ip2pmoney investor slidedeck feb2017

TRANSCRIPT

February 2017 A proposal by

Lebros Connection Sdn. Bhd.

Strictly Confidential

Investor Presentation

2Strictly Confidential

CONTENTS

1. Brief Introduction to Peer to Peer Lending 2. About iP2Pmoney 3. iP2Pmoney Lo-Costs Managed Franchise Model ("LCMFM") 4. Summary Financials

3Strictly Confidential

1 Brief Introduction to Peer to Peer Lending

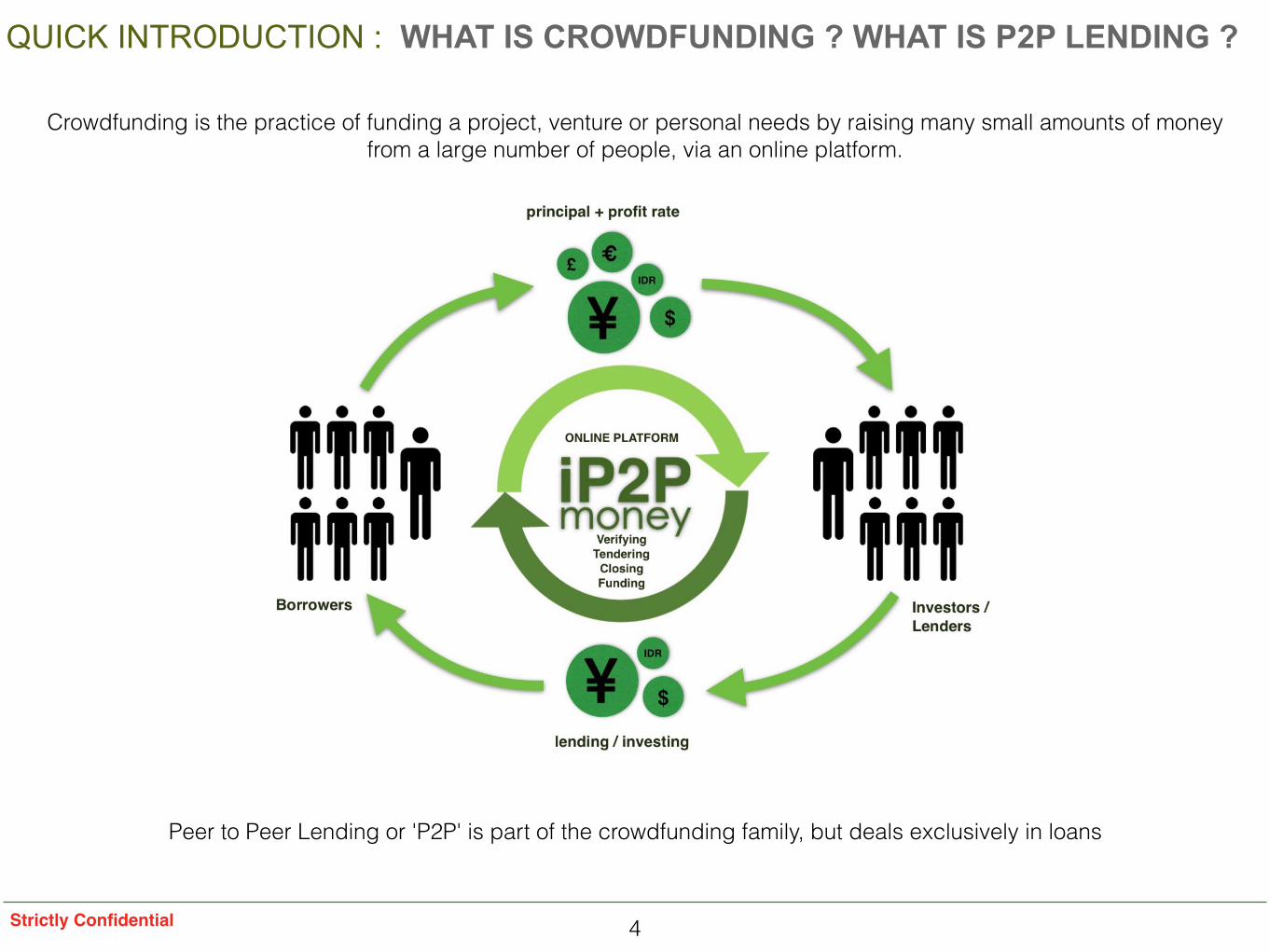

QUICK INTRODUCTION : WHAT IS CROWDFUNDING ? WHAT IS P2P LENDING ?

4

Peer to Peer Lending or 'P2P' is part of the crowdfunding family, but deals exclusively in loans

Strictly Confidential

Crowdfunding is the practice of funding a project, venture or personal needs by raising many small amounts of money from a large number of people, via an online platform.

5Strictly Confidential

ACCESS TO AFFORDABLE CREDIT

FAST & EFFICIENT DECISION

TRANSPARENCY & FAIRNESS

SUPERIOR CUSTOMER

EXPERIENCE

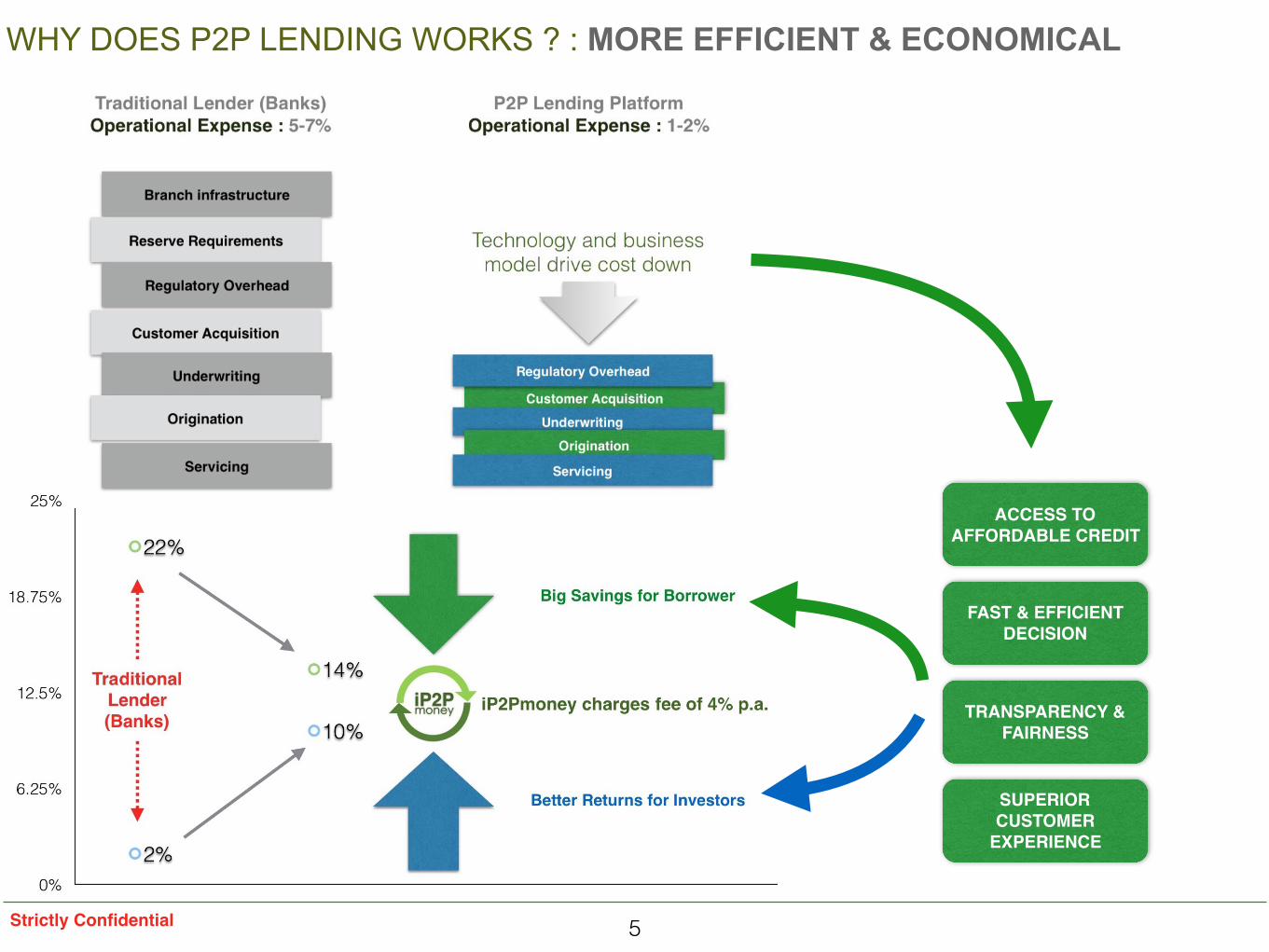

WHY DOES P2P LENDING WORKS ? : MORE EFFICIENT & ECONOMICAL

6

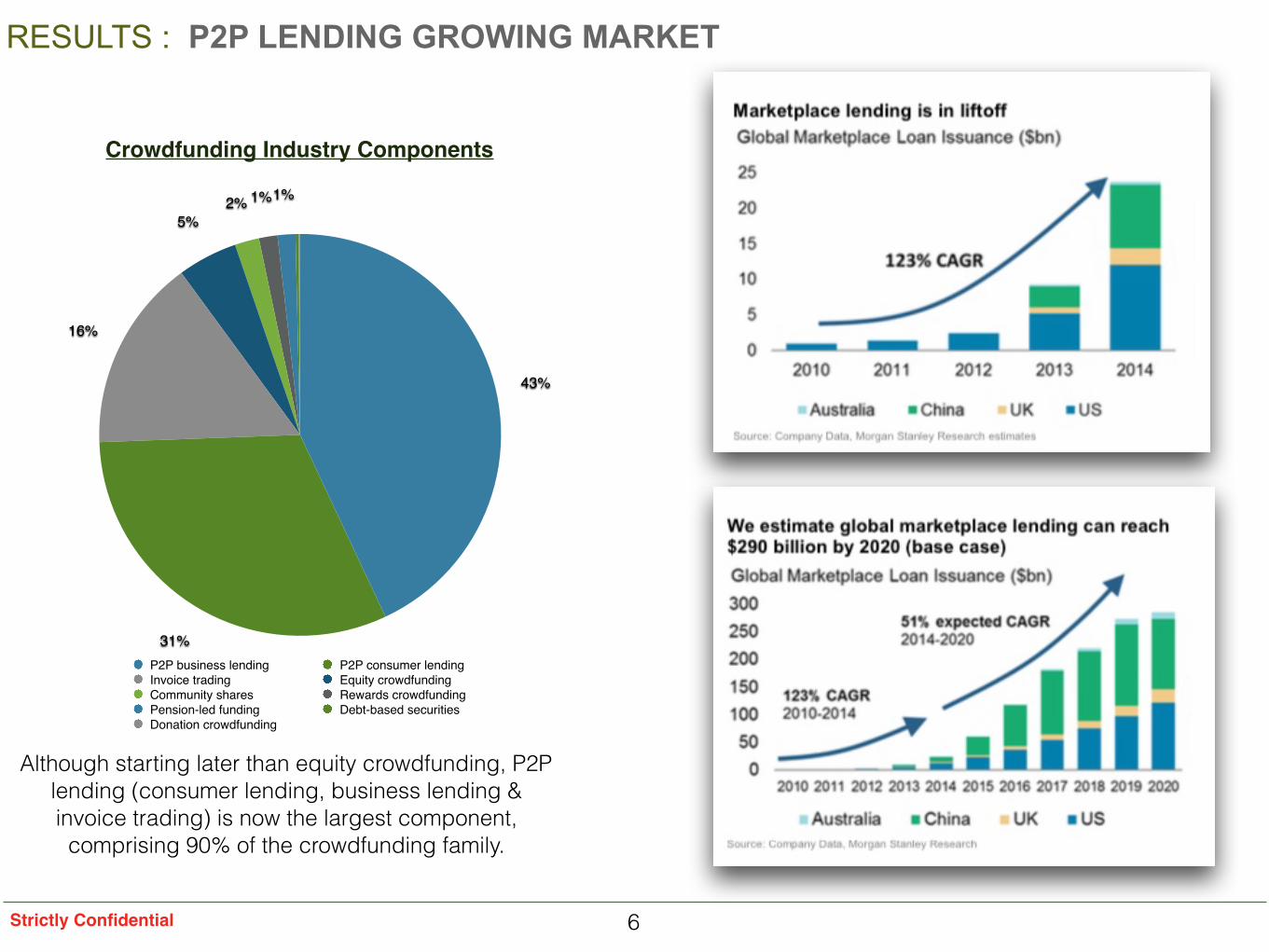

RESULTS : P2P LENDING GROWING MARKET

Strictly Confidential

1%1%2%5%

16%

31%

43%

P2P business lending P2P consumer lendingInvoice trading Equity crowdfundingCommunity shares Rewards crowdfundingPension-led funding Debt-based securitiesDonation crowdfunding

Although starting later than equity crowdfunding, P2P lending (consumer lending, business lending & invoice trading) is now the largest component, comprising 90% of the crowdfunding family.

Crowdfunding Industry Components

7Strictly Confidential

2 About iP2Pmoney

8Strictly Confidential

ABOUT US : OUR MISSION

When the founders first looked into the peer to peer market in early 2015, they noticed that, although the market was growing strongly they were structural weaknesses. These weaknesses relate to lack of product offerings, haphazard pricing levels and completely non-existent secondary trading. There was also no P2P lending platform that provides Sharia compliant products for individuals.

iP2Pmoney was thus founded in the 3rd quarter of 2015. With a combined 75 years experience in banking, factoring, credit underwriting, debt origination, bond trading, and fund management and in both Sharia and conventional finance, the founders planned to make a difference and plug the gaps in the P2P lending market.

IP2Pmoney's mission thus are :

i) To introduce & promote the usage of a variety of sharia compliant finance products for different purposes.

ii) To actively support the Muslim community in the local markets by providing a platform that will provide quality Sharia compliant investment opportunities to investors and flexible micro-financing to individuals.

iii) To give confidence to the users by adopting a bank-grade credit evaluation techniques, market orientated pricing and later a proper secondary trading platform.

iv) To provide a complete dashboard and admin systems where informations are provided in seamless manner

allowing investors to better monitor their investments and borrowers to quickly apply for their loans.

9Strictly Confidential

OUR BACKGROUND

RASHDAN IBRAHIM

ACADEMIC BACKGROUND

Bachelor of Arts (Honours) in Accountancy Studies from Exeter University, Exeter, U.K. from 1992 to 1995

PROFESSIONAL BACKGROUND

Head of Capital Markets at Al Bashayer Investment Company, Abu Dhabi, UAE from 2011 to 2012 Investment Banking (Shariah & Conventional)

Director at Capitas Group International (a member of Islamic Development Bank), Jeddah, KSA from 2010 to 2011 Financial Advisory

Executive Vice President at Arab Real Estate Co KSCC, Dubai, UAE from 2007 to 2010 Property Development

Chief Financial Officer at Pure Investment Holdings Limited, Dubai, UAE from 2006 to 2007 Property Development

Founder and Executive Director of Arcap Inssef Limited, Labuan, Malaysia from 2004 to 2006 Fund Management

Vice President and Head of Institutional Clients Group at Deutsche Bank, Kuala Lumpur, Malaysia from 1997 to 2003 Banking-Treasury

Assistant Fund Manager at PETRONAS Group Treasury, Kuala Lumpur, Malaysia from 1995 to 1997 Fund Management

LEE BOON WAH

ACADEMIC BACKGROUND

Professional Certificate from Malaysian Foreign Exchange Association.

PROFESSIONAL BACKGROUND

Founder of Cofactors Sdn. Bhd., Kuala Lumpur, Malaysia from 2013 to 2015 - Islamic Factoring & SME Finance

Founder and Business Development Director of El Nemr Capital Partners, Kuala Lumpur, Malaysia from 2005 to 2013 Islamic Factoring & SME Finance

Head of Operations at Arcap Inssel Ltd., Labuan, Malaysia from 2003 to 2005 - Fund Management Assistant Treasurer at Deutsche Bank, Kuala Lumpur, Malaysia from 2001 to 2013 Banking - Treasury

Operations Executive at Citibank, Kuala Lumpur, Malaysia from 1989 to 2001 Banking - Operations

Executive at Development Bank of Singapore, Singapore, from 1987 to 1988 Banking

OTHERS

Vice Chairman of Malaysian Factors Association from 2010 to 2011.

MUHAMMAD RADZI IBRAHIM

ACADEMIC BACKGROUND

Bachelor of Science (Honours) in Actuarial Science from Universiti Kebangsaan Malaysia,from 1989 to 1992

PROFESSIONAL BACKGROUND

Founder of Cofactors Sdn. Bhd., Kuala Lumpur, Malaysia from 2013 to 2015 Islamic Factoring & SME Finance Founder and Operations Director at El Nemr Capital Partners, Kuala Lumpur Malaysia from 2005 to 2013 Islamic Factoring & SME Finance

Senior Manager at UB Co Management Sdn. Bhd. Kuala Lumpur, Malaysia from 1994 to 2001 - Factoring & SME Finance

Loan Officer at MBf Finance Berhad, Kuala Lumpur, Malaysia from 1992 to 1994 Consumer Finance

JAMES LOY

ACADEMIC BACKGROUND

Bachelor of Commerce (Major in Accounting) from Australian National University, Australia from 1994 to 1996

PROFESSIONAL BACKGROUND

Vice President at RHB Investment Bank Berhad, Malaysia from 2007 to 2015 Investment Banking (Shariah & Conventional)

Senior Manager at Southern Investment Bank Berhad, Malaysia from 2000 to 2006 Investment Banking (Shariah & Conventional)

Executive at MUI Group, Malaysia from 1997 to 1999 Internal Audit

Agriya is a16 years old custom web development company based out of Chennai, India employing over 200+ developers across a range of discipline which includes php web developer, web designers, UX experts, search engine optimisation experts operating out of a 11,000 sq. feet development facil i ty. Agriya is recognised throughout the world as a cutting edge web development and mobile development company and it's expertise in web development has received exposure in leading media outlets including Time Magazine and Forbes, as well as many industry specific online magazines. The company is widely regarded as one of the leading agile web development company in the World.

Founders Tech Partner

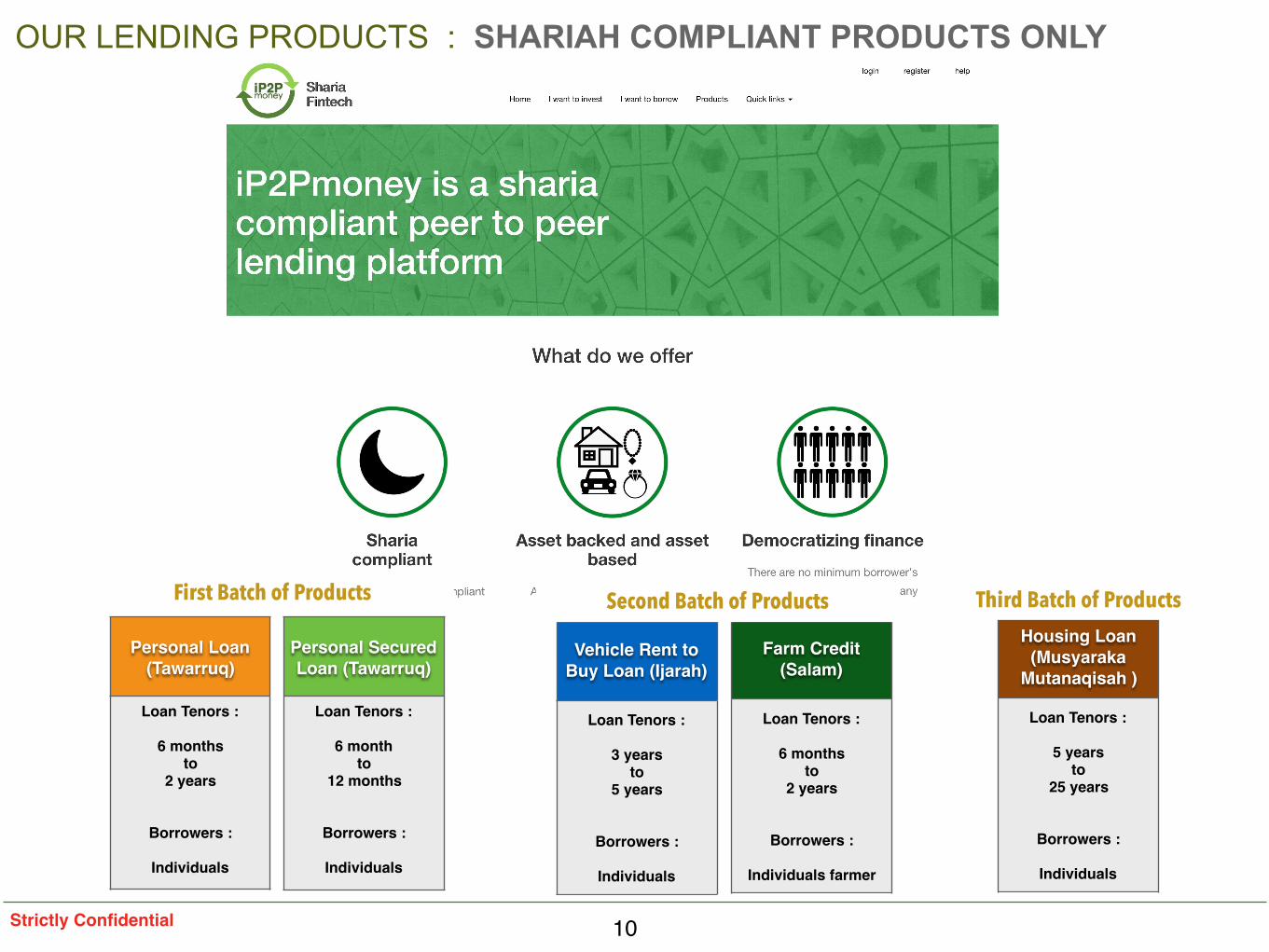

OUR LENDING PRODUCTS : SHARIAH COMPLIANT PRODUCTS ONLY

10Strictly Confidential

Personal Secured Loan (Tawarruq)

Loan Tenors :

6 month to

12 months

Borrowers :

Individuals

Vehicle Rent to Buy Loan (Ijarah)

Loan Tenors :

3 years to

5 years

Borrowers :

Individuals

Personal Loan (Tawarruq)

Loan Tenors :

6 months to

2 years

Borrowers :

Individuals

First Batch of Products

Farm Credit (Salam)

Loan Tenors :

6 months to

2 years

Borrowers :

Individuals farmer

Housing Loan (Musyaraka

Mutanaqisah )

Loan Tenors :

5 years to

25 years

Borrowers :

Individuals

Second Batch of Products Third Batch of Products

11Strictly Confidential

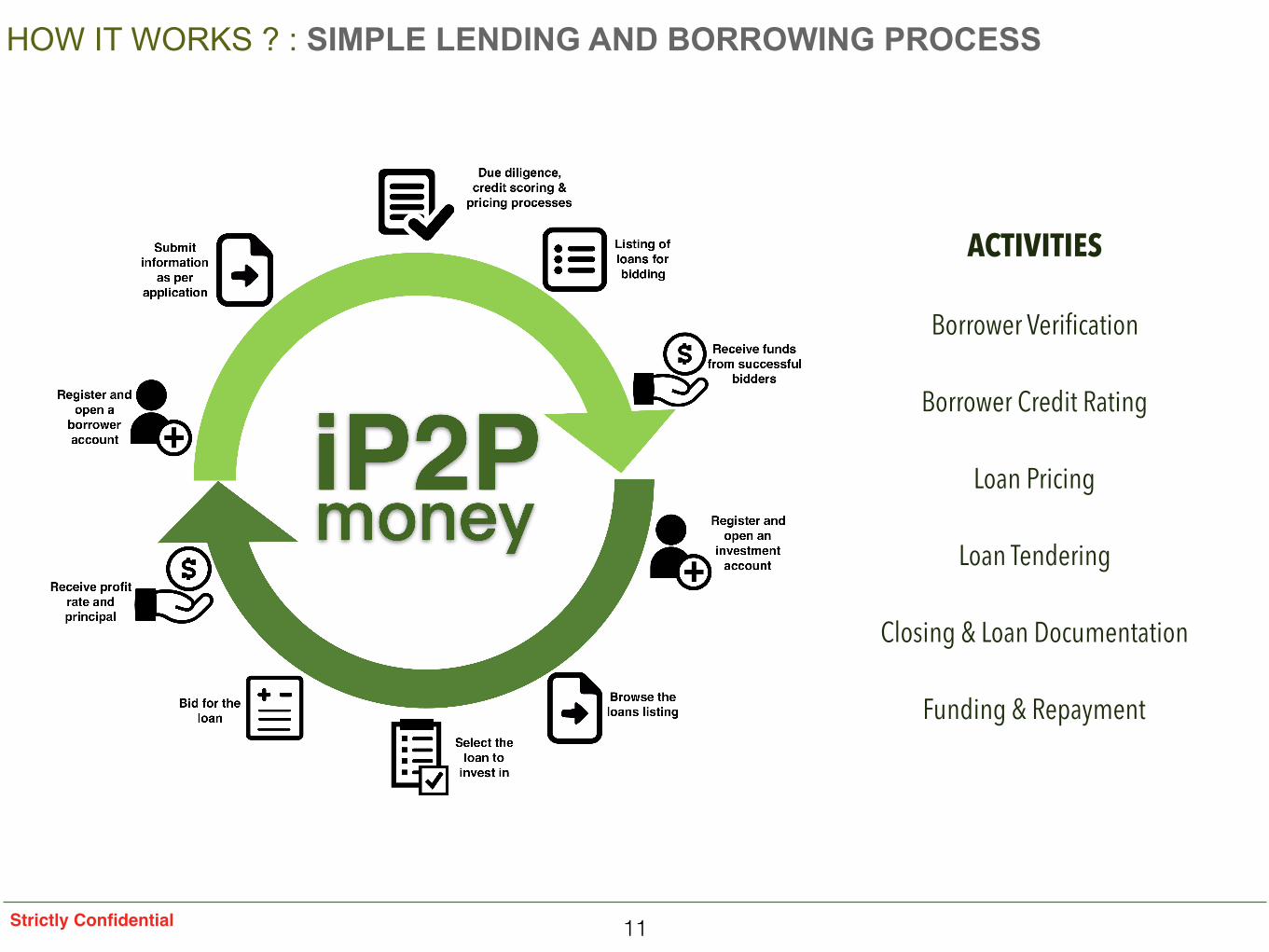

HOW IT WORKS ? : SIMPLE LENDING AND BORROWING PROCESS

ACTIVITIES

Borrower Verification

Borrower Credit Rating

Loan Pricing

Loan Tendering

Closing & Loan Documentation

Funding & Repayment

12

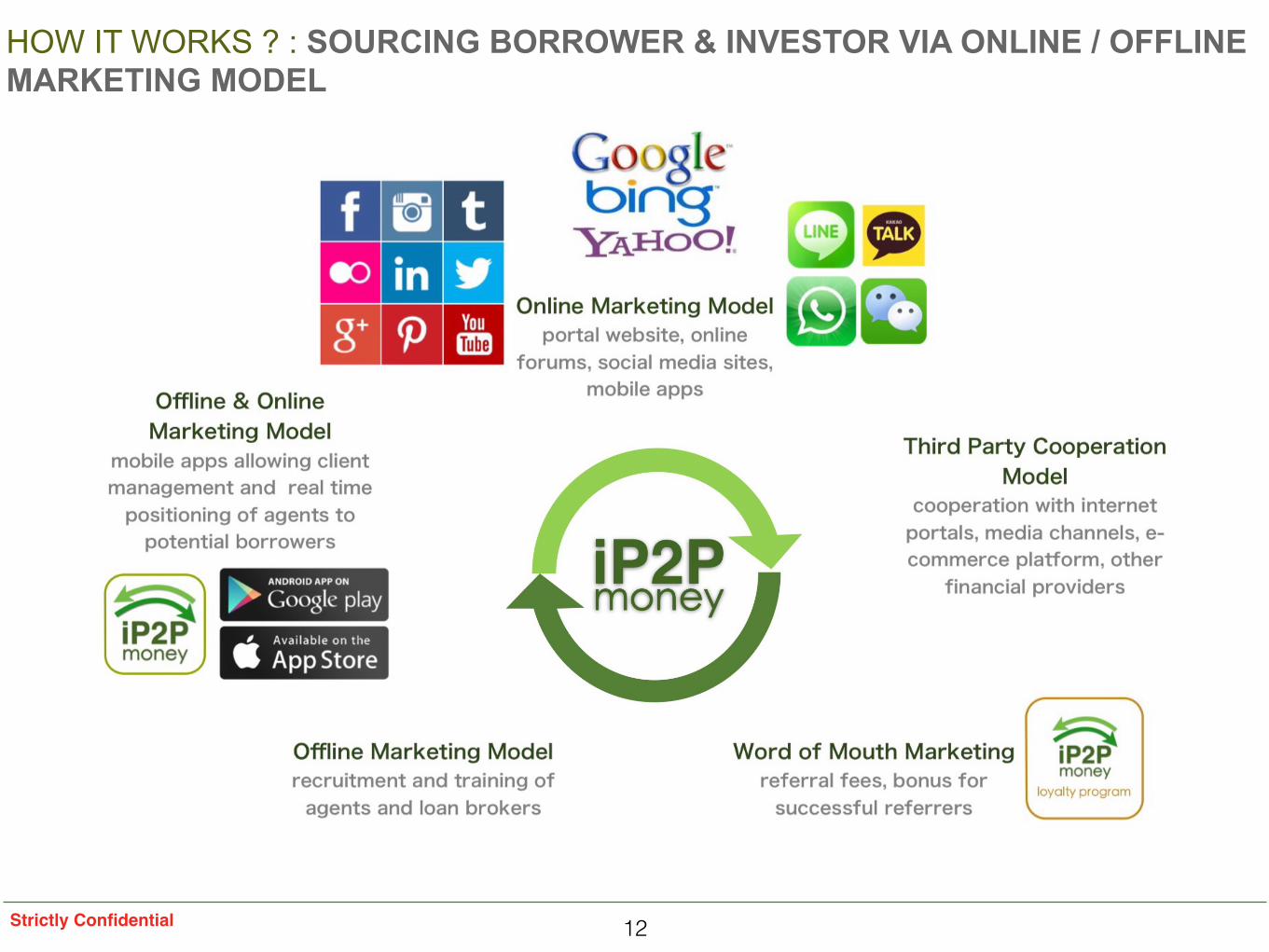

HOW IT WORKS ? : SOURCING BORROWER & INVESTOR VIA ONLINE / OFFLINE MARKETING MODEL

Strictly Confidential

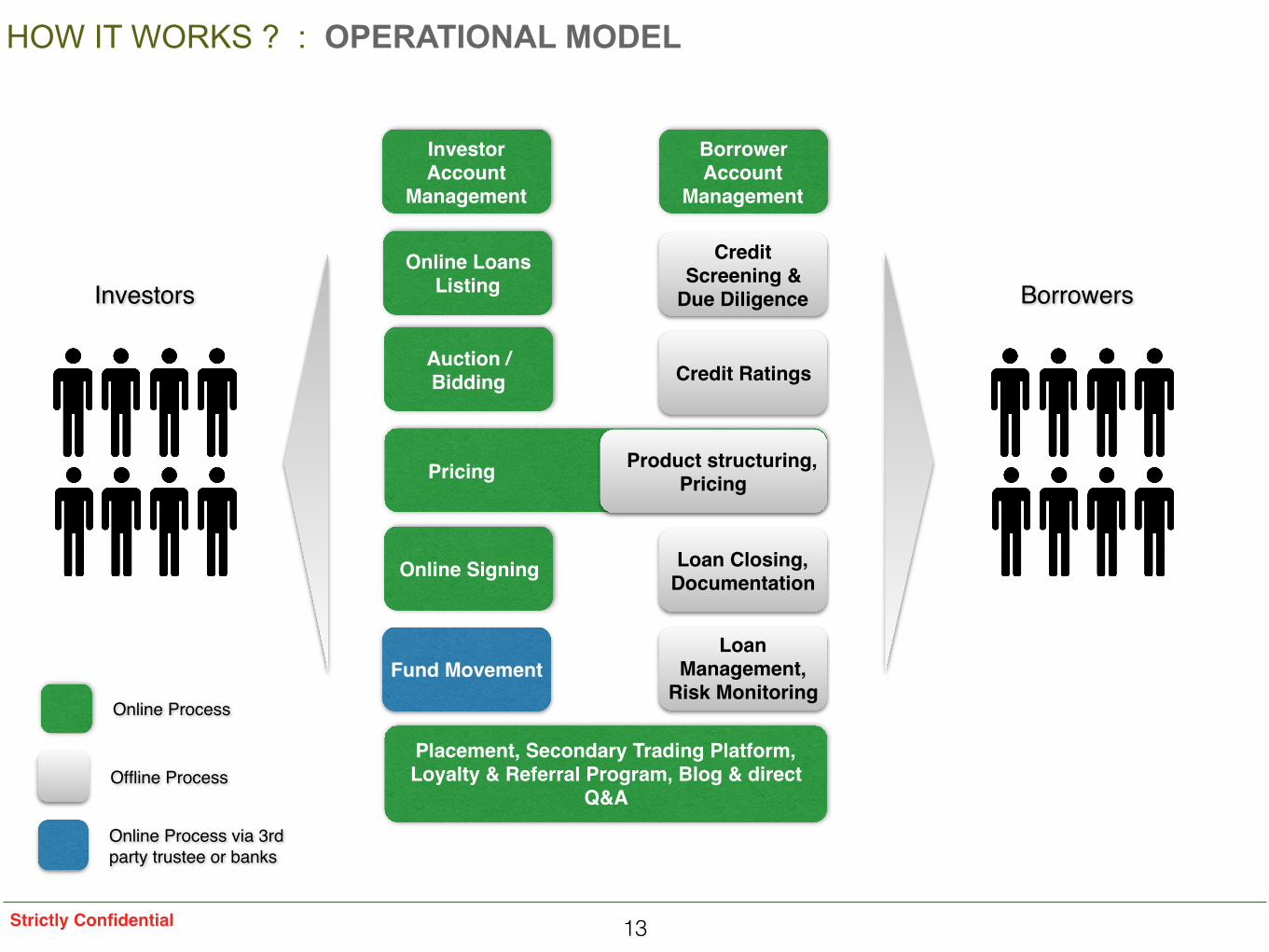

HOW IT WORKS ? : OPERATIONAL MODEL

13

BorrowersInvestors

Pricing

Placement, Secondary Trading Platform, Loyalty & Referral Program, Blog & direct

Q&A

Auction / Bidding

Investor Account

Management

Online Loans Listing

Borrower Account

Management

Online Signing

Online Process

Credit Screening &

Due Diligence

Loan Management,

Risk Monitoring

Credit Ratings

Loan Closing, Documentation

Product structuring,Pricing

Offline Process

Fund Movement

Online Process via 3rd party trustee or banks

Strictly Confidential

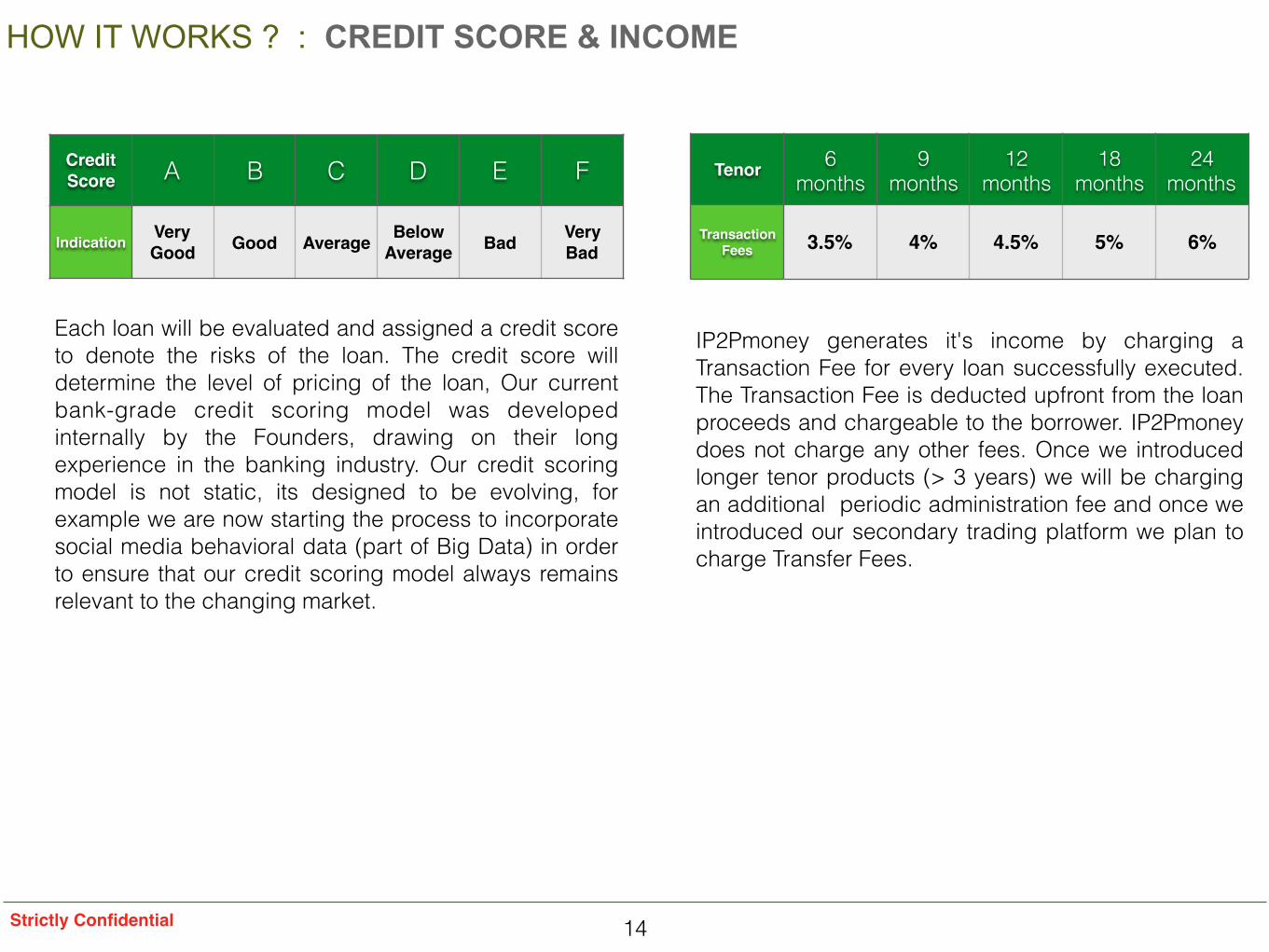

Credit Score A B C D E F

Indication Very Good Good Average Below

Average Bad Very Bad

Each loan will be evaluated and assigned a credit score to denote the risks of the loan. The credit score will determine the level of pricing of the loan, Our current bank-grade credit scoring model was developed internally by the Founders, drawing on their long experience in the banking industry. Our credit scoring model is not static, its designed to be evolving, for example we are now starting the process to incorporate social media behavioral data (part of Big Data) in order to ensure that our credit scoring model always remains relevant to the changing market.

Tenor 6 months

9 months

12 months

18 months

24 months

Transaction Fees 3.5% 4% 4.5% 5% 6%

IP2Pmoney generates it's income by charging a Transaction Fee for every loan successfully executed. The Transaction Fee is deducted upfront from the loan proceeds and chargeable to the borrower. IP2Pmoney does not charge any other fees. Once we introduced longer tenor products (> 3 years) we will be charging an additional periodic administration fee and once we introduced our secondary trading platform we plan to charge Transfer Fees.

HOW IT WORKS ? : CREDIT SCORE & INCOME

14Strictly Confidential

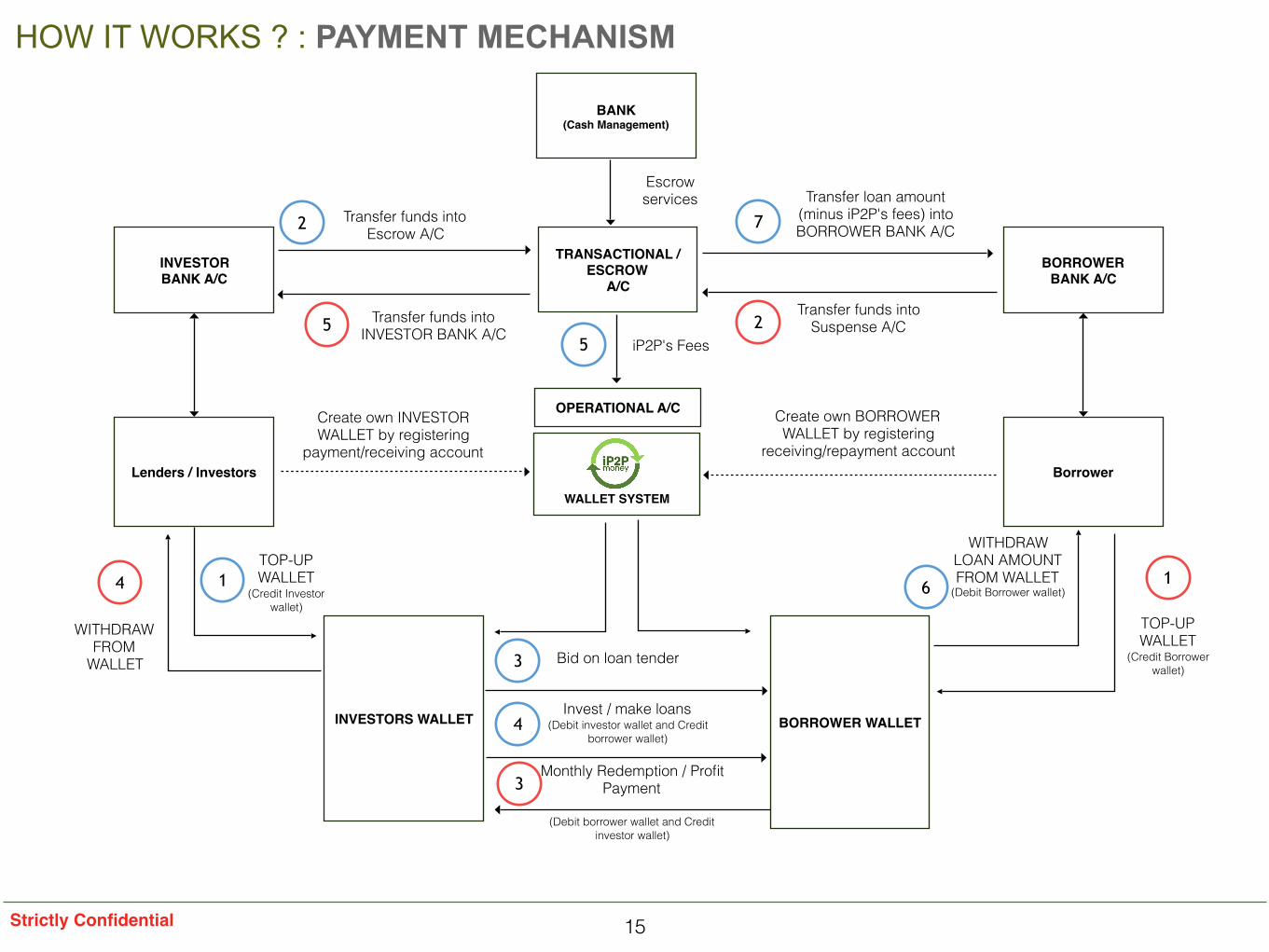

HOW IT WORKS ? : PAYMENT MECHANISM

15

INVESTORS WALLET

Lenders / Investors

Create own INVESTOR WALLET by registering

payment/receiving account

Transfer funds into Escrow A/C

Invest / make loans (Debit investor wallet and Credit

borrower wallet)

Monthly Redemption / Profit Payment

(Debit borrower wallet and Credit investor wallet)

BORROWER WALLET

Borrower

WALLET SYSTEM

TRANSACTIONAL / ESCROW

A/CBORROWER

BANK A/CINVESTOR BANK A/C

Create own BORROWER WALLET by registering

receiving/repayment account

TOP-UP WALLET

(Credit Investor wallet)

WITHDRAW FROM

WALLET

Transfer funds into INVESTOR BANK A/C

1

2

1

WITHDRAW LOAN AMOUNT FROM WALLET

(Debit Borrower wallet)

3 Bid on loan tender

4

Transfer loan amount (minus iP2P's fees) into BORROWER BANK A/C7

6

TOP-UP WALLET

(Credit Borrower wallet)

Transfer funds into Suspense A/C2

3

4

5

BANK (Cash Management)

Escrow services

OPERATIONAL A/C

iP2P's Fees5

Strictly Confidential

16Strictly Confidential

3 iP2Pmoney Lo-costs Managed Franchise Model

17Strictly Confidential

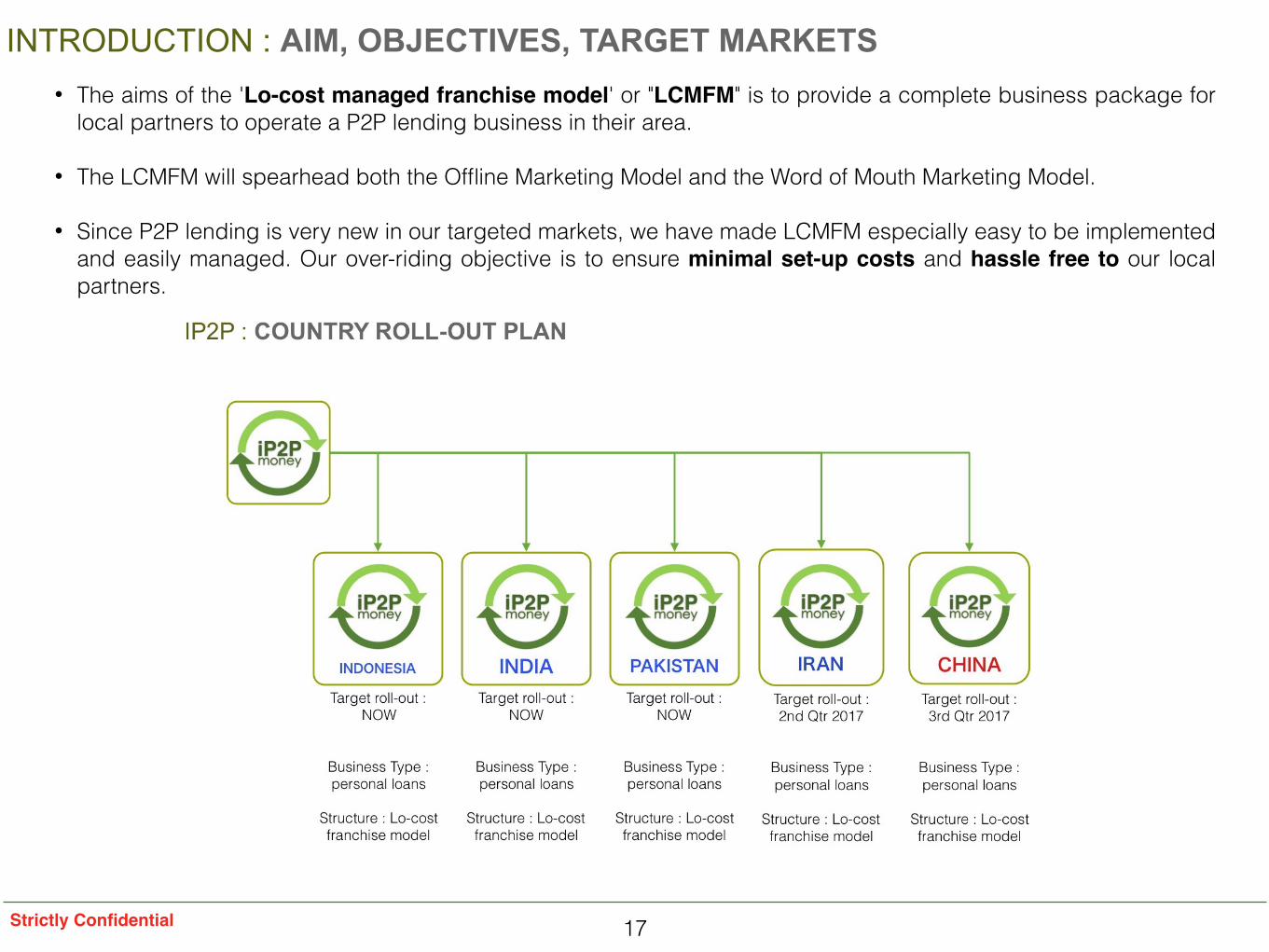

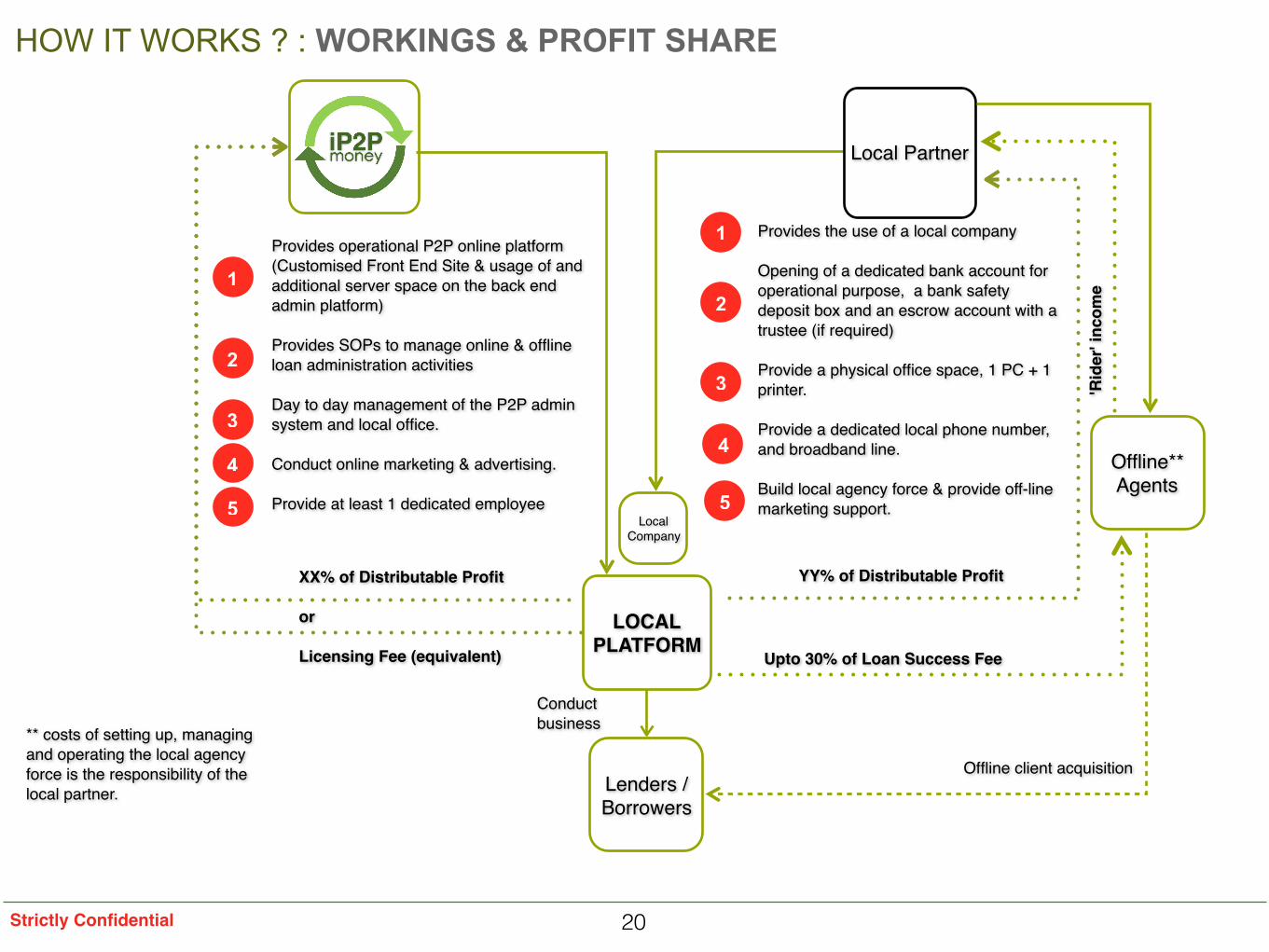

INTRODUCTION : AIM, OBJECTIVES, TARGET MARKETS• The aims of the 'Lo-cost managed franchise model' or "LCMFM" is to provide a complete business package for

local partners to operate a P2P lending business in their area.

• The LCMFM will spearhead both the Offline Marketing Model and the Word of Mouth Marketing Model.

• Since P2P lending is very new in our targeted markets, we have made LCMFM especially easy to be implemented and easily managed. Our over-riding objective is to ensure minimal set-up costs and hassle free to our local partners.

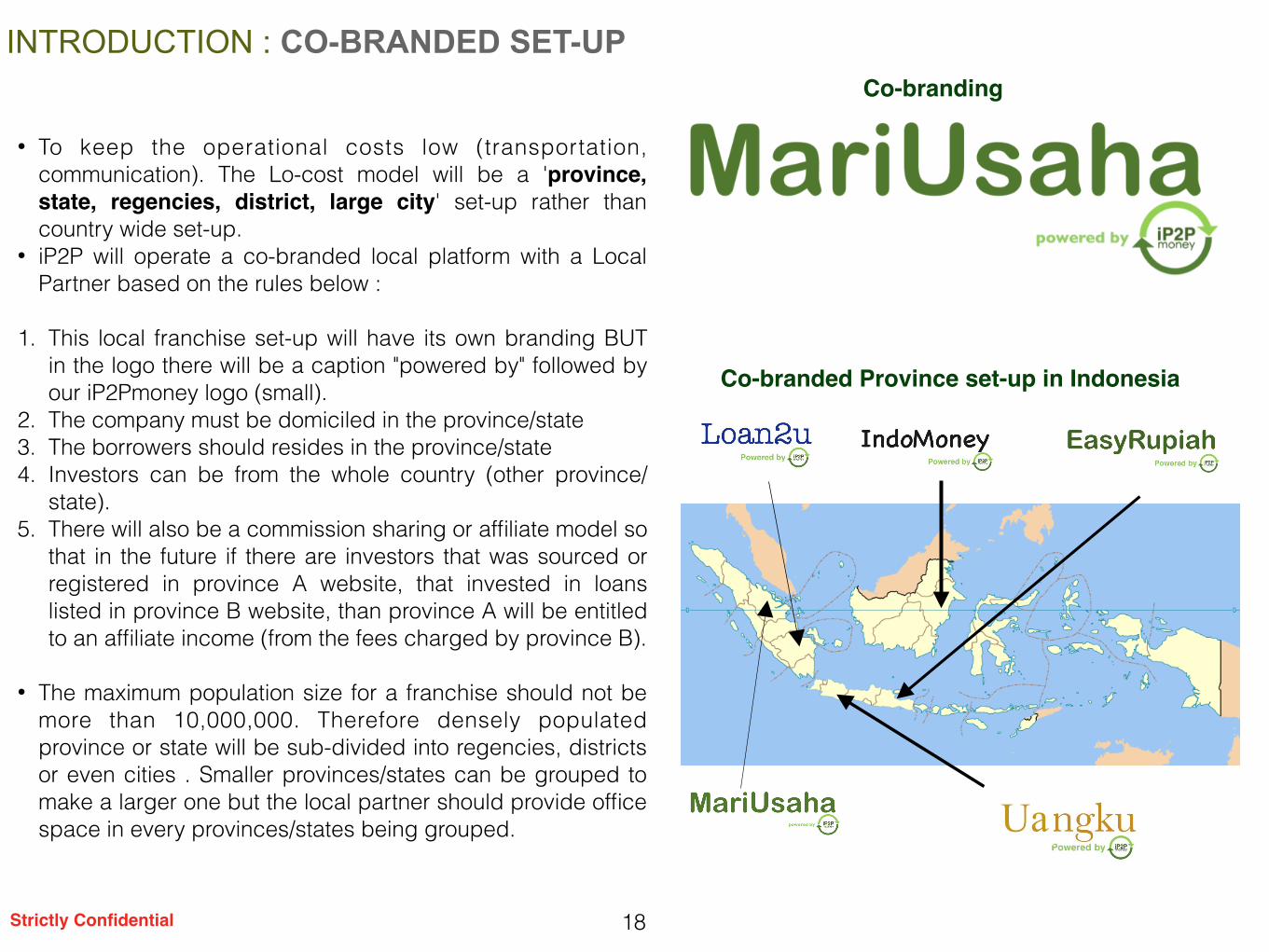

• To keep the operational costs low (transportation, communication). The Lo-cost model will be a 'province, state, regencies, district, large city' set-up rather than country wide set-up.

• iP2P will operate a co-branded local platform with a Local Partner based on the rules below :

1. This local franchise set-up will have its own branding BUT in the logo there will be a caption "powered by" followed by our iP2Pmoney logo (small).

2. The company must be domiciled in the province/state 3. The borrowers should resides in the province/state 4. Investors can be from the whole country (other province/

state). 5. There will also be a commission sharing or affiliate model so

that in the future if there are investors that was sourced or registered in province A website, that invested in loans listed in province B website, than province A will be entitled to an affiliate income (from the fees charged by province B).

• The maximum population size for a franchise should not be more than 10,000,000. Therefore densely populated province or state will be sub-divided into regencies, districts or even cities . Smaller provinces/states can be grouped to make a larger one but the local partner should provide office space in every provinces/states being grouped.

Co-branded Province set-up in Indonesia

18Strictly Confidential

INTRODUCTION : CO-BRANDED SET-UP

Ua

Co-branding

19Strictly Confidential

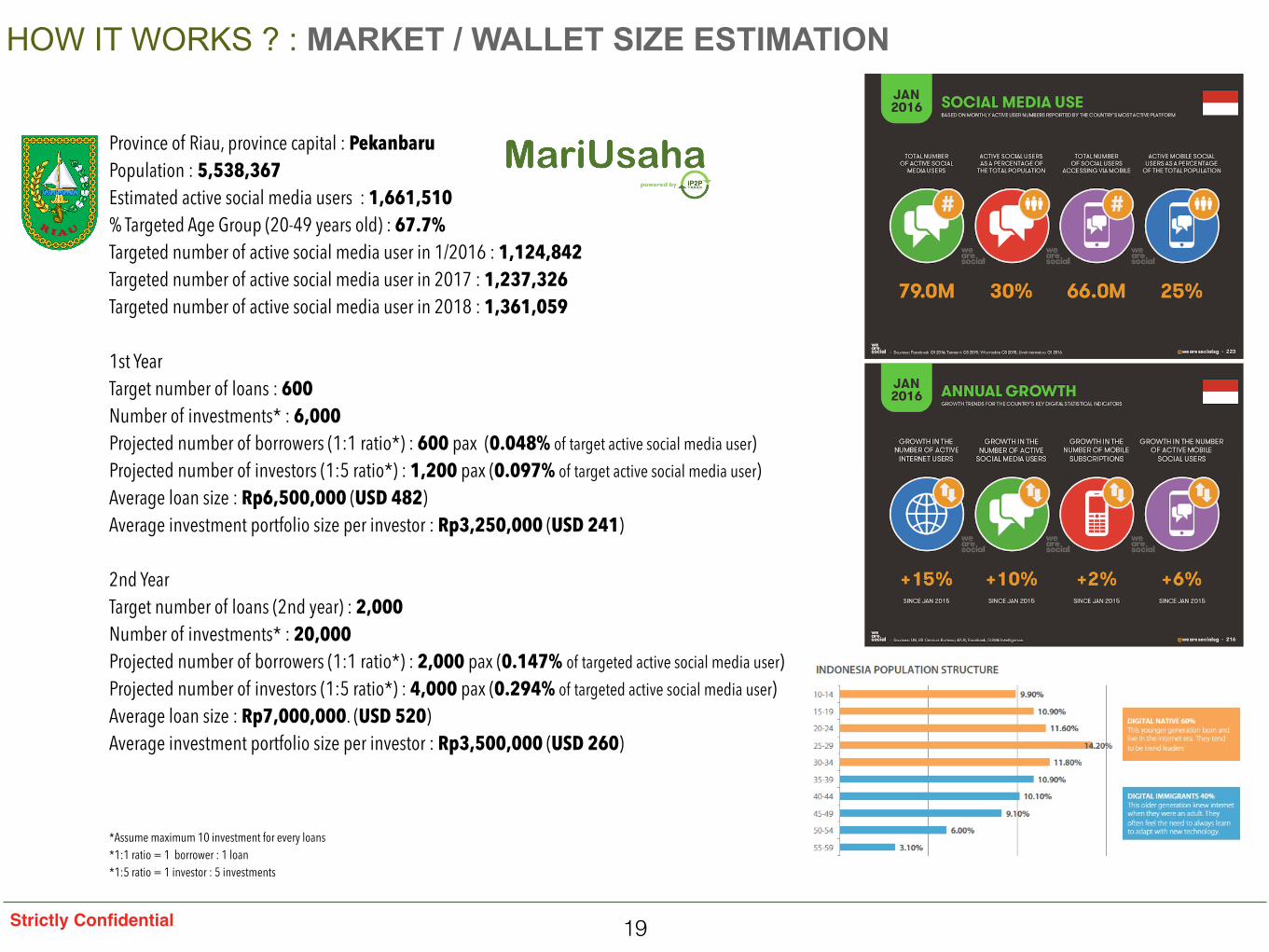

HOW IT WORKS ? : MARKET / WALLET SIZE ESTIMATION

Province of Riau, province capital : Pekanbaru Population : 5,538,367 Estimated active social media users : 1,661,510 % Targeted Age Group (20-49 years old) : 67.7% Targeted number of active social media user in 1/2016 : 1,124,842 Targeted number of active social media user in 2017 : 1,237,326 Targeted number of active social media user in 2018 : 1,361,059

1st Year Target number of loans : 600 Number of investments* : 6,000 Projected number of borrowers (1:1 ratio*) : 600 pax (0.048% of target active social media user) Projected number of investors (1:5 ratio*) : 1,200 pax (0.097% of target active social media user) Average loan size : Rp6,500,000 (USD 482) Average investment portfolio size per investor : Rp3,250,000 (USD 241)

2nd Year Target number of loans (2nd year) : 2,000 Number of investments* : 20,000 Projected number of borrowers (1:1 ratio*) : 2,000 pax (0.147% of targeted active social media user) Projected number of investors (1:5 ratio*) : 4,000 pax (0.294% of targeted active social media user) Average loan size : Rp7,000,000. (USD 520) Average investment portfolio size per investor : Rp3,500,000 (USD 260)

*Assume maximum 10 investment for every loans *1:1 ratio = 1 borrower : 1 loan *1:5 ratio = 1 investor : 5 investments

Local Company

Local Partner

Conduct business

Lenders / Borrowers

2

3

4

Provides operational P2P online platform (Customised Front End Site & usage of and additional server space on the back end admin platform)

Provides SOPs to manage online & offline loan administration activities

Day to day management of the P2P admin system and local office.

Conduct online marketing & advertising.

Provide at least 1 dedicated employee

1

Offline client acquisition

5

1 Provides the use of a local company

Opening of a dedicated bank account for operational purpose, a bank safety deposit box and an escrow account with a trustee (if required)

Provide a physical office space, 1 PC + 1 printer.

Provide a dedicated local phone number, and broadband line.

Build local agency force & provide off-line marketing support.

2

3

4

XX% of Distributable Profit

or

Licensing Fee (equivalent)

YY% of Distributable Profit

Upto 30% of Loan Success Fee

Offline** Agents

** costs of setting up, managing and operating the local agency force is the responsibility of the local partner.

20Strictly Confidential

LOCAL PLATFORM

5

'Rid

er' i

ncom

e

HOW IT WORKS ? : WORKINGS & PROFIT SHARE

21Strictly Confidential

HOW IT WORKS ? : OPERATIONAL P2P ONLINE PLATFORM

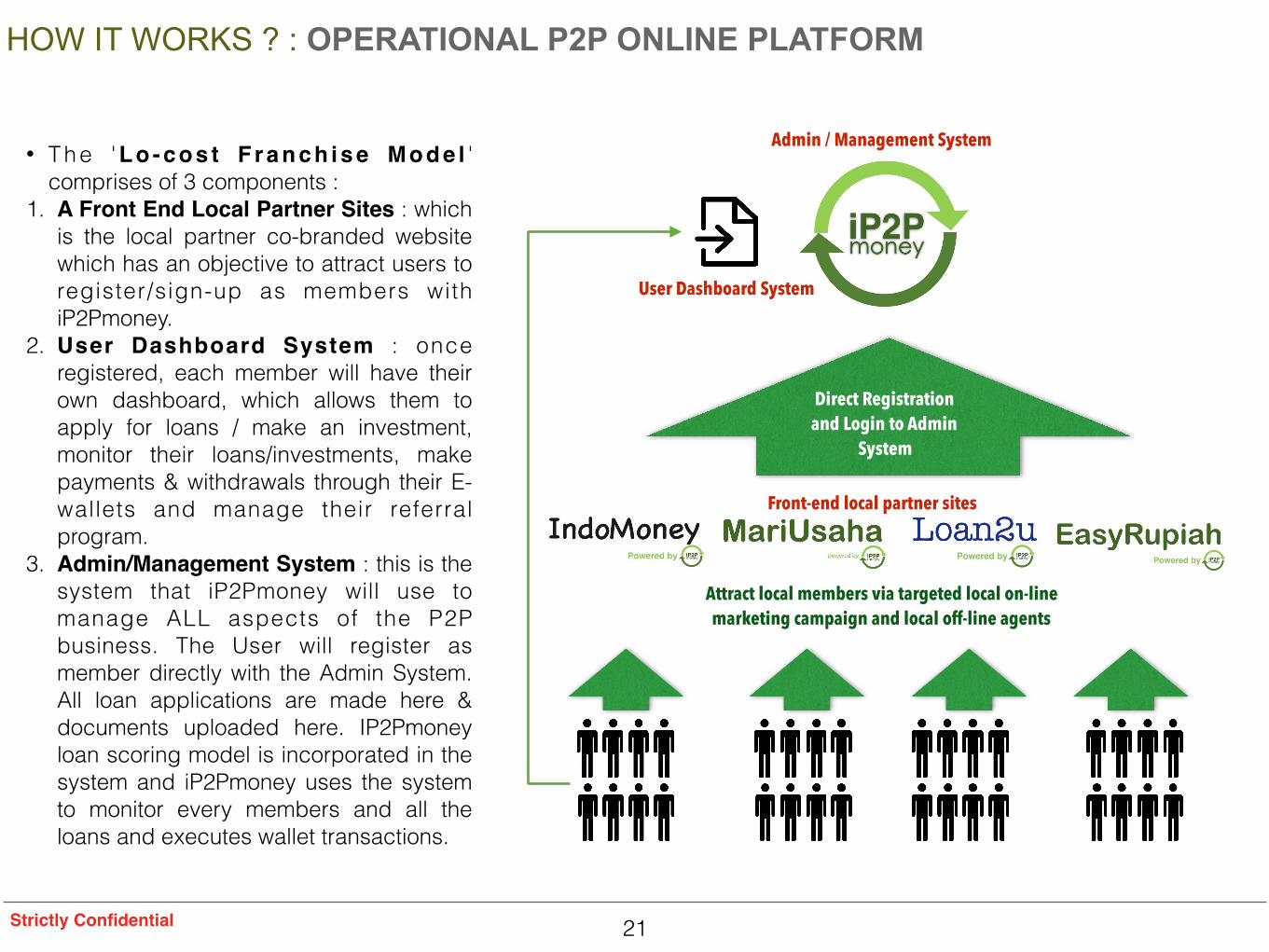

• T h e ' L o - c o s t F r a n c h i s e M o d e l ' comprises of 3 components :

1. A Front End Local Partner Sites : which is the local partner co-branded website which has an objective to attract users to register/sign-up as members with iP2Pmoney.

2. User Dashboard System : once registered, each member will have their own dashboard, which allows them to apply for loans / make an investment, monitor their loans/investments, make payments & withdrawals through their E-wallets and manage their referral program.

3. Admin/Management System : this is the system that iP2Pmoney will use to manage ALL aspects of the P2P business. The User will register as member directly with the Admin System. All loan applications are made here & documents uploaded here. IP2Pmoney loan scoring model is incorporated in the system and iP2Pmoney uses the system to monitor every members and all the loans and executes wallet transactions.

Admin / Management System

Front-end local partner sites

Direct Registration and Login to Admin

System

Attract local members via targeted local on-line marketing campaign and local off-line agents

User Dashboard System

22Strictly Confidential

4 Summary Financials

23Strictly Confidential

FINANCIALS PER LOCATIONS

Projected Loan Volume by Country

$0

$30,000,000

$60,000,000

$90,000,000

$120,000,000

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

$19,905,934

$10,635,564

$4,221,694

$997,074

$15,115

$41,696,677

$24,080,516

$11,541,184

$4,346,316$642,105

$42,896,047

$23,562,022

$10,822,238$3,718,137$445,356

INDIA Loan Volume INDONESIA Loan Volume PAKISTAN Loan Volume

Projected Net Revenue by Country

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

$627,037

$335,020

$132,983

$31,408$476

$1,313,445

$758,536

$363,547$136,909$20,226

$1,351,225$742,204

$340,901$117,121$14,029

INDIA Net Revenue (after deducting Commision)INDONESIA Net Revenue (after deducting Commision)PAKISTAN Net Revenue (after deducting Commision)

Projected Number of LCMFM by Country

0

4

8

11

15

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

776

4

2

1212

10

8

5

121211

7

4

No. INDIA's LCMFM No. INDONESIA's LCMFM No. of PAKISTAN's LCMFM

24Strictly Confidential

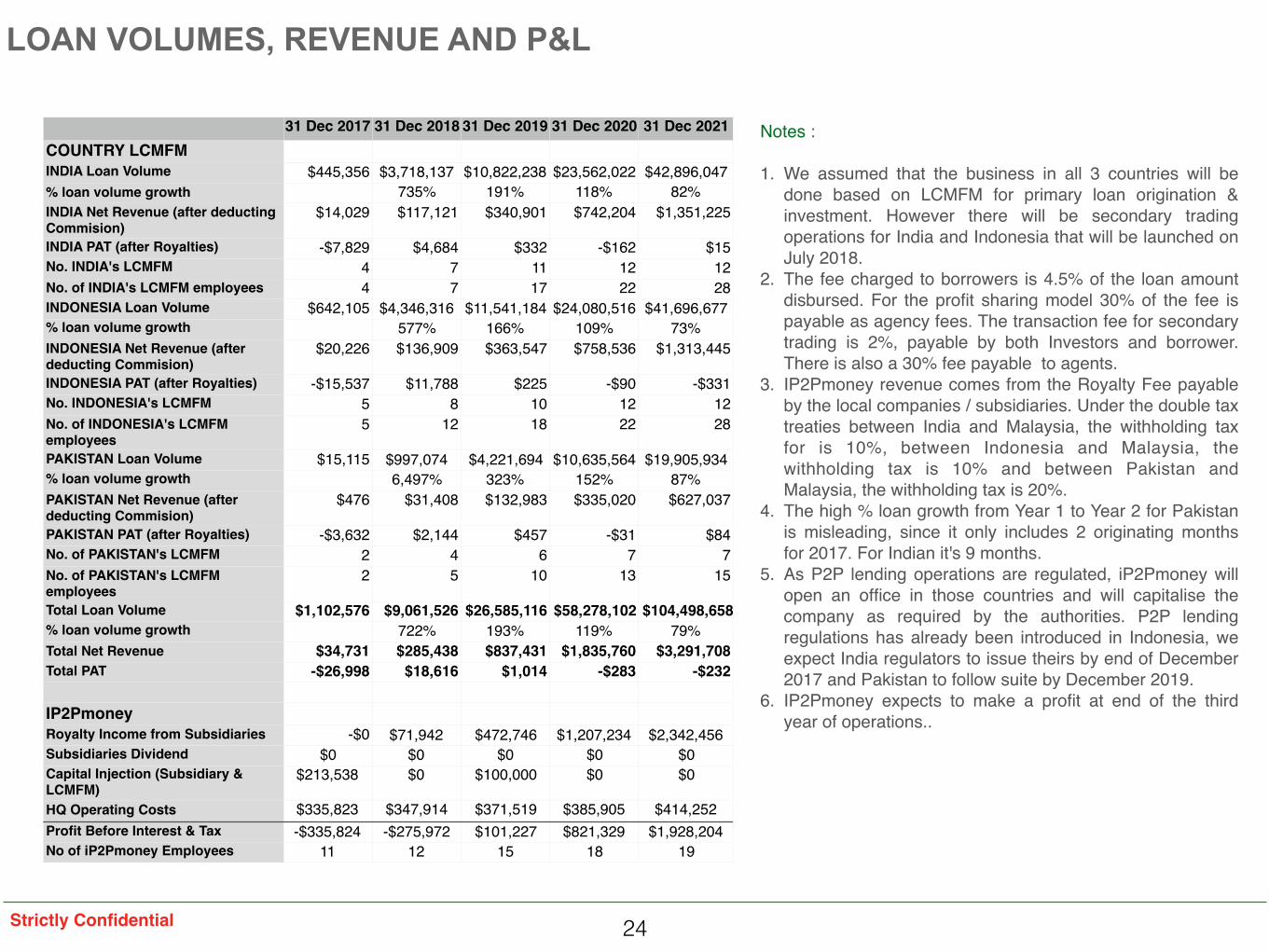

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021COUNTRY LCMFMINDIA Loan Volume $445,356 $3,718,137 $10,822,238 $23,562,022 $42,896,047% loan volume growth 735% 191% 118% 82%INDIA Net Revenue (after deducting Commision)

$14,029 $117,121 $340,901 $742,204 $1,351,225

INDIA PAT (after Royalties) -$7,829 $4,684 $332 -$162 $15No. INDIA's LCMFM 4 7 11 12 12No. of INDIA's LCMFM employees 4 7 17 22 28INDONESIA Loan Volume $642,105 $4,346,316 $11,541,184 $24,080,516 $41,696,677% loan volume growth 577% 166% 109% 73%INDONESIA Net Revenue (after deducting Commision)

$20,226 $136,909 $363,547 $758,536 $1,313,445

INDONESIA PAT (after Royalties) -$15,537 $11,788 $225 -$90 -$331No. INDONESIA's LCMFM 5 8 10 12 12No. of INDONESIA's LCMFM employees

5 12 18 22 28

PAKISTAN Loan Volume $15,115 $997,074 $4,221,694 $10,635,564 $19,905,934% loan volume growth 6,497% 323% 152% 87%PAKISTAN Net Revenue (after deducting Commision)

$476 $31,408 $132,983 $335,020 $627,037

PAKISTAN PAT (after Royalties) -$3,632 $2,144 $457 -$31 $84No. of PAKISTAN's LCMFM 2 4 6 7 7No. of PAKISTAN's LCMFM employees

2 5 10 13 15

Total Loan Volume $1,102,576 $9,061,526 $26,585,116 $58,278,102 $104,498,658% loan volume growth 722% 193% 119% 79%Total Net Revenue $34,731 $285,438 $837,431 $1,835,760 $3,291,708Total PAT -$26,998 $18,616 $1,014 -$283 -$232

IP2PmoneyRoyalty Income from Subsidiaries -$0 $71,942 $472,746 $1,207,234 $2,342,456Subsidiaries Dividend $0 $0 $0 $0 $0Capital Injection (Subsidiary & LCMFM)

$213,538 $0 $100,000 $0 $0

HQ Operating Costs $335,823 $347,914 $371,519 $385,905 $414,252Profit Before Interest & Tax -$335,824 -$275,972 $101,227 $821,329 $1,928,204No of iP2Pmoney Employees 11 12 15 18 19

Notes :

1. We assumed that the business in all 3 countries will be done based on LCMFM for primary loan origination & investment. However there will be secondary trading operations for India and Indonesia that will be launched on July 2018.

2. The fee charged to borrowers is 4.5% of the loan amount disbursed. For the profit sharing model 30% of the fee is payable as agency fees. The transaction fee for secondary trading is 2%, payable by both Investors and borrower. There is also a 30% fee payable to agents.

3. IP2Pmoney revenue comes from the Royalty Fee payable by the local companies / subsidiaries. Under the double tax treaties between India and Malaysia, the withholding tax for is 10%, between Indonesia and Malaysia, the withholding tax is 10% and between Pakistan and Malaysia, the withholding tax is 20%.

4. The high % loan growth from Year 1 to Year 2 for Pakistan is misleading, since it only includes 2 originating months for 2017. For Indian it's 9 months.

5. As P2P lending operations are regulated, iP2Pmoney will open an office in those countries and will capitalise the company as required by the authorities. P2P lending regulations has already been introduced in Indonesia, we expect India regulators to issue theirs by end of December 2017 and Pakistan to follow suite by December 2019.

6. IP2Pmoney expects to make a profit at end of the third year of operations..

LOAN VOLUMES, REVENUE AND P&L

25Strictly Confidential

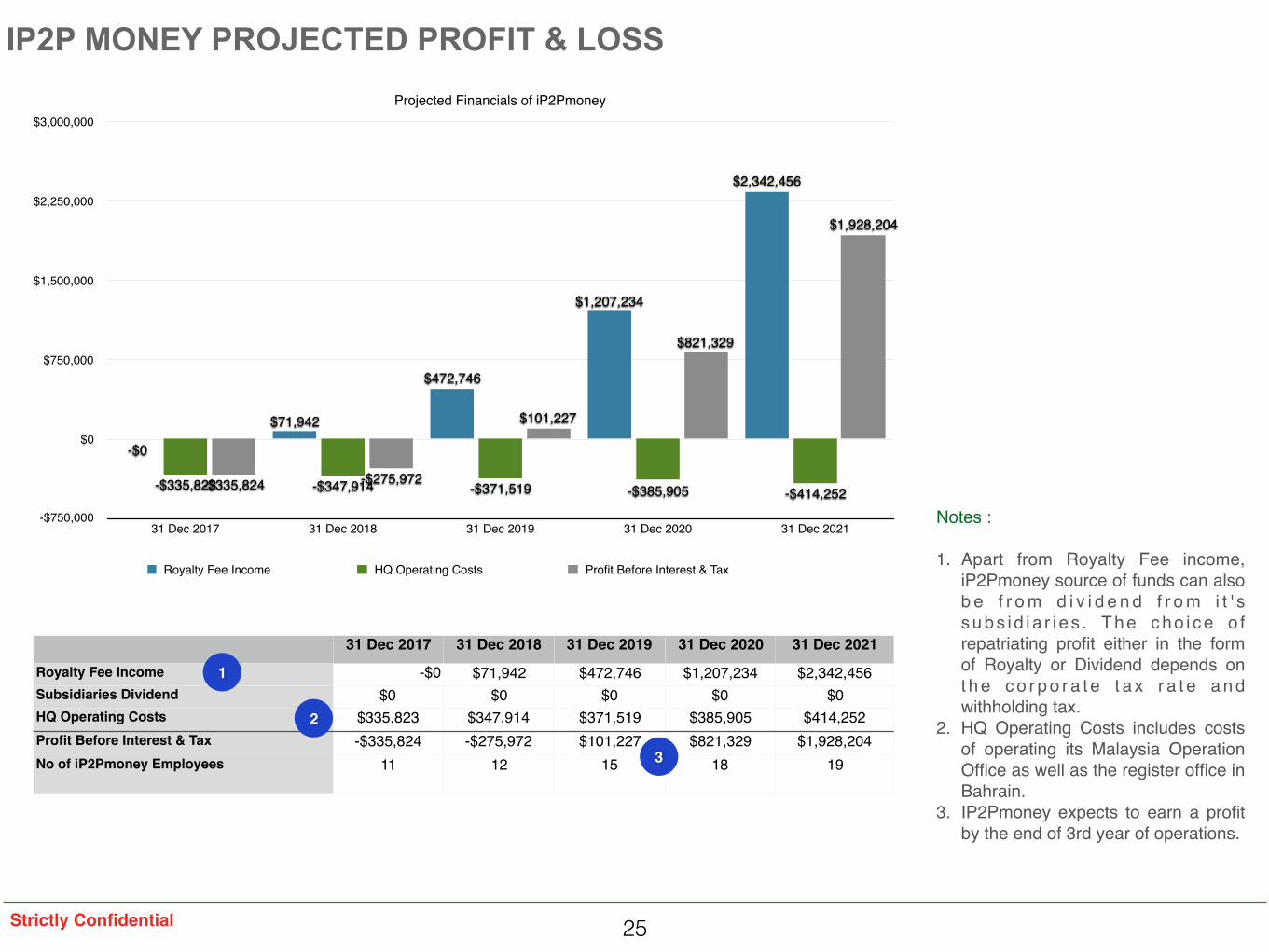

IP2P MONEY PROJECTED PROFIT & LOSS Projected Financials of iP2Pmoney

-$750,000

$0

$750,000

$1,500,000

$2,250,000

$3,000,000

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

$1,928,204

$821,329

$101,227

-$275,972-$335,824 -$414,252-$385,905-$371,519-$347,914-$335,823

$2,342,456

$1,207,234

$472,746

$71,942

-$0

Royalty Fee Income HQ Operating Costs Profit Before Interest & Tax

Notes :

1. Apart from Royalty Fee income, iP2Pmoney source of funds can also b e f r o m d i v i d e n d f r o m i t ' s s u b s i d i a r i e s . T h e c h o i c e o f repatriating profit either in the form of Royalty or Dividend depends on t h e c o r p o r a t e t a x r a t e a n d withholding tax.

2. HQ Operating Costs includes costs of operating its Malaysia Operation Office as well as the register office in Bahrain.

3. IP2Pmoney expects to earn a profit by the end of 3rd year of operations.

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

Royalty Fee Income -$0 $71,942 $472,746 $1,207,234 $2,342,456Subsidiaries Dividend $0 $0 $0 $0 $0HQ Operating Costs $335,823 $347,914 $371,519 $385,905 $414,252Profit Before Interest & Tax -$335,824 -$275,972 $101,227 $821,329 $1,928,204No of iP2Pmoney Employees 11 12 15 18 19

1

2

3

26Strictly Confidential

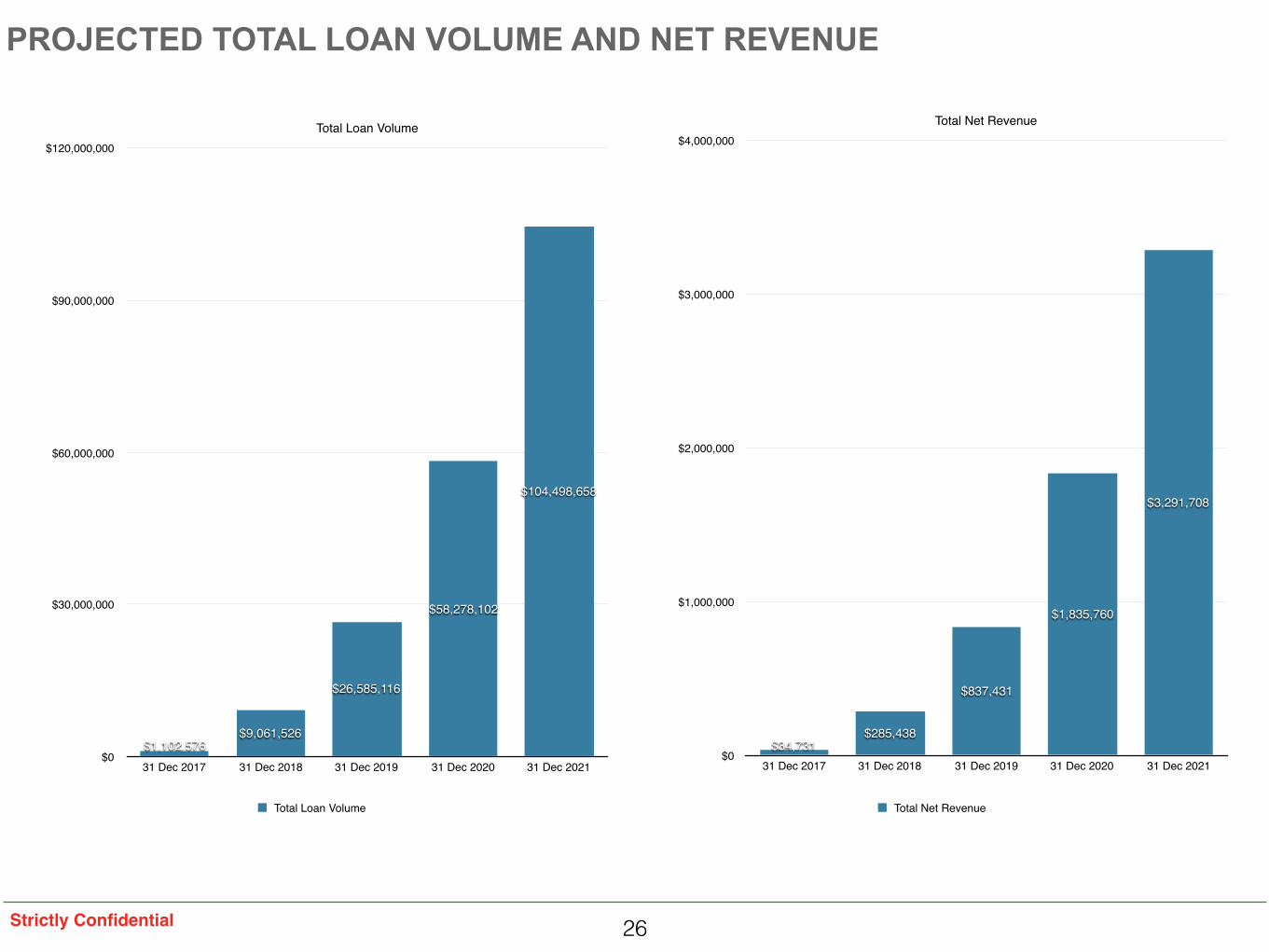

PROJECTED TOTAL LOAN VOLUME AND NET REVENUE

Total Loan Volume

$0

$30,000,000

$60,000,000

$90,000,000

$120,000,000

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

$104,498,658

$58,278,102

$26,585,116

$9,061,526$1,102,576

Total Loan Volume

Total Net Revenue

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

$3,291,708

$1,835,760

$837,431

$285,438$34,731

Total Net Revenue

27Strictly Confidential

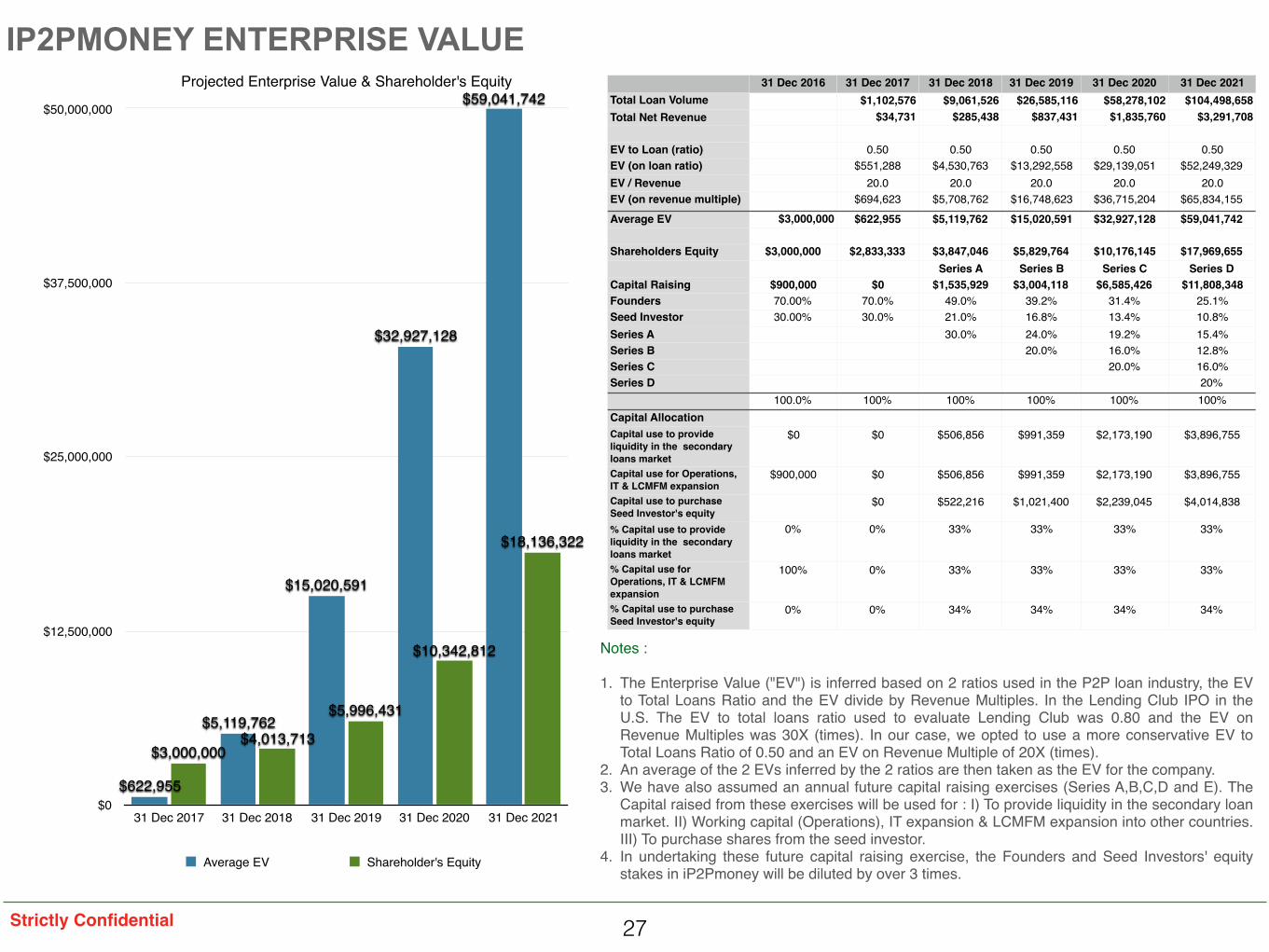

IP2PMONEY ENTERPRISE VALUE

Notes :

1. The Enterprise Value ("EV") is inferred based on 2 ratios used in the P2P loan industry, the EV to Total Loans Ratio and the EV divide by Revenue Multiples. In the Lending Club IPO in the U.S. The EV to total loans ratio used to evaluate Lending Club was 0.80 and the EV on Revenue Multiples was 30X (times). In our case, we opted to use a more conservative EV to Total Loans Ratio of 0.50 and an EV on Revenue Multiple of 20X (times).

2. An average of the 2 EVs inferred by the 2 ratios are then taken as the EV for the company.3. We have also assumed an annual future capital raising exercises (Series A,B,C,D and E). The

Capital raised from these exercises will be used for : I) To provide liquidity in the secondary loan market. II) Working capital (Operations), IT expansion & LCMFM expansion into other countries. III) To purchase shares from the seed investor.

4. In undertaking these future capital raising exercise, the Founders and Seed Investors' equity stakes in iP2Pmoney will be diluted by over 3 times.

31 Dec 2016 31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021Total Loan Volume $1,102,576 $9,061,526 $26,585,116 $58,278,102 $104,498,658Total Net Revenue $34,731 $285,438 $837,431 $1,835,760 $3,291,708

EV to Loan (ratio) 0.50 0.50 0.50 0.50 0.50EV (on loan ratio) $551,288 $4,530,763 $13,292,558 $29,139,051 $52,249,329EV / Revenue 20.0 20.0 20.0 20.0 20.0EV (on revenue multiple) $694,623 $5,708,762 $16,748,623 $36,715,204 $65,834,155Average EV $3,000,000 $622,955 $5,119,762 $15,020,591 $32,927,128 $59,041,742

Shareholders Equity $3,000,000 $2,833,333 $3,847,046 $5,829,764 $10,176,145 $17,969,655Series A Series B Series C Series D

Capital Raising $900,000 $0 $1,535,929 $3,004,118 $6,585,426 $11,808,348Founders 70.00% 70.0% 49.0% 39.2% 31.4% 25.1%Seed Investor 30.00% 30.0% 21.0% 16.8% 13.4% 10.8%Series A 30.0% 24.0% 19.2% 15.4%Series B 20.0% 16.0% 12.8%Series C 20.0% 16.0%Series D 20%

100.0% 100% 100% 100% 100% 100%Capital AllocationCapital use to provide liquidity in the secondary loans market

$0 $0 $506,856 $991,359 $2,173,190 $3,896,755

Capital use for Operations, IT & LCMFM expansion

$900,000 $0 $506,856 $991,359 $2,173,190 $3,896,755

Capital use to purchase Seed Investor's equity

$0 $522,216 $1,021,400 $2,239,045 $4,014,838

% Capital use to provide liquidity in the secondary loans market

0% 0% 33% 33% 33% 33%

% Capital use for Operations, IT & LCMFM expansion

100% 0% 33% 33% 33% 33%

% Capital use to purchase Seed Investor's equity

0% 0% 34% 34% 34% 34%

Projected Enterprise Value & Shareholder's Equity

$0

$12,500,000

$25,000,000

$37,500,000

$50,000,000

31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

$18,136,322

$10,342,812

$5,996,431

$4,013,713$3,000,000

$59,041,742

$32,927,128

$15,020,591

$5,119,762

$622,955

Average EV Shareholder's Equity

28Strictly Confidential

SEED INVESTORS FUTURE CASH FLOWS

Notes :

1. A clause will be put in the agreement allowing seed investors to exit their investments from proceeds of the annual fund raising. Founders are prohibited from selling their shares until after 5 years.

2. Throughout an investment period of 5 years, the seed investors will sell down their shares for cash from 30% in i t ia l shareholding to 10.8% shareholding at the end of 5 years.

3. The IRR for the seed investor is projected to be 89.15% per annum.

4. The remaining 10.8% shareholding in the company is projected to be worth nearly $6.34 million at the end of 5 years.

31 Dec 2016 31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021Tenor (months) 0 12 24 36 48 60Investment -$900,000Share Disposal Proceeds $0 $522,216 $1,021,400 $2,239,045 $4,014,838Valuation at end of Year 5 $6,348,168Internal Rate of Return 1.000 0.521 0.271 0.141 0.074 0.038NPV -$900,000 $0 $141,660 $144,309 $164,762 $397,173IRR = 89.15%

2

3

41

Seed Investors Future Cash Flows

-$1,750,000

$0

$1,750,000

$3,500,000

$5,250,000

$7,000,000

31 Dec 2016 31 Dec 2017 31 Dec 2018 31 Dec 2019 31 Dec 2020 31 Dec 2021

$6,348,168

$0$0$0$0$0

$4,014,838

$2,239,045

$1,021,400$522,216

$0$0 $0$0$0$0$0

-$900,000

Investment Share Disposal Proceeds Valuation at end of Year 5

Strictly Confidential

Thank YouTerimakasih谢谢

LEBROS CONNECTION SDN. BHD.

21-2, Jalan SS 23/15, Taman Sea, 47400 Petaling Jaya, Selangor Darul Ehsan, Malaysia