jacquelin watts - …€¦ · web viewassignment 2. step 7. the contribution margin is the revenue...

TRANSCRIPT

Jacquelin Watts | Jacquelin Watts

Assignment 2

Step 7

The contribution margin is the revenue that remains after a business sells a

product, or a service, and deducts its variable costs. The contribution margin is used

to cover fixed costs, and any revenue remaining is attributed to profit. Contribution

margins can be calculated for individual products or for a product line, and are useful

for determining which products or services are contributing the most to a firm’s profit.

Negative contribution margins should always be avoided as they indicate that the

product, or service, is not profitable, at the current selling price.

Crowdspark Limited is an online publishing company that sells photographs,

videos and news stories to its clients, including Associated Press (AP), Getty Images

and Australian Associated Press (AAP), and many other news agencies around the

world. Crowdspark’s media content is sourced through crowdsourcing, where

amateur and professional photographers can send their media online to Crowdspark,

via the Newzulu app. If the crowdsourced media is chosen for publication and/or

licensing, the photographer or news writer will receive payment from Crowdspark.

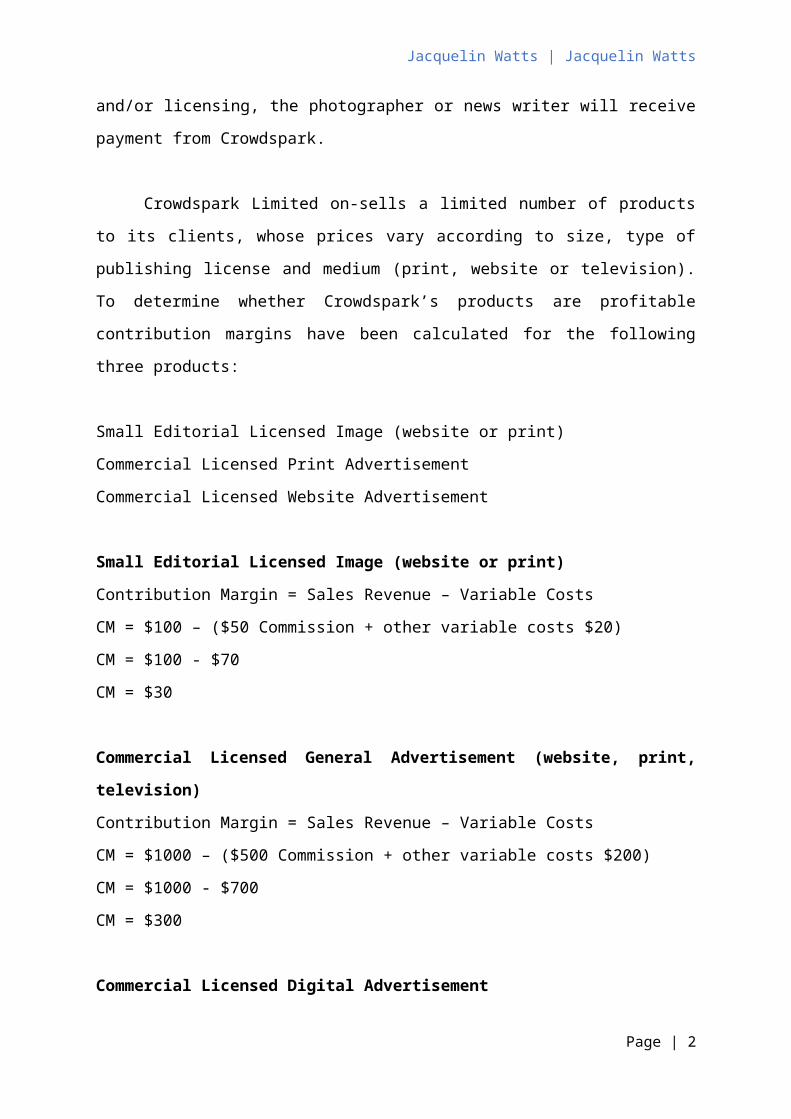

Crowdspark Limited on-sells a limited number of products to its clients, whose

prices vary according to size, type of publishing license and medium (print, website

or television). To determine whether Crowdspark’s products are profitable

contribution margins have been calculated for the following three products:

Small Editorial Licensed Image (website or print)

Commercial Licensed Print Advertisement

Commercial Licensed Website Advertisement

Page | 1

Jacquelin Watts | Jacquelin Watts

Small Editorial Licensed Image (website or print)Contribution Margin = Sales Revenue – Variable Costs

CM = $100 – ($50 Commission + other variable costs $20)

CM = $100 - $70

CM = $30

Commercial Licensed General Advertisement (website, print, television)Contribution Margin = Sales Revenue – Variable Costs

CM = $1000 – ($500 Commission + other variable costs $200)

CM = $1000 - $700

CM = $300

Commercial Licensed Digital AdvertisementContribution Margin = Sales Revenue – Variable Costs

CM = $600 – ($300 Commission + other variable costs $200)

CM = $600 - $500

CM = $100

Crowdspark do not list any prices on their website, other than stating that they

will split the sale price of the media 50/50 with the photographer or news writer. To

get an idea on pricing I researched the prices that Getty Images use, as Getty is the

market leader in licensed images. As the market leader, Getty’s prices are high so I

lowered them for Crowdspark. Crowdspark also sells images to Getty, which I

estimated would be at a lower rate than the price Getty sells its images on its

website, for example, Getty sells a small editorial image or web video for $200.

As a company that operates predominantly online I would estimate that

Crowdspark do not have many variable costs other than marketing, wages, and

commission (50% of the sale price). Similarly, I would not expect them to have

significant fixed costs, but perhaps they did because at the 30 June 2016

Crowdspark had $588,088 of property, plant and equipment. At the 30 June 2017

Crowdspark had reduced its property, plant and equipment to $97,004. Property,

plant and equipment all have fixed costs attached to them, for example, rent,

Page | 2

Jacquelin Watts | Jacquelin Watts

insurance, interest expense, utilities and depreciation. Crowdspark has been

operating at a loss over the last three years and by decreasing fixed costs this would

leave a greater contribution margin for profit.

I would estimate that contribution margins would be similar between products.

Differences in sales price could occur in relation to the content of the media, for

example a crowdsourced photograph of a celebrity would probably fetch a higher

price than a landscape photograph. It is not clear whether Crowdspark edit the

media they receive, and if they do this would increase their variable costs (wages).

Even though editorial media has the lowest contribution margin Crowdspark should

include these in its product line as they are the cheaper alternative for small

businesses. However, Crowdspark face a market constraint with editorial media from

cheaper stock photography websites, like iStock.

Crowdspark, like Getty Images, are in a niche market that will pay a premium

for high quality images, which limits their market to large companies. They face

competition from stock photography websites that sell editorial images at a much

lesser cost, between $5 to $36, which may be more attractive to small businesses.

This market constraint should be considered when Crowdspark are working out their

contribution margins. Crowdspark also relies on crowdsourced material which can

be considered a resource constraint, and should be considered alongside

contribution margins. Additionally, Crowdspark may not have the crowdsourced

media a business is looking for at any given time. No guidelines are given to what

type of photography or media can be sent to Crowdspark, which leaves a lot of

uncertainty as to whether they will have the right product on hand. Crowdspark are

operating at a loss, so market and resource constraints could be producing negative

contribution margins. Looking at Crowdspark’s financial ratio’s will help pinpoint why

Crowdspark has had a negative profit margin over the last four financial years.

References

Dean, T. (2017, April 11). The Cost of Commercial Image Licenses – Average Getty Prices [web blog post]. Retrieved May 23, 2018, from https://blog.bllush.com/research/the-cost-of-commercial-image-licences-average-getty-prices/

Getty Images. (2018). Plans and Pricing. Retrieved from https://www.gettyimages.com.au/plans-and-pricing

Page | 3

Jacquelin Watts | Jacquelin Watts

Step 8

What’s Going on Crowdspark?

Crowdspark Limited continues to operate at a loss in 2018, and is not keeping

up with its peers in the online publishing industry, who on average are profitable and

are generating positive earnings (Lombardo, 2018). On the 4 th May, 2018

Crowdspark’s (ASX:CSK) share price dropped 25% to 5.1c, and their quarterly

figures showed a decrease in sales from $868,000 to $340,000 (Yeo, 2018).

Crowdspark’s expenses are currently higher than its sales and its earning loss is at -

$8.24M (Lombardo, 2018). Working out Crowdspark’s financial ratios for the last four

financial years, will give a clearer picture of ‘what’s going on with Crowdspark’.

Profitability Ratios

Net Profit Margin (NPM)

The net profit margin is a ratio of earnings to revenue (net profit divided by

revenue). It shows how much profit (or loss) each dollar of sales generates, or how

much profit it gets to keep after it pays all its expenses (or how much excess it spent

per dollar of sales).

Page | 4

Jacquelin Watts | Jacquelin Watts

Even though Crowdspark is making a loss, the net profit margin (or negative

profit margin) can still provide useful information. It shows how much extra

Crowdspark spent for each dollar of sales (as shown in the following table).

Net Profit Margin Excess spending per $1 of

revenue

2017 -421.08% $4.21

2016 -599.44% $5.99

2015 -1946.60% $19.47

2014 -176.44% $1.76

The net profit margin also shows how efficient Crowdspark have been in reducing

their loss. In 2016 the amount Crowdspark spent for every $1 of revenue ($5.99)

decreased dramatically from 2015 ($19.47). In 2017 the negative profit margin has

decreased by a further $1.78.

Return on Assets (ROA)

The return on assets (ROA) shows how efficiently a firm is using its assets to

generate income or profit (net income divided by total assets). It determines how

much profit is being generated for each dollar of assets. Like money in the bank, it is

a measure of the return on investment (assets). In a business the purpose of assets

is to generate revenue and profit, and consists of debt and equity used to finance the

business operations (assets = liabilities + equity).

Crowdspark has had a negative ROA for the last four financial years (as

shown in the following table). In the 2017 financial year, every dollar that Crowdspark

invested in assets resulted in a loss of net income by $1.80.

Return on Assets Net Loss per $1 of Assets

2017 -179.6% $1.80

2016 -138% $1.38

2015 -196.2% $1.96

2014 -83.1% 83c

Page | 5

Jacquelin Watts | Jacquelin Watts

Crowdspark’s negative ROA may suggest that they are investing a high amount of

capital (debt and equity) into financing the company, while simultaneously receiving

little income. Even though Crowdspark went through significant restructuring in the

2017 financial year their ROA has resulted in a greater loss than in the 2016 financial

year, because they sold assets (closed several offices and reduced staff numbers).

.

Efficiency (or Asset Management) Ratios

Days of Inventory

The days of inventory, or inventory turnover in days, shows how long it takes

a firm to turn its inventory into sales (inventory divided by average daily cost of

goods sold).

Crowdspark do not have any inventory recorded in their balance sheet, so it is

not possible to work out the days of inventory. One reason that Crowdspark may

have no inventory is that it incurs no costs for its media until it is sold, as the

crowdsourced material remains the property of the photographer, or news reporter,

until it is sold by Crowdspark.

Total Asset Turnover Ratio (TATR)

The total asset turnover ratio shows how efficiently a firm is turning its assets

over to generate revenue (net sales divided by total assets). It indicates how much

revenue a firm is generating for each dollar of assets, including buildings, equipment,

cash and inventories.

In 2017, Crowdspark turned over its assets 0.43 times to generate revenue, or

for every dollar of assets they generated 43c. Crowdspark has been slowly

increasing its asset turnover ratio since 2015 from 0.10, to 0.43 in 2017, which

suggests they are more efficiently using their assets to generate revenue. However,

their asset turnover is still very low, which may be contributing to their negative profit

margin. The negative profit margin may also be contributing to the low turnover of

Page | 6

Jacquelin Watts | Jacquelin Watts

assets. Furthermore, the balance between Crowdspark’s profit margin and its asset

turnover may also be influenced by product demand and cheaper competition.

Crowdspark’s prices may be too high, which reduces their product demand

and results in fewer sales. If Crowdsparks sales increase then their assets would

turn over more quickly. Financial investments, such as stocks and bonds, are also

assets and increasing the amount of investment turnover can ultimately achieve a

higher profit margin. Crowdspark, as an online publishing service industry is not an

asset intensive industry, so their asset turnover should be higher.

Liquidity Ratios

Current Ratio

The current ratio, or working capital ratio, measures a firm’s ability to pay for

its short-term obligations (bills) from its current assets (current assets divided by

current liabilities).

Crowdspark has enough assets to cover its liabilities, and this has been

increasing over the last four financial years from 0.20 in 2014, to 2.75 in 2017. A

current ratio of 2 is preferable, and Crowdspark have had a current ratio of greater

than 2 for the last two financial years. At present Crowdspark has enough assets to

cover its liabilities if it faced liquidation. However, it is important to note the type of

current assets a firm has, and whether they can be quickly converted to cash if

necessary. A firm with a high current ratio may not be any safer than a firm with a

low current ratio if its assets cannot be readily turned into cash, or are of an inferior

quality. Crowdspark’s current assets mainly consist of cash, and cash equivalents,

so if cash was the only current asset considered Crowdspark would still be able to

pay its obligations in 2017 (cash $5,001,740 divided by current assets $2,086,648 =

current ratio of 2.39).

Page | 7

Jacquelin Watts | Jacquelin Watts

Financial Structure Ratios

Debt/Equity Ratio (D/E Ratio)

The debt/equity ratio, compares a firm’s total liabilities with its shareholders’

equity, and reveals a firm’s debt as a percentage of its total market value (total

liabilities divided by total equity). It shows how much a firm depends on borrowed

funds and its ability to meet its financial obligations. A firm that is highly leveraged

(carries a lot of debt) compared with its equity, is less likely to provide a return to its

shareholders. However, some debt can be advantageous to raise capital to expand

and grow the firm, and potentially increase profits.

Over the last three years Crowdspark’s debt/equity ratio has been steadily

climbing from 33.2% in 2015, to 64.3% in 2017. A 64% D/E ratio shows that for every

dollar of equity Crowdspark has 64c worth of debt. There was a big jump in the ratio

from 2016 (38%) to 2017 (64.3%) indicating that Crowdspark have been aggressive

in financing its growth with debt. Aggressive leveraging (attempting to increase value

by using debt to finance projects) can be risky, as it also increases interest expense,

and Crowdspark’s expenses are already exceeding their revenue. In 2014,

Crowdspark had a negative D/E ratio of -230% suggesting that its liabilities

exceeded its assets.

Equity Ratio

The equity ratio measures the amount of equity in a firm, compared to the

amount of assets a firm owns (equity divided by total assets). It indicates what

percentage of a firm’s assets are owned by investors, and therefore safe if the firm

was to go bankrupt. A higher percentage indicates that most of the business is

owned by its shareholders, rather than being leveraged or owned by the bank

through debt.

Page | 8

Jacquelin Watts | Jacquelin Watts

Crowdspark’s equity ratio has decreased from 75% in 2015, to 60% in 2017,

suggesting they are taking on more debt to finance their operations. In 2014

Crowdspark had a negative equity ratio as their total equity on the balance sheet

was -$1,066,143. However, between 2014 and 2015 Crowdspark’s equity ratio

increased from negative 76% to positive 75%, after they raised capital by offering

shares, and their total equity on their balance sheet increased to $10,915,511. A firm

can increase its equity by issuing new shares, or by making a profit, and decrease its

equity by buying back its own shares, buying assets or by operating at a net loss.

Crowdspark increased its equity by buying new shares in 2015, but has still been

operating at a net loss, over the last four financial years, which will also be

contributing to their decrease in equity.

Market Ratios

Earnings per Share (EPS)

The earnings per share (EPS) shows how much of a firm’s profit can be

allocated to one share (net income divided by number of issued ordinary shares).

EPS breaks down a firm’s profit (or loss) on a per share basis, and shows what the

market is willing to pay based on a firm’s net income.

Page | 9

Jacquelin Watts | Jacquelin Watts

Over the last four years, Crowdspark’s EPS has been negative, suggesting

they are operating at a loss, rather than generating profit for its shareholders. A net

loss will result in a lowering of the value of stock. However, sometimes a firm may

spend years operating at a loss as it develops new products, and its EPS will slowly

move towards being positive. This may be the case with Crowdspark as their EPS is

slowly moving towards being positive over the last four years, and their net loss has

also been decreasing. In 2017 Crowdspark developed an app for android and IOS,

and updated its online platform so users can access social media sites for uploading

their content to Crowdspark.

Dividends per Share (DPS)

The dividends per share (DPS) shows how much net income is distributed to

shareholders as dividends (dividends divided by number of issued ordinary shares).

Crowdspark has not paid any dividends in the last four financial years as it

has been operating at a loss. Crowdspark’s EPS has also been negative over the

last four years as there is no profit to put towards shares.

Price Earnings Ratio (P/E Ratio)

The price earnings ratio measures a firm’s current share price relative to its

per share earnings (market value per share divided by earnings per share). It is the

amount an investor can expect to invest in a firm to receive $1 of the firm’s earnings,

for example, a P/E ratio of 20 would indicate that an investor is willing to pay $20 for

$1 of current earnings, or alternatively it would take the investor 20 years to make

$1. A positive P/E ratio shows that the company is making a profit, while a negative

P/E ratio shows the company is making a loss.

For the last four years Crowdspark’s EPS value has been negative which

shows that Crowdspark is losing money, which also directly affects the P/E ratio.

.

Page | 10

Jacquelin Watts | Jacquelin Watts

Ratios based on Reformulated Financial Statements

Return on Equity (ROE)

The return on equity, or return on net worth, shows how much of a firm’s net

income (profit) is returned to its shareholders and investors (net income (CI) divided

by shareholders’ equity).

The ROE is like the ROA, but the ROE also considers financial leverage, or

debt. The fundamental accounting equation states that assets = liabilities + equity,

so if a firm had no debt its assets and equity would be the same (ROA = ROE).

However, if a firm is leveraged (takes on debt) the ROE would rise above the ROA.

Increasing debt increases a firm’s assets, but decreases equity (equity = assets –

liabilities).

Crowdspark has a negative net income (more debt and operating expenses

than revenue) which has a large impact on ROE, when compared to ROA, as they

have no cash left to pay their equity holders. They are also borrowing a lot of money,

with their 2017 debt/equity ratio at 64%, which creates a large difference between

ROA and ROE (see table below).

Return on Assets (ROA) Return on Equity (ROE)

2017 -179.6% -295.01%

2016 -138% -190.47%

2015 -196.2% -261.41%

2014 -83.1% 108.08%

Over the last four financial years Crowdspark’s ROE has fluctuated from positive

108% in 2014 to negative 295% in 2017. In 2017 Crowdspark has lost 295% of its

total shareholder equity. Their loss has increased further since 2016 (190%).

Page | 11

Jacquelin Watts | Jacquelin Watts

Return on Net Operating Assets (RNOA)

The return on net operating assets (RNOA), shows how much operating

income a firm has in relation to its operating assets (operating income (OI) divided

by net operating assets (NOA). It is useful for determining a firm’s long-term ability to

create value for its equity owners, by using its assets to create profit. The RNOA is

like the ROA, except the RNOA considers operating liabilities and operating assets

(NOA), rather than total assets (including financing and investing). If a firms RNOA is

higher than its ROA this suggests a better return on assets.

In 2017 Crowdspark’s RNOA was considering higher than its ROA suggesting

a better return on assets (as shown in the following table).

Return on Assets Return on Net Operating

Assets

2017 -179.6% n/a

2016 -138% -425.9%

2015 -196.2% -374.2%

2014 -83.1% -4975.4%

In 2017, Crowdspark closed several offices and reduced its employees from 84 to 29

which reduced its operating costs significantly. The cash from the sales of assets of

$5.7 million meant that Crowdspark’s financial assets increased significantly.

However, it also meant that operating liabilities (OL) were higher than operating

assets (OA), resulting in net operating liabilities (NOL), rather than net operating

assets (NOA) as seen in previous years. This meant that for 2017 I was unable to

calculate RNOA as Crowdspark had NOL, instead of NOA.

Net Borrowing Cost (NBC)

Page | 12

Jacquelin Watts | Jacquelin Watts

The net borrowing cost (NBC) shows the average interest rate a firm is paying

for its financing, including interest costs (net financial expenses (NFE)/net financial

obligations (NFO).

Crowdspark only had NFO in 2014, and in the remaining years they had net

financial assets (NFA). In 2014, Crowdspark had an interest rate of 0.99%, which

was an excellent interest rate.

As Crowdspark had NFA from 2015 to 2017, I could calculate net financial

income (NFI). However, in 2016 and 2017 Crowdspark had NFE rather than NFI, so I

could only calculate NFI for 2015. In 2015, Crowdsparks NFI was 14.65%, which is

most likely a result of selling 85.7 million shares at $0.042, and raising $3 million, in

2015.

Profit Margin (PM)

The profit margin (PM) shows how much profit (or loss) a firm makes, after

paying for variable costs, but excluding financial expenses (operating income (OI)

divided by sales). The PM takes a wider look at costs compared to the NPM, and is a

better indication of how well a firm’s operations are contributing to profit. Firm’s with

high PM’s can be more competitive by lowering prices, are better able to survive

economic downturns and pay for all their costs.

Crowdspark has had a negative PM over the last four years, and shows only a

slight improvement when compared with its NPM (see table below).

Net Profit Margin Profit Margin

2017 -421.08% -416.34%

2016 -599.44% -586.01%

2015 -1946.60% -1909.55%

2014 -176.44% -174.79%

This suggests that Crowdspark’s business operations (operating income and

expenses), rather than its financial expenses, are contributing the most to its current

loss, and it is requiring a large amount of finances to sustain operations. It is useful

Page | 13

Jacquelin Watts | Jacquelin Watts

to pinpoint where costs can be decreased to generate more profit, and Crowdspark’s

PM has decreased substantially from -1909% in 2015, to -416% in 2017.

Asset Turnover (ATO)

Like the total asset turnover ratio (TATR), the asset turnover (ATO) shows

how efficient a firm is turning assets over to generate revenue. However, it differs to

the TATR by only considering operating assets and operating liabilities (sales

divided by operating assets (NOA). The ATO measures the number of sales

generated for each one dollar of assets, excluding financial assets such as cash (see

table below for Crowdspark’s comparison of TATR and ATO).

Total Asset Turnover Ratio Asset Turnover

2017 0.43 n/a

2016 0.23 0.73

2015 0.10 0.20

2014 0.47 28.47

In 2017, Crowdspark’s TATR meant that for every dollar of assets they were

generating 43c of revenue. However, as they had no net operating assets (NOA) in

2017, the ATO could not be calculated. In 2014, the ATO was a healthy 28.47,

indicating that for every dollar of operating assets Crowdspark was generating

$28.47. This was probably due to Crowdspark having fewer operating assets in

2014, but more sales when compared with their operating assets (see table below).

When operating assets are separated from financial assets it is a much better

indicator of how operating assets are generating revenue for a firm.

Sales NOA ATO

2017 2,491,706 n/a n/a

2016 2,779,242 3,823,952 0.73

2015 1,511,477 7,713,943 0.20

2014 653,110 22,944 28.47

Page | 14

Jacquelin Watts | Jacquelin Watts

Economic Profit (or Loss)

Economic profit (or loss) refers to the difference between a firm’s revenue and

its economic costs, or opportunity costs. (RNOA - cost of capital) x net operating

assets (NOA). The key drivers of economic profit (or loss) are the RNOA, the cost of

capital and the NOA. Furthermore, the RNOA is driven by the PM and the ATO. The

RNOA should cover the cost of capital (WACC). Accounting profit (or loss), as shown

on a firm’s income statement, does not consider the opportunity costs a firm loses or

gains by making one decision over another, which may have led to more (or less)

revenue. Economic profit is a measurement of opportunity cost, and suggests that

firms should make returns above their cost of capital.

Crowdspark have made an economic loss from 2014 to 2016 inclusive, and in

2017 they had net operating liabilities rather than net operating assets, so the

economic profit could not be determined. The economic loss suggests that

Crowdspark have been unable to add value for its shareholders, over and above its

cost of capital. The cost of capital was set at 10% (WACC) as I was unable to locate

a different WACC in Crowdspark’s annual reports.

Crowdspark’s economic loss does not differ much to its accounting loss and

was slightly greater than in all years, except for 2014, where the economic loss was

a slight improvement on the accounting loss.

Economic Loss Accounting Loss

2017 n/a -10,492,000

2016 -16,668,918 -16,659,838

2015 -29,633,759 -28,534,565

2014 -1,143,854 -1,152,329

.

Page | 15

Jacquelin Watts | Jacquelin Watts

The key drivers of economic profit (or loss) are the RNOA (driven by PM and

ATO), the cost of capital and the NOA (see table below for Crowdsparks key

economic and accounting drivers).

PM ATO RNOA Cost of Capital (WACC)

NOA NOL

2017 -416.34% n/a n/a n/a n/a -$756438

2016 -586.01% 0.73 -425.9% -42.59% $3823952

2015 -1909.55% 0.20 -374.2% -37.42% $7713943

2014 -174.79% 28.47 -4975.4% -497.54% $22944

Firms create value for their equity holders by achieving an RNOA greater than its

cost of capital.

In 2014 to 2016, Crowdsparks RNOA could not cover its cost of capital which

was fuelled by large negative profit margins, suggesting that Crowdspark are relying

more on finances than on operations to fund its business. This is a concern for

Crowdspark because if they are not making the sales necessary to sustain the

business, they may eventually run out of cash to fund their business operations.

References

Lombardo, T. (2018, March 27). Dilution Ahead For Crowdspark Limited ASX:CSK Shareholder [web blog post]. Retrieved May 23, 2018, from

Page | 16

Jacquelin Watts | Jacquelin Watts

https://simplywall.st/stocks/au/media/asx-csk/crowdspark-shares/news/dilution-ahead-for-crowdspark-limited-asxcsk-shareholders/

Yeo, M. (2018, May 4). Lunctime Small Cap Wrap: Who’s Jumping Higher and Who’s Falling [web blog post]. Retrieved May 23, 2018, from https://stockhead.com.au/news/lunchtime-small-cap-wrap-whos-jumping-higher-and-whos-falling/

Step 9

Capital Investment Decision

In Crowdsparks 2017 annual report they stated that future developments

included developing its technologies further, and expanding its customer base

around the world. Crowdspark has a website where amateur and professional

photographers and news reporters can send their media (photographs, video’s and

reports) to Crowdspark. Crowdspark uses the crowdsourced material sent to them to

on sell to their clients. If media is purchased by one of Crowdspark’s clients the

photographer or news reporter receives 50% commission from the sale. As far as I

can tell Crowdspark are in the ‘driving seat’ as to who buys their crowdsourced

media. To develop their technology further, and to expand their customer base, I

propose Crowdspark:

(1) set up a new website for stock photography, called iSpark, where they

can offer lower prices, and customers can buy editorial licenced photographs directly

from the website. Cashflow would be generated by users being able to purchase

licenced editorial stock photography directly from the website, and the main

operating expense would involve staff maintaining and supervising the website.

(2) undertake a worldwide marketing campaign using their Facebook logo

‘Capture Newsworthy Events Near You, Upload Your Photos and Videos, Get

Published, Get Paid’.

Page | 17

Jacquelin Watts | Jacquelin Watts

Marketing can be considered a capital investment, rather than an expense, when it is

viewed as being able to create revenue. Through a successful marketing campaign

Crowdspark can direct customers to their website and mobile applications and

increase their customer base, which will directly lead to an increase in revenue, as

they will have more content to offer their clients. Operating expenses would be

minimal and primarily involve marketing staff conducting research on the results of

the advertising campaign.

The following table shows the estimated cash flows that the two projects are

expected to realise over a 10-year period.

iSpark Website Marketing CampaignOriginal Cost $40,000 $800,000Estimated Useful Life 10 years 10 yearsResidual Value $40,000 $800,000Estimated Future Cash Flows31 May 2019 +$5,000 +$400,00031 May 2020 +$10,000 +$200,000 31 May 2021 +$20,000 +$100,00031 May 2022 +$20,000 +$100,00031 May 2023 +$20,000 +$100,00031 May 2024 +$20,000 +$ 50,00031 May 2025 +$20,000 +$ 50,00031 May 2026 +$20,000 +$ 50,00031 May 2027 +$20,000 +$ 50,00031 May 2028 +$20,000 +$ 50,000

Which Capital Investment should Crowdspark Choose?

Page | 18

Jacquelin Watts | Jacquelin Watts

When making capital investment decisions firms use a combination of

methods to determine the best project to pursue. You can use the payback period to

narrow down your options, and then apply the NPV method. Alternatively, you can

use the NPV method to select the most financially viable project and then consider

payback periods to see what project produces a quicker return on capital. The IRR

should be used in conjunction with the NPV and the payback period to help choose

the most profitable project over time.

Payback PeriodThe payback period method shows how many years it takes to recover the

initial capital investment amount. If a project can be paid back within an allocated

time, for example 5 or 10 years, then the project is worth considering. The main

disadvantage of the payback period is that it does not consider the time value of

money, for example two projects could have the same payback period but may

generate cash earlier on, or later in the project. It also does not consider inflation and

the cost of capital, as it considers a dollar today the same as a dollar in the future.

Net Present Value (NPV)The net present value method shows the present value of a capital investment

based on expected cashflow in future years. The value of future cashflows is

discounted at a rate, for example 10%, to reflect what they are worth in the present

day. NPV considers the time value of money (opportunity cost), inflation and the cost

of capital, unlike the payback period method. If the NPV is a positive number, then

the project is worth considering. The NPV is helpful for deciding whether a project is

financially viable by showing the total amount of gain or loss a project will produce. It

allows you to consider the opportunity cost, and whether another opportunity, for

example, investing money in the bank would generate a similar return. A negative

NPV suggests the project will lose money. The main disadvantage to the NPV is that

it is based on assumptions of cashflow and discount rate.

Internal Rate of Return (IRR)

Page | 19

Jacquelin Watts | Jacquelin Watts

The internal rate of return method provides a rate of return for expected

cashflows from a capital investment, and is useful for determining the most profitable

projects. The IRR only considers future cashflows and ignores potential costs,

associated with the project, that may affect future profit. It also assumes that future

cashflows can be reinvested at the same amount as the original IRR. It also does not

consider the size of the capital investment projects. A project that requires

significantly less capital may have a much higher IRR, than a costlier capital

investment. However, the more expensive capital investment with the lower IRR may

generate higher cashflows and more profit.

Recommendation

iSpark Stock Photography WebsiteThe NPV for the website project after 10 years is $60,992, from an initial

investment of $40,000. The payback period is 6 years and the IRR is 33%.

.

Worldwide Marketing CampaignThe NPV for the marketing campaign after 10 years is $155,494, from an initial

investment of $800,000. The payback period exceeds 10 years and the IRR is

17.2%.

The marketing campaign has a healthy IRR of 17.2%, that exceeds the cost of

capital (10%) and the NPV indicates that it will make a profit of $155,494. However,

it’s payback period exceeds 10 years, compared to the payback period of the

website project, which is 6 years. The website project also has an excellent IRR of

33%, that exceeds the cost of capital (10%) by more than 3 times. Additionally, the

website has an NPV of $60,992.

I would recommend to Crowdspark that they pursue the iSpark website project,

as this is the better project overall, based on the NPV, IRR and payback period

methods combined.

Page | 20

Jacquelin Watts | Jacquelin Watts

Feedback Received

The feedback I received was very helpful, and made me think more deeply

about what the numbers were telling me about my firm. I suspected there would

be some errors in my calculations that involved NOA, as I had NOL in 2017, so it

was good to hear from Rahul about my error, as it impacted several other ratios

including my economic profit (loss). Similarly, as I had

PEER FEEDBACK SHEET: ASS#2 Step 7-10

Feedback From: Rahul Singh

Feedback To: Jacqui Watts . J

My Comments

Step 7

Identify three products or services of your firm Estimate selling price, variable cost & CM Commentary – contribution margins Constraints – identify & commentary

1. You may want to comment on why some products and services have low contribution margins (severe competition, “me -too”) and others have very high margins (unique, sophisticated services).

2. Also, touch on constraints the firm operates within – competitive pressures from unorganized sector of free-

Page | 21

Jacquelin Watts | Jacquelin Watts

lancers, niche market, capital and management (folks who can run it profitably).

Step 8

Calculation of ratiosRatios – commentary (blog)Calculate economic profitCommentary – drivers of economic profit (blog)

1. All ratios correctly calculated, except RNOA for 2017 is “not relevant”, as NOA is negative. Showing as a high RNOA reflects a fantastic return which is not the case.

2. The ratios are well explained. You might wish to relook at the 2017 commentary for Economic Profit considering the RNOA was “not relevant” (-ve NOA and -ve OI should not be reported as high RNOA).

Step 9

Develop capital investment decision for your firm Calculation of payback period, NPV & IRR Recommendation & discussion

Step 10

Individual feedback with other students

Overall ASS#3

Feedback Given

Page | 22

1. There are errors in your payback period for both options

2. You may like to comment on strengths and weakness of the models and why you would prefer iSpark despite its lower “created value” (lower NPV).

Jacquelin Watts | Jacquelin Watts

Giving feedback was informative and consolidated the concepts behind the

ratios. I found when I looked at other firms who were making a loss I could better

understand my firm. My firm has a large amount of total assets (operating and

financial) compared to some other firms which puts it in a better position, as it can

use these assets while it tries to improve its sales.

Page | 23