issue 207, 29 july 2013 the time is now

TRANSCRIPT

Issue 207, 29 July 2013

The time is now

I don't have a crystal ball, but I have a pretty good idea that a week tomorrow we'll have a slightlylower cash rate. However, that will be the last rate cut for a while, which means now could be a verygood time to lock in a fixed rate for at least a portion of your home loan.

Also in the Switzer Super Report today, James Dunn finds seven under-70 cents specials, whichinclude some amazing stories like that of diagnostic imaging company Capitol Health and PotashWest. Paul Rickard suggests it's a good practice to compare your SMSF results with what the big gunsare doing, and Penny Pryor shares what one of the big banks think when it comes to extending LimitedRecourse Borrowing Arrangements (LRBAs).

Sincerely,

Peter Switzer

Inside this Issue

Seven sizzling stocks

under 70 cents

by James Dunn

04

02 To fix or not to fix?by Peter SwitzerTime to bet against the banks

04 Seven sizzling stocks under 70 centsby James DunnThere’s value on the edges

07 How well has your SMSF done?by Paul RickardThe best returns in 16 years

09 LRBAs – what the banks really thinkby Penny PryorBare trust or unit trust

10 Buy, Sell, Hold – what the brokers sayby Rudi Filapek-VandyckFBT impacts McMillan Shakespeare

12 Sydney still the star by Penny PryorAnother 80%

Switzer Super Report is published by Switzer Financial Group Pty Ltd AFSL No. 286 531

36-40 Queen Street, Woollahra, 2025

T: 1300 SWITZER (1300 794 8937) F: (02) 9327 4366

Important information: This content has been prepared without taking accountof the objectives, financial situation or needs of any particular individual. It doesnot constitute formal advice. For this reason, any individual should, beforeacting, consider the appropriateness of the information, having regard to theindividual's objectives, financial situation and needs and, if necessary, seekappropriate professional advice.

To fix or not to fix?

by Peter Switzer

Being known and hailed in the media as a so-calledmoney guru effectively means that most people aremore likely to ask me about what the RBA is going todo before they ask me how I am!

And while I know I sound like I’m a shares junkie inmost of my writings and media appearances, that’sonly because I suspect many of my subscribers andviewers feel more vulnerable when it comes tostocks. However, as an investor, financial plannerand personal wealth builder, I have a very healthyrespect for property.

Now or never?

So as we await the RBA’s decision next Tuesday,which will clearly affect those of you who are dreadingthe short-term fate of term deposits, the big questioneveryone is asking me is – is it time to fix my rate?

By the way, lots of our subscribers also havemortgages and, clearly, the better your day-to-daydecisions on any money front, the better theimplications for your future wealth.

Of course, this question is not an easy one to answer,as I think we will see at least one more rate cut fromthe RBA and I hope it’s next week. It should then beuphill until then for rates. It will take time but Iwouldn’t be surprised to see the first rise later in2014. In fact, I hope so, as it will confirm thatAustralia, the USA and the European economies areon the way back.

This will help add power to this great bull market,which has seen our market go up around 85% sinceMarch 2009, if you add in dividends. In fact, withgrossed up dividends, thanks to franking credits, weare back in front, provided your portfolio of stocks isas good, if not better than, the All Ords.

Anyway, back to the task at hand. For investors, orthose with mortgages on their principal home, wherethey know they won’t be moving in the next fiveyears, the five-year fixed rate looks hard to ignoreright now.

The best rates

UBank for refinancing has a 5.16% rate, which on acomparison or AAPR basis is 4.99%. State Custodianhas a 5.53% product, which is effectively a 5.05%rate. Looking at the big banks, the NAB is the bestwith a 5.65% rate, which, on a comparison basis,ends up as 6.01%. On this comparison rate basis, theCBA is at 6.08%, ANZ 6.12% and Westpac is 6.15%.

Why do I focus on the five-year rate? That’s simple,interest rates will start rising again and they could beover these rates within two and a half years, and so ifyou chose three-year fixed, you could be rolling offthese good rates just as rates were rising.

What are the pitfalls?

Well, I could be wrong and a worse recession liesahead and rates would fall further but you’d still belocked into great rates anyway, so the gamble isworth thinking about.

Another problem could be the break cost if you wantto get out of the loan early, but if you want to get outwhen rates are higher, the cost should not beshocking. When you want to get out of a highfixed-rate contract to access lower rates, the slug ishard.

For standard variable investment loan rates,loans.com.au has the best rate at 4.75%, which reallyis 4.78%, to be precise. State Custodians offer4.99%, which is really 4.89%, while UBank is 4.87%for both rates.

02

Big bank loan-wise shows their standard offerings areas follows, NAB at 5.92% (5.93%), ANZ 6.13%(6.23%), CBA 6.15% (6.30%), Westpac 6.26%(6.4%).

By the way, these rates are the same as the standardvariable home loan rates for ordinary borrowers, asopposed to would-be property investors.

In case you didn’t know this, fixed rates are notdirectly linked to what happens to the cash rate, whilestandard variable rates are.

I think global interest rates are now in their trough andthe only way is up, and that’s why I think we’re closeto the bottom of fixed rates. Sure, there could besome more competitive cuts, but I can’t see themgoing all that much lower, unless the ‘you knowwhat’ hits the fan, and I don’t expect this to happen.

By the way, when fixed rates start moving up, theycan be by quite a significant jump.

One final piece of advice – always ask for thecomparison rate as this includes the fees andcharges, which are left out of the headline rate ofinterest, which always sucks a lot of people in whenthey see those standout ads in newspapers and onwebsites. And don’t forget your can always refer toour term deposit rates table which is updated weekly, here.

All rates cited are from www.canstar.com.au.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

03

Seven sizzling stocks under 70 cents

by James Dunn

Outside the S&P/ASX 200, there are another 2,000listed companies, which mostly go unnoticed. Butthere is a myriad of interesting stories down there, forthose who take the time to look. Here are seven suchstocks, all trading at less than 70 cents.

1) AMA Group (AMA, 33.5 cents)

Listed since August 2006, Queensland-based carparts and panel beating business AMA Group,operates in the wholesale vehicle aftercare andaccessories market. Its line-up of businesses includessmash repair shops, automotive and electricalcomponents, vehicle protection bull bars and otherservicing workshops for brakes and transmissions.

Despite some pressure from the weakening miningand resources sector in the first half of FY13, AMAreported that revenue rose by 16% and operatingprofit was up 26%. The company paid a fully-frankedinterim dividend of 1.6 cents a share: even if AMAonly matched last year’s final dividend of 1 cent ashare, that would imply a 7.8% nominal yield.

2) Capitol Health (CAJ, 29.5 cents)

Victorian-based specialised diagnostic imaging (DI)company Capitol Health is the only specialised DIcompany listed on the ASX. Capitol is poised forgrowth in a market estimated to be $3 billion in size,and growing at about 5% a year, driven bydemographics (expanding and ageing population), ashift in healthcare focus to early detection andprevention of conditions, the improving accuracy andcapabilities of imaging techniques and governmentinitiatives (growth in the range of Medicare-eligibleservices). Last week, Capitol reported a 19.5% rise inrevenue for FY13 and an 80% rise in pre-tax profit.The nominal historic yield of 1.9% is nothing to writehome about at present, but should grow in comingyears.

3) Calliden Group (CIX, 33 cents)

04

General insurance specialist Calliden Group reporteda loss of $10.2 million for 2011 (the company usesthe calendar year for its financial year), amid one ofthe most difficult years the global insurance industryhad seen in some time. But it used that downturn totransform itself from general insurer to being more ofan underwriting agency business: it now writespolicies on behalf of three external insurers, as wellas itself. Half of the company’s business now comesfrom policies underwritten by third-party insurers. Italso moved back into the reinsurance business.

Calliden returned to profitability in 2012, earning a netprofit of $1.1 million, and resumed paying fullyfranked dividends with a payout of 0.4 cents a share.This year Calliden is targeting net profit of $10 million,and a dividend payout ratio between 60% – 80% ofnet profit. Having the less-volatile agency business isvital in building the capacity to pay increasingfully-franked dividends. If Calliden could get close to$10 million net profit and pay out 80%, the dividendcould be something like 3.5 cents a share – whichwould start to look pretty attractive on yield grounds,on a 33-cent share price.

4) Red Fork Energy (RFE, 44 cents)

Tulsa, Oklahoma-based Red Fork Energy, listed bothon the ASX and the OTCQX internationalmarketplace in the US, is an oil and gas producerdeveloping the Big River Mississippian project innorthern Oklahoma. Earlier this month, the companyraised $47.7 million from a placement at 43 cents ashare to institutional and sophisticated investors, tobuild further on its holdings of proven production wellsand its 70,000 acres of exploration holdings overground considered highly prospective for bothconventional oil and gas and ‘unconventional’ gas(gas found in shale and rock formations), as well ascoal-bed methane.

05

Red Fork Energy is cashed-up, well-poised in termsof production, project development and expansion,and has a great location in one of North America’smost exciting hydrocarbon provinces. The analysts’consensus estimates for the one-year price target forthis stock is 80 cents.

5) Avita Medical (AVH, 14 cents)

Avita Medical is one of the most promising Australianbiotechs. It is commercialising its ReCell technology,which involves using a patient’s own skin cells tocreate a skin graft that takes away the risk of rejectionor scarring.

A Phase III Food & Drug Administration (FDA) trial isin process, involving 10 US burns centres, helped by$US2.6 million in grant funding from the USDepartment of Defence, the US Army, and the USArmed Forces Institute for Regenerative Medicine(AFIRM). Data from the trial is expected next year.

AFIRM believes ReCell is potentially a“transformational” technology in treating woundedsoldiers. The treatment also has huge implications inthe area of burns and scalds, particularly in children.Given positive results from the Phase III clinical trial,US firm Zacks Investment Research says ReCell hasa potential sales opportunity in the US alone ofUS$100 million a year.

6) Global Construction Services (GCS, 46 cents)

Like many businesses that serve the resourcesindustry, Global Construction Services (GCS) has feltthe pinch of the de-booming of the mining-relatedeconomy. GCS supplies integrated on-site labour andservices – design and engineering, scaffolding, plantand equipment, formwork and concreting, siteaccommodation and specialised site services – tocustomers in the residential, commercial, resourcesand industrial sector. In May, the company reportedthat earnings before interest, tax, depreciation andamortisation (EBITDA) would likely fall by about 10%in FY13, to about $45 million, but the company wasupbeat on expected improvements in financialperformance in FY14.

Since the downgraded earnings guidance, GCS wonthe principal scaffolding contract for all of WoodsideEnergy Limited’s North-West Shelf projects,including onshore and offshore operations, for threeyears, with two further 12-month extension options.GCS will also be supplying specialist managementand labour resources to work with Woodside. Afternot receiving a final dividend in FY12, GCSshareholders were heartened to see an interimdividend for FY13 of 4.25 cents, the same as in FY12,and will be looking for further evidence of recovery inthe current financial year.

7) Potash West (PWN, 13.5 cents)

06

Earlier this year, Goldman Sachs identified potash –used in fertilisers – as a boom commodity for the nextdecade, on the back of growing pressure to feed theworld. That theme is good news for Potash West,whose Dandaragan Trough project in WesternAustralia is potentially one of the world’s largestknown deposits of glauconite, a mineral containingpotassium oxide, an essential ingredient of potashfertilisers.

Australia has never had a potash producer: thecountry imports all of its potash needs, but PotashWest is looking to change that. Potash West controlsalmost 3000 square kilometres of glauconite- andphosphate-rich ground in the Dandaragan region inWestern Australia. The company is presently workingon a scoping study and looking to define its resourcebase to support a bankable feasibility study (BFS).The plan is to complete the BFS in 2015, withproduction by mid-2018. Based on expected potashprice levels, an April 2013 report from NewYork-based financial consulting firm, ArrowheadBusiness and Investment Decisions, reckons theDandaragan Trough project could ultimately justify afair share value for PWN in the $0.44–$3.08 range.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

How well has your SMSF done?

by Paul Rickard

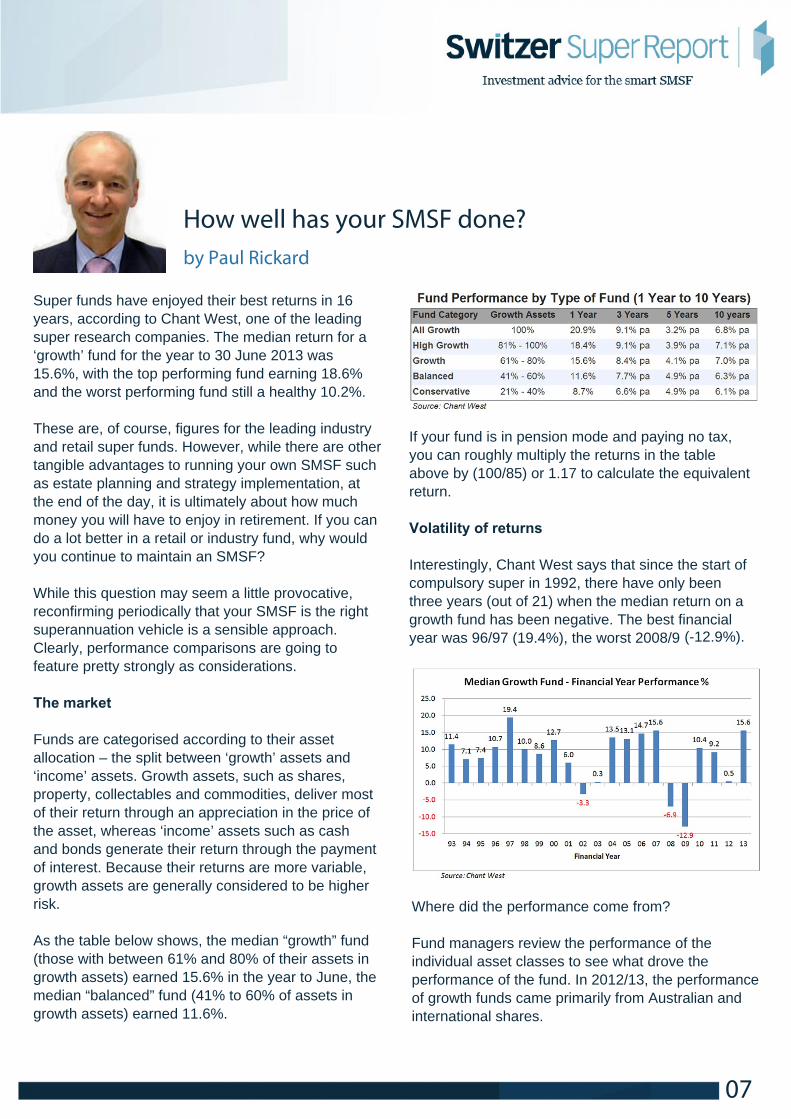

Super funds have enjoyed their best returns in 16years, according to Chant West, one of the leadingsuper research companies. The median return for a‘growth’ fund for the year to 30 June 2013 was15.6%, with the top performing fund earning 18.6%and the worst performing fund still a healthy 10.2%.

These are, of course, figures for the leading industryand retail super funds. However, while there are othertangible advantages to running your own SMSF suchas estate planning and strategy implementation, atthe end of the day, it is ultimately about how muchmoney you will have to enjoy in retirement. If you cando a lot better in a retail or industry fund, why wouldyou continue to maintain an SMSF?

While this question may seem a little provocative,reconfirming periodically that your SMSF is the rightsuperannuation vehicle is a sensible approach.Clearly, performance comparisons are going tofeature pretty strongly as considerations.

The market

Funds are categorised according to their assetallocation – the split between ‘growth’ assets and‘income’ assets. Growth assets, such as shares,property, collectables and commodities, deliver mostof their return through an appreciation in the price ofthe asset, whereas ‘income’ assets such as cashand bonds generate their return through the paymentof interest. Because their returns are more variable,growth assets are generally considered to be higherrisk.

As the table below shows, the median “growth” fund(those with between 61% and 80% of their assets ingrowth assets) earned 15.6% in the year to June, themedian “balanced” fund (41% to 60% of assets ingrowth assets) earned 11.6%.

If your fund is in pension mode and paying no tax,you can roughly multiply the returns in the tableabove by (100/85) or 1.17 to calculate the equivalentreturn.

Volatility of returns

Interestingly, Chant West says that since the start ofcompulsory super in 1992, there have only beenthree years (out of 21) when the median return on agrowth fund has been negative. The best financialyear was 96/97 (19.4%), the worst 2008/9

07

Where did the performance come from?

Fund managers review the performance of theindividual asset classes to see what drove theperformance of the fund. In 2012/13, the performanceof growth funds came primarily from Australian andinternational shares.

(-12.9%).

The cautionary tale

The last financial year has been a great year forsuper, and most SMSF members are going to bepretty happy when they receive their annual memberstatement.

While it is easy to sit back and think things are goingwell, it is a good idea to compare your SMSF’sperformance with the industry benchmark (based onthe risk profile and weighting towards growth assets)to see what sort of job you are really doing. Or, if youare being advised, to help validate the value youradviser may be adding.

Finally, work out what is driving the return. ManySMSFs have material holdings in the four majorbanks and Telstra – and should be enjoying apercentage fund return in the 20s – possibly even 30sfor 2012/13. The cautionary tale here, however, isthat it is very rare for an asset class to be the bestperforming asset class two years in a row. Notunheard of, but unlikely.

08

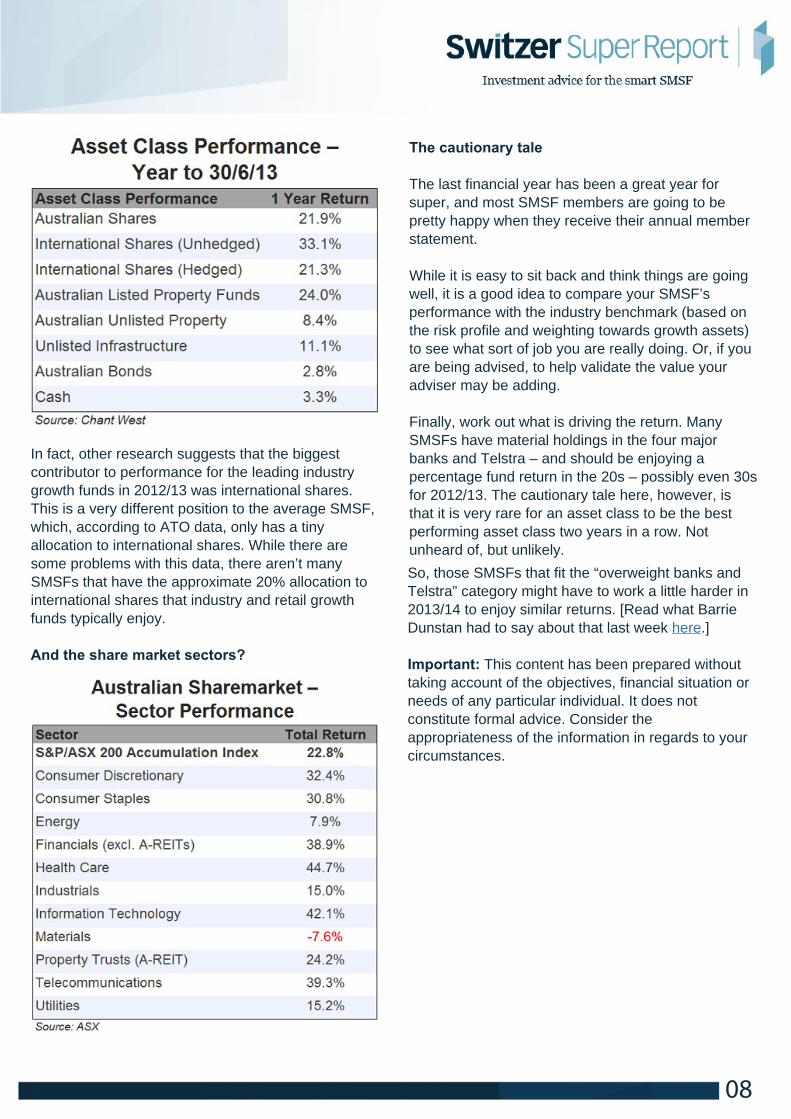

In fact, other research suggests that the biggestcontributor to performance for the leading industrygrowth funds in 2012/13 was international shares.This is a very different position to the average SMSF,which, according to ATO data, only has a tinyallocation to international shares. While there aresome problems with this data, there aren’t manySMSFs that have the approximate 20% allocation tointernational shares that industry and retail growthfunds typically enjoy.

And the share market sectors?

So, those SMSFs that fit the “overweight banks andTelstra” category might have to work a little harder in2013/14 to enjoy similar returns. [Read what BarrieDunstan had to say about that last week here.]

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

LRBAs – what the banks really think

by Penny Pryor

It has been six years now since SMSFs were able toborrow to invest in assets and as a result, it isbecoming much more common place. It is still acomplex process to go through to secure a loan, butmore borrowers now understand this, according toone major player in the market.

Speaking at the SMSF Professional Association ofAustralia’s (SPAA) technical conference, head ofSMSF trustee distribution, Westpac Group, SinclairTaylor, estimated that the size of the loan market inSMSFs was between $6 and $7 billion, of whichWestpac Group has funded $2 billion worth of loans.

“We hold a reasonable chunk of that because we’vebeen in the market since day one,” he said.

They also estimate that 30,000 SMSF funds areborrowers.

“We’re certainly keen to make sure borrowers aregetting into [borrowing to buy property] for the rightreasons.”

And part of that process is educating potentialborrowers that the limited recourse borrowingarrangement (LRBA) is not the kind of thing you do inan afternoon, after you’ve made a bid on a propertyon whim.

“It’s getting borrowers to understand this is oftenweeks and months in the making to lead up to thatloan,” Taylor said.

Westpac Group sees some interesting structuresaround loan requests but the majority of thoseapproved are for residential property andnon-specialised commercial property.

“Vacant land and rural property [we’re] not asinterested [in],” Taylor said.

“We are really keen to understand the underlyingperformance of the asset that has been acquired.”

Bare trust or unit trust

Another tricky question SMSF trustees looking toborrow to invest in property may ask, is what is thebest kind of trust to hold the asset in until the loan ispaid out?

Also on the SPAA panel with Taylor was BelindaAisbett, auditor and director of Super Sphere, who isdefinitely in favour of the bare trust.

“I’m a big fan of it being a bare trust…a unit trustcomplicates things, make its muddy,” she said.

“Also when you’ve a got a unit trust acting in thatcapacity, you’re really just creating problems in termsof in house assets”

It’s not impossible to structure a unit trust so that itcomplies; it’s just very, very difficult.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

09

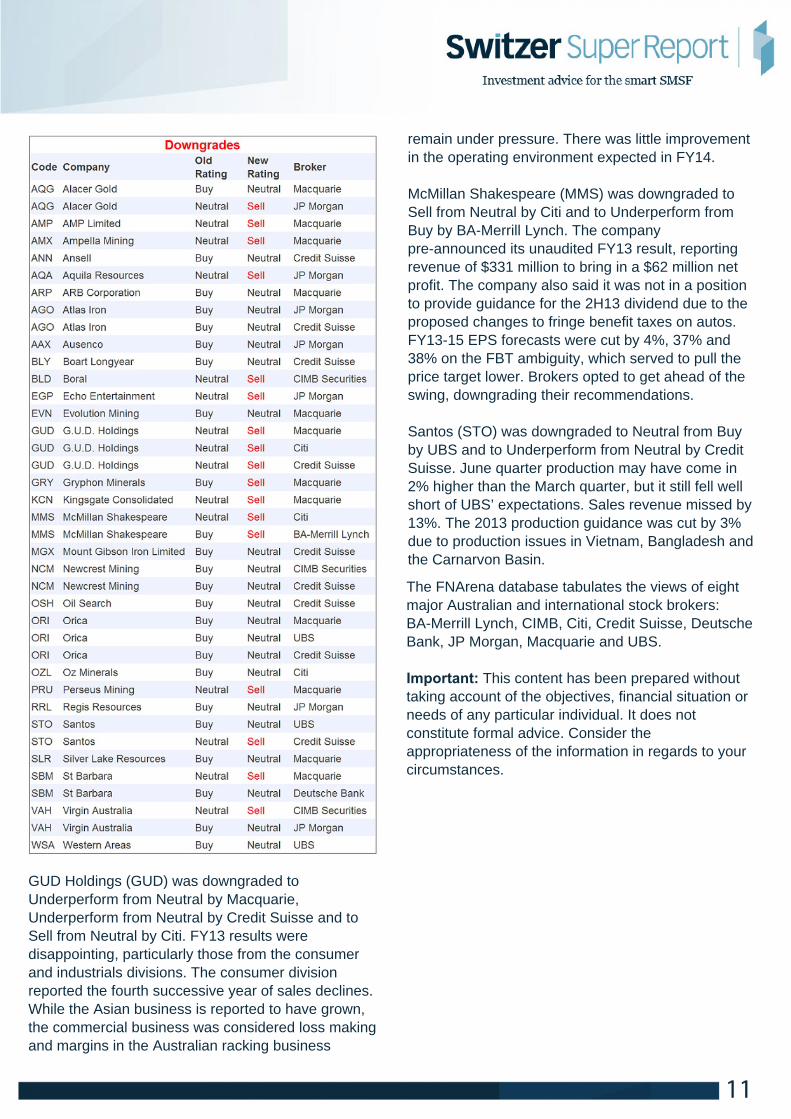

Buy, Sell, Hold – what the brokers say

by Rudi Filapek-Vandyck

Last week saw a number of fourth quarter and halfyear results from the materials space and analystswere not only met with below expectation reports, butalso the need to rebase estimates in the face of stillfalling prices for most commodities. Thus, the list ofdowngrades reads like a who’s who of the materialssector. Upgrades were dominated by CommonwealthBank’s proposals for its retail trusts.

In the good books

CFS Retail Property Trust (CFX) was upgraded toNeutral from Underweight by JP Morgan.Commonwealth Bank (CBA) has a proposal,incomplete, to internalise the management of bothCFS Retail and Commonwealth Property (CPA).There’s no word on the obvious question of price, butJP Morgan estimates the entire platform generates$70 million in annual earnings and could sell for $650million. JP Morgan said this is step one. Step twowould be for CBA to sell out of the real estateinvestment trusts. For the broker, this isgame-changing news. M&A activity is not seen likelyfor CFX, given four interested parties control

34%.

Commonwealth Property Office Fund (CPA) wasupgraded to Neutral from Underperform by Macquarieand to Overweight from Underweight by JP Morgan.Macquarie noted Dexus Property (DXS) has acquireda 14.9% interest in CPA by way of a forward contract.This revealed corporate appetite for CPA sooner thanexpected, after the announcement of a plannedinternalisation of management. The broker said that,whilst it could be difficult for competing bidders toenter the playing field and generate pricing tension,Dexus won’t necessarily be limited to paying thevalue of net tangible assets for CPA if it has thebacking of a wholesale capital provider.

Stockland (SGP) was upgraded to Buy from Neutralby UBS. The broker is expecting 8% EPS growth inFY14, which should flow through to an improvingDPS payout ratio. The broker also noted low interestrates are starting to feed housing activity, and aresilient retail portfolio. Non-discretionary retail andresidential are now preferred by the broker going intoreporting season, with SGP seen as a key pick in theAREIT sector.

In the not-so-good books

Atlas Iron (AGO) was downgraded to Neutral fromOverweight by JP Morgan and to Neutral fromOutperform by Credit Suisse. Guidance for FY14 wasunderwhelming, as it reflected reduced reserves and

10

a shortened mine life at Pardoo. There is alsosignificant uncertainty about how Atlas will unlock the

value of its port allocation beyond Horizon 1.

GUD Holdings (GUD) was downgraded toUnderperform from Neutral by Macquarie,Underperform from Neutral by Credit Suisse and toSell from Neutral by Citi. FY13 results weredisappointing, particularly those from the consumerand industrials divisions. The consumer divisionreported the fourth successive year of sales declines.While the Asian business is reported to have grown,the commercial business was considered loss makingand margins in the Australian racking business

11

remain under pressure. There was little improvementin the operating environment expected in FY14.

McMillan Shakespeare (MMS) was downgraded toSell from Neutral by Citi and to Underperform fromBuy by BA-Merrill Lynch. The companypre-announced its unaudited FY13 result, reportingrevenue of $331 million to bring in a $62 million netprofit. The company also said it was not in a positionto provide guidance for the 2H13 dividend due to theproposed changes to fringe benefit taxes on autos.FY13-15 EPS forecasts were cut by 4%, 37% and38% on the FBT ambiguity, which served to pull theprice target lower. Brokers opted to get ahead of theswing, downgrading their recommendations.

Santos (STO) was downgraded to Neutral from Buyby UBS and to Underperform from Neutral by CreditSuisse. June quarter production may have come in2% higher than the March quarter, but it still fell wellshort of UBS’ expectations. Sales revenue missed by13%. The 2013 production guidance was cut by 3%due to production issues in Vietnam, Bangladesh andthe Carnarvon Basin.

The FNArena database tabulates the views of eightmajor Australian and international stock brokers:BA-Merrill Lynch, CIMB, Citi, Credit Suisse, DeutscheBank, JP Morgan, Macquarie and UBS.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

Sydney still the star

by Penny Pryor

Residential sales activity might be cooling off in otherstates but not Sydney, after it also enjoyed anunseasonably warm Saturday, which may haveprompted another auction clearance rate of over80%.

The auction clearance rate in Sydney was 80.6%according to RP Data and 80.8% according to APM’sstatistics (see table 1 below). The weather reached abalmy 18.7 degrees.

The combined capital city auction clearance rate wasdown slightly to 64% over the week from 65.4% theprevious week (see graph 1 below), but the trend isstill moving in an upward direction.

Melbourne might not look so crash hot next toSydney, but an auction clearance rate of 70.2% isnot bad. The updated data for the previous week hadSydney’s clearance rate slip back to 78.5% andMelbourne come in at 68% (see table 2 below).

But both results are not too bad given that this timelast year both cities had auction clearance rates ofunder 60% (see table 3 below).

The most expensive property sold at auction over theweekend was not in Sydney but Melbourne, where afour-bedroom house in Middle Park (about 6km southof the CBD) was auctioned for just over $3 million.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

12

Did you know?

You should know by now that I am pretty upbeat on this rally, but I always listen to those with a different view. Inthis case that would be Switzer Super Expert Roger Montgomery. I spoke to him on Switzer TV last week.