issues for canadians: economic systems in canada and the united states

TRANSCRIPT

Chapter 6To what extent do different economic systems affect quality of life?

CHAPTER 6TO WHAT EXTENT DO DIFFERENT ECONOMIC SYSTEMS AFFECT QUALITY OF LIFE?

Issues for Canadians: Economic Systems in Canada and the United States

Economic Systems and Quality of Life

Definitions: Match the following terms with their definitions. Place the according letter beside each

word.

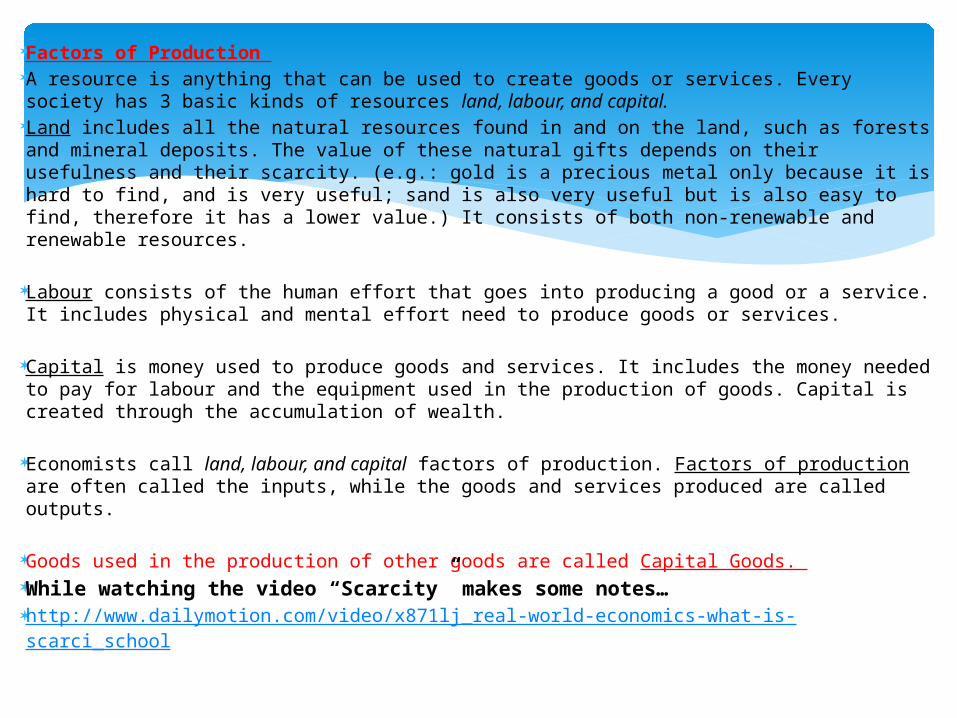

Factors of Production A resource is anything that can be used to create goods or services. Every society

has 3 basic kinds of resources land,labour,andcapital. Land includes all the natural resources found in and on the land, such as forests

and mineral deposits. The value of these natural gifts depends on their usefulness and their scarcity. (e.g.: gold is a precious metal only because it is hard to find, and is very useful; sand is also very useful but is also easy to find, therefore it has a lower value.) It consists of both non-renewable and renewable resources.

Labour consists of the human effort that goes into producing a good or a service. It

includes physical and mental effort need to produce goods or services. Capital is money used to produce goods and services. It includes the money

needed to pay for labour and the equipment used in the production of goods. Capital is created through the accumulation of wealth.

Economists call land,labour,andcapital factors of production. Factors of production are often called the inputs, while the goods and services produced are called outputs.

Goods used in the production of other goods are called Capital Goods. While watching the video “Scarcity” makes some notes… http://www.dailymotion.com/video/x871lj_real-world-economics-what-is-

scarci_school

What are the three basic economic questions? What is the basic rule of Economics?

Explain the difference between a need and a want. Give several examples of each.

Briefly describe the three factors of production.

What impacts might the decision to use “the LAND” have on the land and the people?

In your opinion, which method of organizing the

economy of a country would be most fair to the average person? Why?

How does economic decision making affect the

jobs available to you and your family?

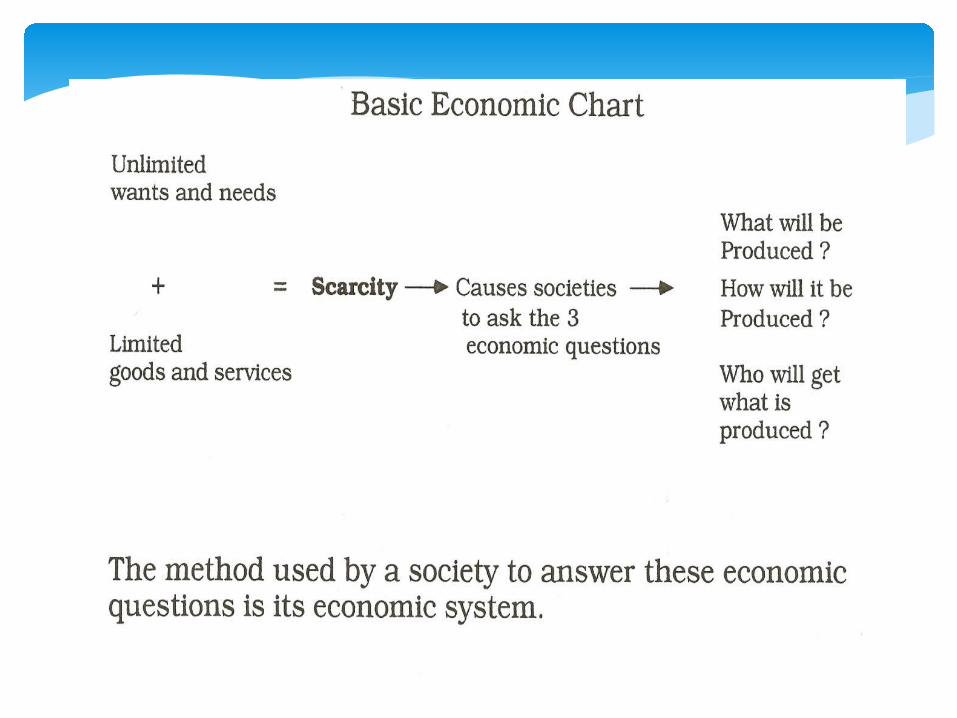

In order for the resources of a society to be shared among the people, there must be some form of organization. This sharing helps resolve the issues experienced with scarcity. You can put them on a continuum, like the one below.

An economic system’s position on the continuum is dynamic, and depends on the underlying values of a society and its government. The positions of Canada and the U.S. on the continuum below reflect a traditional perspective on differences between their economies. Their actual positions on the continuum shift right and left, depending on the political party in power.

PLANNED ECONOMY In the planned economy the economic questions are answered by a central

authority (the government). The government makes all of the decisions about the economy. Historically, it has been an absolute monarch, a dictator, or an elite group for example the former USSR (Russia).

Characteristics include: • Resources are publicly owned. • Government makes decisions on how to use resources. • Individual consumers have little influence on economic decision making.

What is an Economic System? Pages 204

MIXED ECONOMY A mixed economy combines private ownership and

government control. For example, private businesses own some resources and the government owns others. In mixed economies, the level of government involvement fluctuates depending what political party is in power.

Characteristics include: • Some resources are publicly owned and some are

privately owned. • Individuals and government both make decisions about

what to produce. • Individual consumers and government influence

economic decision making. MARKET ECONOMY A market economy is a system where the collective

economic decisions of the individual buyers and sellers shape the economy of the whole society. In this system, buyers establish demands that sellers attempt to meet.

Through give and take, buyers and sellers both meet their needs as best they can. The government does not get involved. The economy is run on the basis of the individual decisions made by buyers and sellers.

Characteristics include: • Resources are privately owned. • Individuals make decisions on how to use resources. • Individual consumers drive economic decision making by

choosing what to buy. Remember that societies are forced to create economies

because they cannot have everything they want. Resources are limited, and they must be shared among the people of the society. Therefore the basic rule of economics is:

The basic rule of economics is that you cannot have everything!

Economic Models Explained with Cows:

SOCIALISM You have 2 cows. You give one to your neighbor. COMMUNISM You have 2 cows. The State takes both and gives you some

milk. Mixed Economy You have 2 cows. The State regulates the production of

milk, asks for some taxes from the owner, you are able to buy and/or sell the milk, but must pay more taxes on the processed milk.

NAZISM (FASCISM) You have 2 cows. The State takes both and shoots you.

BUREAUCRATISM You have 2 cows. The State takes both, shoots one, milks the other, and then

throws the milk away...

TRADITIONAL CAPITALISM You have two cows. You sell one and buy a bull. Your herd multiplies, and the economy grows. You sell them and retire on the income.

What’s an Economic System? Pages 204 – 208

In your own words, what is an economic system?

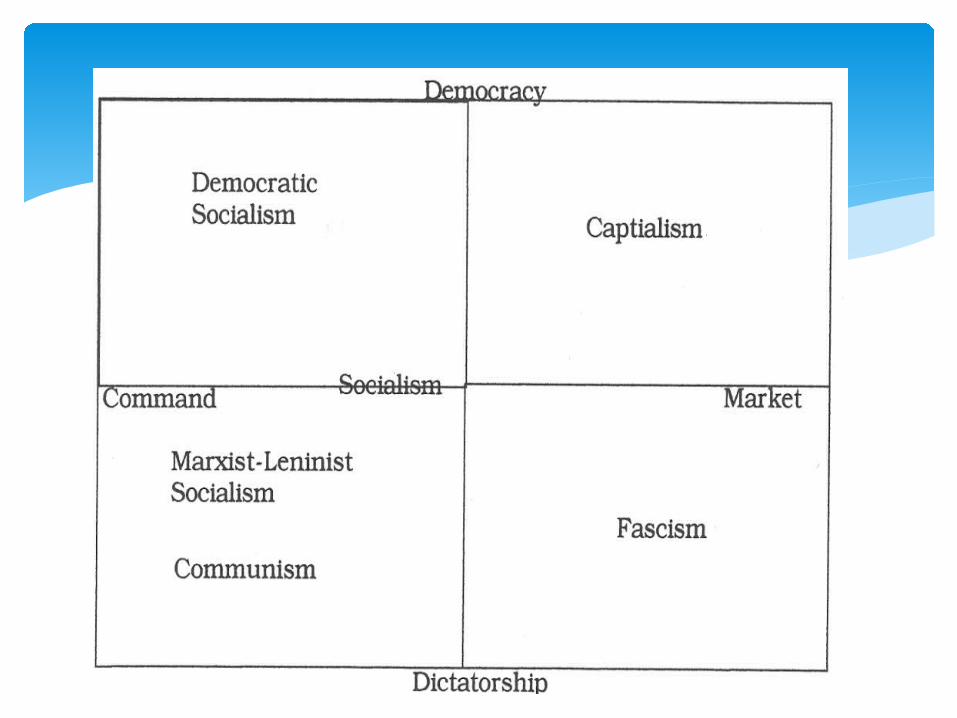

THE ECONOMIC CONTINUUM

Planned Economy

Mixed Economy

Market Economy

-

Characteristics: Characteristics: Characteristics:

Canadian Economic History versus U.S.A. Economic History

“THE PUBLIC GOOD” What does this mean? Compare how Canada & the USA differ in

their views about “the public good”. CANADA: COOPERATION USA: INDIVIDUALISM Why do you think we have answered the question

differently at different points in our histories?

Canadian Economy US Economy

Founding Principles Founding Principles

Values: Values:

CROWN CORPORATIONS

Why does Canada have crown corporations? Identify two crown corporations the government has sold to private

enterprises. Why do you think they sold these? Identify two crown corporations the government still owns. What connection is there between collective rights and crown

corporations? What connection is there between identity and crown corporations?

Canada USA

Shift Left Shift Right

Shift Right Shift Left

SUPPLY & DEMAND: How do market economies work?Use the information on

pages 209-211 to help you fill out this information.

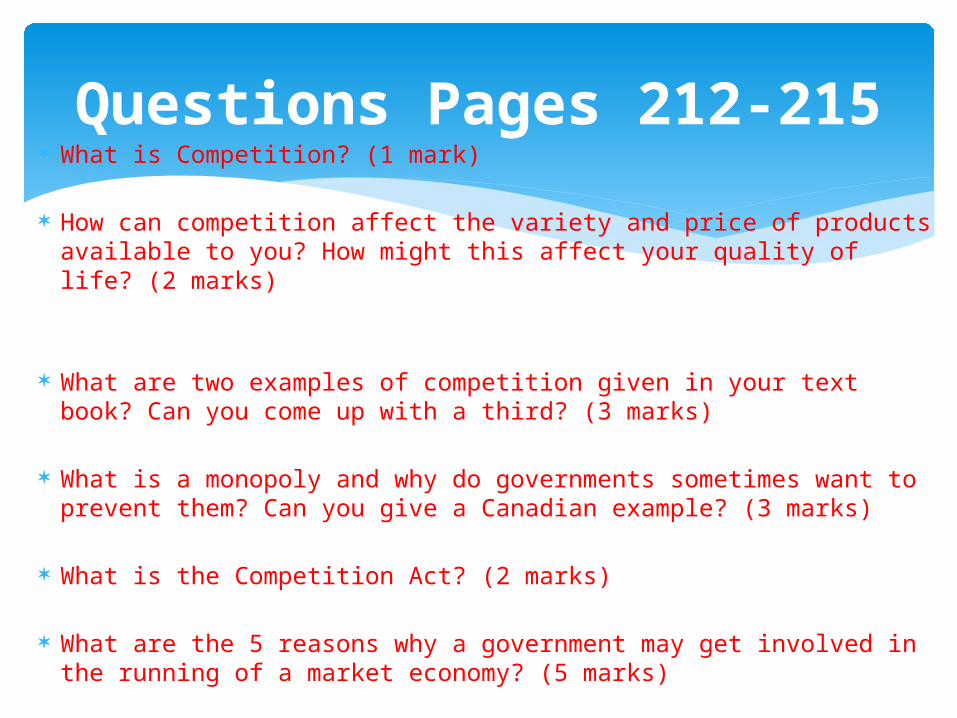

What is Competition? (1 mark) How can competition affect the variety and price of products

available to you? How might this affect your quality of life? (2 marks)

What are two examples of competition given in your text book? Can you come up with a third? (3 marks)

What is a monopoly and why do governments sometimes want to prevent them? Can you give a Canadian example? (3 marks)

What is the Competition Act? (2 marks)

What are the 5 reasons why a government may get involved in the running of a market economy? (5 marks)

Questions Pages 212-215

As a class discuss the following cartoon.