is college still worth it? the new calculus of falling returns · 2020-01-21 · is college still...

TRANSCRIPT

Is College Still Worth It? The New Calculus of Falling Returns

William R. Emmons, Ana H. Kent, and Lowell R. Ricketts

Having a four-year college degree is associated with many positive outcomes, including higher income and wealth, better health, a higher likelihood of being a homeowner and of being partnered (married or cohabiting), and a lower risk of becoming delin-

quent on any obligation (Table 1, Panel A). Among college graduates, families headed by someone who completed a postgraduate degree fare even better on these and other measures than families with a head with only a bachelor’s degree (Table 1, Panel B). The fact that an increasing share of the adult population is completing four years or more of college suggests a widespread belief that college is, indeed, worth it (Figure 1).

Yet signs have emerged that the economic benefits of college may be diminishing. Despite large income and wealth advantages enjoyed on average by families with a head with a bach-elor’s degree or higher over families with a head without a postsecondary degree, recent cohorts of college graduates appear to be faring less well than previous generations.1

The college income premium is the extra income earned by a family whose head has a college degree over the income earned by an otherwise similar family whose head does not have a college degree. This premium remains positive but has declined for recent graduates. The college wealth premium (extra net worth) has declined more noticeably among all cohorts born after 1940. Among families whose head is White and born in the 1980s, the college wealth premium of a terminal four-year bache-lor’s degree is at a historic low; among families whose head is any other race and ethnicity born in that decade, the premium is statistically indistinguishable from zero. Among families whose head is of any race or ethnicity born in the 1980s and holding a postgraduate degree, the wealth premium is also indistinguishable from zero. Our results suggest that college and postgraduate education may be failing some recent graduates as a financial investment. (JEL I26 J15)

Federal Reserve Bank of St. Louis Review, Fourth Quarter 2019, 101(4), pp. 297-329. https://doi.org/10.20955/r.101.297-329

William R. Emmons is the lead economist, Ana H. Kent is a policy analyst, and Lowell R. Ricketts is the lead analyst at the Center for Household Financial Stability of the Federal Reserve Bank of St. Louis. William R. Emmons is also an assistant vice president at the Federal Reserve Bank of St. Louis.

© 2019, Federal Reserve Bank of St. Louis. The views expressed in this article are those of the author(s) and do not necessarily reflect the views of the Federal Reserve System, the Board of Governors, or the regional Federal Reserve Banks. Articles may be reprinted, reproduced, published, distributed, displayed, and transmitted in their entirety if copyright notice, author name(s), and full citation are included. Abstracts, synopses, and other derivative works may be made only with prior written permission of the Federal Reserve Bank of St. Louis.

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 297

Emmons, Kent, Ricketts

298 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

Tabl

e 1

Char

acte

rist

ics

of F

amili

es in

the

2016

SCF

by

Educ

atio

n Le

vel

SCF

resp

onde

nt’s

hi

ghes

t edu

catio

n

Shar

e of

all

U.S

. fam

ilies

(p

erce

nt)

Med

ian

fam

ily in

com

e (2

016

$)

Med

ian

fam

ily

net w

orth

(2

016

$)

Shar

e re

port

ing

resp

onde

nt’s

he

alth

as

good

or

exc

elle

nt

(per

cent

)

Shar

e th

at

own

prim

ary

re

side

nce

(p

erce

nt)

Shar

e m

arri

ed

or c

ohab

itatin

g (p

erce

nt)

Shar

e de

linqu

ent o

n lo

an o

blig

atio

ns

60+

days

(p

erce

nt)

A. F

amili

es h

eade

d by

col

lege

gra

ds a

nd n

on-g

rads

Less

than

a fo

ur-y

ear

colle

ge d

egre

e66

.040

,505

53,5

0266

.358

.253

.86.

9

At l

east

a fo

ur-y

ear

colle

ge d

egre

e34

.091

,947

290,

904

86.3

74.4

62.4

3.7

B. F

amili

es h

eade

d by

four

-yea

r deg

ree

hold

ers

and

post

grad

uate

deg

ree

hold

ers

At m

ost a

four

-yea

r co

llege

deg

ree

20.9

84,2

5122

8,58

085

.072

.459

.74.

2

A p

ostg

radu

ate

degr

ee13

.111

2,20

044

3,14

888

.277

.766

.62.

8

SOU

RCE:

SCF

and

aut

hors

’ cal

cula

tions

.

Emmons, Kent, Ricketts

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 299

We use the Federal Reserve Board’s Survey of Consumer Finances (SCF), which covers family heads born throughout the twentieth century, to determine whether the economic and financial benefits of obtaining a postsecondary degree have changed over time. Our evidence is mixed but discouraging on balance. The income advantage of recent college graduates remains positive but may have declined for some demographic groups relative to older grad-uates. Meanwhile, the wealth-building advantage of higher education has declined among recent graduates of all demographic groups. Among all racial and ethnic groups born in the 1980s, only the wealth premium for White four-year college graduates remains statistically significant. Thus, we identify a striking divergence between the income and wealth outcomes of college graduates across birth cohorts.

Our findings highlight the fact that income and wealth measures, while related, are distinct and may provide different insights into college and postgraduate experiences. We suggest three potential explanations, each of which may contribute something to the patterns we identify:

• The luck of when you were born, since beginning to save and accumulate wealth at a time when asset prices (stocks, bonds, and housing) are high makes subsequent rates of return low and vice versa

• Financial liberalization, which may have created more opportunities for people born in the 1980s than in the 1940s, for example, to use (and misuse) credit when they were young, affecting their wealth but not their incomes

• The rising cost of higher education, which would not reduce college graduates’ incomes but would reduce their wealth, at least early in life

0

5

10

15

20

25

30

35

40

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Percent

Figure 1Share of U.S. Population (25 Years+) That Completed 4+ Years of College, 1940-2017

NOTE: Between 1992 and 2017, the number of college graduates 25 years of age or older increased by 40 million, while the total number of people 25 years of age or older increased by 56 million. Thus, the net increase in college grads con-stituted 71 percent of total net population growth among people 25 years of age or older.

SOURCE: Census Bureau and authors’ calculations.

Emmons, Kent, Ricketts

300 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

The article has four sections. In Section 1, we document the large income and wealth premiums enjoyed on average by the typical family with a head holding a terminal bachelor’s or postgraduate degree over the typical family with a head holding no college degree; this is the conventional wisdom.2 In Section 2, we show with SCF data that aggregate statistics con-ceal important differences between income and wealth trends across college graduates from successive birth cohorts. Section 3 outlines some of the features any plausible explanation of our findings must possess; we leave a detailed investigation of these hypotheses to future research. Section 4 concludes.

1 INCOME AND WEALTH PREMIUMS ENJOYED BY THE TYPICAL COLLEGE GRADUATE

The conventional wisdom that bachelor’s and, even more, postgraduate degrees pay off in terms of higher income and wealth are strongly supported in aggregate data (that is, pooled across race, ethnicity, and birth year). We present income and wealth trends for three separate groups—families headed by someone with both a bachelor’s and a postgraduate degree (post-graduate families); families headed by someone whose highest level of education is a bache-lor’s degree (bachelor’s degree families); and families headed by someone whose highest level of education is less than a four-year college degree (nongraduate families). Our data source throughout is the SCF.3

0

5

10

15

20

25

30

35

40

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

Four-Year Degree Families

Postgrad Families

Percent of All U.S. Families

Figure 2U.S. Families Headed by College Graduates and Postgraduates

NOTE: Postgraduate families are those headed by someone with both a four-year college degree and a postgraduate degree. The total number of U.S. families rose from 93 million in 1989 to 126 million in 2016.

SOURCE: SCF and authors’ calculations.

Emmons, Kent, Ricketts

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 301

Shares of Families with Bachelor’s and Postgraduate Degrees

The share of U.S. families headed by a college graduate has increased significantly in recent years. (Figure 2). In 1989, about 23 percent of families were headed by someone with a four-year college degree or more; by 2016, the share had reached 34 percent. Families headed by someone with a postgraduate (as well as a four-year college) degree increased from almost 9 percent of all families in 1989 to about 13 percent in 2016. Among White families alone (not shown), the share of families with a four-year degree or more increased from 26 to 38 percent between 1989 and 2016, while among families of all other races and ethnicities, the share increased from 14 to 25 percent.4

Family Income. The income premium enjoyed by the median bachelor’s degree family over the median nongraduate family (the college income premium) has held steady during the past few decades at roughly 100 percent (Figures 3 and 4). The income premium enjoyed by the median postgraduate family over the median nongraduate family (the postgraduate income premium) has increased, standing in 2016 at about 175 percent. The share of all income earned by families with a head with at least a bachelor’s degree increased from 45 to 63 percent between 1989 and 2016, as both the number of bachelor’s degree and postgraduate families and their average incomes increased faster than those of nongraduate families.5

Family Wealth (Net Worth). Figure 5 shows that the net worth of both median bache-lor’s degree and postgraduate families increased between 1989 and 2016, while that of the median nongraduate family declined during that period. Thus, the wealth premiums enjoyed by bachelor’s degree and postgraduate families over the nongraduate family (the college and postgraduate wealth premiums, respectively) have climbed greatly during the past few decades (Figure 6). The postgraduate wealth premium increased by a large margin, standing in 2016 at over 700 percent (i.e., eight times as large). The share of all wealth owned by families with a head with at least a bachelor’s degree increased even more than was the case for income—from 50 to 74 percent between 1989 and 2016.6

What These Figures Hide. The median income and net worth figures from aggregate data shown here turn out to be misleading when careful account is taken of key underlying demographic dimensions and family and individual characteristics. Comparing families that are similar in terms of race and ethnicity, decade of birth, and family size, we find that the college income and wealth premiums are quite variable. Moreover, the conclusion that the college wealth premium is larger and increasing faster than the college income premium is reversed when comparing demographically matched groups of families. In fact, we show in Section 2 that the wealth premium has fallen across successive birth cohorts. Among those born in the 1980s, the wealth premiums of bachelor’s degree families and of postgraduate- degree families are statistically indistinguishable from zero for all groups with the single exception of White bachelor’s degree families.

Emmons, Kent, Ricketts

302 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

Postgraduate Degree

Bachelor’s Degree

Less than a Bachelor’s Degree

2016 Dollars

0

Figure 3Median Family Income

SOURCE: SCF and authors’ calculations.

50

100

150

200

250

Bachelor’s Degree Families Postgraduate Families

Percent

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016 0

Figure 4Income Premiums of the Median Bachelor’s Degree Family and the Median Postgraduate Family Over the Median Nongraduate Family

SOURCE: SCF and authors’ calculations.

Emmons, Kent, Ricketts

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 303

0

100,000

200,000

300,000

400,000

500,000

600,000

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

Postgraduate Degree

Bachelor’s Degree

Less than a Bachelor’s Degree

2016 Dollars

Figure 5Median Family Net Worth

SOURCE: SCF and authors’ calculations.

100

200

300

400

500

600

700

800

900

1,000

0 Bachelor’s Degree Families Postgraduate Families

Percent

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

Figure 6Net-Worth Premiums of the Median Bachelor’s Degree Family and the Median Postgraduate Family Over the Median Nongraduate Family

SOURCE: SCF and authors’ calculations.

Emmons, Kent, Ricketts

304 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

2 COLLEGE INCOME AND WEALTH PREMIUMS AMONG DEMOGRAPHICALLY MATCHED FAMILIES

Large and growing income and wealth premiums associated with college degrees measured in aggregate data mask a diverse range of experiences among bachelor’s degree and post-graduate families when compared with nongraduate families of the same race and ethnicity who were born in the same decade. It turns out that very favorable income and wealth out-comes experienced by mostly White college grads born many decades ago cause aggregate data to overstate the income and wealth advantages experienced by more-recent college grads.

To quantify the changing economic and financial benefits of postsecondary degrees, we estimate the income and wealth premiums earned by bachelor’s degree families and, sepa-rately, postgraduate families compared with otherwise demographically similar nongraduate families. The advanced degrees that qualify a family as postgraduate are quite diverse; see Table A1 for a list of those degrees and a description of all variables used in this article.

We focus on college graduates born in one of six decade-long cohorts starting in the 1930s, concluding with those born during the 1980s.7 In previous research, we found evidence of structural, systemic, or other unobservable barriers to income generation and wealth accu-mulation by non-White Americans, perhaps due to historical discrimination and exclusion in education, housing, employment, and wealth-building programs.8 Therefore, we estimate cohort-specific college and postgraduate income and wealth premiums separately for each of the four racial and ethnic groups available in the public release of the SCF.9 Our estimates of the pure life cycle components of both income generation and wealth accumulation differ sub-stantially across racial and ethnic groups, reinforcing the argument that separate regressions by race and ethnicity are more meaningful than a single, pooled regression.10

Income. To measure income for the SCF, the interviewers requested information on the family’s cash income, before taxes, for the full calendar year preceding the survey.11 The com-ponents of income in the SCF are wages; self-employment and business income; taxable and tax-exempt interest; dividends; realized capital gains; food stamps and other related support programs provided by government; pensions and withdrawals from retirement accounts; Social Security; alimony and other support payments; and miscellaneous sources of income for all members of the primary economic unit in the household. All income figures are adjusted for inflation to be comparable with values recorded in 2016.

We adjust for household size as follows:

(1) Yi = yiHi

,

where yi is the income of household i and Hi is the number of people in that household, exclud-ing individuals that do not usually live there and who are financially independent. The square-root adjustment we use is one of the “equivalence scales” recommended by the Organisation for Economic Co-operation and Development to reflect important economies of scale in household consumption.12 This also adjusts for households with multiple income earners. For example, a two-earner household with exactly two members earning $2Y is considered

Emmons, Kent, Ricketts

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 305

1.414 times as large as a single-person one-earner household earning $Y. Due to likely econ-omies of scale in consumption, the two-earner household effectively has higher disposable income but not twice as much.

To assess secular trends in the returns to higher education, we pool responses for all 10 triennial SCF survey years, the first of which was conducted in 1989 and the most recent in 2016. This yields a sample of 47,776 households. Our full specification is a log-quadratic ordinary least-squares regression of the form

(2) ln Yi( )= β0 +β1Ai +β2Ai

2 +β3Ai3 +β4Gi +β5Pi + β6Ci,1 +…+β6+k−1Ci,k−1 +β6+kCi ,1∗Gi +…+

β6+2k−1Ci,k−1∗Gi +β6+2kCi ,1∗Pi +…+β6+3k−1Ci,k−1∗Pi + ε .

We apply the natural-log function to size-adjusted income. Ai is the age of the household respondent, and A2

i A3i are the squared and cubic terms capturing the effects of the life cycle,

respectively.13 Gi and Pi are binary variables equal to 1 if the respondent earned a terminal four-year college degree or continued on and achieved a postgraduate degree, respectively. Therefore, β4 and β5 represent the income premium attributed to a terminal four-year college degree and postgraduate degree, respectively. The effect on expected earnings associated with the respondent’s birth cohort (defined by decades) is captured by k binary variables denoted as Ci,1:k, with k – 1 binaries included in the specification to both avoid perfect multicollinearity and allow control of the reference group. Birth cohorts and education binaries are interacted to capture changes in the college premium over time. For ease of interpretation, we opt to vary the omitted birth cohort and focus on differences in β4 and β5 in order to compare changes in the college premium over time.

For example, when omitting Ci for the 1980s cohort, β4 and β5 are the respective earnings premiums associated with bachelor’s degree families and postgraduate families with a head born in the 1980s relative to nongraduate families with a head also born in the 1980s. Omitting Ci for the 1950s cohort would change the reference group to the average family with a non-college head born in the 1950s, and so on.

Estimation was conducted using R statistical software and relied upon the “survey” and “mitools” packages.14 Source code is available upon request. Nonresponse-adjusted sampling weights were used in the analysis to adjust for the fact that the SCF sample is not an equal- probability design.15 Given the oversample of wealthy households and the use of both wealth and income as dependent variables, we believe that using weights in the regression analyses is appropriate.16 Standard errors are bootstrapped with 999 replicates in accordance with the sample design and are adjusted for imputation uncertainty.17

There is substantial heterogeneity in both income and wealth across racial and ethnic groups, especially among families with a head with a college degree.18 Rather than relying on binary variables to adjust for large and persistent racial and ethnic wealth gaps, we partitioned the sample and estimated regressions separately for each of the four racial and ethnic groups.

Regression results for White and African-American or Black (henceforth Black) families are shown in Tables 2 and 3, respectively. Results for Hispanic and other families are in Tables A2 and A3, respectively. The life cycles of both income and wealth are empirically

Tabl

e 2

Inco

me

Regr

essi

ons:

Whi

te F

amili

esD

epen

dent

var

iabl

e: In

com

eRa

cial

/eth

nic

grou

p: W

hite

Pseu

do R

2 : 0.

16N

: 37,

044

(1)

(2)

(3)

(4)

(5)

(6)

Inde

pend

ent v

aria

bles

βSE

t-St

atp-

Valu

eβ

SEt-

Stat

p-Va

lue

βSE

t-St

atp-

Valu

eβ

SEt-

Stat

p-Va

lue

βSE

t-St

atp-

Valu

eβ

SEt-

Stat

p-Va

lue

Inte

rcep

t6.

750.

1545

.67

0.00

6.89

0.16

44.3

90.

006.

890.

1643

.43

0.00

6.93

0.16

43.3

90.

006.

940.

1642

.28

0.00

7.01

0.15

46.2

20.

00

Life

cyc

le

Age

0.17

0.01

17.7

90.

000.

170.

0117

.79

0.00

0.17

0.01

17.7

90.

000.

170.

0117

.79

0.00

0.17

0.01

17.7

90.

000.

170.

0117

.79

0.00

Age

20.

000.

00–1

4.36

0.00

0.00

0.00

–14.

360.

000.

000.

00–1

4.36

0.00

0.00

0.00

–14.

360.

000.

000.

00–1

4.36

0.00

0.00

0.00

–14.

360.

00

Age

30.

000.

0011

.78

0.00

0.00

0.00

11.7

80.

000.

000.

0011

.78

0.00

0.00

0.00

11.7

80.

000.

000.

0011

.78

0.00

0.00

0.00

11.7

80.

00

Inco

me

prem

ium

Term

inal

four

-yea

r gr

adua

te (G

)0.

750.

0613

.33

0.00

0.66

0.03

24.2

50.

000.

580.

0320

.98

0.00

0.61

0.03

23.2

90.

000.

660.

0417

.97

0.00

0.48

0.04

12.0

20.

00

Post

grad

uate

(P)

1.12

0.04

27.8

90.

000.

980.

0334

.50

0.00

0.98

0.03

33.4

00.

000.

850.

0423

.64

0.00

0.67

0.06

10.3

70.

000.

590.

0511

.33

0.00

Birt

h co

hort

s

Born

bef

ore

1930

or

aft

er 1

989

–0.1

10.

03–4

.07

0.00

–0.2

60.

03–9

.07

0.00

–0.2

50.

03–8

.85

0.00

–0.2

90.

03–8

.76

0.00

–0.3

00.

04–7

.61

0.00

–0.3

70.

04–8

.86

0.00

Born

in 1

930s

(Om

itted

)–0

.14

0.03

–5.0

50.

00–0

.14

0.03

–4.6

80.

00–0

.18

0.04

–5.1

90.

00–0

.19

0.04

–4.4

60.

00–0

.26

0.04

–5.9

30.

00

Born

in 1

940s

0.14

0.03

5.05

0.00

(Om

itted

)0.

000.

020.

010.

99–0

.04

0.02

–1.8

40.

07–0

.05

0.03

–1.4

90.

14–0

.12

0.04

–3.2

80.

00

Born

in 1

950s

0.14

0.03

4.68

0.00

0.00

0.02

–0.0

10.

99(O

mitt

ed)

–0.0

40.

02–1

.93

0.05

–0.0

50.

03–1

.67

0.09

–0.1

20.

04–3

.31

0.00

Born

in 1

960s

0.18

0.04

5.19

0.00

0.04

0.02

1.84

0.07

0.04

0.02

1.93

0.05

(Om

itted

)–0

.01

0.03

–0.2

50.

81–0

.08

0.03

–2.4

70.

01

Born

in 1

970s

0.19

0.04

4.46

0.00

0.05

0.03

1.49

0.14

0.05

0.03

1.67

0.09

0.01

0.03

0.25

0.81

(Om

itted

)–0

.07

0.04

–1.8

30.

07

Born

in 1

980s

0.26

0.04

5.93

0.00

0.12

0.04

3.28

0.00

0.12

0.04

3.31

0.00

0.08

0.03

2.47

0.01

0.07

0.04

1.83

0.07

(Om

itted

)

Coho

rt X

inco

me

prem

ium

Born

bef

ore

1930

or

aft

er 1

989

* G

–0.1

50.

07–2

.30

0.02

–0.0

50.

05–1

.16

0.25

0.02

0.05

0.45

0.66

–0.0

10.

04–0

.21

0.83

–0.0

60.

05–1

.05

0.29

0.12

0.05

2.23

0.03

Born

in 1

930s

* G

(Om

itted

)0.

100.

061.

530.

130.

170.

062.

720.

010.

140.

062.

220.

030.

090.

071.

360.

170.

270.

073.

830.

00

Born

in 1

940s

* G

–0.1

00.

06–1

.53

0.13

(Om

itted

)0.

070.

041.

950.

050.

040.

031.

280.

200.

000.

05–0

.03

0.97

0.17

0.05

3.66

0.00

Born

in 1

950s

* G

–0.1

70.

06–2

.72

0.01

–0.0

70.

04–1

.95

0.05

(Om

itted

)–0

.03

0.04

–0.8

20.

41–0

.08

0.05

–1.6

40.

100.

100.

052.

050.

04

Born

in 1

960s

* G

–0.1

40.

06–2

.22

0.03

–0.0

40.

03–1

.28

0.20

0.03

0.04

0.82

0.41

(Om

itted

)–0

.05

0.04

–1.0

50.

300.

130.

052.

850.

00

Born

in 1

970s

* G

–0.0

90.

07–1

.36

0.17

0.00

0.05

0.03

0.97

0.08

0.05

1.64

0.10

0.05

0.04

1.05

0.30

(Om

itted

)0.

180.

063.

120.

00

Born

in 1

980s

**

G–0

.27

0.07

–3.8

30.

00–0

.17

0.05

–3.6

60.

00–0

.10

0.05

–2.0

50.

04–0

.13

0.05

–2.8

50.

00–0

.18

0.06

–3.1

20.

00(O

mitt

ed)

Born

bef

ore

1930

or

aft

er 1

989

* P

–0.1

00.

05–1

.89

0.06

0.04

0.05

0.75

0.45

0.04

0.05

0.88

0.38

0.17

0.05

3.39

0.00

0.35

0.08

4.57

0.00

0.42

0.06

6.76

0.00

Born

in 1

930s

* P

(Om

itted

)0.

140.

052.

890.

000.

150.

052.

960.

000.

280.

055.

430.

000.

460.

085.

860.

000.

530.

078.

000.

00

Born

in 1

940s

* P

–0.1

40.

05–2

.89

0.00

(Om

itted

)0.

010.

040.

190.

850.

140.

052.

970.

000.

320.

074.

280.

000.

390.

066.

450.

00

Born

in 1

950s

* P

–0.1

50.

05–2

.96

0.00

–0.0

10.

04–0

.19

0.85

(Om

itted

)0.

130.

052.

710.

010.

310.

074.

610.

000.

380.

066.

330.

00

Born

in 1

960s

* P

–0.2

80.

05–5

.43

0.00

–0.1

40.

05–2

.97

0.00

–0.1

30.

05–2

.71

0.01

(Om

itted

)0.

180.

082.

360.

020.

250.

064.

120.

00

Born

in 1

970s

* P

–0.4

60.

08–5

.86

0.00

–0.3

20.

07–4

.28

0.00

–0.3

10.

07–4

.61

0.00

–0.1

80.

08–2

.36

0.02

(Om

itted

)0.

070.

080.

930.

35

Born

in 1

980s

* P

–0.5

30.

07–8

.00

0.00

–0.3

90.

06–6

.45

0.00

–0.3

80.

06–6

.33

0.00

–0.2

50.

06–4

.12

0.00

–0.0

70.

08–0

.93

0.35

(Om

itted

)

NO

TE: S

E, s

tand

ard

erro

r. St

anda

rd e

rror

s ar

e bo

otst

rapp

ed w

ith 9

99 re

plic

ates

in a

ccor

danc

e w

ith th

e sa

mpl

e de

sign

and

are

adj

uste

d fo

r im

puta

tion

unce

rtai

nty.

Non

resp

onse

-adj

uste

d sa

mpl

ing

wei

ghts

wer

e al

so u

sed.

SOU

RCE:

SCF

and

aut

hors

’ cal

cula

tions

.

Tabl

e 3

Inco

me

Regr

essi

ons:

Bla

ck F

amili

esD

epen

dent

var

iabl

e: In

com

eRa

cial

/eth

nic

grou

p: B

lack

Pseu

do R

2 : 0.

11N

: 5,1

86

(1)

(2)

(3)

(4)

(5)

(6)

Inde

pend

ent v

aria

bles

βSE

t-St

atp-

Valu

eβ

SEt-

Stat

p-Va

lue

βSE

t-St

atp-

Valu

eβ

SEt-

Stat

p-Va

lue

βSE

t-St

atp-

Valu

eβ

SEt-

Stat

p-Va

lue

Inte

rcep

t7.

230.

3420

.97

0.00

7.47

0.35

21.3

60.

007.

500.

3521

.27

0.00

7.59

0.37

20.6

30.

007.

740.

3522

.18

0.00

7.55

0.35

21.6

30.

00

Life

cyc

le

Age

0.10

0.02

4.78

0.00

0.10

0.02

4.78

0.00

0.10

0.02

4.78

0.00

0.10

0.02

4.78

0.00

0.10

0.02

4.78

0.00

0.10

0.02

4.78

0.00

Age

20.

000.

00–3

.43

0.00

0.00

0.00

–3.4

30.

000.

000.

00–3

.43

0.00

0.00

0.00

–3.4

30.

000.

000.

00–3

.43

0.00

0.00

0.00

–3.4

30.

00

Age

30.

000.

002.

480.

010.

000.

002.

480.

010.

000.

002.

480.

010.

000.

002.

480.

010.

000.

002.

480.

010.

000.

002.

480.

01

Inco

me

prem

ium

Term

inal

four

-yea

r gr

adua

te (G

)1.

230.

1110

.99

0.00

0.69

0.12

5.58

0.00

0.76

0.07

10.1

70.

000.

730.

0710

.50

0.00

0.74

0.07

11.1

10.

000.

840.

127.

190.

00

Post

grad

uate

(P)

1.38

0.17

7.92

0.00

1.00

0.19

5.32

0.00

1.04

0.09

11.6

10.

000.

750.

145.

410.

000.

930.

0811

.86

0.00

0.71

0.34

2.06

0.04

Birt

h co

hort

s

Born

bef

ore

1930

or

aft

er 1

989

–0.1

10.

07–1

.60

0.11

–0.3

50.

08–4

.15

0.00

–0.3

80.

08–4

.94

0.00

–0.4

70.

09–5

.27

0.00

–0.6

20.

08–7

.28

0.00

–0.4

30.

09–4

.63

0.00

Born

in 1

930s

(Om

itted

)–0

.25

0.07

–3.4

80.

00–0

.28

0.08

–3.5

80.

00–0

.36

0.09

–4.1

60.

00–0

.51

0.09

–5.7

60.

00–0

.32

0.10

–3.3

80.

00

Born

in 1

940s

0.25

0.07

3.48

0.00

(Om

itted

)–0

.03

0.07

–0.4

50.

65–0

.12

0.07

–1.7

20.

09–0

.26

0.08

–3.1

90.

00–0

.08

0.09

–0.8

90.

37

Born

in 1

950s

0.28

0.08

3.58

0.00

0.03

0.07

0.45

0.65

(Om

itted

)–0

.08

0.05

–1.6

70.

09–0

.23

0.06

–4.1

40.

00–0

.04

0.07

–0.6

40.

52

Born

in 1

960s

0.36

0.09

4.16

0.00

0.12

0.07

1.72

0.09

0.08

0.05

1.67

0.09

(Om

itted

)–0

.15

0.05

–2.7

20.

010.

040.

080.

530.

60

Born

in 1

970s

0.51

0.09

5.76

0.00

0.26

0.08

3.19

0.00

0.23

0.06

4.14

0.00

0.15

0.05

2.72

0.01

(Om

itted

)0.

190.

063.

040.

00

Born

in 1

980s

0.32

0.10

3.38

0.00

0.08

0.09

0.89

0.37

0.04

0.07

0.64

0.52

–0.0

40.

08–0

.53

0.60

–0.1

90.

06–3

.04

0.00

(Om

itted

)

Coho

rt X

inco

me

prem

ium

Born

bef

ore

1930

or

aft

er 1

989

* G

–0.5

80.

22–2

.64

0.01

–0.0

40.

24–0

.17

0.86

–0.1

00.

22–0

.47

0.64

–0.0

80.

19–0

.40

0.69

–0.0

90.

19–0

.44

0.66

–0.1

90.

23–0

.80

0.42

Born

in 1

930s

* G

(Om

itted

)0.

540.

163.

400.

000.

470.

133.

650.

000.

500.

133.

740.

000.

490.

124.

040.

000.

390.

172.

270.

02

Born

in 1

940s

* G

–0.5

40.

16–3

.40

0.00

(Om

itted

)–0

.06

0.14

–0.4

50.

65–0

.03

0.14

–0.2

50.

80–0

.04

0.14

–0.3

10.

76–0

.15

0.17

–0.8

40.

40

Born

in 1

950s

* G

–0.4

70.

13–3

.65

0.00

0.06

0.14

0.45

0.65

(Om

itted

)0.

030.

100.

280.

780.

020.

100.

190.

85–0

.08

0.14

–0.6

00.

55

Born

in 1

960s

* G

–0.5

00.

13–3

.74

0.00

0.03

0.14

0.25

0.80

–0.0

30.

10–0

.28

0.78

(Om

itted

)–0

.01

0.10

–0.1

00.

92–0

.11

0.14

–0.7

80.

44

Born

in 1

970s

* G

–0.4

90.

12–4

.04

0.00

0.04

0.14

0.31

0.76

–0.0

20.

10–0

.19

0.85

0.01

0.10

0.10

0.92

(Om

itted

)–0

.10

0.14

–0.7

50.

45

Born

in 1

980s

**

G–0

.39

0.17

–2.2

70.

020.

150.

170.

840.

400.

080.

140.

600.

550.

110.

140.

780.

440.

100.

140.

750.

45(O

mitt

ed)

Born

bef

ore

1930

or

aft

er 1

989

* P

–0.5

90.

23–2

.53

0.01

–0.2

10.

24–0

.89

0.37

–0.2

50.

15–1

.73

0.08

0.03

0.20

0.17

0.86

–0.1

40.

16–0

.91

0.36

0.08

0.37

0.22

0.83

Born

in 1

930s

* P

(Om

itted

)0.

380.

271.

380.

170.

340.

201.

690.

090.

630.

232.

710.

010.

450.

192.

390.

020.

670.

401.

680.

09

Born

in 1

940s

* P

–0.3

80.

27–1

.38

0.17

(Om

itted

)–0

.04

0.19

–0.2

20.

830.

250.

241.

010.

310.

070.

200.

350.

730.

290.

390.

760.

45

Born

in 1

950s

* P

–0.3

40.

20–1

.69

0.09

0.04

0.19

0.22

0.83

(Om

itted

)0.

290.

171.

670.

090.

110.

111.

050.

290.

330.

321.

040.

30

Born

in 1

960s

* P

–0.6

30.

23–2

.71

0.01

–0.2

50.

24–1

.01

0.31

–0.2

90.

17–1

.67

0.09

(Om

itted

)–0

.18

0.17

–1.0

70.

280.

050.

360.

120.

90

Born

in 1

970s

* P

–0.4

50.

19–2

.39

0.02

–0.0

70.

20–0

.35

0.73

–0.1

10.

11–1

.05

0.29

0.18

0.17

1.07

0.28

(Om

itted

)0.

220.

340.

650.

52

Born

in 1

980s

* P

–0.6

70.

40–1

.68

0.09

–0.2

90.

39–0

.76

0.45

–0.3

30.

32–1

.04

0.30

–0.0

50.

36–0

.12

0.90

–0.2

20.

34–0

.65

0.52

(Om

itted

)

NO

TE: S

E, s

tand

ard

erro

r. Se

e Ta

ble

2 no

te.

SOU

RCE:

SCF

and

aut

hors

’ cal

cula

tions

.

Emmons, Kent, Ricketts

308 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

quite different across racial and ethnic groups, as shown by widely varying parameter estimates for the unstandardized age coefficients within our regressions. The relatively small sample sizes for Hispanic and for other non-White college-graduate families greatly diminish the statistical precision of those estimates, as reflected by considerably wider confidence intervals for β4 and β5. Nonetheless, results for these groups do not alter any of our main conclusions.

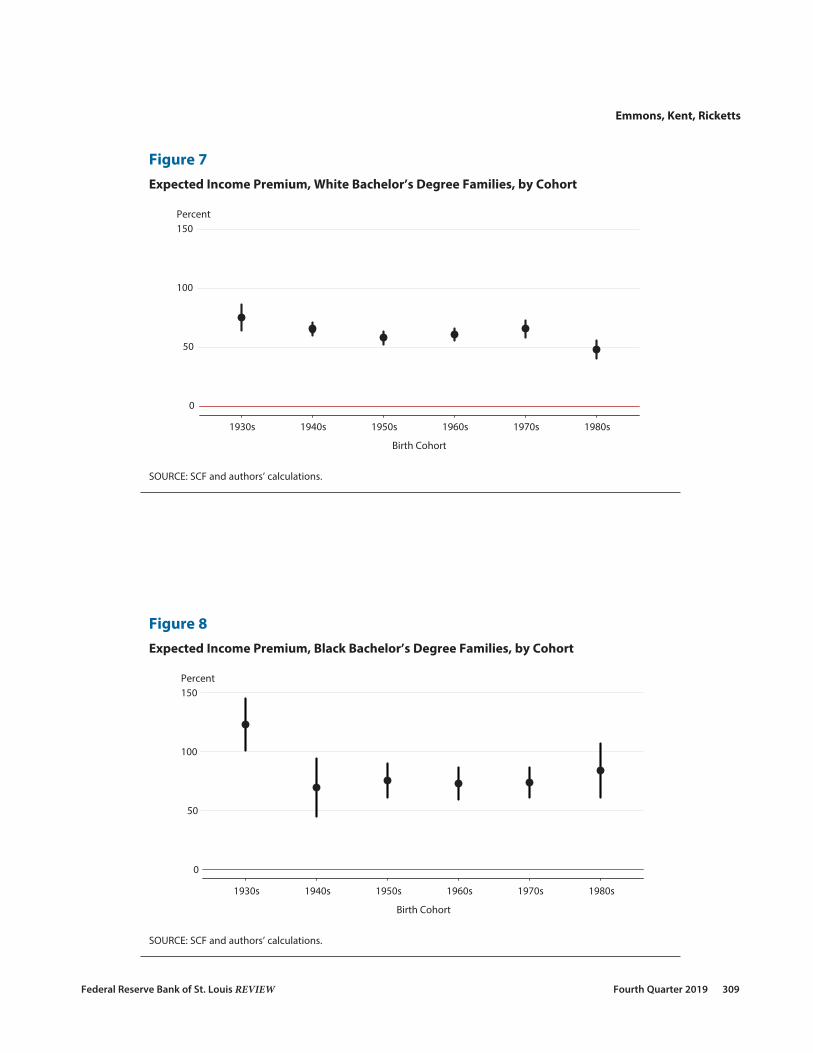

Trends in the Expected Income Premiums for Bachelor’s Degree and Postgraduate Families. We found that the college income premium over otherwise similar nongraduate families—from the same birth decade and race or ethnicity—declined somewhat among White families, on balance, between the 1930s and the 1980s birth cohorts but remained positive (Figure 7). Among Black families, there was no significant change between the 1940s and the 1980s, with all income premiums significantly above zero (Figure 8). The figures show point estimates and corresponding 95 percent confidence intervals.19

The income premium for postgraduate families over nongraduate families was typically higher at the mean relative to that for bachelor’s degree families over nongraduate families (Figures 9 and 10 for Whites and Blacks, respectively, and Figures A3 and A4 for Hispanics and other non-White families, respectively). The income premium for postgraduate White families followed a more pronounced downward trajectory than that for White bachelor’s degree families but remained positive for all cohorts. Among Black postgraduate families, the income premium ranged more widely and was large for all cohorts.20 In sum, the post-graduate families of all races and ethnicities from all six birth decades that we consider enjoy a clear income advantage over families without at least a bachelor’s degree.

Household Net Worth. Household net worth, also adjusted for household size, is our preferred measure of wealth. The SCF is considered the gold standard of balance sheet infor-mation precisely because of its detailed accounting of household assets and liabilities. Family net worth is the difference between a family’s assets and its debts at a point in time. Total assets include both financial assets, such as bank accounts, mutual funds, and securities, and tangible assets, including real estate, vehicles, and durable goods. Total debt includes home-secured borrowing (mortgages), other secured borrowing (such as vehicle loans), and unsecured debts (such as credit cards and student loans). Debt incurred in association with a privately owned business or to finance investment in real estate is subtracted from the asset’s value, rather than being included in the family’s debt. All wealth figures also are adjusted for inflation.

We adjust net worth for household size as for income:

(3) Wi = wi

Hi.

Our wealth specification has the same structural form (explanatory variables and their inter-actions) as that used to estimate the income premium. However, the transformation used for the dependent variable (W) is the inverse hyperbolic sine (IHS) transformation rather than the natural log.21 The transformed dependent variable is given by

(4) sinh−1 θWi( )= ln θWi + θ 2Wi2 +1( )

12

⎡

⎣⎢

⎤

⎦⎥ /θ ,

Emmons, Kent, Ricketts

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 309

0

50

100

150

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 8Expected Income Premium, Black Bachelor’s Degree Families, by Cohort

SOURCE: SCF and authors’ calculations.

0

50

100

150

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 7Expected Income Premium, White Bachelor’s Degree Families, by Cohort

SOURCE: SCF and authors’ calculations.

Emmons, Kent, Ricketts

310 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

0

50

100

150

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 10Expected Income Premium, Black Postgraduate Families, by Cohort

SOURCE: SCF and authors’ calculations.

0

50

100

150

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 9Expected Income Premium, White Postgraduate Families, by Cohort

SOURCE: SCF and authors’ calculations.

Emmons, Kent, Ricketts

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 311

0

200

400

600

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 12Expected Wealth Premium, Black Bachelor’s Degree Families, by Cohort

SOURCE: SCF and authors’ calculations.

0

200

400

600

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 11Expected Wealth Premium, White Bachelor’s Degree Families, by Cohort

SOURCE: SCF and authors’ calculations.

Emmons, Kent, Ricketts

312 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

0

200

400

600

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 14Expected Wealth Premium, Black Postgraduate Families, by Cohort

SOURCE: SCF and authors’ calculations.

0

200

400

600

1930s 1940s 1950s 1960s 1970s 1980s

Percent

Birth Cohort

Figure 13Expected Wealth Premium, White Postgraduate Families, by Cohort

SOURCE: SCF and authors’ calculations.

Tabl

e 4

Wea

lth

Regr

essi

ons:

Whi

te F

amili

esD

epen

dent

var

iabl

e: N

et w

orth

Raci

al/e

thni

c gr

oup:

Whi

tePs

eudo

R2 :

0.30

N: 3

7,04

4

(1)

(2)

(3)

(4)

(5)

(6)

Inde

pend

ent v

aria

bles

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

Inte

rcep

t–2

1,044

2,075

–10.1

40.0

0–2

0,491

2,134

–9.60

0.00

–20,7

582,1

83–9

.510.0

0–2

1,252

2,123

–10.0

10.0

0–2

1,962

2,084

–10.5

40.0

0–2

2,629

1,932

–11.7

10.0

0

Life c

ycle

Age

1,412

127

11.08

0.00

1,412

127

11.08

0.00

1,412

127

11.08

0.00

1,412

127

11.08

0.00

1,412

127

11.08

0.00

1,412

127

11.08

0.00

Age2

–92

–3.90

0.00

–92

–3.90

0.00

–92

–3.90

0.00

–92

–3.90

0.00

–92

–3.90

0.00

–92

–3.90

0.00

Age3

00

0.23

0.82

00

0.23

0.82

00

0.23

0.82

00

0.23

0.82

00

0.23

0.82

00

0.23

0.82

Wea

lth p

rem

ium

Term

inal

four

–yea

r gr

adua

te (G

)12

,451

633

2.47

19.66

0.00

10,82

344

61.9

524

.270.0

010

,476

444

1.85

23.59

0.00

9,791

435

1.66

22.53

0.00

8,483

633

1.34

13.39

0.00

3,511

752

0.42

4.67

0.00

Postg

radu

ate (

P)16

,151

596

4.03

27.10

0.00

15,93

544

93.9

235

.460.0

014

,727

530

3.36

27.77

0.00

13,25

166

12.7

620

.040.0

07,7

0799

51.1

67.7

40.0

02,5

061,2

830.2

81.9

50.0

5

Birth

coho

rts

Born

bef

ore 1

930

or af

ter 1

989

–1,35

438

0–0

.13–3

.560.0

0–1

,907

418

–0.17

–4.56

0.00

–1,64

045

8–0

.15–3

.580.0

0–1

,146

478

–0.11

–2.40

0.02

–436

511

–0.04

–0.85

0.39

232

520

0.02

0.45

0.66

Born

in 19

30s

(Om

itted

)–5

5336

8–0

.05–1

.500.1

3–2

8541

0–0

.03–0

.700.4

920

845

90.0

20.4

50.6

591

848

40.1

01.9

00.0

61,5

8655

40.1

72.8

60.0

0

Born

in 19

40s

553

368

0.06

1.50

0.13

(Om

itted

)26

832

30.0

30.8

30.4

176

137

60.0

82.0

30.0

41,4

7143

90.1

63.3

50.0

02,1

3952

40.2

44.0

80.0

0

Born

in 19

50s

285

410

0.03

0.70

0.49

–268

323

–0.03

–0.83

0.41

(Om

itted

)49

430

90.0

51.6

00.1

11,2

0438

20.1

33.1

50.0

01,8

7149

60.2

13.7

70.0

0

Born

in 19

60s

–208

459

–0.02

–0.45

0.65

–761

376

–0.07

–2.03

0.04

–494

309

–0.05

–1.60

0.11

(Om

itted

)71

033

90.0

72.0

90.0

41,3

7841

10.1

53.3

50.0

0

Born

in 19

70s

–918

484

–0.09

–1.90

0.06

–1,47

143

9–0

.14–3

.350.0

0–1

,204

382

–0.11

–3.15

0.00

–710

339

–0.07

–2.09

0.04

(Om

itted

)66

843

00.0

71.5

50.1

2

Born

in 19

80s

–1,58

655

4–0

.15–2

.860.0

0–2

,139

524

–0.19

–4.08

0.00

–1,87

149

6–0

.17–3

.770.0

0–1

,378

411

–0.13

–3.35

0.00

–668

430

–0.06

–1.55

0.12

(Om

itted

)

Coho

rt X

weal

th p

rem

ium

Born

bef

ore 1

930

or af

ter 1

989 *

G–2

,460

821

–0.22

–2.99

0.00

–831

684

–0.08

–1.22

0.22

–485

725

–0.05

–0.67

0.50

200

677

0.02

0.30

0.77

1,508

849

0.16

1.78

0.08

6,480

960

0.91

6.75

0.00

Born

in 19

30s *

G(O

mitt

ed)

1,629

755

0.18

2.16

0.03

1,975

718

0.22

2.75

0.01

2,660

761

0.30

3.50

0.00

3,968

883

0.49

4.49

0.00

8,940

1,030

1.44

8.68

0.00

Born

in 19

40s *

G–1

,629

755

–0.15

–2.16

0.03

(Om

itted

)34

662

70.0

40.5

50.5

81,0

3165

90.1

11.5

70.1

22,3

3976

60.2

63.0

60.0

07,3

1185

21.0

88.5

90.0

0

Born

in 19

50s *

G–1

,975

718

–0.18

–2.75

0.01

–346

627

–0.03

–0.55

0.58

(Om

itted

)68

560

70.0

71.1

30.2

61,9

9373

90.2

22.7

00.0

16,9

6589

71.0

17.7

70.0

0

Born

in 19

60s *

G–2

,660

761

–0.23

–3.50

0.00

–1,03

165

9–0

.10–1

.570.1

2–6

8560

7–0

.07–1

.130.2

6(O

mitt

ed)

1,308

736

0.14

1.78

0.08

6,280

795

0.87

7.90

0.00

Born

in 19

70s *

G–3

,968

883

–0.33

–4.49

0.00

–2,33

976

6–0

.21–3

.060.0

0–1

,993

739

–0.18

–2.70

0.01

–1,30

873

6–0

.12–1

.780.0

8(O

mitt

ed)

4,972

964

0.64

5.16

0.00

Born

in 19

80s *

* G–8

,940

1,030

–0.59

–8.68

0.00

–7,31

185

2–0

.52–8

.590.0

0–6

,965

897

–0.50

–7.77

0.00

–6,28

079

5–0

.47–7

.900.0

0–4

,972

964

–0.39

–5.16

0.00

(Om

itted

)

Born

bef

ore 1

930

or af

ter 1

989 *

P–1

,369

823

–0.13

–1.66

0.10

–1,15

373

8–0

.11–1

.560.1

255

803

0.01

0.07

0.95

1,531

841

0.17

1.82

0.07

7,075

1,154

1.03

6.13

0.00

12,27

61,2

802.4

19.5

90.0

0

Born

in 19

30s *

P(O

mitt

ed)

216

696

0.02

0.31

0.76

1,424

797

0.15

1.79

0.07

2,900

902

0.34

3.22

0.00

8,444

1,226

1.33

6.89

0.00

13,64

51,3

982.9

19.7

60.0

0

Born

in 19

40s *

P–2

1669

6–0

.02–0

.310.7

6(O

mitt

ed)

1,208

722

0.13

1.67

0.09

2,684

769

0.31

3.49

0.00

8,228

1,125

1.28

7.32

0.00

13,42

91,3

692.8

39.8

10.0

0

Born

in 19

50s *

P–1

,424

797

–0.13

–1.79

0.07

–1,20

872

2–0

.11–1

.670.0

9(O

mitt

ed)

1,476

789

0.16

1.87

0.06

7,020

1,142

1.02

6.14

0.00

12,22

11,4

412.3

98.4

80.0

0

Born

in 19

60s *

P–2

,900

902

–0.25

–3.22

0.00

–2,68

476

9–0

.24–3

.490.0

0–1

,476

789

–0.14

–1.87

0.06

(Om

itted

)5,5

441,1

960.7

44.6

30.0

010

,745

1,329

1.93

8.09

0.00

Born

in 19

70s *

P–8

,444

1,226

–0.57

–6.89

0.00

–8,22

81,1

25–0

.56–7

.320.0

0–7

,020

1,142

–0.50

–6.14

0.00

–5,54

41,1

96–0

.43–4

.630.0

0(O

mitt

ed)

5,201

1,439

0.68

3.61

0.00

Born

in 19

80s *

P–1

3,645

1,398

–0.74

–9.76

0.00

–13,4

291,3

69–0

.74–9

.810.0

0–1

2,221

1,441

–0.71

–8.48

0.00

–10,7

451,3

29–0

.66–8

.090.0

0–5

,201

1,439

–0.41

–3.61

0.00

(Om

itted

)

NO

TE: S

E, s

tand

ard

erro

r. St

anda

rd e

rror

s ar

e bo

otst

rapp

ed w

ith 9

99 re

plic

ates

in a

ccor

danc

e w

ith th

e sa

mpl

e de

sign

and

are

adj

uste

d fo

r im

puta

tion

unce

rtai

nty.

Non

resp

onse

-adj

uste

d sa

mpl

ing

wei

ghts

wer

e al

so u

sed.

Hou

seho

ld-s

ize

adju

sted

net

wor

th w

as tr

ans-

form

ed w

ith th

e in

vers

e hy

perb

olic

sin

e fu

nctio

n, w

ith a

sca

ling

fact

or o

f 0.0

001.

The

Hal

vors

en-P

alm

quis

t tra

nsfo

rmat

ion

prov

ides

a s

imila

r int

erpr

etat

ion

of th

e co

effici

ents

on

bina

ry v

aria

bles

as

that

of a

log-

linea

r mod

el.

SOU

RCE:

SCF

and

aut

hors

’ cal

cula

tions

.

Tabl

e 5

Wea

lth

Regr

essi

ons:

Bla

ck F

amili

esD

epen

dent

var

iabl

e: N

et w

orth

Raci

al/e

thni

c gr

oup:

Bla

ckPs

eudo

R2 :

0.19

N: 5

,186

(1)

(2)

(3)

(4)

(5)

(6)

Inde

pend

ent v

aria

bles

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

βSE

H–P(

β)t–

Stat

p–Va

lue

Inte

rcep

t1,8

193,0

490.6

00.5

53,1

343,1

790.9

90.3

21,4

953,3

990.4

40.6

61,2

943,3

350.3

90.7

01,7

933,2

100.5

60.5

8–9

283,2

25–0

.290.7

7

Life c

ycle

Age

–74

222

–0.33

0.74

–74

222

–0.33

0.74

–74

222

–0.33

0.74

–74

222

–0.33

0.74

–74

222

–0.33

0.74

–74

222

–0.33

0.74

Age2

105

2.22

0.03

105

2.22

0.03

105

2.22

0.03

105

2.22

0.03

105

2.22

0.03

105

2.22

0.03

Age3

00

–2.69

0.01

00

–2.69

0.01

00

–2.69

0.01

00

–2.69

0.01

00

–2.69

0.01

00

–2.69

0.01

Wea

lth p

rem

ium

Term

inal

four

–yea

r gr

adua

te (G

)18

,075

1,680

5.09

10.76

0.00

12,62

61,5

032.5

38.4

00.0

08,1

511,4

431.2

65.6

50.0

010

,201

1,115

1.77

9.15

0.00

1,662

1,420

0.18

1.17

0.24

540

1,799

0.06

0.30

0.76

Postg

radu

ate (

P)16

,542

3,115

4.23

5.31

0.00

18,07

31,4

105.0

912

.820.0

014

,631

1,817

3.32

8.05

0.00

1,664

2,487

0.18

0.67

0.50

1,468

2,844

0.16

0.52

0.61

761

3,706

0.08

0.21

0.84

Birth

coho

rts

Born

bef

ore 1

930

or af

ter 1

989

–2,31

290

0–0

.21–2

.570.0

1–3

,626

815

–0.30

–4.45

0.00

–1,98

785

9–0

.18–2

.310.0

2–1

,786

865

–0.16

–2.07

0.04

–2,28

687

8–0

.20–2

.600.0

143

583

80.0

40.5

20.6

0

Born

in 19

30s

(Om

itted

)–1

,314

757

–0.12

–1.74

0.08

325

867

0.03

0.37

0.71

525

844

0.05

0.62

0.53

2686

40.0

00.0

30.9

82,7

4791

50.3

23.0

00.0

0

Born

in 19

40s

1,314

757

0.14

1.74

0.08

(Om

itted

)1,6

3963

20.1

82.5

90.0

11,8

4065

30.2

02.8

20.0

01,3

4075

50.1

41.7

70.0

84,0

6170

80.5

05.7

40.0

0

Born

in 19

50s

–325

867

–0.03

–0.37

0.71

–1,63

963

2–0

.15–2

.590.0

1(O

mitt

ed)

201

568

0.02

0.35

0.72

–299

715

–0.03

–0.42

0.68

2,422

673

0.27

3.60

0.00

Born

in 19

60s

–525

844

–0.05

–0.62

0.53

–1,84

065

3–0

.17–2

.820.0

0–2

0156

8–0

.02–0

.350.7

2(O

mitt

ed)

–500

612

–0.05

–0.82

0.41

2,222

590

0.25

3.77

0.00

Born

in 19

70s

–26

864

0.00

–0.03

0.98

–1,34

075

5–0

.13–1

.770.0

829

971

50.0

30.4

20.6

850

061

20.0

50.8

20.4

1(O

mitt

ed)

2,721

624

0.31

4.36

0.00

Born

in 19

80s

–2,74

791

5–0

.24–3

.000.0

0–4

,061

708

–0.33

–5.74

0.00

–2,42

267

3–0

.22–3

.600.0

0–2

,222

590

–0.20

–3.77

0.00

–2,72

162

4–0

.24–4

.360.0

0(O

mitt

ed)

Coho

rt X

weal

th p

rem

ium

Born

bef

ore 1

930

or af

ter 1

989 *

G–1

6,824

4,133

–0.81

–4.07

0.00

–11,3

754,0

62–0

.68–2

.800.0

1–6

,901

3,924

–0.50

–1.76

0.08

–8,95

03,9

61–0

.59–2

.260.0

2–4

123,9

34–0

.04–0

.100.9

271

04,1

910.0

70.1

70.8

7

Born

in 19

30s *

G(O

mitt

ed)

5,449

2,260

0.72

2.41

0.02

9,923

2,246

1.70

4.42

0.00

7,874

2,041

1.20

3.86

0.00

16,41

22,1

804.1

67.5

30.0

017

,535

2,575

4.77

6.81

0.00

Born

in 19

40s *

G–5

,449

2,260

–0.42

–2.41

0.02

(Om

itted

)4,4

742,2

890.5

61.9

50.0

52,4

251,8

580.2

71.3

10.1

910

,964

2,204

1.99

4.98

0.00

12,08

62,4

312.3

54.9

70.0

0

Born

in 19

50s *

G–9

,923

2,246

–0.63

–4.42

0.00

–4,47

42,2

89–0

.36–1

.950.0

5(O

mitt

ed)

–2,04

91,7

63–0

.19–1

.160.2

56,4

892,0

450.9

13.1

70.0

07,6

112,0

961.1

43.6

30.0

0

Born

in 19

60s *

G–7

,874

2,041

–0.54

–3.86

0.00

–2,42

51,8

58–0

.22–1

.310.1

92,0

491,7

630.2

31.1

60.2

5(O

mitt

ed)

8,539

1,738

1.35

4.91

0.00

9,661

2,053

1.63

4.71

0.00

Born

in 19

70s *

G–1

6,412

2,180

–0.81

–7.53

0.00

–10,9

642,2

04–0

.67–4

.980.0

0–6

,489

2,045

–0.48

–3.17

0.00

–8,53

91,7

38–0

.57–4

.910.0

0(O

mitt

ed)

1,122

2,405

0.12

0.47

0.64

Born

in 19

80s *

* G–1

7,535

2,575

–0.83

–6.81

0.00

–12,0

862,4

31–0

.70–4

.970.0

0–7

,611

2,096

–0.53

–3.63

0.00

–9,66

12,0

53–0

.62–4

.710.0

0–1

,122

2,405

–0.11

–0.47

0.64

(Om

itted

)

Born

bef

ore 1

930

or af

ter 1

989 *

P–9

,777

6,462

–0.62

–1.51

0.13

–11,3

076,2

20–0

.68–1

.820.0

7–7

,865

6,398

–0.54

–1.23

0.22

5,102

6,451

0.67

0.79

0.43

5,298

6,163

0.70

0.86

0.39

6,004

6,725

0.82

0.89

0.37

Born

in 19

30s *

P(O

mitt

ed)

–1,53

13,2

50–0

.14–0

.470.6

41,9

123,7

300.2

10.5

10.6

114

,879

4,227

3.43

3.52

0.00

15,07

54,2

013.5

23.5

90.0

015

,781

5,345

3.85

2.95

0.00

Born

in 19

40s *

P1,5

313,2

500.1

70.4

70.6

4(O

mitt

ed)

3,442

2,315

0.41

1.49

0.14

16,40

92,9

144.1

65.6

30.0

016

,605

3,172

4.26

5.24

0.00

17,31

14,2

584.6

54.0

70.0

0

Born

in 19

50s *

P–1

,912

3,730

–0.17

–0.51

0.61

–3,44

22,3

15–0

.29–1

.490.1

4(O

mitt

ed)

12,96

72,9

872.6

64.3

40.0

013

,163

3,619

2.73

3.64

0.00

13,86

94,1

533.0

03.3

40.0

0

Born

in 19

60s *

P–1

4,879

4,227

–0.77

–3.52

0.00

–16,4

092,9

14–0

.81–5

.630.0

0–1

2,967

2,987

–0.73

–4.34

0.00

(Om

itted

)19

63,9

210.0

20.0

50.9

690

24,2

850.0

90.2

10.8

3

Born

in 19

70s *

P–1

5,075

4,201

–0.78

–3.59

0.00

–16,6

053,1

72–0

.81–5

.240.0

0–1

3,163

3,619

–0.73

–3.64

0.00

–196

3,921

–0.02

–0.05

0.96

(Om

itted

)70

65,3

490.0

70.1

30.8

9

Born

in 19

80s *

P–1

5,781

5,345

–0.79

–2.95

0.00

–17,3

114,2

58–0

.82–4

.070.0

0–1

3,869

4,153

–0.75

–3.34

0.00

–902

4,285

–0.09

–0.21

0.83

–706

5,349

–0.07

–0.13

0.89

(Om

itted

)

NO

TE: S

E, s

tand

ard

erro

r. Se

e Ta

ble

4 no

te.

SOU

RCE:

SCF

and

aut

hors

’ cal

cula

tions

.

Emmons, Kent, Ricketts

Federal Reserve Bank of St. Louis REVIEW Fourth Quarter 2019 315

where θ is a scaling parameter, which controls how much of the function’s domain is approxi-mately linear and how much resembles the natural logarithm. The IHS transformation is quite useful when working with wealth outcomes because it can accommodate negative and zero balances (unlike the natural log transformation). The scaling parameter is estimated using maximum likelihood, and we use 0.0001 as is typical in the literature.22

As shown in Halvorsen and Palmquist (1980), unlike in a log-linear model, the expected change in wealth attributed to a terminal four-year degree and postgraduate degree is not simply 100 × β4 and 100 × β5. The semi-logarithmic nature of the IHS requires a modified form of the Halvorsen-Palmquist transformation to provide a similar percentage-change interpretation. We use the same form as that used in Gale and Pence (2006): eβθ – 1.

Similar to the regressions of income, we estimate six variations of our wealth specification, switching the omitted birth cohort for each decade. Again, due to considerably different wealth life cycles and historical context, we estimate regressions separately for the four racial and ethnic groups available within the SCF (Tables 4 and 5 for White and Black families, respec-tively, and Tables A4 and A5 for Hispanic and other families, respectively).

Trends in the Estimated Wealth Premiums of College Graduates. In contrast to rela-tively stable income premiums across successive birth decades, the wealth premium enjoyed by bachelor’s degree families over otherwise demographically similar nongraduate families declined progressively between the 1930s and 1980s cohorts. Among White bachelor’s degree families, for example, the 1930s cohort owned 247 percent more wealth and the 1940s cohort owned 195 percent more wealth than nongraduate families of the same age, but the 1980s cohort owned only 42 percent more wealth (Figure 11).

Among Black bachelor’s degree families, the wealth premium peaked at 509 percent in the 1930s cohort, fell to 177 percent for the 1960s cohort, and was statistically indistinguish-able from zero for both the 1970s and the 1980s cohorts (Figure 12). In other words, we cannot reject the null hypothesis that the average Black bachelor’s degree family with a head born between 1970 and 1989 had no more wealth than the average Black nongraduate family with a head born in the same decade.

To be clear, these estimates take into account the fact that the older cohorts have had more time to accumulate wealth than the younger cohorts. Our models explicitly adjust for age by including a flexible life cycle component in each specification. Our estimates of wealth pre-miums are conditional on the amount of wealth accumulation we would expect at any given age.

The results are even starker among postgraduate families. Among White postgraduate families, the 403 percent wealth premium enjoyed by members of the 1930s cohort had shrunk to only 116 percent and 28 percent for the 1970s and 1980s cohorts, respectively (Figure 13). The drop-off for this 1970s cohort is much steeper than that for White bachelor’s degree families in the same cohort. For the 1980s cohort, the expected wealth premium for White postgraduate families over nongraduate families is statistically indistinguishable from zero at standard confidence levels. The t-statistic estimated for β5 falls to 1.95, just below the threshold for rejecting the null hypothesis that β5 = 0.23

Among Black postgraduate families, the expected wealth premium ranged from 509 per-cent for the 1940s cohort to levels slightly above but statistically indistinguishable from zero

Emmons, Kent, Ricketts

316 Fourth Quarter 2019 Federal Reserve Bank of St. Louis REVIEW

for cohorts born in the 1960s, 1970s, and 1980s (Figure 14). This suggests that, on average, postgraduate Black families with heads born in the 1960s, 1970s, or 1980s have not accumu-lated more wealth than Black nongraduate families with heads born in the same decades.

In sum, Whites are the only racial or ethnic group born in the 1980s for whom a bachelor’s degree provides a family with a reliable wealth advantage over comparable nongraduate fam-ilies—albeit one that is much smaller than those enjoyed by earlier cohorts of college gradu-ates. Even more surprisingly, the expected wealth premium among postgraduate families with a head born in the 1980s is indistinguishable from zero at standard confidence levels for all races and ethnicities.24

3 WHY HAS THE COLLEGE INCOME PREMIUM BEEN MORE DURABLE THAN THE WEALTH PREMIUM?

Why has the college wealth premium for college graduates over nongraduates declined in successive cohorts? And why do generational trends in wealth accumulation differ so mark-edly from those for income? Plausible explanations for a declining college wealth premium across successive birth cohorts—even while the college income premium remains largely intact—must satisfy three criteria:

• The explanation describes factors that affect wealth accumulation differently from how they affect income.

• The explanation is consistent with a decline in the college wealth premium that has been underway for many decades, with a large cumulative effect.

• The explanation is not primarily related to the racial and ethnic mix, the educational attainment, or the average family size of particular cohorts, since our premium esti-mates explicitly control for these elements.