iphotonix llc financial statements as of december 31, …

TRANSCRIPT

IPHOTONIX LLC

FINANCIAL STATEMENTS

AS OF DECEMBER 31, 2015

INDEX

Page

Auditors' Report 2

Statement of Financial Position 3

Statement of Comprehensive Income 4

Statement of Changes in Equity 5

Statement of Cash Flows 6-7

Notes to Financial Statements 8-26

-----------

- 2 -

AUDITORS' REPORT

To the Shareholders of

IPHOTONIX LLC

We have audited the accompanying statement of financial position of Iphotonix LLC ("the Company")

as of December 31, 2015 and 2014, and the related statements of profit or loss and other comprehensive

income, changes in equity and cash flows for each of the years then ended. These financial statements are the

responsibility of the Company's board of directors and management. Our responsibility is to express an opinion

on these financial statements based on our audit.

We conducted our audits in accordance with generally accepted auditing standards in Israel, including

those prescribed by the Auditor's Regulations (Auditor's Mode of Performance), 1973. Those standards require

that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are

free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts

and disclosures in the financial statements. An audit also includes assessing the accounting principles used and

significant estimates made by the board of directors and management, as well as evaluating the overall financial

statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, based on our audits, the financial statements referred to above present fairly, in all

material respects, the financial position of the Company as of December 31, 2015 and 2014, and the results of

its operations, changes in equity and cash flows for each of the two years then ended, in conformity with

International Financial Reporting Standards (IFRS).

Tel-Aviv, Israel KOST FORER GABBAY & KASIERER

March 29, 2016 A Member of Ernst & Young Global

Kost Forer Gabbay & Kasierer 3 Aminadav St. Tel-Aviv 6706703, Israel

Tel:+972-3-6232525 Fax: +972-3-5622555 ey.com

IPHOTONIX LLC

- 3 -

STATEMENTS OF FINANCIAL POSITION

December 31,

2015 2014

Note U.S. dollars in thousands

ASSETS CURRENT ASSETS:

Cash and cash equivalents 169 78 Trade receivables 4 1,711 664 Other accounts receivable 6 19 Inventories 5 791 667

2,677 1,428

NON-CURRENT ASSETS: Property, plant and equipment 6 70 184 Intangible assets 7 2,037 615 Goodwill 216 - Deposits 102 100

2,425 899

Total assets 5,102 2,327

LIABILITIES AND EQUITY

CURRENT LIABILITIES:

Short-term credit from bank 10 236 - Trade payables 8 2,159 736 Shareholders - 300 Other accounts payable 9 294 177

2,689 1,213

NON-CURRENT LIABILITIES:

Loan from bank 10 787 - Shareholders 800 - Related party 18 1,913 1,983 Other non-current liabilities 244 -

3,744 1,983 EQUITY (DEFICIT): 11

Ownership units and premium 7,571 4,978 Capital reserve 460 - Reserve for share-based payment transactions 190 190 Deficit (9,552) (6,037)

Total deficit (1,331) (869)

Total liabilities and equity 5,102 2,327

The accompanying notes are an integral part of the financial statements.

March 29, 2016

Date of approval of the

financial statements

Amir Elbaz

Chief Executive Officer

Boaz Gorfung

Director

Chris Ryan

Chief Finance Officer

IPHOTONIX LLC

- 4 -

STATEMENTS OF COMPREHENSIVE INCOME

Year ended

December 31,

2015 2014

Note U.S. dollars in thousands

Revenues from sales 8,171 7,284

Cost of sales 12 5,839 4,938

Gross profit 2,332 2,346

Research and development 13 3,464 2,357

Selling and marketing expenses 14 666 526

General and administrative expenses 15 1,191 1,229

5,321 4,112

Operating loss (2,989) (1,766)

Finance expenses 16 526 13

Loss (3,515) (1,779)

Total comprehensive loss (3,515) (1,779)

The accompanying notes are an integral part of the financial statements.

IPHOTONIX LLC

- 5 -

STATEMENTS OF CHANGES IN EQUITY

The accompanying notes are an integral part of the financial statements.

Ownership units and premium

Other Reserve

Reserve for share-based

payment transaction

Retained earnings

Total equity

U.S. dollars in thousands Balance as of January 1, 2014 2,127 - 123 (4,258) (2,008) Total comprehensive income - - - (1,779) (1,779) Conversion of Shareholders loan to

equity

2,851 -

- - 2,851 Cost of share-based payment - - 67 - 67

Balance as of December 31, 2014 4,978 - 190 (6,037) (869) Total comprehensive income - - - (3,515) (3,515)

Transaction with controlling shareholder and related party

-

460

- - 460

Issue of share capital 2,593 - - - 2,593

Balance as of December 31, 2015 7,571 460 190 (9,552) (1,331)

IPHOTONIX LLC

- 6 -

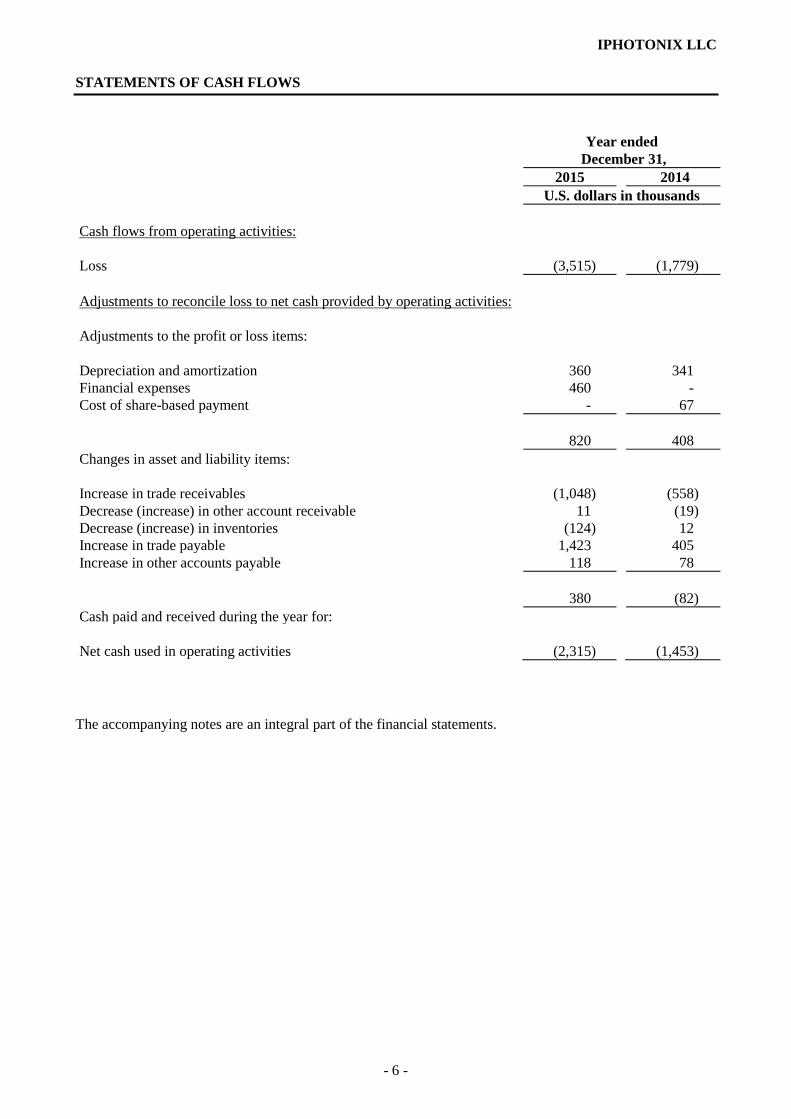

STATEMENTS OF CASH FLOWS

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Cash flows from operating activities:

Loss (3,515) (1,779)

Adjustments to reconcile loss to net cash provided by operating activities:

Adjustments to the profit or loss items:

Depreciation and amortization 360 341

Financial expenses 460 -

Cost of share-based payment - 67

820 408

Changes in asset and liability items:

Increase in trade receivables (1,048) (558)

Decrease (increase) in other account receivable 11 (19)

Decrease (increase) in inventories (124) 12

Increase in trade payable 1,423 405

Increase in other accounts payable 118 78

380 (82)

Cash paid and received during the year for:

Net cash used in operating activities (2,315) (1,453)

The accompanying notes are an integral part of the financial statements.

IPHOTONIX LLC

- 7 -

STATEMENTS OF CASH FLOWS

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Cash flows from investing activities:

Purchase of property, plant and equipment (16) (54)

Net cash used in investing activities (16) (54)

Cash flows from financing activities:

Repayment of bank loan (26) -

Related party (70) (294)

Issue of share capital 2,018 -

Shareholders 500 1,833

Net cash provided by financing activities 2,422 1,539

Increase in cash and cash equivalents 91 32

Cash and cash equivalents at the beginning of the period 78 46

Cash and cash equivalents at the end of the period 169 78

Significant non-cash transactions: Conversion of Shareholders loan to equity - 2,851

Assets acquisitions (see note 1d) 1,868 -

The accompanying notes are an integral part of the financial statements.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 8 -

NOTE 1:- GENERAL

a. Iphotonix LLC ("the Company") is an American Company, based in Richardson,

Texas.The inception date of the Company is January 25, 2012.

The Company is an original design manufacturer (ODM) for the telecommunication

industry. The Company's primary business is Fiber Access Solution.

Iphotonix develops and markets a line of carrier class Customer Premise Equipment

products including the world's broadest independent family of ONT products to original

equipment manufacturers (OEMs) and telecommunications services providers.

On January 26, 2012, under the investment agreement, the Company allocated to Molodan

84% of the Company's ownership units for $ 627 thousand, and for $ 400 thousand the

Company allocated to an additional investor ("Investor") 14% of the Company's ownership

units, the remaining ownership units of the Company is held by the Company's CEO (see

note 18c below).

In addition, the Company granted to the investor option to invest in the Company's capital

up to a total of an additional $ 1.1 million until the end of 2012 (the warrant). The warrant

was recorded in the Company's financial statements at its fair value in amount of $ 64

thousand.

In 2012 the investor exercised the warrant and invested in the Company's equity an

additional $ 1,100 thousand. As a result of this transaction, Molodan share in the

Company's ownership units, was diluted to 49.4% and the CEO's share was diluted to 1.2%

of the Company's ownership units.

Under the new agreement, the investor was granted the right to assign its investment in the

Company only in its entirety and not portions of such investment, to an American Company

traded in NASDAQ (the public corporation), which to the best of the Company's

knowledge, is controlled by the controlling shareholders in the investor. It was further

agreed that if the investor and/or the public corporation shall exercise the option in its

entirety, Molodan shall sell the public corporation at no consideration ownership units

representing 1% of the Company's ownership units whereas the CEO sellthe public

corporation shares representing 2.5% of the Company's against an identical consideration,

pro rata to consideration against which the investor shall sell its holdings to the public

corporation, such that the public corporation shall ultimately hold 51%, Molodan - 46.5%,

and the CEO shall hold 2.5% of the Company's ownership units (the additional warrant).

The fair value of the additional warrant is immaterial.

b. On January 26, 2012, an asset Purchase Agreement was signed between Asymblix (fka -

Iphotonix LLC), a related company (a company held by Molodan at rate of 50% where

Molodan's holdings in the Company are at a rate of 49.4% as of the balance sheet date),

and the Company. According to the agreement, the Company purchased from Asymblix in

consideration of $ 1,005 thousand the ONT business in the field of research, development,

design, manufacture and sale of end-solutions to optical network terminals, including

certain terminals and related software products.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 9 -

NOTE 1:- GENERAL (Cont.)

Purchase Assets includes machinery and equipment, inventory and intangible assets related

to the ONT business.

ONT operations were recorded in the Company's financial statements at their fair value

according to the value of the tangible and intangible assets of the acquired operations that

were estimated by an independent external appraiser. In accordance to the purchase price

allocation, the proceeds of the acquired operations were allocated to the tangible assets that

were acquired, inventory and fixed assets and to intangible assets, technology that was

identified and measured at $ 1,196 thousand.

c. On December 3, 2013 Molodan and SAD. The Company's shareholders signed a new

agreement. SAD's holding in the Company's shares will increase from 50% to 75% and

Molodan's holding in the Company's will decrease from 50% to 25%. The shareholders will

continue to support and finance the Company accordingly to the proportionate of their

holdings.

After the balance sheet date, on March 28, 2016 the shareholders (Molodan and the

Investor) pledged to support the Company up to a total of $600 thousands in order to enable

the Company to meet its cash needs for the next 12 months. Shareholders additionally

guarantee payments to one of the Company's supplier up to a total of $1,000.

d. On March 2, 2015, the Company acquired the assets of Netsocket Inc. ("the Seller"),

American company that engaged in development of NFV technology to Network

virtualization functions.

In consideration for the acquisition the Company:

1. Issued LLC membership interest constituting 6.6% of the Company's membership

interest.

2. Issued a Convertible Promissory Note in the principal amount of $244 thousand. The

Note will be paid on the earlier of: 1) the third anniversary from the closing date or 2)

following the closing of an equity financing (i.e.: any sale by the Company of equity

securities from which the Company realized net cash proceeds in the amount of at least

$3 million).

3. A loan from bank that was expended to the seller in the amount of $1,050 thousand was

assigned to the Company. The loan will be paid in 36 installments and will bear an

interest of 5.5% (See also note 10 below).

The Company estimated the fair value of the identified intangible assets in a total amount

of $1.6 million and the goodwill in the amount of $0.2 million.

e. Definitions:

In these financial statements:

The Company - Iphotonix LLC.

Related parties - As defined in IAS 24.

Dollar - U.S. dollar.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 10 -

NOTE 2:- SIGNIFICANT ACCOUNTING POLICIES

a. Basis of presentation of the financial statements:

1. Measurement basis:

The Company's financial statements have been prepared on a cost basis.

The Company has elected to present profit or loss items using the function of expense

method.

2. Basis of preparation of the financial statements:

These financial statements have been prepared in accordance with International

Financial Reporting Standards ("IFRS").

b. Significant accounting judgments, estimates and assumptions used in the preparation of the

financial statements:

Judgments:

In the process of applying the significant accounting policies, the Company has made the

following judgments which have the most significant effect on the amounts recognized in

the financial statements:

- Determining the fair value of share-based payment transactions:

The fair value of share-based payment transactions is determined using an acceptable

option-pricing model. The assumptions used in the model can include the share price,

exercise price and expected life.

Estimates and assumptions:

The preparation of the financial statements requires management to make estimates and

assumptions that have an effect on the application of the accounting policies and on the

reported amounts of assets, liabilities, revenues and expenses. These estimates and

underlying assumptions are reviewed regularly. Changes in accounting estimates are

reported in the period of the change in estimate.

c. Functional currency and foreign currency:

1. Functional currency and presentation currency:

The presentation currency of the financial statements is the U.S. dollar.

The functional currency, which is the currency that best reflects the economic

environment in which the Company operates and conducts its transactions and is

used to measure its financial position and operating results. The functional currency

of the Company is the U.S. dollar.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 11 -

NOTE 2:-SIGNIFICANT ACCOUNTING POLICIES (Cont.)

2. Transactions, assets and liabilities in foreign currency:

Transactions denominated in foreign currency (other than the functional currency)

are recorded on initial recognition at the exchange rate at the date of the transaction.

After initial recognition, monetary assets and liabilities denominated in foreign

currency are translated at the end of each reporting period into the functional

currency at the exchange rate at that date. Exchange differences, are recognized in

profit or loss. Non-monetary assets and liabilities measured at cost are translated at

the exchange rate at the date of the transaction.

d. Cash equivalents:

Cash equivalents are considered as highly liquid investments, including unrestricted short-

term bank deposits with an original maturity of three months or less from the date of

acquisition or with a maturity of more than three months, but which are redeemable on

demand without penalty and which form part of the Company's cash management.

e. Inventories:

Inventories are measured at the lower of cost and net realizable value. The cost of

inventories comprises costs of purchase and costs incurred in bringing the inventories to

their present location and condition. Net realizable value is the estimated selling price in

the ordinary course of business less the estimated costs of completion and the estimated

selling costs.

Cost of inventories is determined as follows:

Finished goods - on the basis of average costs.

The Company periodically evaluates the condition and age of inventories and makes

provisions for slow moving inventories accordingly.

f. Allowance for doubtful accounts:

The allowance for doubtful accounts is determined in respect of specific debts whose

collection, in the opinion of the Company's management, is doubtful. Impaired debts are

derecognized when they are assessed as uncollectible.

g. Financial instruments:

Financial assets:

Financial assets within the scope of IAS 39 are initially recognized at fair value plus

directly attributable transaction costs, except for investments at fair value through profit or

loss in respect of which transaction costs are recorded in profit or loss.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 12 -

NOTE 2:-SIGNIFICANT ACCOUNTING POLICIES (Cont.)

After initial recognition, the accounting treatment of financial assets is based on their

classification as follows:

Loans and receivables:

The Company has loans and receivables that are financial assets (non-derivative) with fixed

or determinable payments that are not quoted in an active market. After initial recognition,

loans are measured based on their terms at amortized cost using the effective interest

method taking into account directly attributable transaction costs. Short-term receivables

are measured based on their terms, normally at face value.

Financial liabilities:

Financial liabilities measured at amortized cost:

Loans and borrowings are initially recognized at fair value less directly attributable

transaction costs. After initial recognition, loans are measured based on their terms at

amortized cost using the effective interest method taking into account directly attributable

transaction costs. Short-term borrowings are measured based on their terms, normally at

face value.

Derecognition of financial instruments:

Financial assets:

A financial asset is derecognized when the contractual rights to the cash flows from the

financial asset expire or the Company has transferred its contractual rights to receive cash

flows from the financial asset or assumes an obligation to pay the cash flows in full without

material delay to a third party and has transferred substantially all the risks and rewards of

the asset, or has neither transferred nor retained substantially all the risks and rewards of

the asset, but has transferred control of the asset.

Financial liabilities:

A financial liability is derecognized when it is extinguished, that is when the obligation is

discharged or cancelled or expires. A financial liability is extinguished when the debtor

(the Company):discharges the liability by paying in cash, other financial assets, goods or

services; oris legally released from the liability.

Impairment of financial assets:

The Company assesses at the end of each reporting period whether there is any objective

evidence of impairment of a financial asset or group of financial assets as follows.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 13 -

NOTE 2:- SIGNIFICANT ACCOUNTING POLICIES (Cont.)

Financial assets carried at amortized cost:

There is objective evidence of impairment of loans and receivables carried at amortized

cost as a result of one or more events that has occurred after the initial recognition of the

asset and that loss event has an impact on the estimated future cash flows. Evidence of

impairment may include indications that the debtor is experiencing financial difficulties,

including liquidity difficulty and default in interest or principal payments. The amount of

the loss recorded in profit or loss is measured as the difference between the asset's

carrying amount and the present value of estimated future cash flows (excluding future

credit losses that have not yet been incurred) discounted at the financial asset's original

effective interest rate (the effective interest rate computed at initial recognition).The

carrying amount of the asset is reduced through the use of an allowance account (see

allowance for doubtful accounts above). In a subsequent period, the amount of the

impairment loss is reversed if the recovery of the asset can be related objectively to an

event occurring after the impairment was recognized. The amount of the reversal, up to the

amount of any previous impairment, is recorded in profit or loss.

h. Property, plant and equipment

Property, plant and equipment are measured at cost, including directly attributable costs,

less accumulated depreciation.

Depreciation is calculated on a straight-line basis over the useful life of the assets at annual

rates as follows:

%

Computers 33

Equipment 20

The useful life, depreciation method and residual value of an asset are reviewed at least

each year-end and any changes are accounted for prospectively as a change in accounting

estimate. As for testing the impairment of property, plant and equipment, see j below.

i. Other intangible assets:

Separately acquired intangible assets are measured on initial recognition at cost including

directly attributable costs. Intangible assets acquired in a business combination are

measured at fair value at the acquisition date. Expenditures relating to internally generated

intangible assets, excluding capitalized development costs, are recognized in profit or loss

when incurred.After initial recognition, intangible assets are carried at their cost less any

accumulated amortization and any accumulated impairment losses.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 14 -

NOTE 2:- SIGNIFICANT ACCOUNTING POLICIES (Cont.)

According to management's assessment, intangible assets have a finite useful life. The

assets are amortized over their useful life using the straight-line method and reviewed for

impairment whenever there is an indication that the asset may be impaired. The

amortization period and the amortization method for an intangible asset with a finite useful

life are reviewed at least at each financial year end. Changes in the expected useful life or

the expected pattern of consumption of future economic benefits embodied in the asset are

accounted for prospectively as changes in accounting estimates. The amortization of

intangible assets with finite useful lives is recognized in profit or loss.

The useful life of intangible assets is as follows:

Years

Developed technology 6

IPR&D 10

j. Impairment of non-financial assets:

The Company evaluates the need to record an impairment of the carrying amount of non-

financial assets whenever events or changes in circumstances indicate that the carrying

amount is not recoverable. If the carrying amount of non-financial assets exceeds their

recoverable amount, the assets are reduced to their recoverable amount. The recoverable

amount is the higher of fair value less costs of sale and value in use. In measuring value in

use, the expected future cash flows are discounted using a pre-tax discount rate that reflects

the risks specific to the asset. The recoverable amount of an asset that does not generate

independent cash flows is determined for the cash-generating unit to which the asset

belongs. Impairment losses are recognized in profit or loss.

An impairment loss of an asset, is reversed only if there have been changes in the estimates

used to determine the asset's recoverable amount since the last impairment loss was

recognized. Reversal of an impairment loss, as above, shall not be increased above the

lower of the carrying amount that would have been determined (net of depreciation or

amortization) had no impairment loss been recognized for the asset in prior years and its

recoverable amount. The reversal of impairment loss of an asset presented at cost is

recognized in profit or loss.

k. Share-based payment transactions:

The Company's CEO is entitled to remuneration in the form of equity-settled share-based

payment transactions.

Equity-settled transactions:

The cost of equity-settled transactions with employees is measured at the fair value of the

equity instruments granted at grant date. The fair value is determined using a standard

option pricing model.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 15 -

NOTE 2:- SIGNIFICANT ACCOUNTING POLICIES (Cont.)

The cost of equity-settled transactions is recognized in profit or loss, together with a

corresponding increase in equity, during the period which the performance and/or service

conditions are to be satisfied, ending on the date on which the relevant employees become

fully entitled to the award ("the vesting period"). The cumulative expense recognized for

equity-settled transactions at the end of each reporting period until the vesting date reflects

the extent to which the vesting period has expired and the Group's best estimate of the

number of equity instruments that will ultimately vest. The expense or income recognized

in profit or loss represents the change between the cumulative expense recognized at the

end of the reporting period and the cumulative expense recognized at the end of the

previous reporting period.

No expense is recognized for awards that do not ultimately vest, except for awards where

vesting is conditional upon a market condition, which are treated as vesting irrespective of

whether the market condition is satisfied, provided that all other vesting conditions (service

and/or performance) are satisfied.

Cash-settled transactions:

The cost of cash-settled transactions is measured at fair value on the grant date using an

acceptable option pricing model. The fair value is recognized as an expense over the vesting

period and a corresponding liability is recognized. The liability is remeasured at each

reporting date until settled at fair value with any changes in fair value recognized in profit

or loss.

l. Revenue recognition:

Revenues are recognized in profit or loss when the revenues can be measured reliably, it is

probable that the economic benefits associated with the transaction will flow to the

Company and the costs incurred or to be incurred in respect of the transaction can be

measured reliably. Revenues are measured at the fair value of the consideration received

less any trade discounts, volume rebates and returns.

The specific criteria for revenue recognition for the following types of revenues are:

Revenues from the sale of goods:

Revenues from the sale of goods are recognized when all the significant risks and rewards

of ownership of the goods have passed to the buyer and the seller no longer retains

continuing managerial involvement. The delivery date is usually the date on which

ownership passes.

Customer discounts:

Current customer discounts are recognized in the financial statements when granted and

are deducted from sales.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 16 -

NOTE 2:- SIGNIFICANT ACCOUNTING POLICIES (Cont.)

m. Cost of revenues and supplier discounts:

Cost of sales includes expenses for loss, storage and conveyance of inventories to the end

point of sale. Cost of sales also includes provisions for write-downs of inventories,

inventory write offs and provisions for slow-moving inventories.

n. Provisions:

Aprovision in accordance with IAS 37 is recognized when the Companyhas a present

obligation (legal or constructive) as a result of a past event, it is probable that an outflow

of resources embodying economic benefits will be required to settle the obligation and a

reliable estimate can be made of the amount of the obligation.

NOTE 3:- DISCLOSURE OF NEW STANDARDS IN THE PERIOD PRIOR TO THEIR

ADOPTION

a. IFRS 15, "Revenue from Contracts with Customers":

In May 2014, the IASB issued IFRS 15 ("IFRS 15").

IFRS 15 replaces IAS 18, "Revenue", IAS 11, "Construction Contracts", IFRIC 13,

"Customer Loyalty Programs", IFRIC 15, "Agreements for the Construction of Real

Estate", IFRIC 18, "Transfers of Assets from Customers" and SIC-31, "Revenue - Barter

Transactions Involving Advertising Services".

The IFRS 15 introduces a five-step model that will apply to revenue earned from contracts

with customers:

Step 1: Identify the contract with a customer, including reference to contract combination

and accounting for contract modifications.

Step 2: Identify the separate performance obligations in the contract

Step 3: Determine the transaction price, including reference to variable consideration,

financing components that are significant to the contract, non-cash consideration and any

consideration payable to the customer.

Step 4: Allocate the transaction price to the separate performance obligations on a relative

stand-alone selling price basis using observable information, if it is available, or using

estimates and assessments.

Step 5: Recognize revenue when the entity satisfies a performance obligation over time or

at a point in time.

IFRS 15 is to be applied retrospectively for annual periods beginning on or after January

1, 2018. Early adoption is permitted. IFRS 15 allows an entity to choose to apply a modified

retrospective approach, according to which IFRS 15 will only be applied in the current

period presented to existing contracts at the date of initial application. No restatement of

comparative periods is required.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 17 -

NOTE 3:- DISCLOSURE OF NEW STANDARDS IN THE PERIOD PRIOR TO THEIR

ADOPTION (Cont.)

The Company is evaluating the possible impact of IFRS 15 but is presently unable to assess

its effect, if any, on the financial statements.

b. Amendments to IAS 16 and IAS 38 regarding acceptable methods of depreciation and

amortization:

In May 2014, the IASB issued amendments to IAS 16 and IAS 38 ("the amendments")

regarding the use of a depreciation and amortization method based on revenue. According

to the amendments, a revenue-based method to calculate the depreciation of an asset is not

appropriate because revenue generally reflects factors other than the consumption of the

economic benefits embodied in the asset.

As for intangible assets, the revenue-based amortization method can only be applied in

certain circumstances such as when it can be demonstrated that revenue and the

consumption of economic benefits of the intangible asset are highly correlated.

The amendments are to be applied prospectively for annual periods beginning on or after

January 1, 2016. Early adoption is permitted.

c. IFRS 9, "Financial Instruments":

In July 2014, the IASB issued the final and complete version of IFRS 9, "Financial

Instruments" ("IFRS 9"), which replaces IAS 39, "Financial Instruments: Recognition and

Measurement". IFRS 9 mainly focuses on the classification and measurement of financial

assets and it applies to all assets in the scope of IAS 39.

According to IFRS 9, all financial assets are measured at fair value upon initial recognition.

In subsequent periods, debt instruments are measured at amortized cost only if both of the

following conditions are met:

- the asset is held within a business model whose objective is to hold assets in order

to collect the contractual cash flows.

- the contractual terms of the financial asset give rise on specified dates to cash flows

that are solely payments of principal and interest on the principal amount

outstanding.

Subsequent measurement of all other debt instruments and financial assets should be at fair

value. IFRS 9 establishes a distinction between debt instruments to be measured at fair

value through profit or loss and debt instruments to be measured at fair value through other

comprehensive income.

Financial assets that are equity instruments should be measured in subsequent periods at

fair value and the changes recognized in profit or loss or in other comprehensive income

(loss), in accordance with the election by the Company on an instrument-by-instrument

basis. If equity instruments are held for trading, they should be measured at fair value

through profit or loss.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 18 -

NOTE 3:- DISCLOSURE OF NEW STANDARDS IN THE PERIOD PRIOR TO THEIR

ADOPTION (Cont.)

According to IFRS 9, the provisions of IAS 39 will continue to apply to derecognition and

to financial liabilities for which the fair value option has not been elected.

According to IFRS 9, changes in fair value s of financial liabilities which are attributable

to the change in credit risk should be presented in other comprehensive income. All other

changes in fair value should be presented in profit or loss.

IFRS 9 also prescribes new hedge accounting requirements.

IFRS 9 is to be applied for annual periods beginning on January 1, 2018. Early adoption is

permitted.

The Company is evaluating the possible impact of IFRS 9 but is presently unable to assess

its effect, if any, on the financial statements.

d. Amendments to IAS 7, "Statement of Cash Flows", regarding additional disclosures of

financial liabilities:

In January 2016, the IASB issued amendments to IAS 7, "Statement of Cash Flows", ("the

amendments") which require additional disclosures regarding financial liabilities. The

amendments require disclosure of the changes between the opening balance and the closing

balance of financial liabilities, including changes from cash flows, changes arising from

obtaining or losing control of subsidiaries, the effect of changes in foreign exchange rates

and changes in fair value.

The amendments are effective for annual periods beginning on or after January 1, 2017.

Comparative information for periods prior to the effective date of the amendments is not

required. Early application is permitted.

The Company will include the necessary disclosures in the financial statements when

applicable.

NOTE 4:- TRADE RECEIVABLES

a. Composition:

December 31,

2015 2014

U.S. dollars in thousands

Open accounts 1,711 664

Less - allowance for doubtful accounts - -

Trade receivables, net 1,711 664

Trade receivables are non-interest bearing and are generally for 30-45 day terms.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 19 -

NOTE 4:- TRADE RECEIVABLES (Cont.)

An analysis of past due but not impaired trade receivables (allowance for doubtful accounts),

trade receivables, net, with reference to reporting date:

Neither past

due nor

impaired

Total

U.S. dollars in thousands

December 31, 2015 1,711 1,711

December 31, 2014 664 664

NOTE 5:- INVENTORIES

December 31,

2015 2014

U.S. dollars in thousands

Finished goods 692 506

Row Materials 99 161

791 667

NOTE 6:- PROPERTY, PLANT AND EQUIPMENT

Computers

Office furniture

and equipment

Total

Cost: Balance as of January 1, 2015 31 521 552 Acquisitions during the year 35 11 46

Balance as of December 31, 2015 66 532 598 Accumulated depreciation: Balance as of January 1, 2015 20 348 368 Provision during the year 27 133 160

Balance as of December 31, 2015 47 481 528

Depreciated cost at December 31, 2015 19 51 70

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 20 -

NOTE 6:- PROPERTY, PLANT AND EQUIPMENT (CONT.)

Computers

Office furniture

and equipment

Total

Cost: Balance as of January 1, 2014 17 481 498 Acquisitions during the year 14 40 54

Balance as of December 31, 2014 31 521 552 Accumulated depreciation: Balance as of January 1, 2014 17 209 226 Provision during the year 3 139 142

Balance as of December 31, 2014 20 348 368

Depreciated cost at December 31, 2014 11 173 184

NOTE 7:- INTANGIBLE ASSETS

December 31,

2015 2014

U.S. dollars in thousands

Cost 2,818 1,196

Accumulated amortizations 781 581

Balance as of December 31 2,037 615

The intangible assets are being depreciated over a period of 6 years.

NOTE 8:- TRADE PAYABLES

December 31,

2015 2014

U.S. dollars in thousands

Open debts 2,147 733

Notes payable 12 3

2,159 736

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 21 -

NOTE 9:- OTHER ACCOUNTS PAYABLE

December 31,

2015 2014

U.S. dollars in thousands

Employees and payroll accruals 62 70

Warranty accrual 100 28

Deffered expenses 35 6

Other payables 97 73

294 177

NOTE 10:- LOAN FROM BANK

a. Composition:

December 31

2015 2014

U.S. dollars in thousands

Loan from bank 1,023 -

Less - current maturities (236) -

787 -

b. Covenants:

On March 2, 2015 the Company signed a loan agreement with Comerica bank. In

accordance to the loan agreement the Company is obligated to maintain a minimum balance

of cash at bank of not less 125$ thousands.

As of December 31, 2015, the Company is meeting its covenants.

NOTE 11:- EQUITY

a. Composition:

December 31, 2015 and 2014

Ownership Units

Authorized

Issued and

outstanding

Ownership Units 10,000,000 4,918,065

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 22 -

NOTE 11:- EQUITY (CONT.)

b. Unit Appreciation Right (UAR) bonus plan:

iPhotonix LLC established a Unit Appreciation Right (UAR) bonus plan for employees.

The UAR vests if grantee is employed by the Company on the date of a corporate change

of control at which time the grantee will become fully vested in his or her award. The UARs

expire on the earlier 5 years from the date of grant or date of a corporate change of control

if the fair market value of an ownership unit on such date is less than the grant benchmark

value.

As of December 31, 2015, 617,857 UARs were granted.

Upon exercise, grantee is entitled to receive an amount payable for each Unit Appreciation

Right equal to the excess of the Fair Market Value of a share of Ownership Units on the

date of Exercise over the Grant Benchmark value of a share of Ownership Units on the date

of Grant.

The Company estimates that the probability of a Corporate Change, in the next 5 years is

less than 50%. No liability was recognized in the Company's financial statements.

NOTE 12:- COST OF SALES

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Materials 5,378 4,552

Support 53 -

Freight 321 311

Warranty expenses 41 63

Other expenses 46 12

5,839 4,938

NOTE 13:- RESEARCH AND DEVELOPMENT

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Wages, salaries and related expenses 2,505 1,709

Contract labor 78 44

Engineering Prototypes 11 15

Depreciation and amortization 360 341

Other 510 248

3,464 2,357

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 23 -

NOTE 14:- SELLING AND MARKETING EXPENSES

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Wages, salaries and related expenses 444 371

Others 222 155

666 526

NOTE 15:- GENERAL AND ADMINISTRATIVE EXPENSES

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Wages, salaries and related expenses 656 702

Rental and maintenance 176 176

Professional fees 139 106

Others 220 245

1,191 1,229

NOTE 16:- FINANCE EXPENSES

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Interest expense 526 13

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 24 -

NOTE 17:- FINANCIAL INSTRUMENTS

a. Classification of financial assets and liabilities:

The financial assets and financial liabilities in the statement of financial position are

classified by groups of financial instruments pursuant to IAS 39:

December 31,

2015 2014

U.S. dollars in thousands

Financial assets:

Loans and receivables 1,711 664

Financial liabilities:

Financial liabilities measured at amortized cost 6,187 3,026

b. Financial risks factors:

The Company's activities expose it to various financial risks such as credit risk and liquidity

risk.

1. Credit risk:

The Company extends a 30-60 day term to its customers. The Company regularly

monitors the credit extended to its customers and their general financial condition

but does not require collateral as security for these receivables. The Company does

not provide an allowance for doubtful accounts as no accounts have been

uncollectable and all accounts receivable were current at year end.

2. Liquidity risk:

The Company monitors its risk to a shortage of funds using weekly budget and cash

flow tools. Capital calls are made as needed to provide the liquidity the Company

needs to meet its obligations.

December 31, 2015:

Less than one

year 1 to 2 years

2 to 3 years

Not yet determine Total

U.S. dollars in thousands Trade payables 2,159 - - - 2,159 Other account payable 40 - - - 40 Loan from Bank 236 604 183 - 1,023 Shareholders - - - 800 800 Related party - - - 1,913 1,913 Other non-current liabilities - - 244 - 244 2,435 604 427 2,713 6,179

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 25 -

NOTE 17:- FINANCIAL INSTRUMENTS (Cont.)

December 31, 2014:

Less than one

year

Not yet

determine

U.S. dollars in thousands

Trade payables 736 -

Other account payable 7 -

Shareholders - 300

Related party - 1,983

743 2,283

c. Fair value:

Carrying amount Fair value

December 31, December 31,

2015 2014 2015 2014

U.S. dollars in

thousands

U.S. dollars in

thousands

Financial liabilities:

Loan from Bank (1,023) - (1,023) -

Shareholders (800) (300) (350) (208)

Related party (1,913) (1,983) (1,057) (1,147)

The carrying amount of cash and cash equivalents, trade receivables, other accounts

receivable, related party balance, trade payables, other accounts payable and other non-

current liabilities approximate their fair value.

NOTE 18:- BALANCES AND TRANSACTIONS WITH RELATED PARTIES

a. Balances with related parties:

December 31,

2015 2014

U.S. dollars in thousands

Related party- Shareholders (1) (800) (300)

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 26 -

Related party- Fellow subsidiary (2) (1,913) (1,983)

Key management employees (9) (1)

(1) See also Note 1(c).

(2) During 2013, a related party granted the Company a loan in the amount of

approximately $ 2.3 million. The repayment period has not yet been determined.

IPHOTONIX LLC

NOTES TO FINANCIAL STATEMENTS

- 27 -

NOTE 18:- BALANCES AND TRANSACTIONS WITH RELATED PARTIES (Cont.)

b. Transactions with related parties:

Year ended

December 31,

2015 2014

U.S. dollars in thousands

Purchases of inventory from a fellow subsidiary - 152

Services provided by a fellow subsidiary 31 16

Key management employees 176 179

c. On January 26, 2012, the Company allocated in favor of the CEO participation units

representing, on the grant date, 2% of the Company's ownership units. Furthermore,

additional participation units were allocated for the CEO that are blocked participation units

and held by a trustee, under an incentive plan for the CEO, which shall be released in

installments subject to the plan's conditions and the continued employment of the CEO

over three years. Under the plan's conditions, it was determined, among others, that on

January 1, 2013 an adjustment of the participation units quantity issued to the CEO shall

be performed such that as of that date, he shall hold participation units representing 3% of

the Company's ownership units and in the blocked participation units (held by a trustee)

representing 2% of the Company's ownership units and in the aggregate no more than 5%

of the Company's ownership units. The fair value of the participation units allocated to the

Company's CEO is $ 130 thousand. The Company's financial statements for the year ended

December 31, 2014 include an expense of $ 7 thousand in respect of this grant.

On January 14, 2014, the Company allocated in favor of the CEO additional participation

units representing, on the grant date, 2.5% of the Company's ownership units. Furthermore,

additional options were allocated for the CEO representing 2.5% of the Company's

ownership units. Under the plan's conditions, it was determined, that the participation units

and options will be vested on the day of the grant and will be forfeited if the CEO will leave

the Company prior to event of change of control.

The fair value of the participation units and options allocated to the Company's CEO is

$ 60 thousand. The Company's financial statements for the year ended December 31, 2014

include an expense of $ 60 thousand in respect of this grant.

----------------------------------------------

F:\W2000\w2000\60820064\M\15\E12-IPHOTONIX LLC.docx