itc corporate-presentation

TRANSCRIPT

ITC LimitedOne of India’s Most Admired and Valuable Companies

2

ITC Performance Track Record

Sensex (CAGR 95-96 to 13-14) : 11.1%

Rs. cr.

1995-96 2013-1418-yr Cagr

95-96 to 13-14

Net Revenue 2,536 32,883 15.3%

PBDIT 584 13,562 19.1%

PBIT 536 12,662 19.2%

PBT 452 12,659 20.3%

PAT 261 8,785 21.6%

Capital Employed 1,886 27,626 16.1%

ROCE % 28.4 45.8

Market Capitalisation 5,571 280708 24.3%

Total Shareholder Returns % 25.9

Market Cap and TSR based on FY-end prices

3

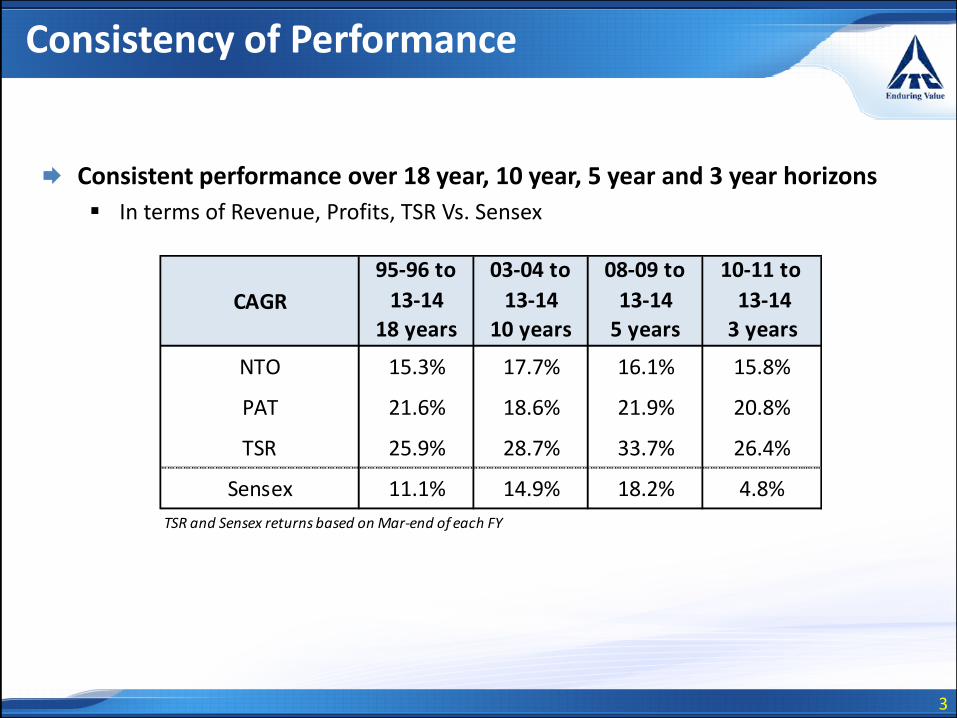

Consistent performance over 18 year, 10 year, 5 year and 3 year horizons

In terms of Revenue, Profits, TSR Vs. Sensex

Consistency of Performance

95-96 to

13-14

03-04 to

13-14

08-09 to

13-14

10-11 to

13-14

18 years 10 years 5 years 3 years

NTO 15.3% 17.7% 16.1% 15.8%

PAT 21.6% 18.6% 21.9% 20.8%

TSR 25.9% 28.7% 33.7% 26.4%

Sensex 11.1% 14.9% 18.2% 4.8%

CAGR

TSR and Sensex returns based on Mar-end of each FY

4

ITC’s rankingAmongst all listed private sector cos.

PBT: No. 6

PAT: No. 5

Market Capitalisation: No. 3

Note: Based on Published Results for FY14, Market Capitalisation based on 30th Jun 2014

5

ITC is the only Indian Company to be ranked

amongst the Top 10 global FMCG companies in

value creation during the period 2008-12

(Boston Consulting)

6

One of the foremost in the private sector in terms of :

– Sustained value creation (BT-Stern Stewart survey)

– Operating profits

– Cash Profits

Only Indian FMCG Company to feature in Forbes 2000 List

– A comprehensive ranking of world’s biggest companies measured by acomposite of sales, profits, assets & market value

Also ranked amongst the Top 10 global FMCG companies in terms of value

creation during the period 2005-2009 by Boston Consulting Group. Is the only

Indian company to feature consistently amongst the Top 10 global FMCG

companies.

One of India’s most valuable and admired companies

7

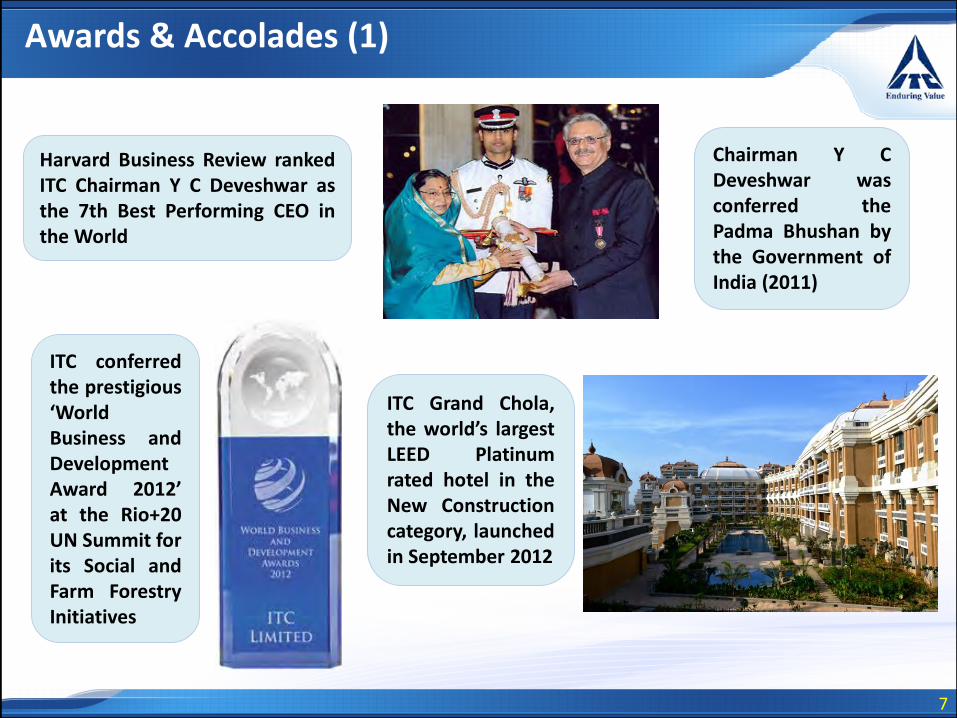

Awards & Accolades (1)

Harvard Business Review rankedITC Chairman Y C Deveshwar asthe 7th Best Performing CEO inthe World

ITC conferredthe prestigious‘WorldBusiness andDevelopmentAward 2012’at the Rio+20UN Summit forits Social andFarm ForestryInitiatives

Chairman Y CDeveshwar wasconferred thePadma Bhushan bythe Government ofIndia (2011)

ITC Grand Chola,the world’s largestLEED Platinumrated hotel in theNew Constructioncategory, launchedin September 2012

8

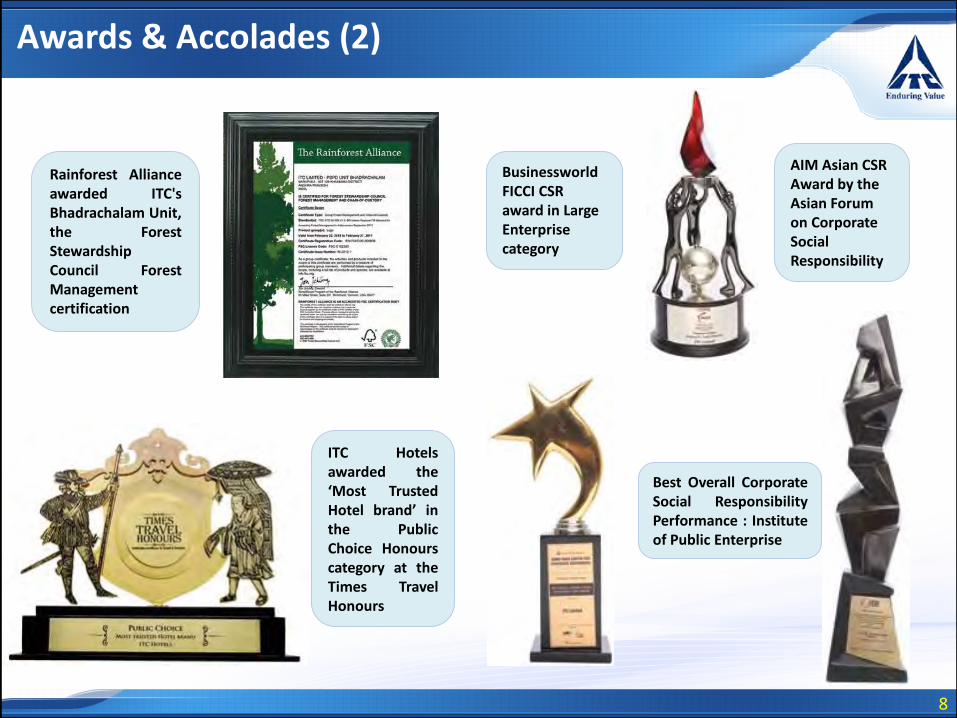

Awards & Accolades (2)

Businessworld FICCI CSR award in Large Enterprise category

Best Overall CorporateSocial ResponsibilityPerformance : Instituteof Public Enterprise

AIM Asian CSR Award by the Asian Forum on Corporate Social Responsibility

Rainforest Allianceawarded ITC'sBhadrachalam Unit,the ForestStewardshipCouncil ForestManagementcertification

ITC Hotelsawarded the‘Most TrustedHotel brand’ inthe PublicChoice Honourscategory at theTimes TravelHonours

9

Accolades & Awards (3)

• e-Choupal initiative wins global recognition:– World Development Report 2008 published by World Bank

– Stockholm Challenge Award 2006 in the EconomicDevelopment category which recognises initiatives thatleverage Information Technology to improve living conditionsand foster economic growth in all parts of the world.

– First Indian Company and second in the world to win theDevelopment Gateway Award 2005 for its trail-blazing e-Choupal initiative

– Corporate Social Responsibility Award from The Energy andResources Institute (TERI)

– World Business Award 2004: International Chamber ofCommerce & the HRH Prince of Wales & InternationalBusiness forum

– Harvard University case study

– Applauded by the then President of India Dr APJ Kalam inhis “special address during the national symposium tocommemorate 60th year of Independence”

10

Accolades & Awards – 2013/14

• ITC was ranked 3rd among 40 leading companies in the Nielsen Corporate Image Monitor 2013-14, and was featured among the top 5 most admired companies in India. ITC was also perceivedto be the ‘Company most active in CSR’ for the third year in a row.

• ITC voted among the top two “Buzziest Brands” in the “Corporate” category by “afaqs”, one ofthe world’s largest marketing and advertising portals.

• The ITC Green Centre at Manesar was awarded the 5 Star rating by the Bureau of EnergyEfficiency, Government of India.

• ITC Hotels was recognised as the Most Respected Company in the Hospitality category by theBusiness World Magazine.

• ITC’s Paperboards and Specialty Papers Business has beenconferred the Green Product of the Year award at the IndiaGreen Business Summit 2014.

• ITC’s Agri Business has bagged the Rural MarketingAssociation of India (RMAI) Flame Award 2013 in thecategory of excellence in Brand Promotion.

12

ITC’s Vision

Make a significant and growing contribution towards :

• mitigating societal challenges

• enhancing shareholder rewards

By

• creating multiple drivers of growth while sustaining leadership in

tobacco, and

• focusing on Triple Bottom Line Performance

Enlarge contribution to the Nation’s

- Financial capital

- Environmental capital

- Social capital

13

Key Corporate Strategies

Focus on the chosen business portfolio

– FMCG; Hotels; Paperboards, Paper & Packaging; Agri Business, Information

Technology

Blend diverse core competencies residing in various businesses to enhance

the competitive power of the portfolio

Position each business to attain leadership on the strength of world class

standards in quality and costs

Craft appropriate strategy of organisation and governance process to :

– Enable focus on each business and

– Harness diversity of portfolio to create unique sources of competitive advantage

14

ITC Business Portfolio

FMCG

Paperboards, Paper & Packaging

Hotels Agri BusinessInformation Technology

Cigarettes Personal CareFoods Lifestyle Retailing

Education & Stationery Safety Matches & Incense Sticks

15

Strategy of Organisation

Strategic Supervision

Board of Directors

Corporate Management Committee

Strategic Management

Divisional Management Committees

Executive Management

Enabling Focus

Harnessing Diversity

16

ITC’s Cigarettes Business

Market leadership

Leadership across all segments - geographic & price

Extensive FMCG distribution network

– Direct servicing of 1,00,000 markets & 2 million retail

outlets

State-of-the-art technology and world class products

17

Cigarette Industry in India

Cigarettes account for less than 12% of tobacco consumed in India unlike

world pattern of 85% due to prolonged punitive taxation

– Cigarettes (<12% of tobacco consumption in India) contribute the bulk of

Revenue to the Exchequer from tobacco sector

48% of adult Indian males consume tobacco. Only 10% of adult Indian males

smoke cigarettes as compared to 16% who smoke biris and 33% who use

smokeless tobacco (Source: Global Adult Tobacco Survey India 2010)

Annual per capita adult cigarette consumption in India is appx. one

ninth of world average

18

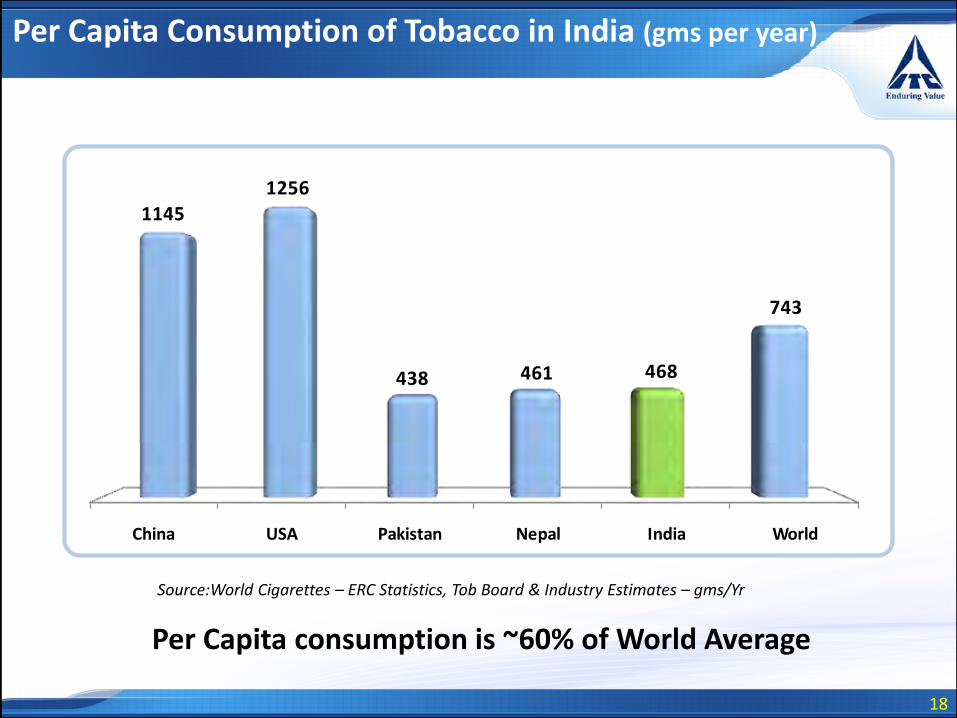

Per Capita Consumption of Tobacco in India (gms per year)

Source:World Cigarettes – ERC Statistics, Tob Board & Industry Estimates – gms/Yr

Per Capita consumption is ~60% of World Average

China USA Pakistan Nepal India World

11451256

438 461 468

743

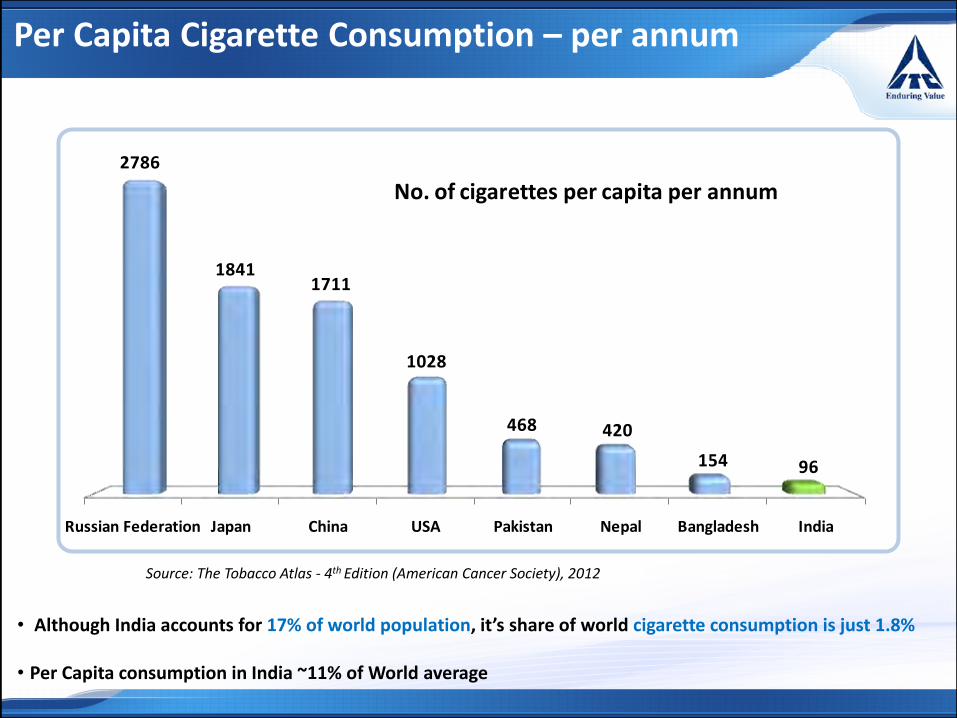

Per Capita Cigarette Consumption – per annum

Source: The Tobacco Atlas - 4th Edition (American Cancer Society), 2012

Russian Federation Japan China USA Pakistan Nepal Bangladesh India

2786

18411711

1028

468 420

154 96

No. of cigarettes per capita per annum

• Although India accounts for 17% of world population, it’s share of world cigarette consumption is just 1.8%

• Per Capita consumption in India ~11% of World average

20

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

5631013

1704

25113014

3642

4482

5545

7012

8122

Rs. crs

Rapid scale up of FMCG businesses…

22

Branded Packaged Foods

Biscuits, Staples, Snacks, Noodles & Pasta, Confectionery & Ready to Eat

23

Branded Packaged Foods

Amongst one of the fastest growing Foods business in the country– Bakery and Confectionery Foods - Biscuits, Confectionery

– Snack Foods - Savoury Snacks, Noodles and Pasta

– Staples, Spices and Ready to Eat Foods - Atta, Salt, Spices, Ready to Eat (RTE)

– Aashirvaad – Staples (Wheat flour, Salt,Spices), Ready to Eat – Ready Meals, InstantMixes

– Sunfeast – Biscuits

– Sunfeast Yippee – Noodles and Pasta

– Bingo! – Potato Chips – Yumitos, FingerSnacks – Mad Angles, Tedhe Medhe, Tangles,Galata Masti

– mint-o & Candyman – Confectionery

– Kitchens of India – Ready Meals, Premiumconserves, chutneys & cooking sauces

Atta (wheat flour) - #1 in Brandedpackaged Atta among national players

Biscuits - #3 All India

Noodles - #2 All India

Savoury Snacks - #2 All India

Confectionery - #3 in Sugar Confectionery

Ready-to-Eat - Leveraging expertise ofHotels business. PremiumConserves/Chutneys– first in India

Driven by strong brands-

24

Products

– Notebooks

– Writing Instruments (Pen, Pencils etc)

– Scholastic products

Education & Stationery

Brands

– Classmate

– Paperkraft

25

Education & Stationery Products Business

Leverages print and paper know-how to address suitable opportunities in

the stationery market.

An emerging (currently `12000 cr. Stationery) market in India - growth

driven by increasing cross-cultural exposure, government spending on

education

Classmate and Paperkraft continue to gain consumer franchise

– Classmate : Market leader in Notebooks segment

26

Personal Care Products

Brands:

• Essenza Di Wills

• Fiama Di Wills

• Vivel

• Superia

• Engage

Product portfolio:• Personal Wash

(Soaps, Shower Gel)

• Deodorants

• Skin Care(Skin Cream, Face Wash etc.)

• Hair Care(Shampoo, Conditioner)

• Talc

27

Personal Care Products

Current market size estimated at over ` 57000 crores

Portfolio approach straddling all consumer segments with 4 umbrella brands

– Essenza Di Wills

– Fiama Di Wills

– Vivel

– Superia

Recently launched ‘Engage’ brand in the fast

growing deodorants segment well received

Laboratoire Naturel – A state-of-the-art consumer and product interaction

centre – leveraged to launch unique and differentiated products

Products continue to receive encouraging consumer response

28

Lifestyle Retailing

• Enhanced lustre & premiumness to brand ‘Wills’ to a position of eminence

• Offering a Lifestyle proposition with portfolio straddling multiple genres

- Wills Lifestyle - a fashion destination, offers a choice of super-premium formals, designer,work, relaxed & evening wear and fashion accessories

- John Players embodies the spirit of the modern youth that is playful, fashionable and cool

29

Lifestyle Retailing

Upmarket product range available in exclusive Wills Lifestyle stores (92) across 40

cities and more than 700 ‘shop-in-shops’ in leading departmental stores and multi-

brand outlets.

Strong distribution network in place for the mid-market brand ‘John Players’

– availability in more than 400 Exclusive Branded outlets, 1600 multi branded

outlets and departmental stores

‘Club ITC’ – a pan-ITC consumer loyalty programme – with over 1.8 Lakh members,

serves as a platform for creating superior bonding with premium consumers and

leverages synergies between Wills Lifestyle and ITC Hotels

30

Safety Matches & Incense sticks (Agarbattis)

Current Safety Matches & Incense sticks industry consumer spend

estimated at ~ ` 6,700 crores

‘AIM’ – India’s largest selling Safety Matches brand

‘Mangaldeep’ : India’s second largest selling Incense sticks brand

ITC markets its brands with value-added products across price points

ITC’s Matches & Incense sticks businesses provide livelihood opportunities

to more than 18000 people

32

Hotels & Tourism industry

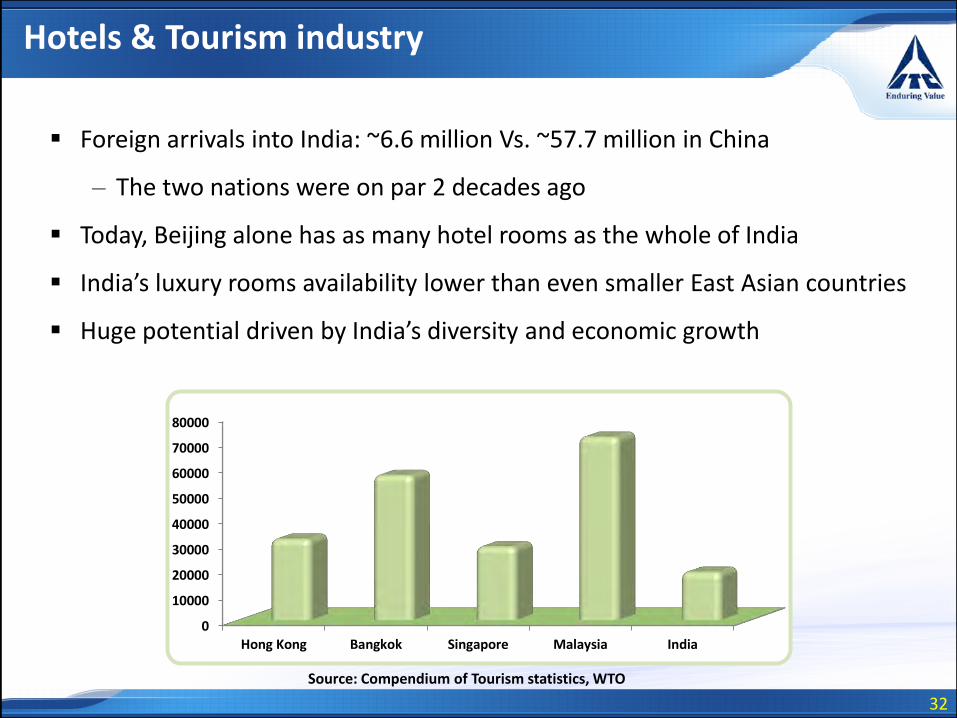

Source: Compendium of Tourism statistics, WTO

Foreign arrivals into India: ~6.6 million Vs. ~57.7 million in China

– The two nations were on par 2 decades ago

Today, Beijing alone has as many hotel rooms as the whole of India

India’s luxury rooms availability lower than even smaller East Asian countries

Huge potential driven by India’s diversity and economic growth

0

10000

20000

30000

40000

50000

60000

70000

80000

Hong Kong Bangkok Singapore Malaysia India

33

Indian Hotel Industry

Current supply – ~183,000 rooms of which 5 Star category represents

nearly 50,000 of total inventory

India needs an additional 50,000 rooms in the next 3/5 years to

service projected tourist arrivals

Present high levels of room inventory in key Indian cities leading to a

relatively weak pricing scenario to persist over the short term

As infrastructure for trade & commerce improves - potential for

leisure tourism to grow

34

100 properties across 70 locations

– 4 Brands – ITC Hotels, WelcomHotel, Fortune & WelcomHeritage

20 Five-Star Deluxe/ Five-Star Properties with over 4500 rooms

43 Fortune Hotels with nearly 3600 rooms

37 WelcomHeritage Properties with over 900 rooms

Added four new hotels under Management Contract at New Delhi,Chandigarh, Kollam and Kozhikode in 2013/14.

‘ITC Hotels’ rated as greenest luxury hotel chain in the world

– ITC Grand Chola - First 5 Star 'Green Rating for Integrated Habitat Assessment'

(GRIHA) rated luxury hotel by the Ministry of New and Renewable Energy.

Projects underway at Kolkata, Classic Golf Resort (near Gurgaon) andHyderabad.

ITC Hotels

“Responsible Luxury” ethos weaved into the Brand Identity

ITC Hotels: World’s Greenest Luxury Hotel Chain

All ITC Luxury Hotels LEED Platinum certified

36

Paperboards & Packaging Business

• No. 1 in Size

• No. 1 in Profitability

• No. 1 in Environmental Performance

37

Indian Paperboard market

Annual paperboard demand over 2 million tonnes

Low per capita usage of paper at around 9 kgs p.a. (world average –over 55 kgs p.a.)

Indian paperboard market growing at 6% p.a.

Value-added Paperboards- the fastest growing segment (12% p.a.)in India driven by :

Increasing demand for branded packaged products

Rising Income table and growing consumer base

Increasing proliferation of organised retail

38

Market leader in growth segment – Value-Added Paperboards

World-class contemporary technology– Ozone bleached Pulp Mill fully operational – one of its kind in Asia meeting world-class

environmental standards– Fully integrated with in-house pulping capacity at ~3 lakh MT

Internationally competitive quality and cost

Social farm forestry in mill command area to improve access to cost effective fibre &to attain self-sufficiency– Biotech research based high yielding clones – effectiveness tested in approx. 165000

hectares

Newly commissioned 1 lakh MT per annum Paperboard machine running well

ITC’s packaging SBU - India’s largest converter of Paperboard into high quality printedpackaging– Provides superior packaging solutions to the cigarettes and new FMCG businesses– Leading supplier to Indian FMCG industry– Fully integrated packaging unit at Haridwar operationalised and running well

ITC’s Paperboards, Paper & Packaging businesses

39

Agri Business

• No. 1 in Leaf Tobacco

• No. 2 in Agri commodities

• Pioneer in rural transformation

40

Indian Leaf Tobacco industry

India – the second largest producer of tobacco

However, India’s share is only at 8% of world tobacco trade

ITC – India’s largest buyer, processor, consumer & exporter of cigarettetobaccos– 5th largest leaf tobacco exporter in the world

Pioneering cultivation of flavourful Flue-cured and superior Burleytobaccos in India

Robust growth in exports in recent years with improvement in realizations

41

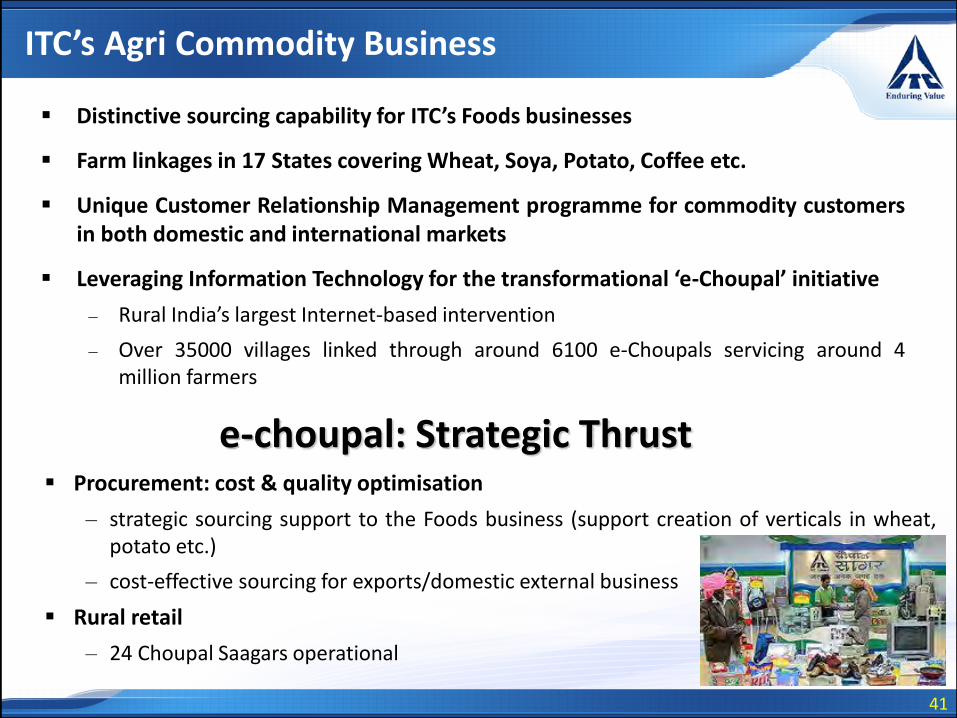

ITC’s Agri Commodity Business

Distinctive sourcing capability for ITC’s Foods businesses

Farm linkages in 17 States covering Wheat, Soya, Potato, Coffee etc.

Unique Customer Relationship Management programme for commodity customersin both domestic and international markets

Leveraging Information Technology for the transformational ‘e-Choupal’ initiative

– Rural India’s largest Internet-based intervention

– Over 35000 villages linked through around 6100 e-Choupals servicing around 4million farmers

e-choupal: Strategic Thrust Procurement: cost & quality optimisation

– strategic sourcing support to the Foods business (support creation of verticals in wheat,potato etc.)

– cost-effective sourcing for exports/domestic external business

Rural retail

– 24 Choupal Saagars operational

42

ITC - Key Financials – 2013/14

Rs. Cr.

2013-14 2012-13 Goly %

Gross Turnover 46713 41810 11.7

Net Turnover 32883 29606 11.1

PBDIT 13562 11566 17.3

PBIT 12662 10771 17.6

PBT 12659 10684 18.5

PAT 8785 7418 18.4

43

Segment Revenue - 2013/14

Rs. Cr.

2013-14 2012-13 %

Segment Revenue (Net)

a) FMCG - Cigarettes 15456 13970 10.6

- Others 8099 6983 16.0

Total FMCG 23555 20953 12.4

b) Hotels 1133 1074 5.5

c) Agri Business 7752 7201 7.7

d) Paperboards, Paper & Packaging 4861 4237 14.7

Total 37301 33464 11.5

Less : Inter segment revenue 4418 3859 14.5

Net sales / income from operations 32883 29606 11.1

Full YearGOLY(%)

44

Segment Results - 2013/14

Rs. Cr.

2013-14 2012-13

Segment Results

a) FMCG - Cigarettes 9858 8326 18.4

- Liab. no longer reqd. written 158 0

FMCG - Cigarettes 10016 8326 20.3

- Others 22 (81)

Total FMCG 10038 8245 21.7

b) Hotels 140 138 1.5

c) Agri Business 835 731 14.2

d) Paperboards, Paper & Packaging 892 964 (7.4)

Total 11905 10078 18.1

Less: i) Finance Costs 38 86 (56.4)

Liab. no longer reqd. written back (35) 0

Finance Costs 3 86 (96.6)

ii) Other Unallocable Exp/(Inc.) - Net (757) (693) 9.3

Profit Before Tax 12659 10684 18.5

Full YearGOLY(%)

45

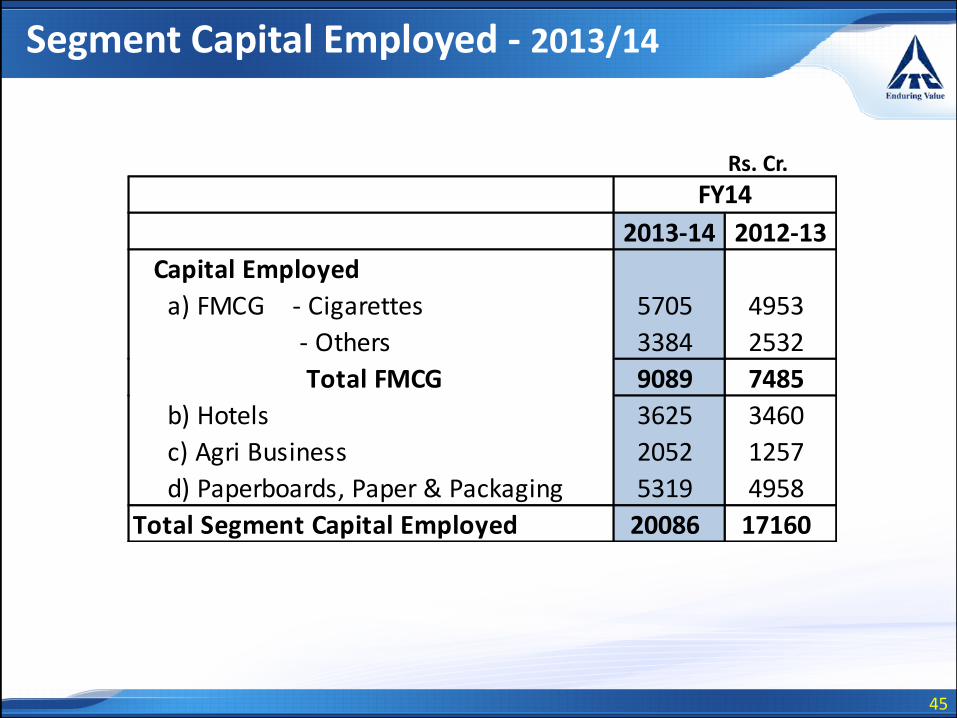

Segment Capital Employed - 2013/14

2013-14 2012-13

Capital Employed

a) FMCG - Cigarettes 5705 4953

- Others 3384 2532

Total FMCG 9089 7485

b) Hotels 3625 3460

c) Agri Business 2052 1257

d) Paperboards, Paper & Packaging 5319 4958

Total Segment Capital Employed 20086 17160

FY14Rs. Cr.

46

ITC - Key Financials – Q1 2014/15

Rs. Cr.

Q1 14/15 Q1 13/14 Goly %

Net Revenue 9164 7339 24.9

PBDIT 3512 2994 17.3

PBIT 3281 2779 18.0

PBT 3266 2762 18.2

PAT 2186 1891 15.6

47

Segment Revenue - Q1 2014/15

` Crs.

Q42013-14 2014-15 2013-14

Segment Revenue (Net)

4079 a) FMCG - Cigarettes 4201 3537 18.8

2315 - Others 1935 1745 10.9

6393 Total FMCG 6136 5282 16.2

321 b) Hotels 249 250 (0.5)

2004 c) Agri Business 3296 2189 50.6

1261 d) Paperboards, Paper & Packaging 1288 1163 10.8

9979 Total 10969 8884 23.5

834 Less : Inter segment revenue 1804 1546 16.8

9145 Net sales / income from operations 9164 7339 24.9

Q1GOLY(%)

Rs. Cr.

48

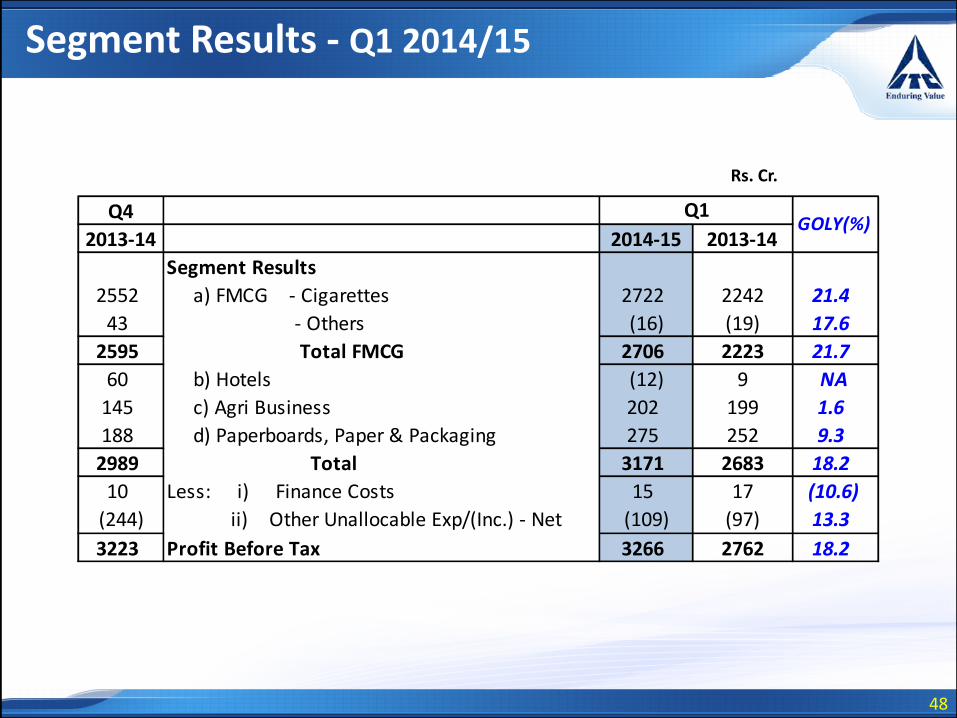

Segment Results - Q1 2014/15

` Crs.

Q4

2013-14 2014-15 2013-14

Segment Results

2552 a) FMCG - Cigarettes 2722 2242 21.4

43 - Others (16) (19) 17.6

2595 Total FMCG 2706 2223 21.7

60 b) Hotels (12) 9 NA

145 c) Agri Business 202 199 1.6

188 d) Paperboards, Paper & Packaging 275 252 9.3

2989 Total 3171 2683 18.2

10 Less: i) Finance Costs 15 17 (10.6)

(244) ii) Other Unallocable Exp/(Inc.) - Net (109) (97) 13.3

3223 Profit Before Tax 3266 2762 18.2

Q1GOLY(%)

Rs. Cr.

49

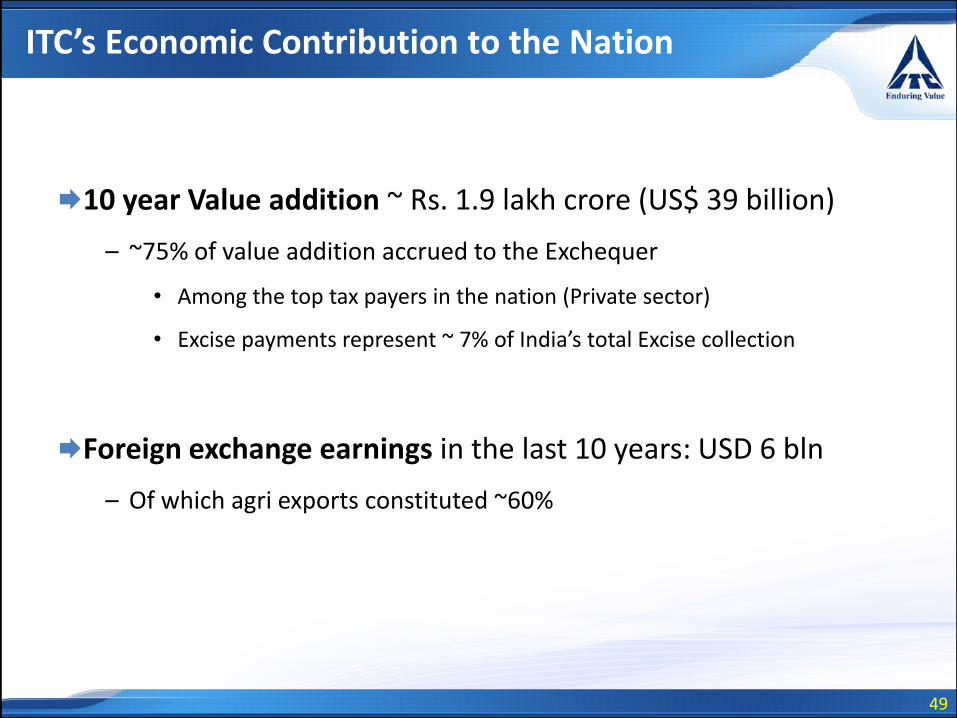

ITC’s Economic Contribution to the Nation

10 year Value addition ~ Rs. 1.9 lakh crore (US$ 39 billion)

– ~75% of value addition accrued to the Exchequer

• Among the top tax payers in the nation (Private sector)

• Excise payments represent ~ 7% of India’s total Excise collection

Foreign exchange earnings in the last 10 years: USD 6 bln

– Of which agri exports constituted ~60%

50

Social Performance

Direct employment ITC Group : 30,000

Supported creation of 6 million sustainable livelihoods

e-choupal: world’s largest rural digital infrastructure serving around 4million farmers

Social and Farm forestry initiative has greened nearly 164,500hectares & provided over 73 million person-days of employmentamong tribals & marginal farmers

Significant thrust on social sector investments– Natural resource management– Sustainable livelihoods– Community development programmes in the economic vicinity of

operating locations

51

Environmental Performance

Carbon positive enterprise – 9 years in a row– Sequestering one and half times the amount of CO2

that the company emits

Water positive - 12 years in a row– Creating twice the rainwater harvesting potential

than ITC’s net water consumption

Solid waste recycling positive – 7 years in a row

Over 38% of total energy consumed is fromrenewable sources

Only Company in the world of comparable dimensions to have achieved the global environmental distinction of being Carbon positive, Water positive and Solid

waste recycling positive

52

Forward-looking Statements

Statements in this presentation describing the Company’s objectives, future prospects, estimates, expectations etc. may be “forward looking statements” within the meaning

of applicable securities laws and regulations. Investors are cautioned that “forward looking statements” are based on certain assumptions of future events over which the

Company exercises no control. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new

information, future events, or otherwise. Therefore there can be no guarantee as to their accuracy. These statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those that may be

projected or implied by these forward looking statements. Such risks and uncertainties include, but are not limited to: growth, competition, acquisitions, domestic and

international economic conditions affecting demand, supply and price conditions in the various businesses in the Company’s portfolio, changes in Government

regulations, tax regimes and other statutes, and the ability to attract and retain high quality human resource.