ipe ii: monetary macroeconomics · 4.institutional analysis of monetary, fiscal and exchange rate...

TRANSCRIPT

IPE II: Monetary Macroeconomics

(Module MW25.3)

Prof. Dr. A. Freytag, PD Dr. M. Pasche

Friedrich Schiller University Jena

Work in progress! Bug report to: [email protected]

1

Outline:

1. Introduction

2. Exchange Rates and Current Account

2.1 Preliminaries2.2 Determinants of Exchange Rates2.3 Exchange Rates and Current Account Response

3. Monetary Macroeconomic Models

3.1 Overshooting Model (Dornbusch)3.2 New Keynesian Model

4. Institutional Analysis of Monetary, Fiscal and Exchange RatePolicy

4.1 Historical Exchange Rate Regimes4.2 Rule Binding and Discretionary Monetry Policy in an Open

Economy4.3 Rules, Independence, Credibility – the Problem of

Interdependence of Monetary and Fiscal Policy4.4 Governmental Debt, Inflation and Currency Crisis

2

5. Currency Crisis

5.1 Models of Currency Crisis5.2 Currency Crisis in a Monetary Union

Basic Literature:

I Cukierman, A.S. (1992), Central Bank Strategy, Creditibility andIndependence. Theory and Evidence. Cambridge/Mass. and London.The MIT Press.

I de Haan, J., Oosterloo, S., Schoenmaker, D. (2009), EuropeanFinancial Markets and Institutions. Cambridge: CambridgeUniversity Press:

3

I Fischer, S., Vegh, S., Vegh, C. (2002), Modern Hyper- and HighInflations. Journal of Economic Literature, Vol. XL, pp. 837-880.

I Hayek, F.A. von (1990), Denationalisation of Money – TheArgument Refined. Institute of Economic Affairs, Hobart PaperSpecial 70, London.

I Krugman, P.R., Obstfeld, M., Melitz, M. (2014), InternationalEconomics: Theory and Policy, 10th edition, Prentice Hall.

I MacDonald, R. (2007), Exchange Rate Economics: Theory andEvidence. London and New York: Routledge.

I Obstfeld, M., Rogoff, K. (1996), Foundations of InternationalMacroeconomics. Cambridge: MIT Press.

I White, L. (1999), The Theory of Monetary Institutions. Malden andOxford: Blackwell Publishers.

4

Time schedule (summer term 2018):

Week Tuesday Thursday

15 ch.1 (Freytag) –16 ch.2 (Pasche) –17 ch.2 (Pasche) –

18 –∗) –

19 ch.3 (Pasche) –∗)

20 ch.3 (Pasche) exercise (Pasche)21 ch.3 (Pasche) exercise (Pasche)22 ch.4 (Freytag) exercise (Pasche)23 ch.4 (Freytag) exercise (Pasche)24 ch.4 (Freytag)25 ch.4 (Freytag)26 ch.5 (Pasche)27 ch.5 (Pasche)28 ch.5 (Freytag) exercise (Pasche)

∗) public holiday

5

Type of course:

I Elective course in specialization areas “World Economy” and“Public Economics”

I 2 hours per week lecture, exercises up to 2 hours per week(see schedule); 6 ECTS

Examination:

I 60 min. endterm exam (100%)

6

1. Introduction – Goals of the lecture

Understanding exchange rates

I Exchange rates as price, adjustment parameter and policyvariable

I RER, effective ER, future ER

I What can policy obtain with a depreciation?

I What explains exchange rate fluctuations?

I Can central banks be effective on forex markets?

I How do fixed ER regimes work?

I History of ER regimes

7

1. Introduction – Goals of the lecture

US-Dollar per Euro since 2000 (Source: ECB)

8

1. Introduction – Goals of the lecture

What happened to the Rand? (Source: Bloomberg)

9

1. Introduction – Goals of the lecture

Source: ECB Monthly Bulletin 02/2018

10

1. Introduction – Goals of the lecture

Understanding the balance of payments

I The accounting mechanism

I Is a trade surplus a good thing?

I What about a bilateral deficit?

I Is China doing well with its enormous trade surplus?

I What is a sustainable deficit in the current account?

I Debt cycle

I What is a global imbalance?

11

1. Introduction – Goals of the lecture

Source: Freytag, A. (2008), That Chinese “juggernaut” –should Europe really

worry about its trade deficit with China?, ECIPE Policy Brief 2/2008, Brussels, p.5.

12

1. Introduction – Goals of the lecture

Source: IMF

13

1. Introduction – Goals of the lecture

Understanding the macroeconomics of open economies

I Interaction of forex markets with capital and goods markets

I Interaction of forex rates, interest rates and inflation

I Analysis of fiscal and monetary policy (depending on theexchange rate regime)

I Can interest rate policy of central banks be an effectivemeasure in an open economy?

14

1. Introduction – Goals of the lecture

Understanding the political economy of monetary policy

I Costs of inflation

I Basic monetary rules

I Rules vs. discretion: time consistency and economic policy

I Central bank independence

I Interdependence of monetary and fiscal policy: nohyperinflation without public debt crisis!

15

1. Introduction – Goals of the lecture

Source: ECB Economic Bulletin 02/2018

16

1. Introduction – Goals of the lecture

Source: ECB Economic Bulletin 02/2018

17

1. Introduction – Goals of the lecture

Reserves Composition

Source: IMF; http://data.imf.org/?sk=E6A5F467-C14B-4AA8-9F6D-5A09EC4E62A4

18

1. Introduction – Goals of the lecture

Understanding currency crisis

I Causes for currency crises

I Currency crisis by generation

I Role of speculation

I Early warning systems

19

1. Introduction – Goals of the lecture

Euroland

I Is Euroland an optimum currency area?

I What are the advantages of a common currency?

I Necessary conditions for stability

I Is the Euro crisis a currency crisis?

I Incentives in the SGP

20

1. Introduction – Goals of the lecture

Source: ECB Economic Bulletin 02/2017

21

1. Introduction – Goals of the lecture

Source: ECB Economic Bulletin 02/2017

22

1. Introduction – Goals of the lecture

Source: ECB Monthly Bulletin 02/2017

23

1. Introduction – Goals of the lecture

Target2 balances in the Euro area January 2018

Source: Statistia

24

2. Exchange Rates and Current Account

Literature:

* Krugman, P.R., Obstfeld, M., Melitz, M. (2014), InternationalEconomics: Theory and Policy, 10th ed., Prentice Hall.

I Obstfeld, M., Rogoff, K. (1996), Foundations of InternationalMacroeconomics. Cambridge: MIT Press.

I Krueger, A.O. (1983), Exchange-rate determination.Cambridge University Press.

I Gartner, M. (1993), Macroeconomics Under FlexibleExchange Rates. LSE Handbooks in Economics.

25

2. Exchange Rates and Current Account2.1 Preliminaries

I Exchange rate: Nominal price of a currency, expressed inunits of another currency

I Price notation:

ep =domestic currency

foreign currencye.g. ep = 0.8

[e

$

]I Quantity notation:

eq =foreign currency

domestic currencye.g. eq = 1.25

[$

e

]I Depreciation/devaluation of the domestic currency:

ep increases, eq decreases

I Appreciation/upvaluation of the domestic currency:ep decreases, eq increases

I Notation: If we use e without an index, then price notation

26

2.1 Preliminaries2.1 Preliminaries

I The exchange rate in price or quantity notation is a bilateralexchange rate (ER).

I In order to display the value of a currency compared to thecurrencies of n relevant trade partners, one can construct anindex called effective exchange rate:

eeff =n∑

i=1

giei with 0 < gi < 1,n∑

i=1

gi = 1

or

eeff =n∏

i=1

egii with 0 < gi < 1,

n∑i=1

gi = 1

with ei as the ER to the currency of country i .

I Weights gi adjusted according to what?

27

2. Exchange Rates and Current Account2.1 Preliminaries

I ER as defined above is a nominal variable (money price).

I Real exchange rate = exchange rate of goods, not currencies

er =p

p∗=

peep · p∗$

=

[e

domestic good

e$ ·

$foreign good

]=

[foreign good

domestic good

]I Real exchange rate tells how many foreign (imported) goods a

country receives for one unit of a domestic (exported) good.

I In the literature, sometimes the terms of trade (t.o.t.) aredefined as a synonym for the real exchange rate, sometimesthey are defined as the reciprocal value of the real exchangerate. This is pure convention! We use it as a synonym.

28

2. Exchange Rates and Current Account2.1 Preliminaries

I In case of tradable and non-tradable goods the real ER isgiven by

er =pT

p∗T(1)

where pT , p∗T are the price indices for domestic and foreign

traded or tradable goods.

The overall price level is then composed as

p = αpT + (1− α)pNT

with pNT as the price level of non-tradable goods.

29

2.1 Preliminaries2.1 Preliminaries

Is a depreciation of domestic currency “good”?

I One the one hand (elasticity approach):

ep ↑ ⇒ [Ex(ep)− Im(ep)] ↑ ⇒ Y ↑

if Marshall-Lerner condition holds true (discussed later).

I But on the other hand:

ep ↑ ⇒ er (t.o.t.) ↓

For a unit of domestic goods the country receives less foreigngoods = decrease of welfare.

I The first argument requires non-utilized production capacities,the second argument is based on a total competitiveequilibrium.

30

2.1 Preliminaries2.1 Preliminaries

Effect of depreciation:

export good

import good

t.o.t.=pEx/e0 · pIm

depreciation e1 > e0

export good relatively cheaper[ImEx

]↓

t.o.t.=pEx/e1 · pIm

welfare declines

31

2.1 Preliminaries2.1 Preliminaries

Forex Markets:

I Agents: Banks and other Financial Intermediaries, Firms,Central Bank, private traders.

I Each agent can act on the supply as well as on the demandside.

I Traded currencies are deposits, not cash.

I The majority of transactions are OTC, not via registered andregulated foreign exchange markets.

I The majority of transactions is processed electronically.

32

2.1 Preliminaries2.1 Preliminaries

I Spot Market: Trade contracts in t are executed immediatelyto the current spot rate et .

I Forward Markets: Contract in t to exchange (buy/sell)currencies in t + T to the forward rate et,T , where T are atleast 3 days, or 1, 2, 3, 6, 12 or more months.

This is typically done in order to reduce the risk of futureexchange rate changes (hedging).

33

2.1 Preliminaries2.1 Preliminaries

I Swap Market: Combination of spot and forward contract.

Swap rate: St,T =et,T−et

etwhere S > 0 is called “report” and

S < 0 is called “deport”.

Reasons: evtl. diverging expectations about future spot rates.

I Option Market: An option is the right to buy/sell a specificamount of a specific currency at a specific time point to aspecific exchange rate. This contract need not to be executed.

34

2.1 Preliminaries2.1 Preliminaries

Global foreign exchange market turnover by instrument

Average daily turnover in April, in billions of US dollars

Source: Bank of International Settlement, Triennial Central Bank Survey 2016

Instrument 1998 2001 2004 2007 2010 2013 2016Spot transactions 568 386 631 1.005 1.488 2.046 1.652Outright forwards 128 130 209 362 475 680 700Forex swaps 734 656 954 1.714 1.759 2.228 2.378Currency swaps 10 7 21 31 43 54 82Options/other 87 60 119 212 207 337 254Total 1.527 1.239 1.934 3.324 3.971 5.345 5.067

35

2.1 Preliminaries2.1 Preliminaries

Currency distribution of global foreign exchange market turnoverPercentage shares of daily average turnover in April.Each transaction involves two currencies, so that percentages will sum up to 200%.

Source: Bank of International Settlement, Triennial Central Bank Survey 2016

Currency 1998 2001 2004 2007 2010 2013 2016US dollar 86.8 89.9 88.0 85.6 84.9 87.0 87.6Euro ... 37.9 37.4 37.0 39.1 33.4 31.4Japanese yen 21.7 23.5 20.8 17.2 19.0 23.0 21.6Pound sterling 11.0 13.0 16.5 14.9 12.9 11.8 12.8Australian dollar 3.0 4.3 6.0 6.6 7.6 8.6 6.9Swiss franc 7.1 6.0 6.0 6.8 6.3 5.2 4.8Canadian dollar 3.5 4.5 4.2 4.3 5.3 4.6 5.1South African rand 0.4 0.9 0.7 0.9 0.7 1.1 1.0Chinese renminbi 0.0 0.0 0.1 0.5 0.9 2.2 4.0...

......

......

......

...Total 200 200 200 200 200 200 200

36

2.1 Preliminaries2.1 Preliminaries

Motives of agents on Forex markets:

I Purchasing and selling goods induces demand and supply ofcurrencies

I Capital transfers:I Providing and repaying credits in foreign currenciesI FDI: long-run investment in foreign assetsI Portfolio investment: short-run investments in foreign assets

I Arbitrage

I Speculation

I Hedging

I Central Bank interventions

37

2.1 Preliminaries2.1 Preliminaries

Arbitrage:

I Using existing differences in exchange rates at a time point.

I Simple arbitrage (example): Buying Dollar at ep in Frankfurtand selling it at the same time at e ′p > ep in New York. Bydoing so, the excess Dollar demand in Frankfurt and theexcess Dollar supply in New York will equalize the rates.

I Triangle arbitrage (example): Buying Dollar for Euro, buyingYen for Dollar, selling Yen for Euro if this is advantagous.

I Since transaction costs are low, Forex markets can beconsidered to be nearly “arbitrage free” (law of one price)

38

2.1 Preliminaries2.1 Preliminaries

Speculation:

I Using expected differences in exchange rates in a timeinterval.

I Spot market speculation:I without interest rate effects: E [et+1] > et

I with interest rate effects: (E [et+1]− et)/et > i − i∗

I Forward market speculation: Buying foreign currency to agiven forward rate if you expect that it is lower then thefuture spot rate: E [et+T ] > et,T .

39

2.1 Preliminaries2.1 Preliminaries

Effects of speculation:

I If underlying expectations contain valuable information aboutthe “fundamentals” of a currency, then a speculative agentwill buy a currency which is expected to be “undervalued”.This will help to adjust the price system to importantinformation which will enhance allocation efficiency. It mayhelp to smoothen ER fluctuations.

I If underlying expectations are not fundamentally justifiable,then speculation may induce self-fulfilling prophecies, leadingto bubbles and increased volatility. Note, that suchexpectations are not neccessarily “irrational” since they maybe fully consistent along the bubble path.

40

2.1 Preliminaries2.1 Preliminaries

Hedging:

If a contract contains future payments in a foreign currency, thenthe domestic agent faces an exchange rate risk. A risk averse agentwill try to avoid this risk.

I Contract contains payments in domestic currency (but then thetrade partner faces the same risk).

I Contract is accompanyied by a reverse forward contract. Example:exporter has future claims of 1000 Dollar in 3 months. Then he sellstoday the 1000 Dollar on the 3-months-forward market to the givenforward rate.

I Hedging (narrow sense): Trading the risk by an accompanying loan.Example: exporter has future claims of 1000 Dollar in 3 months. Hedemands a loan of 1000 Dollar to a rate of i0, changes it in Euro atet and invests it for 3 months with an interest rate i1 < i0. In 3months he receives 1000 Dollar from the export contract and repaysthe loan. The cost of risk avoidance are the difference i0 − i1.

41

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates

Outline:

2.2.1 Asset Market Perspective: ER and Interest Rates

2.2.2 Monetary Perspective: ER and Money Supply

2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

2.2.4 Production, Income and ER

2.2.5 Expectations and Speculative Bubbles

42

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

I Investing financial wealth in domestic or foreign assets.Goal: return on investment

I We consider only one interest rate i , i∗

(“∗” denotes foreign country).

I Demand for foreign currency is determined byinterest rate differentials.

43

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

(Uncovered) interest rate parity:

I Invested capital is changed into foreign currency: K/et

I After the investment period the wealth is: (1 + i∗)K/et .

I Changing back into domestic currency at the expectedexchange rate: (1 + i∗)K/et · eexp

t+1.

44

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

I Due to arbitrage the returns of foreign and domestic investmentopportunities will be equalized:

(1 + i)K = (1 + i∗)K ·eexp

t+1

et

which leads to the uncovered interest rate parity (IRP):

1 + i

1 + i∗=

eexpt+1

et| − 1

1 + i

1 + i∗− 1 + i∗

1 + i∗=

eexpt+1

et− et

et

⇒ i − i∗

1 + i∗=

eexpt+1 − et

et≈ i − i∗

⇒ R∗ ≡ i∗ +eexp

t+1 − et

et≈ i

45

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

I Another notation using the approximation ln(1 + x) ≈ x :

i − i∗ ≈ ln eexpt+1 − ln et

Interest rates difference = expected change of ER.

I Example: eexpt+1 = 0.8, i∗ = 0.05

et R∗

0.75 0.12 (expected depreciation)0.8 0.05 (no change expected)

0.84 0.002 (expected appreciation)

46

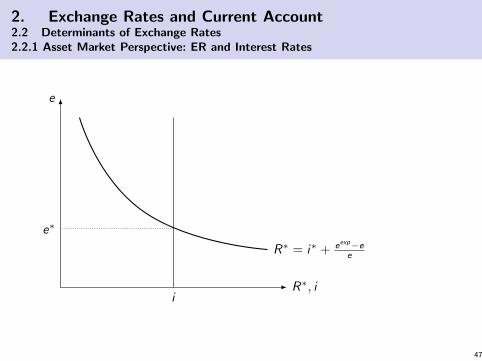

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

e

R∗, i

R∗ = i∗ + eexp−ee

i

e∗

47

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

(a) Expected depreciatione

R∗, ii

e∗1e∗2

(b) Increase of domestic interest ratee

R∗, ii1

e∗1

i2

e∗2

(c) Increase of foreign interest ratee

R∗, ii

e∗1

e∗2

48

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

Covered IRP:

I Avoiding the risk of exchange rate changes by making aforward contract.

I Risk-free no-arbitrage condition then reads

eT ,t − et

et= i − i∗ = swap rate

I If covered and uncovered IRP would hold true, then theforward rate equals the expected spot rate.

49

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

Limited IRP:

eexpt − et

et+ RP = i − i∗ with RP as risk premium

with risk aversion and/or imperfect substitutability of domestic andforeign investment opportunities.

Analogoulsy for limited covered IRP.

RP might be time-varying.

50

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

Forward Premium Puzzle:

I In case of rational expectations the expected future spot rateis identical with the forward rate (UIRP and CIRP hold true),otherwise we would have systematic arbitrage possibilities.

I An OLS test of

et+T︸︷︷︸spot

= α + β eT ,t︸︷︷︸forward

+εt+T

should give α = 0, β = 1 which is not the case.Moreover, εt+T is serially correlated.

I This implies that we cannot simply replace eexpt+T = et+T .

Therefore we cannot test directly the UIRP approach.

51

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

Testing IRP:

I Since we neither can observe expected ER nor rely on rationalexpectations, we use the covered IRP approach.

I Starting with the original no-arbitrage condition

(1 + it) = (1 + i∗t )eT ,t

et

Using logarithmic approximation ln(1 + x) ≈ x we have

i = i∗ + ln(eT ,t)− ln(et)

52

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.1 Asset Market Perspective: ER and Interest Rates

I OLS approach:

⇒ ln(eT ,t)− ln(et) = α + β(it − i∗t ) + εt

I Tested hypothesis of (covered) IRP:

α = 0, β = 1

I Moderate evidence for CIRP at least in times of not toovolatile markets (Monatsbericht Juni 2005, DeutscheBundesbank).

I Weak evidence for UIRP.

I General problem: Volatility of ER hard to explain.

53

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.2 Monetary Perspective: ER and Money Supply

Given the IRP, we can relate the money market and central bankpolicy to the exchange rate:

I Assume real money demandL(Y , i) with∂L/∂Y > 0, ∂L/∂i < 0

I Assume autonomously fixedreal money supply M/P.

I Equilibrium M/P = L(Y , i).

i

L, Mp

L(Y , i)

Mp

i∗

54

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.2 Monetary Perspective: ER and Money Supply

(a) Increased money supplye

R∗, i

Mp, L

UIRP

i1

e∗1

L(Y , i)Mp

M′

p

i2

e∗2

(b) Increased incomee

R∗, i

UIRP

Mp, L

i

e∗1

L(Y , i)Mp

L(Y ′, i)

i2

e∗2

55

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

I Exchange rates determine relative prices of domestic andforeign goods.

I Trade of goods influences supply and demand for currencies⇒ exchange rate

I Simplfying Assumptions:

I All goods are tradable.I All goods are homogenous.I No transaction and transportation costs.

⇒ Law of one price (no arbitrage condition)

56

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

Absolute purchasing power parity (PPP):

P = eP∗ ⇒ e =P

P∗

or in growth rates

wP = we + wP∗ ⇒ we = wP − wP∗

ER changes according to inflation differential.

57

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

I Objection: Not all goods are tradable.Assume the following decomposition of the price index:

P = αPT + (1− α)PN

P∗ = α∗P∗T + (1− α∗)P∗NLet β = PN/PT , β

∗ = P∗N/P∗T . Then

P = (α + (1− α)β)PT = γPT

P∗ = (α∗ + (1− α∗)β∗)P∗T = γ∗P∗T

I PPP holds true only for tradables:

e =PT

P∗T=

P

P∗γ∗

γ

or in growth rates:

we = (wP − wP∗) + (wγ∗ − wγ)

which is the relative PPP.

58

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

I If goods and price structure is stable, i.e.

wγ∗ = wγ = 0

then the result in growth rates is the same as in case ofabsolute PPP.

I The change of PT ,PN , α depends on the macroeconomicdevelopment of the open economy.

59

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

Structural change and emerging countries:

I Income is determined by labor productivity (among others). Itis reasonable that productivity differences accross countriesare more pronounced in the tradable good sector.

I Increase in the tradable good sector productivity leads tohigher wages in the economy, leading to higher costs (andprices PN) in the non-tradable good sector. Prices in thetradable good sector are determined on the world market andwill not be changed by productivity growth.

I Catching-up countries will therefore typically have a higherinflation rate (Balassa-Samuelson effect).

60

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

Balassa-Samuelson effect:

I Assume that prices are primarly determined by wages P = l/θ withl = wage rate and θ = labor productivity.

I Then we have wP = wl − wθ.

I There are two sectors N and T , but only one wage rate. Therefore

wPT− wPN

= wθN− wθT

I Inflation rate is composed as

wP = αwPN+ (1− α)wPT

= wPT+ α(wθN

− wθT)

and for two countries

wP∗ − wP = wP∗T− wPT︸ ︷︷ ︸

0 (PPP)

+α [(wθ∗T − wθ∗N )− (wθT− wθN

)]︸ ︷︷ ︸>0 (typically)

61

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

The real exchange rate under PPP:

er =PT

eP∗T

I If PPP holds true, PT = eP∗T , then er = 1.

I Example: BigMac index (www.economist.com).

62

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

Source: www.economist.com

63

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

With PPP we should expect that nominal ER adjust according toinflation differences so that real ER do not change!

Empirical evidence:

I Nominal and real ER are highly correlated.

I No evidence for absolute PPP. Evidence for PPP only in caseof very high inflation countries. Weak evidence for relativePPP.

I Weak/moderate evidence also when applying PPP to tradablegoods only.

I ER are much more volatile than could be expected by PPP orIRP.

64

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.3 Real Perspective: ER, Trade, and Purchasing Power Parity

Reasons for deviation from PPP:

I Short run price rigidities: Nominal shocks are translated intoreal shocks

I Transportation costs

I Trade barriers

I Imperfect markets: differentiated products, market power

I Not all goods are tradable, Balassa-Samuelson effect

I Different preferences ⇒ different consumption bundles ⇒different measurement of price index

65

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.4 Production, income and ER

A simple macroeconomic model of an open economy(Mundell-Fleming):

Y = C (Y ) + I (i) + Ex(Y ∗, e)− Im(Y , e) + A

M

P= L(Y , i)

Current account:

I Trade account X (Y ,Y ∗, e) = Ex(Y ∗, e)− Im(Y , e).

I Capital account B(i , i∗) = K Im(i , i∗)− KEx (i , i∗).

I Without interventions of the central bank (zero currencyaccount), we have:

X (Y ,Y ∗, e) = −B(i , i∗)

which is called ZZ curve.66

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.4 Production, income and ER

ZZ curve in (Y , i)-space:

X (Y ,Y ∗, e) = −B(i , i∗)

I Combination of (Y , i) above this curve: domestic interest rate“too high” for equilibrium ⇒ capital inflow, excess demandfor domestic currency ⇒ appreciation.

I Combination of (Y , i) below this curve: domestic interest rate“too low” for equilibrium ⇒ capital outflow, excess demandfor foreign currency ⇒ depreciation.

Slope of curve depends on capital market imperfection (perfectcapital market: horizontal curve).

67

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.4 Production, income and ER

Domestic country:

Y = C (Y ) + I (i) + X (Y ,Y ∗, e) + A

M

P= L(Y , i)

X (Y ,Y ∗, e) = −B(i , i∗)

Foreign country:

Y ∗ = C ∗(Y ∗) + I ∗(i∗) + X ∗(Y ∗,Y , e) + A∗

M∗

P∗= L∗(Y ∗, i∗)

X ∗(Y ∗,Y , e) = −B∗(i∗, i)Because X = −X ∗ and B = −B∗ the last equation is redundant.

System with 5 equations and 5 endogeneous variables(Y ,Y ∗, i , i∗, e).What happens if domestic demand (income) increases? 68

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.4 Production, income and ER

i

Y

IS

LM

ZZA

IS ′

B

A ↑

IS ′′

ZZ ′

e ↓

e ↓

C

69

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.4 Production, income and ER

Increased domestic autonomous demand:

I Domestic income and imports increase. Trade balancedecreases, demand for foreign currency increases.

I Domestic interest level increases, inducing more capitalinflows. This leads to increased demand for domestic currency.

I Increasing interest rates dampen positive income effect.

I We obtain a net excess demand for domestic currency →appreciation → dampening effect.

70

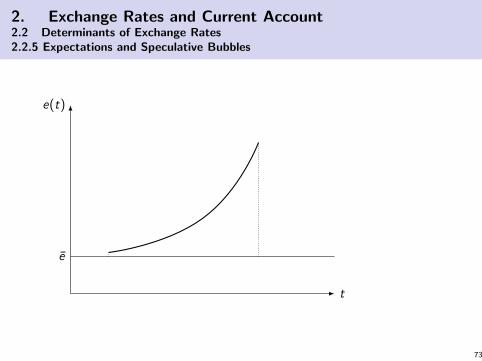

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.5 Expectations and Speculative Bubbles

Example of a simple bubble model:

I Uncovered IRP always holds true:

i − i∗ =E [et+1]− et

et= E [∆ ln e]

I Assume that there is a “fundamental” equilibrium level eI If realized ER differs from its equilibrium level, there is a

probability p that ER adapts to its equilibrium level (e − et).The rate of ER change is therefore (ln e − ln e).

I With probability (1− p) agents expect that the deviation fromthe equilibrium level increases with a constant rate (“bubblepath”): ∆ ln e. And with p the bubble will burst.

I Rational agents will account for both possible events andexpect

E [∆ ln e] = p(ln e − ln e) + (1− p)(∆ ln e)

71

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.5 Expectations and Speculative Bubbles

I Employing IRP gives

i − i∗ = p(ln e − ln e) + (1− p)(∆ ln e)

I Solving to ∆ ln e gives

∆ ln e =1

1− p(i − i∗) +

p

1− p(ln e − ln e)

I This means that the increase of the bubble is larger, the largerthe deviation from the equilibrium level is already, i.e. thebubble path is exponential until the bubble bursts.

I Note, that expectations are always rational, even on thebubble path!

72

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.5 Expectations and Speculative Bubbles

e(t)

t

e

73

2. Exchange Rates and Current Account2.2 Determinants of Exchange Rates2.2.5 Expectations and Speculative Bubbles

Problems of this simple model:

I Initial creation and burst of the bubble are not explained.

I Exogenous probabilities of burst.

I ER bubbles should influence interest rates and prices (here:given as parameters, not endogenous variables)

I Difficult to prove empirical evidence.

Similar approach: herding behavior

74

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Structure of the balance of payments:

1. Current account

1.1 Trade account1.2 Services account1.3 Direct income transfers1.4 Other transfers

2. Capital account

2.1 FDI account2.2 Account of financial assets2.3 Other capital transfers

3. Currency account

4. Statistically not assignable transactions

75

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Since each accounting record has two entries, all net total of theaccounts have to add up to zero (closed system).

I An exporter sells goods and receives foreign currency:

current accountEx = 100

NX = 100

capital accountKEx = 100

B = −100

I A domestic bank sells foreign currency to the central bank:

capital accountKEx = −100

B = 100

currency account∆C = 100

∆R = 100

76

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I An importer buys foreign goods and the foreign firm has openclaims:

current accountIm = 100

NX = −100

capital accountK Im = 100

B = 100

I An investor buys a foreign firm and pays with foreign currency:

capital accountK Im

long = 100

K Imshort = −100

77

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I Net balances:I Current account NX = Ex − Im (net export)I Capital account B = K Im − KEx (net capital import)I Currency account ∆R = NX + B (net change of foreign

reserve stock)

I In case of flexible exchange rates, the central bank has not topurchase/sell foreign currencies: ∆R = 0⇒ NX = −B

I Capital and current account are then like a “mirror”.

78

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I From macroeconomic accounting we have

Y = C + I + Ex − Im

Y − C − I = S − I = Ex − Im = NX

⇒ S − I = ∆R − B = NX

and for ∆R = 0 we have

S − I = KEx − K Im

I Positive net exports mean that domestic savings exceeddomestic investments. There are more domestic saversinvesting abroad than vice versa = net capital outflow.

I How does the current account respond to changes of theexchange rate?

79

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

The Marshall-Lerner condition:

I Depreciation enables export firms to charge a lower price inforeign currency. The sold quantity as well as the price indomestic currency and henceforth Ex will increase.

I The imports will become more expensive in domestic currencyso that the imported quantity will decrease. Therefore wehave countervailing effects so that the resulting effect on thevalue Im is ambigous. Hence, the effect on NX is ambigous.

I Therefore, the intuitive effect that NX increases in case ofdepreciation (“normal” response) holds true only undercertain conditions.

I Note, that an increase of NX has no normative imlpications.

80

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

NX (e) = Ex(e)− Im∗(e)e

dNX

de=

dEx

de− dIm∗

dee − Im∗

We say a “normal” reaction is dNX/de > 0 and presume abalanced trade Ex = Im∗e ⇒ Im∗ = Ex/e:

0 <dEx

de

e

ExIm∗ − dIm∗

de

e

Im∗Im∗ − Im∗

0 <dEx

de

e

Ex− dIm∗

de

e

Im∗− 1

1 < ηEx − ηIm∗

81

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I In the short-run, demand and supply side in export andimport markets cannot respond immediately to ER changes(e.g. existing contracts).

⇒ If e increases, then it takes some time until Im∗(e) decreases.

I But the value of imports in domestic currency e · ¯Im∗

willincreases immediately.

I The resulting effect is that in the short-run we may observe asharp fall of NX before the “normal reaction” takes place.The time-path is characterized by the “J-curve effect”.

82

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

NX

t

depreciation shock

83

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I We have only analyzed how exogenous changes of ER affectsceteris paribus the trade balance.

I We have seen, however, that trade balance corresponds withcapital balance.

I Trade depends on prices, capital flows depend on interestrates, both are determining the nominal exchange rate.

I In equilibrium, individual plans which determine B and NXhave to be consistent – which implies a certain real exchangerate.

I Such an equilibrium does not neccessarily imply balancedtrade and capital accounts.

84

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Capital flows as an intertemporal decision problem:

I For capital accumulation we need savings and production ofinvestment goods.

I This requires an intertemporal decision: Partial waive forconsumption today enables larger output and consumptiontomorrow.

I Transfer of capital is not physical capital but financial capital. It canbe used in the foreign country either for additional consumption oradditional investment.

I Home country has then claims on the future GDP of the foreigncountry: The interest rate payments to the home country has to beraised from the foreign’s future GDP.

I For the domestic intertemporal consumption/saving decision, the(real) interest rates r , r∗ play an important role. With a given worldcapital market interest rate r = r∗ and given intertemporalpreferences, the net exports and the trade balance are implicetlydetermined (see below).

85

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Intertemporal calculus:

I 2 periods, only one good that can either be consumed orinvested

I perfect capital market with one interest rate for lending andborrowing

I Intertemporal budget constraint with lending/borrowing:

Ct+1 = Yt+1 + (1 + r)(Yt − Ct)

⇒ Ct +1

1 + rCt+1 = Yt +

1

1 + rYt+1

86

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I Consumers maximize the net present utility

U = U(Ct) +1

1 + ρU(Ct+1)

with ρ as the intertemporal discount rate (reflectingpreference for the presence or “impatience”). They have tomaximize utility conditional to the intertemporal budgetconstraint (DD in the following figure).

87

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Yt+1,Ct+1

Yt ,Ct

45

PYt+1

Yt

D

D

determined by r

CCt+1

Ct

A

(a)

(a) Borrowing in t (Import)

(b)

(b) Repaying in t + 1 (Export)

88

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I In t the households consume more than it is produced= positive net imports Imt

= negative trade balance AC (= positive capital balance).The consumption is partially financed by foreign savings (debt)

I In t + 1 the debt is repaid including interest rate: AP,implying a positive trade balance (= negative capital balance).

I Both imbalances in t and t + 1 reflect optimal behavior, notdisequilibrium.

89

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I Now consider that Y can not only be consumed but also beinvested.

I Investment leads to capital accumulation. Thus theproduction frontier shifts and we have

Yt+1 = Yt + F (It)

with F (·) as the production effect of investments andF ′ > 0,F ′′ < 0

I Saving and investment therefore lead to an intertemporalproduction frontier (RP in the following graphic).

90

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

I The calculus of an investor is whether to invest into thephysical project It or to invest the funds at the world capitalmarket at the rate r . The returns from investment F (It) aretherefore discounted with 1/(1 + r).

I Profit maximization gives

maxItπ =

1

1 + rF (It)− It

FOC ⇒ dF

dIt= 1 + r

which is the tangential point Q at the intertemporalproduction frontier RP.

I Due to the increased production in t + 1 the intertemporalbudget constraint shifts to D ′D ′.

I The same calculus for intertemporal consumption is applied tothe new constraint. The achievable utility is higher thanbefore.

91

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Yt+1,Ct+1

Yt ,Ct

45

P

Yt

D

D

R

D’

D’

QYt+1

It

shift of budget constraint

92

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Yt+1,Ct+1

Yt ,Ct

45

Yt

D

D

R

D’

D’

QYt+1

It

CCt+1

Ct

Imt

Ext+1

A B

93

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

The complete result of intertemporal consumtpion and investmentdecisions:

I In t we have a negative trade balance (positive capitalbalance) AC , and investment AB.

I In t + 1 the foreign debt is repaid inclduing interest paymentsAQ which implies a positive trade balance.

I Borrowing and repaying capital is indirectly borrowing andregiving goods.

94

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Consider two countries with different investment opportunities anddifferent time preferences:

I An optimal positive trade balance in t in country 1 implies anoptimal negative trade balance in t in country 2, and viceversa in t + 1.

I Given the time preferences and different returns oninvestments (different intertemporal production frontiers), theoptimal plans for consumption and investment (andhenceforth exports and imports) must be consistent.

I The world market interest rate r adjusts so that intertemporalplans of both countries are coordinated.

95

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Yt+1, Ct+1

Yt , Ct

45

Yt

Country 1

−(1 + r)

Yt+1

ItCtExt

Imt+1

Yt+1, Ct+1

Yt , Ct

45

Yt

Country 2

−(1 + r)

Yt+1

It

Ct

Ext+1

Imt

Left side: low marginal productivity of It , patient consumersRight side: large marginal productivity of It , less patient consumers

96

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Empirical picture – UNCTAD World Investment Report 2014:

I FDI outflow 2013:I Developed countries: 899 billion USDI Developing and emerging countries: 553 billion USD

I FDI inflow 2013:I Developed countries: 566 billion USDI Developing and emerging countries: 886 billion USD

I In former decades these net flows from developed todeveloping countries had a much lower relative value....

I ... and national saving and investment rates are highlycorrelated (Feldstein-Horioka puzzle).

Possible reasons:

Other influences on savings, investments, cross-border flow ofcapital: uncertainty about economic and political development;quality of institutions (rule of law, corruption; enforcement ofproperty rights). 97

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

The “debt cycle”:

I In a n-period model or in a continous time model, theintertemporal problem will first create increasing capitalinflows (debt accumulation), and in later periods net capitaloutflows (repaying debt), creating a “cycle” in trade andcapital net positions.

I There is some empirical evidence that such debt cyclesoccured (e.g. USA, South Africa, see the slide in the“Introduction”)

98

2. Exchange Rates and Current Account2.3 Exchange Rates and Current Account Response

Relation to ER:

I The intertemporal calculus implies that Ex − Im and S − I isplanned simultanously.

I The export/import plans of the country must be consistentwith the plans of the other country (or “rest of the world”).There exists an er = P/eP∗ where plans are consistent.

I The same holds true for planned S − I . The saving/investmentplans of both countries are coordinated by interest rates.

I Therefore the equilibrium exchange rate is implicitlydetermined by the intertemporal plans, and depends onprice differentials, interest rate differentials, and time prefencerates.

99

3. Monetary Macroeconomic Models

Outline:

3.1 Overshooting Model (Dornbusch)

3.2 (New) Keynesian Model

Literature:

I Krugman, P.R., Obstfeld, M., Melitz, M. (2014), InternationalEconomics: Theory and Policy, 10th edition, Prentice Hall.

I Rogoff, K. (2002), Dornbusch’s Overshooting Model afterTwenty-Five Years. IMF Staff Papers, Vol. 49, IMF Annual ResearchConference (2002), pp. 1-

I Dornbusch, R. (1976), Expectations and Exchange Rate Dynamics.Journal of Political Economy 84 (6), 1161–1176.

100

3. Monetary Macroeconomic Models3.1 Overshooting Model

Model by R. Dornbusch (1976):

I Slow goods market, fast capital market

I Short run: uncovered interest rate partity, fixed prices

I Long run: flexible prices, purchasing power parityI Analysing the impact of monetary shocks:

I If prices are flexible, nominal shocks in money supply inducenominal price increase, but real variables, including realexchange rate, are unaffected.

I With short-run rigid prices, the nominal shock has real effects;interest rate decreases and currency depreciates.

I When prices adapt to the new equilibrium level, investorsexpect appreciation.

I In the new equilibrium real interest rate and real exchange rateare on their initial levels. Nominal exchange rate has decreasedcompared to overshooting level.

101

3. Monetary Macroeconomic Models3.1 Overshooting Model

Notation:

y = lnY log incomem = lnM log nominal money supplyp = lnP log price level

e log exchange rateη > 0 income elasticity of money demandλ > 0 semi interest rate elasticity of money demand

102

3. Monetary Macroeconomic Models3.1 Overshooting Model

I From equilibrium condition for the money market we have

m − p = ηy − λi (2)

I Interest rate parity on the capital market is given by:

E [∆e] = i − i∗ ⇒ i = E [∆e] + i∗ (3)

I Expectations are given by

E [∆e] = θ(e − e) (4)

where e is determined by the PPP.I Inserting (4) and (3) into (2) gives the short run equilibrium

on money and capital market:

m = p + ηy − λ(θ(e − e) + i∗) (5)

⇒ p = λ(i∗ + θ(e − e))− ηy + m (SRE)

103

3. Monetary Macroeconomic Models3.1 Overshooting Model

I The relative PPP holds in the long run:

e = p − p∗ + Z (LRE)

I Before we analyze the interplay between (SRE) and (LRE) welook what happens with the short-run equation (5) in thelong-run: we replace p = p and consider e = e so that weobtain

m = p + ηy − λi∗ (6)

I Equalizing (5) and (6) and rearranging gives

e = e +1

λθ(p − p)

104

3. Monetary Macroeconomic Models3.1 Overshooting Model

Result:

I If the long-run price level p and henceforth the long-runequilibrium exchange rate e increase due to the nominalshock, then the short-run exchange rate e increases sharply ifprices are rigid.

I If then the price level p increases in time, the difference inbrackets become smaller so that the new exchange rateapproaches its new equilibrium level “from above”.

Graphic:

Recall that (SRE) shifts in case of a monetary shock:

SRE1 : p = λ(i∗ + θ(e1 − e))− ηy + m1

SRE2 : p = λ(i∗ + θ(e2 − e))− ηy + m2

105

3. Monetary Macroeconomic Models3.1 Overshooting Model

p

e

LRE

45 SRE0

p1

e1

SRE1

e

fast

p2

e2

slow

106

3. Monetary Macroeconomic Models3.1 Overshooting Model

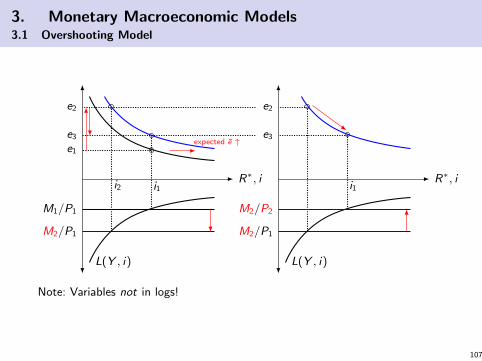

R∗, i

L(Y , i)

M1/P1

i1

e1

M2/P1

expected e ↑

e2

i2

e3

R∗, i

L(Y , i)

M2/P1

e2

M2/P2

i1

e3

Note: Variables not in logs!

107

3. Monetary Macroeconomic Models3.1 Overshooting Model

money volume

time

interest rate

time

price level

time

exchange rate

time

108

3. Monetary Macroeconomic Models3.1 Overshooting Model

A dynamic model (discrete time version):

Assumptions:

I Long run equilibrium output y

I Foreign price level p∗ = 0 normalized to zero

I No interest rate dependency of demand (IS curve)

I IS curve: yt − y = b(et + p∗ − pt)

I LM curve: mt − pt = yt − βitI Interest rate partity : E [et+1 − et ] = it − i∗

I Rational expectations: E [et+1 − et ] = et+1 − et

I Phillips curve (price rigidity): pt+1 − pt = δ(yt − y)

109

3. Monetary Macroeconomic Models3.1 Overshooting Model

I From IS curve and Phillips curve we obtain

∆p = pt+1 − pt = δb(et − pt) (7)

I From LM curve and IRP we obtain

∆e = et+1 − et =1

β[yt −mt ]− i∗ +

1

βpt (8)

I The steady state is characterized by ∆p = ∆e = 0 andhenceforth it = i∗, yt = y , et = pt .

I In the steady state, (8) gives

et = pt = mt − y + βi∗

and therefore long-run neutrality of money:dp/dm = de/dm = 1, i.e. nominal variables are determined bymoney.

110

3. Monetary Macroeconomic Models3.1 Overshooting Model

e

p

∆e = 0

∆p = 0

111

3. Monetary Macroeconomic Models3.1 Overshooting Model

Disequilibrium:

I We have ∆e < 0 for pt < pss and vice versa.

I We have ∆p > 0 for et > pt and vice versa.

Graphical analysis:

I The ∆e = 0- and ∆p = 0-lines are isoclines. Theirintersection point characterizes the steady state.

I The arrows denote the dynamic motions as mentioned above.

I There exists only one stable path to the equilibrium(“saddle path”).

I Along this saddle path we have rational expectations.Different expectation hypothesis may eventually not lead to astable adaption path towards equilibrium.

112

3. Monetary Macroeconomic Models3.1 Overshooting Model

e

p

∆p = 0

p1

∆e = 0

e1

p1

∆e = 0

p2

∆e = 0

saddle path

e2

113

3. Monetary Macroeconomic Models3.1 Overshooting Model

Overshooting:

I With ∆m > 0 we have in the long run ∆p = ∆m. Theisocline ∆e = 0 shifts to the right.

I Starting from the initial equilibrium, the exchange rate“shoots up” to the saddle path.

I Then the price level and exchange rate move along the saddlepath to the new equilibrium.

Remark:

I There are different versions of the basic Dornbusch model,including e.g. continous time versions, and goods marketswith interest rate dependent investment, taxation etc..

114

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Outline:

(a) Standard Keynesian Model of an Open Economy

Mankiw, N.G. (2010), Macroeconomics. 7th ed., Worth Publishers.

Krugman, P.R., Obstfeld, M., Melitz, M. (2014), International

Economics: Theory and Policy, 10th edition, Prentice Hall.

(b) New Consensus Models: Closed Economy

Carlin, W., Soskice, D. (2015), Macroeconomics. Institutions,

Instability, and the Financial System. Oxford University Press.

(c) New Consensus Models: Open Economy

Bofinger, P., Mayer, E., Wollmershauser, T. (2006), The BMWModel: A New Framework for Teaching Monetary Economics.Journal of Economic Education 37(1), 98-117.

Bofinger, P., Mayer, E., Wollmershauser, T. (2009), Teaching New

Keynesian Open Economy Macroeconomics at the Intermediate

Level. Journal of Economic Education 40(1), 80-101.

115

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

(a) Standard Keynesian Model of an Open Economy(Keynes-Mundell-Fleming model)

Y = C (Y ) + G + I (i) + NX (Y ,Y f , τ) (IS)

M

P= L(Y , i) (LM)

NX (Y ,Y f , τ) = −B(i , i f ) (ZZ)

where τ = eP f /P are the terms of trade.

I Assumption: Marshall-Lerner condition holds true.

I In case of fixed prices, τ can be replaced by e.

116

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

ZZ curve:NX (Y ,Y f , e) = −B(i , i f )

I Goods exporters and capital importers demand domesticcurrency.

I Goods importers and capital exporters demand foreigncurrency.

I With an equilibrium exchange rate e planned NX and planned−B are identical.

I Various combinations of (Y , i) with a given e lead to foreignexchange market equilibrium.

117

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

i

Y

IS

LM

ZZ

Above ZZ: appreciation presuure (e ↓)Below ZZ: depreciation pressure (e ↑)

118

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Various cases in this model framework.....

Perfect versus imperfect capital markets:

I Imperfect: domestic and foreign currency are not perfectsubstitutes ⇒ IRP does not hold perfectly, i.e. there couldexist interest rate differences i 6= i f in equilibrium

⇒ upwards sloped ZZ curve

I Perfect: IRP holds: E [∆e] = i − i f = 0 in equilibrium. In caseof a small country: i f is a given fixed parameter.

⇒ horizontal ZZ curve

119

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Small country versus large country:

I Small country: no effect on the “rest of the world”⇒ i f and Y f are given.

I Large country: various additional feedback mechanisms!

⇒ Since Im = Ex f , an increase of domestic imports affectsforeign income Y f which again stimulates domestic exports.

⇒ This has an effect on foreign inrterest rate i f . Both has animpact on the exchange rate e.

120

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Flexible versus fixed exchange rate regime:

I Flexible ER: e is an endogenous variable (like Y and i) in thesystem of equations IS-LM-ZZ.; autonomous monetary policyis possible.

I Fixed ER: e = e is exogenously given, Central Bank (CB) hasto stabilize e by intervention ∆R 6= 0.

M + ∆R

P= L(y , i)

I Pressure on the exchange rate (intersection of IS and LM isnot on ZZ curve) induces a shift of LM.

I In case of a large country: Buying reserves = reducing foreignmoney supply in the private sector.

121

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Fixed versus flexible prices

I Fixed prices: P = P and P f = P f (price rigidity).

I Flexible prices: modelling the supply side where expansion ofY is possible only with increasing P (short-/long-run Phillipscurve)

I Additional feedback mechanisms:I Effect on real money supply M/P = shift of LM curve.I Effect on terms of trade τ = shift of IS and ZZ curve.

122

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Example I:

I small country

I fixed prices

I perfect capital markets

I flexible exchange rates

123

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Monetary Policyi

Y

IS

LM

ZZA

LM’

M ↑

B

Point B: depreciation induced

IS ′

e ↓

C

Fiscal Policyi

Y

IS

LM

ZZA

IS ′

G ↑

B

Point B: appreciation induced

IS ′′

C

e ↑

124

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Monetary policy is very effective but not due a decrease of ibut due to an induced depreciation which stimulates thegoods market.

I Fiscal policy is ineffective because the induced appreciationcrowds out the stimulus completely.

125

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Example II:

I small country

I fixed prices

I perfect capital markets

I fixed exchange rates

126

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Monetary Policyi

Y

IS

LM

ZZA

LM’

M ↑

B

Point B: depreciation pressure⇒ CB must sell reserves

LM ′′

C

M ↓

Fiscal Policyi

Y

IS

LM

ZZA

IS ′

G ↑

B

Point B: appreciation pressure⇒ CB must buy reserves

LM’

M ↑

C

127

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Monetary policy is ineffective because it induces adepreciation which has to be offset by selling reserves (Mdeclines).

I Fiscal policy is very effective because it induces anappreciation which “forces” the central bank to buy reserveswhich means that monetary policy has to be expansive, too.(Not really independent CB.)

128

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Example III:

I small country

I fixed prices

I imperfect capital markets

I flexible exchange rates

129

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Fiscal policy:

i

Y

IS

LM

ZZA

IS ′

B

A ↑

IS ′′

ZZ ′

e ↓

e ↓

C

130

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Fiscal policy works like in the standard IS-LM model except foran additional (negative) feedback from induced appreciation.

I Crowding-out effect because of higher interest rate andappreciation ⇒ low fiscal multipliers.

131

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Excourse: supply side – flexible prices

I We confine to a closed economy!

I If prices are seen as flexible, we can solve LM to i and plug it intothe IS curve in order to establish a negative relationship between Yand P (aggregated demand curve, AD)

I In addition, we have to model the supply side (AS curve) so thatprice level is determined endogenously.

132

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Wage bargaining: Nominal wage level is determinedaccording to the expected price level and the unemploymentrate u. A lower u implies higher bargaining power for theworkers:

w = Pe f (u), withdf

du< 0 (9)

I Price setting of firms: Since labor is the unique variableinput factor, wages w determine the marginal cost. Allowingfor imperfect markets, the price P is set with a certainmarkup on the marginal cost:

P = (1 + µ)w (10)

133

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Determining the “natural rate of unemployment”:

I In the long run expected and realized price levels are equal:Pe = P.

I From (9) and (10) we have

w

Pe= f (u) (11)

w

P=

1

1 + µ(12)

I In the long run expected and realized price levels are equal:Pe = P. Replacing this in (11) and equalizing both equations,we obtain the natural unemployment rateun = f −1(1/(1 + µ)).

134

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

From unemployment to production (income):

I The unemployment rate u is defined by u = (L− N)/L(with L = labor force, N =employed workers).

I Assume a fixed labor productivity Y /N = 1/η ⇒ N = ηY .Then we have

u = 1− ηY

L(13)

I Inserting wage bargaining equation (9) into the pricedetermination (10) and substituting u by (13) we have theshort run aggregated supply function

P = Pe(1 + µ)f

(1− ηY

L

)(14)

which is a positively sloped function in the (P,Y )-space.

135

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Combining the equilibriumconditions for goods and moneymarket with the aggregatedsupply we have a complete modelof determining endogenouslyprices, wages, income,employment, and interest rates.

i

Y

IS

LM

P

Y

AS (short run)parametrized by πe

AD

136

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

From short to long run

In the short run expected andrealized price may differ (here:Pe < P). Hence, output andemployment may deviate fromtheir “natural” values. Whenprice expectation adapt, theAS curve shifts to the left.This process holds true forany AD curve ⇒ long-run AScurve.

P

Y

AS with Pe = P0

ADA

P0

P1

AS with Pe = P1

AS with Pe = P∗

P∗ B

Yn

long-run AS

B

137

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Critique of Old Keynesian models:

I No microfoundation; intertemporal calculus should depend onreal interest rate instead of nominal one.

I In contrast to the original work of Keynes, uncertainty andexpectations play a minor or no role.

I The model is based on price level rather than on (expected)inflation rates (Walsh (2001)).

I The IS-LM-AD-AS construction is logically inconsistent.The AD curve represents already IS-LM equilibria, includingall multiplier effects from the supply side (Colander (1995)).

138

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I LM curve is obsolete: central banks use interest rates asinstrumental variables and operating targets rather thanmonetary aggregates. The latter should be regarded as anendogenous variable. Thus, the LM curve construction isquestionable and does not reflect central bank behavior(Romer (2000)).

I Even in case of flexible prices a Walrasian equilibrium is a veryunlikely artificial situation ⇒ existence of non-market clearingprices ⇒ rationing effects and effective demand. Agent’scalculus should therefore respond to quantity rationing effects,not only to prices (Neo Keynesianism, Benassy (2002)).

139

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

New Keynesian Macroeconomic Models:

I Replacing LM curve by interest rate based monetary policyrules (optimal policy or Taylor rule)

I Microfoundation: IS curve and Phillips curve derived from acalculus.

I Based on real interest rates and inflation (expectations).

I DSGE models versus comparative-static counterparts(“New Consensus” models)

I Is this really “Keynes”?

140

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

(b) New Consensus Model: Closed Economy

Agenda:

I The demand side

I The supply side

I The monetary policy rule

I The 3-equation model

141

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Demand side:

I Goods market equilibrium is based on an intertemporalcalculus of the household ⇒ Euler equation (see courses

“Advanced Macroeconomics”, “Monetary and Fiscal Policy”).

I Permanent income hypothesis (decisions based on expectedlifetime income instead of current income).

I Real interest rate according to Fisher equation: r = i − πe

I In some models there is no explicit investment behavior.

I Resulting IS curve:y = A− br

with y as the “output gap” (difference between current andpotential output), and r = i − πe as the real interest rate.

142

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Consumption

Investment

Demand

Permanent income

Real interest rate

Fisher equationnominal interest rate expected inflation

143

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Monetary policy: There is no LM curve! Instead, central bankdirectly determines r , and thus (via IS curve) the output.

r

y

IS

monetary policy

144

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Supply side:

Goods market:

I Firms are price setting (monopolistic competition).

I However, prices are not fully flexible: price changes mughtbe costly; firms might not be able to adjust prices in eachperiod (staggered price setting); firms might not beinstantabously informed about demand changes (stickyinformation).

⇒ This leads to sticky prices due to goods marketimperfections. Prices adjust with interia to changing demandand changing marginal cost = wages.

145

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Labor market:

I Labor market is imperfect, too. Examples: informationasymmetries leading to efficiency wages; institutional issuessuch like power of trade unions or labor protection law; costlywage bargaining process.

⇒ Might lead to sticky wages and a natural unemploymentrate un (NAIRU, see above).

⇒ The natural unemployment rate determines the natural outputlevel Yn.

146

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Consider wage bargaining (11) and price setting equations(12):

W

Pe= f (u) = F (Y )

W

P=

1

1 + µ

where the negative function f (u) is replaced by a positivefunction F (Y ).

I Now we are calculating the time derivatives:

W − πe = F ′(Y − Yn︸ ︷︷ ︸y

)

W − π = 0

Change of the (log) output level is expressed by the deviationfrom the natural output level (output gap).

147

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Assuming that F ′ = α is a constant we obtain theNew Keynesian Phillips Curve:

π = πe + α(Y − Yn︸ ︷︷ ︸y

) (15)

I This implies that in the long run, when there is no systematicerror: πe = π, we have Y = Yn or output gap y = 0.

I In the short run, any positive or negative shocks (shifts of ISor PC) will have real output effects and thereforeunemployment effects.

148

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I According to the intertemporal calculus, any shocks on supplyor demand side are propagated to future periods via theintertemporal consumption/saving and eventually labor supplydecisions, as well as to adaptations of inflation expectations.

I Deviations from the natural output level as well as deviationsfrom the targeted inflation rate (see below) decrease welfare.The process back to equilibrium can be smoothened byappropriate monetary policy (or fiscal policy) intervention.

I Question: How are inflation expectations πe determined?I adaptive expectations: πe

t+1 = πt

I Rational expectations: πet+1 = E [πt+1|Ωt ] (requires the

knowledge of the full model, including the correct anticipationof dynamic

149

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

The role of the central bank:

I In traditional Keynesian models the CB determines the moneysupply, and the nominal interest rate is an endogenousvariables which equilibrates money supply and money demand.

I As Romer (2000) pointed out:

(a) most CB around the world don’t try (and are not able to)“determine” money supply (money is created in a fractionalreserve banking system more or less endogenously).

(b) CB’s policy instruments are much more closely related to theinterest rate. Thus it is more reasonable to assume that r isdetermined by the CB.

150

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

y

π

y

PC

π

y

r

IS

r monetary policy

y

151

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Inflation and the goals of the CB:

I Inflation, especially fluctuating high inflation rates, inducehigh social cost, thus it is reasonable to stabilize inflation on alow level (could be zero or a small positive rate, see module“Money and Financial Markets”). Let πT be the targetinflation rate.

I Commitment to inflation targeting has been successful inmany countries.

152

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

(Source: Carlin/Soskice (2015), graphic 3.2)

153

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Inflation and the goals of the CB (cont.):

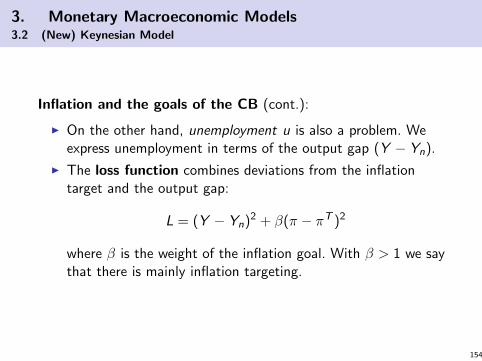

I On the other hand, unemployment u is also a problem. Weexpress unemployment in terms of the output gap (Y − Yn).

I The loss function combines deviations from the inflationtarget and the output gap:

L = (Y − Yn)2 + β(π − πT )2

where β is the weight of the inflation goal. With β > 1 we saythat there is mainly inflation targeting.

154

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

y

π

yn

πT

PCdecreasing utility

155

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Note that there might be problems of time-inconsistency(Barro-Gordon model, see next chapter).

I The consequences from this literature are that CB should becommitted to the inflation goal only.

I However, inflation is driven by the output gap, andmonetary policy operates with a lag = targets futureinflation arte. Therefore, for targeting inflation CB must havean eye also on the output gap (Svensson 1997).

I If the CB formulates an optimal policy path after a shock, weassume that CB is credible, so that for each t the inflationexpectations are following the announced path. Stochasticdeviations do not undermine credibility.

156

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Note that the PC is a constraint to the loss minimizationprogram!

I As long as PC with πE = πT is stable, the CB can determinefor any IS curve a real interest rate r such that themacroeconomic equilibrium can be achieved. It could respondto any demand shock in an optimal manner.

I If PC shifts, the long-run macroeconomic equilibrium cannotbe achieved but we can find the optimal compromise betweeninflation and output gap (which depends on parameter β).

157

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

y

π

yn

πT

PC

A

PC ′

B

B: stabilizing πTC

C: stabilizing ynD

D: best compromise

monetary policy rule

158

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Analytically:

min L = (y − yn)2 + β(π − πT )2

s.t. π = πE + α(y − yn) (PC)

The PC can be directly plugged into the goal function.

Although the policy variable is r we can use y instead because with agiven IS curve, y could be directly achieved by the choice of r :

L = (y − yn)2 + β(πE + α(y − yn)− πT )2

∂L

∂y= 2(y − yn) + 2αβ(πE + α(y − yn)− πT )

FOC: 0 = (y − yn) + αβ(πE + α(y − yn)− πT )

Solving PC to πE = π − α(y − yn) and plugging into FOC:

0 = (y − yn) + αβ(π − πT )

(y − yn) = −αβ(π − πT )

which is the monetary policy response rule(downwards sloped in (π, y)-space). 159

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Now we have the full 3-equation model:

y = A− ar (IS)

π = πE + α(y − yn) (PC)

(y − yn) = −αβ(π − πT ) (MR)

160

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

y

r

IS

re

ye

y

π

ye

PC

πT

MR

161

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Variations:

I All variables could have a time index t.

I We can assume “adaptive” expectations πEt = πt−1.

I We can assume a dynamic IS curve: yt = A− art−1.

We will use these assumptions (dynamic 3-equation model).

Let’s do some exercises to find out how the model responds toshocks....

162

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Inflation shock:

y

r

IS

re

ye

A

r0C

Dr1

y

π

ye

PC(πE = πT )

MR

πTA

PC(πE = π0)

π0B

y1

π1C

PC(πE = π1)

y2

π2 D

t

π

πT

shock

π0

t

y

ye

y1

t

r

re

r0

163

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Inflation shock:

I We start in an equilibrium (point A).

I We have an inflation shock, shifting the this PC upwards andleading to π0 > πT (point B).

I CB responds according to the monetary policy rule by increasing thereal interest rate to r0 > re .

I This dampens inflation to π1 < π0 but leads also to an output gap:y1 < yn (point C)

I Inflation expectations are reduced to πE = π1, shifting the PCdownwards.

I Inflation rate falls, and CB responds by reducing r aas well (pointD).

I Process is going on until initial equilibrium is reached.

164

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Temporary demand shock:

y

r

IS

re

ye

A

IS ′B

Cr0D

y

π

ye

PC(πE = πT )

MR

πTA

π0B

y0

PC(πE = π0)

π1C

y1

PC(πE = π1)

D

t

π

πT

shock

π0

t

y

ye

y0

y1

t

r

re

r0

165

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Temporary demand shock:

I We start in an equilibrium (point A).

I IS curve shifts to the right for one period.

I With given r output and inflation increase to y0 > yn and π0 > πT .

I Expectations will adapt and thus PC shift upwards.

I CB intervenes according to the policy rule by increasing real interestrate to r0 > re .

I With the given new PC the realized point C implies now a negativeoutput gap y1 < yn, and a slightly reduced inflation rate π1.

I Expectations aeapt again, PC shifts downwards, inflation declines,CB reduces r , process converges to inirial situation again.

I As a result, we see an “overshooting” in the output.

I Note that all these adaption processes crucially dpend on theformation of expectations!

166

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Permanent supply “shock”: (structural parameters z)

y

r

IS

reA

ye

r1C

y ′e

Dr ′e

y

π

ye

PC(πE = πT , ye)

MR

πTA

PC(πE = πT , y ′e)

MR ′

y ′e

π0 B

PC(πE = π0, y′e)

y1

π1C

D

t

π

πT

shock

π0

t

y

ye

y ′e

y1

t

r

rer ′er1

167

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

Permanent supply “shock”: (structural parameters z)

I Phillips Curve shifts downwards (same output yn at lower inflationrates, or at the same target inflation level highe equilibrium outputlevel y ′n).

I The optimal monetary response rule shifts as well because it isparametrized by the (new) equilibrium output level.

I Immeadiate drop of inflation to π0 (point B).

I Inflation expectations adapt to π0 so that Phillips curve shiftsfurther.

I Optimal policy response (reduction to r1, point C).

I Result is high output y1 at inflation rate π1.

I Now inflation expectations adapt to π1 (upwards shift of Phillipscurve) which also leads to policy responses.

I Phillips curve converges to the initial situation after the shock (withhigher equilibrium output).

168

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

(c) New Consensus Model: Small Open Economy

I GDP also consists of net exports, thus the IS curve reads

y = a(r0 − r) + cq (16)

with q = real exchange rate (in logs),and s is the spot rate (in logs).

I From definition of real exchange rate we have∆q = ∆s + πf − π.

I PPP: ∆s = π − πf .

I UIRP: ∆se = i − i f .

169

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Long run scenario: PPP holds true and no systematic error(∆se = ∆s). This implies:

i − i f = ∆se = ∆s = π − πf

end henceforthr = r f

I Consequence: if UIRP and PPP hold true, then r isexogenously determined by r f , thus there is no room formonetary policy in case of a small country, even in case offlexible exchange rates.

I CB can choose the nominal interest rate i which induceschanges of s and finally of inflation π.

I But this means that CB does not have any real effect.

170

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Short-run scenario: UIRP holds true, but not PPP

I Let q be the long-run equilibrium real exchange rate (in logs).For simplicity assume q = 0.

I For any deviation from q, the market participants excpect acorrection ∆q = α(q − q).

I Again, if UIRP holds true and there is no systematic error(∆se = ∆s) we have ∆q = r − r f .

I With q = 0 and assuming α = 1, it follows

r − r f = ∆q = α(q − q)

= −q⇒ q = r f − r

171

3. Monetary Macroeconomic Models3.2 (New) Keynesian Model

I Plugging into the IS curve:

y = a(r0 − r) + c(r f − r) = ar0 + cr f − (a + c)r

(IS curve is somehow flatter in (r , y)-space.)

I Therefore, the graphical analysis of the open economy case isessentially the same like for the closed economy case. Theimpact on the real sector is now enhanced via the interestrate effect on the exchange rate (UIRP).

172

4. Institutional Analysis of Monetary, Fiscal and Exchange Rate Policy

Outline:

4.1 Historical Exchange Rate Regimes

4.2 Rule Binding and Discretionary Policy in an Open Economy

4.3 Rules, Independence, Credibility – the Problem ofInterdependence of Monetary and Fiscal Policy

4.4 Governmental Debt, Inflation and Currency Crisis

173

4. Institutional Analysis of Monetary, Fiscal and Exchange Rate Policy

This chapter is about

I the interdependence of domestic and foreign monetary policy,

I the interdependence of fiscal policy with monetary policy –home and abroad,

I the role of rules

I the problems that occur if rules are not enforced

174

4. Institutional Analysis of Monetary, Fiscal and Exchange Rate Policy

4.1 Historical Exchange Rate Regimes

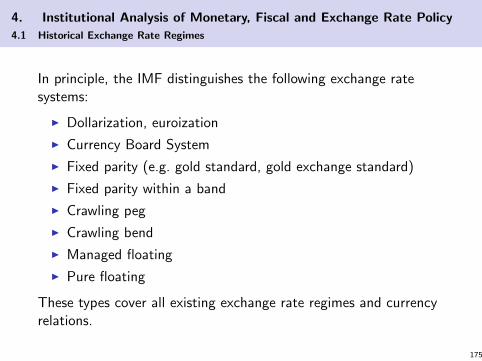

In principle, the IMF distinguishes the following exchange ratesystems:

I Dollarization, euroization

I Currency Board System

I Fixed parity (e.g. gold standard, gold exchange standard)

I Fixed parity within a band

I Crawling peg

I Crawling bend

I Managed floating

I Pure floating

These types cover all existing exchange rate regimes and currencyrelations.

175

4. Institutional Analysis of Monetary, Fiscal and Exchange Rate Policy

4.1 Historical Exchange Rate Regimes

Relevant Systems in the past: