islamic financial instruments mbf 709 by dr. syed zulfiqar ali shah ph.d (finance), acma ref: own,...

TRANSCRIPT

Islamic Financial InstrumentsMBF 709

ByDr. Syed Zulfiqar Ali Shah

Ph.D (Finance), ACMARef: Own, Md Noor Ul Islam, Book

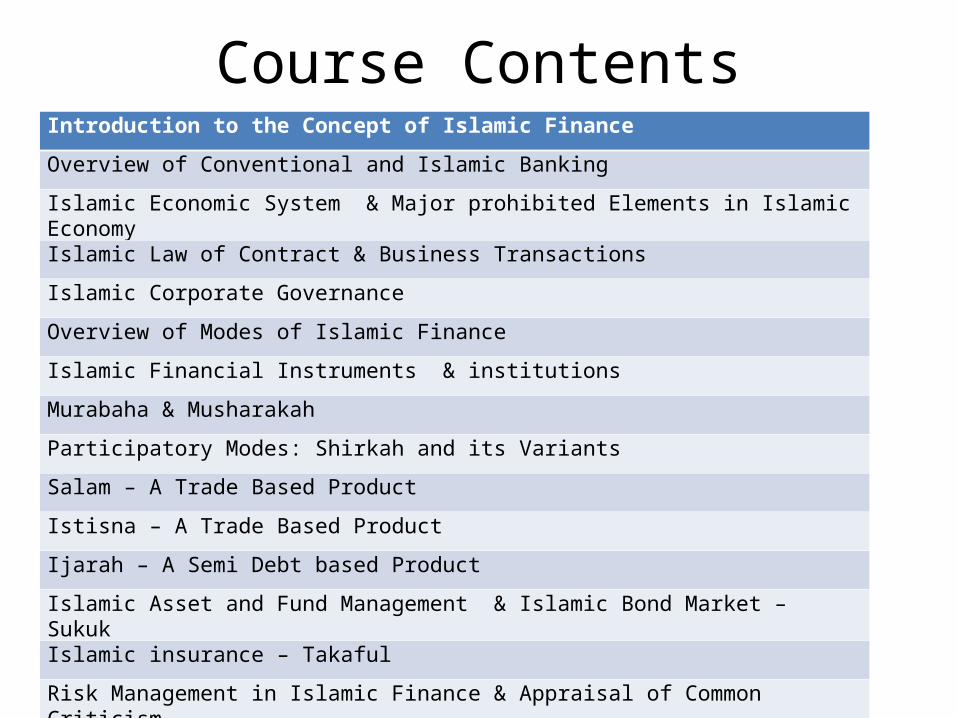

Course ContentsIntroduction to the Concept of Islamic Finance

Overview of Conventional and Islamic Banking

Islamic Economic System & Major prohibited Elements in Islamic Economy

Islamic Law of Contract & Business Transactions

Islamic Corporate Governance

Overview of Modes of Islamic Finance

Islamic Financial Instruments & institutions

Murabaha & Musharakah

Participatory Modes: Shirkah and its Variants

Salam – A Trade Based Product

Istisna – A Trade Based Product

Ijarah – A Semi Debt based Product

Islamic Asset and Fund Management & Islamic Bond Market – Sukuk

Islamic insurance – Takaful

Risk Management in Islamic Finance & Appraisal of Common Criticism

Plan of Today's Lecture Finance in General Perspective General Decisions in Finance Fundamental Principles of Islam: Maqasid Al-Shariah: The Strategy: The Islamic World View: Islamic Financial System(ifs): Differences Between CFS & IFS Principles of An Islamic Financial System The Objectives Islamic Economics and Banking Principles of Islamic Economics Systems: Deposit Products of Islamic Bank: Future of Islamic Banking

Finance

Decision Making

Four types of decisions• Investment Decision• Financing Decision• Asset Management Decision• Dividend Policy Decision

Investment Decision

• Estimation of Cash Flows• Required rate of return• Tools and techniques to evaluate proposal

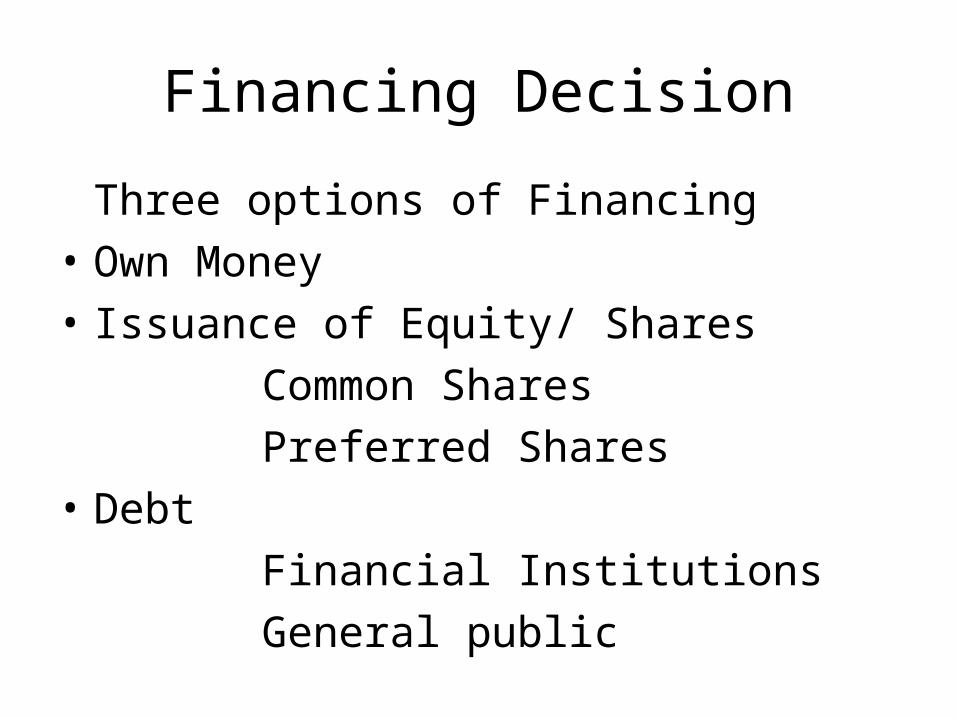

Financing Decision

Three options of Financing• Own Money• Issuance of Equity/ Shares Common Shares Preferred Shares• Debt Financial Institutions General public

Asset Management Decision

Assets• Current Assets• Non Current Assets

Dividend Policy Decision

Why Dividend Policy’• To avoid expected Risk• To have money for future investments

Fundamental Principles of Islam

Tawhid (Oneness And Unity of Allah Allah is One, Unique & Supreme

Khilafah (Vicegerency)The Concept of Khilafah has a Number of

Implications or Corollaries. These are:Universal BrotherhoodResources are a TrustHumble Life StyleHuman Freedom

Adalah (Justice)Need Fulfillment Respectable Source of EarningEquitable Distribution of Income & WealthGrowth & Stability

Maqasid Al-Shariah:Maqasid al-Shariah is to promote the welfare of the people by safeguarding their- Faith Prosperity (descendant)

Life & intellect Wealth

Maqasid (objectives of) al-Shariah There have been efforts by jurists to add to the list of these five requisites and also to change their sequence, but it seems that these attempts have, in general, not satisfied most jurists.

Imam Abu iIhaq-Al-Shatibi (d. 790/1388), writing a little less than three centuries after Al-Ghazali, put his stamp of approval on his list as well as the sequence, thereby indicating that both of these are the most preferable in terms of their harmony with the essence of the Shariah.

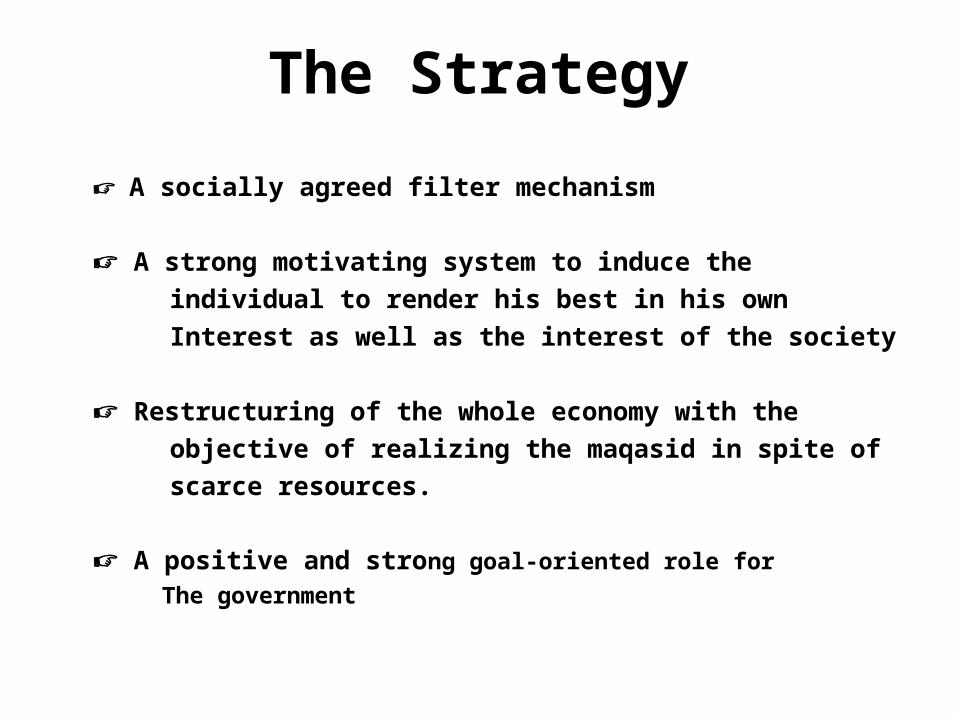

The Strategy

A socially agreed filter mechanism

A strong motivating system to induce the individual to render his best in his own Interest as well as the interest of the society

Restructuring of the whole economy with the objective of realizing the maqasid in spite of scarce resources.

A positive and strong goal-oriented role for The government

The Islamic World View

Inability of the capitalist & socialist countries as well as the developing economies to realize simultaneously the goals of both efficiency & equity

Social Darwinism, survival of the fittest, class struggle, maximum want satisfaction, material condition of life proved unsuccessful.

Maqasid Al-Shariah

Human well-being to be realized by ensuring the enrichment of the following five ingredients for every individual.

‘AqlIntellect

DinFaith

NaslPosterity

NafsSelf

MalWealth

Islamic Financial System Islamic financial system(ifs):• A financial system that is based on Islamic principles and values, which

eliminates riba and ensure a profit sharing mechanism in the financial system, may be called IFS.

• It may be characterized by the absence' of interest based financial institution & transactions, doubtful transactions or gharar, stocks of companies dealing in unlawful activities, unethical or immoral transactions such as market manipulation, insider trading short-selling etc.

Differences between CFS & IFS• The conventional financial system is of two types.

1) socialistic financial system and 2) capitalistic financial system

- both systems have been proved inefficient to establish economic balance in the society.

Islamic Financial SystemBasis of Difference CFS IFS

1. Religious Belief Secular & separates Religion from

other Parts human life

Belief in unity of God & relates this

belief to economic Life of a man

2. Freedom of Economic

Activity

In socialism govt. enjoys

economic freedom but in

capitalism Individuals enjoys

freedom.

Restrictive freedom is allowed in the

light of Shariah both by the govt. &/or

individuals

3. Ownership of meansSocialism-state ownership,

Capitalism-individual ownership

Allah is the exclusive owner. Man is

the caretaker of the property

4. Goals of financial SystemSocialism-profit of the society

Capitalism-Individual’s profit

Welfare of both here and hereafter.

5. Competition Socialism-No competition

Capitalism- Logical & unethical

competition

Logical Competition and financial co-

operation

6. Wealth distributionSocialism-Equal

Capitalism – Unequal

Equitable

Islamic Financial SystemBasis of Difference CFS IFS

7. Basis of Economic SystemRiba or Interest Interest Free; PLS, Zakat &

Compensation based

8. Sources of the System Intellects brain storming of the

economic problems of men’s life

Devine book “Al-Quran” &

Prophets(SM) speeches

9. Result Capitalism concentration of

income & economic power in few

hands. Inefficiency

Maximum & equitable Distribution of

economic opportunities and higher

production in the society

10. Social & environmental

welfare

Do not consider the social &

environmental welfare

Ensure social & environmental welfare

11. Owners exception in respect

of respect of investment

Dividend or part of profit in case

of equity financing

Part of Profit or Loss

12. Lender or Bank’s

expectation in terms of dept

financing

Interest Profit or Loss Sharing

13. Modes of Investment Loan, Overdraft & Cash Credit Mudarabah, Musharaka, Murabahah

etc.

Principles of an Islamic Financial System

The basic framework for an Islamic financial system is a set of rules and laws, collectively referred to as Shariah, governing economic, social, political and cultural aspects of Islamic societies. Shariah originates from the rules dictated by the Quran and its practices, and explanations rendered (more commonly known as Sunnah) by the Prophet Muhammad. Further elaboration of the rules is provided by scholars in Islamic jurisprudence within the framework of the Quran and Sunnah. The basic principles of an Islamic financial system can be summarized as follows:

Prohibition of interest : Prohibition of Riba, a term literally meaning "an excess" and interpreted as "any unjustifiable increase of capital whether in loans or sales" is the central tenet of the system. More precisely, any positive, fixed, predetermined rate tied to the maturity and the amount of principal (i.e.) guaranteed regardless of the performance of the investment) is considered Riba and is prohibited. The general consensus among Islamic scholars is that Riba covers not only usury but also the charging of "interest" as widely practiced.

Islamic Financial System

• This prohibition is based on arguments of social justice, equality, and property rights. Islam encourages the earning of profits but forbids the charging of interest because profits, determined ex post, symbolize successful entrepreneurship and creation of additional wealth whereas interest, determined ex ante, is a cost that is accrued irrespective off the outcome of business operations and may not create wealth if there are business losses. Social justice demands that borrowers and lenders share rewards s well as losses in an equitable fashion and that the process of wealth accumulation and distribution in the economy be fair and representative of true productivity.

• Risk sharing: Because interest is prohibited, suppliers of funds become investors instead of creditors. The provider of financial capital and the entrepreneur share business risks in return for shares of the profits.

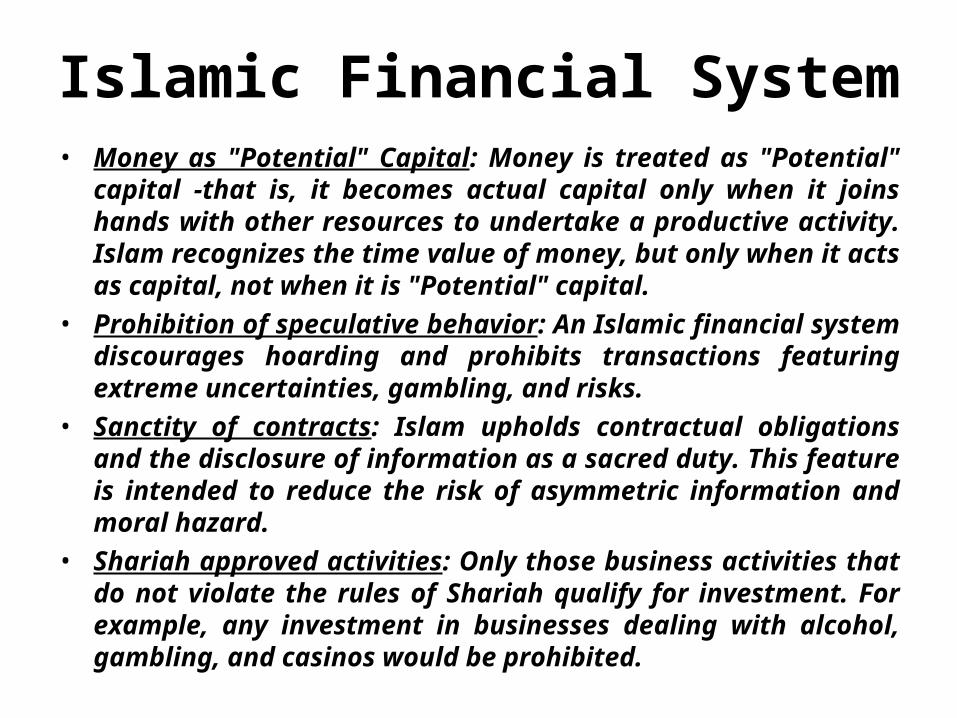

Islamic Financial System• Money as "Potential" Capital: Money is treated as "Potential" capital -

that is, it becomes actual capital only when it joins hands with other resources to undertake a productive activity. Islam recognizes the time value of money, but only when it acts as capital, not when it is "Potential" capital.

• Prohibition of speculative behavior: An Islamic financial system discourages hoarding and prohibits transactions featuring extreme uncertainties, gambling, and risks.

• Sanctity of contracts: Islam upholds contractual obligations and the disclosure of information as a sacred duty. This feature is intended to reduce the risk of asymmetric information and moral hazard.

• Shariah approved activities: Only those business activities that do not violate the rules of Shariah qualify for investment. For example, any investment in businesses dealing with alcohol, gambling, and casinos would be prohibited.

Islamic Financial SystemThe Objectives Islamic Economics and BankingThe Objectives of Shariah

• The very objective of the Shariah is to promote the welfare of the people which lies in safeguarding their faith, their life, their intellect, their posterity, and their wealth. Whatever ensures the safeguarding of these five serves public interest and is desirable. (AI-Ghazali)

• The-basis of the Shariah is wisdom and welfare of the people in this world as well as the Hereafter. This welfare lies in complete justice, mercy, well being and wisdom. Anything that departs from justice to oppression, from mercy to harshness, from welfare to misery and from wisdom to folly, has nothing to do with the Shariah (Ibn AI-Quayyum).Definition of EconomicsProf. L. Bobbins -“Economics is a science which studies human behavior as a relationship between ends end scarce means which have alternative uses.

Islamic Financial SystemDefinition of Islamic Economics

1. Islamic Economics is that branch of knowledge which helps realize human well-being through an allocation and distribution of scarce resource that is in conformity with Islamic teachings without unduly curbing individual freedom or creating continued macro-economic and ecological imbalances- Oman Chapra.

2. Islamic Economics aims at the study of human falah achieved by organizing the resources of the earth on the basis of co-operation and participants (Muhammad Akram Khan).

3. Islamic Economics is the Muslim thinker's response to the economic challenges of their times. In this Endeavour they are aided by the Quran and the Sunnah as well as by reason and experience- M Negatullah Siddiq.

4. Islamic Economics is the science of how man uses resources and means of production to study his worldly needs according to a predetermined code given by Allah (SWT) in order to achieve the greatest equity- Princes Muhammad Al-Faisal Soud.

5. Islamic Economics is a social science which studies the economic problem of the people imbued with the values of Islam. It is a composite social science which studies the problem of production, distribution and consumption through integrative system of exchange and transfer overtime and their social through integrative system of exchange and transfer overtime and their social and moral consequences in the light of Islamic rationalism. It assumes the presence of Islamic man. M.A. Mannan.

Islamic Financial SystemObjectives of Islamic Economics 1. To establish justice in the Economy (5:58) (16:90), Nahal, Nisa)

- Surely Allah enjoins justice and the doing good (to others) (16:90 Al-Nahal)- Whenever you judge between people, you judge with justice 5:58 (An-Nisa)

2. To protect the interest of the deprived and the oppressed. (28:5) (Kisas)

- And we desired to bestow a favour upon those who were deemed weak in the land, and to make them the leaders, and to make them the Heirs 28:5 (Al-Qasas)

3. To establish good practices and institutions in the economy and to eliminate bad practice and bad institutions from Economy (22:41)- [Well aware of] those who, if we firmly establish them in the land (on earth) will keep up prayer (remain constant prayer) and give in charity and enjoin good and forbid bad 22:41 (Al-Hajj)

Islamic Financial System4. To make life easy and bearable (7:157) 5. To ensure full utilization of resources.

6. Proper of distribution of wealth and Resources. 7. Maximum production of useful production. 8. Bring stability in the value of money and exchange rates 9. Ensure economic efficiency and accelerated rate of growth 10. Ensure broad based economic well being, balanced monetary expansion

and fill employment.

Islamic Financial SystemPrinciples of Islamic Economics Systems:1. Sole purpose is to obey and please Allah.2. The wealth and asset in all their forms given under trust by Allah.3. Moral values and guiding factors for all Economic activities.4. Maximum equitable utilization of human and material resources given by

Allah 5. Human dignity and respect of Labour.6. 'Maximum freedom for economic activity within a just framework.7. Equitable distribution of wealth and income and disciplined private

ownership. 8. Simplicity economy and austerity in expenditure.9. Adal and Ihsan (Justice and kindness).10. Strict prohibition of Riba, Interest and Usury in all forms.

Islamic Banking

Modern banking system was introduced into the Muslim countries at a time when they were politically and economically at a low ebb, in the late 19th century.

Governance structures are quite different from these under Islamic banking because the institution must obey a different set of rules - those of the Holy Qur'an - and meet the expectations of Muslim community by providing Islamically-acceptable financing modes.

The Islamic financial system employs the concept of participating in Halal business opportunities, utilizing the funds at risk on a profit-and-loss-sharing basis.

ISLAMIC BANKING MOVEMENT IN THE WORLD

The objective of Islam injunction is welfare of the whole humanity. Islamic Banking, based on the Islamic economic system, is not restricted to Muslims only.

Malaysia is the first country to issue bonds on Islamic basis. In August 1983, the Iranian government had passed the law

for riba free banking Islamic Banking and finance started in 1963 when Mit

Ghambr Savings Bank began offering interest free banking in Egypt.

Principles of Islamic Banking

An Islamic bank is based on the Islamic faith and must stay within the limits of Islamic Law or the sharia in all of its actions and deeds. The original meaning of the Arabic word sharia was 'the way to the source of life' and it is now used to refer to legal system in keeping with the code of behaviour called for by the Holly Qur'an (Koran). Four rules govern investment behaviour:

the absence of interest-based (riba) transactions; the avoidance of economic activities involving speculation

(ghirar); the introduction of an Islamic tax, zakat; the discouragement of the production of goods and

services which contradict the value pattern of Islamic (haram)

What is Riba?• The word "riba" means excess, increase or addition, which

correctly interpreted according to Shariah terminology, implies any excess compensation without due consideration (consideration does not include time value of money).

• This definition of riba is derived from the Quran and is unanimously accepted by all the Islamic scholars. There are two types of riba, identified to date by these scholars namely

• 'Riba an-Nasiyah' and 'riba al Fadl'. • 'Riba an-Nasiyah' is defined as excess, which results

From predetermined interest (Sood) which a lender receives over and above the principle (Ras ul Maal).

• 'Riba al Fadl' is defined as the excess compensation without any consideration resulting from a sale of goods

Speculation Another feature condemned by Islamic is economic transactions involving elements of speculation. Buying goods or shares at low and selling them for higher price in the future is considered to be illicit. Similarly an immediate sale in order to a void a loss in the future is condemned. The reason is that speculators generate their private gains at the expense of society at large.

ZakatA mechanism for the redistribution of income and wealth is inherent is Islam, so that every Muslim is guaranteed a fair standard of living, nisab. An Islamic tax, zakat (a term derived from the Arabic zaka, meaning "pure") is the most important instrument for the redistribution of wealth. This tax is a compulsory levy, one of the five basic tenets of Islam and the generally accepted amount of the zakat is one fortieth (2.5 per cent) of Muslim's annual income in cash or kind from all forms of assessed wealth exceeding nisab.

Haram A strict code of 'ethical investment' operates. Hence it is forbidden for islamic banks to finance activities or items forbidden in islam, haram, such as trade of alcoholic beverage and pork meat.

Profit-sharing agreements Although the restriction against the use of interest

might seem to be a binding constraint upon expansion, Islamic banks and financial institutions have in fact grown rapidly.

As the use of interest rates in financial transactions is prevented, Islamic banks are expected to undertake operations only on the basis of Profit and Loss Sharing (PLS) arrangements or other acceptable modes of financing. Mudarabah and musharaka are the two profit-sharing arrangements preferred under Islamic law

Sources of fundsBesides their own capital and equity, Islamic banks rely on two main sources of funds,\

a) transaction deposits, which are risk free but yield no return and,

b) investment deposits, which carry the risks of capital loss for the promise of variable. In all, there are four main types of accounts:

Current accountsCurrent accounts are based on the principle of Al-Wadiah, whereby the depositors are guaranteed repayment of their funds. At the same time, the depositor does not receive remuneration for depositing funds in a current account, because the guaranteed funds will not be used for PLS ventures

Savings Accounts

Savings accounts also operate under the al-Wadiah principle. Savings accounts differ from current deposits in that they earn the depositors income: depending upon financial results, the Islamic bank may decide to pay a premium, hiba, at its discretion, to the holders of savings accounts.

Investment accountsAn investment account operates under the Mudarabah al-Mutlaqa principle, in which the Mudarib (active partner) must have absolute freedom in the management of the investment of the subscribed capital.

Special investment accountsSpecial investment accounts also operate under the Mudarabah principle, and usually are directed towards larger investors and institutions

The Basic Difference between Capitalist and Islamic Economy

The basic difference between capitalist and Islamic economy is that in secular capitalism.

• Capital economy is based on the market forces.

• Islamic economy based on the Principles of Qur’an and Sunah.

The Performance of the Islamic Banks

• Islamic banking has become today an undeniable reality.

• The number of Islamic banks and the financial institutions is ever increasing.

• New Islamic Banks with huge amount of capital are being established.

• Conventional banks are opening Islamic windows or Islamic subsidiaries for the operations of Islamic banking.

Islamic Financial SystemDeposit Products of Islamic Bank:1.Al-wadeeah Current Deposits2. Mudarabah Savings Deposits3.Mudaraba Special Notice Deposits4.Mudaraba Term Deposits5.Mudaraba Hajj Savings A/c6.Mudaraba Savings Bond7.Mudaraba Special Savings Scheme8.Mudaraba Monthly Profit Dep. Schemes(MMPDS)9.MUDARABA MUHOR SAVINGS A/C10.Mudaraba Waqf Cash Deposit A/C11.Mudaraba Savings Deposits(RDS)

Islamic Financial SystemUNDER CAPITALISM UNDER ISLAM

1. Economic Laws are like physical laws 1. Economic laws are like natural laws

2. Positivism: Economics is a positive science as like as biology, physics which have no value, value neutral

2. Economics is value oriented. Permissible & prohibition have to be observed

3. Motive for More: Pecuniary interest. Man is rational economic being. Survival of the fittest, destruction of the poor

3. Man does not work for only personal interest. He has to secure the interest of this world & the world hereafter.

4. Market Oriented: Market can solve all the problems. Poor's’ need is not reflected in the market. Demand is backed by purchasing power. Result is the mismatch in resource allocation.

4. Market can solve major problem but not all. At least 20% economic problems to be solved by the government. Communism prescribes 100% solution by government. Capitalists leaves it 100% to market.

5. Little concern for poor humanity 5. Major concern for poor. Poverty alleviation by Zakat, Sadaqa & gives emphasis on economic progress

6. Nearly 100 corporate of ¾ countries control the world economy in the name of globalization.

6. No concentration of wealth in few hand. Wide dispersal of wealth & property

7. 18-20% people in Bangladesh live below poverty line (not getting two meals a day)

7. None can live below poverty line if Islamic economic system is established

The Future of Islamic Banking Islamic banking is here to stay. financial institutions predict that Islamic

finance will be the world's fastest-growing banking sector for years.

with a predicted modest estimate of 20 percent annual increase in deposits.

bankers are realizing that Islamic banking is big business that is only getting bigger

Japan is also planning to start Islamic banking

THANK YOU