jennie price

DESCRIPTION

Jennie Price. Chief Executive Sport England. Sport and Recreation Alliance Conference Delivering Government’s priorities for sport. Government’s current priorities What we have learnt Future direction of travel The Big Society – how does it fit in. Government’s current priorities. - PowerPoint PPT PresentationTRANSCRIPT

1

Jennie PriceChief ExecutiveSport England

Sport and Recreation Alliance Conference

Delivering Government’s priorities for sport

2

• Government’s current priorities

• What we have learnt

• Future direction of travel

• The Big Society – how does it fit in

3

Government’s current priorities

4

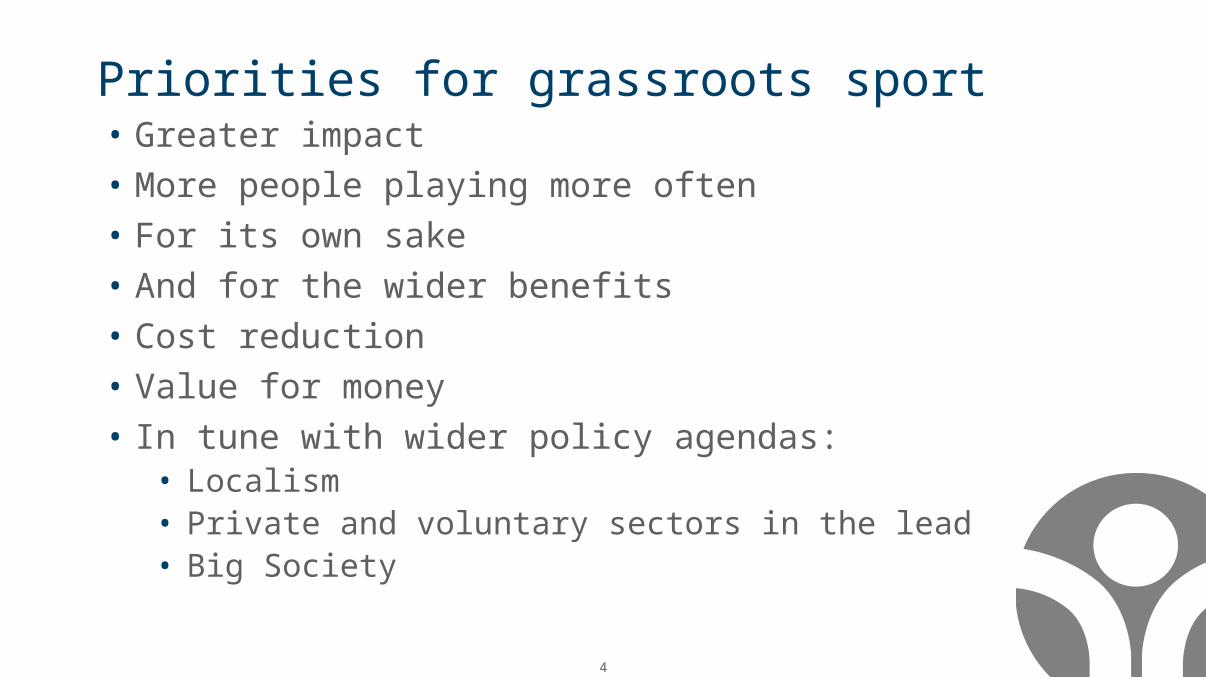

Priorities for grassroots sport• Greater impact

• More people playing more often

• For its own sake

• And for the wider benefits

• Cost reduction

• Value for money

• In tune with wider policy agendas:• Localism• Private and voluntary sectors in the lead• Big Society

5

Signals in the Comprehensive Spending Review

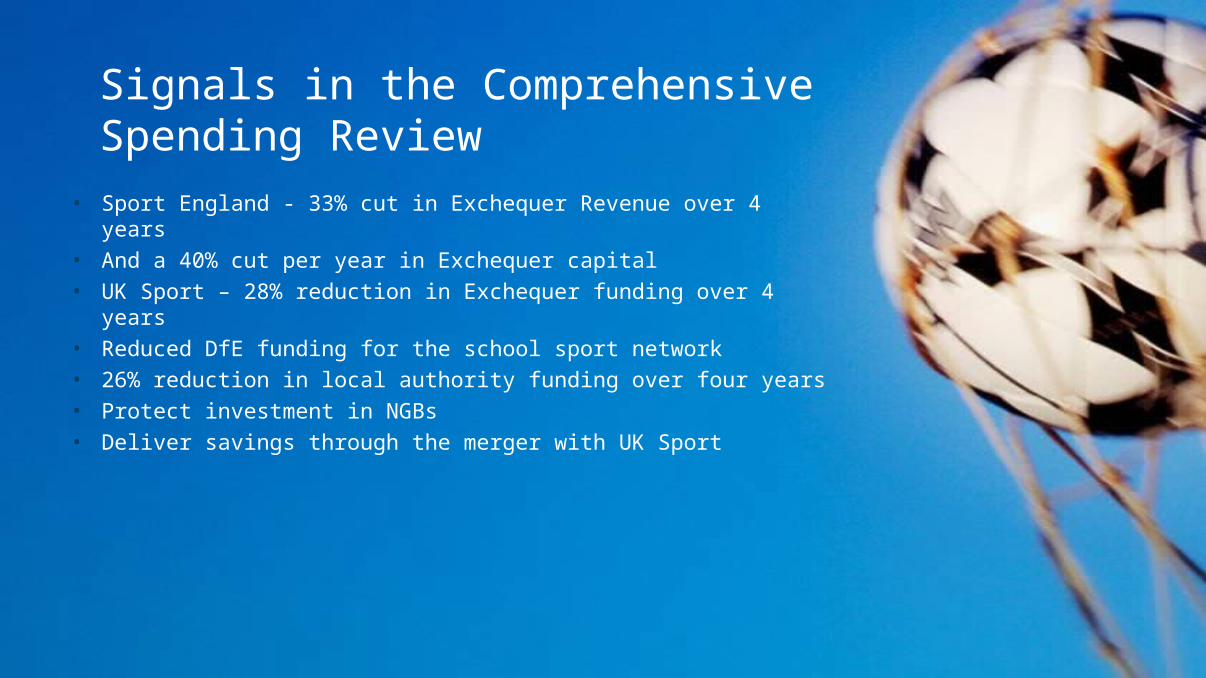

• Sport England - 33% cut in Exchequer Revenue over 4 years• And a 40% cut per year in Exchequer capital• UK Sport – 28% reduction in Exchequer funding over 4 years• Reduced DfE funding for the school sport network • 26% reduction in local authority funding over four years• Protect investment in NGBs• Deliver savings through the merger with UK Sport

6 6

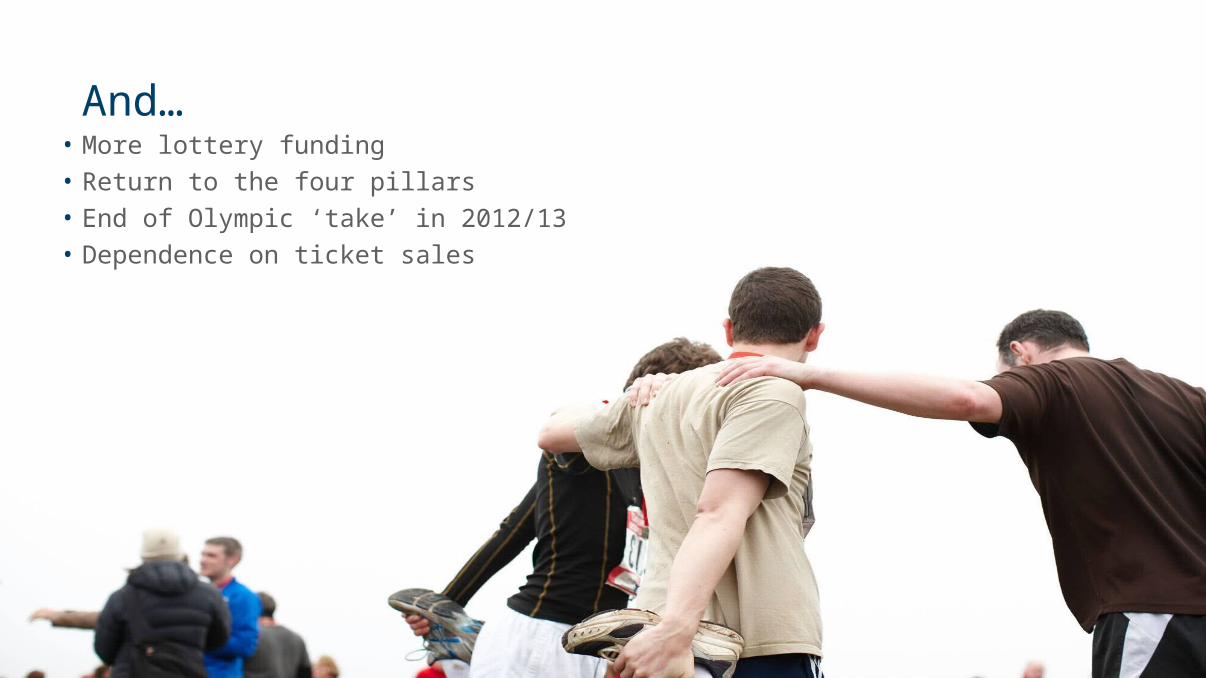

And…• More lottery funding• Return to the four pillars• End of Olympic ‘take’ in 2012/13• Dependence on ticket sales

7

More broadly• Structural changes in the NHS• No RDAs• Fewer cross Departmental programmes• Less money in the third sector

8

Participation: what we have learnt

9

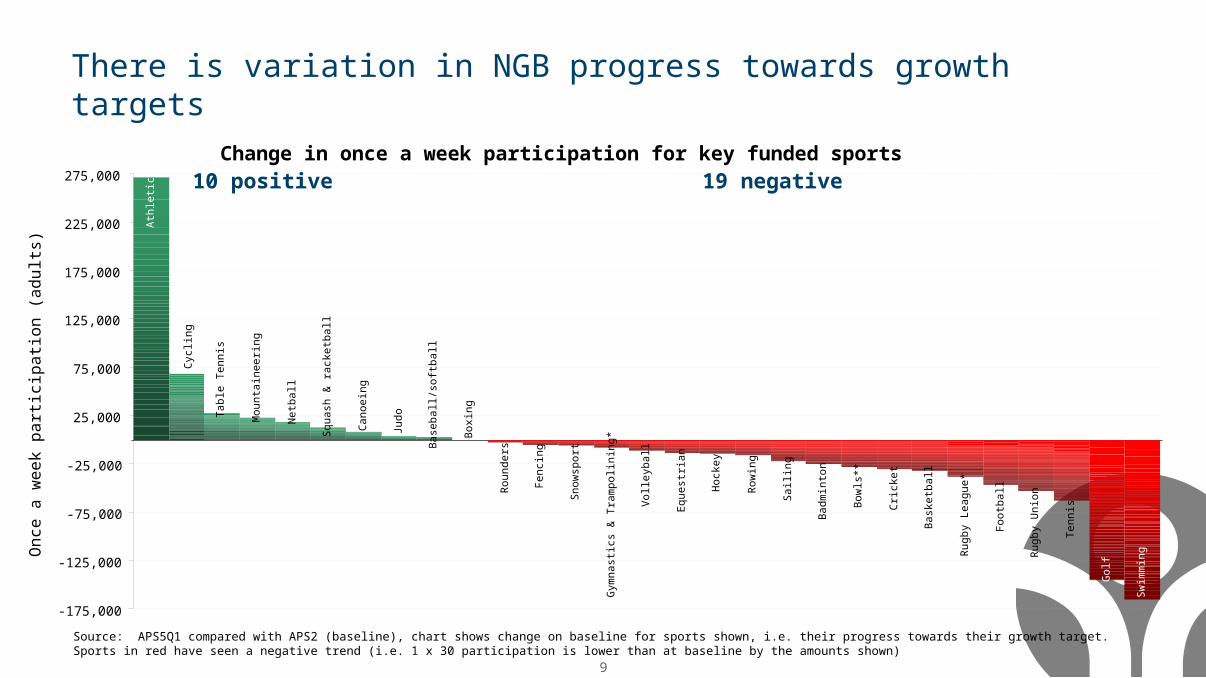

Source: APS5Q1 compared with APS2 (baseline), chart shows change on baseline for sports shown, i.e. their progress towards their growth target. Sports in red have seen a negative trend (i.e. 1 x 30 participation is lower than at baseline by the amounts shown)

On

ce a

we

ek

pa

rtic

ipa

tion

(a

du

lts)

Change in once a week participation for key funded sports

-175,000

-125,000

-75,000

-25,000

25,000

75,000

125,000

175,000

225,000

275,000

There is variation in NGB progress towards growth targets

Tab

le T

enni

s

Mou

ntai

neer

ing

Net

ball

Squ

ash

& r

acke

tbal

l

Can

oein

g

Judo

Bas

ebal

l/sof

tbal

l

Box

ing

Cyc

ling

Ath

letic

s 10 positive 19 negative

Rou

nder

s

Fen

cing

Sno

wsp

ort

Gym

nast

ics

& T

ram

polin

ing*

Vol

leyb

all

Equ

estr

ian

Hoc

key

Row

ing

Sai

ling

Bad

min

ton

Bow

ls**

Cric

ket

Bas

ketb

all

Rug

by L

eagu

e*

Foo

tbal

l

Rug

by U

nion

Ten

nis

Gol

f

Sw

imm

ing

10

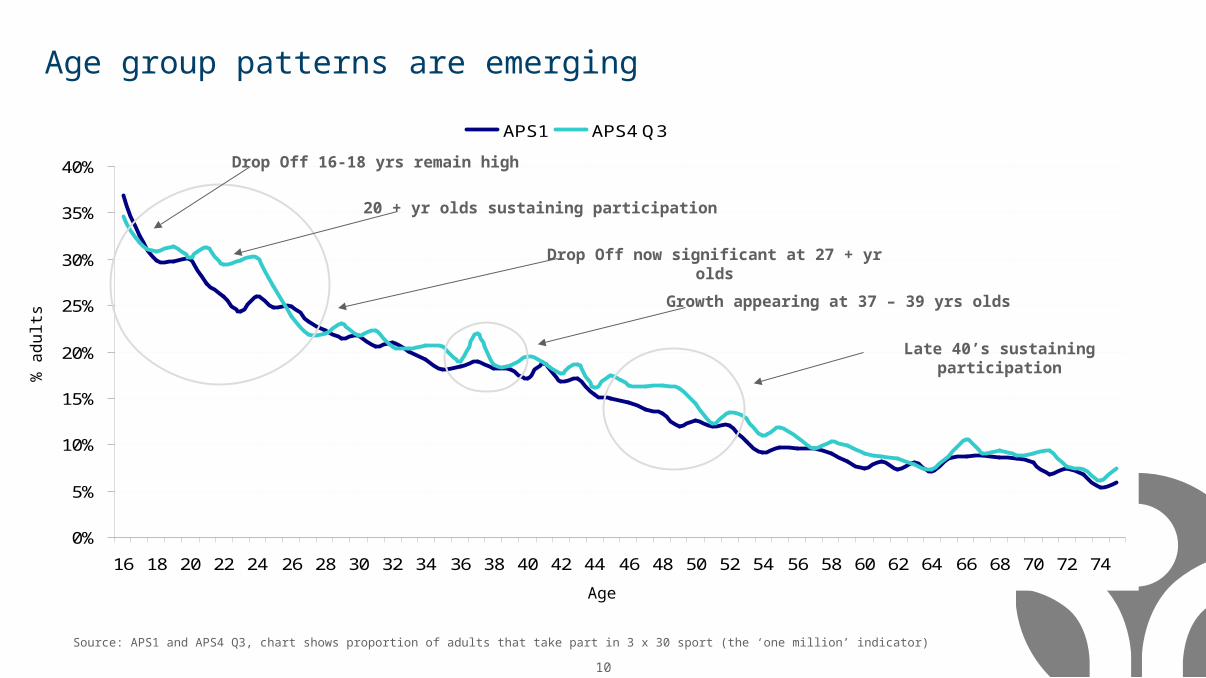

Age group patterns are emerging

0%

5%

10%

15%

20%

25%

30%

35%

40%

16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60 62 64 66 68 70 72 74

APS1 APS4 Q3

Drop Off 16-18 yrs remain high

20 + yr olds sustaining participation

Drop Off now significant at 27 + yr olds

Growth appearing at 37 – 39 yrs olds

Late 40’s sustaining participation

% a

du

lts

Age

Source: APS1 and APS4 Q3, chart shows proportion of adults that take part in 3 x 30 sport (the ‘one million’ indicator)

11

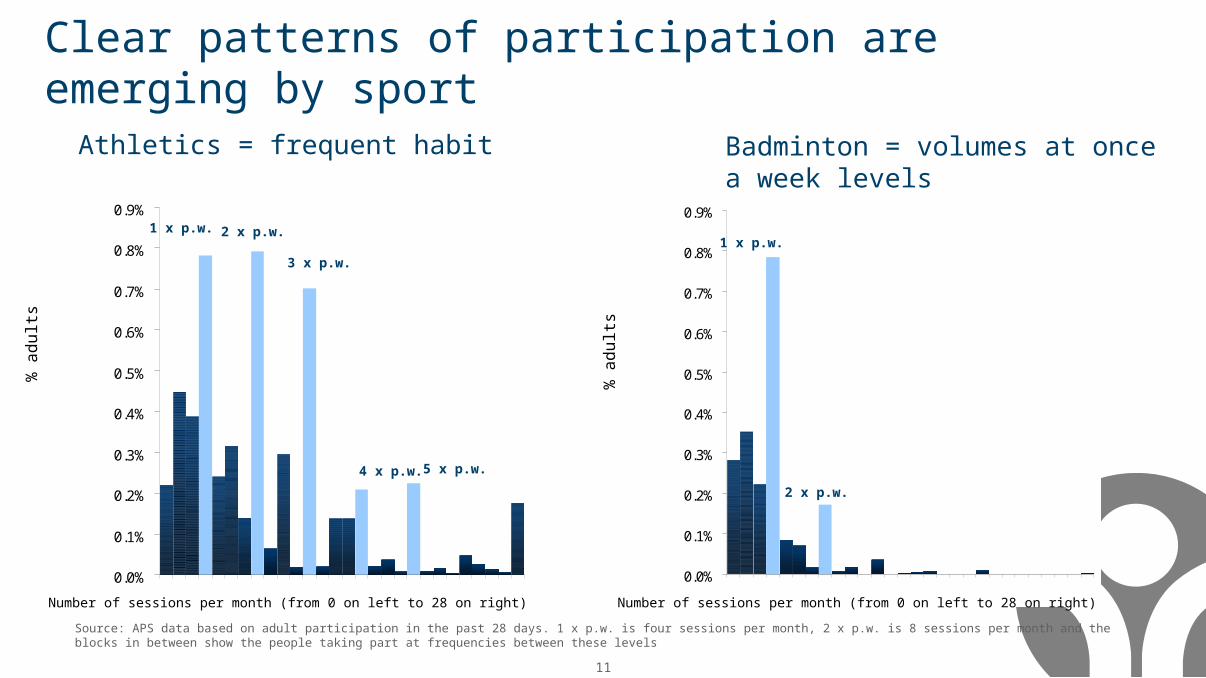

Clear patterns of participation are emerging by sport

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1 2 3 4 5 6 7 8 9 101112131415161718192021222324252627280.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1 2 3 4 5 6 7 8 9 10 111213 1415 1617 181920 2122 2324 252627 28

Athletics = frequent habit Badminton = volumes at once a week levels

1 x p.w. 2 x p.w.

3 x p.w.

4 x p.w. 5 x p.w.

1 x p.w.

2 x p.w.

Source: APS data based on adult participation in the past 28 days. 1 x p.w. is four sessions per month, 2 x p.w. is 8 sessions per month and the blocks in between show the people taking part at frequencies between these levels

% a

du

lts

% a

du

ltsNumber of sessions per month (from 0 on left to 28 on right) Number of sessions per month (from 0 on left to 28 on right)

12

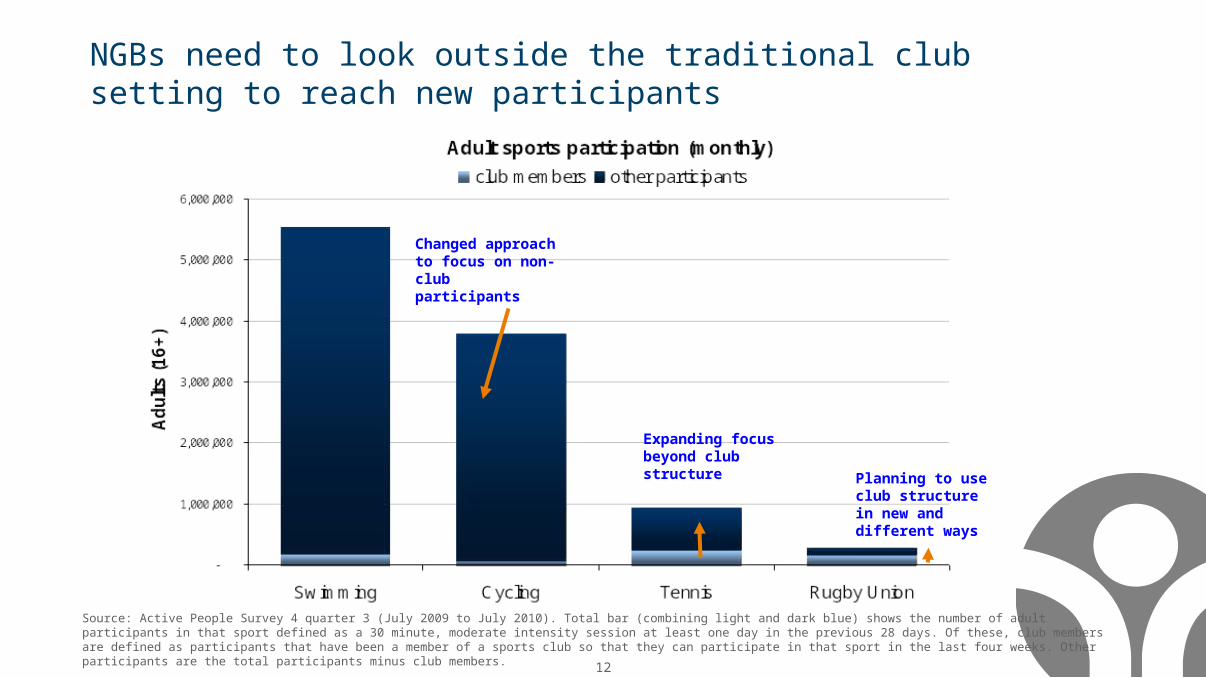

Source: Active People Survey 4 quarter 3 (July 2009 to July 2010). Total bar (combining light and dark blue) shows the number of adult participants in that sport defined as a 30 minute, moderate intensity session at least one day in the previous 28 days. Of these, club members are defined as participants that have been a member of a sports club so that they can participate in that sport in the last four weeks. Other participants are the total participants minus club members.

NGBs need to look outside the traditional club setting to reach new participants

Changed approach to focus on non-club participants

Expanding focus beyond club structure Planning to use club

structure in new and different ways

13

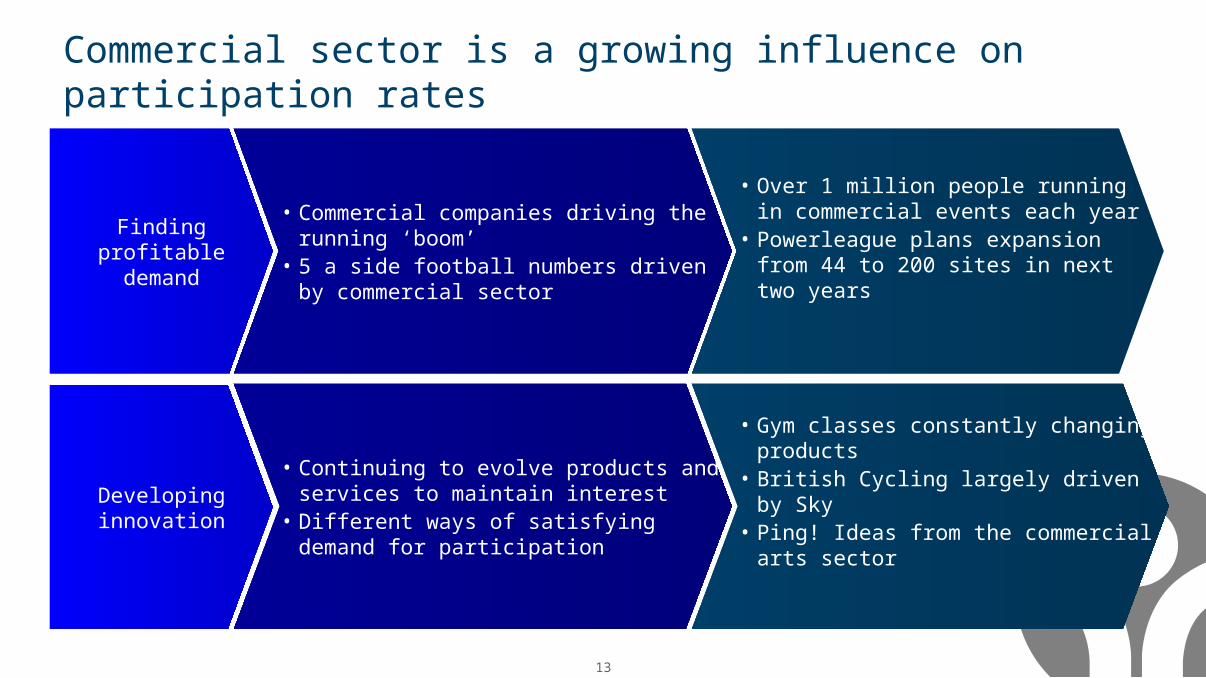

Commercial sector is a growing influence on participation rates

Finding profitable demand

• Commercial companies driving the running ‘boom’

• 5 a side football numbers driven by commercial sector

• Over 1 million people running in commercial events each year

• Powerleague plans expansion from 44 to 200 sites in next two years

Developing innovation

• Continuing to evolve products and services to maintain interest

• Different ways of satisfying demand for participation

• Gym classes constantly changing products

• British Cycling largely driven by Sky• Ping! Ideas from the commercial arts

sector

14

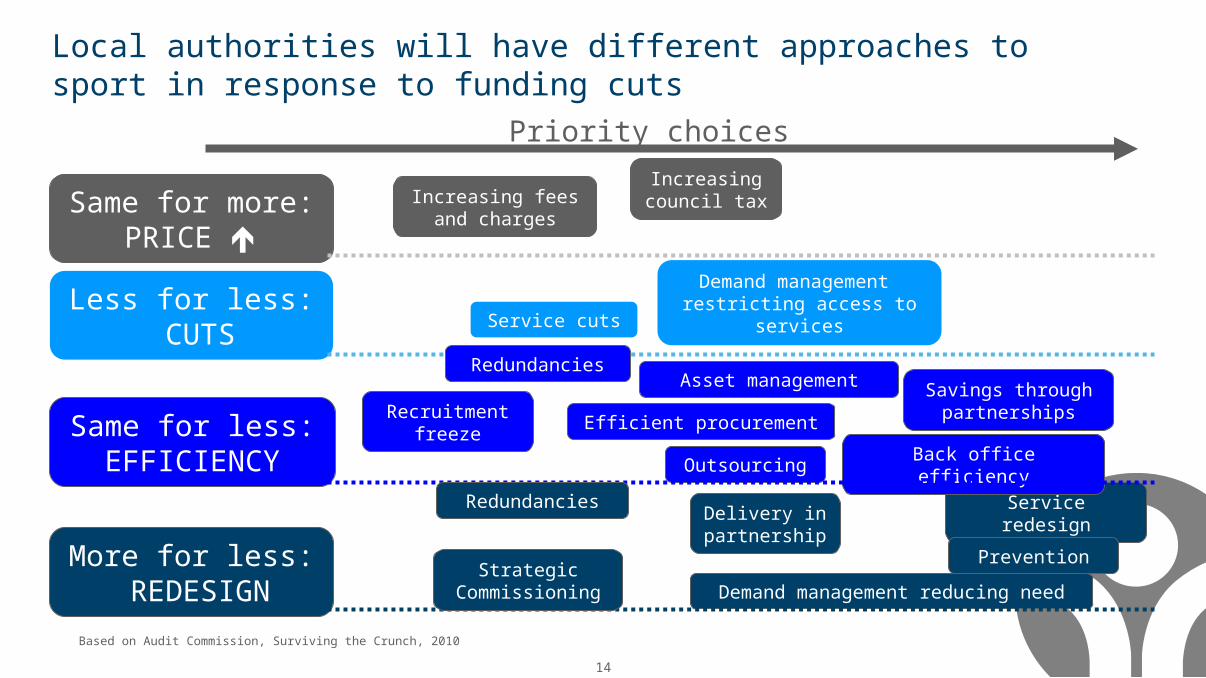

Local authorities will have different approaches to sport in response to funding cuts

More for less: REDESIGN

Same for less: EFFICIENCY

Less for less: CUTS

Same for more: PRICE

Delivery in partnership

Service redesign

Demand management reducing need

Prevention

Asset management

Back office efficiency

Savings through partnershipsEfficient procurement

Recruitment freeze

Outsourcing

Service cuts

Demand management restricting access to services

Increasing fees and charges

Increasing council tax

Redundancies

Redundancies

Priority choices

Based on Audit Commission, Surviving the Crunch, 2010

Strategic Commissioning

15

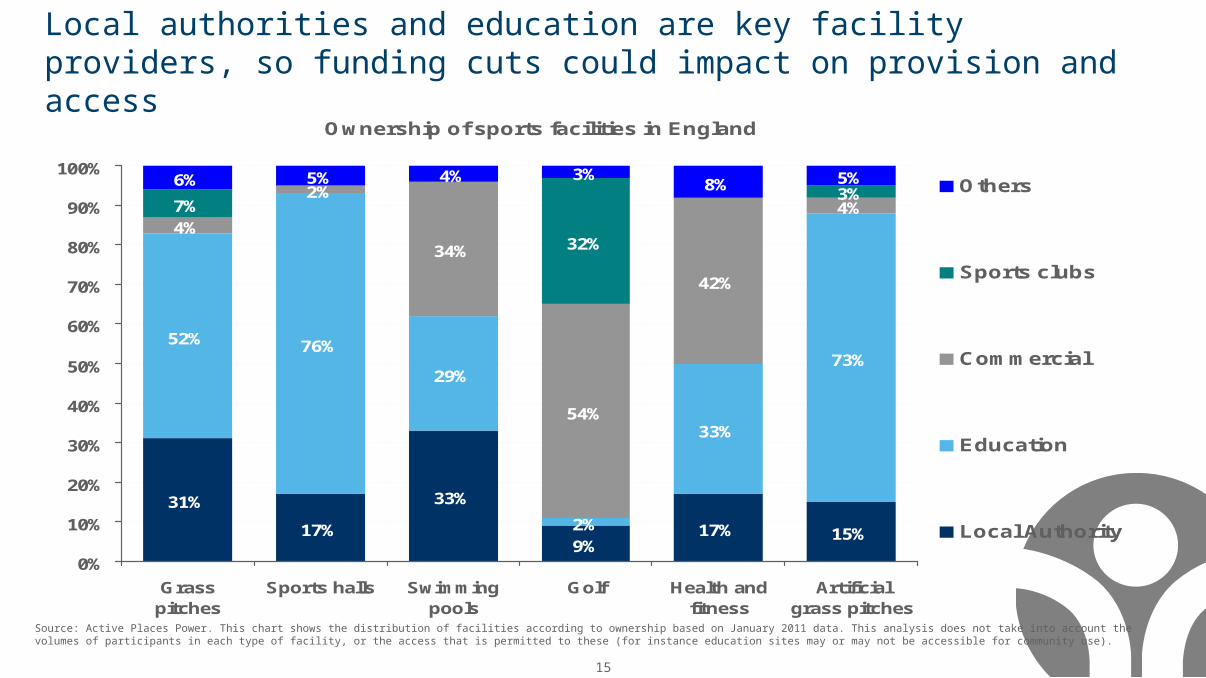

Local authorities and education are key facility providers, so funding cuts could impact on provision and access

Ownership of sports facilities in England

31%

17%

33%

9%17% 15%

52% 76%

29%

2%

33%

73%

4%

2%

34%

54%

42%

4%7%

32%

3%6% 5% 4% 3%

8% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Grasspitches

Sports halls Swimmingpools

Golf Health andfitness

Artificialgrass pitches

Others

Sports clubs

Commercial

Education

Local Authority

Source: Active Places Power. This chart shows the distribution of facilities according to ownership based on January 2011 data. This analysis does not take into account the volumes of participants in each type of facility, or the access that is permitted to these (for instance education sites may or may not be accessible for community use).

16

Future direction of travel

17

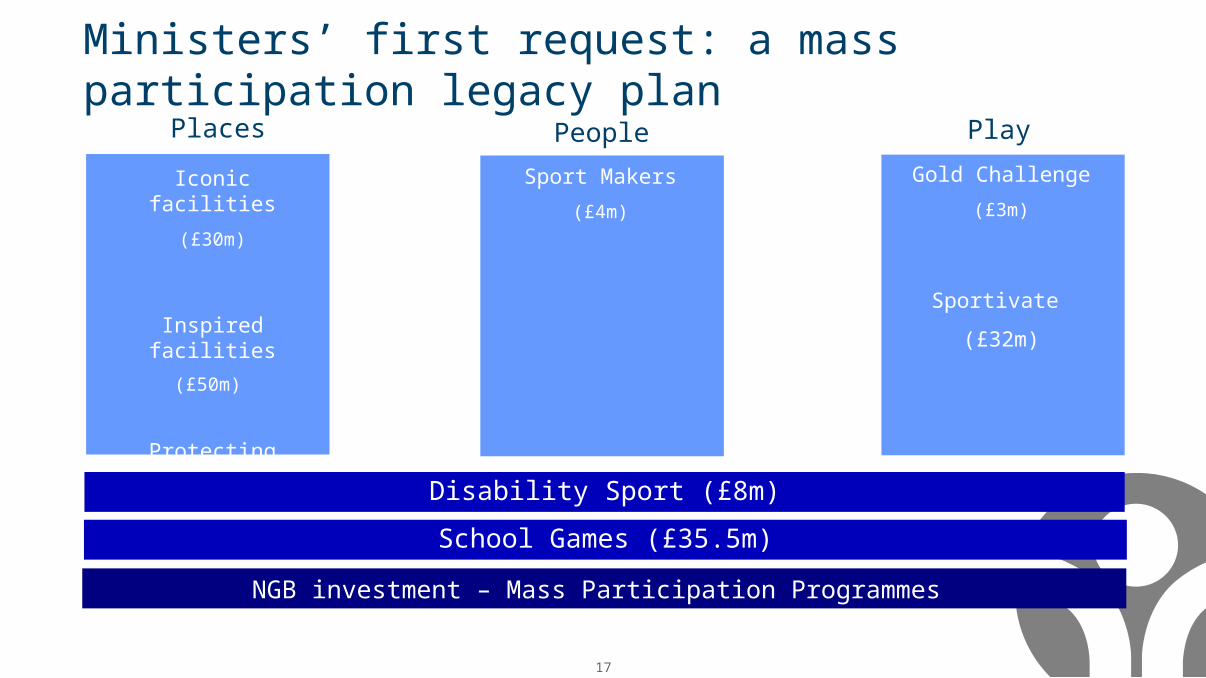

Ministers’ first request: a mass participation legacy plan

Iconic facilities

(£30m)

Inspired facilities

(£50m)

Protecting Playing fields

(£10m)

Places People Play

Sport Makers

(£4m)

Gold Challenge

(£3m)

Sportivate

(£32m)

Disability Sport (£8m)

NGB investment – Mass Participation Programmes

School Games (£35.5m)

18

NGBWhole Sport Plans

Places People Play

Local ProvisionStatutory roles and

funded partners

Admin costs

2011/12 is a transitional year

Strategic work/ market development

School Games Funding

19

The Big Society in sport• More local decision making

• Less ring fencing of spend, more devolution to individuals

• Asset transfer

• Emphasis on the voluntary sector

• Transparency and public accountability

• Impact not ‘targets’