jim furey – lehman brothers small-cap strategy 1 the high productivity, low barrier era lehman...

TRANSCRIPT

1Jim Furey – Lehman Brothers Small-Cap Strategy

The High Productivity, Low Barrier EraLehman Brothers Small-Cap StrategyJames H. Furey, CFA, Managing Director

02/02/05

Lehman Brothers does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report.

Customers of Lehman Brothers in the United States can receive independent, third-party research on the company or companies covered in this report, at no cost to them, where such research is available. Customers can access this independent research at www.lehmanlive.com or can call 1-800-2-LEHMAN to request a copy of this research.

Investors should consider this report as only a single factor in making their investment decisions.

PLEASE SEE ANALYST(S) CERTIFICATION(S) AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 37

02/02/05 2Jim Furey – Lehman Brothers Small-Cap Strategy

Today’s “Small” Talking Points

The “High Productivity, Low Barrier Era” and Its Effects on Small-Caps.

Is the Small-Cap Cycle Over?

Our Approach to Small-Cap Decision-Making

3Jim Furey – Lehman Brothers Small-Cap Strategy

High Productivity, Low Barrier Era

02/02/05 4Jim Furey – Lehman Brothers Small-Cap Strategy

The High Productivity, Low Barrier Era What is the “High Productivity, Low Barrier Era”?

The Digital Revolution still defines our time.

Era of Unintended Consequences

Portfolio Manager “DNA” must change: Sector Performance in Up & Down Markets Seasonality

02/02/05 5Jim Furey – Lehman Brothers Small-Cap Strategy

High Productivity, Low Barrier Era “Digital Revolution” still defines our time but

unintended consequences exist and are the key to investing success

Connecting the disparate dots…

Fiscal and monetary policy,

High cash on the balance sheet,

Rapidly rising commodity prices,

China’s emergence as a global economic force

Outsourcing appeal and political backlash,

Poor technology stock market returns,

Loss of value by traditional broadcast and radio.

High bond prices and low yields,

Reticence to hire and spend capital,

Rising real estate prices,

Why China’s growth is the envy and worry of the world,

Weak US dollar,

Technology’s multiple compression,

Financials, Industrials, Materials, Energy, Utilities strength.

02/02/05 6Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Cap Portfolio Manager DNA

Cons. Cons. Health Info. Telco.Dscr. Stpls. Energy Fin. Care Ind. Tech. Mat. Srvc. Util. R2000

Average Nominal Return 9.5 7.5 7.1 8.1 11.2 8.7 13.0 7.9 12.3 6.0 9.3

Average Relative Return 0.2 -1.9 -2.3 -1.2 1.8 -0.6 3.7 -1.4 3.0 -3.4 0.0

# of Positive Nominal Quarters 45 48 34 45 44 49 45 46 44 48 52

% of Positive Nominal Quarters 87% 92% 65% 87% 85% 94% 87% 88% 85% 92% 100%

# of Outperforming Quarters 27 25 25 21 30 22 31 16 33 13 NA

% of Outperforming Quarters 52% 48% 48% 40% 58% 42% 60% 31% 63% 25% NA

Rank 4 9 10 7 3 6 1 8 2 11 5

…this sector had the following statistics:

Whe

n th

e R2

000 h

ad

positiv

e no

min

al

qua

rterly

ret

urns

…

When R2000 had positive nominal returns…

Analysis of Sector Statistics in a Rising Small-Cap Market (1Q85 to 4Q04)

Analysis of Sector Statistics in a Declining Small-Cap Market (1Q85 to 4Q04)

Cons. Cons. Health Info. Telco.Dscr. Stpls. Energy Fin. Care Ind. Tech. Mat. Srvc. Util. R2000

Average Nominal Return -8.2 -4.5 -4.2 -3.6 -9.2 -7.5 -13.1 -5.9 -13.0 -1.4 -7.7

Average Relative Return -0.4 3.3 3.5 4.2 -1.5 0.2 -5.3 1.9 -5.2 6.3 0.0

# of Negative Quarters 24 16 17 19 26 25 23 21 22 20 28

% of Negative Quarters 86% 57% 61% 68% 93% 89% 82% 75% 79% 71% 100%

# of Outperforming Quarters 10 20 16 20 9 15 8 16 10 24 NA

% of Outperforming Quarters 36% 71% 57% 71% 32% 54% 29% 57% 36% 86% NA

Rank 8 4 3 2 9 6 11 5 10 1 7

…this sector had the following statistics:

Whe

n th

e R2

000 h

ad

negativ

e no

min

al

qua

rterly

ret

urns

…

When R2000 had negative nominal returns…

Source: Lehman Brothers and FactSet

Source: Lehman Brothers and FactSet

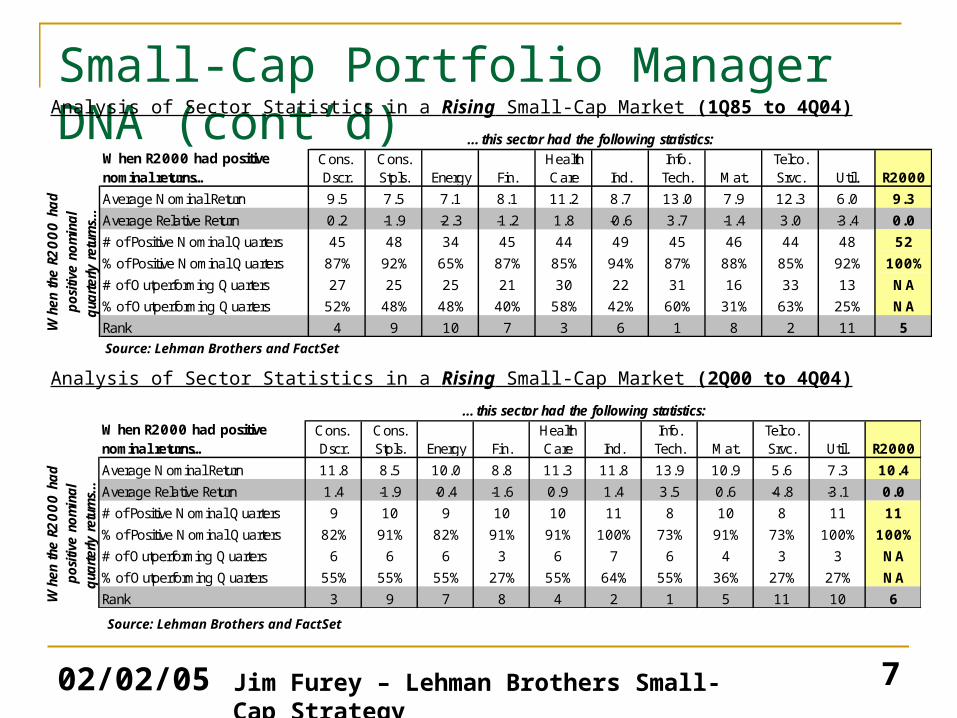

02/02/05 7Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Cap Portfolio Manager DNA (cont’d)

Cons. Cons. Health Info. Telco.Dscr. Stpls. Energy Fin. Care Ind. Tech. Mat. Srvc. Util. R2000

Average Nominal Return 9.5 7.5 7.1 8.1 11.2 8.7 13.0 7.9 12.3 6.0 9.3

Average Relative Return 0.2 -1.9 -2.3 -1.2 1.8 -0.6 3.7 -1.4 3.0 -3.4 0.0

# of Positive Nominal Quarters 45 48 34 45 44 49 45 46 44 48 52

% of Positive Nominal Quarters 87% 92% 65% 87% 85% 94% 87% 88% 85% 92% 100%

# of Outperforming Quarters 27 25 25 21 30 22 31 16 33 13 NA

% of Outperforming Quarters 52% 48% 48% 40% 58% 42% 60% 31% 63% 25% NA

Rank 4 9 10 7 3 6 1 8 2 11 5

…this sector had the following statistics:

Whe

n th

e R2

000 h

ad

positiv

e no

min

al

qua

rterly

ret

urns

…

When R2000 had positive nominal returns…

Analysis of Sector Statistics in a Rising Small-Cap Market (1Q85 to 4Q04)

Analysis of Sector Statistics in a Rising Small-Cap Market (2Q00 to 4Q04)

Cons. Cons. Health Info. Telco.Dscr. Stpls. Energy Fin. Care Ind. Tech. Mat. Srvc. Util. R2000

Average Nominal Return 11.8 8.5 10.0 8.8 11.3 11.8 13.9 10.9 5.6 7.3 10.4

Average Relative Return 1.4 -1.9 -0.4 -1.6 0.9 1.4 3.5 0.6 -4.8 -3.1 0.0

# of Positive Nominal Quarters 9 10 9 10 10 11 8 10 8 11 11

% of Positive Nominal Quarters 82% 91% 82% 91% 91% 100% 73% 91% 73% 100% 100%

# of Outperforming Quarters 6 6 6 3 6 7 6 4 3 3 NA

% of Outperforming Quarters 55% 55% 55% 27% 55% 64% 55% 36% 27% 27% NA

Rank 3 9 7 8 4 2 1 5 11 10 6

…this sector had the following statistics:

Whe

n th

e R2

000 h

ad

pos

itive

nom

inal

qua

rterly

ret

urns

…

When R2000 had positive nominal returns…

Source: Lehman Brothers and FactSet

Source: Lehman Brothers and FactSet

02/02/05 8Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Cap Portfolio Manager DNA (cont’d)Analysis of Sector Statistics in a Declining Small-Cap Market (1Q85 to 4Q04)

Analysis of Sector Statistics in a Declining Small-Cap Market (2Q00 to 4Q04)

Cons. Cons. Health Info. Telco.Dscr. Stpls. Energy Fin. Care Ind. Tech. Mat. Srvc. Util. R2000

Average Nominal Return -8.2 -4.5 -4.2 -3.6 -9.2 -7.5 -13.1 -5.9 -13.0 -1.4 -7.7

Average Relative Return -0.4 3.3 3.5 4.2 -1.5 0.2 -5.3 1.9 -5.2 6.3 0.0

# of Negative Quarters 24 16 17 19 26 25 23 21 22 20 28

% of Negative Quarters 86% 57% 61% 68% 93% 89% 82% 75% 79% 71% 100%

# of Outperforming Quarters 10 20 16 20 9 15 8 16 10 24 NA

% of Outperforming Quarters 36% 71% 57% 71% 32% 54% 29% 57% 36% 86% NA

Rank 8 4 3 2 9 6 11 5 10 1 7

…this sector had the following statistics:

Whe

n th

e R2

000 h

ad

negativ

e no

min

al

qua

rterly

ret

urns

…

When R2000 had negative nominal returns…

Cons. Cons. Health Info. Telco.Dscr. Stpls. Energy Fin. Care Ind. Tech. Mat. Srvc. Util. R2000

Average Nominal Return -7.1 -1.8 -2.8 0.8 -9.3 -7.0 -24.3 -5.2 -24.1 -2.4 -9.4

Average Relative Return 2.3 7.6 6.6 10.2 0.1 2.4 -14.9 4.2 -14.8 7.0 0.0

# of Negative Quarters 6 3 5 4 7 6 8 5 7 6 8

% of Negative Quarters 75% 38% 63% 50% 88% 75% 100% 63% 88% 75% 100%

# of Outperforming Quarters 3 6 6 8 4 6 1 5 1 8 NA

% of Outperforming Quarters 38% 75% 75% 100% 50% 75% 13% 63% 13% 100% NA

Rank 7 2 4 1 8 6 11 5 10 3 9

When R2000 had negative nominal returns…

…this sector had the following statistics:

Whe

n th

e R2

000 h

ad

negativ

e no

min

al

qua

rterly

ret

urns

…

Source: Lehman Brothers and FactSet

Source: Lehman Brothers and FactSet

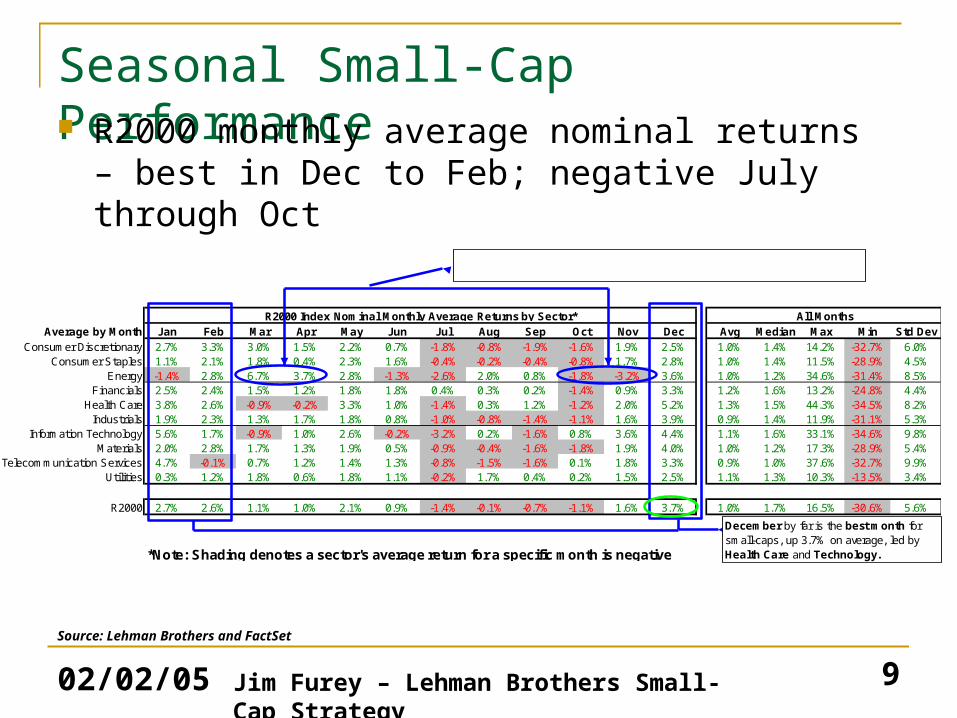

02/02/05 9Jim Furey – Lehman Brothers Small-Cap Strategy

Seasonal Small-Cap Performance

Average by Month Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Avg Median Max Min Std DevConsumer Discretionary 2.7% 3.3% 3.0% 1.5% 2.2% 0.7% -1.8% -0.8% -1.9% -1.6% 1.9% 2.5% 1.0% 1.4% 14.2% -32.7% 6.0%

Consumer Staples 1.1% 2.1% 1.8% 0.4% 2.3% 1.6% -0.4% -0.2% -0.4% -0.8% 1.7% 2.8% 1.0% 1.4% 11.5% -28.9% 4.5%Energy -1.4% 2.8% 6.7% 3.7% 2.8% -1.3% -2.6% 2.0% 0.8% -1.8% -3.2% 3.6% 1.0% 1.2% 34.6% -31.4% 8.5%

Financials 2.5% 2.4% 1.5% 1.2% 1.8% 1.8% 0.4% 0.3% 0.2% -1.4% 0.9% 3.3% 1.2% 1.6% 13.2% -24.8% 4.4%Health Care 3.8% 2.6% -0.9% -0.2% 3.3% 1.0% -1.4% 0.3% 1.2% -1.2% 2.0% 5.2% 1.3% 1.5% 44.3% -34.5% 8.2%

Industrials 1.9% 2.3% 1.3% 1.7% 1.8% 0.8% -1.0% -0.8% -1.4% -1.1% 1.6% 3.9% 0.9% 1.4% 11.9% -31.1% 5.3%Information Technology 5.6% 1.7% -0.9% 1.0% 2.6% -0.2% -3.2% 0.2% -1.6% 0.8% 3.6% 4.4% 1.1% 1.6% 33.1% -34.6% 9.8%

Materials 2.0% 2.8% 1.7% 1.3% 1.9% 0.5% -0.9% -0.4% -1.6% -1.8% 1.9% 4.0% 1.0% 1.2% 17.3% -28.9% 5.4%Telecommunication Services 4.7% -0.1% 0.7% 1.2% 1.4% 1.3% -0.8% -1.5% -1.6% 0.1% 1.8% 3.3% 0.9% 1.0% 37.6% -32.7% 9.9%

Utilities 0.3% 1.2% 1.8% 0.6% 1.8% 1.1% -0.2% 1.7% 0.4% 0.2% 1.5% 2.5% 1.1% 1.3% 10.3% -13.5% 3.4%

R2000 2.7% 2.6% 1.1% 1.0% 2.1% 0.9% -1.4% -0.1% -0.7% -1.1% 1.6% 3.7% 1.0% 1.7% 16.5% -30.6% 5.6%

*Note: Shading denotes a sector's average return for a specific month is negative

R2000 Index Nominal Monthly Average Returns by Sector* All Months

December by far is the best month for small-caps, up 3.7% on average, led by Health Care and Technology.

Energy's best performance occurs in March & April; Energy's worst months are October & November.

R2000 monthly average nominal returns – best in Dec to Feb; negative July through Oct

Source: Lehman Brothers and FactSet

02/02/05 10Jim Furey – Lehman Brothers Small-Cap Strategy

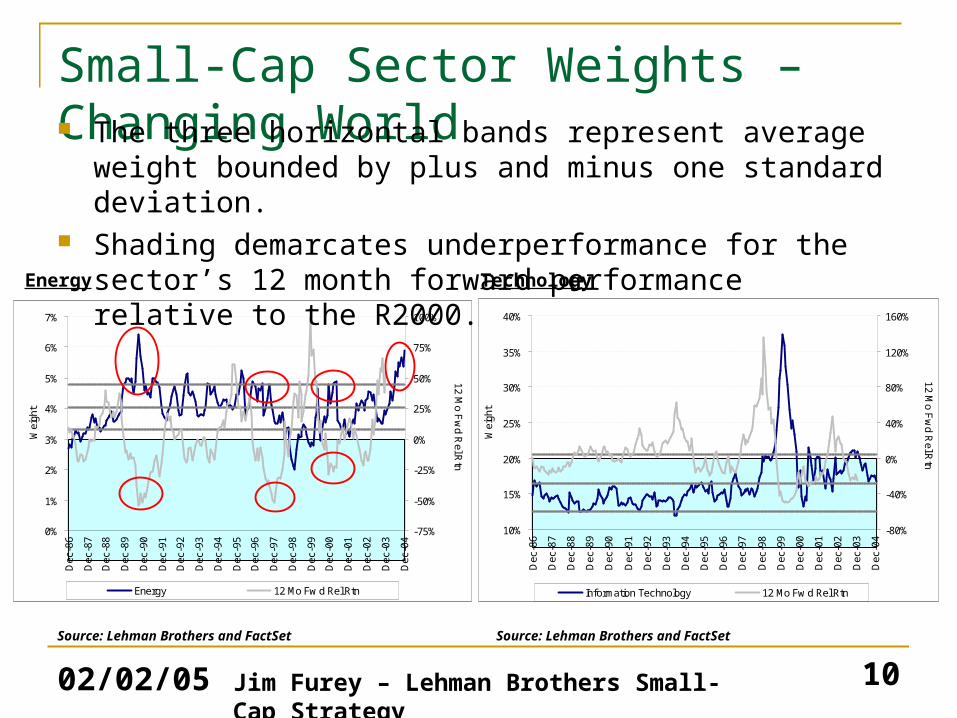

Small-Cap Sector Weights – Changing World

WEIGHT PROFILESector Decile

vs. Self History

BEARISH

0%

1%

2%

3%

4%

5%

6%

7%

Dec

-86

Dec

-87

Dec

-88

Dec

-89

Dec

-90

Dec

-91

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Wei

ght

-75%

-50%

-25%

0%

25%

50%

75%

100%

12 Mo F

wd R

el Rtn

Energy 12 Mo Fw d Rel Rtn

WEIGHT PROFILESector Decile

vs. Self History

No Signal

10%

15%

20%

25%

30%

35%

40%

Dec

-86

Dec

-87

Dec

-88

Dec

-89

Dec

-90

Dec

-91

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Wei

ght

-80%

-40%

0%

40%

80%

120%

160%

12 Mo F

wd R

el Rtn

Information Technology 12 Mo Fw d Rel Rtn

The three horizontal bands represent average weight bounded by plus and minus one standard deviation.

Shading demarcates underperformance for the sector’s 12 month forward performance relative to the R2000.

Energy Technology

Source: Lehman Brothers and FactSet Source: Lehman Brothers and FactSet

11Jim Furey – Lehman Brothers Small-Cap Strategy

Is the Small-Cap Cycle Over?

02/02/05 12Jim Furey – Lehman Brothers Small-Cap Strategy

Is the Small-Cap Cycle Over? Bears Argue… Is it “Simply Irresistible” to Short Small-Caps & Go Long Large?

What the Small-Cap Bears are saying Monetary policy, 10-2 year US Government spreads, Real Fed Funds, Small-cap nominal valuation (P/S, P/B, P/E) & relative (P/E)

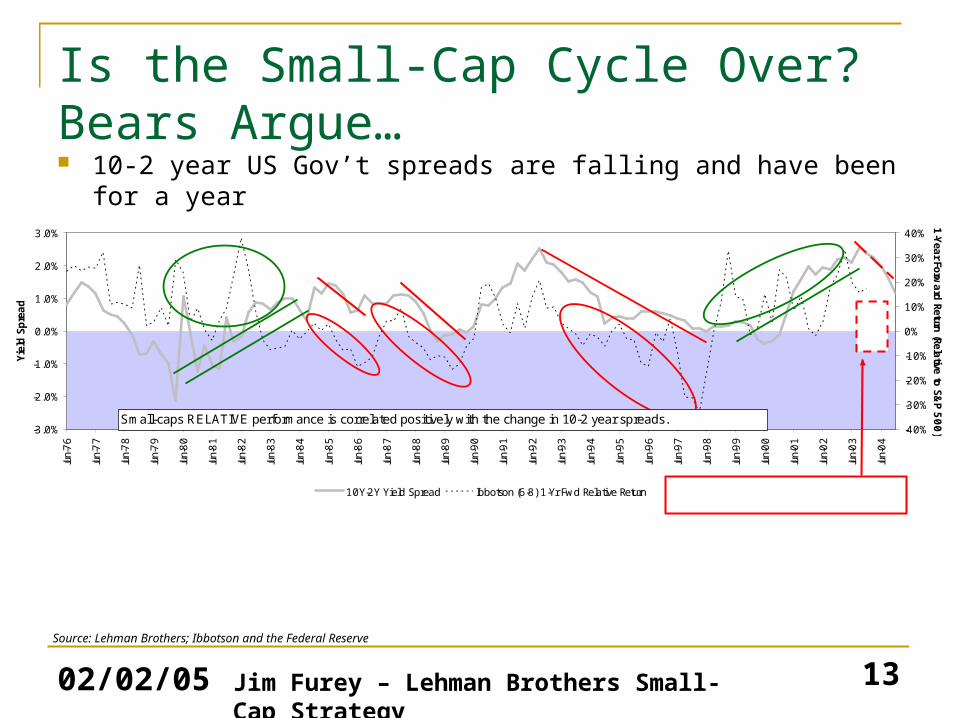

02/02/05 13Jim Furey – Lehman Brothers Small-Cap Strategy

Is the Small-Cap Cycle Over? Bears Argue… 10-2 year US Gov’t spreads are falling and have been for a year

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

Jun-

76

Jun-

77

Jun-

78

Jun-

79

Jun-

80

Jun-

81

Jun-

82

Jun-

83

Jun-

84

Jun-

85

Jun-

86

Jun-

87

Jun-

88

Jun-

89

Jun-

90

Jun-

91

Jun-

92

Jun-

93

Jun-

94

Jun-

95

Jun-

96

Jun-

97

Jun-

98

Jun-

99

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Yie

ld S

pre

ad

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1-Yea

r Forward

Return (Relative to S&

P 500)

10Y-2Y Yield Spread Ibbotson (6-8) 1-Yr Fwd Relative Return

Small-caps RELATIVE performance is correlated positively with the change in 10-2 year spreads.

?

Declining 2-10 spreads are BEARISH for small-caps RELATIVE performance.

Source: Lehman Brothers; Ibbotson and the Federal Reserve

02/02/05 14Jim Furey – Lehman Brothers Small-Cap Strategy

Is the Small-Cap Cycle Over? Bears Argue… Small-cap P/S and P/B are expensive nominally

Mean + 1StD = 1.0x

Mean = 0.8x

Mean - 1StD = 0.6x

0.20x

0.30x

0.40x

0.50x

0.60x

0.70x

0.80x

0.90x

1.00x

1.10x

1.20x

1.30x

1.40x

1/

31/

1985

1/

31/

1986

1/

30/

1987

1/

29/

1988

1/

31/

1989

1/

31/

1990

1/

31/

1991

1/

31/

1992

1/

29/

1993

1/

31/

1994

1/

31/

1995

1/

31/

1996

1/

31/

1997

1/

30/

1998

1/

29/

1999

1/

31/

2000

1/

31/

2001

1/

31/

2002

1/

31/

2003

1/

30/

2004

Pric

e to

Sal

es

(-40)

(-20)

0

20

40

60

80

1-Year Forw

ard Return

LTM P/ S 1-Year Forward Return

Mean + 1StD = 2.3x

Mean = 1.9x

Mean - 1StD = 1.6x

1.00x

1.25x

1.50x

1.75x

2.00x

2.25x

2.50x

2.75x

3.00x

1/

31/

1985

1/

31/

1986

1/

30/

1987

1/

29/

1988

1/

31/

1989

1/

31/

1990

1/

31/

1991

1/

31/

1992

1/

29/

1993

1/

31/

1994

1/

31/

1995

1/

31/

1996

1/

31/

1997

1/

30/

1998

1/

29/

1999

1/

31/

2000

1/

31/

2001

1/

31/

2002

1/

31/

2003

1/

30/

2004

Pric

e to

Boo

k(-40)

(-20)

0

20

40

60

80

1-Y

ear Forw

ard

Return

P/ B 1-Year Forward Return

R2000 P/S w/12mo Fwd Nom Rtn R2000 P/B w/12mo Fwd Nom Rtn

Source: Lehman Brothers and FactSet.

02/02/05 15Jim Furey – Lehman Brothers Small-Cap Strategy

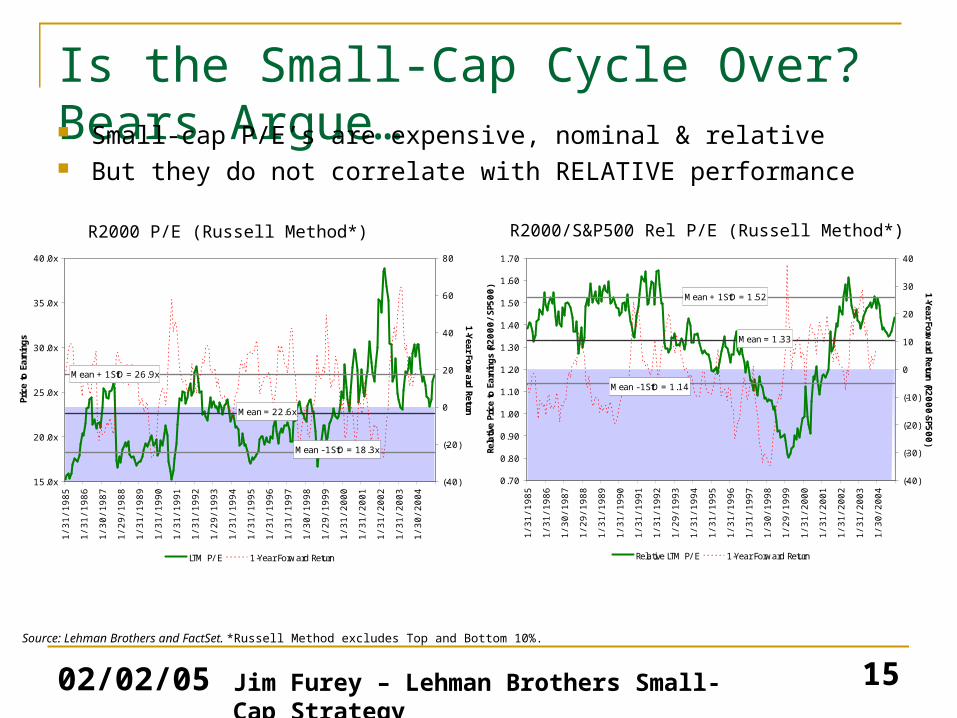

Is the Small-Cap Cycle Over? Bears Argue… Small-cap P/E’s are expensive, nominal & relative But they do not correlate with RELATIVE performance

R2000 P/E (Russell Method*) R2000/S&P500 Rel P/E (Russell Method*)

Mean + 1StD = 26.9x

Mean = 22.6x

Mean - 1StD = 18.3x

15.0x

20.0x

25.0x

30.0x

35.0x

40.0x

1/

31/

1985

1/

31/

1986

1/

30/

1987

1/

29/

1988

1/

31/

1989

1/

31/

1990

1/

31/

1991

1/

31/

1992

1/

29/

1993

1/

31/

1994

1/

31/

1995

1/

31/

1996

1/

31/

1997

1/

30/

1998

1/

29/

1999

1/

31/

2000

1/

31/

2001

1/

31/

2002

1/

31/

2003

1/

30/

2004

Pric

e to

Earn

ings

(-40)

(-20)

0

20

40

60

80

1-Y

ear Forw

ard

Return

LTM P/ E 1-Year Forward Return

Mean + 1StD = 1.52

Mean = 1.33

Mean - 1StD = 1.14

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1/

31/

1985

1/

31/

1986

1/

30/

1987

1/

29/

1988

1/

31/

1989

1/

31/

1990

1/

31/

1991

1/

31/

1992

1/

29/

1993

1/

31/

1994

1/

31/

1995

1/

31/

1996

1/

31/

1997

1/

30/

1998

1/

29/

1999

1/

31/

2000

1/

31/

2001

1/

31/

2002

1/

31/

2003

1/

30/

2004

Rela

tive

Pric

e to

Ear

ning

s (R

2000/SP

500)

(-40)

(-30)

(-20)

(-10)

0

10

20

30

40

1-Year Forw

ard Return (R2000-SP5

00)

Relative LTM P/ E 1-Year Forward Return

Source: Lehman Brothers and FactSet. *Russell Method excludes Top and Bottom 10%.

02/02/05 16Jim Furey – Lehman Brothers Small-Cap Strategy

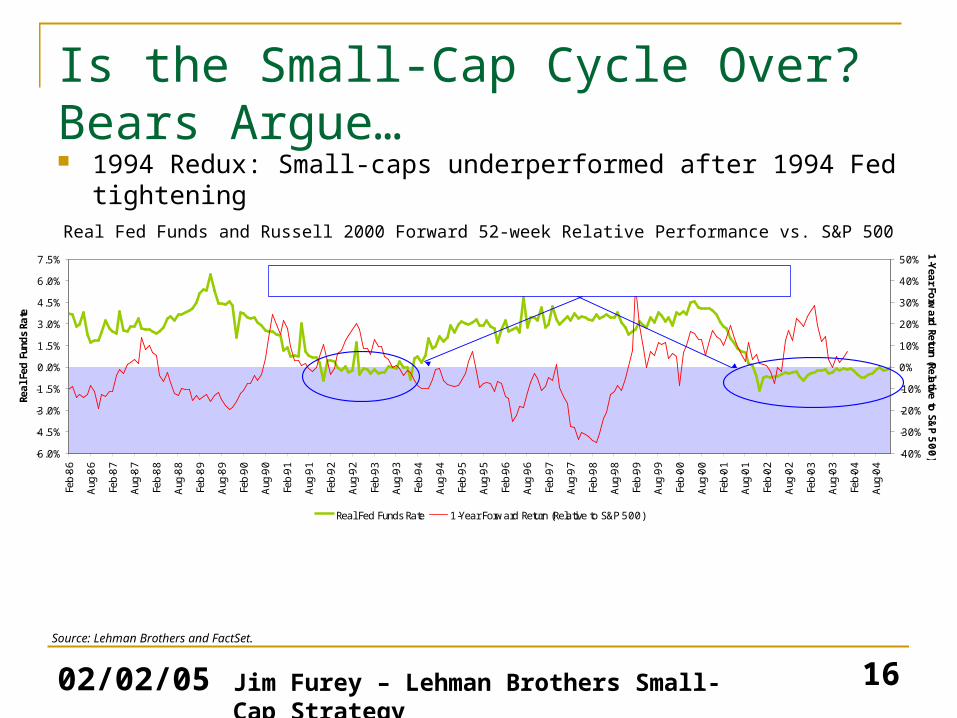

Is the Small-Cap Cycle Over? Bears Argue… 1994 Redux: Small-caps underperformed after 1994 Fed tightening

Real Fed Funds and Russell 2000 Forward 52-week Relative Performance vs. S&P 500

Source: Lehman Brothers and FactSet.

-6.0%

-4.5%

-3.0%

-1.5%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

Feb-

86

Aug

-86

Feb-

87

Aug

-87

Feb-

88

Aug

-88

Feb-

89

Aug

-89

Feb-

90

Aug

-90

Feb-

91

Aug

-91

Feb-

92

Aug

-92

Feb-

93

Aug

-93

Feb-

94

Aug

-94

Feb-

95

Aug

-95

Feb-

96

Aug

-96

Feb-

97

Aug

-97

Feb-

98

Aug

-98

Feb-

99

Aug

-99

Feb-

00

Aug

-00

Feb-

01

Aug

-01

Feb-

02

Aug

-02

Feb-

03

Aug

-03

Feb-

04

Aug

-04

Real F

ed F

unds

Rate

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

1-Y

ear Forw

ard

Return (Relative to S&

P 500)

Real Fed Funds Rate 1-Year Forward Return (Relative to S&P 500)

Real Fed Funds negative and small-caps 52-week relative performance beats large-caps.

02/02/05 17Jim Furey – Lehman Brothers Small-Cap Strategy

Is the Small-Cap Cycle Over? Bears Argue… Relative price to sales expands when Real Fed Funds are negative

but can contract when Real Fed Funds rise as they did in 1994

Real Fed Funds and Russell 2000 Relative Price to Sales Valuation vs. S&P 500

Source: Lehman Brothers and FactSet.

Source: Lehman Brothers and FactSet Research

-3.0%

-1.5%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

Feb-

86

Aug

-86

Feb-

87

Aug

-87

Feb-

88

Aug

-88

Feb-

89

Aug

-89

Feb-

90

Aug

-90

Feb-

91

Aug

-91

Feb-

92

Aug

-92

Feb-

93

Aug

-93

Feb-

94

Aug

-94

Feb-

95

Aug

-95

Feb-

96

Aug

-96

Feb-

97

Aug

-97

Feb-

98

Aug

-98

Feb-

99

Aug

-99

Feb-

00

Aug

-00

Feb-

01

Aug

-01

Feb-

02

Aug

-02

Feb-

03

Aug

-03

Feb-

04

Aug

-04

Real F

ed F

unds

Rate

0.4x

0.5x

0.6x

0.7x

0.8x

0.9x

1.0x

LTM P/

S (Relative to S&

P 500)

Real Fed Funds Rate LTM P/ S (Relative to S&P 500)

Relative price to sales expands when Real Fed Funds are negative but can contract when Real Fed Funds rise as they did in 1994.

Relative valuation inflects negatively when Real Fed Funds cross zero.

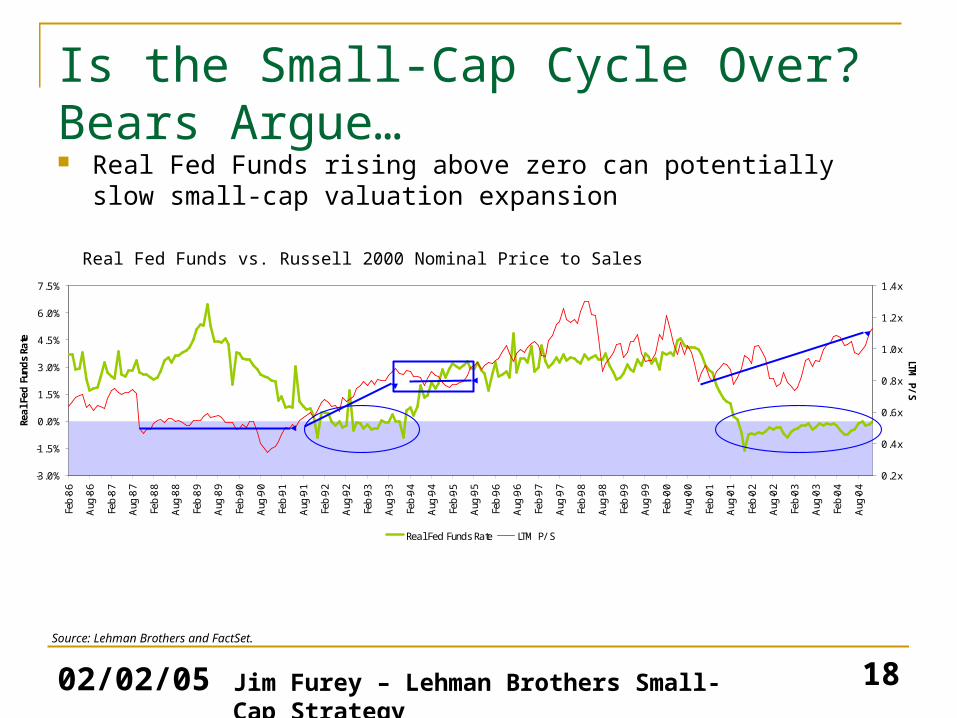

02/02/05 18Jim Furey – Lehman Brothers Small-Cap Strategy

Is the Small-Cap Cycle Over? Bears Argue… Real Fed Funds rising above zero can potentially slow small-cap

valuation expansion

Real Fed Funds vs. Russell 2000 Nominal Price to Sales

Source: Lehman Brothers and FactSet.

Source: Lehman Brothers and FactSet Research

-3.0%

-1.5%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

Feb-

86

Aug

-86

Feb-

87

Aug

-87

Feb-

88

Aug

-88

Feb-

89

Aug

-89

Feb-

90

Aug

-90

Feb-

91

Aug

-91

Feb-

92

Aug

-92

Feb-

93

Aug

-93

Feb-

94

Aug

-94

Feb-

95

Aug

-95

Feb-

96

Aug

-96

Feb-

97

Aug

-97

Feb-

98

Aug

-98

Feb-

99

Aug

-99

Feb-

00

Aug

-00

Feb-

01

Aug

-01

Feb-

02

Aug

-02

Feb-

03

Aug

-03

Feb-

04

Aug

-04

Real F

ed F

unds

Rate

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

1.4x

LTM P/

S

Real Fed Funds Rate LTM P/ S

Rising Real Fed Funds do not necessarily cause valuation compression so much as they cause valuation stagnation.

02/02/05 19Jim Furey – Lehman Brothers Small-Cap Strategy

Is the Small-Cap Cycle Over? Bears Argue… Their “Short Small-cap / Long Large-cap” trade is not a “Go Short

ALONE” strategy Small-caps since 1986 are most often profitable as long as Real Fed

Funds are less than 3.25%.

Real Fed Funds and Forward 52-Week Russell 2000 Nominal Returns

Source: Lehman Brothers and FactSet.

Source: Lehman Brothers and FactSet Research

-3.0%

-1.5%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

Feb-

86

Aug

-86

Feb-

87

Aug

-87

Feb-

88

Aug

-88

Feb-

89

Aug

-89

Feb-

90

Aug

-90

Feb-

91

Aug

-91

Feb-

92

Aug

-92

Feb-

93

Aug

-93

Feb-

94

Aug

-94

Feb-

95

Aug

-95

Feb-

96

Aug

-96

Feb-

97

Aug

-97

Feb-

98

Aug

-98

Feb-

99

Aug

-99

Feb-

00

Aug

-00

Feb-

01

Aug

-01

Feb-

02

Aug

-02

Feb-

03

Aug

-03

Feb-

04

Aug

-04

Real F

ed F

unds

Rate

-30%

-15%

0%

15%

30%

45%

60%

75%

1-Yea

r Forward

Nom

inal Return

Real Fed Funds Rate 1-Year Forward Nominal Return

Real Fed Funds and forward 52-week Russell 2000 nominal returns are inveresly correlated. Circled are two periods, including the current one, when Real Fund Funds were less than zero and returns positive. Unless Real Fed Funds are above 3.25% small-caps are typically profitable.

02/02/05 20Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Caps Can Still Outperform. Bulls Argue… “High Productivity, Low Barrier Era” forces likely

Keep REAL and NOMINAL rates low,

Favor “more local” less intellectual property (IP) based small-caps,

Support high valuation.

Investors bearish on small-caps’ RELATIVE performance may be underestimating the “High Productivity, Low Barrier Era” ability to keep rates low, policy stimulative, and investors focused on small-caps where there is less IP .

02/02/05 21Jim Furey – Lehman Brothers Small-Cap Strategy

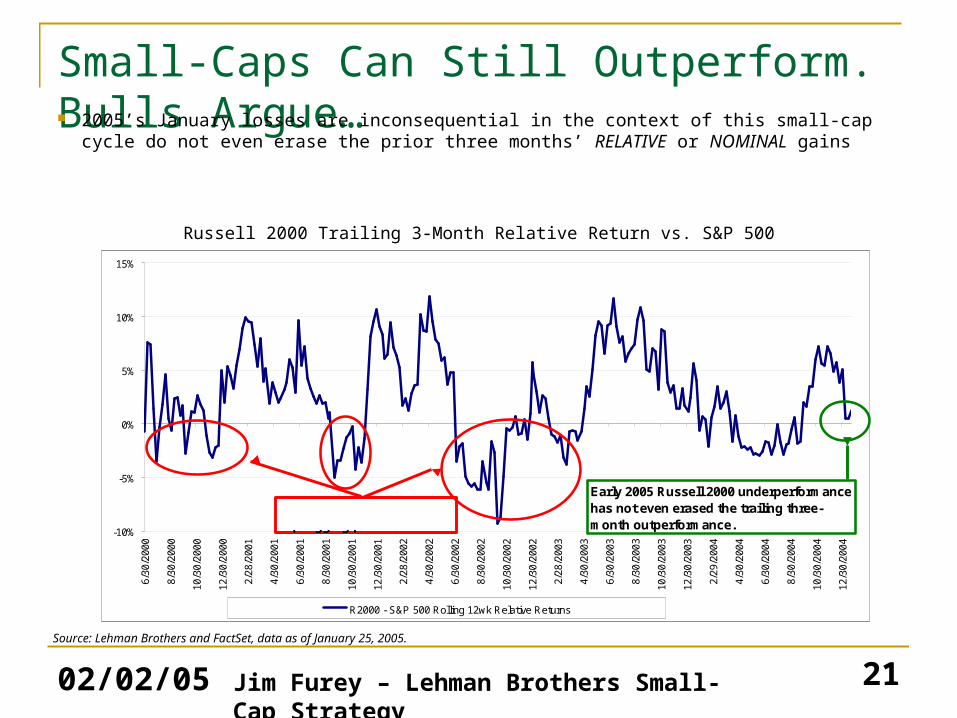

Small-Caps Can Still Outperform. Bulls Argue… 2005’s January losses are inconsequential in the context of this small-cap cycle

do not even erase the prior three months’ RELATIVE or NOMINAL gains

Russell 2000 Trailing 3-Month Relative Return vs. S&P 500

Source: Lehman Brothers and FactSet, data as of January 25, 2005.

-10%

-5%

0%

5%

10%

15%

6/30

/200

0

8/30

/200

0

10/3

0/20

00

12/3

0/20

00

2/28

/200

1

4/30

/200

1

6/30

/200

1

8/30

/200

1

10/3

0/20

01

12/3

0/20

01

2/28

/200

2

4/30

/200

2

6/30

/200

2

8/30

/200

2

10/3

0/20

02

12/3

0/20

02

2/28

/200

3

4/30

/200

3

6/30

/200

3

8/30

/200

3

10/3

0/20

03

12/3

0/20

03

2/29

/200

4

4/30

/200

4

6/30

/200

4

8/30

/200

4

10/3

0/20

04

12/3

0/20

04

R2000 - S&P 500 Rolling 12wk Relative Returns

(post Mar '00 Bubble) Early 2005 Russell 2000 underperformance has not even erased the trailing three-month outperformance.

This cycle has seen small-cap lagging periods.

02/02/05 22Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Caps Can Still Outperform. Bulls Argue… Small-Caps have outperformed in the past dating to 1958 when

Real US Government 10-year rates were less than 2.5%, as is also the case today

Real 10-Year US Gov’t Interest Rates plotted vs. Small-Cap Forward 52-Week Relative Returns

Source: Lehman Brothers; Ibbotson and the Federal Reserve

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Mar

-58

Mar

-59

Mar

-60

Mar

-61

Mar

-62

Mar

-63

Mar

-64

Mar

-65

Mar

-66

Mar

-67

Mar

-68

Mar

-69

Mar

-70

Mar

-71

Mar

-72

Mar

-73

Mar

-74

Mar

-75

Mar

-76

Mar

-77

Mar

-78

Mar

-79

Mar

-80

Mar

-81

Mar

-82

Mar

-83

Mar

-84

Mar

-85

Mar

-86

Mar

-87

Mar

-88

Mar

-89

Mar

-90

Mar

-91

Mar

-92

Mar

-93

Mar

-94

Mar

-95

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Real 1

0-Y

ear Yi

eld

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1-Y

ear Forw

ard

Return (Relative to S&

P 500)

US Gov't Real 10-Year Yield Ibbotson (6-8) 1-Yr Fwd Relative Return

When Real 10-Yr US rates < 2.5% the avg annual fwd relative return is 10% & SMALL OUTPERFORMS. When real rates > 2.5% the avg annual fwd relative return is 0% & small is not advantaged.

Examples of low Real rates & small-caps lagging.We could be wrong.

02/02/05 23Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Caps Can Still Outperform. Bulls Argue… History supports the view that small-caps outperform when

NOMINAL 10-year US Government rates are below 5.0%

Nominal US Government 10-Year Rates and Forward 52-Week RELATIVE Performance

Source: Lehman Brothers; Ibbotson and the Federal Reserve

-15.0%

-12.0%

-9.0%

-6.0%

-3.0%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

Mar

-58

Mar

-59

Mar

-60

Mar

-61

Mar

-62

Mar

-63

Mar

-64

Mar

-65

Mar

-66

Mar

-67

Mar

-68

Mar

-69

Mar

-70

Mar

-71

Mar

-72

Mar

-73

Mar

-74

Mar

-75

Mar

-76

Mar

-77

Mar

-78

Mar

-79

Mar

-80

Mar

-81

Mar

-82

Mar

-83

Mar

-84

Mar

-85

Mar

-86

Mar

-87

Mar

-88

Mar

-89

Mar

-90

Mar

-91

Mar

-92

Mar

-93

Mar

-94

Mar

-95

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Nom

10-Y

ear Yie

ld

-40%

-32%

-24%

-16%

-8%

0%

8%

16%

24%

32%

40%

1-Y

ear Forw

ard

Return (Relative to S&

P 500)

Nom US Gov't 10-Year Yld Ibbotson (6-8) 1-Yr Fwd Relative Return

When 10-Year rates < 5.0% the fwd 52-week small-cap relative return is 7.1% and when 10-year rates are > 5.0%, the avg fwd 52-week performance is 3.2%. Our point: low nominal rates may be a positive for small-caps.

02/02/05 24Jim Furey – Lehman Brothers Small-Cap Strategy

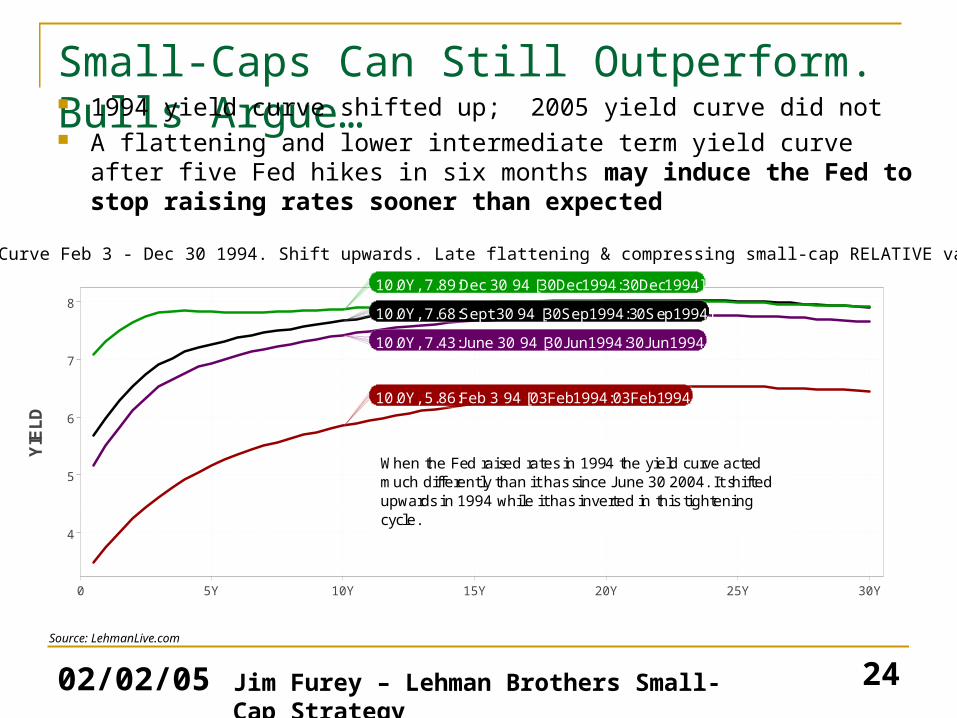

Small-Caps Can Still Outperform. Bulls Argue… 1994 yield curve shifted up; 2005 yield curve did not A flattening and lower intermediate term yield curve after five Fed

hikes in six months may induce the Fed to stop raising rates sooner than expected

Yield Curve Feb 3 - Dec 30 1994. Shift upwards. Late flattening & compressing small-cap RELATIVE valuation

Source: LehmanLive.com

N U G G E T T A G : u s e r N a m e = n u ll& p lo t N a m e = n u ll

4

5

6

7

8

YIE

LD

0 5Y 10Y 15Y 20Y 25Y 30Y

Source: LehmanLive.com

When the Fed raised rates in 1994 the yield curve acted much differently than it has since J une 30 2004. It shifted upwards in 1994 while it has inverted in this tightening cycle.

10.0Y, 7.43:J une 30 94 [30J un1994:30J un1994]

10.0Y, 7.68:Sept 30 94 [30Sep1994:30Sep1994]

10.0Y, 5.86:Feb 3 94 [03Feb1994:03Feb1994]

10.0Y, 7.89:Dec 30 94 [30Dec1994:30Dec1994]

02/02/05 25Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Caps Can Still Outperform. Bulls Argue… The Fed may have to drop their tightening regimen if 10-year rates

keep declining and that will be bullish for small-caps

The Yield Curve from Jun 30, 2004 to Today. Flattening with Risk of Inverting. Sm-Cap Valuation Expands?

Source: LehmanLive.com

N U G G E T T A G : u s e r N a m e = n u ll& p lo t N a m e = n u ll1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

YIE

LD

0 5Y 10Y 15Y 20Y 25Y 30Y

Source: LehmanLive.com

Fed begins hiking June 30 04. Seven months later 10-year rates are 47 bp lower AND small-caps have outperformed by 2.8%, rising 5.2%, even after the J anuary 2005 losses.

The Fed will control small-cap's fate

10.0Y, 4.22:J an 24 05 [Close:24J an2005]

10.0Y, 4.76:J une 30 04 [30J un2004:30J un2004]

10.0Y, 4.26:Sept 30 04 [30Sep2004:30Sep2004]

02/02/05 26Jim Furey – Lehman Brothers Small-Cap Strategy

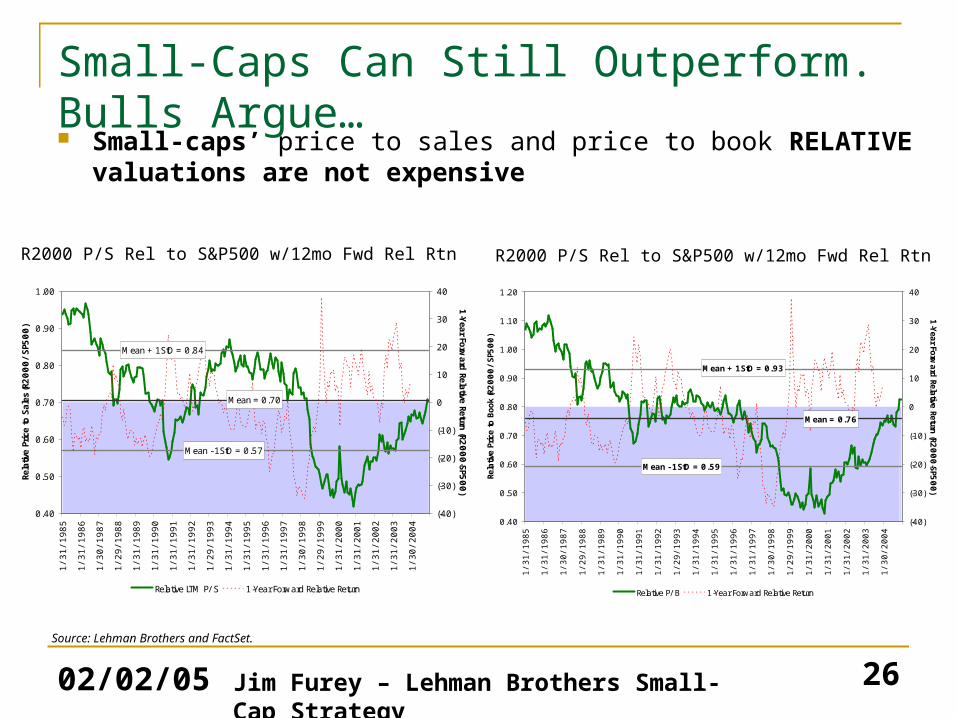

Small-Caps Can Still Outperform. Bulls Argue… Small-caps’ price to sales and price to book RELATIVE valuations

are not expensive

R2000 P/S Rel to S&P500 w/12mo Fwd Rel Rtn

Source: Lehman Brothers and FactSet.

R2000 P/S Rel to S&P500 w/12mo Fwd Rel Rtn

Mean + 1StD = 0.84

Mean = 0.70

Mean - 1StD = 0.57

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1/

31/

1985

1/

31/

1986

1/

30/

1987

1/

29/

1988

1/

31/

1989

1/

31/

1990

1/

31/

1991

1/

31/

1992

1/

29/

1993

1/

31/

1994

1/

31/

1995

1/

31/

1996

1/

31/

1997

1/

30/

1998

1/

29/

1999

1/

31/

2000

1/

31/

2001

1/

31/

2002

1/

31/

2003

1/

30/

2004

Rela

tive

Pric

e to

Sal

es (R2

000/SP

500)

(-40)

(-30)

(-20)

(-10)

0

10

20

30

40

1-Year Forw

ard Relative Return (R2000-SP5

00)

Relative LTM P/ S 1-Year Forward Relative Return

Mean + 1StD = 0.93

Mean = 0.76

Mean - 1StD = 0.59

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1/

31/

1985

1/

31/

1986

1/

30/

1987

1/

29/

1988

1/

31/

1989

1/

31/

1990

1/

31/

1991

1/

31/

1992

1/

29/

1993

1/

31/

1994

1/

31/

1995

1/

31/

1996

1/

31/

1997

1/

30/

1998

1/

29/

1999

1/

31/

2000

1/

31/

2001

1/

31/

2002

1/

31/

2003

1/

30/

2004

Rela

tive

Pric

e to

Boo

k (R

2000/SP

500)

(-40)

(-30)

(-20)

(-10)

0

10

20

30

40

1-Y

ear Forw

ard

Relative Return (R2

000-SP5

00)

Relative P/ B 1-Year Forward Relative Return

02/02/05 27Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Caps Can Still Outperform. Bulls Argue… Other factors support further small-cap outperformance

Large-cap Healthcare’s larger weight in the S&P 500 and its struggle with new drug discovery sufficient to replace patent expiration,

Large-cap Technology’s high S&P 500 weight and its vulnerability to “High Productivity, Low Barrier Era” pressures,

Currently bullish tax policy with low favorable capital gains,

Hedge & Quant funds’ affinity for small-caps

Positive 2005 relative earnings strength

Small-caps being “more local and less global”

Real Fed Funds may not turn positive until Fed Funds reach 3.0%, indicating monetary policy remains stimulative

02/02/05 28Jim Furey – Lehman Brothers Small-Cap Strategy

Small-Caps at Risk but Not Rolling Over To Summarize, the Bearish & Bullish Arguments:

The Bearish RELATIVE performance data points Why small-caps may lead another six to 12 months

Chatter that 2005 mirrors 1994 when Real Fed Funds crossed into positive territory

“High Productivity, Low Barrier Era” forces favor small-caps

Large early 2005 nominal and relative small-cap losses 2005 small-cap relative and nominal losses are small in context

The Fed talking more “hawkishly” REAL 10-year US Government rates remain below 2.5%

Declining 10 to 2-year US Government spreads NOMINAL 10-year US Government rates are below 5.0%

Lg-cap relative PEs are at the low end of their historic range Fed may stop raising rates earlier than the consensus believes

Small-caps are expensive nominally Real Fed Funds may not turn positive until Fed Funds reach 3%

P/ S and P/ B RELATIVE valuations are not expensive

29Jim Furey – Lehman Brothers Small-Cap Strategy

Our Approach to Small-Cap Decision Making

02/02/05 30Jim Furey – Lehman Brothers Small-Cap Strategy

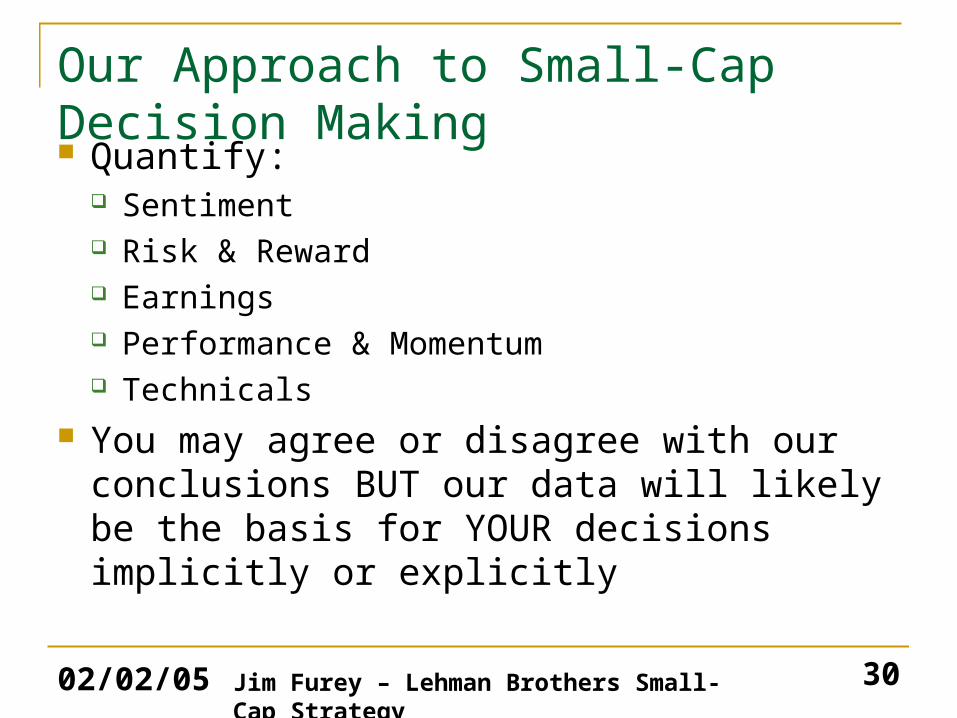

Our Approach to Small-Cap Decision Making Quantify:

Sentiment Risk & Reward Earnings Performance & Momentum Technicals

You may agree or disagree with our conclusions BUT our data will likely be the basis for YOUR decisions implicitly or explicitly

02/02/05 31Jim Furey – Lehman Brothers Small-Cap Strategy

Sector Performance/Momentum

Nominal Performance Forced Performance Ranking Nominal Change in Forced Ranking of RankingsINDUSTRY 12 Mo 6 Mo 3 Mo 1 Mo 12 Mo 6 Mo 3 Mo 1 Mo 12 - 6 Mo 6 -3 Mo 3 -1 Mo Perf. ChangeConsumer Discretionary 11.1 9.4 7.3 -5.1 5 10 6 5 -5 4 1 6 8Consumer Staples 20.7 14.9 12.4 -1.0 3 4 2 2 -1 2 0 3 4Energy 56.2 26.3 14.1 2.1 1 1 1 1 0 0 0 1 6Financials 9.2 11.1 3.1 -6.1 6 7 9 6 -1 -2 3 8 7Health Care -0.3 11.5 7.1 -7.2 9 6 7 9 3 -1 -2 9 3Industrials 16.3 14.1 9.3 -6.7 4 5 4 8 -1 1 -4 4 9Information Technology -13.7 9.4 1.1 -10.4 10 9 10 10 1 -1 0 10 5Materials 34.8 17.0 9.0 -6.3 2 2 5 7 0 -3 -2 2 10Telecommunications 0.1 15.9 9.5 -5.1 8 3 3 4 5 0 -1 7 1Utilities 9.0 11.0 5.9 -2.7 7 8 8 3 -1 0 5 5 2

R2000 -- Avg. 6.1 12.4 8.7 -5.9

R2000 -- Med. 3.0 9.3 6.1 -6.0

Russell 2000 Sector Performance and Momentum

Source: Lehman Brothers and Baseline

02/02/05 32Jim Furey – Lehman Brothers Small-Cap Strategy

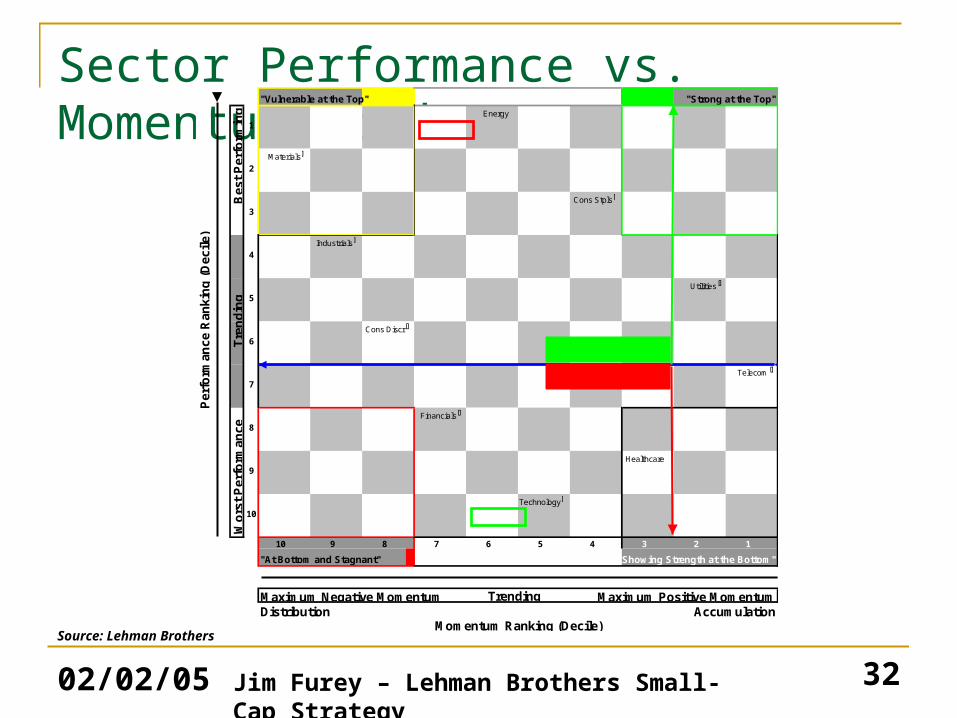

Sector Performance vs. Momentum Grid

"Vulnerable at the Top" "Strong at the Top"

Energy

1

Materialsf

2

Cons Stplsf

3

Industrialsf

4

Utilities f

5

Cons Discr f

6

Telecom f

7

Financials f

8

Healthcare

9

Technologyf

10

10 9 8 7 6 5 4 3 2 1

"At Bottom and Stagnant" "Showing Strength at the Bottom"

Maximum Negative Momentum Maximum Positive MomentumDistribution Accumulation

Momentum Ranking (Decile)

Pe

rfo

rma

nce

Ran

kin

g (

Dec

ile)

Wo

rst

Per

form

ance

Be

st P

erfo

rmin

gT

ren

din

g

Trending

Underperforming

Outperforming

Source: Lehman Brothers

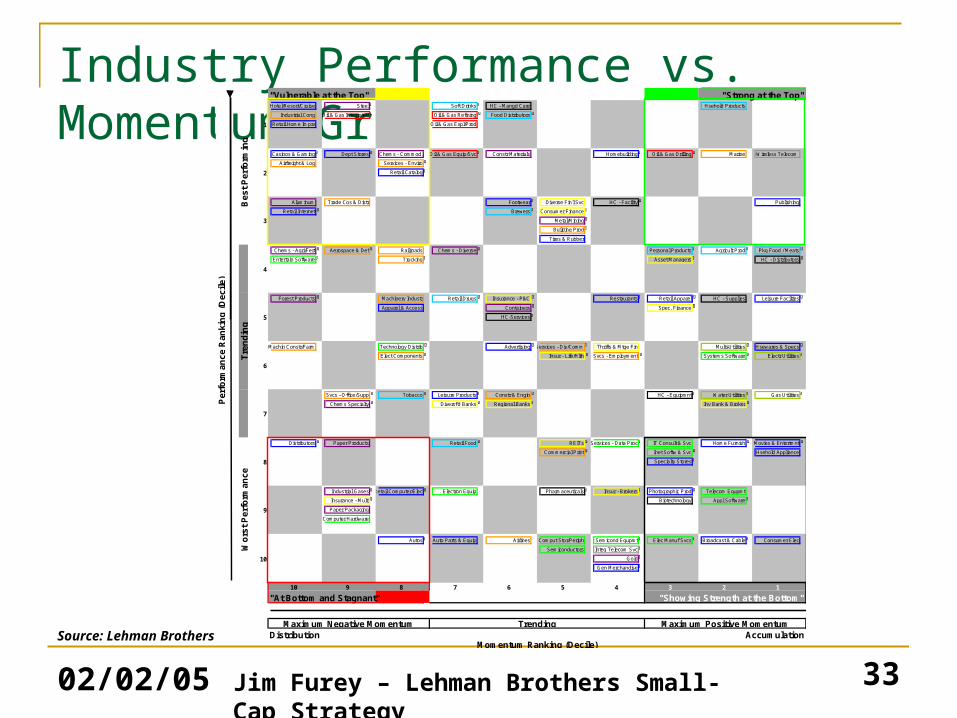

02/02/05 33Jim Furey – Lehman Brothers Small-Cap Strategy

Industry Performance vs. Momentum Grid

"Vulnerable at the Top" "Strong at the Top"Hotel/Resort/Cruise Steel f Soft Drinks f HC - Mangd Care Hsehold Products

Industrial Cong Oil & Gas Integrated f Oil & Gas Refining f Food Distributors f

Retail Home Imprv Oil & Gas Expl/Prod

Casinos & Gaming f Dept Stores f Chems - Commod. Oil & Gas Equip/Svc f Constr Materials Homebuilding f Oil & Gas Drilling f Marine Wireless Telecom

Airfreight & Log Services - Enviro f

Retail Catalog f

Aluminum Trade Cos & Distr Footwear f Diverse Fin'l Svc HC - Facility f Publishing

Retail Internet f Brewers f Consumer Finance f

Metal/Mining f

Building Prod f

Tires & Rubber

Chems - Agri/Fert f Aerospace & Def f Railroads Chems - Diverse f Personal Products f Agricult Prod f Pkg Food / Meats f

Entertain Software f Trucking f Asset Managers f HC - Distributors f

Forest Products f Machinery Industr Retail Drugs f Insurance - P&C f Restaurants f Retail Apparel f HC - Supplies Leisure Facilties f

Apparel & Access Containers f Spec. Finance f

HC-Services f

Machin Constr/Farm Technology Distrib f Advertising f Services - Div/Comm f Thrifts & Mtge Fin Multi-Utilities f Hsewares & Specs f

Elect Components f Insur - Life/Hlth f Svcs - Employment f Systems Software f Electr Utilities f

Svcs - Office/Supp f Tobacco f Leisure Products f Constr & Engin f HC - Equipmnt f Water Utilities f Gas Utilities f

Chems Specialty f Diversf'd Banks f Regional Banks f Inv Bank & Broker f

Distributors f Paper Products Retail Food f REITs f Services - Data Proc f IT Consult & Svc Home Furnish f Movies & Entertmnt f

Commercial Print f Inet Softw & Svc f Hsehold Appliance

Specialty Stores f

Industrial Gases f Retail Computer/Elec f Electron Equip Pharmaceuticals f Insur - Brokers f Photographic Prod f Telecom Equpmt

Insurance - Multi f Biotechnology Appl Software f

Paper Packaging

Computer Hardware

Autos f Auto Parts & Equip Airlines Comput Stor/Periph Semicond Equpmt f Elec Manuf Svcs f Broadcast & Cable f Consumer Elec

Semiconductors Integ Telecom Svc f

Gold f

Gen Merchandise f

10 9 8 7 6 5 4 3 2 1

"At Bottom and Stagnant" "Showing Strength at the Bottom"

Distribution AccumulationTrending Maximum Positive MomentumMaximum Negative Momentum

Momentum Ranking (Decile)

Pe

rfo

rman

ce R

anki

ng

(D

eci

le)

Bes

t P

erfo

rmin

gT

ren

din

gW

ors

t P

erfo

rma

nc

e

2

1

6

5

4

3

10

9

8

7

Source: Lehman Brothers

02/02/05 34Jim Furey – Lehman Brothers Small-Cap Strategy

Assigning Values to Perf. vs. Mom. Grid 1/28/2005

Underweight Neutral Overweight

Information Technology Consumer Discretionary Utilities

Telecommunication Services Financials Energy

Materials Health Care Consumer Staples

Industrials

Index Sector

Consumer Discretionary- Neu 15.1% 100.0%Advertising 0.6% 4.3% Advertising Apparel Accessories & Luxury Goods 0.7% 4.4% Apparel & Lux Gds

Apparel Retail 1.3% 8.4% Apparel RetailAuto Parts & Equipment 0.7% 4.5% Auto Parts & Equipment Automobile Manufacturers 0.3% 2.0% Automobile Manufacturers Broadcasting & Cable TV 0.7% 4.6% Broadcasting & Cable TV Casinos & Gaming 1.2% 7.7% Casinos & GamingCatalog Retail 0.3% 1.8% Catalog RetailComputer & Electronics Retail 0.1% 0.7% Computer & Electronics Retail Consumer Electronics 0.0% 0.1% Consumer Electronics Department Stores 0.0% 0.1% Department StoresDistributors 0.1% 0.9% Distributors Footw ear 0.4% 2.4% Footw earGeneral Merchandise Stores 0.3% 1.7% Home Furnishings 0.4% 2.9% Home Furnishings Home Improvement Retail 0.0% 0.3% Home Improvement RetailHomebuilding 0.8% 5.0% HomebuildingHotels Resorts & Cruise Lines 0.4% 2.7% Hotels Resorts & CruiseHousehold Appliances 0.0% 0.1% Household AppliancesHousew ares & Specialties 0.7% 4.7% Housew ares & SpecialtiesInternet Retail 0.2% 1.4% Internet Retail Leisure Facilities 0.2% 1.1% Leisure FacilitiesLeisure Products 0.7% 4.5% Leisure Products Movies & Entertainment 0.2% 1.1% Movies & EntertainmentPublishing 0.9% 5.7% PublishingRestaurants 1.8% 11.9% RestaurantsSpecialty Stores 1.8% 12.3% Specialty Stores Tires & Rubber 0.4% 2.7% Tires & Rubber

Consumer Staples- OW 2.8% 100.0%Agricultural Products 0.3% 12.3% Agricultural ProductsBrew ers 0.0% 0.7% Brew ersDistillers & Vintners 0.0% 0.2% Drug Retail 0.2% 6.3% Drug Retail Food Distributors 0.3% 12.4% Food DistributorsFood Retail 0.3% 10.7% Food Retail Household Products 0.2% 8.3% Household ProductsPackaged Foods & Meats 0.8% 27.2% Packaged Foods & MeatsPersonal Products 0.4% 13.0% Personal ProductsSoft Drinks 0.0% 1.7% Soft DrinksTobacco 0.2% 7.1% Tobacco

Energy- OW 5.9% 100.0%Integrated Oil & Gas 0.0% 0.5% Integrated Oil & GasOil & Gas Drilling 0.5% 8.9% Oil & Gas DrillingOil & Gas Equipment & Services 1.7% 29.6% Oil & Gas Equip & ServicesOil & Gas Exploration & Production 3.0% 51.1% Oil & Gas Expl & Production

0.6% 9.9% Oil & Gas Refin, Mkt & Transp

Financials- Neu 22.0% 100.0%Asset Management & Custody Banks 0.6% 2.7% Asset ManagementConsumer Finance 0.4% 1.9% Consumer FinanceInsurance Brokers 0.2% 0.7% Insurance Brokers

Investment Banking & Brokerage 0.4% 1.8% Investment Bank & BrokLife & Health Insurance 0.7% 3.2% Life & Health Insurance Multi-line Insurance 0.1% 0.3% Multi-line Insurance Property & Casualty Insurance 1.6% 7.2% Prop & Casualty Insurance Real Estate Investment Trusts 7.0% 32.0% REITs Real Estate Management & Development 0.4% 1.9% Real Estate Mgmt & DevRegional Banks 7.8% 35.5% Regional Banks Reinsurance 0.0% 0.1% Specialized Finance 0.3% 1.2% Specialized FinanceThrifts & Mortgage Finance 2.6% 11.7% Thrifts & Mortgage Finance

Health Care- Neu 12.6% 100.0%Biotechnology 3.3% 26.0% Biotechnology Health Care Distributors 0.2% 1.9% Health Care DistributorsHealth Care Equipment 2.7% 21.8% Health Care Equipment Health Care Facilities 1.1% 9.1% Health Care FacilitiesHealth Care Services 1.7% 13.9% Health Care Services Health Care Supplies 1.1% 8.9% Health Care SuppliesManaged Health Care 0.8% 6.2% Managed Health CarePharmaceuticals 1.6% 12.4% Pharmaceuticals

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

-1 -1 -1 1 1 1 1 1 1 1

-1 -1 -1 -1 1 1 1 1 1 1

-1 -1 -1 -1 1 1 1 1 1 1

-1 -1 -1 -1 -1 -1 1 1 1 1

-1 -1 -1 -1 -1 -1 -1 1 1 1

Per

form

ance

MomentumSource: Lehman Brothers

02/02/05 35Jim Furey – Lehman Brothers Small-Cap Strategy

“Voice of the Small-Cap Market”1/28/2005

Underweight Neutral Overweight

Information Technology Consumer Discretionary Utilities

Telecommunication Services Financials Energy

Materials Health Care Consumer Staples

Industrials

Index Sector

Industrials- Neu 14.3% 100.0%Aerospace & Defense 1.5% 10.6% Aerospace & Defense Air Freight & Logistics 0.3% 1.9% Air Freight & LogisticsAirlines 0.5% 3.7% Airlines Building Products 0.9% 6.6% Building ProductsCommercial Printing 0.3% 2.4% Commercial Printing Construction & Engineering 0.7% 4.8% Construction & Engineering Construction & Farm Machinery & Heavy Trucks1.1% 7.7% Constr & Farm Machinery Diversif ied Commercial Services 2.0% 14.0% Divers Commercial Svcs Electrical Components & Equipment 1.2% 8.1% Electrical Components & Eq Employment Services 0.5% 3.7% Employment Services Environmental Services 0.3% 2.1% Environmental ServicesIndustrial Conglomerates 0.2% 1.2% Industrial ConglomeratesIndustrial Machinery 2.2% 15.4% Industrial Machinery Marine 0.3% 1.9% MarineOffice Services & Supplies 0.4% 2.8% Office Services & Supplies Railroads 0.3% 1.9% Railroads Trading Companies & Distributors 0.3% 2.4% Trading Co & DistributorsTrucking 1.3% 8.9% Trucking

Information Technology - UW 16.8% 100.0%Application Softw are 2.5% 15.0% Application Softw are Communications Equipment 2.0% 11.7% Communications Equipment Computer Hardw are 0.4% 2.6% Computer Hardw are Computer Storage & Peripherals 1.3% 7.5% Computer Storage & Periphs

0.6% 3.6% Data Processing Svcs Electronic Equipment Manufacturers 1.5% 9.2% Electronic Equipment Manuf Electronic Manufacturing Services 0.7% 4.1% Electronic Manufacturing Services Home Entertainment Softw are 0.3% 1.7% Internet Softw are & Services 2.3% 13.7% Internet Softw are & Services IT Consulting & Other Services 1.2% 7.0% IT Consulting & Other Services Semiconductor Equipment 1.3% 7.6% Semiconductor Equipment Semiconductors 1.7% 10.2% Semiconductors Systems Softw are 0.7% 4.2% Systems Softw areTechnology Distributors 0.3% 2.1% Technology Distributors

Materials - UW 6.1% 100.0%Aluminum 0.1% 1.3% Aluminum Commodity Chemicals 0.3% 5.1% Commodity ChemicalsConstruction Materials 0.4% 6.2% Construction MaterialsDiversif ied Chemicals 0.4% 7.3% Diversif ied Chemicals Diversif ied Metals & Mining 0.3% 4.1% Diversif ied Metals & Mining

Fertilizers & Agricultural Chemicals 0.2% 3.6% Fertilizers & Agri Chemicals Forest Products 0.0% 0.6% Forest Products Gold 0.0% 0.4% Gold Industrial Gases 0.1% 2.2% Industrial Gases Metal & Glass Containers 0.5% 8.7% Metal & Glass Containers Paper Packaging 0.2% 3.8% Paper Packaging Paper Products 0.3% 5.3% Paper Products Precious Metals & Minerals 0.2% 2.9% Specialty Chemicals 1.5% 25.2% Specialty Chemicals Steel 1.4% 23.3% Steel

Telecommunication Services - UW 1.0% 100.0%Integrated Telecommunication Services 0.5% 48.3% Integrated Telecom Svcs Wireless Telecommunication Services 0.5% 51.7% Wireless Telecom Svcs

Utilities- OW 3.4% 100.0%Electric Utilities 1.2% 34.7% Electric UtilitiesGas Utilities 1.4% 40.1% Gas UtilitiesMulti-Utilities & Unregulated Pow er 0.7% 20.1% Multi-Utilities & Unreg Pow erWater Utilities 0.2% 5.1% Water Utilities

Weight Within:

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

1 1 1 1 1 1 1 1 1 1

-1 -1 -1 1 1 1 1 1 1 1

-1 -1 -1 -1 1 1 1 1 1 1

-1 -1 -1 -1 1 1 1 1 1 1

-1 -1 -1 -1 -1 -1 1 1 1 1

-1 -1 -1 -1 -1 -1 -1 1 1 1

Per

form

ance

Momentum

Source: Lehman Brothers and FactSet

36Jim Furey – Lehman Brothers Small-Cap Strategy

Thank You.

Jim Furey, CFA, Managing DirectorLehman Brothers Small-Cap Strategy

212.526.7715; [email protected]

02/02/05 37Jim Furey – Lehman Brothers Small-Cap Strategy

Analyst CertificationI, James Furey, hereby certify (1) that the views expressed in this research email accurately reflect my personal views about any or all of the subject securities or

issuers referred to in this email and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this email.

Lehman Brothers does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this email communication.

Investors should consider this communication as only a single factor in making their investment decision.

Important Disclosures:

The analysts responsible for preparing this report have received compensation based upon various factors including the Firm’s total revenues, a portion of which is generated by investment banking activities.

Stock price and ratings history charts along with other important disclosures are available on our disclosure website at www.lehman.com/disclosures

And may also be obtained by sending a written request to: LEHMAN BROTHERS CONTROL ROOM , 745 SEVENTH AVENUE, 19TH FLOOR NEW YORK, NY 10019

This material has been prepared and/or issued by Lehman Brothers Inc., member SIPC, and/or one of its affiliates ("Lehman Brothers") and has been approved by Lehman Brothers International (Europe), authorized and regulated by the Financial Services Authority, in connection with its distribution in the European Economic Area. This material is distributed in Japan by Lehman Brothers Japan Inc., and in Hong Kong by Lehman Brothers Asia Limited. This material is distributed in Australia by Lehman Brothers Australia Pty Limited, and in Singapore by Lehman Brothers Inc., Singapore Branch. This material is distributed in Korea by Lehman Brothers International (Europe) Seoul Branch. This document is for information purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy the securities or other instruments mentioned in it. No part of this document may be reproduced in any manner without the written permission of Lehman Brothers. With the exception of disclosures relating to Lehman Brothers, this research report is based on current public information that Lehman Brothers considers reliable, but we make no representation that it is accurate or complete, and it should not be relied on as such. In the case of any disclosure to the effect that Lehman Brothers Inc. or its affiliates beneficially own 1% or more of any class of common equity securities of the subject company, the computation of beneficial ownership of securities is based upon the methodology used to compute ownership under Section 13(d) of the United States' Securities Exchange Act of 1934. In the case of any disclosure to the effect that Lehman Brothers Inc. and/or its affiliates hold a short position of at least 1% of the outstanding share capital of a particular company, such disclosure relates solely to the ordinary share capital of the company. Accordingly, while such calculation represents Lehman Brothers' holdings net of any long position in the ordinary share capital of the company, such calculation excludes any rights or obligations that Lehman Brothers may otherwise have, or which may accrue in the future, with respect to such ordinary share capital. Similarly such calculation does not include any shares held or owned by Lehman Brothers where such shares are held under a wider agreement or arrangement (be it with a client or a counterparty) concerning the shares of such company (e.g. prime broking and/or stock lending activity). Any such disclosure represents the position of Lehman Brothers as of the last business day of the calendar month preceding the date of this report.

This material is provided with the understanding that Lehman Brothers is not acting in a fiduciary capacity. Opinions expressed herein reflect the opinion of Lehman Brothers and are subject to change without notice. The products mentioned in this document may not be eligible for sale in some states or countries, and they may not be suitable for all types of investors. If an investor has any doubts about product suitability, he should consult his Lehman Brothers representative. The value of and the income produced by products may fluctuate, so that an investor may get back less than he invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Past performance is not necessarily indicative of future results. If a product is income producing, part of the capital invested may be used to pay that income. © 2005 Lehman Brothers. All rights reserved. Additional information is available on request. Please contact a Lehman Brothers entity in your home jurisdiction.

Lehman Brothers policy for managing conflicts of interest in connection with investment research is available at www.lehman.com/researchconflictspolicy. Ratings, earnings per share forecasts and price targets contained in the Firm's equity research reports covering U.S. companies are available at www.lehman.com/disclosures.