 2001 2002 2003 2004** Q1 '05 Q2 '05 Q3 '05 Q4 '05

EBITDA* per adjusted claim

* A reconciliation of EBITDA to net income and to net cash prov ided by operating activ ities can be found in the Investor Relations

section of Express Scripts’ Web site, www.express-scripts.com under Presentations.

** Exc luding $25 million charge to increase legal reserves for the cost of defense and $5.5 million termination payment received.

*** Based on average EBITDA per adj. c laim for 2005 of $1.29

2005

14% CAGR***

2000-04

8% CAGR

+

+

+

+ Lower drug acq.

cost+Site cons

+ Lower drug acq.

cost+Site cons

+ Lower drug acq.

cost -DoDretail

+ Lower drug acq.

cost -DoD retail

- DoD retail

Other

36.0%32.0%29.0%23.0%13.5%Specialty penetration

55.4%54.5%53.9%53.7%50.5%Generic utilization

21.6%22.1%21.7%20.8%22.3%PBM Home delivery penetration

© 2006 Express Scripts, Inc.All Rights Reserved 115

Components Of EPS Growth

9%

-9%

7%

40%5%

-4%

22%

-20%

-10%

0%

10%

20%

30%

40%

50%

2004

Rx Growth EBITDA/Rx GrowthCap Structure/Other 2006 Combined

2006*

* Based on guidance and First Call estimates

Strong EBITDA per Claim Growth Is Even More Important in 2006

© 2006 Express Scripts, Inc.All Rights Reserved 116

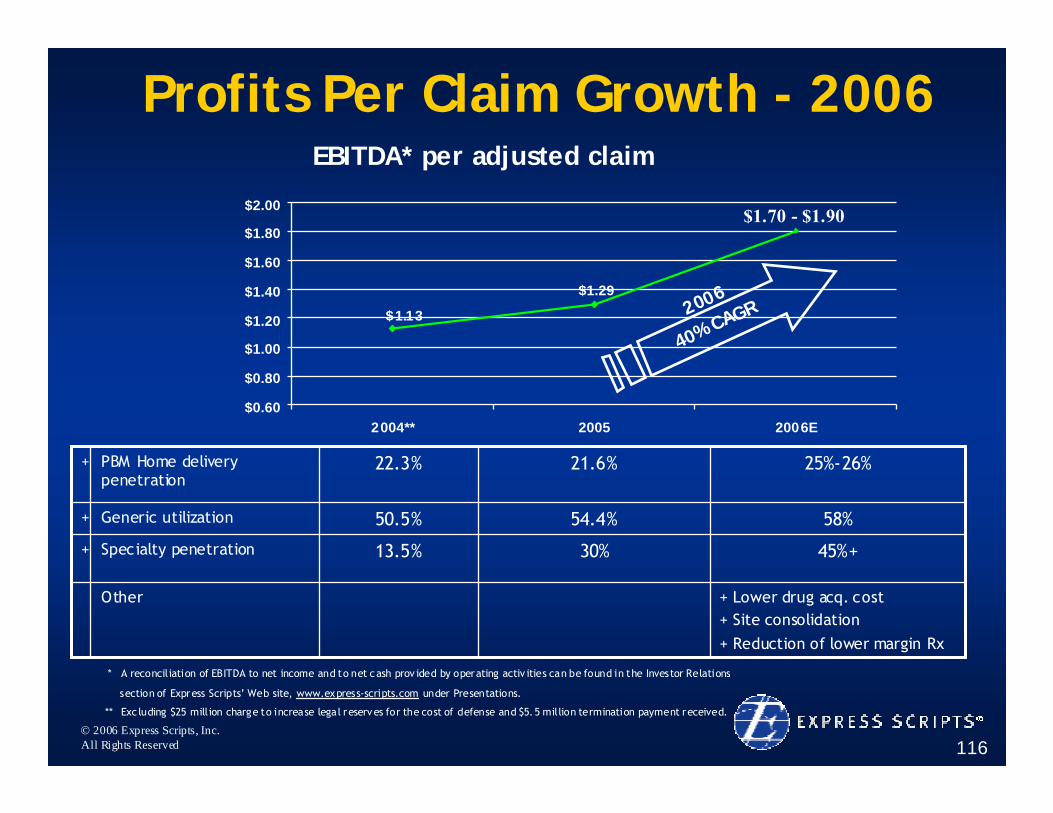

Profits Per Claim Growth - 2006

$1.13

$1.29

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

2004** 2005 2006E

EBITDA* per adjusted claim

$1.70 - $1.90

2006

40% CAGR

* A reconciliation of EBITDA to net income and to net cash prov ided by operating activ ities can be found in the Investor Relations

section of Express Scripts’ Web site, www.express-scripts.com under Presentations.

** Exc luding $25 million charge to increase legal reserves for the cost of defense and $5.5 million termination payment received.

+

+

+

+ Lower drug acq. cost+ Site consolidation+ Reduction of lower margin Rx

Other

45%+30%13.5%Specialty penetration

58%54.4%50.5%Generic utilization

25%-26%21.6%22.3%PBM Home delivery penetration

© 2006 Express Scripts, Inc.All Rights Reserved 117

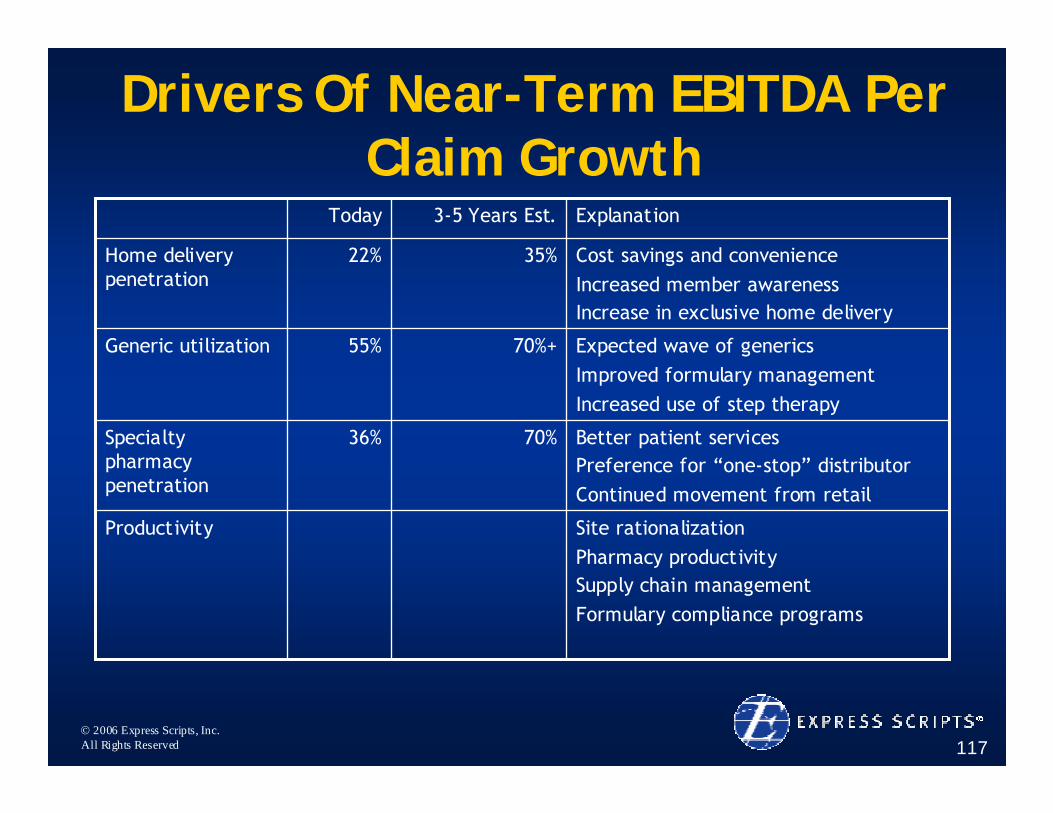

Drivers Of Near-Term EBITDA Per Claim Growth

Better patient servicesPreference for “one-stop” distributorContinued movement from retail

70%36%Specialty pharmacy penetration

Site rationalizationPharmacy productivitySupply chain managementFormulary compliance programs

Productivity

Expected wave of generics Improved formulary managementIncreased use of step therapy

70%+55%Generic utilization

Cost savings and convenienceIncreased member awarenessIncrease in exclusive home delivery

35%22%Home delivery penetration

Explanation3-5 Years Est.Today

© 2006 Express Scripts, Inc.All Rights Reserved 118

Drivers Of Future EBITDA Growth Generic Utilization

The Next Five Years Provide a Historic Cost Savings Opportunity For Our Clients

0

2

4

6

8

10

12

2005 2006 2007 2008 2009

Annu

al S

ales

, in

billio

ns ($

)

Oxycontin

Duragesic

Zithromax

Other

Zocor

Zoloft

Allegra

Pravachol

Other

Norvasc

Ambien

Zyrtec

Other

Advair

Effexor/XR

Fosamax

Risperdal

Other

Prevacid

Lexapro

AvandiaTopamax

Other

$10.0$11.3 $11.1

$10.4$9.9

Brand Drugs Going Generic

© 2006 Express Scripts, Inc.All Rights Reserved 119

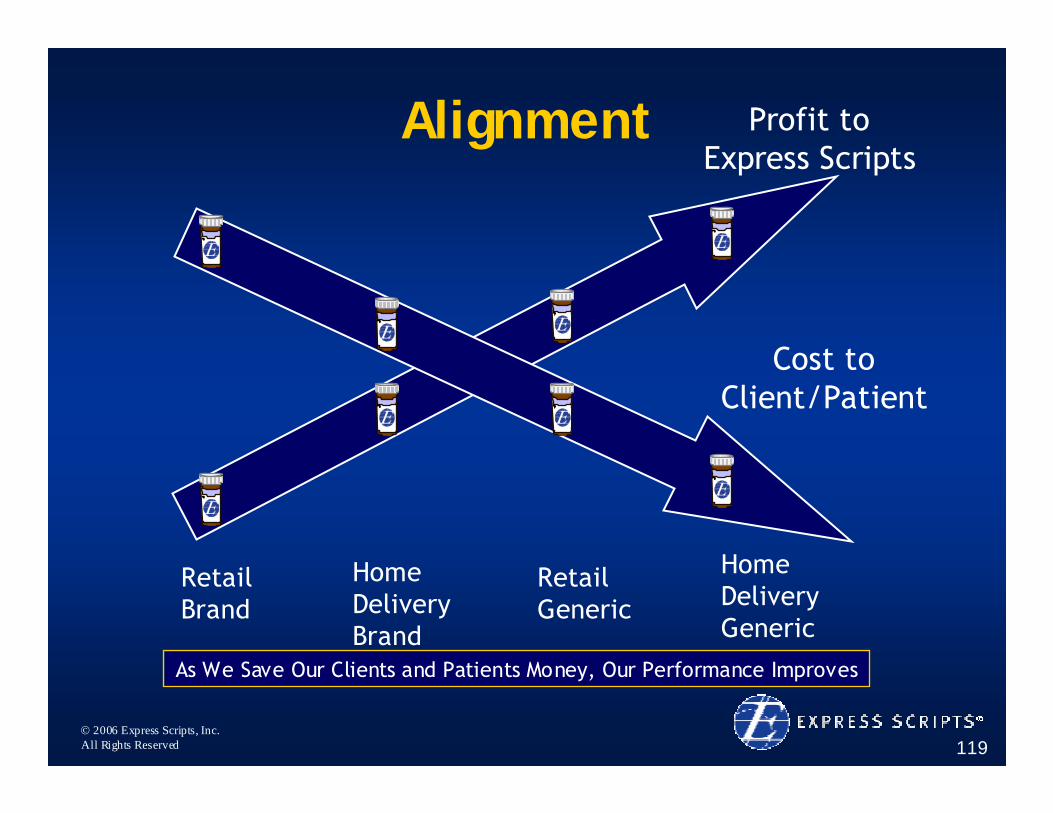

Alignment Profit to Express Scripts

Cost toClient/Patient

RetailBrand

Home DeliveryBrand

Retail Generic

HomeDelivery Generic

As We Save Our Clients and Patients Money, Our Performance Improves

© 2006 Express Scripts, Inc.All Rights Reserved 120

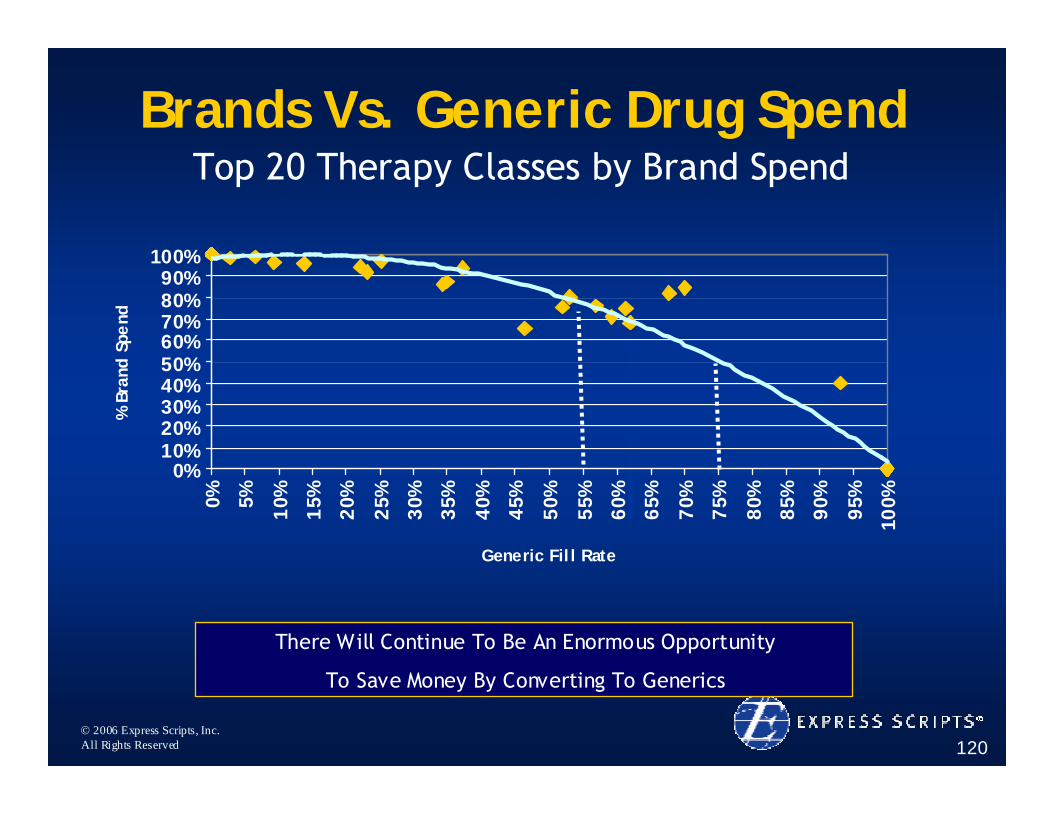

Brands Vs. Generic Drug SpendTop 20 Therapy Classes by Brand Spend

There Will Continue To Be An Enormous Opportunity

To Save Money By Converting To Generics

0%10%20%30%40%50%60%70%80%90%

100%

0% 5% 10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Generic Fil l Rate

% B

rand

Spe

nd

© 2006 Express Scripts, Inc.All Rights Reserved 121

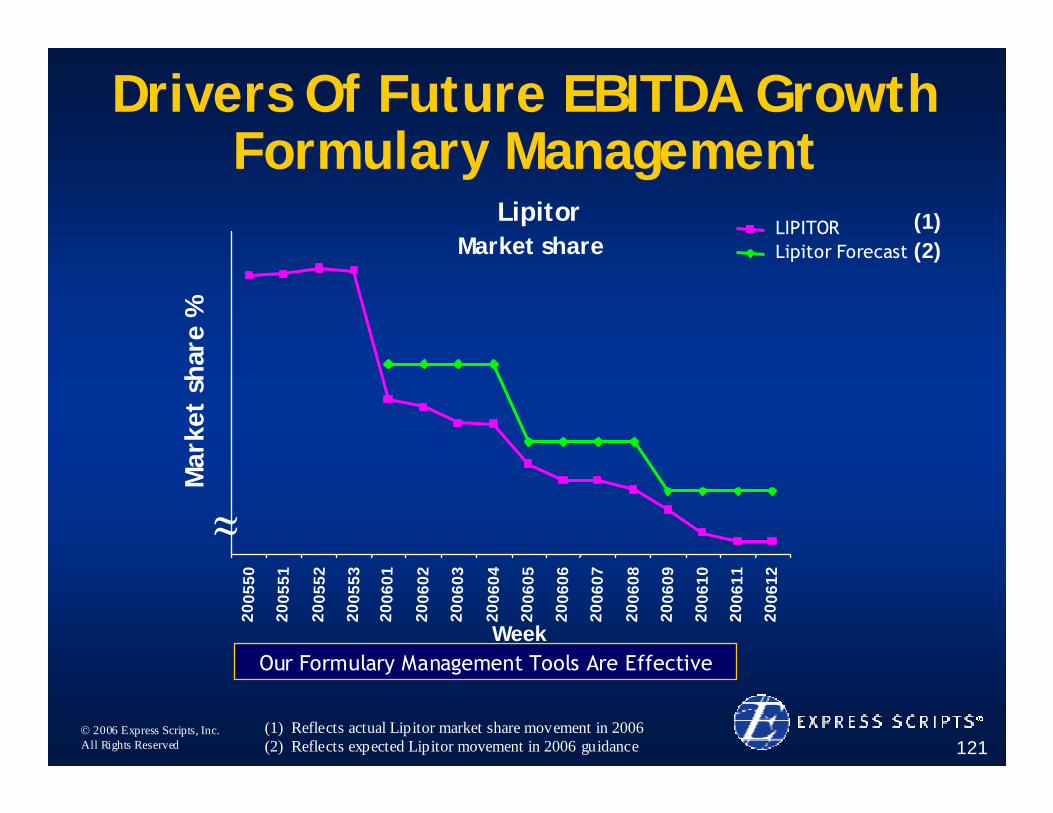

Drivers Of Future EBITDA Growth Formulary Management

(1) Reflects actual Lipitor market share movement in 2006(2) Reflects expected Lipitor movement in 2006 guidance

Our Formulary Management Tools Are Effective

LipitorMarket share

2005

50

2005

51

2005

52

2005

53

2006

01

2006

02

2006

03

2006

04

2006

05

2006

06

2006

07

2006

08

2006

09

2006

10

2006

11

2006

12

Week

Mar

ket

shar

e %

LIPITORLipitor Forecast

≈

(1)(2)

© 2006 Express Scripts, Inc.All Rights Reserved 122

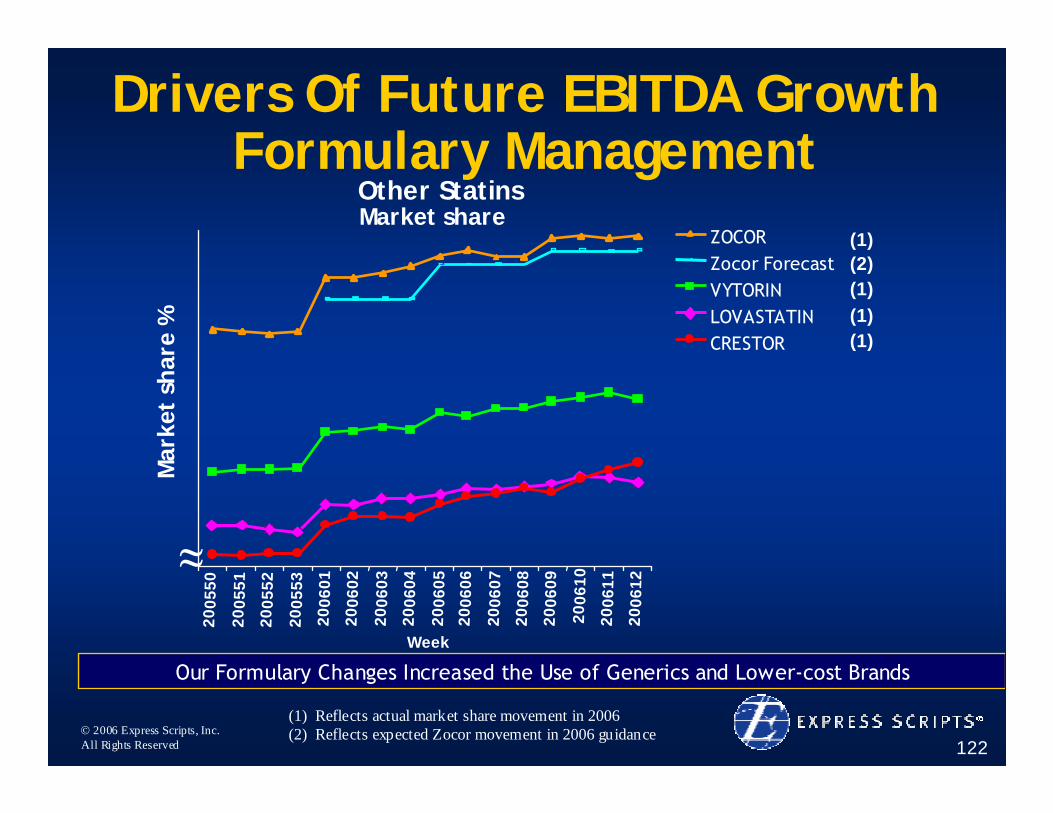

(1) Reflects actual market share movement in 2006(2) Reflects expected Zocor movement in 2006 guidance

Our Formulary Changes Increased the Use of Generics and Lower-cost Brands

Drivers Of Future EBITDA Growth Formulary Management

Other StatinsMarket share

Week

Mar

ket

shar

e %

2005

50

2005

51

2005

52

2005

53

2006

01

2006

02

2006

03

2006

04

2006

05

2006

06

2006

07

2006

08

2006

09

2006

10

2006

11

2006

12

ZOCORZocor ForecastVYTORINLOVASTATINCRESTOR

(1)(2)(1)(1)(1)

≈

© 2006 Express Scripts, Inc.All Rights Reserved 123

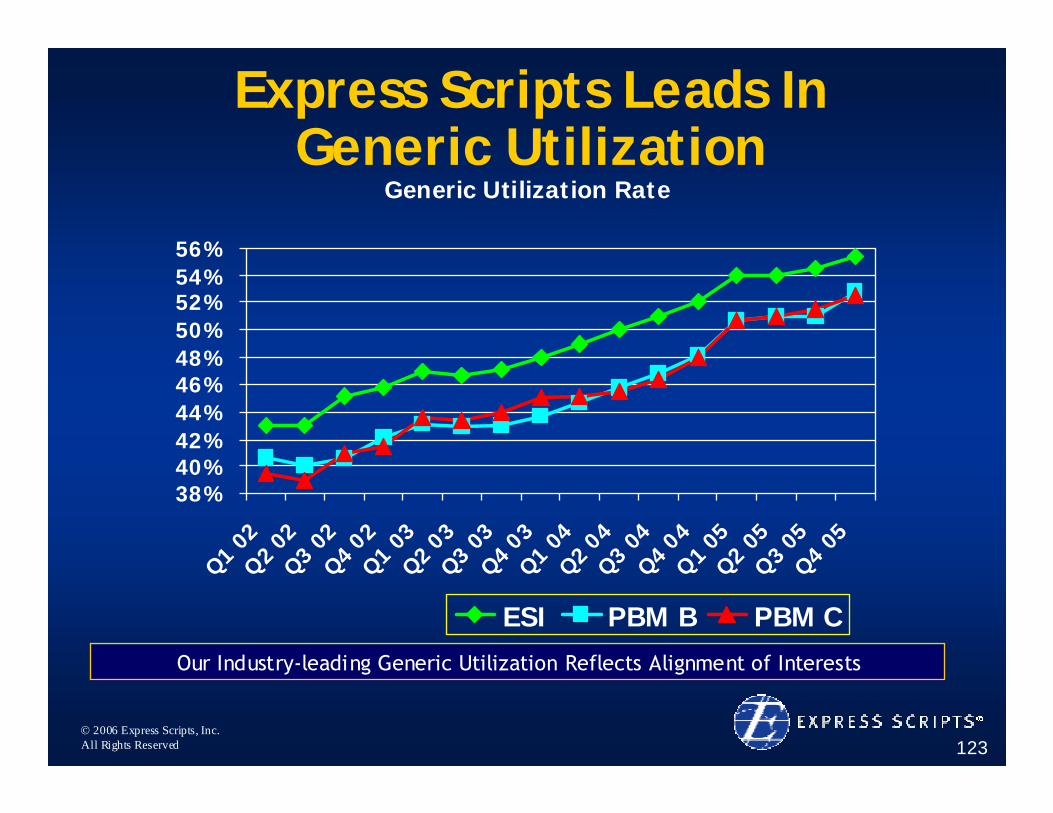

Express Scripts Leads In Generic Utilization

Generic Utilization Rate

38%40%42%44%46%48%50%52%54%56%

Q1 02

Q2 02

Q3 02Q4

02Q1 03Q2

03Q3 03Q4

03Q1 04Q2

04Q3 04Q4

04Q1

05Q2

05Q3

05Q4 05

ESI PBM B PBM COur Industry-leading Generic Utilization Reflects Alignment of Interests

© 2006 Express Scripts, Inc.All Rights Reserved 124

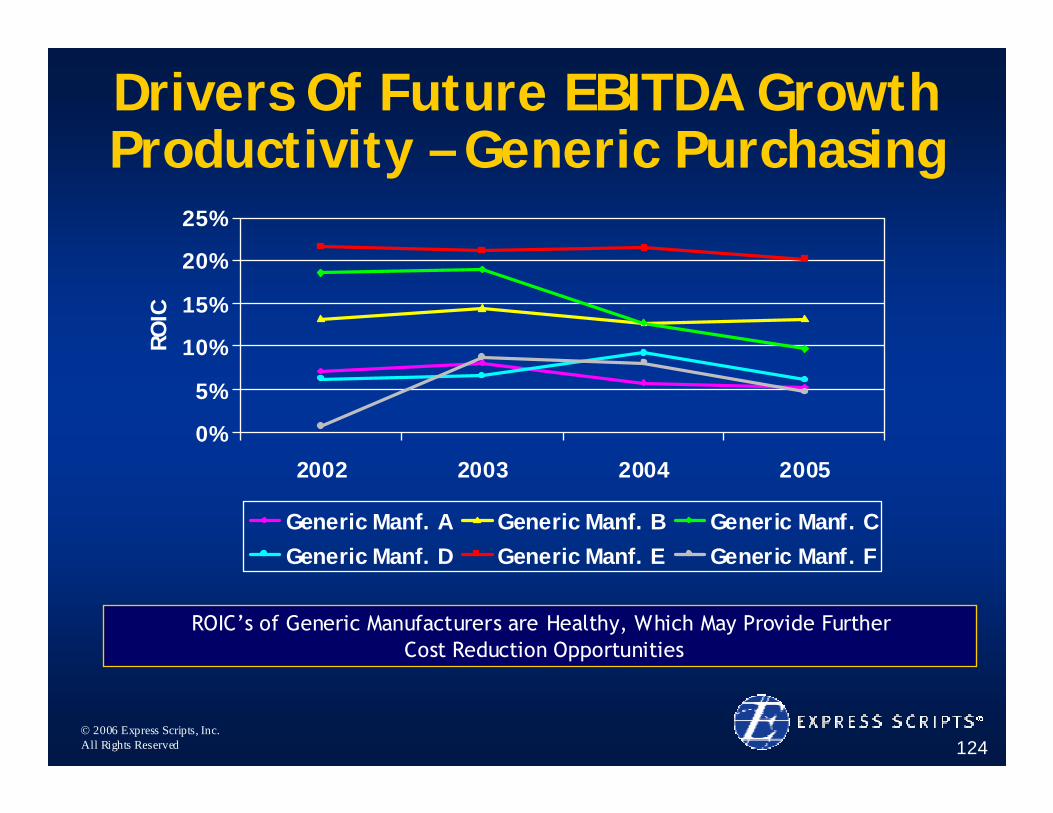

Drivers Of Future EBITDA Growth Productivity – Generic Purchasing

0%

5%

10%

15%

20%

25%

2002 2003 2004 2005

ROIC

Generic Manf. A Generic Manf. B Generic Manf. CGeneric Manf. D Generic Manf. E Generic Manf. F

ROIC’s of Generic Manufacturers are Healthy, Which May Provide FurtherCost Reduction Opportunities

© 2006 Express Scripts, Inc.All Rights Reserved 125

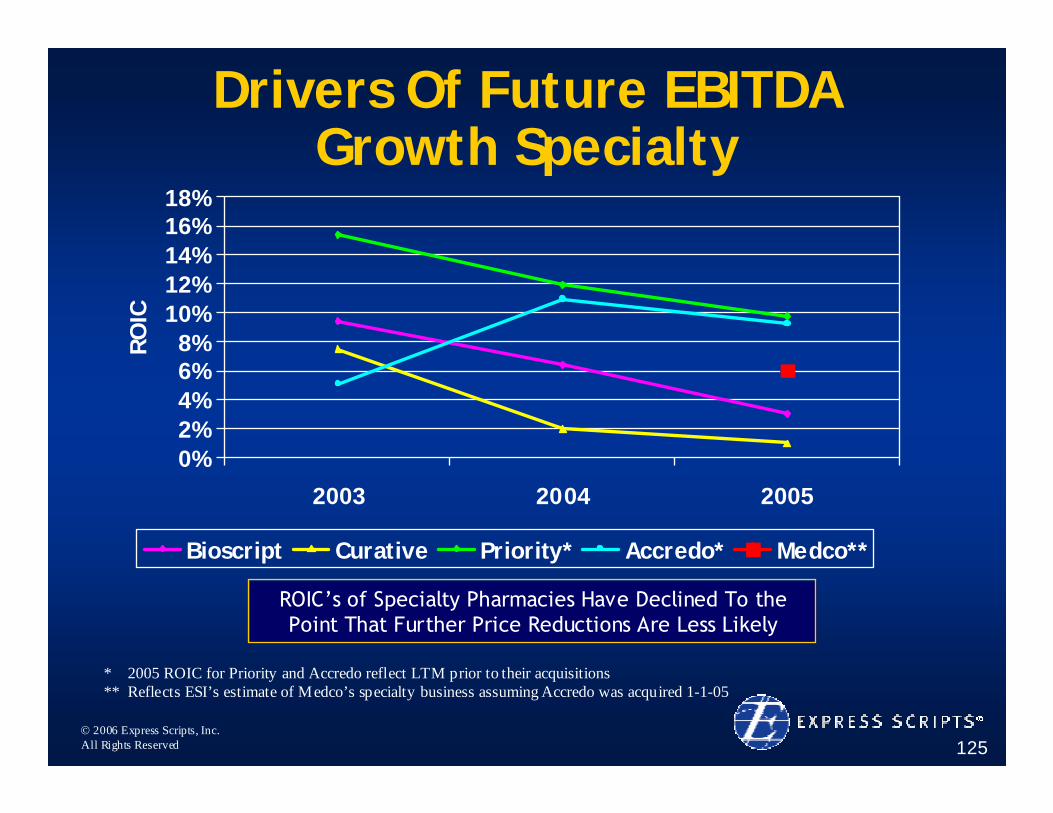

Drivers Of Future EBITDA Growth Specialty

0%2%4%6%8%

10%12%14%16%18%

2003 2004 2005

RO

IC

Bioscript Curative Priority* Accredo* Medco**

* 2005 ROIC for Priority and Accredo reflect LTM prior to their acquisitions** Reflects ESI’s estimate of Medco’s specialty business assuming Accredo was acquired 1-1-05

ROIC’s of Specialty Pharmacies Have Declined To the Point That Further Price Reductions Are Less Likely

© 2006 Express Scripts, Inc.All Rights Reserved 126

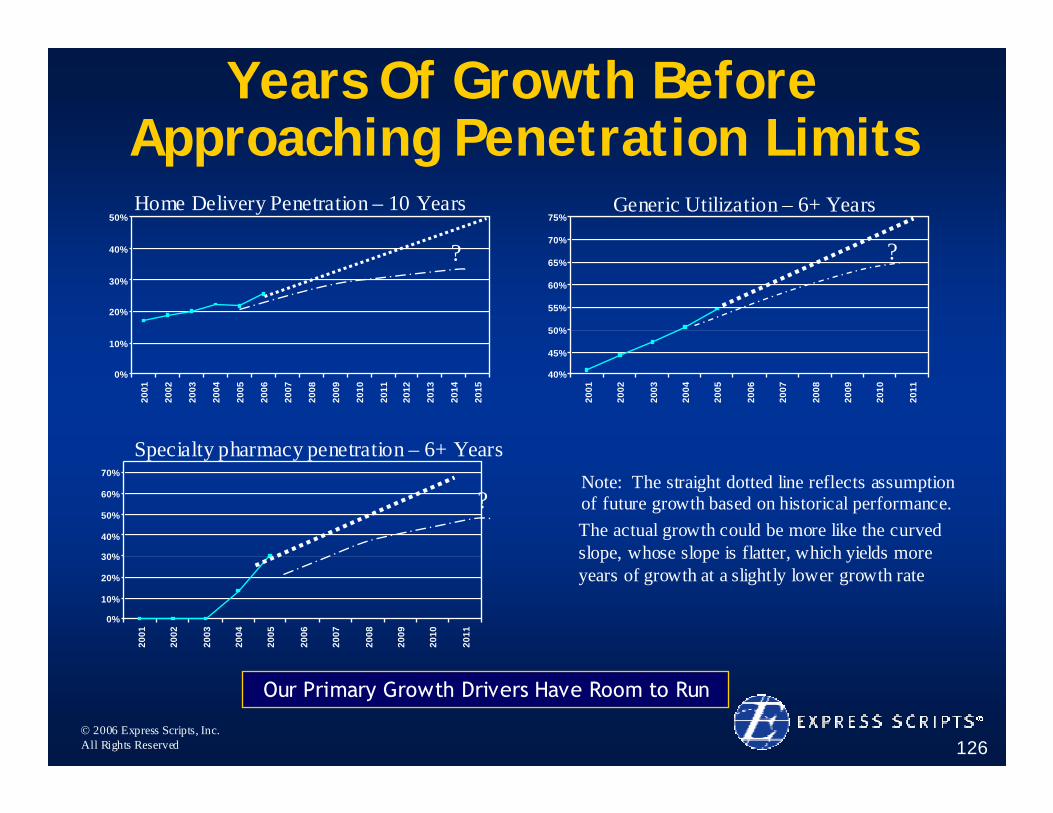

Years Of Growth Before Approaching Penetration Limits

0%

10%

20%

30%

40%

50%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

40%

45%

50%

55%

60%

65%

70%

75%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Home Delivery Penetration – 10 Years Generic Utilization – 6+ Years

Specialty pharmacy penetration – 6+ Years

0%

10%

20%

30%

40%

50%

60%

70%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

? ?

?Note: The straight dotted line reflects assumption of future growth based on historical performance. The actual growth could be more like the curved slope, whose slope is flatter, which yields more years of growth at a slightly lower growth rate

Our Primary Growth Drivers Have Room to Run

© 2006 Express Scripts, Inc.All Rights Reserved 127

What Will Supplement Growth In The Future?

• Productivity improvements• Strategic, accretive acquisitions• Specialty generics• Physician connectivity

We Are Focused on Long-term Growth

© 2006 Express Scripts, Inc.All Rights Reserved 128

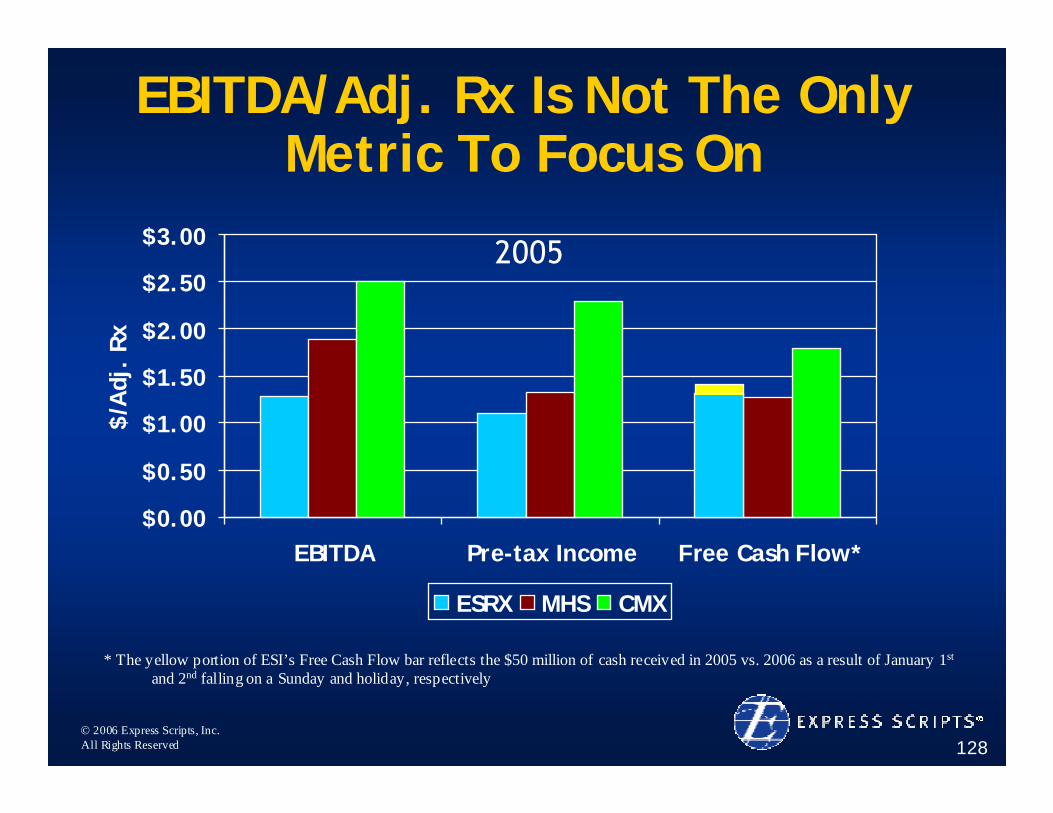

EBITDA/Adj. Rx Is Not The Only Metric To Focus On

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

EBITDA Pre-tax Income Free Cash Flow*

$/A

dj.

Rx

ESRX MHS CMX

* The yellow portion of ESI’s Free Cash Flow bar reflects the $50 million of cash received in 2005 vs. 2006 as a result of January 1st

and 2nd falling on a Sunday and holiday, respectively

2005

© 2006 Express Scripts, Inc.All Rights Reserved 129

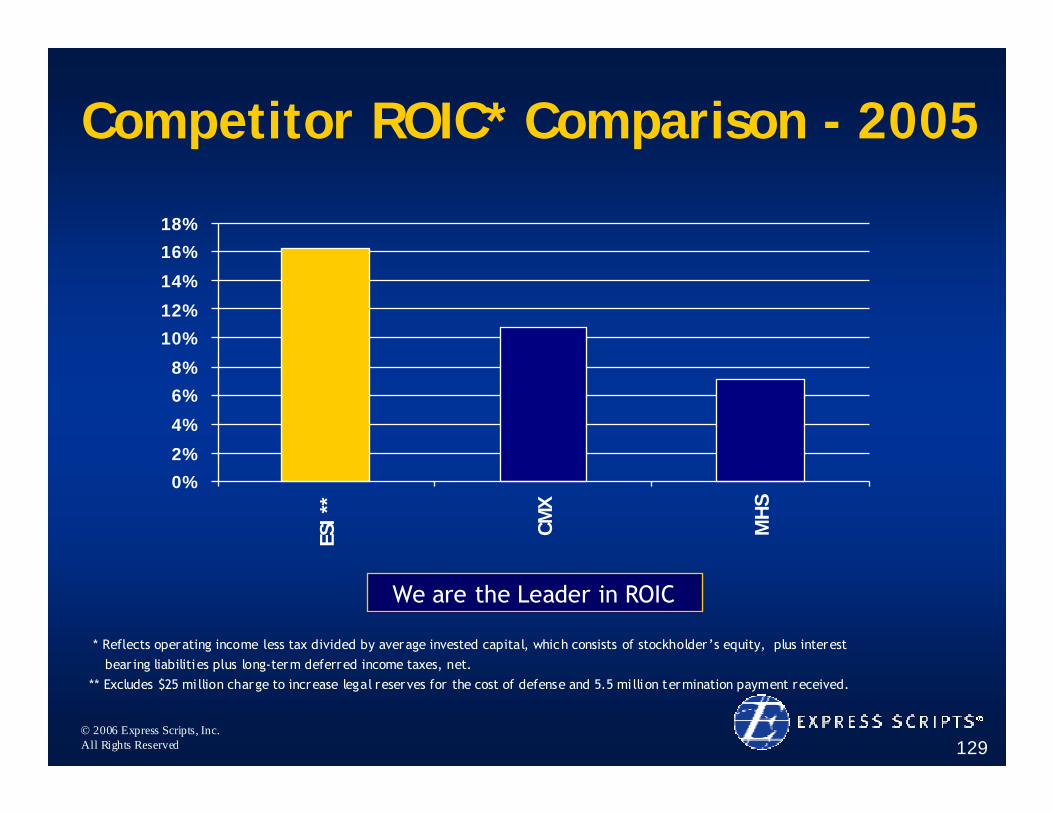

Competitor ROIC* Comparison - 2005

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

ESI *

*

CMX

MH

S

* Reflects operating income less tax divided by average invested capital, which consists of stockholder’s equity, plus interestbear ing liabilities plus long-term deferred income taxes, net.

** Excludes $25 mi llion charge to increase legal reserves for the cost of defense and 5.5 mi llion termination payment received.

We are the Leader in ROIC

© 2006 Express Scripts, Inc.All Rights Reserved 130

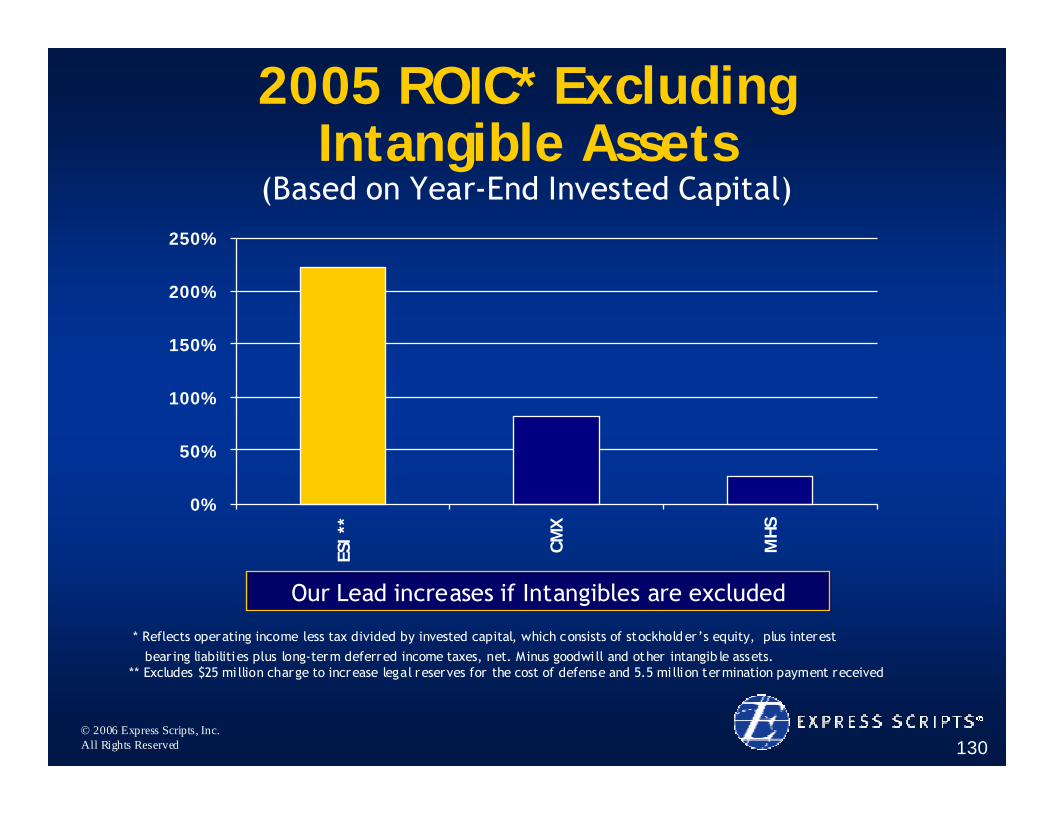

2005 ROIC* Excluding Intangible Assets

(Based on Year-End Invested Capital)

0%

50%

100%

150%

200%

250%

ESI *

*

CMX

MHS

* Reflects operating income less tax divided by invested capital, which consists of stockholder’s equity, plus interestbear ing liabilities plus long-term deferred income taxes, net. Minus goodwi ll and other intangib le assets.

** Excludes $25 mi llion charge to increase legal reserves for the cost of defense and 5.5 mi llion termination payment received

Our Lead increases if Intangibles are excluded

© 2006 Express Scripts, Inc.All Rights Reserved 131

Why Express Scripts?• Differentiation Through Alignment

– We deliberately price our business in a way that aligns our interests with our clients’ interest

– We will take aggressive actions to give our clients the best value, considering both clinical and cost factors

• Strategic Execution– Our disciplined focus on our industry-leading ROIC will continue to

produce superior returns for shareholders

• Room to Run– We see 6-plus years of good contributions from generics, home

delivery and specialty growth

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

George PazPresident and CEO

Express Scripts’ Value Proposition Positioning Us For the Future

© 2006 Express Scripts, Inc.All Rights Reserved 133

• Formulary and Trend Management• Generics, Home Delivery and Specialty• New Sales, Upsells and Retention• Innovative Product Development• Operational and Service Excellence• Strategic Deployment of Capital

Express Scripts is Well Positioned for the Future

© 2006 Express Scripts, Inc.All Rights Reserved 134

Why Express Scripts?• Differentiation Through Alignment

– A proud legacy of alignment, transparency and disclosure

• Strategic Execution– Growth by reducing drug costs, without compromising

health outcomes, while maximizing patient satisfaction

• Room to Run– Generics, home delivery and specialty pharmacy:

Platforms for long-term growth

Superior Growth, ROIC and Shareholder Value

© 2006 Express Scripts, Inc.All Rights Reserved

Our Pathways to Patients: Alignment in Action