issue is there a “roth 401(k) or 403(b)” in your future?

TRANSCRIPT

Congressional Outreach....... 3

Hybrid Pension Plans........... 4

Cash Balance Br ief ing........ 5

IRS “Best Practices” Memo ... 6

Interprofessional Activities ... 8

New ASPA Board Members ..... 15

DOL Bluepr int...................... 29

Membership Survey............ 30

Focus on CE.......................... 31

Focus on ASPA PERF........ 32

Focus on E&E....................... 33

Calendar of Events............. 35

PIX Digest ............................. 36

WASHINGTON UPDATE

Continued on page 27

IN THIS ISSUE

March

Madnessby Brian H. Graff, Esq.

Actuaries, Consultants, Administrators and Other Benefits Professionals

Is There A “Roth 401(k)

Or 403(b)” In Your

Future?by Steven Oberndorf, Esq. and Richard Hochman, APM, Esq.

Vol. XXIX, Number 2 March-April 1999

Other Highlights of the “Retirement Savings

Opportunity Act of 1999”

Other changes that the Senator from Delaware would like to seeinclude:

• increased annual pre-tax contribution limits for 401(k) plans,403(b) plans, SIMPLE plans, and IRAs;

Senate Finance Committee Chairman William V. Roth, Jr. (R-DE) is hard at work again. The father of the

popular Roth IRA and proponent of increased saving forretirement wants to give individuals the option of payingtaxes on their contributions to 401(k) plans. In return forpaying taxes up front on the contributions, the 401(k) planwould resemble a Roth IRA. This results in earnings being

sheltered from current taxation and being withdrawntax-free upon distribution. Tax-sheltered 403(b) ar-rangements also will be eligible to take advantage ofthe Senator’s proposal that he titled the “RetirementSavings Opportunity Act of 1999” (another hard topronounce acronym – RSOA ‘99).

The phrase doesn’t just apply tocollege basketball. Now that the im-peachment trial is over, Members ofCongress from both sides of the aisleare chomping at the bit to introduce leg-islation affecting pensions. In addition,the Federal agencies are soon expectedto release a flurry of important guidance.There is a lot going on, and you can be

2 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

American Society of Pension Actuaries, Suite 820, 4350 North Fairfax Drive, Arlington, Virginia 22203-1619Phone: (703) 516-9300, Fax: (703) 516-9308, E-mail: [email protected], World-Wide Web: http://www.aspa.org

The Pension Actuary is produced by the executive director and Pension Actuary Com-mittee. Statements of fact and opinion in this publication, including editorials and letters tothe editor, are the sole responsibility of the authors and do not necessarily represent theposition of ASPA or the editors of The Pension Actuary.

The purpose of ASPA is to educate pension actuaries, consultants, administrators, andother benefits professionals, and to preserve and enhance the private pension system as partof the development of a cohesive and coherent national retirement income policy.

Editor in ChiefBrian H. Graff, Esq.

Pension Actuary Committee ChairStephanie D. Katz, CPC, QPA

Pension Actuary CommitteeDonald MackanosChristine Stroud, MSPADaphne M. Weitzel, QPA

Managing EditorStephanie D. Katz, CPC, QPA

Associate EditorJane S. Grimm

Technical Review BoardLawrence Deutsch, MSPAKevin J. Donovan, APMDavid R. Levin, APMMarjorie R. Martin, MSPADuane L. Mayer, MSPANicholas L. Saakvitne, Esq.Mark Wincek, Esq.

Layout and DesignChip Chabot and Alicia Hood

Copy EditorAmy E. Emery

ASPA Officers

PresidentCarol R. Sears, FSPA, CPC

President-electJohn P. Parks, MSPA

Vice PresidentsCraig P. Hoffman, APMScott D. Miller, FSPA, CPCGeorge J. Taylor, MSPA

SecretaryGwen S. O’Connell, CPC, QPA

TreasurerCynthia A. Groszkiewicz, MSPA, QPA

Immediate Past PresidentKaren A. Jordan, CPC, QPA

Continued on page 12

• catch-up contributions to qualifiedplans and IRAs for older Ameri-cans;

• elimination of the 415(c) 25%compensation limit for definedcontribution plans;

• liberalization of the Roth IRA eli-gibility and promotion of IRAcontributions to employer plans;and

• increase of the full funding limitfor defined benefit plans.

Thrift Plans with a Twist: TheRoth 401(k) and Roth 403(b)?

The Senator’s description of the“Retirement Savings OpportunityAct of 1999” provides that employ-ers would have the option to let par-ticipants in employer-sponsored401(k) and 403(b) plans decidewhether they want to make their con-tributions on a before or after-taxbasis. If the decision is to allow af-ter-tax contributions, the plan wouldoperate much like an old-fashionedthrift plan but with a new twist. (Re-member, many of the earliest 401(k)

plans had their roots as after-tax thriftplans.) Taxes on earnings would notmerely be deferred until distribution,but they would never be taxed. Thiseffectively creates a “Super” RothIRA, because the higher qualifiedplan limit ($10,000 in 1999), insteadof the IRA annual limit ($2,000), de-termines the maximum annual con-tribution the individual personallymay make.

Unlike a Roth IRA, however, thequalified plan rules will continue toapply to these plans, and this raisesmore questions of how to administerthe plan than it answers. [See “Wash-ington Update” for answers to someof these questions.] For example, thebill’s summary notes that the mini-mum required distribution rules willcontinue to apply to the Roth 401(k)and 403(b) plans, but does not givedetails about which other qualifiedplan rules also will continue to ap-ply. These rules may prevent employ-ees from making their maximumemployee contribution for a givenyear, unless the antidiscriminationrules are adjusted for the shift from

pre-tax to after-tax contributions.Other questions, such as the follow-ing, need to be answered: Will theADP and ACP tests, as currently ap-plied, continue to limit how muchhighly compensated participants willbe able to defer? Will testing provi-sions and procedures be modified toaccommodate significant shifts ofcontributions from the ADP to theACP test? While the proposal infersthat existing plan distribution ruleswill continue to apply, can this be thecase? In profit-sharing plans after-tax money may be withdrawn with-out a holding period. Does this meanthat the after-tax 401(k) contributionswill be immediately eligible for with-drawal, or will a holding period simi-lar to a Roth IRA ultimately berequired? May participants completea Roth 401(k) “conversion” of cur-rent elective deferrals and earnings?If so, how can this be effected withinthe context of a qualified plan? (Thismay prove an especially thorny is-sue to quantify because of the meth-

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 3

Continued on page 17

FOCUS ON GAC

Developing a

Relationship with a

Congressional

Memberby Sarah E. Simoneaux, CPC

Continued on page 10

Before I spoke to Michelle, Iasked Brian to give me some politi-cal background on Breaux. As a reg-istered Republican with conservativeleanings, I wanted to make sure thatI did not alienate Senator Breaux, amoderate Democrat, or his staffer.Brian noted that Senator Breaux wassupported by unions, lower to middleincome families, public employeesand women.

I then asked Brian for informa-tion on what Michelle might want toknow and how I should representASPA’s position. He gave me theGAC summary of the differencesbetween SAFE and SMART and saidthat I should emphasize qualifiedplans over IRAs, repeal of top-heavyand the 25% limit, and SAFE as asmall plan DB alternative.

In my first conversation withMichelle, I told her about the localbusinesses, which I represented, and

that I “worked with small businessretirement plans”. I tried to avoidjargon, and even such words as “pen-sions” or “qualified plans”. We alsospoke about where she came from inLouisiana and how my husband andI fit into Louisiana, to try to developa personal tie, so that she would re-member me the next time she called.

I then asked if she had any spe-cific questions about retirement is-sues being raised by the commissionand Senator Breaux. She admittedthat she was new to the area, but hadread up on qualified plans. Shewanted to know about how “we” (notmeaning ASPA specifically, but re-ally small businesses in Louisiana)felt about adding “catch up” provi-sions to qualified plans and “giantIRAs” instead of expanding qualifiedthrough SAFE/SMART or 401(k)modifications.

Over one year ago, Senator John Breaux (D-Louisi- ana), a member of the Senate Finance Committee,

was appointed to a bipartisan commission studying retire-ment issues. He designated one of his newer staffers, MichellePrejean, to be responsible for the qualified plan issues raisedby the commission. Brian Graff called and asked me to speakwith Michelle about qualified plans in general and ASPA’spoint of view specifically.

Marching to

the Hillby Edward H. Thomson, III,MSPA, QPA

It is that time of year again. TheOctober 15 deadline haspassed and(hopefully) all the December 31,1997 cases have been shipped out thedoor to the plan sponsors for signa-tures. And, yes, it’s ASPA time. Thismeans two things - it is time for ourannual conference and time for thehearty few to march to the Hill tospeak with their respective Memberof Congress. I have been fortunateto have had the opportunity to be apart of the last four or five trips tothe Hill and have found them to be atthe least, interesting, and at best, alot of fun.

The first question is “What’s thepoint?” To start with, the “Point” isto begin a relationship with the Mem-ber. Whether it’s your Representa-tive or Senator, you want to havesomeone to contact when importantpension issues arise. All of the Mem-bers have a staff person assigned toemployee benefit issues. You aremost likely to meet with that personwhen you go to the Hill. “Why isthe staffer important?” Without thestaffer, you go nowhere. With all thepeople that are vying for theMember’s time, as well as all of theissues he must review and consider,the most important person to knowis the staffer assigned to your issue.The staffer is the filter through whichall information flows. The easiestway to get your issue to the top ofthe pile is through your relationshipwith that staffer. The Member isprobably not going to be in Wash-ington when we are there for our con-ference. He is usually back in his

4 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

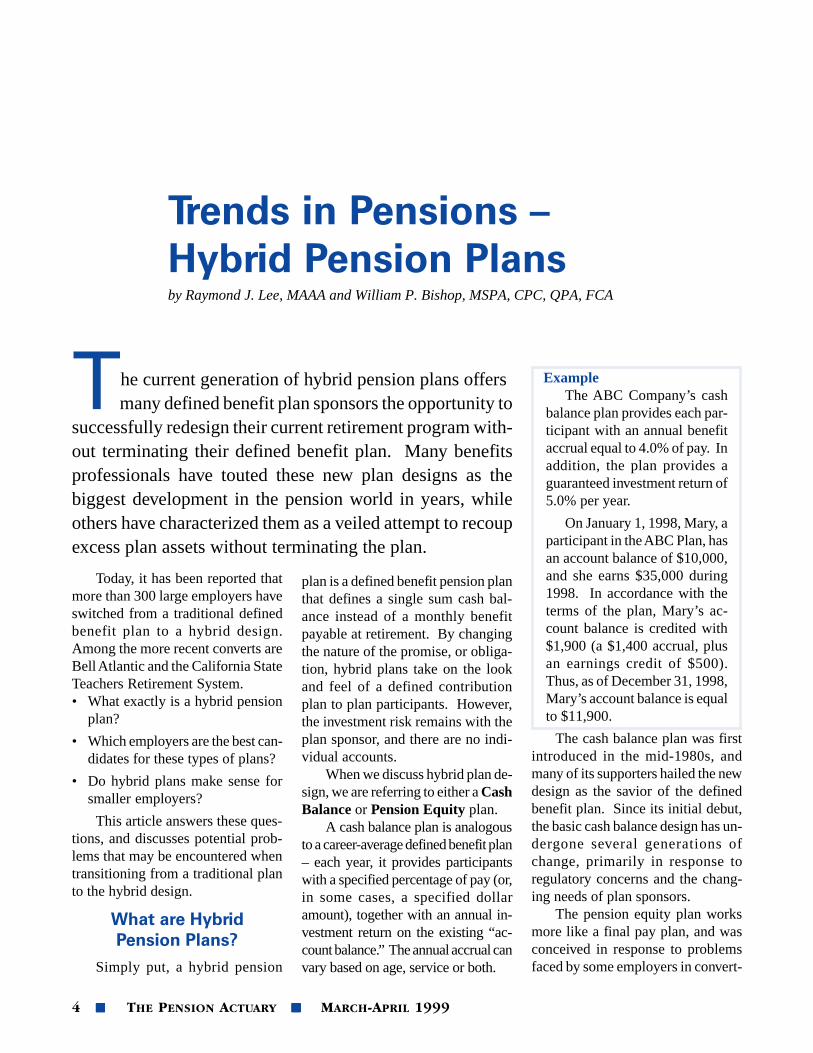

Trends in Pensions –

Hybrid Pension Plansby Raymond J. Lee, MAAA and William P. Bishop, MSPA, CPC, QPA, FCA

Today, it has been reported thatmore than 300 large employers haveswitched from a traditional definedbenefit plan to a hybrid design.Among the more recent converts areBell Atlantic and the California StateTeachers Retirement System.• What exactly is a hybrid pension

plan?

• Which employers are the best can-didates for these types of plans?

• Do hybrid plans make sense forsmaller employers?

This article answers these ques-tions, and discusses potential prob-lems that may be encountered whentransitioning from a traditional planto the hybrid design.

What are Hybrid

Pension Plans?

Simply put, a hybrid pension

plan is a defined benefit pension planthat defines a single sum cash bal-ance instead of a monthly benefitpayable at retirement. By changingthe nature of the promise, or obliga-tion, hybrid plans take on the lookand feel of a defined contributionplan to plan participants. However,the investment risk remains with theplan sponsor, and there are no indi-vidual accounts.

When we discuss hybrid plan de-sign, we are referring to either a CashBalance or Pension Equity plan.

A cash balance plan is analogousto a career-average defined benefit plan– each year, it provides participantswith a specified percentage of pay (or,in some cases, a specified dollaramount), together with an annual in-vestment return on the existing “ac-count balance.” The annual accrual canvary based on age, service or both.

ExampleThe ABC Company’s cash

balance plan provides each par-ticipant with an annual benefitaccrual equal to 4.0% of pay. Inaddition, the plan provides aguaranteed investment return of5.0% per year.

On January 1, 1998, Mary, aparticipant in the ABC Plan, hasan account balance of $10,000,and she earns $35,000 during1998. In accordance with theterms of the plan, Mary’s ac-count balance is credited with$1,900 (a $1,400 accrual, plusan earnings credit of $500).Thus, as of December 31, 1998,Mary’s account balance is equalto $11,900.

The cash balance plan was firstintroduced in the mid-1980s, andmany of its supporters hailed the newdesign as the savior of the definedbenefit plan. Since its initial debut,the basic cash balance design has un-dergone several generations ofchange, primarily in response toregulatory concerns and the chang-ing needs of plan sponsors.

The pension equity plan worksmore like a final pay plan, and wasconceived in response to problemsfaced by some employers in convert-

The current generation of hybrid pension plans offersmany defined benefit plan sponsors the opportunity to

successfully redesign their current retirement program with-out terminating their defined benefit plan. Many benefitsprofessionals have touted these new plan designs as thebiggest development in the pension world in years, whileothers have characterized them as a veiled attempt to recoupexcess plan assets without terminating the plan.

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 5

ing their final pay plans to accountbalance defined benefit plans. Ingeneral, a pension equity plan defineseach participant’s account balance asthe product of points earned duringthe participant’s career and a speci-fied percentage of his or her finalaverage pay at termination. Like acash balance plan, the points earnedunder a pension equity plan can varybased on age, service or both.

ExampleUnder the XYZ Company’s

pension equity plan, eachparticipant’s account balance isdefined as 10% of high five-yearaverage pay, multiplied by thepoints accumulated in accor-dance with the following sched-ule:

1 point per year of service up to10, plus

2.5 points for each year of ser-vice in excess of 10.

John, a participant in theXYZ Plan, has 18 years of ser-vice and final average pay of$35,000. His account balanceis equal to $105,000.

Target Market

Initially, the adoption of hybridplan designs was limited to large em-ployers in the finance and health careindustries. However, as the hybriddesign has matured and become moremainstream, its target market hasbecome defined more by the goalsand objectives of the individual spon-sor rather than by industry or plansize. Today, aside from the obviousemployer goals to attract and retainemployees, we believe there are sev-eral compelling reasons to introducethis concept to smaller employers –even those with 100 or fewer employ-ees.

Desire to manage interest rate riskWe are all well aware of the as-

set growth experienced by most re-

tirement plans due to the excellentreturns in the equity markets over thepast several years. During this pe-riod, however, defined benefit planliabilities have also increased sub-stantially due to falling interestrates1. Some plans that providesingle sum distributions have beenfaced with restrictions on these dis-tributions to restricted employees,while others have had to face unex-pected increases in their minimumcash contribution as a result of thedeficit reduction contribution re-quirements. Most plans have in-curred higher PBGC premiums.

For the typical rank-and-file em-ployee, the significant drop in inter-est rates has been an unappreciatedwindfall. Most employees are noteven aware of how valuable theirpension benefit is or how its valuechanges until they actually leaveemployment and apply for benefits.Compare this indifference with theattention paid to 401(k) plans.

The predictable response fromemployers is “Why bother with the fi-nancial uncertainties of maintaining adefined benefit plan when no one paysmuch attention to it anyway?”

The hybrid plan design allowsplan sponsors to mitigate the inter-est rate risk inherent in traditionalplans by defining the single sumamount rather than the monthly an-nuity. The hybrid design also lendsitself to easier communication of thebenefit to participants.

Desire to eliminate earlyretirement subsidies

Another example would be theemployer that originally establishedits plan with significant early retire-ment subsidies, perhaps with thefounders of the company in mind oras a means to turn the workforce overwithout forcing out the older, longservice employees. Times havechanged. Retirements are being post-

Continued on page 18

Cash Balance

Briefing on

Capitol HillBy Lisa Bleier, Esq.

On February 16, 1999 ASPAjointly hosted a briefing on CapitolHill to explain the basic workings ofa cash balance plan in response to sev-eral unfavorable articles in the press.Carol Sears, President of ASPA, spokeabout the benefits of a cash balanceplan option for small businesses. (Acopy of her speech is provided onpage 26.) Also speaking to the Con-gressional staffers were RonaldGebhardtsbauer and other experts.

Some Senators and Representa-tives are contemplating legislationwhich would require enhanced dis-closure in the case of a plan amend-ment reducing future benefit accrualsunder a defined benefit or moneypurchase plan, including conversionsto a cash balance plan. One optioncurrently being considered would beto amend ERISA section 204(h) torequire the employer to provide eachaffected employee with an individualstatement showing specifically howhis or her benefits would be affected.A second option being consideredwould be to require illustrative ex-amples of how various employees atdifferent ages and with varying yearsof service with the employer wouldbe affected by the plan amendment.

A second part of the legislationbeing considered would be to adjustthe timing of the advance notice be-fore a plan amendment reducing fu-ture benefit accruals takes effect.Currently, an employer need onlyprovide 15-day advance written no-tice to employees. Senators and Rep-resentatives are contemplatingincreasing the notice period to 30, orpossibly even to 60 days.

The Government Affairs Com-mittee is continuing to work with

Continued on page 26

6 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

IRS “Best Practices” Memo

Provides Guidance on EPCRSby C. Frederick Reish, APM, Bruce L. Ashton, APM, and Nicholas J. White, APM

Plan Document Failures UnderWalk-in CAP

The memo states that, in the caseof a plan document failure, if the plansponsor corrects the violation by theadoption of a model amendment or astandardized master or prototypeplan, the plan sponsor is not requiredto apply for a determination letterruling. However, if the plan docu-ment failure cannot or is not cor-rected by a model amendment orstandardized document, the plansponsor must submit a determinationletter application with the appropri-ate user fee. This means that the de-termination letter application should

not be filed in Cincinnati, as is theusual case. The determination letterapplication will be processed by thelocal Walk-in CAP Coordinator orthe local Revenue Agent who handlesthe Walk-in CAP application. At theconclusion of the case, the closingagreement and the favorable deter-mination letter will be issued to-gether.

Under ordinary circumstances, aplan is not required to obtain a fa-vorable determination letter from theIRS in order to be a qualified plan.The memo’s requirement of a deter-mination letter runs contrary to thisrule and effectively conditions relief

from plan disqualification underWalk-in CAP on applying for a de-termination letter (unless a modelamendment or standardized docu-ment is used).

These procedures will becomeincreasingly important as plans arereviewed and amended for the pro-visions of GATT, USERRA, SBJPAand TRA ‘97 (“GUST”). Presum-ably, non-amenders will be discov-ered in the course of preparing theGUST amendments. Under the newprocedures, in order to correct theplan document failure, the sponsors ofsuch plans will have to submit filingsfor Walk-in CAP, and those filings willneed to include determination letterapplications — unless the failure canbe corrected by adopting modelamendments or an approved proto-type plan document.

Plan Document FailuresDiscovered During TheDetermination Letter Process

The IRS memo also discussesthe situation where a plan documentfailure, for which no Walk-in CAPrequest has been filed, is discoveredduring the course of a determinationletter review. The memo instructsRevenue Agents that the proceduresto be used in this case depend on whodiscovers the failure.

If the IRS discovers the failure,it will be resolved under Audit CAP;therefore, the sanction structure in

The IRS formally established the Employee Plans Com-pliance Resolutions System (EPCRS), by consolidat-

ing APRSC, VCR, Walk-in CAP and Audit CAP as inte-grated programs in March 1998 (Rev. Proc. 98-22). InDecember 1998, the IRS issued a “best practices” memo asadditional informal guidance on: (1) plan document failuresunder Walk-in CAP (i.e., the failure of plan documents tocomply with current qualification requirements—also knownas “nonamenders”); (2) plan document qualification failuresdiscovered during the determination letter process; (3) IRSexaminations of plans submitted under Walk-in CAP; and (4)treatment of certain excise taxes under Walk-in and AuditCAP. (A copy of the IRS best practices memo may beobtained from the authors’ website at http://www.benefitslink.com/reish.)

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 7

Plan sponsors who havefiled determination letterapplications can resolvea later-discovered qualifi-cation failure under Walk-in CAP.

Continued on page 20

Section 15 of Revenue Procedure 98-22 will apply (that is, a negotiatedsanction based, at least partially, onthe taxes due if the plan were dis-qualified). This is not new. What isnew, however, is a previously unrec-ognized type of plan document fail-ure—a “minor” failure and theamount of the sanction for a “minor”failure. The memo states that, if theplan document failure is “minor,”there will be a ceiling on theamount of the Audit CAP sanctionof “no higher than the presump-tive amount that would apply if theWalk-in CAP Compliance Correc-tion fees were applied.” Thus, for“minor” violations, the sanctionwill be limited to a relatively smallamount, depending on the size ofthe plan. (For a plan, which cov-ers no more than 10 participants,the maximum sanction would be$2,000.)

Unfortunately, the memo fails todefine or give examples of a “minor”defect. Based on our experience, webelieve that a failure to timely amenda plan which has been updated forTRA ’86, but not for UCA ’92 orOBRA ’93, would be treated as mi-nor. This belief is based on informalconversations with IRS officials.

If the plan sponsor discovers theplan document failure and voluntar-ily discloses it to the IRS (i.e., to theRevenue Agent reviewing the deter-mination letter application), the casewill be handled under Walk-in CAP.Section 11.01(2) of Revenue Proce-dure 98-22 states the general rule thata submission under Walk-in CAP“may not be made as part of a deter-mination letter application.” Thememo changes this rule to allow theplan sponsor to “perfect” the deter-mination letter application into aWalk-in CAP submission by follow-ing the procedures set forth in Sec-tion 12 of Revenue Procedure 98-22.(The memo is not entirely clear aboutwhere the Walk-in CAP application

is to be filed; however, it would ap-pear to be with the Revenue Agentwho is reviewing the determinationletter application.) This is a signifi-cant departure from prior practice,since it permits, on a voluntary ba-sis, the immediate disclosure ofqualification failures during the de-termination letter process withoutfirst filing a Walk-in CAP submis-sion – although, of course, a Walk-in

CAP application must thereafter besubmitted.

This change makes it possible forplan sponsors who have filed deter-mination letter applications to re-solve a later-discovered qualificationfailure under Walk-in CAP, wherethey can take advantage of the re-duced Compliance Correction Fees.As part of this, the memo places apremium on careful review of theplan document—even after filing adetermination letter application—inorder to identify and correct qualifi-cation failures. Not doing so mayresult in the IRS discovering thequalification failure, and imposing asubstantial sanction under AuditCAP.

Audit Matters Under EPCRSWith respect to plan audits, the

memo instructs Revenue Agents that“neither a full nor limited scope ex-amination should be conducted onWalk-in CAP cases.” This instruc-tion is significant, because we areaware of cases in the past where planswhich had filed a Walk-in CAP ap-plication were subjected to audits as

part of the application process. Thiswas particularly likely to occur in theIRS’ Northeast District (Brooklyn).The memo now precludes this prac-tice and specifically acknowledgesthat “routine examinations of Walk-in CAP cases would have a negativeimpact on voluntary compliance.”

The memo does advise RevenueAgents to “review” (not examine)Forms 5500 to “confirm that there are

no additional significant prob-lems not identified in the submis-sion (e.g., a violation of thecoverage requirements).” Andthe memo gives two examples of“limited circumstances” in whichaudits under Walk-in CAP shouldbe made. These are: (1) wherethe IRS finds “an unrelated quali-fication failure from the face ofthe Form 5500 submitted with the

application”; and (2) where the IRSand “the plan sponsor cannot reachagreement with respect to the correc-tion of any [qualification] failure(s)or the amount of the compliance cor-rection fee.” Initiating an audit un-der these circumstances is not new;it is consistent with existing IRSpractice.

Finally, the memo discusses thedisclosure of compliance audit re-ports during an IRS audit. These re-ports are internal audit documents,generally prepared for larger plans ormultiemployer plans, where a law-yer, accountant, consultant or thirdparty administrator has reviewed thedocumentation and operation of theplan for compliance with the quali-fication rules. The IRS memo in-structs Revenue Agents to “notrequest copies of a plan sponsor’scompliance audit report.” (Appar-ently, in some IRS field offices, Rev-enue Agents have been routinelyrequesting copies of any complianceaudit report.)

8 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

ASPA’s Interprofessional

Activities –

Are They Worth It?by Karen A. Jordan, CPC, QPA

If you are neither an actuary noron ASPA’s board of directors, youmight not even be aware of the ex-tent that ASPA is involved in theseactivities. You could begin by open-ing up your latest Yearbook and re-viewing the following sections:

• ASPA Representatives onIntersocietal Groups

• Council of Presidents

• Code of Professional Conductfor Actuaries

• Working Agreement

The first thing you should lookat is the Working Agreement, whichis located toward the end of the Year-book. This document sets forth thecooperative goals of the NorthAmerican actuarial organizations. Asexplained in its preamble, the Work-ing Agreement is intended to facili-tate the participating organizations’efforts to increase the quality and

variety of educational and profes-sional opportunities available toNorth American actuaries. Its otherpurpose is to eliminate unnecessaryduplication of activity between thevarious organizations, thereby mak-ing more efficient use of the partici-pating organizations’ resources.

The Working Agreement also ex-plains the role and makeup of theCouncil of Presidents. By the way,this organization is often referred toas COP/COPE because it includesthe presidents-elect of each organi-zation, as well as the respective presi-dents. If you review the section onthe Council of Presidents in theASPA Yearbook, you will see a shortdescription of each organization thatis included in the Working Agree-ment. You might be rather amazed tosee that there are, in fact, nine actu-arial organizations in North America.Five of them are in the United States.

Besides the commitments thatare defined by the Working Agree-ment, ASPA is also directly involvedwith the American Academy of Ac-tuaries (AAA). Each ASPA presidentand president-elect (along with thecounterparts of the other U.S. actu-arial organizations) sits on the boardof the AAA, as Special Directors.Furthermore, each actuarial organi-zation has certain AAA committeeslots that the organization is expected(or encouraged) to fill. If you lookin the Yearbook section titled “ASPARepresentatives of IntersocietalGroups,” you will see which commit-tees ASPA is currently staffing. TheASPA president appoints some ofthese positions, and the chair of therespective committee appoints oth-ers, usually with input from ASPA’spresident. If you are interested inlearning more about the various AAAcommittees, the best place to gain in-formation is to locate an AAA Year-book. If you want even moreinformation, you should feel free tocontact the ASPA committee repre-sentative listed in our Yearbook.

Also, as a result of our involve-ment with the AAA, there is usuallyat least one ASPA member servingon the Actuarial Board for Counsel-ing and Discipline (ABCD) and onthe Actuarial Standards Board(ASB). The presidents and presi-dents-elect of the participating orga-

ASPA devotes a significant amount of its resources (both monetary and human) to its interprofessional

activities with the other North American actuarial organiza-tions. The purpose of this article is to explain what ASPA’sinterprofessional activities entail, and to hopefully demon-strate how this time, effort and money benefit the ASPAmembership. As you read this article, keep in mind that thisis from the perspective of a non-actuary and represents onlyone person’s opinion.

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 9

nizations appoint these board mem-bers. ASPA always lists memberswho are on these two boards and whoalso are members of ASPA. So, if youhave questions about the ABCD orthe ASB, you could contact these in-dividuals.

ASPA’s commitment to theseinterprofessional activities is signifi-cant in both financial resources andhuman resources. In fact, there havebeen critics of our involvementwho feel that a major drawbackis the amount of time that ASPAleaders have to spend on these ac-tivities. These critics argue that thisinvolvement draws our leadersaway from other activities thatwould be more beneficial to ASPA.It is also argued that the financialcommitment (that is, paying the ex-penses of committee members whohave been asked to serve on behalfof ASPA) is too large. I have beenasked countless times by actuaries,as well as non-actuaries, if I felt thatit is worth this expenditure of ourlimited resources.

After my two years of participat-ing in Academy board meetings andtwo years of COP/COPE meetings,my opinion is that this involvementis extremely valuable for ASPA’s ac-tuarial members. I also believe thatthis involvement has brought valueto the organization as a whole, whichindirectly benefits ASPA’s non-actu-arial members. But, I also feel verystrongly that the leaders of ASPAmust continue to be vigilant in moni-toring the accompanying costs ofthese commitments and continuouslywork to keep the costs reasonable.

OK, so what value does all of thisbring to ASPA and its members?

For our actuaries, it brings sig-nificant value, such as:

• Involvement with the develop-ment and maintenance of theActuarial Code of ProfessionalConduct.

• Valuable input into the work-ings of the ABCD and the ASB.

• A way to demonstrate the valueof our organization to the actu-arial profession.

• Participation in the public re-lations efforts on the part of theactuarial profession.

• Coordination with the AAA inthe pension public policy area.

• Improved relations with theSOA in our shared duties withrespect to the Enrolled Actuar-ies examinations and the JointBoard.

• Input into the formation of Ac-tuarial Qualification Standards.

• International representationthrough the International Actu-arial Association.

• Methods to resolve cross-bor-der disciplinary actions.

However, as I stated above, thebenefits are not just for our actuarialmembers. The COP/COPE meetingsact very much like our own BusinessLeadership Conference, in that they aregreat forums to share information onhow to run successful professional so-cieties. I found the meetings to beextremely valuable in helping us makeASPA a better society. These meet-ings included comparing and sharinginformation about:

• computer software,

• administrative systems,

• education activities,

• strategic planning, and

• investing reserves.

But, there are other benefits too.The COP/COPE meetings also in-clude the executive directors of thevarious societies, and they havefound the time they have been ableto spend together to work on theircommon problems as very helpful.

We also have discovered areas ofmutual cooperation that havehelped us with various educationand examination issues. Finally,ASPA has been able to gain firsthand experience with the work-ings of the ABCD and the ASB,through our members who haveserved on these boards and ourleaders’ involvement on the AAAboard of directors. I believe thiswill be invaluable as we explorewhether we, as a society, are ready

to venture into the area of profes-sional standards for non-actuarialbenefits work, and the resulting dis-cipline process.

So, is it worth the time and ex-pense? Well, each person looking atthis issue will come up with a differ-ent answer I’m sure, but no one candeny that there are both benefits andcosts to this commitment. How valu-able are the benefits, in relation tothe costs? I would equate this analy-sis to trying to decide if public rela-tions efforts are “worth it.” Theanswer cannot be made on a purelyobjective basis, but I sincerely feelthat without this involvement, ASPAwould not be as good a society as itis and the cost has been minimal incomparison.

Karen A. Jordan, QPA, CPC, is theimmediate past president of ASPAand is co-owner of Alaska PensionServices, Ltd., of Anchorage, Alaska.

I sincerely feel that with-out this interprofes-sional involvement,ASPA would not be asgood a society as it is,and the cost has beenminimal in comparison.

10 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

Instead of getting into specificson SAFE/SMART or 401(k)s, I firsttalked about how IRAs are used byhigher income taxpayers and rarelyused by lower income constituents,especially by single mothers andworking women. I also spoke abouthow unions and public employeescontinue to support qualified plansover IRAs, viewing IRAs as notfavorable for rank and file mem-bers. I then spoke about the mostimportant issue for us and forBreaux: expanding retirement cov-erage among lower income work-ers and women, especially thosewho leave the workforce for a timeor are single parents. I explainedthat qualified plans, especiallyDB-type employer-paid plans likeSAFE, are great for lower incomeworkers and women who need to“catch up” after leaving theworkforce to raise children or takecare of aging parents. “Catch up”provisions are part of SAFE and arealso a reason for getting rid of the25% limit. I explained that the 25%of pay limit also hurt part-time work-ers and second income, lower paidworkers (i.e., women).

Had I been talking to a conserva-tive Republican member’s staffer, Iwould have emphasized how SAFEwas good for small business ownersand the necessity to preserve the quali-fied plan tax deduction for small busi-nesses. I would also have noted the

unfairness of the top-heavy rules andthe need for more simplification (i.e.,get rid of the multiple use test, althoughI would not have used those words) inthe overall qualified plan rules.

Michelle was extremely gratefulfor my input and has since called me

regularly when qualified plan issuescome up. Since she often would needinformation as Senator Breaux washeading to a meeting, I gave her myhome and cell phone numbers, aswell as my e-mail address, and en-couraged her to call me any time. Iwas always willing to drop whateverI was doing to talk to her and thatgave me a good deal of influence. Iftime permitted, I would call Brian toget the ASPA viewpoint before Icalled Michelle.

During every call, I wouldalso bring her up-to-date on localhappenings to cement the personalside of the relationship and alwaystried to give Breaux’s constituentviewpoint on a particular issue.She agreed to try to see me if shegot to New Orleans, and I plannedto visit her in Washington, DC.I recently spoke to Michelle, atBrian’s request, about the poten-tial DOL regulation requiring in-stitutional trustees for smallplans. I explained that ASPA haddrafted a letter to the DOL fromCongressional members, and Iwould like Breaux’s support andhis signature on the letter. Be-

fore I even had a chance to outlinethe issue, she said, “If you tell methat Senator Breaux needs to sign thisletter, just send it over and I will havehim sign it.” The relationship that Ihad developed with her meant she

C O N T I N U E D F R O M P A G E 3

Developing a Relationship with a

Congressional Member

Qualified plans, espe-cially DB-type em-ployer-paid plans likeSAFE, are great forlower income workersand women who needto "catch up" after leav-ing the workforce toraise children or takecare of aging parents.

Be sure to check the web site for the recent letter sent from ASPAregarding our comments on the issuance of Notice 98-52. This no-tice contained guidance on safe harbor 401(k) plans. The ASPA let-ter sent to Roger Kuehnle of the Employee Plans Division of the IRSproposes several changes to the guidance, including the flexibilityto choose the safe harbor option annually, a more simplified noticeto plan participants, the removal of the 4% cap on discretionarymatching contributions, and several other provisions.

ASPA GAC Issues a Comment Letter on IRS Notice 98-52

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 11

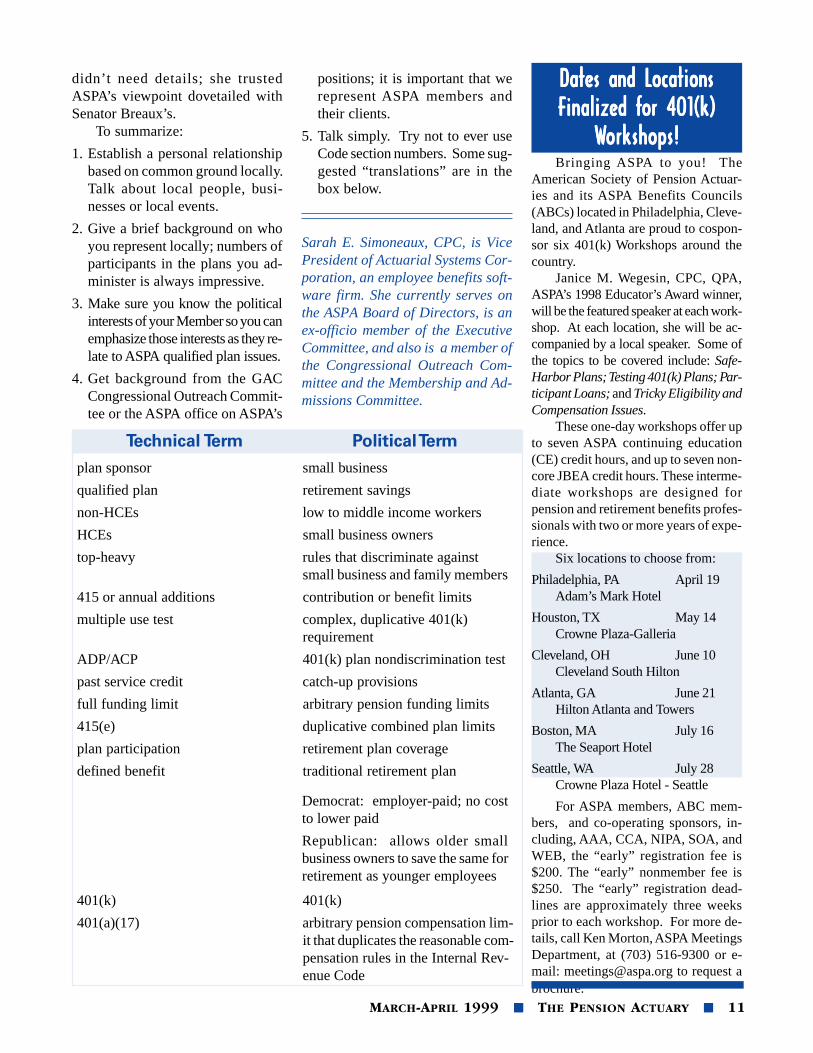

Technical Term Political Term

plan sponsor small business

qualified plan retirement savings

non-HCEs low to middle income workers

HCEs small business owners

top-heavy rules that discriminate againstsmall business and family members

415 or annual additions contribution or benefit limits

multiple use test complex, duplicative 401(k)requirement

ADP/ACP 401(k) plan nondiscrimination test

past service credit catch-up provisions

full funding limit arbitrary pension funding limits

415(e) duplicative combined plan limits

plan participation retirement plan coverage

defined benefit traditional retirement plan

Democrat: employer-paid; no costto lower paid

Republican: allows older smallbusiness owners to save the same forretirement as younger employees

401(k) 401(k)

401(a)(17) arbitrary pension compensation lim-it that duplicates the reasonable com-pensation rules in the Internal Rev-enue Code

didn’t need details; she trustedASPA’s viewpoint dovetailed withSenator Breaux’s.

To summarize:

1. Establish a personal relationshipbased on common ground locally.Talk about local people, busi-nesses or local events.

2. Give a brief background on whoyou represent locally; numbers ofparticipants in the plans you ad-minister is always impressive.

3. Make sure you know the politicalinterests of your Member so you canemphasize those interests as they re-late to ASPA qualified plan issues.

4. Get background from the GACCongressional Outreach Commit-tee or the ASPA office on ASPA’s

positions; it is important that werepresent ASPA members andtheir clients.

5. Talk simply. Try not to ever useCode section numbers. Some sug-gested “translations” are in thebox below.

Sarah E. Simoneaux, CPC, is VicePresident of Actuarial Systems Cor-poration, an employee benefits soft-ware firm. She currently serves onthe ASPA Board of Directors, is anex-officio member of the ExecutiveCommittee, and also is a member ofthe Congressional Outreach Com-mittee and the Membership and Ad-missions Committee.

Bringing ASPA to you! TheAmerican Society of Pension Actuar-ies and its ASPA Benefits Councils(ABCs) located in Philadelphia, Cleve-land, and Atlanta are proud to cospon-sor six 401(k) Workshops around thecountry.

Janice M. Wegesin, CPC, QPA,ASPA’s 1998 Educator’s Award winner,will be the featured speaker at each work-shop. At each location, she will be ac-companied by a local speaker. Some ofthe topics to be covered include: Safe-Harbor Plans; Testing 401(k) Plans; Par-ticipant Loans; and Tricky Eligibility andCompensation Issues.

These one-day workshops offer upto seven ASPA continuing education(CE) credit hours, and up to seven non-core JBEA credit hours. These interme-diate workshops are designed forpension and retirement benefits profes-sionals with two or more years of expe-rience.

Six locations to choose from:

Philadelphia, PA April 19Adam’s Mark Hotel

Houston, TX May 14Crowne Plaza-Galleria

Cleveland, OH June 10Cleveland South Hilton

Atlanta, GA June 21Hilton Atlanta and Towers

Boston, MA July 16The Seaport Hotel

Seattle, WA July 28Crowne Plaza Hotel - Seattle

For ASPA members, ABC mem-bers, and co-operating sponsors, in-cluding, AAA, CCA, NIPA, SOA, andWEB, the “early” registration fee is$200. The “early” nonmember fee is$250. The “early” registration dead-lines are approximately three weeksprior to each workshop. For more de-tails, call Ken Morton, ASPA MeetingsDepartment, at (703) 516-9300 or e-mail: [email protected] to request abrochure.

Dates and LocationsDates and LocationsDates and LocationsDates and LocationsDates and LocationsFinalized fFinalized fFinalized fFinalized fFinalized for 401(k)or 401(k)or 401(k)or 401(k)or 401(k)

WWWWWorkshops!orkshops!orkshops!orkshops!orkshops!

12 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

C O N T I N U E D F R O M P A G E 2

Is There A “Roth 401(k) Or 403(b)” In

Your Future?

Senator Roth proposesto remove the Section415(c) 25% limit, leavingonly the $30,000 limit.

ods for calculating basis recovery un-der Code Section 72(e). An even big-ger issue is how the taxes will be paid.Will the participant be allowed to pay

the taxes with assets outside the trustthus allowing the participant to pre-serve more assets within the retirementtrust?) How much additional cost andrelated administrative burdens will becreated for employers and service pro-viders by the addition of Roth 401(k)and 403(b) accounts?

A potential Achilles heel is therevenue loss the Roth 401(k) maycreate for the Federal government infuture years. Although participantswill pay taxes currently, the govern-ment will forego a potentially muchlarger “cut” at the time distributionsoccur. Imposing taxes at the front-endinstead of at distribution requires acomplete reversal of 90 years of fed-eral retirement and income tax policyassumptions. Another important, butunanswered, administrative question ishow to coordinate reporting of distri-butions that include contributionsmade under both the old and new rules.This may become extremely compli-cated when the minimum required dis-tribution rules also come into play.

Increased Contribution Limitsfor 401(k)s, 403(b)s, andSIMPLEsFor those who still prefer pre-taxcontributions to 401(k) and 403(b)plans, the bill increases the annual

limit on elective deferrals and salaryreduction contributions from $10,000to $15,000. Individuals over age 55who took time off to raise children

get an even better deal be-cause they would be allowedto contribute up to $22,500annually. This latter proposi-tion is not new, and it mayreceive significant supportfrom individuals who lost

years of savings opportunities be-cause of family priorities. The Uni-formed Services Employment andReemployment Act of 1994 providesample precedent for such catch-upcontributions, and the potential lob-bying group is certainly larger in thisinstance.

Contributors to SIMPLE IRAsand SIMPLE 401(k)s also get higherannual contribution limits to preservethe differential between the contri-bution limits that apply to qualifiedplans and the SIMPLE plans. Theannual limit on contributions to anySIMPLE would increase from $6,000to $10,000 under the proposal.

The chief resistance to higher an-nual contribution limits again will bebased on revenue considerations anda perception that only the highlycompensated will be able to take fulladvantage of the increase. However,the secondary family wage earnermight have an incentive to increaseretirement saving contributions un-der the plan. Existing 401(k) plansmay see a decrease in elective defer-rals and ADP testing failures with-out revision of the antidiscriminationrules because of a shift to after-taxcontributions. This result may beunavoidable unless plans adopt safeharbor contribution formulas.

Elimination of the Section 415(c)25% of Compensation Limit

The maximum amount that maybe contributed to a defined contribu-tion plan in a limitation year is thelesser of 25% of compensation or$30,000. The $30,000 limit is subjectto a cost-of-living increase in multiplesof $5,000. In reality, the $30,000 limitapplies to highly compensated employ-ees but does not affect nonhighly com-pensated employees. Instead, the 25%of compensation limit has a dramaticimpact on the lower paid. The 25%usually results in lower employee andemployer contributions for these indi-viduals. The Senator would removethe 25% limit, leaving only the $30,000limit. The $30,000 limit would con-tinue to be adjustable for inflation.

There has been support for therepeal of the 25% limit in the past.Repeal may allow some lower paidparticipants to maximize electivedeferrals and employer contributions.Since the beginning of the 1998 planyear, compensation for this purposeincludes elective contributions madeby the individual to 401(k), 403(b),457, and Section 125 cafeteria plans.However, repeal does not resolve theinherent conflict created by theCode’s definition of compensationfor annual additions as gross com-pensation and definition of compen-sation for employer deductions ascompensation net of elective contri-butions. In order for this change tohave its desired result, the definitionof compensation for deductions un-der Code Section 404 will need to bechanged. Otherwise, the employermay not be able to deduct all theemployee elective deferrals and willbe reluctant to provide them.

IRA ImprovementsIRA owners get to keep pace,

too. Senator Roth noted that the$2,000 maximum annual contribu-tion limit has never been adjusted forinflation since IRAs were created in

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 13

1975. If the law had provided forindexing, the current annual limitwould be $4,930 or $2,970 more thanthe current limit. The bill would ad-dress this perceived inequity by al-lowing annual contributions of up to$5,000. To make up for the lack ofcost-of-living adjustments, workersage 50 and over get an increased con-tribution limit of up to $7,500. Inaddition, all income limits that pre-vent individuals covered under anemployer’s plan to make a full con-tribution to a traditional IRA or limittheir eligibility to have a Roth IRAwould be abolished. To encouragemore Roth IRA conversions, the billdramatically raises the current$100,000 adjusted gross incomelimit. As modified, any individualwith adjusted gross income of lessthan $1 million would be allowed toconvert an existing traditional IRAto a Roth IRA.

As a means of encouraging em-ployee saving, Senator Roth’s pro-posal authorizes employer plans toaccept IRA contributions to em-ployer plans, and encourages em-ployers to establish payroll deductionprograms for these contributions.The Clinton Administration hasmade similar proposals in the past.The rationale for including this in thebill is that employees would benefitfrom economies of scale and loweradministrative costs by investingtheir funds through their employer’splan. This coincidentally revives theconcept of the qualified voluntaryemployee contribution, a type of con-tribution repealed by TRA ’86.

These provisions are particularlyvulnerable to the critics’ argumentsthat they give too much to upper-in-come Americans at too high a rev-enue cost. This is because theproposal essentially destroys most ofthe current income limits on IRA eli-gibility. One reason given in 1986for placing income limits on the abil-

ity to have deductible IRAs was abelief by some members of Congressthat the IRA was mostly a “tool forthe wealthy.” Is this really a validconcern? A revenue loss may not infact occur since theoretically the in-dividual doing the conversion is in ahigher tax bracket at the time of theconversion than he or she will be atthe time of distribution. Thus, UncleSam realizes more tax revenuesooner, with a higher present value.

More troubling to some practi-tioners, however, may be the blurringof the lines between qualified plansand IRAs. This could be counterpro-ductive, as employers would be moreapt to accelerate the trend of shiftingadministrative costs to the accountsof participants. Ironically, those forwhom this reform is intended mayreap the reward of lower returns.

Full Funding Limit for DefinedBenefit Plans

Currently, employers maintain-ing defined benefit plans have limi-tations on what they deduct ascontributions to such plans. Contri-butions may not be deducted if theyexceed 150% of the plan’s currentliability. The bill would remove the150% limit because it fails to takeinto account the plan’s projected pen-sion benefits.

This change would have the ef-fect of reintroducing stability to thefunding of defined benefit plans.However, since the 150% limit basi-cally was imposed as a way to limitdeductions, resistance can be ex-pected from those who believe thatthe government would forego toomuch tax revenue.

Roth’s Other Idea: PersonalRetirement Accounts

In addition, Senator Roth has re-newed his call for using a portion ofthe budget surplus to create personalretirement accounts. The Senatorintroduced legislation in the last Con-

gress to create these accounts, andreintroduced it this year as the “Per-sonal Retirement Accounts Act of1999.”

Under this proposal, Americanswho have earned a minimum of fourquarters of Social Security coveragewould receive a minimum of $250annually over the next five years(2000 to 2004). This contributionwould be used to fund individually-owned personal retirement accounts.The amount received will vary basedupon the amount of payroll taxes paidby the individual. The monies dedi-cated for this program could not beused for any purpose other than re-tirement benefits and associated ad-ministrative expenses. Although thepersonal retirement accounts wouldexist apart from the Social SecuritySystem, it is envisioned that they arethe first step in the process of creat-ing permanent private Social Secu-rity Accounts.

The Senator describes this pro-posal as a means to rebate regressivepayroll taxes to workers. For ex-ample, an individual earning the cur-rent minimum wage ($12,980 in1999) would have, over the life of theprogram, $1,853 or 35% of his or herpayroll taxes deposited into the per-sonal retirement account. An aver-age wage earner (approximately$28,840 in 1999) would see an ef-fective rebate of $2,589 or 22%. Aworker earning more than the SocialSecurity taxable wage base ($72,600in 1999) would see an effective re-bate of $4,561 or 16% during thesame period. Assuming a 7.5% re-turn, by 2039 these hypothetical ac-counts are projected to grow on atax-deferred basis to $26,930,$37,537, and $65,980, respectively.

The accounts created under thisbill are modeled after those providedunder the Federal Thrift SavingsPlan. An independent board ap-pointed by the President and Con-

14 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

gressional leaders, subject to Senateconfirmation, would oversee the pro-gram. The members of the boardwould be subject to prudent fiduciaryrules similar to those contained inERISA. Initially, three investmentchoices would be provided, but ex-panding the list of permissible invest-ment funds would be an option. Theinitial investment funds include astock index fund, a fund investing incorporate bonds and other fixed in-come investments, and a fund thatinvests exclusively in US Treasurybonds. The account owner woulddirect how much of his or her accountwill be invested in the available in-vestment choices. To insulate equityinvestments from political concerns,the stock fund would be managed byprivate sector managers who wouldhave the exclusive authority to voteproxies. Benefits, which are fullytaxable, become payable at the timethe individual begins to collect So-cial Security payments. The indi-vidual may choose to receive benefitseither as an annuity or as an annualpayment based upon life expectancy.

The major difference betweenthe Roth proposal and similar initia-tives launched by the Administrationis the greater reliance on the indi-vidual making investment decisionsrather than the government. The useof an independent board to adminis-ter the program and limiting theavailable investment funds may al-low it to serve as an attractive middleway between those demanding com-plete privatization of the Social Se-curity system and those rejecting anyprivatization of the system. How-ever, based on the history of certaininvestments made by state retirementfunds, it would be very interesting towatch how investment decisions andproxy votes are made when electionseason draws near.

ConclusionBecause of the potential negative

impact on future government rev-enues and assertions that theSenator’s proposal disproportion-ately favors wealthier Americans, itis not certain that either of theSenator’s proposals will become law.However, Senator Roth is a deter-mined proponent of retirement sav-ings by individuals. For example,when President Clinton entered of-fice in 1993, who actually believedthat the Roth IRA had a reasonablechance of enactment? Republicansand Democrats certainly pay atten-tion to the Senator, and have beenknown to borrow an idea or two.Witness this year’s State of the UnionAddress where President Clintonproposed dedicating $15 billion ofthe budget surplus as seed money for

creating voluntary retirement savingsaccounts, albeit with considerablymore governmental control. Perhapsthe best thing about the Senator’sproposals is that it may at last pro-voke serious discussion and selectionof a rational retirement policy for thenext century. Apparently, the “pow-ers that be” in Washington are finallystarting to take note of the need todo something about the Social Secu-rity shortfall.

Steven R. Oberndorf, Esq., is an At-torney with McKay Hochman Com-pany, Inc., and Richard Hochman,APM, Esq., is President of McKayHochman Company, Inc., a Butler,New Jersey, employee benefits con-sulting firm.

DB workshops will be offered inthree cities in 1999.

• Newark, New Jersey – May 11Early registration deadline:April 18

• Dallas, Texas – May 24Early registration deadline:May 3

• San Francisco, California – July 10(preceding ASPA’s new SummerConference)Early registration deadline:June 21

The Defined Benefits Workshopswill cover topics on safe harbor plandesign; aggregating DB and DCplans for testing; actuarial cost meth-ods and funding, and a lot more. TheWorkshops will also offer five casestudies in designing a new plan, and

strategies for dealing withoverfunded DB plans.

Learn from two experienced andknowledgeable speakers: Joan A.Gucciardi, MSPA, CPC, President,Gucciardi Benefit Resources, Inc.;and Norman Levinrand, FSPA, CPC,President, Summit Benefits & Actu-arial Services, Inc.

The “early” registration fee is $250for ASPA members and $320 fornonmembers. More details are out-lined in the brochure that you willreceive in the mail in the middle ofMarch.

For more information, call JanetKamvar, Meetings Coordinator, at(703) 516-9300, or [email protected].

DEFINED BENEFITS WORKSHOPS IN 1999

MARK YOUR CALENDAR!!MARK YOUR CALENDAR!!MARK YOUR CALENDAR!!MARK YOUR CALENDAR!!MARK YOUR CALENDAR!!THE DEFINED BENEFITS WTHE DEFINED BENEFITS WTHE DEFINED BENEFITS WTHE DEFINED BENEFITS WTHE DEFINED BENEFITS WORKSHOPS ARE COMING SOON !!ORKSHOPS ARE COMING SOON !!ORKSHOPS ARE COMING SOON !!ORKSHOPS ARE COMING SOON !!ORKSHOPS ARE COMING SOON !!

Newark - Dallas - San Francisco

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 15

Deutsch,

Haslauer, and

Rosen Elected to

ASPA’s Board of

Directors

Lawrence Deutsch, MSPA, Beverly B. Haslauer, CPC,QPA, and Stephen H. Rosen, MSPA, CPC have been

elected to serve on ASPA’s Board of Directors for the 1999-2001 term.

Larry Deutsch, MSPA is an En-rolled Actuary and a member of theAmerican Academy of Actuaries. Hehas been practicing as an actuarysince 1976. Larryis chair of ASPA’sStandards Com-mittee and cur-rently serves onASPA’s Govern-ment AffairsCommittee and thePrinciples, Practices and Risk Manage-ment Committee. Also, he is a techni-cal reviewer for The Pension Actuary.He is a frequent author for technicalarticles in professional journals and afrequent speaker at professional meet-ings.

As president of Larry DeutschEnterprises, of North Hills, CA, Larryis responsible for running the corpo-ration and for maintaining the actuarialprograms that are used by his clients.In addition, he provides consulting ser-vices to clients on both actuarial andpension matters. Larry has a bachelor’sdegree in mathematics from the Uni-versity of California at Irvine.

Bev Haslauer, CPC, QPA is thepresident of Haslauer, Husley & Hall,Inc., a retirement plan consulting and

administration firm in Metairie,Louisiana. In addition to serving asan ASPA Board member, Bev is thechairman of theP u b l i c a t i o n sCommittee of theEducation andE x a m i n a t i o nCommittee and amember of the An-nual ConferenceCommittee. She is a past president ofthe Association of Employee BenefitPlanners of New Orleans, a past presi-dent of the Women’s ProfessionalCouncil, and a member of the NewOrleans Estate Planning Council. Bevis a frequent speaker at conferences andseminars, has published many articleson the subject of qualified retirementplans, and is a co-author of the Life In-surance Answer Book.

Bev was raised in New Orleans,Louisiana. She has been married forover 21 years and has three childrenbetween the ages of 11 and 26. Sheand her husband will become grand-parents for the first time this summer.Bev is vice president of the ClearyPlayground Booster Club and has beena coach there from time to time.

Steve Rosen, MSPA, CPC is anindependent consulting actuaryspecializing in the design andimplementation of employee benefitplans. His firm,Stephen H. Rosenand Associates,Inc., is located inHaddonfield, NewJersey. Steve is anEnrolled Actuary(EA) as well as a member of the Ameri-can Academy of Actuaries. He servesas chair of the ABC Committee, vicechair of ASPA PERF and as a regionalcoordinator on GAC's CongressionalOutreach Committee. Also, he hasserved as program co-chair for theAnnual Conference and co-chair fortwo Eastern regional conferences.

Mr. Rosen is a past president andcurrent board member of the ASPABenefits Council of the DelawareValley. Steve co-authored a book onthe Tax Reform Act of 1984 and pub-lished articles in Taxation for Ac-countants and the Pennsylvania CPAJournal on the 1986 Tax Reform Act.In addition, Steve served on the fac-ulty at The Institute of EmployeeBenefits in Pennsylvania and is co-author of Accountants Guide to Em-ployee Benefit Plans. Steve is alsoco-founder of The Haddon StrategicAlliances (HSA), a Haddonfield firmthat forms alliances with insurancecompanies and mutual fund familiesto provide daily valuation capabili-ties to retirement plans. HSA bringsto its clients the ability to have “stateof the art” benefit programs whilebenefiting from a local investmentadvisor, with coordinated administra-tive services provided by Stephen H.Rosen and Associates, Inc.

Steve was raised in Camden,New Jersey. He has a wife, Mary Jo,and 5 children ranging from 7 to 20years of age. Steve coaches soccerin his spare time and also enjoys theseashore.

16 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

To All Prospective Attendees:

The Business Lead-ership Conference isan incredible oppor-tunity to spend fourvalue-packed dayshelping your busi-ness. This confer-

ence offers you the opportunity tohear nationally recognized speakersas well as to network with a group ofyour peers. I have the honor of chair-ing the 11th annual Business Lead-ership Conference, the “BLC.” TheBLC is much more than a confer-ence, it has become a valuable re-source to our businesses. It is aresource that has spawned new busi-ness relationships, helped initiatenew lines of business, and providedsupport when businesses reallyneeded it.

This year’s conference theme isSkills and Strategies for the New Mil-lennium. With the theme in mind,an excellent line-up of speakers andfacilitators have been gathered to pre-pare conferees for the coming busi-ness challenges the new millenniumwill bring.

This conference is designed tobenefit retirement and pension pro-fessionals who have attained a posi-tion in their organization where theirdecisions impact their business’ life-blood, including presidents, princi-pals, owners, vice presidents, and keymanagers.

New for 1999: Previously openonly to ASPA members, the BLC isavailable to members of cooperatingsponsor organizations, including theAmerican Academy of Actuaries, theConference of Consulting Actuaries,and the Society of Actuaries.

The BLC is divided among In-teractive Workshops, Peer Net-working Groups, and FeaturedSpeakers. Our outside speakers willaddress a variety of topics from ser-vice issues (Malcolm BaldridgeImplementation), to the changingskyline of our industry (Alliances,Mergers, and Acquisitions), and fi-nally to the lifeblood of running ourbusinesses (Strategic Planning).

The Interactive Workshops wereexpanded this year so that attendeeswill have a forum to ask about spe-cific issues rather than hearing howto handle general problems. Someof the current topics include HumanResource Issues such as attraction,retention, and motivation of employ-ees. They will also address officeautomation including software andhardware; revenue sharing and dis-closure; and on-going daily and bal-ance forward issues.

Add Peer Networking Groups tothis dynamic mix, and you will un-derstand why this conference has be-come so special to attendees. I hopeto see you in Boca for the 1999 BLC.

Sincerely,Bryan J. Smith1999 BLC Chair

Conference Dates:May 2 - 5, 1999

Conference Location:Boca Raton Resort & Club501 East Camino RealBoca Raton, FL 33431-0825Hotel Reservations:(561) 447-3000

There are five types of rooms tochoose from:

Villa Room $180Cloister Room $215

Addison Court $215

Tower Room $270

Boca Beach Club $330Oceanfront

Hotel Reservation Cut-Off Date:April 2, 1999

Continuing Education Information:The BLC is worth 10 ASPA CE credithours.

For CPAs in Arkansas, Iowa,Kansas, Minnesota, Missouri, Ne-braska, North Dakota, Oklahoma,South Dakota, Texas, and Wisconsin:ASPA is registered with the NationalAssociation of State Boards of Ac-countancy as a sponsor of continu-ing education on the NationalRegistry of CPE sponsors. In accor-dance with the standards of the Na-tional Registry of CPE sponsors, CPEcredits will be granted on a 50 minutehour. ASPA recommends up to 20CPE credits for this conference. Onthis basis, state boards of accoun-tancy have the final authority on theacceptance of courses. Complaintsregarding registered sponsors may beaddressed to NASBA, 150 FourthAvenue North, Suite 700, Nashville,TN 37219, (615) 880-4200. Nocourse information may be obtainedat this number.

ASPA is willing to apply forother types of credit if the applica-tion and fee are not prohibitive.Please call ASPA and request a “Con-tinuing Education Checklist.”

What Are YWhat Are YWhat Are YWhat Are YWhat Are YouououououMissing?Missing?Missing?Missing?Missing?

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 17

home state either campaigning forhimself, or helping one of his col-leagues.

The next question is “What do Ido when I get there?” Don’t be ner-vous. Staffers are usually young andeager to learn from you about the pri-vate pension system. The better jobyou do of educating, the bigger friendyou will make. Remember, you aremaking this person a star in the eyesof their boss. If you should get anolder staffer, they are a delight to talkwith. They have been around the track

a few times and will make your meet-ing very relaxed. And, they are veryinterested in retirement. You will havefifteen to thirty minutes, so be brief,to the point, and know what you wantto cover while you are there. Sinceyou will most likely have folks withyou, share the presentation; andSOMEONE should take notes of anyquestions asked and follow-up on anyinformation to be sent.

The last question is “What do Ido when it’s over?” Start by leaving.Make sure to thank him for his timeand get his card. Someone should doa follow-up letter thanking him again,indicating any information that is ei-ther enclosed or will be forth comingand noting that you will be contact-ing him from time to time. You alsoshould make it part of your follow-up

to continue to contact the Member’sstaff in case a staffer should leave.You want to know who took theplace of the departing staffer. (Lifeexpectancy of a staffer is aboutthree to six years.)

Given that this past year was anelection year and Congress was notin session during the ASPA annualconference, our marchers met withtheir representative’s legislativestaffer. The 30 appointments, whichencompassed about twenty states,included 13 Representatives and 17

Senators. I would like to sum upthe “Hill Experience” withsome of the feed back com-ments from this year’s march.

Our New York group, AlanNahoum, Roger Ramsay,Michael Hoffman and TaraDonovan who met with Sena-tor Moynihan’s staffer StanFendley, reported:

“He was very interested inthe National Retirement Policy.He was puzzled at the reason

for the decline in pension cov-erage. He was knowledgeableand attentively taking notes. Bythe way, he was age 50 and isactively saving for retirement.”

Paul Donovan of Pennsylvania,who met with staffer MichelleKitchen from Senator RickSantorum’s office, said:

“The staffer seemed well re-ceptive to our meeting. In fact,she took extensive notes and hadeven prepared questions for dis-cussion.”

Calvin Nystrom of Florida whomet with Caroline Berver and RussellSullivan, staffers for Senator BobGraham, reports:

“This is an interesting and

enjoyable experience. I metRussell at our Florida retire-ment summit, and we hit it offwell. They are eager to learnfrom us (ASPA), and it is en-couraging to be listened to.”

Finally my group, which con-sisted of Gerry Gebauer, SheilaHickey, Sandi Thomson and I, metwith staffer Matt Tenellan, fromSenator Bob Torricelli’s office. I’lljust share one of our member’s clos-ing comments which sums up our en-counter perfectly:

“We shortened our presen-tation somewhat to prevent thestaffer from sinking into acoma!!”

Don’t let my latest experiencediscourage you. I have had manymore good than bad experiences, allequally important. Relationships donot happen over night. It takes all ofus, year after year, to go back up tothe Hill to fight for the private pen-sion system. I see the tide starting toturn in our favor. My closing com-ment to my staffer did wake him up....

“Do you realize that therewill be more people retiringover the next 15 to 20 years asa percentage of the U.S. popu-lation, than there ever has beenin the history of our country?By the way, without private pen-sions who’s paying for it???You are !!!”

Edward H. Thomson, III, MSPA,QPA is the President of E.H.Thomson & Co., Inc., of Sea Girt,New Jersey. He is also the ViceChair of GAC’s CongressionalOutreach Committee. Mr. Thomsonis a Trustee of the Public EmployeeRetirement System of New Jerseyand a member of the Actuarial Se-lection Committee for the PensionSystem of the State of New Jersey.

C O N T I N U E D F R O M P A G E 3

Marching to the Hill

Relationships do nothappen over night. Ittakes all of us, year af-ter year, to go back upto the Hill to fight forthe private pensionsystem.

18 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

In moving to a hybrid de-sign, the organization needsto decide if they wish to pro-vide a benefit based on fi-nal or career average pay.

C O N T I N U E D F R O M P A G E 5

Hybrid Pension Plans

poned, and many employees nowview early retirement subsidies as“penalties” for retiring early. Manyemployers are also finding that thereplacement workforce is not alwaysavailable, and question whether afully trained workforce will be avail-able in the 21st century. As a result,we have seen a trend away frompermanent early retirementsubsidies in favor of strategicincentives (early retirementwindows).

A properly designed hy-brid plan can, over time, effec-tively eliminate the earlyretirement subsidy, yet keepthe availability of an early re-tirement incentive program withinthe plan.

Desire to provide supplementalexecutive benefits

Another instance where a hybridplan may be attractive to smalleremployers is where they are lookingto maximize the benefits payable toa select group of employees throughthe qualified plan. Think of a hybriddefined benefit plan as a defined con-tribution plan without the $30,000annual addition limitation. In thislight, we have found hybrid plans tobe a very attractive means of provid-ing benefits to older, highly compen-sated employees.

These are just a few instanceswhere a hybrid plan design mightsatisfy an employer’s needs and ob-jectives. However, it represents amajor change in benefit delivery.Thus, one should proceed with cau-tion when discussing the concept andperhaps avoid introducing the con-cept to an employer that already hasa plan that is working well.

Establishing the Basic Plan

The starting point in moving toa hybrid plan design is to decide ifthe organization wishes to provide abenefit based on final average pay(pension equity) or career averagepay (cash balance). Certainly, all elsebeing equal, the pension equity plan

will be a higher cost plan. If theycurrently sponsor a final pay plan, itwill be easier to move to a pensionequity plan. But if their goals andobjectives are to reduce costs, thecash balance plan would be theproper choice.

Once the basic plan design issettled upon, then they must decidewhat benefit level will be providedto employees who are career employ-ees, and if the ultimate cost of theplan will be within their budget. Ananalysis of the benefit provided bythe plan throughout a “typical”employee’s career will illustrate theadequacy of the benefit – one maywant to compare the accruals underthe current plan and the proposedplan to allow the plan sponsor to bet-ter understand this concept. Astraight valuation of the normal costof the hybrid plan, using the currentpopulation, will provide the sponsorwith the ultimate cost of the plan –assuming that the employee demo-graphics will not change over time.

When considering a formula thatincreases with age and/or years ofservice, one has to test the accrualpattern to be certain that the formulais not back loaded (should look topass the 1331/

3% test). Although this

is a relatively easy test to pass, it isalso just as easy to overlook. Sincethe interest accumulation factorsneed to be included in the accrual ratetest, one should have wide latitudewithin the accrual rate. For example,if you are looking to offer a 2% ac-

crual rate before age 30 and a4% annual interest accrual rate,you can provide an accrual rateof 12½% at age 60 and stillmeet the accrual rules. Re-member that the Age Discrimi-nation in Employment Act(ADEA) will not allow you toreduce the accrual rates at spe-cific ages. Therefore, if theaccrual rates grow too high as

the employee population attains re-tirement age, it may be difficult toget them to retire.

We often recommend that the hy-brid plan offer a single sum paymentoption at termination and/or retire-ment. However, there may be indi-vidual instances when the sponsorwill not want to pay benefits at ei-ther point; for example, the employermay view single sums as too costly,or single sums conflict with theplan’s sponsor paternalistic nature.Of course, benefits must be providedin the form of a qualified joint andsurvivor annuity for all participantswho are offered payment options,and options must be offered to allemployees with a lump sum value inexcess of $5,000.

Grandfathering

Provisions

Once the basic plan is estab-lished, one will want to demonstratethe effect the plan will have on theplan sponsor’s current employee

MARCH-APRIL 1999 ■■■■■ THE PENSION ACTUARY ■■■■■ 19

group. We refer to this as the “win-ners vs. losers” analysis. This analy-sis compares the benefits eachemployee would receive at retirementunder a given set of assumptions un-der both the current plan and the pro-posed plan. If costs are to remainconstant and some participants willbe better off under the hybrid plan(short service employees), some par-ticipants will not fare as well. Weuse this demonstration to assist thesponsor with deciding which groupand how many employees can be pro-tected from a cutback in benefitswithin the sponsor’s cost parameters.This protected group is the“grandfathered group” under theplan.

We have seen some sponsorswho have grandfathered all currentemployees in the existing plan, whileothers have grandfathered no one. Ofcourse, the key question is where todraw the line. Generally, those mostnegatively impacted by the planchange are those who fall just shortof the protected group. We con-stantly have to remind our clients thatthere is no free lunch, and that as theyextend the grandfathered groupdeeper and deeper into the employeepopulation, the short-term cost of theplan will continue to grow. Thegrandfathering provision also adds acertain cost to administering the plan.

There are a number of ways tomitigate the need to grandfather ben-efits under the current plan. If thecurrent plan is well funded, the spon-sor can use some of the surplus as-sets to provide an enhanced cashbalance at transition. Of course, thisalternative leaves the plan sponsoropen to the risk of granting windfallsto participants who terminate soonafter the plan is converted. Our fa-vorite option is to provide a “kickerbenefit” to all current employees whohave attained a specific age and ser-vice level. This allows the sponsor

to provide greater benefits to a man-ageable group of employees whilekeeping the same general plan design– you should never lose focus of try-ing to keep the plan design as clearand concise as possible.

Communication and

Recordkeeping

Though not often uttered fromthe mouths of actuaries, we muststress that communicating the planafter if has been designed is most im-portant. If the plan remains misun-derstood, the employees will have nogreater appreciation of this plan thanthe old plan.

We also feel that the plan spon-sor should be up front with the par-ticipants. Glossy charts and graphs,if done well, can convey a wealth ofinformation. But, if they are mislead-ing, the employees will eventuallyview the entire program with skepti-cism. If the employer must reducethe costs of the defined benefit planto remain competitive, or to affordan increase in the match to a 401(k)plan, let the employees know thetruth. Employers must be counseledthat if they attempt to hide some-thing, their employees will find out,and the plan may become the sub-ject of a lead story in a local or na-tional newspaper.

Keep in mind that any hybridplan will require more recordkeepingand administration than a traditionalfinal pay plan. Whether maintain-ing a hypothetical account balancethroughout employees’ careers (in-cluding special awards and interestcompounding) or counting pointsbased on age and/or service, the or-ganization probably will not beequipped to handle the task. Wenever go into a hybrid plan designassignment without being preparedto offer our client either anoutsourcing solution to recordkeeping

Ideas? Comments? Questions?Want to write an article?

The Pension Actuary welcomes your views!Send to:

The Pension ActuaryASPA, Suite 8204350 North Fairfax DriveArlington, VA 22203-1619(703) 516-9300

or e-mail to [email protected]

or fax to (703) 516-9308

or software that allows them to admin-ister the plan in-house. Mid-size andsmaller clients (under 1,500 activelives) can be easily administered us-ing spreadsheet technology (e.g., Ex-cel or Lotus 123). However, largerclients may require more robust data-bases. If a selling point of the plan isits similarity to a 401(k) plan, then theclient should be ready to provide an-nual or quarterly statements as timelyas 401(k) statements are produced.

Endnotes1 This is due to the fact that the

benefits promised by tradi-tional plans behave like bonds:as interest rates fall, the valueof the obligations increase, andvice versa).

Raymond J. Lee, MAAA, is a VicePresident and Chief Technical Actu-ary with The Savitz Organization inPhiladelphia, PA. Mr. Lee has over 20years of experience in the pension field,and has assisted clients in analyzingthe benefits of hybrid pension planssince 1987. William P. Bishop, MSPA,CPC, QPA, FCA, is the President ofthe Savitz Organization. Mr. Bishophas over 15 years of experience in thepension field. He provides actuarialand consulting services to both singleemployer and multiemployer groupsand is a frequent speaker on employeebenefits topics at both regional andnational seminars and conferences.

20 ■■■■■ THE PENSION ACTUARY ■■■■■ MARCH-APRIL 1999

C O N T I N U E D F R O M P A G E 7

IRS “Best Practices” Memo

Provides Guidance on EPCRS