issue 23 january 2014 india watch - grant thornton...

TRANSCRIPT

India WatchISSUE 23 JANUARY 2014

In association with

Welcome to the Winter edition ofGrant Thornton’s India Watch, in associationwith the London Stock Exchange

After a mixed year for India’s economy in 2013, the upcoming elections are set to play a pivotal role.

Our guest contributor, Ibukun Adebayo, Co-Head of Emerging Markets at the London Stock Exchange, outlines that private Indian companies should take advantage of the two year window offered by the Finance Ministry to raise equity capital on overseas exchanges by issuing and listing depository receipts, without a prior or simultaneous listing at home. He also highlights the not so obvious benefits of international listings for Indian companies.

Lastly, we review whether tax is a deterrent for investments in India, discussing the latest Indian tax developments and how they may affect your investments.

If you would like to discuss any of the matters arising in this issue or how Grant Thornton’s South Asia group can help you please contact us.

In this issue we highlight that the Grant Thornton India Watch Index underperformed in 2013, echoing India’s economic performance. The Index fell by 23% in 2013 compared with an increase of 14.4% in the FTSE 100, whilst the FTSE AIM All Cap Asean was flat. The Index witnessed a significant fall in Q4 as compared to the modest drop seen in the previous three quarters of 2013. Continuing investor concerns on the macro economic situation plus issues of policy paralysis, combined with failure by some companies to deliver has led to the general underperformance of the index for the full year.

India M&A remains resilient despite one of the most uncertain years in recent times. The last quarter of 2013 showed a similar deal-volume run-rate to the first three quarters combined, adding 123 deals to the 377 at the end of Q3 to close the year with 500 deals. Overall PE activity, both value and volumes, was strong making up for some of the drop seen in corporate M&A activity during the year.

We take a look at the performance of the Indian economy over the past year as well as look forward to what we can expect in 2014.

Anuj Chande Partner, Corporate Finance and Head of South Asia GroupGrant Thornton UK LLPT +44 (0)20 7728 2133 E [email protected]

Arjun MehtaDirectorGrant Thornton Advisory Private LimitedT +91 124 4628 000E [email protected]

2

India Watch - Issue 23 January 2014

Grant Thornton India Watch Index underperformsin 2013 echoing India’s economic performance The Grant Thornton India Watch Index fell by 23% in 2013 compared with an increase of 14.4% in the FTSE 100 whilst the FTSE AIM All Cap Asean was flat. The Index witnessed a significant fall in Q4 as compared to the modest drop seen in the previous three quarters of 2013 - 1.9%, 1.5% and 3.4% respectively. Continuing investor concerns on the macro economic situation plus issues of policy paralysis, combined with failure by some companies to deliver has led to the general underperformance of the index for the full year.

7075

808590

95

100105

110

115

120

125130135140

145

Dec-13Nov-13Oct-13Sep-13Aug-13Jul-13Jun-13May-13Apr-13Mar-13Feb-13Jan-13

–– GT India Watch – ALL

–– GT India Watch – smaller caps

–– FTSE 100

–– FTSE All Cap Asean

–– FTSE AIM All Share

–– FTSE AIM 100

–– FTSE AIM 50

Source: Factset

Investors continued to remain cautious in Q4 due to stubbornly high inflation and the political uncertainty surrounding general elections due in May 2014. However, December registered an uptick in the Index as markets reacted relatively

calmly to the US Federal Reserve’s decision to taper its expensive quantitative easing programme and the Reserve Bank of India keeping the repurchase (repo) lending rate steady.

3

India Watch - Issue 23 January 2014

Winners and losers in the quarter There was good news for Kolar Gold as it gained 41% in the quarter. In October, the company announced that the Jonnagiri Mining Lease had been granted by the Andhra Pradesh Government to the company’s partner Geomysore Services India Private Limited (GMSI). Kolar Gold holds a 30% equity interest in GMSI and therefore in all of its gold projects, including the Jonnagiri Gold Project in India.

DQ Entertainment, an animation, gaming, live action, entertainment production and distribution company, increased by 35%. In November, the company was engaged by Wild Canary, USA, to produce ‘Miles from Tomorrowland’ for Disney Jr. It appears that investors anticipate the company to continue to win new production contracts to increase profitability, which has been reflected in the share price.

The energy sector saw mixed results. Greenko, the Indian developer, owner and operator of clean energy projects, reported solid results for the six months to September 2013, increasing their share price by 38% in Q4. Revenue increased by 32.4% and adjusted EBITDA grew by 67% in constant currency terms. The company added 183MW of operational wind capacity in the last six months.

Whereas Essar Energy, the India-focused integrated energy company, was not that fortunate and faced further delays in approvals in the power business in India. Further, Essar Oil (part of Essar Energy) reported a lower gross refining margin for the July - September quarter

leading to investors raising concerns around the balance sheet. The management is taking action to address its debt position, which is likely to require co-operation and negotiation with a number of Indian and overseas lenders. Essar Energy was down 44% in the quarter.

Nandan Cleantec, a vertically integrated bio fuel producer, was down 35% in the quarter. The company’s results for the year to June 2013 reflected the delay in implementing operations at the Vizag refinery. Funding was still to be formally agreed and the auditors had qualified the accounts in reflection of this. However, a successful resolution of the funding and operational issues could lead to a substantial increase in share price.

OutlookEvidently, there are various challenges facing the Indian economy in 2014. However, we anticipate there will be more clarity on the country’s future economic policy subsequent to the general elections and we continue to remain positive on the long term outlook for Indian companies.

Anuj ChandePartner, Corporate Finance and Head of South Asia GroupGrant Thornton UK LLPT +44 (0)20 7728 2133 E [email protected]

Vishal JainAssociate Director, Corporate FinanceGrant Thornton UK LLPT +44 (0)20 7865 2269E [email protected]

* The India Watch Index consists of 31 Indian companies listed on AIM or the Main Market (excluding GDRs). We only consider companies to be Indian if they are domiciled in India and/or foreign companies holding Indian assets or Investment companies with Indian promoters. The index has been created via Factset and is weighted by Market Value. To avoid distortion of index trends, the two largest market cap entities, Essar Energy and Vedanta Resource, are excluded.

** Note that we have removed Photon Kathaas Limited (delisted) and Eros (moved to the NYSE) from the Index.

4

India Watch - Issue 23 January 2014

Indian M&A remains resilient despite one of the most uncertain years in recent times

India M&A remains resilient, despite India’s economy slowdown. The last quarter of 2013 showed a similar deal-volume run-rate to the first three quarters combined, adding 123 deals to the 377 at the end of Q3 to close the year with 500 deals.

Deal Summary Volume Value (US$ billion)

2011 2012 2013 2011 2012 2013

Domestic 216 234 220 5.04 6.08 5.75

Cross border 288 262 221 39.58 14.51 17.89

Mergers and internal restructuring 140 102 59 - 14.80 4.55

Total M&A 644 598 500 44.61 35.38 28.19

PE 373 401 450 8.75 7.38 10.39

Grand total 1,017 999 950 53.36 42.76 38.58

Cross border includes

Inbound 142 140 139 28.73 5.96 8.64

Outbound 146 122 82 10.84 8.55 9.25

Overall PE activity, both value and volumes, was strong making up for some of the drop seen in corporate M&A activity during the year. Inbound deal volume for the year remained at levels seen in previous years but with a substantial jump in deal value, although the weaker rupee appears to have curtailed Indian appetite to acquire overseas.

Deal summary in 2013With 500 deals amounting to US$28.19 billion, the Indian M&A market showed subdued levels of deal activity in 2013, lower both in volume and value, when compared to 2011 and 2012.

Overall M&A values dipped by 20% year-on-year coupled with a 16% decline in the number of

deals. However, if we take into account the large US$12 billion Vedanta group restructuring deal in 2012 (excluding mergers and internal restructuring deals), M&A values were actually up 15% during 2013. This translates to a fairly resilient performance given the backdrop of the Indian economy in 2013. That said, we are yet to see the levels of activity seen in 2010 or 2011.

It is interesting to see a continuously declining trend in outbound deal volumes between 2011 and 2013. However, overall deal values have remained steady largely due to the big ticket deals seen in ONGC’s outbound oil block acquisitions totalling over US$5 billion.

5

India Watch - Issue 23 January 2014

On the other hand, inbound M&A deal values have not been able to get back to earlier levels, though deal volume has remained steady possibly due to the drying up of blockbuster billion-dollar plus deals during the year. Slated to be one of the largest deals of the year, the US$2.5 billion deal between Apollo Tyres and Cooper Tyre & Rubber was called off just a few days before it’s closure. Although it was to be the biggest deal in the history of the Indian Automotive industry, the impassable differences between the two companies led to the deal falling through.

2013 witnessed five M&A deals valued at over a billion dollars each, compared to four in 2012, although this is a sharp drop from the 10 deals we saw in 2011.

Topping the M&A deal list during the year was Unilever’s stake increase in Hindustan Unilever for US$3.1 billion followed by ONGC’s Rovuma oil block acquisitions for over US$2.5 billion each. Unilever’s open offer was the largest such deal in the history of India’s capital markets.

Sectors to watch continue to be pharma and aviation. The drug deficit in the global pharmaceutical industry (mainly in the US) is one of the principal drivers of Pharma M&A in Indian companies, especially for those with USFDA approved facilities. The drying up of the R&D pipeline globally coupled with the expected patent cliff in the US drug market in the next two to three years and the constant pressure on manufacturing cost reduction will make India a sought after manufacturing destination.

The recent approval of the Jet-Etihad deal by the fair trade regulator Competition Commission of India (CCI) is a welcome sign for many more deals after the government of India relaxed FDI rules in the aviation sector in 2012.

Top M&A sectors in 2013

Top M&A deals in 2013

Acquirer Target Sector US$ million Deal type

Unilever Plc Hindustan Unilever Limited FMCG, Food & Beverages 3,092.5 Increasing stake to 67.26%

ONGC Videsh Ltd Rovuma Area 1 Offshore Block Oil & Gas 2,640.0 Minority stake

Oil India Ltd, ONGC Videsh Ltd Rovuma Area 1 Offshore Block Oil & Gas 2,475.0 Minority stake

Mylan Inc Agila Specialties Pvt Ltd (Strides’s injectable business) Pharma, Healthcare & Biotech 1,800.0 Acquisition

Vodafone International Holdings B.V. Vodafone India Limited Telecom 1,640.8 Increasing stake to

100%

Amtek Auto Ltd Neumayer Tekfor Group Automotive 665.0 Acquisition

UltraTech Cement Ltd Jaypee Cement's 5 MTPA Gujarat facility Cement 590.0 Majority stake

Ambuja Cements Holcim (India) Pvt Ltd holding arm of Holcim Cement 585.0 Internal restructuring

ONGC Videsh Ltd Parque das Conchas, Brazilian oilfield Oil & Gas 529.0 Increasing stake to 27%

Cipla Ltd Cipla Medpro Pharma, Healthcare & Biotech 512.0 Acquisition

Oil & Gas [20%]

Pharma, Healthcare & Biotech [15%]

FMCG, Food & beverages [12%]

Telecom [9%]

Power & Energy [5%]

Automotive [5%]

Cement [5%]

Real Estate [5%]

IT & ITeS [5%]

Others [19%]

6

India Watch - Issue 23 January 2014

Atul MongaAssociate Director Grant Thornton UK LLPT +44 (0)20 7865 2534E [email protected]

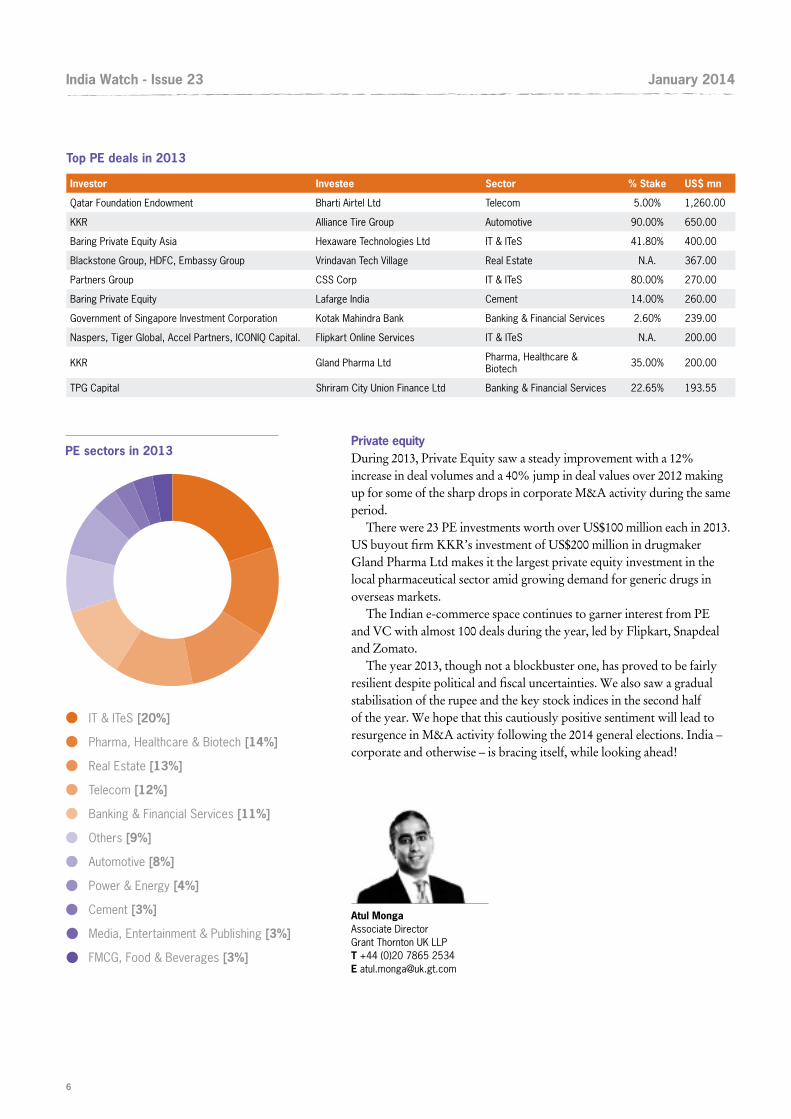

PE sectors in 2013

Top PE deals in 2013

Investor Investee Sector % Stake US$ mn

Qatar Foundation Endowment Bharti Airtel Ltd Telecom 5.00% 1,260.00

KKR Alliance Tire Group Automotive 90.00% 650.00

Baring Private Equity Asia Hexaware Technologies Ltd IT & ITeS 41.80% 400.00

Blackstone Group, HDFC, Embassy Group Vrindavan Tech Village Real Estate N.A. 367.00

Partners Group CSS Corp IT & ITeS 80.00% 270.00

Baring Private Equity Lafarge India Cement 14.00% 260.00

Government of Singapore Investment Corporation Kotak Mahindra Bank Banking & Financial Services 2.60% 239.00

Naspers, Tiger Global, Accel Partners, ICONIQ Capital. Flipkart Online Services IT & ITeS N.A. 200.00

KKR Gland Pharma Ltd Pharma, Healthcare & Biotech 35.00% 200.00

TPG Capital Shriram City Union Finance Ltd Banking & Financial Services 22.65% 193.55

IT & ITeS [20%]

Pharma, Healthcare & Biotech [14%]

Real Estate [13%]

Telecom [12%]

Banking & Financial Services [11%]

Others [9%]

Automotive [8%]

Power & Energy [4%]

Cement [3%]

Media, Entertainment & Publishing [3%]

FMCG, Food & Beverages [3%]

Private equityDuring 2013, Private Equity saw a steady improvement with a 12% increase in deal volumes and a 40% jump in deal values over 2012 making up for some of the sharp drops in corporate M&A activity during the same period.

There were 23 PE investments worth over US$100 million each in 2013. US buyout firm KKR’s investment of US$200 million in drugmaker Gland Pharma Ltd makes it the largest private equity investment in the local pharmaceutical sector amid growing demand for generic drugs in overseas markets.

The Indian e-commerce space continues to garner interest from PE and VC with almost 100 deals during the year, led by Flipkart, Snapdeal and Zomato.

The year 2013, though not a blockbuster one, has proved to be fairly resilient despite political and fiscal uncertainties. We also saw a gradual stabilisation of the rupee and the key stock indices in the second half of the year. We hope that this cautiously positive sentiment will lead to resurgence in M&A activity following the 2014 general elections. India – corporate and otherwise – is bracing itself, while looking ahead!

7

India Watch - Issue 23 January 2014

Overview of the Indian economy in 2013

In this economic update we take a look at the performance of the Indian economy over the past year as well as look forward to what we can expect in 2014. After a mixed year for India’s economy, the upcoming elections are set to play a pivotal role on clarifying the country’s future economic policy.

While official figures are not yet available with regard to the performance of India’s economy over the last quarter of 2013, it was reported in November that the economy expanded at an annual rate of 4.8% in the third quarter of 2013 (the second quarter of India’s fiscal year). This growth is up from 4.4% in the prior quarter and is faster than many analysts had forecast.

Notwithstanding this, India’s growth rate has remained below 5% for the preceding 12 months. In addition, the prior quarter’s growth rate of 4.4% was the lowest for four years. So, while an increase in growth is an extremely positive sign, consistent quarter-on-quarter growth and a strong economic recovery are far from guaranteed.

Inflation rates and the weakening rupee continued to hamper India’s growth in the second half of 2013. As at the end of the year, the rupee was down 11% against the dollar, a small recovery from its lowest point in the year but the decline made the currency one of

Asia’s worst performers in 2013. With regard to inflation, India’s battle became more challenging in December when a sharp increase in the cost of food drove the highest retail price rise on record. Retail inflation reached 11.24% in November from 10.7% in October on the back of these increased cost. The Reserve Bank of India have continued to increase interest rates to counteract rising inflation levels but poor economic output in conjunction with the depreciating value of the rupee are continuing to have a significant adverse effect on these counter measures.

With regard to India’s equity capital markets, the Sensex ended the year on a bullish note rising 17.8% in the last four months of the year. This significant year-end rise resulted in a 9% gain for the Sensex in 2013. In addition, the National Stock Exchange’s benchmark Nifty gained 6.7% over the period. Sharekhan, one of India’s largest broking houses, stated in a note that, “Just like [at the beginning of] 2013, the market is high on hopes again. The hopes this time around

8

India Watch - Issue 23 January 2014

Arjun MehtaDirectorGrant Thornton Advisory Private LimitedT +91 124 4628 000E [email protected]

are pinned on the economy bottoming out and corporate earnings improving”. The increasing likelihood of a pro-business BJP government coming into power in May 2014 has also undoubtedly spurred the markets.

Overall, 2013 was a very mixed year for India’s economy. While equity capital markets saw growth over the period, disappointing economic output, the nation’s battle with inflation and the rupee’s depreciation continued.

So what does 2014 have in store for India’s economy? With the elections in May, India’s economy is expected to be played out in two parts this year. Little to no economic policy changes are expected before the elections are concluded, which is likely to result in further low growth during the period. However, as the elections come to an end, further clarity on the country’s future economic policy will be garnered. With the Prime Minister, Manmohan Singh, already announcing that he will not stay in the post if his party wins the election, hopes have been reinvigorated for effective fiscal policy change.

Questions will of course remain as to whether any new policy changes implemented by a new government will result in growth and greater inflation control. However, for India’s economy to rebound, clear and real fiscal changes need to be implemented and a revitalised government cannot come at a more suitable time.

Sources:BBCReutersLivemintEconomic Times

9

India Watch - Issue 23 January 2014

Unexpected Diwali giftIn a year when the Indian economy has grown at an unflattering 5%, when the rupee has depreciated by 10%, domestic IPOs have raised a mere US$340 million, depository receipt issues haven’t topped US$50 million, India Inc and its anxious private equity benefactors may well have set off a few extra fireworks last Diwali after the Finance Ministry rather unexpectedly opened a window that had been firmly shuttered since 2005.

Undoubtedly this decision has the potential to go a long way in providing a badly needed long-term financing option for private limited companies.

The not-so-obvious benefitsWhile most of the benefits of an international listing for Indian companies are self-evident (improved valuations, capital availability, liquidity, acquisition currency, higher profile, etc), the choice of listing venue can bring incremental perks. For instance a London listing: • enables the financing of a company through the various

stages of its life cycle with a relatively easy process to make follow-on offers

• allows the choice of the right market for the right company in a cost effective manner. One size doesn’t fit all in London, hence AIM, the Professional Securities Market and the Specialist Fund Market to complement the Main Market

• accommodates offers and securities of varying complexities

• targets investors beyond the usual FII audience • allows the possibility of FTSE index inclusion• enables the adoption of the highest standards of corporate

governance.

London is ready…The Indian government’s decision to allow private companies to IPO abroad has coincided with a notable upsurge in London IPOs and further offers. In 2013 alone, over US$18 billion has been raised in more than 90 IPOs on the Main Market and on AIM. Institutional investor appetite in London is good, especially for robust foreign paper.

…but India may not beThough the Finance Ministry’s announcement was made at the end of September, final clarity and go-ahead on the new policy is still awaited. The Sahoo Committee‘s report on Depository Receipts and Convertible Bonds has been submitted to the Finance Ministry but is yet to be made public and further measures if any, are yet to be announced. Meanwhile India Inc is still nervous about international investor interest; a recent record breaking rally in the Sensex was limited to a few blue chips (and in dollar terms the market cap of the Sensex is actually quite a way from it’s highest ever value). Moreover, political and economic uncertainty persist as the country heads cautiously towards general elections in May. So it is unlikely that we will know whether 2014 will be the year for Indian overseas issues until the second half of the year is upon us.

Ibukun AdebayoCo-Head Emerging MarketsEquity Primary MarketsLondon Stock Exchange GroupT +44 (0)20 7797 1085E [email protected]

Overseas listings open up again for Indian private companies

Private Indian companies should take advantage of the two year window offered by the Finance Ministry to raise equity capital on overseas exchanges by issuing and listing depository receipts, without a prior or simultaneous listing at home. But don’t expect a deluge. At least not just yet.

10

India Watch - Issue 23 January 2014

Is tax a deterrent for foreign investment in India?

The assessment of the tax cost of doing business in India is important for foreign investors. In this article we discuss the latest developments that could potentially prompt a reconsideration of the costs and benefits of doing business in and with India.

Tax disputes continue to increase on subjects that sometimes defy logic: taxability of indirect transfer of shares, adjustment of notional interest on the undervalued amount of a share price as well as new discoveries such as adjustments on advertisement, marketing and promotion expenditure or controversial software taxation. On-going tax amendments and notifications limiting possible tax benefits are adding to the challenge of operating in India without additional levies.

Cyprus specified as Notified Jurisdictional Area (NJA)In November 2013, the Indian government notified Cyprus as a NJA due to a lack of effective information exchange requisitioned by the Indian tax authorities – Indian tax laws contain the provisions for notifying the delinquent jurisdictions and penalising the transacting parties through levy of higher tax rates. The Cypriot government responded to this notification by issuing a statement that it is addressing, in consultation with the Indian government, the issues of effective information exchange and the long standing demand for re-negotiation of the India-Cyprus tax treaty so that Cyprus attains ‘compliant’ status.

The two governments reached a resolution; Cyprus continues to be black-listed, meaning the following tax consequences in India:• transfer pricing regulations apply to all

transactions undertaken with any person located in Cyprus

• a person paying to another located in Cyprus is not allowed a tax deduction in the absence of prescribed documents and information

• payments to a person located in Cyprus attract a minimum withholding tax of 30%

• receipts from a person located in Cyprus are deemed as income of the recipient unless the recipient satisfactorily explains the source of such receipts.

For existing Cypriot investors, all of the above would mean maintenance of robust documentation, additional compliance obligations and higher tax outflows for the group as a whole.

Furthermore, Cypriot companies are currently exempt from capital gains taxation on capital gains earned on the sale of the Indian company’s shares because of a favourable capital gains article in the India-Cyprus tax treaty. This might change in the future given that the treaty is under renegotiation and that may lead to inclusion of a clause limiting such benefits to only few specified cases.

11

India Watch - Issue 23 January 2014

Prospective investors with Cypriot structures should thoroughly evaluate the reasons compelling them to route their investments through Cyprus before actualising their investment path.

Reigniting controversy on software taxationThe debate on taxability and consequent tax withholding on software payments resurfaced recently with Nokia India’s case. The tax authorities alleged that Nokia India was under obligation to withhold tax on payments to Nokia Finland for software downloaded onto its handsets, manufactured in India, since these payments are the royalty for the right to use copyright, on which tax was required to be withheld. Nokia India held a contrary view. Nokia’s case, which is pending adjudication at the higher appellate forums, is in the spotlight because of the quantum of tax bill raised on Nokia.

Since the Indian Courts (particularly High Courts, second to the Supreme Court) have pronounced conflicting judgments, software taxation remains unresolved and litigation is continuing.

Therefore, taxpayers entering into cross-border transactions of any nature should thoroughly examine all the possible tax levies since the tax authorities are aggressively scanning these deals or transactions.

The abovementioned cases and a number of other tax disputes revealed in 2013 that the Indian government and the tax authorities have a tough stance on matters of alleged tax evasion and non-compliances. However, such a stance should not discourage investors to enter the country. We advise investors to ensure that their organisation structuring meets the business justification and entails commercial substance. Cross border transactions are completely examined for any tax levies.

Nidhi GuptaAssociate DirectorWalker Chandiok & AssociatesE [email protected]

© 2014 Grant Thornton UK LLP. All rights reserved.

‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires.

Grant Thornton UK LLP is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another’s acts or omissions.

This publication has been prepared only as a guide. No responsibility can be accepted by us for loss occasioned to any person acting or refraining from acting as a result of any material in this publication.

grant-thornton.co.uk

V23677

About Grant Thornton UK LLPGrant Thornton UK LLP established a dedicated South Asia Group in 1991 to serve Asian owned businesses in the UK as well as those investing into and from the Indian subcontinent. We are proud to be one of the first UK accountancy firms to focus on this region.

We are widely recognised as one of the leading international firms advising on India-related matters and have been in involved in every IPO involving an Indian company on AIM, with the exception of the real estate sector.

For those clients requiring advice in both the UK and India we offer a seamless service building on the already strong and close relationship between Grant Thornton UK LLP and Grant Thornton India.

About Grant Thornton India LLPGrant Thornton India LLP is one of the oldest and most prestigious accountancy firms in the country. Today, it has grown to be one of the largest accountancy and advisory firms in India with nearly 1,000 professional staff in New Delhi, Bangalore, Chandigarh, Chennai, Gurgaon, Hyderabad, Kolkata, Mumbai and Pune, and affiliate arrangements in most of the major towns and cities across the country.

The firm’s mission is to be the adviser of choice to dynamic Indian businesses with global ambitions – raising global capital, expanding into global markets, adopting global standards or acquiring global businesses.

International and emerging markets blogAs part of our commitment to remaining at the forefront of changes and developments in regards to UK-India relationship we will be using this space to post original thought leadership and research relevant to the industry. The idea is to encourage discussion around these issues and to open up new areas and debate.

To participate: www.grant-thornton.co.uk/thinking/international-markets

More information about our South Asia Group can be found at: www.grant-thornton.co.uk/sectors/emerging-markets/south-asia