issues in revised schedule vi -...

TRANSCRIPT

Issues in Revised Schedule VIIssues in Revised Schedule VI

SUSHRUT CHITALE205A, AGRAWAL SHYAMKAMAL, VILE PARLE EAST, MUMBAI -400057

Landline: +91-22-2614 3127 website: www.mmchitale.com

15 July 201215 July 2012

Overview of Presentation• Background and Applicability

• Significant Features

• Major Changes

• Structure of Revised Schedule VI

• Form of Balance Sheet

• Statement of Profit and Loss

• Comparison with Existing Schedule VI

SUSHRUT CHITALE 2

Background and ApplicabilityRevised Schedule VI is primarily necessitated due to the followingreasons:

• To harmonize and synchronize with IFRS/Ind AS

• Comparison of financial statements with global companies

• Liquidity Based Presentation-Current vs. Non-currentclassification

• Enhancing the disclosure requirements - Changes in outdateddisclosures and eliminate redundant disclosures

SUSHRUT CHITALE 3

Background and Applicability• Notification for Schedule VI was issued by MCA vide S.O.No.441

dated March 21, 1961.

• Ministry of Corporate Affairs issued Original Notification –S.O.No.447(E) dated February 28, 2011 specifying requirementsof Revised Schedule VI. This was amended on March 30, 2011specifying applicability for financial statements commencing onor after April 1, 2011.

• Guidance Note to Revised Schedule VI to the Companies Act, 1956issued by ICAI(Dec. 2011).

• ICAI has also come out with FAQs on revised schedule VI

SUSHRUT CHITALE 4

Background and Applicability• Applicable to all Companies, except those referred to in Proviso to

Section 211(1) and Section 211(2) of the Companies Act,1956,i.e. Banking Companies or

Insurance Companies orElectricity Companies,

which are required to prepare financial statements in a formatprescribed by another statute.prescribed by another statute.

• However, neither the Electricity Act, 2003 nor the Rules framedthereunder prescribe any specific format, hence ElectricityCompanies are to follow Revised Schedule VI.

SUSHRUT CHITALE 5

Background and ApplicabilityQuestion: CALENDAR YEAR

• A company prepares its financial statements for calendar year2011, but prepares its tax accounts as per financial year – FY12?Whether, revised schedule VI will be applicable for financialstatements for FY12?

Yes, Revised Schedule VI is applicable for the financial yearcommencing from on or after 1 April,2011. So for tax accounts,revised schedule VI will be applicable.

SUSHRUT CHITALE 6

Background and ApplicabilityQuestion: IPO/FPO FILINGS

• A company wants to file for IPO/FPO in July 2012. Whetherfinancial statements (including past 5 years numbers) should beprepared using revised schedule VI or old schedule VI?

As per MCA’s General Circular No.62/2011 dated 5th

September,2011, the presentation of financial statements for thelimited purpose of Initial Public Offer/Further Public Offer duringlimited purpose of Initial Public Offer/Further Public Offer duringFY 2011-12 maybe in the format of Old Schedule VI under theCompanies Act, 1956, as reclassifying previous year’s figures inaccordance with Revised Schedule VI would be difficult and makecomparables unrealistic. However, for period beyond 31st March2012, they would prepare only in the new format as prescribed bythe present Schedule VI of the Companies Act, 1956.

SUSHRUT CHITALE 7

Significant Features• Vertical Format only. Horizontal Format is withdrawn.• Format of Profit and Loss is introduced for the first time.• Part IV – Balance Sheet Abstract and Company’s Business Profile –

Omitted.• Based on Accounting Standards.• Concept of Schedules eliminated.• All information in Notes with Cross Referencing.• All information in Notes with Cross Referencing.• Simplification of Disclosure Requirements.• Striking Balance to be maintained between providing excessive

details and not providing important information as a result of toomuch aggregation.

• Rounding off (where opted for) simplified.• Explicit requirement to use the same unit of measurement

uniformly throughout the financial statements.

SUSHRUT CHITALE 8

Significant Features• Requirements of the Act and/or Notified Accounting Standards will

prevail over the Schedule.

• Minimum requirements are specified. They are in addition to and notin substitution of the disclosure requirements specified in theAccounting Standards .

• Other Disclosures as required by Companies Act and other legal• Other Disclosures as required by Companies Act and other legalrequirements shall be made in the notes to accounts.

• Comparatives (including corresponding amounts and notes) forthe immediately preceding reporting period shall also be given.

• Terms Used herein shall be as per the applicable Accounting Standards.

• The Schedule shall stand modified in accordance with any changes intreatment or disclosure as per the Act/ Accounting Standards.

SUSHRUT CHITALE 9

Major Changes in Balance Sheet• Equity and Liabilities will be written instead of Sources of Funds.• Assets will be written instead of Application of Funds.• Liabilities & assets will be classified under two heads Current and Non

Current.• Fixed Assets will be classified into Tangible Assets and Non-Tangible

Assets. Movement during the year is to be given in addition to Openingand Closing Balances on the face of the Balance Sheet.

• Money received against share warrants is a new line item in equity. It isclassified as a separate component of Equity.classified as a separate component of Equity.

• Share Application Money pending allotment is a new line item which isclassified in between equity and liabilities.

• Deferred Tax Assets/Liability(Net) shall be classified under the headNon-Current Assets / Non-Current Liabilities.

• Debit Balance of Profit & Loss A/c or Accumulated Losses will be shownas a negative figure under “Reserves & Surplus”.

• Current maturities of a long term borrowing will have to be classifiedunder the head “Other Current Liabilities.”

SUSHRUT CHITALE 10

Major Changes in Profit and Loss • Now termed as ‘Statement of Profit and Loss for the year ended……’.• Format specified in Revised Schedule.• Disclose by nature of expense. Functional classification is prohibited.• Exceptional and extraordinary items need to be disclosed separately

on the face of the Statement of Profit and Loss.• The items to be disclosed under Revenue from Operations have been

specifically indicated for both finance companies and others.• Any item of income or expenditure which exceeds one percent of the• Any item of income or expenditure which exceeds one percent of the

revenue from operations or Rs. 100,000, whichever is highershould be disclosed separately.

SUSHRUT CHITALE 11

Disclosures No Longer Required

• Investments purchased and sold during the year.• Investments, Sundry Debtors and Loans and Advance pertaining

to companies under the same management.• Break up of Bank Balances between Scheduled and Other banks,

break up between current account, call account and depositaccounts, Details of names, amount, maximum amounts with non-scheduled bank.

• Commission, brokerage and non-trade discounts paid to sellingagents.

• Managerial Remuneration u/s. 198 and computation of net profitsfor calculation of commission.

• Information on licensed capacity, installed capacity and actualproduction.

SUSHRUT CHITALE 12

Structure of Existing Schedule VI

• Part I – Form of the Balance Sheet–Option betweenA. Horizontal Form andB. Vertical Form

• General Instructions for preparation of Balance Sheet

• Part II – Requirements as to Profit and Loss Account

• Part III – Interpretation – for the purpose of Parts I and II ofSchedule VI unless the context otherwise requires

• Part IV – Balance Sheet abstract and Company’s General businessprofile

SUSHRUT CHITALE 13

Structure of Revised Schedule VI

• General Instructions

• Part I – Form of the Balance Sheet

• General Instructions for preparation of Balance Sheet

• Part II – Form of Statement of Profit and Loss• Part II – Form of Statement of Profit and Loss

• General Instructions for preparation of Statement of Profit andLoss

SUSHRUT CHITALE 14

Part I – Form of the Balance Sheet

(Rupees in…)

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

I EQUITY AND LIABILITIES

(1) Shareholders’ Funds

(a) Share Capital(a) Share Capital

(b) Reserves and Surplus

(c) Money received against ShareWarrants

(2) Share Application Money pendingallotment

SUSHRUT CHITALE 15

Part I – Form of the Balance Sheet

(Rupees in…)

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

I EQUITY AND LIABILITIES

(3) Non-Current Liabilities(3) Non-Current Liabilities

(a) Long-Term Borrowings

(b) Deferred Tax Liabilities (Net)

(c) Other Long Term Liabilities

(d) Long-Term Provisions

SUSHRUT CHITALE 16

Part I – Form of the Balance Sheet(Rupees in…)

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

I EQUITY AND LIABILITIES

(4) Current Liabilities

(a) Short-Term Borrowings

(b) Trade Payables

(c) Other Current Liabilities

(d) Short-Term Provisions

TOTAL

SUSHRUT CHITALE 17

Part I – Form of the Balance Sheet(Rupees in…)

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

I ASSETS

(1) Non-Current Assets

(a) Fixed Assets

(i) Tangible Assets

(ii) Intangible Assets

(iii) Capital Work-In-Progress

(iv) Intangible Assets under Development

SUSHRUT CHITALE 18

Part I – Form of the Balance Sheet(Rupees in…)

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

II ASSETS

(1) (b) Non-Current Investments

(c) Deferred Tax Assets (net)

(d) Long-Term Loans and Advances

(e) Other Non-Current Assets

(2) Current Assets

(a) Current Investments

(b) Inventories

SUSHRUT CHITALE 19

Part I – Form of the Balance Sheet

(Rupees in…)

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

II ASSETS

(c) Trade Receivables

(d) Cash and Cash Equivalents

(e) Short-Term Loans and Advances

(f) Other Current Assets

TOTAL

See accompanying notes to financial statements

SUSHRUT CHITALE 20

Share CapitalDisclosure for each class of share capital (different classes ofpreference shares to be treated separately) :

• Number and Amount of shares authorized,• Number of shares issued, subscribed and fully paid, and

subscribed but not fully paid,• Par Value per share,• Reconciliation of the number of shares outstanding at the• Reconciliation of the number of shares outstanding at the

beginning and at the end of the reporting period,• Rights, preferences and restrictions attaching to each class of

shares,• Shares held by entire chain of Subsidiaries and Associates starting

from holding company and ending right upto the ultimate holdingcompany,

SUSHRUT CHITALE 21

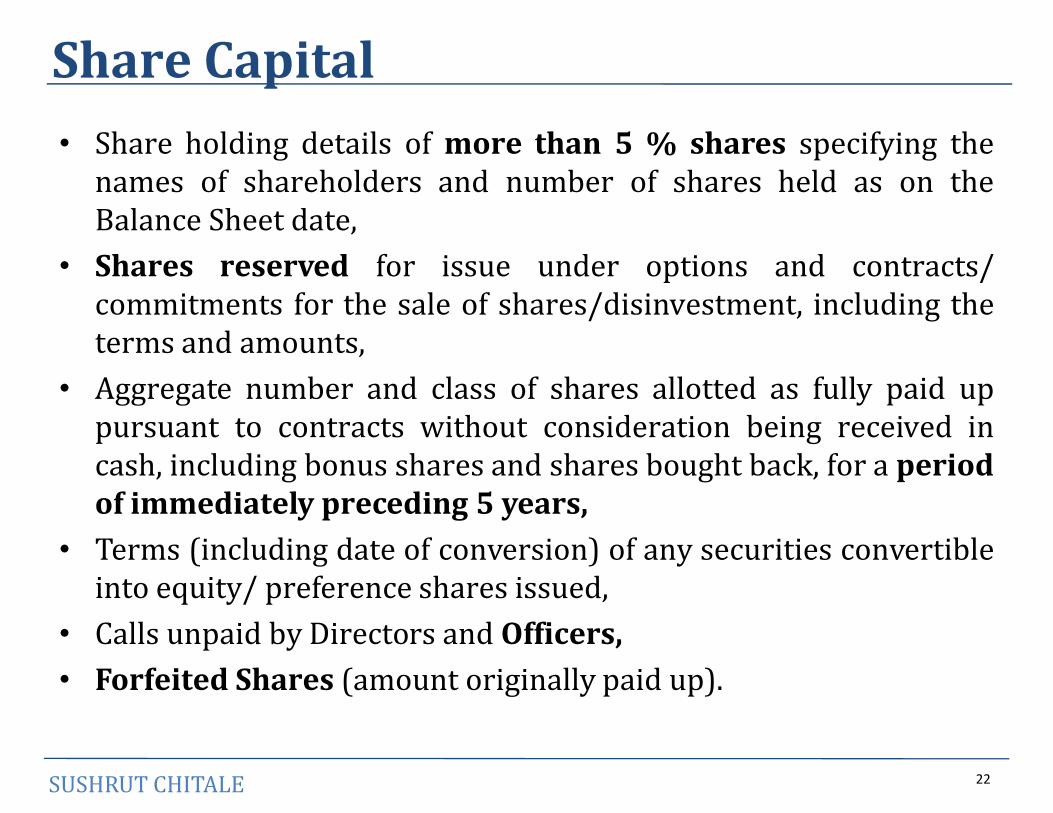

Share Capital• Share holding details of more than 5 % shares specifying the

names of shareholders and number of shares held as on theBalance Sheet date,

• Shares reserved for issue under options and contracts/commitments for the sale of shares/disinvestment, including theterms and amounts,

• Aggregate number and class of shares allotted as fully paid uppursuant to contracts without consideration being received incash, including bonus shares and shares bought back, for a periodof immediately preceding 5 years,

• Terms (including date of conversion) of any securities convertibleinto equity/ preference shares issued,

• Calls unpaid by Directors and Officers,• Forfeited Shares (amount originally paid up).

SUSHRUT CHITALE 22

Share CapitalQuestion: PREFERANCE SHARES-LIABILITY OR EQUITY

• Revised Schedule VI states that different classes of PreferenceShares are to be treated separately. Whether Preference Sharesshould be presented as share capital or a company compulsorilyneeds to decide whether they are liability or equity based on itseconomic substance using AS-31?

Revised Schedule VI deals with only presentation and disclosurerequirements. Accounting for various items is governed by AS.However, as AS-30,31 and 32 on Financial Instruments are yetto be notified and Section 85(1) of the Act refers to PreferenceShares as a kind of Share Capital, they will have to be classified asShare Capital.

SUSHRUT CHITALE 23

Reserves and Surplus• Classified as:- Capital Reserves, Capital Redemption Reserve,

Securities Premium Reserve, Debenture Redemption Reserve,Revaluation Reserve, Share Options Outstanding Account,Other Reserves (residual),

• Surplus, i.e. balance in Statement of P&L disclosing allocationsand appropriations such as dividend, bonus shares and transferto/from reserves etc.

• Movement under each Reserve is to be shown,• Reserves specifically represented by earmarked investments shall

be termed as Fund.• Debit balance of statement of profit and loss to be shown as a

negative figure under the head ‘Surplus’.

SUSHRUT CHITALE 24

Money Received Against Share Warrants• Issued to promoters and others, in case of listed companies, in

terms of Guidelines for Preferential Issues (i.e. SEBI(ICDR) Guidelines, 2009.

• AS 20 defines Share Warrants as ‘financial instruments which give the holder the right to acquire equity shares.’

• Disclosed as a separate line item, since shares are yet to be allotted against the same.

SUSHRUT CHITALE 25

Share Application Money Pending Allotment

• Disclosed between ‘Shareholders’ Fund’ and ‘Non-CurrentLiabilities.’

• Share application money not exceeding the issued capital andto the extent non-refundable can only be classified under thishead – as ‘Equity.’

• Other amounts to the extent refundable, including interest – tobe classified as ‘Other Current Liabilities.’

• If a company’s Authorized Share Capital is not sufficient to coverallotment of fresh shares on account of share application money –to be disclosed under ‘Other Current Liabilities.’

• Other disclosures include: Terms & conditions, No. of sharesproposed to be issued, premium, if any, period before whichshares shall be allotted, reasons, including period, in case it ispending beyond the period of allotment.

SUSHRUT CHITALE 26

Non-Current LiabilitiesLONG-TERM BORROWINGS:

• Classified as Bonds/Debentures, Term Loans from banks andother parties, Deferred payment liabilities, Deposits, Loans andadvances from related parties, Long term maturities of financelease obligations, Other loans and advances.

• Further sub-classification into Secured and Unsecured specifyingthe nature of security, rate of interest and other terms ofrepayment.

• Loans guaranteed by directors and others to be specified.• Period and amount of continuing default as on the balance sheet

date in repayment of loans and interest, to be specifiedseparately in each case.

SUSHRUT CHITALE 27

Non-Current LiabilitiesDEFERRED TAX LIABILITES(NET):

• AS 22 simply specifies that they should be presented separately.Now, to be specifically disclosed under Non-Current Liabilities.

OTHER LONG TERM LIABILITIES:• Classified as Trade Payables and Others.

LONG TERM PROVISIONS:• Classified into Provision for Employee Benefits and Others.• AS-15 governs the measurement of various employee benefit

obligations, but classification as Current and Non-CurrentLiability will be governed by Revised Schedule VI.

SUSHRUT CHITALE 28

Current Liability A liability shall be classified as current when it satisfies any of

the following criteria:• it is expected to be settled in the company’s normal operating

cycle;• it is held primarily for the purpose of being traded;• it is due to be settled within twelve months after the reporting

date; or• the company does not have an unconditional right to defer• the company does not have an unconditional right to defer

settlement of the liability for at least twelve months after thereporting date.

All other liabilities shall be classified as Non-Current.

SUSHRUT CHITALE 29

Current vs. Non Current Liabilities• Classification will depend on facts of each case, rights/obligations

of parties, past experience, etc.

EXAMPLES• If Loan is repayable within 12 months – Current.

• If Loan is repayable after 12 months and if the company is• If Loan is repayable after 12 months and if the company isexpected to exercise option available to it to pre-pay – Current.

• If Loan is not repayable after 12 months and if the company is notexpecting to exercise option available to repay – Non-Current.

SUSHRUT CHITALE 30

Operating Cycle• An Operating Cycle is the time between the acquisition of

assets for processing and their realization in cash or cashequivalents.

• Where the normal operating cycle cannot be identified, it isassumed to be of duration of 12 months.

• Generally, it is calculated as:Average Inventory Holding Period(+) Average Production Period(+) Average Collection Period

• Creditors payment period is not reduced while computingoperating cycle

SUSHRUT CHITALE 31

Operating CycleQuestion: OPERATING CYCLE

• An entity manufactures passenger vehicles. Time betweenpurchasing of raw materials for manufacture & completion ofmanufacture and delivery to customers is 11 months. Dues aresettled after period of 8 months from date of sale. Will Inventoryand the Trade Receivables be Current or Non-Current in nature?

Both Inventory and Trade Receivables would be classified underCurrent Assets as the Operating Cycle is of 19 months (11months + 8 months).

Question:Q. Can operating cycle be calculated for each customer

separately?Q. Whether normal operating cycle be considered or actual?Q. Should the operating cycle be disclosed in Notes to Accounts?

SUSHRUT CHITALE 32

Trade Payables• A payable shall be classified as a trade payable if it is in respect of

the amount due on account of goods purchased or servicesrendered in the normal course of business.

• Payables towards the purchase of Capital items, amounts dueunder Statutory Obligations, etc. are not Trade Payables –classified as ‘Other Current Liabilities’.

• Acceptances are disclosed as Trade Payables.

• Trade Payable is to be bifurcated as Current & Non-Current basedon principles of Current/ Non-Current classification.

Question:Q. Where should salary payable to employees be disclosed?

SUSHRUT CHITALE 33

Current Liabilities• Classified as Short Term Borrowings, Trade Payables, Other

Current Liabilities and Short Term Provisions• Short Term Provisions are further classified as Provision for

employee benefits and others (eg., provision for dividend,taxation, warranties, etc.)

Question: DISCLOSURE FOR PROPOSED DIVIDEND• As per Revised Schedule VI, proposed dividend is required to be• As per Revised Schedule VI, proposed dividend is required to be

disclosed only in the notes. Whether it is required to be providedfor?

AS-4 requires dividends to be stated in respect of the period coveredby the financial statements, whether proposed or declared after theBalance Sheet date even before approval of the financialstatements. Hence, Proposed Dividend is required to be providedfor, unless AS-4 is revised.

SUSHRUT CHITALE 34

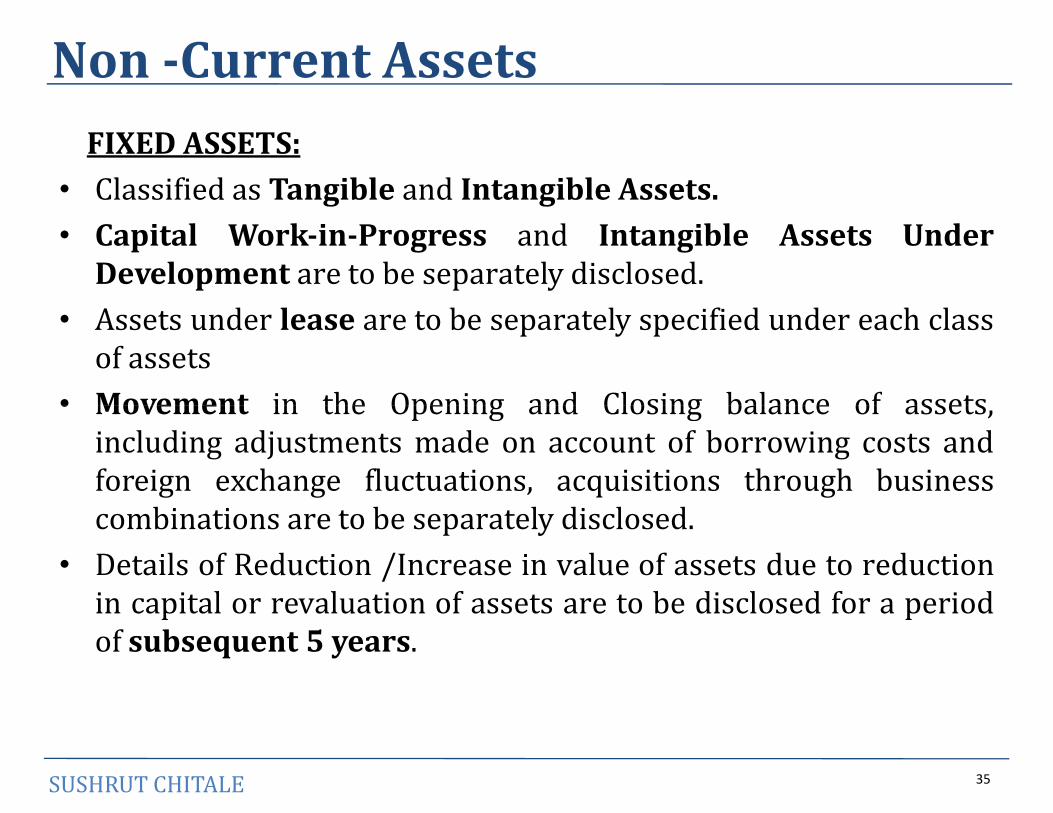

Non -Current AssetsFIXED ASSETS:

• Classified as Tangible and Intangible Assets.• Capital Work-in-Progress and Intangible Assets Under

Development are to be separately disclosed.• Assets under lease are to be separately specified under each class

of assets• Movement in the Opening and Closing balance of assets,• Movement in the Opening and Closing balance of assets,

including adjustments made on account of borrowing costs andforeign exchange fluctuations, acquisitions through businesscombinations are to be separately disclosed.

• Details of Reduction /Increase in value of assets due to reductionin capital or revaluation of assets are to be disclosed for a periodof subsequent 5 years.

SUSHRUT CHITALE 35

Non-Current AssetsNON-CURRENT INVESTMENTS:

• Classified as Trade Investments and Other Investments• Further classified as Investment in Property, Financial

Instruments, Partnership firms, Other Investments.• In case of Investment in Partnership Firms, names of firms

alongwith names of partners, total capital and share of eachpartner is to be given.partner is to be given.

• LLP is a body corporate and not a partnership firm – to bedisclosed under Other Investments.

• Aggregate amount of quoted/unquoted investments , marketvalue thereof, provision for dimunition in value of investments isalso to be disclosed.

SUSHRUT CHITALE 36

Non-Current AssetsDEFERRED TAX ASSETS(NET)

LONG-TERM LOANS AND ADVANCES:• Classified as Capital Advances, Security Deposits, Loans and

Advances to related parties,• Further sub-classification under Secured & Unsecured considered

good and Doubtful to be madegood and Doubtful to be made• Allowances for bad and doubtful loans to be made• Loans and advances due by directors, officers of the company and

their associated are to be disclosed separately.

OTHER NON-CURRENT ASSETS:• Classified as Long Term Trade Receivables and Others.

SUSHRUT CHITALE 37

Current AssetsAn asset shall be classified as current when it satisfies any of thefollowing criteria:

• It expects to realise the asset, or intends to sell or consume it, innormal operating cycle,

• It holds asset primarily for the purpose of trading,• It is expected to be realised within 12 months after reporting

period,period,• It is cash and cash equivalents, unless it is restricted from being

exchanged or used to settle a liability for at least twelve monthsafter the reporting date.

All others are to be treated as ‘Non-current’.

SUSHRUT CHITALE 38

Trade Receivables• A receivable shall be classified as a Trade Receivable if it is in

respect of the amount due on account of goods sold orservices rendered in the normal course of business.

• Trade Receivables outstanding for a period of 6 months from thedate they are due for payment should be separately shown.

(Old Schedule VI required separate presentation of debtorsoutstanding for a period exceeding 6 months(i.e. based on billingoutstanding for a period exceeding 6 months(i.e. based on billingdate) and other debtors.)

Question:Q. Can effective credit period be considered or actual credit

period as per invoice / contract be considered?

SUSHRUT CHITALE 39

Current AssetsCURRENT INVESTMENTS: Same principles of classification &

disclosure as applicable to Non-Current Investments.

INVENTORIES: Classified as Raw Materials, WIP, Finished Goods,Stock-in-Trade, Stores & Spares, Loose Tools & Others.

• Goods-in-Transit to be disclosed separately under relevant sub-head.head.

• Mode of valuation is to be stated.

TRADE RECEIVABLES: Further sub-classified as Secured andUnsecured considered good and Doubtful.

Question:Q. There may be certain loose tools / stores which are in nature

of slow moving inventory? Will they be still disclosed ascurrent assets?

SUSHRUT CHITALE 40

Current AssetsCASH AND CASH EQUIVALENTS:

• Classified as:-Balances with banks, Cheques/drafts on hand, Cashon hand, Others (specify nature).

• Earmarked balances with banks (eg., for unpaid dividend)to beseparately stated

• Separate disclosure for Balances with banks to the extent held asmargin money or security against the borrowings, guarantees,margin money or security against the borrowings, guarantees,other commitments, etc.

• Repatriation restrictions, if any, in respect of cash and bankbalances to be separately stated.

• Separate disclosure for Bank deposits with more than 12months maturity .

SUSHRUT CHITALE 41

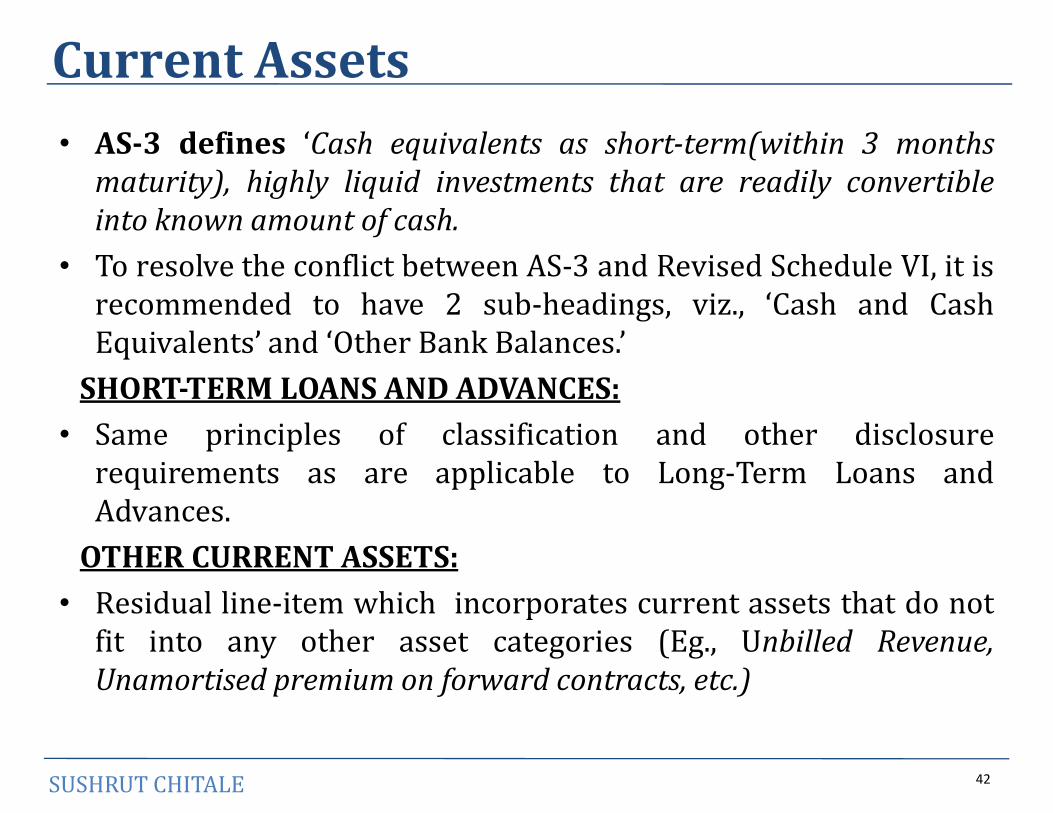

Current Assets• AS-3 defines ‘Cash equivalents as short-term(within 3 months

maturity), highly liquid investments that are readily convertibleinto known amount of cash.

• To resolve the conflict between AS-3 and Revised Schedule VI, it isrecommended to have 2 sub-headings, viz., ‘Cash and CashEquivalents’ and ‘Other Bank Balances.’

SHORT-TERM LOANS AND ADVANCES:• Same principles of classification and other disclosure

requirements as are applicable to Long-Term Loans andAdvances.

OTHER CURRENT ASSETS:• Residual line-item which incorporates current assets that do not

fit into any other asset categories (Eg., Unbilled Revenue,Unamortised premium on forward contracts, etc.)

SUSHRUT CHITALE 42

Contingent Liabilities And Commitments

Two separate classifications:(As a footnote to Balance Sheet)Contingent liabilities to be classified as:

• Claims against the company not acknowledged as debt,• Guarantees,• Other money for which the company is contingently liable.

Commitments to be classified as:• Estimated amount of contracts remaining to be executed on• Estimated amount of contracts remaining to be executed on

capital account and not provided for,• Uncalled liability on shares and other investments partly paid,• Other commitments (specify nature) which will include, non-

cancellable contractual commitments, cancellation of whichresults in a penalty disproportionate to the benefits involved.

SUSHRUT CHITALE 43

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

I Revenue from OperationsII Other IncomeIII Total Revenue ( I + II )IV Expenses:

Part II –Form of Statement of Profit and Loss(Rupees in…)

IV Expenses:

Cost of Material Consumed

Purchases of Stock-in-Trade

Changes in Inventories of Finished Goods, Work- in-Progress and Stock-in-Trade

SUSHRUT CHITALE 44

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

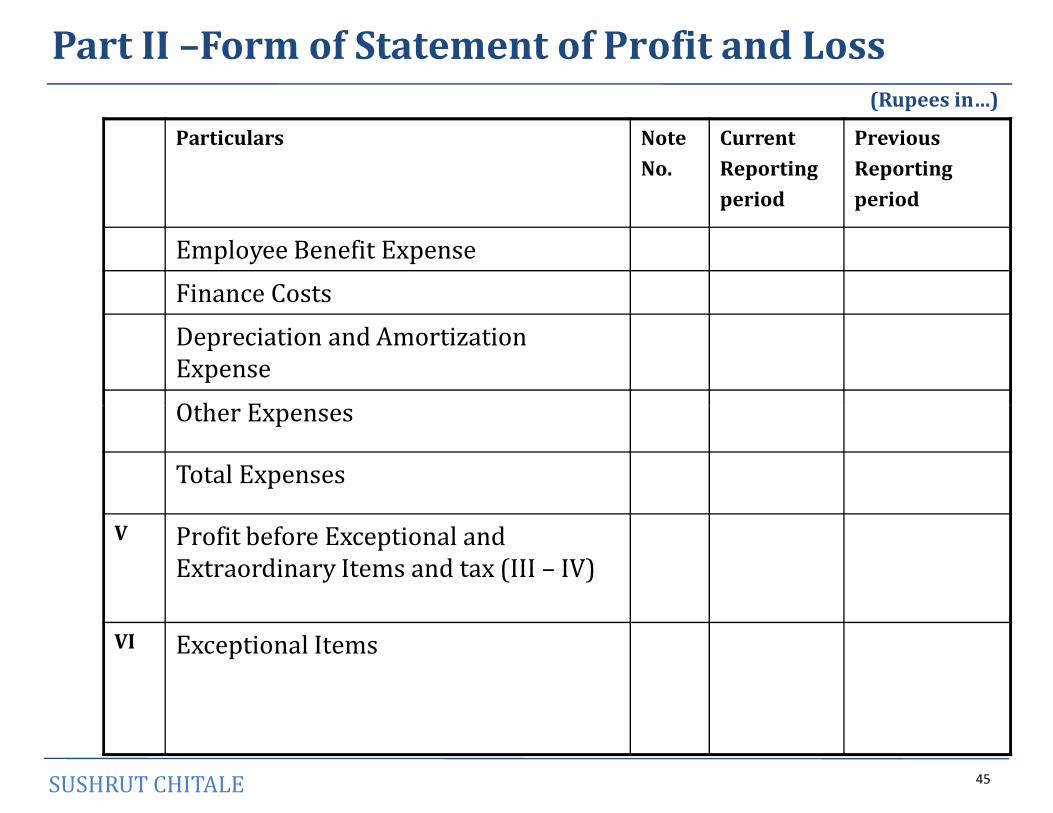

Employee Benefit Expense

Finance Costs

Depreciation and Amortization Expense

Other Expenses

Part II –Form of Statement of Profit and Loss(Rupees in…)

Other Expenses

Total Expenses

V Profit before Exceptional and Extraordinary Items and tax (III – IV)

VI Exceptional Items

SUSHRUT CHITALE 45

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

VII Profit before Extraordinary Items and Tax (V – VI)

VIII Extraordinary Items

IX Profit before Tax (VII – VIII)

Part II –Form of Statement of Profit and Loss(Rupees in…)

IX Profit before Tax (VII – VIII)

X Tax Expense:

(1) Current Tax

(2) Deferred Tax

XI Profit /(Loss) for the period from Continuing Operations (VII – VIII)

SUSHRUT CHITALE 46

Part II –Form of Statement of Profit and Loss(Rupees in…)

Particulars NoteNo.

CurrentReportingperiod

PreviousReportingperiod

XII Profit/(Loss) from Discontinuing Operations

XIII Tax Expense of Discontinuing Operations

XIV Profit / (Loss) from Discontinuing Operations (after tax) (XII-XIII)

XV Profit / (Loss) for the period (XI + XIV)

XVI Earnings per equity share :(1) Basic(2) Diluted

See accompanying notes to the financial statements

SUSHRUT CHITALE 47

Classification by nature vs functionRevised Schedule VI requires companies to classify expenses by nature and not be function. An example out of ‘Infosys’ financial statements for FY11 and FY12 is presented below:

FY11Consolidated Profit and loss AccountIncome from software services, products & business process management

XX

FY12Consolidated Statement of Profit and LossIncome from software services and products XXOther income XXTotal revenue XX

Revised Schedule VIOld Schedule VI

SUSHRUT CHITALE 48

business process managementSoftware development and business process management expenses

XX

Gross Profit XX

Selling and marketing expenses XXGeneral and administration expenses XX

EBITDA XX

Total revenue XX

ExpensesEmployee benefit expenses XXCost of technical sub-contractors XXTravel expenses XXCost of software packages & others XXCommunication expenses XXProfessional charges XXDepreciation XXOther expenses XX

Profit before tax XX

Revenue From OperationsA Non-Finance Company shall disclose separately, revenue from:• Sale of Products,• Sale of Services,• Other Operating Revenues

Less:• Excise Duty

A Finance Company shall disclose separately, revenue from:• Interest, and• Other Financial Services

SUSHRUT CHITALE 49

Other Operating RevenuesQuestion: REVENUE FROM OPERATIONS VS. OTHER INCOME

• A Company engaged in manufacture and sale of industrial andconsumer products, also has a real estate arm and is continuouslyengaged in leasing of real estate properties.

Rent in such a case will be classified as ‘Other Operating Income’

• Another Consumer Products Company, owns a 12 storied buildingand temporarily lets out one floor on rent which is currently notin use. In such a case, how should such lease rent should beaccounted?

Rent in such case shall be classified as ‘Other Income’, since this isnot a routine operating activity for the company.

SUSHRUT CHITALE 50

Other Operating RevenuesQuestion: REVENUE FROM OPERATIONS VS. OTHER INCOME

• In case of an auto component manufacturing company, whetherprofit on sale of fixed asset and sale of manufacturing scrapshould be classified as ‘Other Operating Revenue’?

Profit on sale of fixed asset – Other Income Sale of manufacturing scrap – Other Operating Revenue. Sale of manufacturing scrap – Other Operating Revenue.

• Revenue arising from principal or ancillary revenue- generatingactivities would be classified under ‘Other Operating Revenues’.

SUSHRUT CHITALE 51

Revenue From OperationsQuestion: INDIRECT TAXES

• Whether revenue of the company should be presented as net ofindirect taxes such as Vat, Service Tax, etc. as required by RevisedSchedule VI for Excise Duty?

If the company is acting as a principal and hence responsible forpaying tax on its own account-revenue may also be grossed up forpaying tax on its own account-revenue may also be grossed up forthe tax billed to the customer and the tax payable may be shown asan expense or ,if it is acting as an agent i.e. simply collecting andpaying tax on behalf of government authorities, then revenueshould be presented net of taxes.

However, in case of VAT, the guidance note specifically states thatVAT is collected on behalf of Government authorities. Hence, VATshould not be included either as revenues or as expenses.

SUSHRUT CHITALE 52

Other IncomeDisclosure showing separately:• Interest Income (In case of Non-Finance Companies)• Dividend Income• Net Gain/Loss on sale of Investments• Other non-operating income (net of expenses directly attributable

to such income)

• Classification of income would also depend on the purpose forwhich the particular asset is acquired/held.

SUSHRUT CHITALE 53

Other IncomeQuestion: DIVIDEND FROM SUBSIDIARY COMPANIES

• What would be the treatment of dividend from SubsidiaryCompanies, as unlike the Old Schedule VI, the Revised ScheduleVI, does not prescribe any accounting treatment ?

Dividend Income from Subsidiary Companies should berecognized in accordance with AS-9 i.e. only when the right toreceive the same is established on or before the Balance Sheetdate.

For example – A subsidiary company approves payment ofdividend at its AGM held on 30 June 2012. This dividend shall beconsidered as income by the holding company in the financialyear 2012-2013, even though it is declared out of the profits ofthe year ended 31st March 2012.

SUSHRUT CHITALE 54

Other IncomeSHARE IN PROFITS/LOSS IN PARTNERSHIP FIRMS/LLP/

SUBSIDIARY COMPANIES /ASSOCIATES

• No specific requirement to disclose separately, unlike OldSchedule VI.

• However, disclosure should be made on Accrual Concept, i.e.when accounted for by the Associates.when accounted for by the Associates.

• Should be guided by AS-21 (Subsidiaries), AS-23 (Associates) andAS-27(Consolidated Financial Statements) .

• In case of differences between the reporting dates,adjustments to be made for significant transactions and if thedifference is more than 6 months, disclosure is required.

SUSHRUT CHITALE 55

ExpensesDisclosure is to be made on the face of Statement of Profit andLoss :

• Cost of Materials Consumed.• Purchases of Stock-in-Trade: Goods purchased normally with the

intention to resell or trade-in.• Changes in Inventories of Finished Goods, Work-in-Progress and

Stock-in-Trade: Separate disclosure is required.Stock-in-Trade: Separate disclosure is required.• Employee Benefit Expense: In addition to Salary & Wages,

Contribution to PF and Other Funds, Staff Welfare, Expense onESOP/ESPP is to be disclosed separately.

• Finance Costs: Besides, Interest Expense and Other BorrowingCosts, Applicable Net Gain/Loss on Foreign Currency Transactionsand Translation.

SUSHRUT CHITALE 56

Expenses• Depreciation and Amortization Expense.• Other Expenses: Any item of expenditure which exceeds 1% of the

Revenue from Operations or Rs.1,00,000, whichever is higher is tobe separately disclosed.

• Besides, under ‘Other Expenses’: Separate disclosure forConsumption of stores and spare parts, Power and fuel, Rent,Repairs to building and machinery, Insurance, Rates and taxes(excluding taxes on income) and Miscellaneous expenses isrequired.

• Tax Expense: Bifurcated into Current Tax and Deferred Tax. Incase of MAT, disclosure in this regard should be made:

Current Tax (MAT)Less: MAT Credit EntitlementNet Current Tax

SUSHRUT CHITALE 57

ExpensesQuestion: SUBSTITUTION OF LINE

ITEMS• The Revised Schedule VI specifies a

format for statement of profit and loss.Whether any additional line items, sub-line items, sub-totals can be inserted inthe format to suit the sector /requirements of the Company?

FY12Statement of Profit and Loss AccountINCOMEService Revenue XXOther Income XXTotal XX

OPERATING EXPENDITURErequirements of the Company?

Yes, additional line items, sub-lineitems, sub-totals can be inserted.Similarly, existing prescribed formatcan be substituted in case the nature ofthe business of the company sodemands. For example, in a telecomcompany, the statements of profit andloss is illustrated herein:

SUSHRUT CHITALE 58

OPERATING EXPENDITUREPersonnel Expenditure XXNetwork expenses & IT Outsourcing cost XXLicense Fees & WPC Charges XXRoaming & Access charges XXSubscribver acquisition & servicing expenditure XXAdvertisement & business promotion expenses XXAdministration & other expenses XX

EBITDA XX

AppropriationsQuestion: DIVIDEND DECLARED BY COMPANY

• The Revised Schedule VI specifies a format for statement of profitand loss. In such a scenario, where should dividends declared bedisclosed?

Dividends declared should be disclosed under the notescontaining reserves & surplus. This is illustrated below:

FY11 FY12

SUSHRUT CHITALE 59

FY11Profit and Loss AccountNet Profit for the year XXBalance brought forward XXAmount Available for Appropriations XX

AppropriationsInterim dividend XXProposed final dividend XXTax on dividend XXGeneral reserve XXBalance carried to balance sheet XX

FY12Reserves & SurplusSurplus in Statement of profit and loss XXOpening Balance XXAdd: Profit for the year XXLess: AppropriationsInterim dividend XXProposed final dividend XXTax on dividend XXGeneral reserve XXBalance in statement of profit and loss XX

Additional InformationAdditional information regarding aggregate expenditure andincome:

• Adjustments to the carrying amount of investments.• Net gain or loss on foreign currency transaction and translation

(other than considered as finance cost).• Payments to the auditor.• Prior period items.• Prior period items.• Purchases, Sales, Consumption of Raw Material, Work-in-Progress

and the Gross Income from Services rendered – as applicable areto be shown under broad heads. Broad Heads to be decidedtaking into account the concept of materiality and presentation oftrue and fair view of financial statements. (10% of total value isgenerally considered as acceptable threshold limit).

SUSHRUT CHITALE 60

Additional Information• The aggregate, if material, of any amounts set aside or proposed

to be set aside to reserve and any amounts withdrawn from suchreserves.

• The aggregate, if material, of the amounts set aside to provisionsmade for meeting specific liabilities, contingencies orcommitments and any amounts withdrawn from such provisions,as no longer required.

• Provisions for losses of Subsidiary Companies.

SUSHRUT CHITALE 61

Other DisclosuresStatement of Profit and Loss shall also contain by way of a note:

• Value of imports calculated on C.I.F basis by the companyduring the financial year in respect of Raw Materials, Componentsand spare parts, Capital goods;

• Expenditure in foreign currency during the financial year onaccount of royalty, know-how, professional and consultation fees,account of royalty, know-how, professional and consultation fees,interest, and other matters;

• Total value if all imported and indigenous raw materials, spareparts and components consumed during the financial year andthe percentage of each to the total consumption;

SUSHRUT CHITALE 62

Other Disclosures• The amount remitted during the year in foreign currencies on

account of dividends with a specific mention of the total numberof non-resident shareholders, the total number of shares held bythem on which the dividends were due and the year to which thedividends related;

• Earnings in foreign exchange classified as: Export of goodscalculated on F.O.B. basis, Royalty, know-how ,professional andconsultation fees, Interest & Dividend and Other Income,indicating the nature thereof.

SUSHRUT CHITALE 63

SUSHRUT CHITALE 64

Sushrut ChitaleMukund M Chitale & Co.

205A, Agrawal Shyamkamal Building,Vile Parle East, Mumbai – 400057

Tel: 91-22-26143127/ 91-22-26143130Email: [email protected]: www.mmchitale.com