irp version 5 0 narrative final v8-5-07 - cre finance council

TRANSCRIPT

CREFC INVESTOR REPORTING PACKAGE®X Version 6.0 Working Exposure Draft #1 © 2008 Commercial Real Estate Finance Council

CREFC Investor Reporting Package

TABLE OF CONTENTS

I. Overview of the CREFC Investor Reporting Package................................................................... 3 II. Change Matrix for Version 6.0 ................................................................................................... 25 III. CREFC Supplemental Reports..................................................................................................... 31

1) Servicer Watchlist/Portfolio Review Guidelines................................................................ 32 2) Delinquent Loan Status Report........................................................................................... 35 3) REO Status Report.............................................................................................................. 36 4) Comparative Financial Status Report ................................................................................. 37 5) Historical Loan Modification and Corrected Mortgage Loan Report ................................ 38 6) Loan Level Reserve/LOC Report ....................................................................................... 39 7) Total Loan Report…(Includes sample) .............................................................................. 40 8) Advance Recovery Report.................................................................................................. 42

IV. CREFC/MBA Methodology for Analyzing and Reporting Property Income Statements........... 43

1) Commercial Operating Statement Analysis Report............................................................ 51 2) Commercial NOI Adjustment Worksheet .......................................................................... 52 3) Multifamily Operating Statement Analysis Report ............................................................ 53 4) Multifamily NOI Adjustment Worksheet........................................................................... 54 5) Lodging Operating Statement Analysis Report.................................................................. 55 6) Lodging NOI Adjustment Worksheet................................................................................. 56 7) Healthcare Operating Statement Analysis Report .............................................................. 57 8) Healthcare NOI Adjustment Worksheet............................................................................. 58 9) Master Coding Matrix ........................................................................................................ 59

V. CREFC Disclosure Templates....................................................................................................... 63

1) Appraisal Reduction ........................................................................................................... 64 2) Servicer Realized Loss…(Includes sample)....................................................................... 65 3) Reconciliation of Funds...................................................................................................... 67 4) Historical Bond/Collateral Realized Loss Reconciliation…(Includes sample) ................. 68 5) Historical Liquidation Loss ................................................................................................ 70 6) Interest Shortfall Reconciliation......................................................................................... 71 7) Servicer Remittance to Trustee (Includes sample and field descriptions)......................... 72 8) Significant Insurance Event Report (Includes Form Key) ................................................. 75

VI. Guidance for Specific Situations ................................................................................................ 81 VII. Frequently Asked Questions ...................................................................................................... 87

I. Overview of the CREFC Investor Reporting Package

Page 3 CREFC IRP Version 6.0-Draft #1– 1/9/09

– 1/9/09Ed

Overview of the CREFC Investor Reporting Package®x v6.0 (CREFC IRP®x v6.0)

Past to Present

This package constitutes a working exposure draft of IRPx v6.0 of the Commercial Real Estate Finance Council Investor Reporting Package® (CREFC IRP), and is the first version using an eXtensible Markup Language (“XML”) data transfer specification. The CREFC IRP Committee, responsible for developing periodic updates to the CREFC IRP, consists of a representative group of investors, servicers, trustees, underwriters and rating agencies. For the past 10 years, the CMBS industry has exchanged flat data files in Excel spreadsheet format which conforms to previous CREFC IRP guidelines developed by the CREFC IRP Committee. CREFC has elected to facilitate the transmission of IRP data in XML in order to achieve a number of benefits for firms that are obligated to produce and/or report the IRP, and to utilize the Mortgage Industry Standards Maintenance Organization (MISMO) standards, framework and processes to accomplish the conversion to XML. MISMO, a not-for-profit subsidiary of the Mortgage Bankers Association (MBA), is the leading standards development body for the development of electronic data standards and electronic document formats for the residential and commercial real estate finance industries. Supported by over 100 organizations, MISMO was started in 1999 by MBA to promote, coordinate and facilitate the mortgage industry's efforts to create standardized Internet-based real estate finance transactions. Mortgage bankers, lenders, servicers, vendors and service providers are adopting MISMO standards. These standards promote consistency throughout the industry. Additionally, these standards reduce costs, increase transparency and boost investor confidence in mortgages as an asset class. MISMO has working agreements with many major data standards development organizations and has developed a language of industry data elements, stored in a common electronic data dictionary. These data elements are used to create all MISMO transactions. In 2003, the MBA and CREFC announced that MISMO will be authorized to incorporate the contents of the CREFC IRP into the MISMO data dictionary. Under this arrangement, CREFC will retain both the ownership and the responsibility for revising and updating the IRP. MISMO will establish an XML - based data transfer specification that will provide information consistent with the CREFC IRP. The CREFC Investor Reporting Committee formed a working group with MISMO that is creating the XML specifications to contain at a minimum all of the information required by the CMSA IRP v5.0. This document will detail the business and reporting requirements as well as provide an overview of the technical issues of moving to an XML standard. The actual XML reporting specifications, schema and technical implementation issues are included in the MISMO XML standards located on the internet at www.MISMO.org under Commercial Mortgage Specifications. The current economic crisis and its impact on CMBS issuance has delayed some aspects of this effort. As a result of the continued Capital Markets turmoil, some industry participants have questioned the necessity of finalizing this standard during this period of uncertainly. However, it is believed that this is the best time to finalize these standards since the benefits that are discussed below will positively and directly impact the industry’s existing $1.8 trillion of outstanding CMBS. In addition, as the industry stabilizes, new forms of commercial property financing may appear. Consequently, these standards could become commercial mortgage reporting standards as this would facilitate transparent analysis and comparison of commercial mortgage loan performance regardless of the funding source. Discussion regarding the effective implementation date will be deferred until the second half of 2009

Page 4 CREFC IRP Version 6.0-Draft #1 – 1/9/09

once the XML standard is closer to being finalized. This XML transition is a revolutionary change from existing IRP standards that will provide concrete benefits and efficiencies to the industry as discussed in this document. The nature of this change will require additional detail and supporting documentation in the IRPx v6.0 standards document than what was included in previous versions to clearly explain the changes and new standards. This working Exposure draft document is the first of a series as comments and further discussion will result in revisions and changes to the XML standards. In addition, scheduled industry discussion conference calls are anticipated to review and discuss feedback received on this working Exposure draft to evaluate revisions to the new standards. Since subsequent versions of this working Exposure draft document will reflect any necessary changes that result, it is anticipated that multiple versions of the IRPx v6.0 Exposure draft will be released during this extended comment period. The tentative schedule for these conference calls and the working exposure draft release dates are as follows: January 12, 2009 Working Exposure draft version 1 published February 20, 2009 Deadline to submit comments/questions for March 6 conference call March 6, 2009 3PM EST Conference call to discuss version 1 feedback/questions April 10, 2009 Working Exposure draft version 2 published May 15, 2009 Deadline to submit comments/questions for discussion at June CREFC June 8, 2009 IRP Committee meeting to discuss version 2 feedback/questions July 2009 Final Exposure draft published

Application and Benefits of XML

As previously mentioned, the new XML standard will result in the move from the existing Excel based delivery approach (CSV data files, Excel file supplemental reports and the remittance template) to an XML data file delivery approach. The conversion of the CREFC IRP from Excel to XML will incorporate the primary CMBS reporting dataset into MISMO’s mortgage industry data standards. The XML data file will be essential to support continued growth and liquidity within the secondary market through standardization that provides investors and rating agencies more consistent and reliable information. Further, this provides greater efficiencies, due both to the inherent benefits of XML and the explicit benefits of a standardized commercial mortgage vocabulary and data model. Finally, additional benefits include enhanced transparency and security for aggregating and transmitting data and the ability to easily add new data elements as required. The new XML standard should be utilized whenever the reporting requirements in a servicing agreement call for reporting in accordance with the CREFC IRP. In some servicing agreements, the reporting requirements define the CREFC IRP “as it may be modified from time to time.” While it is expected the CMBS marketplace will adopt the new CREFC IRP XML reporting standard, to the extent that a particular servicing agreement requires different reporting formats or different methodologies, the user should adhere to the terms of that servicing agreement. Users of the CREFC IRP should be

Page 5 CREFC IRP Version 6.0-Draft #1 – 1/9/09

advised that the data contained within the CREFC IRP XML data files do not take into account every different servicing agreement and securitization structure. It is the responsibility of the user to understand the structure of particular transactions and utilize the data files provided accordingly.

Delivery of data using XML The new XML standard will require servicers to deliver XML data files rather than a combination of data files and supplemental reports/templates. The frequency of delivery of XML data files will vary depending on the structure of the related servicing agreement. Generally, the following standards should be followed for delivery by the Servicer to the Trustee:

• A Setup File transmission will be sent prior to the initial reporting cycle. This file will only include the fields that are included in the existing IRP 5.0 setup file.

• On a monthly basis, one (1) XML data file transmission should be sent. This delivery date of

this single file will depend on the specifics of the servicing agreement, but should be the earlier reporting date if the servicing agreement required multiple submissions consisting of an initial Loan Periodic Update File as of the determination date followed by a collateral file. If the initial XML file requires a revision, the entire XML data file should be resubmitted after discussion and agreement with the Trustee. It should be noted that the earlier delivery of the property and collateral information under this single file approach means that the servicer will lose a few days that may have been previously used to process additional property and collateral information. This can be offset by the servicer moving up their property and collateral review schedule and/or a delay in reporting that information until the following month. Since this only relates to a couple of days of processing time, it is not expected to have a material impact.

While the existing IRP defined Master Servicer to Trustee reporting standards, IRPx v6.0 has been expanded to also include 1) new Subservicer to Master and 2) Special Servicer to Master Servicer XML reporting standards. This will facilitate the timely transmission of subserviced and specially serviced loan information to the Master Servicer and ultimately to the Trustee and Investors. The specific delivery dates of these files will depend on the related subservicing agreement and/or PSA and may be subject to discussion between the Master and Subservicer or Special Servicer. While this requirement may not be specifically detailed in existing servicing agreements, it is expected that Subservicers will provide these files to facilitate the Industry’s move to this new standard since not doing so would complicate the Master Servicers ability to deliver IRPx v6.0 compliant files. Additional fields were added to the XMLx v6.0 schema to facilitate the electronic transfer of information from the Subservicer to the Master Servicer. As a result, Subservicers will be expected to provide an IRPx v6.0 compliant XML file to the Master Servicer monthly. In addition, a new Special Servicer to Master Servicer XML reporting standard was developed to facilitate the electronic transfer of specific information for specially serviced mortgage loans from the Special Servicer to the Master Servicer. This will require the Master Servicer to develop a process to capture the information contained in these files into their system. This will facilitate the Master Servicer’s ability to generate an XMLx v6.0 compliant file for each CMBS deal by combining the appropriate information from the subservicer and Special Servicer with other information maintained by the Master Servicer.

Page 6 CREFC IRP Version 6.0-Draft #1 – 1/9/09

In addition to the new XML standard, CREFC will develop an IRP XML Reader (the “Reader”), a tool that that will provide a standardized method of reading, parsing and presenting the data contained in the IRP XML files. The Reader was designed to 1) work exclusively with the MISMO XML standard for the CMSA IRP, and 2) bridge the gap created by the move away from the delivery of files and supplemental reports/templates via Excel to the XML data file standard. As of the publication of working Exposure draft version 1, the RFP for the creation of the reader was not complete. While it is anticipated to have certain functionality as discussed below, those specifics were not yet available and will be updated in working Exposure draft version 2. The Reader will present data in the XML data file as well as perform certain calculations that were previously performed by the Servicer in the generation of the Excel based supplemental reports using data in the XML file.

Future Changes The CREFC IRP Committee will continue to periodically review and update as necessary both the data included in the XML document and the content of the standard IRP reports generated by the Reader using the existing IRP change process. Under this change process, the CREFC IRP Committee collects questions, comments, suggested changes and enhancements every year and solicits feedback from its members to develop any necessary IRP changes. In addition, subcommittees are formed to address more significant reporting issues or committee projects. The working copy for changes to the IRP is the Change Matrix. The CREFC IRP Committee will take all the comments and suggestions under advisement and issue modifications to the IRP on an as needed basis, not necessarily annual. The Change Matrix will be distributed as needed to the entire working group until finalized.

Summary of IRPx v6.0 Changes to the CREFC Investor Reporting Package

As stated above, the goal of this CREFC IRP change was to develop the XML standard using the existing IRP v5.0. However, there were additional changes necessary to either 1) better align with an existing MISMO data field or 2) to comply with other changes occurring in the industry. There were no changes to supplemental reports or templates. The necessary changes, which are detailed on the attached Change Matrix include, but are not limited to, the following:

• The IRP v5.0 Legend provided descriptions to various codes or abbreviations included in the

IRP data files and reports. In an XML schema (or data layout), legends are replaced with enumerations (or listings) that result in the use of a more descriptive field name as well as providing some sort of description.

• Previous versions of the IRP only provided Master Servicer, Special Servicer, and Trustee

reporting standards. IRPx v6.0 incorporates XML reporting standards for the electronic transfer of information from both the Subservicer and Special Servicer to the Master Servicer to facilitate the Master Servicer’s delivery of their XML files.

• Most CMBS transactions define certain restricted reporting standards in the servicing

agreement based on standard IRP data files and reports. While this may impact the efficient delivery and data transparency benefits provided by XML, the XML schema will need to address this restriction requirement. One solution that has been discussed involves the encryption of the data that should be restricted under the servicing agreement. Under this approach, the user of a standard IRP XML file would not be able to view the restricted

Page 7 CREFC IRP Version 6.0-Draft #1 – 1/9/09

information in that file without the decryption key. This issue is still under discussion and will be updated in the next exposure draft update. Please provide any feedback or suggestions you may have on this topic.

• Previous versions of the IRP required the Master Servicer to deliver fields that were derived

from other fields included in the data files (i.e. calculated fields). The XML schema changes this as certain calculated fields will remain in the XML file delivered by the Master Servicer while others will be calculated by the Reader.

• The MBA has developed a standard property inspection form that has been accepted by CREFC

for property inspection reporting purposes. The MBA issued a revised inspection form in May 2008 that introduced the use of a primary and secondary property type for property classification. This required a change to the single property type classification previously used in IRP v5.0. This new form also adopted a 5 scale numeric based property assessment rating which differed from the 4 scale terms used in the IRP. Interim guidance was provided by CREFC that mapped the 5 scale numerical assessment to the terms used in the IRP. It is anticipated that additional discussion on adopting the numerical scale in IRPx v6.0 will occur during the comment period. See the CREFC website under Industry Standards, CREFC Investor Reporting Package for additional details on the interim guidance.

Page 8 CREFC IRP Version 6.0-Draft #1 – 1/9/09

IRPx v6.0 Analysis Since the IRP is so well-established, there are many people throughout the CMBS industry who are intimately familiar with all of the intricacies of the IRP. Since adoption of MISMO’s standards in commercial finance is only just beginning, there is a lack of familiarity with XML. The initial reaction of many IRP users to IRPx v6.0 will likely be “What the heck is this?” This analysis is intended to alleviate all concerns about the content and usability of IRPx v6.0, and also to introduce business users to MISMO’s proven approach to data and information. Before the new IRP is reviewed, there are three key facts that must be communicated. The first thing a business user needs to understand is that, irrespective of appearances, all of the content of IRP v5.0 has been carried over to IRPx v6.0. There are only a handful of new data points introduced in IRPx v6.0. The overall effort of the MISMO CREFC IRP Workgroup in its work to convert from flat files to XML has been to use substantially the same content in the new version. The second key fact is that MISMO XML provides a highly structured approach to data. Upon initial review, this structured approach may seem very complicated. It is because this structured approach requires a dramatic shift in the understanding of data that the MISMO Workgroup chose to add only a few new data points to IRPx v6.0. The migration to structured data will initially be complex enough without adding new information. The third key fact is that the migration to XML is entirely worth the effort. Once the shift to using structured data has taken place, business users from servicers, trustees, ratings agencies and investors will absolutely see the benefit, the value and the potential of this migration. The Difference Between Flat and Structured Data Using Excel for IRP v5.0 is based on a flat approach to data. The basis of flat data is the name-value pair. The best way to describe this is with real-world examples. In IRP v5.0, the Loan Periodic Update data file establishes a data point named “Actual Balance.” Actual Balance is defined as

“Outstanding actual balance of the loan as of the determination date. This figure represents the legal remaining outstanding principal balance related to the borrower’s mortgage note. For partial defeasances, the balance should reflect the appropriate allocation of the balance prior to the defeasance between the non-defeased and defeased loans based on the provisions of the loan documents.”

In IRP v5.0, the name-value pair is “Actual Balance” and the amount (say, $5,123,987.66). This is critical information, and the IRP unambiguously establishes it. This information should be perfectly understood by any analyst and it can be retrieved from any servicing system. There is another way to look at data – through its relationships with other information. For instance, “Actual Balance” is unambiguously one component of a larger group of information called “Loan Data.” Loan Data can include information about the loan terms, the various balances, features such as reserves and lockboxes and the characteristics of interest rate changes. Looking at data in this way establishes a hierarchy of relationships. A “Loan” contains “Loan Term” data, “Loan Attribute” data, “Balance” data, “Rate Change” data and so forth. Consider the vast amount of information contained in the IRP. There is property data, loan data, borrower data, servicer- and trustee-specific data and bond data. All this information is stored in and produced by systems, all of which in turn rely on internal data structures. One of the serious issues with the flat file IRP is the difficulty of extracting structured data and inserting it into an unstructured

Page 9 CREFC IRP Version 6.0-Draft #1 – 1/9/09

format in a way that users can rely on it. This requires effort by producers of data to comfort the information and ensure that it is reliable. Moving to a structured format for the IRP will increase the efficiency with which this is done. It will also improve the ability to incorporate new data requirements. Currently, implementing incremental changes to the content of the IRP requires significant testing and programming work. Servicers have to identify where in their systems the desired data is located and build processes to extract it and insert it into the Excel spreadsheet at the exact spot where it is required. Eliminating the traditional flat spreadsheet and using a structured data file instead will dramatically reduce the complexity and effort involved. The MISMO Approach to Data MISMO has established a comprehensive way to structure information for commercial real estate finance. The fundamental value of this is a uniform method for arranging of data for commercial loans regardless of type or execution. By creating a single data model that is usable for all loans, MISMO has solved the problem of how to send and receive information electronically whether the information is used to report on a group of loans that have been contributed to a CMBS issuance, the origination of an individual agency loan or the management of a portfolio loan that has gone into default. MISMO uses XML (eXtensible Markup Language) as the manner by which loan information is transmitted because XML operates very, very well in a structured environment. The core of the MISMO data model is the “Deal” structure. A Deal is essentially a single container that holds three basic groupings of data: Loan data, Collateral data and Party data (a Party is any entity involved in the transaction, such as a borrower, servicer or trustee). It simplistically looks like:

The Loan, Collateral and Party containers in turn hold containers of related data, in groups of ever-increasing specificity until you get to the specific data in question. For example, information about the Phase 1 report for a property securing a CMBS loan would branch off the Collateral container as follows

Page 10 CREFC IRP Version 6.0-Draft #1 – 1/9/09

One extraordinary benefit of this approach to data is the ability to seamlessly incorporate complex structures. Take, for instance, a loan secured by three properties. Using a flat structure to capture the information on the three properties is manageable but cumbersome. How does one tie together information about these three properties? Is there a master spreadsheet that summarizes the information from each individual spreadsheet for a property, or is there an alternate method? XML provides the capability to accomplish this easily through its technical features, and MISMO simplifies this by setting forth a uniform way of representing these relationships. MISMO works hand in glove with XML. There is one more threshold concept that is very important for the MISMO approach to data. Not only does MISMO structure data in a way that makes sense to a finance professional, it also normalizes the data. Let’s go back to the concept of “Actual Balance” used previously. A loan can have many different types of balances over its life: Original, Actual, Scheduled, etc. If you tracked the different balances over time, you could realistically have a huge number of balances: January 2009 Actual Balance, January 2009 Scheduled Balance, February 2009 Actual Balance, February 2009 Scheduled Balance and so on. If you are looking at identifying individual name-value pairs, this can quickly become overwhelming for an individual loan, much less a portfolio of loans or over many portfolios of loans. Normalization changes the rules. Rather than identifying a specific data point, normalization provides you the method to identify a category of similar data points and to simply describe them in a consistent way. Rather than looking for the January 2009 Actual Balance needle in a haystack, normalization establishes that there is a group of haystacks called “Balances.” One of these haystacks contains only Principal Balance data points, and each data point has a set of labels that identifies the characteristics of that data point – date, type, and amount. Structuring information in this way makes it much easier to find the January 2009 Actual Balance. If this type of organizational structure seems like overkill, consider the vast volume of loans serviced by an institution. Large numbers of loans require a simple yet robust method for consistently accessing information. Normalization solves this problem. *Important Note: Normalization of data is not the same as normalization of Net Operating Income. MISMO does not issue standards for normalization of financial statements. MISMO and the IRP

Congratulations and thank you for making it this far through the narrative. We’ve tried to reduce the technical jargon and complexity to the minimum necessary to understand the differences between IRP v5.0 and IRPx v6.0. Going forward, we will be able to use real world examples to describe the new

Page 11 CREFC IRP Version 6.0-Draft #1 – 1/9/09

IRP. Remember that the substance of IRPx v6.0 is unchanged from IRP v5.0 – only the way the information is relayed has changed. Consider a loan with an A-B-C note structure. IRP v5.0 sets forth several specific data points for multi-note loan structures: A-Note Debt Service B-Note Debt Service C-Note Debt Service A-Note Paid Through Date B-Note Paid Through Date C-Note Paid Through Date A-Note Scheduled Loan Balance B-Note Scheduled Loan Balance C-Note Scheduled Loan Balance This information is found in IRPx v6.0, but instead of relying on a few specific data points they are instead embedded in the normalized structure. Each loan (the A, B and C pieces) will have its own LOAN container. Each Loan container (A, B or C) can hold the full range of loan information set forth in the IRP such as Loan Terms, Loan Attributes or Balances. In each LOAN Container, there is a child container called LOAN_ATTRIBUTES. There is an element (data point) in LOAN_ATTRIBUTES labeled “CMSALoanStructureType” (Note that there are no spaces in a MISMO XML label). The only valid inputs for this field are those set forth in the Loan Structure Legend in IRP v5.0. These are the enumerated values

WholeLoan SplitLoanWithPariPassuDebtOutsideTrust ANoteInABParticipation BNoteInABParticipation ANoteInABCParticipation BNoteInABCParticipation CNoteInABCParticipation MezzanineDebt.

The subject loan will be identified by its appropriate enumerated value. This means that all data in this LOAN Container are of the type described. In addition to LOAN_ATTRIBUTES, the LOAN Container has other child containers all of which hold specific data points. One such container is LOAN_PERIODIC_STATISTICS, and in that container is a data point called “SubjectLoanAnnualDebtService” and it is here where the “Note Debt Service” data in IRP 5.0 is found. In this same container there is another data point called “PaidThroughDate” and it is here where the “Note Paid Through Date” data in IRP 5.0 is found. Lastly, there are several related data points to determine “Note Scheduled Loan Balance.” The LOAN Container has yet another child container called BALANCES. The actual A, B or C Note Scheduled Balance would be input into the data point called “BalanceAmount.” But remember the concept of data normalization. A balance is a generic data point until it is identified. This identification is accomplished by selecting the appropriate description from the corresponding enumerated list in the data point “BalanceType.” There are 40 different balance types used in the IRP, and the appropriate one in this case is “CurrentEndingScheduledPrincipalBalance.” This illustrates two important points. First, every single data point in IRP v5.0 can be mapped to a corresponding data point (or set of data points) in IRPx v6.0. In some cases, there are some additional steps involved. This leads to the second point. By changing to a structured, normalized data format it is easy to see how data transparency is improved. It is possible to provide more information than is required in the current version of the IRP. In the case of an A-B-C deal, the path is clear for providing detailed information about each loan’s structure and terms. The decision to do so in the future will be

Page 12 CREFC IRP Version 6.0-Draft #1 – 1/9/09

CREFC’s, which is the owner of the IRP and which has the organizational structure to balance the needs of investors with the capabilities of servicers.

Page 13 CREFC IRP Version 6.0-Draft #1 – 1/9/09

Transition from IRP v5.0 to IRPx v6.0

As mentioned earlier, the IRPx v6.0 document will contain much more information than previous versions due to the nature of the transition to XML. These changes can be summarized by comparing the table of contents for these documents:

IRP v5.0 IRPx v6.0 I. Overview Same II. Change Matrix Same III. IRP legend Replaced by enumerations in XML schema IV. IRP Data Dictionary Included in the XML schema V. Data files Included in XML schema and discussed below VI. Supplemental Reports See below. Examples included in document VII. CMSA/MBA Methodology… Unchanged VIII. Disclosure templates See below. Examples included in document IX. Guidance for Specific situations Unchanged Frequently asked questions section is new CREFC Data Files IRP v5.0 presented information in two different formats: electronic data files and reports (supplemental reports, reports for operating statement analysis, and templates). The IRP v5.0 data files will be included in the XML data standard as follows:

1. CREFC Loan Setup File - Setup XML File transmission (only including those fields not included in the monthly XML data transmission) sent by the Servicer to the Trustee

2. CREFC Loan Periodic Update File – Part of the single, combined XML monthly data transmission sent by the Servicer to the Trustee

3. CREFC Property File – Part of the single, combined XML monthly data transmission sent by the Servicer to the Trustee

4. CREFC Financial File – Part of the single, combined XML monthly data transmission sent by the Servicer to the Trustee

5. CREFC Special Servicer Loan File – A single, monthly XML data transmission sent by the Special Servicer to the Servicer. The fields from this file are included in the ??, ?? data element containers.

6. CREFC Bond Level File – Part of the single, monthly XML data transmission sent by the Servicer to the Trustee. The fields from this file are included in the Bond_Periodic, Bond_Balance and Bond_Ratings data element containers.

7. CREFC Collateral Summary File – Part of the single, monthly XML data transmission sent by the Servicer to the Trustee. The fields from this file are included in the Trust, Trust_Periodic_Statistics_detail data elements containers.

The Reader will generate these IRP v5.0 data files from the XML files in addition to supplemental reports as discussed below. Please see the XML Implementation and Business Process guide in this document for additional details.

Page 14 CREFC IRP Version 6.0-Draft #1 – 1/9/09

CREFC Supplemental Reports The IRP v5.0 supplemental reports include the following and will be available using the Reader:

1. Servicer Watchlist/Portfolio Review Guidelines 2. Delinquent Loan Status Report 3. REO Status Report 4. Comparative Financial Status Report 5. Historical Loan Modification and Corrected Mortgage Loan Report 6. Loan Level Reserve/LOC Report 7. Advance Recovery Report

All of these Reports will be available from the CREFC XML IRP Reader since all of the underlying data will be included in the XML file. The only CREFC supplemental that will not be available using the Reader in IRPx v6.0 is the Total Loan Report. The Total Loan Report will be a manual report transmitted by Master Servicers to the related Trusts. CREFC Supplemental Report Descriptions Although information needs may vary widely from one investor to another, the supplemental reports will continue to provide investors with a variety of ways to analyze and evaluate the current status of a particular loan, property and/or the overall portfolio. The seven (7) supplemental reports produced by the Reader in addition to the Total Loan Report, which will not be produced by the reader, fall into one of the following three categories:

1. Status Reports 2. Financial Reports (Debt Service Coverage Information) 3. Historical Information Reports

Note: All CREFC supplemental reports should continue to be as of the determination date.

Page 15 CREFC IRP Version 6.0-Draft #1 – 1/9/09

Status Reports Servicer Watchlist/Portfolio Review Guidelines This report represents loans that have an increased risk of default which could result in transfer to the Special Servicing. The Portfolio Review Guidelines (PRG) represent a list of criteria that can be applied systematically to determine whether a loan will be reported on the Servicer Watchlist and establish a release threshold that defines when a loan should be removed from the Servicer Watchlist. If a loan has triggered one or more items within the PRG, then the loan will be reported on the Servicer Watchlist. The PRG consist of the following six categories:

1. Financial Conditions 2. Borrower Issues 3. Property Condition Issues 4. Lease Rollover, Tenant Issues and Vacancy 5. Maturity 6. Other (Servicer Discretion)

Please note that watchlist comments need to be clear in regards to what period financials were used in driving the PRG’s since the raw data will be transferred by the Servicer in the XML file and the user may have some flexibility within the CREFC XML IRP Reader to present financial data for periods which may different from those used to determine whether the loan appears on the ServicerWatchlist. Delinquent Loan Status Report This report includes matured performing loans where the maturity date has passed without paying off and a monthly payment (assumed scheduled payment) is still being received from the borrower, matured non-performing loans where the maturity date has passed without paying off and a monthly payment (assumed scheduled payment) is not being received from the borrower, as well as those loans that are both current and specially serviced. Loans should only appear in one category. The report excludes REO Mortgage Loans. Information falls into one of the six (6) following categories as of the determination date:

1. Delinquent 90 days or more (not matured) 2. Delinquent 60-89 days (not matured) 3. Delinquent 30-59 days (not matured) 4. Current and specially serviced 5. Matured performing loans 6. Matured non-performing loans

REO Status Report This report contains the following information with respect to REO properties included in the Trust Fund:

1. Acquisition date of the REO property

Page 16 CREFC IRP Version 6.0-Draft #1 – 1/9/09

2. Value of the REO property based on the most recent appraisal or other valuation available to the Master Servicer as of the determination date. Loss using 90% of value should not be a negative number. If it is a negative number, it is a gain and should be reported as zero.

Loan Level Reserve/LOC Report This report displays common reserve account types, such as reserves for repair and replacement, tenant improvements, leasing commissions and debt service, as well as letter of credit (LOC) balances and expiration dates. Reserve balances “at contribution” are shown and the report provides the most recent monthly activity including reserve monies deposited and disbursed. A loan should only appear on the report if it has any ending reserves, LOC balances or activity. Advance Recovery Report This report monitors the reimbursement of workout delayed reimbursements (WODRAs) and other non-recoverable advances reimbursed to the Master Servicer through the use of “pool level” senior bondholder trust level principal. The report will present advance recoveries from pool principal and interest on a current and cumulative basis, and the cumulative payments by the borrower on the related advance obligation. Instances of the recovery of WODRAs and non-recoverables will appear on separate rows. Depending on the structure of the servicing agreement governing the loan and the underlying securitization(s), this report may not be feasible. The loans remain on the report until all principal is recovered or the loan is liquidated. Total Loan Report The concept of dividing loans and placing them in multiple transactions led to a need for a report to be prepared by the primary servicer of the aggregate of the pari passu loans (the “Total Loan”). The report will be disseminated by the lead Servicer to all the Master Servicers involved with each pari passu piece of the Total Loan and would be included in the monthly CREFC reporting for all transactions that have a pari passu piece of the Total Loan. The Master Servicer should provide this report to the Trustee of the underlying securitization of each pari passu piece outside of the XML data transmission. As in previous CREFC IRP’s, this report is not necessary if a single primary servicer does not exist for the Total Loan. Since each transaction may only have one of the pari passu pieces, the Total Loan Report may reflect loans that are not included in the Trust, but these are properly identified on the report.

Financial Reports (Debt Service Coverage Information) Financial reports provide information at the property level, comparing financial information such as the revenues, expenses or debt service coverage ratio (DSCR) as shown in the prospectus to more current financial information that has been received. The data should be normalized and may be annualized to allow an easy comparison from year to year. Comparative Financial Status Report (CFSR) PLEASE NOTE: The CREFC IRP Reader may provide additional flexibility to the creation of these reports. As a result, this section may change once the business specifications for the Reader have been

Page 17 CREFC IRP Version 6.0-Draft #1 – 1/9/09

developed. This is a monthly report that compares (if the information is provided by the borrower) among other things, the occupancy, revenue, NCF or NOI and debt service coverage ratio for a particular loan for each of three periods

1. Most recent available year-to-date or trailing 12-months normalized data 2. Prior two full fiscal years (separate consecutive and not combined years) 3. At contribution

The sections containing annual information ultimately roll off, leaving room for the new annual information by deleting the oldest year. The year-to-date or trailing 12-months section will also begin to show the new year-to-date or trailing information. Both the trailing 12-months information and year-to date information will be updated as new information becomes available. The rolling of property financial data on the Comparative Financial Status Report is important in the evaluation of property operating information and gives the viewer the ability to track trends at the property level from year to year. Since the Fiscal Year Operating Information report headings are not defined, there are two acceptable methods of handling the reporting of operating information on this report. This information should be normalized and may be annualized to allow for easy comparison from year to year.

1. Roll all financial data from the column entitled Most Recent Financial Information to the column entitled Preceding Fiscal Year, the data from the column entitled Preceding Fiscal Year to the column entitled Second Preceding Fiscal Year, and rolling off the third year on a specific date each year. Under this method, the Fiscal Year Operating Information columns would contain information for a particular fiscal year. By utilizing this method, the user can categorize the data for similar periods and track the servicers financial statement collection rates. The Most Recent column would begin to show the new year-to-date or trailing 12-months information as it becomes available.

2. Roll the financial data as mentioned above, however instead of rolling "all" the financial information on a specific date, the servicer could roll the operating data as information is received from the borrower and analyzed on each property. Under this method, the Fiscal Year Operating Information columns would represent the two most recent consecutive years for each property, rather than the same fiscal year operating information for all properties. Given these two options, you may have situations where the sub-servicer prepares this report one way, while the Master Servicer uses the other option. The two choices listed above provide the flexibility in this situation for the sub-servicer and Master Servicer to continue to prepare the report in the manner they prefer.

. The detail income and expense amounts which support the summary level amounts on the CFSR can be found on the Operating Statement Analysis Report. Operating Statement Analysis Report (OSAR) This is a property-level comparison of the borrower’s current financial information (year-to-date or

Page 18 CREFC IRP Version 6.0-Draft #1 – 1/9/09

trailing 12-month periods or interim statements received after the fiscal year end) to the three preceding annual periods and “at contribution.” The OSAR reflects standard revenue, expense, TI/LC’s, capital expenditure and debt service line items. (See CREFC/MBA Standard Methodology for Analyzing and Reporting Property Income Statements.) The OSAR information is provided by either the Master Servicer or Special Servicer for each property showing a comparison of the borrower’s operating statements. Operating information is “normalized” for all periods. Periods shown are:

1. At contribution 2. Prior three annual years “normalized” 3. Year-to-date or trailing 12-month information “normalized”

Each section (excluding “at contribution”) should contain the information for a particular year. The sections containing annual information ultimately roll off, leaving room for the new annual information by deleting the oldest year. The year-to-date or trailing 12-months section will also begin to show the new year-to-date or trailing information. Both the trailing 12-months information and year-to-date information will be updated, as new information becomes available. The Preceding Year column comes from the most recent annual NOI Adjustment Worksheet. NOI Adjustment Worksheet This report/worksheet reports and explains the adjustments made to “normalize” a borrower’s actual operating statement. This worksheet shows the difference between the borrower’s actual operating statement and the normalized operating statement. It shows the adjustments made to normalize a borrower's actual operating property-level numbers. The “normalized” numbers are then placed in the appropriate column of the OSAR and may be annualized as long as six months of data is available.

Historical Information Report Historical Loan Modification and Corrected Mortgage Loan Report This monthly report includes information regarding all loans that have been modified or for which the maturity date has been extended, both for the current period as well as for prior periods in addition to corrected mortgage loans. The report does not include loan assumptions or loans that are extended subject to pre-existing extension provisions in the loan documents. The following items are addressed in the report:

1. Realized losses (on a loan-by loan basis) incurred by the Trust as well as an estimate of potential losses because of an interest rate change.

2. Original and revised terms of all loans modified since “contribution.” 3. Corrected mortgage loans

If a loan has been modified in any way, it will appear only under the modified section and not BOTH modified and corrected (e.g. there does not need to be duplicate reporting on this report). The priority for presentation on the report is modified then corrected. CREFC Disclosure Templates

Page 19 CREFC IRP Version 6.0-Draft #1 – 1/9/09

The CREFC Disclosure Templates section of the IRP was added to include templates that reflect common servicing agreement calculations and events. CREFC Disclosure Templates are ONLY recommended or suggested formats and are not considered mandatory as these templates may not be applicable to all securitization structures and/or may be adapted for differences in structures. In addition to the CREFC Disclosure Templates, information on the current MBA inspection form accepted by CREFC is also provided below. Each of the templates should be prepared and delivered to the related trustee or investor, as applicable to the related securitization with the exception of the Servicer Remittance to Trustee. The Servicer Remittance to Trustee will be the only template viewable via an “enhanced” CREFC IRP Reader at this time. The templates are in suggested formats and may be modified to fit transactions with different requirements/calculations. The eight CREFC Disclosure Templates are as follows:

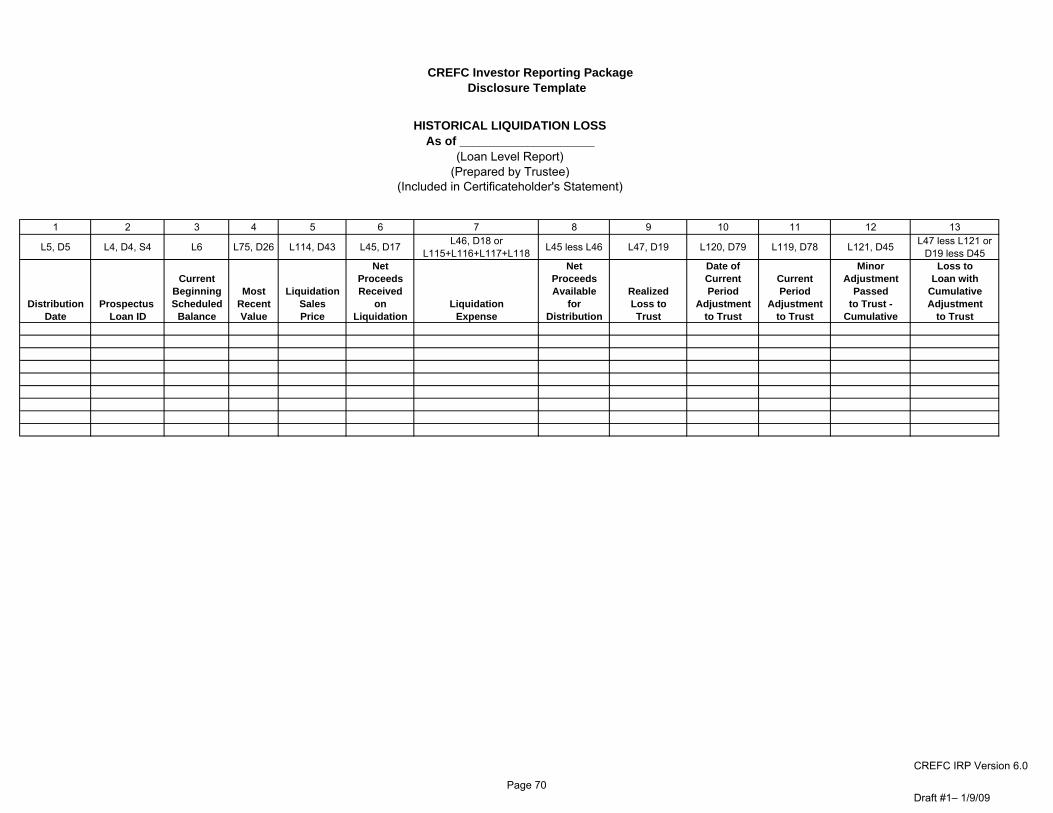

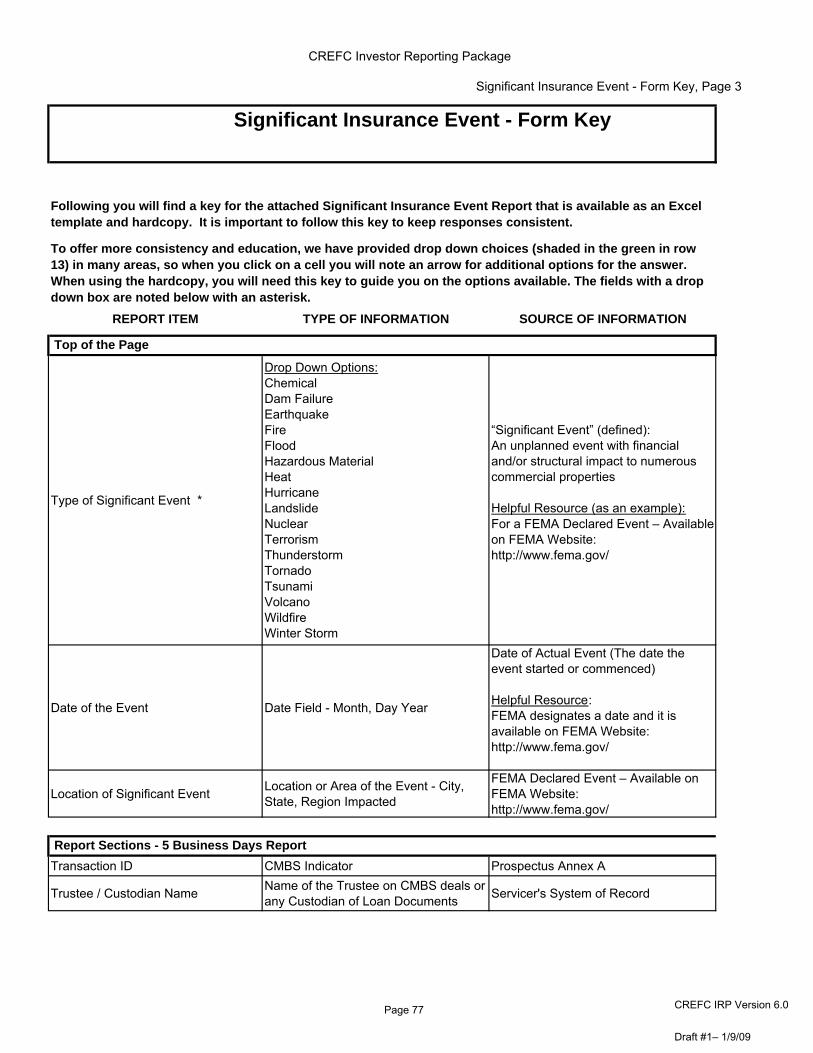

1. Appraisal Reduction (Servicer or Special Servicer) 2. Servicer Realized Loss (Servicer or Special Servicer) 3. Reconciliation of Funds (Trustee) 4. Historical Bond/Collateral Realized Loss Reconciliation (Trustee) 5. Historical Liquidation Loss (Trustee) 6. Interest Shortfall Reconciliation (Trustee) 7. Servicer Remittance to Trustee (Produced using the “enhanced” Reader) 8. Significant Insurance Event Report (Servicer)

Appraisal Reduction This template can be prepared by the servicer and will reflect the calculations of an appraisal reduction and the related ASERs. Servicer Realized Loss This template can be prepared by the servicer or special servicer and will reflect the calculations of a realized loss at the loan level. When a loan incurs a Current Period Adjustment to the Trust, the ‘Notes/Instructions to MS and Trustee’ field can be updated by the Special Servicer to include a description of how the funds are being categorized at the loan level. For each adjustment, this field can include the description Principal Recovery, Principal Loss, Additional Proceeds, or Additional Expense. This will provide direction to the Master Servicer and Trustee as to how the adjustments are being applied. Reconciliation of Funds This is a monthly template prepared by the Trustee. It is based on loan level information provided by the Master Servicer and bond level information determined by the Trustee. The purpose of the template is to reconcile the funds collected by the Master Servicer reduced by fees, advances, etc. to the funds distributed to the investors/certificateholders by the Trustee. Historical Bond/Collateral Realized Loss Reconciliation

Page 20 CREFC IRP Version 6.0-Draft #1 – 1/9/09

This template will be prepared by the Trustee and will reflect reconciliations of the differences between bond losses and loan losses. The losses may result from the timing of realizing a loss or applying the loss to principal versus interest. Historical Liquidation Loss This template will be prepared by the Trustee and replaces the Historical Loan Liquidation Report that was previously prepared by the Servicer as reflected in earlier versions of the IRP. Interest Shortfall Reconciliation This template will be prepared by the Trustee. Servicer Remittance to Trustee This is a monthly template will be viewable by both the Master Servicer and Trustee using an “enhanced” reader” using data from the XML data file transmission. This template will provide summary level information for the funds being wired to the Trustee. The purpose is to provide a consistent and thorough categorization of the funds being passed to the Trust so that the Trustee can determine how to apply those funds. In addition to the format presented herein, it is also acceptable for Master Servicers to provide the data in a format similar to the Reconciliation of Funds template, so long as the necessary data points are included and the field names are consistent. Significant Insurance Event Report In an effort to provide standardized reporting of insurance information in connection with possible property damage resulting from a significant natural disaster or similar event, the Mortgage Bankers Association (MBA) has developed a Significant Insurance Event Report. CREFC has decided to incorporate this standard report format into the IRP as a disclosure template. This will facilitate consistent delivery of information to all stakeholders. The Master Servicer is responsible for providing the report to the Trustee for all Master Serviced CMBS loans under the schedule provided on the Significant Insurance Event Report included in the CREFC Disclosure Template section. Additional information on the condition of the properties and the extent of any damage will be included on the watchlist report using the Portfolio Review Guidelines. The timing of this information on the Watchlist is dependent on a number of factors including the extent and nature of the damage, and the servicers ability to contact the borrowers. This will require that the Master Servicer obtain the same standardized reporting from any sub-servicers. The adoption of this standard report across the industry will facilitate this effort. Property Inspection Form The MBA has developed a standard property inspection form that has been accepted by CREFC for property inspection reporting purposes. While not typically a required reporting item, the form is available for the servicer and special servicer’s use and is provided via the CREFC website. For the

Page 21 CREFC IRP Version 6.0-Draft #1 – 1/9/09

current version of the inspection form, please visit the CREFC website at www.crefc.org and click on “Industry Standards”. The form can be found under the sub-section entitled “Standard Forms”.

Page 22 CREFC IRP Version 6.0-Draft #1 – 1/9/09

NOTE: The following sections provide information that was provided in IRP v5.0. It was unclear at publication whether or how this information would be included in IRPx v6.0. Consequently, it appears here for further discussion. XML GUIDANCE SECTION Servicer XML Data File Guidance Need to address how the following will be handled in the XML data transmission. How can the user reference the old data file fields via the new data dictionary in order to be clear on this guidance? 1. For Setup File data…what parts of this original language still applies if we are not yet sure what this file will contain? This data file is generally provided by the Master Servicer using information that is prepared by theunderwriter at the time of issuance. This file generally contains static information. The underwriter should provide the CREFC Loan Setup File and the “at contribution fields” or “static fields” in the CREFC Property File to the Master Servicer. In addition, the underwriter should provide the revenue and expense line items utilized to derive Net Operating Income (NOI) and Net Cash Flow (NCF) since these are needed to complete the underwriting column of the OSAR. However, at times this does not happen, and the Master Servicer should create this file using loan files and whatever other information is available. The file may be made available to investors by the Trustee on its web site. The Loan Setup File will contain the majority of the loan-level information found in the prospectus. Such information includes cut-off balance, original note rate, maturity date and general prepayment information, as well as “at contribution” financial data. 2. When a loan pays off (or is repurchased or substituted), it will stay on the file with a zero balance effective with the 4.0 release. Loans liquidated on or after the effective date of version 4.0 will remain on this file. 3. At the loan level, how will this section be handled… Servicers can elect to backfill loans liquidated prior to that date, although not required. Fields L6 'Current Beginning Scheduled Balance' and L7 'Current Ending Scheduled Balance' should be zero. Other fields which must be populated include L1, L2, L3, L4, L5&, L29, L32, L41, L42, L43, L44, L45, L46, L47, L109&, L114, L115, L116, L117, L118, L119*, L120*, L121& and L124&. (Notes: The two fields marked by an asterisk “*” are fields that should be updated only during a period when there is an adjustment, and will be populated for that month only. If there are no subsequent adjustments, these two fields should remain blank. The fields marked with a “&” are fields that may change subsequent to the payoff (or repurchase or substitution). The remaining fields listed should remain static as of the month of liquidation.) 4. CREFC Property File - For property data…what parts of this original language still applies for property data? This data file is always produced, both when a transaction has one loan for one property and when a transaction has multiple properties as collateral for one loan. The underwriter should provide “at contribution or static fields” within the Property File to the Master Servicer and Trustee. The Master Servicer should also furnish an updated file to the Trustee each successive month or as required by the servicing agreement. The file data can change over time for many fields. Major file changes may occur if a loan allows for substitution of different properties as collateral for a particular loan. Further discussion of issues affecting the Property File including defeasance, partial defeasance, substitution and partial releases can be found in Section IX – Guidance for Specific Situations.

Page 23 CREFC IRP Version 6.0-Draft #1 – 1/9/09

Page 24 CREFC IRP Version 6.0-Draft #1 – 1/9/09

5. CREFC Financial File - How do the 4 property types drive the OSAR/NOIWS and use the right template. This data file provides line-by-line revenue and expense detail for various property types in order to facilitate analysis and reporting for issuers, investors and potential investors. The file is useful for making comparisons between individual properties within a transaction regarding operating performance as well as for making comparisons across various transactions. Not only can performance be monitored on a current basis, but a property’s ongoing performance can also be compared with its status at the time of original underwriting and for prior annual periods. The Financial File is prepared by the Master Servicer and sent to the Trustee on a monthly basis. (See Financial File Overview for additional detail regarding frequency of preparation and submission of the file). 6. CREFC Special Servicer Loan File - This data file is prepared by the Special Servicer and delivered to the Master Servicer. The purpose of the file is to electronically transfer data for Specially Serviced Mortgage Loans and REO data in a consistent format from the Special Servicer to the Master Servicer. The file will not include any financial statement fields from the Special Servicer to the Master Servicer since the assumption is that the Master Servicer performs the financial statement analysis. This data file is not sent to the Trustee. When a loan pays off (or is repurchased or substituted) it will stay on the file with a “liquidation/ prepayment code.” For all loans liquidated on or after the effective date of version 4.0, the Special Servicer should keep all loans on this data file. Special Servicers can elect to backfill loans liquidated prior to that date, although not required. The following data fields are the only data fields that should be populated (either to remain static or to be updated in the event of adjustments to realized loss) starting the month after liquidation: D1, D2, D3, D4, D5* (updated monthly), D7, D8, D13, D15, D16, D17, D18, D19, D43, D45*, D70*, D71, D72*, D74, D75, D76, D77, D78*, D79* and D80*. (Note: Those fields marked by an asterisk * are fields that should be updated in any month when there is a future adjustment, as applicable. The remaining fields should remain static as of the month after liquidation.) Additionally, at the special servicer’s option, fields D47 through D52 (the comment fields) can be populated with a comment explaining the liquidation of the asset. This comment may also be updated in the event any significant adjusted loss is passed through, but would otherwise be expected to remain static. 7. Are we going to add guidance on the Subservicer XML data file? Trustee XML Data File Guidance 1. CREFC Bond Level File – This data file is prepared by the Trustee and consists of updated monthly information on the bonds. This file reports such items as updated bond balances, the amount of interest and principal received on the bonds, and other information typically contained in a statement to certificateholders. It also contains bond ratings whenever provided by the rating agencies to the Trustee. 2. CREFC Collateral Summary File– This data file is prepared by the Trustee utilizing information provided by the Master Servicer. This file consists of updated information on the collateral in a transaction such as principal balances or delinquency information. It summarizes the information found in the monthly statement to certificateholders.

II. Change Matrix

f

Page 25 CREFC IRP Version 6.0-Draft #1– 1/9/09

– 1/9/09Ed

CREFC Investor Reporting Package - Change Matrix IRPx v6.0 DRAFT

Item No.

CREFC Data Files/ Reports/Templates

Discussion Topic Source Comments presented for initial discussion IRPx v6.0 Determination for 1st Exposure Draft

1 General New format of files and method of delivery

IRP group, continuous discussion

Microsoft Excel .xls or .csv files will no longer be the standard format of files and they will no longer be delivered in their current form of separate files for Property File, LPU, Setup File, etc.

The new standard will require servicers to deliver files in XML format in a single transmission.

The nature of the new IRPx 6.0 which will be delivered in an .XML format is significantly different than prior IRP versions that have been delivered in a series of .csv, .txt or Excel files. Please refer to the IRPx 6.0 package (including Narrative) for explanation.

2 general New addition to IRP Spring 2008 teleconferences by sub/master workgroup.

Provide a standard transmission package for use between subservicers and master servicers.

IRPx v6.0 incorporates a XML reporting standard for Subservicer to Master Servicer to facilitate the Master Servicer’s delivery of their XML files. As a result, the subservicer will be expected to provide an IRPx v6.0 compliant XML file to the Master Servicer monthly and the Master Servicer will need to develop a process to capture the information contained in these files into their system. Please see the discussion in the IRPx 6.0 Narrative for additional detail. The Sub to MS transmission will be same as regular MS transmission, except for adding the following fields that are unique to the Sub to MS transmission only: Actual Gross Interest Collected/Remitted Actual Net Interest Collected/Remitted Principal Collected/Remitted Actual Primary Servicing Fee Actual Additional Primary Servicing Fee Net Interest Payment Late Charges Assumption Fees Default Interest Additional Fees Collected Date Payment Received Next Payment Due

3 General all fields populated with Y/N January 29-30, 2008 meeting in Chicago

Y/N not optimal for XML Change all fields requiring a Y/N entry to YES/NO

4 General Calculated fields January 29-30, 2008 meeting in Chicago

Remove fields from IRP XML transmission that are calculations where elements of the calculation are already provided. Define calculations in the DD and have Reader calculate the fields.

The results for any field that is derived from a calculation of other data fields within the XML file will either be included in the Servicer submission or calculated within the Reader. If the field is included in the XML data file, the schema will define the data element and how it is derived. If the calculated field is not included in the XML schema, it will be calculated within the Reader and noted in the XML schema as a calculation. There are two types of calculations--calculations that combine other data elements and calculations that take property level information and roll them up to the loan level for loan level reporting. Both are noted below.

The preliminary list of calculations are: Total Principal Distribution: The calculation is "Scheduled Principal Amount (B9) plus Unscheduled Principal Collections (B10)" Total Scheduled P&I Due: The calculation is "Scheduled Interest Amount (L23) plus Scheduled Principal Amount (L24)" Net Rate: The calculation is "Note Rate (L10) less the sum of the Fee Rate/Strip Rates 1 through 5 (fields L12 through L17)" Number of Properties: (for rolling multiple properties to loan level) The calculation is intended to automate a count of reported properties. Balloon (Yes/No): The calculation is "if Original Term of Loan (S6) = Original Amortization Term (S7), populate No, else Yes". Most Recent Value: The calculation is intended to review each value presented and include the value associated with the most recent date in this field.

5 General Restricted versus Unrestricted Data

IRP group, continuous discussion

Many PSAs require that some information be classified as Restricted Reports but the PSA refers to the files as they exist in v5.0. With our transition to IRPx6.0, there will be one data file and restriction of certain information is more complex.

This item requires further discussion and remains outstanding.

CREFC IRP Version 6.0-Draft #1– 1/9/09

CREFC Investor Reporting Package - Change Matrix IRPx v6.0 DRAFT

Item No.

CREFC Data Files/ Reports/Templates

Discussion Topic Source Comments presented for initial discussion IRPx v6.0 Determination for 1st Exposure Draft

6 Special Servicer Loan F Entire file January 29-30, 2008 meeting in Chicago

Some fields require reporting of information at property level instead of loan level, however, all fields have always been reported by the SS at loan level.

Create separate data transmission between SS and MS.

There have been 2 main issues with the SS Loan file which can be addressed with our transition to XML. First, the SS Loan file has always been a combination of fields that should be reported at the property level (eg "REO Date") and others that should be reported at the loan level. Since only one file has been required, the SS has always reported at the loan level. The second issue is that some of the fields reported by the SS are incorporated by the MS directly into the LPU or Property File while others are added to what the MS has to report (e.g. Other Advances could be a combination of what the SS has outstanding and what the MS has outstanding). This represented a difficulty in attempting to add the SS Loan File fields to the schema when there is overlap with fields that are also reported by the MS. The committee identified all of the fields that would be required in this transmission. For now, these fields were incorporated into the overall schema which would result in this data being included in the Master Servicer transmission to the Trustee and Investors. HOWEVER, this remains an outstanding item as there are a number of questions that need to be discussed on this approach including: · Should the required Special Servicer data set be a separate smaller XML schema that will only occur between the SS and MS? If so, we will need to dev · Should the required Special Servicer data set be included in the overall Master Servicer schema?

7 Special Servicer Loan File (or new SS to MS transmission)

Date Asset Expected to be Resolved or Foreclosed (D31)

June 2008 teleconference where the SS to MS transmission was defined/developed.

Change definition Change definition to allow for this field to remain blank (as some special servicers currently do) in the event there is no reasonably firm projection of the date of resolution or foreclosure."Estimated date the Special Servicer expects resolution. If multiple properties, print latest date from the affiliated properties. If in foreclosure = expected date of foreclosure and if REO = expected sale date. If the Special Servicer does not have a reasonably firm estimation of projected resolution, this field may be left blank"

8 Data Dictionary Add definitions January 29-30, 2008 meeting in Chicago

Add definitions for fields occuring only on Supplemental Reports The data dictionary developed through IRP v5.0 included definitions for every data file field and some Supplemental Reports but not all fields on Supplemental Reports. New definitions have been developed.

A final list of these new definitions is under development and will be included in a later version of this exposure draft.

9 Data Dictionary Reimbursed Interest on Advances (L107)

January 29-30, 2008 meeting in Chicago

Change definition L107 Reimbursed Interest on Advances 5.0 definition - Cumulative accrued interest on advances reimbursed to the servicer(s) for the current period pursuant to the servicing agreement.

Sugg IRPx definition - Interest on advances reimbursed to the servicer(s) for the current period pursuant to the servicing agreement. This amount will impact the cash flow to the Trust for the current period.

10 Legends Remove codes from Legend items

January 29-30, 2008 meeting in Chicago

Delete Legend Fields that require population from a pre-defined set of allowable entries will have an associated set of "enumerations" within the XML framework. In lieu of providing a legend similar to the form contained in IRP 5.0, each legend item has now been provided a definition and has also been given a "human readable" descriptor, rather than a code (i.e. Workout Strategy populated with a 1 was defined in the legend as "Modification". In XML, the field "Workout Strategy" will have an enumeration list associated with it that includes the various strategies and they will be labeled with the appropriate name (Modification) instead of a code (1).) Definitions have been provided for each legend item and they are now incorporated into the new Data Dictionary on the Enumerations tab. Detail on the legend codes translation to enumerations is included in the Attachment B to this change matrix.

11 Legend/enumerated fieldMost Recent Financial Indicator (L82, P75)

January 29-30, 2008 meeting in Chicago

Delete enumeration "TA" In the new list of enumerations (see CM item #11 above), delete the "TA" (Trailing Twelve Months Actual) option. This is not necessary under the methodology published in 4.1 and later versions which require that any TTM statements received must be normalized.

12 Legend/enumerated fieldDSCR Indicator January 29-30, 2008 meeting in Chicago

delete enumerations "A" and "W" In the new list of enumerations (see CM item #11 above), delete the "A" (Average) and "W" (Worst Case) options.

13 Legend/enumerated fieldProperty Condition (P89) March 2008 teleconferenChange definition of enumerations.

MBA Inspection form ratings as they translate to CMSA IRP ratings previously on the Legend, no change to the enumerations of "Excellent, Good, Fair, Poor" but the mapping needs to be incorporated into the definition

The new MBA Inspection form utilizes a numerical rating scale for the overall property assessment. CMSA published interim guidance in 11/2008 to advise users how to translate the new MBA rating scale (1 to 5) to the existing CMSA word scale (E, G, F, P). Please refer to the CMSA interim guidance for explanation (available on the CMSA website). Permanent guidance on the mapping vs. adoption of the new MBA numerical scale by CMSA IRP will be discussed by the committee for final determination.

14 Legend/enumerated fieldProperty Type (P13) May 2008 teleconferences and email discussions

Delete enumeration "Warehouse" In the new list of enumerations (see CM item #11 above), delete the "Warehouse" option. Warehouse will now be a Secondary Property Type under the "Industrial" Property Type.

CREFC IRP Version 6.0-Draft #1 – 1/9/09

CREFC Investor Reporting Package - Change Matrix IRPx v6.0 DRAFT

Item No.

CREFC Data Files/ Reports/Templates

Discussion Topic Source Comments presented for initial discussion IRPx v6.0 Determination for 1st Exposure Draft

15 Loan level information New field - "Trustee" January 29-30, 2008 meeting in Chicago

Add new field Trustee – Entity that carries out the provisions of the governing documents of the transaction and acts as a fiduciary that protects the interests of the investors. If this is a different entity than the Bond Administrator, the entity is generally referred to as a “Passive” or “Nominal” Trustee.

16 Loan level information New field - "Bond Administrator"

October 2008 teleconferences and email discussions

Add new field, making distinction between Bond Administrator and Trustee

Bond Administrator – Entity that is generally responsible for creating the “trustee report” and making investor payments.

17 Loan level information New field - "Master Servicer"

January 29-30, 2008 meeting in Chicago

Add new field Add this information at the loan level. This will provide clarity for deals where there are multiple parties that has become prevalent in our industry.

New Definition: Master Servicer: This servicer is a party to the servicing agreement. Their responsibilities generally include reporting and remitting to the Bond Administrator, advancing, transferring non-performing/defaulted loans to the Special Servicer, monitoring Primary/Sub-Servicers, and handling borrower special requests.

18 Loan level information New field - "Primary Servicer"

January 29-30, 2008 meeting in Chicago

Add new field Add this information at the loan level. This will provide clarity for deals where there are multiple parties that has become prevalent in our industry.

New Definition: Primary Servicer: This servicer is obligated to provide services to the Master Servicer pursuant to the terms of the sub-servicing/primary servicing agreement. Generally, the Primary Servicer retains direct contact with the borrower and performs ongoing servicing functions, such as monthly payment billing and collections, escrow administration, operating statement collections, and remits P&I collections to the Master Servicer.

19 Loan level information New field - "Special Servicer"

January 29-30, 2008 meeting in Chicago

Add new field Add this information at the loan level. This will provide clarity for deals where there are multiple parties that has become prevalent in our industry.

New Definition: Special Servicer: This servicer is a party to the servicing agreement. Typically there is one special servicer named for the pool; however, certain individual loans or groups of loans may have a different special servicer either because the loan is not serviced under the given servicing agreement (an outside serviced loan), or because there is a specific controlling holder for an individual loan or group of loans and that entity has appointed a different special servicer. While the individual Special Servicers are named in the servicing agreement at origination, servicing transfers may occur over time and this field will indicate the current special servicer.

20 Bond File Bond file fields were not previously all defind in the data dictionary

January 29-30, 2008 meeting in Chicago

Definitions are needed New definitions have been created and some field names have been changed. Detail on these fields/definitions is included in the Attachment A to this change matrix.

21 Bond File Notional Flag field January 29-30, 2008 meeting in Chicago

Yes/null not allowed in XML Change field population options to YES/NO.

22 Loan Setup File Original Term of Loan field (S6)

January 29-30, 2008 meeting in Chicago

Change definition Final review of this definition is open pending review of full data dictionary.

23 Loan Setup File Original Amortization Term field (S7)

January 29-30, 2008 meeting in Chicago

Change definition Final review of this definition is open pending review of full data dictionary.

24 Loan Setup File Interest in Arrears (Y/N) (S16)

January 29-30, 2008 meeting in Chicago

Change definition Change IRP definition to delete "or subsequent" and change Y to Yes and N to No (conforming to CM item #3) so that it reads: "Flag indicating whether interest portion of the periodic payment is due for the preceding or subsequent period. Yes=interest collected for the preceding acounting period, No = interest is not collected for the preceding accounting period."

25 Loan Setup File Payment Type (S17) January 29-30, 2008 meeting in Chicago

Change field name Change field name to "Life of Loan Amortization Type" in lieu of "Payment Type".

26 Loan Periodic Update FiCurrent Beginning Scheduled Balance (L6)

January 29-30, 2008 meeting in Chicago

Change field name Change field name to remove "Current". New field name to be "Beginning Scheduled Balance". This data point is always associated with its distribution date so there is no need to include "current".

27 Loan Periodic Update FiCurrent Ending Scheduled Balance (L7)

January 29-30, 2008 meeting in Chicago

Change field name Change field name to remove "Current". New field name to be "Ending Scheduled Balance". This data point is always associated with its distribution date so there is no need to include "current".

28 Loan Periodic Update FiCurrent Index Rate (L9) January 29-30, 2008 meeting in Chicago

Change field name Change field name to remove "Current". New field name to be "Index Rate". This data point is always associated with its distribution date so there is no need to include "current".

CREFC IRP Version 6.0-Draft #1– 1/9/09

CREFC Investor Reporting Package - Change Matrix IRPx v6.0 DRAFT

Item No.

CREFC Data Files/ Reports/Templates

Discussion Topic Source Comments presented for initial discussion IRPx v6.0 Determination for 1st Exposure Draft

29 Loan Periodic Update FiCurrent Note Rate (L10) January 29-30, 2008 meeting in Chicago

Change field name Change field name to remove "Current". New field name to be "Note Rate". This data point is always associated with its distribution date so there is no need to include "current".

30 Loan Periodic Update FiForeclosure Start Date (L42) January 29-30, 2008 meeting in Chicago

Change field from loan level data point to property level data point. Loan level rollup of info will be handled by the Reader. Field will still be defined in DD and available in the Reader.