is voluntary compliance becoming less voluntary

TRANSCRIPT

Is Voluntary Compliance Becoming Less Voluntary? A Whistleblower Case Study and Other Tax Compliance Topics

Presented byMegan L. Brackney, Kostelanetz & Fink, LLPBrian W. Kittle, Mayer Brown LLP*John P. Steines, New York University School of LawMario J. Verdolini, Davis Polk & Wardwell LLP

January 23, 2018

*Providing no comments on case study

Agenda

A Whistleblower Case Study: CaterpillarInternal Investigations in Tax CasesShould We Let Sleeping Dogs Lie? Mistakes in Prior Returns

1

A Whistleblower Case Study:Caterpillar

2

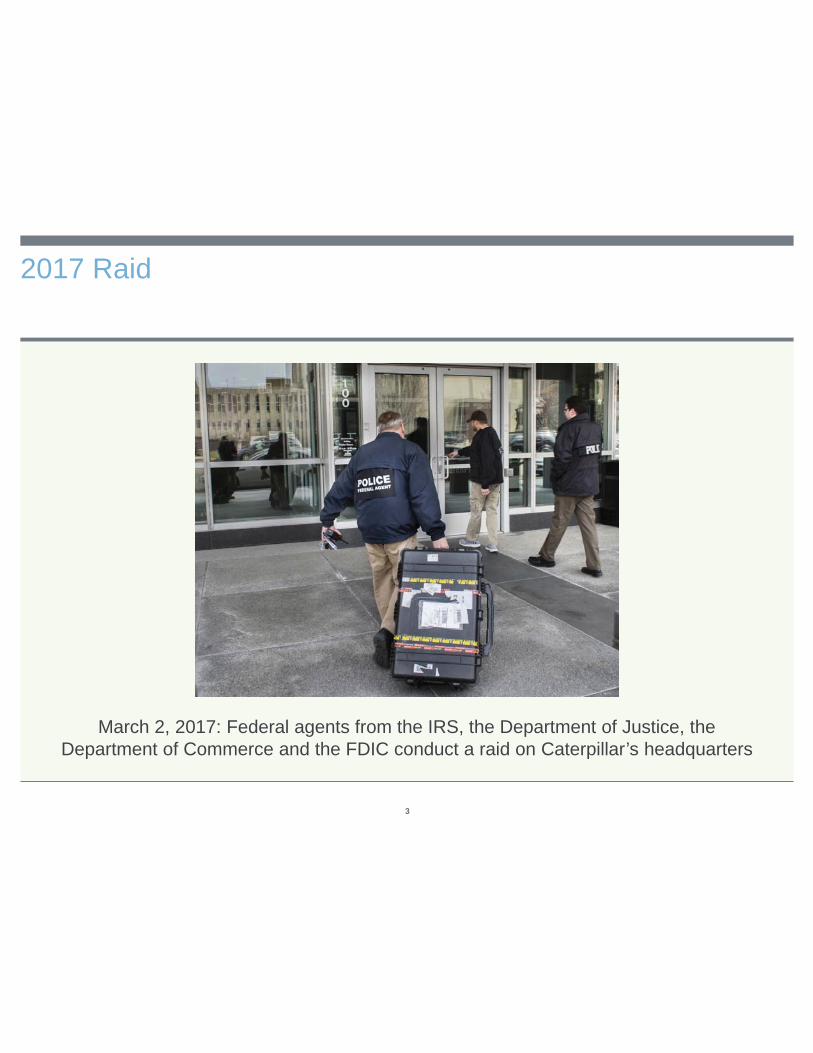

2017 Raid

March 2, 2017: Federal agents from the IRS, the Department of Justice, the Department of Commerce and the FDIC conduct a raid on Caterpillar’s headquarters

3

2014 Senate Hearing

April 1, 2014: Senator Carl Levin (D-Mich.), Chairman of Permanent Subcommittee on Investigations, at hearing on Caterpillar’s Offshore Tax Strategy

4

Whistleblower Claim and IRS Proposed Adjustment

In 2008, Daniel Schlicksup (Global Tax Strategy Manager) sends claim to IRS

In June 2009, Schlicksup files retaliation lawsuit against company, bringing Caterpillar tax strategy to attention of Senate Permanent Subcommittee on Investigations

In December 2013, IRS asserts $2.4B in adjustments against Caterpillar for years 2007 to 2009 relating to non-U.S. Caterpillar subsidiary, CSARL

5

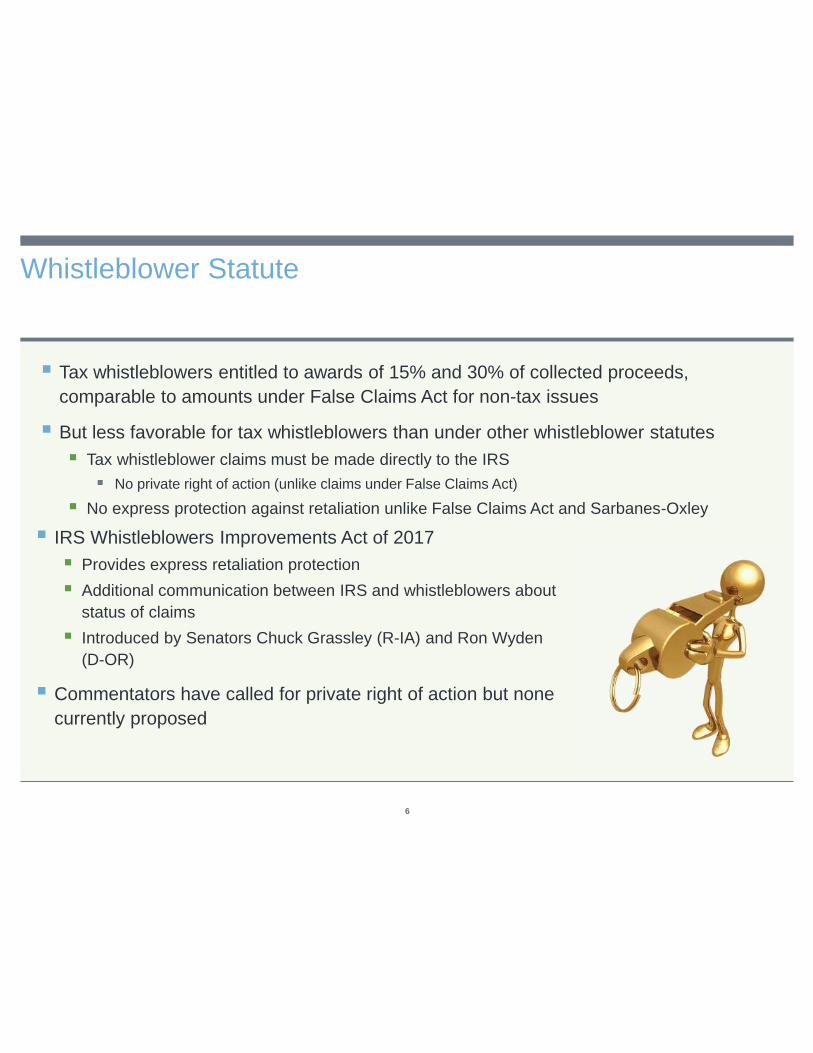

Whistleblower Statute

Tax whistleblowers entitled to awards of 15% and 30% of collected proceeds, comparable to amounts under False Claims Act for non-tax issues

But less favorable for tax whistleblowers than under other whistleblower statutesTax whistleblower claims must be made directly to the IRS

No private right of action (unlike claims under False Claims Act)

No express protection against retaliation unlike False Claims Act and Sarbanes-Oxley

IRS Whistleblowers Improvements Act of 2017Provides express retaliation protectionAdditional communication between IRS and whistleblowers about status of claimsIntroduced by Senators Chuck Grassley (R-IA) and Ron Wyden (D-OR)

Commentators have called for private right of action but none currently proposed

6

How Aggressive Was Caterpillar’s Planning?

From 1960 to 1999, Caterpillar purchased Caterpillar-designed replacement parts from third party manufacturers and sold them to COSACOSA:

oversaw distribution of replacement parts outside United Statesacted as lead marketing company for Europe, Africa and Middle Eastdeveloped and maintained Caterpillar’s non-U.S. dealer network

Caterpillar recognized income from parts sales to COSACOSA’s income from parts sales was Subpart F income

Pre-1999 Supply Chain

Third Party Suppliers

Caterpillar (U.S.)

COSA (Switzerland)

Non-U.S. Dealers

7

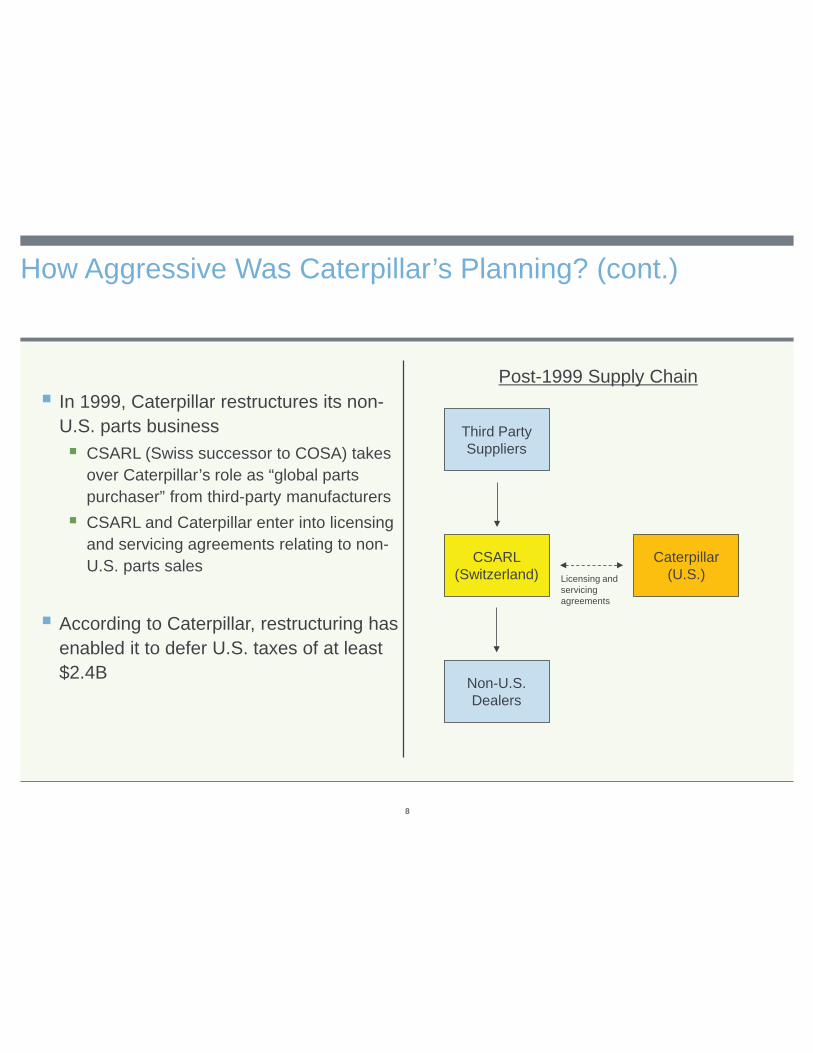

How Aggressive Was Caterpillar’s Planning? (cont.)

In 1999, Caterpillar restructures its non-U.S. parts business

CSARL (Swiss successor to COSA) takes over Caterpillar’s role as “global parts purchaser” from third-party manufacturersCSARL and Caterpillar enter into licensing and servicing agreements relating to non-U.S. parts sales

According to Caterpillar, restructuring has enabled it to defer U.S. taxes of at least $2.4B

Post-1999 Supply Chain

Third Party Suppliers

CSARL(Switzerland)

Non-U.S. Dealers

Caterpillar (U.S.)Licensing and

servicing agreements

8

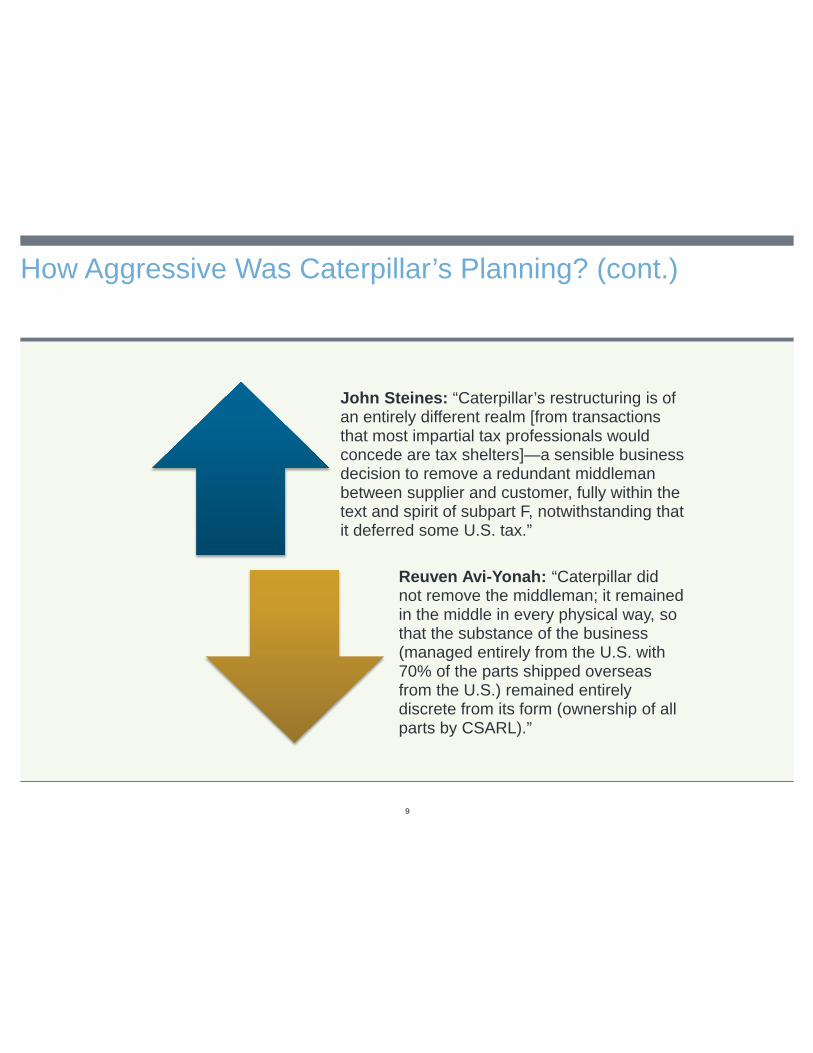

How Aggressive Was Caterpillar’s Planning? (cont.)

John Steines: “Caterpillar’s restructuring is of an entirely different realm [from transactions that most impartial tax professionals would concede are tax shelters]—a sensible business decision to remove a redundant middleman between supplier and customer, fully within the text and spirit of subpart F, notwithstanding that it deferred some U.S. tax.”

Reuven Avi-Yonah: “Caterpillar did not remove the middleman; it remained in the middle in every physical way, so that the substance of the business (managed entirely from the U.S. with 70% of the parts shipped overseas from the U.S.) remained entirely discrete from its form (ownership of all parts by CSARL).”

9

Mitigation Opportunities?

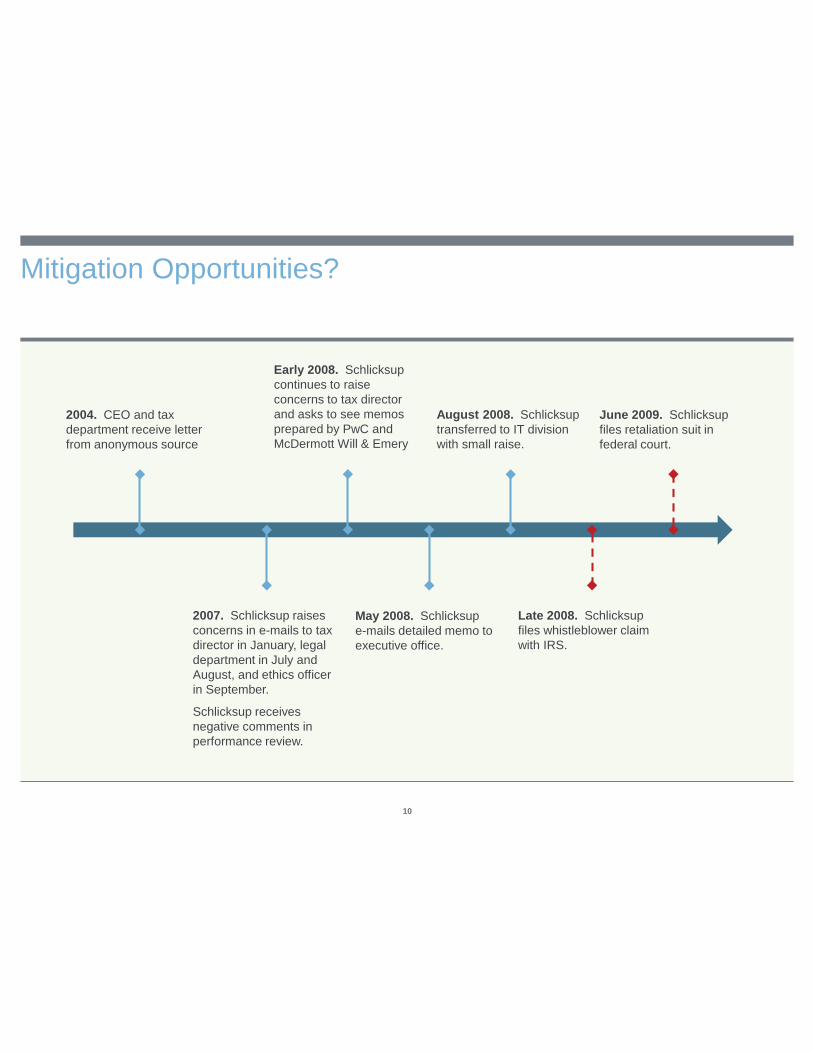

2004. CEO and tax department receive letter from anonymous source

2007. Schlicksup raises concerns in e-mails to tax director in January, legal department in July and August, and ethics officer in September.

Schlicksup receives negative comments in performance review.

Early 2008. Schlicksup continues to raise concerns to tax director and asks to see memos prepared by PwC and McDermott Will & Emery

May 2008. Schlicksupe-mails detailed memo to executive office.

August 2008. Schlicksup transferred to IT division with small raise.

Late 2008. Schlicksup files whistleblower claim with IRS.

June 2009. Schlicksup files retaliation suit in federal court.

10

Inside the Mind of a Whistleblower

Whistleblowers are generally not motivated by bounties

They want results and they want their concerns to be taken seriously—likelihood of external report increases dramatically if employee feels initial report was ignored

Perception that management behaves ethically and pays attention to internal reporting decreases likelihood of external reporting

Employees generally prefer reporting internally, first to direct supervisors (notwithstanding the loss of anonymity), then to more senior managers

Typically report externally only when either ignored internally or no internal option

Source: Ethics Resource Center, Inside the Mind of a Whistleblower: A Supplemental Report of the 2011 National Business Ethics Survey (2012).

11

Inside the Mind of the Agency

In the IRS Whistleblower Program, Fiscal Year 2016, Annual Report to Congress, the Director of the IRS Whistleblower Office, Mr. Martin, penned “[S]ince 2007 . . . the IRS

has approved more than $465 million in monetary awards to whistleblowers.”

12

Whistleblower Mitigation Strategies

General strategiesCommunicate culture of complianceFoster transparency and internal reporting of issuesPublicize whistleblower policy, including non-retaliation policy

Define retaliation to educate employees Have an anonymous reporting systemTrain management in handling whistleblower claimsShow that claims are taken seriouslyConduct performance reviews based on objective criteria

Tax-specific whistleblower mitigationTrain employees with access to sensitive information on uncertain tax positions and their justificationImplement internal controls for tax-related information

Coordinate with, and leverage, non-tax policies

13

Internal Investigations in Tax Cases

14

Execution of the Internal Investigation

Identify clientSet scopeFix timelinePick team:

In-house counsel or other personnel (legal, accounting, compliance, HR, etc.)Outside counselForensic investigators and experts

Obtain documentsDocument retention policy/document holdEmails and other electronic dataBoard minutes and notesLook for privileged documents

15

Execution of the Internal Investigation (Cont’d)

Interview witnessesConsider who should be present and who should take the leadConsider sequence of interviewConsider former as well as current employeesConsider whether Upjohn disclosures are appropriateConsider need for separate counsel and joint defense agreementsConsider indemnification and advancement of fees

Document results of investigationHow to report and summarize the investigation?How to disclosure results?How to monitor reaction to results and remedial action?How to address public relations issues?

Privilege issuesWork product doctrine

Fact v. opinion work productAttorney client privilege

Focus on who is the clientSection 7525

16

Yates Memo on Individual Accountability for Corporate Wrongdoing

Keep in mind that internal investigation may lead to civil or criminal investigation Premise of Yates Memo that effective way to combat fraud is to hold individuals who perpetrated wrongdoing accountablePuts pressure on individual witnesses in corporation investigations and highlights stakes involved in witness interviewsYates Memo applies to civil and criminal cases

17

Ethical Issues in Internal Investigations

Importance of identifying who client isDuties of loyalty and confidentiality to clientAttorney/client and other privileges

Model Rule of Professional Conduct 1.13: Organization as ClientLawyer retained by organization represents organizationIn dealing with organization’s directors, officers, employees or other constituents, lawyer shall explain identity of lawyer's clientLawyer may represent organization’s directors, officers, employees, or other constituents as well as the organization provided that parties consent to dual representation as required by model Rule 1.7

Model Rule 1.7: Conflicts of Interest: Current ClientsLawyer shall not represent client if representation involves concurrent conflict of interest unless:

Lawyer reasonably believes that lawyer can provide competent and diligent representation to each affected client;Representation is not prohibited by law;Representation does not involve assertion of a claim by one client against another client represented by lawyer in same litigation or proceeding; andAffected clients each gives her informed consent, confirmed in writing.

18

Should We Let Sleeping Dogs Lie? Mistakes in Prior Tax Returns

19

An Enduring Issue: Mistakes in Prior Returns:An Example

Example:

Parent distributes subsidiary in tax-free spin-off transaction

Later discovers that its spin-off year tax return failed to report deferred intercompany items triggered by spin

20

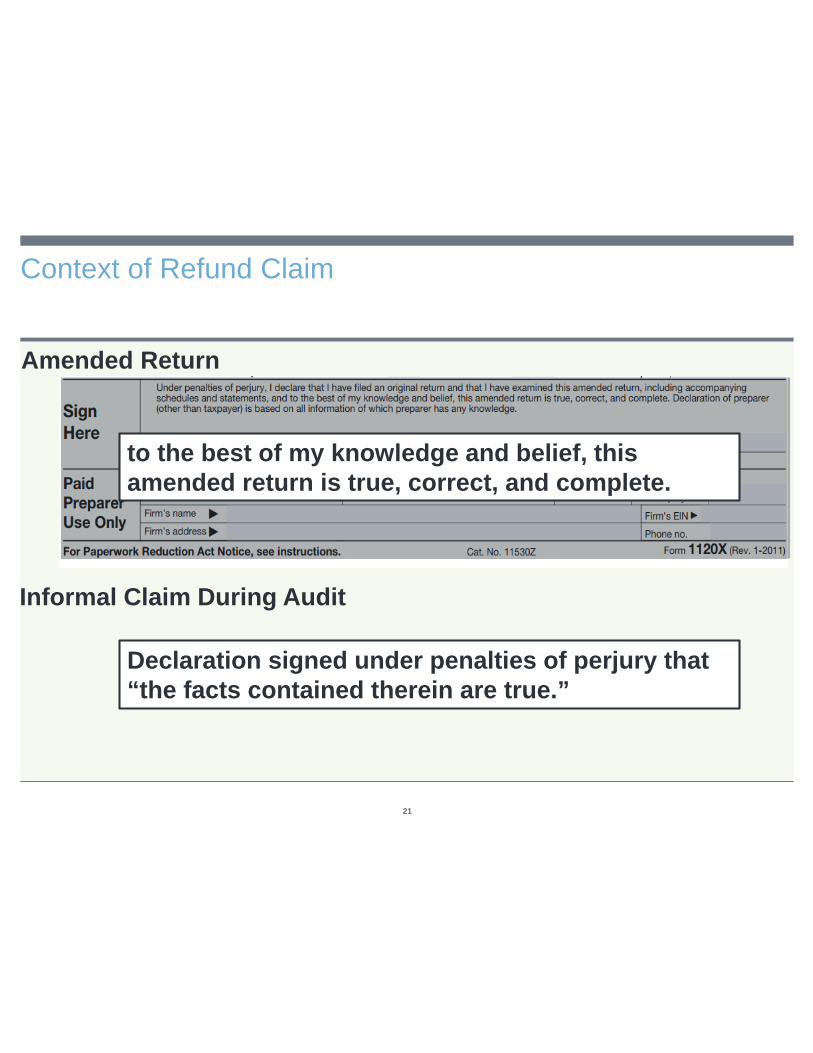

Context of Refund Claim

Amended Return

Declaration signed under penalties of perjury that “the facts contained therein are true.”

to the best of my knowledge and belief, this amended return is true, correct, and complete.

Informal Claim During Audit

21

Gating Considerations, In Sum

Is it an error? Is there a defense?Is there an offset?Are there reserve and UTP effects?Is correction barred by statute of limitations?

Duty of consistency

Does special rule apply, e.g., Form W-2?Does it establish accounting method or otherwise affect current return?Does it implicate contractual indemnities or insurance claims?

Mitigation, notice

Are you otherwise amending return containing error?

22

“Should” vs. “Shall” Correct Errors

23

Treasury regulations provide that amended return “should” be filed to correct failure to report gross income, deduction or loss in proper year

Treas. Reg. Section 1.451-1(a)

Treas. Reg. Section 1.461-1(a)(3)

Under limited circumstances, taxpayers may be required to file amended returns

No “Legal Requirement” to Amend

No “legal requirement” to file amended return; no separate penalty for failure to amend

Broadhead v. Comm’r, T.C. Memo 1955-328Badaracco v. Comm’r, 464 U.S. 386 (1984)

Amending return or voluntary disclosure in audit reduces likelihood that IRS will assert penalties

Professional organizations and IRS require adviser to inform his/her client of error and its consequences

IRS Circular 230, Section 10.21AICPA SSTS No. 6ABA Formal Opinion 85-352

24

What Is Your Ethical Duty Regarding Advice to Amend?

Circular 230 § 10.21“A practitioner who . . . knows that the client has not complied with the revenue laws of the United States or has made an error in or omission from any return . . . must advise the client promptly of the fact of such noncompliance, error, or omission.” “The practitioner must advise the client of the consequences as provided under the Code and regulations of such noncompliance, error, or omission.”

25

Note that CPAs Have a Greater Ethical Duty.

AICPA Statements on Standards for Tax Services, No. 6

(4) A member should inform the taxpayer promptly upon becomingaware of an error in a previously filed return, an error in a returnthat is the subject of an administrative proceeding, or a taxpayer’s failureto file a required return. A member also should advise the taxpayerof the potential consequences of the error and recommend the corrective measures to be taken. . . .

(5) If a member is requested to prepare the current year’s return and the taxpayer has not taken appropriate action to correct an error in a prior year’s return, the member should consider whether to withdraw from preparing the return and whether to continue a professional or employment relationship with the taxpayer.

26

Other Practical and Ethical Considerations

27

Decision to correct error should be informed by practical andethical considerations, including:

Taxpayer’s policies/reputation

Moral/philosophical considerations

Whistleblower risk

What about Failure to File? Can You Advise a Client Not to File a Tax Return that Is Legally Required?

28

Failure to file is a misdemeanor (26 U.S.C. § 7203)Failure to file with affirmative acts of evasion is a felony (26 U.S.C. § 7201)Adviser could be accused of aiding, abetting, counseling or commanding a criminal violation under 18 U.S.C. § 2

Manner of Correction

Amended return

Superseding return On audit

29

Manner of Correction (Cont’d)

Voluntary Disclosure

30

IRS Voluntary Disclosure Practice

Internal Revenue Manual 9.5.11.9

• It is currently the practice of the IRS that a voluntary disclosure will be considered along with all other factors in the investigation in determining whether criminal prosecution will be recommended.

• This voluntary disclosure practice creates no substantive or procedural rights for taxpayers as it is simply a matter of internal IRS practice, provided solely for guidance to IRS personnel.

• Taxpayers cannot rely on the fact that other similarly situated taxpayers may not have been recommended for criminal prosecution.

Requirements:Truthful, timely, and complete;Legal Source Income;Pay or make good faith arrangements to pay.

31