january 13, 2012. real property – land and improvements personal property – everything not...

TRANSCRIPT

January 13, 2012

Real property – land and improvements

Personal property – everything not included in real property

Class One – Industrial & Commercial

Class Two – Agricultural

Class Three – Residential

Class Four – Residential Rental

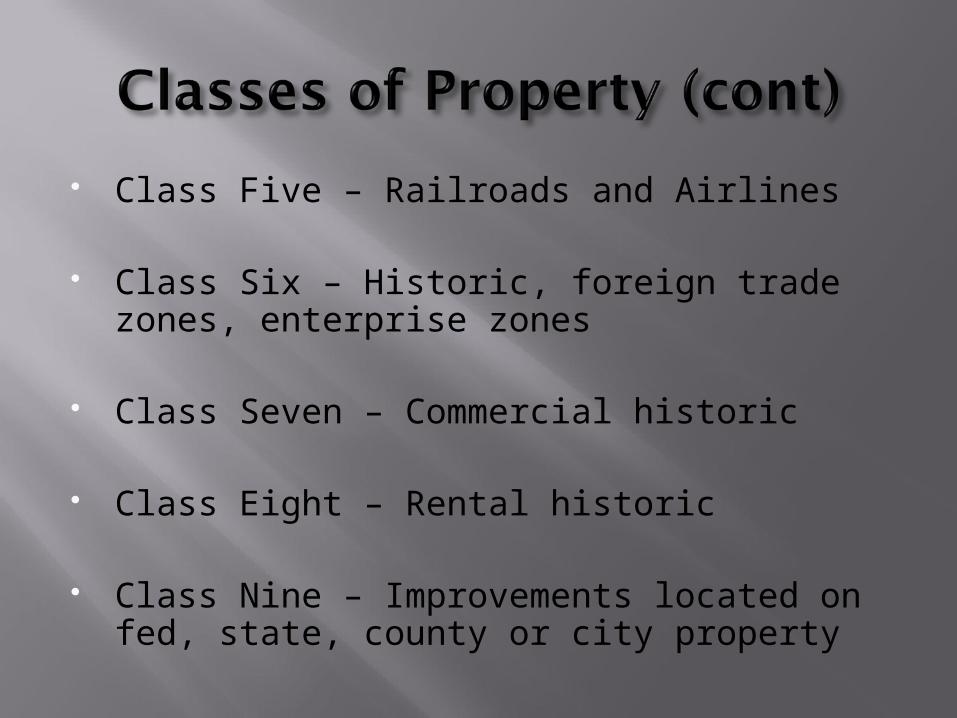

Class Five – Railroads and Airlines

Class Six – Historic, foreign trade zones, enterprise zones

Class Seven – Commercial historic

Class Eight – Rental historic

Class Nine – Improvements located on fed, state, county or city property

Class 1 – 34%

Class 2 – 7%

Class 3 - 50%

Class 4 - 7%

Class 1 – 36%

Class 2 - 6%

Class 3 – 47%

Class 4 – 9%

Class 1 – 20% Class 2 – 16% Class 3 – 10% Class 4 – 10% Class 5 – 15% Class 6 – 5% Class 7 – 20% Class 8 – 10% Class 9 – 1%

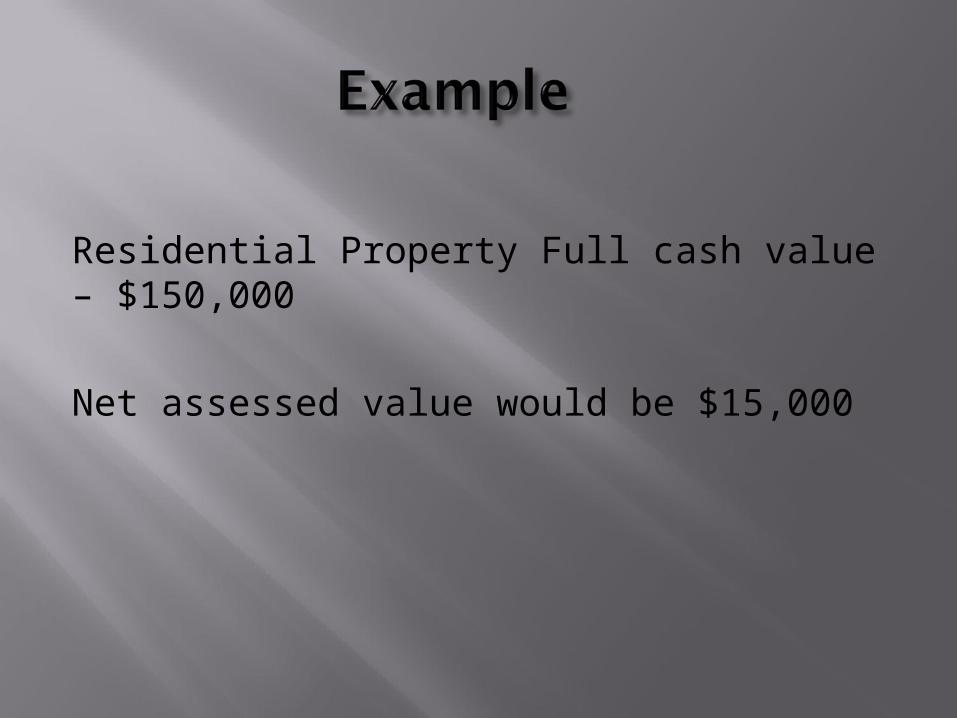

Residential Property Full cash value – $150,000

Net assessed value would be $15,000

Class one –2005 – 25%

2011 – 20%

Class five –2005- 21%

2011 – 15%

Primary (limited) values

Secondary (full cash) values

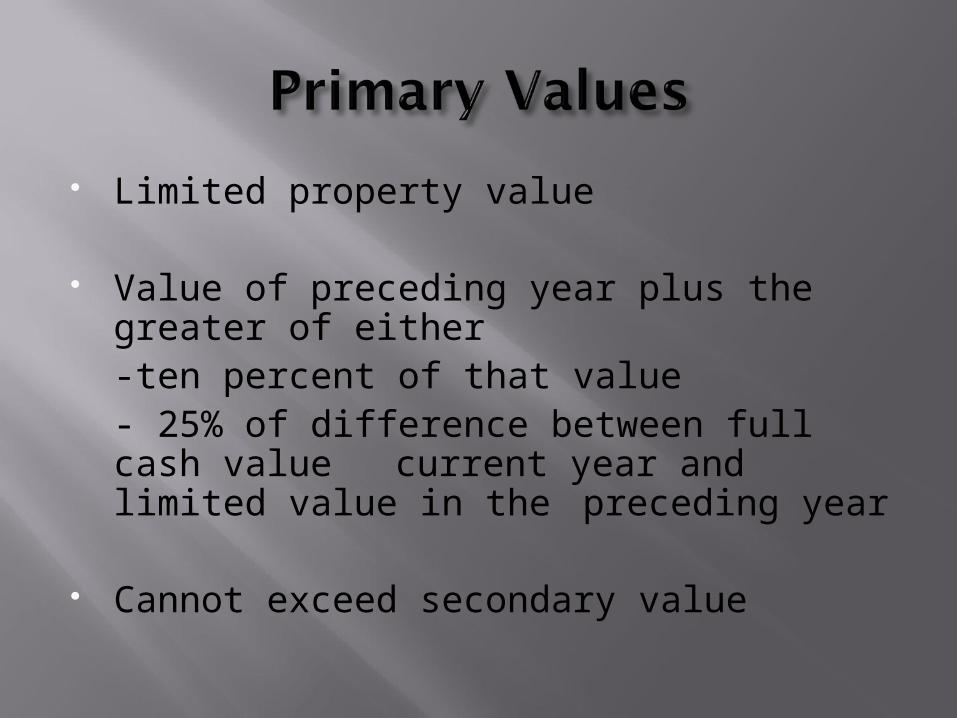

Limited property value

Value of preceding year plus the greater of either-ten percent of that value- 25% of difference between full cash value current year and limited value in the preceding year

Cannot exceed secondary value

Market value

No limit to the increase from prior year

Centrally assessed

Locally assessed

Levy – the amount of money raised against property in a district

Primary – funds operations

Secondary – funds debt service and special districts

Counties, cities and community college districts are restricted by a levy limit

School districts are not limited by the constitution, but are limited by the legislature each year

Levy limit calculated off a base year of 1979 and reset in 2006

Levy limit increases each year by 2% plus new construction

Maximum allow levy 2010 4,701,477Multiplied by 1.02 4,795,507Net assessed value 2010 12,801,750Net assessed value 2011 13,070,873

Max allowable tax rate 4,795,507/12,801,570 .3746Max levy limit for 2011 13070873 x .3746 4,896,349

Actual primary levy 2,943,561Under levy limit 1,952,788

Tax rate .2252

Class 3 property – combined primary tax from all jurisdictions cannot exceed 1% of primary value

In cases where it exceeds that amount, the school district taxes are reduced and the state provides additional aid to that school district

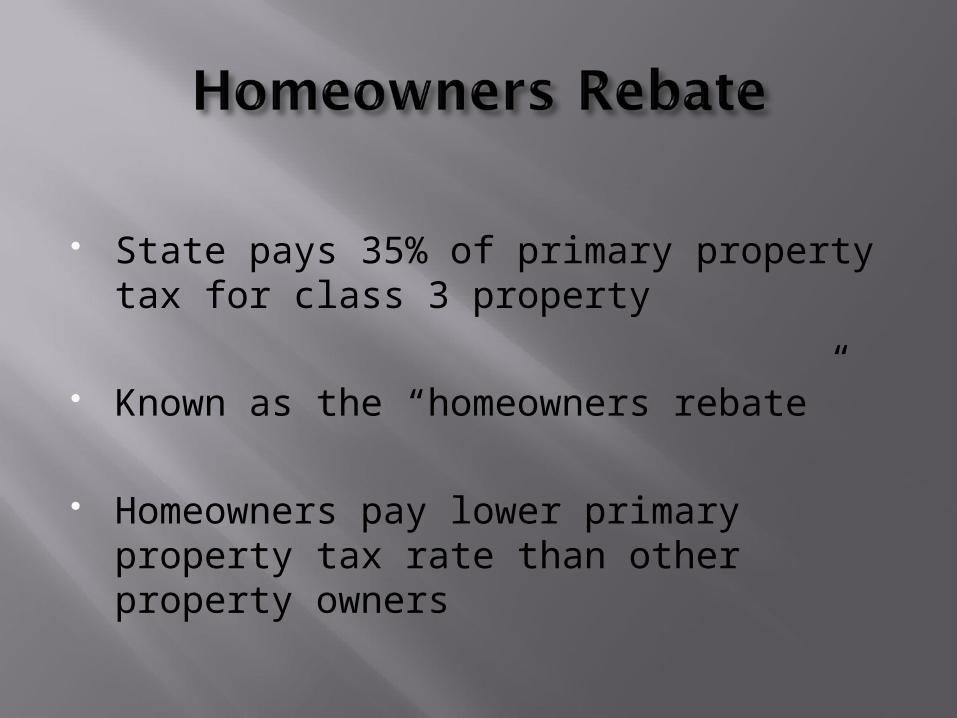

State pays 35% of primary property tax for class 3 property

Known as the “homeowners rebate”

Homeowners pay lower primary property tax rate than other property owners

Primary Assessed value - $150,000Net assessed value - $15,000

Secondary Assessed value - $200,000Net assessed value - $20,000

Primary property tax rate – 9.8432Secondary property tax rate – 4.3214

Primary - 15,000 x 9.8432/100 = 1,476.48Less homeowners rebate 516.77Net primary – 959.71

Secondary - 20,000 x 4.3214/100 = 864.28

Total – 1,8233.99

February 10 – Values released Third Monday in August – property tax rates set October 1 – First half taxes due December 31 – Full year due March 1 – Second half taxes due

September 30 – cutoff for new construction

February – valuation notices sent

Owner may appeal their valuation

Must file an appeal within 60 days of assessor notice

You can either meet with an assessor of file written evidence to support your claim

If appeal is denied, can appeal to the State Board of Equalization

Budget to the rate

Budget to the levy

Primary property tax rate .22 Secondary property tax rate 1.37

Total rate – 1.59

Good times - $33.7 million Tough times - $20.8 million

Primary levy – $3.6 million Secondary levy - $30.1 million

Good times rate – 1.59 Tough times rate – 2.57

Maricopa County – 2008 Primary valuation - $44,881,602,698 Secondary valuation - $58,303,635,287

Maricopa County – 2011 Primary valuation - $38,491,699,290 Secondary valuation - $38,760,296,498

Decrease of 14% and 34% respectively

Predicted 14% decline for Fy12-13

In Glendale we are assuming a further 7% decline for FY13-14

Business pay less

Other changes