is service-led growth a miracle for india

TRANSCRIPT

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 1/42

1

Lecture Note (Session 7)

Is Service-led Growth a Miracle for India?

Services represent the fastest growing sector of the global economy

and accounts for two-thirds of global output (WTO, 2009) 1. Introduction

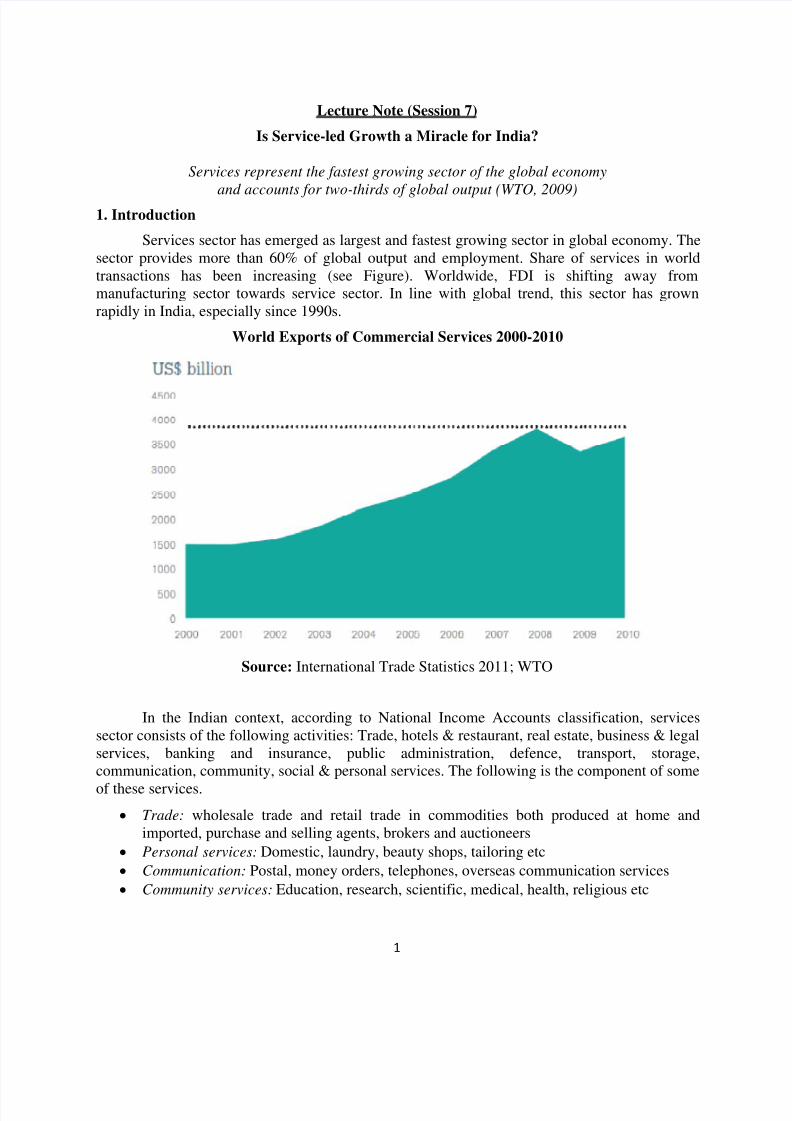

Services sector has emerged as largest and fastest growing sector in global economy. Thesector provides more than 60% of global output and employment. Share of services in worldtransactions has been increasing (see Figure). Worldwide, FDI is shifting away frommanufacturing sector towards service sector. In line with global trend, this sector has grownrapidly in India, especially since 1990s.

World Exports of Commercial Services 2000-2010

Source: International Trade Statistics 2011; WTO

In the Indian context, according to National Income Accounts classification, servicessector consists of the following activities: Trade, hotels & restaurant, real estate, business & legalservices, banking and insurance, public administration, defence, transport, storage,communication, community, social & personal services. The following is the component of some

of these services.

• Trade: wholesale trade and retail trade in commodities both produced at home andimported, purchase and selling agents, brokers and auctioneers

• Personal services: Domestic, laundry, beauty shops, tailoring etc

• Communication: Postal, money orders, telephones, overseas communication services

• Community services: Education, research, scientific, medical, health, religious etc

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 2/42

2

• Dwelling & real estate: Services associated with construction (building real estate oncontract basis, building design, interior design etc)

In terms of income generation, services activities can be broadly classified as low-earningand high earning activities. Some of the examples of low-earning services activities are repairand maintenance services, local transport services, cobblers, shoe-shine, catering, hair dressing

and dry cleaning. Examples of high earning services activities are legal services, IT/ITES,telecommunication services, financial & accountancy services, customer relations management,health and educational services, construction, housing and engineering and tourism, Retail,entertainment and media. The significant point to be noted here is development of high-earningservices sector can automatically create demand for low-earning services. For example, IT boomin India has generated demand for transport services, dry cleaning, hair dressers, air-conditionmechanics, courier services, physical security, catering etc

2. Significance of Services Sector for India:

Currently services sector is the fastest growing sector of the Indian economy (Tables 1and 2). A growing ‘tertiarisation’ of structure of production and employment has been taking

place in India. Since 1990s, services sector emerged as major sector of economy both in terms of growth rates and share in GDP. While other sectors experienced phases of deceleration,stagnation and growth, services sector has shown a uniform growth trends overtime. A majorpart of decline in share of primary sector in GDP was picked up by service sector. This isconsidered to be a unique feature witnessed by India.

Sectoral Growth of GDP (%) (Base: 1999-00)

Period Agriculture

and allied

activities

Agriculture Industry Manufacturing Service sector

1950-51 to 1979-80 2.16 2.16 5.36 5.21 4.55

1980-81 to 1991-92 2.97 3.04 6.10 5.58 6.20

1992-93 to 2007-08 2.70 2.70 6.06 6.39 7.98

1992-93 to 2010-11* 2.73 2.68 6.34 6.74 8.27

* - Data from 2008-09 to 2010-11 are not final estimates

Source: Instructor's calculation based on Handbook of Statistics on Indian Economy (HSIE), 2011

(RBI)

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 3/42

3

Table 2: Sectoral Composition of GDP (%)

Year Agriculture and Allied

Activities*

Industry and

Manufacturing**

Services

1950-51 55 (48) 11 (9) 34

1960-61 51 (45) 13 (11) 36

1970-71 44 (39) 15 (13) 40

1980-81 38 (34) 17 (14) 45

1990-91 31 (29) 20 (15) 49

2000-01 24 (22) 20 (15) 56

2008-09 16 (13) 20 (16) 64

2010-11 14 (NA) 20 (16) 66

* Figures in brackets indicate the share of agriculture in GDP** Figures in brackets indicate the share of manufacturing sector in GDP

Source: Handbook of Statistics on Indian Economy, RBI.

Growth pattern in services sector has not been uniform across all services (Table 3). Inpost-1990s business services (which includes IT), communications & banking sectorsexperienced maximum growth. Growth of trade and communications increased consistently overthe decades. In the first half of the current decade, majority of the service segments witnessed

high growth. This trend clearly indicates that apart from ITES (which comes under businessservices), many other sectors have made credible contributions to the new found dynamism of the service sector.

Table 3: Growth Rate within the Services Sector

Sixth Plan

(1980-85)

Seventh Plan

(1985-89)

Eighth Plan

(1992-1997)

Ninth Plan

(1997-2002)

Tenth Plan

(2002-2007)

Trade 5.3 6.5 9.1 7.3 9.3

Hostels&

Restaurant 5.4 6.9 11.2 9.3 9

Railways 2.8 5.7 1.9 4.7 7.7

Other Transport 6.9 7 8.4 6 11.4

Storage 3.5 1.8 2.4 2.2 5.6

Communications 6.7 5.3 14.1 21.8 22.1

Banking &

Insurance 7.5 13.4 8.2 9 9.3

Real Estate 7.3 8.1 6.1 7.2 8.3

Public

Administration 6.1 7.9 3.9 8.5 5.2

Other services 3.9 6 7 7 7.6

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 4/42

4

Source: Government of India (2008)

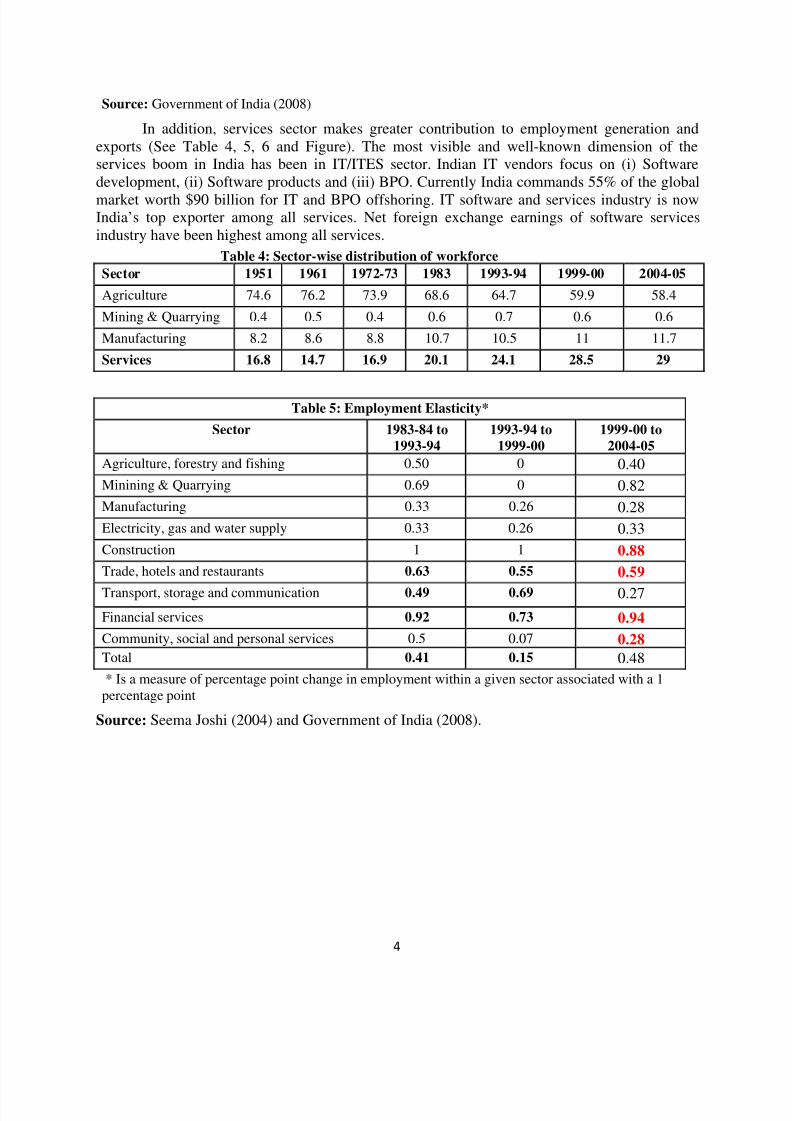

In addition, services sector makes greater contribution to employment generation andexports (See Table 4, 5, 6 and Figure). The most visible and well-known dimension of theservices boom in India has been in IT/ITES sector. Indian IT vendors focus on (i) Softwaredevelopment, (ii) Software products and (iii) BPO. Currently India commands 55% of the global

market worth $90 billion for IT and BPO offshoring. IT software and services industry is nowIndia’s top exporter among all services. Net foreign exchange earnings of software servicesindustry have been highest among all services.

Table 4: Sector-wise distribution of workforce

Sector 1951 1961 1972-73 1983 1993-94 1999-00 2004-05

Agriculture 74.6 76.2 73.9 68.6 64.7 59.9 58.4

Mining & Quarrying 0.4 0.5 0.4 0.6 0.7 0.6 0.6

Manufacturing 8.2 8.6 8.8 10.7 10.5 11 11.7

Services 16.8 14.7 16.9 20.1 24.1 28.5 29

Table 5: Employment Elasticity*

Sector 1983-84 to

1993-94

1993-94 to

1999-00

1999-00 to

2004-05

Agriculture, forestry and fishing 0.50 0 0.40

Minining & Quarrying 0.69 0 0.82

Manufacturing 0.33 0.26 0.28

Electricity, gas and water supply 0.33 0.26 0.33

Construction 1 1 0.88

Trade, hotels and restaurants 0.63 0.55 0.59

Transport, storage and communication 0.49 0.69 0.27

Financial services 0.92 0.73 0.94

Community, social and personal services 0.5 0.07 0.28

Total 0.41 0.15 0.48

* Is a measure of percentage point change in employment within a given sector associated with a 1percentage point

Source: Seema Joshi (2004) and Government of India (2008).

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 5/42

Source:

Figure:

Internationa

eading Exp

l Trade Stat

orts of Co

istics, 2008

5

mercial S

(WTO)

rvices* (G owth 2000 2007)

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 6/42

6

3. Explanations for the Boom in the Services Sector in India:

The major reasons for India’s success in IT-ITES and other services are as follows:

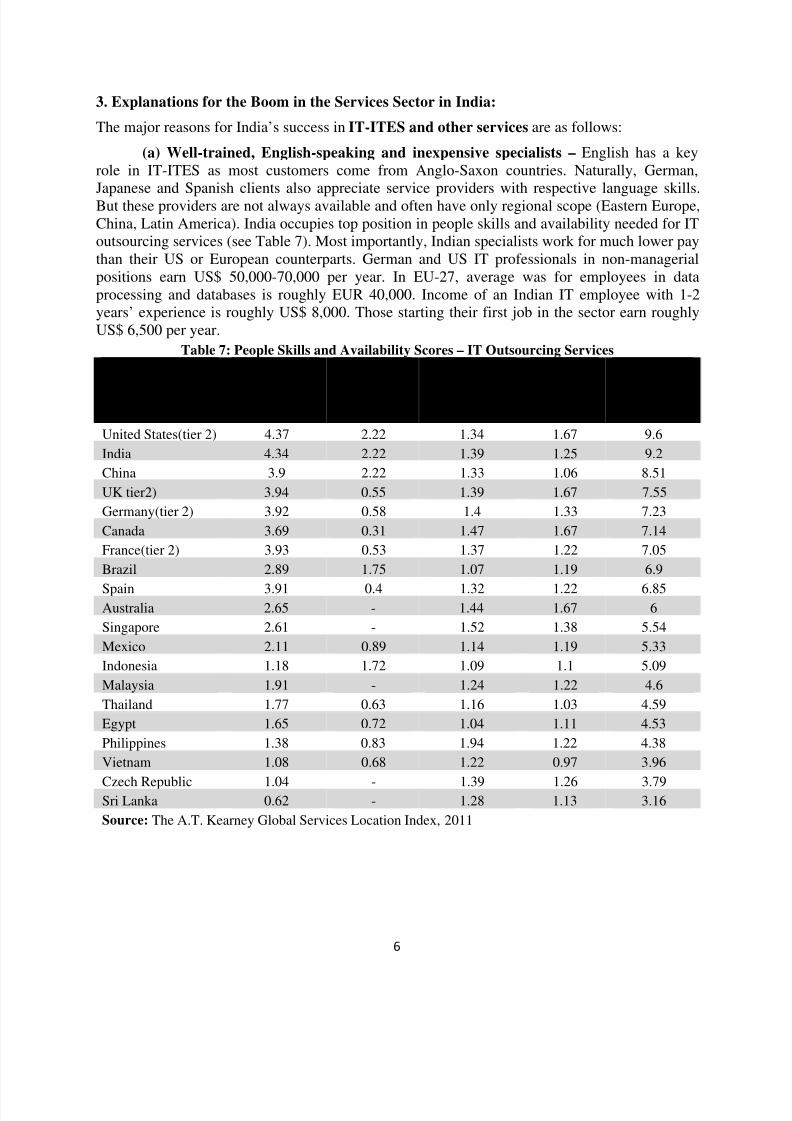

(a) Well-trained, English-speaking and inexpensive specialists – English has a keyrole in IT-ITES as most customers come from Anglo-Saxon countries. Naturally, German,Japanese and Spanish clients also appreciate service providers with respective language skills.But these providers are not always available and often have only regional scope (Eastern Europe,China, Latin America). India occupies top position in people skills and availability needed for IToutsourcing services (see Table 7). Most importantly, Indian specialists work for much lower paythan their US or European counterparts. German and US IT professionals in non-managerialpositions earn US$ 50,000-70,000 per year. In EU-27, average was for employees in dataprocessing and databases is roughly EUR 40,000. Income of an Indian IT employee with 1-2years’ experience is roughly US$ 8,000. Those starting their first job in the sector earn roughlyUS$ 6,500 per year.

Table 7: People Skills and Availability Scores – IT Outsourcing Services Country Relevant

experience

Size and

availability

of labour

force

Education Language

capabilities

Total

Score

United States(tier 2) 4.37 2.22 1.34 1.67 9.6

India 4.34 2.22 1.39 1.25 9.2

China 3.9 2.22 1.33 1.06 8.51

UK tier2) 3.94 0.55 1.39 1.67 7.55

Germany(tier 2) 3.92 0.58 1.4 1.33 7.23

Canada 3.69 0.31 1.47 1.67 7.14

France(tier 2) 3.93 0.53 1.37 1.22 7.05

Brazil 2.89 1.75 1.07 1.19 6.9

Spain 3.91 0.4 1.32 1.22 6.85Australia 2.65 - 1.44 1.67 6

Singapore 2.61 - 1.52 1.38 5.54

Mexico 2.11 0.89 1.14 1.19 5.33

Indonesia 1.18 1.72 1.09 1.1 5.09

Malaysia 1.91 - 1.24 1.22 4.6

Thailand 1.77 0.63 1.16 1.03 4.59

Egypt 1.65 0.72 1.04 1.11 4.53

Philippines 1.38 0.83 1.94 1.22 4.38

Vietnam 1.08 0.68 1.22 0.97 3.96

Czech Republic 1.04 - 1.39 1.26 3.79Sri Lanka 0.62 - 1.28 1.13 3.16

Source: The A.T. Kearney Global Services Location Index, 2011

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 7/42

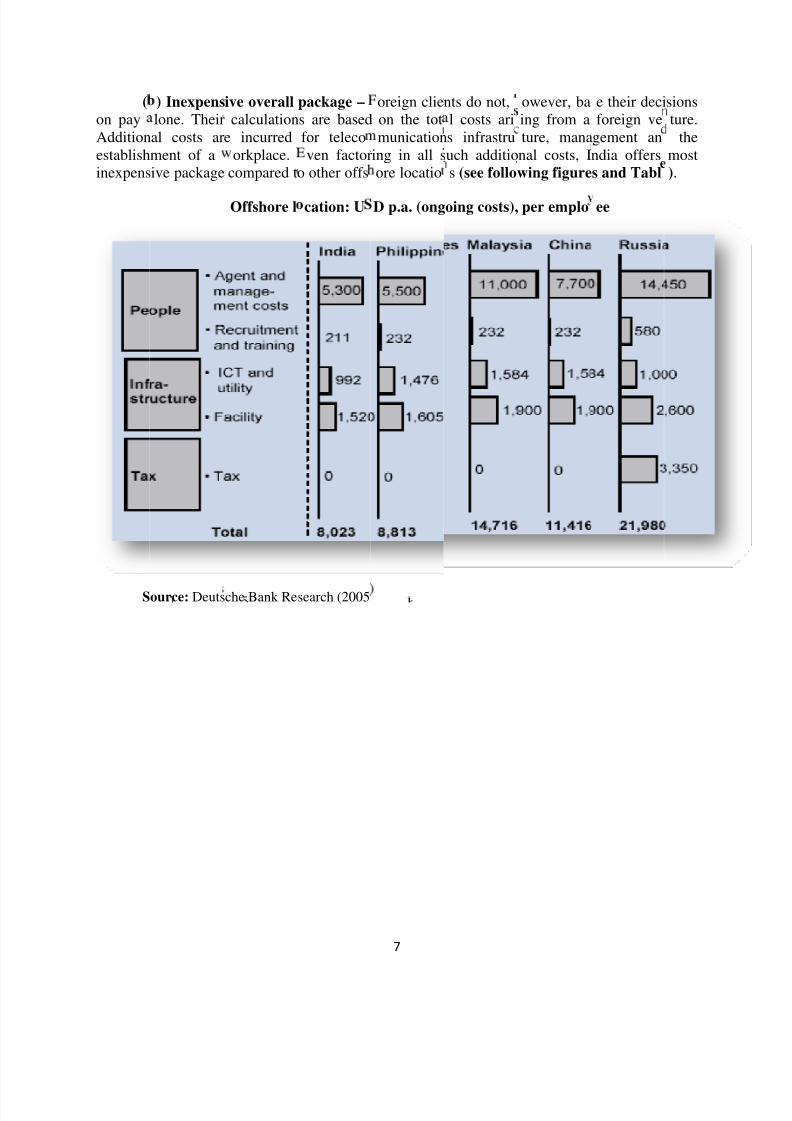

(on payAdditionestablishinexpens

S

) Inexpenslone. Theiral costs arment of aive package

ource: Deuts

ive overallcalculation

e incurredorkplace.

compared t

Offshore l

che Bank Re

package – s are basedfor telecoven factor

o other offs

cation: U

search (2005

7

oreign clieon the totmunication

ing in all sore locatio

D p.a. (ong

nts do not,l costs aris infrastruuch additios (see follo

oing costs),

owever, baing from ature, mananal costs, Iwing figure

per emplo

e their deciforeign ve

gement anndia offerss and Tabl

ee

sionsture.

themost).

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 8/42

Country

A.T.

attractiven

Kearney

8

ess for out

lobal Servi

ourcing an

ces Locatio

d offshorin

n Index

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 9/42

(to intern

from IndLevel 5 r

(

(

(

(contributcontinueprofessi

Bangalo(

(iwere dofor serviunits inc

) High quaationally re

ia. Of theating - high

) Populatio

) Liberal ec

) Strong de

) Global nion. Theyto cultivatnal experie

e are run b) High inco

) Splinterie internallyes from in

reasingly o

lity standaognised qu

oftware cost rating th

n at workin

onomic poli

and from i

etwork of Istablishedthese contce gained i

Indians whme elasticit

g (meansby individustrial sect

utsourced n

ds – Highality standa

mpanies wot a softwar

age is high

cy environ

ndustrial na

ndian emiirst contact

acts. In Indn the US. E

o have livedof demand

utsourcinal firms. Sr. In their

on-core fun

9

umbers of Irds (Six Si

rldwide witcompany c

ent

ions

rants - Inds in orderia itself thexample: 95

and workefor service

) – Meanslintering rerive to bec

ctions such

T companima, CMM

h a Capabilan attain –

ian expatrito seal intemanagers

of intern

abroad, m

contractingsults in an ioming moras account

s that are cLevel 5 an

ity Maturitajority are

tes in thernational core also oftetional com

stly in US

out businesncrease incompetitiv

ing or payr

rtified accod ISO 900

Model (Cfrom India

S made antracts andn returneesanies in ST

s operationet input de

e, manufactoll manage

rding) are

MM)

ajortheywith

Ps in

thatmanduringment,

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 10/42

securityindustry.

(jparticulaprocesse

softwarecontext,India: 6commer

(companithree Inemployerevenuesoffshoreis accoustructurethese usu

guards, dri

) Protectir importancs of his cli

which is nsoftware pi% (in 20ially.

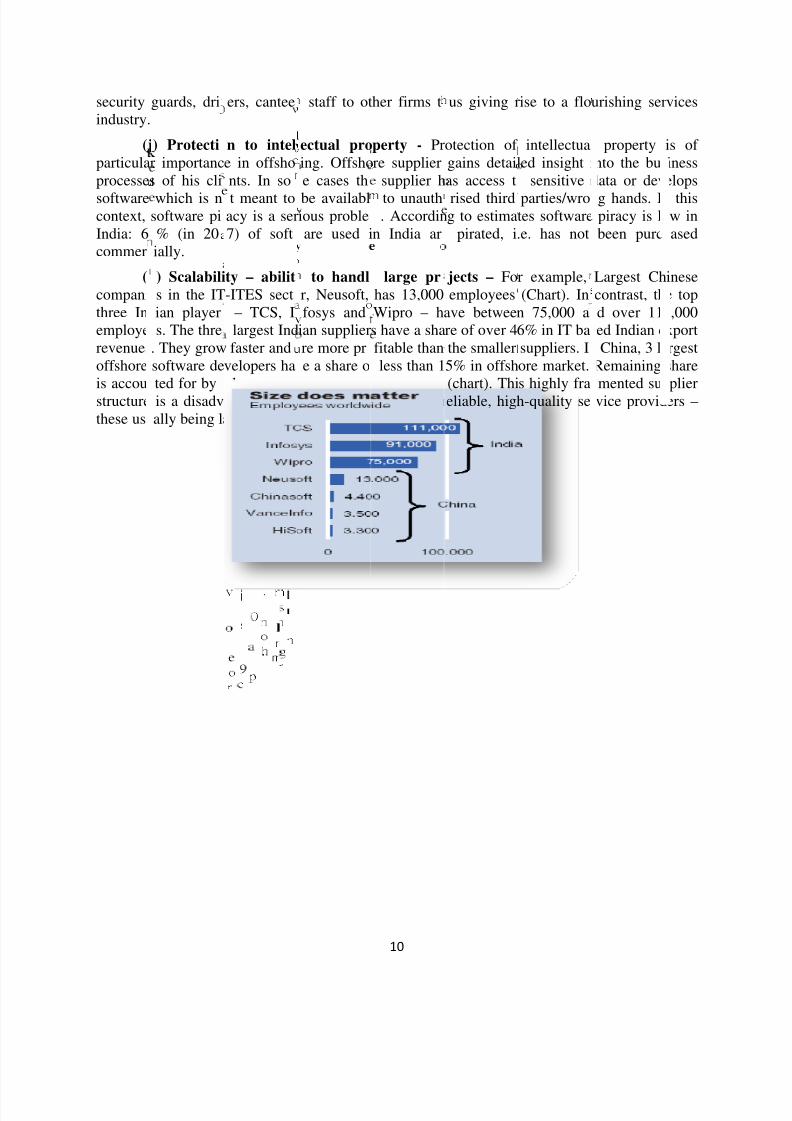

) Scalabilis in the ITian players. The thre

. They growsoftware deted for byis a disadvally being l

ers, cantee

n to intele in offshonts. In so

t meant toacy is a ser7) of soft

ty – abilit-ITES sect

– TCS, Ilargest Indfaster and

velopers halarge num

antage as carge supplie

staff to ot

ectual proing. Offshoe cases th

be availablious probleare used i

to handlr, Neusoft,fosys and

ian supplierre more pre a share oer of smallstomers wi

rs

10

her firms t

perty - Prre supplier

supplier h

to unauth. Accordin

n India ar

large prhas 13,000Wipro – hs have a shafitable thanless than 1r suppliers

sh to have r

us giving r

otection of gains detailas access t

rised thirdg to estima

pirated, i

jects – Foemployees

ave betweere of over 4the smaller5% in offsh(chart). Thieliable, hig

ise to a flo

intellectualed insight i

sensitive

parties/wrotes software.e. has not

r example, (Chart). In

n 75,000 a6% in IT basuppliers. Iore market.s highly frah-quality se

urishing ser

propertynto the busdata or dev

g hands. Ipiracy is lbeen purc

Largest Chcontrast, thd over 11ed Indian eChina, 3 l

Remainingmented suvice provid

vices

is of inesselops

thisw inased

inesee top,000

xportrgestshareplierers –

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 11/42

(l

(becausecontrolsIT/ITESlike texticontractsmargineven thotelephonkicked ipolicy ch

Ggrowthand arewere abwhichintensivedependepoorly dextent thnot applindustria

(represseservices,

1 In the prservices, f

) Global IT

) Easy othey usuall(e.g. restricand telecoles or steel.has been

n sales-a leugh the poly, vast unta, have allanges in 19

upta et al.f industriesmore labouve the medere belowness grew 1t on markeveloped fin

at servicesto them,

l sector.

) Demand demand1 from educa

-liberalisationr the most pa

revolution,

tion – Forrequire les

ive labourmunicationThe cost aassive, and

vel unthink icy challenped demanwed a prof 99 and 2003

2008) use dthat are mintensive.

ian in termsthe media9 per cents for financancial mark firms have lhey have b

-repressiohave createion to healt

period, telecot, were confin

hich provi

many entrs physical iolicies not

s was vastlrbitrage betit has bee

ble for maes have be

d, and a shaitability tha.

ata from thre dependeThey find tof infrastru; those w

less than the grew 18 pets and rigiower infraseen in a be

- Servicd a huge mh services, a

m services wed to a narrow

11

ded great o

preneurs,nfrastructurapplicable).greater tha

ween Indiaroutine fo

ufacturingen substantirp reductiot has made

Annual Snt upon infrhat, in thecture intensich werese which

er cent less.labour law

tructure detter positio

s sector irket for sernd even tra

re scarce; the turban elite.

portunity f

ervices arethan indu

The profitn that of oland the mar IT firms tompanies.ve and repin costs asaccess to

rvey of Indastructure,post-deliceiveness greabove theere belowThat is, ths were signendence, ato grow t

simply pices, rangisport.

ransport netw

r IT/ITES.

an easiertry and arebility of suer manufacrkets that oo enjoy a 3In telecomtitive, thethe economapital easy,

ustries (ASIhave greatersing period

10 per cemedian inhe median;costs of po

ificant diffed restrictivan their co

laying catcg from tele

rk was rudim

egment tosubject to

nrise sectorturing indufered offsh0 per centunications,rrival of mies of scaleespecially

) to comparfinancial n

, companiet less than

terms of land, thoseor infrastrurentiators. T

labour launterparts i

h-up-decadoms to fin

entary; and fin

enterewerlike

tries,oringrofitalso,obilehaveafter

e theeeds,

thatthosebourmoreture,o thes do

n the

s of ncial

ancial

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 12/42

12

(o) Subversive entrepreneurship - In some cases, the growth of the services sector wasbased on subversive entrepreneurship. A good example is the cable TV industry, whichmushroomed in a grey legal area, and was considered too small and fragmented to meritgovernment attention until as many as 60 per cent of all TV households were hooked on to cable.When this stage was reached, even the industry wanted some clear rules, especially to facilitate

access to capital.4. Is India’s Services Boom Unique or Unusual?

The standard development model has involved seeing the share of agriculture going downand that of industry going up in terms of both gross domestic product (GDP) and employment;and, after a fairly long period in which per capita incomes climb to upper-middle income levels,the share of the services sector rises while that of industry falls-with agriculture, by then, havinga share of between 5 and 10 per cent. It is often argued that the Indian growth model appears

to have skipped the intermediate stage, giving rise to a debate whether a growth model heavilybased on service sector growth is sustainable. Many observers have argued that in a low incomeeconomy like India 66 per cent (in 2010-11) share of services in GDP is unnatural. It is in thissense that India is perceived to be an outlier.

However, Jim Gordon and Poonam Gupta (2003) argue that the outlier thesis does nothold if one looks at the empirical evidence. Using cross-country data, they plot the rise in theshare of services as per capita income rises: in 1990, India was very much on the trend line. Itmoved above the trend by 2001, when followed the decade in which services significantlyoutpaced industry. However, even then, the variation was less than in many other economies (seeFigure). Perhaps, perceptions of the 'distorted' nature of Indian growth could be a result, in part,of China's well-known success in manufacturing. The industry-services mismatch seemsparticularly sharp when India-China comparisons are made. Interestingly, however, Jim

Gordon and Poonam Gupta find that the outlier is not India but China, whose preponderance

of manufacturing is what is truly unusual.

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 13/42

5. Is the

Tgrowth teconom

( in privattotal conthat is, f

present gr

his is indeeurnpike, m.

) Changinfinal cons

sumption bom around

wth patter

d the case,re services

Consumptumption exsket (at 19per cent in

of service

as will bewill be a

ion patternenditure w9/2000 pric1950/1 to

13

in India s

argued beloded to the

: Till the lis a straight

es) rose by11 per cent

stainable?

w. As newlist of rap

beralizationforward onaround 3 pein 1960/1; 1

service secidly growin

of the early-the sharercentage po4 per cent i

ors get ontg sectors i

1990s, thef services i

ints each den 1970/1; 1

o thethe

trendn thecade:7 per

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 14/42

cent in 12000/1, tpoints. Bfurther iside imp

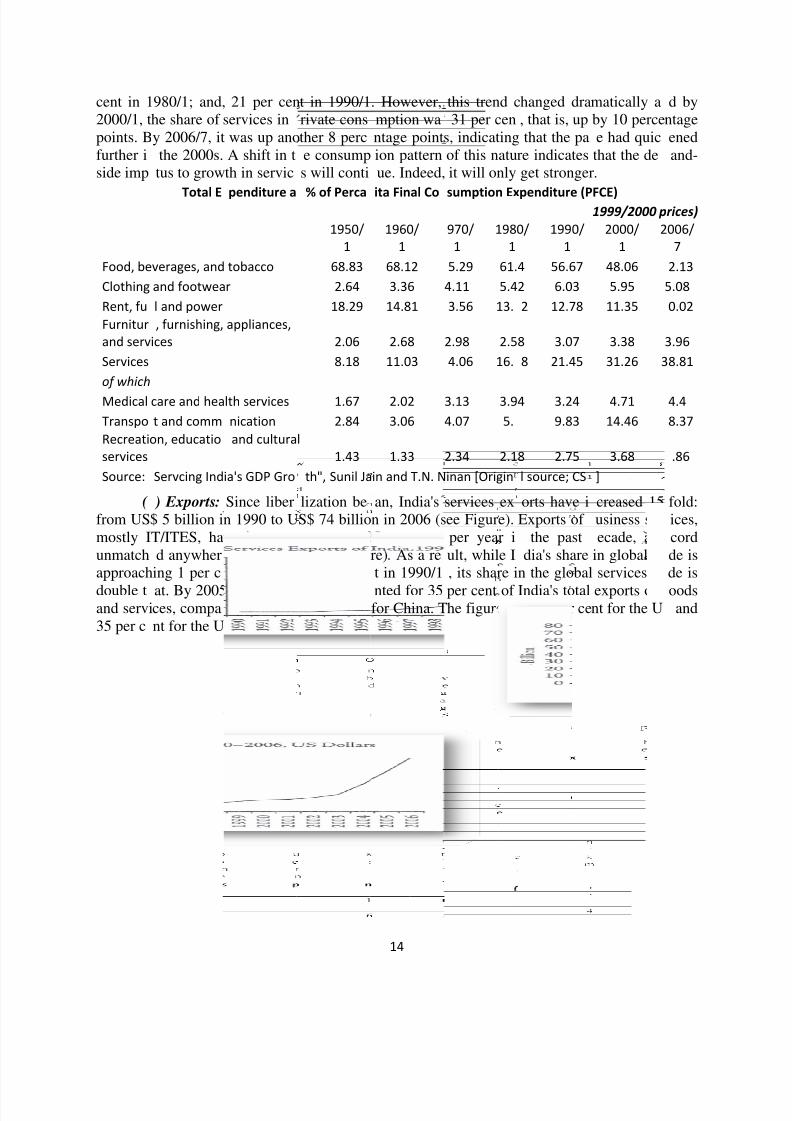

Food, be

Clothing Rent, fu

Furnitur

and serv

Services of which

Medical Transpo

Recreati

services Source:

( from USmostly Iunmatchapproach

double tand servi35 per c

980/1; and,he share of y 2006/7, itthe 2000s.tus to grow

Total E

verages, and

and footwea

l and power , furnishing,

ices

care and hea

t and comm

on, educatio

Servcing Ind

) Exports:$ 5 billion iT/ITES, had anywhering 1 per c

at. By 2005ces, compant for the U

21 per censervices inwas up anoA shift in tth in servic

penditure a

tobacco r appliances,

lth services nication and cultura

ia's GDP Gro

Since libern 1990 to Uve increase

in the worlnt (up from

, services eed to a merK.

t in 1990/1rivate consther 8 perce consumps will conti

% of Perca

1950/

1 68.83 2.64

18.29 2.06 8.18 1.67 2.84

l 1.43

th", Sunil Ja

lization beS$ 74 billio

at over 2d (see Figu0.4 per ce

ports acco9 per cent

14

. However,mption wantage pointion patternue. Indeed,

ita Final Co

1960/

1 68.12 3.36

14.81 2.68

11.03 2.02 3.06 1.33

in and T.N. Nan, India'sn in 2006 (s5 per centre). As a ret in 1990/1

nted for 35for China. T

this trend c31 per cen

s, indicatingof this natuit will only

sumption Ex

970/

1 198

1

5.29 61.

4.11 5.4

3.56 13.

2.98 2.5

4.06 16.

3.13 3.9

4.07 5.

2.34 2.1

inan [Origin

services exee Figure).per year iult, while I, its share i

per cent of he figure w

hanged dra, that is, upthat the pa

re indicatesget stronger

penditure (P

0/ 1990/

1 4 56.67 2 6.03 2 12.78

8 3.07 8 21.45

4 3.24 9.83

8 2.75 l source; CS

orts have iExports of

the pastdia's share

n the global

India's totalas 28 per ce

matically aby 10 percee had quicthat the de.

FCE) 1999/2000 p2000/

1 2

48.06 5.95

11.35 3.38

31.26 3

4.71

14.46 3.68

] creased 15usiness serecade, a r

in global trservices tr

exports of nt for the U

d byntageenedand-

rices)

006/

7 2.13

5.08 0.02

3.96 8.81 4.4 8.37 .86 fold:ices,cordde isde is

oodsand

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 15/42

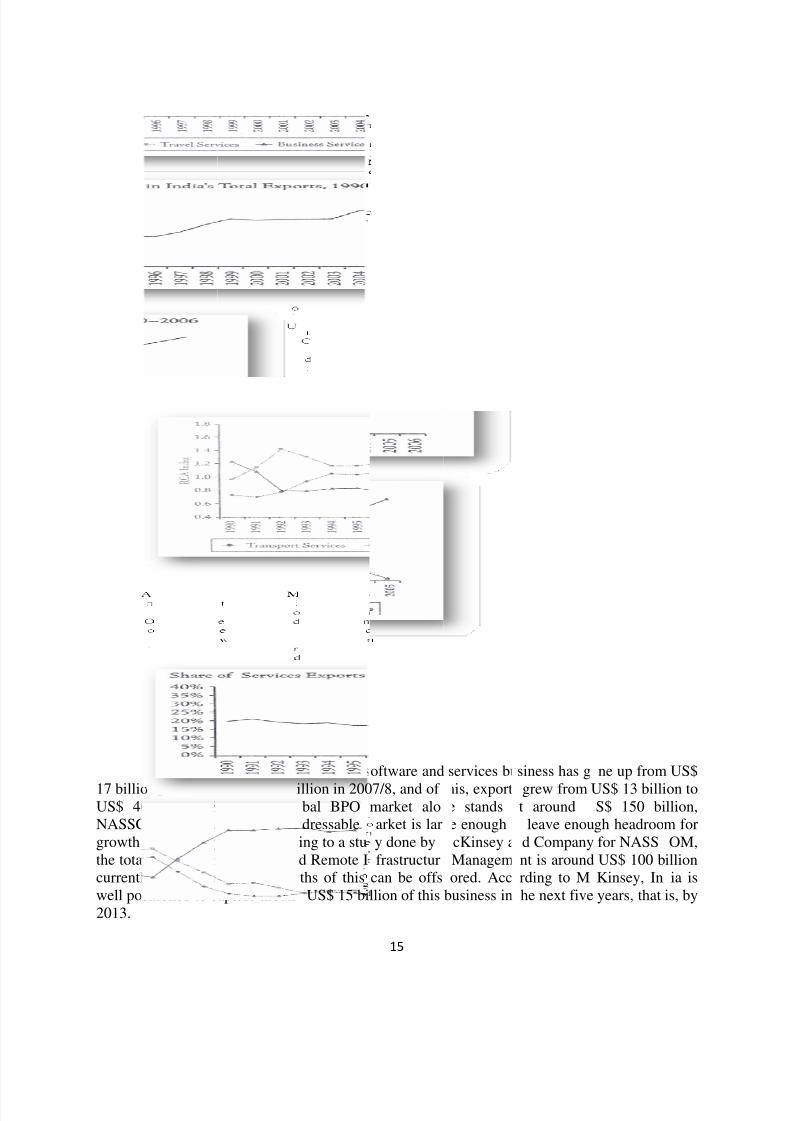

17 billioUS$ 40NASSCgrowth f the totalcurrentlywell posi2013.

ccording to

in 2003/4billion. SiM estimatr several y

market for, and arountioned to ca

NASSCO

o US$ 52 bnce the gls that the aars. Accordhat is calle

d three-foupture aroun

, the total s

illion in 200bal BPOdressableing to a stud Remote Iths of thisUS$ 15 bil

15

oftware and

7/8, and of market aloarket is lary done byfrastructur

can be offslion of this

services bu

his, exportse stands ae enough tcKinsey aManagemored. Acco

business in

siness has g

grew fromt around

leave enoud Companynt is aroundrding to Mhe next five

ne up from

US$ 13 billiS$ 150 bigh headroofor NASSUS$ 100 bKinsey, Inyears, that

US$

on tollion,m forOM,

illionia is

is, by

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 16/42

stands tomedicalFortis, tservices

software(

organizeCouncilUS$ 35by homelike Walmom anretail seccent by 2by 2017/

(

grown b

industryby 2012. just a fenext fivHollywo

ver time, asave over

treatment oe healthcarin India for

services. ) The reta

d retailingor Researcillion will

grown Indi-Mart andpop stores

tor will gro011/12. Ac18.

) Entertaiaround 19

will continuWithin this

years agoyears, in

od involvin

host of neS$ 1.5 billierseas forgroup of

nationals o

l sector: Aas grownon Internae investedn firms asarrefour. Iwill grow

w 45-50 perording to th

Siz

ment: Oveper cent pe

e to grow at, animation. The Bollluding (if the co-pro

service aron annuallyust 15 lowompanies)other coun

s India's mirom its tinional Econin organize

ell as by jRIER esti

13 per centcent per ane consultin

e of Indian

r the pastr annum, an

around theand gamingwood film

the ADAGuction of fi

16

eas are alsif only 10 prisk procedhas calculattries can be

ddle classy beginninmic Relatiretailing oint ventureates that

nnually betnum. It wilfirm Tech

Retail Ind

-4 years, td according

same rate, tare new phindustry isgroup for

lms.

likely toer cent of Uures. Harpaed that thecompared t

has growns. Accordins (ICRIEer the next

s with well-hile the to

ween 2006/

l also increaopak, this

stry (US$

he entertainto FICCI P

touch annnomena, elikely to ny is anyth

row. For inS patients cl Singh (forscope for po what has

in both sizeg to a stu) on the ret5-7 years.known interal retail bu

7 and 2011/ se its mark ill rise furt

illion)

ment andricewaterho

al revenueerging as aarly doubl

ing to go

stance, thehoose to unmer chairmroviding mbeen achiev

and propoy by the Iil sector, arhis will benational retsiness (incl12, the orgat share to 1er to 25 pe

edia sectouse Cooper

f US$ 28 bserious busin size ov

by) tie-ups

USAergo

an of dicaled in

rtion,dian

ounddoneailersding

nized6 percent

r hass, the

illioninessr thewith

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 17/42

( two-waybeing inbuying f fees paidCommittat this trrisen to

changesremoved

) Internatiflow of mested in ph

irms in othefor a variet

ee on Makiansition anaround 36

in policy thvirtually all

Size

nal Financney has in

ysical capitr countries,y of financing Mumbai

its impact,per cent, a

at have creaphysical co

of Indian M

ial Servicesvolved froal as well athere has all services.an Internatiis to look d the peri

ted a realistntrols on in

volution of

17

dia Busines

: With Indibeing not

s in stocksso been anccording t

onal Financat the traded of increa

ic market f ernational t

the Trade/G

s (Rs million

integrating just paymeand bonds.outflow of the Report

ial Centre (to-GDP ratse can alm

r the rupee,rade (see Fi

DP Ratio

)

into the glont for tradeMoreover,capital as wof the High

MIFC), theio to beginost directly

dropped taure).

bal econombut also mith Indian

ell as substPowered E

best way towith. It hasbe correlat

riffs sharply

, theoneyfirmsntial

xpertlook nowd to

, and

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 18/42

1990s toincrease.Indian fithe nextfinancialbankersis to becthe medithis figur

(

Tsector's cbe remeunbankein the cohave acccredit. Tcountry -

Tagricultu

agricultuthe geogareas. Tquartile,This sugstringentquartilesector is

s a result, tover US$Based on tms to invesdecade. It tfirms locaor differentme an inter

um-low pre could incr

) Banking S

he impactontributionbered that, For instan

untry haveess to formhis kind of less than a

he Invest Inral farm la

ral wage laraphical spre same isless than hgests thatfor most pre at intere

clearly larg

Gro

he gross flo150 billionhe projectedtment bank en works oed outsideservices, Mnational fin jections of ease substa

ctor:

f the spreato GDP rosthis contri

ce, Nationalo access tol credit. Allexclusion i

fifth of the i

dia Savingsour having

our, at 25 pead of the balso bornelf of thoseank formalople. Givenst rates of .

th of Gros

ws have ristoday. In tsize of ex

rs overseas,ut what thisthe countrIFC calculancial centr

overall flotially.

of bankinfrom 7.5

ution took Sample Sucredit, eithtold, arouns worst inndebtednes

Survey of bank acco

er cent. Theanking sectout by thewho take loities may bthat arounver 36 per

18

Flows on t

n from arorms of shaorts/Importetc., the Mmeans in t. Based ontes the total. The estims. A highe

g on GDPer cent in 2place whenrvey data rer informal

d three-quathe central,in this regi

007 revealunts. The

se numbersor which, aact that, eans take the too cum

half the locent per ye

he Current

nd US$ 15re of GDPs, FII and FIFC projectrms of broa weighte

fees that Inate for 201degree of

rowth is w001/2 to 10

the vastveal that ovor formal.ters of farmeastern, an

on is to for

d similar trigure was

indicate thais well kn

en in the cm from theersome, orans taken bar, the sco

Account

billion a qualso, this rDI inflows,the total exerage fees,

d averagedia stands t

is US$ 48integration

ell establishper cent inajority of Ir half the 4nd of theseers have nod north-easal sources

nds, with jonly a littl

t the problewn, is stillase of thebanking secredit risk

y those in te for growt

arter in thepresents athe fees paternal flowscurrently paid to mergain if Mu

billion, baswould mea

ed. The ba2006/7. It sndians rem

million fa, just arounaccess to f

tern parts of credit.

st 14 per cbetter for

is not justpoor in theop-most inctor (see Tassessmente lowest inh in the ba

earlysharpid byoverid tohant

mbaid onthat

kingould

ainedmershalf

rmalf the

nt of non-

withruralomeble).

s tooomeking

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 19/42

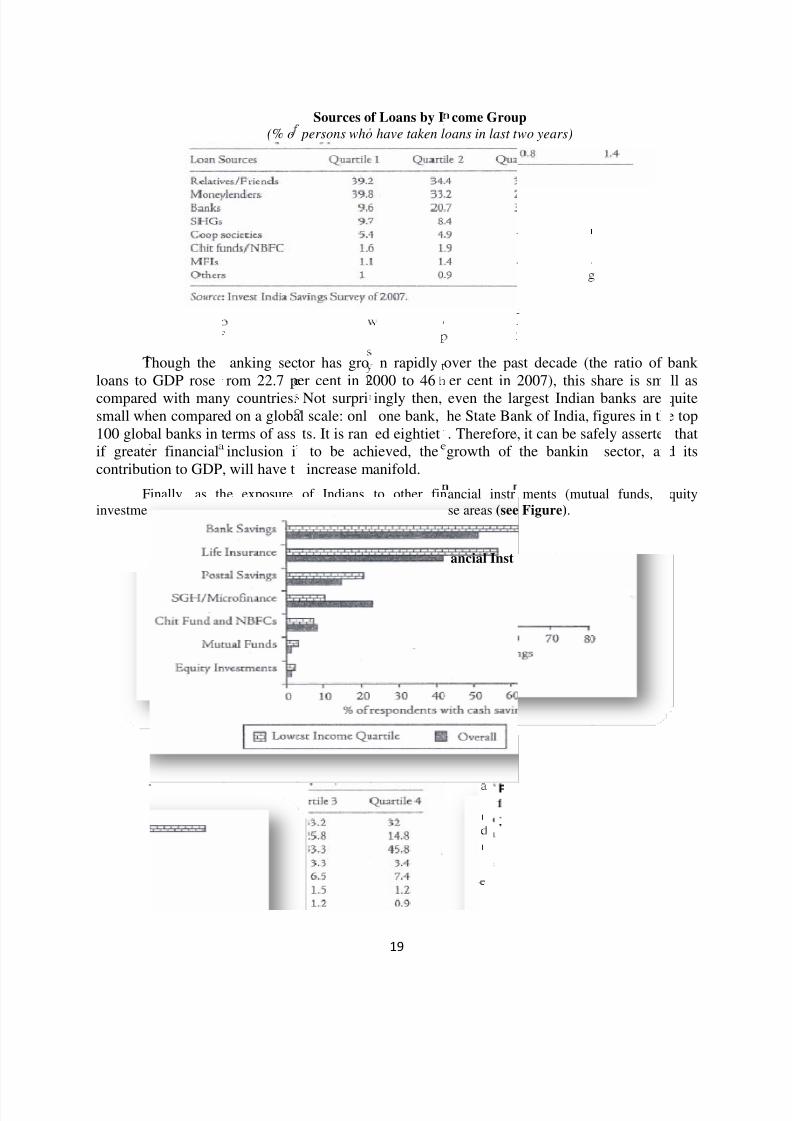

Tloans to

comparesmall wh100 globif greatecontribut

Finvestme

hough theGDP rose

d with manen compareal banks in tr financialion to GDP,

inally, as thts, microfin

(% o

anking secrom 22.7 p

y countries.d on a globaerms of assinclusion iwill have t

e exposurence) is limite

Incidence o

Sources opersons who

tor has groer cent in 2

Not surpril scale: onlts. It is ranto be achincrease m

of Indiansd, vast poten

f Savings in

19

f Loans by Ihave taken l

n rapidly000 to 46

ingly then,one bank,ed eightietieved, theanifold.

to other fintial lies in th

Different Fi

come Grouoans in last t

over the paer cent in

even the lahe State Ba. Therefore,growth of

ancial instrse areas (see

ancial Inst

pwo years)

st decade (t2007), this

rgest Indiannk of India,it can be sa

the bankin

ments (mutFigure).

uments

he ratio of share is sm

banks arefigures in thfely asserte

sector, an

ual funds,

bank ll as

quitee topthat

d its

quity

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 20/42

6. Factor

6.

Toffshorinadded sesoftwarecosts, rismaintainnewer bareas sucIndia). H

Io

Ta

But, theoffshorin

s determini

1. Moving u

raditional Ig in India.rvices suchproducts (sk, entry baleadershipsiness modh as remoteowever, in t

dia attaineffshore mar

he scope f ddressable

bigger qug?

g the sustai

the value c

services –f the total I

as engineere Figure). riers (MNosition, Ind

els that candiagnostic

he near futu

competitivet and 46%

or future eglobal IT/I

stion is wh

ability of I

ain:

software anT export reing & R&DThis is due

dominancian IT indudeliver greare and tel

re, we seem

e strength ishare of gl

pansion cES market

at if other

20

-ITES grow

d applicatioenues only; off-shoreto various b), and softtry will hater value t-pathologyto be in the

n offshore Ibal BPO in

ntinues tohas been re

(China, P

th:

developm16% (in 20product dearriers such

are piracye to invest ithe custo

in medical‘safety zon

T servicesdustry

be large alized

hilippines e

nt – represe6-07) comeelopment aas high R&in domestin innovatioers. Exampield (starte’ due to fol

ith 65% sh

s only 10

tc) catch u

nt lion’s shfrom high-d made-in-

D and mark mkt. Henand in evo

le: Innovatihappening

lowing fact

are of the g

of poten

p with us i

re of valueIndiaetinge, tolvingon infrom:

lobal

ially

n IT

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 21/42

industrygrown ficentres.and Rs 5grown to

in the pglobal Iin the bFinacle.developi

in 2009-There arinstance,and mulsome of only too23 years

governBox).

(

(companiequipmeconsumproducts

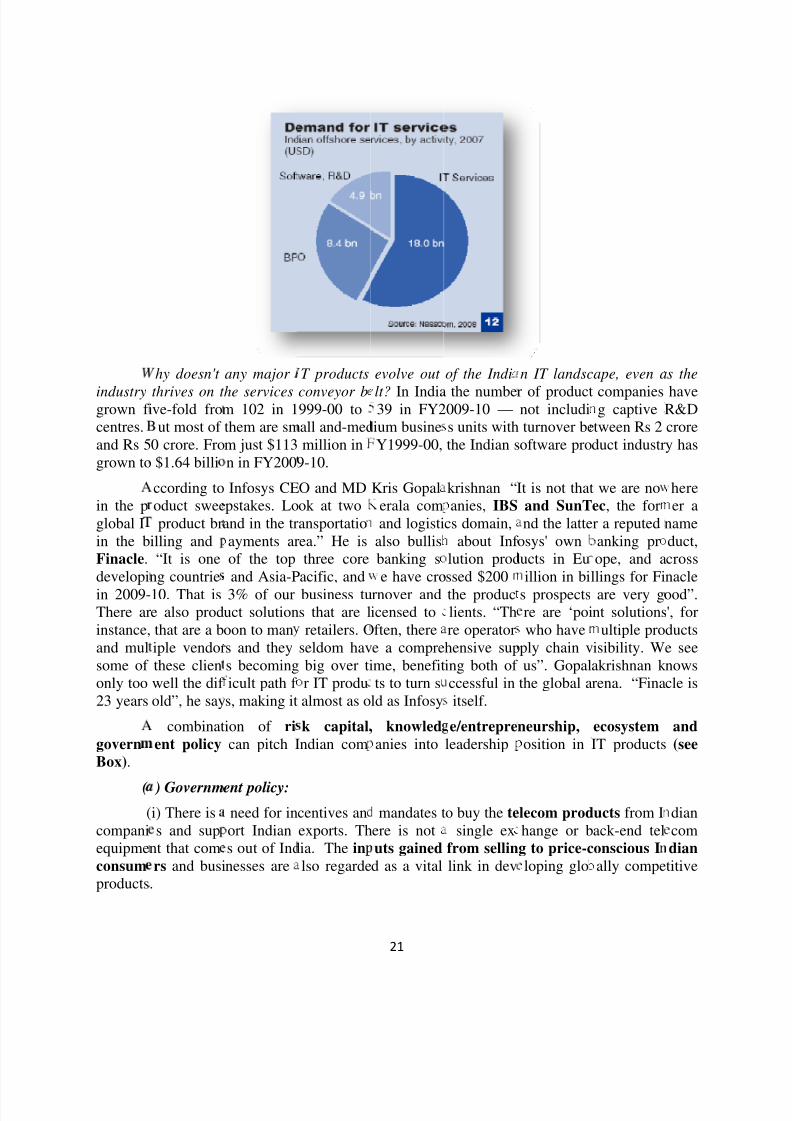

hy doesn't

thrives on t ve-fold frout most of

0 crore. Fro$1.64 billi

ccording tooduct sweeproduct br

illing and“It is one

ng countrie

10. That ise also prodthat are a biple vendorthese clienwell the dif old”, he say

combinatent policy

) Governm

i) There iss and sup

nt that comrs and busi

.

any major

he servicesm 102 in 1them are smm just $113n in FY200

Infosys CEpstakes. Loand in the trayments arof the topand Asia-P

3% of ouruct solutionoon to mans and theys becomingicult path f s, making it

ion of rican pitch I

ent policy:

need for inort Indians out of Indnesses are

T products

conveyor b999-00 toall and-medmillion in

9-10.

O and MDok at twoansportatioea.” He isthree coreacific, and

business tus that are lretailers. O

seldom havbig over tir IT produalmost as o

k capital,ndian com

centives anexports. Thia. The inlso regarde

21

evolve out

lt? In India39 in FY2ium busineY1999-00,

Kris Gopalerala comand logisti

also bullisbanking se have cro

rnover andicensed toften, theree a compreme, benefitts to turn s

ld as Infosy

knowledanies into

mandates tere is notuts gainedd as a vital

of the Indi

the numbe009-10 —s units withthe Indian s

krishnan “anies, IBS

cs domain,about Inf

lution prodssed $200

the produclients. “Thre operatorhensive suping both of ccessful initself.

e/entrepreleadership

o buy the tesingle ex

from sellinlink in dev

n IT landsc

r of productnot includiturnover beoftware pro

It is not thatand SunTnd the latte

osys' ownucts in Euillion in bi

s prospectsre are ‘poiwho have

ply chain vus”. Gopal

the global a

neurship,osition in

lecom prodhange or bg to price-cloping glo

ape, even a

companiesg captive

tween Rs 2duct industr

we are noec, the forr a reputedanking prope, and a

llings for Fi

are very gnt solutions

ultiple proisibility. Wakrishnan k rena. “Fina

ecosystemIT products

ucts from Iack-end telonscious Ially compe

s the

haveR&Dcrorey has

hereer a

nameduct,crossnacle

ood”.', forductse seenowscle is

and(see

diancomdiantitive

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 22/42

22

(ii) Local start-ups should be provided the opportunity for local start-ups to compete ongovernment projects (like Israel does). For example, the US and Israel’s defence and high-techindustries offer some fresh insights. The US has for long pursued programmes such as 8(A) andHUB Zone to harness the innovative potential of the SMEs for military and economic strength.Federal agencies including the department of defence and NIH set aside 2.8% of their annual

research budgets for SMEs and commercialisation of academic research. India’s ministry of defence’s new procurement policy says that “prime contractors” should set aside a portion of their business for SMEs. If the policy is strictly implemented, software product firms in theaerospace, machine system automation and controls can reap benefits. The ministry should notonly protect public sector navratna companies, but also ensure that private SMEs can benefitfrom set-offs of global tenders.

(iii) Government should apply more technology. Directly or indirectly, government willbe much bigger than the private sector. E-governance projects often explicitly rule outinvolvement of local niche software players, even if the company has credible deployments.Qualification criterion like independent revenue (not the company’s total revenue) is a difficulthurdle to cross for many SMEs. Domestic software firms have built successful products in

documentation management, IT infrastructure, language tools, recognition and payments. Settingaside certain percentage of projects for Indian SME product companies in e-governance projectsis a must to encourage local innovation.

(b) Entrepreneurship: The approach of the entrepreneurs and investors to buildingtechnology companies in India has been timid/nervous. Indian companies need to be alert aboutgrabbing opportunities as in the way start-ups like Tejas Networks have done. Once the collapseof the World Trade Centre upset their business plan of targeting global markets, the start-up did aquick turnaround and picked up business in India just the point when domestic demand started toboom. Today 80-90% of India’s ethernet traffic for local area network goes to Tejas equipment.

(c) Capital: Access to institutional finance is yet another area that needs to be addressed.

The number of VC and PE investments has grown substantially but the value of these funds aresmall and their portfolio strategies limits their interest, investment and hence the development of key technologies. Software product entrepreneurs should have easy access to collateral-freefunding. IP valuation for collateral is an accepted practice in all developed world and Indianbanks must be educated and encouraged to adopt the practice. Credible external benchmarkingcan also help Indian software product companies to fortify their true claims and challenge thecompetitors. Finally, angel investors should be free to open up their wallets even more. 13-14deals in a year is low. We need every angel to do at least 5 deals.

(d) Ecosystem: A mature ecosystem, Sillicon Valley for instance, should be able togenerate start-ups in new areas every 10 to 15 years. We went through a cycle where failure wasnot accepted and risk taking was an issue. We as a society were always focused on self reliance

and import substitution. If you look like product companies that are world leaders now,Microsoft or Oracle, nobody paid attention to them in their first few years. And that wasimportant as you need time to privately evolve. In India, all that is getting developed now. Thereis angel funding. Money is not a major issue now. We are starting to see a lot of experiencedpeople coming out and starting up ventures, especially from large MNCs.

Also, assembling talent from other sources takes time. We have to get that foundationready. Once we get going in the Sillicon Valley, we draw from a pool of talent from even giants

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 23/42

23

like Google, Yahoo and Microsoft. Don Valentine, the founder of Sequoia drew talent fromSillicon Velley (IBM and Xerox PARC). He was the original investor in Apple and then Ciscoand Google. Their foundational companies were IBM and Xerox.

BOX: Higher Productivity will be a Dream Unless Mindset Changes

Indian IT industry is at a crossroads. The professional services model is no longer fuelling the growth it

once did. Productivity, as measured by revenue per employee, has long been stagnant among Indian IT

majors.

The leading Indian IT powerhouses bring in $45,000 per employee per year while for the second‐and

third‐tier firms, it sinks to $30,000 per year. Compare that to Google and Facebook, which make

upwards of $1 million per employee per year in revenue, and enterprise software companies like Oracle

bring in $350,000 per employee per year. In Indian IT, these numbers are a distant dream. They don't

have to be.

Yet, higher productivity will remain a distant dream unless there is a wholesale cultural and mindset

change. Google and Facebook are rewarded with high productivity because of their f lexible cultures

that empower employees and their intrinsic risk taking attitude.

Indian companies, by contrast, have very conservative topdown corporate cultures. The services

business model also encourages bloat, and the bloat becomes a core part of a culture.

In a product company, all our incentives are aligned to use people as efficiently as possible. In a services

business model, the more headcount a project can justify, the more money it makes, which makes it

difficult for a project manager to use resources efficiently.

At Zoho, we resisted the easy allure of the services business in our early days (in the late 1990s), instead

choosing to forge a path based on creating compelling products. It was a difficult path at first, because

there just wasn't any expertise in building products in India and penetrating a market with new products

is never easy.

After a slow start, we have emerged as one of the leading software product companies coming out of

India. Our productivity is not yet on par with our global peers, but it is still substantially ahead of Indian

services companies. We have set ourselves the goal of reaching global productivity levels in the next 5

years.

How do we do it? It all comes down to culture. We turn every piece of received wisdom in Indian IT on

its head. We do not care about certifications like CMM. Our recruitment model focuses on real ability

and passion than on degrees and paper credentials. We are proud to say that most of our people

actually were originally rejected by the major IT companies in India ‐‐ their loss was our gain.

We do not have the rigid hierarchy, endless meetings, and a slavish devotion to process that

characterise the life of most IT professionals. Instead, we emphasise f lexibility, adaptation and cultivate

a certain disregard for authority in our people ‐ we absolutely prohibit ancestor worship in our

company! Our

promotions

are

based

on

demonstrated

performance,

not

on

the

number

of

years

spent

doing it. It is not uncommon for relatively "junior" people in positions of authority in our firm.

We do not force anyone to stay with us; we follow the same "atwill" employment rule that is common in

the US, meaning that anyone can leave us anytime, with absolutely no notice to us if they choose. Yet

our attrition rate is among the lowest. That is not for lack of opportunity: our employees all know that

their experience at Zoho is very valuable, but they voluntarily choose to stay because of the culture and

opportunity.

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 24/42

24

We believe the path ahead for Indian IT is in embracing more f lexibility and innovation, discarding ideas

that may have worked in the past but no longer work in today's age. The path to productivity lies in

empowering employees to reach their full human potential.

Source: Authored by Sridhar Vembu. He is founder and CEO of Zoho Corporation. ZOHO Corporation are

the makers of the online Zoho Office Suite as well as several business applications. He has been in the

news not

only

for

creating

one

of

the

first

online

(Cloud

Computing)

office

suites

as

a company,

but

also

for the unique staffing practices of ZOHO which hires economically disadvantaged high school graduates

and puts them through two years of education with a strong focus on engineering / software. This article

appeared in The Economic Times dated 14 February 2012.

6.2. HR related challenges:

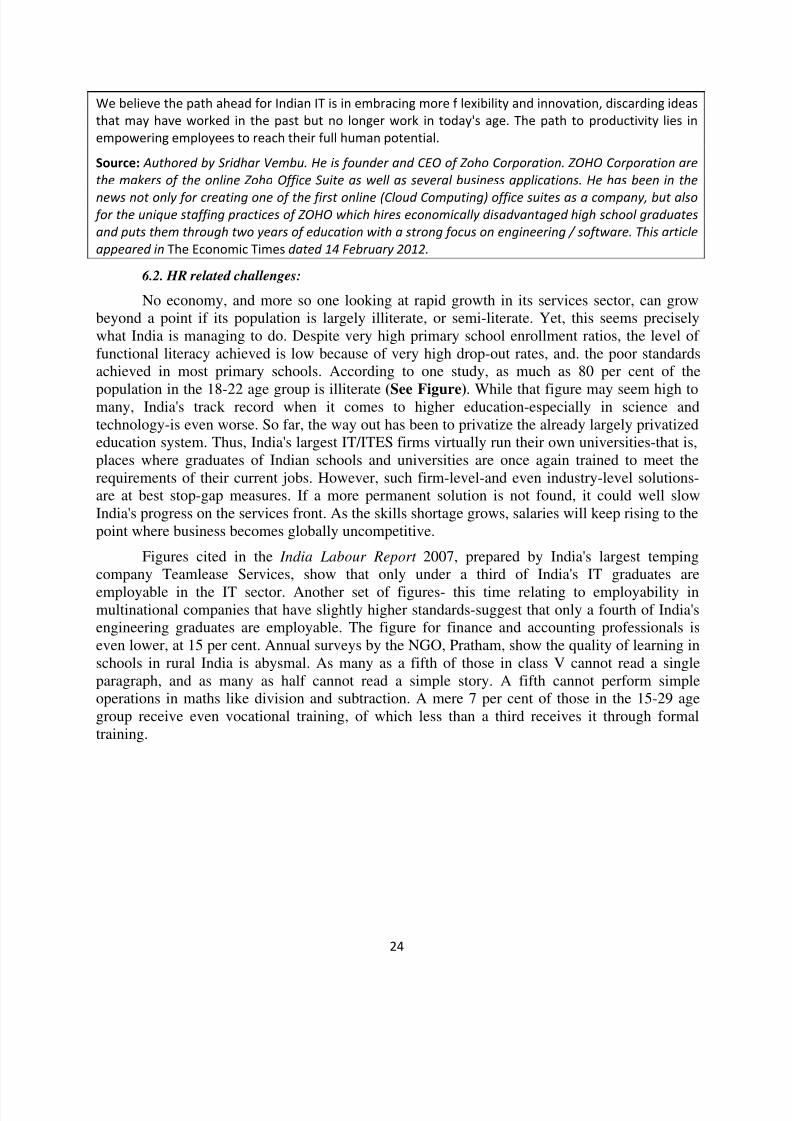

No economy, and more so one looking at rapid growth in its services sector, can growbeyond a point if its population is largely illiterate, or semi-literate. Yet, this seems preciselywhat India is managing to do. Despite very high primary school enrollment ratios, the level of functional literacy achieved is low because of very high drop-out rates, and. the poor standardsachieved in most primary schools. According to one study, as much as 80 per cent of the

population in the 18-22 age group is illiterate (See Figure). While that figure may seem high tomany, India's track record when it comes to higher education-especially in science andtechnology-is even worse. So far, the way out has been to privatize the already largely privatizededucation system. Thus, India's largest IT/ITES firms virtually run their own universities-that is,places where graduates of Indian schools and universities are once again trained to meet therequirements of their current jobs. However, such firm-level-and even industry-level solutions-are at best stop-gap measures. If a more permanent solution is not found, it could well slowIndia's progress on the services front. As the skills shortage grows, salaries will keep rising to thepoint where business becomes globally uncompetitive.

Figures cited in the India Labour Report 2007, prepared by India's largest tempingcompany Teamlease Services, show that only under a third of India's IT graduates are

employable in the IT sector. Another set of figures- this time relating to employability inmultinational companies that have slightly higher standards-suggest that only a fourth of India'sengineering graduates are employable. The figure for finance and accounting professionals iseven lower, at 15 per cent. Annual surveys by the NGO, Pratham, show the quality of learning inschools in rural India is abysmal. As many as a fifth of those in class V cannot read a singleparagraph, and as many as half cannot read a simple story. A fifth cannot perform simpleoperations in maths like division and subtraction. A mere 7 per cent of those in the 15-29 agegroup receive even vocational training, of which less than a third receives it through formaltraining.

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 25/42

C

levels of servicesWorld BTable):economicountry'scountrie

Countr

USA Korea. Re

Malaysia Russia Brazil China Indonesia

India

ertainly, In

education,sector is theank capturit takes in

incentivepopulation..

y

Recent

9.1 p. 7.67

6.16 5.58 5.5 4.36 3.27 3.04

Penetr

ia's educati

what alsoextent of ths most of to account

regime inTo no one'

EI E

1995 R

9.51 9.

7.85 5.

6.04 6.

5.53 1.

5.03 4.

3.48 4.

3.46 3.

3.13 3.

tion Level

on budgets

matters fore use of inf hese paramlevels of ea country,

s surprise, I

Knowlonomic Inc

nd Instructi

Regime

ecent 1

6 9.2

7 6.75

6 7.21

5 2.43

4.81

1 3.31

6 4.02

7 3.48

25

of Educati

are nowher

an economormation teeters in itsducation, i

and thendia's absol

edge Econntive

onal In

95 Rec

9.45

8.47

6.82

6.88

6.06

5.1

3.31

3.95

on (18-22

e near what

trying tohnology, aKnowledgeformationnormalizeste scores la

my Indexovation

nt 1995

9.58 8.16 6.2 5.61 5.88 4.26 2.4 3.61

ge Group)

are needed

develop onwell as R&Economy I

technology,them keepig behind th

Education

Recent 19

8.79 9.4

7.89 8.3 4.35 4.1

7.62 8.0

5.78 3.9

4.06 3.6

3.45 3.9

2.11 2.5

. Apart fro

the basis oD spendingndex (KEI)as well a

ng in minse of peer

IC

5 Recent

9.02 8.74 7.3 6.26 5.87 4.28 2.94 2.45

the

f the. The(see

s thethe

roup

1995 9.83 8.2 6.57 6.05 5.5 2.74 3.5 2.87

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 26/42

Tis also acomes tsupply,higher s

levels of 6.

IwitnessiorientedIT adopt40% of insurancdemand

Tin IndiaOpportu

(ion IT sespends astaff and

(i

providercommitdomestic

(iadvantagoutsourcservices

he governmgreater wiltechnical

s also (onelaries com

the illiterat 3. Lack of f

dian IT ig gradual(Graph). Lion was witomestic IT, and manor IT servic

he followinas highlightity.

) Significanrvices accocount forassociated

i) Majority

. Also, CIent and exIT market i

ii) The levee has beening in Indiaand relate it

ent has nolingness toeducation.hopes) quaanded by a

are compar cus on dom

dustry ishange in I

iberalisationessed in telservices spfacturing;es in near f

g are the md in a NAS

t portion of unts for mo5%. In-houverheads

of CIOs fel

s felt thatertise that ts still not a

l of awarenpoor. The

. Hence, ITto business

set its minallow theand for pulity. The dn educated

ed with tho stic IT mark

redominantndia: from

is the keyecom and bnding in Innd e-goverture.

jor reasonsSCOM-ID

domestic cre than halsing IT spe

t that dome

IT servicehey offer thpreciated b

ess about thcost arbitrcompaniesbenefits

26

d to increasrivate sectlic-privatemand for eerson-the

e having pet:

ly exportpredominandriver of inanking sectdia. Pressunance initia

for the narrStudy on t

orporate ITof corpor

ding includ

stic custom

roviders haeir global cmany of d

e potentialge continuneed to cle

ing public sr an expanpartnershipducation, iedian mult

st-graduate

riented. Btly hardwarreased IT

ors. These te of competives are e

w base of the Domesti

spends lieste IT spenes training

rs were no

rdly offer Iustomers.mestic IT s

of using ITs to be le

arly articula

pending onded role, es. All of t

turn, williple being s

degrees.

t, domestie driven todoption in I

wo sectorstition in secpected to e

he domesticc Services (

in-house. Iin India,

osts, salari

t a focus ar

ndian custoIOs believeervices pro

as an enabls attractivete value pr

education.pecially wis will im

be driven bven when s

IT demawards a serndia. Signiccounted f tors like airnhance do

IT-ITES mIT-ITES) M

-house spehile outso

s of in-hou

ea for IT se

mers the kithat potentiders

r of compe justificatioposition of

hereen itrove

y thealary

d isvicesicantr 35-lines,estic

arketarket

dingrced

se IT

rvice

d of ial of

titiven fortheir

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 27/42

(iadvantagfrom rouof their texpected

(tourism,

(major gr

6.4.

Eavoid risreluctantEast Asi

6

IBPO delin 30 locreation

6 E

substantithe totalprojects

v) CIOs aree) deliveretine IT operime and eff to play a k

) Apart frhealthcare)

i) Larger awth engine

ountry-spe

fforts at exk. But thisto engagefor more b

.5. Metro-c

SEZ areivery footprations. The

of both soci

.6. Infrastrven in theal amountsindustry cnd infrastr

under pressfrom IT in

ations to strort in day-ty role in hel

m banking,need to be d

d mature Ifor domesti

cific conce

anding UKarket is stiith India d

usiness

Geogra

ntered IT d

urther incrint had gro

implicatioal and physi

cture constmetros, leton transporst. Moneycture creati

ure to justif vestments.ategic IT m-day operaping CIOs i

financial seveloped to

users incrc IT market

tration of e

and Europll dominatee to langua

hical Conc

evelopment

asing digitn beyond aof this is

cal infrastru

raints:lone Tier-Iation, powsaved on tn in Tier II

27

IT investHigher expnagement.ions of ITn streamlini

ervices andexpand IT

asingly pre.

ports (US

an marketsby the U.Se hurdle. I

ntration of

or “slow ge

l divide. Bfew metros

the need tocture in the

I and Tier-Ir, communiese frontsand Tier III

ent by demctations fr

This meanssolution. Hng their IT

telecom nervices mar

er end-to-e

& Europe

have intensand East Emajors are

T-BPO Exp

ographical

ut, off lateto encompincrease d

Tier 2 and 3

II cities, ITcation andcan be depcities.

onstrating vm IT requithat they nere, IT serviperations

w verticalsket in India.

d IT servic

:

ified in theurope. Contalso targeti

orts

spread” IT:

things are css some 25livery centcities.

industry hsecurity. Alloyed for

lue (compee CIOs toed to spendes provide

(manufact

s. This will

ast few yeinental Eurng Southeas

hanging: In0 deliveryes which

s been spel these addore constru

titivemovemosts are

ring,

be a

rs tope ist and

dia’sointseans

dingup toctive

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 28/42

28

6.7. Growing global competition:

Competition from Pakistan, Bangladesh, Israel, Latin America, Ireland, Singapore,China, Malaysia, Philippines, Eastern Europe, South America, South Africa, and Sri Lanka hasbeen increasing. The last 5 are aggressively competing for BPO space by offering a variety of fiscal and other incentives. However, dominant Indian players are adopting a proactive approach.

They recruit experts from competitors (Pakistan, Bangladesh and China) and thereby expandingtheir capacity.

According to Infosys CEO and MD Kris Gopalakrishnan it's no more a case of Indian ITcompanies being seen as local companies with big turnovers, but global players in the true senseof the word. According to him one can see a distinct trend of companies extending theirfootprints across the globe. And these are primarily because of two reasons: Firstly, there is theneed to support clients and their businesses in languages other than English, for which a single-location operation will not suffice. And secondly, there is the need to take advantage of time-zone differences. We are, after all, talking about 24X7 services and no company can afford tooffer any less in a globally competitive arena.

For Infosys, that global mantra is quite evident. “The company has full-fledgedoperations out of the Philippines, China, Poland, Czech Republic, Mexico and Brazil, andconsultancy offices in 40 countries.” It is all about multiple delivery capabilities in multiplelocations. A closer look at those locations reveals that it is a winning mix of locations that featuredifferent languages and cost-effective operations.

6.8. Low R&D spending:

Presently only 2-4% of total spending of software companies in India are spend on R&D.Against this, internationally reputed software firms spend 14-19%

6.9. Growing competition from MNC IT companies:

Today, 80% of top 100 IT companies in the world have their presence in India. In 2002-2003 foreign affiliates accounted for about 58% of India’s exports of back office services usingoffshore mode. They are competing with local companies both for Indian workers and foreigncontracts. This combination is driving up wages and squeezing margins. From the perspective of financial capability, pedigree (record), heritage MNCs have an edge. However, expertise of dominant Indian players puts them 10 to 15 years ahead of their international rivals.

6.10. Persistent threat from anti-outsourcing lobby in USA:

Results in difficulty of securing right type and number of American visas. Hence,handling political process in US will be important. However, Cognizant CEO Francisco D’Souzasays the recent protectionist measures by USA cannot be treated as rhetoric. He thinks thereare some real pressures in the US right now because of high unemployment rate (10%). To him,the discussion needs to go back to what is the alternative question. Because the challenge wehave in the US is that while unemployment is at 10%, the IT unemployment is very low. Thereality is that US is not producing scientists and engineers at the rate that the industry

needs. So, it’s a real problem for US companies. To compete in the US companies in the worldis becoming more technology intensive. He thinks the Border Protection Bill, the visa bill wasunfortunate because sufficient debate didn’t happen around the broad implications of such amove when it comes to competitiveness of companies inside the US. It’s in everyone’s interestfor the economies of the world to recover, and the fastest way to achieve this is by making the

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 29/42

29

companies healthy. He thinks it’s very very dangerous when you try to hold back a key pool thatcompanies need in order to be competitive: which is talent. Many companies are responding tothe backlash by announcing more local hiring in the US.

7. Service sectors that will see accelerated growth in the coming years (i.e. in the medium

term) in India:

a) Telecommunications: Telecom density has grown by leaps and bounds because priceshave been cut to the bone, with local and long distance calls costing a tiny fraction of what theyused to. The result is that the industry is able to make a profit even when the average revenue peruser has dropped to a couple of hundred rupees per month. A supporting role has been played bythe steady drop in handset prices.

b) ITES: The labour cost arbitrage and satellite connectivity that drove the initialbusiness successes have been supplemented by movement up the value chain for the delivery of more sophisticated services, including business consulting which ties in with the re-engineeringof business processes and their eventual outsourcing/off shoring. These have proved to be

sustainable business models, driven by focused companies that have demonstratedentrepreneurial drive and ingenuity.

c) Road transport: The rapidly expanding road network, with a proper system of national highways, has speeded up truck movement by 50 per cent and more.

d) Rail transport: The improved traffic and operating ratios achieved by the railways,and the large investments planned for expanding the system (like the dedicated freight corridorsfrom the north to ports in the west and east) mean that there will be active competition betweenroad and rail.

e) Civil aviation: Could sustain the growth if oil prices are at reasonable levels.

f) Financial services: The banking system still serves only the top 40 per cent of thepopulation. Life insurance penetration is low, and capital market risks are taken only by a smallminority. All this will change, aided by the advent of aggressive players in the private sector, likethe ICICI Bank, which are grabbing market share from the legacy of public sector giants. Greaterdomestic inclusion (one of the key issues addressed in the report of the Raghuram Rajan!Committee) and operations in the international world of finance (an area of opportunity as speltout by the Percy Mistry'' Committee on making Mumbai an international financial centre) are thetwo broad thrusts required to raise the share of financial services' contribution to GDP.

g) Media and Entertainment: It has also emerged as a rapid growth sector: the growingcorporatization of the Mumbai film industry, the financial muscle of the entertainment TVbusiness (born in 1992 with the advent of satellite TV), and ambitious plans, like the Anil

Dhirubhai Ambani Group's proposed investment of $ 1billion to make movies with StevenSpielberg, are all symptomatic of this changing reality.

h) Modern retail: Modern retail, which is in early stages, is set to capture 16 per cent of the total retail market by 2013, and 25 per cent by 2018, compared to just 3 per cent today. Infact, in urban areas, it already accounts for 8 per cent of retail spending. [For more details referthe lecture note titled “Organised Retailing in India: A Blessing or a Curse?”]

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 30/42

i)educatio(pronouneducatio2008 and

Tschoolswell as cstill morplayers.low whiIT eductechniqu

Tinstitutesto develthoughinfrastruforeignprivate eyears.

Educationindustry

ced "k twe) and highis expected

he Indian ere highest iolleges with

than fiftyIn respect th emphasiztion and hs.

he Indian e (see Figurp the structthe governture whichniversities

ducation m

: Accordingin India halve"/"k to tr educationto grow at

ducation inthe countra focus on

percent of tthe countr

es the needas enhance

ducation sy). With eco

ure of the Iment hascan be fulfilwhich willrket of US$

to the 2009s been gro

elve" is asegments.12% CAG

ustry is inand there i

IT educatiohe market iy's populatiof training i

the need

tem comprnomic growdian educataken manled by privahelp in sh38 billion i

30

Netscribesing strong

designationhe educati

R to INR 8

its develops a strong n. The Gov

s untappedn and num

nstitutes. Thfor trainin

ises of forth and enhaion sector.y initiativete players.ping the es expected t

report on H

ly with mafor the su

on industrybn by 201

ent stage.ed to set urnment haswhich shober of stude growing Imarket as

al and infonced techno

unds are as for thehe governucation ino grow to

igher Educa

jor contribof primar

was valued.

The numbehigher sec

set up mans an oppornts, trainedT industry iwell as en

rmal netwology it has bmajor concdevelopmeent has opeustry structS$ 108 billi

tion in Indi

tion fromy and secoat INR 50

s of juniorndary schoICT school

unity for pteacher's ra

n India is drhanced tea

k of educatecome necern in the mt of educ

ned the dooure. The con in the ne

, theK-12dary

bn in

basicls ass butivatetio isivinghing

ionalssaryarketationrs forrrentxt 10

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 31/42

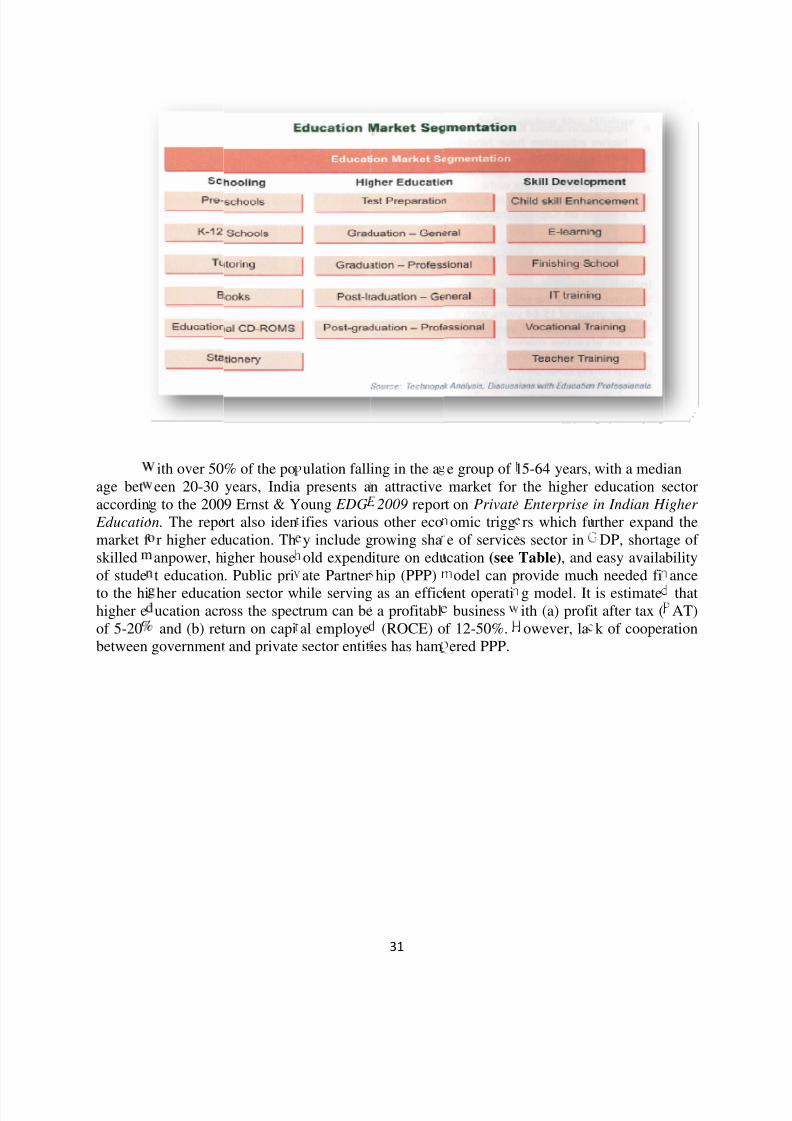

age betaccordin Educatio

market f skilledof stude

to the hihigher eof 5-20between

ith over 50een 20-30

g to the 200n. The repor higher edanpower, ht education

her educatiucation acrand (b) ret

government

% of the poyears, India9 Ernst & Yrt also idenucation. Thigher house. Public pri

on sector woss the specurn on capiand private

ulation fallpresents a

oung EDG

ifies variouy include gold expendate Partner

hile servingtrum can beal employesector entiti

31

ing in the an attractive2009 repor

s other ecorowing shaiture on eduhip (PPP)

as an efficia profitabl(ROCE) o

es has ham

e group of 1market fort on Private

omic trigge of servicecation (seeodel can p

ent operatibusiness

f 12-50%.ered PPP.

5-64 years,the higher Enterprise

rs which fus sector inTable), androvide muc

g model. Itith (a) profiowever, la

with a medieducation sin Indian H

rther expanDP, shortaeasy availa

h needed fi

is estimatet after tax (k of cooper

anectorigher

d thege of bilityance

thatAT)

ation

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 32/42

PPP and

32

High Education

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 33/42

33

8. WTO and Indian Services Sector

The General Agreement on Trade in Services (GATS) was one of the major areas of theGeneral Agreement on Tariffs and Trade (GATT) in the Uruguay Round, which concluded inGeneva on Dec. 15, 1993. The Uruguay Round expanded the scope of the multilateral tradingsystem to cover trade in services through the GATS. The GATS is the first multilateral

agreement to provide legally enforceable rights to trade in a wide range of services. The GATS,which came into force on 1 January 1995, was aimed at facilitating trade and investment inservices through the progressive liberalisation of restrictions on trade and investment flows inservices.

One of the important objectives of GATS is to promote trade in services throughprogressive liberalisation and enhancing the participation of developing countries in it. TheGATS is the first and only multilateral framework of principles and rules for governinginternational trade in services. The developed countries account for major share in serviceexports (approximately 80 per cent) in contrast to developing countries who despite theiradvantageous position in producing cheaper services fail to reap the maximum benefits becauseof a plethora of tariff and non-tariff barriers on trade. In this context, the role of GATS becomescrucial for shaping the future course of world trade as it has brought services sector trade underits ambit.

Traditionally speaking, services are considered to be non-tradeable because as comparedto goods they are having certain distinct characteristics such as intangibility, non-storability, and also these are embodied in the person or thing in question. Some of them require physicalproximity of the provider and the consumer (for example, the doctor and patient) as they have tobe consumed as soon as they are produced. Therefore, services were outside the purview of GATT/WTO negotiations for long. However, with the development in technology (advent of internet services, telecommunication revolution, and advent of satellite communication) andreduction in transportation cost it has become possible to overcome many of these constraints

associated with trading services. As a result, many of the previously non-tradeable services havebecome tradeable internationally.

In the light of the ongoing `service revolution' in India, naturally it is expected thatservices sector has vast export growth potential under WTO regime.

8.1. What is the significance of trade in services?

(a) Foreign exchange earning potential

(b) Both services and manufacturing sectors are inextricably linked throughintersectoral linkages. `Splintering' of industrial activity will lead to further push in the growth of services across the world by way of increasing the demand for service inputs for production of manufacturing goods. This may open up vast export opportunity for Indian services. On the otherhand, in this modern era of globalisation and competition, the use of quality service inputs isbecoming a pre-requirement for making our goods internationally competitive. Therefore, theneed for various complementary or producer services whether indigenous or imported, is boundto increase for Indian manufacturing sector in the near future. In a free services trade regimesuch service requirements can be imported.

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 34/42

34

(c) Some of the services are relatively cheaper in some countries than others due todifference in their factor endowments (e.g. cheap labour). WTO regime offers immenseopportunities to open up trade in those services.

(d) Trade in services can prove to be instrumental in generating additional employment

opportunities for the professional and technical personnel by creating a demand for their

services (doctors, nurses, teachers, computer experts, etc.) abroad.

8.2. Modes of Service Transaction Available under GATS:

GATS defines trade in services as "the supply of a service from the territory of any other

member; in the territory of one member to the service consumer of any other member; by a

service supplier of one member, through commercial presence in the territory of any other

member; and by a service supplier of one member, through presence of natural persons of a

member in the territory of any other member.” There are four modes specified in the agreementthrough which trade in services can materialise:

Mode 1: Cross-border supply - In this case physical movement of provider or user notrequired because of usage of information technology. Examples are IT-ITES services, e-banking,telemedicine, distance learning, export of CDs of movies, music concerts, dance performances.

Mode 2: Consumption abroad - In this case there will be a movement of user to theprovider. Examples are foreign tourist visiting India and utilising hotel services, foreign patientsutilising our health services and vice versa.

Mode 3: Commercial presence – Under this mode, the suppliers of a service of aparticular country establish a legal territorial presence in another country to provide theirservices. This involves setting up of a service establishment like a construction or an engineeringfirm or bank offering construction or engineering or banking services through FDI mode.

Mode 4: Movement of natural persons - In this case, the provider of service goes to the

user, but only on temporary basis, i.e. not for entry into the permanent labour market. This modeof services trade involves movement/presence of natural persons. Examples are temporarymovement of natural persons such as Indian teachers, doctors visiting foreign universities forteaching and research, engineers, consultants going abroad on short term basis.

As per the WTO estimates, Mode 3 accounts for the highest share in world trade in

services (57%) followed by Mode 1(about 28%), Mode 2 (14%) and Mode 4 (1%) respectively.

8.3. What are the Potential Areas of Services Trade for India?

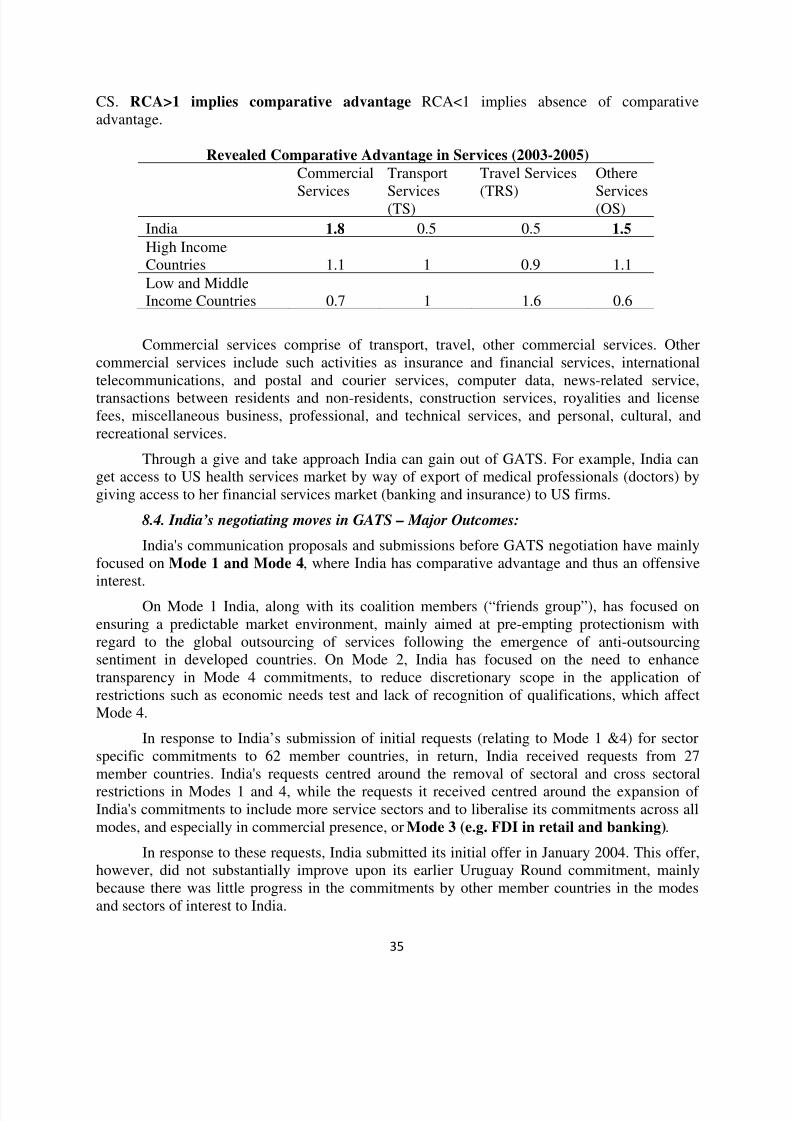

India has a clear cut Revealed Comparative Advantage (RCA) in the exports of commercial services and this is mainly due to the advantage we have in other commercial

services than transport and travel services (Table).RCA is the ratio of two different ratios. The numerator is the ratio of export of

commercial services (CS) of the region/country to its total exports (merchandise + CS). Thedenominator is the ratio of world export of CS to world exports. In case of components of CS,the numerator is the ratio of export of a component of commercial services (TS/TRS/OS) of theregion/country to its total exports of CS. The denominator remains the same for eachregion/country and is the ratio of world export of that particular component to world exports of

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 35/42

35

CS. RCA>1 implies comparative advantage RCA<1 implies absence of comparativeadvantage.

Revealed Comparative Advantage in Services (2003-2005)

Commercial

Services

Transport

Services(TS)

Travel Services

(TRS)

Othere

Services(OS)

India 1.8 0.5 0.5 1.5

High IncomeCountries 1.1 1 0.9 1.1

Low and MiddleIncome Countries 0.7 1 1.6 0.6

Commercial services comprise of transport, travel, other commercial services. Othercommercial services include such activities as insurance and financial services, internationaltelecommunications, and postal and courier services, computer data, news-related service,

transactions between residents and non-residents, construction services, royalities and licensefees, miscellaneous business, professional, and technical services, and personal, cultural, andrecreational services.

Through a give and take approach India can gain out of GATS. For example, India canget access to US health services market by way of export of medical professionals (doctors) bygiving access to her financial services market (banking and insurance) to US firms.

8.4. India’s negotiating moves in GATS – Major Outcomes:

India's communication proposals and submissions before GATS negotiation have mainlyfocused on Mode 1 and Mode 4, where India has comparative advantage and thus an offensiveinterest.

On Mode 1 India, along with its coalition members (“friends group”), has focused onensuring a predictable market environment, mainly aimed at pre-empting protectionism withregard to the global outsourcing of services following the emergence of anti-outsourcingsentiment in developed countries. On Mode 2, India has focused on the need to enhancetransparency in Mode 4 commitments, to reduce discretionary scope in the application of restrictions such as economic needs test and lack of recognition of qualifications, which affectMode 4.

In response to India’s submission of initial requests (relating to Mode 1 &4) for sectorspecific commitments to 62 member countries, in return, India received requests from 27member countries. India's requests centred around the removal of sectoral and cross sectoral

restrictions in Modes 1 and 4, while the requests it received centred around the expansion of India's commitments to include more service sectors and to liberalise its commitments across allmodes, and especially in commercial presence, or Mode 3 (e.g. FDI in retail and banking).

In response to these requests, India submitted its initial offer in January 2004. This offer,however, did not substantially improve upon its earlier Uruguay Round commitment, mainlybecause there was little progress in the commitments by other member countries in the modesand sectors of interest to India.

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 36/42

36

In August 2005, India submitted a revised offer in which it not only showed a willingnessto expand the scope of its Uruguay Round commitments by tabling several new service sectorsand subsectors for negotiations, but also signalled that it was willing to remove commercialpresence restrictions in some key areas that it had already committed. Eleven sectors and 94 sub-sectors were covered in the revised offer as opposed to seven sectors and 47 sub-sectors in the

initial conditional offer. The change in stance reflected a new strategy on the part of India, of being more forthcoming in the services negotiations, by tabling more sectors, including somedomestically sensitive sectors, and by offering to bind its commitments at higher levels of liberalisation in areas where India had been a recipient of many requests, in the hope of receivingimproved revised offers in modes 1 and 4, where there had been little progress.

8/2/2019 Is Service-Led Growth a Miracle for India

http://slidepdf.com/reader/full/is-service-led-growth-a-miracle-for-india 37/42

37

APPENDIX: Interview with Professor Jagdish Bhagwati

Quid pro quo in services sector negotiations is needed. But so are rules on hiring and firing.

Professor Bhagwati is the University Professor at Columbia University and Senior Fellow in International

Economics at the Council on Foreign Relations. He is regarded as one of the foremost international trade