ipsos mediact syndicated event presentation booklet

TRANSCRIPT

© Ipsos MORI

© Ipsos MORI | Version 1

Understanding the Global Affluent and Elite Powered by Syndicated Surveys

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Welcome

The global Affluent and Business

Elite surveys have been in

existence for many years, but

never have we seen these two

complimentary surveys side by

side, until now.

The Affluent and Business Elite

represent the wealthiest, and most

influential group of individuals in

the world.

2

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

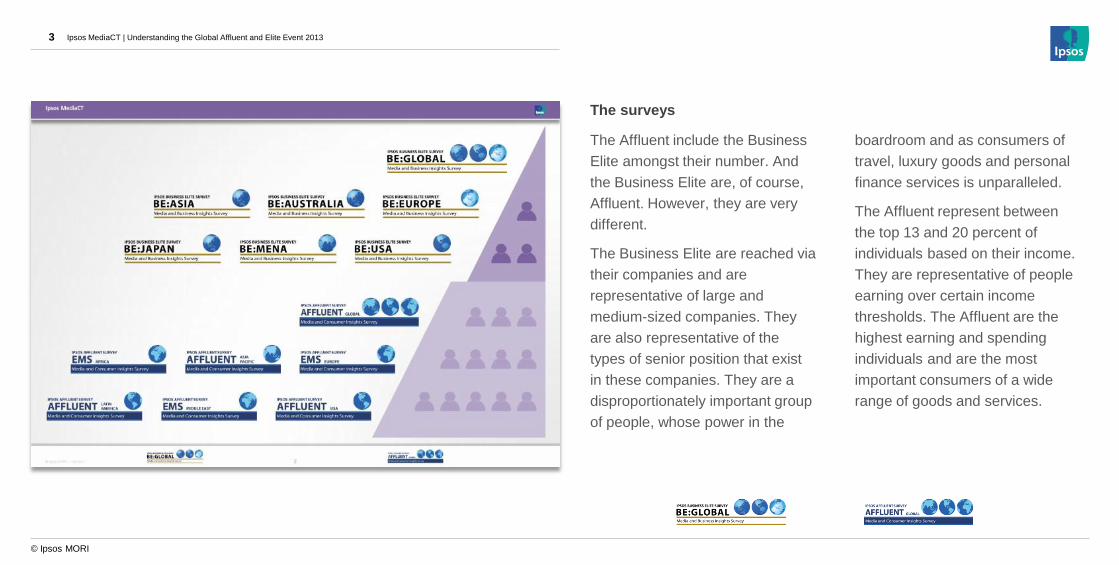

The surveys

The Affluent include the Business

Elite amongst their number. And

the Business Elite are, of course,

Affluent. However, they are very

different.

The Business Elite are reached via

their companies and are

representative of large and

medium-sized companies. They

are also representative of the

types of senior position that exist

in these companies. They are a

disproportionately important group

of people, whose power in the

boardroom and as consumers of

travel, luxury goods and personal

finance services is unparalleled.

The Affluent represent between

the top 13 and 20 percent of

individuals based on their income.

They are representative of people

earning over certain income

thresholds. The Affluent are the

highest earning and spending

individuals and are the most

important consumers of a wide

range of goods and services.

3

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Portraits

And this chart really helps us to

understand how the groups are

different. The Business Elite are

business focused and are signing

off large budgets, have substantial

financial worth and travel

frequently in business and first

class.

The affluent by nature are big

shoppers, owning premium goods

such as luxury cars, and fly

frequently.

4

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Change

Change happens the whole time. It

effects absolutely everyone in

many different ways:

A change in the weather dictates

what you wear in the morning

A change in technology in how you

access content

However much it challenges us it’s

necessary and enables us to

continue. We’re pretty much in a

permanent state of change.

5

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Pace of change

And, to help add to this, the pace

of change we face is becoming

ever quicker. The more often ideas

come together, the more

frequently it occurs.

To put this into perspective,

scientists think the age of the earth

is about 4 and half billion years.

The first telephone call was made

in 1876, 137 years ago. 97 years

on the first mobile phone call was

made in 1973 and now 40 years

on from here we have phones that

fit in your pocket that can pretty

much do anything from monitoring

how well you’ve slept to playing

music that suits your mood.

And interestingly, now more

people in the world have access to

a mobile phone than a working

toilet!

6

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Two areas

So, we’re now going to focus on

two areas of change that we’ve

seen more recently in the 21st

century:

• Economic changes

• And, the development of

technology

We’ll be looking at these and

specifically how two audiences

have reacted: the Global Affluent,

and the Global Business Elite.

7

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Economies

Economies around the world have

changed dramatically. Some have

seen growth. Others have slumped

into recession. It’s a very mixed

picture. So around the world,

depending on who you are, and

where you are, you will react

differently to different situations.

8

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Chocolate – recession proof

In mature markets, such as

Europe and the US the recession

hit hard. The average person cut

back on spending – from the

weekly shop to a new TV.

However, what they could afford

was chocolate – widely considered

a recession proof food. With

consumers eating out less and

eating at home more, chocolate

allowed them that inexpensive

indulgence. In fact, in 2009 Swiss

chocolate makers had record

sales.

There has been a fundamental

change to how many of us live.

So, that’s an example of how the

average react to change,

specifically in recession. The

affluent and business elite react

differently….

9

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Global Affluent

But that’s how the average have

reacted in markets that are in

recession. The affluent react

slightly differently….

The ‘Global Affluent’ come in all

shapes and sizes, with a myriad of

different wants and needs from

Turkey, Brazil, Singapore to the

USA. Yet, these individuals have

one thing in common they are

disproportionately important to

most marketers of many products

and services.

10

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Busy lives

They lead every busy lives, 60%

work more than 40 hours a week

and travel for business or pleasure

on a regular basis, which could

explain why 41% find it difficult to

find a balance between private life

and work. 7 out of 10 feel that

there is just not enough time in a

day. When they do have some

time off, they use it to unwind and

relax.

So while unemployment continues

to be a problem for the general

population it isn’t for the affluent….

11

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Income

The mean income of the average

affluent respondent has remained

stable over the last few years and

we do not see any decline in their

buying patterns, however, they are

being more conservative in how

they invest possibly to protect their

existing wealth. The proportion of

people trading stocks and shares

at least 6 times a year has

declined from 27% in 2011 to 10%

in 2013 although the actual total

value of their investments has

increased significantly + 2 billion

euros.

12

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Disposable income

So, they continue to be the big

spenders with the disposable

income to purchase high value

items.

They like to treat themselves – and

it’s not chocolate – it’s with the

latest gadgets, fast cars or high

fashion.

Take the Affluent in the Middle

East for instance. 14% spend

1,500 euros or more on jewellery

in a year, which is similar to the

amount of what the European

affluent wear on their wrists.

The value of their main watch is

nearly 1,000 euros, and they are

planning to spend even more on

the next one.

13

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Spending on cars

Whereas the population are

holding off replacing cars, the

affluent still have enough to spend

- in Europe, 1.7 million are

planning to spend over 50,000

euro on a new car in the next 12

months.

These are the people that keep the

industry – luxury cars that make

the most money for the

companies…

14

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Travel

Travel is widespread among

affluents in the USA, both for

business and pleasure, with 86%

having made at least one round

trip in the last year. Two thirds

agree that it is worth paying extra

for comfort and service when

travelling. It would be fair to

describe The Affluent as ‘Global

Citizens’ – they travel frequently,

speak multiple languages and

consume international media.

Among the Affluent in Asia Pacific

there is a 14% year-on-year

increase for the number of air trips

taken. So they do continue to go

on holiday, the amount of holidays

taken in the past 12 months

remains the same.

15

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Business is central

The Business Elite being a

different audience, think and

behave differently. How they’ve

reacted and adapted to the

economic changes is distinctive

and unique.

So what was on their mind… As

per their name, Business is

central. They live and breathe it.

Change is something that the

Business Elite actively embrace –

it allows them to develop and

progress.

16

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

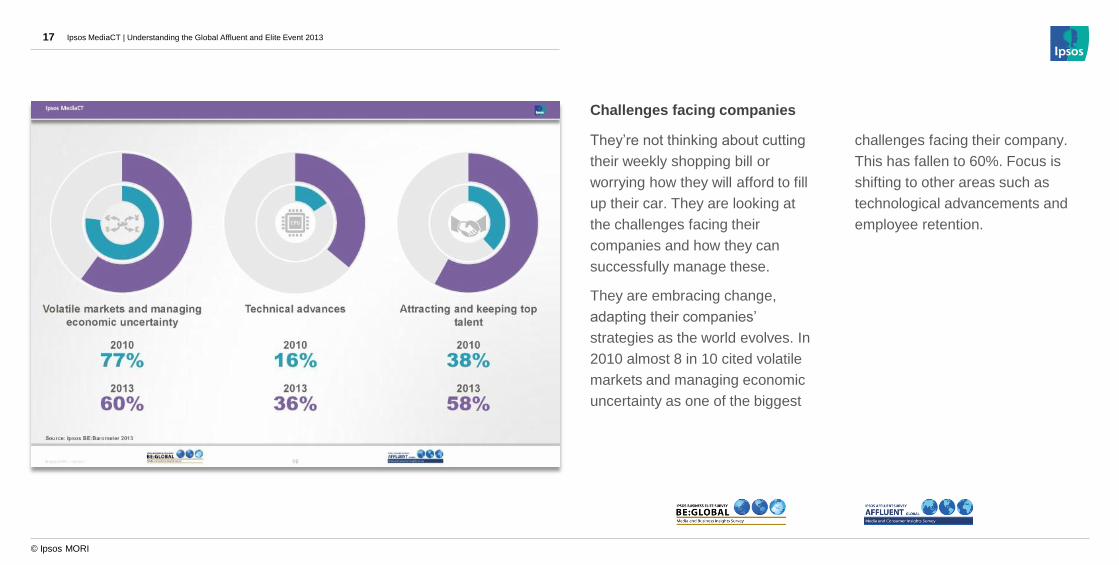

Challenges facing companies

They’re not thinking about cutting

their weekly shopping bill or

worrying how they will afford to fill

up their car. They are looking at

the challenges facing their

companies and how they can

successfully manage these.

They are embracing change,

adapting their companies’

strategies as the world evolves. In

2010 almost 8 in 10 cited volatile

markets and managing economic

uncertainty as one of the biggest

challenges facing their company.

This has fallen to 60%. Focus is

shifting to other areas such as

technological advancements and

employee retention.

17

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Fuel and raw materials

With continued uncertainty in the

middle east putting pressure on oil

prices it’s maybe not surprising

that the number of Business Elite

citing the price of fuel and raw

materials as one of the biggest

challenges has increased by a

third since 2010. Fuel and raw

materials allow their companies to

produce technologically advanced

goods and services that keep them

competitive and thus profitable. It’s

all a very long way away from your

local garage forecourt…

18

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

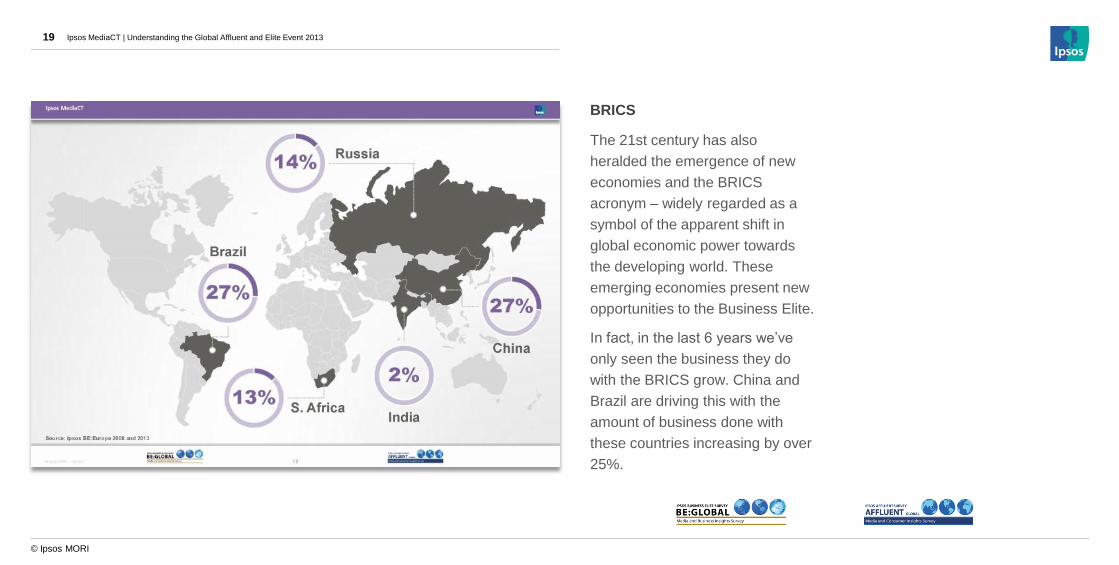

BRICS

The 21st century has also

heralded the emergence of new

economies and the BRICS

acronym – widely regarded as a

symbol of the apparent shift in

global economic power towards

the developing world. These

emerging economies present new

opportunities to the Business Elite.

In fact, in the last 6 years we’ve

only seen the business they do

with the BRICS grow. China and

Brazil are driving this with the

amount of business done with

these countries increasing by over

25%.

19

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Salary and net worth

A by product of being one of the

most senior business executives in

a company is a high salary and net

worth. Given the change in

economic conditions we saw the

European Business Elite take the

biggest pay cut we’ve seen in a

while between 2008 and 2009.

However, the number receiving

shares from their company

increased by almost a fifth. So

they are still benefitting.

It’s all a very different world they

exist in. They don’t have to watch

what they put in their shopping

trolley.

20

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Business Elite wealth

However, given the differing

economic situations around the

world we’ve seen some shifts in

the Business Elite’s wealth. 2010

was a pretty significant year.

Asia’s growth saw the proportion

of millionaires amongst the Asian

Business Elite overtake that of

their European counterparts for the

first time ever. And the gap is only

getting wider…

21

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

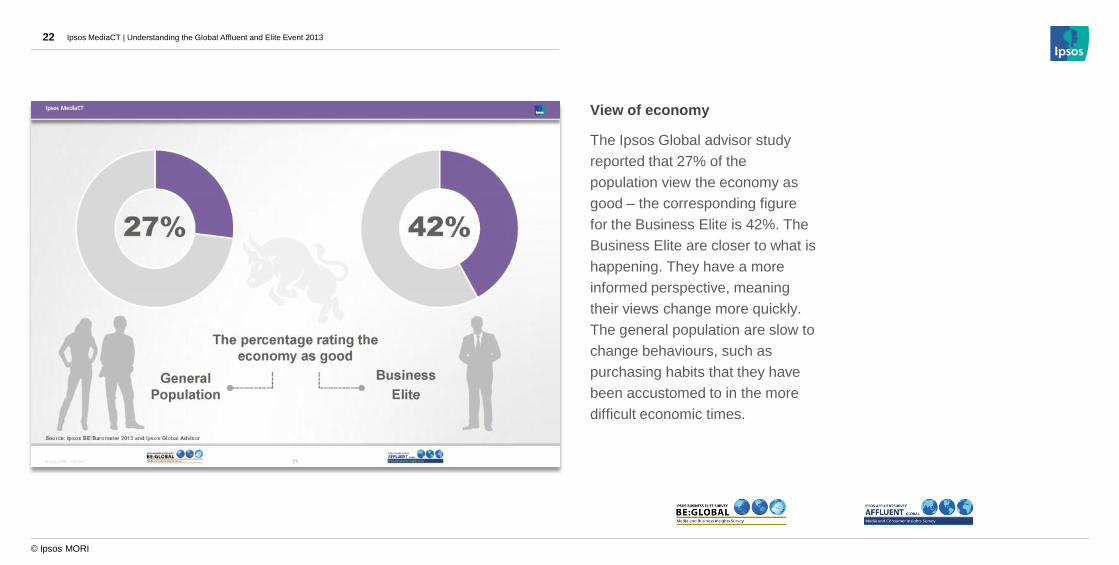

View of economy

The Ipsos Global advisor study

reported that 27% of the

population view the economy as

good – the corresponding figure

for the Business Elite is 42%. The

Business Elite are closer to what is

happening. They have a more

informed perspective, meaning

their views change more quickly.

The general population are slow to

change behaviours, such as

purchasing habits that they have

been accustomed to in the more

difficult economic times.

22

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

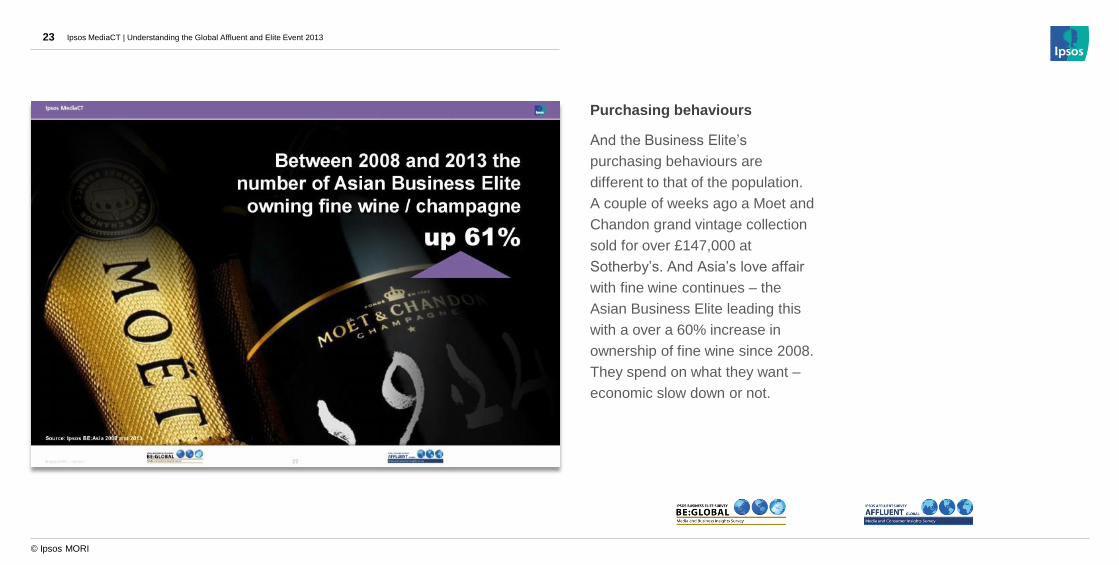

Purchasing behaviours

And the Business Elite’s

purchasing behaviours are

different to that of the population.

A couple of weeks ago a Moet and

Chandon grand vintage collection

sold for over £147,000 at

Sotherby’s. And Asia’s love affair

with fine wine continues – the

Asian Business Elite leading this

with a over a 60% increase in

ownership of fine wine since 2008.

They spend on what they want –

economic slow down or not.

23

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Technological change

We will now look at the quickening

pace of technological change and

the specific affect this has had on

the Affluent and Business Elite.

But first lets just put into context

where we are now…

24

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

People online

There are 3 billion people now

online. This allows better

communication, facilitating the

sharing of ideas allowing the

digital evolution to continue at an

ever faster rate.

25

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

iPhone

Apple launched the first iPhone in

June 2007 – over six years later

24% of the population now own

one.

30% of the UK population now

own a tablet, up from 6% just two

years ago.

26

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Multiple screens

So people are now accessing

content through multiple screens.

Connected devices are becoming

ever more fragmented creating big

opportunities, but also big

challenges! Mobile is enabling new

forms of entertainment,

communication, media and

commerce.

It’s changing how we consume.

But not everyone is at the same

place in terms of technological

evolution…

27

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Digital adoption

When it comes to digital adoption,

the affluent are at least 12 months

ahead, they are early adopters and

using multi-screens has been a

regular part of the lives for

years. 9 out of 10 own a mobile

device. Given their busy lives E-

commerce is massive time saver

and they purchase items from

flowers, holidays and the latest

smart phone online. The average

value of their online purchasing in

the last 6months has increased by

over 50% in the last 2 years, with

over 76% spending a minimum of

E100. This will undoubtedly

continue to rise.

28

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Social networking

The affluent actively pick and

choose which content they want to

engage with, for example social

networking, access to this content

is available anytime, anywhere.

And regardless of geography and

preference, online social venues

are also increasingly a place to

communicate and socialize with

friends, colleagues but also

customers and prospects. Social

media continues to grow rapidly,

the top 3 network sites have all

increased universe sizes in the last

12 months.

While social media is undoubtedly

growing, the top 4 networking sites

among Europe’s affluent are

Facebook, Google+, LinkedIn and

Twitter.

29

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Daily life has become more digital

It is a fact that reading print and

watching TV still make up a large

proportion of upscale media

consumption, but at the same time

daily life has become more digital,

whether in the office, at home or when

travelling on business or for pleasure.

Mobile digital connectivity is the norm

among Europe’s affluent, 90 own at

least one mobile device, whether it be

a smartphone, tablet, e- reader or

netbook.

The growth of digital platforms has

had 2 primary effects:

Affluent consumers who previously

could not easily purchase a particular

print title or have a connection to a

specific channel can do so easily via

the internet.

Shifting consumption patterns across

platforms. Consumers are able to

access content via different platforms

allowing consumers to access the

content they want on whichever

platform is most convenient.

No matter where they are, the affluent

are always connected, over 16.4%

using an average of 3 devices. Given

the multiplicity of devices in use, it

becomes increasingly important for

brands to have an online presence

that is optimized for computers, tablets

and mobile phones, alike.

30

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Business model innovation.

Technology also plays a big part in

the Business Elite’s lives. It helps

their companies to innovate and

remain profitable.

Just over two years ago

(September 2011) Snapchat

launched. It was said that

Facebook offered to buy it just the

other week for US$3 billion. That’s

big growth quickly. And while

people are sharing 350 million

pictures a day on Snapchat, it’s

probably safe to say it’s not the

Business Elite.

However, the Business Elite are

still very interested in companies

like this – if not involved in them,

they are learning from them.

There’s David Butler here the VP

of Innovation at Coca-Cola –

obviously in his Sunday best! He’s

said the only way to get this kind of

growth is through business model

innovation.

31

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

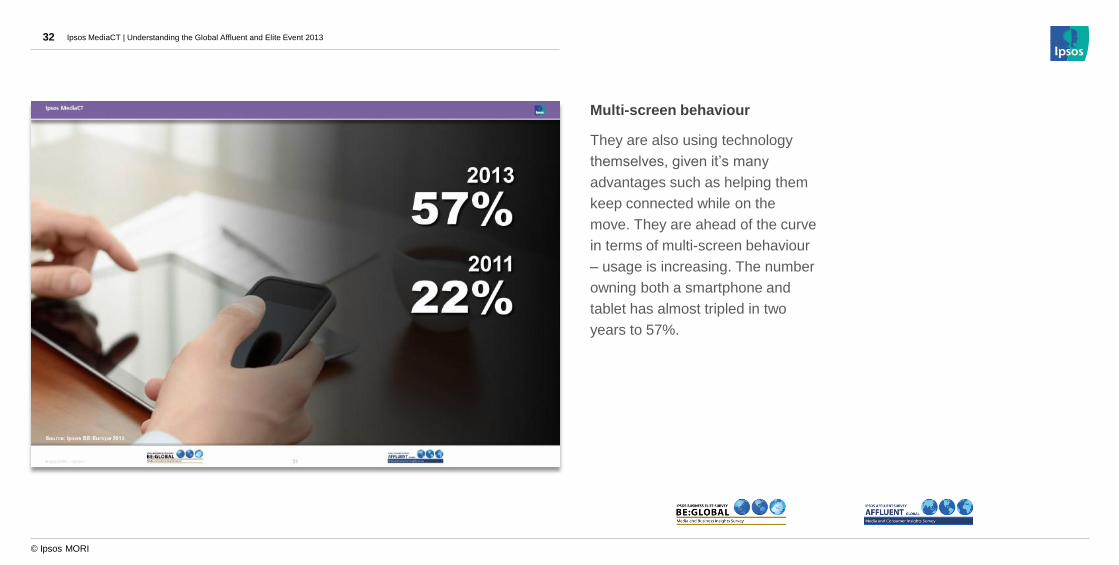

Multi-screen behaviour

They are also using technology

themselves, given it’s many

advantages such as helping them

keep connected while on the

move. They are ahead of the curve

in terms of multi-screen behaviour

– usage is increasing. The number

owning both a smartphone and

tablet has almost tripled in two

years to 57%.

32

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Device usage

And they’re using their devices for

a variety of activities from watching

TV to reading. And interestingly to

play games, and to shop…

This technological transformation

is changing the lives and

behaviours of both the affluent and

business elite.

33

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Traditional platforms

However, while we see this

increased use of digital it’s

important to remember that they

are also continuing to consume by

more traditional platforms such as

print and TV, remaining loyal to

those brands they have

progressed through life with.

34

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

The future

In just the last few years we’ve

seen dramatic changes taking

place and how both the affluent

and elite have reacted to this. A

question that remains is what will

happen in the future? Of course

we can’t be absolutely sure but…

35

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Connected devices

There’s going to be even more

connected devices such as

watches and smart glasses

meaning that how we consume

content and go about our every

day life will continue to evolve. The

Affluent are going to be among the

first to buy these and the business

elite the first to make them.

36

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

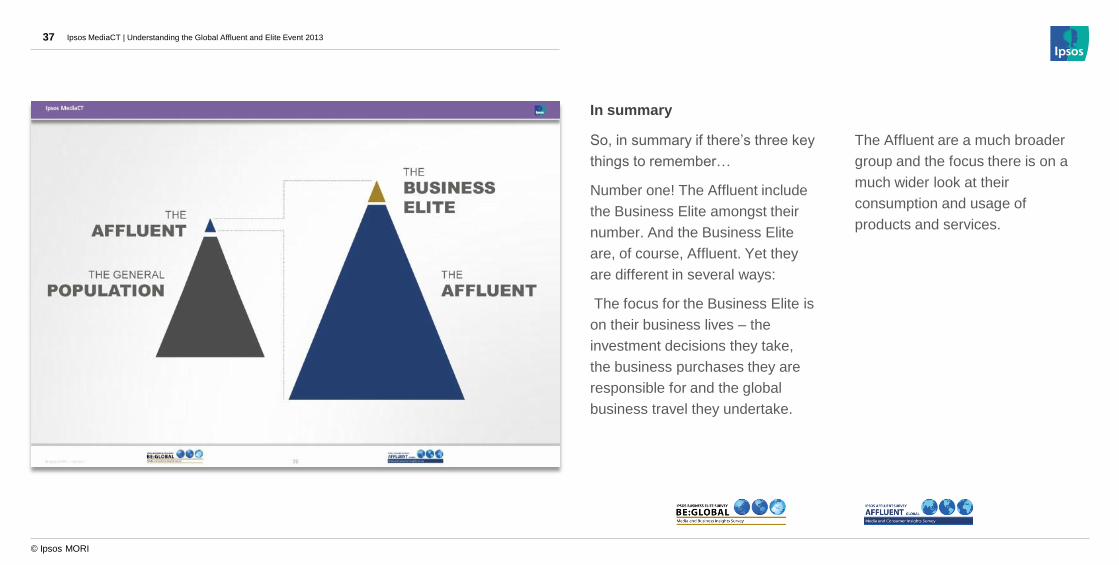

In summary

So, in summary if there’s three key

things to remember…

Number one! The Affluent include

the Business Elite amongst their

number. And the Business Elite

are, of course, Affluent. Yet they

are different in several ways:

The focus for the Business Elite is

on their business lives – the

investment decisions they take,

the business purchases they are

responsible for and the global

business travel they undertake.

The Affluent are a much broader

group and the focus there is on a

much wider look at their

consumption and usage of

products and services.

37

Ipsos MediaCT | Understanding the Global Affluent and Elite Event 2013

© Ipsos MORI

Key take-aways

Secondly. Despite everything

going on around the world, the

affluent, being the highest earning

and spending individuals, are the

most important consumers for a

wide range of goods and services.

And, as the most senior business

people in the worlds medium and

large companies, the Business

Elite remain a key audience for

B2B marketing and

communications, travel, finance

and luxury goods.

Key take away number 3. Both

audiences consume large amounts

of content through a variety of

platforms and more often than not

are ahead of the curve in terms of

digital adoption.

38

James Torr

Director of Sales and Marketing

t: +44 (0)20 8861 8173

www.ipsos-mori.com

Nathalie Sodeike

EMS Director

t: +31 (0)20 6070 822

www.ipsos-nederland.nl/ems