it risks and controls revised on 2014. content internal control what is internal control? ...

TRANSCRIPT

IT Risks and Controls

Revised on 2014

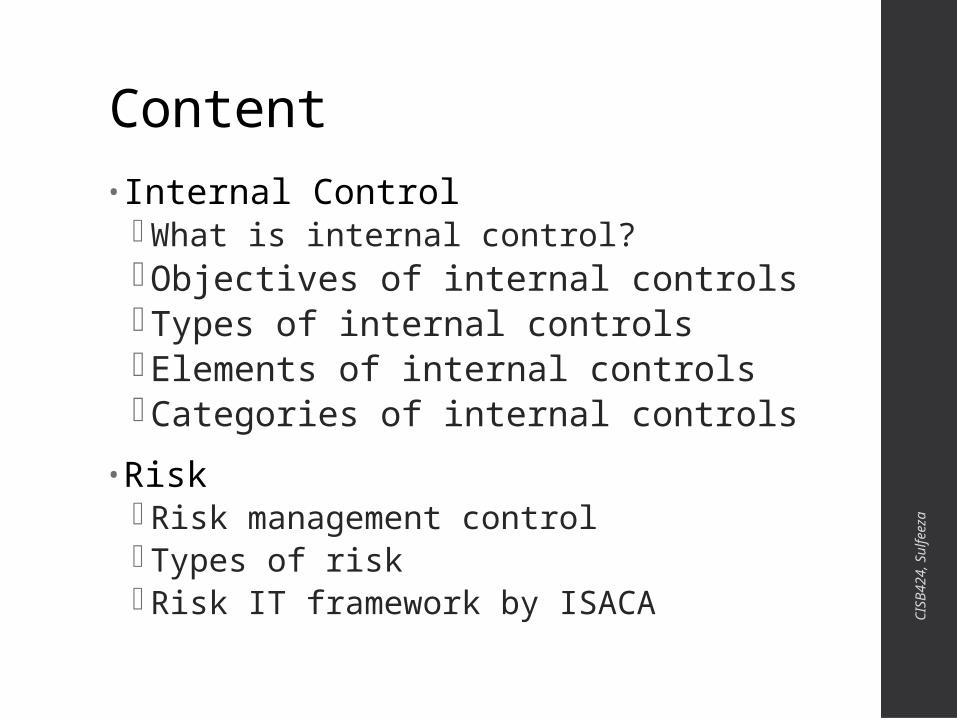

Content• Internal Control

What is internal control?Objectives of internal controls Types of internal controlsElements of internal controlsCategories of internal controls

• Risk Risk management control Types of risk Risk IT framework by ISACA

CIS

B424,

Sulfeeza

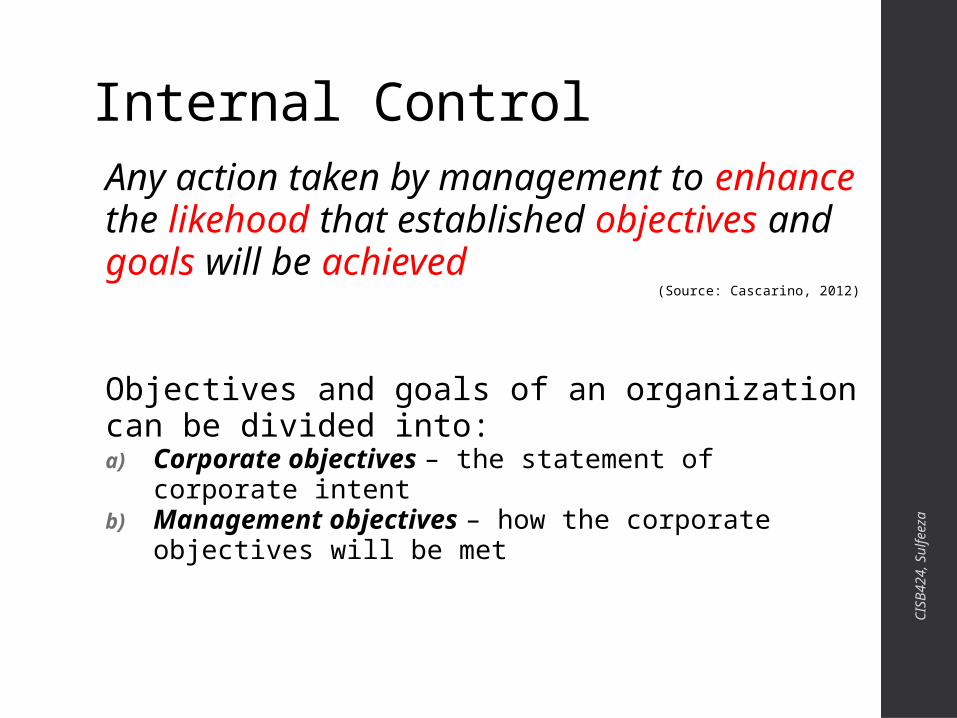

Internal ControlAny action taken by management to enhance the likehood that established objectives and goals will be achieved

(Source: Cascarino, 2012)

Objectives and goals of an organization can be divided into:a) Corporate objectives – the statement of

corporate intentb) Management objectives – how the corporate

objectives will be met

CIS

B424,

Sulfeeza

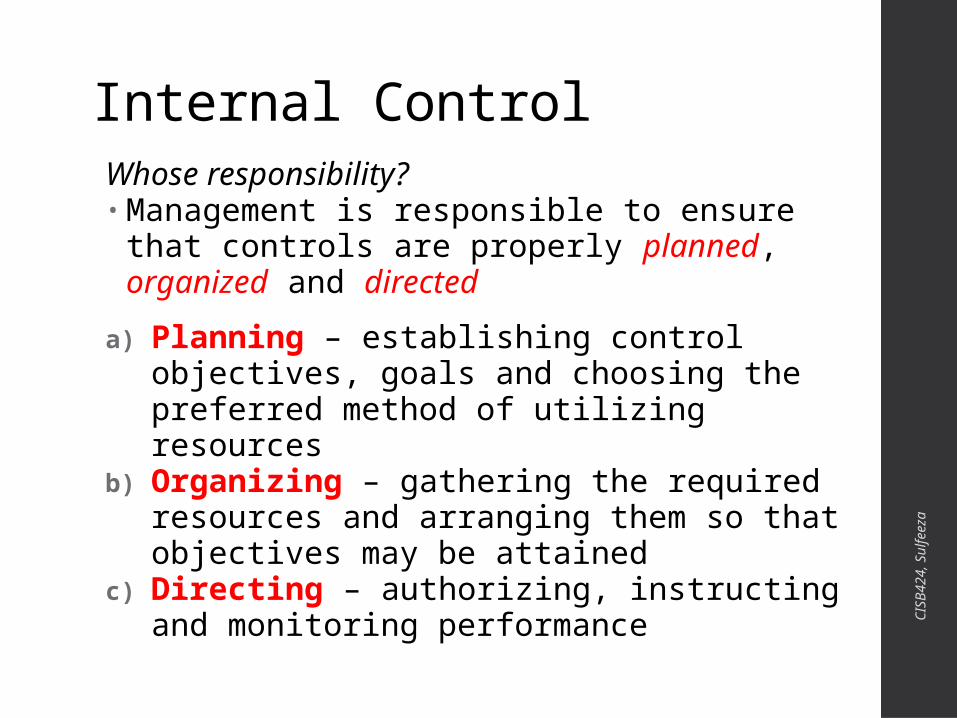

Internal ControlWhose responsibility?• Management is responsible to ensure

that controls are properly planned, organized and directed

a) Planning – establishing control objectives, goals and choosing the preferred method of utilizing resources

b) Organizing – gathering the required resources and arranging them so that objectives may be attained

c) Directing – authorizing, instructing and monitoring performance

CIS

B424,

Sulfeeza

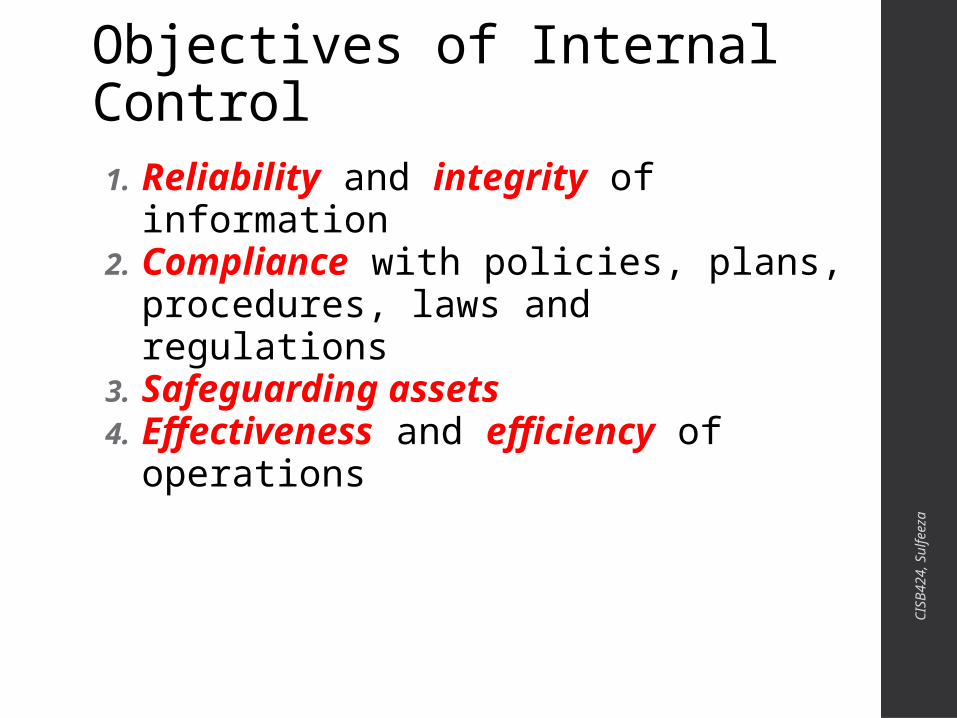

Objectives of Internal Control1.Reliability and integrity of

information2.Compliance with policies, plans,

procedures, laws and regulations3.Safeguarding assets4.Effectiveness and efficiency of

operations

CIS

B424,

Sulfeeza

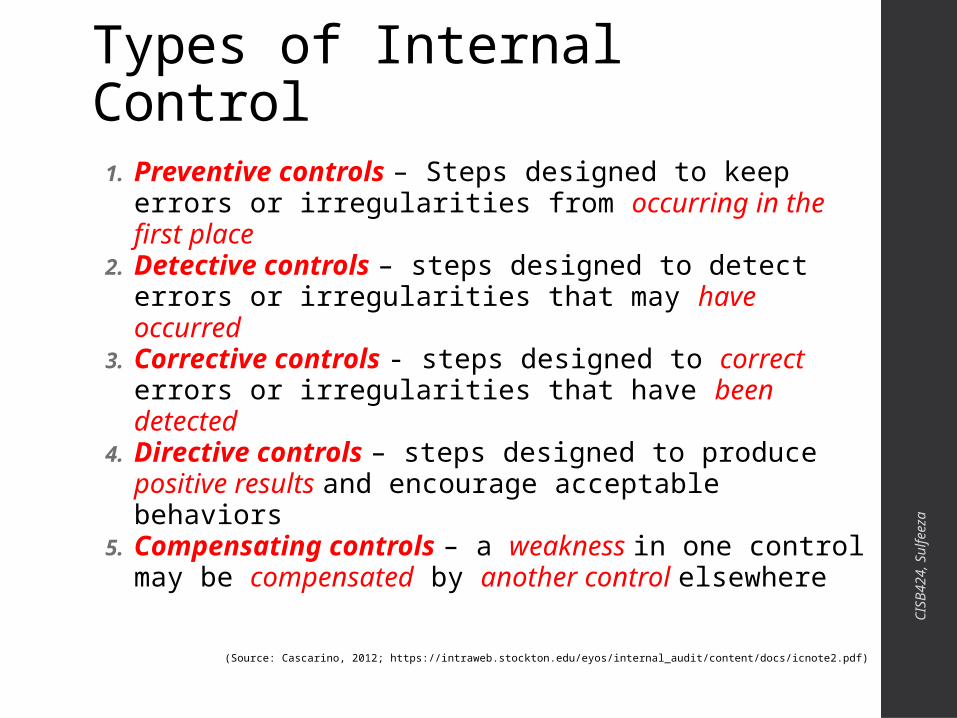

Types of Internal Control1. Preventive controls – Steps designed to keep

errors or irregularities from occurring in the first place

2. Detective controls – steps designed to detect errors or irregularities that may have occurred

3. Corrective controls - steps designed to correct errors or irregularities that have been detected

4. Directive controls – steps designed to produce positive results and encourage acceptable behaviors

5. Compensating controls – a weakness in one control may be compensated by another control elsewhere

(Source: Cascarino, 2012; https://intraweb.stockton.edu/eyos/internal_audit/content/docs/icnote2.pdf)

CIS

B424,

Sulfeeza

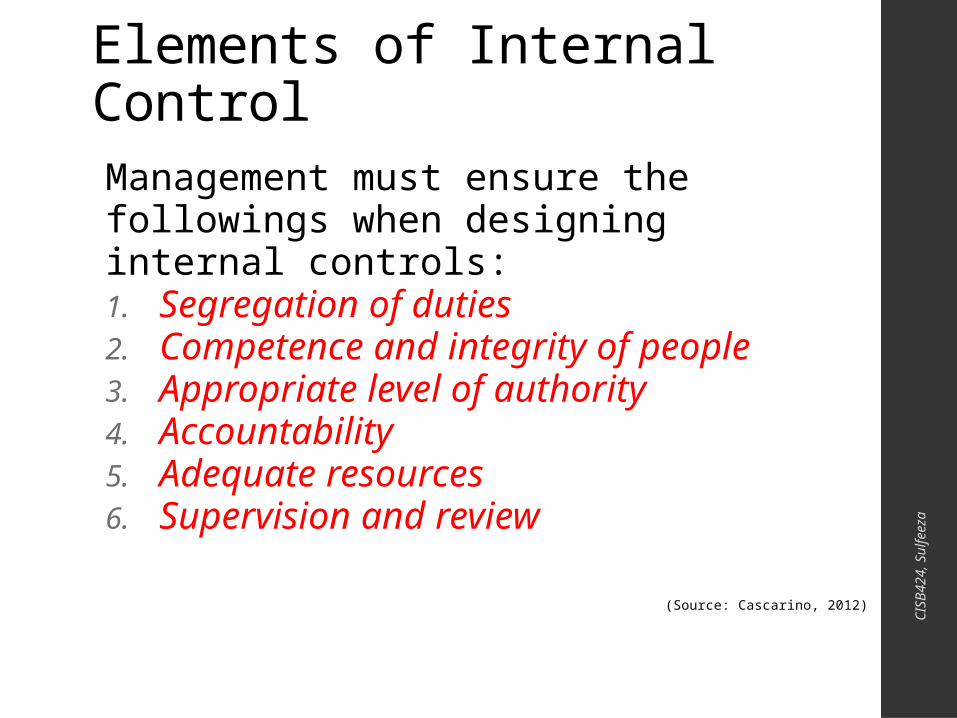

Elements of Internal ControlManagement must ensure the followings when designing internal controls: 1. Segregation of duties2. Competence and integrity of people3. Appropriate level of authority4. Accountability5. Adequate resources6. Supervision and review

(Source: Cascarino, 2012)

CIS

B424,

Sulfeeza

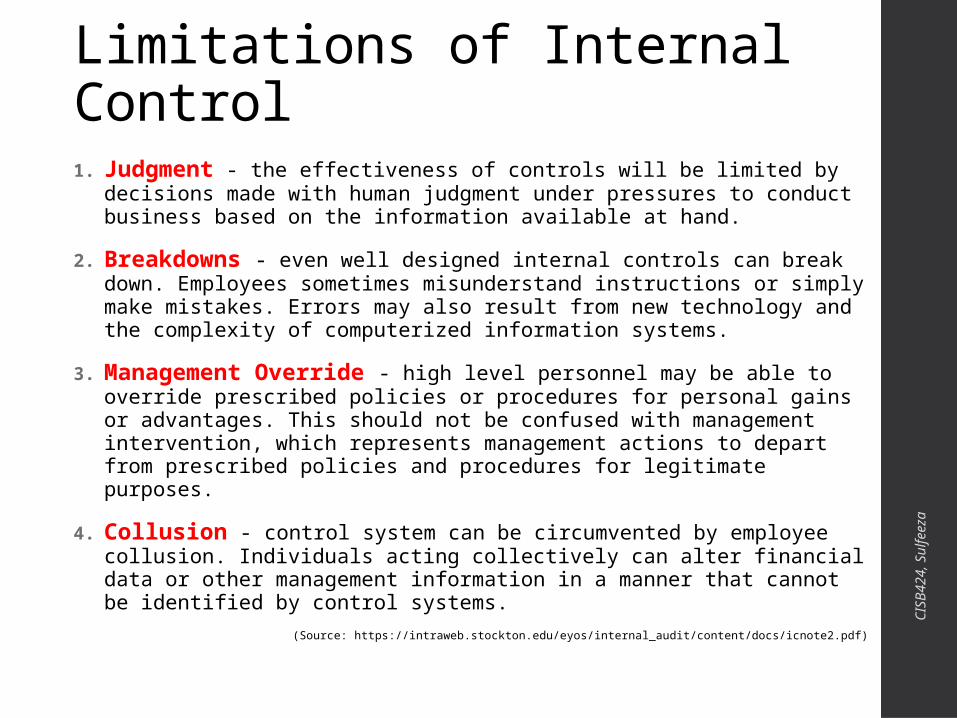

Limitations of Internal Control1. Judgment - the effectiveness of controls will be limited by

decisions made with human judgment under pressures to conduct business based on the information available at hand.

2. Breakdowns - even well designed internal controls can break down. Employees sometimes misunderstand instructions or simply make mistakes. Errors may also result from new technology and the complexity of computerized information systems.

3. Management Override - high level personnel may be able to override prescribed policies or procedures for personal gains or advantages. This should not be confused with management intervention, which represents management actions to depart from prescribed policies and procedures for legitimate purposes.

4. Collusion - control system can be circumvented by employee collusion. Individuals acting collectively can alter financial data or other management information in a manner that cannot be identified by control systems.

(Source: https://intraweb.stockton.edu/eyos/internal_audit/content/docs/icnote2.pdf)

CIS

B424,

Sulfeeza

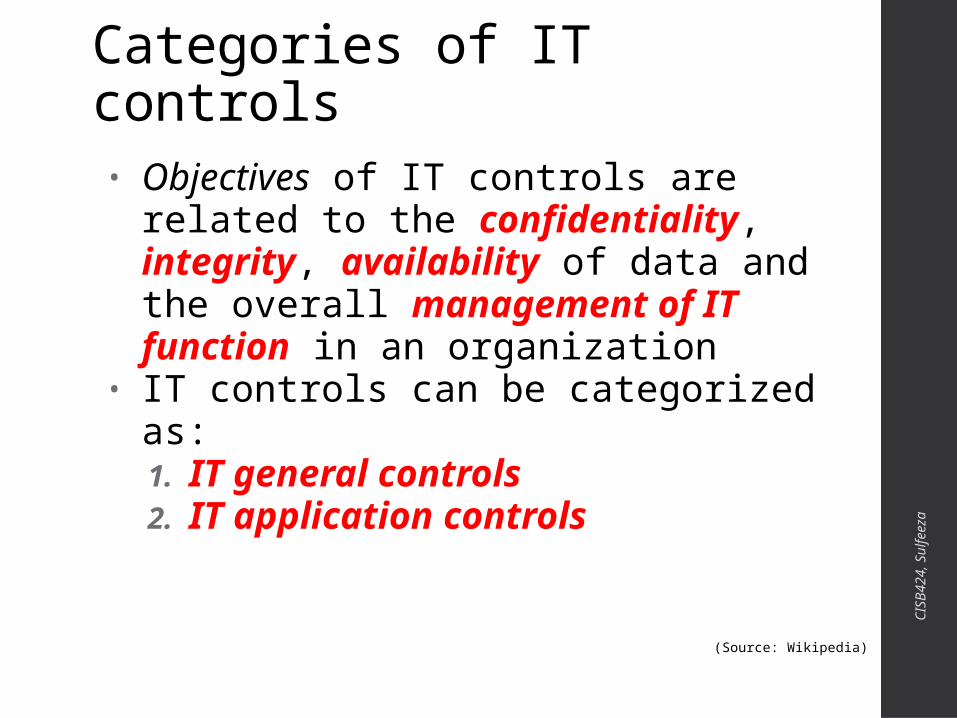

Categories of IT controls• Objectives of IT controls are related to

the confidentiality, integrity, availability of data and the overall management of IT function in an organization

• IT controls can be categorized as:1. IT general controls 2. IT application controls

(Source: Wikipedia)

CIS

B424,

Sulfeeza

IT General Controls• Helps to ensure the reliability of

data generated by IT systems• Areas included:

1. General IT controls2. Computer operations3. Physical security4. Logical security5. Program change control6. Systems development

(Source: Cascarion, 2012, Wikipedia)

CIS

B424,

Sulfeeza

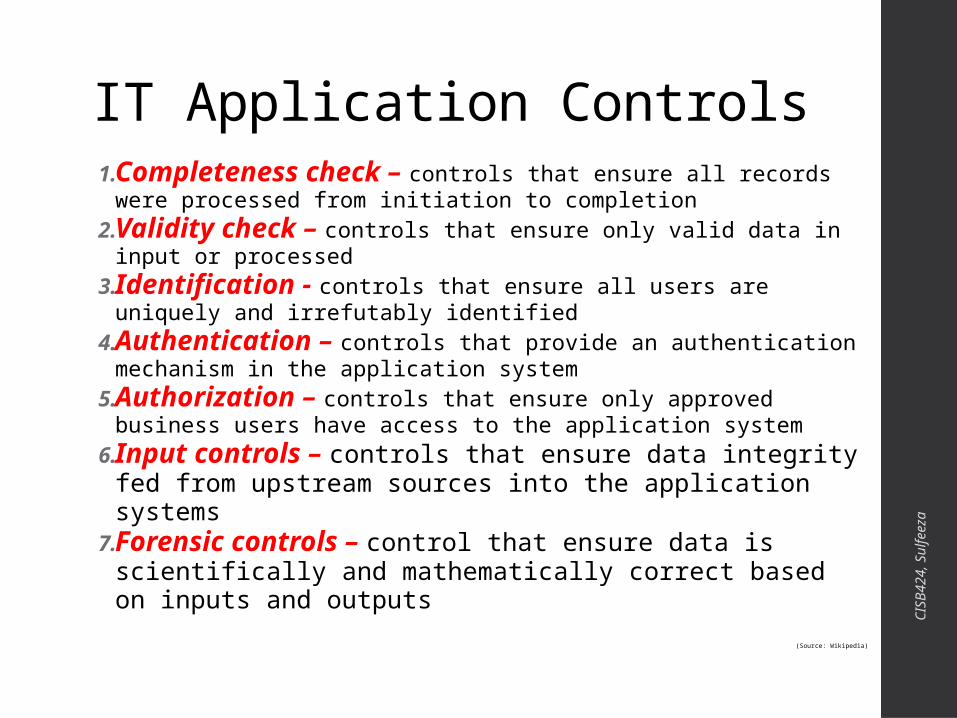

IT Application Controls• Helps to ensure the completeness and

accuracy of data processing, from input to output

• Among the controls that can be implemented:1. Completeness check2. Validity check3. Identification4. Authentication5. Authorization6. Input controls7. Forensic controls

(Source: Wikipedia)

CIS

B424,

Sulfeeza

IT Application Controls1. Completeness check – controls that ensure all

records were processed from initiation to completion2. Validity check – controls that ensure only valid data in

input or processed3. Identification - controls that ensure all users are

uniquely and irrefutably identified4. Authentication – controls that provide an

authentication mechanism in the application system5. Authorization – controls that ensure only approved

business users have access to the application system6. Input controls – controls that ensure data integrity

fed from upstream sources into the application systems

7. Forensic controls – control that ensure data is scientifically and mathematically correct based on inputs and outputs

(Source: Wikipedia)

CIS

B424,

Sulfeeza

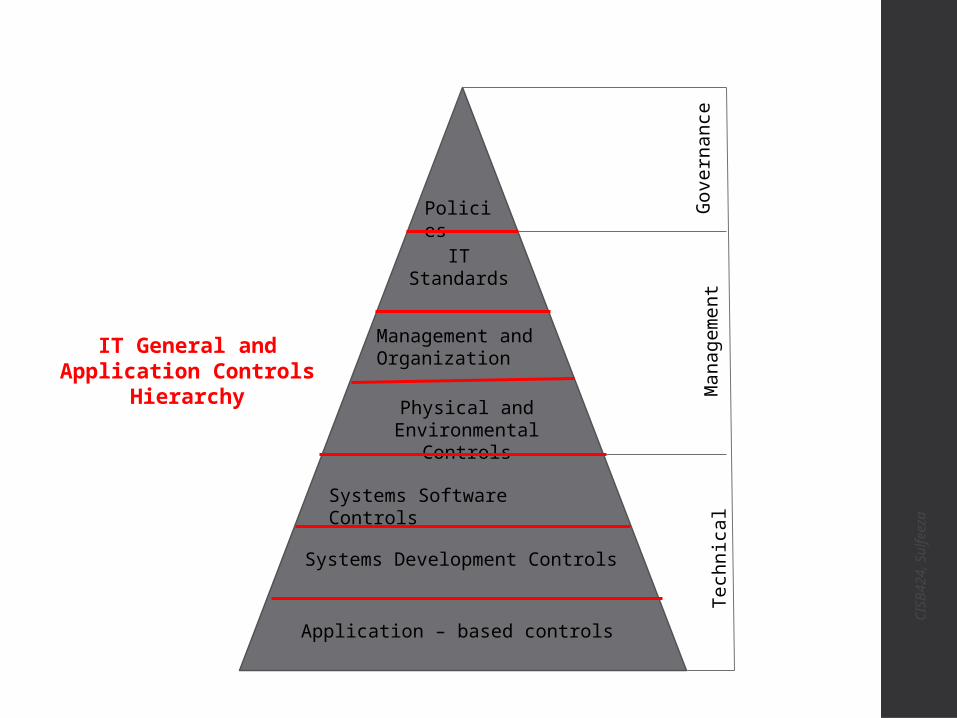

Policies

IT Standards

Management and Organization

Physical and Environmental Controls

Systems Software Controls

Systems Development Controls

Application – based controls

IT General and Application Controls

Hierarchy

Govern

ance

Man

ag

em

ent

Tech

nic

al

CIS

B424,

Sulfeeza

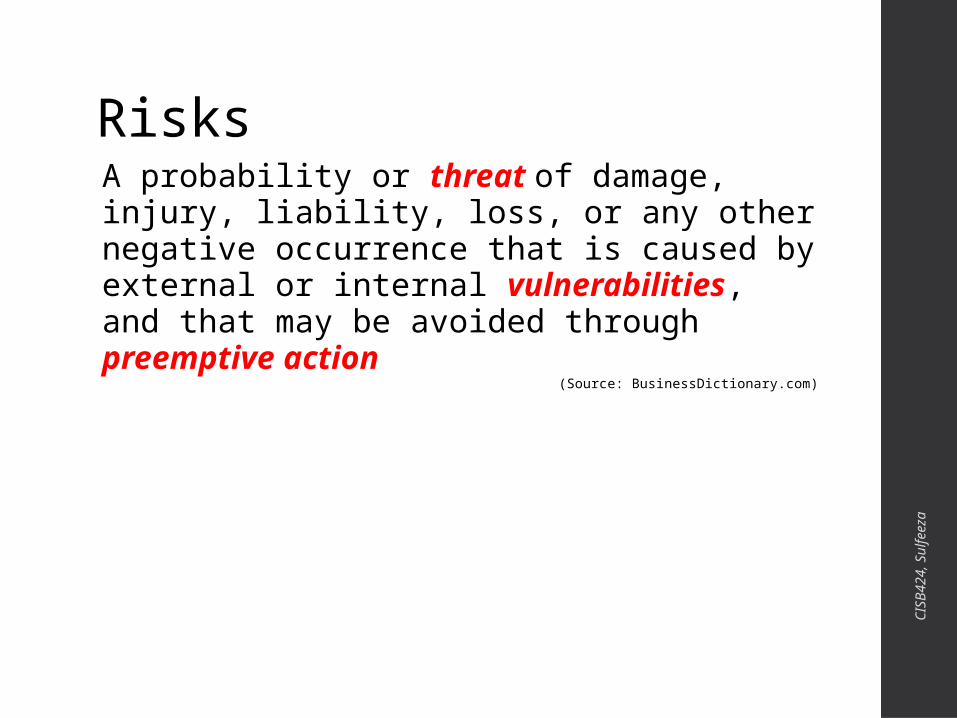

RisksA probability or threat of damage, injury, liability, loss, or any other negative occurrence that is caused by external or internal vulnerabilities, and that may be avoided through preemptive action

(Source: BusinessDictionary.com)

CIS

B424,

Sulfeeza

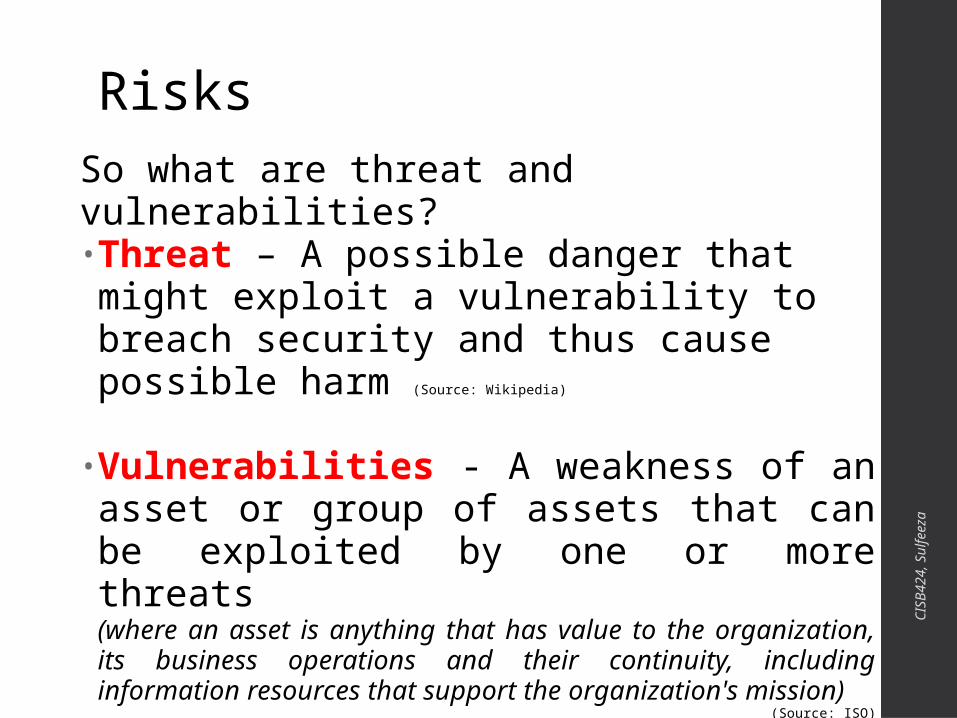

RisksSo what are threat and vulnerabilities?• Threat – A possible danger that might exploit a vulnerability to breach security and thus cause possible harm (Source: Wikipedia)

•Vulnerabilities - A weakness of an asset or group of assets that can be exploited by one or more threats(where an asset is anything that has value to the organization, its business operations and their continuity, including information resources that support the organization's mission)

(Source: ISO) CIS

B424,

Sulfeeza

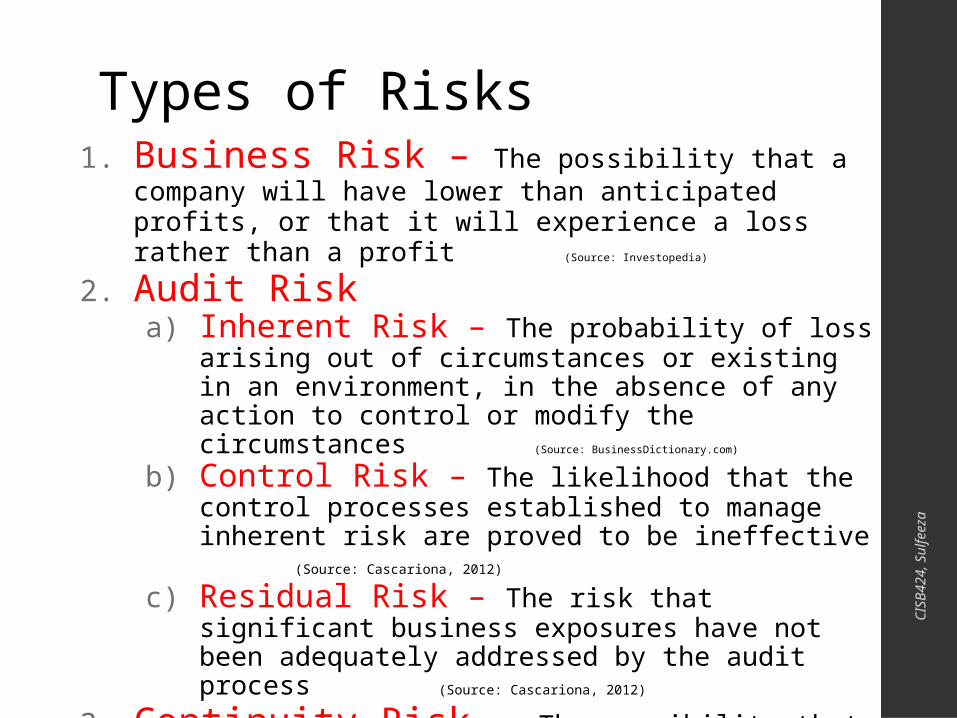

Types of Risks1. Business Risk – The possibility that a company

will have lower than anticipated profits, or that it will experience a loss rather than a profit (Source:

Investopedia)

2. Audit Risk a) Inherent Risk – The probability of loss arising

out of circumstances or existing in an environment, in the absence of any action to control or modify the circumstances

(Source: BusinessDictionary.com)

b) Control Risk – The likelihood that the control processes established to manage inherent risk are proved to be ineffective (Source: Cascariona, 2012)

c) Residual Risk – The risk that significant business exposures have not been adequately addressed by the audit process(Source: Cascariona, 2012)

3. Continuity Risk – The possibility that a company will not be able to continue its operations due to weakness in control

CIS

B424,

Sulfeeza

IT Risks

The potential that a given threat will exploit vulnerabilities of an asset or group of assets and thereby cause harm to the organization. It is measured in terms of a combination of the probability of occurrence of an event and its consequence

(Source: ISO)

CIS

B424,

Sulfeeza

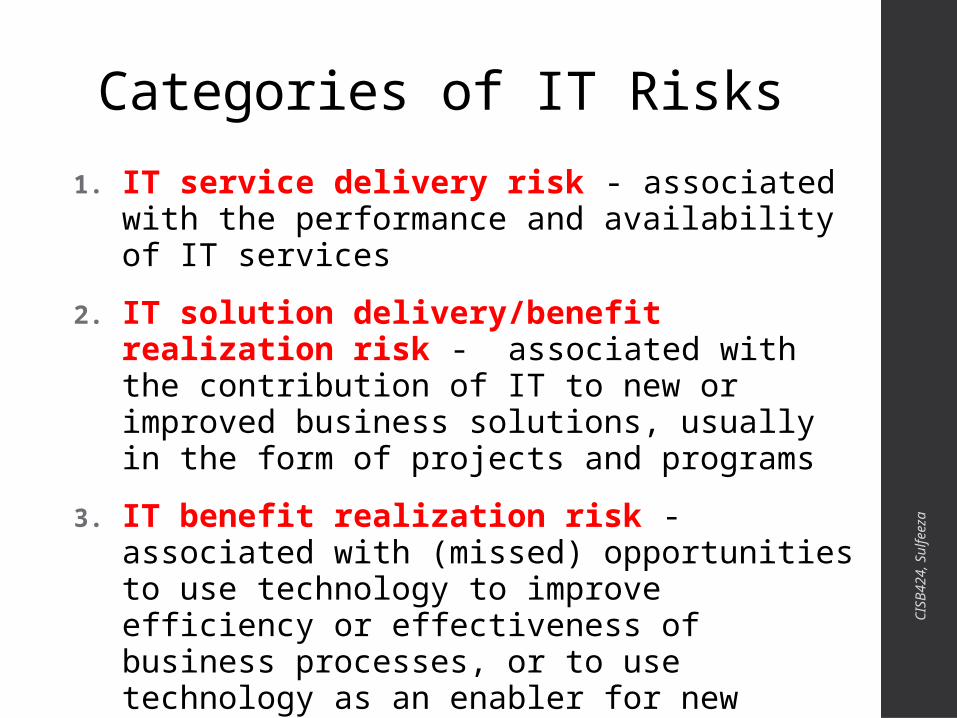

Categories of IT Risks

1. IT service delivery risk - associated with the performance and availability of IT services

2. IT solution delivery/benefit realization risk - associated with the contribution of IT to new or improved business solutions, usually in the form of projects and programs

3. IT benefit realization risk - associated with (missed) opportunities to use technology to improve efficiency or effectiveness of business processes, or to use technology as an enabler for new business initiatives

CIS

B424,

Sulfeeza

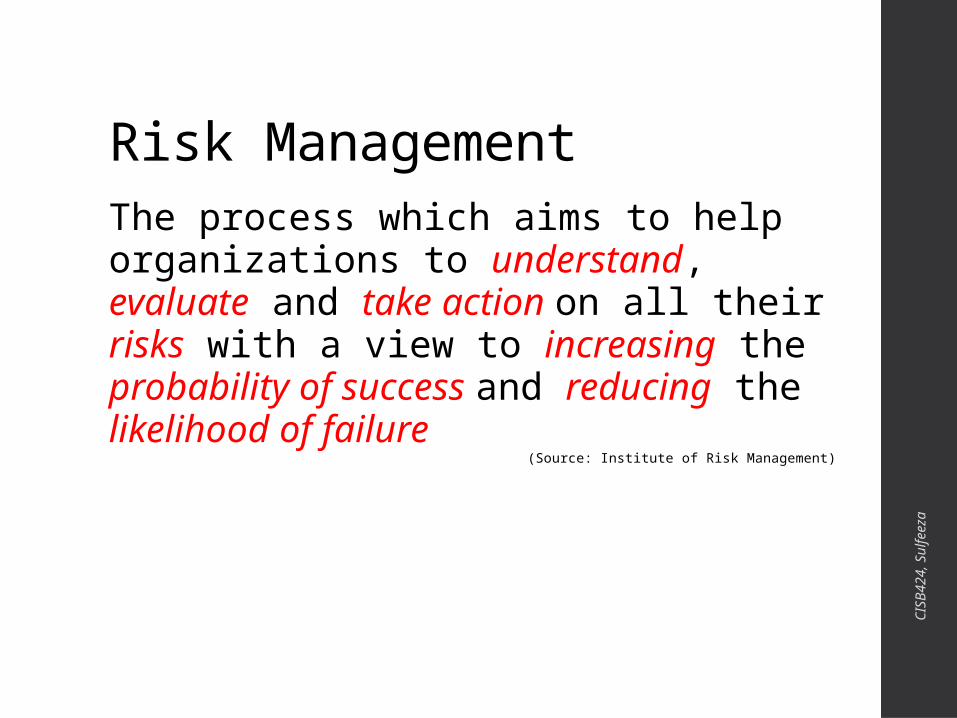

Risk ManagementThe process which aims to help organizations to understand, evaluate and take action on all their risks with a view to increasing the probability of success and reducing the likelihood of failure

(Source: Institute of Risk Management)

CIS

B424,

Sulfeeza

Risk IT Framework

CIS

B424,

Sulfeeza

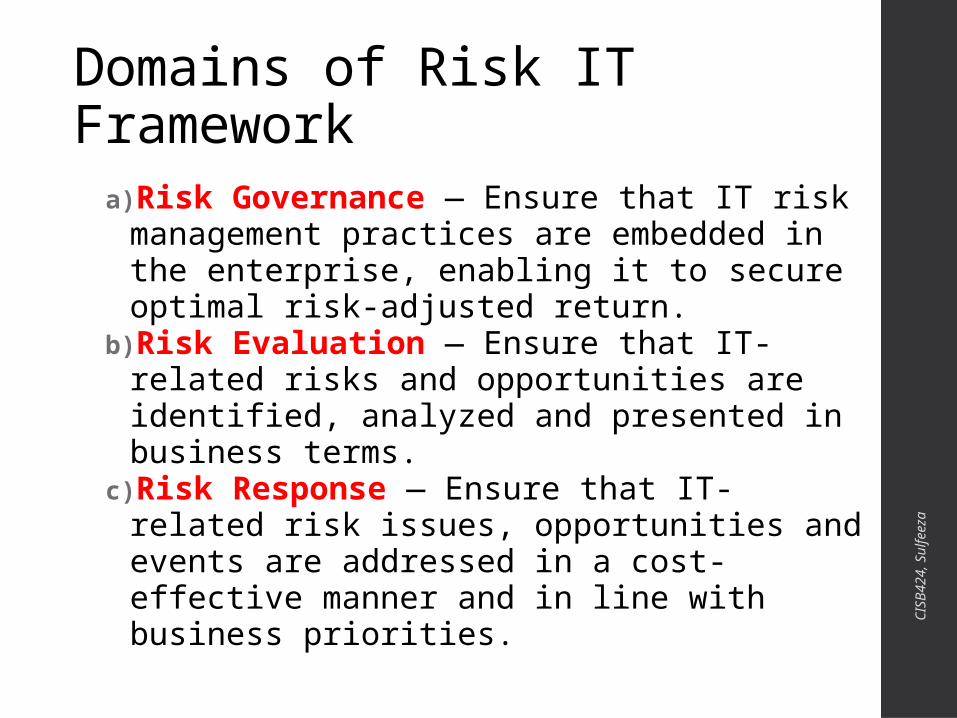

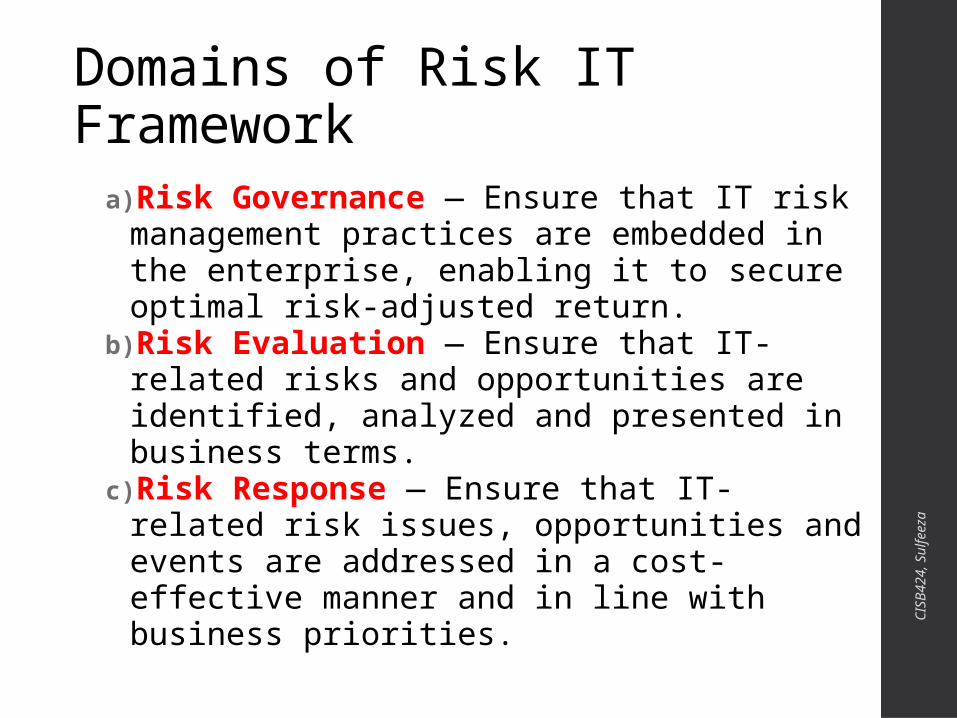

Domains of Risk IT Framework

a)Risk Governance — Ensure that IT risk management practices are embedded in the enterprise, enabling it to secure optimal risk-adjusted return.

b)Risk Evaluation — Ensure that IT-related risks and opportunities are identified, analyzed and presented in business terms.

c)Risk Response — Ensure that IT-related risk issues, opportunities and events are addressed in a cost-effective manner and in line with business priorities.

CIS

B424,

Sulfeeza

Domains of Risk IT Framework

a)Risk Governance — Ensure that IT risk management practices are embedded in the enterprise, enabling it to secure optimal risk-adjusted return.

b)Risk Evaluation — Ensure that IT-related risks and opportunities are identified, analyzed and presented in business terms.

c)Risk Response — Ensure that IT-related risk issues, opportunities and events are addressed in a cost-effective manner and in line with business priorities.

CIS

B424,

Sulfeeza