isbank earnings presentation 2018 q3 · 6 7 8 jan mar may jul sep usd/try bist 100 2y bm yield 10...

TRANSCRIPT

ISBANK

EARNINGS

PRESENTATION

2018 Q3

2018 Q3 Recent Developments in the Economy

Emerging markets have remained under pressuremainly due to unfavorable global funding conditions.

-50

0

50

100

150

17Q1 17Q2 17Q3 17Q4 18Q1 18Q2 18Q3 Oct

Total Portfolio Flows into Emerging Markets(billion USD)

Equity

Debt

In the third quarter, volatility was significantlyhigher in domestic markets.

40

45

50

55

60

Jan Mar May Jul Sep

Manufacturing PMI

0

10

20

30

Jan Mar May Jul Sep

Annual CPI Inflation (%)

Slowdown in the domestic economic activity hasgained momentum while price stability became thefocal point.

3

4

5

6

7

8

Jan Mar May Jul Sep

USD/TRY

BIST 100

2Y BM Yield

10

15

20

25

30

80

90

100

110

120

130

Jan Mar May Jul Sep

(%)(000)

Bin

ler

BIST 100 - 2Y Benchmark

IIF data

2

3

Period’s Highlights

Sustained strong performance in core revenue items:

8.8% QoQ growth in SWAP Adjusted NII Strong contribution of fee income continued in Q3 – YoY fee income growth

reached 27.5%

3.92% SWAP adjusted NIM for the first nine months is above the full-year guidance

TL loan – deposit spread maintained above 6% Highest share of demand deposits among peers – at 27%

Lower NPL ratio* compared to peers and average of private-sector banks

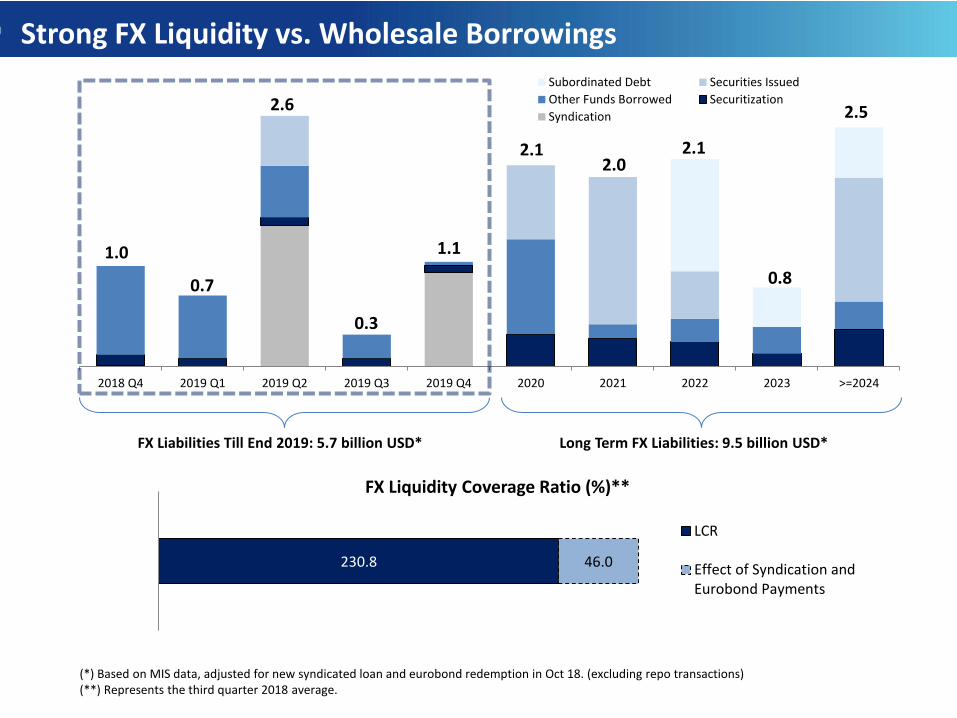

Strong FX liquidity – FX LCR at 230.8% for Q3 average, despite repayment of thesyndicated loan (1.1 bn USD) and redemption of Eurobond (750 mn USD).

Comfortable level of CAR above 14% without the impact of the current temporary measures

*Adjusted for NPL sales made by peers.

14.8%

27.2%

27.5%

35.1%

24.3%

-6.3%

8.4%

5.4%

18.6%

RoAA & RoATA

1.84%1.55%

1.85%

1.56%

2017 2018 Q3

RoAA RoATA

15.4%13.6%

16.3%

14.2%

2017 2018 Q3

RoAE RoATE

8.8%

4

Strong Growth in Major Revenue Items Maintained

2018 Q3 Revenue Growth & OPEX

RoAE & RoATE

(1) 2017 9M vs 2018 9M(2) 2018 Q3 and 9M income figures include income from participations according to IAS 27 and excludes 504 mn TL of IFRS 9 impact on other operating income(3) Tangible Equity (TE) and Tangible Assets (TA) are calculated by the deduction of M-t-M valuation differences regarding AFS (FVOCI) portfolio and real estates from shareholders’

equity and total assets. (4) Calculated using restated figures according to IAS 27(5) 9M figures are annualized.(6) Adjusted for non-recurring and other items

NII

Net F&C

QoQ YoY(1)

OPEX

(4) (4)(5) (5)

NII (Swap adj.)

Total Op. Income (2)

Profitability Ratios (3)

Cost / Income

42.3%37.6%

40.5%35.1%

2017 2018 Q3

Reported Adjusted

(4) (2) (5)

(6)

QoQ Growth. YtD Growth.

• Highest market share in total loans • Largest demand deposits

• Share of loans in total assets is at . • Share of demand deposits: 26.8% in total ( in TL, in FX deposits)

IEAs make up of total assets as of 2018 Q3.

28.9%

-8.8%

-10.4%

-2.8%

2.6%

13.9%

10.9%

Total TL FX (USD)-5.7%

-8.5%

-1.5%

-2.8%

2.7%

1.0%

3.1%

0.1%

11.5%

9.3%

8.3%

11.6%

Total TL FX (USD)

5

Selective Growth Funded with a Cost-Oriented Approach

Assets Liabilities

Deposits

Non- DepositFunding

Shareholders’Equity

(1) Interest earning assets include Central Bank reserves.(2) Non-deposit funding includes repo&money market, funds borrowed, securities issued and subordinated debt.(3) Among private sector banks(4) Excluding interbank deposits.

(1)

(2)

65.6%

89.7%

24.7%(4)

QoQ Growth.

(3) (3)

Total Assets

Total IEA

Securities

Loans

3.4%

21.7%

3.2%

-4.6%

18.1%

12.3%

-10.5%

20.3%

6.4%

-11.5%

22.7%

7.7%

-8.1%

19.3%

3.3%

-15.7%

36.4%

12.4%

-8.6%

8.4%

YtD Growth.

(4)

2018 Q4 2019 Q1 2019 Q2 2019 Q3 2019 Q4 2020 2021 2022 2023 >=2024

Subordinated Debt Securities Issued

Other Funds Borrowed Securitization

Syndication

1.0

0.7

2.6

0.3

2.12.0

2.1

0.8

2.5

1.1

FX Liabilities Till End 2019: 5.7 billion USD* Long Term FX Liabilities: 9.5 billion USD*

Strong FX Liquidity vs. Wholesale Borrowings

230.8 46.0

FX Liquidity Coverage Ratio (%)**

LCR

Effect of Syndication andEurobond Payments

(*) Based on MIS data, adjusted for new syndicated loan and eurobond redemption in Oct 18. (excluding repo transactions)(**) Represents the third quarter 2018 average.

4,2515,040

3,7394,329

2018 Q2 2018 Q3

NII NII (incl. swap cost)

Swap Adjusted NIM Evolution

7

Solid NIM Performance Maintained

Net Interest Income (TL mn.)

Yield/Cost (Quarterly)(1)

NIM(1)(2)

(1) Based on MIS data.(2) Interest earning assets include Central Bank reserves. NPL accruals are excluded. (3) Including demand deposits.

9,653

13,040

8,55810,626

2017 9M 2018 9M

18.6%

8.8%24.3%

35.1%

14.31% 14.67% 15.28% 15.71%17.80%

10.15% 10.87% 10.61%11.88%

14.77%

9.22% 9.20% 9.16% 9.22%

11.61%

Loan Yield

SecuritiesYield

DepositCost

7

TL

FX5.52% 5.73% 6.02% 6.56% 7.54%

4.28% 4.71% 4.76% 5.26%6.56%

1.36% 1.35% 1.41% 1.44% 1.68%

17 Q3 17 Q4 18 Q1 18 Q2 18 Q3

(3)

4.03%3.72%

+82 bps +32 bps +4 bp-55 bps

-51 bps-43 bp

Quarterly. Cumulative.

4.86% 4.97%

4.03%3.72%

18 Q2 18 Q3

NIM NIM - Swap Adjusted

4.39%4.85%

3.86% 3.92%

2017 18 9M

40.1%

99.9%

59.9%

Floating Fixed

60.2%

39.1%

86.1%

13.3%

Held fortradingAFS

HTM

(TL mn.) 2017 2018 Q2 2018 Q3 ∆ QoQ ∆ YtD

Total Securities 57,352 62,576 67,754 8.3% 18.1%

TL Securities 46,069 50,182 51,716 3.1% 12.3%

FX Securities 11,283 12,394 16,038 29.4% 42.2%

FX Securities (USD mn) 3,013 2,736 2,695 -1.5% -10.5%

8

Increasing Contribution from Securities

Securities

FX TL

• As of 2018 Q3 CPI Linkers make up 46.7% of TL securities.

• By the end of September 2018, if the current inflation rate (24.52%) was used in CPI Linker valuation:

• 9M Swap adj. NIM would stand at 4.10% vs 3.92%

• RoAA would be 1.71% vs 1.55%

• RoATE would stand at 15.6% vs 14.2%

Composition of Securities2018 Q3 2017

2018 Q3

FVTPL

FVOCI

FVMaAC

CPI Linkers

CPI Linkers 18 Q1 18 Q2 18 Q3

Quarterly Yield 11.28% 13.53% 18.05%

Quarterly Interest Income (TL mn) 551 698 1,019

Inflation 18 Q2 18 Q3

Expected-12 Months 10.47% 14.46%

Expected-24 Months 9.18% 11.42%

Actual 15.39% 24.52%

2,439

3,110

2017 9M 2018 9M

9

Robust Fee Income Performance Sustained

Net Fees & Commissions (TL mn.)

F&C Growth (2018 Q3)

• Share of net F&C income in total operatingincome* is 18.9% as of 2018 9M.

•OPEX coverage of Net F&C income reached50.2% as of 2018 9M.

Net Fees & Commissions Composition

5.4%

22.8% 20.3%

39.2% 42.2%

8.2% 7.7%

29.8% 29.8%

2017 9M 2018 9M

Lending Related Fees

Mutual Fund Man. &Other Inv. Acc. Fees

Payment Systems

Other

27.5%

* Total operating income includes income from participations according to IAS 27. IFRS 9 impact of 504 mn TL on other operating income in 2018 9M is excluded.

1,066 1,123

2018 Q2 2018 Q3

Growth ∆ QoQ ∆ YoY

Cash Loans -4.9% 9.9%

Non-Cash Loans 15.6% 39.8%

Mutual Fund Man. & Other Inv. Acc. Fees 10.8% 20.6%

Payment Systems 8.7% 37.2%

Other -7.0% 13.8%

Total F&C (Net) 5.4% 27.5%

• Specific Gross CoR (6) is 133 bps by 2018 9M.

• Share of Stage 2 Loans is 10.3%.

• Around 55% of Stage I+II provision expenses in Q3 stems from the model impact.

0.57%2.29%

3.73%

Net NPL Formation Rate

77

9 1,8

61

3,1

37

43

2

40

9

56

0

34

6

1,4

53

2,5

77

18 Q1 18 Q2 18 Q3

Additions Recoveries Net NPL Formation

Net Cost of Risk (2018 9M) (5)

3.6%

5.3%

2.4%

5.6%

3.7%

2.1%

4.6%

3.3%

4.2%

3.4%

Consumer

Credit Cards

Corp. & Comm.

SME

Total

Isbank Private-Sector Banks

(1) Adjusted for the NPL sales made by peer group banks in the period.(2) Net NPL Formation / Average Performing Loans

10

Lowest NPL Ratio Among Peers (1)

NPL Trends (Quarterly) (TL mn.)

NPL Ratios by Loan Categories (2018 Q3)

Coverage Ratios

Coverage Ratios

2018 Q1 2018 Q2 2018 Q3

PerformingLoans

Stage 1 0.7% 0.8% 0.9%

Stage 2 8.8% 9.8% 10.9%

NPLStage 3 71.7%(3) 65.8%(3) 57.5%(3)

Stage 3-Total 157.6%(4) 143.6%(4) 128.8%(4)

(3) Provisions for Stage 3 Expected Credit Losses / Non-performing Loans(4) (Provisions for Stage 1+2+3 Expected Credit Losses + Free Provisions) / Non-performing Loans(5) (Stage 1+2+3 Expected Credit Losses-Reversals) / Average Performing Loans(6) Stage 3 Expected Credit Losses / Average Performing Loans

Total

Prov. for Exp. Credit Loss. (TL mn) Q1 Q2 Q3 9M

Stage 1 7 269 664 940

Stage 2 589 357 1,065 2,011

Stage 3 532 824 1,228 2,584

Reversals (TL mn) (-) Q1 Q2 Q3 9M

Stage 1+2 504 11 3 518

Stage 3 211 303 155 669

Net CoR 223 bps

(2)

17.42%

0.36%

0.56%

0.16%

-0.30%

-2.47%

0.96%

2.27%

15.88%

2018 Q3

Net Income

Other

Real Estate Revaluation

MtM Losses in the period

Currency Depreciation Impact

BRSA Forbearance (MtM Losses)

BRSA Forbearance (Currency Fix.)

2018 Q2

(%) 2018 2019

Capital Conservation Buffer 1.875 2.5

Counter Cyclical Buffer 1.875 2.5

SIFI Buffer (4) 1.5 2

Min. Legal Requirement for CAR 8 8

CAR (Bank-only) 11.75 13.00

CAR (Consolidated) 13.25 15.00

RWAs vs. Regulatory Capital

11

Comfortable Capitalization

Capital Adequacy Ratio

(TL mn.)

(3) As of 2018 Q3, %0.04 on a bank-only basis(4) Taken into consideration only on a consolidated basis

16

.98

%

16.6

5%

16

.51

%

15

.88

%

17

.42

%

14

.06

%

13

.99

%

13

.78

%

13

.06

%

14

.26

%

17 Q3 2017 18 Q1 18 Q2 18 Q3

CAR Tier I Ratio

286,

600

303,

609

320,

567

340,

577

34

5,9

22

48,6

72

50

,56

0

52,9

27

54,0

89

60,2

47

17 Q3 2017 18 Q1 18 Q2 18 Q3

RWAs Regulatory Capital

154 bps

Change in CAR M

ax.

(3)

Max.

(1) Includes both impacts on RWA and capital (due to the general provision cap on Tier 2 capital).(2) Includes other impacts both on RWA and equity.(3) Forbearance impacts are calculated indivually. Including the combined impact, CAR stands at14.41% excluding forbearance measures.

(1)

(2)

(3)

12

Page 12 – Digitalisation

Page 13 – Asset Structure

Page 14 – Loans

Page 15 – Loan Composition

Page 16 – Securities

Page 17 – Liabilities Structure

Page 18 – Deposits

Page 19 – Income Statement Highlights

Page 20 – Fees & Commissions Income

Page 21– Market Shares

Appendix

Strong Focus on Digitalisation

13

(*) Source: TBA, as of 2018/Q2 (*) Number of sales in 2018 Q3

Evolution of Share of Transactions per Channel Digital Banking-Number of Customers (‘000)

Mobile Banking Market Shares * Share of Digital Channels in Retail Sales *

7 mndigital

customers

2071,620

5,219

2,792

5,596

2,788

5,925

2,753

6,317

2,738

Mobile Banking Internet Banking

2011 2017 2018 Q1 2018 Q2 2018 Q3

# Transactions Mobile Banking

Investment 30,2%

Credit Cards 17,9%

Money Transfer 14,5%

Payments 13,5%

37.6%

14.2%

30.3% 18.9%

2.2%

51.6%

74.8%

88.4%

2011 2014 2015 2016 2017 2018Q1

2018Q2

2018Q3

Internet Banking ATM Mobile Banking Total Non-Branch

61.0%67.4%

TL Time Deposits GPLs

91.5% 91.6% 89.7%

IEA / Total Assets

7.5% 7.5% 8.9%

66.1% 65.5% 65.6%

15.8% 15.7% 15.2%

10.6% 11.3% 10.3%

2017 2018 Q2 2018 Q3

Cash & Banks

Securities

Loans

Participations & Other Assets

14

Asset Structure

Asset Composition

Assets(TL mn.) 2017 2018 Q2 2018 Q3 ∆ QoQ ∆ YtD

Cash & Banks 38,424 44,879 45,848 2.2% 19.3%

Securities (Net) 57,352 62,576 67,754 8.3% 18.1%

Loans 239,409 261,043 291,276 11.6% 21.7%

Participations (Net) 13,802 14,838 16,837 13.5% 22.0%

Fixed Assets (Net) 5,163 5,159 5,851 13.4% 13.3%

Other Assets 8,095 9,843 16,769 70.4% 107.2%

Total Assets 362,244 398,340 444,334 11.5% 22.7%

TL Assets 221,167 232,049 238,266 2.7% 7.7%

FX Assets 141,077 166,291 206,069 23.9% 46.1%

FX Assets (USD mn.) 37,671 36,709 34,633 -5.7% -8.1%

Loans

15

Loan Portfolio

(1) Including overdraft accounts(2) (3) SME definition includes companies with number of employees < 250 and turnover or total assets <= TL 40 mn. for 2017 ; companies with number of employees < 250 andturnover or total assets <= TL 125 mn. for 2018 Q2 and 2018 Q3.

(TL mn.) 2017 2018 Q2 2018 Q3 ∆ QoQ ∆ YtD

Total Loans 239,409 261,043 291,276 11.6% 21.7%

TL Loans 147,442 151,989 152,112 0.1% 3.2%

Retail Loans 56,913 58,102 59,219 1.9% 4.1%

Housing Loans 20,852 21,372 21,304 -0.3% 2.2%

Auto Loans 676 700 688 -1.7% 1.8%

GPLs(1) 23,354 23,863 24,141 1.2% 3.4%

Credit Card Loans 12,031 12,167 13,085 7.5% 8.8%

Non-Retail Loans 90,529 93,887 92,893 -1.1% 2.6%

SME Loans(2) 51,611 59,450 56,553 -4.9% 9.6%

Commercial and Corporate Loans 38,918 34,438 36,339 5.5% -6.6%

FX Loans 91,967 109,054 139,164 27.6% 51.3%

SME Loans(2) 3,457 7,384 9,081 23.0% 162.7%

Commercial and Corporate Loans 88,510 101,670 130,083 27.9% 47.0%

FX Loans (USD mn.) 24,557 24,074 23,389 -2.8% -4.8%

SME Loans(2) 923 1,630 1,526 -6.4% 65.3%

Commercial and Corporate Loans 23,634 22,444 21,863 -2.6% -7.5%

96.2% 93.2% 93.5%

3.8% 6.8% 6.5%

2017 2018 Q2 2018 Q3

SME

Commercial& Corporate

26.4% 22.7% 23.9%

35.0% 39.1% 37.2%

38.6% 38.2% 38.9%

2017 2018 Q2 2018 Q3

Retail

SME

Commercial &Corporate

16

Loan Composition

(1) Including retail overdraft accounts(2) Shows retail credit card balances only(3) SME definition includes companies with number of employees < 250 and turnover or total assets <= TL 40 mn. for 2017 ; companies with number of employees < 250 andturnover or total assets <= TL 125 mn. for 2018 Q2 and 2018 Q3. (4) Including retail credit cards and overdraft accounts

Currency Mix

Loan Composition - FX LoansLoan Composition - TL Loans

Loan Composition - Total Loans

(3)

(2)

(3)

(3)(4)

(1)

61.6% 58.2% 52.2%

38.4% 41.8% 47.8%

2017 2018 Q2 2018 Q3

FX

TL

53.2% 52.1% 57.1%

23.0% 25.6% 22.5%5.0% 4.7% 4.5%

18.7% 17.6% 15.8%

2017 2018 Q2 2018 Q3

Consumer

Credit Cards

SME

Commercial& Corporate

Liabilities Composition

Liabilities Structure

(TL mn.) 2017 2018 Q2 2018 Q3 ∆ QoQ ∆ YtDDeposits 203,752 219,102 243,039 10.9% 19.3%

REPOs & Money Market 19,834 25,425 25,293 -0.5% 27.5%

Funds Borrowed 38,424 45,462 50,300 10.6% 30.9%

Securities Issued 25,911 30,076 37,841 25.8% 46.0%

Other 31,338 33,200 41,271 24.3% 31.7%

Equity 42,984 45,075 46,591 3.4% 8.4%

Total Liabilities & Equity 362,244 398,340 444,334 11.5% 22.7%

TL Liabilities 184,941 191,429 198,704 3.8% 7.4%

FX Liabilities 177,303 206,911 245,630 18.7% 38.5%

FX Liabilities (USD bn.) 47,344 45,676 41,282 -9.6% -12.8%

Liabilities

(*) Includes subordinated debt.

(*)

(*)

81.8% 82.8% 83.1%

IBL / Total Liabilities

17

25

.4%

25

.4%

25

.3%

26

.6%

24

.5%2

8.1

%

27

.4%

26

.0%

28

.0%

29

.0%

26

.4%

26

.3%

25

.3%

27

.0%

26

.8%

17 Q3 2017 18 Q1 18 Q2 18 Q3

TL FX Total

18

Deposit Base

Deposits

Demand Deposits / Total Deposits Demand Deposits Market Share

(*) Excluding interbank deposits

(*)(*)

15.3% 15.5% 14.7% 14.5% 14.4%

17 Q3 2017 18 Q1 18 Q2 18 Q3

(TL mn.) 2017 2018 Q2 2018 Q3 ∆ QoQ ∆ YtD

Total Deposits 203,752 219,102 243,039 10.9% 19.3%

TL Deposits 97,050 97,784 100,299 2.6% 3.3%

TL Saving Deposits 66,682 68,217 69,179 1.4% 3.7%

TL Commercial Deposits 25,045 25,258 25,572 1.2% 2.1%

Other TL Deposits 5,323 4,310 5,548 28.7% 4.2%

FX Deposits 106,702 121,317 142,740 17.7% 33.8%

FX Deposits (USD mn.) 28,492 26,781 23,990 -10.4% -15.8%

Demand Deposits 53,501 59,073 65,243 10.4% 21.9%

(TL mn.) 2018 Q2 2018 Q3 ∆ QoQ 2017 9M 2018 9M ∆ YoY

Net Interest Income 4,251 5,040 18.6% 9,653 13,040 35.1%

(-) SWAP Cost 712 1,191 67.3% 1,102 2,415 119.1%

Net Interest Income Incl. Swap Cost 3,539 3,849 8.8% 8,551 10,625 24.3%

Net Fees & Commissions 1,066 1,123 5.4% 2,439 3,110 27.5%

Net Trading Gains/Losses Excl. Swap Cost -57 -39 -31.9% -126 -261 106.7%

Other Operating Income 379 228 -39.9% 915 1,404 53.5%

Total Operating Income 4,927 5,162 4.8% 11,778 14,879 26.3%

HR Expenses 1,007 864 -14.2% 2,511 2,786 10.9%

Non-HR Expenses 1,176 1,181 0.4% 2,882 3,406 18.2%

Total Operating Expenses 2,183 2,045 -6.3% 5,393 6,192 14.8%

(-) Pre-provision for pension fund 125 150 20.0% 180 365 102.8%

Total Operating Expenses - Adj. 2,058 1,895 -7.9% 5,213 5,827 11.8%

Operating Profit 2,744 3,116 13.6% 6,385 8,687 36.0%

Operating Profit - Adj. 2,869 3,266 13.9% 6,565 9,052 37.9%

Stage 3 Expected Credit Losses 824 1,228 48.9% 1,610 2,584 60.5%

Stage 1+2 Expected Credit Losses 625 1,729 176.6% 325 2,950 807.3%

Other Provision Charges 154 -146 NM 106 11 -89.3%

Total Provision Charges 1,604 2,811 75.3% 2,041 5,545 171.7%

(-) Free Provisions 150 -150 NM 0 0 NM

Total Provision Charges - Adj. 1,454 2,961 103.7% 2,041 5,545 171.7%

Income from Participations 669 902 35.0% 1,161 2,081 79.2%

Tax Provisions 280 -31 -110.9% 948 650 -31.5%

Net Income 1,528 1,238 -19.0% 4,557 4,573 0.4%

NM: Not meaningful(1) Based on MIS data(2) 504 mn TL of this figure is resulting from IFRS 9 impact on other income. 19

Income Statement Highlights

(1)

(2)

20

Fees & Commissions Income

(TL thousand) 2018 Q2 2018 Q3 ∆ QoQ 2017 9M 2018 9M ∆ YoY

Non-Cash Loans 196,014 226,660 15.6% 420,505 587,726 39.8%

Cash Loans 114,100 108,462 -4.9% 307,431 337,976 9.9%

Mutual Fund Man. & Other Inv. Acc. Fees 76,674 84,940 10.8% 199,117 240,036 20.6%

Payment Systems 458,528 498,444 8.7% 956,594 1,312,026 37.2%

Other 220,385 204,856 -7.0% 555,389 632,204 13.8%

Total Fees & Commissions Income (Net) 1,065,700 1,123,363 5.4% 2,439,036 3,109,968 27.5%

Total Fees & Commissions Income (Gross) 1,298,465 1,413,050 8.8% 2,926,411 3,815,791 30.4%

*

* Including fund transfer, insurance, account keeping and other fees

2017 2018 Q3 2017 2018 Q3

Total Assets 11.7 11.4 1st 1st

Total Loans 11.8 11.6 1st 1st

TL Loans 11.0 10.8 1st 2nd

FX Loans 13.4 12.8 1st 1st

Consumer Loans(3) 11.7 11.5 2nd 2nd

Non-Retail Loans 11.8 11.6 1st 1st

Total Deposits 12.0 11.4 1st 2nd

TL Deposits 10.5 9.9 1st 2nd

FX Deposits 13.8 12.8 1st 1st

Demand Deposits 15.5 14.3 1st 1st

Market Shares (%) (1) Rank (2)

21

Market Shares

(1) Market share calculations are based on weekly BRSA data excluding participation banks. Total assets market share is based on monthly BRSA data.(2) Ranking among private banks. (3) Including retail overdraft accounts

Largest Private Bank…

22

Disclaimer

The information in this document has been obtained by Türkiye İş Bankası A.Ş. (“Isbank”) from sources believedto be reliable, however, Isbank cannot guarantee the accuracy, completeness, or correctness of suchinformation. This document has been issued for information purposes only. The financial reports andstatements announced by Isbank to the public and the relevant corporations are accepted to be the solematerial. Isbank does not accept any liability whatsoever for any direct, indirect or consequential loss arisingfrom any use of this document or its contents due to the misleading information in this document. Allestimations, opinion, all forward looking statements and projections expressed, implied, contained in thisdocument are the current beliefs or expectations of Isbank’s management as of the date of this document andare subject to significant risks, uncertainties and changes in circumstances. Actual results, performance orevents could differ materially from those expressed or implied in the estimations, opinions and forward-lookingstatements in this document. All estimations, opinions and forward-looking statements contained in thisdocument can be subject to change without notice. Isbank expressly disclaims any obligation or undertaking torelease publicly any updates or revisions to any estimations, opinions, forward-looking statements contained inthis document to reflect any change in Isbank’s expectations with regard thereto or any change in events,conditions or circumstances on which any such statement is based. This document can not be interpreted as anadvice to the investors or as an offer or solicitation for the purchase or sale of any financial instrument or theprovision of an offer to provide investment services and Isbank can not be held responsible for the results ofinvestment decisions made on account of this document. This document has been issued specially to the person,whom the document is concerned and may not be reproduced, distributed, published or shared with thirdparties for any purpose. All rights of Isbank are reserved.

23

Contact Information:

Türkiye İş Bankası A.Ş.Head OfficeInvestor Relations Division

Phone: + 90 212 316 16 02Fax: + 90 212 316 08 39E-mail: [email protected]