islamic capital market, an overview

TRANSCRIPT

ISLAMIC CAPITAL

MARKET A Complete Overview

ABSTRACT Islamic Capital Market (ICM) is the result of

growing need for Islamic finance. This paper

discussed various topics related to capital market

and their Islamic appraisal. The sukuk market

have been discussed in more detail. A global

scenario have been highlighted and Islamic

finance in Bangladesh have been discussed with

problems and prospects.

Mohammad Shiblu

www.fb.com/amar.kotha.barta

Executive Summary

Islamic Finance is a growing industry. Islamic Capital Market (ICM) is the result of

worldwide Islamic finance growth. ICM can be called as a capital market according to

Islamic Shari’ah. However, as a new industry, it has some limitations, problems that

should be overcome.

In the first part of this report, conventional capital market is viewed from risk and return

perspective. Functions of a conventional capital market are discussed. Also, the main two

items of capital market i.e. stock and bonds are discussed in very brief before going into

discussion about ICM. In the second part of the report, Justification for establishing a ICM

is given and why we need a Islamic Capital Market have been discussed. Also, the risk and

return from Islamic perspective have been discussed in brief.

In the third part, Islamic equity market is discussed. The contractual form between the

firm and shareholders are discussed with the concept of limited liability from Islamic

perspective. Different screening criteria are discussed that are being implemented

throughout the word. Also, the permissibility or prohibition about short selling is

discussed in some detail with the topic of speculation.

In the fourth part, the most important part of Islamic capital market, the sukuk market

are discussed. The types of sukuk with some innovative model like GDP-Linked sukuk,

Commodity-Linked sukuk have been discussed. These model have solved some problem

with present sukuk structures. Also, the tradability of different sukuk and a practical

example of ADIB sukuk issuances are given. Some shari’ah concerns about present sukuk

practices are also discussed. A snapshot of current global sukuk market have been given,

it have been seen that sukuk market is growing very fast though some setback occurred

in 2008 in the time of global economic crisis. Sukuk market have crossed USD 100 billion

milestone.

In part 5, derivatives market instruments like options, futures, forwards, swap etc have

been discussed from Islamic perspectives. The Islamic alternatives like bai al arbun, bai

al salam have some features of derivatives. In 6th part, the paper is concluded by

discussing some problems and prospects of Islamic finance industry in Bangladesh.

Contents

Contents Pages

1.Overview of the capital market 2

1.1 Functions of capital market 2

1.2 Risk & Return 3

1.3 Bond 3

1.4 Stocks 4

2. Overview of Islamic capital market 6

2.1 Justification of ICM 7

2.2 Risk & Return 7

3. Overview of Islamic equity market 9

3.1 Contract form 9

3.2 Stock Screening 10

3.2.1 Issues in screening process 12

3.3 Short selling 12

3.3.1 Eligibility of stocks to be a subject matter of a loan contract 13

3.3.2 Bai al-mad’um (selling what the seller doesn’t own) 13

3.3.3 Issues of benefitting from a loan contract 14

3.4 Speculation 15

4. Overview of the Sukuk Market 17

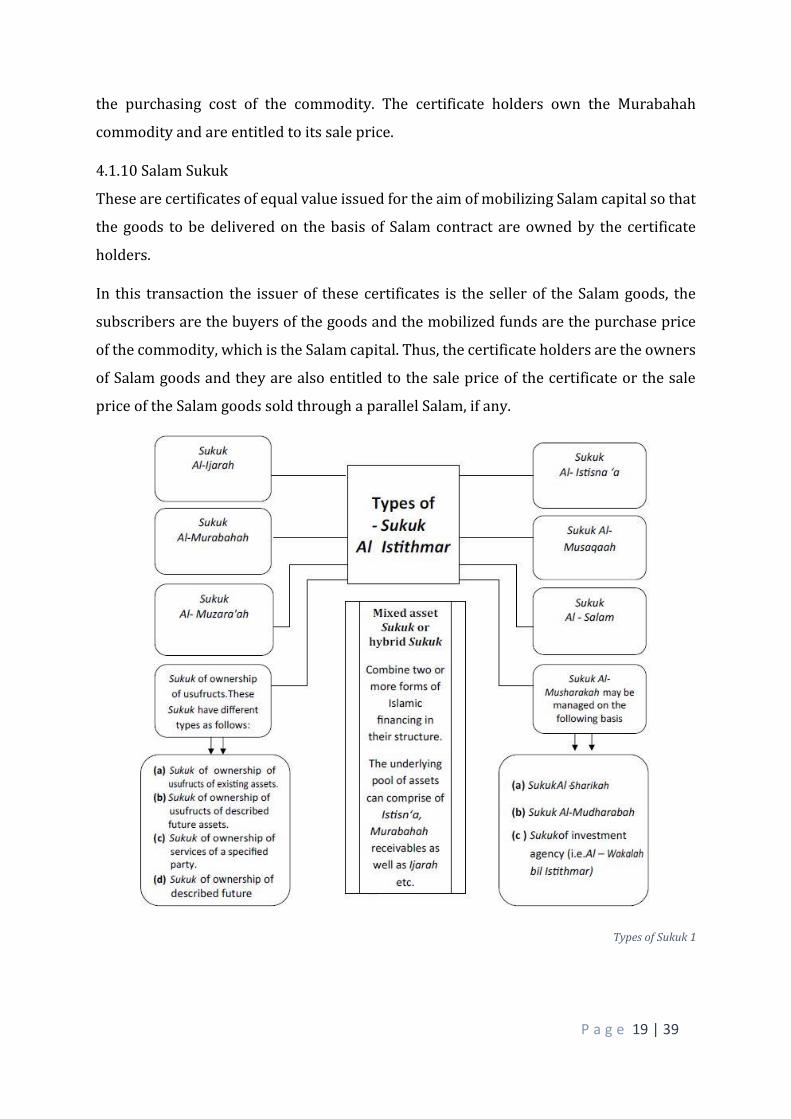

4.1 Types of Sukuk 17

4.1.1 Mudarabah Sukuk 17

4.1.2 Musharaka Sukuk 17

4.1.3 Wakala Sukuk 17

4.1.4 Muzara’a (Sharecropping) Sukuk 18

4.1.5 Musaqa (irrigation) Sukuk 18

4.1.6 Mugharasha (Agricultural) Sukuk 18

4.1.7 Ijarah Sukuk 18

4.1.8 Istisna Sukuk 18

4.1.9 Murabaha Sukuk 18

4.1.10 Salam Sukuk 19

4.2 Innovative Sukuk 20

4.2.1 GDP-Linked Sukuk (GLS) Model 20

4.2.2 Commodity Linked Sukuk (CLS) Model 20

4.4 Secondary Market of Sukuk (Tradability) 22

4.5 Global Sukuk Market – A Snapshot 22

4.5.1 Distribution of Sukuk Issuance by Issuer States 23

4.5.2 Distribution of Sukuk Issuances by Structure 25

4.5.3 Distribution of Sukuk Issuances by Region 27

4.6 A Case Study – Abu Dhabi Islamic Bank (ADIB) Example 27

4.6.1 Abstract 27

4.6.2 ADIB Sukuk Explanation 28

4.7 Sharia’h Concerns in Sukuk 29

5. Overview of the Derivative Instruments 31

5.1 Forward & Futures 31

5.1.1 Islamic appraisal 31

5.2 Options 32

5.2.1 Islamic Appraisal 32

5.3 SWAP 32

5.3.1 Islamic Appraisal 32

5.4 Islamic Alternatives 33

5.4.1 Bai al Salam 33

5.4.2 Bai al Arbun 33

6. Problems & Prospects of Islamic Finance in Bangladesh 35

6.1 Problems of Islamic Finance 35

6.1.1 Absence of Islamic Money Market 35

6.1.2 Absence of Suitable Long-term Assets 35

6.1.3 Shortage of Supportive and Link Institutions 35

6.1.4 Organizing Relationship with Foreign Banks 36

6.1.5 Long-term Financing 36

6.2 The Future of Islamic Finance in Bangladesh 36

6.2.1. New banking philosophy for the Islamic Banks 36

6.2.2. Banking Policies and practices should be modernized 36

6.2.3. Policy and Strategy should be formulated 36

6.2.4. Stepping for Distributional Efficiency 37

6.2.5. Allocating Efficiency should be promoted 37

6.2.6. Government and Central bank's Responsibilities 37

6.2.7. Inter-Islamic Bank Co-operation and Perspective Plan 37

Bibliography 38

P a g e 1 | 39

01. Capital Market (CM)

1. Overview of capital market

1.1 Functions of the capital market

1.2 Risk & Return

1.3 Bond

1.4 Stocks

P a g e 2 | 39

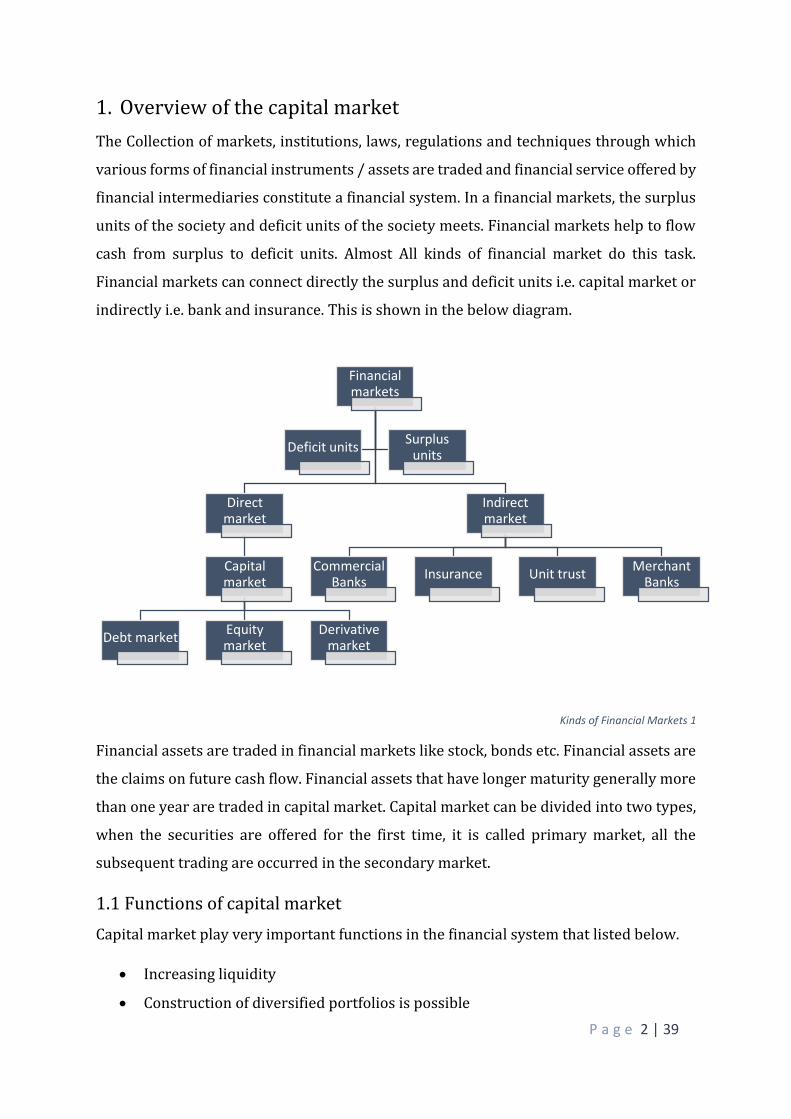

1. Overview of the capital market

The Collection of markets, institutions, laws, regulations and techniques through which

various forms of financial instruments / assets are traded and financial service offered by

financial intermediaries constitute a financial system. In a financial markets, the surplus

units of the society and deficit units of the society meets. Financial markets help to flow

cash from surplus to deficit units. Almost All kinds of financial market do this task.

Financial markets can connect directly the surplus and deficit units i.e. capital market or

indirectly i.e. bank and insurance. This is shown in the below diagram.

Kinds of Financial Markets 1

Financial assets are traded in financial markets like stock, bonds etc. Financial assets are

the claims on future cash flow. Financial assets that have longer maturity generally more

than one year are traded in capital market. Capital market can be divided into two types,

when the securities are offered for the first time, it is called primary market, all the

subsequent trading are occurred in the secondary market.

1.1 Functions of capital market

Capital market play very important functions in the financial system that listed below.

Increasing liquidity

Construction of diversified portfolios is possible

Financial markets

Direct market

Capital market

Debt marketEquity market

Derivative market

Indirect market

Commercial Banks

Insurance Unit trustMerchant

Banks

Deficit unitsSurplus

units

P a g e 3 | 39

Mobilizing the capital

Provides risk management tools

Reduce transaction costs (through efficient pricing)

Measuring economic performance

Management evaluation

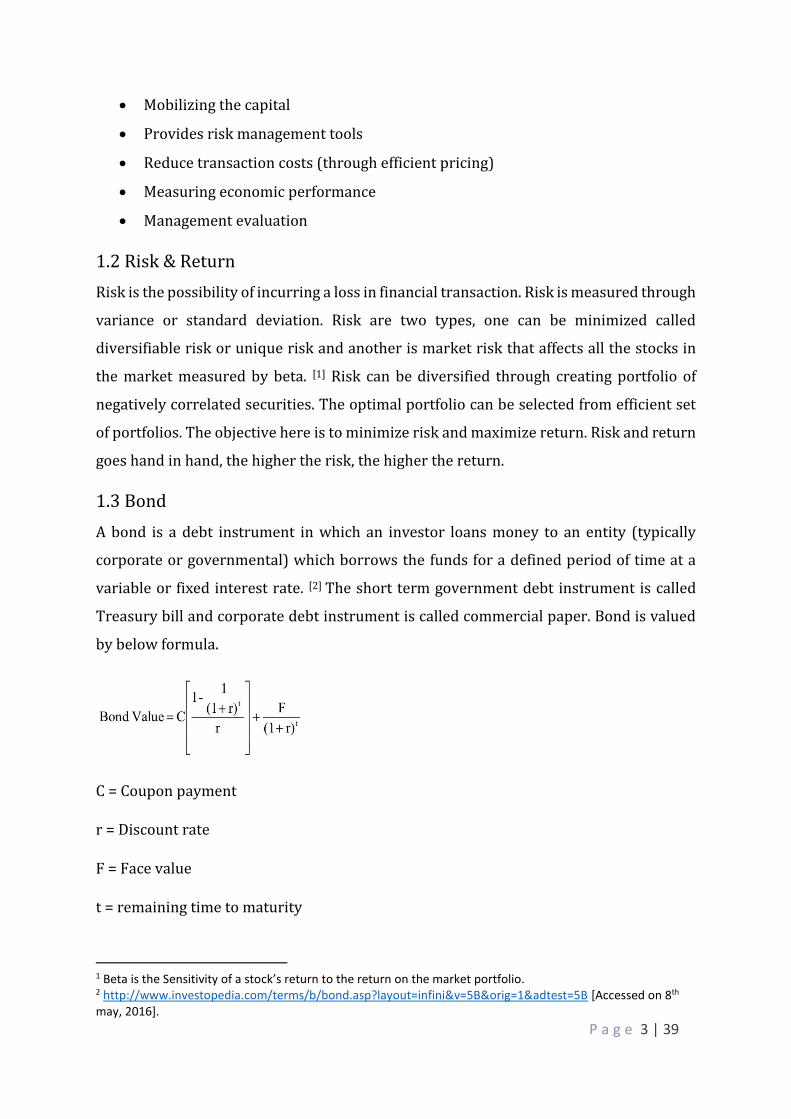

1.2 Risk & Return

Risk is the possibility of incurring a loss in financial transaction. Risk is measured through

variance or standard deviation. Risk are two types, one can be minimized called

diversifiable risk or unique risk and another is market risk that affects all the stocks in

the market measured by beta. [1] Risk can be diversified through creating portfolio of

negatively correlated securities. The optimal portfolio can be selected from efficient set

of portfolios. The objective here is to minimize risk and maximize return. Risk and return

goes hand in hand, the higher the risk, the higher the return.

1.3 Bond

A bond is a debt instrument in which an investor loans money to an entity (typically

corporate or governmental) which borrows the funds for a defined period of time at a

variable or fixed interest rate. [2] The short term government debt instrument is called

Treasury bill and corporate debt instrument is called commercial paper. Bond is valued

by below formula.

C = Coupon payment

r = Discount rate

F = Face value

t = remaining time to maturity

1 Beta is the Sensitivity of a stock’s return to the return on the market portfolio. 2 http://www.investopedia.com/terms/b/bond.asp?layout=infini&v=5B&orig=1&adtest=5B [Accessed on 8th may, 2016].

P a g e 4 | 39

1.4 Stocks

A stock is a type of security that signifies ownership in a corporation and represents a

claim on part of the corporation's assets and earnings. [3] Stock can be common stock or

preferred stock. Preferred stock have similarity with both equity instrument and debt

instrument. Stock can be valued by discounting future dividends, by using dividend

discount model. If the dividends growth rate is constant, dividends can be measured

through below formula.

𝑃 = 𝐷1

𝑟 − 𝑔

D1 = Forward dividend

r = Discount rate

g = Growth rate

3 http://www.investopedia.com/terms/s/stock.asp?layout=infini&v=5B&orig=1&adtest=5B [Accessed on 8th may,2016]

P a g e 5 | 39

02. Islamic Capital Market (ICM)

2. Overview of the Islamic Capital Market

2.1 Justification of ICM

2.2 Risk & Return

P a g e 6 | 39

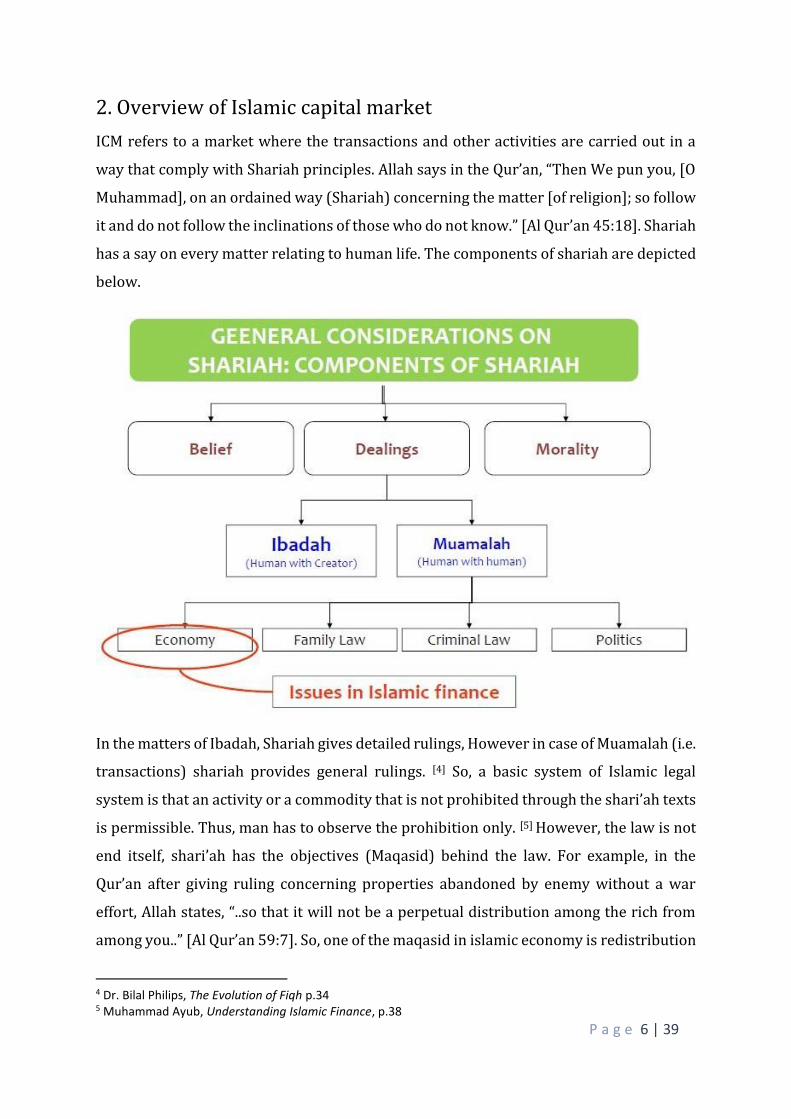

2. Overview of Islamic capital market

ICM refers to a market where the transactions and other activities are carried out in a

way that comply with Shariah principles. Allah says in the Qur’an, “Then We pun you, [O

Muhammad], on an ordained way (Shariah) concerning the matter [of religion]; so follow

it and do not follow the inclinations of those who do not know.” [Al Qur’an 45:18]. Shariah

has a say on every matter relating to human life. The components of shariah are depicted

below.

In the matters of Ibadah, Shariah gives detailed rulings, However in case of Muamalah (i.e.

transactions) shariah provides general rulings. [4] So, a basic system of Islamic legal

system is that an activity or a commodity that is not prohibited through the shari’ah texts

is permissible. Thus, man has to observe the prohibition only. [5] However, the law is not

end itself, shari’ah has the objectives (Maqasid) behind the law. For example, in the

Qur’an after giving ruling concerning properties abandoned by enemy without a war

effort, Allah states, “..so that it will not be a perpetual distribution among the rich from

among you..” [Al Qur’an 59:7]. So, one of the maqasid in islamic economy is redistribution

4 Dr. Bilal Philips, The Evolution of Fiqh p.34 5 Muhammad Ayub, Understanding Islamic Finance, p.38

P a g e 7 | 39

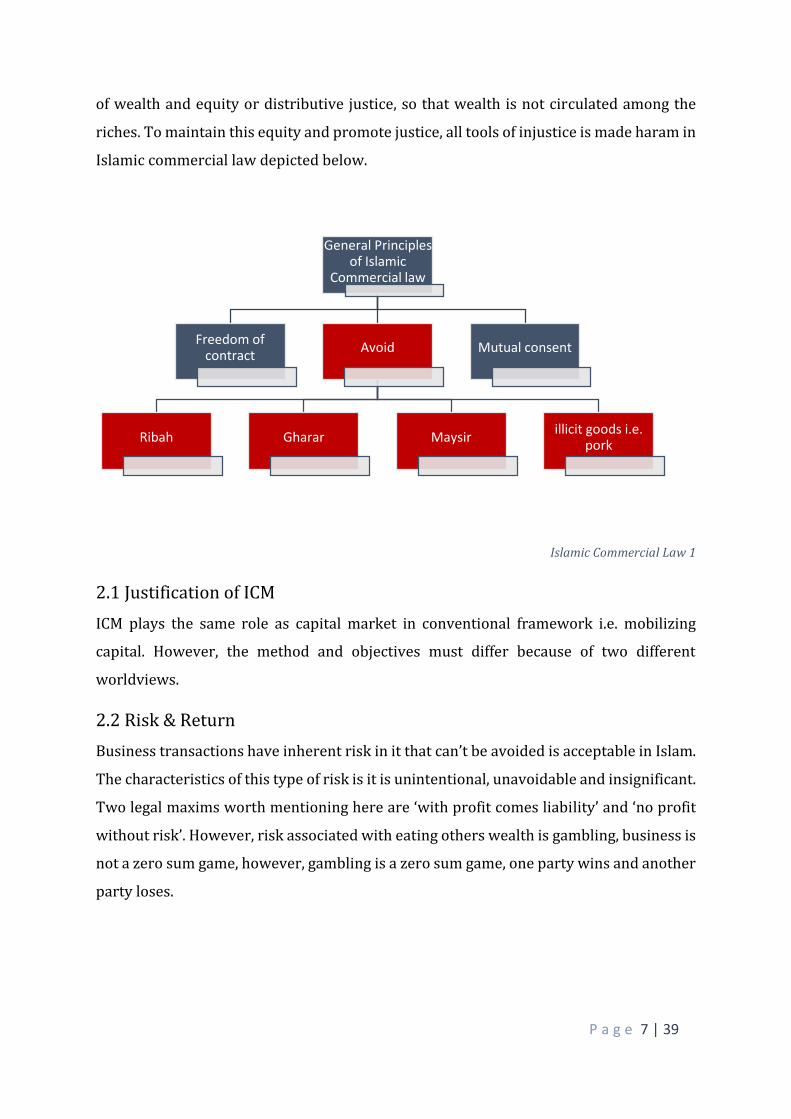

of wealth and equity or distributive justice, so that wealth is not circulated among the

riches. To maintain this equity and promote justice, all tools of injustice is made haram in

Islamic commercial law depicted below.

Islamic Commercial Law 1

2.1 Justification of ICM

ICM plays the same role as capital market in conventional framework i.e. mobilizing

capital. However, the method and objectives must differ because of two different

worldviews.

2.2 Risk & Return

Business transactions have inherent risk in it that can’t be avoided is acceptable in Islam.

The characteristics of this type of risk is it is unintentional, unavoidable and insignificant.

Two legal maxims worth mentioning here are ‘with profit comes liability’ and ‘no profit

without risk’. However, risk associated with eating others wealth is gambling, business is

not a zero sum game, however, gambling is a zero sum game, one party wins and another

party loses.

General Principles of Islamic

Commercial law

Freedom of contract

Avoid

Ribah Gharar Maysirillicit goods i.e.

pork

Mutual consent

P a g e 8 | 39

03. Islamic Equity Market

3. Overview of the Islamic equity market

3.1 Contract form

3.2 Stock screening

3.2.1 Issues in stock screening

3.3 Short Selling

3.3.1 Eligibility of stocks to be a subject matter of a loan

3.3.2 Selling what the seller doesn’t own

3.3.3 Issue of Benefitting from a loan contract

3.4 Speculation

P a g e 9 | 39

3. Overview of Islamic equity market

Islamic capital market is the natural outcome of the growing Islamic finance industry. The

very initial entrants in the field of Islamic finance were Islamic savings and investment

companies at small level. Mit Ghimar Bank (1961) in Egypt is earliest example of this.

A very early review and identification of shari’ah compliant stocks was undertaken in

1983 by Bank Malaysia Berhad., which lead to introduction of a centralized process of

such identification of Securities Commission of Malaysia in june 1997. The first equity

Index was first launched in Malaysia by RHB Unit Trust Management Berhad. in May

1996. It was followed by Dow Jones Islamic Market Index (DJIMI) in February 1999, Kuala

Lumpur Shariah Index (KLSI) in April 1999 and Financial Times Stock Exchange Global

Islamic Index (FTSE-GII). The next was DJMI Turkey Index in 2004 and many countries

have introduced shariah index. [6]

Investment in stocks of shari’ah compatible business always deemed fit in Muslim

societies. If a firm conducting halal business, sharing in it through stock is perfectly

legitimate. [7] The main shariah issues pertaining to trade in stocks are given below.

The business of the company whose stock are to be traded

The form of stock/share contract

Shari’ah compatibility of trading practices pertaining to stocks.

3.1 Contract form

The modern corporation is a legal entity, management is separate from ownership. The

shareholders are the real owners of the corporation who provides capital and elect board

of directors. Board of directors select management bodies who operate the business. The

relationship between shareholders can be considered as a partnership or musharaka

contract and the relationship between board of directors and management or

shareholders can be seen as wakala [8] or ijarah [9] contract.

However, the issue is about limited liability. Islamic norms is that the debtor will be liable

to the creditor for his debt and have to pay the full amount. OIC Fiqh Academy has

6 Salman Syed Ali, Islamic Capital Market Products: Developments and Challenges, p. 18 7 Salman Syed Ali, Islamic Capital Market Products: Developments and Challenges, p. 15 8 Agency contract 9 Lease contract

P a g e 10 | 39

approved investing in stock whose business is licit and accepted the two terms limited

liability and legal entity provided that the parties dealing with these companies limited

capacity to liability and presumably consent to it.

3.2 Stock Screening

Islamic prohibition to maintain justice and equity and prohibition against illicit activities

demand stock screening to find out the shar’ah compliant stocks. The business of the

company mustn‘t be involved in Ribah, Gharar, Maysir and illicit goods and services. The

majority of the assets should be in illiquid form for trading in secondary market because

of restrictions of trading in debt and money. The illicit income should be below the certain

level. There is no international single standards on screening process. The conditions

listed by Usmani (1999) may be guiding principles listed below.

1. The main business of the company doesn’t break the shari’ah rules.

2. If the main business of the company is licit, like automobiles, textile, etc. but they

deposit their surplus amounts in an interest-bearing account or borrow money on

interest, the shareholder must express his disapproval against such dealings,

preferably by raising his voice against such activities in the annual general meeting of

the company.

3. If some income from interest-bearing accounts is included in the income of the

company, the proportion of such income in the dividend paid to the shareholder must

be given in charity.

4. The shares of a company are freely negotiable only if the company owns some illiquid

assets.

These are the general criteria, each stock exchange have adopted different criteria for

sharia screening. Some stock exchange adopts both income statement and balance sheet

screening but stock exchange in Malaysia only adopts income statement screening. The

screening process can be divided into two steps.

1. The core screening: Here a stock is declared permissible when the issuing

company produces output that are free from elements prohibited by Shari’ah.

2. The financial screening: Computation of a set of financial ratios & compare them

against specified benchmarks.

P a g e 11 | 39

The comparisons of various stock selection criteria are given below. The first table

compares core screening and second table compares financial screening.10

Core Screening 1

Financial Screening 1

P a g e 12 | 39

Once shari’ah compliant securities may be declared non sharia compliant because of

leverage ratio or other ratio. The exchanges declare the lists of shari’ah compliant stocks

from time to time. If the stock is declared non shari’ah compliant which was shari’ah

compliant before, the fund managers and stock holders should immediately liquidate the

stock if the price is greater than investment price and wait until price increasing if the

price is below investment price. However, if the shareholder keep the share and sell it

later date the price increase between announcement date and selling date must channel

to charity. The fund managers must separate the non-permissible income portion from

the portfolio income and channel them to charity before distributing dividend, this is

called income purification.

3.2.1 Issues in screening process

Two issues are concerned in screening process. First is that some non-permissible

activity is tolerated i.e. interest income up to 5% to promote screening process, however,

this should be seen as a transitory process. Second is that there is no international

standard or criteria. Shari’ah compliant today doesn’t necessarily imply presence of good

business ethics. This criteria should be added to screening process.

3.3 Short selling [11]

One of the most popular and commonly used financial instruments in conventional

capital market is short selling. Many finance literature assert that short-selling provides

liquidity, drives down overpriced stocks and generally increases efficiency of the

markets, facilitates hedging. The demerits are that the possible loss from short selling is

theoretically infinite and the unrestrained short selling pressure could lead to collapse in

the share prices. Besides the debate of the merit and demerits of short selling, shari’ah

compliancy criteria is also included in Islamic finance. The issues concerning short selling

can be divided in three.

1. Eligibility of stocks to be a subject matter of a loan contract

2. Bai al-mad’um (selling what the seller doesn’t own)

10 Salman Syed Ali, Islamic Capital Market Products: Developments and Challenges, p. 18-22 11 Short selling is the sale of a security that is not owned by the seller, or that the seller has borrowed. Short selling is motivated by the belief that a security's price will decline, enabling it to be bought back at a lower price to make a profit.

P a g e 13 | 39

3. Issue of Benefitting from a loan contract [12]

3.3.1 Eligibility of stocks to be a subject matter of a loan contract

With the exception of Hanafi jurists, most jurists (the Malikis, Shafi`is and Hanbalis) ruled

that loans are permissible for all goods eligible for forward sale (salam). This includes

fungible goods (mithli) and non-fungible goods (qimi). This view is supported by the

below hadith.

"It was narrated by Rafi` that the Prophet (pbuh) borrowed a young camel, and then received

a charity of camels and ordered Rafi` to repay the man another young camel, Rafi` said that

the closest he could find was a six year old camel (which is more valuable). Then the Prophet

(pbuh) ordered him to give it to the man, and added “the best among you is the one who is

the best in repaying his debts” [13]

The Hanafies, on the other hand, argue that homogeneous (mithli) properties are the only

proper object for the loan contract. They argue that a loan contract cannot validly be

concluded with regard to non-homogeneous (qimi) properties at it is almost impossible

to find an equivalent good to repay the loan. [14]

Based on the above, according to all jurists including the Hanfis, since stocks satisfy the

homogeneous (mithli) properties, they are qualified to become the subject matter of a

loan contract.

3.3.2 Bai al-mad’um (selling what the seller doesn’t own)

According to Imam ibn Taymiyya [15] and his student ibn Qayyum16, what was narrated in

the Hadith is the prohibition of sales with excessive risk and uncertainty (gharar), where

the object may be undeliverable, whether it exists or not (e.g. a runaway horse or camel).

They assert that the emphasis of the Hadith is on the seller’s inability to deliver, which

entails excessive risk and uncertainty.

12 Dusuki and Abozaid , Fiqh Issues in Short Selling as Implemented in the Islamic Capital Market in Malaysia, p. 65 13 Sahih Muslim, Abu Dawud, Tirmidhi, Nasa’I, Ibn Majah. 14 Dusuki and Abozaid , Fiqh Issues in Short Selling as Implemented in the Islamic Capital Market in Malaysia, p. 15 Ibn Taymiyya was a prominent scholar, died in 1328 CE. 16 Ibn Qayyum was the student of Ibn Taymiyya, died in 1350 CE.

P a g e 14 | 39

In general, selling what the seller does not own at the time of sale in a non-salam contract

is valid only according to Ibn Taymiyah and Ibn Qayyim, while it is invalid according to

the majority of jurists. The majority scholars of Islamic jurisprudence assert the rationale

(`illah) of prohibiting sale prior taking possession (qabd) was mainly due to the presence

of gharar (excessive risk and uncertainty), which may lead to dispute amongst the

transacting parties. This was because of the concern that the goods might not be delivered

due to damage or other factors. Thus Islam prohibits any transactions involving bay`

ma`dum since the delivery of the subject matter cannot be effected and this brings about

the prohibited element of gharar.17

According to Shariah Advisory Council of Malaysia’s view, the issue of gharar can be

overcome and hence eliminated in Regulated Short Selling (RSS) with the inclusion of

Securities Borrowing and Lending (SBL) principles. In other words, the introduction of

SBL can increase the probability that the shares sold will be delivered. When the

probability of delivery is high, then the element of gharar will no longer be significant.

Consequently, when an obstacle that hinders the recognition of a certain activity as

Shari`ah compliant is overcome, then that transaction or activity can be classified as

Shari`ah compliant. [18]

3.3.3 Issues of benefitting from a loan contract

In short selling, the lender gets certain percentage of return as a profit from lending. For

example: in Malaysia, this is 2%. However, this is clearly ribah, any stipulated excess from

the loan constitute ribah.

Finally, there is a debate about whether short selling is permitted or not. Opponents

argues based on the literal meaning of the hadith, ‘don’t sell what you do not possess’.

17 Dusuki and Abozaid , Fiqh Issues in Short Selling as Implemented in the Islamic Capital Market in Malaysia, p. 72 18 Their arguments are based on a well-known fiqh maxim: “When an issue that impedes (the permissibility) is removed, then the activity which was initially forbidden becomes permissible”.

P a g e 15 | 39

3.4 Speculation

Much of the issues about short selling is about speculation. Some of the arguments about

speculation is given below.

The proponent’s argument are-

Speculation reduces price fluctuations

Speculation activates the market as it encourages the circulation of large amounts

of stocks or goods, increases liquidity.

The speculator seeks to obtain a personal profit and there is nothing wrong with

that.

The opponent’s argument are-

Speculation aggravates price fluctuations as it originally relies on such

fluctuations and it finds no room if the prices stayed stable

The brokers and the well-informed speculators are the ones who benefit from the

intense heat produced by speculation

Speculation does not differ from gambling but rather it is one of its modern forms

(it does not encourage production…)

More losers than gainers (the experienced ones)

Speculation is zero sum game.

P a g e 16 | 39

04. Sukuk Market

4. Overview of the Sukuk Market

4.1 Types of Sukuk

4.2 Innovative Sukuk

4.2.1 Commodity Linked Sukuk (SLS) Model

4.2.2 GDP Linked Sukuk (GLS) Model

4.3 Sukuk Al- Istithmar vs Conventional Instruments

4.4 Secondary Market of Sukuk (Tradability)

4.5 Global Sukuk Market - A Snapshot

4.6 A Case Study- ADIB example

4.7 Shari’ah Concerns in Sukuk

P a g e 17 | 39

4. Overview of the Sukuk Market

The early Muslims have used the word Assakk, which means certificate or order of

payment. And the plural of this ‘Arabic term is Sukuk. They used Sukuk in those early days

as a form of papers representing financial obligations originating from trade or any other

commercial activities. However, in the modern day Islamic financial system, Sukuk are

known as instruments of the Islamic capital Market and it is one of the best financial

instruments and mechanisms that are commensurate with the needs of

issuers/originators and investors. [19]

According to AAOIFI “Investment Sukuk (Sukuk al Istithmar) are certificates of equal

value representing undivided shares in ownership of tangible assets, usufructs and

services or (in the ownership of) the assets of particular projects or special investment

activity”. [20]

4.1 Types of Sukuk

AAOIFI identified fourteen types of sukuk. Each of these sukuk is formed according to

known Islamic transaction contracts such as wakala, mudarabah, ijarah etc. Some of them

are described here.

4.1.1 Mudarabah Sukuk

These are certificates that represent project or activities managed on the basis of

Mudarabah by appointing one of the partners or another person as the mudarib for the

management of the operation.

4.1.2 Musharakah Sukuk

These are certificates representing projects or activities managed on the basis of

Musharaka by appointing one of the partners or another person to manage the operation.

4.1.3 Wakalah Sukuk

These are certificates that represent projects or activities managed on the basis of an

investment agency by appointing an agent to manage the operation on behalf of the

certificate holders.

19 IIFM Sukuk Report (3rd edition) : A Comprehensive Study of the Global Sukuk Market, p. 3 20 IIFM Sukuk Report (3rd edition) : A Comprehensive Study of the Global Sukuk Market, p. 4

P a g e 18 | 39

4.1.4 Muzara’a (Sharecropping) Sukuk

These are certificates of equal value issued for the purpose of using the funds mobilised

through subscription for financing a project on the basis of Muzara’a so that the certificate

holders become entitled to a share in the crop according to the terms of the agreement.

4.1.5 Musaqa (irrigation) Sukuk

These are certificates of equal value issued for the purpose of employing the funds

mobilized through subscription for the irrigation of fruit bearing trees, spending on them

and caring for them on the basis of a Musaqa contract so that the certificate holders

become entitled to a share in the crop as per agreement.

4.1.6 Mugharasha (Agricultural) Sukuk

These are certificates of equal value issued on the basis of a Mugharasa contract for the

purpose of employing the funds for planting trees and undertaking the work and

expenses required by such plantation so that the certificate holders become entitled to a

share in the land and the plantation.

4.1.7 Ijarah Sukuk

These are certificates of equal value issued either by the owner of a leased asset or a

tangible asset to be leased by promise, or they are issued by a financial intermediary

acting on behalf of the owner with the aim of selling the asset and recovering its value

through subscription so that the holders of the certificates become owners of the assets.

4.1.8 Istisna Sukuk

These are certificates of equal value issued with the aim of mobilizing funds to be

employed for the production of goods so that the goods produced come to be owned by

the certificate holders.

4.1.9 Murabaha Sukuk

These are certificates that represent equal value issued for the purpose of financing the

purchase of Murabahah commodity and therefore, the certificate holders become the

owners of the purchased commodity.

In this transaction, the issuer of these certificates is the seller of the Murabahah

commodity, the subscribers are the buyers of that commodity and mobilized funds are

P a g e 19 | 39

the purchasing cost of the commodity. The certificate holders own the Murabahah

commodity and are entitled to its sale price.

4.1.10 Salam Sukuk

These are certificates of equal value issued for the aim of mobilizing Salam capital so that

the goods to be delivered on the basis of Salam contract are owned by the certificate

holders.

In this transaction the issuer of these certificates is the seller of the Salam goods, the

subscribers are the buyers of the goods and the mobilized funds are the purchase price

of the commodity, which is the Salam capital. Thus, the certificate holders are the owners

of Salam goods and they are also entitled to the sale price of the certificate or the sale

price of the Salam goods sold through a parallel Salam, if any.

Types of Sukuk 1

P a g e 20 | 39

4.2 Innovative Sukuk

In this section, some innovative sukuk models are provided that solve the present

shari’ah problem of the sukuk practice around the world.

4.2.1 GDP-Linked Sukuk (GLS) Model

This model is based on forward ijarah where return is linked to the GDP of the issuing

country. It is a model for sovereign [21] sukuk where actual economic indicator is used to

calculate return on non-income generating government assets or projects. Here, Return

is linked to GDP that measures the actual performance of a economy, so it matches the

payment obligation to payment ability. The investors share the economic performance

risk of the issuers. The return is calculated through below formula.

𝑅𝑒𝑡𝑢𝑟𝑛 = 𝑥𝑘% = 𝐼𝑘 × 𝑋0%

𝐼𝑘 = 𝐺𝑘

𝐺0

Xk = The rate of return at kth year, after issuance

Gk = is the growth rate of GDP at year k

G0 = is the growth rate of GDP agreed upon by contracting parties.

4.2.2 Commodity Linked Sukuk (CLS) Model

This model is also based on forward ijarah. Government can raise funds for non-income

generating projects where return is linked to price index of a basket of issuing countries

export commodities. The model also matches the payment obligation to payment ability.

The investors share the risk arising from the volatility of the commodity market. This

model constitute a hedging components.

𝑅𝑒𝑡𝑢𝑟𝑛 = 𝑥𝑘% = 𝐼𝑘 × 𝑋0%

𝐼𝑘 = 𝑃𝑘

𝑃0

21 Sovereign sukuk are Sukuk issued by a national government. The term usually refers to Sukuk issued in foreign currencies, while Sukuk issued by national governments in the country’s own currency are referred to as government Sukuk.

P a g e 21 | 39

Ik = Basket Price Index

Pk = The price of the commodity in the basket, in the year k

xk% = Annual Profit Rate in the Year k

4.3 Sukuk Al- Istithmar vs Conventional Instruments

Sukuk Al-Istithmar is characterized with many features that distinguish them from the

non Shari ‘ah complaint bonds. These features include:

(a) Sukuk Al-Istithmar are certificates of equal value issued in the name of investor

therefore, a legitimate claim of its owner/investor over the financial rights and

obligations represented by the certificate can be established.

(b) It represents a common share in the ownership of the tangible assets earmarked for

investment, usufructs, services etc. and hence, it does not represent debt as in the case of

non Shari ‘ah compliant bonds.

(c) It is issued on the basis of known and acceptable Shari ‘ah investment contracts and

in accordance with Shari ‘ah principles which governing its issuance as well as its trading.

(d) Investors in Sukuk Al-Istithmar share the profit according to the agreement set forth

in the prospectus and also bear the losses if any, based on the percentage/proportion

owned by each investor.

The fundamental difference between bonds and sukuk is that while bonds are fixed-

income securities, sukuk Al-Istithmar are not fixed – income securities, because they do

not represent debts between the issuer and the investors. Rather, the investors share

Sukuk returns and proceeds according to percentages stated in the prospectus, and bear

losses in proportion to the number of the Sukuk certificates held by them.

Sukuk have very similarity with conventional securitization process. However, the

Shariah compliance condition for the transaction requires the presence of Shariah

advisory board in the process. Furthermore, the prohibitive stance of the majority of

Muslim scholars towards the sale of debt makes it inoperative to securitize a pool of asset

composed of a majority of receivables.

P a g e 22 | 39

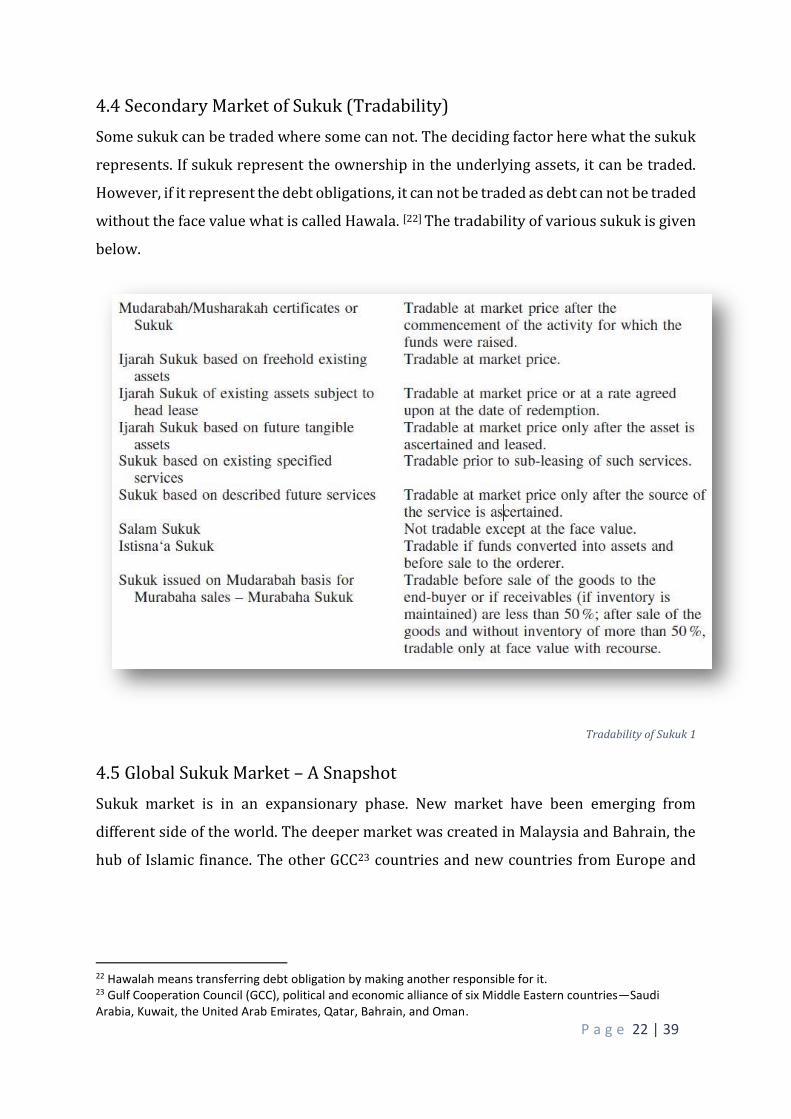

4.4 Secondary Market of Sukuk (Tradability)

Some sukuk can be traded where some can not. The deciding factor here what the sukuk

represents. If sukuk represent the ownership in the underlying assets, it can be traded.

However, if it represent the debt obligations, it can not be traded as debt can not be traded

without the face value what is called Hawala. [22] The tradability of various sukuk is given

below.

Tradability of Sukuk 1

4.5 Global Sukuk Market – A Snapshot

Sukuk market is in an expansionary phase. New market have been emerging from

different side of the world. The deeper market was created in Malaysia and Bahrain, the

hub of Islamic finance. The other GCC23 countries and new countries from Europe and

22 Hawalah means transferring debt obligation by making another responsible for it. 23 Gulf Cooperation Council (GCC), political and economic alliance of six Middle Eastern countries—Saudi Arabia, Kuwait, the United Arab Emirates, Qatar, Bahrain, and Oman.

P a g e 23 | 39

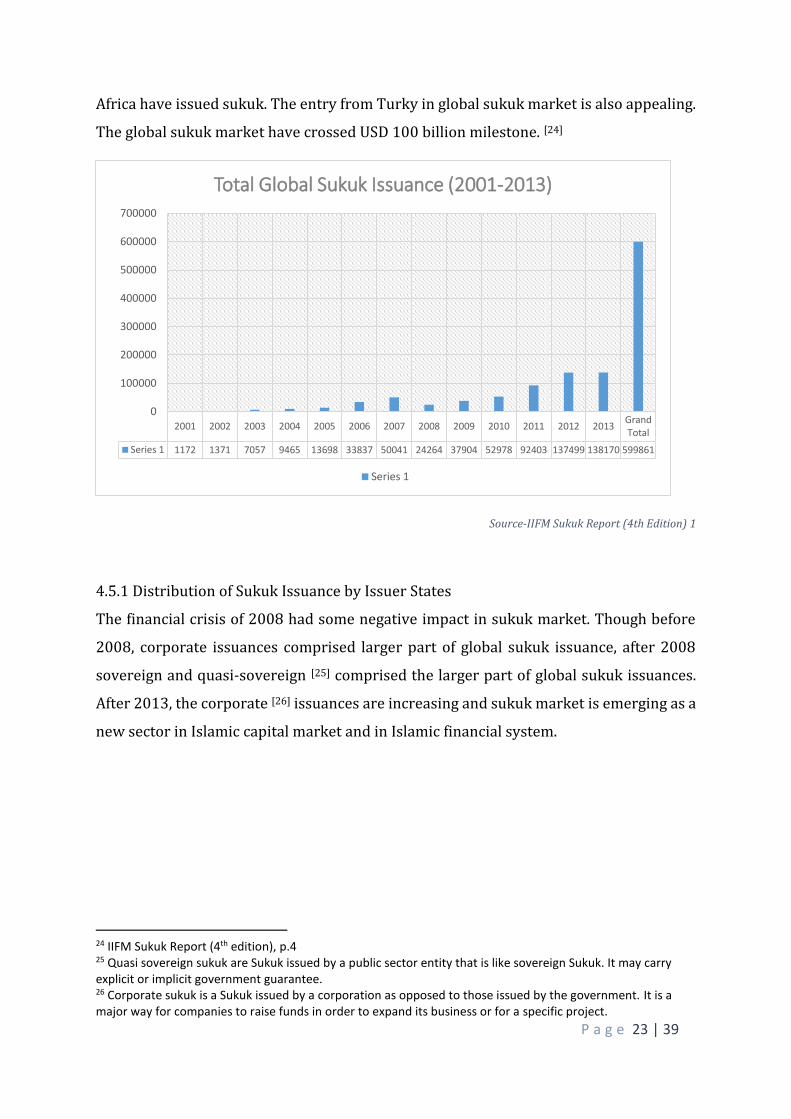

Africa have issued sukuk. The entry from Turky in global sukuk market is also appealing.

The global sukuk market have crossed USD 100 billion milestone. [24]

Source-IIFM Sukuk Report (4th Edition) 1

4.5.1 Distribution of Sukuk Issuance by Issuer States

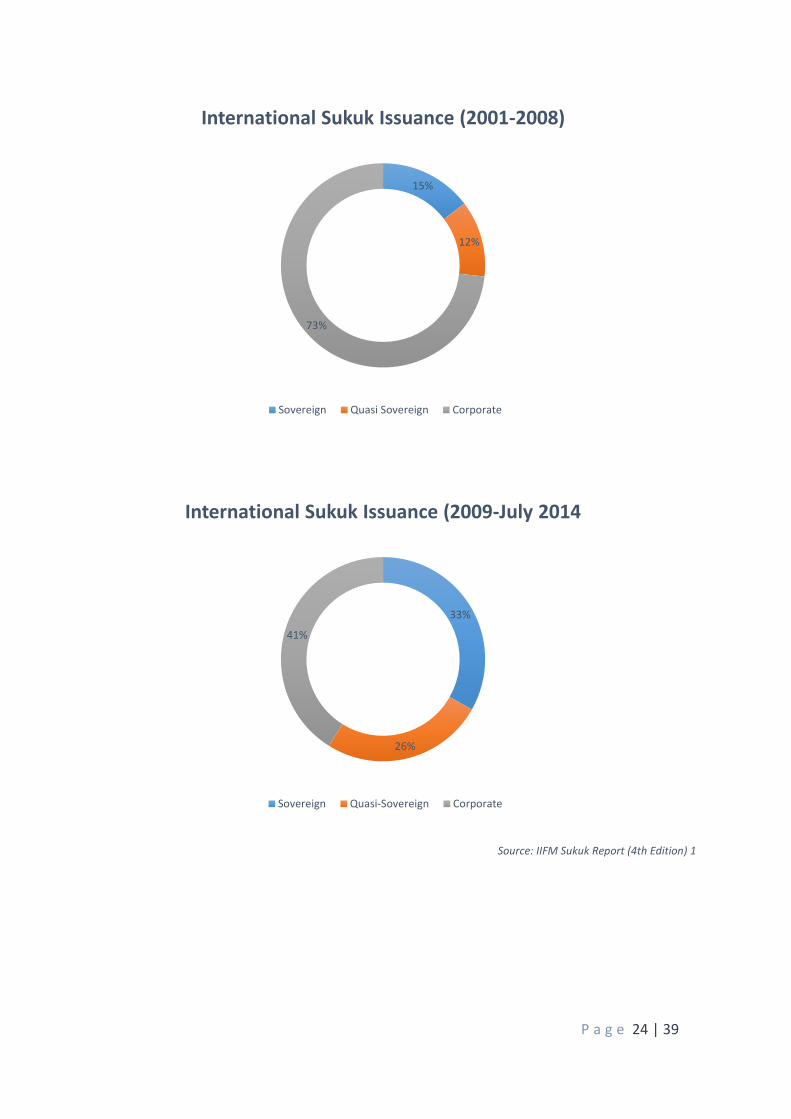

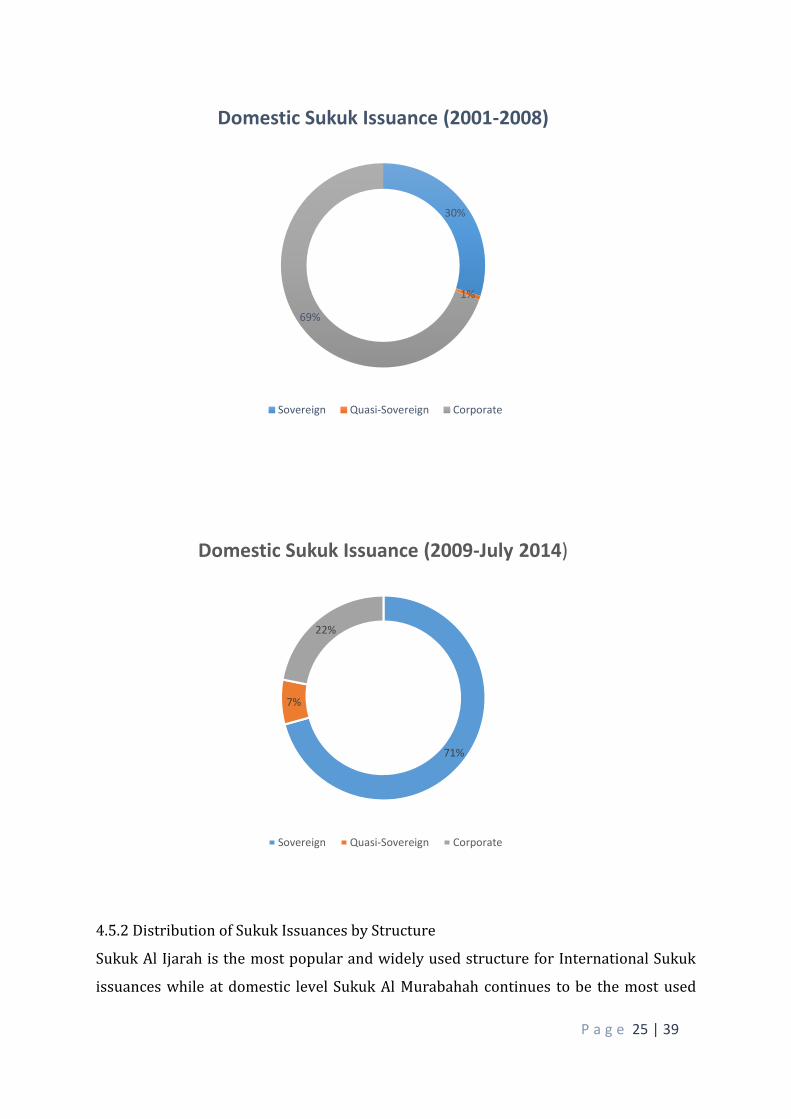

The financial crisis of 2008 had some negative impact in sukuk market. Though before

2008, corporate issuances comprised larger part of global sukuk issuance, after 2008

sovereign and quasi-sovereign [25] comprised the larger part of global sukuk issuances.

After 2013, the corporate [26] issuances are increasing and sukuk market is emerging as a

new sector in Islamic capital market and in Islamic financial system.

24 IIFM Sukuk Report (4th edition), p.4 25 Quasi sovereign sukuk are Sukuk issued by a public sector entity that is like sovereign Sukuk. It may carry explicit or implicit government guarantee. 26 Corporate sukuk is a Sukuk issued by a corporation as opposed to those issued by the government. It is a major way for companies to raise funds in order to expand its business or for a specific project.

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013GrandTotal

Series 1 1172 1371 7057 9465 13698 33837 50041 24264 37904 52978 92403 137499 138170 599861

0

100000

200000

300000

400000

500000

600000

700000

Total Global Sukuk Issuance (2001-2013)

Series 1

P a g e 24 | 39

Source: IIFM Sukuk Report (4th Edition) 1

15%

12%

73%

International Sukuk Issuance (2001-2008)

Sovereign Quasi Sovereign Corporate

33%

26%

41%

International Sukuk Issuance (2009-July 2014

Sovereign Quasi-Sovereign Corporate

P a g e 25 | 39

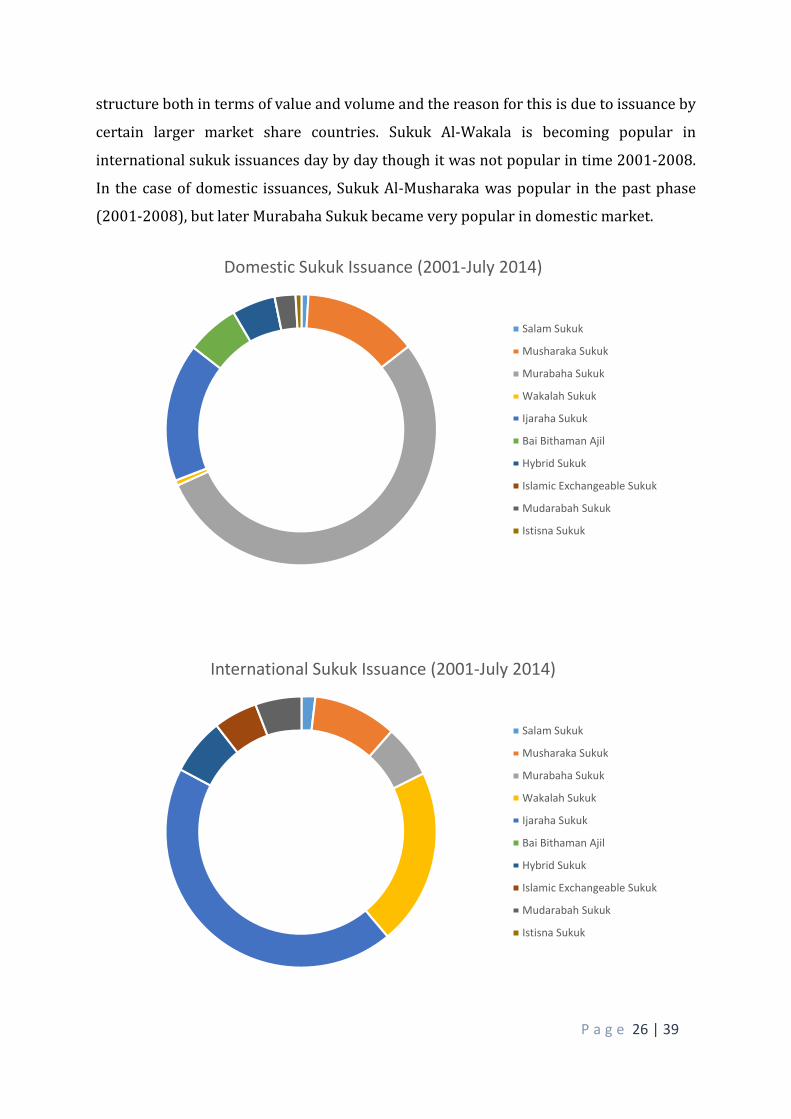

4.5.2 Distribution of Sukuk Issuances by Structure

Sukuk Al Ijarah is the most popular and widely used structure for International Sukuk

issuances while at domestic level Sukuk Al Murabahah continues to be the most used

30%

1%

69%

Domestic Sukuk Issuance (2001-2008)

Sovereign Quasi-Sovereign Corporate

71%

7%

22%

Domestic Sukuk Issuance (2009-July 2014)

Sovereign Quasi-Sovereign Corporate

P a g e 26 | 39

structure both in terms of value and volume and the reason for this is due to issuance by

certain larger market share countries. Sukuk Al-Wakala is becoming popular in

international sukuk issuances day by day though it was not popular in time 2001-2008.

In the case of domestic issuances, Sukuk Al-Musharaka was popular in the past phase

(2001-2008), but later Murabaha Sukuk became very popular in domestic market.

International Sukuk Issuance (2001-July 2014)

Salam Sukuk

Musharaka Sukuk

Murabaha Sukuk

Wakalah Sukuk

Ijaraha Sukuk

Bai Bithaman Ajil

Hybrid Sukuk

Islamic Exchangeable Sukuk

Mudarabah Sukuk

Istisna Sukuk

Domestic Sukuk Issuance (2001-July 2014)

Salam Sukuk

Musharaka Sukuk

Murabaha Sukuk

Wakalah Sukuk

Ijaraha Sukuk

Bai Bithaman Ajil

Hybrid Sukuk

Islamic Exchangeable Sukuk

Mudarabah Sukuk

Istisna Sukuk

P a g e 27 | 39

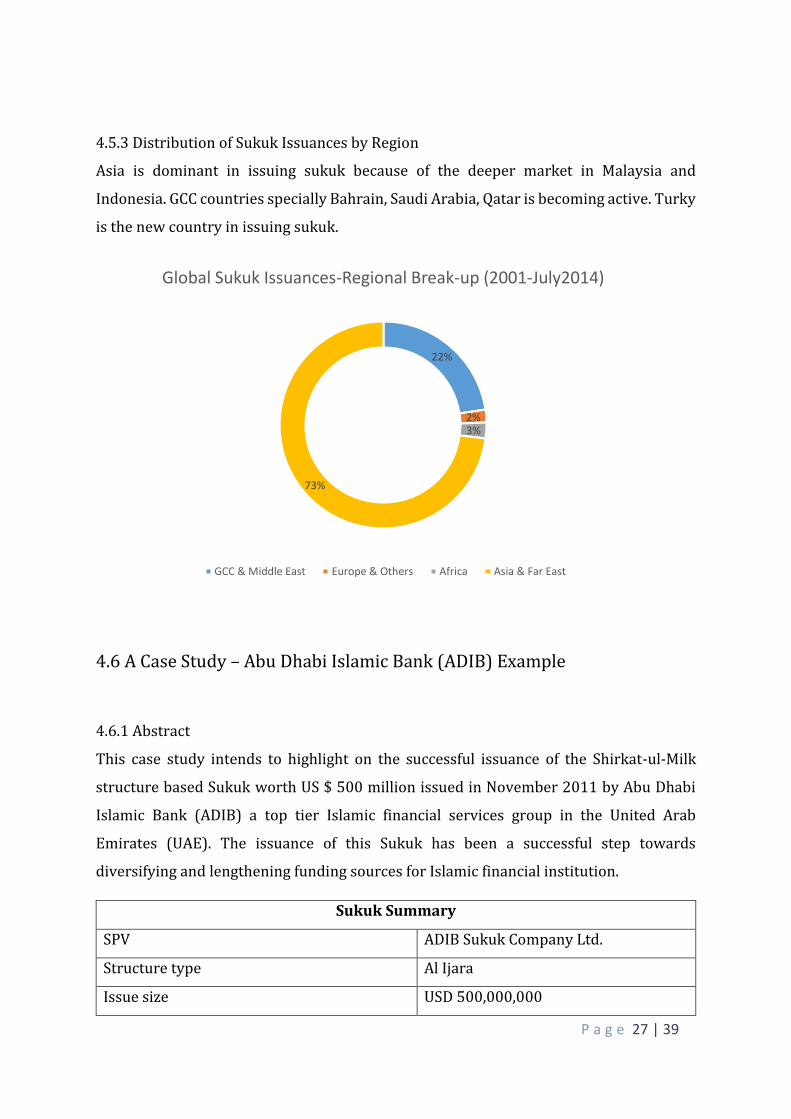

4.5.3 Distribution of Sukuk Issuances by Region

Asia is dominant in issuing sukuk because of the deeper market in Malaysia and

Indonesia. GCC countries specially Bahrain, Saudi Arabia, Qatar is becoming active. Turky

is the new country in issuing sukuk.

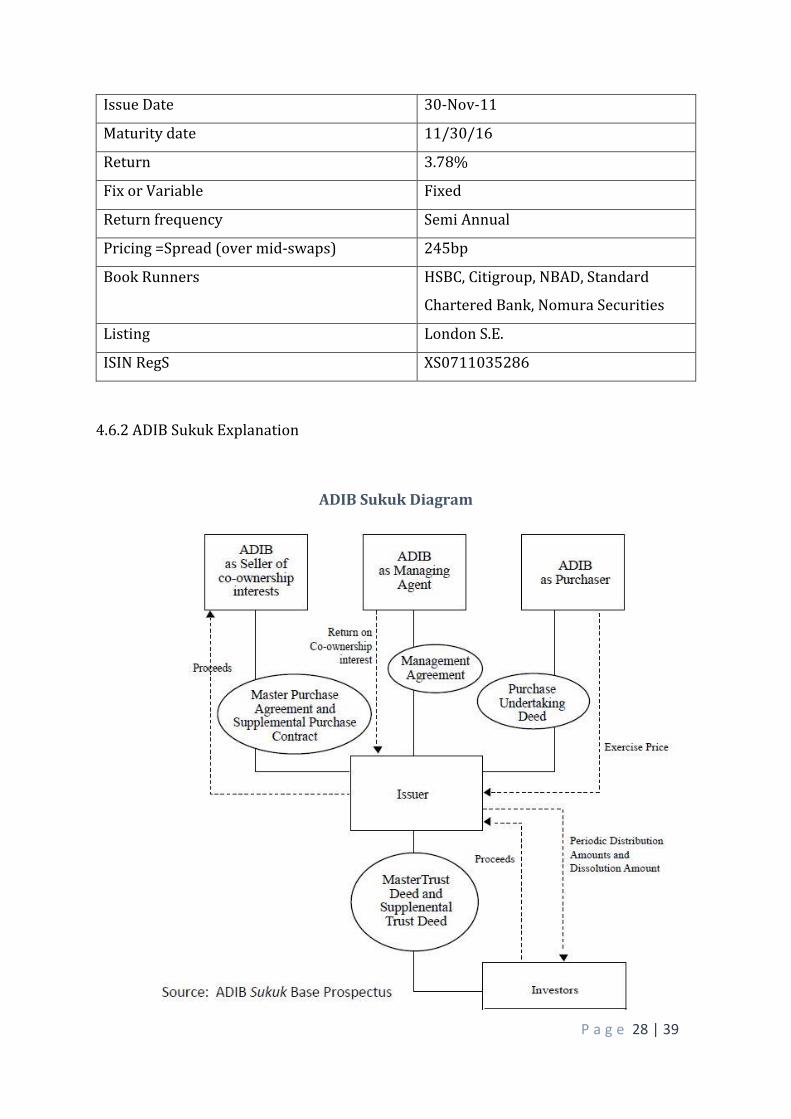

4.6 A Case Study – Abu Dhabi Islamic Bank (ADIB) Example

4.6.1 Abstract

This case study intends to highlight on the successful issuance of the Shirkat-ul-Milk

structure based Sukuk worth US $ 500 million issued in November 2011 by Abu Dhabi

Islamic Bank (ADIB) a top tier Islamic financial services group in the United Arab

Emirates (UAE). The issuance of this Sukuk has been a successful step towards

diversifying and lengthening funding sources for Islamic financial institution.

Sukuk Summary

SPV ADIB Sukuk Company Ltd.

Structure type Al Ijara

Issue size USD 500,000,000

22%

2%3%

73%

Global Sukuk Issuances-Regional Break-up (2001-July2014)

GCC & Middle East Europe & Others Africa Asia & Far East

P a g e 28 | 39

Issue Date 30-Nov-11

Maturity date 11/30/16

Return 3.78%

Fix or Variable Fixed

Return frequency Semi Annual

Pricing =Spread (over mid-swaps) 245bp

Book Runners HSBC, Citigroup, NBAD, Standard

Chartered Bank, Nomura Securities

Listing London S.E.

ISIN RegS XS0711035286

4.6.2 ADIB Sukuk Explanation

ADIB Sukuk Diagram

P a g e 29 | 39

1. On the Issue Date, the certificate holders will pay the issue price to ADIB Sukuk

Company (as Issuer/Trustee).

2. The proceeds will be used by ADIB Sukuk Company to purchase a co-ownership

interest in a portfolio of Ijarah assets from ADIB (as Seller) under a Purchase Agreement.

3. ADIB (as Managing Agent) agrees to maintain the co-owned Ijarah assets through a

Management Agreement.

4. ADIB will pay to the Issuer an amount representing its share of profit in respect of the

co-ownership as sets on each Periodic Distribution Date. If the profit returns are

insufficient to fund the periodic distribution payment, ADIB will make up for the shortfall

by providing Shari‘ah compliant funding to ADIB Sukuk Company. However, if profit

returns are more than the amount needed to pay the relevant periodic distribution, the

excess will be paid to ADIB as an incentive fee.

5. The Issuer will sell its co-ownership interest in the co-ownership assets to ADIB (as

Purchaser) on the Maturity Date, pursuant to a Purchase Undertaking.

6. The Exercise Price paid by ADIB is intended to fund the dissolution amount payable by

the Issuer under the Trust Certificates.

4.7 Sharia’h Concerns in Sukuk

The sukuk issuances so far raises some shari’ah concerns that need to be addressed and

solved. The guarantee in annual payment to investors make sukuk almost like

conventional debt. It is difficult to find some neutral third party who guarantee the

payment to the investors. Another issue is about purchasing the sukuk at face value or

pre-agreed price that is almost like Bai-al inah. The combination of different contracts to

make a sukuk issuance is also cumbersome and sometimes the investor doesn’t

understand the mechanisms. Scholars should look on this topic to solve the problem and

make a shari’ah complient sukuk market.

P a g e 30 | 39

05. Derivative Market

5. Overview of the Derivatives Instruments

5.1 Forward & Futures

5.2 Options

5.3 SWAP

5.4 Islamic Derivative Instruments

5.4.1 Bai Salam

5.4.2 Bai al-Arbun

P a g e 31 | 39

5. Overview of the Derivative Instruments

Most popular derivative instruments are forward, futures, options and recently swap

contracts. These instruments have different versions also. These are called derivatives

because they derive their value from underlying assets. Derivative instruments are used

for hedging [27] against price risk, exchange risk, interest rate risk etc, for arbitraging [28]

and for speculating [29]. In this section we will appraise all these instruments from Islamic

perspectives with the probable Islamic alternatives like salam and arbun contracts.

5.1 Forward & Futures

A Forward contract is a customized arrangement between two parties to carry out a

transaction at a future date but at a price determined today. Forward contracts have some

limitations like multiple coincidence of needs, potential for price squeeze, counterparty

or default risk etc. that leads to the emergence of futures that solved the problem. Future

contract are organized and exchange traded forward contracts.

5.1.1 Islamic appraisal

Forwards and futures are rejected by many shari’ah scholars including Mufti Taqi Usmani

on the basis of gharar, maysir etc. The reasons are given below.

The issue of non-existence of the subject matter (bay' al ma'dum) at the time of the

conclusion of the contract.

The issue of selling debt for debt which means both the price and goods are deferred.

Imam Ahmad Ibn Hanbal reported a consensus on its prohibition.

Derivatives markets are mostly used for speculative transaction, so it is a zero sum

game.

The underlying assets may not be halal.

However some scholars like Hashim Kamali accepts forwards and futures with the

assumptions that underlying assets are halal. There arguments are given below.

The essential element of a sale is delivery of the thing sold, and if the seller is unable

to deliver, this becomes garar.

27 Hedgers are the players whose objective is risk reduction by taking long or short position. 28 Arbitraging are the players whose objective is to profit from pricing differentials/mispricing. 29 Speculators are the players who establish positions based on their expectations of future price movements.

P a g e 32 | 39

The hadith reporting selling debt for debt is weak according to some jurists.

Futures and forwards are halal if underlying assets are halal based on maslahah

(public welfare) and darurah (needs).

5.2 Options

Options give the holders the right to buy and sell the assets at exercise price in future

date. However, options doesn’t create obligation, it give options to exercise.

5.2.1 Islamic Appraisal

When viewed solely as a promise to buy or sell an asset at a predetermined price within

a stipulated period, shari’ah scholars find nothing objectionable with options. It is in the

trading of these promises and the charging of premiums that objections are raised. And

based on this two issues, some scholars disapproved options. Conventional options have

some similarities with two concepts in the Islamic commercial law, namely: al-Khiyar[30]

and al-urbun.

5.3 SWAP

Swaps are customized bilateral transactions in which the parties agree to exchange cash

flows at fixed periodic intervals, based on an underlying asset.

5.3.1 Islamic Appraisal

It is one of the principles of the Shariah that two financial transactions cannot be tied

together in the sense that entering into one transaction is made a precondition to

entering into the second. In interest rate swap, one party pays the difference to another

for nothing.

In foreign exchange swap, parties involved want to change currency in future with rate

that is fixed by today and contract sealed today. This doesn’t fulfill the sale of Currency

(bay` al sarf) condition, that is, it should be exchanged by using spot rate.

30 The concept of al-khiyar arises in exchange contracts. These options may provide the contracting parties a right, either to confirm or to cancel the contract within a stipulated time period [e.g. option as a condition or stipulation (khiyar al-shart); option for defect (khiyar alayb); option of determination or choice (khiyar altayeen); option of inspection (khiyar al-ruyat); and option of acceptance (khiyar al-majlis)].

P a g e 33 | 39

5.4 Islamic Alternatives

Two contracts in Islamic finance have derivatives features. These are bai al salam and

bai al arbun. These two are described below.

5.4.1 Bai al Salam

Bai al Salam is a contract where one party (buyer) pays in advance where the

commodity is deferred to a future date. Bai salam is almost like conventional forward

contract, the big difference between the two is that in bai salam price is paid in advance,

commodity is deferred, where in forward both are deferred. Bai salam have also default

risk, the seller may not provide the commodity in time. The buyer can take security to

minimize the risk.

5.4.2 Bai al Arbun

Bai al-’urbun refers to a sale in which the buyer deposits earnest money with the seller

as part of part payment of the price in advance, but agrees that if he fails to ratify the

contract, he will forfeit the deposit money, which the seller can keep. While the three

schools of law (Hanafi, Maliki, and Shafii), consider al-urbun as an invalid contract, the

Hanbali school held that it is a legal contract.

P a g e 34 | 39

06. Islamic Finance in Bangladesh

Problems & Prospects

P a g e 35 | 39

6. Problems & Prospects of Islamic Finance in Bangladesh

6.1 Problems of Islamic Finance

6.1.1 Absence of Islamic Money Market

In the absence of Islamic money market in Bangladesh, the Islamic banks cannot invest

their surplus fund i.e., temporary excess liquidity to earn any income rather than keeping

it idle. Because all the Government Treasury Bills, approved securities and Bangladesh

Bank Bills in Bangladesh are interest bearing. Naturally, the Islamic banks cannot invest

the permissible part of their Security Liquidity Reserve and liquid surplus in those

securities. As a result, they deposit their whole reserve in cash with Bangladesh Bank.

Similarly, the liquid surplus also remains uninvested. On the contrary, the conventional

banks of the country do not suffer from this sort of limitations. As such, the profitability

of the Islamic banks in Bangladesh is adversely affected.

6.1.2 Absence of Suitable Long-term Assets

The absence of suitable long term assets available to Islamic banks is mirrored by lack of

short term tradable financial instruments. At present there is no equivalent of an inter-

bank market in Bangladesh where banks could place, say, over-night funds, or where they

could borrow to satisfy temporary liquidity needs. Trading of financial instruments is also

difficult to arrange when rates of return are not known until maturity. Furthermore, it is

not clear whether Islamic banks in Bangladesh can utilize more exotic instruments, such

as derivatives, that are becoming increasingly popular with conventional banks.

Obviously, these factors place Islamic banking in Bangladesh at a distinct disadvantage

compared to its conventional banking counterpart.

6.1.3 Shortage of Supportive and Link Institutions

Any system, however well integrated it may be, cannot thrive exclusively on its built-in

elements. It has to depend on a number of link institutions and so is the case with Islamic

banking. For identifying suitable projects, Islamic banking can profitably draw the

services of economists, lawyers, insurance companies, management consultants, auditors

and so on. They also need research and training forums in order to prompting

entrepreneurship amongst their clients. Such support services properly oriented towards

Islamic banking are yet to be developed in Bangladesh.

P a g e 36 | 39

6.1.4 Organizing Relationship with Foreign Banks

Another important issue facing Islamic banks in Bangladesh is how to organize their

relationships with foreign banks, and more generally, how to conduct international

operations. This is, of course, an issue closely related to the creation of financial

instruments, which would be simultaneously consistent with Islamic principles and

acceptable to interest-based banks, including foreign banks.

6.1.5 Long-term Financing

Islamic Banks stick very closely to the pricing policies of the government. They cannot

benefit from hidden costs and inputs, which elevate the level of prices by certain

entrepreneurs without any justification. On the other hand, Islamic banks as financial

institutions are even more directly affected by the failure of the projects they finance. This

is because the built in security for getting back their funds, together with their profits, is

in the success of the project. Islamically, it is not lawful to obtain security from the partner

against dishonesty or negligence, both of which are very difficult if not impossible to

prove.

6.2 The Future of Islamic Finance in Bangladesh

6.2.1. New banking philosophy for the Islamic Banks

There seems to be a gap between the ideals and actual practice of Islamic banks in

Bangladesh. In their reports, booklets, bulletins and posters their banks express their

commitment to striving for establishing a just society free from exploitation. Study shows

that a little progress has been achieved so far in that direction.

6.2.2. Banking Policies and practices should be modernized

Islamic banks, with a view to facing the growing competition either fellow-Islamic banks

or the conventional banks which have launched Islamic banking practices, will have to

adapt their functioning in line with modern business practices.

6.2.3. Policy and Strategy should be formulated

The first action that deserves immediate attention is the promotion of the image of

Islamic banks as PLS banks. Strategies have to be carefully devised so that the image of

Islamic character and solvency as a bank is simultaneously promoted.

P a g e 37 | 39

6.2.4. Stepping for Distributional Efficiency

The task is more challenging for Islamic banks, as they have to promote their

distributional efficiency from all dimensions together with profitability, Islamic banks,

step by step, have to be converted into profit loss-sharing banks by increasing their

percentage share of investment financing though PLS modes.

6.2.5. Allocating Efficiency should be promoted

The Islamic banks can improve their Allocative efficiency by satisfying social welfare

conditions in the following manner. First, they should allocate a reasonable portion of

their investible funds in social priority sectors such as agriculture (including poultry and

fishery), small and cottage industries and export-led industries like garment, shrimp

cultivation. Secondly, when the percentage shares of allocation of investible funds are

determined among the sectors of investment financing, profitability of projects should be

the criterion for allocating investment funds. The criterion would be best satisfied if more

and more projects were financed under PLS modes.

6.2.6. Government and Central bank's Responsibilities

Government should think actively for the promotion of Islamic banking in Bangladesh

considering its pre-development role. Bangladesh Bank should develop some Islamic

Monetary and saving instruments and create separate window for transactions with the

Islamic banks and a full-fledged Islamic banking Department for analyzing, supervising,

monitoring and guiding purpose, thereby facilitating Islamic banks for their smooth

development in Bangladesh.

6.2.7. Inter-Islamic Bank Co-operation and Perspective Plan

All Islamic banks should come forward to help each other’s and adopt a perspective plan

say for 27 years for Islamization of the banking system of Bangladesh. To actualize this

mission, they should set-up immediately an Apex Research Academy and Training

Institute designed with modern tools.

P a g e 38 | 39

Bibliography

Abdou Diaw, O. I. B. A. L., 2011. Public Sector Funding and Debt : A Case Study for GDP

Linked Sukuk. MPRA Paper No. 46008, posted 30. January 2014 03:15 UTC.

Ali Akkas, B. K. H. S. H. M. I. N. I. S. A. S., 2008. Text Book on Islamic Banking. 2nd ed.

Dhaka: Islamic Economics Research Bureau.

Ali, S. S., 2005. Islamic Capital Market : Products & Challenges. 1st ed. Jeddah: IRTI.

Asyraf Wajdi Dusuki, A. A., 2008. Fiqh Issues in Short Selling as Implemented in the

Islamic Capital Market in Malaysia. JKAU: Islamic Econ., Volume 21, pp. 63-78.

Auda, J., 2007. Maqasid al-SharϢah as philosopy of Islamic law, A systems approach.

London: The International Institute of Islamic Thought (IIIT).

Ayub, M., 2007. Understanding Islamic Finance. 2nd ed. London: John Wiley & Sons, Ltd.

Bacha, O. I., 1999. Derivative Instruments and Islamic : Some Thoughts for a

Reconsideration. International Journal of Islamic Financial Services, pp. Volume 1, No 1.

IIFM, 2013. Sukuk Report : A Comprehensive Study of The Global Sukuk Market (3rd

Edition), Bahrain: International Islamic Financial Market.

IIFM, 2014. Sukuk Report : A Comprehensive Study of The Global Sukuk Market (4th

Edition), Bahrain: IIFM.

Obaidullah, M., n.d. Islamic Financial Services. s.l.:Islamic Economics Research Centre.

S.Kevin, 2007. Security Analysis and Portfolio Management. 2nd ed. Delhi: Prentice Hall

of India Private Limited.

Shahfoundationbd.org. (2016). Islamic Banking: Problems and Prospects. [online]

Available at: http://www.shahfoundationbd.org/hannan/article10.html [Accessed 8

May 2016].

Ullah, M. and Chowdhury, S. (2013). Prospects of Islamic Banking in Bangladesh. 1st ed.

Kuala Lumpur, Malaysia.

Usmani, M. (1998) An Introduction to Islamic Finance, Karachi

P a g e 39 | 39