it capability maturity framework introduction to it-cmf ......it capability maturity framework...

TRANSCRIPT

IT Capability Maturity Framework

Introduction to IT-CMF

Financial Critical Capabilities (CCs)

©2012 David Consulting Group

Michael Harris

President & CEO

Tier 2 Accredited IT-CMF Associate

David Consulting Group

ITFMA April 2012

©2011 David Consulting Group

Executive Summary

• IT-CMF is a powerful new tool which we

recommend

• It focuses on the business value of IT

• It allows users to understand how their IT

organization is performing

• Aims to move IT from a business necessity to a

business changer

©2011 David Consulting Group

The Business Value of IT

• DCG’s The Business Of Value of IT, published in March

2008, provided answers to the challenges of measuring

and managing the value of IT. Mike Harris, David Herron

and Stasia Iwanicki of DCG shared their experiences and

lessons learned in this foundational analysis.

• Since publication, DCG has helped a number of clients with

IT Governance issues at the Business-IT interface.

• At the same time, we have been participating and

monitoring the state of the art and how the subject matter

has moved forward

• The strongest initiative has been led by Intel and the

Innovation Value Institute and has resulted in the IT

Capability Maturity Framework (IT-CMF)

“The challenge is to characterize how an IT investment, for new capabilities or

for “keeping the lights on,” helps the business that bears the cost to achieve

its financial performance targets and business objectives.” Harris, Herron &

Iwanicki, “The Business Value of IT,” page 15.

©2011 David Consulting Group

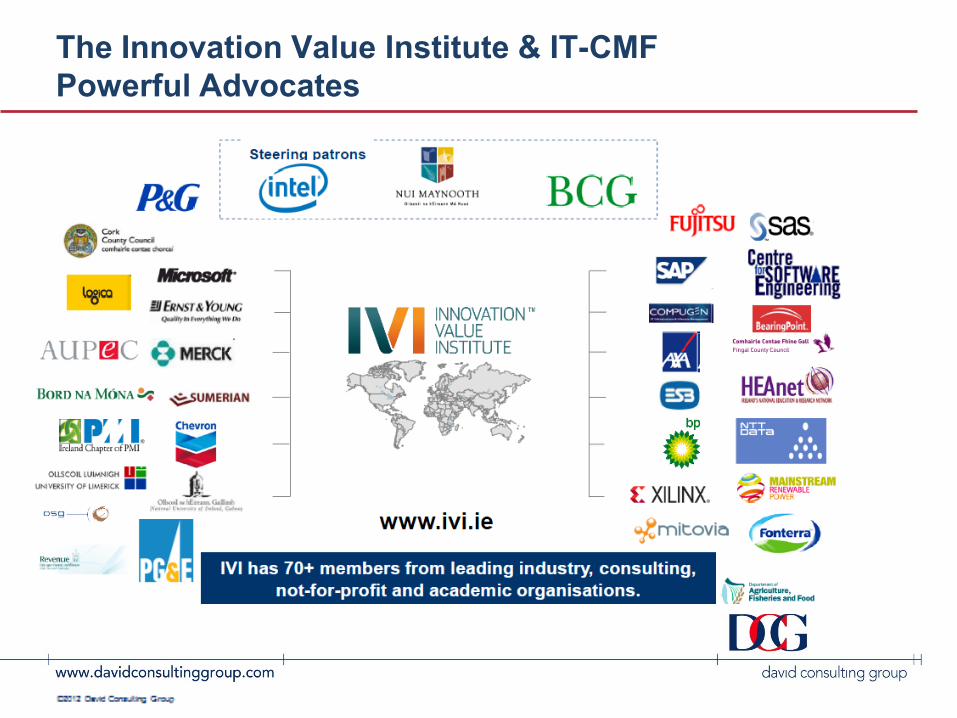

The Innovation Value Institute & IT-CMF

Powerful Advocates

©2011 David Consulting Group

Why another framework?

In short, the other frameworks have strengths (DCG is an SEI Partner for

CMMI) but identifying and enhancing business value is not one of them

Source:

©2011 David Consulting Group

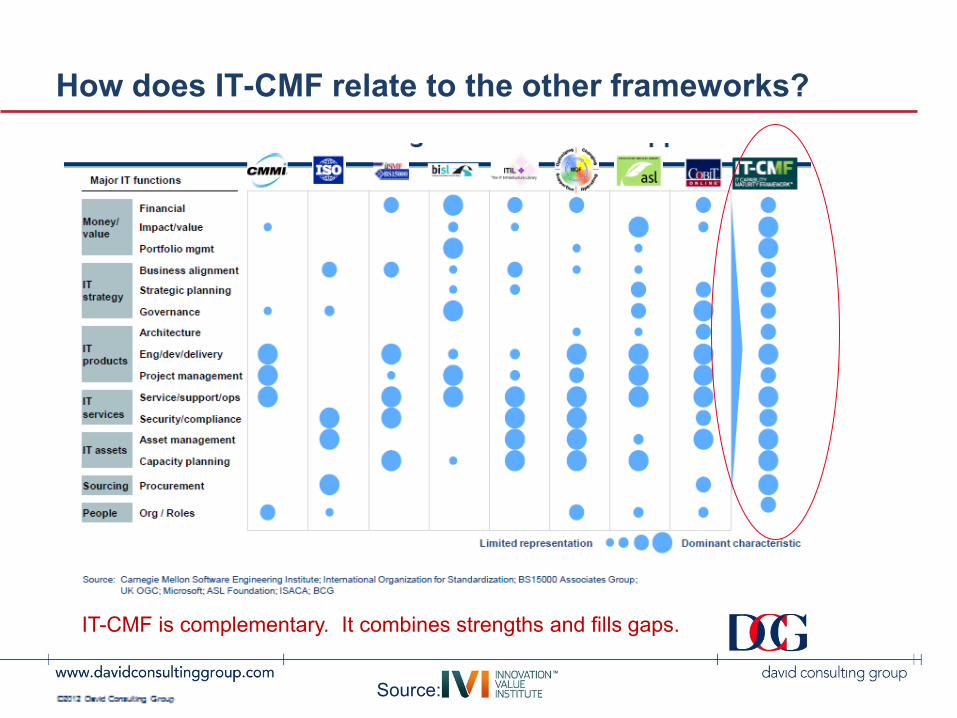

How does IT-CMF relate to the other frameworks?

IT-CMF is complementary. It combines strengths and fills gaps.

Source:

©2011 David Consulting Group

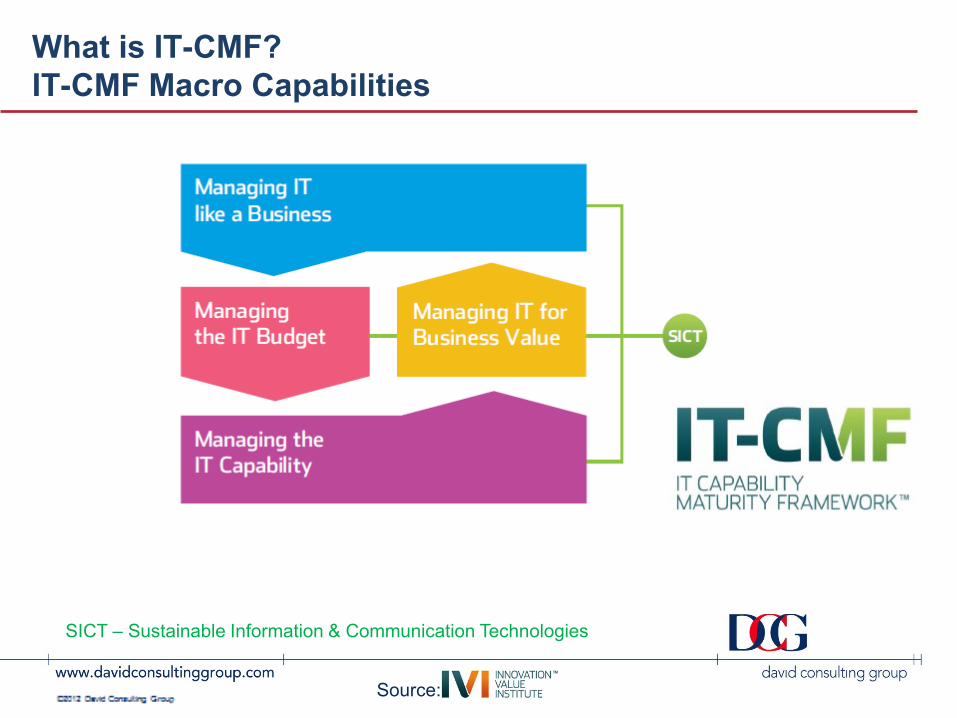

What is IT-CMF?

IT-CMF Macro Capabilities

SICT – Sustainable Information & Communication Technologies

Source:

©2011 David Consulting Group

Critical Capabilities

Source:

©2011 David Consulting Group

IT-CMF – A journey (not a certificate) of small steps

Source:

©2011 David Consulting Group

Typical Output of an Executive Assessment

Source:

This is only one view many more are available from the IVI toolset

©2011 David Consulting Group

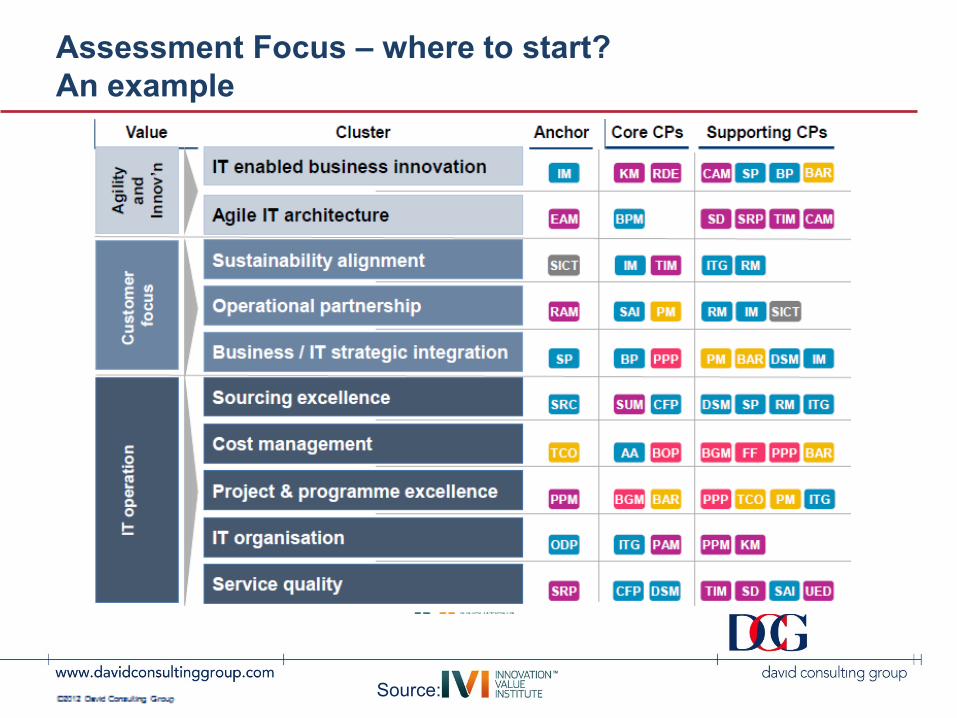

Assessment Focus – where to start?

An example

Source:

©2011 David Consulting Group

IT-CMF Maturity Levels

Maturity

Levels

Managing IT

like a

Business

Managing the

IT Budget

Managing the

IT Capability

Managing IT

for Business

Value

Initial Unmanaged Unmanaged Unmanaged Unmanaged

Basic Cost center Predictable

Performance

Technology

Supplier

Total cost of

ownership

Intermediate Service center Systemic cost

reduction

Technology

Expert

ROI and

business case

Advanced Investment

center

Expanded

funding

options

Strategic

business

partner

Options &

portfolio

management

Optimizing Value Center Budget

amplification

Corporate

core

competency

Optimized

value

Source:

©2011 David Consulting Group

Managing the IT Budget

Maturity Indicators

Source:

“… the IT budgets of

some organizations

are a complete

mystery to the

businesses that pay

for them and may

not be delivering

commensurate

value.” Harris,

Herron & Iwanicki,

“The Business Value

of IT,” page 15.

©2011 David Consulting Group

Critical Capabilities – Financial

Source:

©2011 David Consulting Group

Overview of Funding & Budgeting Process Flow

Strategic

Planning

Business

Planning

Funding

level

Funding &

Financing

Portfolio Planning

& Prioritisation

Target spending

by portfolio

Budget

Management

TCO

Accounting &

Allocation

Budget Oversight

& Performance

Analysis

Capacity

Forecasting And

Planning

Capex/Opex

budget

Performance

vs. budget

Planned spend

by Portfolio

Cost accounting model

Charge back model

Variance analysis

IT intensity vs. Benchmark

Funding and Budgeting CC

Other CC

Variance analysis

IT Leadership &

Governance

Financing

guidelines

Cost Data and budget

refinements

Updates

Cost information

Note: Simplified picture, additional dependencies exists

After budget cycle During budget cycle Before budget cycle

©2011 David Consulting Group

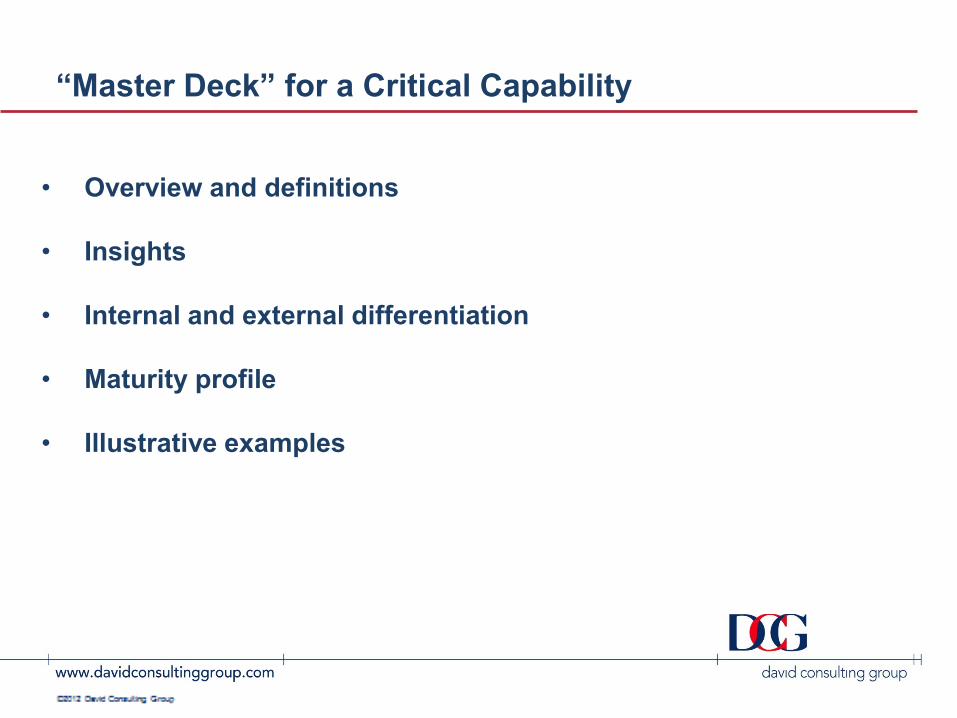

“Master Deck” for a Critical Capability

• Overview and definitions

• Insights

• Internal and external differentiation

• Maturity profile

• Illustrative examples

©2011 David Consulting Group

Overview of Total Cost of Ownership

Definition Total Cost of Ownership tracks, compares, and controls direct and indirect costs associated with IT assets (infrastructure and systems) in order to maximise value. Accurate understanding of current and future TCO over the full IT asset lifecycle leads to more informed budgeting and portfolio management decisions.

• Cost calculation (Acquisition, Operating,

Control, End of life decision making)

• A normalised approach to IT asset cost

comparison

• IT planning using TCO

• Communicating use and benefit of TCO

• Refinement of IT spending plan (based

on calculated TCO) (BGM)

• Allocation/chargeback of direct and

indirect costs (AA)

What’s in scope What’s out of scope

©2011 David Consulting Group

Category Capability

building block Description

Model &

Tools

Scope Covered

Cost drivers (e.g. direct, indirect) and list of assets (infrastructure components,

enterprise applications, etc) being tracked, as well as the frequency with which

models are refreshed based on actual costs realised. Costs include for example

acquisition, operating, control and end of life decision making costs.

Tools and

Methods

Sophistication

Sophistication of tools used to track TCO and coordination capabilities with finance

department systems

Reliability

The reliability with which TCO is able to be tracked, and the costs for differing IT

assets compared, over the entire lifecycle within an organisation. Most reliable

would include optimal set of cost drivers per asset class (normalised to enable

comparison), and coverage of full range of assets

Impact

Impact on Cost Use of TCO to set appropriate cost structure to support business objectives

Impact on

Strategic

Planning

Depth and scope of the impact that TCO management has on investment /

retirement decisions, portfolio planning, and evaluation of business cases

Alignment

Communication Communication of TCO to key business, IT, and Finance stakeholders

Business

Alignment

The extent to which key IT and business stakeholders are involved in TCO

decisions and the impact of this involvement on how IT is perceived

Description of categories and underlying capability

building blocks for Total Cost of Ownership

Draft Update at April 2012

©2011 David Consulting Group

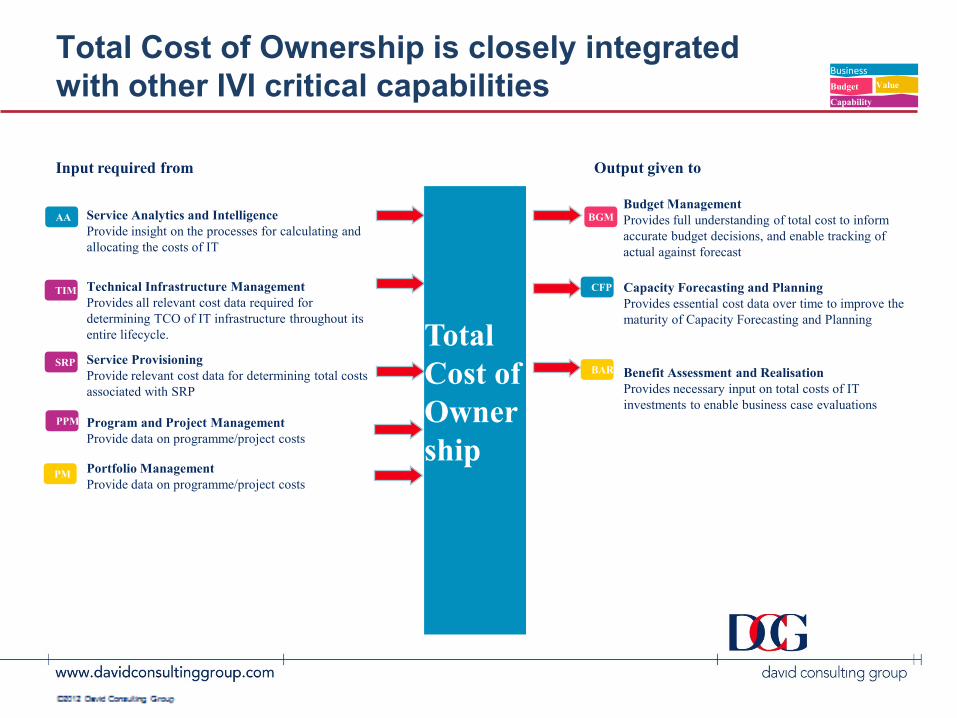

Total Cost of Ownership is closely integrated

with other IVI critical capabilities

Budget Management

Provides full understanding of total cost to inform

accurate budget decisions, and enable tracking of

actual against forecast

Capacity Forecasting and Planning

Provides essential cost data over time to improve the

maturity of Capacity Forecasting and Planning

Service Analytics and Intelligence

Provide insight on the processes for calculating and

allocating the costs of IT

Technical Infrastructure Management

Provides all relevant cost data required for

determining TCO of IT infrastructure throughout its

entire lifecycle.

Output given to Output given to Input required from Input required from

Business

Capability

Budget Value

BGM

TIM

AA

CFP

Total

Cost of

Owner

ship

BAR Benefit Assessment and Realisation

Provides necessary input on total costs of IT

investments to enable business case evaluations

Portfolio Management

Provide data on programme/project costs

Program and Project Management

Provide data on programme/project costs

Service Provisioning

Provide relevant cost data for determining total costs

associated with SRP

SRP

PPM

PM

©2011 David Consulting Group

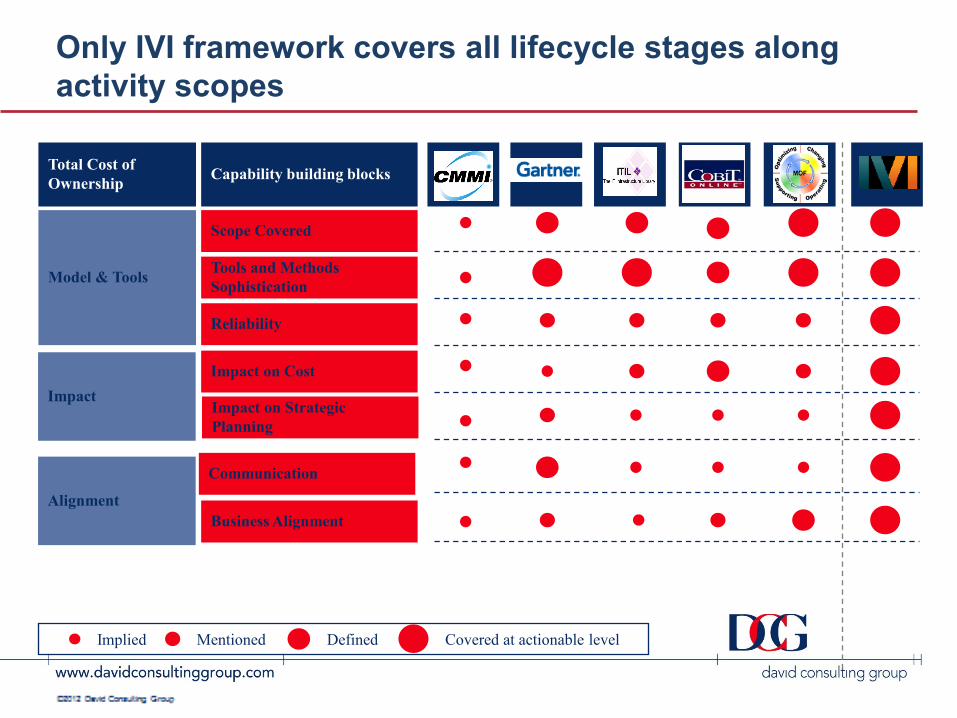

Total Cost of

Ownership

Scope Covered

Tools and Methods

Sophistication

Reliability

Impact on Cost

Impact on Strategic

Planning

Model & Tools

Impact

Capability building blocks

Only IVI framework covers all lifecycle stages along

activity scopes

Add

logo

Add

logo

Add

logo

Add

logo

Implied Covered at actionable level Mentioned Defined

Alignment

Communication

Business Alignment

©2011 David Consulting Group

Models & Tools

Impact Alignment

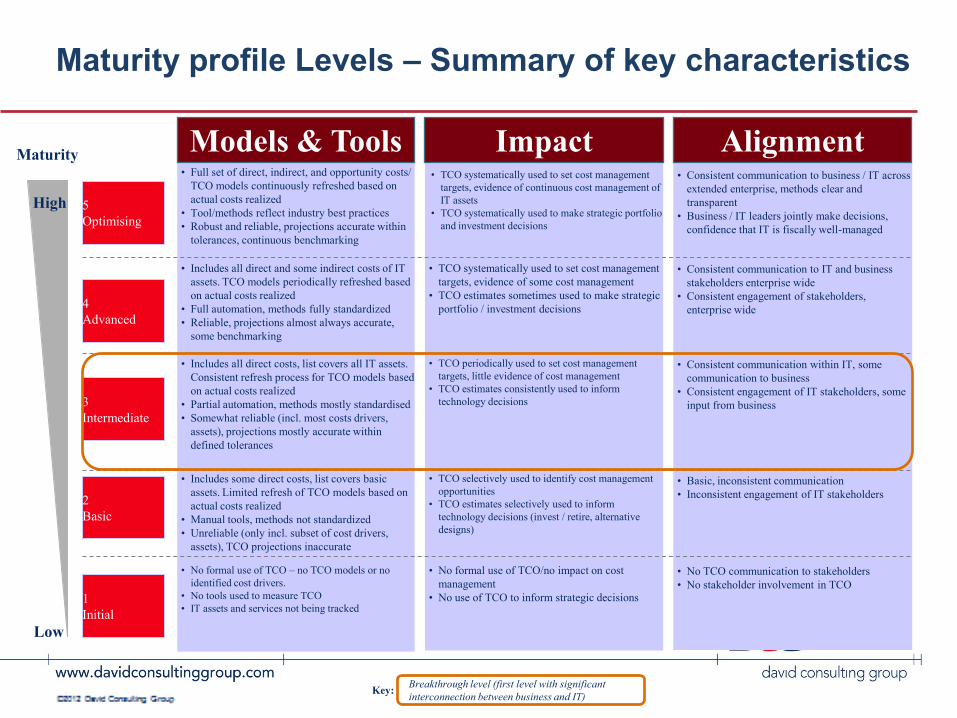

Maturity profile Levels – Summary of key characteristics

• Full set of direct, indirect, and opportunity costs/

TCO models continuously refreshed based on

actual costs realized

• Tool/methods reflect industry best practices

• Robust and reliable, projections accurate within

tolerances, continuous benchmarking

• TCO systematically used to set cost management

targets, evidence of continuous cost management of

IT assets

• TCO systematically used to make strategic portfolio

and investment decisions

• Consistent communication to business / IT across

extended enterprise, methods clear and

transparent

• Business / IT leaders jointly make decisions,

confidence that IT is fiscally well-managed

Breakthrough level (first level with significant

interconnection between business and IT) Key:

Maturity

High

Low

• Includes all direct and some indirect costs of IT

assets. TCO models periodically refreshed based

on actual costs realized

• Full automation, methods fully standardized

• Reliable, projections almost always accurate,

some benchmarking

• TCO systematically used to set cost management

targets, evidence of some cost management

• TCO estimates sometimes used to make strategic

portfolio / investment decisions

• Consistent communication to IT and business

stakeholders enterprise wide

• Consistent engagement of stakeholders,

enterprise wide

• Includes all direct costs, list covers all IT assets.

Consistent refresh process for TCO models based

on actual costs realized

• Partial automation, methods mostly standardised

• Somewhat reliable (incl. most costs drivers,

assets), projections mostly accurate within

defined tolerances

• TCO periodically used to set cost management

targets, little evidence of cost management

• TCO estimates consistently used to inform

technology decisions

• Consistent communication within IT, some

communication to business

• Consistent engagement of IT stakeholders, some

input from business

• Includes some direct costs, list covers basic

assets. Limited refresh of TCO models based on

actual costs realized

• Manual tools, methods not standardized

• Unreliable (only incl. subset of cost drivers,

assets), TCO projections inaccurate

• TCO selectively used to identify cost management

opportunities

• TCO estimates selectively used to inform

technology decisions (invest / retire, alternative

designs)

• Basic, inconsistent communication

• Inconsistent engagement of IT stakeholders

• No formal use of TCO – no TCO models or no

identified cost drivers.

• No tools used to measure TCO

• IT assets and services not being tracked

• No formal use of TCO/no impact on cost

management

• No use of TCO to inform strategic decisions

• No TCO communication to stakeholders

• No stakeholder involvement in TCO

4

Advanced

3

Intermediate

2

Basic

5

Optimising

1

Initial

©2011 David Consulting Group

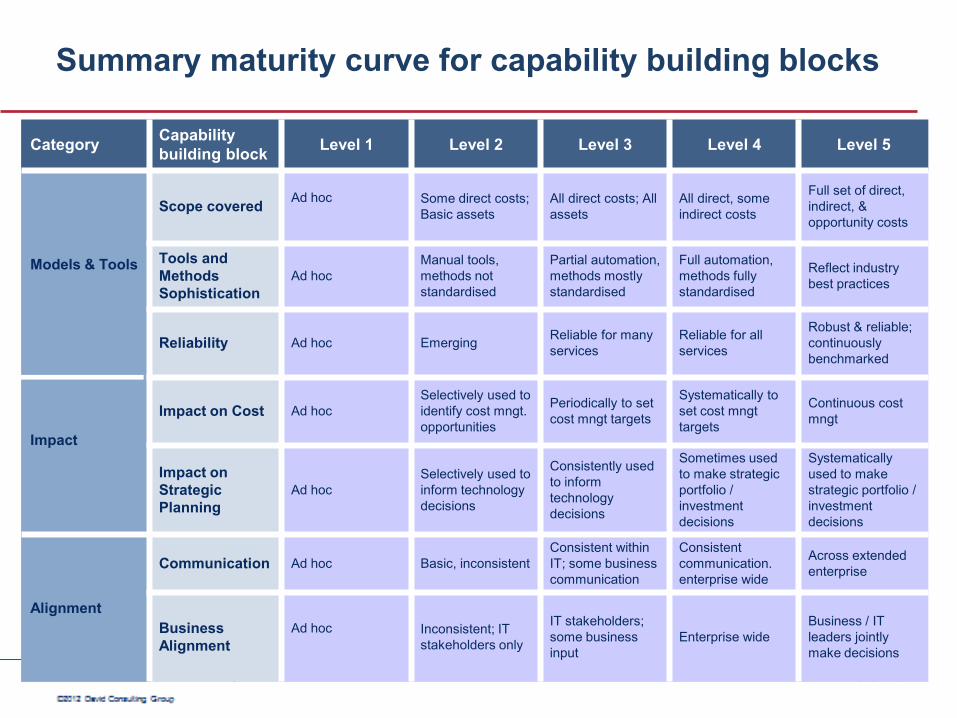

Summary maturity curve for capability building blocks

Category Capability

building block Level 1 Level 2 Level 3 Level 4 Level 5

Models & Tools

Impact

Scope covered Ad hoc

Some direct costs;

Basic assets

All direct costs; All

assets

All direct, some

indirect costs

Full set of direct,

indirect, &

opportunity costs

Tools and

Methods

Sophistication

Ad hoc

Manual tools,

methods not

standardised

Partial automation,

methods mostly

standardised

Full automation,

methods fully

standardised

Reflect industry

best practices

Reliability Ad hoc Emerging Reliable for many

services

Reliable for all

services

Robust & reliable;

continuously

benchmarked

Impact on Cost Ad hoc

Selectively used to

identify cost mngt.

opportunities

Periodically to set

cost mngt targets

Systematically to

set cost mngt

targets

Continuous cost

mngt

Impact on

Strategic

Planning

Ad hoc

Selectively used to

inform technology

decisions

Consistently used

to inform

technology

decisions

Sometimes used

to make strategic

portfolio /

investment

decisions

Systematically

used to make

strategic portfolio /

investment

decisions

Alignment

Communication Ad hoc Basic, inconsistent

Consistent within

IT; some business

communication

Consistent

communication.

enterprise wide

Across extended

enterprise

Business

Alignment

Ad hoc

Inconsistent; IT

stakeholders only

IT stakeholders;

some business

input

Enterprise wide

Business / IT

leaders jointly

make decisions

©2011 David Consulting Group

4

Advanced

3

Intermediate

2

Basic

5

Optimising

1

Initial

Summary of key practices, outcomes, and key metrics

• TCO includes all direct, indirect and opportunity

costs

• Models refreshed continuously based on actual

costs

• Tools and methods standardised and reflect

industry standards

• Business and IT jointly make TCO decisions for

all projects and investments

• TCO sets appropriate cost structures that

optimises overall unit costs

• High degree of confidence that IT is fiscally

well managed

• Systematic usage of TCO to make strategic

investment decisions

• Share (%) of projects that exceed TCO

forecast tolerances

• Rate of cost reduction % by project and area

• TCO includes all direct costs, some indirect

costs and all assets

• TCO Models refreshed consistently

• TCO tools and methods standardised

• Communicate benefits enterprise wide

• Projected TCO accurate within defined

tolerances and benchmarked against industry

standards

• TCO shows cost reduction over time

• Improved engagement of stakeholders

enterprise wide

• % of direct and indirect cost coverage

• % cost reduction per year by project

• Frequency of TCO model review

• Historical tracking of TCO projections vs.

actual

• TCO calculated for selected projects

• TCO covers most direct costs and basic assets

• Models seldom updated based on actual costs

• Tools and methods not standardised

• TCO selectively used in investment decisions

• TCO tracking reliability improved

• TCO projections are sometimes inaccurate

• % of projects which use TCO

• % direct costs tracked

• % of projects which exceed TCO

projections

• No formal use of TCO

• No expected formal outcomes • No metrics

Maturity

High

Low

Key metrics Key metrics Key practices Key practices Outcome Outcome

• TCO consistently used for investment

decisions

• Projected TCO usually accurate within

defined tolerances

• TCO used for cost reduction targets but no

evidence of historical trends

• Improved engagement of IT and some

business stakeholders

• TCO calculated for all projects

• TCO covers all direct costs and all IT assets

• Models periodically refreshed based on actual

costs

• Partially automated TCO tools

• Communicate TCO to IT and some business

stakeholders

©2011 David Consulting Group

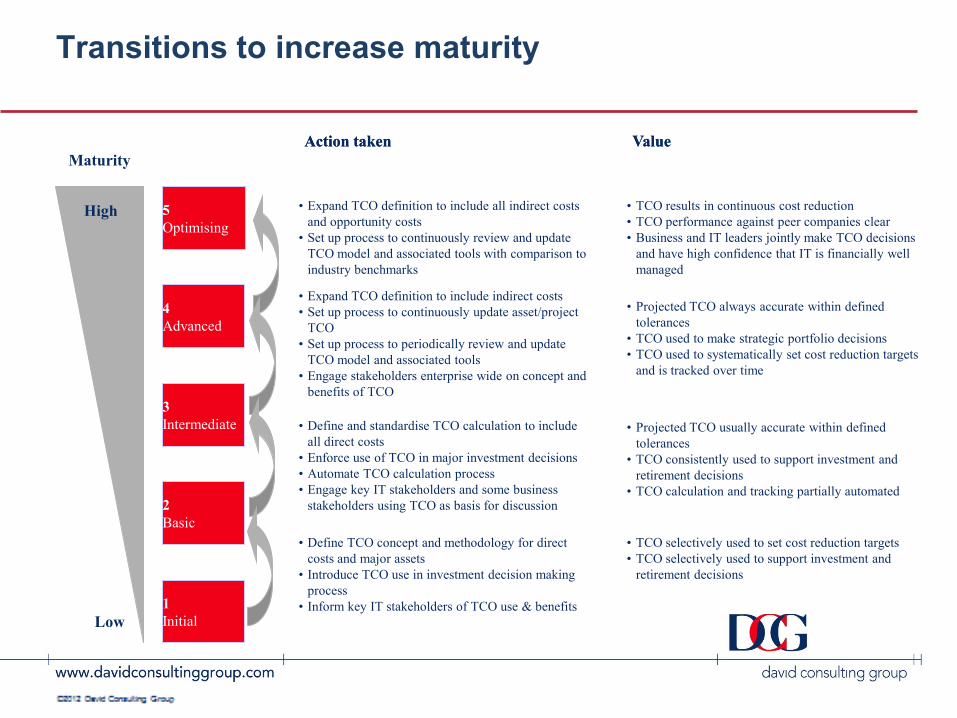

Transitions to increase maturity

• Expand TCO definition to include all indirect costs

and opportunity costs

• Set up process to continuously review and update

TCO model and associated tools with comparison to

industry benchmarks

• TCO results in continuous cost reduction

• TCO performance against peer companies clear

• Business and IT leaders jointly make TCO decisions

and have high confidence that IT is financially well

managed

• Expand TCO definition to include indirect costs

• Set up process to continuously update asset/project

TCO

• Set up process to periodically review and update

TCO model and associated tools

• Engage stakeholders enterprise wide on concept and

benefits of TCO

• Projected TCO always accurate within defined

tolerances

• TCO used to make strategic portfolio decisions

• TCO used to systematically set cost reduction targets

and is tracked over time

• Define and standardise TCO calculation to include

all direct costs

• Enforce use of TCO in major investment decisions

• Automate TCO calculation process

• Engage key IT stakeholders and some business

stakeholders using TCO as basis for discussion

• Projected TCO usually accurate within defined

tolerances

• TCO consistently used to support investment and

retirement decisions

• TCO calculation and tracking partially automated

• Define TCO concept and methodology for direct

costs and major assets

• Introduce TCO use in investment decision making

process

• Inform key IT stakeholders of TCO use & benefits

• TCO selectively used to set cost reduction targets

• TCO selectively used to support investment and

retirement decisions

Maturity

High

Low

Action taken Action taken Value Value

4

Advanced

3

Intermediate

2

Basic

5

Optimising

1

Initial

©2011 David Consulting Group

Illustrative Example: TCO at Coca Cola Enterprise

Description:

• Coca Cola has grown exponentially through aggressive acquisitions resulting in a very heterogeneous

organisation with multiple, and often duplicated, tools and processes

Action taken:

• Corporate decided to implement a TCO approach for major cost buckets

• Key element of driving TCO down was implementing information gathering systems to "be able to keep

the environment at an optimal state"

Impact:

• Through a multi-tiered approach costs were driven down at several major processes, e.g. printer HW

costs decreased by 10% and printer supplier costs by 17%

Key Learning:

• "Keeping TCO low is about keeping the environment at an optimal state based on current business

requirements. You can’t do that effectively unless you have accurate and timely information.” – Coca

Cola Program Manager

©2011 David Consulting Group

Illustrative Example: Integrating IT TCO with Finance

Department

Description:

• TCO calculation performed offline / manually in the IT organisation.

• TCO data was only updated at the 'last minute' in preparation for budget reviews – TCO data wasn’t

reviewed or utilised at any other time

• Often at budget reviews, the TCO information presented was challenged by the business as it did not

agree to the recorded/published budgets and financials

Action taken:

• The IT organisation liaised with the finance organisation as much of the required data already existed

in finance systems, e.g. IT started using standard financial reports to populate TCO model and keep

the model data 'live'

Impact:

• TCO model was fully adopted as a strategic, ongoing monitoring tool, rather than being seen as an

admin drain and a pre-budget meeting exercise

• By using reports from a single system the data was robust and wasn’t challenged as being

inaccurate at budget meetings

• Focus on budget reviews moved to longer term strategic performance, rather than trying to

understand the TCO inaccuracies

• Interaction while updating the TCO model between IT and finance forged a closer working

relationship, leading to a more collaborative ‘team’ approach, duplicate information sources, duplicate

effort and unnecessary admin was eradicated

Key Learning:

• Integrating IT TCO with finance department decreases workload and increases usability of measure

©2011 David Consulting Group

Next Steps?

• Assess your current status with an Executive

Assessment

– Review status against other companies

• Decide what are the most important and urgent

CCs for you

– not everyone process needs to be at the highest level

– you decide not the model

• Assess your capability in those CCs

• Determine and deliver improvement activities

• Repeat regularly

©2011 David Consulting Group

Questions?

Mike Harris

+1.610.644.2856