irs w-9 and w-8 forms - iofm.com · form w-9 v forms w-8 • u.s. persons – individuals • u.s....

TRANSCRIPT

IRS W-9 and W-8 Forms

Marianne Couch, J.D. Mary Kallewaard

Cokala Tax Information Reporting Solutions, LLC

www.cokala.com

Form W-9 v Forms W-8 • U.S. persons

– Individuals • U.S. citizens • U.S. “green” card holders • U.S. resident aliens

– Substantial presence test

– Entities • Organized under U.S. law (50 states

and D.C.)

• Form W-9/1099 backup withholding and reporting rules

• Non-U.S. persons – Chapter 3 rules

• Individuals – Non-resident aliens

» Not U.S. citizens; not “green” card holders; not residents (have not passed the SPT)

• Entities – Organized under the laws of a

country other than the U.S.

– Chapter 4 (FATCA) rules • Foreign financial institutions (FFIs) • Non-financial foreign entities (NFFEs)

• Forms W-8 (8233)/1042-S withholding and reporting rules

Form W-9 Purposes

• Is a withholding certificate

• Signed Form W-9 certifies that: – Payee is a U.S. person

– The TIN provided on the form is correct (certified TIN)

– The payee is not subject to backup withholding on payments of interest and dividends

– The FATCA code provided, if any, is correct

• FATCA codes needed only for certain accounts maintained outside of the U.S.

• An unsigned Form W-9 is acceptable if none of the above certifications is required (e.g., Form 1099-MISC, and certain other Form 1099 , reportable payments; payee is not in a B Notice situation, etc.)

4

Form W-9 TIN Solicitation Rules

• If paying – Bank-deposit Interest (1099-INT) – Dividends (1099-DIV) – Gross broker proceeds (1099-B) – Original Issue Discount (1099-OID) – Patronage Dividends (1099-PATR)

• Or – In a first B-notice situation

• The payee must certify under penalties of perjury that the TIN (taxpayer identification number) they've provided is correct. – See IRC Sec. 31.3406

5

Form W-9

• For other payments (e.g., most of those reported on Form 1099-MISC) – The payee may provide the TIN either orally or in writing. – No penalty of perjury signature is required. – See IRC Sec. 31.3406

• Recommendation: written documentation is better, but the regs. do allow you to take the TIN over the phone, for example, or by email, etc.

• But there are other reasons besides obtaining a TIN for which a Form W-9 or acceptable substitute is required.

6

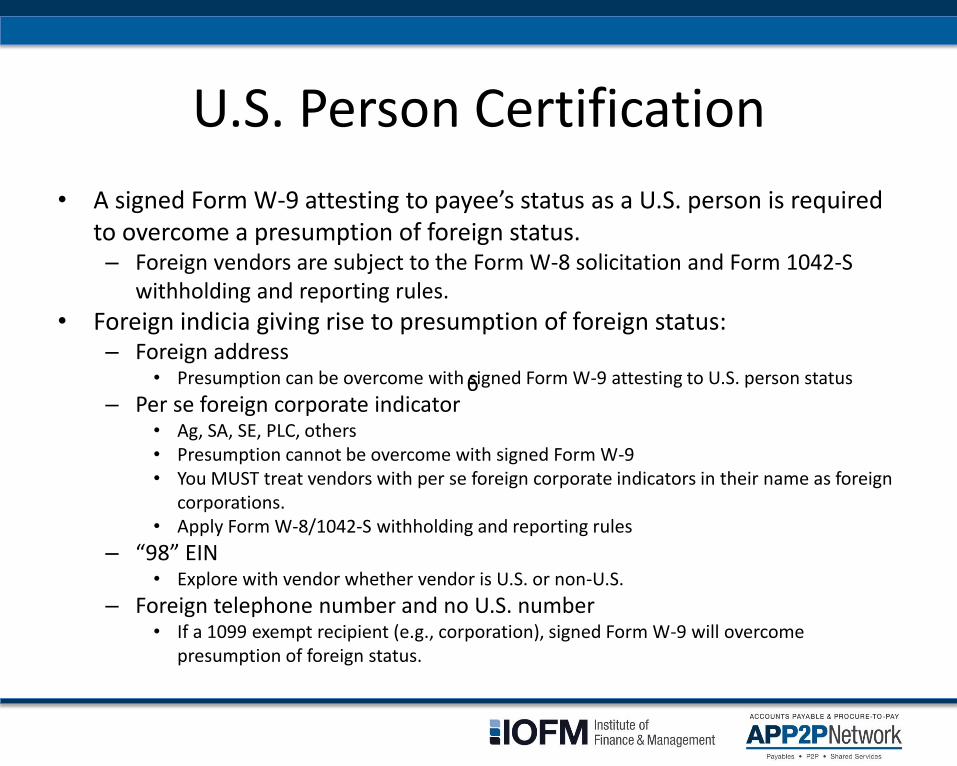

U.S. Person Certification

• A signed Form W-9 attesting to payee’s status as a U.S. person is required to overcome a presumption of foreign status. – Foreign vendors are subject to the Form W-8 solicitation and Form 1042-S

withholding and reporting rules.

• Foreign indicia giving rise to presumption of foreign status: – Foreign address

• Presumption can be overcome with signed Form W-9 attesting to U.S. person status

– Per se foreign corporate indicator • Ag, SA, SE, PLC, others • Presumption cannot be overcome with signed Form W-9 • You MUST treat vendors with per se foreign corporate indicators in their name as foreign

corporations. • Apply Form W-8/1042-S withholding and reporting rules

– “98” EIN • Explore with vendor whether vendor is U.S. or non-U.S.

– Foreign telephone number and no U.S. number • If a 1099 exempt recipient (e.g., corporation), signed Form W-9 will overcome

presumption of foreign status.

7

U.S. Person Certification and the FATCA Presumption

• The FATCA regulations require you to presume that the following types of entities, to which you are making U.S. source FATCA income payments, are foreign: – Corporations – Financial institutions (including banks and insurance companies – Brokers, swap dealers, nominees and custodians

• A signed Form W-9 attesting to payee’s status as a U.S. person overcomes this presumption. – The signed Form W-9 establishes the vendor’s status as U.S. – FATCA is not applicable to U.S. vendors

• Without this documentation, you would be required to treat the vendor as foreign, withhold 30% of the payment, and report the payment on a Form 1042-S.

8

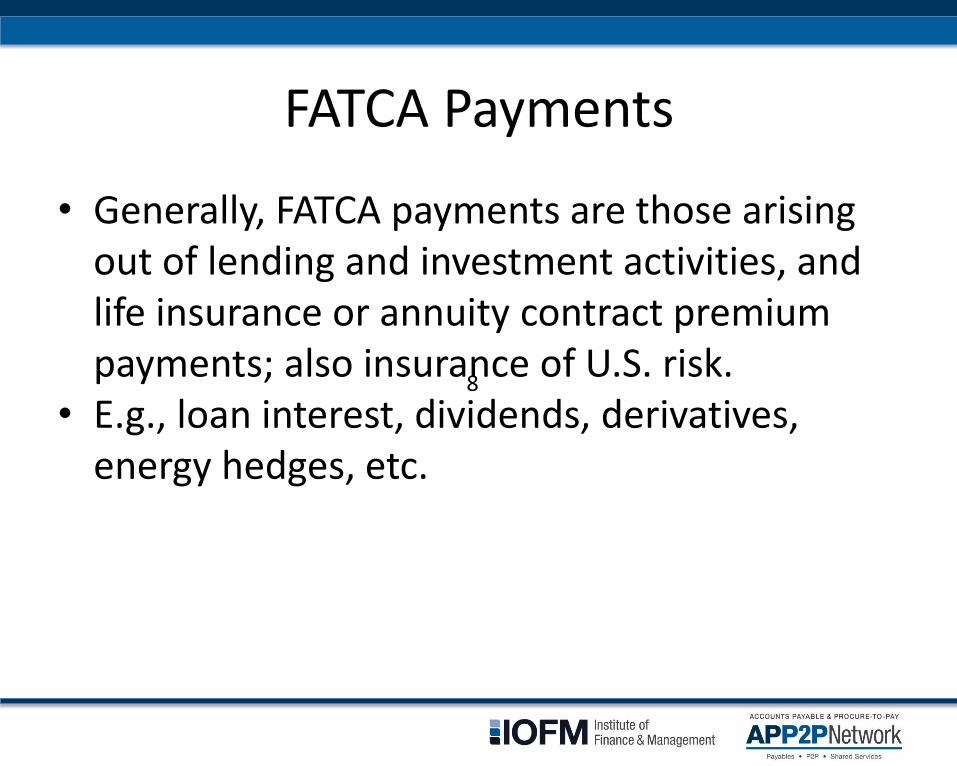

FATCA Payments

• Generally, FATCA payments are those arising out of lending and investment activities, and life insurance or annuity contract premium payments; also insurance of U.S. risk.

• E.g., loan interest, dividends, derivatives, energy hedges, etc.

9

Form W-9

• Also provides information on vendor’s tax status • Knowing tax status can help you determine:

– whether vendor is subject to Form 1099 reporting or is an exempt recipient • Corporations (except for medical or legal services providers) • Tax-exempt entities • Government entities • Others

– What the vendor’s correct name is (for tax reporting purposes) • Individual name? • Entity/business name?

10

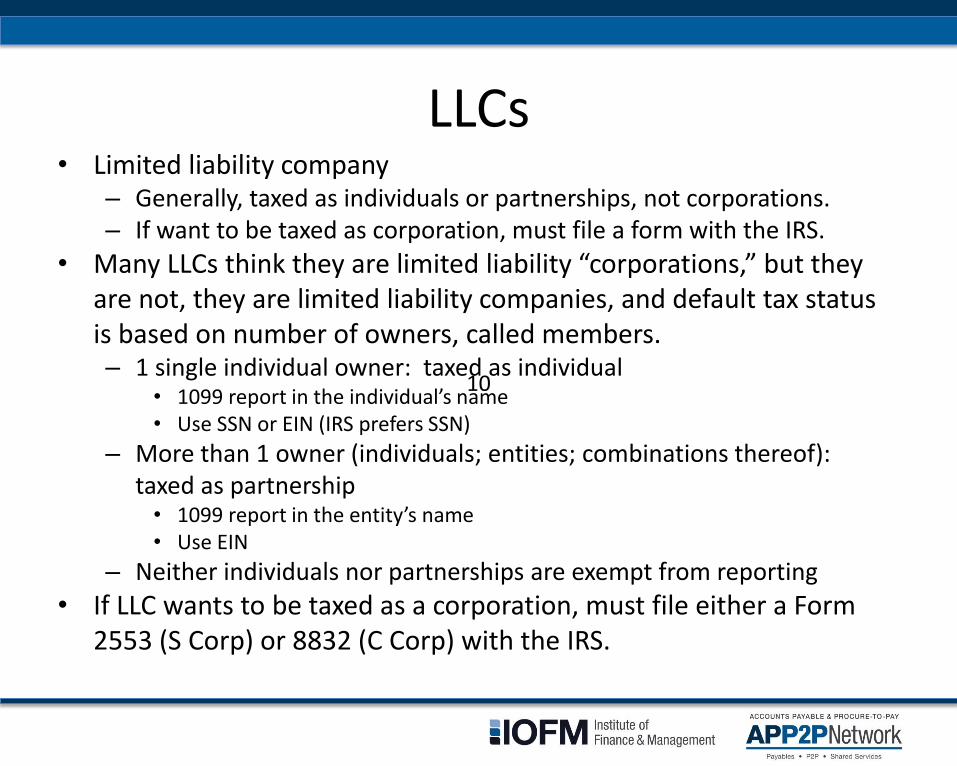

LLCs • Limited liability company

– Generally, taxed as individuals or partnerships, not corporations. – If want to be taxed as corporation, must file a form with the IRS.

• Many LLCs think they are limited liability “corporations,” but they are not, they are limited liability companies, and default tax status is based on number of owners, called members. – 1 single individual owner: taxed as individual

• 1099 report in the individual’s name • Use SSN or EIN (IRS prefers SSN)

– More than 1 owner (individuals; entities; combinations thereof): taxed as partnership • 1099 report in the entity’s name • Use EIN

– Neither individuals nor partnerships are exempt from reporting

• If LLC wants to be taxed as a corporation, must file either a Form 2553 (S Corp) or 8832 (C Corp) with the IRS.

11

Disregarded Entities

• Disregarded entities are entities that are disregarded as separate from their owners.

• For tax reporting purposes (e.g., 1099 reporting) treat the payment as made to the owner even if you made it to the DE. – E.g., payment made to Veritas Auto Designs, LLC, which is a DE

owned by Takei Motors, Inc. • Reportable payee is Takei Motors, Inc., not Veritas Auto Designs, LLC. • In this situation, you can apply the corporate exemption, since the

corp. is the beneficial owner of the income, and do not need to report the payment (since Takei is not a medical or legal services provider).

• Veritas’s Form W-9 should be completed with Takei’s name in line 1; Veritas’s name in line 2; Takei’s EIN in the TIN field; and Takei’s status indicated by the appropriate checkbox (C or S Corp).

12

Sole Proprietors

• 1099 report in individual owner’s name, not the business or d/b/a name.

• Use the sole proprietor’s SSN or EIN – IRS prefers SSN

• Sole proprietors should include the owner’s name in line 1 of the Form W-9; the business name in line 2; should check the individual/sole proprietor/single-member LLC box; provide the individual’s SSN or EIN (IRS prefers SSN) + -

13

Corporations

• We recommend not using the “eyeball” test to exempt your U.S. corporations from Form W-9 solicitation.

• Soliciting the Form W-9 can help: – Flush out your potentially foreign vendors – Protect you from the 30% withholding liability on

FATCA payments to U.S. corps. , financial institutions, brokers, swap dealers, nominees and custodians

– Prevent erroneously giving the corporate exemption to LLCs that are not taxed as corporations, and to incorporated medical and legal services providers

14

Form W-9 Line 4 Codes

• Exempt Payee Code (entities only) – Optional – If payee indicates elsewhere on the form that it’s an

exempt recipient (e.g., checks one of the corporation boxes), payer may give the payee the exemption as long as it has no reason to question the claim of corporate status, and as long as the recipient is not a medical or legal services provider; an exemption code is not required.

• FATCA exemption code (entities only) – Needed only for certain accounts maintained outside the

United States by certain foreign financial institutions. – If FATCA exemption codes do not apply to your payees, IRS

has stated that you may pre-fill this line with NA or Not Applicable.

19

Forms W-8

• Purposes: – Documents beneficial owner’s or agent’s/intermediary’s

status as non-U.S person. – Claim ECI (effectively connected income) on Form W-8ECI. – Claim treaty benefits on Form W-8BEN, -BEN-E or 8233. – Provide FATCA certifications for U.S. source FATCA income

payments (Form W-8BEN-E). – Claim intermediary/agent status (i.e., intermediary/agent

is not the beneficial owner of income paid to it) on Form W-8IMY.

– Claim exempt status as foreign government or foreign tax-exempt entity (Form W-8EXP; rarely applicable to payments).

• Form W-8CE (covered expatriate) used for certain deferred compensation payments.

20

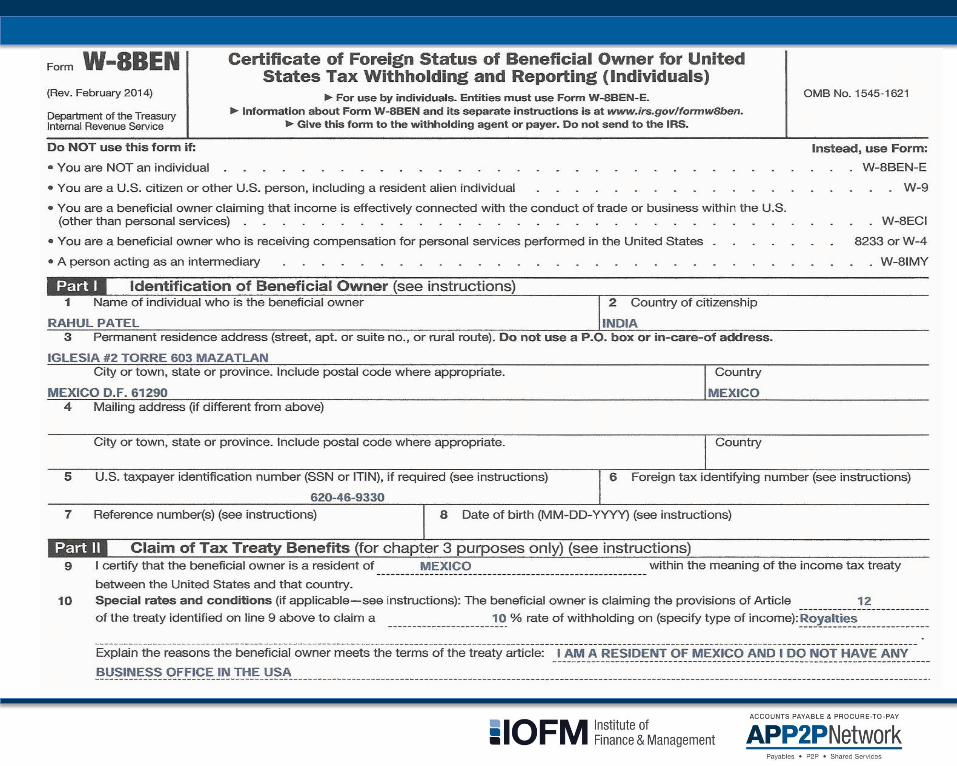

Form W-8BEN (individuals)

• If using the form simply to document a payee’s status as a non-U.S. person (i.e., there are no treaty claims or payment is documented as non-U.S. source income), beneficial owner needs to complete only: – Line 1 (name) – Line 2 (country of citizenship) – Line 3 (permanent residence address; cannot be U.S.; may

not be same as country of citizenship) – Signature, printed name, date

• Date of birth is required for financial accounts at U.S. offices of financial institutions (though it becomes required on all forms beginning 2017 if no foreign TIN is provided on the form)

21

Form W-8BEN (individuals) - Treaty Claims

• Treaty claims on U.S. source FDAP income (e.g., interest, dividends, royalties, non-qualified scholarships, etc.) – Treaty claims on U.S. source services income are made

on Form 8233 – Treaty claims are made in Part II of the form

• Treaty must exist and must apply – You will need to read treaty to make sure it applies

• If treaty applies, withhold at treaty rate (might be zero or some other amount less than 30%)

• Form must include U.S. or foreign TIN for treaty claim

22

Treaty Claims Form W-8BEN – Line 10

• Line 10 must be used if the beneficial owner is claiming treaty benefits that require the beneficial owner to meet conditions not covered by the representations made on line 9 and Part III. – For example, persons claiming treaty benefits on royalties must

complete this line if the treaty contains different withholding rates for different types of royalties.

• However, this line should always be completed by foreign students and researchers claiming treaty benefits.

• This line is generally not applicable to treaty benefits under an interest or dividends (other than dividends subject to a preferential rate based on ownership) article of a treaty.

23

New Form W-8BEN (January 2017 Version; Use Required by July 2017)

• The new version requires more detail in Line 10. – Requires not just the Article number but also the specific

paragraph number within the Article of the treaty. – Also makes it more clear, than in the 2014 version, that the

written explanation must provide details of qualification for the benefit, saying, • “Explain the additional conditions in the Article and paragraph the

beneficial owner meets to be eligible for the rate of withholding.”

Form 8233

• Individual

• U.S. source services income

• Treaty – Requires U.S. TIN.

– If no treaty is available, use the Form W-8BEN or presumption rules to document your payee’s non U.S. status.

25

Form 8233 • Used by individuals to make treaty claims on U.S. source services income (i.e., for

services performed in the U.S.)

• This form requires a U.S. TIN; foreign TINs are insufficient for treaty claims on Form

8233

• This form must be an original; faxed, emailed, photocopied, etc. forms are not

acceptable

• This form must be signed by both beneficial owner and payer

• This form must be sent to the IRS for verification of treaty claims within 5 days of

payer’s acceptance of it (usually counted from the day the payer signs the form)

• IRS has 10 days to respond to the claim; if they do not respond, payer can assume

treaty claim is valid and release funds without withholding

31

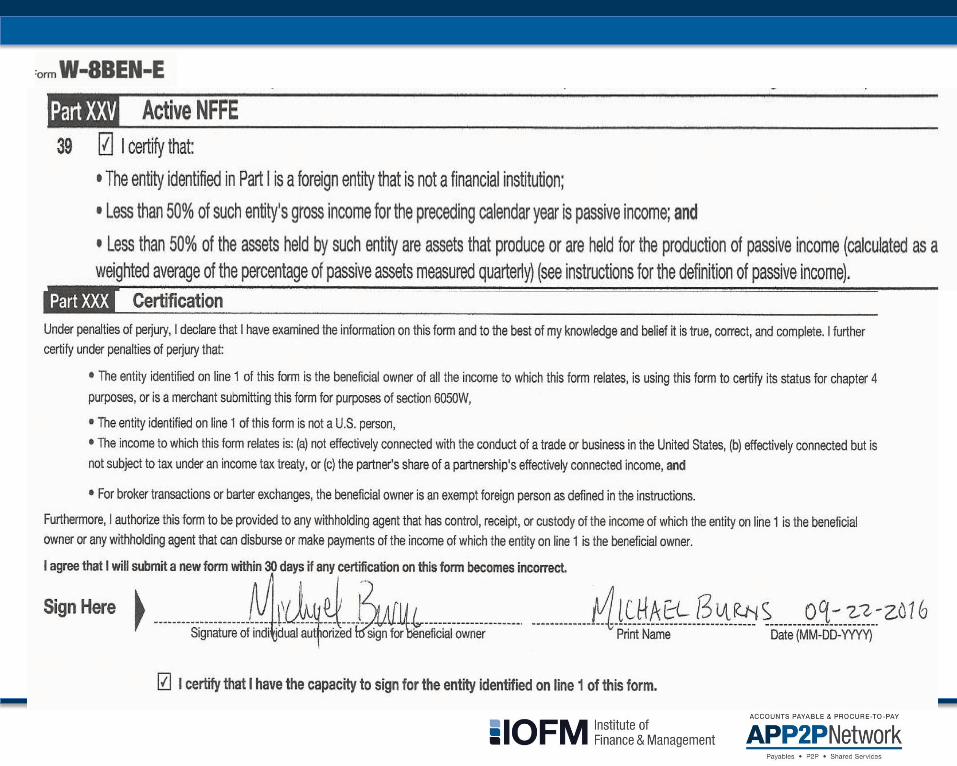

Form W-8BEN-E • Entities, only • Includes sections regarding FATCA payments and

sections regarding Chapter 3 payments. • If making a U.S. source FATCA income payment

(payments arising out of lending, investing and insurance activities) to a non-U.S. entity, the entity must provide you with the necessary FATCA certifications on the form. – If payee does not provide necessary FATCA certifications,

30% FATCA withholding is required; payment(s) is/are reported on Form 1042-S. • No Chapter 3 analysis is conducted

• Note: a new version of the Form W-8BEN-E was finalized by the IRS in April; is required for forms received after October 31, 2016. – Discussion of the changes upcoming.

32

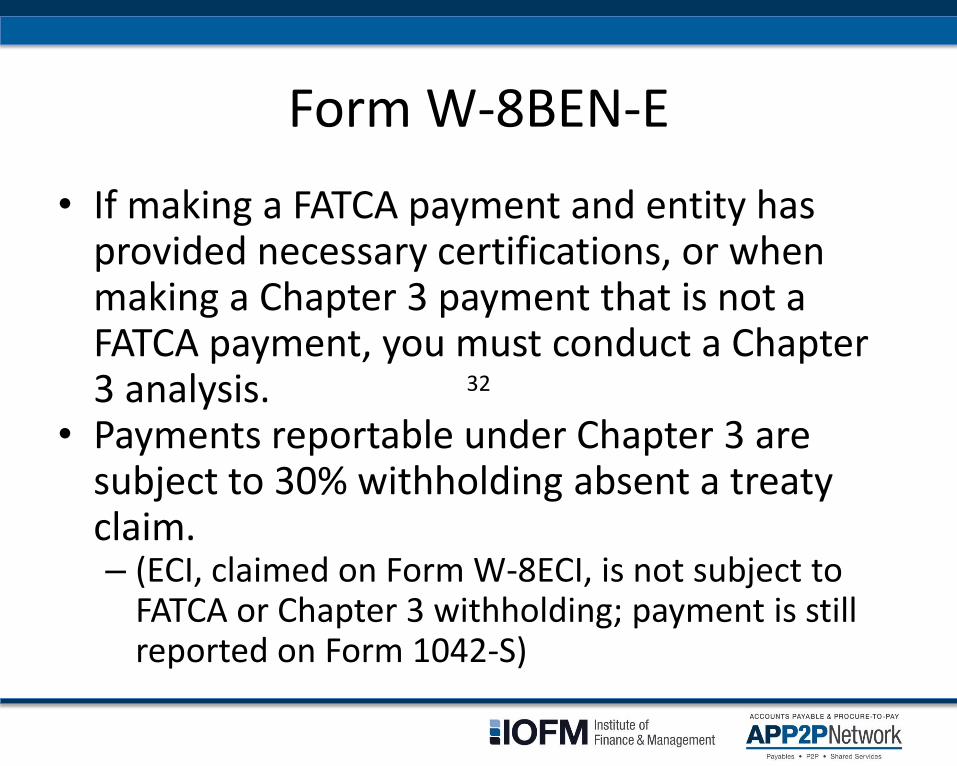

Form W-8BEN-E

• If making a FATCA payment and entity has provided necessary certifications, or when making a Chapter 3 payment that is not a FATCA payment, you must conduct a Chapter 3 analysis.

• Payments reportable under Chapter 3 are subject to 30% withholding absent a treaty claim. – (ECI, claimed on Form W-8ECI, is not subject to

FATCA or Chapter 3 withholding; payment is still reported on Form 1042-S)

33

Form W-8BEN-E

• If using form just to document vendor’s status as a non-U.S. entity, it needs to complete only: – Line 1 (name) – Line 2 (country of incorporation or organization) – Line 4 (type of entity for Chapter 3 purposes) – Line 6 (permanent residence address) – Signature, printed name, date, capacity check box

• If the vendor is making a treaty claim on the payment, it must complete the above lines plus – Line 8 (U.S. TIN) or 9b (foreign TIN) – Part III (treaty section)

34

Form W-8BEN-E Treaty Claim, cont

• Line 15 (comparable to Line 10 on Form W-8BEN) must be used if the vendor is claiming treaty benefits that require it to meet conditions not covered by the representations made in line 14.

• This line is generally not applicable to claiming treaty benefits under an interest or dividends (other than dividends subject to a preferential rate based on ownership) article of a treaty.

• The following are examples of persons who should complete this line. – Exempt organizations claiming treaty benefits under the exempt organization articles of the

treaties with Canada, Mexico, Germany, and the Netherlands. – Foreign corporations that are claiming a preferential rate applicable to dividends based on

ownership of a specific percentage of stock in the entity paying the dividend. – Persons claiming treaty benefits on royalties if the treaty contains different withholding rates

for different types of royalties. – Persons claiming treaty benefits under an “other income” treaty article.

35

New Form W-8BEN-E (finalized 4/16)

• New Limitation on Benefits section for treaty claims.

• Limitation on Benefits provisions in income tax treaties are intended to prevent a foreign entity with U.S.-source income, resident in a country that doesn’t have an attractive income tax treaty with the United States, from claiming a U.S. tax reduction under a third country’s treaty through a shell entity the foreign entity sets up in the third country.

• Must be using new version on and after 11/1/16.

Form W-8ECI – Income Effectively Connected to the Conduct of a Trade or Business in the U.S. (“ECI”)

• Form W-8ECI is used by a foreign person:

– to claim that the income is effectively connected with the conduct of a trade or business in the U.S.

– to claim beneficial ownership of the income

– to state that the income is includible in the payee’s U.S. gross income (to be included in a U.S. tax return)

– to establish foreign status (remember a foreign company cannot sign a W-9)

What Is “Effectively Connected Income” or “ECI”?

• Usually all non-passive income from U.S. sources when the party is engaged in the conduct of a trade or business in the U.S. (but can include passive income like royalties if trade or business related)

• ECI is income that is effectively connected with a U.S. trade or business (“ECI”)

– Involves business activity in the U.S., e.g., construction, transportation, engineering, consulting, retail store owner

– Subject to much the same rules as U.S. taxpayers

Taxed at marginal rates just like a U.S. taxpayer

Requires filing U.S. tax returns, i.e., 1040NR, 1120F

• ECI is exempt from FATCA

Processing Form W-8ECI

• All ECI listed on the W-8ECI regardless of type is subject to special Form 1042-S reporting even though not subject to 30% withholding. – Use exemption code “01” in Box 3a of 1042-S.

– 1042-S even includes passive income like bank deposit interest as long as listed on the W-8ECI.

• W-8ECI must have a U.S. TIN to be valid.

• W-8ECI requires payees to be registered as U.S. taxpayers, and to certify that they are meeting U.S. tax obligations as to the income received on their own U.S. tax returns.

• No need to withhold, but still need to report on Form 1042-S so IRS can match ECI against the payee’s U.S. tax return to verify obligations are being met.

– One of the bigger processing errors the IRS encounters is a payment exempted from withholding with exemption code 01 (ECI) and no U.S. TIN on the Form 1042-S.

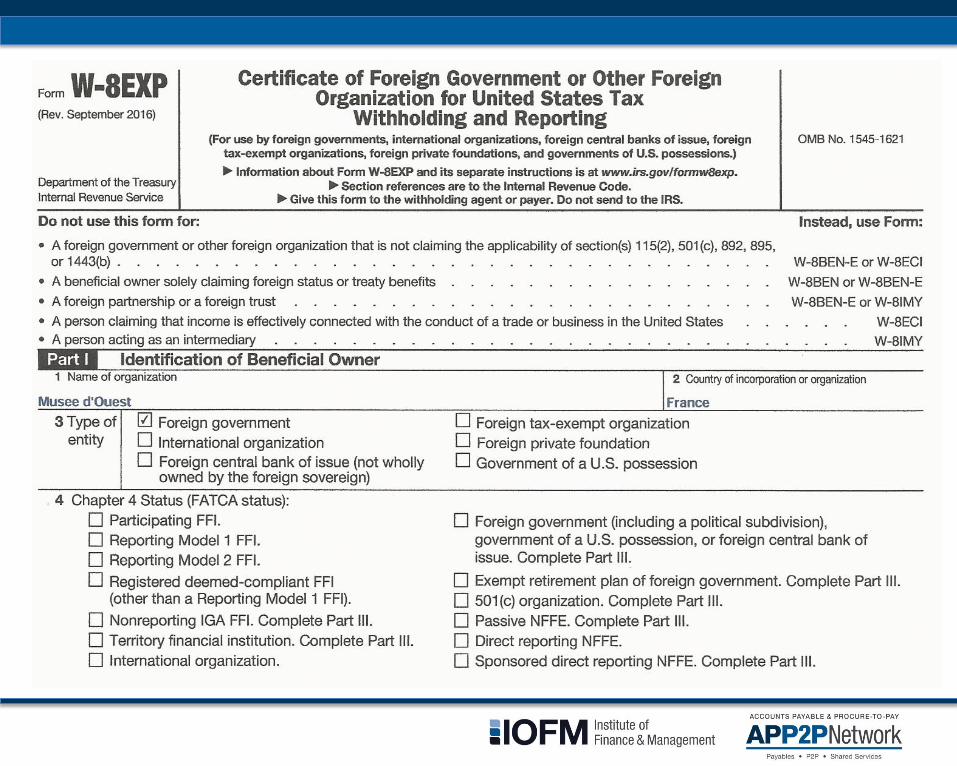

Form W-8EXP Foreign Governments and Exempt Intl Orgs

• VERY limited application – In general, payments to a foreign government (including a foreign

central bank of issue wholly-owned by a foreign sovereign) from investments in the United States in stocks, bonds, other domestic securities, financial instruments held in the execution of governmental financial or monetary policy, and interest on deposits in banks in the United States are exempt from withholding.

– Other foreign tax-exempt organizations must be exempt under 501(c).

• Beneficial owner must include the date the IRS issued the exemption letter or attach an opinion of counsel that it would qualify for tax-exempt status under U.S. law if it applied for it.

• If a Form W-8EXP crosses your desk, if it very likely the wrong form. – Assume it’s incorrect until established otherwise.