january 9, 2015 rating matrix solar industries (solexp...

TRANSCRIPT

January 9, 2015

Initiating Coverage

ICICI Securities Ltd | Retail Equity Research

Detonating to explosive growth… Solar Industries India (SIIL) is the market leader in the Indian industrial explosives market with a 27% market share. The company also has the distinction of being the largest exporter of explosives with 50% market share. SIIL’s core strength lies in its ability to grow continuously through smart revenue diversification that it has achieved by being the leader in all categories of explosives & through geographical expansion via exports & overseas manufacturing operations. With a revival in mining operations in India, the next phase of growth for SIIL will come through strengthening of its leadership position, focus on expanding exports & overseas operations and foray into the defence segment. We expect revenues & PAT to grow at a CAGR of 20.5% & 25.2% in FY14-17E along with 261 bps EBITDA margin expansion & return ratios improving to 20.2%, 20.3% (RoE, RoCE), respectively. We initiate coverage on SIIL valuing it at 26x P/E on FY17E EPS of | 128.6 with a target price of | 3342 & BUY rating. Well poised to capitalise on opportunity from mining sector In FY09-14, SIIL achieved a volume CAGR of 2.2x volume CAGR of the overall industry (bulk + cartridge), which was at 5.8%. In the same period, production in coal mining, the largest consumer of explosives, grew at a muted 2.9% CAGR. However, with an expected revival in mining activity coupled with the government’s thrust on increased infrastructure spending, we believe SIIL is well placed to witness a volume CAGR of 16.9%, 12.5% in bulk, cartridge segment in FY14-17E, respectively. Higher capacity utilisation and product diversification will ensure revenues grow at a CAGR of 20.5% to | 1657.7 crore and | 1971 crore in FY16E and FY17E, respectively. Overseas operations & defence business to provide incremental growth SIIL’s high margin overseas operation has a notable contribution in the consolidated revenues, with its share increasing from 12.8% in FY11 to 18.8% in FY14. We expect the share of the overseas operation to increase to 21.6% in FY17E, with its revenues expected to increase at a CAGR of 25.5% to | 459.8 crore in FY17E. Significant revenues from the defence business from FY16E onwards (6% of consolidated revenues in FY17E) are expected to provide an uptick in revenue growth. Growth story far from over We believe SIIL possesses a wide moat in the form of de-risked business model, industry leadership, significant entry barriers and optimal product mix to benefit the most from a revival in mining & infrastructure activity. We initiate coverage on Solar Industries with a target price of | 3342, valuing the company at 26x P/E (implying PEG of 1x over FY14-17E) on the FY17E EPS of | 128.6. We have a BUY recommendation on the stock. Exhibit 1: Financial Performance (Consolidated) (Year-end March) FY13 FY14 FY15E FY16E FY17ENet Sales (| crore) 1,119.7 1,125.7 1,337.6 1,657.7 1,971.0 EBITDA (| crore) 190.0 203.0 265.4 336.0 406.6 Net Profit (| crore) 116.3 118.4 154.7 190.8 232.7 EPS (|) 64.3 65.4 85.5 105.4 128.6 P/E (x) 44.7 43.9 33.6 27.3 22.4 Price / Book (x) 9.1 7.9 6.6 5.5 4.5 EV/EBITDA (x) 28.5 27.1 20.4 16.0 13.1 RoCE (%) 18.1 15.9 18.5 19.8 20.3 RoE (%) 20.3 17.9 19.6 20.1 20.2

Source: Company, ICICIdirect.com Research

Solar Industries (SOLEXP)| 2875

Rating Matrix Rating : Buy

Target : | 3342

Target Period : 18-24 months

Potential Upside : 16%

YoY growth (%)

(YoY Growth) FY14 FY15E FY16E FY17ENet Sales 0.5 18.8 23.9 18.9EBITDA 6.8 30.8 26.6 21.0Net Profit 1.8 30.6 23.3 22.0EPS (Rs) 1.8 30.6 23.3 22.0

Valuation summary (Consolidated)

FY14 FY15E FY16E FY17EP/E 43.9 33.6 27.3 22.4Target P/E 51.1 39.1 31.7 26.0EV / EBITDA 27.1 20.4 16.0 13.1P/BV 7.9 6.6 5.5 4.5RoNW 17.9 19.6 20.1 20.2RoCE 15.9 18.5 19.8 20.3

Stock Data

Stock DataMarket Capitalization | 5203.2 CroreTotal Debt (FY14) | 442.8 CroreCash and Investments (FY14) | 147.7 CroreEV | 5498.2 Crore52 week H/L 3.5Equity capital | 18.1 CroreFace value | 10MF Holding (%) 14.9FII Holding (%) 0.8

Comparative return matrix (%)

Return % 1M 3M 6M 12MSolar Industries 4.1 13.9 32.6 205.2Premier Explosives 12.9 38.0 91.5 230.0Keltech Energies (1.5) 48.4 87.7 211.7Gulf Oil Corp. (7.7) 0.5 1.9 80.8

Price movement

05001,0001,5002,0002,5003,0003,500

Jan-

15

Aug

-14

Mar

-14

Nov

-13

Jul-1

3

Feb-

13

Oct-1

2

Jun-

12

Feb-

12

0

2,000

4,000

6,000

8,000

10,000

Price (R.H.S) Nifty (L.H.S)

Research Analyst

Chirag J Shah [email protected]

Nishit Zota [email protected]

ICICI Securities Ltd | Retail Equity Research Page 2

Company background Solar Industries India (SIIL), founded by Satyanarayan Nuwal, is the largest manufacturer of industrial explosives & initiating systems in India with 27% market share in the domestic market and 50% market share in exports market. SIIL has a licensed capacity of 2,16,107 metric tonne (MT) of bulk explosives and 74,665 MT of cartridge explosives as of H2FY15. Playing on the economies of scope, the company has established itself as a major player across the product value chain with a product basket that includes bulk explosives, cartridge explosives, detonators, detonating fuse, cast boosters, Pentaerythritol tetranitrate (PETN - raw material for detonators) and High Melting Explosive (HMX - warhead in missiles). Mining industry is a major consumer of explosives accounting for 90% of total explosives demand (coal industry consumes 70% of total demand). Coal India (CIL) is the largest consumer of SIIL. The company enjoys a location advantage, as all its 16 facilities of bulk explosives are located in a 50-60 km radius from major mining regions. SIIL expanded its base to other geographies by setting up manufacturing facilities in partnership with local trading companies in countries like Zambia, Nigeria and Turkey. Consolidated revenues in FY14 were at | 1,126 crore, with domestic, overseas & export segments contributing ~70%, ~20% & ~10%, respectively. A huge demand-supply gap along with a set of progressive policies has driven SIIL to enter the defence sector. The company has already obtained an industrial license for HMX, propellants & new generation explosives. SIIL has commissioned an HMX plant with capacity of 50 MT. The HMX business will start generating revenues from FY15 onwards while its capacity will be gradually raised from 50 MT to 150 MT. The company is also in the process of setting up an initial propellant capacity of 2500 units where it has a license to manufacture 10,000 units.

Exhibit 2: Solar Industries India milestones

s

Starts production of explosives with a license capacity of 6000 MT

Starts plants in Waidhan for production of bulk explosives

Commences business as a trader in explosives

Commences production of detonators Starts exporting & slowly gains acceptance in international market

Initial public offer; gets listed

1984 1998

Establishes another bulk explosive unit in Chandrapur with 7750 MT capacity

Imports first cartridge manufacturing machine from US

Expands domestic operations to 19 locations

Starts exporting to 25 countries

2007-20141996 2000 2002-2005 2006

Introduces cast boosters & PETN in product portfolio Manufacturing units in

Zambia, Nigeria & Turkey

Expansion in Zambia

Foray into defence business by setting up up manufacturing facilities of HMX & propellant

2001

Source: Company, ICICIdirect.com Research,

Shareholding pattern (%) – Q2FY15

Shareholder's Category Holding (%)

Promoters 72.9

Institutional Investors 18.9

General Public 8.2

FII & DII holding trend (%)

1.3 1.2 1.1 1.2 1.2 1.2 0.8 0.8

18.6 18.9 19.0 18.7 18.3 18.1 18.1 17.9

0

5

10

15

20

Q3FY

13

Q4FY

13

Q1FY

14

Q2FY

14

Q3FY

14

Q4FY

14

Q1FY

15

Q2FY

15

%

FII DII

ICICI Securities Ltd | Retail Equity Research Page 3

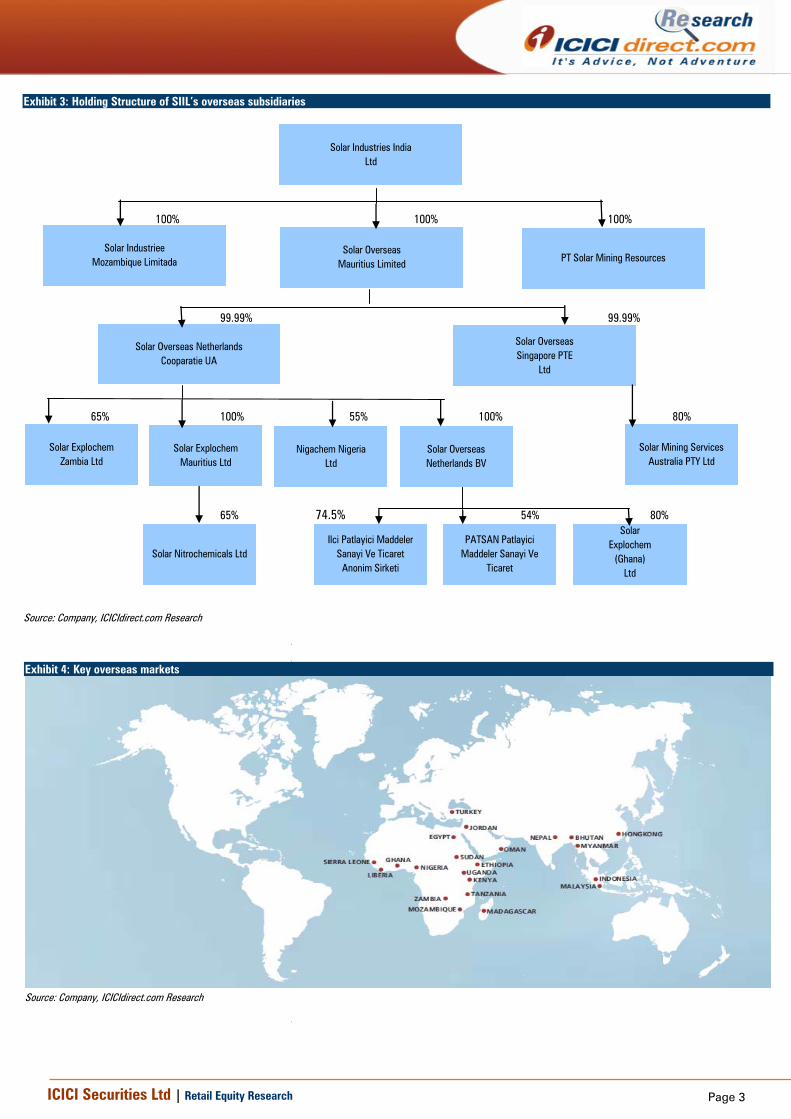

Exhibit 3: Holding Structure of SIIL’s overseas subsidiaries

100% 100% 100%

99.99% 99.99%

65% 100% 55% 100% 80%

65% 74.5% 54% 80%

Solar Industries IndiaLtd

Solar IndustrieeMozambique Limitada

Solar OverseasMauritius Limited PT Solar Mining Resources

Solar Overseas NetherlandsCooparatie UA

Solar OverseasSingapore PTE

Ltd

Solar ExplochemZambia Ltd

Solar ExplochemMauritius Ltd

Nigachem NigeriaLtd

Solar OverseasNetherlands BV

Solar Mining ServicesAustralia PTY Ltd

Solar Nitrochemicals LtdIlci Patlayici Maddeler

Sanayi Ve TicaretAnonim Sirketi

PATSAN PatlayiciMaddeler Sanayi Ve

Ticaret

Solar Explochem

(Ghana)Ltd

Source: Company, ICICIdirect.com Research

Exhibit 4: Key overseas markets

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 4

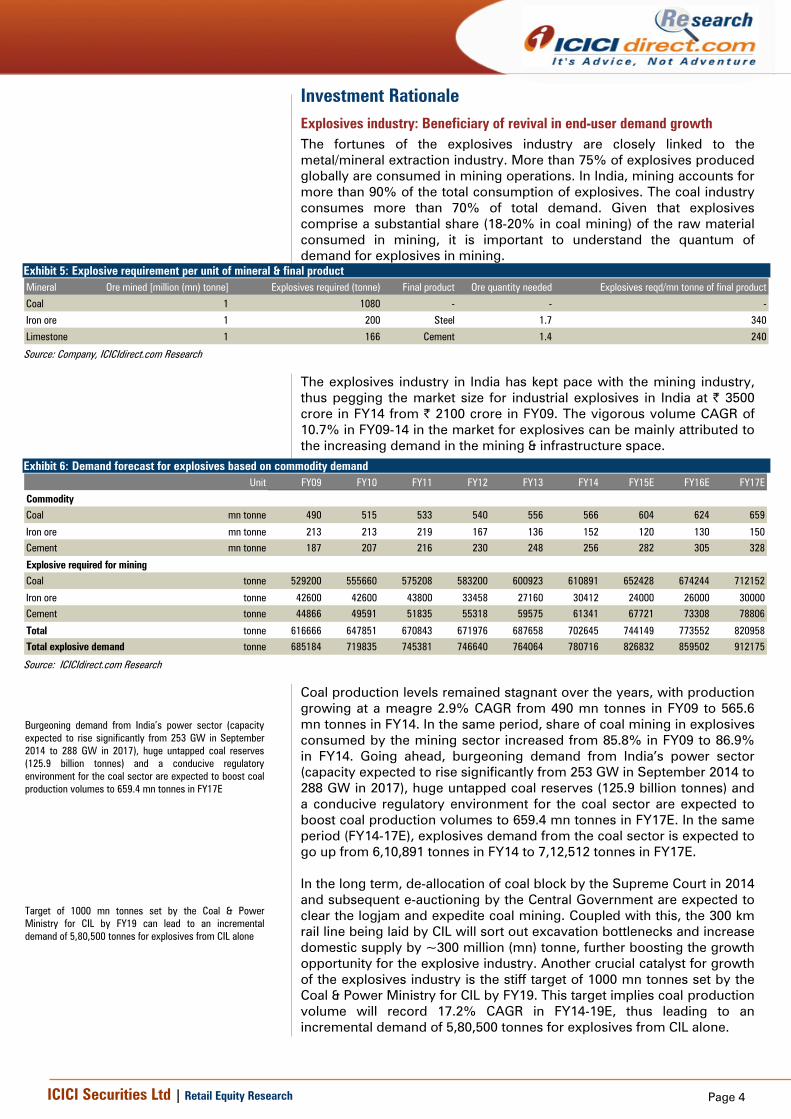

Investment Rationale Explosives industry: Beneficiary of revival in end-user demand growth The fortunes of the explosives industry are closely linked to the metal/mineral extraction industry. More than 75% of explosives produced globally are consumed in mining operations. In India, mining accounts for more than 90% of the total consumption of explosives. The coal industry consumes more than 70% of total demand. Given that explosives comprise a substantial share (18-20% in coal mining) of the raw material consumed in mining, it is important to understand the quantum of demand for explosives in mining.

Exhibit 5: Explosive requirement per unit of mineral & final product Mineral Ore mined [million (mn) tonne] Explosives required (tonne) Final product Ore quantity needed Explosives reqd/mn tonne of final product

Coal 1 1080 - - -

Iron ore 1 200 Steel 1.7 340

Limestone 1 166 Cement 1.4 240

Source: Company, ICICIdirect.com Research

The explosives industry in India has kept pace with the mining industry, thus pegging the market size for industrial explosives in India at | 3500 crore in FY14 from | 2100 crore in FY09. The vigorous volume CAGR of 10.7% in FY09-14 in the market for explosives can be mainly attributed to the increasing demand in the mining & infrastructure space.

Exhibit 6: Demand forecast for explosives based on commodity demand Unit FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

CommodityCoal mn tonne 490 515 533 540 556 566 604 624 659

Iron ore mn tonne 213 213 219 167 136 152 120 130 150Cement mn tonne 187 207 216 230 248 256 282 305 328

Explosive required for miningCoal tonne 529200 555660 575208 583200 600923 610891 652428 674244 712152

Iron ore tonne 42600 42600 43800 33458 27160 30412 24000 26000 30000Cement tonne 44866 49591 51835 55318 59575 61341 67721 73308 78806

Total tonne 616666 647851 670843 671976 687658 702645 744149 773552 820958Total explosive demand tonne 685184 719835 745381 746640 764064 780716 826832 859502 912175

Source: ICICIdirect.com Research

Coal production levels remained stagnant over the years, with production growing at a meagre 2.9% CAGR from 490 mn tonnes in FY09 to 565.6 mn tonnes in FY14. In the same period, share of coal mining in explosives consumed by the mining sector increased from 85.8% in FY09 to 86.9% in FY14. Going ahead, burgeoning demand from India’s power sector (capacity expected to rise significantly from 253 GW in September 2014 to 288 GW in 2017), huge untapped coal reserves (125.9 billion tonnes) and a conducive regulatory environment for the coal sector are expected to boost coal production volumes to 659.4 mn tonnes in FY17E. In the same period (FY14-17E), explosives demand from the coal sector is expected to go up from 6,10,891 tonnes in FY14 to 7,12,512 tonnes in FY17E. In the long term, de-allocation of coal block by the Supreme Court in 2014 and subsequent e-auctioning by the Central Government are expected to clear the logjam and expedite coal mining. Coupled with this, the 300 km rail line being laid by CIL will sort out excavation bottlenecks and increase domestic supply by ~300 million (mn) tonne, further boosting the growth opportunity for the explosive industry. Another crucial catalyst for growth of the explosives industry is the stiff target of 1000 mn tonnes set by the Coal & Power Ministry for CIL by FY19. This target implies coal production volume will record 17.2% CAGR in FY14-19E, thus leading to an incremental demand of 5,80,500 tonnes for explosives from CIL alone.

Burgeoning demand from India’s power sector (capacity expected to rise significantly from 253 GW in September 2014 to 288 GW in 2017), huge untapped coal reserves (125.9 billion tonnes) and a conducive regulatory environment for the coal sector are expected to boost coal production volumes to 659.4 mn tonnes in FY17E

Target of 1000 mn tonnes set by the Coal & Power Ministry for CIL by FY19 can lead to an incremental demand of 5,80,500 tonnes for explosives from CIL alone

ICICI Securities Ltd | Retail Equity Research Page 5

The second most important segment for the explosives market is the construction sector. The sector that attracted investment of | 12.5 trillion in FY09-14, is expected to witness 1.5x growth in investment (| 19 trillion) in the next five years. This will generate strong steel demand in India. It will also generate demand for iron ore (an important raw material for making steel), whose production has contracted over the last few years due to regulatory issues. From the highs of 213 mn tonnes in FY09, production has fallen to 152.1 mn tonnes in FY14. In the same period of FY09-14E, the share of iron ore mining in the explosives demand pie has declined from 6.9% in FY09 to 4.3% in FY14. The iron ore production is expected to bottom out in FY15E to 120 mn tonnes. However, with a number of mines in Karnataka and Goa receiving clearances, iron ore production is expected to revive FY15E onwards, growing at a CAGR of 11.8% in FY15-17E to 150 mn tonnes in FY17E. Non-CIL + institutional (mostly steel sector) contribute ~18% of SIIL’s sales and explosives demand. Explosives demand from iron ore mining is expected to be at 30,000 tonnes in FY17E.

Exhibit 7: Coal production to grow at 5.3% CAGR in FY14-17E

490 515 533 540 556 566604 624

659

0

100

200

300

400

500

600

700

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E(M

n to

nne)

CAGR of 5.3%

CAGR of 2.9%

Source: Company, ICICIdirect.com Research

With a number of mines in Karnataka and Goa receiving clearances, iron ore production is expected to revive from FY15E onwards, growing at a CAGR of 11.8% in FY15-17E to 150 mn tonnes in FY17E. Explosives demand from iron ore mining is expected to be 30,000 tonnes in FY17E

Exhibit 8: Iron ore production to grow at 11.8% CAGR in FY15-17E

213 213 219

167

136152

120130

150

0

50

100

150

200

250

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(Mn

tonn

e)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 6

Another sector that would be the beneficiary of a pick-up in investment activity in construction space is the cement sector. The capacity utilisation of the cement industry has bottomed out at ~69% in FY14. Low capacity addition and demand recovery driven by increased investments in infrastructure sector are expected to push utilisation levels to 78% in FY17E. Total cement production in India is expected to grow from 255.6 mn tonnes in FY14 to 328.4 mn tonnes in FY17E, implying a CAGR of 8.7%. The explosives find their application in mining of limestone, which is a key raw material for manufacturing of cement. The growth in cement production is expected to drive explosives demand from 61,341 tonnes in FY14 to 78,806 tonnes in FY17E. Exhibit 9: Cement production to grow at 7% CAGR in FY14-17E

187207 216

230248 256

282305

328

0

50

100

150

200

250

300

350

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(Mn

tonn

e)

Source: Company, ICICIdirect.com Research

Total cement production in India is expected to grow from 255.6 mn tonnes in FY14 to 328.4 mn tonnes in FY17E, implying a CAGR of 8.7%.The growth in cement production is expected to drive explosives demand from 61,341 tonnes in FY14 to 78,806 tonnes in FY17E

ICICI Securities Ltd | Retail Equity Research Page 7

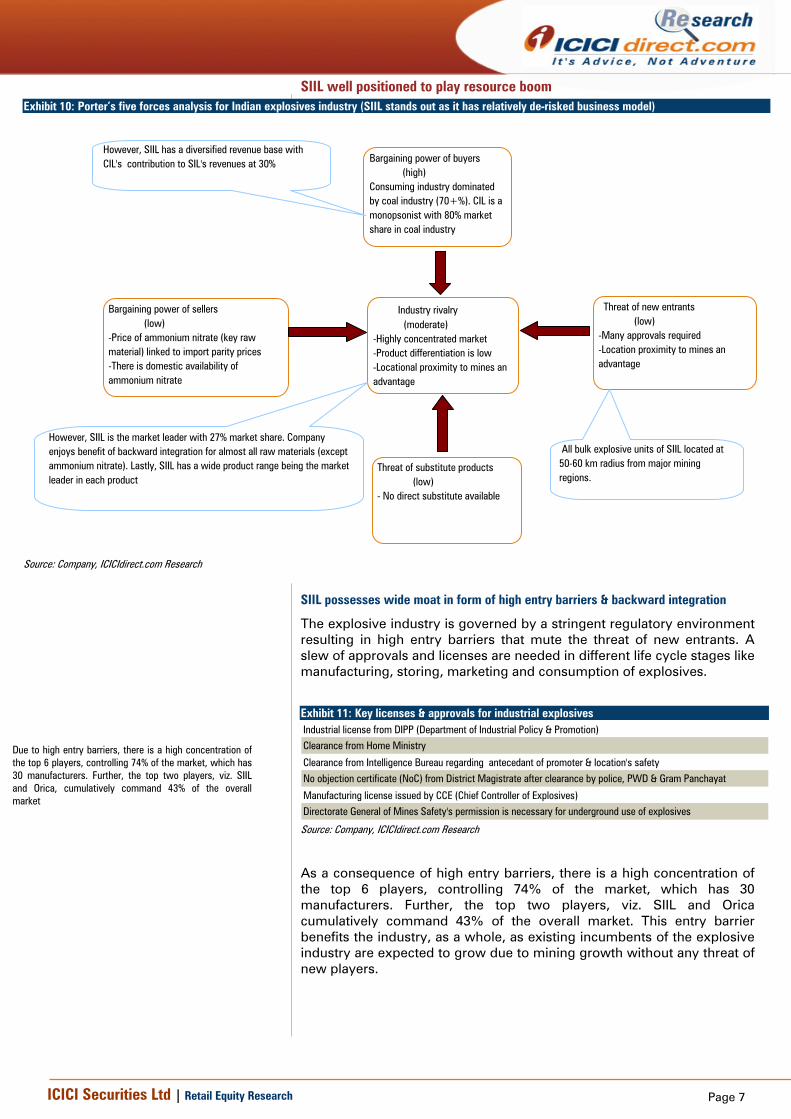

SIIL well positioned to play resource boom Exhibit 10: Porter’s five forces analysis for Indian explosives industry (SIIL stands out as it has relatively de-risked business model)

Industry rivalry (moderate)-Highly concentrated market-Product differentiation is low-Locational proximity to mines an advantage

Bargaining power of buyers (high)Consuming industry dominated by coal industry (70+%). CIL is a monopsonist with 80% market share in coal industry

Threat of new entrants (low)-Many approvals required-Location proximity to mines an advantage

Threat of substitute products (low)- No direct substitute available

Bargaining power of sellers (low)-Price of ammonium nitrate (key raw material) linked to import parity prices-There is domestic availability of ammonium nitrate

However, SIIL has a diversified revenue base with CIL's contribution to SIL's revenues at 30%

However, SIIL is the market leader with 27% market share. Company enjoys benefit of backward integration for almost all raw materials (except ammonium nitrate). Lastly, SIIL has a wide product range being the market leader in each product

All bulk explosive units of SIIL located at 50-60 km radius from major mining regions.

Source: Company, ICICIdirect.com Research

SIIL possesses wide moat in form of high entry barriers & backward integration

The explosive industry is governed by a stringent regulatory environment resulting in high entry barriers that mute the threat of new entrants. A slew of approvals and licenses are needed in different life cycle stages like manufacturing, storing, marketing and consumption of explosives.

Exhibit 11: Key licenses & approvals for industrial explosives Industrial license from DIPP (Department of Industrial Policy & Promotion)Clearance from Home Ministry

Clearance from Intelligence Bureau regarding antecedant of promoter & location's safety

No objection certificate (NoC) from District Magistrate after clearance by police, PWD & Gram Panchayat

Manufacturing license issued by CCE (Chief Controller of Explosives)Directorate General of Mines Safety's permission is necessary for underground use of explosives

Source: Company, ICICIdirect.com Research

As a consequence of high entry barriers, there is a high concentration of the top 6 players, controlling 74% of the market, which has 30 manufacturers. Further, the top two players, viz. SIIL and Orica cumulatively command 43% of the overall market. This entry barrier benefits the industry, as a whole, as existing incumbents of the explosive industry are expected to grow due to mining growth without any threat of new players.

Due to high entry barriers, there is a high concentration of the top 6 players, controlling 74% of the market, which has 30 manufacturers. Further, the top two players, viz. SIIL and Orica, cumulatively command 43% of the overall market

ICICI Securities Ltd | Retail Equity Research Page 8

Exhibit 12: SIIL - Market leader Company Market Share (%)

Solar Industries 27Orica 16

IBP (IOCL) 11Gulf Oil 10

Premier Explosives 5Keltech Energies 5

Total 74

Source: Company, ICICIdirect.com Research

Coupled with this structural entry barrier, SIIL possesses a strategic entry barrier in the form of location proximity to the mines. For bulk explosives, distance is an important parameter, as it has to be the least between a seller and a buyer. All bulk explosive units of the company are located at a 50-60 km radius from the major mining regions.

Exhibit 13: Location of SIIL’s manufacturing plants in India State No of Plants Clients Served

Maharashtra (Chakdoh,Nimji,Sawanga, Warur) 4 Western Coalfield Ltd., SCCLMP (Waidhan 1, Waidhan 2) 2 Northern Coalfield Ltd., Reliance Power (Sasan)

Chattisgarh (Korba,Manendragarh) 2 South Eastern Coalfield Ltd, Jindal Power, Sharda Energy,Lafarge, Parsak (Adani group)Jharkand (Dhanbad, Ramgarh Cant) 2 Tisco,Central Coalfield Ltd., Bharat Coking Coalfield

Odisha (Jharsuguda,Talchar) 2 Mahanadi Coalfield Ltd., TiscoAP (Ramagundam, Kothagudem) 2 SCCL

Rajasthan (Bhilwara) 1 Hindustan Zinc, Jindal SawWest Bengal (Asansol) 1 Eastern Coalfield Ltd.

Source: Company, ICICIdirect.com Research

The main raw material for industrial explosives is ammonium nitrate (AN), which accounts for ~70% of the raw material consumed. SIIL procures this key raw material domestically from Rashtriya Chemicals & Fertilisers (RCF), Gujarat Narmada Fertiliser Corporation (GNFC) and Deepak Fertilizers based on monthly contracts and quantity wise pricing. After the implementation of the Ammonium Nitrate Rules 2012 under Explosives Act, which requires the approval of the Chief Controller of Explosives for import of AN, 90% of the required AN is sourced domestically and 10% through imports. SIIL enjoys the benefit of backward integration for the rest of the raw material required like PETN, sodium nitrate, zinc nitrate, calcium nitrate, sodium percolate, etc. This benefit enables the company to enjoy healthier margins compared to the rest of the industry.

SIIL enjoys the benefit of backward integration for all raw materials except ammonium nitrate. This benefit enables the company to enjoy healthier margins compared to the rest of the industry

ICICI Securities Ltd | Retail Equity Research Page 9

Strategic expansion + product diversification = Pole position in concentrated industry

SIIL, a late entrant in the Indian explosive industry, today has a licensed capacity of 2,16,107 metric tonne (MT) of bulk explosives and 74,665 MT of cartridge explosives, making the company the leader in the sector (27% market share in domestic market and 50% market share in exports of industrial explosives in value terms). SIIL has achieved this feat by recognising that its future competitiveness depends on quickly expanding its capacity at strategic locations and diversifying to meet the growing resource demand. The company has not only scaled up its capacity since inception but has also developed a well diversified portfolio of products.

Exhibit 15: Well diversified product portfolio

Detonators

Products

Cartridge ExplosivesBulk Explosives Detonating FuseSegments

106988 tonnesVolumes 68955 tonnes 133 million nos 59 million metre

Performance

Volume CAGR: 14.7%Revenue(FY14) :|380.3 croreTopline Contribution: 30.6%Rev CAGR (FY09-14) : 21.6%

Volume CAGR: 9.2%Revenue(FY14):|400.8 croreTopline Contribution: 32.3%Rev CAGR (FY09-14) : 15.6%

Volume CAGR: 12.8%Revenue(FY14):|174.1 croreTopline Contribution: 14%Rev CAGR (FY09-14) : 15.9%

Volume CAGR: 18.4%Revenue(FY14):|44.6 croreTopline Contribution: 3.6%Rev CAGR (FY09-14) : 23%

End-use Large open caste minesUnderground & small open cast

mines, infra projects To initiate explosives To initiate explosives

Source: Company, ICICIdirect.com Research

Exhibit 14: EBIT margin profile of explosives segment of industry players (standalone)

12.313.8

12.1 12.4

6.0

-0.6

3.5

15.4 16.2 15.7

7.6

10.09.8

0.5

5.5

10.7

6.89.0

2.21.5

-202468

1012141618

FY10 FY11 FY12 FY13 FY14

(%)

Solar Industries Gulf Oil Corp. Premier Explosives Keltech Energies

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 10

Exhibit 16: Domestic capacity of SIIL Product Licensed CapacityBulk explosives 219,240 MTCartridge explosives 74,655 MTDetonators 190 Mn. UnitsDetonating Fuse 75 Mn. MetersCast Boosters 1,500 MTPETN 1,650 MTHMX 50 MTComposite Propellants 2500 MT

Source: Company, ICICIdirect.com Research

Exhibit 17: Volume CAGR of bulk & cartridge segment

8.7

14.7

1.2

9.27.3

13.6

5.46.6

0

4

8

12

16

20

Industry SIL Industry SIL

Bulk Cartridge

(%)

FY09-14 FY14-17E

Source: Company, ICICIdirect.com Research

Bulk volumes expected to grow at 16.9% CAGR over FY14-17E In the bulk segment, SIIL has witnessed a rapid and strategic build-up in capacity, starting from a modest capacity of 6,000 MT at a single location of Waidhan (Madhya Pradesh) in 2000, to the current capacity of 219,240 MT spread across 16 locations in India. SIIL’s volumes in the bulk segment have grown from 53,912 MT in FY09 to 1,06,988 MT in FY14, implying a CAGR of 14.7%. In the same period (FY09-14), industry volumes in the bulk segment have grown at a CAGR of 8.7% from 3,43,019 MT to 5,21,419 MT. Bulk explosives volumes declined from 1,14,330 MT in FY13 to 1,06,988 MT in FY14, as SIIL lost business in Singareni Collieries due to non-remunerative pricing and the unachievable performance criteria set by Singareni Collieries. However, Singareni Collieries floated a tender with revised norms for FY15 and FY16 in which SIIL has received maximum order quantity. Additionally, SIIL has already commissioned a new bulk explosive facility at Kothagudem (Andhra Pradesh), which will add ~10,000 MT to the utilised capacity. Two new proposed facilities at Barbil (Odisha) and Kota (Rajasthan) in H1FY16 are expected to add another ~15,000 MT to the utilised capacity. This additional capacity will contribute significantly to volume growth. In FY09-14, when India’s coal production was stagnant and grew at a CAGR of just 2.9%, the bulk segment of the industry grew at a healthy CAGR of 8.7%. Going ahead, domestic coal production is expected to grow at a CAGR of 5.2% from 565.6 MT in FY14 to 659.4 MT in FY17E. Given the context of better growth rates in coal production, we have pencilled in a conservative CAGR of 7.3% for the industry, where bulk explosive volumes are expected to increase to 6,45,000 MT by FY17. Historically, SIIL has achieved superior volume growth compared to the

Historically, SIIL has achieved superior volume growth compared to the industry. SIIL’s volumes in the bulk segment grew at a CAGR of 14.7% in FY09-14, when industry volumes in the bulk segment grew at 8.7% CAGR

ICICI Securities Ltd | Retail Equity Research Page 11

industry. We expect the same trend to continue. Hence, we expect SIIL’s bulk volumes to grow at a CAGR of 16.9% to 170881 MT in FY17E. Exhibit 18: Industry volumes (bulk segment) expected to grow at 7.3% CAGR over FY14-17E

343019389825

359943

483838 495946 521419554000

598000645000

0

100000

200000

300000

400000

500000

600000

700000

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(MT)

Source: Company, ICICIdirect.com Research

Although SIIL was a late entrant in the bulk segment, location proximity and strategic expansion have been key to SIIL’s market prominence, whose market share in the bulk explosive segment has increased from 16% in FY09 to 21% in FY14. Going ahead, we expect the market share in the bulk segment at 26.5% by FY17E, on the back of capacity expansion and higher utilisation. Exhibit 19: SIIL volumes (bulk segment) expected to grow at 16.9% CAGR over FY14-17E

53912 5785779880

170881155347

129455

106988114330

94962

26.526.023.420.5

23.119.622.2

15.7 14.8

0

25000

50000

75000

100000

125000

150000

175000

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(MT)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

(%)

Bulk (Solar) Market Share

Source: Company, ICICIdirect.com Research

Cartridge volumes expected to grow at 12.5% CAGR over FY14-17E The cartridge segment is not too far behind in its contribution towards SIIL’s growth story. Volumes in the cartridge segment have grown from 44,312 MT in FY09 to 68,955 MT at a CAGR of 9.2%, whereas in the same period, the industry grew a meagre 1.2% from 2,54,808 MT to 2,69,999 MT, clearly indicating that SIIL ate into other player’s market share. The estimated investment of | 19 trillion in the construction sector in FY14-19E is expected to be a potent demand booster for steel, cement and power production. An increase in the production of coal, iron ore and other minerals will augur well for accelerated cartridge demand. Riding on these demand boosters, we expect industry volumes in the cartridge segment to grow at a CAGR of 5.4% to 3,16,000 MT in FY17E. In the same period (FY14-17E), we expect SIIL’s cartridge volumes to grow at a CAGR of 12.5% to 98,123 MT.

Location proximity and strategic expansion have led SIIL’s market share to increase from 16% in FY09 to 21% in FY14

ICICI Securities Ltd | Retail Equity Research Page 12

Exhibit 20: Industry volumes (cartridge segment) expected to grow at 5.4% CAGR over FY14-17E

254808225615

183533

238193267275 269999

287000301000

316000

0

50000

100000

150000

200000

250000

300000

350000

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(MT)

Source: Company, ICICIdirect.com Research

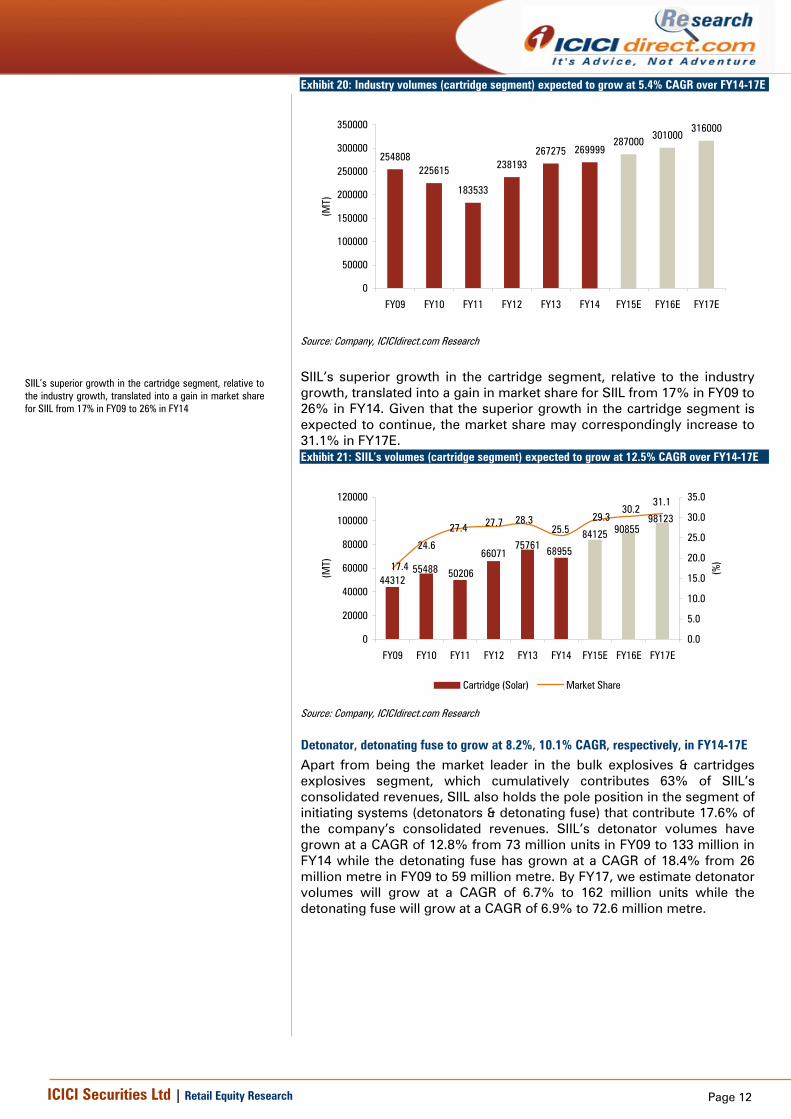

SIIL’s superior growth in the cartridge segment, relative to the industry growth, translated into a gain in market share for SIIL from 17% in FY09 to 26% in FY14. Given that the superior growth in the cartridge segment is expected to continue, the market share may correspondingly increase to 31.1% in FY17E. Exhibit 21: SIIL’s volumes (cartridge segment) expected to grow at 12.5% CAGR over FY14-17E

981239085584125

689557576166071

502065548844312

31.130.2

29.325.5

28.327.727.4

24.6

17.4

0

20000

40000

60000

80000

100000

120000

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(MT)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

(%)

Cartridge (Solar) Market Share

Source: Company, ICICIdirect.com Research

Detonator, detonating fuse to grow at 8.2%, 10.1% CAGR, respectively, in FY14-17E Apart from being the market leader in the bulk explosives & cartridges explosives segment, which cumulatively contributes 63% of SIIL’s consolidated revenues, SIIL also holds the pole position in the segment of initiating systems (detonators & detonating fuse) that contribute 17.6% of the company’s consolidated revenues. SIIL’s detonator volumes have grown at a CAGR of 12.8% from 73 million units in FY09 to 133 million in FY14 while the detonating fuse has grown at a CAGR of 18.4% from 26 million metre in FY09 to 59 million metre. By FY17, we estimate detonator volumes will grow at a CAGR of 6.7% to 162 million units while the detonating fuse will grow at a CAGR of 6.9% to 72.6 million metre.

SIIL’s superior growth in the cartridge segment, relative to the industry growth, translated into a gain in market share for SIIL from 17% in FY09 to 26% in FY14

ICICI Securities Ltd | Retail Equity Research Page 13

Exhibit 22: Industry volumes (detonator) expected to grow at 2% CAGR in FY14-17E

610698 724

971 992 1032 1053 1074 1095

0

200

400

600

800

1000

1200

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(Mn

nos.

)

Source: Company, ICICIdirect.com Research

Exhibit 23: SIIL volumes (detonator) expected to grow at 8.2% CAGR in FY14-17E

123 141 133 128147

169

108

73

1031215 15

1314

13 1214

15

0

30

60

90

120

150

180

FY09

FY10

FY11

FY12

FY13

FY14

FY15

E

FY16

E

FY17

E

(Mn

nos)

0

3

6

9

12

15

18

(%)

Detonators (Solar) Market Share

Source: Company, ICICIdirect.com Research

Exhibit 24: Industry volumes (detonator fuse) expected to grow at 8% CAGR in FY14-17E

334391

285

371

649

428462

499539

0

100

200

300

400

500

600

700

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(Mn

met

re)

Source: Company, ICICIdirect.com Research

Exhibit 25: SIIL volumes (detonator fuse) expected to grow at 10.1% CAGR in FY14-17E

26 30

7969

605949

6759

8 8

2118

8

14 13 14 15

0

15

30

45

60

75

90

FY09

FY10

FY11

FY12

FY13

FY14

FY15

E

FY16

E

FY17

E

(Mn

met

re)

0

5

10

15

20

25

(%)

Detonating Fuse (Solar) Market Share

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 14

Prudent diversification: key to stability of revenues SIIL has successfully diversified its revenue base by catering to newer customers in the domestic market, enhancing exports and venturing into overseas geographies. Diversification has aided the company to grow even in periods of tepid demand. Exhibit 26: Revenue diversification

Diversification

Customers

Overseas

Geography

Exports

Source: Company, ICICIdirect.com Research

Mitigation of concentration risk through balanced customer portfolio Coal India (CIL) accounts for a major portion of consumption of the domestic explosive industry’s output, which gives it significant bargaining power. For pricing, CIL uses a vendor rating system that incorporates evaluation parameters such as manufacturing infrastructure, random tests of products, distribution systems and delivery performance in the previous year, to be qualified for price bid. Given that CIL effectively acts as a price setter for most non-traded explosives and its pricing mechanism plays a significant role in the explosive industry’s health, SIIL has smartly diversified its revenue base in recent years by increasing the share of institutional players, export & overseas. CIL’s contribution to SIIL’s consolidated revenue has declined from 58% in FY07 to 33% in FY14. The company has reduced its concentration on CIL but at the same time retained its leadership position by spreading its markets to other segments. SIIL is still the largest supplier of explosives to CIL, meeting 27.5% of CIL’s requirement in FY14.

Although CIL’s contribution to SIIL’s consolidated revenue has declined from 58% in FY07 to 33% in FY14, SIIL remains the largest supplier of explosives to CIL, meeting 27.5% of CIL’s requirement in FY14

ICICI Securities Ltd | Retail Equity Research Page 15

Exhibit 27: Customer revenue trend - CIL’s share in SIIL’s topline has declined

58

45

3126 27

33

7 6 7 73

36

4740

35 35 37

6 8

22 22

106

2

25303535

2823

1014 101815

0

10

20

30

40

50

60

70

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

(%)

Coal India SCCL Inst. & Trade Export & Overseas A.N. Trading & others

Source: Company, ICICIdirect.com Research

Expanding footprint through exports & overseas operations SIIL started exporting explosives & accessories to various African, South-East Asian and Middle-East countries in FY04. Acceptance in the international market got translated to repeat business from international customers, despite intense competition from other global players. Today, SIIL exports to over 22 countries with a market share in explosive exports of 50%. Cartridges and initiating systems have helped SIIL strengthen its position in the export market. SIIL’s export revenues have grown at 10.7% CAGR from | 72.2 crore in FY09 to | 119.9 crore in FY14. Given that India’s explosive export account for just ~$40 million in a global explosive market size of $10 billion and as India is a cost-efficient manufacturer, there is huge potential in export of explosives & initiating systems. In FY14, exports comprised 10% of SIIL’s consolidated revenues. Exhibit 28: Exports grow at 10.7% CAGR in period FY09-14

7261

7566

90

120

0

20

40

60

80

100

120

140

FY09 FY10 FY11 FY12 FY13 FY14

| cr

ore

Source: Company, ICICIdirect.com Research

India’s explosive export account for just ~$40 million in a global explosive market size of $10 billion and as India is a cost-efficient manufacturer, there is huge potential in export of explosives & initiating systems

ICICI Securities Ltd | Retail Equity Research Page 16

The company set up a strong dealer network and marketing tie-ups with institutional buyers in the countries to which it exported. In line with its broad strategy to expand business overseas, the next step for SIIL after exports was to set up manufacturing facilities in markets with untapped demand. The company ventured into newer geographies by partnering with local companies to acquire licenses. SIIL started its first overseas manufacturing unit in Zambia in FY11, by manufacturing bulk explosives under the 65% subsidiary Solar Explochem Zambia Ltd. Going ahead, SIIL expanded its overseas business by setting up manufacturing capacities in Nigeria through a 55% stake in Nigachem Nigeria in FY11 and in Turkey through a 74.5% stake in the company Ilci Patlayici Maddeler Sanayi Ve Ticaret Anonim Sirketi in FY13. Exhibit 30: SIIL’s overseas operations Country SIL's stake (%) Product Licensed Capcity ExpansionZambia 65 Bulk 10,000 MT 10,000 MT

Cartridge 5,000 MTNigeria 55 Bulk 2,000 MT

Cartridge 5,000 MTTurkey 74.5 Bulk 2500 MT

ANFO 40,000 MTCartridge 5,000 MT

Detonators 6 mn nos

Source: Company, ICICIdirect.com Research

SIIL’s choice of geographic locations for its overseas operations has been strategic because:

• All three countries are growing economies

• Zambia is a mineral rich land-locked nation (Africa’s leading copper producer); tax benefits to mining related industry

• Nigeria’s explosive market is dominated by a single player Nigachem Nigeria Ltd (SIIL’s local partner in Nigeria). The company’s previous experience as a distributor of explosives in Nigeria augured well for setting up capacity

• Turkey’s explosive market is equivalent to India’s in terms of size

Exhibit 29: Global industrial explosives market

Global Market - $10 bnIndian Exports - $40 mnAustralia

13%

North America25%

Latin America12%Western Europe

5%Eastern Europe5%

Africa7%

Russia5%

China16%

India5%

South East Asia7%

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 17

Exhibit 31: Annual GDP growth of Zambia, Nigeria & Turkey

67.3

6.44.9 4.3

5.4

-4.8

9.2 8.8

2.1

4

6.87.67.86.9

-6

-4

-2

0

2

4

6

8

10

12

2009 2010 2011 2012 2013

(%)

Zambia Nigeria Turkey

Source: World Bank, ICICIdirect.com Research

Exhibit 32: Revenues & profit from overseas operations

FY11 FY12 FY13 FY14 FY11 FY12 FY13 FY14 FY11 FY12 FY13 FY14Revenues 14.8 69.2 61.4 35.6 71.8 74.3 107.4 148.8 9.6 19.7 16.6 48.4

PBT 1.8 14.6 5.5 -1.1 16.0 12.4 26.7 36.2 0.2 -0.2 -0.1 1.3PAT 1.8 14.6 5.3 -0.4 10.9 8.5 18.6 24.7 0.2 -0.2 -0.1 1.3

Zambia Nigeria Turkey

Source: Company, ICICIdirect.com Research

As seen in Exhibit 31, the Nigeria and Turkey operations are running smoothly, as can be inferred from their earnings growth. However, Zambia’s financials have been volatile, with revenues dropping from | 61.4 crore in FY13 to | 35.6 crore in FY14 while profitability of | 5.3 crore turned into losses of | 0.4 crore in FY14. This can mainly be attributed to the tumbling prices of copper. Falling copper prices coupled with the high cost base of the Zambian mining industry has put mining players under pressure. Mining players, in a bid to reduce their operating cost, have attempted to lay off employees. This has brought them into a face-off with the government, which has threatened to revoke their mining licenses. Lower mining output has impacted explosives sales.

Exhibit 33: Falling global copper prices

6000

6800

7600

8400

9200

10000

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

($/M

T)

Source: Bloomberg, ICICIdirect.com Research

Exhibit 34: Zambia’s copper production

534

698 686 668 690

830

500

600

700

800

900

1000

2008 2009 2010 2011 2012 2013

(Mn

tonn

e)

Source: U.S. Geological Survey, ICICIdirect.com Research

SIIL tried to mitigate this risk by diversifying its product basket in Zambia and setting up a cartridge facility in FY14. We expect to see a pick-up in revenue of the Zambian subsidiary with a revival of global copper prices.

Zambia’s financials have been volatile, with revenues dropping from | 61.4 crore in FY13 to | 35.6 crore in FY14 while profitability of | 5.3 crore turned into losses of | 0.4 crore in FY14

ICICI Securities Ltd | Retail Equity Research Page 18

In FY11-14, revenues from overseas operations recorded growth at 34% CAGR. Going ahead, SIIL is in the process of enhancing the bulk capacity in Zambia and Turkey by 10,000 MT and 2,500 MT, respectively. The company will also explore opportunities in other African countries like Tanzania and Mozambique. Owing to the company's focus on expansion in overseas operations, we estimate the overseas revenues will grow from | 232.9 crore in FY14 to | 459.8 crore in FY17E at a CAGR of 25.5%. Given that the overseas business yields EBITDA margins in excess of 20% (higher than domestic operations), we expect a gradual improvement in EBITDA margins at the consolidated level.

Defence business: Important trigger for next wave of growth A demand-supply mismatch, huge potential in terms of increased defence outlay and economies of scale prompted SIIL to foray into the defence space in FY12. The company plans to tap the opportunity in the defence sector by supplying propellants and HMX explosives (warheads) to Bharat Dynamics (BDL) and ordnance factories for use in missile systems. Currently, India imports almost all its entire requirement of HMX. SIIL had an initial capex plan of | 220 crore for setting up a production capacity of 50 tonne per annum of HMX and 10,000 propellants. The company has already invested | 156 crore in the defence space, which was utilised to set up a capacity of 2500 propellant and 50 TPA of HMX. Going ahead, the company has capex plans of ~| 90 crore to increase the propellant capacity from 2,500 units to 10,000 units and HMX capacity from 50 TPA to 100 TPA. The company has participated in tenders for HMX, which are expected to yield revenues of | 5 crore in Q4FY15. The additional HMX capacity of 50 TPA is expected to be commissioned in FY16E. Given that SIIL will be the only player in India to supply HMX, we have assumed a higher capacity utilisation of 80% and 100% for FY16E and FY17E, respectively. Assuming realisation of | 1 crore per tonne of HMX, we have estimated the HMX production will generate revenues of | 40 crore and | 100 crore in FY16E and FY17E, respectively. SIIL has also participated in the limited tender floated for 500 units of Pinaka missile and 700 units of Akash missile. The company has guided that Pinaka missile order will be executed in FY16 while the execution of the Akash missile order will be spread across FY16 and FY17. Assuming a realisation of | 6 lakh per propellant for Pinaka and | 7 lakh per propellant for Akash, we estimate the Pinaka and Akash missile orders will generate revenues of | 30 crore and | 49 crore, respectively.

ICICI Securities Ltd | Retail Equity Research Page 19

Exhibit 35: Return profile of defence business for expected order book Unit FY15E FY16E FY17E

ProductionHMX tonne 5 40 100

Propellant (Akash) nos. 0 300 400Propellant (Pinaka) nos. 0 500 0

RealizationHMX | crore 1 1 1

Propellant (Akash) | crore 0.07 0.07 0.07Propellant (Pinaka) | crore 0.06 0.06 0.06

RevenueHMX | crore 5 40 100

Propellant (Akash) | crore 0 21 28Propellant (Pinaka) | crore 0 30 0

Total | crore 5 91 128EBITDA

Margin % 20 20 20EBITDA | crore 1 18 26

Depreciation | crore 0.04 0.73 1.02EBIT | crore 1.0 17.5 24.6

Capital employed | crore 245 245 245ROCE % 0.4 7.1 10.0

Source: Company, ICICIdirect.com Research

As seen in exhibit 35, we expect defence revenues to jump from | 5 crore in FY15E to | 128 crore in FY17E. Although the company has guided for a 25-30% EBITDA margin for the defence business, we have assumed a conservative EBITDA margin of 20% for the initial years of operation. The RoCE of 7-10% for FY16-17E may appear below par due to lower utilisation levels. However, once the additional capacity gets commissioned and the business stabilises, we expect higher utilisation levels to drive significant jump in the profitability, margins and return ratios.

ICICI Securities Ltd | Retail Equity Research Page 20

Financials Revenue growth of 20.5% CAGR in FY14-17E to be driven by all segments We expect consolidated revenues to increase from | 1,133 crore in FY14 to | 1,980.9 crore in FY17E at a CAGR of 20.5%, mainly on the back of stable domestic growth, expanding overseas operations and a burgeoning defence business (largely FY16E onwards). Over FY09-14, SIIL registered consolidated revenue CAGR of 18.4% on the back of growing market share in India from ~23% in FY09 to ~27% in FY14. Revenues from overseas operation commenced from FY11, which scaled up from | 95 crore in FY11 to | 232.9 crore in FY14 at a CAGR of 34.8%. Exhibit 36: Revenues to grow at 20.5% CAGR in FY14-17E

1121.8 1133.01343.7

1665.9

1980.9

0

500

1000

1500

2000

2500

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

Source: Company, ICICIdirect.com Research

Going ahead, we expect revenues from domestic operations to grow at a CAGR of 15.2% from | 1,008.5 crore in FY14 to | 1,543 crore in FY17E. Growth in domestic revenues is expected to be driven at 21.6% CAGR in bulk explosive revenues for FY14-17E. The cartridge, detonator and detonator fuse revenues are expected to grow at a CAGR of 13.4%, 8.1% and 7.6%, respectively, for the same period. Overseas operations are expected to continue the growth momentum, with overseas revenues expected to grow from | 232.9 crore in FY14 to | 459.8 crore at 25.5% CAGR in FY14-17E. Defence business revenues are expected to grow rapidly from | 5 crore in FY15E to | 128 crore in FY17E, contributing a meaningful 6% in FY17E consolidated revenues.

Exhibit 37: Domestic revenue break-up (including exports)

683.5

408.8

164.6

59.9

582.5

472.5

380.3384.9

583.8517.9

467.6400.8

220.1191.4174.1150.555.541.435.344.630.1 8.7

0100

200300400500600700

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

Bulk Cartridge Detonator Detonator Fuse Trading

Source: Company, ICICIdirect.com Research

Exhibit 38: Consolidated revenue break-up

84.7 81.2 79.2 74.4 72.4

15.3 18.820.5 21.6

5.1 6.020.40.3

0

20

40

60

80

100

FY13 FY14 FY15E FY16E FY17E

(%)

Domestic Overseas Defense

Source: Company, ICICIdirect.com Research

Over FY09-14, SIIL registered consolidated revenue CAGR of 18.4% on the back of growing market share in India from ~23% in FY09 to ~27% in FY14

ICICI Securities Ltd | Retail Equity Research Page 21

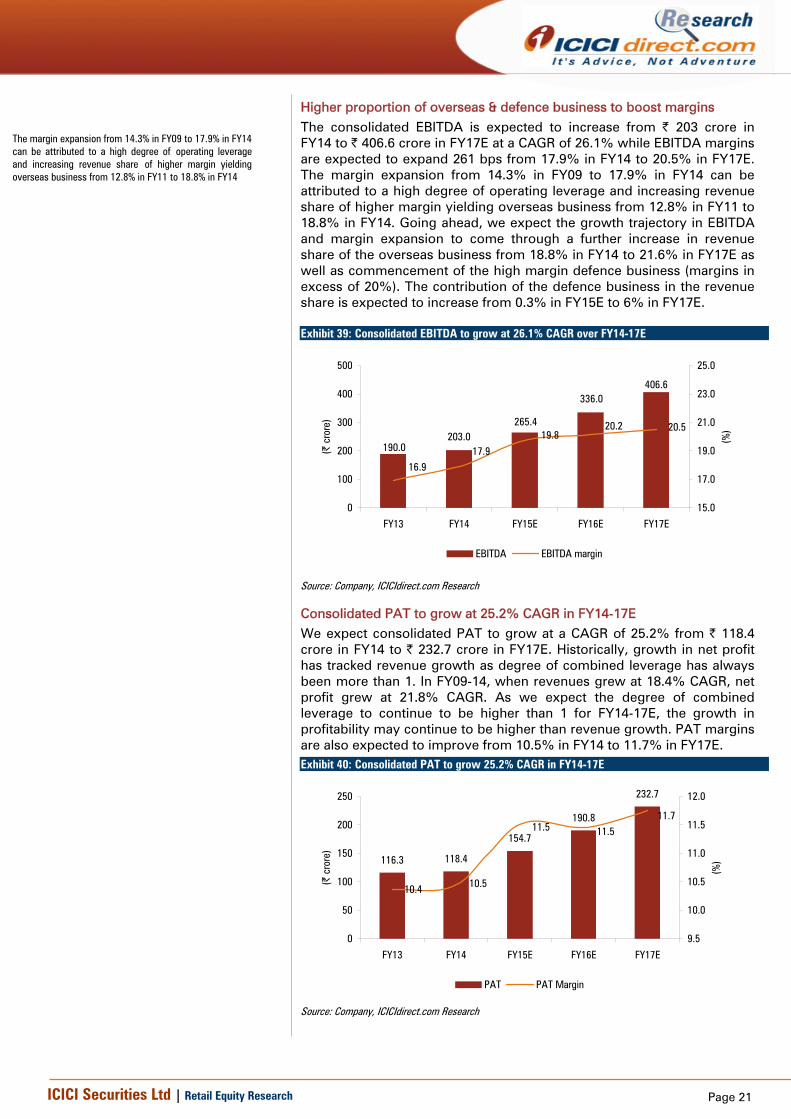

Higher proportion of overseas & defence business to boost margins The consolidated EBITDA is expected to increase from | 203 crore in FY14 to | 406.6 crore in FY17E at a CAGR of 26.1% while EBITDA margins are expected to expand 261 bps from 17.9% in FY14 to 20.5% in FY17E. The margin expansion from 14.3% in FY09 to 17.9% in FY14 can be attributed to a high degree of operating leverage and increasing revenue share of higher margin yielding overseas business from 12.8% in FY11 to 18.8% in FY14. Going ahead, we expect the growth trajectory in EBITDA and margin expansion to come through a further increase in revenue share of the overseas business from 18.8% in FY14 to 21.6% in FY17E as well as commencement of the high margin defence business (margins in excess of 20%). The contribution of the defence business in the revenue share is expected to increase from 0.3% in FY15E to 6% in FY17E. Exhibit 39: Consolidated EBITDA to grow at 26.1% CAGR over FY14-17E

190.0203.0

265.4

406.6336.0

16.917.9

19.820.520.2

0

100

200

300

400

500

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

15.0

17.0

19.0

21.0

23.0

25.0

(%)

EBITDA EBITDA margin

Source: Company, ICICIdirect.com Research

Consolidated PAT to grow at 25.2% CAGR in FY14-17E We expect consolidated PAT to grow at a CAGR of 25.2% from | 118.4 crore in FY14 to | 232.7 crore in FY17E. Historically, growth in net profit has tracked revenue growth as degree of combined leverage has always been more than 1. In FY09-14, when revenues grew at 18.4% CAGR, net profit grew at 21.8% CAGR. As we expect the degree of combined leverage to continue to be higher than 1 for FY14-17E, the growth in profitability may continue to be higher than revenue growth. PAT margins are also expected to improve from 10.5% in FY14 to 11.7% in FY17E.

Exhibit 40: Consolidated PAT to grow 25.2% CAGR in FY14-17E

116.3 118.4

154.7

190.8

232.7

10.4 10.5

11.511.7

11.5

0

50

100

150

200

250

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

9.5

10.0

10.5

11.0

11.5

12.0

(%)

PAT PAT Margin

Source: Company, ICICIdirect.com Research

The margin expansion from 14.3% in FY09 to 17.9% in FY14 can be attributed to a high degree of operating leverage and increasing revenue share of higher margin yielding overseas business from 12.8% in FY11 to 18.8% in FY14

ICICI Securities Ltd | Retail Equity Research Page 22

RoE, RoCE set to improve to 20.2%, 20.3%, respectively, by FY17E In the last few years, the RoE, RoCE have declined from 22.1%, 21% in FY10 to 17.9%, 15.9%, respectively, in FY14. This was on the back of the company incurring a capex to increase the licensed capacity for domestic operations, its expansion in overseas subsidiaries and foray in the defence business. However, going ahead, we expect RoE, RoCE to resurrect back to 20.2%, 20.3%, respectively, on the back of expansion in margins & improvement in asset turnover due to higher capacity utilisation in bulk operations (current capacity utilisation for bulk explosives is 49%). Exhibit 41: RoE, RoCE trend

20.3

18.1 18.517.919.6

20.220.1

15.9

20.3

19.8

10

13

16

19

22

25

FY13 FY14 FY15E FY16E FY17E

(%)

ROE ROCE

Source: Company, ICICIdirect.com Research

Cash flows set to improve; CFO/EBITDA at 0.5x; D/E to reduce to 0.5x The company is expected to generate strong cash flows with cash flow from operations (CFO) increasing from | 123.1 crore in FY14 to | 218.4 crore in FY17E. Strong CFO will ensure repayment of working capital loans and smooth execution of the annual capex of | 100 crore p.a. guided by the company for the next three years. The FCF that is expected to turn positive on the back of strong CFO may grow to | 118.4 crore in FY17E. The CFO/EBITDA, a measure of quality of earnings, is also expected to stabilise at ~0.5x by FY17E. The D/E is expected to reduce from 0.7x in FY14 to 0.5x in FY17E.

Exhibit 42: CFO, EBITDA, CFO/EBITDA trend

218.

4

203.

0

265.

4

336.

0

406.

6

164.

5

233.

8

123.

1

92.9

190.

0

0.50.6

0.9

0.5 0.5

050

100150200250300350400450

FY13 FY14E FY15E FY16E FY17E

(| c

rore

)

0.0

0.2

0.4

0.6

0.8

1.0

(x)

CFO EBITDA CFO/EBITDA

Source: Company, ICICIdirect.com Research

Exhibit 43: Free cash flow, free cash flow yield

133.8

64.5

118.4

(19.0)(37.4)

2.3

1.2

2.5

-0.4-0.7

-50

0

50

100

150

FY13 FY14E FY15E FY16E FY17E

(| c

rore

)

-1.0-0.50.00.51.01.52.02.53.0

(%)

FCFF FCFF yield

Source: Company, ICICIdirect.com Research

The return ratios are set to improve on the back of expansion in margins & improvement in asset turnover due to higher capacity utilisation in bulk operations

ICICI Securities Ltd | Retail Equity Research Page 23

Exhibit 44: Trend in debt & debt/equity

344.5

442.8 445.4

515.4

581.4

0.6

0.7

0.60.50.5

300

350

400

450

500

550

600

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

(x)

Debt Debt/Equity

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 24

Risks & Concerns Lower volume growth due to slowdown in mining & infrastructure Coal mining & infrastructure currently account for 51% of SIIL’s revenues. Non-CIL institutional clients (mostly metal & steel sector) account for 18% of SIIL’s revenue. Any slowdown in mining, power & infrastructure sectors can affect SIIL’s volume growth negatively. However, in FY09-14, when mining & infrastructure activity was muted, revenue diversification and an increasing market share enabled SIIL to witness volume growth of 14.7%, and 9.2% CAGR in bulk and cartridge explosives, respectively. Given that the bulk and cartridge segment contribute 63% of consolidated revenues, we have calculated the sensitivity of FY16E and FY17E EPS to the volume growth in the bulk & cartridge segment.

Exhibit 45: Sensitivity of FY16E EPS to volume growth

Bulk volumes growth (%)

106.85469 -10 10 20 30 40

-8 90.2 96.8 100.2 103.5 106.8

0 92.8 99.5 102.8 106.1 109.4

Cartridge volume growth (%) 8 95.5 102.1 105.4 108.7 112.1

16 98.1 104.7 108.0 111.4 114.7

24 100.7 107.3 110.7 114.0 117.3

Source: Company, ICICIdirect.com Research

Exhibit 46: Sensitivity of FY17E EPS to volume growth (assuming base case for FY16E)

Bulk volume growth(%)

130.38957 -10 0 10 20 30

-8 113.9 118.2 122.5 126.9 131.2

0 116.9 121.2 125.5 129.9 134.2

Cartridge volume growth (%) 8 119.9 124.2 128.6 132.9 137.2

16 122.9 127.2 131.6 135.9 140.2

24 125.9 130.3 134.6 138.9 143.3

Source: Company, ICICIdirect.com Research

We have estimated the consolidated EPS of | 105.4 and | 128.6 for FY16E and FY17E, respectively (base case). As can be seen in exhibit 50, every 10% point change in FY16E bulk volume growth will result in | 3.4 change in FY16 EPS whereas an 8% point change in FY16E cartridge volume growth will result in | 2.6 change in FY16E EPS. Similarly, every 10% change in FY17E volume growth will result in | 4.3 change in FY17E EPS while an 8% change in FY17E cartridge volume growth will result in a | 3 change in FY17E EPS.

Slowdown in overseas subsidiaries’ growth Overseas subsidiaries (Zambia, Nigeria and Turkey) contributed 18.8% of SIIL’s consolidated revenues in FY14 while the share is expected to increase to 21.7% in FY17E. The Zambian subsidiary runs the risk of volatility in earnings due to dampened copper prices. SIIL’s Nigerian operations also face a risk given that concerns regarding the Nigerian economy are rising with falling crude prices. Crude oil accounts for ~75% of the government revenues and ~90% of exports for Nigeria. This African country is also prone to insurgencies, with the latest being Boko Haram, a militant movement based in Northern Nigeria. These factors could impact the stability of operations in Nigeria, which contributed 63.9% of the consolidated revenues in FY14. SIIL has always tried to mitigate such political & operational risk by partnering with local companies for its foreign operations. We draw some comfort from the fact that SIIL has been associated with Nigachem Nigeria since 2005 (previously as a dealer).

Given that the bulk and cartridge segment contribute 63% of consolidated revenues, slowdown in mining, power and infrastructure can adversely impact the company’s profitability

Every 10% change in FY17E volume growth will result in | 4.3 change in FY17E EPS while an 8% change in FY17E cartridge volume growth will result in a | 3 change in FY17E EPS

Overseas subsidiaries (Zambia, Nigeria and Turkey) contributed 18.8% of SIIL’s consolidated revenues in FY14 while the share is expected to increase to 21.7% in FY17E

ICICI Securities Ltd | Retail Equity Research Page 25

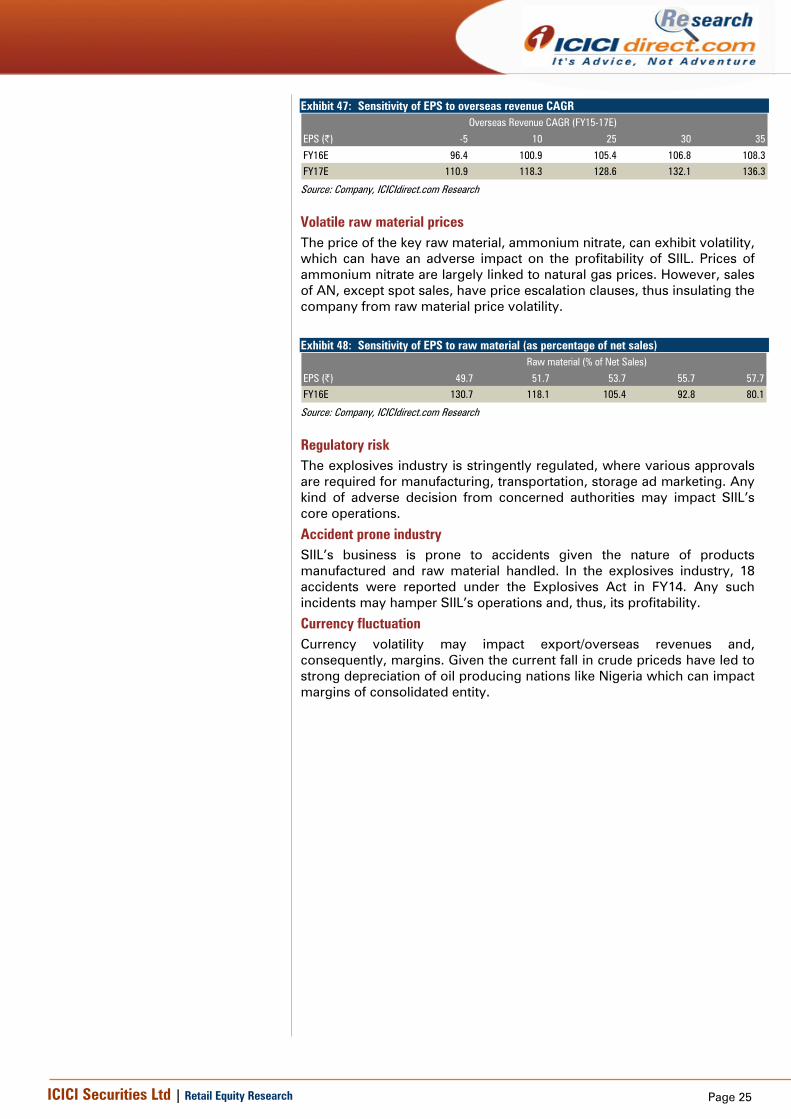

Exhibit 47: Sensitivity of EPS to overseas revenue CAGR

Overseas Revenue CAGR (FY15-17E)

EPS (|) -5 10 25 30 35

FY16E 96.4 100.9 105.4 106.8 108.3FY17E 110.9 118.3 128.6 132.1 136.3

Source: Company, ICICIdirect.com Research

Volatile raw material prices The price of the key raw material, ammonium nitrate, can exhibit volatility, which can have an adverse impact on the profitability of SIIL. Prices of ammonium nitrate are largely linked to natural gas prices. However, sales of AN, except spot sales, have price escalation clauses, thus insulating the company from raw material price volatility. Exhibit 48: Sensitivity of EPS to raw material (as percentage of net sales)

EPS (|) 49.7 51.7 53.7 55.7 57.7FY16E 130.7 118.1 105.4 92.8 80.1

Raw material (% of Net Sales)

Source: Company, ICICIdirect.com Research

Regulatory risk The explosives industry is stringently regulated, where various approvals are required for manufacturing, transportation, storage ad marketing. Any kind of adverse decision from concerned authorities may impact SIIL’s core operations.

Accident prone industry SIIL’s business is prone to accidents given the nature of products manufactured and raw material handled. In the explosives industry, 18 accidents were reported under the Explosives Act in FY14. Any such incidents may hamper SIIL’s operations and, thus, its profitability.

Currency fluctuation Currency volatility may impact export/overseas revenues and, consequently, margins. Given the current fall in crude priceds have led to strong depreciation of oil producing nations like Nigeria which can impact margins of consolidated entity.

ICICI Securities Ltd | Retail Equity Research Page 26

Valuation SIIL possesses a wide moat in the form of a de-risked business model, industry leadership, significant entry barriers and an optimal product mix to benefit the most from a revival in mining & infrastructure activity. Even in the export & overseas business, we believe SIIL has just scratched the surface of growth, with many more un-penetrated markets yet to be explored. A foray in new business segments like defence will further solidify SIIL’s business model at a time when the government’s prerogative is to indigenise defence manufacturing, which will allow SIIL to scale the defence business at a faster pace. Even during times of moderate/muted business environment, SIIL had witnessed robust revenue CAGR of 18.4%, over FY09-14, backed by a strong 12.4% volume CAGR (bulk + cartridge) coupled with capacity expansion and market share gains. This speaks volumes for the pedigree of the management and business model that has evolved over time and reiterates our confidence in the company to capture the upcoming opportunity with a revival in industrial activity. Hence, SIIL is a rare combination of excellent growth track record, proactive management, conservative leverage approach, expanding margins & return ratios along with 25%+ growth guidance from management for the next three years. Going ahead, the Coal & Power Ministry have set CIL a stiff target to achieve 1000 mn tonnes of coal production till FY19E. This implies 17.2% production volume CAGR over FY14-19E. This, in turn, will create an incremental demand of ~7,71,008 tonnes of explosives, implying a rise of ~99% over the same period. Being the largest player, SIIL is well set to capitalise on the forthcoming opportunity given the kind of product mix, existing capacities and future capex plans it commands. We expect revenues, EBITDA and PAT to grow at a CAGR of 20.5%, 26.1% and 25.2%, respectively, over FY14-17E. Consistency in revenue, PAT growth, disciplined capex programmes (leverage of 0.7x) and logical overseas and new segment diversification have already led to a re-rating of the P/E multiples of the stock. The YTD rally of 205% in the stock price has made the forward multiples look rich at 22x F17E EPS given the markets are pricing in 8-10% growth for the industry over FY16E-17E. However, SIIL, on an average, has produced industry beating growth rates owing to the factors discussed above. Also, as the leader of the industry, SIIL deserves premium valuations. The crucial catalyst for a further re-rating depends on the execution of the 1000 mn tonne target of coal production by FY19E. Hence, in case the stiff coal production target sees the light of the day, then the Street would be undermining the earnings growth for the industry and SIIL, in particular. However, to capture the emerging growth opportunities in the explosives and defence business, we would base our valuations on the basis of PEG ratio. We are pencilling in 25.2% PAT CAGR over FY14-17E for SIIL and ascribing a PEG multiple of 1x, implying a target P/E of 26x. Hence, we arrive at a fair value of | 3342 and initiate coverage with a BUY rating.

SIIL is a rare combination of excellent growth track record, proactive management, conservative leverage approach, expanding margins & return ratios along with 25%+ growth guidance from management for the next three years.

ICICI Securities Ltd | Retail Equity Research Page 27

Trading multiples

Exhibit 49: Two year forward P/E

0

500

1000

1500

2000

2500

3000

3500

Oct-0

8

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Jan-

12

Apr-1

2

Jul-1

2

Oct-1

2

Jan-

13

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4

(|)

Price 23x 19x 16x 12x 10x 8x 7x

Source: Reuters, ICICIdirect.com Research

Sensitivity Analysis We have constructed a bull and bear-case scenario analysis around our revenue CAGR estimates of SII to better assess the risk reward outcomes. Bull case scenario… In the bull case, we expect consolidated revenues to grow to | 2174.4 crore at a CAGR of 24.3% over FY14-17E. Domestic explosives revenues are expected to grow at a CAGR of 18.6% (vs. 15.2% in the base case). We expect the overseas business to grow at CAGR of 29% (vs. 25.5% in base case). We expect defence revenues to touch | 200 crore in FY17E (against our estimate of | 128 crore). The PAT is expected to grow at a CAGR of 29.8% over FY14-17E (vs. 25.2% in the base case). For the bull case, we ascribe 1.0x PEG over FY14-17E earning CAGR to arrive at a target multiple of 30x and derive a target price of | 4299 providing a robust upside potential of 49.5%. Bear case scenario… In the bear case, we have assumed a volume CAGR of 10% for all segments in explosives (bulk, cartridge, detonator & detonating fuse). Accordingly, we expect consolidated revenues of SIIL to grow to | 1721.6 crore at a CAGR of 15% over FY14E-17E. Domestic explosives revenues are expected to grow at a CAGR of 10.7%. We expect the overseas business to grow slowly at CAGR of 15.2%. We maintain the base case assumptions for the defence business. The PAT is expected to grow at a CAGR of 18.8% over FY14-17. For the bear case, we ascribe 1.0x PEG over FY14-17E earning CAGR to arrive at a target multiple of 19x and derive a target price of | 2084, implying a downside of 27.5%. Exhibit 50: Bull-base-bear sensitivity

Base Case Bull Case Bear Case

Revenue (FY17E) 1980.9 2174.4 1721.6

Revenue CAGR (FY14-17E) 20.5 24.3 15.0

EBITDA Margin (FY17E) 20.5 20.5 20.5

FY17E EPS 128.6 143.3 109.7

Fwd P/E FY17 (x) 22.4 20.1 26.2

PEG Ratio (x) 1 1 1

PAT CAGR (FY14-17E) 25.2 29.8 18.8

Target P/E (x) 26 30 19

Target Price 3342 4299 2084

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 28

Exhibit 51: Peer comparison (Financials) Company EBITDA Margin (%)

FY12 FY13 FY14 FY12 FY13 FY14 FY12 FY13 FY14 FY12 FY13 FY14 FY12 FY13 FY14 FY12 FY13 FY14

Domestic

Solar Industries 5203 976 1122 1133 175 190 203 18.0 16.9 17.9 101.2 116.3 118.4 25.0 20.3 17.9 22.4 18.1 15.9

Premier Explosives 266 108 109 145 18 10 17 16.2 9.0 11.8 11.9 5.3 9.2 29.3 11.4 17.4 30.1 13.2 19.3

Keltech Energies 78 178 155 154 10 10 12 5.6 6.2 8.1 5.0 4.3 5.9 10.4 8.2 19.1 10.7 9.5 17.8

Gulf Oil Corp Ltd 762 1236 1265 1301 68 23 41 5.5 1.8 3.2 48.2 50.2 67.7 6.4 4.7 6.1 7.9 -5.4 5.1

International

Orica Ltd 34340 36157 38675 38175 6341 6706 6472 17.5 17.3 17.0 2182.2 3328.2 3384.3 12.3 16.9 14.8 16.4 20.4 19.1

Incitec Pivot Ltd 28998 18966 19119 18828 3962 3658 4148 20.9 19.1 22.0 2766.7 2062.1 1388.0 13.2 8.9 5.7 20.8 7.1 10.0

Revenues EBITDA ROEPATMcap (| crore)

ROCE

Source: Bloomberg, ICICIdirect.com Research

Exhibit 52: Peer comparison (Valuation) Company Mcap (| crore) P/E Mcap/Sales

FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

Solar Industries India Ltd 5203 33.6 27.3 22.4 20.4 16.0 13.1 3.9 3.1 2.6

Orica Ltd 34340 11.4 10.7 9.9 7.5 7.1 6.8 0.9 1.0 1.0

Incitec Pivot Ltd 28998 14.9 13.7 11.0 9.1 8.5 6.9 2.0 1.9 1.7

EV/EBITDA

Source: Bloomberg, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 29

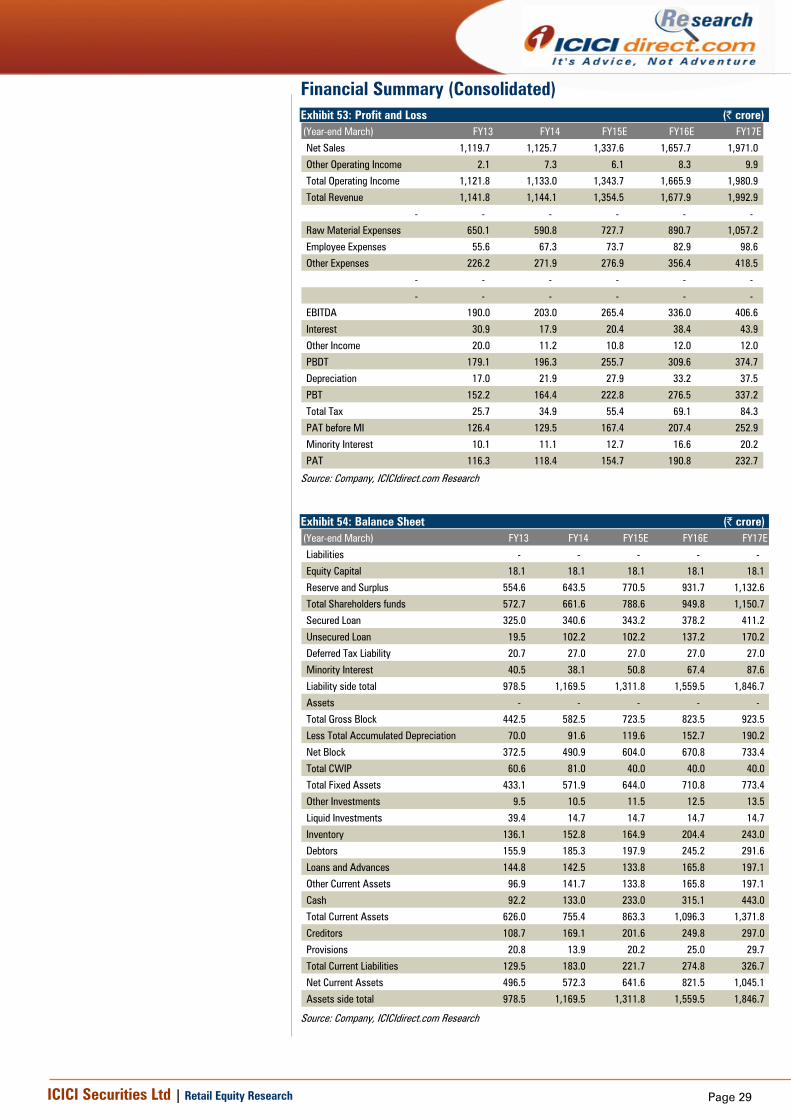

Financial Summary (Consolidated) Exhibit 53: Profit and Loss (| crore)(Year-end March) FY13 FY14 FY15E FY16E FY17E

Net Sales 1,119.7 1,125.7 1,337.6 1,657.7 1,971.0

Other Operating Income 2.1 7.3 6.1 8.3 9.9

Total Operating Income 1,121.8 1,133.0 1,343.7 1,665.9 1,980.9

Total Revenue 1,141.8 1,144.1 1,354.5 1,677.9 1,992.9

- - - - - -

Raw Material Expenses 650.1 590.8 727.7 890.7 1,057.2

Employee Expenses 55.6 67.3 73.7 82.9 98.6

Other Expenses 226.2 271.9 276.9 356.4 418.5

- - - - - -

- - - - - -

EBITDA 190.0 203.0 265.4 336.0 406.6

Interest 30.9 17.9 20.4 38.4 43.9

Other Income 20.0 11.2 10.8 12.0 12.0

PBDT 179.1 196.3 255.7 309.6 374.7

Depreciation 17.0 21.9 27.9 33.2 37.5

PBT 152.2 164.4 222.8 276.5 337.2

Total Tax 25.7 34.9 55.4 69.1 84.3

PAT before MI 126.4 129.5 167.4 207.4 252.9

Minority Interest 10.1 11.1 12.7 16.6 20.2

PAT 116.3 118.4 154.7 190.8 232.7

Source: Company, ICICIdirect.com Research

Exhibit 54: Balance Sheet (| crore)(Year-end March) FY13 FY14 FY15E FY16E FY17E

Liabilities - - - - -

Equity Capital 18.1 18.1 18.1 18.1 18.1

Reserve and Surplus 554.6 643.5 770.5 931.7 1,132.6

Total Shareholders funds 572.7 661.6 788.6 949.8 1,150.7

Secured Loan 325.0 340.6 343.2 378.2 411.2

Unsecured Loan 19.5 102.2 102.2 137.2 170.2

Deferred Tax Liability 20.7 27.0 27.0 27.0 27.0

Minority Interest 40.5 38.1 50.8 67.4 87.6

Liability side total 978.5 1,169.5 1,311.8 1,559.5 1,846.7

Assets - - - - -

Total Gross Block 442.5 582.5 723.5 823.5 923.5

Less Total Accumulated Depreciation 70.0 91.6 119.6 152.7 190.2

Net Block 372.5 490.9 604.0 670.8 733.4

Total CWIP 60.6 81.0 40.0 40.0 40.0

Total Fixed Assets 433.1 571.9 644.0 710.8 773.4

Other Investments 9.5 10.5 11.5 12.5 13.5

Liquid Investments 39.4 14.7 14.7 14.7 14.7

Inventory 136.1 152.8 164.9 204.4 243.0

Debtors 155.9 185.3 197.9 245.2 291.6

Loans and Advances 144.8 142.5 133.8 165.8 197.1

Other Current Assets 96.9 141.7 133.8 165.8 197.1

Cash 92.2 133.0 233.0 315.1 443.0

Total Current Assets 626.0 755.4 863.3 1,096.3 1,371.8

Creditors 108.7 169.1 201.6 249.8 297.0

Provisions 20.8 13.9 20.2 25.0 29.7

Total Current Liabilities 129.5 183.0 221.7 274.8 326.7

Net Current Assets 496.5 572.3 641.6 821.5 1,045.1

Assets side total 978.5 1,169.5 1,311.8 1,559.5 1,846.7

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 30

Exhibit 55: Cash flow statement (| crore)(Year-end March) FY13 FY14 FY15E FY16E FY17E

Profit after Tax 116.3 118.4 154.7 190.8 232.7

Depreciation 17.0 21.9 27.9 33.2 37.5

Cash Flow before working capital changes 164.1 158.1 203.1 262.3 314.1

- - - - - -

Net Increase in Current Assets (46.7) (88.6) (8.0) (150.8) (147.7)

Net Increase in Current Liabilities (24.6) 53.5 38.7 53.0 51.9

Net cash flow from operating activities 92.9 123.1 233.8 164.5 218.4

- - - - - -

(Purchase)/Sale of Fixed Assets (112.1) (160.7) (100.0) (100.0) (100.0)

Net Cash flow from Investing Activities (145.9) (133.1) (88.3) (84.4) (80.8)

- - - - - -

Inc / (Dec) in Equity Capital 0.8 - - - -

Inc / (Dec) in Loan Funds 58.1 15.5 2.6 35.0 33.0

Inc / (Dec) in Loan Funds 3.2 82.7 - 35.0 33.0

Net Cash flow from Financing Activities 82.3 50.8 (45.4) 2.0 (9.7)

- - - - - -

Net Cash flow 29.3 40.8 100.0 82.1 127.9

Cash and Cash Equivalent at the beginning 62.9 92.2 133.0 233.0 315.1

Closing Cash/ Cash Equivalent 92.2 133.0 233.0 315.1 443.0

Source: Company, ICICIdirect.com Research

Ratios

Exhibit 56: Ratio Analysis (Year-end March) FY13 FY14 FY15E FY16E FY17EPer Share DataEPS 64.3 65.4 85.5 105.4 128.6 Cash EPS 73.6 77.5 100.9 123.7 149.3 BV 316.4 365.5 435.8 524.8 635.8 Operating profit per share 105.0 112.1 146.6 185.7 224.7

Operating RatiosEBITDA / Total Operating Income 16.9 17.9 19.8 20.2 20.5 PAT / Total Operating Income 10.4 10.5 11.5 11.5 11.7

Return RatiosRoE 20.3 17.9 19.6 20.1 20.2 RoCE 18.1 15.9 18.5 19.8 20.3 RoIC 22.0 19.3 23.2 25.5 27.4

Valuation RatiosEV / EBITDA 28.5 27.1 20.4 16.0 13.1 P/E 44.7 43.9 33.6 27.3 22.4 EV / Net Sales 4.8 4.9 4.0 3.3 2.7 Sales / Equity 2.0 1.7 1.7 1.7 1.7 Market Cap / Sales 4.6 4.6 3.9 3.1 2.6 Price to Book Value 9.1 7.9 6.6 5.5 4.5

Turnover RatiosAsset turnover 1.3 1.0 1.1 1.2 1.2 Debtors Turnover Ratio 7.2 6.1 6.8 6.8 6.8

Creditors Turnover Ratio 10.3 6.7 6.6 6.6 6.6

Solvency RatiosDebt / Equity 0.6 0.7 0.6 0.5 0.5 Current Ratio 4.8 4.1 3.9 4.0 4.2 Quick Ratio 3.8 3.3 3.2 3.2 3.5

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 31

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction; Buy: >10%/15% for large caps/midcaps, respectively; Hold: Up to +/-10%; Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 1st Floor, Akruti Trade Centre, Road No. 7, MIDC, Andheri (East) Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 32

ANALYST CERTIFICATION We /I, Chirag Shah, PGDBM and Nishit Zota, MBA Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.