is ireland? entrepreneurial · how entrepreneurial is ireland? ... list of figures page figure 1:...

TRANSCRIPT

TThhee IIrriisshh RReeppoorrtt

How

Entrepreneurial

is Ireland?

TThhee GG

lloobb

aall EE

nnttrree

pprree

nneeuurrss

hhiipp

MMoo

nniittoo

rr 22000011

TThhee IIrriiss

hh RR

eepp

oorrtt

PPaauullaa FFiittzzssiimmoonnssCCoollmm OO’’GGoorrmmaannFFrraannkk RRoocchhee

PPaauullaa FFiittzzssiimmoonnssCCoollmm OO’’GGoorrmmaannFFrraannkk RRoocchhee

HHooww EEnnttrreepprreenneeuurriiaall iiss IIrreellaanndd??

Sponsored by:

How Entrepreneurial is Ireland?

The Global Entrepreneurship Monitor 2001

The Irish Report

Paula Fitzsimons Colm O’Gorman Frank Roche

Sponsored by: Enterprise Ireland and Forfas

Enterprise Ireland and Forfas are the principal sponsors of this independent report, the findings of which donot necessarily represent the views of these organisations.

The authors have attempted to ensure accuracy and completeness of the information contained in thispublication. However, no responsibility can be accepted for any errors and inaccuracies that occur.

This report was published by the

Department of Business AdministrationUniversity College Dublin.

Printed by Cahill Printers Limited, East Wall Road, Dublin 3

Contents

Page

Executive Summary … … … … … … … … … … … … 1

1. THE GEM PROJECT … … … … … … … … … … … 5

1.1. History of the Project … … … … … … … … … … 5

1.2. GEM Definition of Entrepreneurship … … … … … … … … 5

1.3. Thesis to be Proven … … … … … … … … … … 5

1.4. The GEM Theoretical Model … … … … … … … … … 5

1.5. How GEM Collects Data … … … … … … … … … 7

2. THE GEM RESULTS… … … … … … … … … … … … 9

2.1. The GEM Results … … … … … … … … … … … 9

2.2. Level of Entrepreneurship Across Countries … … … … … … 10

2.3. Entrepreneurship and Economic Growth … … … … … … … 12

2.4. Entrepreneurial Motivation … … … … … … … … … 12

2.5. Personal Characteristics of Entrepreneurs … … … … … … … 15

2.6. Entrepreneurial Framework Conditions … … … … … … … 18

2.6.1. Cultural and Social Norms … … … … … … … … 182.6.2. Financial Support … … … … … … … … … 192.6.3. Government Policies … … … … … … … … … 20

2.7. Formal and Informal Business Investment … … … … … … … 21

3. 3. HOW ENTREPRENEURIAL IS IRELAND? … … … … … … … … 23

3.1. Introduction … … … … … … … … … … … 23

3.2. Overall Results … … … … … … … … … … … 23

3.3. Backdrop to Entrepreneurship in Ireland … … … … … … … 25

3.4. Key Entrepreneurial Framework Conditions: Ireland’s Relative Position … … 26

3.4.1. Financial Support … … … … … … … … … 263.4.2. Cultural and Social Norms … … … … … … … … 273.4.3. Government Policies … … … … … … … … … 28

3.5. The Other Entrepreneurial Framework Conditions … … … … … 29

3.5.1. Government Programmes … … … … … … … … 293.5.2. Education and Training … … … … … … … … 303.5.3. R & D Transfer … … … … … … … … … … 313.5.4. Professional and Commercial Infrastructure … … … … … 313.5.5. Internal Market Openness … … … … … … … … 323.5.6. Access to Physical Infrastructure … … … … … … … 32

iii

Global Entrepreneurship Monitor

3.6. Entrepreneurial Characteristics Among the Irish People … … … … … 32

3.6.1. Entrepreneurial Opportunity … … … … … … … … 333.6.2. Entrepreneurial Capacity … … … … … … … … 333.6.3. Age and Gender of Entrepreneurs … … … … … … … 35

3.7 Conclusion … … … … … … … … … … … … 35

4. MAKING IRELAND MORE ENTREPRENEURIAL … … … … … … … 37

4.1 What GEM Has Achieved for Ireland… … … … … … … … 37

4.2 The Focus of the Recommendations … … … … … … … … 37

4.3 Championing Entrepreneurial Activity … … … … … … … 38

4.4 Actively Encouraging More Women Entrepreneurs … … … … … 39

4.5 Building Entrepreneurial Capacity … … … … … … … … 39

4.6 Making Seed Funding More Accessible … … … … … … … 40

4.7 Commercialising Publicly Funded Research … … … … … … … 41

4.8 Removing Infrastructural Inefficiencies … … … … … … … 41

APPENDIX 1

GEM 2000 and GEM 2001: Understanding the Change in Ireland’s Position … … … 43

iv

List of Figures

Page

Figure 1: The GEM Theoretical Model … … … … … … … … 2

Figure 2: Total Entrepreneurial Activity … … … … … … … … 10

Figure 3: Nascent vs. New Firm Entrepreneurs … … … … … … … 11

Figure 4: Opportunity vs. Necessity Entrepreneurship … … … … … … 13

Figure 5: Entrepreneurial Activity by Gender and Age … … … … … … 16

Figure 6: Entrepreneurial Activity by Gender and Educational Attainment … … … 17

Figure 7: Informal Investment by Country … … … … … … … … 21

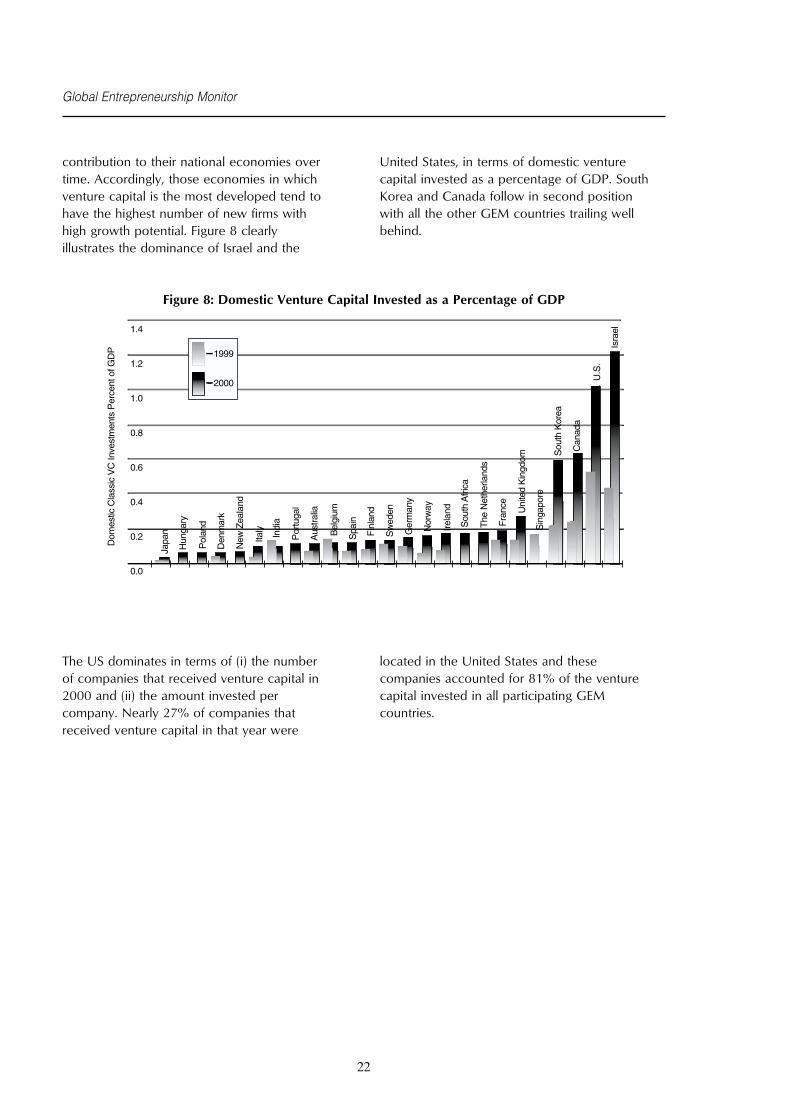

Figure 8: Domestic Venture Capital Invested as a Percentage of GDP … … … 22

v

List of Tables

Page

Table 1: GEM Countries Categorised on the Basis of their Entrepreneurial Activity 11

Table 2: Entrepreneurship Motives and Selected Sectors … … … … … 14

Table 3: Entrepreneurship Motives and Growth Expectations… … … … … 15

Table 4: Educational Attainment and Type of Entrepreneurial Ventures … … … 18

Table 5: Global Experts’ Evaluations: Culture and Social Norms … … … … 19

Table 6: Global Experts’ Evaluations: Financial Support … … … … … 20

Table 7: Global Experts’ Evaluations: Government Policy … … … … … 20

Table 8: Summary of the Results for Ireland … … … … … … … 24

Table 9: Summary of All Experts’ Evaluations … … … … … … … 25

Table 10: Ireland’s Relative Position … … … … … … … … … 26

Table 11: Experts’ Evaluations: Financial Support … … … … … … … 27

Table 12: Experts’ Evaluations: Cultural and Social Norms … … … … … 27

Table 13: Experts’ Evaluations: Government Policy … … … … … … 29

Table 14: Experts’ Evaluations: Government Programmes … … … … … 30

Table 15: Experts’ Evaluations: Education and Training … … … … … … 30

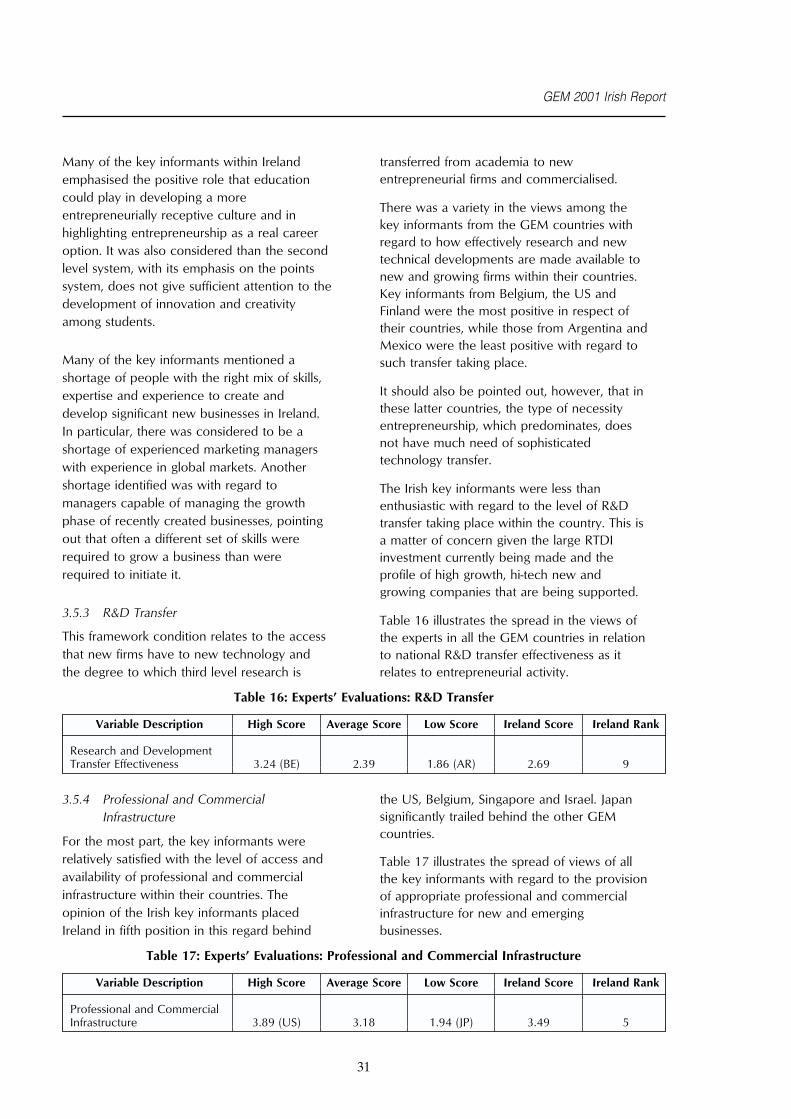

Table 16: Experts’ Evaluations: R&D Transfer … … … … … … … 31

Table 17: Experts’ Evaluations: Professional and Commercial Infrastructure … … … 31

Table 18: Experts’ Evaluations: Internal Market Openness … … … … … 32

Table 19: Experts’ Evaluations: Physical Infrastructure … … … … … … 32

Table 20: Experts’ Evaluations: Entrepreneurial Opportunity … … … … … 33

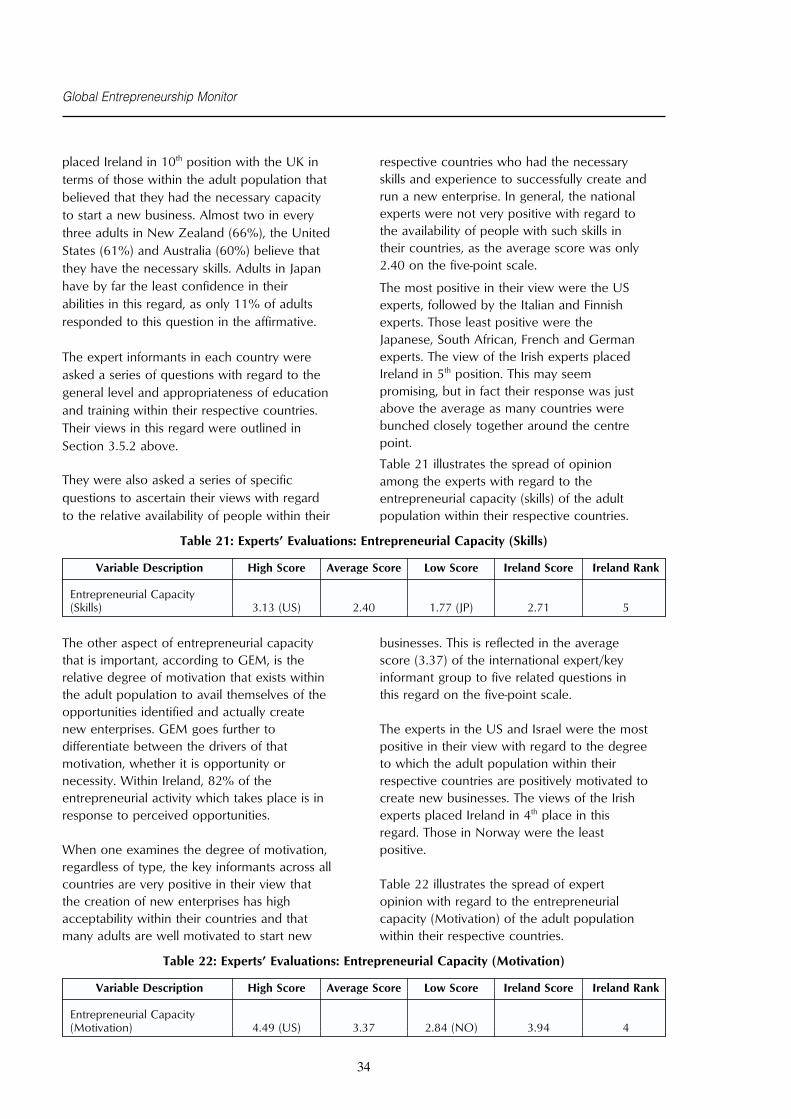

Table 21: Experts’ Evaluations: Entrepreneurial Capacity (Skills) … … … … 34

Table 22: Experts’ Evaluations: Entrepreneurial Capacity (Motivation) … … … 34

vi

Acknowledgements

The Irish GEM team would like to thank all theexpert informants that were interviewed as partof this research. They gave generously of theirtime and their insights enriched ourunderstanding of the current state ofentrepreneurship in Ireland.

vii

We would also like to thank our sponsors,Enterprise Ireland and Forfas, without whosegenerous sponsorship Ireland’s participation inGEM 2001 would not have been possible.

The GEM 2001 Irish Research Team

Paula Fitzsimons, the national co-ordinator for Contact DetailsGEM, is an independent strategy and Paula Fitzsimons, 10 Grove Lawn, Malahide,management consultant, specializing in Co. Dublin.sectoral and enterprise development strategies. Tel: +353 87 277 4385;Her clients include government development Fax: +353 1 845 0770;agencies and individual start-up and developing E-mail: [email protected].

Dr. Colm O’Gorman is a lecturer in the Contact DetailsUndergraduate Business School and the Dr. Colm O’Gorman,Michael Smurfit Graduate Business School in Tel: +353 1 7168210;the Faculty of Commerce at the University Fax: +353 1 7161132;College, Dublin. He specialises in the areas of E-mail: [email protected] strategy and enterprisedevelopment.

Dr. Frank Roche holds the Berber Family Chair Contact Detailsof Entrepreneurship and is Head of the Dr. Frank Roche,Department of Business Administration and Tel: +353 1 7168820;Director of the Enterprise Centre at the Fax: +353 1 7168954Michael Smurfit Graduate School of Business E-mail: [email protected] University College Dublin. His teaching andresearch are now concentrated in the area ofentrepreneurship and corporate venturing. Heis Vice Chairman of the Dublin BusinessInnovation Centre and works closely with anumber of start-up companies.

Dublin, June 2002

ix

Executive Summary

The recently completed GlobalEntrepreneurship Monitor 2001 (GEM) ranksIreland 6th in terms of the overallentrepreneurial propensity of its adultpopulation across 29 countries. This is arevised result and corrects the very lowposition that Ireland obtained in GEM 2000.1

GEM is an international research programmerun jointly by London Business School andBabson College in the USA. It seeks to bringtogether some of the world’s leadingresearchers in the area of entrepreneurship toexplore three related questions:

• Does the level of entrepreneurialactivity vary between countries, and, ifit does, to what extent?

• Does the level of entrepreneurialactivity affect a country’s rate ofeconomic growth and prosperity?

• What makes a country entrepreneurial?

As a result of its analysis over three years,GEM clearly demonstrates that the level ofentrepreneurial activity differs betweencountries, and that entrepreneurial motivationdiffers between developing countries (‘‘push’’or necessity entrepreneurship) and those withmore developed economies (‘‘pull’’ oropportunistic entrepreneurship). Ireland quiteclearly falls into the latter category with 82% ofentrepreneurs responding to perceivedopportunities. The link betweenentrepreneurship and growth, however, is notas clear as originally thought. The level ofentrepreneurship and growth can only beclearly demonstrated in those countries withless developed economies.

1 New information came to light in September 2001, which cast doubt on the accuracy of the previous results for Ireland.Appendix 1 gives a detailed explanation as to how this situation came about.

2 ‘‘Capacity’’ in this context means possessing both the skills and motivation to bring the perceived entrepreneurial opportunity tocommercial reality.

1

The year 2001 is the third consecutive year inwhich this study has taken place. Each yearmore countries are becoming involved. GEMbegan as a pilot study in 1999 with 10countries involved. It grew to involve 21countries in 2000 and 29 countriesparticipated in the 2001 study. This is Ireland’ssecond year of participation. Forfas andEnterprise Ireland co-sponsored Ireland’sinvolvement in GEM in 2001.

GEM uses four research instruments in exactlythe same way in each of the participatingcountries. In this way, cross countycomparisons can be made. The instruments areas follows:

(i) A population survey of approximately2,000 adults;

(ii) Face to face in-depth interviews with atleast 36 key or expert informants onvarious aspects of entrepreneurship;

(iii) A detailed questionnaire completed bythe experts interviewed; and

(iv) Various comparable national economicdata.

GEM identifies nine framework conditions that,together with the degree of entrepreneurialrecognition and capacity2 within the adultpopulation, have a significant bearing on thediffering levels of entrepreneurial activityamong the adult population betweencountries.

The GEM 2001 results of the adult populationsurvey for Ireland confirm the views of theexperts interviewed. A generally supportiveenvironment now exists within Ireland for

Global Entrepreneurship Monitor

entrepreneurship. A summary of the mainresults of GEM 2001 for Ireland is as follows:

• 7.2% of the adult population iscurrently engaged in the process oftrying to start a new business. These arereferred to as nascent entrepreneurs.This level of activity places Ireland 12th

among the 29 countries;

• 4.8% of the adult population currentlypartly or fully own and operate abusiness that was started since 1998.These are referred to as new firmentrepreneurs. This level of activityamong new firm entrepreneurs placesIreland 6th; and

• 3% of all start-ups are perceived bytheir founders to have high growthpotential3. This result places Ireland in10th place among the 29 countries.

GEM clearly demonstrates the importance ofinformal or ‘‘business angel’’ investment insupporting new ventures. Just over 3% of Irishadults have informally invested in this way overthe last three years in a new venture started bysome one else. This result places Ireland justabove the average among GEM participatingcountries in terms of business angel investmentin new enterprises.

Areas that GEM highlights as a matter ofconcern for Ireland is the relative unavailabilityof seed funding, the low number of womenentrepreneurs, and infrastructural inefficienciesthat are beginning to have a negative effect onthe country’s overall relative internationalcompetitiveness.

There is general agreement that the positiveenvironment for entrepreneurship that exists inIreland should be further strengthened. To thisend, six recommendations are outlined whichare designed to achieve this objective bybuilding on Ireland’s strengths in this area,while seeking to overcome identifieddeficiencies.

3 ‘‘High growth potential’’ is defined as being capable of employing 50 people within five years.

2

In summary, the recommendations that arebeing proposed for Ireland by the Irish GEMteam are as follows:

• Entrepreneurial activity and itsconsequent benefits should bechampioned at national level.

• The barriers preventing a greaterinvolvement by women inentrepreneurial activity should besystematically identified and theirparticipation must be activelyencouraged and supported.

• A series of educational and traininginitiatives should be designed todevelop both the required skills andconfidence in individuals, through theformal general education system andthrough entrepreneurial specificinitiatives.

• The availability of pre- and start-up seedcapital for different types of business’needs should be reviewed and any gapsin the availability of financing should beaddressed. The relative attractivenessfor investors of investing in early stageenterprises should also be examinedand the risk/reward of such investmentmade more attractive through fiscalincentives

• Means of transferring the significantresearch, technological developmentand innovation (RTDI) investment,currently being implemented, into newentrepreneurial initiatives should beactively encouraged and any barriers toits transfer should be identified andremoved.

• The inefficiencies and shortcomings inthe country’s physical andtelecommunications infrastructureshould be addressed with a real senseof urgency.

These recommendations are detailed inSection 4.

GEM 2001 Irish Report

GEM has given Ireland for the first time ameans of benchmarking the entrepreneurialpropensity of its adult population against 28other countries. It also provides access to arange of international research and policyinitiatives, so that Ireland can learn from theexperience of other countries, ways and meansof encouraging a greater level ofentrepreneurial drive and initiative among itsadult population. International researchindicates that the more entrepreneurial activitythere is within a country, the greater thenumber of value adding, high growth potentialnew ventures that will be initiated.

3

The number of countries participating in GEMis set to rise to almost 40 in 2002 as more andmore countries perceive the benefits whichparticipation can convey. The Irish GEM teamis determined to ensure that Ireland will remainfully committed to GEM so that the countrycan continue to enjoy the benefits of collectivelearning, together with the means of measuringprogress towards the goal of becoming aleading entrepreneurial nation.

CHAPTER 1

The GEM Project

1.1 History of the Project

The Global Entrepreneurship Monitor (GEM) isa research programme run jointly by LondonBusiness School and Babson College in theUSA. The research also involves a consortiumof teams from each of the countries involvedin the study. In 2001, 29 countriesparticipated4.

The aim of GEM is to create an annualassessment of the levels of entrepreneurialactivity across countries. The research alsoexplores a variety of factors both within andacross countries that might give rise tosystematic differences in entrepreneurshiprates. Through a greater understanding of thesefactors, policies to enhance the level ofentrepreneurial activity can be based on solidresearch and the role of entrepreneurship incontributing to a positive economicenvironment can be better understood.

GEM began in 1999. The first study began with10 countries5, expanded to 216 in the year2000, and to 297 countries in 2001. In 2002, itis expected that the number of participatingcountries will rise to about 40.

1.2 GEM Definition ofEntrepreneurship

For the purposes of the research, GEM uses avery comprehensive definition ofentrepreneurship, which encompasses any type

4 Argentina, Australia, Belgium, Brazil, Canada, Denmark, Finland, France, Germany, Hungary, India, Ireland, Israel, Italy, Japan,Mexico, Netherlands, Norway, New Zealand, Poland, Portugal, Russia Singapore, South Africa, Spain, South Korea, Sweden, UK,and USA.

5 Canada, Denmark, Finland, France, Germany, Israel, Italy, Japan, UK and USA.6 Ireland was among the countries that participated in GEM for the first time in 2000. The other first time participants in that year

were Argentina, Australia, Belgium, Brazil, India, Norway, Singapore, Spain, South Korea and Sweden.7 The first time participants in GEM 2001 were Hungary, Mexico, Netherlands, New Zealand, Poland, Portugal, Russia and South

Africa.

5

of entrepreneurial initiative, including self-employment. The Total EntrepreneurshipActivity (TEA) rating is made up of thoseactively planning to become entrepreneurs,and taking some specific actions to bring thisabout, (categorised by GEM as ‘‘nascent’’entrepreneurs) and those who have set up anew enterprise in the 42 months prior to thecarrying out of the adult population survey(categorised by GEM as ‘‘new firm’’entrepreneurs).

1.3 Thesis to be Proven

GEM was designed to answer threefundamental questions:

(i) Does the level of entrepreneurialactivity vary between countries, and, ifit does, to what extent?

(ii) Does the level of entrepreneurialactivity affect a country’s rate ofeconomic growth and prosperity?

(iii) What makes a country entrepreneurial?

1.4 The GEM Theoretical Model

Most studies of economic performance focuson the ‘primary economy’ of large, establishedfirms and industries, and the ‘secondaryeconomy’ of small and medium sizedenterprises. The focus is, therefore, onenterprises already established, in other words

Global Entrepreneurship Monitor

the ‘‘status quo’’. The entrepreneurial sector,(i.e. start-ups and new firms), is missing.

The GEM model specifically incorporates boththe established and entrepreneurial sectors andillustrates the relationship between them. GEM

Figure 1: The GEM Theoretical Model

General NationalFramework Conditions

MajorEstablished Firms

Micro, Small andMedium Firms

EntrepreneurialOpportunities

EntrepreneurialFramework Conditions

EntrepreneurialCapacity

BusinessChurning

Social,Cultural,PoliticalContext

NationalEconomicGrowth

The general environment, which pertains withina particular country at a point in time,influences both new and existing firms. Thecharacteristics of this general environment arereferred to in GEM as the ‘‘NationalFramework Conditions’’.

The National Framework Conditions are asfollows:

• The relative openness of the economy,

• The role and extent of Governmentintervention,

• The efficiency of the financial markets,

• The level and intensity of technologyand R&D,

• The physical infrastructure,

• The availability and extent ofmanagement skills,

6

seeks to examine the strength and influence ofthe entrepreneurial sector, (i.e. the effect ofnew firm creation and growth,) on theeconomy.

The model for GEM is illustrated indiagrammatic form in Figure 1.

• The degree of flexibility in the labourmarket,

• The degree to which institutions areunbiased and the rule of law prevails.

In addition to this, there is a set of factors thatGEM has identified as specifically influencingthe entrepreneurial sector. These are termedthe ‘‘Entrepreneurial Framework Conditions’’.The Entrepreneurial Framework Conditions areas follows:

• Financial

• Government Policies

• Government Programmes

• Education and Training

• R&D Transfer

• Commercial Infrastructure

GEM 2001 Irish Report

• Internal Market Openness

• Physical Infrastructure

• Cultural and Social Norms.

There is somewhat of an overlap between theNational Framework Conditions and thosespecifically affecting entrepreneurship, butwithin the Entrepreneurial FrameworkConditions, it is the relative effect of theCondition for a new firm that is the issue. Forexample, there may be instances withincountries whereby the general financialenvironment is supportive of establishedbusinesses, but is less available to and lesssupportive of new businesses.

GEM suggests that at the heart of theexplanation of the relative entrepreneurialpropensity of a country’s adult population is acombination of the following:

• Differences in the nine EntrepreneurialFramework Conditions betweencountries;

• The relative perceptiveness of the adultpopulation of new ventureopportunities, (‘‘entrepreneurialopportunity’’); and

• The capacity and motivation of theadult population to capitalise on suchopportunities (‘‘entrepreneurialcapacity’’).

1.5 How Gem Collects Data

The GEM model incorporates four fundamentalresearch instruments8 in order to explore thesequestions. These instruments are as follows:

(i) A population survey, based on arandom sample of approximately 2,000adults.

(ii) Face-to-face interviews with at least 36experts (called ‘key informants’) onvarious aspects of entrepreneurship.

(iii) A detailed questionnaire completed bythe experts interviewed.

8 (i) and (iv) are the responsibility of the GEM central co-ordination team and (ii) and (iii) are the responsibility of the nationalteam.

7

(iv) The use of selected national economicdata, measured in standard units, fromcredible international sources includingthe Organisation for EconomicCooperation and Development(OECD), the World Bank, and theWorld Competitiveness Yearbook.

Details of each of these instruments arecontained in the paragraphs that follow.

(i) Adult Population Survey

Professional survey research firms in eachcountry administer the adult populationsurveys, which are based on a random sampleof approximately 2,000 adults. Samplingprocedures vary somewhat, but all of thesurvey firms are able to provide samples thatare, when properly weighted, representative ofthe adult population in each country.

Telephone interviews are utilized in Ireland, asin most of the developed countries, wheremost households have a telephone. Theinterview completion time ranges from a lowof 60 seconds to a high of 15 minutes,depending on the extent of the respondent’sinvolvement in entrepreneurial activity. The firstfour items asked of all those interviewed arerelated to participation in entrepreneurialactivities — starting a new firm, owning andmanaging a new firm and informally investingin another’s new firm. Anyone engaged in anyof these activities is asked for additionalselected details about that activity.

A further six items, also asked of all thoseinterviewed, are for assessing attitudes towardsand knowledge of the entrepreneurial climate.

(ii) Expert Informant Interviews

Expert informants are chosen by reputationand referrals to represent the nineentrepreneurial framework dimensions in theGEM model as outlined above. At least threeexperts should come from each of the nineentrepreneurial framework conditions and 25%of them should be entrepreneurs. The GEMnational team conducts face-to-face interviews

Global Entrepreneurship Monitor

with at least 36 such experts, called ‘‘keyinformants’’. The interviews attempt toascertain the views of national experts on thefactors that have been shown to influence thelevel of entrepreneurial activity.

(iii) Detailed Questionnaires Completed bythe ‘‘Key Informants’’

The experts interviewed also complete adetailed questionnaire. The group of experts,chosen for an in-depth face-to-face interview,complete this questionnaire in the presence ofthe interviewer at the end of the interview,while experts interviewed in the precedingyear(s) are requested to complete thequestionnaire and return it by post.

Expert self-completed questionnaires, translatedinto the national languages, consist of those

8

items asked in the adult population survey,plus an additional 69 five-point scale itemscovering a range of topics relating to theEntrepreneurial Framework Conditions, theentrepreneurial capacity and opportunityrecognition perceptiveness of the adultpopulation, as well as other socio-demographicitems. These questionnaires take about 15minutes to complete.

(iv) National Economic Data

Standardized cross-national data on a variety ofnational characteristics and attributes (e.g.,growth in GDP) are assembled from a widerange of harmonized international sources.Sources include the United Nations, Eurostat,ILO, U.S. Census International Data Base,World Bank, and International Monetary Fund,among others.

CHAPTER 2

The GEM Results

2.1 The GEM Results

GEM has identified the following trends acrossthe participating countries.

(i) The level of entrepreneurship differssubstantially between countries.

(ii) Only in the less developed countrieshas a link between entrepreneurshipand growth been demonstrated.

(iii) There is a distinct difference inentrepreneurship motivation (Necessityvs. Opportunistic) between countries.This has a significant impact on thegrowth potential of the entrepreneurialactivity in a country. For example, onein seven opportunity drivenentrepreneurs expects that their newbusiness will grow significantly, whileonly one in fifty necessityentrepreneurs have such growthexpectations. Opportunityentrepreneurship is also more prevalentin certain sectors of the economy.

(iv) The age, gender and educationalattainment levels of the adultpopulation has a profound effect onthe level, type and scale ofentrepreneurial activity within acountry.

Those who believe that there are goodopportunities within their communitiesto start a business are three times morelikely to be entrepreneurially activethan are those who do not believe thatsuch opportunities exist. While thosethat consider that they have the skillsto create and run a successful businessare six times more likely to beentrepreneurially active. Among thosepursuing opportunities, it is those withthe higher levels of education who arethe most entrepreneurially active. Thisholds true for both men and women.

9

(v) Three Entrepreneurial FrameworkConditions are generally considered bythe international group of experts asparticularly facilitating higher levels ofentrepreneurial activity. These are asfollows:

• Cultural and Social Norms,

• Financial Supports, and

• Government Policies.

The key informants, in the moreentrepreneurially active countries,placed particular emphasis on the needto encourage women and minorities tobe more entrepreneurial and to createa mind-set of creativity and innovation;to improve the risk assessment culturein the financial community; to increasethe long-term, strategic focus ingovernments’ perception of thebenefits of encouraging and supportingentrepreneurship; and to deepengovernments’ understanding ofentrepreneurship.

(vi) The level of informal and formalbusiness investment differs significantlybetween countries, with the USdominating in virtually every area inthis regard. Policy makers oftenunderestimate the significance ofinformal investment in entrepreneurialventures, with few realising that itrepresents the equivalent of 1.1% ofGDP on average across all GEMcountries. While venture capital isinvested in a much smaller number ofnew enterprises, those in which it isinvested tend to grow larger morequickly.

The paragraphs that follow analyse the GEMresults across the 29 countries in more detail ineach of the areas (i) to (vi) outlined above.

Global Entrepreneurship Monitor

Section 3 ‘‘How Entrepreneurial is Ireland?’’focuses specifically on the results for Ireland.

2.2 Level of Entrepreneurship acrossCountries

Figure 2 illustrates the results of GEM 2001 interms of the entrepreneurial activity of theadult populations across the 29 countries. Therange of entrepreneurial activity across the

Figure 2: Total Entrepreneurial Activity

Per

sons

per

100

Adu

lts, 1

8-64

Yrs

old

(95%

Con

fiden

ce In

terv

al)

25.00

20.00

15.00

10.00

5.00

0.00

Bel

gium

Japa

n

Sin

gapo

re

Isra

el

The

Net

herla

nds

Sw

eden

Rus

sia

Ger

man

y

Por

tuga

l

Fra

nce

Uni

ted

Kin

gdom

Spa

in

Den

mar

k

Nor

way

Fin

land

Sou

th A

frica

Pol

and

Italy

Arg

entin

a

Can

ada

Indi

a

Hun

gary

U.S

.

Irela

nd

Bra

zil

Kor

ea Aus

tralia N

ew Z

eala

nd

Mex

ico

All

Cou

ntrie

s

Upper

Average

Lower

The GEM study divides countries, based ontheir adult population survey, into twogroupings in terms of their entrepreneurialactivity rating. Counties are categorised as‘‘High’’ or ‘‘Low’’ based on the level ofentrepreneurial activity among their adultpopulations. Within the ‘‘High’’ category isincluded any country equal to or above the

10

participating countries differs substantially, froma low of less than 5% in Belgium to a high ofapproximately 18% in Mexico.

Mexico and New Zealand appear to lead agroup of five countries with generally higherentrepreneurial prevalence rates than all otherGEM 2001 countries. However, the rank orderamong the five is uncertain since thedifferences between the countries are notstatistically significant.

median prevalence rate. Within the ‘‘Low’’category is included any country below themedian prevalence rate on the TotalEntrepreneurial Activity (TEA) Index.

Table 1 lists the countries in alphabetical orderin each category.

GEM 2001 Irish Report

Table 1: GEM countries categorized on the basis of their entrepreneurial activity

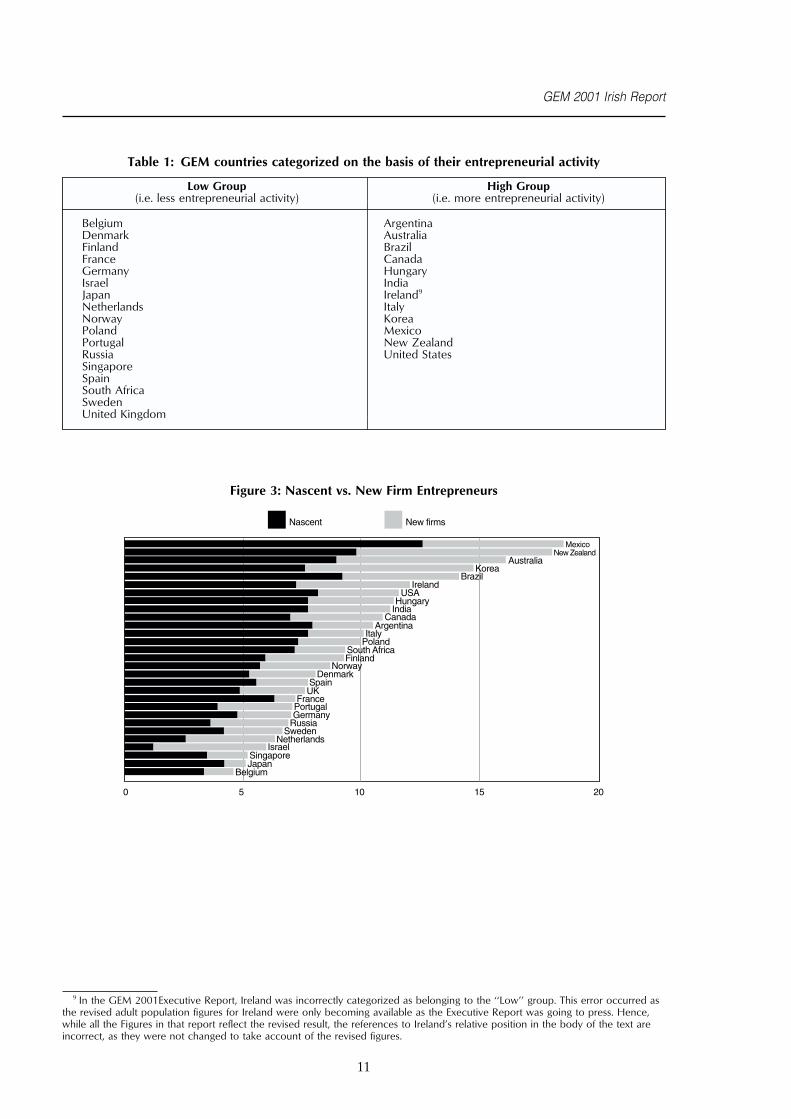

Low Group High Group(i.e. less entrepreneurial activity) (i.e. more entrepreneurial activity)

Belgium ArgentinaDenmark AustraliaFinland BrazilFrance CanadaGermany HungaryIsrael IndiaJapan Ireland9

Netherlands ItalyNorway KoreaPoland MexicoPortugal New ZealandRussia United StatesSingaporeSpainSouth AfricaSwedenUnited Kingdom

Figure 3: Nascent vs. New Firm Entrepreneurs

Mexico

0 5 10 15 20

Nascent New firms

New ZealandAustralia

KoreaBrazil

IrelandUSA

HungaryIndia

CanadaArgentina

ItalyPoland

South AfricaFinland

NorwayDenmark

SpainUK

FrancePortugalGermany

RussiaSweden

NetherlandsIsrael

SingaporeJapan

Belgium

9 In the GEM 2001Executive Report, Ireland was incorrectly categorized as belonging to the ‘‘Low’’ group. This error occurred asthe revised adult population figures for Ireland were only becoming available as the Executive Report was going to press. Hence,while all the Figures in that report reflect the revised result, the references to Ireland’s relative position in the body of the text areincorrect, as they were not changed to take account of the revised figures.

11

Global Entrepreneurship Monitor

As might be expected, in almost everycountry10 there are much greater numbers ofpeople planning to start a new business(nascent entrepreneurs) than actually bring anew enterprise into being (new firmentrepreneurs).

Across the GEM countries, 6.3% of all adultsare actively planning a new business and arecategorised as ‘‘nascent entrepreneurs’’, while3.5% of entrepreneurs identified by GEMacross all countries have actually started a newenterprise over the previous 42 months andare categorised as ‘‘new firm’’ entrepreneurs.

Figure 3 illustrates for each of the countries therelative proportion of nascent and new firmentrepreneurs.

2.3 Entrepreneurship and EconomicGrowth

One of the initial objectives of GEM was toenquire whether the level of entrepreneurialactivity affected a country’s rate of economicgrowth and prosperity.

While the first study (1999) appeared to showa strong correlation between the level ofentrepreneurial activity in a country and itsgrowth rate, as the number of countriesinvolved in GEM expanded and included agreater variety in terms of size, stage ofdevelopment and propensity to tradeinternationally, the connection betweenentrepreneurship and economic growth wasperceived to be more complex.

The 2000 Report asserted that despite variousresearch initiatives ‘‘. . . remarkably little isknown about the relationship betweenentrepreneurship and economic growth,including how it works, what determines itsstrength and the extent to which it holds fordiverse countries.’’11

GEM 2001 was able to demonstrate a positivecorrelation between ‘‘Necessity’’entrepreneurship and GDP growth. In otherwords, where there was a high level of

10 Israel is a clear exception to this trend in 2001. This may have more to do with the political situation within in the country atthis time, however, rather than an inherently different underlying trend.

11 Reynolds, Hay, Bygrave, Camp and Autio, 2000.12 Garelli Stephane, The World Competitiveness Yearbook: 2000. Lausane, Switzerland International Institute for Management

Development. In 1999 and again in 2000, Singapore was ranked 2nd, just behind the United States.13 GEM 2000 (4.1% — 21st/21) and GEM 2001 (5.2% — 27th/29).14 Ireland is ranked 7th in the 2000 report, having been ranked 5th in the previous year’s report. Ireland’s relative position for 2001

has, however, fallen back to 10th position.

12

necessity entrepreneurship, and this tended tooccur in the less affluent, less developedcountries, the level of economic growth in thecountry tended to be high. India, Mexico andBrazil are examples of countries where thisrelationship is present. This correlation was notfound between ‘‘Opportunity’’entrepreneurship and GDP growth.

In the more developed countries, GEMsuggests that the desirable combination is ahigh degree of competitiveness relative toother countries, allied to a high level ofentrepreneurial propensity among its adultpopulation. Moreover, the entrepreneurialmotivation will tend to be based on a responseto perceived opportunity rather than on‘‘necessity entrepreneurship’’.

In certain countries, such as Singapore, whilethe country ranks well in the WorldCompetitiveness Index12, the level ofentrepreneurial activity among its adultpopulation is relatively low13. In response tothis situation, the Government of Singapore isactively promoting technology-basedentrepreneurship through its‘‘Technopreneurship 21’’ initiative, which itlaunched in 2000.

Ireland, on the other hand, ranks relatively wellon all three dimensions- relative internationalcompetitiveness14; a high level ofentrepreneurial activity among its adultpopulation; and a high level of opportunityrather than necessity driven entrepreneurship.

2.4 Entrepreneurial Motivation

GEM clearly demonstrates that the level ofentrepreneurial activity differs betweencountries. It also shows that the motivationaldrive behind the entrepreneurial activity differsbetween countries.

GEM 2001 Irish Report

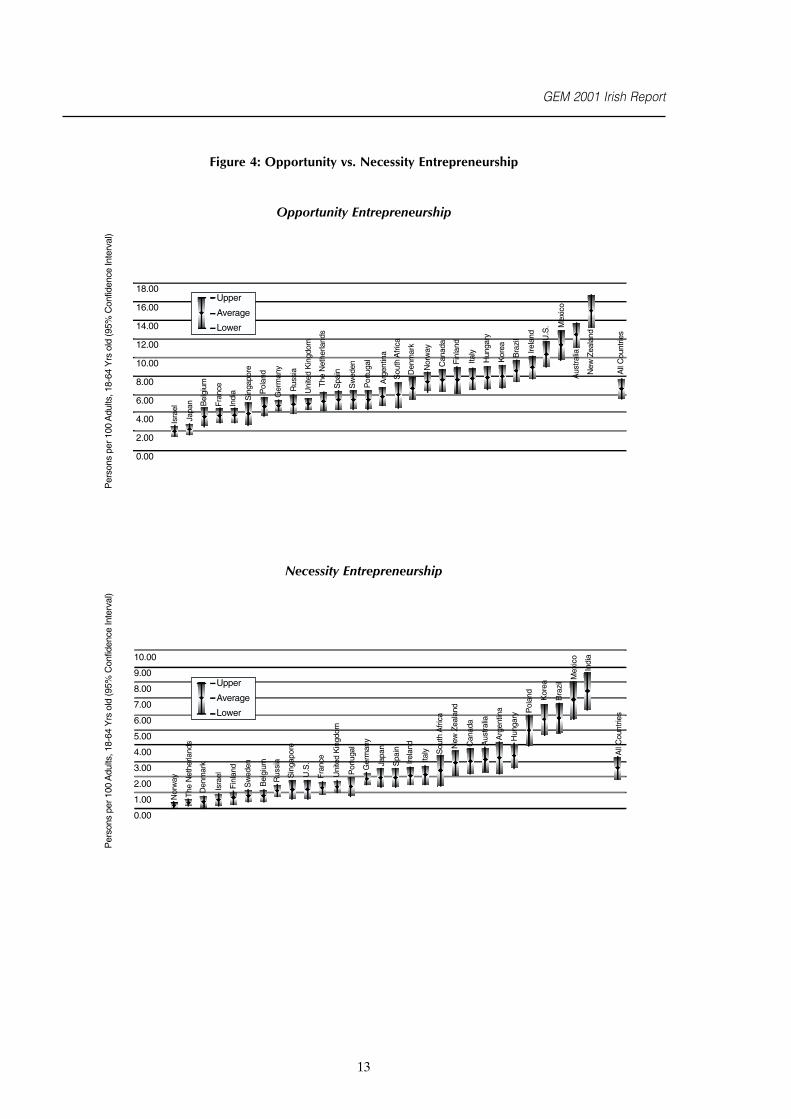

Figure 4: Opportunity vs. Necessity Entrepreneurship

Opportunity Entrepreneurship

Upper

Average

Lower

18.00

16.00

14.00

12.00

10.00

8.00

6.00

4.00

2.00

0.00

Isra

el

Japa

n Bel

gium

Fra

nce

Indi

a

Sin

gapo

re

Pol

and

Ger

man

y

Rus

sia

Uni

ted

Kin

gdom

The

Net

herla

nds

Spa

in

Sw

eden

Por

tuga

l

Arg

entin

a

Sou

th A

frica

Den

mar

k

Nor

way

Can

ada

Fin

land

Italy

Hun

gary

Kor

ea

Bra

zil

Irela

nd U.S

. Mex

ico

Aus

tralia

New

Zea

land

All

Cou

ntrie

s

Per

sons

per

100

Adu

lts, 1

8-64

Yrs

old

(95%

Con

fiden

ce In

terv

al)

Necessity Entrepreneurship

Upper

Average

Lower

10.00

9.00

8.00

7.00

6.00

5.00

4.00

3.00

2.00

1.00

0.00

Isra

el

All

Cou

ntrie

s

Indi

a

Mex

ico

Bra

zil

Kor

ea

Pol

and

Ger

man

y

Japa

n

Bel

gium

Fra

nce

Sin

gapo

re

Rus

sia

Uni

ted

Kin

gdom

The

Net

herla

nds

Spa

in

Sw

eden

Por

tuga

l

Arg

entin

a

Sou

th A

frica

Den

mar

k

Nor

way

Can

ada

Fin

land

Italy

Hun

gary

Irela

nd

U.S

.

Aus

tralia

New

Zea

land

Per

sons

per

100

Adu

lts, 1

8-64

Yrs

old

(95%

Con

fiden

ce In

terv

al)

13

Global Entrepreneurship Monitor

Two distinct types of motivation are identified.The first relates to those involved in creatingand growing new firms who do so in responseto a perceived opportunity. These efforts arereferred to as ‘‘opportunity entrepreneurship’’,reflecting the voluntary nature of participation.Opportunity entrepreneurs have other optionsopen to them, but choose to start a newbusiness out of personnel preference. Incontrast, the second group become involvedbecause they perceive that they have ‘‘nobetter choices for work’’. Such efforts arereferred to as ‘‘necessity entrepreneurship’’,reflecting the individuals’ perception that suchactions present the best option available foremployment, but not necessarily the preferredoption.

About 54% of those involved in creating andgrowing new businesses across the entire GEMcountries were responding in a positive way toa perceived opportunity (‘‘opportunityentrepreneurship’’); 43% became involved out

Table 2: Entrepreneurship Motives and Selected Sectors

Opportunity NecessityEntre- Entre- Mixed or

Total preneurship preneurship Other

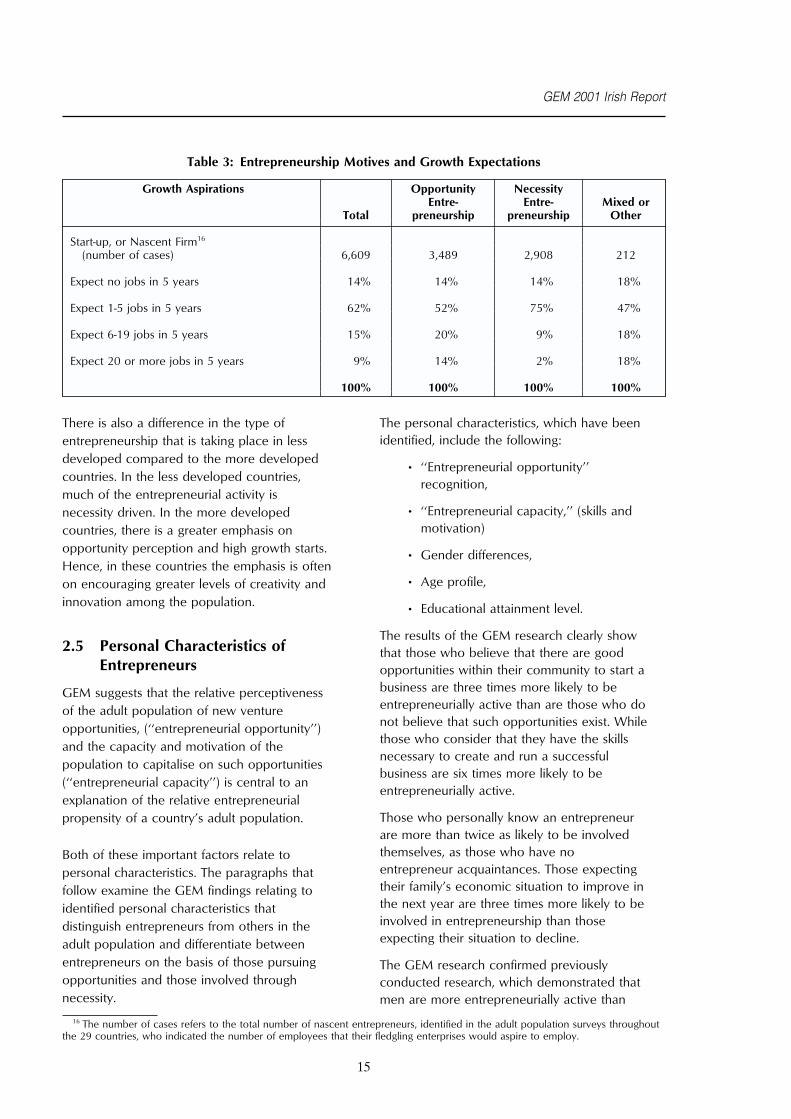

Start-up, or Nascent Firm (number of cases)15 6,609 3,489 2,908 212

Extractive:Farming, Fishing, Hunting, Forestry, Mining 4% 4% 4% 8%

Transforming:Construction, Manufacturing, Transportation,Wholesale, Communications, Utilities 33% 30% 37% 36%

Business Services:Financial, Insurance, Real Estate, Consulting,Business Professionals 14% 21% 5% 13%

Consumer-Oriented:Retail, Hotels, Restaurants, Consumer Services,Health, Education, Social Services 49% 45% 54% 43%

100% 100% 100% 100%

Growth aspirations also differ very dramaticallybetween necessity and opportunity drivenentrepreneurs, as is illustrated in Table 3.About 14% of opportunity entrepreneursexpect their new ventures to be high growthstart-ups, i.e. to produce 50 or more jobs infive years, compared with only 2% of necessity

15 The number of cases refers to the total number of nascent entrepreneurs, identified in the adult population surveys throughoutthe 29 countries, who indicated the sector in which their fledgling enterprises are active.

14

of necessity (‘‘necessity entrepreneurs’’); and3% became involved for other reasons.The pattern of participation in opportunity and

necessity entrepreneurship varies dramaticallyacross the GEM countries. Necessityentrepreneurship is much more prevalent inthe developing countries than it is in the moredeveloped economies.

Figure 4 separately illustrates the opportunityand necessity entrepreneurship rates for all 29GEM countries.

The results of GEM 2001 also show thatconsumer oriented businesses represent almost50% of all entrepreneurial activity. A muchgreater percentage of opportunity motivatedentrepreneurial activity occurs in the businessservices sector (21%), than in other individualsectors, while necessity entrepreneurship ismost prevalent in consumer-oriented services(54%). The relationship between the motivesfor entrepreneurship and the sectors in whichthe entrepreneurs engage is illustrated inTable 2.

entrepreneurs who have such expectations.Moreover, 90% of necessity entrepreneursexpect their new businesses to beemploying no more than 5 in the next fiveyears.

GEM 2001 Irish Report

Table 3: Entrepreneurship Motives and Growth Expectations

Growth Aspirations Opportunity NecessityEntre- Entre- Mixed or

Total preneurship preneurship Other

Start-up, or Nascent Firm16

(number of cases) 6,609 3,489 2,908 212

Expect no jobs in 5 years 14% 14% 14% 18%

Expect 1-5 jobs in 5 years 62% 52% 75% 47%

Expect 6-19 jobs in 5 years 15% 20% 9% 18%

Expect 20 or more jobs in 5 years 9% 14% 2% 18%

100% 100% 100% 100%

There is also a difference in the type ofentrepreneurship that is taking place in lessdeveloped compared to the more developedcountries. In the less developed countries,much of the entrepreneurial activity isnecessity driven. In the more developedcountries, there is a greater emphasis onopportunity perception and high growth starts.Hence, in these countries the emphasis is oftenon encouraging greater levels of creativity andinnovation among the population.

2.5 Personal Characteristics ofEntrepreneurs

GEM suggests that the relative perceptivenessof the adult population of new ventureopportunities, (‘‘entrepreneurial opportunity’’)and the capacity and motivation of thepopulation to capitalise on such opportunities(‘‘entrepreneurial capacity’’) is central to anexplanation of the relative entrepreneurialpropensity of a country’s adult population.

Both of these important factors relate topersonal characteristics. The paragraphs thatfollow examine the GEM findings relating toidentified personal characteristics thatdistinguish entrepreneurs from others in theadult population and differentiate betweenentrepreneurs on the basis of those pursuingopportunities and those involved throughnecessity.

16 The number of cases refers to the total number of nascent entrepreneurs, identified in the adult population surveys throughoutthe 29 countries, who indicated the number of employees that their fledgling enterprises would aspire to employ.

15

The personal characteristics, which have beenidentified, include the following:

• ‘‘Entrepreneurial opportunity’’recognition,

• ‘‘Entrepreneurial capacity,’’ (skills andmotivation)

• Gender differences,

• Age profile,

• Educational attainment level.

The results of the GEM research clearly showthat those who believe that there are goodopportunities within their community to start abusiness are three times more likely to beentrepreneurially active than are those who donot believe that such opportunities exist. Whilethose who consider that they have the skillsnecessary to create and run a successfulbusiness are six times more likely to beentrepreneurially active.

Those who personally know an entrepreneurare more than twice as likely to be involvedthemselves, as those who have noentrepreneur acquaintances. Those expectingtheir family’s economic situation to improve inthe next year are three times more likely to beinvolved in entrepreneurship than thoseexpecting their situation to decline.

The GEM research confirmed previouslyconducted research, which demonstrated thatmen are more entrepreneurially active than

Global Entrepreneurship Monitor

women. Across the 29 GEM countries, 70% ofall adults identified, as being entrepreneuriallyactive, were men.

In general, the most entrepreneurially activeage group is 25-44 year olds, with 55% of allentrepreneurs across all GEM countries beingwithin this age group. Patterns relating to age,however, are quite different for opportunityand necessity entrepreneurship. For men andwomen, opportunity entrepreneurship ishighest in the age group 35 to 44 years.Necessity entrepreneurship for men is highestin the 18 to 24 age group, and then declines

Figure 5: Entrepreneurial Activity by Gender and Age

TEA Opportunity18-24 yrs 3.1 6.625-34 yrs 4.0 9.735-44 yrs 4.9 9.745-54 yrs 4.3 6.355-64 yrs 2.4 4.5

TEA Overall18-24 yrs 5.5 17.2

Number Numberper 100 Women Men per 100

25-34 yrs 7.3 18.935-44 yrs 8.3 14.945-54 yrs 6.8 9.455-64 yrs 3.2 9.0

TEA Necessity18-24 yrs 2.3 10.525-34 yrs 3.1 8.735-44 yrs 3.1 4.845-54 yrs 2.3 2.855-64 yrs 0.7 4.0

Nascent Firms18-24 yrs 3.4 11.925-34 yrs 4.9 11.035-44 yrs 5.0 9.945-54 yrs 4.6 5.955-64 yrs 2.5 6.4

New Firms18-24 yrs 2.2 5.9

10 8 6 4 2 0 2 4 6 8 10 12 14 16 18 20

25-34 yrs 2.5 8.635-44 yrs 3.6 5.445-54 yrs 2.4 3.955-64 yrs 0.9 2.6

The GEM analysis shows that those who havecompleted secondary or third level educationor training, represent the majority (74%) ofthose currently active as entrepreneurs.

When all types of activity are considered, asshown in Figure 6, there are quite differentpatterns for men and women. Participation inentrepreneurial activity increases with more

16

steadily in the older age categories. Women,on the other hand, are equally represented upto the age of 54, when there is a dramaticdecline in their level of entrepreneurial activity.

Figure 5 illustrates the entrepreneurialprevalence rates for men on the right, and forwomen on the left, for all five GEM measuresof entrepreneurial activity (i.e. overall TotalEntrepreneurship Activity Rate (TEA), TEAOpportunity, TEA Necessity, NascentEntrepreneurs, and ‘‘New Firm’’ Entrepreneurs).The age categories are also presented for eachtype of entrepreneurial activity.

education for women, with a major jumpamong those who go beyond completion ofsecondary education. For men, in contrast,there is a reduced participation among thosewho go beyond secondary education, with thelowest levels among those with the most (i.e.,graduate experience) or least (i.e., non-completion of second level) amount ofeducation.

GEM 2001 Irish Report

When those pursuing opportunities, however,are compared with those involved inentrepreneurial activities out of necessity, thepatterns are quite different. Among thosepursuing opportunities, it is those with thehigher levels of education (at least secondaryschool completed) that are the mostentrepreneurially active. This is particularly truefor women who become moreentrepreneurially active as their level ofeducation increases. The pattern for necessity

Figure 6: Entrepreneurial Activity by Gender and Educational Attainment

Graduate Experience 9.3 9.7

TEA Opportunity

Post Secondary 7.2 9.5

Secondary Degree 3.6 9.8

No Secondary Degree 2.2 3.0

Graduate Experience 1.1 1.6

TEA Necessity

Post Secondary 1.9 5.8

Secondary Degree 2.0 7.3

No Secondary Degree 3.3 7.4

Graduate Experience 6.3 4.9

10 8 6 4 2 0 2 4 6 8 10 12 14 16 18

Nascent Firms

Post Secondary 4.9 10.0

Secondary Degree 4.0 12.0

No Secondary Degree 4.0 7.0

Graduate Experience 4.2 7.6

New Firms

Post Secondary 5.1 6.2

Secondary Degree 2.1 6.1

No Secondary Degree 1.7 3.9

Graduate Experience 10.5 11.7

TEA Overall

Post Secondary 9.5 15.8

Secondary Degree 6.0 17.6

No Secondary Degree 5.6 10.6

Number Numberper 100 Women Men per 100

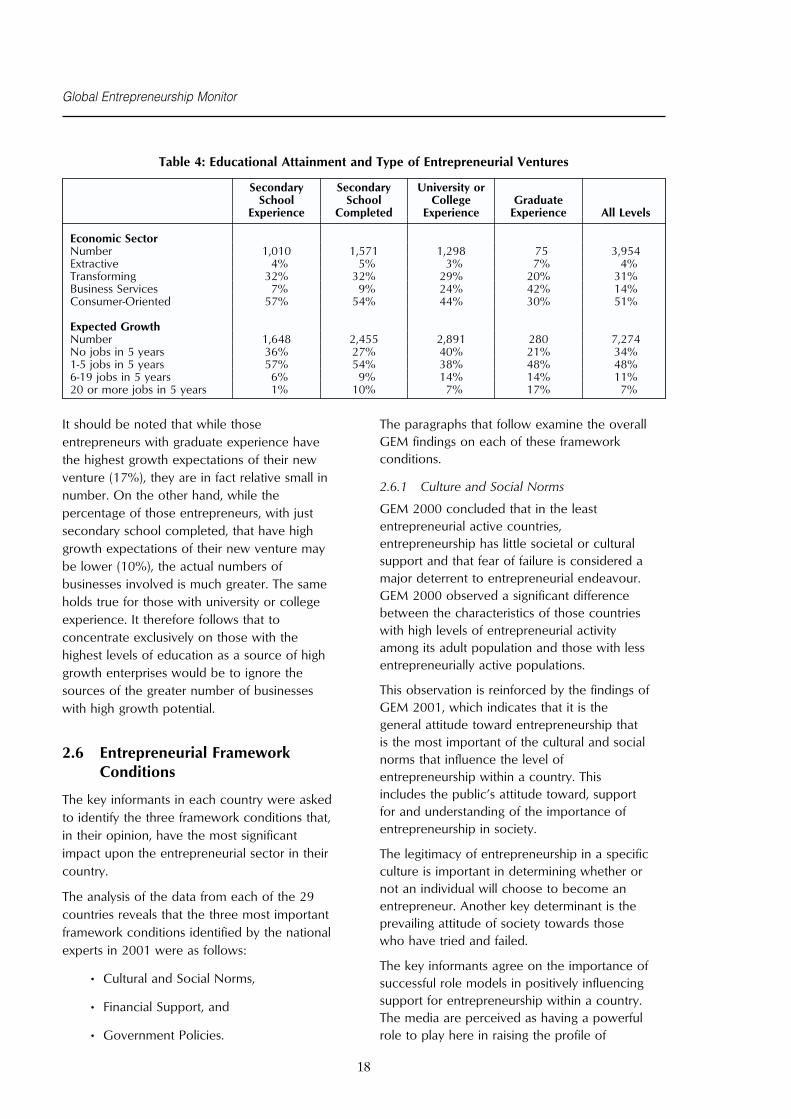

The GEM results also show that the type andscale of the entrepreneurial activity is directlyrelated to the educational attainment levels ofthe entrepreneurs. This is illustrated in Table 4.

17

entrepreneurship is reversed for both men andwomen. It is also true that those in the upperthird of household incomes within theircountries are much more active in pursuingopportunity entrepreneurship. This is onceagain particularly true for women.

The general patterns by gender andeducational attainment for the five types ofentrepreneurial activity are presented inFigure 6.

The most highly educated have the greatestexpectations that their enterprise will growsignificantly. They also tend to be the mostinvolved in Business Services.

Global Entrepreneurship Monitor

Table 4: Educational Attainment and Type of Entrepreneurial Ventures

Secondary Secondary University orSchool School College Graduate

Experience Completed Experience Experience All Levels

Economic SectorNumber 1,010 1,571 1,298 75 3,954Extractive 4% 5% 3% 7% 4%Transforming 32% 32% 29% 20% 31%Business Services 7% 9% 24% 42% 14%Consumer-Oriented 57% 54% 44% 30% 51%

Expected GrowthNumber 1,648 2,455 2,891 280 7,274No jobs in 5 years 36% 27% 40% 21% 34%1-5 jobs in 5 years 57% 54% 38% 48% 48%6-19 jobs in 5 years 6% 9% 14% 14% 11%20 or more jobs in 5 years 1% 10% 7% 17% 7%

It should be noted that while thoseentrepreneurs with graduate experience havethe highest growth expectations of their newventure (17%), they are in fact relative small innumber. On the other hand, while thepercentage of those entrepreneurs, with justsecondary school completed, that have highgrowth expectations of their new venture maybe lower (10%), the actual numbers ofbusinesses involved is much greater. The sameholds true for those with university or collegeexperience. It therefore follows that toconcentrate exclusively on those with thehighest levels of education as a source of highgrowth enterprises would be to ignore thesources of the greater number of businesseswith high growth potential.

2.6 Entrepreneurial FrameworkConditions

The key informants in each country were askedto identify the three framework conditions that,in their opinion, have the most significantimpact upon the entrepreneurial sector in theircountry.

The analysis of the data from each of the 29countries reveals that the three most importantframework conditions identified by the nationalexperts in 2001 were as follows:

• Cultural and Social Norms,

• Financial Support, and

• Government Policies.

18

The paragraphs that follow examine the overallGEM findings on each of these frameworkconditions.

2.6.1 Culture and Social Norms

GEM 2000 concluded that in the leastentrepreneurial active countries,entrepreneurship has little societal or culturalsupport and that fear of failure is considered amajor deterrent to entrepreneurial endeavour.GEM 2000 observed a significant differencebetween the characteristics of those countrieswith high levels of entrepreneurial activityamong its adult population and those with lessentrepreneurially active populations.

This observation is reinforced by the findings ofGEM 2001, which indicates that it is thegeneral attitude toward entrepreneurship thatis the most important of the cultural and socialnorms that influence the level ofentrepreneurship within a country. Thisincludes the public’s attitude toward, supportfor and understanding of the importance ofentrepreneurship in society.

The legitimacy of entrepreneurship in a specificculture is important in determining whether ornot an individual will choose to become anentrepreneur. Another key determinant is theprevailing attitude of society towards thosewho have tried and failed.

The key informants agree on the importance ofsuccessful role models in positively influencingsupport for entrepreneurship within a country.The media are perceived as having a powerfulrole to play here in raising the profile of

GEM 2001 Irish Report

entrepreneurs and in influencing a positiveattitude towards their activities.

Difficulties arise in those countries in whichthere is less entrepreneurial activity and where,consequently, fewer role models are available.According to the key informants, thesecountries are focused on efforts to get societyto simply accept entrepreneurship and toappreciate its wider economic benefits in theircommunities.

In the more entrepreneurially active countries,the focus is on the identification of ways ofencouraging women and minorities to be moreentrepreneurial, and here again the positive

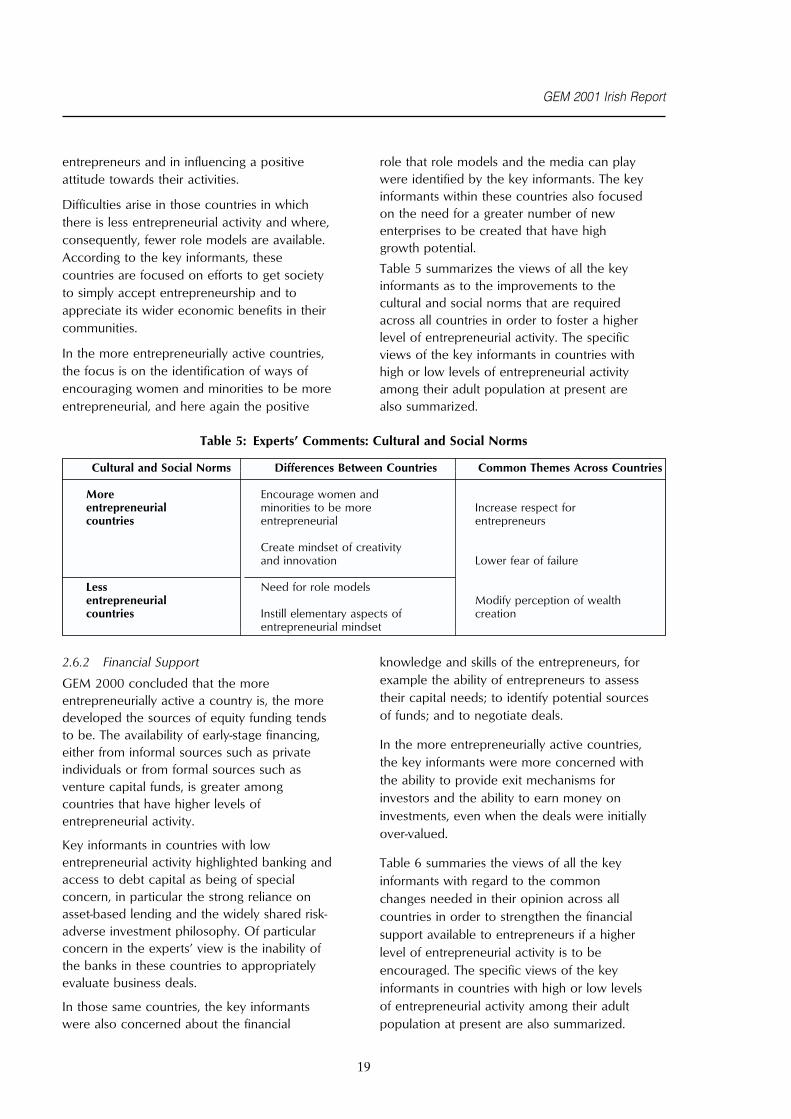

Table 5: Experts’ Comments: Cultural and Social Norms

Cultural and Social Norms Differences Between Countries Common Themes Across Countries

More Encourage women andentrepreneurial minorities to be more Increase respect forcountries entrepreneurial entrepreneurs

Create mindset of creativityand innovation Lower fear of failure

Less Need for role modelsentrepreneurial Modify perception of wealthcountries Instill elementary aspects of creation

entrepreneurial mindset

2.6.2 Financial Support

GEM 2000 concluded that the moreentrepreneurially active a country is, the moredeveloped the sources of equity funding tendsto be. The availability of early-stage financing,either from informal sources such as privateindividuals or from formal sources such asventure capital funds, is greater amongcountries that have higher levels ofentrepreneurial activity.

Key informants in countries with lowentrepreneurial activity highlighted banking andaccess to debt capital as being of specialconcern, in particular the strong reliance onasset-based lending and the widely shared risk-adverse investment philosophy. Of particularconcern in the experts’ view is the inability ofthe banks in these countries to appropriatelyevaluate business deals.

In those same countries, the key informantswere also concerned about the financial

19

role that role models and the media can playwere identified by the key informants. The keyinformants within these countries also focusedon the need for a greater number of newenterprises to be created that have highgrowth potential.

Table 5 summarizes the views of all the keyinformants as to the improvements to thecultural and social norms that are requiredacross all countries in order to foster a higherlevel of entrepreneurial activity. The specificviews of the key informants in countries withhigh or low levels of entrepreneurial activityamong their adult population at present arealso summarized.

knowledge and skills of the entrepreneurs, forexample the ability of entrepreneurs to assesstheir capital needs; to identify potential sourcesof funds; and to negotiate deals.

In the more entrepreneurially active countries,the key informants were more concerned withthe ability to provide exit mechanisms forinvestors and the ability to earn money oninvestments, even when the deals were initiallyover-valued.

Table 6 summaries the views of all the keyinformants with regard to the commonchanges needed in their opinion across allcountries in order to strengthen the financialsupport available to entrepreneurs if a higherlevel of entrepreneurial activity is to beencouraged. The specific views of the keyinformants in countries with high or low levelsof entrepreneurial activity among their adultpopulation at present are also summarized.

Global Entrepreneurship Monitor

Table 6: Experts’ Comments: Financial Support

Financial Support Differences Between Countries Common Themes Across Countries

Improve the ability of lendingMore Improve the risk investment institutions and equity investorsentrepreneurial culture in the financial to assess entrepreneurialcountries community opportunities

Lower cost of capital forImprove banking and access entrepreneurs

Less to debt capitalentrepreneurial Modify inadequate regulationcountries Improve entrepreneurs’ by Government of the supply of

ability to assess capital needs capital

2.6.3 Government Policies

The experts in all of the GEM 2001 countriesidentified government policies in the area ofentrepreneurship as being important and inneed of attention. In countries with lowerlevels of entrepreneurial activity, the keyinformants focused on the need to improveoperational efficiencies in terms of the policiesand programmes that their governments arealready implementing in this area and the needfor a greater co-ordination between the variousprogrammes. In the more entrepreneuriallyactive countries, the key informants are moreconcerned with the need for their governmentsto take a more strategic approach to policyformulation in order to create the best climatefor entrepreneurship.

Key informants across all countries agreed onthe need for governments to deepen andextend their understanding of entrepreneurshipand its impact on the economy. For experts inthe less entrepreneurially active countries, the

Table 7: Experts’ Comments: Government Policy

Government Policies Differences Between Countries Common Themes Across Countries

Increase the long-term focus ofgovernment support for

More entrepreneurship Reduce administrative burdenentrepreneurial of regulatory compliancecountries Deepen government

understanding ofentrepreneurship

Increase coordination ingovernmental support Increase fiscal incentives to

Less initiatives stimulate entrepreneurialentrepreneurial initiativescountries Change government negative

perception of entrepreneurship

20

issue is image and awareness, both in terms ofthe need to overcome the general sense ofmistrust and disrespect that, in the opinion ofthe key informants, policy-makers have forentrepreneurs and the need to bring about amore supportive attitude towardsentrepreneurs and their activities among theirgeneral populations.

For experts in the more entrepreneurially activecountries, the issue is more about policyeffectiveness, including policies that reduce thebarriers to growth for young, emergingentrepreneurial enterprises.

Table 7 summarizes the views of all the keyinformants with regard to the commonchanges in government policy across all theGEM countries that are necessary, in theopinion of the key informants, in order tofoster a greater level of entrepreneurship. Thespecific views of the key informants incountries with high or low levels ofentrepreneurial activity among their adultpopulation at present are also summarized.

GEM 2001 Irish Report

2.7 Formal and Informal BusinessInvestment

There is a section in the 2001 GEM ExecutiveReport, specially written by William D,Bygrave, which takes a closer look at theavailability of informal finance and venturecapital for new enterprises and the relativeamounts invested through these means.

Policy makers often overlook the importanceof informal sources of finance andunderestimate its significance. While venturecapital is well known as a source of financingfor new enterprises, the flow of informalinvestment is in fact the source of the largestshare of the funds for new businesses. In allGEM 2001 countries, informal investorsallocated more money for start-ups andgrowing businesses than did professionalventure capital firms. On average across allGEM countries, for every one Euro of classic ortraditional venture capital that was invested,

Figure 7: Informal Investment by Country

All

Cou

ntrie

s8.00

7.00

6.00

5.00

4.00

3.00

2.00

1.00

0.00Per

sons

per

100

Adu

lts, 1

8Yrs

and

Old

er (9

5% C

onfid

ence

Inte

rval

)

Bel

gium

Japa

n

Sin

gapo

re

Isra

el

The

Net

herla

nds

Sw

eden

Rus

sia

Ger

man

y

Por

tuga

l

Fra

nce U

nite

d K

ingd

om

Spa

in

Den

mar

k

Nor

way Fin

land

Sou

th A

frica

Pol

and

Italy

Arg

entin

a

Can

ada

Indi

a

Hun

gary

U.S

.

Irela

nd

Bra

zil

Kor

ea

Aus

tralia

New

Zea

land

Mex

ico

Upper

Average

Lower

About 50% of informal funds go to familymembers and relatives; 30% goes to co-workers, friends and neighbours; and theremainder goes to ‘‘strangers with good ideas.’’This combined group of informal investors arealso known as ‘‘Business Angels’’.

21

there was an average of about \1.60 ofinformal capital invested.

It is estimated that informal investors, provide atotal of \215 billion in funds per year to start-up and growing companies in the participatingGEM countries. In the context of nationaleconomies, the total informal investment in theyear 2000 was 1.1% of the combined GDP forall GEM countries.

The proportion of adults, within the variousGEM countries, that was active as informalinvestors in 2001 averaged just over 3%, witha range from less than 1% in Brazil to over 6%in New Zealand. The rate of informalinvestment in Ireland is just above the midpoint for all GEM countries.

Figure 7 illustrates the level of informalinvestment by country.

The impact of classic venture capital is verysignificant for new and growing enterprises,although it is less important in terms of thetotal investment pool than informal investment.The companies that receive venture capitalfunding tend to grow faster and make a greater

Global Entrepreneurship Monitor

contribution to their national economies overtime. Accordingly, those economies in whichventure capital is the most developed tend tohave the highest number of new firms withhigh growth potential. Figure 8 clearlyillustrates the dominance of Israel and the

Figure 8: Domestic Venture Capital Invested as a Percentage of GDP

1999

2000

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0.0

Bel

gium

Japa

n Sin

gapo

re

Isra

el

The

Net

herla

nds

Sw

eden

Ger

man

y

Por

tuga

l

Fra

nce

Uni

ted

Kin

gdom

Spa

in

Den

mar

k

Nor

way

Fin

land

Sou

th A

frica

Pol

and

Italy

Can

ada

Indi

a

Hun

gary

U.S

.

Irela

nd

Sou

th K

orea

Aus

tralia

New

Zea

land

Dom

estic

Cla

ssic

VC

Inve

stm

ents

Per

cent

of G

DP

The US dominates in terms of (i) the numberof companies that received venture capital in2000 and (ii) the amount invested percompany. Nearly 27% of companies thatreceived venture capital in that year were

22

United States, in terms of domestic venturecapital invested as a percentage of GDP. SouthKorea and Canada follow in second positionwith all the other GEM countries trailing wellbehind.

located in the United States and thesecompanies accounted for 81% of the venturecapital invested in all participating GEMcountries.

CHAPTER 3

How Entrepreneurial is Ireland?

3.1 Introduction

In 2001, with sponsorship from Forfas andEnterprise Ireland, Ireland participated for thesecond time in GEM.

The paragraphs that follow detail the overallresults for Ireland as obtained from the adultpopulation survey carried out in September2001, from the expert key informant interviewscarried out slightly earlier in the year, and fromthe detailed questionnaires completed by thekey informants interviewed in 2000 and in2001. The environment for entrepreneurship inIreland relative to the entrepreneurialframework conditions is also examined. Finally,the entrepreneurial characteristics of the Irishadult population are analysed in the light of theGEM findings.

The GEM 2001 Global Executive Report ranksIreland 6th in terms of the overallentrepreneurial propensity of its adultpopulation across 29 countries. It should benoted that this is a revised result and correctsthe very low position that Ireland obtained inGEM 2000. For a full explanation of why theGEM 2000 Executive Report incorrectlyreported Ireland’s entrepreneurial ranking seeAppendix 1.

3.2 Overall Results

On the basis of the adult population survey for2001, the following results were obtained withregard to the level of entrepreneurial activity inIreland:

• 7.2% of the adult population arecurrently engaged in the process ofstarting a business. This level of activityranks Ireland in 12th position across the29 GEM countries.

• 4.8% of the adult population currently

17 High growth potential is defined as aspiring to employ 50 within 5 years.

23

partly or fully own and operate abusiness started since 1998. These are‘‘new firm’’ entrepreneurs. This level ofnew enterprise development placesIreland in 6th position.

• 82% of those actively involved in newentrepreneurial activity in Ireland areresponding to a perceived opportunityrather than being forced to do sothrough necessity. Ireland is ranked 5th

across the 29 GEM countries in termsof the proportion of its adult populationthat are pursuing opportunity drivenentrepreneurial activity.

• 3% of all nascent entrepreneurs believethat their new venture will have highgrowth potential.17 Ireland is rankedjoint 10th of the 29 countries in thisregard.

• The number of Business Angelsidentified among the Irish adultpopulation is just under 3.5 %. Thisplaces Ireland joint 12th and just abovethe average (3.1%) across all 29 GEMcountries.

Ireland’s overall entrepreneurial ranking (TEA)is 6th of the 29 GEM countries. This ranking isbased on the number of nascent and new firmentrepreneurs identified in each country’s adultpopulation survey.

In accordance with the general pattern acrosscountries, a greater number of Irish people areplanning new enterprises than have yet set upnew businesses.

The movement in Ireland’s relative rankingbetween nascent and new firm entrepreneurswould appear to indicate that either (i) Irelandhas a higher conversion rate of nascententrepreneurs (i.e. those planning new

Global Entrepreneurship Monitor

enterprises) into new firm entrepreneurs (i.e.those who have brought their entrepreneurialplans to reality) than is the norm across theGEM countries, or (ii) that there will be fewerfirms actually set up in the immediate futureand Ireland’s relative position in respect of newfirm entrepreneurs will decline as relativelyfewer people are actually planning newbusinesses at present.

From the available data it is not possible toascertain which is the correct interpretation toplace on these figures. The results of the 2002adult population survey, which will be carriedout shortly, should give further clarification inthis area.

Table 8: Summary of the Results for Ireland

Selective Measures of Highest Rate Average Rate Lowest Rate of Ireland’s Ireland’sEntrepreneurial Activity of all GEM of all GEM all GEM Rate Ranking

Countries Countries Countries18

Total Entrepreneurial Activity 18.7% (MX) 9.7% 4.5% (BE) 12.0% 6

Nascent Entrepreneurs 12.7% (MX) 6.3% 1.2% (IL) 7.2% 12

High Growth Nascent Start-Ups 7.0% 2.6% 0.0%19 3.0% 10(+)20

(ZA/NL/NO)

New Firm Entrepreneurs 7.2% (AU) 3.4% 0.8% (JP) 4.8% 6

Opportunity Driven Entrepreneurs 12.8% (NZ) 6.5% 2.0% (IL) 9.2% 5

Informal Investors 7.0% (NZ) 3.1% 1.0% 3.0% 12(+)20

(NL/BR/JP/PT)

The Irish key informants considered the framework condition the highest-ranking country,conditions prevailing in Ireland to be relatively the average score across all experts in all GEMfavorable to entrepreneurial activity. The countries, the lowest ranking country, the Irishquestionnaires, completed by 50 Irish key result and the relative position of Ireland. It alsoinformants, asked the experts to respond in terms illustrates the experts’ views on the relativeof a five point scale from True (5) to False (1). entrepreneurial characteristics of the adultTable 9 summarises for each entrepreneurial population.

18 International Country CodesAR = Argentina AU = Australia BE = Belgium BR = Brazil CA = CanadaDE = Germany DK = Denmark ES = Spain FI = Finland FR = FranceHU = Hungary IE = Ireland IL = Israel IN = India IT = ItalyJP = Japan KR = Korea MX = Mexico NL = Netherlands NO = NorwayNZ = New Zealand PL = Poland PT = Portugal RU = Russia SE = SwedenSG = Singapore UK = United Kingdom US = United States ZA = South Africa

19 No high growth nascent start-ups were identified in eight countries.20 More than one country was on this rank.

24

When the percentage of active entrepreneursis translated into numbers of people within theadult population, between the ages of 18-64,the results for Ireland indicate the following:

• Over 160,000 adults are currentlyengaged in the process of starting abusiness.

• Approximately 110,000 adults currentlypartly or fully own and operate abusiness started since 1998

• Almost 5,000 adults believe that thenew venture, which they are currentlyplanning, will employ at least 50 peopleafter 5 years from the start of the newenterprise.

GEM 2001 Irish Report

Table 9: Summary of all Experts’ Evaluations

Variable Description High Score Average Score Low Score Ireland Score Ireland Rank

Finance — Ease of Access 4.10 (US) 3.12 1.79 (AR) 3.64 5

Finance — Presence of VC,Business Angel and Other 4.49 (US) 3.02 1.85 (BR) 3.66 3

Cultural and Social Norms 3.64 (US) 2.43 1.89 (SE) 2.99 3

Cultural and Social Norms —Acceptance of CareerVolatility 4.32 (US) 3.50 2.92 (JP) 3.61 9

Government Policy 3.20 (DE) 2.71 1.37 (AR) 3.14 6

Government Policy — Ease,Speed and Lack of RegulatoryBurden 3.54 (SG) 2.23 1.22 (AR) 3.24 2

Government Programme —Efficiency and Effectiveness 3.57 (GER) 2.66 1.42 (AR) 3.16 6

Education and TrainingEffectiveness 2.79 (SG) 2.14 1.55 (PT) 2.60 3

Research and DevelopmentTransfer Effectiveness 3.24 (BE) 2.39 1.86 (AR) 2.69 9

Professional and CommercialInfrastructure 3.89 (US) 3.18 1.94 (JP) 3.49 5

Market Stability 3.64 (JP) 2.82 2.13 (NOR) 2.45 18

Relative Lack of Barriers toMarket Entry 3.44 (US) 2.63 1.22 (ZA) 2.93 8

Access to PhysicalInfrastructure 4.46 (SG) 3.82 2.88 (IN) 3.04 22

Entrepreneurial Opportunity 4.20 (US) 3.26 2.46 (AR) 3.74 2

Entrepreneurial Capacity(Skills) 3.13 (US) 2.40 1.77 (JP) 2.71 5

Entrepreneurial Capacity(Motivation) 4.49 (US) 3.37 2.84 (NO) 3.94 4

3.3 Backdrop to Entrepreneurship inIreland

In common with the other developedcountries, the factors that are of particularconcern to Ireland are the relativecompetitiveness of its environment for businessrelative to other countries; the level ofentrepreneurial activity of its adult population;and the proportion of its adult population thatare pursuing perceived opportunities.

While Ireland ranks relatively well on theentrepreneurial dimensions, 6th in overallentrepreneurial activity and 5th in terms ofproportion of opportunity entrepreneurship, itsrelative competitiveness rating is underpressure due to infrastructural shortcomings. Inthe 2002 World Competitiveness Yearbook,Ireland’s relative position on the World

21 The World Competitiveness Yearbook: 2002. Lausane, Switzerland International Institute for Management Development.

25

Competitiveness Index21 was 10th, representinga decrease in the country’s relative ranking forthe second year in a row (previous rankingswere 7th and 5th).

Table 10 illustrates Ireland’s relative ranking forsome of the various dimensions that go tomake up the World Competitiveness Index.Ireland is well positioned on most of thedimensions that affect the national frameworkconditions. While the low ranking oninfrastructure should come as no surprise,deficits in the availability and relative cost oftelecommunications and in the necessaryinfrastructure for exporting, can be a significantinhibitor of entrepreneurial activity and growthin a country like Ireland. With a small homemarket, new ventures, if they are to grow, mustexport at an early stage in their development.

Global Entrepreneurship Monitor

Table10: Ireland’s Relative Position

World Competitive Index Rankings (Gem Countries Only)22

Ireland’s RankingHighest Ranking GEM Lowest Ranking GEM (relative to GEM

Country Country countries only)

Economic Performance(Domestic Economy) USA Argentina 2nd

Government Efficiency Singapore Argentina 4th

Business Efficiency USA Argentina 6th

Infrastructure USA India 17th

3.4 Key Entrepreneurial FrameworkConditions: Ireland’s RelativePosition

The 36 key informants interviewed in Ireland23

were asked to highlight the three frameworkconditions that they considered to have themost important impact on the entrepreneurialsector in Ireland. As was the case in themajority of countries surveyed, these expertscited the following:

• Financial Support,

• Cultural and Social Norms, and

• Government Policy.

The paragraphs that follow summarise Ireland’sstanding on each of these conditions asperceived by the key informants.

3.4.1 Financial Support

In terms of adequate availability of debt andequity funding for new and growing firms andthe availability of sufficient governmentsubsidies in this area24, the Irish experts gave arelatively high rating. As Table 11 illustrates,comparing across countries, Ireland came out5th in terms of the satisfaction rating of itsexperts25. Experts in the US, Germany and theNetherlands gave the highest ratings to thesituation prevailing in their countries in thisregard. The experts in Argentina and Mexicoconsidered the situation in their countries to bethe most unsatisfactory with regard to

22 The World Competitiveness Yearbook: 2002. Lausane, Switzerland International Institute for Management Development.23 In Ireland, the thirty-six experts interviewed included government officials, development and support agency executives, private

sector providers of advice, supports and finance to new enterprises, academics and successful entrepreneurs.24 Finance- Ease of Access variables.25 It should be pointed out that the experts were only asked to comment on the situation within their own country. It is only after

all the results are collected and compared across countries that the relative position emerges.

26

entrepreneurs trying to finance their new andgrowing businesses.

The key informants were also asked for theiropinion on the situation in their country withregard to the availability of informal (‘‘BusinessAngel’’) and formal (Venture Capital) riskcapital and the relative importance of IPOs asan important source of equity. The Irishexperts’ views placed Ireland 3rd in this regard.However, quite a number of countriesreceived a broadly similar rating from their keyinformants. Not surprisingly, the US scoredparticularly well and far ahead of the othercountries. Once again, it was the experts in theless developed countries, such as Brazil,Hungary and Argentina that considered thattheir entrepreneurs have major difficulties inthis area.

The level of Business Angel investment,however, was much higher among the keyinformants than it was among the general adultpopulation. Of the key informants, 38%confirmed that they had personally providedfunds, in the last three years, for a newbusiness start-up that was not their own. Someexperts suggested that much of this businessangel activity is going to hi-tech, high-growthfirms and that the entrepreneurs with lesssophisticated and smaller-scale enterprises findit difficult to get access to this type of informalinvestment.

Ireland scored well in terms of the financialsupport available to entrepreneurs in thecountry as Table 11 illustrates.

GEM 2001 Irish Report

Table 11: Experts’ Evaluations: Financial Support

Variable Description High Score Average Score Low Score Ireland Score Ireland Rank

Finance — Ease of Access 4.10 (US) 3.12 1.79 (AR) 3.64 5

Finance — Presence of VC,Business Angel and Other 4.49 (US) 3.02 1.85 (BR) 3.66 3

Most of the Irish key informants point out thateven in the current more cautious climate,there is more venture capital available nowthan there was in the past. They do, however,highlight a lack of seed capital as a problem.The difficulty entrepreneurs have in securingrelatively small amounts of money iscompounded by the amount of paperworkinvolved.

Some claimed that sources of capital in Ireland,including the banks, are less interested in thenumerous smaller-scale new ventures than theyare in the relatively small number of hi-techstarts, that are perceived to have high growthpotential.

3.4.2 Cultural and Social Norms

In terms of the questions posed to the keyinformants with regard to cultural and socialnorms, the first set related to the value placedon self-sufficiency, the relative protectionoffered by social welfare support and theacceptance of income diversity. The expertsfrom the US considered that self-sufficiencywas well developed within their country, whilethe Nordic counties, particularly Sweden,

Table 12: Experts’ Evaluations: Cultural and Social Norms

Variable Description High Score Average Score Low Score Ireland Score Ireland Rank

Cultural and Social Norms 3.64 (US) 2.43 1.89 (SE) 2.99 3