jean-luc michel, head of global commercial development, merial

TRANSCRIPT

M E R I A L A N I M A L H E A L T H

©Merial 2016. All rights reserved. Information contained in this document is

indicative only. It is provided without liability and is subject to change

without notice

GLOBAL CHALLENGES & DRIVERS FOR ANIMAL HEALTH

Jean-Luc Michel, Head of Global

Commercial Development

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

5 continents

R&D

locations 13

750+ scientists

MERIAL – A DISTINGUISHED LEGACY OF CARE AND INNOVATION

Employees worldwide

+

manufacturing sites

R&D centers

15 13

6,900

Present in

countries worldwide 150

8 countries

Manufacturing

manufacturing sites 15

2,800+ employees >2,5 billion in sales in 2015

€

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

Demographic Growth

Environmental Changes

THE GLOBAL TRENDS SHAPING TOMORROW

Sources: United Nations; Grant Thornton International Business Report 2015; OCDE; Roland Berger; McKinsey; World Development Indicators

Social

Health Wellness

Economic

Increasing Urbanization

Globalization Digitization

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

MAJOR DEMOGRAPHIC TRENDS BY 2050

Worldwide Population (in Billions)

Source: INED, World Population Prospects. United Nations. 2015

7,349

2015 2050

9,725 +32%

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

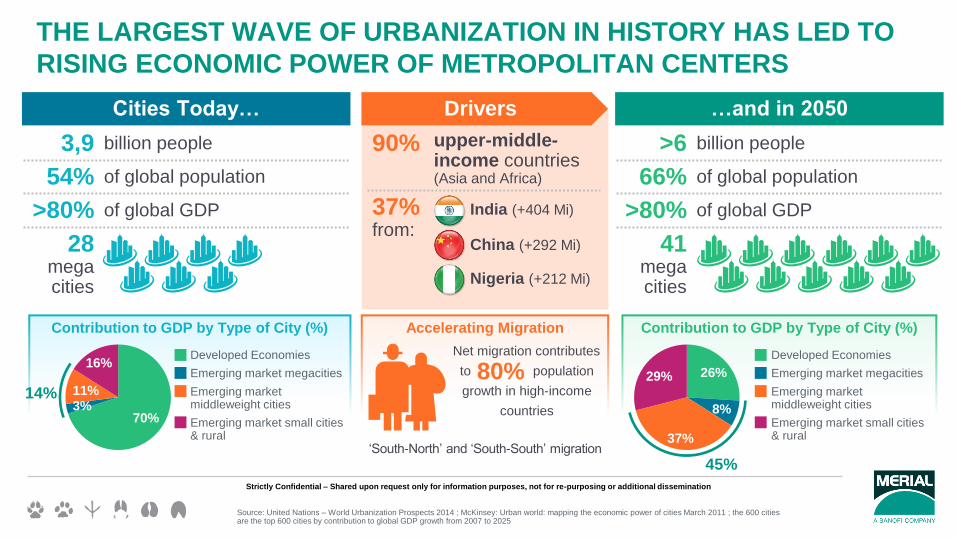

>6 billion people

66% of global population

>80% of global GDP

41 mega cities

Contribution to GDP by Type of City (%) Contribution to GDP by Type of City (%)

3,9 billion people

54% of global population

>80% of global GDP

28 mega cities

Cities Today…

THE LARGEST WAVE OF URBANIZATION IN HISTORY HAS LED TO

RISING ECONOMIC POWER OF METROPOLITAN CENTERS

70% 3% 11%

16% Developed Economies

Emerging market megacities

Emerging market middleweight cities

Emerging market small cities & rural

Source: United Nations – World Urbanization Prospects 2014 ; McKinsey: Urban world: mapping the economic power of cities March 2011 ; the 600 cities are the top 600 cities by contribution to global GDP growth from 2007 to 2025

…and in 2050

26%

8%

37%

29%

Developed Economies

Emerging market megacities

Emerging market middleweight cities

Emerging market small cities & rural

45%

Drivers

90% upper-middle-income countries (Asia and Africa)

37% from:

India (+404 Mi)

China (+292 Mi)

Nigeria (+212 Mi)

Accelerating Migration

Net migration contributes

to population

growth in high-income

countries

80%

‘South-North’ and ‘South-South’ migration

14%

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

SHIFTING WORLD TO DEVELOPING ECONOMIES:

DOMINATION OF THE TOP 3 ECONOMIES, RISE OF ASIA

Source: The Economist Intelligence Unit Limited 2015 ;1: The globalist MGI CompanyScope; McKinsey Global Institute Analysis; World Development Indicators, The World Bank

Top Ten Economies in 2050 at Market Exchange Rate

Rise of Asia Geographical Base of the Fortune 500 Global Companies

0%

20%

40%

60%

80%

100%

2001-10 2011-18 2019-30 2031-40 2041-50

Reg

ion

al S

ha

re o

f G

lob

al G

DP

Africa & Middle East

Europe

Americas

Asia-Pacific

2015 Nominal GDP (US$ Trillions) Rise of Asia…

• China’s Economy will be larger than U.S. by 2028 when measured at market exchange rates(1), but it has been larger since 2014, when adjusted for purchasing power (IMF), real growth average 7%

• India 3rd, real growth average 5%

• Indonesia and Mexico leap into top ten

Newly Emerging Economies:

• Nigeria, Vietnam, Colombia, Poland, Malaysia, Chile, Peru, Mexico, Philippines

…Collectively Rich, Not So Individually

• Looking at individual spending power, Western advanced economies are likely to continue to dominate (2015 GDP/capita USA 54 kUSD vs. China 7,6 kUSD)

US

$17.9 China

$10.8 Japan

$4.1 Germany

$3.3 UK

$2.8 France

$2.4 Brazil

$1.7 Italy

$1.8 India

$2.0 Russia

$1.3

China

$105.9 US

$70.9 India

$63.8 Indonesia

$15.4 Japan

$11.4 Germany

$11.3 Brazil

$10.3 Mexico

$9.8 UK

$9.8 France

$9.7

2050 Nominal GDP (US$ Trillions)

Developed Emerging

415

271

54

120

10

34

8

26

8

11 4

12

1 26

2010 2025

Africa and Middle East

Southeast Asia

South Asia

Eastern Europe & Central Asia

Latin America

China

Developed

Emerging countries: From 85 companies in 2010, up to 230 in 2025

Emerging

Developed

500 500

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

DIGITAL IS ALSO DRIVING FUNDAMENTAL CHANGES IN OUR

INDUSTRY, ACROSS ALL VERTICALS

Source: WE Forum

Business New markets (on-line marketplace, car-hire

schemes, vacation like a local, etc.)

Education Connecting neglected and underserved

communities around the world

Advanced management system New job, home-based work, connected

plant

Health Tailor medical approaches to an

individual’s lifestyle and genetic profile

Opportunities

Social Economic

Technologic

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

DIGITIZATION : AN UNPRECEDENTED TRANSFORMATION!

Happening on the web in 60 seconds…

Any Time

Any Device

Any Content

Any Where

Web sites & Apps:

Responsive Design

Security system for

confidentiality

Infrastructure: cloud

Connected Objects

Referential: Master Data

Management

Exploit Data: Big data

WHO?

GAFA (Google, Amazon, Facebook, Apple), Netflix,

Spotify, Chronodrive, Dropbox…

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

ASIA HAS THE LARGEST BASE OF INTERNET USERS

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

…… AND THE LARGEST BASE OF SOCIAL MEDIA ACCOUNTS

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

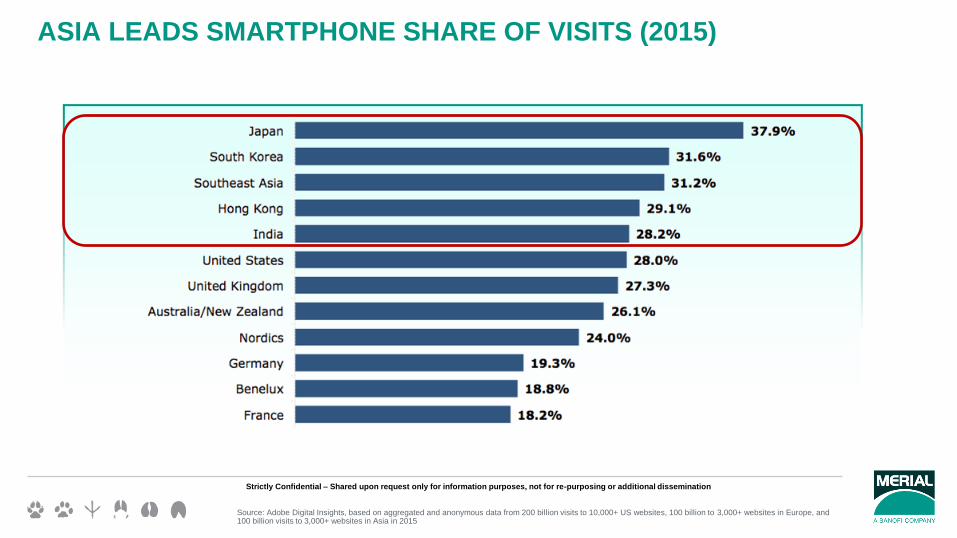

ASIA LEADS SMARTPHONE SHARE OF VISITS (2015)

Source: Adobe Digital Insights, based on aggregated and anonymous data from 200 billion visits to 10,000+ US websites, 100 billion to 3,000+ websites in Europe, and 100 billion visits to 3,000+ websites in Asia in 2015

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

HOW MUCH ONLINE SHOPPERS AROUND THE WORLD ARE SPENDING

Over the past few years, online shopping has become increasingly popular around the world.

In markets such as the United Kingdom, Japan and Germany, e-commerce penetration has already climbed past 70% of

the adult population, and emerging markets such as Brazil and China are seeing rapid growth in online shopping

adoption.

Source: Statista Digital Market Outlook, Estimated average e-commerce revenue per online shopper in 2015

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

End of one-size-fits-all Safer, Faster, Less invasive,

Cost-Effective

Wellness Program, Consumer Medicines, Digitized medicine

Adapt life style, Care Delivery provided in or near the home

Biomarkers, Diagnosis Tools, Big Data

ALL THESE CHANGES AND TRENDS HAVE RESULTED IN AN EVER-GROWING

PARADIGM SHIFT IN HEALTH – PREVENTION TAKING OVER TREATMENT

Demographic Urbanization Global Warming

Cultural Change

Globalization Economic Digitization

The 4P

Predictive Personalized Preventive Participative

Direct Impact of Global Trends

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

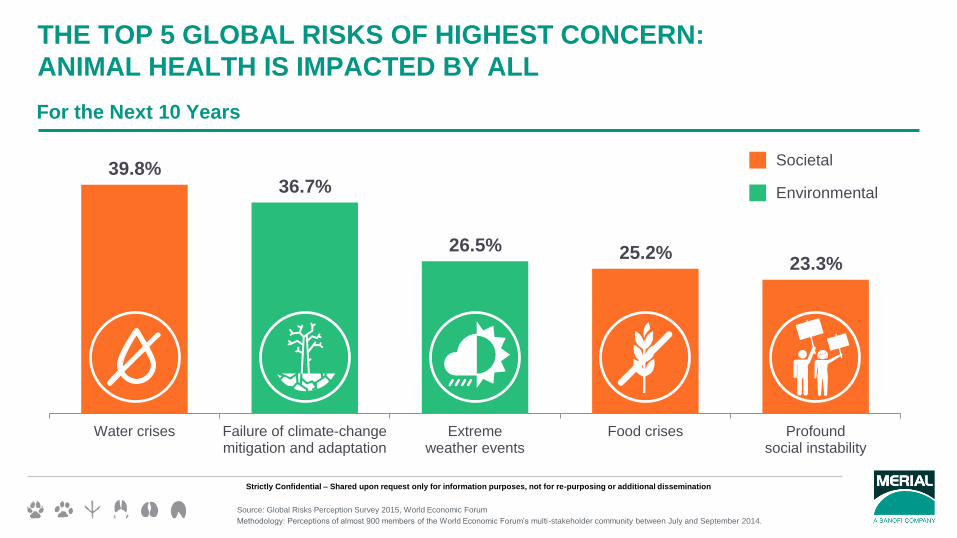

THE TOP 5 GLOBAL RISKS OF HIGHEST CONCERN:

ANIMAL HEALTH IS IMPACTED BY ALL

Source: Global Risks Perception Survey 2015, World Economic Forum

Methodology: Perceptions of almost 900 members of the World Economic Forum’s multi-stakeholder community between July and September 2014.

39.8% 36.7%

26.5% 25.2% 23.3%

Water crises Failure of climate-changemitigation and adaptation

Extremeweather events

Food crises Profoundsocial instability

Societal

Environmental

For the Next 10 Years

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

Demographic Growth

Environmental Changes

THE GLOBAL TRENDS SHAPING TOMORROW

Sources: United Nations; Grant Thornton International Business Report 2015; OCDE; Roland Berger; McKinsey; World Development Indicators

Social

Health Wellness

Economic

Increasing Urbanization

Globalization Digitization

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

SOME WILL HAVE GREATER IMPACT ON OUR INDUSTRY

Growing middle class globally

Increasing demand for protein

Humanization of pets

Growing cluster of animal health start-ups

Regulation and surveillance of antibiotic use

One Health

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

Feed 2.5Bn additional people

Younger population

Growing Middle class

in Emerging markets

Healthier Planet

Sustainable development

Fair trade

Productivity (less waste)

Healthier Animals

Animal Welfare

Prevention rather than cure

Regulatory Excellence (ex. Ab)

Healthier People

Food safety

Transparency (social media)

Regulatory Excellence

Value added services

Globalization

Emergence of new markets

Changing World demographics

Business consolidations

Emergence of different business models (niche, local)

Emergence of new diseases

Social media

Digital Technology

Information technology

Nano-technology

Bio Technologies

Delivery

Food industry

Product transformation (convenience / lifestyle)

Customer centric

Services

Productivity enhancing Tech

Lower median income

Industry productivity driven

Price pressure

Constraints of arable land

Animal feed supply

Water shortage

Energy supply

Labor cost and resources

DESPITE CHALLENGES, OUR INDUSTRY IS ADAPTING TO GLOBAL

TRENDS THROUGH IMPROVED ANIMAL HEALTH & PRODUCTIVITY

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

OUR INDUSTRY REMAINS BUOYANT – HERE ARE SOME OF THE

REASONS WE CONTINUE TO BE EXCITED ABOUT ANIMAL HEALTH

RECESSION-RESILIENT SECTOR – annual growth of 4–5% near/long term

Need for PROTEIN, growing global MIDDLE CLASS and HUMANIZATION of pets

Climate and shifting prevalence in zoonotic and trans-boundary diseases, supporting ‘ONE HEALTH’ approach

GROWING CLUSTER OF ANIMAL HEALTH START-UPS in companion animals and the food animal sector

FIRMS EXPERIENCING GOOD UNDERLYING GROWTH despite currency issues – boosted by new pet products and existing strong food animal brands

STILL LOTS OF UNMET NEEDS and areas that require next-gen treatments, e.g., mastitis, pet cancer, biologics

Antimicrobial reduction stoking INNOVATION FOR ALTERNATIVES

1

2

3

4

5

6

7

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

VALUE DRIVERS AND TRENDS IMPACTING THE INDUSTRY

Value Driver Category Key Value Drivers Key Trends

Innovation • R&D for new chemical entities (NCE)

• Lifecycle strategies • Declining R&D productivity has led to highly mature

product portfolios

Portfolio Advantage & Commercial Excellence

• Growing demand

• Relative power in AH value chain

• Economies of scale in commercial (direct sales)

• Branding

• Customer loyalty

• Product-portfolio-led economies of scope (share of wallet)

• Effective channel management

• There are limited opportunities for leading players to grow through further industry consolidation

• Increased downstream consolidation in the Production Animal value chain has weakened AH’s position

• Vets are less influential in purchase decisions

• Technological innovations and growth of new adjacencies may be considered in growth plans

Competitive Forces • Industry structure and competitive intensity

• New entrants

• Branded sales could be threatened by growth of generics and OTC/private label products, driven by regulatory changes in the U.S. and E.U., plus channel shift in Companion Animal segment

Operational Effectiveness

• Manufacturing and supply chain quality and efficiency

• Profit pressure could be increasing

• Increasingly global food producers require global operating structures

Regulation • Product exclusivity regulations and regulatory

process

Source: PwC analysis

1

2

3

4

5

Strictly Confidential – Shared upon request only for information purposes, not for re-purposing or additional dissemination

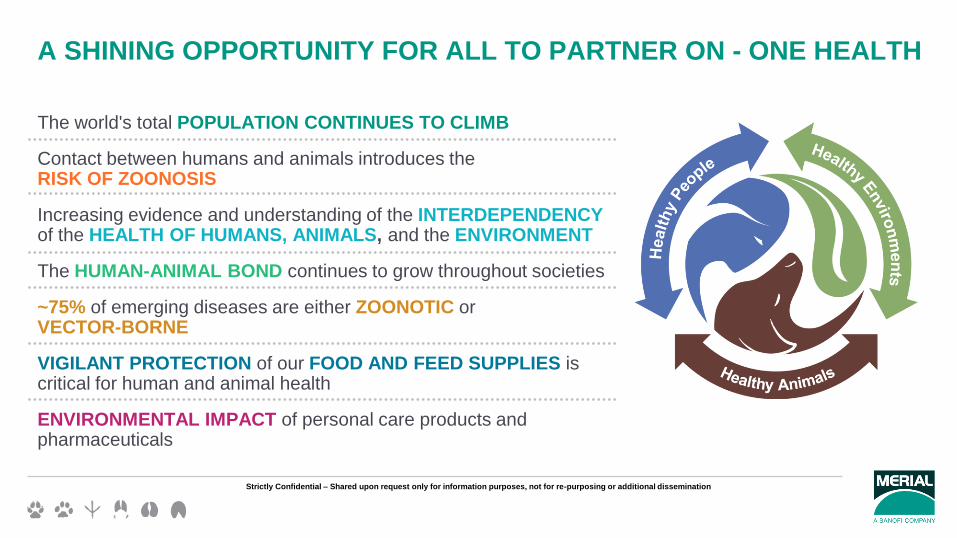

A SHINING OPPORTUNITY FOR ALL TO PARTNER ON - ONE HEALTH

The world's total POPULATION CONTINUES TO CLIMB

Contact between humans and animals introduces the RISK OF ZOONOSIS

Increasing evidence and understanding of the INTERDEPENDENCY of the HEALTH OF HUMANS, ANIMALS, and the ENVIRONMENT

The HUMAN-ANIMAL BOND continues to grow throughout societies

~75% of emerging diseases are either ZOONOTIC or VECTOR-BORNE

VIGILANT PROTECTION of our FOOD AND FEED SUPPLIES is critical for human and animal health

ENVIRONMENTAL IMPACT of personal care products and pharmaceuticals