issue no. 165 - july–september 2007 / rajab–ramadan 1428

TRANSCRIPT

GLOBAL PERSPECTIVE ON ISLAMIC BANKING & INSURANCE

ISSUE NO. 165JULY–SEPTEMBER 2007

RAJAB–RAMADAN 1428

MALAYSIA: LEADING THE WAY

POINT OF VIEW: STRUCTURED DERIVATIVESIN ISLAMIC FINANCE

IIBI RECEIVES ODL QC ACCREDITATION

FAIR FINANCE: INCLUSIVEBANKING

PRIVATE EQUITY – MODERN DAYMUSHARAKAH?

CASE STUDY: FIRST DAWOOD ISLAMIC BANK

PUBLISHED SINCE 1991

24 Malaysia: Leading the way

www.newhorizon-islamicbanking.com IIBI 3

NEWHORIZON Rajab–Ramadan 1428

Features

Regulars

10 The loan shark hunter

16 Structured derivatives in Islamic finance: keeping one step ahead of ibaha, or providing valuable protection?

18 Financing the Poor: Towards Islamic Microfinance

22 Sixth sense

CONTENTS

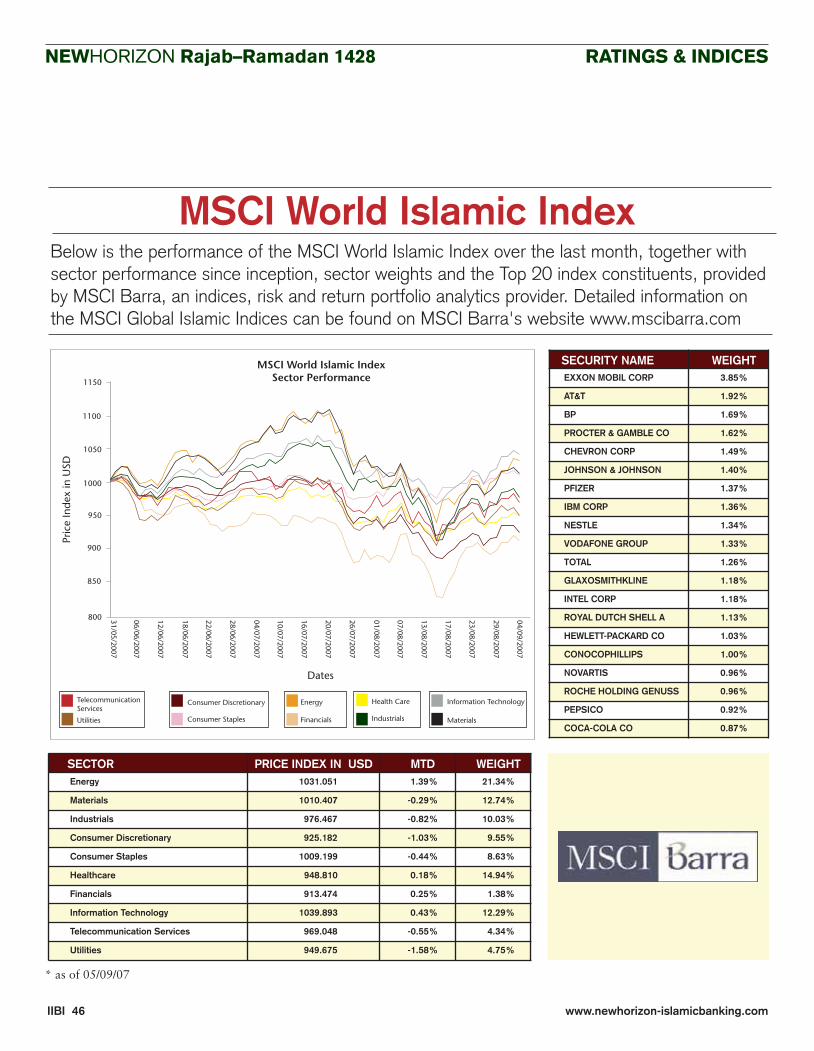

46 RATINGS & INDICESMSCI World Islamic Index, sector performance, sector weights and Top 20 constituents.

47 CALENDAR A comprehensive diary of upcoming Islamic finance events across the globe.

50 GLOSSARY

34 ACADEMIC ARTICLEPrivate equity – modern day musharakah?

38 IIBI NEWSCambridge workshop review; Introduction of the new logo;ODL QC accreditation.

40 IIBI LECTURESJuly, August, September lectures.

05 NEWSA round-up of the important stories from the last quarter around the globe.

14 APPOINTMENTS

32 ANALYSISLooking through the Islamic windowAnalysis of the performance of eight banks offering Islamic banking services in Malaysia.

24

44 Tales from the production line

An in-depth report on the Islamic microfinancesymposium held at Harvard University.

An interview with Warren Edwardes, CEO of London-based Delphi Risk Management.

Faisel Rahman, CEO of UK loans firm, Fair Finance,talks about how his company lives up to its name.

With a Muslim population of 16.3 million people, Malaysia’s high demand forShari’ah-compliant financial services is met by the committed support of theindustry from the country’s government and the central bank.

Zafar Alam, global head of private investor products and Islamic banking at ABN Amro, expounds on product development for Shari’ah-compliantfinance.

Nikolaus Schwarz, CEO of a new entrant to thePakistani Islamic banking market, First Dawood IslamicBank, reflects on the industry’s state of play in thisIslamic heartland.

4 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007

Executive Editor’s Note

EXECUTIVE EDITORMohammad Ali Qayyum,Director General, IIBI

EDITORTanya Andreasyan

IIBI EDITORMohammad Shafique

CONTRIBUTING EDITORSTom AlfordDon Brownlow

NEWS EDITORJames Ling

IIBI EDITORIAL ADVISORY PANELMohammed AminAjmal BhattyStella CoxDr Humayon Dar Iqbal KhanDr Imran Ashraf Usmani

SENIOR DESIGN CONSULTANTBecky Ellison

JUNIOR DESIGN CONSULTANTEmily Brown

PUBLISHED BY IBS Publishing Ltd8 Stade StreetHythe, Kent, CT21 6BEUnited KingdomTel: +44 (0) 1303 262 636Fax: +44 (0) 1303 262 646Email: [email protected]: www.ibspublishing.com

CONTACTAdvertisingIBS Publishing LtdGreg DavisAdvertising & Sponsorship ManagerTel: +44 (0) 1303 263 533Fax: +44 (0) 1303 262 646Email: [email protected]

SUBSCRIPTION IBS Publishing Limited8 Stade Street, Hythe, Kent, CT21 6BE, United KingdomTel: +44 (0) 1303 262 636Fax: +44 (0) 1303 262 646Email: [email protected]: newhorizon-islamicbanking.com

©Institute of Islamic Banking and InsuranceISSN 0955-095X

This third issue of NewHorizon in 2007, which comesout in Ramadan – the Holy Month for Muslims, marks a number of positive developments in Shari’ah-compliantfinance around the globe, as well as – no less important –developments within the Institute itself. You may havenoticed the new look of the IIBI’s logo on the cover of the magazine. This encompasses a fresh take on thetraditional crescent-shaped logo that has been an integralpart of the Institute’s brand for the last 16 years. Thecombination of three crescents in the new logo representsthe key objectives of the Institute: education, promotionand the implementation of Islamic finance in all its forms.

Also, the IIBI has received accreditation from the UKguardian of quality in open and distance learning, ODLQC, which marks a major step forward in this type ofIslamic finance education. The Institute is currentlydeveloping a new range of courses (in both Islamicbanking and insurance) aimed at the widest scope of takers around the world.

As part of the IIBI’s global reach strategy, NewHorizonnow becomes available online, with regularly updatednews and recruitment sections, a calendar of upcomingevents and, of course, complete contents of the currentand previous issues of the magazine.

This issue of NewHorizon brings you, amongst otherthings, a comprehensive analysis of Islamic finance inMalaysia; an assessment of the Islamic banking market in Pakistan through the eyes of its newest player, FirstDawood Islamic Bank; and a review of a controversialdebate on how structured derivatives can fit into Shari’ah-compliant finance. And there is much more to read andreflect upon within the pages of the magazine. We hopethat NewHorizon will help you to do exactly what theIIBI’s slogan states – to discover new perspectives.

EDITORIAL

Deal not unjustly,and ye shall not be dealt with unjustly.

Surat Al Baqara, Holy Quran

This magazine is published to provide information on developments in Islamic finance, and not to provide professional advice. The views expressed inthe articles are those of the authors alone. The Publishers, Editors and Contributors accept no responsibility to any person who acts, or refrains fromacting, based upon any material published in the magazine. The Editorial Advisory Panel exists to provide general advice to the editors regardingmatters that may be of interest to readers. All decisions regarding the published content of the magazine are the sole responsibility of the Editors,and the Editorial Advisory Panel accepts no responsibility for the content.

Mohammad Ali QayyumDirector General, IIBI

www.newhorizon-islamicbanking.com IIBI 5

NEWHORIZON Rajab–Ramadan 1428

First Islamic bank launchedin Kyrgyzstan

NEWS

The Islamic Financial ServicesBoard (IFSB) believes that theabsence of a clear regulatoryframework is hindering the growth of the takafulindustry. The standard-settingorganisation believes that the growth of the sector is

stunted by a lack of legal and regulatory certainty, andresultant inadequacies in riskmanagement. It is calling for a dialogue within the industry to adapt current insuranceregulations to meet thespecificities of Islamic finance.

IFSB calls for takaful regulation

The first half of 2007 hasseen the global sukuk markethit a new high with marketvalue totalling $24.5 billion,75 per cent growth from the same period last year. This figure comes from IFISAnalysts’ Sukuk MarketReport First Half 2007.

The report covers the periodJanuary to June 2007, andshows that the internationalsukuk market has grown by 83.3 per cent over the

past year. Also in the reportwas a league table of sukukbook runners. CIMB Islamictopped the overall table,having issued $3.15 billion indomestic and internationalbonds. It also topped thedomestic table with a total of $2.87 billion issued inMalaysia.

The largest international bookrunner was Deutsche Bank,aggregating $952 million insukuk issuance.

Global sukuk market hits new high

The Pak-Qatar group hasbecome the first company to receive a family takafullicence from the Securitiesand Exchange Commission of Pakistan (SECP). This nowmakes it the first company tohave both family and generaltakaful under one umbrella in the country.

The group has set up two separate companies: Pak-Qatar Family Takafuland Pak-Qatar GeneralTakaful. These companiesdiffer in the types of productsthey will offer. The generaltakaful company will offerproducts covering property,auto, marine, engineering and other areas, whereas thefamily takaful company will

offer financial protection forfamilies in the case of death ordisability to the breadwinner,health benefits, educationplans, retirement income plansand other savings schemes.

The group’s backing comesfrom Qatari investors. It hasbacking from Qatar IslamicInsurance Company, QatarIslamic Bank, QatarInternational Islamic Bank,Qatar National Bank and the Amwal Group. The SECPgranted both companies theirlicences on 16th August.Family Takaful has a paid-upcapital of $8.26 million(Rs500 million) and GeneralTakaful has a paid-up capital of $4.95 million (Rs300 million).

Pak-Qatar receives first family takaful licence

in Pakistan

Kyrgyzstan

direction of Islamic financefollowing a technical assistancegrant from the IDB. There havebeen recent legal changes inKyrgyzstan to try to make it a regional leader in Islamicfinance. Under these lawchanges double taxation onIslamic leasing operations hasbeen abolished and incometaxes on corporate and personalincome have been reduced. In the last issue (April–June2007), NewHorizon extensivelyreported on the development of Islamic banking in thispredominantly Muslim CIScountry.

EcoBank, the first bank inKyrgyzstan to open an Islamicwindow, has been officiallylaunched. The bank was arecipient of funding from theIslamic Corporation for theDevelopment of the PrivateSector (ICD) which wasrepresented at the launch byCEO Dr Ali Soliman. Alsopresent was the nation’spresident H.E. KurmanbekBakiev and H.E. Dr Ahmed M Ali, president of the IslamicDevelopment Bank (IDB) group.Representatives of the ICD andIDB were in the country for aseries of meetings to discuss the

www.newhorizon-islamicbanking.comIIBI 6

NEWHORIZON Rajab–Ramadan 1428

Responsible Lending finds that 90 per cent of paydaylending revenues are based on fees stripped from trappedborrowers, with 91 per cent of payday loans going toborrowers with five or moreloan transactions per year. Thisfigure is virtually unchangedfrom its 2003 findings.

The report also notes that thetypical payday borrower paysback $793 for a $325 loan. The Center concludes that‘predatory payday lending nowcosts American families $4.2billion per year in excessivefees’.

Mahdi Bray (above), MASFreedom Foundation’s executivedirector, is calling for payday

Extreme riba comes under attack in US

loan operations to be shutdown. ‘This form of lendingcannot be justified in any form of scripture in Judaism,Christianity, or Islam,’ he says.He adds that ‘as Muslims, weknow that our Holy Quranprohibits usury in commerce’.With payday loans seeminglyrepresenting the most extremeform of this practice, MAS‘completely supports theconsumer advocates whodemand an end to this form of financial exploitation’.

MAS has drawn support from the first elected Muslimrepresentative in Congress,Keith Ellison. He is co-sponsoring an act of federallegislation, known as the PayDay Loan Reform Act of 2007,which has already beenpresented to the House ofRepresentatives. Similar legis-lation, which would severelylimit the interest rates applied to these loans, is currentlybefore the Washington, DC City Council.

In the UK, Faisel Rahman’s FairFinance organisation is seekingto counter similar lendingpractices (see p10 in this issue).

NEWS

The Muslim American Society(MAS) has linked up withmembers of the Washington, DC interfaith community in aprotest against so-called paydayconsumer loans.

Supporters of the MAS FreedomFoundation and the interfaithcommunity joined in a Julydemonstration, centred on acapital city-based loan shop,protesting against the $28billion a year industry whichthey criticise for unfairlytargeting poor and minoritycommunities with loans subjectto interest rates often in excessof 400 per cent.

A counter-demonstration wasmounted by a number of loanshop employees who wavedplacards proclaiming their ‘love’ for their loan customers.

MAS’s Ibrahim Ramey was not impressed. ‘They love theircustomers in the same way thatliquor stores love alcoholics,’ hesays. ‘These people prey on poorand financially desperate people,and participate in the economicexploitation of communities.’The practice of making paydayloans has also attracted the

attention and anger of consumeradvocates throughout the US.They are supporting legislationat local, state, and federal levelsto regulate the industry.

The loans, typically offered tolow-income people with little or no access to establishedfinancial institutions, can meaninstant credit for severalhundred to several thousanddollars. The borrower handsover post-dated cheques to thelender, usually timed to coincidewith the receipt of a pay cheque.

Apart from the ultra-highinterest rates, problems oftenstart when borrowers cannotmeet the full repayment of their loan, forcing them either to extend it for a fee or add to it – techniques known in theindustry as roll-over and loanflipping.

Each loan extension compoundsthe interest accrued on the loan. This, he adds, makes the original amount of moneyborrowed ‘almost impossible to re-pay’.

A November 2006 report by the US-based Center for

Bahrain-based AlbarakaBanking Group has beenlicensed to establish a newsubsidiary in Syria.

The Islamic banking giant hastargeted the country becauseof the economic and trade

relationships it has with the rest of the world.

The subsidiary, to be calledAlbaraka Bank Syria, willprovide Islamic bankingproducts and services toindividuals and companies.

Albaraka eyes Syria and Asia

A branch network has beenplanned to cover the main cities in the country.

The bank will start itsoperations by the end of this year with an authorisedcapital of $100 million.

The Bahraini banking group isplanning further expansion intonew countries. Asia seems to bethe next target, with a reported$300 million to be invested in operations in India, China,Indonesia, and Malaysia overthe next four years.

7 IIBIwww.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007NEWS

Software suppliers are seeingincreased popularity for theirIslamic banking offerings in theMiddle East. Some of the biggestvendors have recently had winsfor their systems at a variety ofIslamic financial institutions inthe region.

Meezan Bank has decided totake the T24 Islamic model bankfrom Swiss vendor Temenos. Setup five years ago, Meezan Bankis a purely Islamic bank withover 60 branches in Pakistan.

According to Temenos’ generalmanager for the Middle East,Juan Cerudo, with ‘largeexpansion plans’ to increase itspresence to 250 branches in thenext five years, the bank ‘felt aninternational banking systemwould help them take their plans forward’.

Another Pakistani bank withsimilar ambitious growthstrategy, Bankislami, has alsobeen busy with its systemsselection. On the core back

office side it has opted foriMAL from Kuwait-based Pathto be deployed across the bank’s19-branch network. The otherselected system is the XM3 anti-money laundering solution fromUS vendor Haydrian. The wincame out of the vendor’sKarachi office, and is its first inPakistan.

Albaraka Banking Group (ABG)has selected UK-based Misys’Equation for three sites:Bahrain, Beirut, and Durban in South Africa. ABG is madeup of ten banks in differentgeographies around the world,and is one of the largest Islamicbanking groups in existence.

Equation will be implementedfirst in Bahrain in the course of twelve months. The SouthAfrican site is most likely to be the next on the list. Theinstallations are set to take less time in each instance; thesecond is scheduled for tenmonths with this reduced tonine for the final project.

Islamic systems fly off the shelfin the Middle East

governor of Bank NegaraMalaysia (central bank), for‘outstanding contribution to the development of an Islamic capital market’ for her role in establishing Malaysia as the most developed Islamiccapital market in the world.

Lord Eddie George (interviewedin New Horizon, April-June2007), former governor of theBank of England (central bank),also won an award for‘outstanding contribution to thedevelopment of Islamic financein the UK’.

The Investment Dar has wonthe award for ‘most innovativefinancing transaction’ for itsacquisition of the Aston MartinCar Company at the inauguralIslamic Finance Awards. Thetransaction, completed in mid-June, was worth £479 million($965 million). The deal wasmade up of 60 per cent financedthrough equity contributionswith the rest funded through amurabaha facility arranged bythe London branch of WestLB.

Also recognised at the awardswas Dr Zeti Akhtar Aziz,

The largest ever M&A(Mergers and Acquisitions)transaction in Islamic bankingis set to see another foreigninvestor enter the Turkishbanking industry. SaudiArabia’s National CommercialBank (NCB), the largest bankby assets in the Kingdom, isattempting to buy a 60 per

NCB in largest ever Islamic banking M&A transaction

cent equity stake in TürkiyeFinans Katilim Bankasi.

Türkiye Finans is a participationbank. These are Shari’ah-compliant banks that do notcharge or pay interest on loansor deposits, but instead offercustomers participation in theirprofits. The bank was formed as

the result of a merger betweenAnadolu Finans and FamilyFinans in 2005. The bank isjointly owned by BoydakGroup and Ülker Group; at the end of the last financialyear it had a 125-branchnetwork, and assets of $3.2billion. Under the terms of the deal NCB, which is being

advised by White and Case,would pay around $1.08 billionfor its 60 per cent stake in thebank. The remaining 40 per cent of the company would beequally split between Boydakand Ülker. The deal is subject to regulatory approval, and isexpected to close by the end of the first quarter of 2008.

Aston Martin deal wins Islamic finance award

Aston Martin

8 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007

Kuwaiti banks target UK for new Islamic subsidiaries

Two Kuwaiti banks are tryingto set up subsidiaries in the UK.Boubyan Bank and SecuritiesHouse have both targeted thecountry as a location for newIslamic financial institutions.

Boubyan Bank has entered theUK market with a 20 per centstake in Bank of London andthe Middle East (BLME). The new institution recentlyreceived authorisation from the Financial Services Authority(FSA) to launch as a standalone,wholesale, Shari’ah-compliantbank.

The bank, which is based inLondon, will focus on fourmain business lines. These areIslamic treasury and financialinstitutions; corporate banking;private banking and investmentmanagement; and investmentbanking.

BLME has raised $347 million(£175 million) from itsinstitutional shareholders. The remaining 80 per cent notowned by the Kuwaiti bank is held by a combination offinancial institutions,investment companies andemployees. Humphrey Percy has been appointed as CEO of the new bank.

Also trying to enter the UK isSecurities House. The companyhas set up a wholly-ownedpublic limited company in theUK and applied for a licencefrom the FSA. The licence it hasapplied for would allow it to actas a deposit-taking bankingentity within the UK. Securities

NEWS

House says that the newcompany will be established inLondon as a Shari’ah-compliantwholesale investment bank. Itwill focus on Islamic capitalmarkets, Islamic treasurybusiness and asset management.The new company will have apaid-up capital of $396 million(£200 million) and David Testahas been appointed as its CEO.

The UK is trying to establishitself as a hub for Islamicfinance and two new Islamicbanks goes some way toconsolidating this position. The UK government has the set aims of entrenchingLondon’s position as a globalgateway for Islamic finance with sukuk seeming to be themain point on its agenda.

The UK’s plans for the tradingof sukuk were set out by theneconomic secretary Ed Balls atThe London Islamic FinancialServices Summit in January(NewHorizon, January–March2007). These have been backedup by his successor Kitty Ussherat the first meeting of the UK’sIslamic Finance Experts Group.

At the meeting, the groupdiscussed the feasibility of theUK government issuing the firststerling sovereign sukuk, withthe discussion focusing on thepotential benefits of issuing a sukuk. The group also talked about recent marketdevelopments, and how thebusiness and Islamic comm-unities could work together todrive Islamic finance forward in the UK.

It has been a busy time forShari’ah-compliant mortgageprovider Sakana HolisticHousing Solutions. TheBahrain-based financialinstitution has signedagreements making it thepreferred Islamic mortgageprovider for two developmentsin the Kingdom. It has alsobecome the first lender inBahrain to offer mortgagefinance for more than onemillion Bahraini Dinars.

The first deal is with Bahrainiproperty developer Al Saraya.The intention is to allow morebuyers to enter the market by taking advantage of amortgage which is in line withtheir faith. Under the terms of the agreement, Sakana willprovide finance approval forpotential buyers interested inAl Saraya properties such asthe recently completed AlMarsa floating city in theAmwaj Islands.

The deal was signed by SakanaCEO R Lakshmanan (belowright) and Al Saraya generalmanager Yasser Al Sharrah(below left).

This deal follows on from an earlier memorandum ofunderstanding signed withanother domestic propertydeveloper, Durrat Al Bahrain. It sees Sakana become thepreferred Islamic mortgageprovider for the largest luxuryresidential, commercial andresort development in theKingdom.

These are the latest in a stringof partnerships that Sakana has entered into across theKingdom. According toLakshmanan, the reason forsigning agreements like these is to ‘facilitate the home buying process’.

The Islamic lender has alsoextended its line of mortgagecredit to $3.32 million(BD1.25 million). This is thefirst time a mortgage of thisvalue has been available to thepublic in the Kingdom. Prior to this offering, to receive aline of credit of this valuepeople would have to apply for a commercial loan. Themortgage can be taken out forone property, or split over a number of investments. There will be a period of threemonths for the borrower todecide how to allocate thefunds which can be used tofinance residential, commercialand investment properties.Sakana is jointly owned by two of Bahrain’s leading banks,Bank of Bahrain and Kuwaitand Shamil Bank.

Bahraini developments select Sakana as preferred Islamic mortgage provider

A complete library of knowledge & news at your fingertips

www.newhorizon-islamicbanking.com

For more information on how to promote your business on www.newhorizon-islamicbanking.com or to place a vacancy in our recruitment section click on Media Information on the website

October 2007 marks a landmark point in the development of NewHorizon, the journal of the Institute of Islamic Banking and Insurance.

As the phenomenon of Islamic finance continues its explosive growth, NewHorizon constantly seeks to improve its coverage of all the important issues, combined with complete and convenient access.

For the first time, anyone can read all of the published material via the internet. Whilst the major articles are available for analysis at your leisure, there will be no need to wait for the quarterly publication for news stories, which will be updated weekly.

All material will be archived and can be searched and accessed, using convenient keyword look-up.

Our ‘On The Move’ articles will keep you abreast of personnel changes worldwide, and our recruitment section will let you search for job opportunities in the world of Islamic finance, or advertise to fill those specialist vacancies. Whether you are seeking staff or a new challenge locally or globally, NewHorizon will be your first port of call for all recruitment issues.

www.newhorizon-islamicbanking.comshould always be kept in your ‘Favourites’ section on your PC, and accessed regularly. Make sure that you are always up to date and fully informed on all the key Islamic finance topics and views.

To access premium content you will need a username and password. To apply email: [email protected]

tool in helping to attract the unbanked poor and in encouraging them to seek their economic upliftment. Both Islamic financeand microfinance share the noble goal of a society free from economic elevation.

Fair Finance is a small, not-for-profit operation, but it is growing. When it firstopened its doors for business, it employedtwo debt advisors, two loan officers, an administrator and Rahman himself. Theteam has now been boosted to twelve, threeof whom are lenders, with the remainderdebt advisors.

While Fair Finance operates on conven-tional interest-based principles, its commit-ment is very much to responsible lending.Rahman estimates Fair Finance has savedhis customers almost the same total as thefirm’s first year total book-value in excessive

10 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007PROFILE

and Haringey, together making up a culturally diverse community of about 1.5 million people. It’s a naturally vibrant community but also represents a meltingpot of one of the UK’s highest concentra-tions of the financially dispossessed, righton the doorstep of the world’s financial capital.

With such an obvious disparity, Rahmanwas motivated from the outset by ‘the challenge of injustice’. From this standpointhis challenge to society is to seek an answeras to why the poor pay more for servicesthat the rest of us take for granted and toaddress the issue of why they are excludedfrom enjoying the benefits of a growingeconomy.

With Fair Finance, he is not just asking thequestions, he is taking positive action. Andthrough Fair Finance he is throwing downthe gauntlet to mainstream financial-providers to think about what they aredoing to an increasing mass of people. Underscoring his point, Rahman amusinglymisappropriates NatWest Bank’s advertisingtagline which states that ‘there is anotherway’. Indeed there is according to Rahman – and it doesn’t involve using the services of NatWest.

Islamic finance, with its primary goal of social justice and the eradication of interest,is still seen by many as an option mainly forthe rich and not for the often neglected anddisadvantaged poor. Microfinance, thoughbased on charging interest to poor clients,has demonstrated successes as a finance

No one could accuse Fair Finance boss,Faisel Rahman, of not doing his homeworkbefore setting up the business. Having spentfive months as an intern with Nobel PeacePrize winner, Muhammad Yunus’ GrameenBank – an organisation devoted to bankingthe unbanked in Bangladesh – he moved onto research microfinance for a year at theWorld Bank.

And following a stint as a trainee under-writer at Lloyds of London, Rahman, theson of Bengali immigrants to London, isnow putting to good use his worldly experi-ence and solid belief that finance should beinclusive not exclusive. Fair Finance waslaunched in April 2005 using the £5000($10,000) limit on Rahman’s personal credit card.

His aim was, and still is, to deliver ‘a single,holistic organisation that could provide arange of financial services to financially ex-cluded individuals’ who are generally thepoor and unbanked segment of society. Thistranslates into solid debt advice and a saferfinancial alternative to the loan sharks thatprey upon some of the UK’s poorest com-munities, primarily in London’s east-endboroughs which have a large Muslim population: Rahman’s first office was lo-cated in the heart of a council-run housingestate in Stepney in the London Boroughof Tower Hamlets.

To meet increasing demand, a second officehas opened in the London Borough ofHackney. The catchment area also takes inthe boroughs of Newham, Waltham Forest

The loan shark hunter For UK loans firm, Fair Finance, losing a customer to the mainstream financial markets is a signof success. As a link between the financially excluded and the financially included, it offers fairand equitable access to credit as well as advice and support which, although interest-based,bears close resemblance to some of the principles supporting Islamic finance. There may besome lessons to be learnt by Islamic banks. Tom Alford, NewHorizon’s contributing editor, talks to CEO, Faisel Rahman.

Faisel RahmanFair Finance

www.newhorizon-islamicbanking.com IIBI 11

NEWHORIZON Rajab–Ramadan 1428 PROFILE

payments to less scrupulous lenders. Someof these will charge more than 1000 (yes,one thousand) per cent APR to the peopleleast able to afford it. As a mark of whatthis represents, in its first year of trading,1000 people approached for a loan, ofwhom more than 300 were accepted forloans, worth around £500,000 ($1 million).This year, the loan book has reached 500from over 2000 applicants. The word isspreading amongst this sprawling conflu-ence of the unbanked and unbankable.

Perhaps most prevalent in the sort of com-munities in which Fair Finance operates arethe so-called door-step lenders. Agents ofthese firms literally knock on doors offeringsmall personal consumption loans – perhapsa few hundred pounds – often for basiccommodities such as fridges and cookers.This industry serves over two million peoplein the UK alone, subjecting customers tostarting interest rates of more than 400 percent; this can be discounted to around 200per cent if the customer proves to be a goodpayer. ‘What we wanted to do was developa method that would allow us to get to those people and offer them an alternative,’ says Rahman. With his Grameen Bank microfinance training, he also saw that there was potential to help a growing armyof skilled individuals ready but not able tostart their own businesses. ‘We wanted to

lend to people who had recently been bankrupted but wanted to start a business,and to people who had never been in the financial system but wanted to start a business,’ he says. The latter group includes recent immigrants to the UK who, throughno fault of their own, simply don’t have anycredit history and are unable to access main-stream funding to grow their ideas.

Fair Finance loans to consumers typicallystart at around £600 ($1200) over 14months, with business loans extending to

around £2000 ($4000) over 30 months. Interest rates reflect the higher risk and arehigher than current UK credit card levels.But they are nowhere near the loan sharknumbers. As a not-for-profit organisation it does not have to serve shareholders de-manding high returns on their capital invest-ments. And with the largest personal loanrising to just £2000 ($4000), Rahman statesthat Fair Finance is leaving its market fo-cused on the ‘very poor’.

The company has two distinct borrowertypes that serve to highlight an interestingdichotomy in the financial market. On theone side, there is financial exclusion, and on the other, financial exploitation. For the latter group, who often have too muchcredit, Rahman saw a desperate need fordebt advice to ensure that these people hada way of managing their finances, finding away to stick to their payment plans and todeal with the practical and emotional fall-out from consumer debt. ‘In a way,what we are trying to do is what the bank-ing industry did about 15 or 20 years ago,’he says. ‘And that is to actually talk toclients.

‘Our priority is about making responsibleloans, which I don’t think is happening thatmuch,’ he notes, pointing out that there isoften an ill-judged separation between

collection and lending operations withinsome of the high-pressure loans companies.Forming a financial pincer movementaround the vulnerable – by incentivising onedepartment to lend as much as possible andthen incentivising a different department tocollect as much as possible – does not createan environment conducive to sensible lending practice for the customer.

But there is a problem: the unbanked areseemingly subject to an infuriating bankingCatch-22 which means an individual cannot

In a way, what we are trying to do is what the banking industrydid about 15 or 20 years ago. And that is to actually talk to clients.

get credit without a credit history. But howcan an individual get a credit history without having credit?

One of the major problems for the financially excluded, therefore, is buildingup a credit history that can help them break free from the murky world of door-step lending. Even if someone does pay up regularly on a 400 per cent APR loan, they will still not be taken seriously by themainstream, simply because they are not in the system.

Fair Finance sees itself as an intermediary in a position to create ‘an appropriatecredit history’ for its customers on its own database. This data can filter through tothe mainstream and help build a bridge between the two worlds.

This falls into line with Fair Finance’s thirdstrand of activity which sees it involved insocial policy and campaigning. Rahman iskeen to promote issues of over-indebtednessand exploitative lending. ‘In a sense, our organisation is part delivery, part service,’he says. ‘It’s about offering a real, fair financial deal to people.’

He certainly has the ear of some of the mostinfluential individuals and organisations inthe UK financial industry. The company itself was officially declared open for business by Anna Bradley, the director ofthe FSA at the time, and Stephen Timms,chief secretary to the Treasury and MP forthe local East Ham of London ward. Theinvolvement of the wider financial commu-nity extends to the boardroom too, withmembers of the Royal Bank of Scotland(RBS) taking their place at the helm.

Rahman views the development of relation-ships with the traditional banking and fi-nance world as a vital part of the plan. Buthe acknowledges that deeply held attitudesand beliefs will not change overnight. ‘Getting them to be involved and see an alternative has always been the first stage,’he says. ‘Getting them to change their practices is a much longer-term thing and I don’t think we can see any real changesyet.’

Part of the problem of exclusion he attrib-utes to the automation of many of the basicbanking processes. This, he believes, has al-lowed banks to generate more profits in lesstime ‘because they can spend less on train-ing staff and use IT systems’ instead. Auto-mated links to credit bureaux, for example,whilst no doubt efficient, do not allow allthe facts to be considered. Simply feedingpersonal data into a system and waiting foran automated loan decision does not favourindividuals who do not exactly fit thebanks’ criteria. The three key criteria areemployment, credit history and home own-ership. Anyone falling outside of what is acceptable to the banks will be given a dis-proportionately high risk rating, whetherthe individual is a bad risk or not.

‘By making the systems faster and more efficient, they have dropped a whole load of people outside the system,’ Rahman says.‘Getting a bank to change that system isgoing to be very hard.’

Fair Finance is trying to show that it is possible to lend to people and develop anunderwriting methodology that can be efficient as well as equitable: it’s not simplyabout lending to them, it’s about giving advice too. Cold, hard risk assessment technology is therefore not used by Fair Finance. It prefers the human touch.

Every potential customer will be offered aninterview and part of this time will be takenup with an in-depth review of the individ-ual’s finances. This review considers every-thing including the financial minutiae such as how much is spent each week on cigarettes (if the applicant is a smoker) and entertainments. This process creates an accurate picture of what is affordableand whether the loan is even appropriate. Loan delinquency still happens, but Rahman believes his team can tell quitequickly whether a late payment is a matterof ‘won’t pay or can’t pay’, the latter beinghandled sympathetically. Actual bad debtlevels in the first year ran at just over oneper cent. Provision in the budget was for tenper cent. ‘It is quite a risky market in many

directly with one of their few big-hittingsupporters, RBS, which seemingly under-stands the principles behind an organisationlending to people that it would not normallyentertain. But RBS also knows that onceFair Finance’s customers have hauled themselves into the mainstream with a good credit rating, it has a ready-madeclient-base. ‘It’s the kind of partnership that we are trying to encourage with other banks,’ says Rahman hopefully.

Fair Finance did have a working relationship with Barclays, but the UK’sthird largest bank has since moved on toother areas. All is not lost though, and thetwo businesses are back and talking to eachother once more. Fair Finance also has theear of a number of ‘strategic banks’ such as UBS and Citibank; the latter is trying tomake a bigger UK consumer presence hav-ing bought the Egg credit card business.

In a move calculated to spread the goodword, Rahman is seeking to offer Fair Finance’s skills and knowledge of the sectorto the banks to show them how they can deliver their services through his business.But he explains that it has been ‘extremelyhard’ to engage other banks into this agenda. He cites some of the largest banksin the world as being ‘completely disen-gaged’ from the financial exclusion agenda,and from that of ensuring that finance canbe provided for all those outside the system.

There is a potential market out there, as RBS has seen, and he is clearly disap-pointed that some financial institutions lackthe foresight to reach out beyond their safemarkets, perhaps for fear of damaging theirquarterly results. Persuading banks to sharea vision is one thing, but drumming up thecapital to keep that vision going is quite another.

Fair Finance is registered as an industrialand provident society (IPS). This means that any investment is at risk and any one investor is capped at £20,000 ($40,000).This could restrict its investment appeal andgrowth potential. But aside from its own

12 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007

ways, because people are poor and thingschange rapidly,’ Rahman says. ‘The trick isto be flexible and ensure that the productyou deliver is appropriate to their needs.’

Of course, there is a world of difference between processing a few thousand peoplea year and a few million, but Rahmannonetheless believes he can prove to thebanks that the people they have forgottenare potentially people they should be lending to. The inclusion of enthusiasticRBS personnel on the Fair Finance board ispartly about demonstrating what lending inthe Fair Finance target community is like.But Rahman admits that, whilst it has a lot of high-level support in principle from the big banks, it has received very little practical commitment.

The big banks could hardly be more awareof the issue. The UK government’s TreasurySelect Committee frequently hounds themfor excluding poor people. But, as Rahmannotes, that positive response at the top isstill taking time to be converted into posi-tive action on the ground.

Some banks are making token gestures byoffering the basic bank account concept to the unbanked. These are no frills affairswith practically no services offered, no interest payments, no advice and no credit-scoring payoff. It is questionable whetheranyone would really want to place what little money they have into an account thatdid nothing for them. ‘The banks will saythey are trying to do something, but whatthey are delivering are products and servicesthat are inappropriate to the needs of poorpeople,’ complains Rahman with justifica-tion.

This is precisely the point where Fair Finance makes its entry as an intermediary:an organisation that can sit below thebanks, but above the loan sharks, money-lenders, cheque-cashers and pawn shops.

Having moved on from the early days ofsupporting loans with his personal creditcard, Rahman and Fair Finance now work

PROFILE

more ambitious plan. In the mid-term hecan see the programme drawing up to £15million ($30 million) of investment, allow-ing it to be rolled out across London andperhaps beyond. ‘There is no reason why all finance shouldn’t be fair finance,’ hesays, obviously aware of the marketing po-tential of such a statement. ‘What we offerwill not only compete with the sub-primemarket but also show the mainstream mar-ket that there is a better way of deliveringfinancial services – one that puts people before profits.’

Rahman believes that Fair Finance is veryclearly an ethically rooted organisation with a not-for-profit structure that has a

lot of resonance with the Islamic finance principles of justice and equality.

He believes that with the right type of ethically-minded investors in Islamic finance institutions, there is real potential to create an investment partnership to deliver a Shari’ah-compliant model throughFair Finance (in both its consumer and microfinance products) that is relevant and appropriate to the poor communities of London. As many of his existing clientsare poor Muslims living in deprived neigh-bourhoods, the potential for working with more people excluded from the system is a compelling argument for those who want to use Islamic finance principles to make a difference in their lives.

While the straightforward moral and ethicalarguments for using finance as a tool for inclusion and as a means to alleviate the financial problems of the poor are not always perceived as beneficial to financial institutions, with people like Rahman committed to the principles of a fairer financial system, it could ultimately help to create a more equitable society free from economic exploitation.

www.newhorizon-islamicbanking.com IIBI 13

NEWHORIZON Rajab–Ramadan 1428

self-generated funds (it reinvests 100 percent of its profits), Fair Finance has fairlysolid backing. The list includes: social investors (who, in some cases, have put in up to that cap) as well as banks such as RBS which have lent money at preferen-tial rates; sympathetic charitable invest-ment funds that approve of the work being done; government funding made accessible because Fair Finance is not onlyhelping to create businesses through its microfinance programme, but also helping to manage debts through its advice pro-gramme; and a number of London housingassociations that pay for advice dispensedto tenants.

It’s a diverse range of capital, but it has notbeen easy to maintain the flow. ‘When youare a small organisation like ours, it is veryhard to find the capacity-building resourcesto grow the infrastructure of the organisa-tion itself, to be big enough to be sustain-able,’ notes Rahman. The VC community,for example, is quite prepared to invest alot of money quickly into a small numberof agencies to make a systemic and sustain-able change. But in Fair Finance’s sector,where the business model is less well under-stood, Rahman reports that investors onlywish to drip-feed the funding over a longerperiod of time.

This makes it hard to reach the kind ofscale that the business needs in order to besustainable. Sticking resolutely to the remit of delivering services to customers not in-vestors makes it even harder to raise thefinance. The conscience of Fair Financemeans that it has to be ‘very tough’ aboutmaking sure it gets finance that doesn’t in-terfere with its job of delivering a service to the poor and excluded.

Naturally, Fair Finance is interested in encouraging more private and social investors. With a new form of tax reliefbeing introduced that will give such in-vestors a return, it may well drive that interest forward. ‘We’re hoping to use that to raise a substantial amount ofmoney,’ says Rahman.

The real challenge for him and his teamthough is to locate potential investors whoaren’t too risk-averse and who want to seetheir money doing good things in the community without looking for the kind ofreturns that the major retail or investmenthouses offer. The new tax relief on offershould bring some immediate measure of return for those that do venture this way. But Fair Finance is also placing great storein a new investment deal. Anyone investingfor a five-year period will receive an annualdividend of 8.33 per cent of what they haveput in, with the capital returned at the endof that time. It’s still a risk, says Rahman,asking investors to believe in the businessmodel.

This plan, he says, could become part of aportfolio offered by ethical investment IFAs,a number of whom he is in discussion with.The issue has also been raised with a number of banks as a proposition for their private wealth clients. Rahman claims ‘quite substantial’ interest to date.

Explaining the attraction of such an invest-ment, he maintains that this is a movementthat people are beginning to see more often.‘It’s kind of in vogue to talk about socialbusinesses that can make a return, especiallywith Muhammad Yunus recently winningthe Nobel Peace Prize.’

It could put corporate and social responsi-bility beyond the PR department and intothe mainstream of what investors want todo, he believes. ‘Everybody wants to seehow they can make their money work more than just simply making a return.’

The target for the first year of this newstrand of investment is £1 million ($2 mil-lion). If it can achieve this and demonstratethat it is benefiting those who really needthe money, he feels Fair Finance will be wellplaced to go back to the investors with a

There is no reason why all finance shouldn’t be fair finance... It’s about offering a real, fair financial deal to people.

PROFILE

Abu Dhabi Islamic – he has been on thebank’s board.

AXA Insurance Gulf has named PaulBromley as strategic development manager,responsible for the management of lifebusiness development in the Gulf Region.Bromley has 38 years’ experience in finance,life assurance and family takaful, 12 ofwhich he acquired working in the MiddleEast for Zurich Financial Services, SaudiBritish Bank and SALAMA.

Bank of London and the Middle East(BLME), an Islamic investment bankrecently established in the UK, has namedHumphrey Percy as CEO. Percy has over 30 years’ experience in banking. Yacob Al-Muzaini, chairman and managingdirector of BLME’s major shareholder,Kuwait-based Boubyan Bank, has beennamed chairman of BLME. Derek Weist hasbeen appointed head of structured finance.

Bahrain-based investment bank GulfFinance House (GFH) has appointed a new chairman, Esam Janahi, who has held the position of CEO since the bank’sestablishment. Janahi is one of the foundersof GFH and currently also chairs BahrainFinancial Harbour, Energy City Qatar andBayan Holding Company.

Bradley Brandon-Cross (left) hasbeen appointedCEO of the BritishIslamic InsuranceCompany, which iscurrently awaitinglicence from the

UK’s Financial Services Authority (FSA)to commence operations. Brandon-Crossis a co-founder of Rubicon, an insuranceservice provider in the UK.

Bahrain-basedBankMuscatInternational(BMI) hasappointed anew CEO,AndrewBainbridge(left). He joinsBMI from

Barclays, with 18 years of experienceworking at Barclays’ sites in the UK,Europe, Africa and the Middle East.

major contribution to establishing andlaunching Tejoori.

Bahrain-based investment bank, IthmaarBank, has appointed Michael McKinlayas executive director, private equity. Withover 25 years’ experience in banking andinvestments (of which 15 years have been in the Middle East), McKinlay will ‘addtremendously to the bank’s pool ofinvestment expertise’, according to Michael P Lee, CEO of Ithmaar.

Tan Sri Abi Musa Asa'ari Mohamed Nor,former secretary-general of the Ministry of Agriculture and Agro-based Industry,Malaysia, has been appointed chairman ofthe Pilgrims Fund Board (Tabung Haji, TH).TH is a Malaysian corporation that providesfinancial services to Muslim pilgrims.

Abu Dhabi Islamic Bank has namedRagheed Najib al-Shanti as acting CEO andKhamis Buharoon as managing director ofthe bank. These appointments follow theresignation of Ahmed Darwish Al-Marar asmanaging director. Buharoon joins the bankfrom the UAE-based Commercial BankInternational, while Shanti is already with

www.newhorizon-islamicbanking.comIIBI 14

NEWHORIZON Rajab–Ramadan 1428

On the move

APPOINTMENTS

Sultan Choudhury has taken the role ofcommercial director at the Islamic Bank of Britain (IBB), the UK’s first Shari’ah-compliant financial institution. He will beoverseeing sales, marketing and operationsfunctions of the bank.

International Islamic Financial Market(IIFM) has made a number of appoint-ments. Khalid Hamad, executive director,banking supervision at the Central Bank of Bahrain, has been named new chairmanand Mubarak El Tayeb El Amin, associatedirector, treasury at the Islamic Develop-ment Bank, has been appointed vicechairman.

Saleh Al Omair has been named CEO of a new takaful company currently beingestablished in Saudi Arabia. The companywill be a joint venture between domesticAhad Insurance Company and Bahrain-based Solidarity, one of the world’s largesttakaful operators.

Mrs Ilke Toklu has been appointed generalmanager of Dubai-based Tejoori Limited,the world’s first independent Islamicinvestment company to be listed on theAlternative Investment Market of theLondon Stock Exchange. Toklu made a

Volaw Trust &CorporateServices Limited,a fiduciaryservices providerbased in Jersey,has appointedJames Hume(left) as CEO

of the company’s new office in Dubai.Hume has extensive knowledge of Islamicfinance and over 25 years’ experience inprivate banking and trust services.

16 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007

In the conventional banking world, banksare able to use an array of derivativeproducts to manage risk – often to reducerisk, but sometimes to generate risk so thatthey can benefit from the increased returnsthat risk brings. Islamic financial institutions(IFI) also need to manage risk, not only interms of the institutions’ own treasurymanagement but also to create products thatallow their customers to do the same, forexample, in order to reduce an individual’sor corporation’s exposure to currency risk.

Edwardes thinks that derivatives havegained a reputation for being dangerousgambling instruments following the debaclesat Procter & Gamble, Bankers Trust and thewidely publicised excesses of Nick Leeson atthe defunct Baring Brothers. IFIs, in order toremain Shari’ah-compliant, must qualifytheir products and strategies through thescholars that provide supervisory authority.

There are various prohibitions in Islamregarding banking that must be abided byand in this regard the Shari’ah prohibitsuncertainty (gharar) and gambling (qimar). As a result, many of the structures that havebeen created to provide the characteristics of conventional derivatives while stillmaintaining Shari’ah compliance areproprietary and are often not generally

POINT OF VIEW

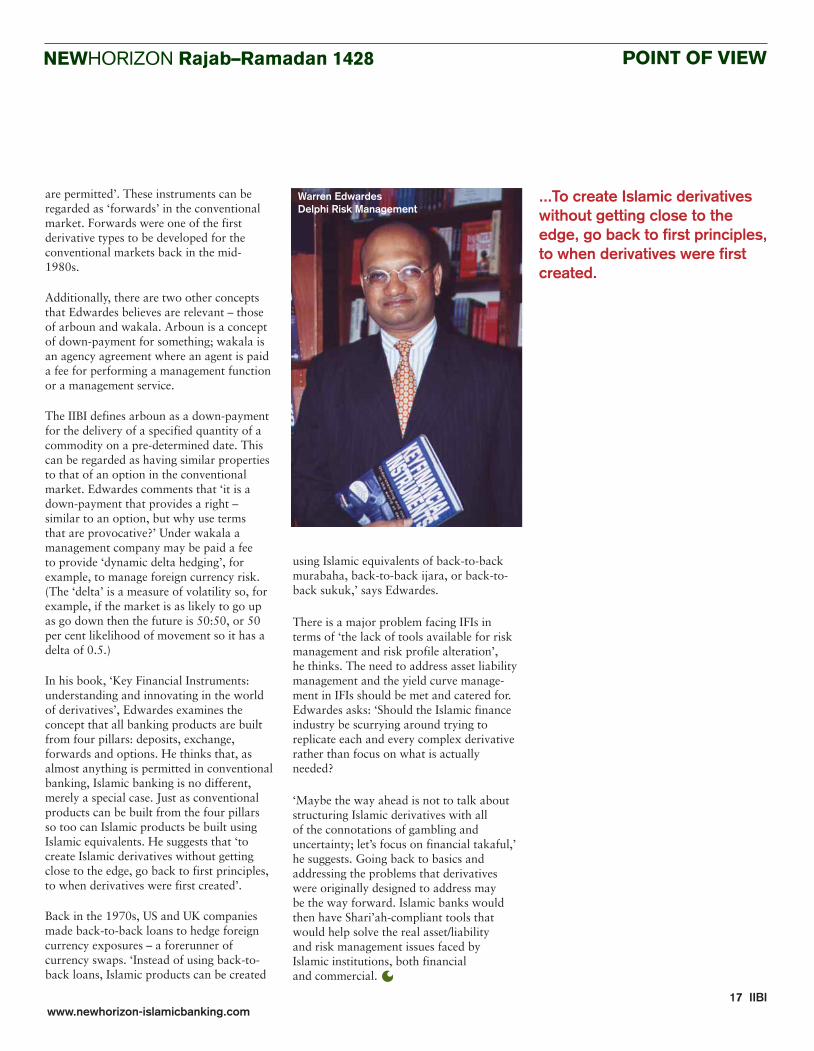

Structured derivatives in Islamic finance:keeping one step ahead of ibaha, or providing valuable protection?The mention of ‘structured derivatives’ often arouses connotations of wild excesses of risk taking and of high volatility, whereas the actuality is that these products were originallydeveloped to provide low-cost protection, or hedging, against unwanted market trends. To findout how these products can fit into Islamic finance, Don Brownlow, NewHorizon’s contributingeditor, spoke to Warren Edwardes, CEO of London-based Delphi Risk Management andmember of the IIBI’s informal Board of Governors.

openly available. But, according toEdwardes, ‘there is the concept of ibahawhich means that if something is not bannedthen it is permitted’. Under this principle, hecautions that ‘because something appears tobe similar to something that is banned, thendon’t assume that it too is banned’. Hepoints out that ‘looking at some of thefinancial products on the market, it seemsthat everything is possible using murabaha.Who am I to disagree, bearing in mind theprinciple of ibaha?’

He points out that using ‘murabaha aninvestor can “invest” in an “arm’s lengthSpecial Purpose Vehicle” [a specially formedcompany] that in turn could create “trades”in anything – from options to futures towarrants’.

In any event, he argues that derivatives canbe seen as permitted by saying ‘murabahaand salam could be regarded as derivatives:one is buying or selling something withdeferred payment [murabaha], the other is buying or selling something for deferreddelivery [salam]. They are derivativesbecause one is buying/selling for futurepayment and the other is buying/selling for future delivery – forward payment or forward delivery. So derivatives arepermitted because murabaha and salam

Should the Islamic financeindustry be scurrying aroundtrying to replicate each andevery complex derivative ratherthan focus on what is actuallyneeded?

are permitted’. These instruments can beregarded as ‘forwards’ in the conventionalmarket. Forwards were one of the firstderivative types to be developed for theconventional markets back in the mid-1980s.

Additionally, there are two other conceptsthat Edwardes believes are relevant – thoseof arboun and wakala. Arboun is a conceptof down-payment for something; wakala isan agency agreement where an agent is paida fee for performing a management functionor a management service.

The IIBI defines arboun as a down-paymentfor the delivery of a specified quantity of acommodity on a pre-determined date. Thiscan be regarded as having similar propertiesto that of an option in the conventionalmarket. Edwardes comments that ‘it is adown-payment that provides a right –similar to an option, but why use terms that are provocative?’ Under wakala amanagement company may be paid a fee to provide ‘dynamic delta hedging’, forexample, to manage foreign currency risk.(The ‘delta’ is a measure of volatility so, forexample, if the market is as likely to go upas go down then the future is 50:50, or 50per cent likelihood of movement so it has adelta of 0.5.)

In his book, ‘Key Financial Instruments:understanding and innovating in the worldof derivatives’, Edwardes examines theconcept that all banking products are builtfrom four pillars: deposits, exchange,forwards and options. He thinks that, asalmost anything is permitted in conventionalbanking, Islamic banking is no different,merely a special case. Just as conventionalproducts can be built from the four pillars so too can Islamic products be built usingIslamic equivalents. He suggests that ‘tocreate Islamic derivatives without gettingclose to the edge, go back to first principles,to when derivatives were first created’.

Back in the 1970s, US and UK companiesmade back-to-back loans to hedge foreigncurrency exposures – a forerunner ofcurrency swaps. ‘Instead of using back-to-back loans, Islamic products can be created

NEWHORIZON Rajab–Ramadan 1428 POINT OF VIEW

using Islamic equivalents of back-to-backmurabaha, back-to-back ijara, or back-to-back sukuk,’ says Edwardes.

There is a major problem facing IFIs interms of ‘the lack of tools available for riskmanagement and risk profile alteration’, he thinks. The need to address asset liabilitymanagement and the yield curve manage-ment in IFIs should be met and catered for.Edwardes asks: ‘Should the Islamic financeindustry be scurrying around trying toreplicate each and every complex derivativerather than focus on what is actuallyneeded?

‘Maybe the way ahead is not to talk aboutstructuring Islamic derivatives with all of the connotations of gambling anduncertainty; let’s focus on financial takaful,’he suggests. Going back to basics andaddressing the problems that derivativeswere originally designed to address may be the way forward. Islamic banks wouldthen have Shari’ah-compliant tools that would help solve the real asset/liability and risk management issues faced by Islamic institutions, both financial and commercial.

17 IIBI

...To create Islamic derivativeswithout getting close to theedge, go back to first principles,to when derivatives were firstcreated.

Warren EdwardesDelphi Risk Management

www.newhorizon-islamicbanking.com

18 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007

The Islamic finance sector has for some timefocused on the development of its business,including the standardisation and conso-lidation of the industry. This approach has marginalised a large number of‘unbankable’ members of society. Micro-finance is one such area that has beenneglected by the industry, and manyfinancial institutions around the world are working to address this – not just forphilanthropic reasons, but because this is a vast sector on which they can capitalise. The Islamic International Ratings Agency(IIRA) is currently involved in discussionswith the Islamic Development Bank as tohow to promote microfinance in Muslimcountries. Financial institutions such asDeutsche Bank and the Islamic Bank ofThailand have also decided to venture intoShari’ah-compliant microfinance. Otherefforts are under way on an experimentalbasis, although it is more difficult to provide a detailed account of these.

While Islamic finance aspires to create anequitable economy, it has in the eyes ofmany become a banking system for the rich.Conventional microfinance, meanwhile, has demonstrated success as a tool to helpreduce poverty and encourage economicgrowth in neglected, rural parts of theworld, but the flip side of this coin revealscriticism of the industry’s tendency to chargethe poor exorbitant interest rates and fees.These are often necessitated by the hightransaction costs incurred in microfinance,including the provision of services to

Financing the Poor: Towards Islamic Microfinance

This symposium held at Harvard University brought together a diverse group of internationalspeakers and a number of noted individuals from the microfinance and Islamic finance sectors.Nazim Ali, director of the Islamic Finance Project (IFP) at Harvard Law School, gave theopening address, and reports on the event for NewHorizon.

monitor and supervise entrepreneurialendeavours, health insurance, and so on.With the two industries sharing the common goal of social justice, the aim ofthe IFP symposium was to bring togetherrepresentatives from both, so that eachparty could learn from the other and move towards a viable system of Shari’ah-compliant microfinance.

The IFP symposium wanted to explore the role of the Islamic finance industry as a source of funding for microfinancinginitiatives and to serve as a medium topromote alternative financial instrumentswithin the Islamic finance industry. Withmany microfinance services offered on anot-for-profit basis, the viability ofharnessing traditional Islamic financialinstitutions that use zakat and waqf as asource of funding was discussed. Alsoconsidered was the potential collaborationbetween industry and academia to providebetter tailored microfinance models whichwould serve the needs of increasinglysophisticated microfinance institutions,while simultaneously creating alternatives,with lower service costs and increasedaccountability and transparency, forborrowers on the ground.

Misconceptions about intangible hurdleswhich have to be overcome within theIslamic finance industry, as well asmicrofinance, were aired within thesymposium. Many suggestions were offeredas means of overcoming sources of mutual

SYMPOSIUM REVIEW

Microfinance is not reaching the poorest of the poor, eventhough this is its purpose, andloans are going to activitiesunrelated to entrepreneurship.Islamic finance could, inprinciple and in practice,correct these defects.

www.newhorizon-islamicbanking.com IIBI 19

NEWHORIZON Rajab–Ramadan 1428 SYMPOSIUM REVIEW

misunderstanding, with a view to betterserving the poor, particularly in Muslimeconomies. Communication is key.

Baber Johansen, acting director of theIslamic Legal Studies Program and affiliatedprofessor at Harvard Law School, chairedthe symposium. He opened the session bycommenting on the burgeoning interest infinancing the poor and the Islamic financeindustry’s long-standing desire to promoteequitable economic development. In hisopinion, this offers a strategic approachtowards a charitable goal.

Robert Annibale, global director ofmicrofinance for Citigroup, was the firstkeynote speaker. He shared his insights into both Islamic finance and microfinance. He described microfinance institutions asself-styled ‘bankers of the poor’, originallyrooted in domestic, local markets butincreasingly expanding into larger marketsand offering a broader range of services. He noted that the high operating costs,passed on to the customer in the form ofhigh interest rates, are a hurdle for the poor.Annibale encouraged institutions to try tomake their operations more cost-effective,because the customer inevitably pays forany inefficiencies. He felt that this waswhere there is potential for Islamic financeto make a difference.

Under conventional microfinance, risk isborne by borrowers and rarely held by the institutions. Non-governmentalorganisations (NGOs) and other non-profit institutions offer efficient services tosupplement their lending, but these servicesadd to the cost base. Islamic finance focuseson interest-free methods of providingcapital, because the Shari’ah holds lendingto be a purely charitable exercise, ratherthan a means of making a profit. Islamicfinance is also accustomed to methods ofrisk–reward sharing between the institutionand the borrower.

Taking a step back, Annibale then reviewedthe market, highlighting the work of theMicrofinance Information Exchange and itstransparent analysis of microfinance groups.He noted that there were only small-scale

microfinance offerings across North Africaand Pakistan and that competition in thispart of the world would be beneficial.Indonesia and Bangladesh, on the otherhand, have more developed microfinancemarkets. In fact, microfinance institutionsenjoy greater penetration than traditionalcommercial banks in Bangladesh.

Microfinance has grown significantly in India, but the industry there faces anumber of restrictions, imposed to protectcustomers from very high interest rates, aswell as objections raised against usury andexploitation from religious leaders. In hisclosing remarks, Annibale stressed that the industry is in need of competition and innovation if it is ultimately to be of benefit to its customers.

Aamir Rehman, former global head ofstrategy at HSBC Amanah, presented thesecond keynote address on behalf of IqbalKhan, HSBC Amanah’s founding CEO.Rehman considered the extent to which the Islamic finance ethos is compatible with the spirit of microfinance. From theperspective of the Shari’ah, Islamic financeshould focus on ethics and values thatencourage community-based, alternativeprogrammes to promote genuine economicactivity. As a nascent industry, however, itstill faces a number of challenges to itscredibility in the finance world. As a result,it has focused less on the alleviation ofpoverty in the past because it has beenworking to meet world-class bankingstandards and to serve its clients in aShari’ah-compliant way. At the same time as being seen as a viable system of financing,it has had to prove itself to be profitable aswell. While the social goals of the Shari’ahare important, Rehman stressed that Islamicfinance has to meet commercial standardsfirst. He added that the industry has had to move from a consumer-debt industry to a savings industry, dovetailed by micro-finance, because it assists businessdevelopment and economic activity.

If Islamic finance and microfinance couldconverge, the industry could reach a threebillion person market. Trade, Rehmanreminded the audience, has played an

integral part in the spread of Islam andIslam has a long history of valuing tradeand entrepreneurship. Moving on, Rehman described how traditional banksseek growth through the expansion ofcustomer debts while Islamic banks havetried to move away from this debt-basedapproach. He could envisage a paradigmshift in Islamic finance away from a‘Shari’ah-compliant’ to a ‘Shari’ah-based’industry, which uses its commercial servicesto partner with microfinance institutions with access to rural and poor communities.

Following these two keynote speeches,proposals for, and case studies of, Islamic microfinance were presented in the symposium’s first panel session. Thesession was moderated by Asim Khwaja,associate professor of public policy for the JFK School of Government, HarvardUniversity.

Opening with an alternative view ofmicrofinance, Samer Badawi of theConsultative Group to Assist the Poor(CGAP) expressed the view that, while there is evidence to support the value of microfinance, there is also alarmingevidence to the contrary. Microfinance is not reaching the poorest of the poor, even though this is its purpose, and loans are going to activities unrelated toentrepreneurship. Islamic finance could, in principle and in practice, correct thesedefects.

Professor Hans Dieter Seibel from the University of Cologne, Germany,presented a case study on Indonesia, thelargest Muslim country in the world, with a mixed history of Islamic microfinance.Seibel noted that Islamic microfinancebanks have statistically not done wellcompared with their conventionalcounterparts. Absentee ownership, together with a lack of competence inIslamic finance, have been partly respon-sible for this, but mudarabah savings andfixed deposits have still been successful.Seibel also emphasised that a proper legal framework and regulation of interest rates are important factors in the success of Islamic microfinance.

20 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007

The second session was moderated bySamuel L Hayes, III, Jacob Schiff professoremeritus of the Harvard Business School.The panellists spoke of the challenges of integrating Islamic finance withmicrofinance. Shari’ah scholar SheikhNizam Yaquby noted that the fight againstpoverty is an important one for Islam andfor microfinance. But he pointed out that,unlike conventional microfinance, Islamdoes not allow exploitation with higherreturns. Nadeem Hussain, president andCEO of Tameer Microfinance Bank,expressed his reservations that the lack of fundamental assets make it difficult toapply microfinance to Islamic finance.

The speakers also contended, however, thatthese issues could be resolved if people fromthe Islamic finance and microfinance sectorswere to work together. Aamir Rehman and Robert Annibale reiterated that ahybrid model, integrating philanthropic and commercial goals, or a not-for-profitmodel using charitable sources such aszakat, offer a relationship between theIslamic finance and microfinance industries.

Michael Ainley of the UK Financial Services Authority (FSA) compared thecurrent development of microfinance with Europe’s transition from credit unions and community banks to its contemporaryeconomic system. Ainley also noted theimportance of effective government reg-ulation and supervision of the industries in this process. Aqil Abdus Sabur, interimpresident of the Philadelphia CommercialDevelopment Corporation, linked thediscussion through microfinance aspractised by the Prophet Muhammad’s(PBUH) companions over a thousand years ago.

The panellists offered closing remarks,reminding the audience of Islam’s history in finance and the scope of potential forIslamic microfinance. This is a project thatis growing in the US and the UK, as well asin the rest of Europe, the Middle East, andAsia. As Sheikh Nizam Yaquby advised thesession, however, it is important to bear inmind that the goal is to eliminate poverty,not to cloak goals to exploit people.

Contrasting Afghanistan with Indonesia,Siraj Sait, a senior lecturer in law at theUniversity of East London, talked about the Global Land Tool Network (GLTN),which uses Islamic land tools as a means ofempowering the poor. The goal is to createpro-poor, scalable, and replicable tools; tocross-fertilise generic tools with Islamictools; and to define stakeholders. He alsohighlighted end-user scepticism overShari’ah compatibility and lack of stateregulation as representing challenges for the industry.

Taha Abdul Basser, a Ph.D. candidate atHarvard University, presented a paper by Dr Muhammad Anas Zarqa, advisor to the International Investor company. Basserexplained that, as a young industry, Islamicfinance still has to focus on social justice. Inorder to do so, it has to be more convincingto its clients and it needs to hone managerialtalent. Basser discussed the viability of theIslamic instrument of monetary waqf (cashtrust) as a means of financing Shari’ah-compliant microfinance. In addition toinitial donations, a monetary waqf furthermobilises temporary funds that can beextended to the productive poor asmicrocredits. Basser presented Dr Zarqa’sopinion that there should additionally betwo tiers of philanthropic guarantors for a monetary waqf to strengthen its securitystanding: guarantors of liquidity andguarantors of losses. Not only would this help to increase the credit standing of a waqf, but it would also attract aconsiderable quantity of temporary funds.

Saif I Shah Mohammed, from the ColumbiaUniversity School of Law, spoke next. Heagreed with Badawi that microfinance hadbeen over-hyped. Mohammed was of theview that a partnership between Islamicfinance and microfinance would offer thebest approach, especially in the case ofBangladesh. He pointed out, however, thatIslamic microfinance institutions need toovercome distrust in the microfinancemarket and clarify terms that have in thepast caused confusion. Mohammed alsoappealed to Shari’ah scholars to take aproactive role in clarifying these terms for the population.

SYMPOSIUM REVIEW

If Islamic finance andmicrofinance could converge,the industry could reach a three billion person market.

I like to believe that we are oneof the last banks to get anIslamic licence [in Pakistan].

Nikolaus Rafiq Schwarz,FDIB CEO

dynamic segment, especially while furthercompetition is effectively being stifled. Infact, the Karachi-based single-branch FDIBis touting aggressive growth plans byscheduling another eight offices for openingthis year alone.

The percentage of booked Islamic assets todate is proof-positive for Schwarz that thereis considerable ‘room for growth’, to thepoint where the market, despite what SBPsays, could even ‘digest a couple moreIslamic financial institutions’.

The mention of Malaysia in the openingparagraphs is no idle reference. Schwarzbelieves the development of the Islamicbanking market in Pakistan is taking asimilar route to that of the South East Asian country.

Here, the government has a highlysupportive Islamic banking framework thatit has built up over the past 15 or 20 years,allowing it to harbour almost a quarter ofall banked assets in the country.

Malaysia and Pakistan share a structuralapproach to banking that is not found in theGCC for example, being considerably morein favour of universal banking operations,whereas the GCC region prefers to offermore niche investment and private banking-type services.

Whether Pakistan can emulate Malaysia’seconomic pattern is yet to be seen, ofcourse. But FDIB’s wide-open remit to catch as much corporate and consumertrade as possible seems to be in tune withthe brandishing of its heroic growth

22 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2007

issuing any more new banking licences inthe foreseeable future. ‘I like to believe thatwe are one of the last banks to get anIslamic licence [in Pakistan],’ says FDIB’sCEO, Nikolaus Rafiq Schwarz, convincedof FDIB’s good fortune.

And as the head of a new, lean operationwith a universal banking remit, Schwarz issetting his sights on taking advantage of this

CASE STUDY

Despite Pakistan being an Islamic country,its banking market has to date remainedmostly served by non-Islamic institutions.But, as with the Malaysian market some 20 years ago, it is changing – and changing fast. With the total assets of Islamicbanking institutions in the country almosttripling to 54 billion rupees ($899.1million) in the fiscal year 2006, from 18.8billion rupees ($313.02 million) at the endof 2005, the local market is taking on adecidedly wholesome new shape.

Although Islamic-banked assets currentlyonly represent around three per cent of thetotal in Pakistan, Islamic banking is clearlyreaching out to its people more than ever. It is now available in 16 cities in all fourprovinces of the country through fully-fledged Islamic banking operations – bankssuch as Meezan Bank, Al Baraka IslamicBank, BankIslami Pakistan, EmiratesGlobal Islamic Bank, and Dubai IslamicBank Pakistan. But in addition to theseexclusively Islamic financial institutions,some 39 branches of eleven conventionalbanks are also providing exclusively Islamicbanking services to their customers.

And with the likes of Qatar Islamic Bankknown to be looking to make an entranceinto Pakistan, it could not have been morefortuitous for First Dawood Islamic Bank(FDIB) to have opened its doors last Aprilas the sixth fully Islamic bank in thecountry, just as the State Bank of Pakistan’s(SBP) attitude to licensing changed.

It now looks rather as if SBP is to draw aline under the 40 or so banks currentlyoperating in the country and will not be

Sixth sense It’s a well known fact that the take-up of Islamic banking is expanding at a rate of knots acrossthe globe. But how is it faring in an Islamic heartland such as Pakistan? Tom Alford,NewHorizon’s contributing editor, talks to a new entrant in that market, First Dawood IslamicBank, to find out the state of play.

Shari’ah-permissible raw materials andcommodities. In addition, an ijara wa iqtina(Islamic leasing) facility provides finance forthe purchase of machinery and equipmentfor new projects and business expansion.

Car ijara and housing finance are availablefor the salaried and self-employed, while thediminishing musharakah facility providesfinance for capital expenditure in theconstruction and manufacturing industries.In the trade finance realm, as a first inPakistan, FDIB is also offering under the Al-Mustaqeem brand, a service ijaraproduct, a post-shipment export facility and a local goods supply finance product. ‘FDIB is also offering a very innovativerunning musharakah facility,’ says Schwarz.

The bank’s first tough test will come in theform of regional commercial competitionfrom global banks such as HSBC Amanah,Deutsche Bank and Citibank. These tier oneinstitutions are potentially a threat to asmall operation like FDIB.

Although he believes many of the Islamicoffshoots of the global players in Pakistando not really cover ‘the full spectrum ofcorporate finance and consumer finance’,Schwarz is realistic enough to acknowledgethat if any of these banks decided to stepinto the fully-fledged Islamic bankinglimelight with a fuller set of products, theirvast scales of economy would be ‘verydifficult’ to overcome.

For now though, he remains ‘veryoptimistic’ about FDIB’s prospects.Although over the next twelve months or so the bank intends to stay within Pakistan’sborders protecting its rapidly expandinglocal interests, the exponential growth ofIslamic banking in the region will surely see FDIB adding to its client base.

There’s no shortage of willing customers.Indeed, wherever an Islamic financialinstitution opens in Pakistan, Schwarz,clearly happy to scoop up the new business,reports waves of clients ‘closing their ac-counts with non-halal banks’ and movinginto the world of Shari’ah-compliantbanking.

experience to stand a chance of seriouslycompeting with the bigger, more establishedplayers in Pakistan.

The technology may help deliver efficiencyand customer delight, but how does itsproduct-set stand up? Although Schwarzdescribes FDIB’s initial offering as ‘plainvanilla’, he is quick to explain that this is allpart of the plan to get the single-branchoperation established before engaging inmore complex and exotic instruments for itscorporate and private customers. ‘First weneed to establish ourselves as a crediblefinancial institution in Pakistan,’ he states.

The follow-on offering is likely to include a unique (for Pakistan) ijara product toenable customers to save for their Hajj and Umra. Continuing the Malaysianconnection, this sort of product has beenavailable in that country since 1963 and isnow administered by Lembaga TabungHaji, or the Pilgrim Fund Board ofMalaysia.

FDIB is also looking to offer differentiationin structured finance products, partly as abenefit of its major shareholders’ ownbanking know-how. ‘This is what we would like to focus on in the comingmonths,’ says Schwarz, stressing that theidea is not to create two pillars of bankingwhere an investment banking divisionworks ‘in parallel’ with a corporate bank-ing division: ‘It confuses customers,’ saysSchwarz.

With the emphasis on being a unifiedoperation, FDIB is looking to expand itsclient portfolio quickly but progressively.After eight to twelve months of growth, itintends to return to its clients with moresophisticated offerings and engage in someserious cross- and up-selling.

For now though, FDIB’s ‘plain vanilla’offering encompasses deposits under thebranding of Al-Mustaqeem, such as current accounts, saving accounts, termdeposits, receipts and basic bankingaccounts. It also delivers Al-Mustaqeembranded financing which includes amurabaha facility for the purchase of

www.newhorizon-islamicbanking.com IIBI 23

NEWHORIZON Rajab–Ramadan 1428

strategy. Although in terms of capitalisationit is, in Schwarz’s words, ‘a lot smaller thanmost of the Islamic institutions’, FDIB is still in a reasonably strong financial position to reach out to the local market in flamboyant fashion.

Prior to opening its doors for business, it had secured initial capital of two billionrupees ($33.3 million), with its three majorinvestors each taking a 21 per cent stake.Bahrain-based Unicorn Investment Bank,Pakistan’s First Dawood Group, and theIslamic Corporation for the Development ofthe Private Sector (a unit of Jeddah-basedIslamic Development Bank) are now happyto promote the aggressive growth planespoused by Schwarz and his board. Inaddition to the branches to be opened by the end of this year, the blueprint talks of afurther 18 branches and offices openingthroughout 2008.