january conference presentation - jegi · the americas represented 64% of transaction value in q1...

TRANSCRIPT

June 7, 2017

2

JEGI only engages when we can outperform our competition and meet or exceed client expectations – we turn down or defer consideration on numerous potential assignments

Every member of JEGI’s Leadership Team has a vested interest in the performance of the firm and each transaction’s successful closing

Senior bankers average 14 years at JEGI, completing 600+ M&A transactions

Second longest-tenured boutique investment bank on Wall Street

Given our unique, highly selective engagement model, 80% of the firm’s time is spent on execution, not pitching

Engagements closed:

Engagements where valuation exceeded

expectations:

Average time to close:

•

•

•

•

4

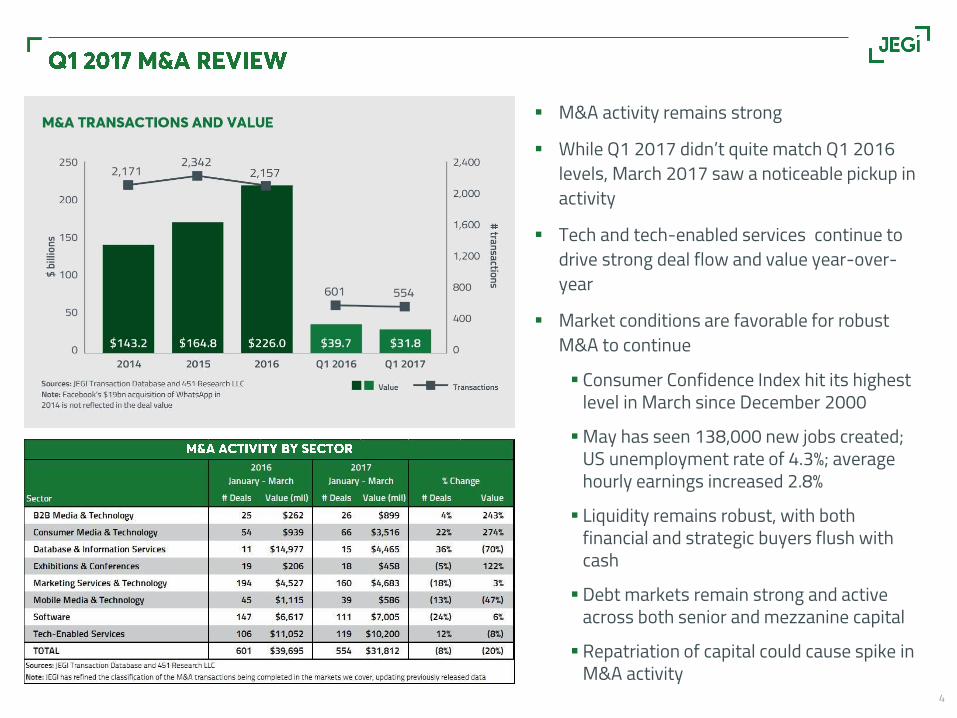

M&A activity remains strong

While Q1 2017 didn’t quite match Q1 2016 levels, March 2017 saw a noticeable pickup in activity

Tech and tech-enabled services continue to drive strong deal flow and value year-over-year

Market conditions are favorable for robust M&A to continue Consumer Confidence Index hit its highest

level in March since December 2000May has seen 138,000 new jobs created;

US unemployment rate of 4.3%; average hourly earnings increased 2.8%

Liquidity remains robust, with both financial and strategic buyers flush with cash

Debt markets remain strong and active across both senior and mezzanine capital

Repatriation of capital could cause spike in M&A activity

5

PE dry powder, or uninvested cash, is at a record high of nearly $1.5 trillion

Strategics also have unprecedented levels of cash on hand – S&P Global estimates $1.8 trillion of total cash on the balance sheets of nonfinancial corporates

• Much of this capital is being held overseas, given the current tax laws; Trump administration discussing lowering taxes for repatriation of this capital; could significantly impact M&A and infrastructure investment

Source: Bain Capital

6

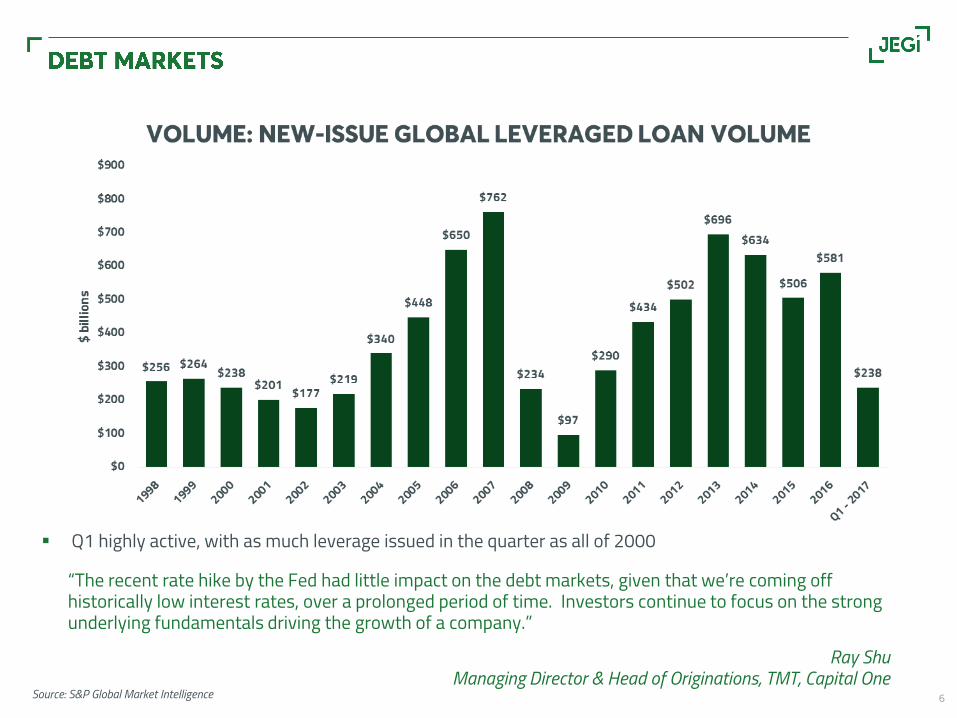

“The recent rate hike by the Fed had little impact on the debt markets, given that we’re coming off historically low interest rates, over a prolonged period of time. Investors continue to focus on the strong underlying fundamentals driving the growth of a company.”

Ray ShuManaging Director & Head of Originations, TMT, Capital One

Q1 highly active, with as much leverage issued in the quarter as all of 2000

Source: S&P Global Market Intelligence

PE Deal Flow by Year Mid-Market PE Deal Flow by Year

Median Buyout Multiples and Debt Key Observations

Large number of newly-formed PE funds targeting middle market, driving competition for quality assets

Middle market deals accounting for 57% of PE deals in Q1-17

EV/EBITDA multiples at 10.8x in Q1-17, up from 9.2x in 2014

Median equity contributions at 6.2x

Credit markets have tightened, but lenders remain active; unitranche notably aggressive

Add-ons represented 64% of 2016 volume

$512

$889

$359

$167

$350

$422

$472

$514

$660

$653

$648

$119

2,810

3,499

2,743

1,858

2,705 3,068

3,467 3,354

4,162 4,211 3,871

Deal Value ($bn) # of Deals Closed

745

$275

$336

$194

$93

$237

$276

$316

$300

$447

$399

$357

$91

1,464

1,842

1,292

710

1,292 1,477

1,891 1,709

2,186 2,180 2,123 Deal Value ($bn) # of Deals Closed

4.6x 5.2x

4.7x 5.

5x

5.2x 5.7x

5.4x 6.

2x

3.5x 4.

0x

3.8x 3.

8x

4.0x 4.

5x 5.3x 4.

6x

8.1x9.1x

8.5x9.3x 9.2x

10.1x10.7x

2010 2011 2012 2013 2014 2015 2016 Q1-2017

Debt / EBITDA Equity / EBITDA Valuation / EBITDA

7

10.8x

422

Source: Pitchbook

•

•

•

•

9

Despite a series of political shockwaves, 2016 global M&A activity saw more than 40K deals valued at $3.6 trillion vs. 39K deals and $3.9 trillion in value in 2015

Nearly 10K deals totaling $752 billion were announced in the first quarter of 2017, an increase in both deal value and number of deals from Q1-2016’s 9,500 deals and $745 billion in value

The Americas represented 64% of transaction value in Q1 2017

Source: Bloomberg

10

11

Both strategic companies and private equity firms are attracted to scale, high growth, and high-margin recurring revenue models, on mature businesses

In tech and tech enabled sectors, business model, addressable market and topline growth rates/prospects drive value

Creative solutions to help buyers achieve these goals and help sellers accelerate transformation: Pre-pack merger

Proprietary deal structure, where two or more independent companies are merged on paper to create a single “notional new company”

Pro-forma financials reflect full benefit of all synergies – revenue and costs Combined positioning of the two companies Single management team and organizational footprint

12

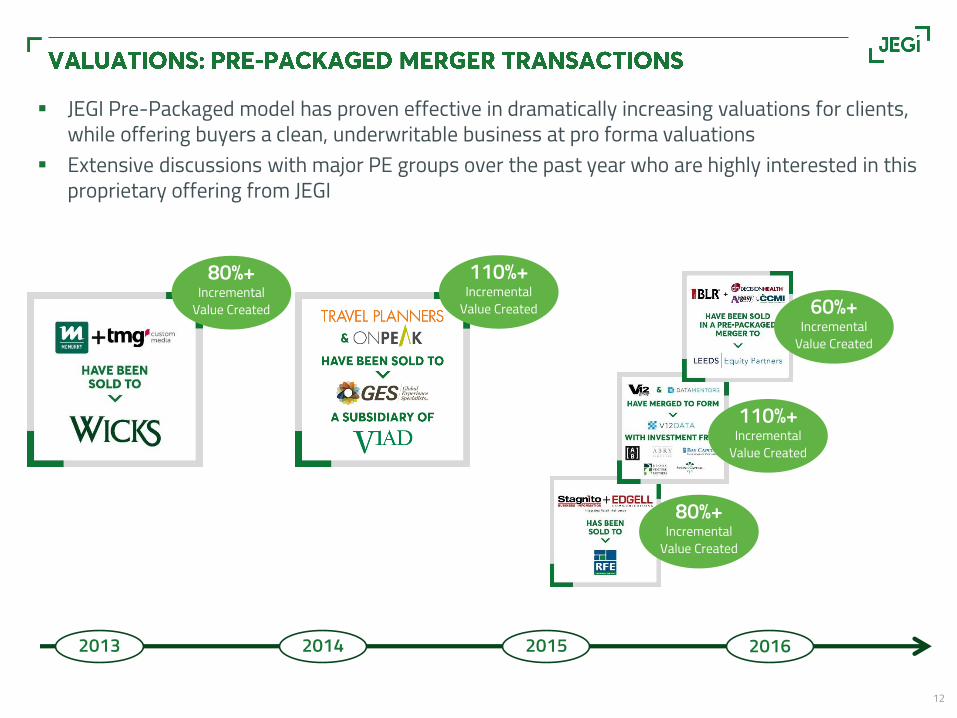

JEGI Pre-Packaged model has proven effective in dramatically increasing valuations for clients, while offering buyers a clean, underwritable business at pro forma valuations

Extensive discussions with major PE groups over the past year who are highly interested in this proprietary offering from JEGI

80%+ Incremental

Value Created

110%+ Incremental

Value Created

2013 2014 2015 2016

60%+ Incremental

Value Created

110%+ Incremental

Value Created

80%+ Incremental

Value Created

•

•

•

•

14

B2B media continues to diversify away from ad-supported print; tradeshows, conferences, data businesses and content marketing are all strategic targets

Scale will continue to be a major driver in B2B media deals

UK and European based companies are highly focused on the US as a geographical expansion opportunity

Will continue to see divestiture of non-core, slower growth assets

PE buyers interested in businesses with in-person, experiential and/or end-user and recurring subscription revenue streams

Continued interest in B2B media assets from Asian buyer/investor groups

15

Events

($ millions) Valuation Multiples

Ascential 1,802 2,091 2.6x 370 106 29% (21%) 5.7x 19.7x 4.3x 13.5xDMGT 2,966 3,705 2.3x 2,497 327 13% (10%) 1.5x 11.3x 1.7x 10.0xEmerald Expo Events 1,526 2,228 4.8x 324 147 45% 6% 6.9x 15.1x - -Euromoney 1,586 1,705 0.7x 525 150 28% (14%) 3.2x 11.4x 3.1x 11.7xGL Events 623 1,117 3.0x 1,006 136 14% (2%) 1.1x 8.2x 1.0x 7.2xInforma 7,285 9,206 3.5x 1,662 522 31% (7%) 5.5x 17.6x 4.1x 12.1xITE Group 541 654 2.0x 175 42 24% (15%) 3.7x 15.7x 3.5x 16.4xRELX Group 43,720 30,707 2.2x 8,513 2,552 30% (3%) 3.6x 12.0x 3.2x 9.1xTarsus Group 419 513 3.8x 84 23 27% (30%) 6.1x 22.2x 3.2x 9.3xUBM 3,668 4,491 2.6x 1,066 291 27% (6%) 4.2x 15.4x 3.5x 11.4xWilmington 299 352 1.8x 141 31 22% (6%) 2.5x 11.5x 2.3x 10.3xMean 26% (10%) 4.0x 14.6x 3.0x 11.1xMedian 27% (7%) 3.7x 15.1x 3.2x 10.9xSource: S&P Capital IQ, as of June 2, 2017Note: All data is based on fiscal year end

Company Market Cap Enterprise Value Net Debt/EBITDA

Financial Data

2016 2016 2017F

TEV/Rev TEV/EBITDA Revenue EBITDA Margin YoY Rev Growth

TEV/Rev TEV/EBITDA

16

Deal Size: $1.6 billion, 4.2x revenue, 11x EBITDA

Target: Information services and marketing company, with the three largest revenue streams being events, digital and marketing services

Buyer Rationale: Penton enables Informa to dramatically increase its US presence, bolster its core verticals, add a number of tradeshows at scale and provide new capabilities – services, brands & communities, and marketing solutions

Insider View “Since the acquisition announcement, our interaction with the Penton team has reaffirmed our belief that this combination will enhance our presence in attractive market segments.”

Stephen Carter, CEO, Informa

acquires

17

Deal Size: $151 million, 3x revenue

Target: Insight division provides professional information services for financial, risk, insurance and financial technology specialists

Buyer Rationale: As a 100% French business, Infopro is actively looking to expand into new geographies; PE backer has committed €500 million of equity to this strategy

Insider View “The acquisition will support Infopro Digital’s digital transformation and international growth strategies. Following this acquisition, we will do nearly a quarter of our business in international markets.”

Christophe Czajka, CEO, Infopro

acquires

18

Deal Size: Undisclosed

Target: Market leading US business travel and meetings event organizer, supplemented by an integrated media offering and additional marketing solutions

Buyer Rationale: Strong market position, entrepreneurially driven, high profitability and growth prospects; US based business with scope to geo-clone against a strategic buyer’s portfolio of events in other industries

Insider View “Connect Meetings is a strong brand, led by an entrepreneurial team with a track record of delivering exceptional growth. There is a great opportunity to quicken that growth further by expansion and replication within the US and other selected territories and to launch into new verticals.”

Douglas Emslie, CEO, Tarsus

acquires

•

•

•

•

End-user, subscription based, recurring revenue streams continue to be in high demand by both strategic and PE acquirers

Lending levels for businesses with high recurring revenues and strong margins are at the top end of the range exceeding 5x.

Driven by data & analytics, financial information is one of the most active verticals Morningstar’s acquisition of Pitchbook for 7x revenue highlights the

continued attraction to subscription driven database platforms Broadridge Financial’s acquisition of Thomson Reuters’ Fiduciary

Services and Competitive Intelligence unit Provides data on investment product classifications, pricing, performance,

benchmarking, product asset positions, and product flows

Leeds acquisition of Covenant Review Credit research, data and analytics firm that pioneered bond and loan covenant research

and analysis; subscription-based model with high renewal and retention rates

20

21

Business Information

($ millions) Valuation Multiples

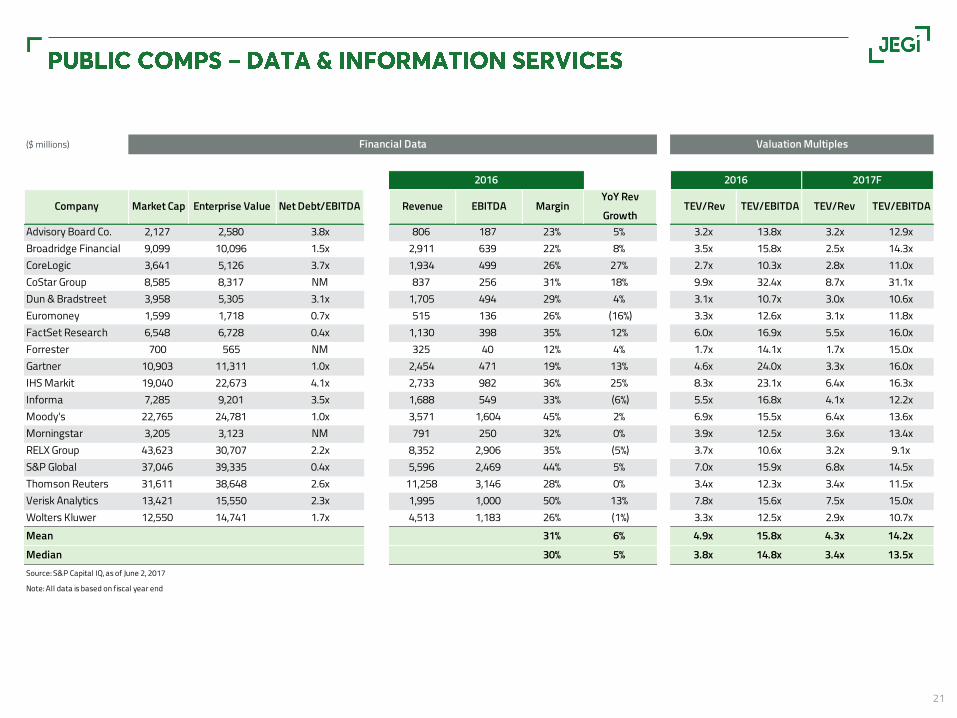

Advisory Board Co. 2,127 2,580 3.8x 806 187 23% 5% 3.2x 13.8x 3.2x 12.9xBroadridge Financial 9,099 10,096 1.5x 2,911 639 22% 8% 3.5x 15.8x 2.5x 14.3xCoreLogic 3,641 5,126 3.7x 1,934 499 26% 27% 2.7x 10.3x 2.8x 11.0xCoStar Group 8,585 8,317 NM 837 256 31% 18% 9.9x 32.4x 8.7x 31.1xDun & Bradstreet 3,958 5,305 3.1x 1,705 494 29% 4% 3.1x 10.7x 3.0x 10.6xEuromoney 1,599 1,718 0.7x 515 136 26% (16%) 3.3x 12.6x 3.1x 11.8xFactSet Research 6,548 6,728 0.4x 1,130 398 35% 12% 6.0x 16.9x 5.5x 16.0xForrester 700 565 NM 325 40 12% 4% 1.7x 14.1x 1.7x 15.0xGartner 10,903 11,311 1.0x 2,454 471 19% 13% 4.6x 24.0x 3.3x 16.0xIHS Markit 19,040 22,673 4.1x 2,733 982 36% 25% 8.3x 23.1x 6.4x 16.3xInforma 7,285 9,201 3.5x 1,688 549 33% (6%) 5.5x 16.8x 4.1x 12.2xMoody's 22,765 24,781 1.0x 3,571 1,604 45% 2% 6.9x 15.5x 6.4x 13.6xMorningstar 3,205 3,123 NM 791 250 32% 0% 3.9x 12.5x 3.6x 13.4xRELX Group 43,623 30,707 2.2x 8,352 2,906 35% (5%) 3.7x 10.6x 3.2x 9.1xS&P Global 37,046 39,335 0.4x 5,596 2,469 44% 5% 7.0x 15.9x 6.8x 14.5xThomson Reuters 31,611 38,648 2.6x 11,258 3,146 28% 0% 3.4x 12.3x 3.4x 11.5xVerisk Analytics 13,421 15,550 2.3x 1,995 1,000 50% 13% 7.8x 15.6x 7.5x 15.0xWolters Kluwer 12,550 14,741 1.7x 4,513 1,183 26% (1%) 3.3x 12.5x 2.9x 10.7xMean 31% 6% 4.9x 15.8x 4.3x 14.2xMedian 30% 5% 3.8x 14.8x 3.4x 13.5xSource: S&P Capital IQ, as of June 2, 2017

Note: All data is based on fiscal year end

TEV/Rev TEV/EBITDA Revenue EBITDA Margin YoY Rev Growth

TEV/Rev TEV/EBITDA

Financial Data

2016 2016 2017F

Company Market Cap Enterprise Value Net Debt/EBITDA

22

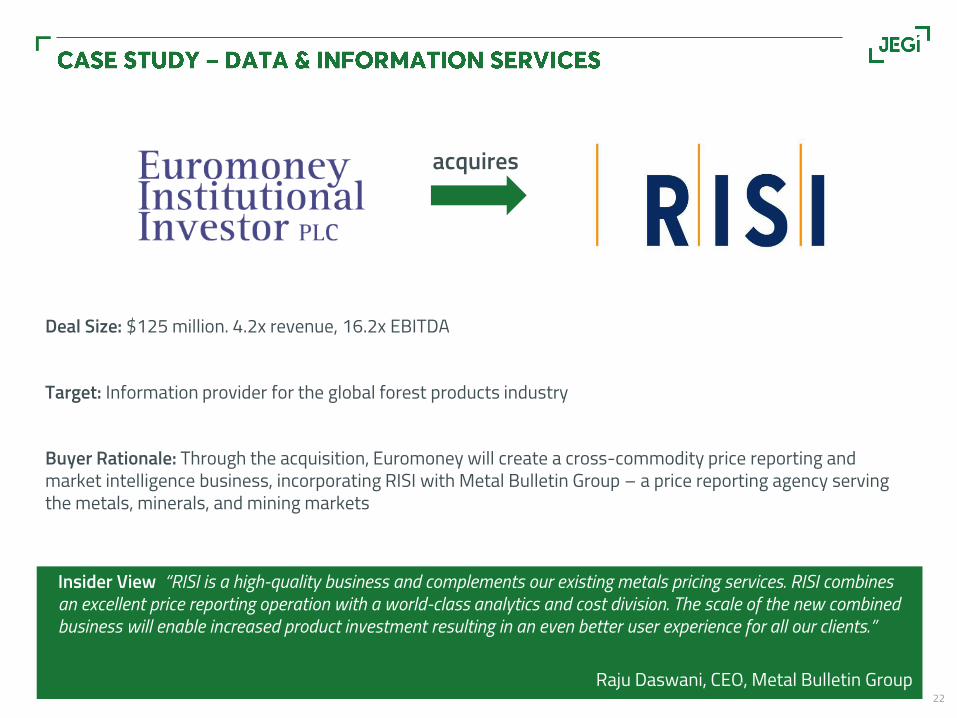

Deal Size: $125 million. 4.2x revenue, 16.2x EBITDA

Target: Information provider for the global forest products industry

Buyer Rationale: Through the acquisition, Euromoney will create a cross-commodity price reporting and market intelligence business, incorporating RISI with Metal Bulletin Group – a price reporting agency serving the metals, minerals, and mining markets

Insider View “RISI is a high-quality business and complements our existing metals pricing services. RISI combines an excellent price reporting operation with a world-class analytics and cost division. The scale of the new combined business will enable increased product investment resulting in an even better user experience for all our clients.”

Raju Daswani, CEO, Metal Bulletin Group

acquires

23

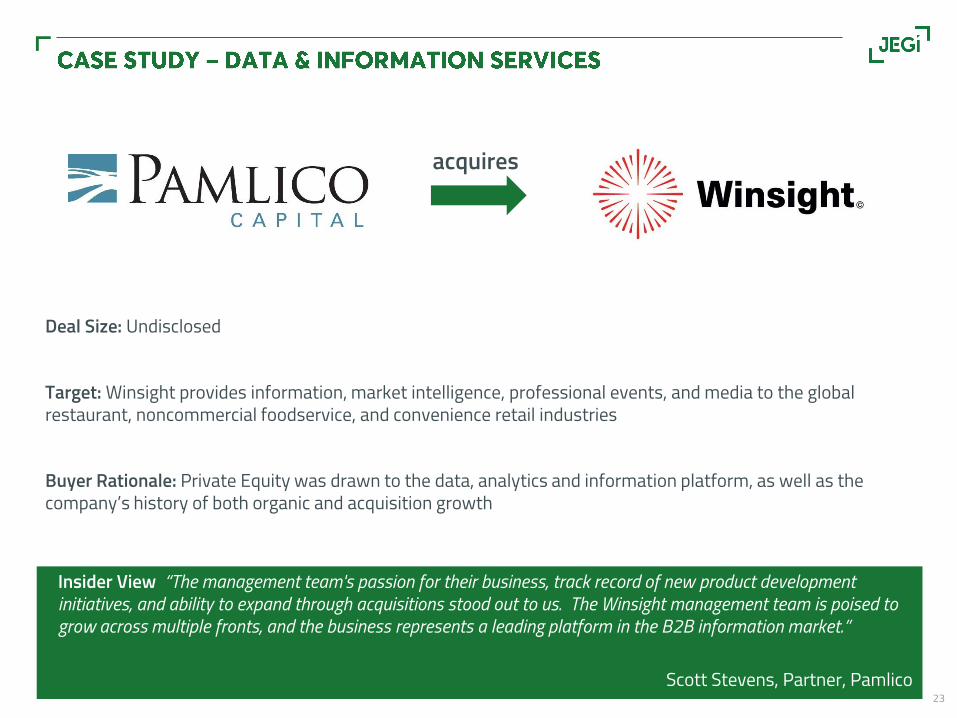

Deal Size: Undisclosed

Target: Winsight provides information, market intelligence, professional events, and media to the global restaurant, noncommercial foodservice, and convenience retail industries

Buyer Rationale: Private Equity was drawn to the data, analytics and information platform, as well as the company’s history of both organic and acquisition growth

Insider View “The management team's passion for their business, track record of new product development initiatives, and ability to expand through acquisitions stood out to us. The Winsight management team is poised to grow across multiple fronts, and the business represents a leading platform in the B2B information market.”

Scott Stevens, Partner, Pamlico

acquires

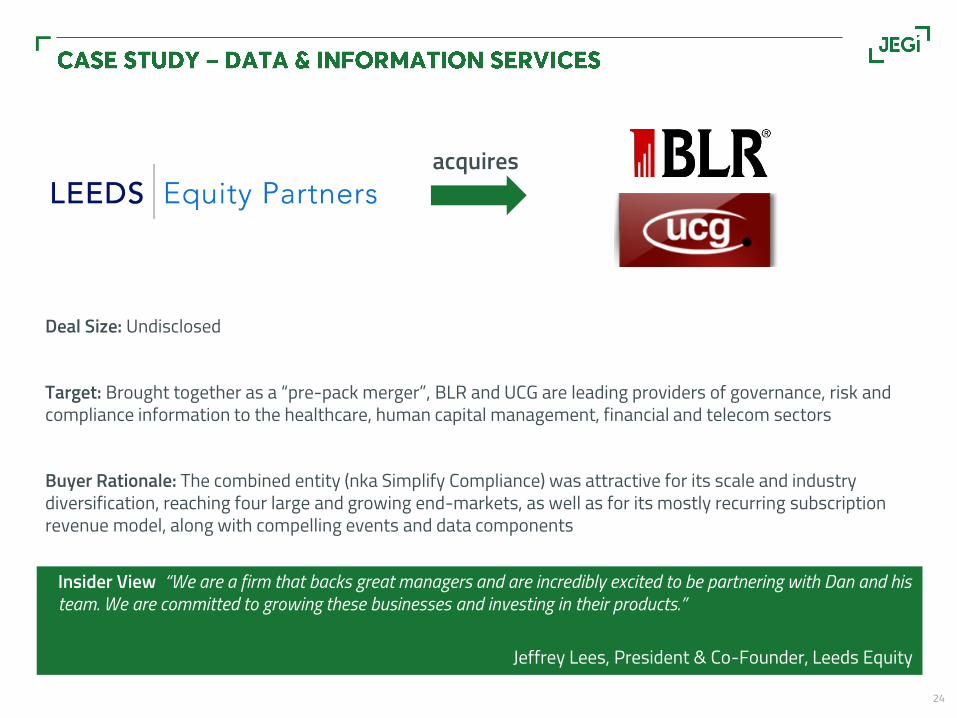

24

Deal Size: Undisclosed

Target: Brought together as a “pre-pack merger”, BLR and UCG are leading providers of governance, risk and compliance information to the healthcare, human capital management, financial and telecom sectors

Buyer Rationale: The combined entity (nka Simplify Compliance) was attractive for its scale and industry diversification, reaching four large and growing end-markets, as well as for its mostly recurring subscription revenue model, along with compelling events and data components

Insider View “We are a firm that backs great managers and are incredibly excited to be partnering with Dan and his team. We are committed to growing these businesses and investing in their products.”

Jeffrey Lees, President & Co-Founder, Leeds Equity

acquires

•

•

•

•

26

Industry that is highly fragmented, with primarily creative and technical professionals, making it ripe for innovation

Significant venture and private equity capital seeking to either fortify the role of “traditional” survey research or build a bridge between research and digital marketing

Signs of a converged and redefined market taking hold, where “Insight and Analytics”, “Customer Experience” and “Market Intelligence” are displacing “research” as the working terms of art

Digital marketing “competing” with market research Proprietary data, behavioral data, transactional & CRM data, media pricing &

consumption data

27

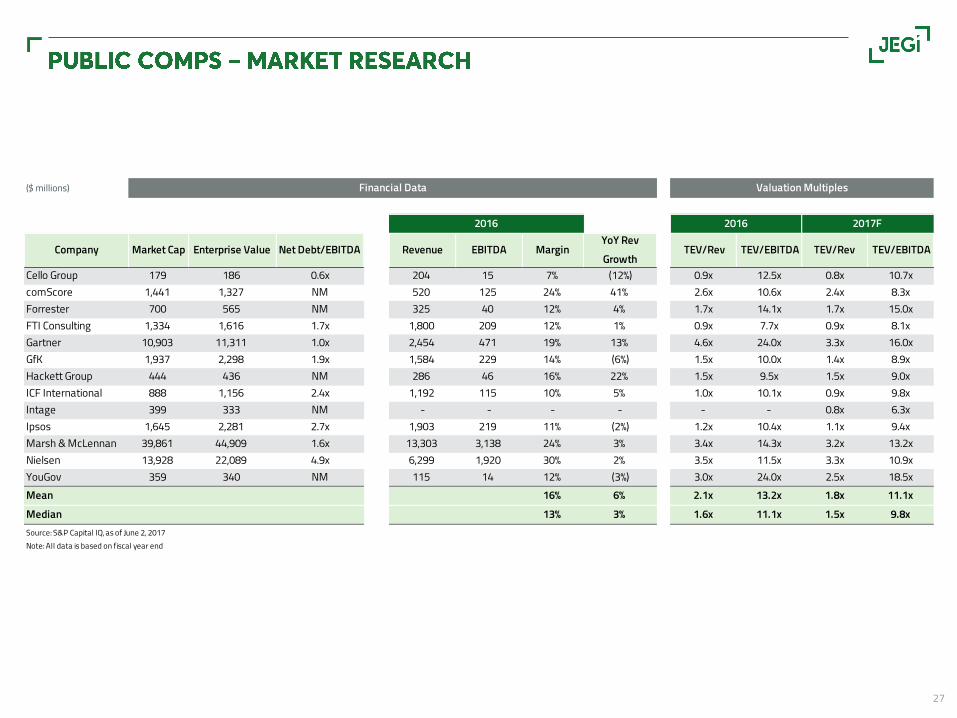

Market Research & Consulting

($ millions) Valuation Multiples

Cello Group 179 186 0.6x 204 15 7% (12%) 0.9x 12.5x 0.8x 10.7xcomScore 1,441 1,327 NM 520 125 24% 41% 2.6x 10.6x 2.4x 8.3xForrester 700 565 NM 325 40 12% 4% 1.7x 14.1x 1.7x 15.0xFTI Consulting 1,334 1,616 1.7x 1,800 209 12% 1% 0.9x 7.7x 0.9x 8.1xGartner 10,903 11,311 1.0x 2,454 471 19% 13% 4.6x 24.0x 3.3x 16.0xGfK 1,937 2,298 1.9x 1,584 229 14% (6%) 1.5x 10.0x 1.4x 8.9xHackett Group 444 436 NM 286 46 16% 22% 1.5x 9.5x 1.5x 9.0xICF International 888 1,156 2.4x 1,192 115 10% 5% 1.0x 10.1x 0.9x 9.8xIntage 399 333 NM - - - - - - 0.8x 6.3xIpsos 1,645 2,281 2.7x 1,903 219 11% (2%) 1.2x 10.4x 1.1x 9.4xMarsh & McLennan 39,861 44,909 1.6x 13,303 3,138 24% 3% 3.4x 14.3x 3.2x 13.2xNielsen 13,928 22,089 4.9x 6,299 1,920 30% 2% 3.5x 11.5x 3.3x 10.9xYouGov 359 340 NM 115 14 12% (3%) 3.0x 24.0x 2.5x 18.5xMean 16% 6% 2.1x 13.2x 1.8x 11.1xMedian 13% 3% 1.6x 11.1x 1.5x 9.8xSource: S&P Capital IQ, as of June 2, 2017Note: All data is based on fiscal year end

TEV/Rev TEV/EBITDA Revenue EBITDA Margin YoY Rev Growth

TEV/Rev TEV/EBITDA

Financial Data

2016 2016 2017F

Company Market Cap Enterprise Value Net Debt/EBITDA

28

Deal Size: $190 million, 2.9x revenue, 11.5x EBITDA

Target: MarketCast is the leading provider of strategic insights and data analytics to marketers and researchers in the global entertainment industry

Buyer Rationale: RLJ bought MarketCast in 2014 for $90 million at 9x EBITDA; from 2014 to 2016, revenue grew from $40 million to $65 million and EBITDA from $10 million to $16.5 million; PE saw an opportunity to partner with management to continue this growth on a strong platform with a broad suite of data-driven products and services and a scalable infrastructure serving the global entertainment marketplace

Insider View “We see tremendous growth opportunities for MarketCast, both organically and through strategic acquisition, and look forward to partnering with management in the next phase of the Company’s development.”

Ahmed I. Wahla, Partner, Kohlberg

acquires

29

Deal Size: $260 million, 5.7x revenue, 19.3x EBITDA

Target: eMarketer provides research on marketing in a digital world; the company aggregates and analyzes information from more than 3,000 global sources and produces data, reports and insights that enable professionals to understand marketing trends and consumer behavior

Buyer Rationale: Traditional German publisher aggressively expanding into digital businesses in English speaking markets; looking to gain audience in the US and strengthen business intelligence and paid subscription revenue model; follows acquisition of Business Insider for $343 million in 2015

Insider View “By acquiring eMarketer, Axel Springer also strengthens its paid content activities and supplements its existing business media. The convincing growth and margin prospects for eMarketer make this transaction another element in Axel Springer’s successful digital transformation.”

Mathias Doepfner, CEO, Axel Springer

acquires

30

Deal Size: Undisclosed

Target: Pioneer in movie marketing research with a key focus on working with the major and independent studios and their home entertainment divisions

Buyer Rationale: NRG is a global leader in Hollywood market research and its product innovation was seen as a key ingredient for success in a rapidly changing entertainment marketing landscape

Insider View “We are excited to welcome NRG into the Stagwell family of companies, and as a market research practitioner for the last 40 years, I'm particularly pleased to add these key capabilities.”

Mark Penn, Managing Partner & President, Stagwell Group

acquires

•

•

•

•

32

Digital marketing, data & technology continue to drive strong valuations, with traditional agencies being at the lower end of value ranges

New market entrants will continue to manifest: Consulting (Deloitte, Accenture, BCG); and Tech Services & Implementation (Cognizant, Valtech, Infosys)

Activity continues to be driven by major agency consolidators – WPP and Dentsu were the two most active acquirers in JEGI’s market in 2016

Major technology companies are in a race to create the digital marketing machine: Marketing, Commerce and Content platforms

Oracle and Salesforce – 16 marketing acquisitions each since 2010; IBM – 13; Adobe – 12;Microsoft – 10; SAP – 5

Experiential marketing and face to face is picking up momentum as marketers are focused on experiences and reaching the consumer directly, rather than strictly online

33

Agencies

($ millions) Valuation Multiples

Aimia 262 364 1.1x 1,703 92 5% (4%) 0.2x 4.0x 0.2x 2.0xAlliance Data Systems 13,242 32,046 12.9x 3,292 1,462 44% (2%) 9.7x 21.9x 4.1x 16.0xDentsu 14,625 13,009 1.4x 7,181 1,501 21% (8%) 1.8x 8.7x 1.5x 7.6xEnero Group 76 54 NM 159 11 7% (3%) 0.3x 4.7x 0.7x 7.4xHavas 4,303 4,153 NM 2,403 386 16% 1% 1.7x 10.7x 1.5x 9.5xHuntsworth 238 279 1.5x 267 27 10% (13%) 1.0x 10.5x 1.1x 8.2xInnerWorkings 599 683 1.9x 1,091 44 4% 6% 0.6x 15.4x 0.6x 10.4xInterpublic Group of Cos. 9,901 11,315 1.0x 7,847 1,098 14% 3% 1.4x 10.3x 1.4x 9.7xM&C Saatchi 351 359 NM 278 15 6% 5% 1.3x 23.3x 1.2x 9.6xMDC Partners 478 1,559 5.8x 1,386 150 11% 4% 1.1x 10.4x 1.0x 7.6xNext Fifteen Comm. 376 392 0.4x 184 24 13% 16% 2.1x 16.6x 1.8x 11.1xOmnicom 19,648 22,878 1.1x 15,417 2,302 15% 2% 1.5x 9.9x 1.5x 9.8xOPT 300 305 NM 598 25 4% 12% 0.5x 12.3x 0.4x 9.9xPublicis 16,975 18,458 0.8x 10,274 1,809 18% (1%) 1.8x 10.2x 1.6x 9.2xSt. Ives 79 170 1.7x 488 46 9% (9%) 0.3x 3.7x 0.4x 3.6xWPP 28,078 33,989 1.6x 17,766 3,131 18% (2%) 1.9x 10.9x 1.7x 10.0xMean 13% 0% 1.7x 11.5x 1.3x 8.8xMedian 12% (0%) 1.4x 10.4x 1.3x 9.6xSource: S&P Capital IQ, as of June 2, 2017

Note: All data is based on fiscal year end

TEV/Rev TEV/EBITDA TEV/Rev TEV/EBITDA Company Market Cap Enterprise Value Net Debt/EBITDA Revenue EBITDA Margin

2017FYoY Rev Growth

Financial Data

2016 2016

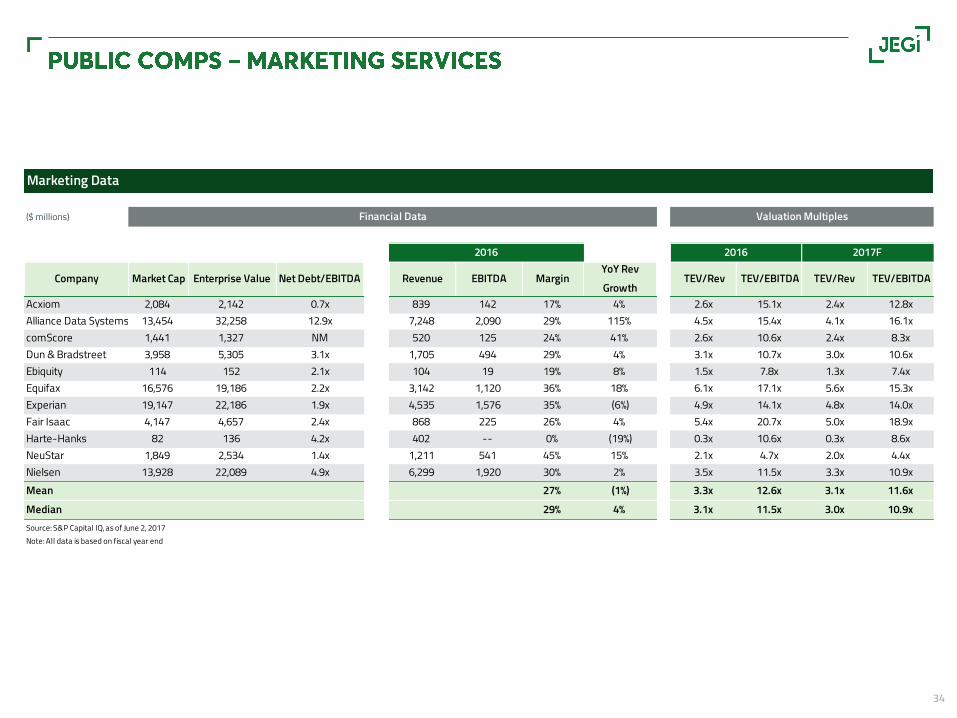

34

Marketing Data

($ millions) Valuation Multiples

Acxiom 2,084 2,142 0.7x 839 142 17% 4% 2.6x 15.1x 2.4x 12.8xAlliance Data Systems 13,454 32,258 12.9x 7,248 2,090 29% 115% 4.5x 15.4x 4.1x 16.1xcomScore 1,441 1,327 NM 520 125 24% 41% 2.6x 10.6x 2.4x 8.3xDun & Bradstreet 3,958 5,305 3.1x 1,705 494 29% 4% 3.1x 10.7x 3.0x 10.6xEbiquity 114 152 2.1x 104 19 19% 8% 1.5x 7.8x 1.3x 7.4xEquifax 16,576 19,186 2.2x 3,142 1,120 36% 18% 6.1x 17.1x 5.6x 15.3xExperian 19,147 22,186 1.9x 4,535 1,576 35% (6%) 4.9x 14.1x 4.8x 14.0xFair Isaac 4,147 4,657 2.4x 868 225 26% 4% 5.4x 20.7x 5.0x 18.9xHarte-Hanks 82 136 4.2x 402 -- 0% (19%) 0.3x 10.6x 0.3x 8.6xNeuStar 1,849 2,534 1.4x 1,211 541 45% 15% 2.1x 4.7x 2.0x 4.4xNielsen 13,928 22,089 4.9x 6,299 1,920 30% 2% 3.5x 11.5x 3.3x 10.9xMean 27% (1%) 3.3x 12.6x 3.1x 11.6xMedian 29% 4% 3.1x 11.5x 3.0x 10.9xSource: S&P Capital IQ, as of June 2, 2017Note: All data is based on fiscal year end

TEV/Rev TEV/EBITDA Revenue EBITDA Margin YoY Rev Growth

TEV/Rev TEV/EBITDA

Financial Data

2016 2016 2017F

Company Market Cap Enterprise Value Net Debt/EBITDA

35

Deal Size: $150 million, 2.5x revenue

Target: Provides sales and marketing professionals with actionable market and company information enhanced by software

Buyer Rationale: Avention’s software offerings enhance D&B’s positioning to serve its core markets, supplementing D&B’s foundational company and contact data

Insider View “The Sales Acceleration space offers a big opportunity for Dun & Bradstreet. We believe, as the global leader in commercial information, we are well positioned to take market share and accelerate our growth strategy.”

Bob Carrigan, CEO, D&B

acquires

36

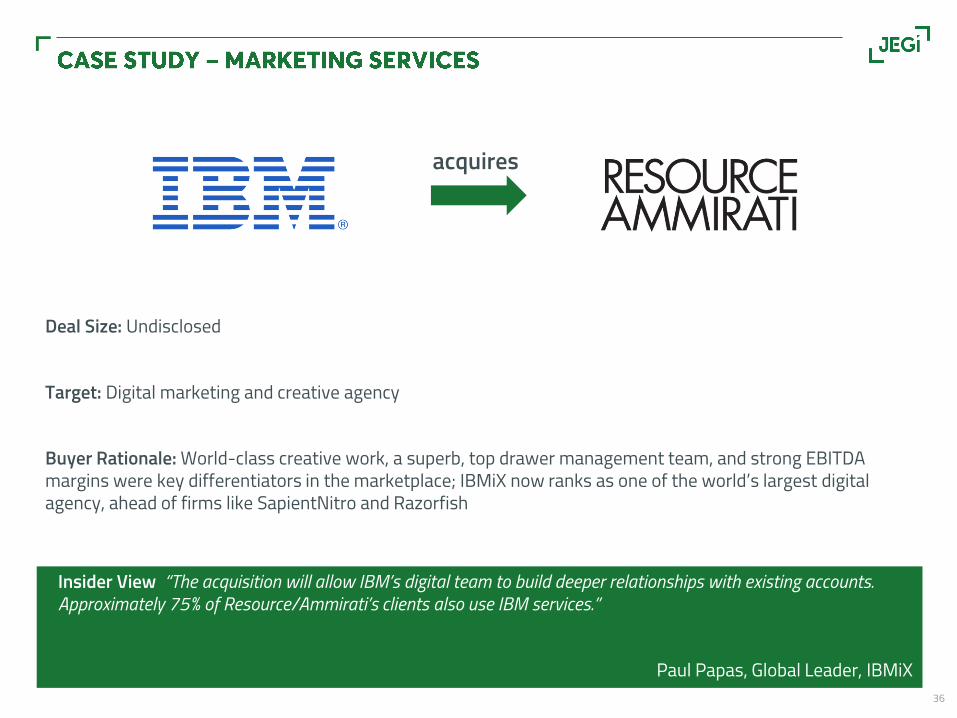

Deal Size: Undisclosed

Target: Digital marketing and creative agency

Buyer Rationale: World-class creative work, a superb, top drawer management team, and strong EBITDA margins were key differentiators in the marketplace; IBMiX now ranks as one of the world’s largest digital agency, ahead of firms like SapientNitro and Razorfish

Insider View “The acquisition will allow IBM’s digital team to build deeper relationships with existing accounts. Approximately 75% of Resource/Ammirati’s clients also use IBM services.”

Paul Papas, Global Leader, IBMiX

acquires

37

Deal Size: $413 million, undisclosed multiples

Target: Provides “Private Brand” products with marketing strategy, including branding, sourcing & logistics, retail merchandising services and consumer experience

Buyer Rationale: PE was drawn to the Asian market, as well as the Company’s scale, its leading global market position and its impressive track record of consistent revenue growth

Insider View “We are thrilled to join forces with Daymon and look forward to working with them on the many growth opportunities this transaction will bring in the U.S. and Asia’s emerging economies.”

Jonathan Zhu, Managing Director, Bain Capital

acquires

•

•

•

•

39

Take into account the relative

cultures of the organizations

Ensure that the key market-facing players will continue with the business

at least long enough to transition domain expertise and relationships

Understand the role and importance of the founders/sellers

Be open to exploring different options for organizational structures and processes

Incentivize key personnel to

align objectives

Expect IT integration across platforms to take longer

than anticipated

Consider town hall meeting with new

employees to deliver message and strategy

Strike the right balance between granting

autonomy and centralizing operations

Give full attention to the communications strategy and look to control the message to

key stakeholders

40

+ Potential tax holiday+ Proposed lower corporate tax rates

+ Pro-business+ GOP platform potentially good for M&A

- Policies likely to drive up costs for US companies- Could impact international deals- Limited experience and bombast could have

negative impact+ Repatriation of capital = greater investment/M&A

+ Low interest rate environment- Projected future rate increases

+ Slow growth economy encourages inorganic growth+ Acquisitions add talent, scale and synergies+ Divestiture of slow-growth assets = greater M&A

+ Dow 20K+ = CEO confidence+ Strong strategic valuations+ Lots of cash on balance sheets

•

•

•

•

42

Managing Director

Founder & CEO Co-President

Managing Director

Managing Director

New York/Boston

Partner Partner Partner

London/Sydney

Managing Director Managing Director

Managing Director

Managing Director BD Director COODirector

Managing Director

Senior AdvisorManaging DirectorManaging Director CMO COO EVPDirector Managing Director

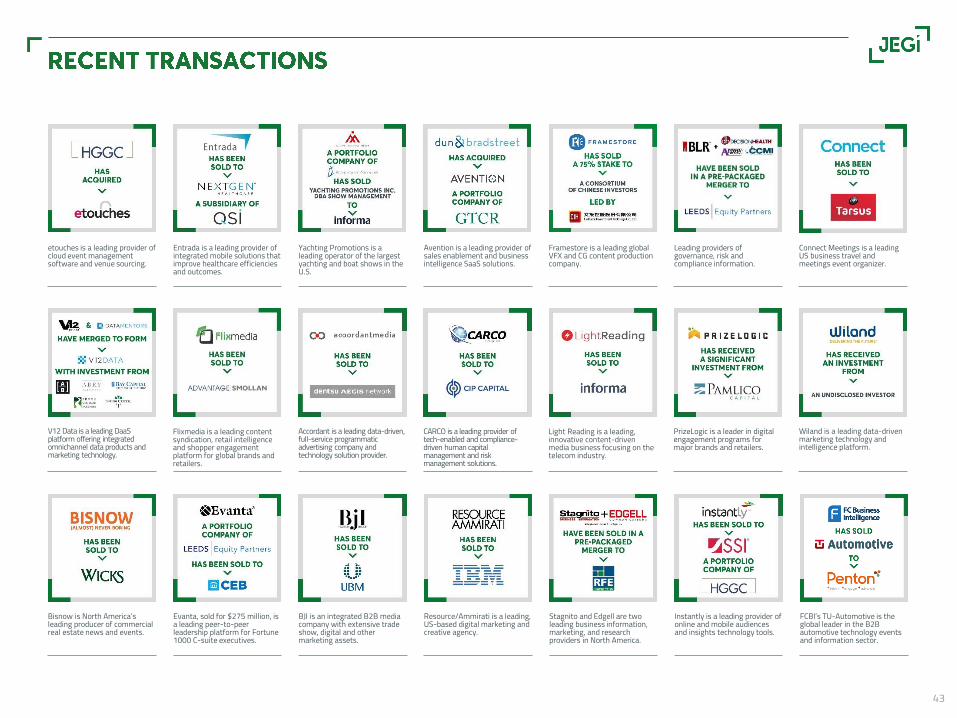

Avention is a leading provider of sales enablement and business intelligence SaaS solutions.

43

Leading providers of governance, risk and compliance information.

Stagnito and Edgell are two leading business information, marketing, and research providers in North America.

Resource/Ammirati is a leading, US-based digital marketing and creative agency.

Instantly is a leading provider of online and mobile audiences and insights technology tools.

FCBI’s TU-Automotive is the global leader in the B2B automotive technology events and information sector.

Entrada is a leading provider of integrated mobile solutions that improve healthcare efficiencies and outcomes.

Yachting Promotions is a leading operator of the largest yachting and boat shows in the U.S.

Flixmedia is a leading content syndication, retail intelligence and shopper engagement platform for global brands and retailers.

BJI is an integrated B2B media company with extensive trade show, digital and other marketing assets.

Evanta, sold for $275 million, is a leading peer-to-peer leadership platform for Fortune 1000 C-suite executives.

Bisnow is North America’s leading producer of commercial real estate news and events.

Wiland is a leading data-driven marketing technology and intelligence platform.

PrizeLogic is a leader in digital engagement programs for major brands and retailers.

Light Reading is a leading, innovative content-driven media business focusing on the telecom industry.

CARCO is a leading provider of tech-enabled and compliance-driven human capital management and risk management solutions.

Accordant is a leading data-driven, full-service programmatic advertising company and technology solution provider.

Connect Meetings is a leading US business travel and meetings event organizer.

V12 Data is a leading DaaS platform offering integrated omnichannel data products and marketing technology.

Framestore is a leading global VFX and CG content production company.

etouches is a leading provider of cloud event management software and venue sourcing.

44

AMER

ICAS

UK

Select cross-border transactions, leveraging our US, European and Australian offices

ASIA

-PAC

IFIC

EMEA

45

Serving founders and entrepreneurs, VC and Private Equity investors, and global corporations

Positioned at the center of converging markets, bringing strategic advice and creative ideas to its clients

Deep knowledge of markets served, providing unexpected acquisition and investment opportunities

Track record of surpassing client expectations

46

BOSTONJEGI, 50 Milk Street 16th FloorBoston, MA 02109+1 617 294 6555www.jegi.com

LONDONClarity, 90 Long AcreLondon, WC2E 9RA+44 20 3402 4900www.claritycp.com

NEW YORKJEGI, 150 East 52nd Street 18th Floor New York, NY 10022+1 212 754 0710www.jegi.com

SYDNEYClarity, 100 Barangaroo AvenueSydney NSW 2000+61 2 8046 6840www.claritycp.com