jll’s global market perspective report - jll. · pdf filethe pace of improvement in the...

TRANSCRIPT

[Type text]

Real Estate Markets Thrive

Despite Economic Headwinds

Global Market Perspective | Q3 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 2

Global Market Perspective, Third Quarter 2015

Global Market Perspective

Contents

Real Estate Markets Thrive despite Economic Headwinds ........................................................................................... 3

Global Economy ................................................................................................................................................................ 6

Real Estate Capital Markets ............................................................................................................................................. 8

Investment Volumes ............................................................................................................................................................ 8

Capital Values and Yields ................................................................................................................................................. 13

Corporate Occupiers ...................................................................................................................................................... 14

Global Real Estate Health Monitor ................................................................................................................................. 16

Office Markets ................................................................................................................................................................. 17

Office Demand Dynamics ................................................................................................................................................. 17

Office Supply Trends ......................................................................................................................................................... 20

Office Rental Trends ......................................................................................................................................................... 23

Retail Markets .................................................................................................................................................................. 26

Industrial Warehousing Markets .................................................................................................................................... 28

Hotel Markets ................................................................................................................................................................... 29

Residential Markets ........................................................................................................................................................ 32

Key Investment Transactions in Q2 2015 ..................................................................................................................... 35

Illustrative Office Occupational Transactions in Q2 2015 ........................................................................................... 39

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 3

Real Estate Markets Thrive despite Economic Headwinds

Investment and occupational markets move in tandem

Momentum continues to build in the world’s major commercial real estate markets and, for the first time in the current

cycle, growth in leasing activity has matched that of investment. Significantly, office leasing volumes are at their highest

level for more than three years, with healthy uplifts recorded across all three global regions. Meanwhile, investor

appetite for real estate shows no signs of abating, with a potential Grexit, China stock market volatility and expectations

of rising U.S. interest rates doing little to knock real estate investment off its stride.

Investors push yields to new lows

Investment activity has continued to expand vigorously. Volumes during the first half of the year, at US$177 billion, were

9% up on H1 2014 and an impressive 19% higher when denominated in local currencies. Larger single-asset and

portfolio deals are now a regular feature of the dominant markets. The weight of money is still pushing yields to new

lows, with yields compressing at their fastest pace for five years.

Prime Office Yields, 2007-2015

*20 Major Office Markets

Source: JLL, July 2015

The U.S. has been the standout investment market, with year-to-date volumes increasing 29% on 2014. Germany and

the UK have also registered a strong first half of the year, while China has bounced back robustly during Q2. Investor

demand is high in Australia and Japan, but activity in these markets has been constrained by a lack of product.

The ‘Super Cities’ shine

Investor demand for prime assets in the ‘Super Cities’ has reached new heights, with New York and London having

their busiest first half of the year since 2006, accounting for a record 15% of global activity. Their scale, liquidity,

transparency and ‘safe haven’ attributes are attracting significant capital from sovereign wealth funds, global institutions

and HNWIs.

4.8

5.2

5.6

6.0

6.4

6.8

7.2

-40-30-20-10

010203040506070

Q12007

Q22007

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Mean Prime Office Yields*

5.50%

4.94%

Yield Compression (bps)

%

bps

6.92%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 4

Global Market Perspective, Third Quarter 2015

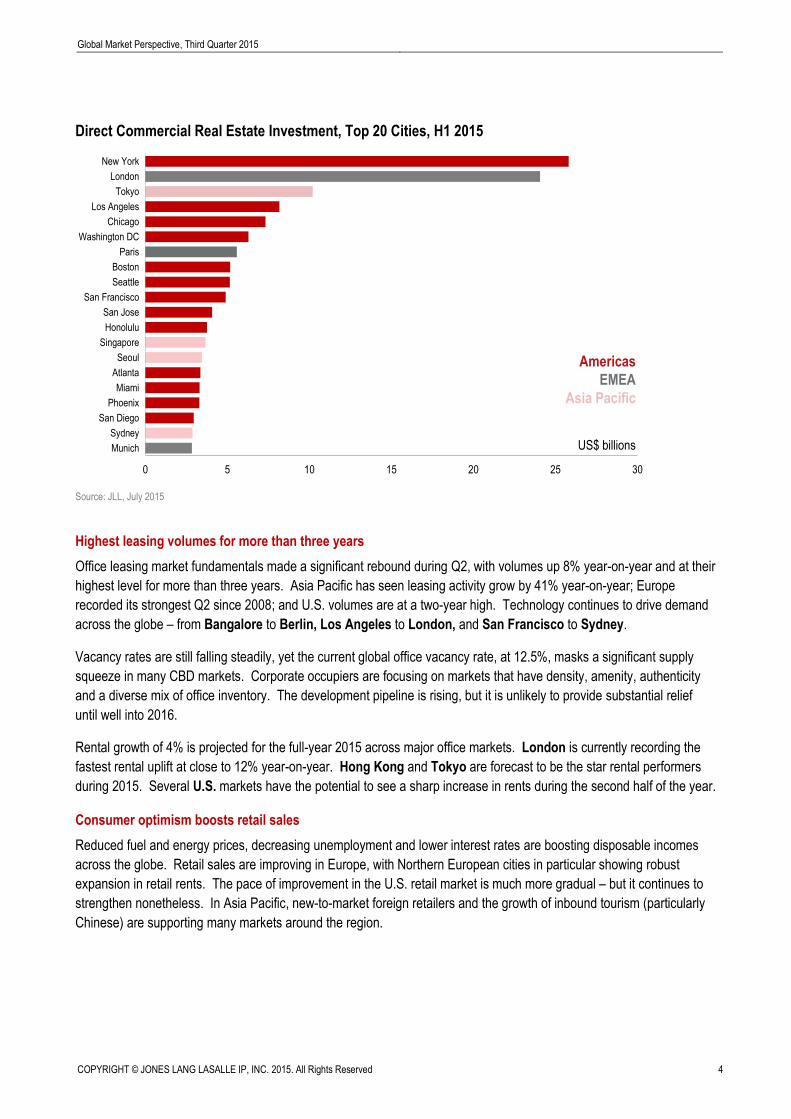

Direct Commercial Real Estate Investment, Top 20 Cities, H1 2015

Source: JLL, July 2015

Highest leasing volumes for more than three years

Office leasing market fundamentals made a significant rebound during Q2, with volumes up 8% year-on-year and at their

highest level for more than three years. Asia Pacific has seen leasing activity grow by 41% year-on-year; Europe

recorded its strongest Q2 since 2008; and U.S. volumes are at a two-year high. Technology continues to drive demand

across the globe – from Bangalore to Berlin, Los Angeles to London, and San Francisco to Sydney.

Vacancy rates are still falling steadily, yet the current global office vacancy rate, at 12.5%, masks a significant supply

squeeze in many CBD markets. Corporate occupiers are focusing on markets that have density, amenity, authenticity

and a diverse mix of office inventory. The development pipeline is rising, but it is unlikely to provide substantial relief

until well into 2016.

Rental growth of 4% is projected for the full-year 2015 across major office markets. London is currently recording the

fastest rental uplift at close to 12% year-on-year. Hong Kong and Tokyo are forecast to be the star rental performers

during 2015. Several U.S. markets have the potential to see a sharp increase in rents during the second half of the year.

Consumer optimism boosts retail sales

Reduced fuel and energy prices, decreasing unemployment and lower interest rates are boosting disposable incomes

across the globe. Retail sales are improving in Europe, with Northern European cities in particular showing robust

expansion in retail rents. The pace of improvement in the U.S. retail market is much more gradual – but it continues to

strengthen nonetheless. In Asia Pacific, new-to-market foreign retailers and the growth of inbound tourism (particularly

Chinese) are supporting many markets around the region.

0 5 10 15 20 25 30

Munich

Sydney

San Diego

Phoenix

Miami

Atlanta

Seoul

Singapore

Honolulu

San Jose

San Francisco

Seattle

Boston

Paris

Washington DC

Chicago

Los Angeles

Tokyo

London

New York

Americas

EMEA

Asia Pacific

US$ billions

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 5

Realignment of logistics networks heightens demand

Continued innovation in order fulfilment and delivery is driving further adaption of logistics networks and heightening

demand in multimodal locations, for automated facilities and for facilities supporting efficient urban logistics. Demand is

also being boosted by a strengthening manufacturing sector. In the U.S., absorption is still outpacing new supply and

vacancy rates remain low. Likewise, vacancy is very low in Europe, but here speculative development is, as yet,

extremely limited.

Global hotel investment going from strength to strength

Global hotel transaction volumes have gone from strength to strength, reaching a new high of US$42 billion in H1 2015,

up 55% from the same period last year. Europe continues to be a magnet for foreign investment in hotel assets.

Investors from the Middle East and mainland China have been the major exporters of capital.

Robust appetite for institutional-grade residential product

Demand for institutional-grade residential product continues apace in many markets across the globe. In the U.S.,

multifamily investment sales momentum exceeds the 2007 peak; volumes are at record levels in Germany; and there is

growing investor appetite for institutional-grade rental product in the fledging UK market. Policy restrictions remain in

place in various Asian residential markets, but sales activity is slowly increasing and China has relaxed its down-

payment rules for buyers of second homes. Dubai has seen a notable decline in residential sales, but falls in prices

have been modest. Australia is also showing signs of capital growth moderation.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 6

Global Market Perspective, Third Quarter 2015

Global Economy

Global upswing still faces headwinds and Grexit risks remain

After a disappointing start to the year, it has been an unsettled quarter for the global economy. While there have been

more encouraging signs on economic activity in the advanced economies, most notably in the U.S. and the Eurozone,

lingering risks and uncertainties refuse to dissipate and continue to cloud the outlook. While few expect a reversal in the

slow revival, forecasts remain cautious for this year and there appears little prospect of an acceleration in global GDP

before 2016.

A last-minute deal for Greece was passed in July that included controversial austerity measures. The schedule for

securing funding is tight and, although progress has been made, the Grexit danger has still not disappeared. Creditors

will be demanding further market reforms to improve economic performance which will likely be difficult for the Greek

administration to accept, particularly as debt relief seems to be off-the-table in the near term.

While Greece dominated headlines for much of July, a sharp sell-off in Chinese equities has also reminded investors

about the risks to financial stability in the world’s second largest economy. The reaction of the Chinese authorities was

swift, but also interventionist, raising further concerns about the depth of market reforms in China.

These global uncertainties have been reflected in a patchy set of forecast revisions over the last three months. The U.S.

and UK have received downgrades, though this largely reflects historic weakness and more recent news has been more

upbeat. Similarly, Germany has also suffered from a poorer-than-expected Q1 and a subsequent downgrade to the

year’s outlook, though this contradicts the improving tone of most other Eurozone data, including figures from France.

Of the few of our focus markets to be upgraded, Japan has received the most notable boost.

GDP Projections for 2015 in Major Economies – Recent Movements

Australia China France Germany India Japan UK U.S.

April 2.7 6.6 1.2 2.4 7.5 0.8 2.8 2.7

July (Latest) 2.6 6.6 1.3 1.9 7.5 1.0 2.6 2.3

Change (bps) -10 0 +10 -50 0 +20 -20 -40

Source: Oxford Economics, July 2015

Bumpy ride for Eurozone bonds, while U.S. tightening moves ever closer

After the ECB’s QE announcement in Q1, European monetary developments have been dominated by its

implementation from March. The initial impact of the liquidity injection in the Eurozone was falling bond rates, but this

trend was reversing by the summer as a result of receding deflation fears. Since then there has been considerable

volatility, including a slight increase of peripheral Eurozone spreads (Spain, Portugal, Italy and Ireland, relative to

Germany) as contagion risk has heightened in the Greek crisis. Markets have calmed post-deal, while bond rates

remain at historically low levels with the 10-year bund rate still sub-1%.

Providing that the Eurozone situation stabilises, attention will shift back to the U.S. in Q3 with the impending Fed rate

hike. The U.S. is still expected to lead the tightening in global rates during 2015, but there continues to be intense

speculation about the timing. Events in Greece and China have provided a sobering reminder of global fragility and

were noted in recent FOMC notes, but are also set against improving U.S. data during Q2. The consensus remains that

U.S. rates will rise during Q3, probably in September. However, policymakers will continue to err on the side of caution if

there is any sign of uncertainty, and there is still a significant chance that the decision could be delayed.

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 7

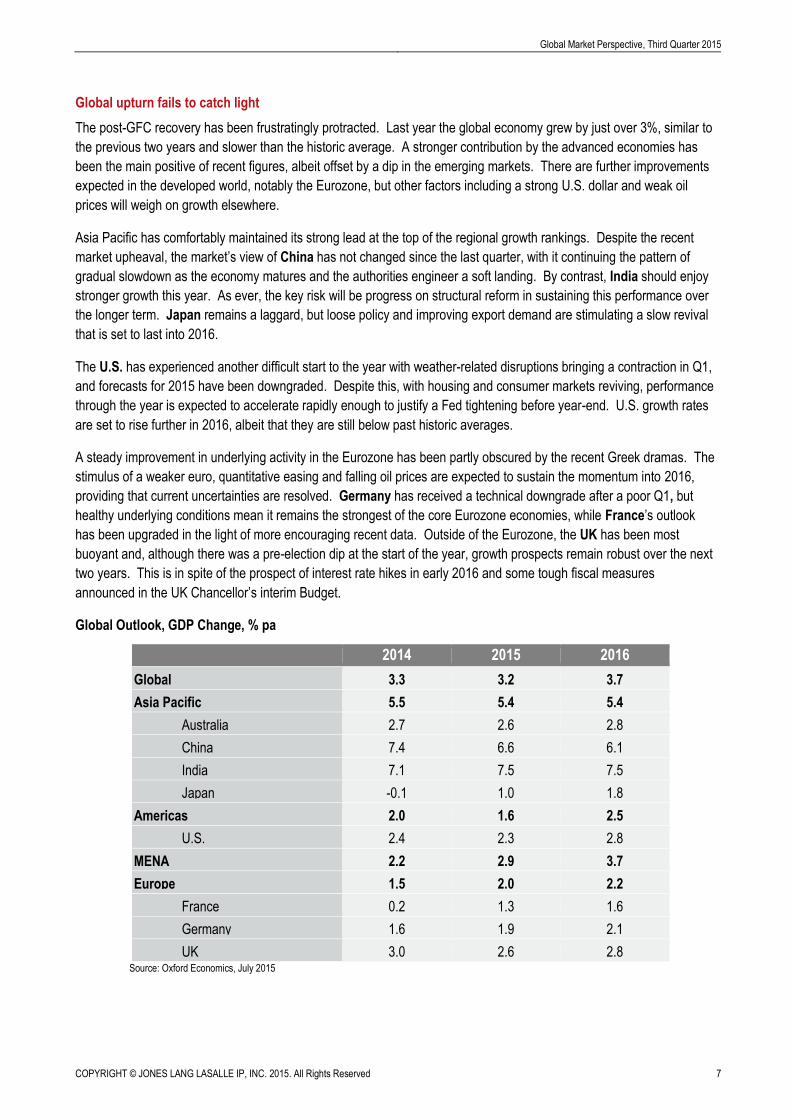

Global upturn fails to catch light

The post-GFC recovery has been frustratingly protracted. Last year the global economy grew by just over 3%, similar to

the previous two years and slower than the historic average. A stronger contribution by the advanced economies has

been the main positive of recent figures, albeit offset by a dip in the emerging markets. There are further improvements

expected in the developed world, notably the Eurozone, but other factors including a strong U.S. dollar and weak oil

prices will weigh on growth elsewhere.

Asia Pacific has comfortably maintained its strong lead at the top of the regional growth rankings. Despite the recent

market upheaval, the market’s view of China has not changed since the last quarter, with it continuing the pattern of

gradual slowdown as the economy matures and the authorities engineer a soft landing. By contrast, India should enjoy

stronger growth this year. As ever, the key risk will be progress on structural reform in sustaining this performance over

the longer term. Japan remains a laggard, but loose policy and improving export demand are stimulating a slow revival

that is set to last into 2016.

The U.S. has experienced another difficult start to the year with weather-related disruptions bringing a contraction in Q1,

and forecasts for 2015 have been downgraded. Despite this, with housing and consumer markets reviving, performance

through the year is expected to accelerate rapidly enough to justify a Fed tightening before year-end. U.S. growth rates

are set to rise further in 2016, albeit that they are still below past historic averages.

A steady improvement in underlying activity in the Eurozone has been partly obscured by the recent Greek dramas. The

stimulus of a weaker euro, quantitative easing and falling oil prices are expected to sustain the momentum into 2016,

providing that current uncertainties are resolved. Germany has received a technical downgrade after a poor Q1, but

healthy underlying conditions mean it remains the strongest of the core Eurozone economies, while France’s outlook

has been upgraded in the light of more encouraging recent data. Outside of the Eurozone, the UK has been most

buoyant and, although there was a pre-election dip at the start of the year, growth prospects remain robust over the next

two years. This is in spite of the prospect of interest rate hikes in early 2016 and some tough fiscal measures

announced in the UK Chancellor’s interim Budget.

Global Outlook, GDP Change, % pa

2014 2015 2016

Global 3.3 3.2 3.7

Asia Pacific 5.5 5.4 5.4

Australia 2.7 2.6 2.8

China 7.4 6.6 6.1

India 7.1 7.5 7.5

Japan -0.1 1.0 1.8

Americas 2.0 1.6 2.5

U.S. 2.4 2.3 2.8

MENA 2.2 2.9 3.7

Europe 1.5 2.0 2.2

France 0.2 1.3 1.6

Germany 1.6 1.9 2.1

UK 3.0 2.6 2.8 Source: Oxford Economics, July 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 8

Global Market Perspective, Third Quarter 2015

Real Estate Capital Markets

Investment Volumes

Deals are getting bigger and more sophisticated as volumes increase further

Transactional volumes in Q2 2015 were US$177 billion, which is 9% higher than the second quarter of 2014. On a year-

to-date basis, volumes at US$333 billion are also 9% higher than last year with larger deals and portfolios now a regular

feature of the investment market. However, the strength of the U.S. dollar over the first half of the year is masking the

true level of transactional activity around the world. This is particularly true for the Eurozone, UK, Japan, Australia and

South Korea where the dollar is between 10% and 20% stronger than a year ago. If fixed exchange rates were used,

then volumes would be up 19% globally over the first half of 2015 compared to 2014.

Threat of rising Fed rate yet to knock real estate off its stride

The United States continues to be the major driver of activity in the Americas and globally, with growth over 30% up on

Q2 last year and 29% higher than 2014’s first six months. This has helped increase regional volumes almost 20%, both

on a year-on-year and year-to-date basis, to US$153 billion. Elsewhere in the region, volumes in Canada are 6% down

year-to-date against 2014, with falls in Brazil and Mexico even more pronounced; both countries are circa 80% lower

than the first six months of 2014.

Potential Grexit and Brexit does little to disrupt investment in real estate assets

European volumes in local currency terms continue to move higher, up 28% on Q2 2014 and 26% on H1 2014. Growth

over the first half of the year has been spread region-wide with uplifts in the UK and Germany being supported by

increases in the Nordics and Southern Europe, despite the Greek turmoil. Even Russia is showing some signs of

renewed optimism with stronger levels of activity. In U.S. dollar terms, volumes are slightly higher both year-on-year and

over the first six months at US$124 billion, with the difference to local currency activity almost entirely due to foreign

exchange factors.

New York and London account for 15% of transactions globally

New York and London have witnessed one of their busiest first halves of the year, with US$26 billion and US$24 billion

transacted respectively. They stand head-and-shoulders above all other cities and, between them, accounted for 15% of

global transactions in H1 2015. Their scale and liquidity continues to attract capital, with global institutions, sovereign

wealth funds and HNWIs representing a notable share of buyers.

Stable first half with market-setting assets on the horizon to trade

Asia Pacific’s biggest markets of Japan and Australia are feeling the effects of the stronger U.S. dollar; both country’s

currencies are 15% weaker than the same period last year and this is also feeding through into weaker transactional

volumes for Australia. This has had the effect of depressing regional volumes by 2% compared to Q2 2014 but half-year

volumes are 2% higher than H1 2014 at US$56 billion. Regionally, the second half of the year looks as if it will be much

stronger than the first with a number of large transactions set to close in Singapore, Australia and China. Hong Kong

has been one of the bright spots over the first half with volumes up 66% year-on-year.

Structural shift in investment habits continues to support real estate investment

The second quarter of the year has been dominated by discussions around Greece’s role in the Eurozone and the

extreme volatility we have seen in equities in China. What has garnered less attention, but is probably more important,

is the continuing decline in global interest rates, with Sweden cutting its interest rate to minus 0.35% despite the

economy forecast to grow by 3% in 2015, and China also cutting rates for the fourth time since November 2014. This

decline in global interest rates makes real estate investment more attractive and should support transactional activity for

the remainder of 2015. The longer-term structural shift of institutional capital allocating more to real estate also

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 9

continues, with a recent PwC report estimating that alternative investments, including real estate, could reach US$15

trillion by 2020, up from US$8 trillion today. JLL maintains its full-year 2015 forecast at US$750-760 billion which

represents a 5% rise on 2014 transactional activity.

Direct Commercial Real Estate Investment – Regional Volumes, 2014-2015

Source: JLL, July 2015

Direct Commercial Real Estate Investment – Largest Markets, 2014-2015

Source: JLL, July 2015

REGIONS IN FOCUS

U.S. momentum builds further

The Americas region is well on pace to achieve a new high-water mark in 2015 – exceeding the record volumes seen

over the 2006-2007 period (on an ex-entity deal-level basis) and 20% higher than 2014. Growth is being entirely driven

by the U.S. market where there is a very active transaction pipeline across sectors and geographies.

A combination of attributes is continuing to make the U.S. commercial property market a highly sought-after destination

for capital placement for both domestic and global investors, including relative economic outperformance among

advanced economies, a broad ‘safe haven’ appeal, and attractive yield on offer against the backdrop of very low interest

rates worldwide. Of particular note is that large portfolio transactions are being increasingly pursued and, by extension,

this includes an increase in M&A activity among REITs and other property investment firms (although those transactions

are, by and large, not included in volumes cited in this report).

US$ billions Q1 15 Q2 15

% change

Q1 15-Q2 15 Q2 14

% change

Q2 14-Q2 15 YTD 2014 YTD 2015

% change

YTD 2014- YTD 2015

Americas 73 81 11% 67 20% 129 153 19%

EMEA 59 65 11% 63 3% 120 124 3%

Asia Pacific 25 31 24% 31 -2% 55 56 2%

TOTAL 156 177 13% 162 9% 304 333 9%

US$ billions Q1 15 Q2 15

% change

Q1 15-Q2 15 Q2 14

% change

Q2 14-Q2 15 YTD 2014 YTD 2015

% change

YTD 2014- YTD 2015

U.S. 69.5 75.7 9% 56.8 33% 112.7 145.3 29%

UK 23.7 24.4 3% 21.3 14% 43.3 48.1 11%

Germany 10.4 14.9 44% 8.6 72% 19.8 25.2 27%

China 2.6 7.9 210% 5.1 54% 8.1 10.5 29%

Japan 12.9 6.4 -50% 8.4 -23% 20.6 19.3 -6%

Australia 2.5 4.4 74% 7.8 -44% 11.9 6.9 -42%

Norway 1.8 4.2 128% 2.0 109% 2.8 6.0 115%

Hong Kong 1.0 3.8 284% 1.9 102% 2.9 4.8 66%

Canada 2.6 3.5 37% 2.8 28% 6.5 6.1 -6%

France 4.8 3.3 -32% 11.2 -70% 16.9 8.2 -52%

South Korea 0.7 3.2 329% 2.6 23% 3.4 3.9 13%

Sweden 1.8 2.9 58% 4.2 -33% 7.4 4.7 -37%

Netherlands 0.8 2.5 232% 2.9 -13% 4.9 3.3 -34%

Spain 2.6 2.2 -18% 2.0 6% 3.6 4.8 32%

Singapore 2.0 1.8 -8% 2.4 -24% 3.6 3.8 6%

Czech Republic 0.9 1.7 97% 0.5 219% 0.8 2.5 200%

Italy 2.3 1.6 -28% 1.4 21% 2.5 3.9 58%

Finland 0.8 1.3 59% 0.6 141% 1.4 2.2 60%

Malaysia 0.7 1.1 66% 0.4 172% 0.4 1.8 324%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 10

Global Market Perspective, Third Quarter 2015

Weaker investment activity across Latin America

Transaction activity remained far weaker in Latin America during the second quarter. Although both Brazil and Mexico

are subject to the ‘lumpiness’ of large individual and portfolio sales in their developing markets, there has nonetheless

been a marked slowing in deal velocity thus far in 2015. Brazil, in particular, is also being impacted by its recession and

property market downturn. Nevertheless, the second half of 2015 is likely to bring improved transaction activity to both

markets on a relative basis.

Direct Commercial Real Estate Investment – 2007-2015

Source: JLL, July 2015

Uncertainty drives investors to ‘safe haven’ asset classes in Europe

The euro has come under sustained pressure since the middle of last year due to a combination of expectations of a

return to the rate hike cycle in the U.S., an aggressive quantitative easing programme in Europe and, more recently,

concerns over the viability of the European project as a result of Greece’s debt crisis. Though the impact on the euro is

meaningful, if anything, the uncertainty in Europe has driven investors further towards ‘safe haven’ asset classes such

as real estate.

UK and Germany outperform as investors focus on core markets

The UK, Europe’s largest market, continues to perform strongly, rising by 26% year-on-year in local currency terms to

£15.9 billion, accounting for 37% of the region’s volumes. Activity in Germany has also been strong, with year-on-year

volumes more than doubling in euro terms to €13.4 billion.

Smaller European markets mixed in both local currency and U.S. dollar terms

Southern Europe has remained resilient in the second quarter, despite concerns over the future of Greece, with

investment up 16% year-on-year at US$4.5 billion driven by Portugal and Italy. Investment in the Nordics overall was

strong, with impressive increases in Finland and Norway, but volumes have fallen in Sweden. Volumes have also been

weaker in the Benelux. Activity in the CEE region was up over Q2 (66% year-on-year) to US$2.9 billion.

0

30

60

90

120

150

180

210

240

Q10

7

Q20

7

Q30

7

Q40

7

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Q40

9

Q11

0

Q21

0

Q31

0

Q41

0

Q11

1

Q21

1

Q31

1

Q41

1

Q11

2

Q21

2

Q31

2

Q41

2

Q11

3

Q21

3

Q31

3

Q41

3

Q11

4

Q21

4

Q31

4

Q41

4

Q11

5

Q21

5

Americas EMEA Asia Pacific Rolling Four-Quarter Average

US

$ bi

llion

s

205

107110100

113

7369666666

100

118120

159

204

190

119

91

110100

163

41 4335

108

124

146

211

142

162

175

231

156

177

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 11

Market to remain robust in Europe

While it is hard to draw conclusions from one quarter of data, investment activity across Europe remains robust. The

region does not yet show any signs of slowing down due to concerns about the future of Greece and its possible

exclusion from the euro. Indeed, Europe is still benefiting from low borrowing costs in its core markets, plentiful liquidity

and a continued move to ‘safe haven’ assets. JLL’s forecast for full-year 2015 is for a 5% increase on 2014 in euro

terms, which would signify a 10%-15% fall in U.S. dollar terms (at quarter-end exchange rates).

Asia Pacific still on track for record year

In general, the Asia Pacific investment market remains active with strong investor appetite demonstrated by a wave of

large transactions and the appearance of more trophy assets on the market over the past six months. Furthermore, the

region has witnessed an increase in portfolio transactions in H1 2015. Investment volumes are expected to pick up

significantly during the second half of the year; JLL maintains its forecast for transaction volumes of US$140 billion for

the full-year 2015, which translates to a year-on-year gain of 5%-10%.

Meanwhile, Asian debt markets experienced a period of volatility over the second quarter. New debt issues continue to

be present in most Asian markets but moderated in Q2 2015 as investors focused more on longer-term maturity fixed

rate bonds to avoid near-term refinancing risk.

Australia’s investment volumes constrained by lack of product

The limited availability of good-quality stock after several years of robust investment activity is constraining transactions

in Australia. Moreover, the sale of the Investa portfolio is diverting attention, with investors and vendors awaiting new

pricing from the sale before bringing assets to the market. Overseas investors, especially from Asia, continue to be

attracted to Australian assets, in part due to the weak Australian dollar and attractive yields.

Liquidity is high in Japan

The market in Japan was stable in local currency terms in H1 2015. There is still ample liquidity as more equity funds

were raised in Q2, and foreign investor demand remains at an unprecedented level on the back of a weak currency.

Regional leader China’s volumes up 54% year-on-year on more stimulus measures

China ranked first in investment volumes in the region during Q2 with volumes up 54% year-on-year. Sentiment in core

offices is improving in the country’s Tier 1 or top-end Tier 2 cities driven by sufficient liquidity from core and core-plus

funds looking for assets with strong yields. Lower interest rates and bank reserve requirement ratios are likely to reduce

the costs of borrowing going forward and may provide more upside for the real estate investment market. However, the

recent volatility seen in China’s equity market may potentially slow the investment decision process and lead to more

outbound investment.

ADIA’s hotel portfolio deal boosts Hong Kong volumes

In Hong Kong, transaction volumes for Q2 2015 more than doubled year-on-year largely due to the three-hotel property

portfolio platform deal between Abu Dhabi Investment Authority (ADIA) and New World Development for US$2.4 billion.

The high-profile acquisitions mark ADIA’s largest investment in Asia to date.

Investors struggle to access product in India

India’s transaction volumes in the second quarter were flat year-on-year, with access to stock remaining a barrier to

entry. Investors continue to prefer stabilised assets in the retail and logistics sectors and there is still abundance of

liquidity as new private equity funds look to take in India’s growth story.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 12

Global Market Perspective, Third Quarter 2015

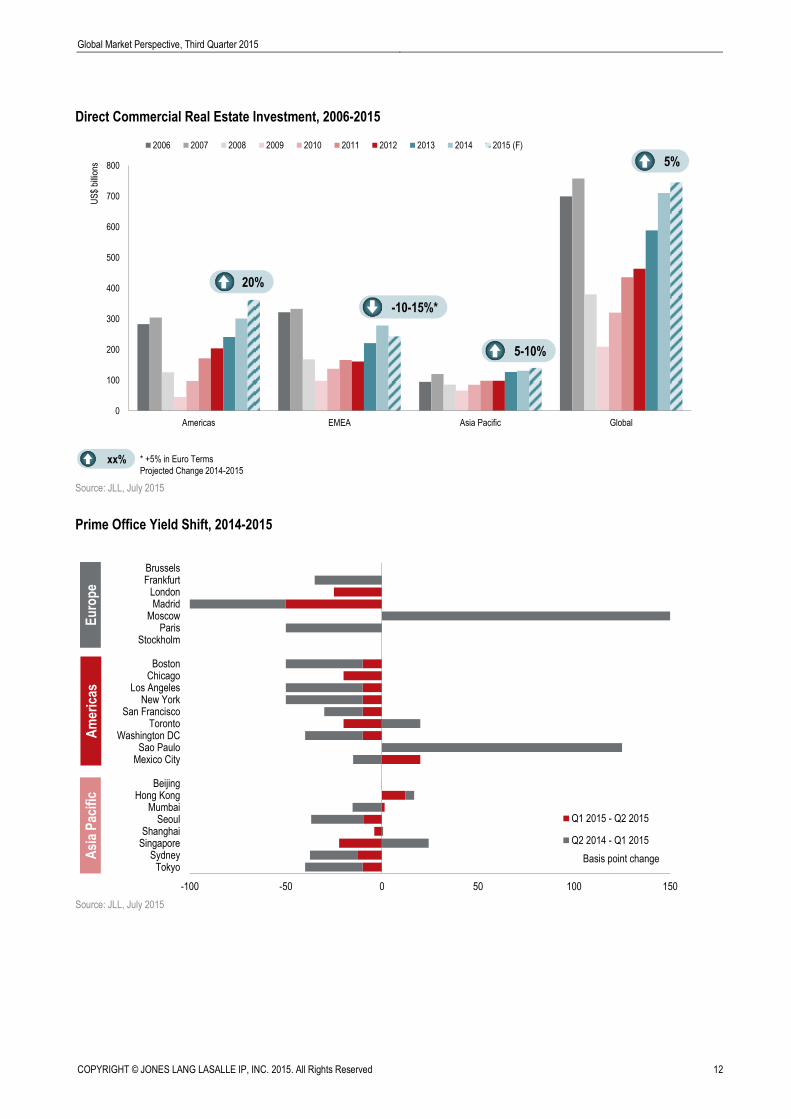

Direct Commercial Real Estate Investment, 2006-2015

Source: JLL, July 2015

Prime Office Yield Shift, 2014-2015

Source: JLL, July 2015

0

100

200

300

400

500

600

700

800

Americas EMEA Asia Pacific Global

US

$ bi

llion

s

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 (F)

xx% * +5% in Euro Terms

Projected Change 2014-2015

5-10%

-10-15%*

20%

5%

-100 -50 0 50 100 150

TokyoSydney

SingaporeShanghai

SeoulMumbai

Hong KongBeijing

Mexico CitySao Paulo

Washington DCToronto

San FranciscoNew York

Los AngelesChicagoBoston

StockholmParis

MoscowMadrid

LondonFrankfurtBrussels

Q1 2015 - Q2 2015

Q2 2014 - Q1 2015

Basis point change

Am

eric

asE

uro

pe

Asi

a P

acif

ic

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 13

Capital Values and Yields

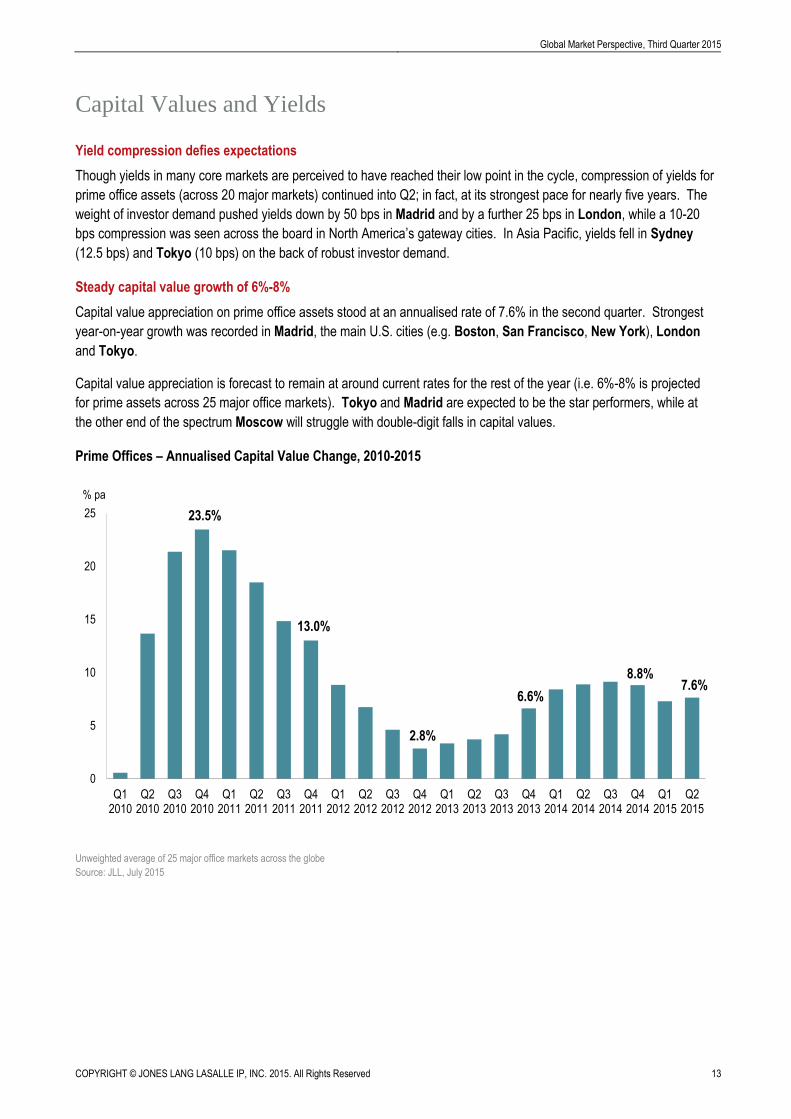

Yield compression defies expectations

Though yields in many core markets are perceived to have reached their low point in the cycle, compression of yields for

prime office assets (across 20 major markets) continued into Q2; in fact, at its strongest pace for nearly five years. The

weight of investor demand pushed yields down by 50 bps in Madrid and by a further 25 bps in London, while a 10-20

bps compression was seen across the board in North America’s gateway cities. In Asia Pacific, yields fell in Sydney

(12.5 bps) and Tokyo (10 bps) on the back of robust investor demand.

Steady capital value growth of 6%-8%

Capital value appreciation on prime office assets stood at an annualised rate of 7.6% in the second quarter. Strongest

year-on-year growth was recorded in Madrid, the main U.S. cities (e.g. Boston, San Francisco, New York), London

and Tokyo.

Capital value appreciation is forecast to remain at around current rates for the rest of the year (i.e. 6%-8% is projected

for prime assets across 25 major office markets). Tokyo and Madrid are expected to be the star performers, while at

the other end of the spectrum Moscow will struggle with double-digit falls in capital values.

Prime Offices – Annualised Capital Value Change, 2010-2015

Unweighted average of 25 major office markets across the globe

Source: JLL, July 2015

0

5

10

15

20

25

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

% pa

23.5%

13.0%

2.8%

6.6%7.6%

8.8%

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 14

Global Market Perspective, Third Quarter 2015

Corporate Occupiers

Occupier activity on the rise globally

The second quarter of 2015 has seen a surge of occupier activity across global markets. Despite continued volatility in

operating and macroeconomic conditions, business sentiment remains robust with corporates increasingly moving into

growth mode. According to a recent CEO Survey from PwC, 50% of CEOs questioned reported plans to increase their

headcount in 2015. An uplift in global leasing volumes of 24% on the quarter and 8% year-on-year provides clear

evidence of this growth trajectory.

M&A driving portfolio change

M&A is particularly high on the corporate agenda and, after 2014 witnessed the strongest increase in M&A since the

GFC, 2015 year-to-date M&A volumes remain at multi-year highs. A growing number of companies are absorbing new

real estate, consolidating, and reassessing enterprise footprints and resultant real estate portfolios. Divestments are

also increasingly common as corporates recast and optimise their businesses, with some rationalisation still apparent in

financial services. Notwithstanding these areas of ongoing restructuring, expansionary demand is now on the rise

across the majority of major global markets and sectors.

In search of authenticity

A combination of changing occupier preferences and real estate market conditions are reshaping space requirements in

some markets. In the U.S., demand for Class B space is skyrocketing among tenants. Technology, media and creative

firms are showing more interest in the character of the space, neighbourhood and the amenities that they can get within

their space than an address on Fifth Avenue or the most prestigious trophy building. A search for ‘authenticity’ appears

to be spilling into real estate from other industries.

In Asia Pacific, in addition to robust domestic activity and solid demand from MNCs, the continuing strength of smaller

occupiers is apparent; especially finance players in the key financial markets of Hong Kong, Shanghai, Singapore and

Tokyo. Flexibility is key for these high-growth occupiers who favour two-three year lease patterns, may take 500 square

metres, and grow within 18 months to double or triple that space.

In Europe, many markets are now facing a declining number of high-quality space options. In some markets, this fall in

prime supply has been sharp, driving increasing occupier mobility and forcing occupiers to plan further ahead in their real

estate strategies.

People, productivity and cost will continue to shape strategy

JLL’s recently launched global CRE survey points to a range of pressures impacting corporate real estate decision-

making; however, some themes stand out. People and productivity certainly continue to drive real estate decisions but

reducing operating expenses remains a core success factor for CRE teams. In a volatile operating environment,

flexibility is increasingly sought by occupiers with many reviewing their traditional portfolio balance of leased and owned

space. Finally, the data is clear that the volume of strategic and operational demands being placed on occupiers is

driving many towards increasing partnership and outsourcing as a way to deliver greater performance from their real

estate.

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 15

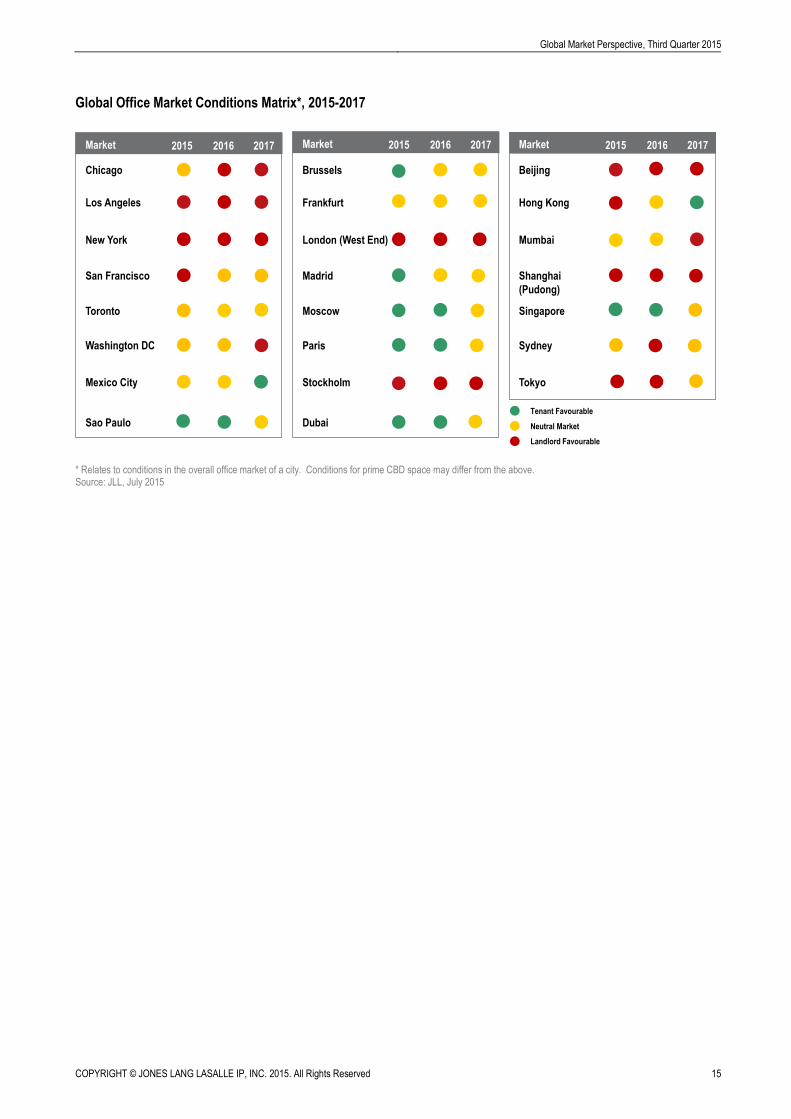

Global Office Market Conditions Matrix*, 2015-2017

* Relates to conditions in the overall office market of a city. Conditions for prime CBD space may differ from the above. Source: JLL, July 2015

MARKET

Brussels Beijing

Frankfurt Hong Kong

London (West End) Mumbai

Madrid Shanghai

(Pudong)

Moscow Singapore

Paris Sydney

Stockholm

Dubai

Market 2015 2016 2017 Market 2015 2016 2017

Tokyo

Neutral Market

Landlord Favourable

Tenant Favourable

Market

Chicago

Los Angeles

New York

San Francisco

Toronto

Washington DC

Mexico City

Sao Paulo

2015 2016 2017

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 16

Global Market Perspective, Third Quarter 2015

Global Real Estate Health Monitor

Economy Real Estate Investment Markets Real Estate Occupier Markets

Metro

GDP

OECD

Leading

Indicator

City

Investment

Volumes

Capital

Value

Change

Prime

Yield Yield Gap

Rental

Change

Net

Absorption

Vacancy

Rate

Supply

Pipeline

Dubai 4.8% na -64% 2.3% 7.5% na 2.3% na 21.0% 14.0%

Frankfurt 2.0% 0.10 77% 9.6% 4.4% 358 1.4% 1.1% 10.0% 1.5%

Hong Kong 2.9% na 69% 2.0% 3.1% 127 7.9% 2.8% 3.5% 4.5%

London 3.9% -0.20 0% 19.9% 3.5% 147 11.9% 1.8% 3.9% 5.1%

Madrid 3.2% -0.10 170% 31.1% 4.3% 194 6.1% 1.4% 11.1% 0.8%

Mexico City 3.7% -0.40 26% -1.2% 7.5% 144 2.2% 10.0% 11.0% 16.2%

Moscow -4.6% 0.10 -39% -34.5% 10.5% -58 -23.6% 4.0% 17.0% 8.0%

Mumbai 5.2% 0.10 569% -3.3% 10.0% 195 -4.7% 8.0% 19.8% 13.0%

New York 2.8% -0.10 25% 21.2% 3.3% 97 2.5% 1.4% 9.7% 0.9%

Paris 1.6% 0.00 -18% 9.7% 3.5% 230 -4.1% -0.7% 7.6% 2.6%

Sao Paulo 0.2% -0.30 -61% -18.3% 9.8% 498 -6.3% 3.4% 23.4% 18.6%

Seoul 3.4% -0.10 24% 6.9% 4.7% 225 -0.9% -0.2% 11.5% 3.2%

Shanghai 6.5% -0.20 -21% 5.9% 5.9% 227 5.3% 16.3% 10.7% 37.6%

Singapore 3.6% na -25% 0.0% 4.0% 128 0.5% 4.8% 6.0% 12.6%

Sydney 2.4% -0.20 -32% 9.5% 6.0% 297 2.4% 2.4% 8.8% 5.2%

Tokyo 1.4% 0.00 6% 20.6% 3.1% 266 6.8% 3.3% 3.3% 10.5%

Toronto 2.4% -0.10 45% 6.8% 4.9% 322 2.7% 1.0% 9.9% 2.2%

Real estate data as at end Q2 2015

Definitions and Sources

Metropolitan Region GDP: Change in Real GDP. Projection, 2015. Source: Oxford Economics

OECD Leading Indicator: Composite Leading Indicator. Change in Index. Latest Month. Source: OECD

City Investment Volumes: Direct Commercial Real Estate Volumes. Metro Area Data. Rolling Annual Change. Source: JLL

Capital Value Change: Notional Prime Office Capital Values. Year-on-Year Change. Latest Quarter. Source: JLL

Prime Yield: Indicative Yield on Prime/Grade-A Offices. Latest Quarter. Source: JLL

Yield Gap: Basis Points that Prime Office Yields are above or below 10-year Government Bond Yields. Latest Quarter. Source: JLL, Datastream

Rental Change: Prime Office Rents. Year-on-Year Change. Latest Quarter. Source: JLL

Net Absorption: Annual Net Absorption as % of Occupied Office Stock. Rolling Annual. Source: JLL

Vacancy Rate: Metro Area Office Vacancy Rate. Latest Quarter. Source: JLL

Supply Pipeline: Metro Area Office Completions (2015-2016) as % of Existing Stock. Source: JLL

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 17

Office Markets

Office Demand Dynamics

Highest leasing volumes for more than three years

After a slow first quarter, office leasing market fundamentals made a significant rebound during the second quarter.

Global leasing volumes improved by 24% on Q1 and were up 8% year-on-year. At 10.4 million square metres in Q2,

global corporate occupier activity (for the markets tracked by JLL) was at its highest level since Q4 2011. The strongest

gains were recorded in Asia Pacific, up 41% year-on-year, while the U.S. and Europe also registered healthy growth.

Modest uplift in volumes for full-year 2015

Despite the recent improvement, JLL still expects gross leasing volumes to be only moderately higher for the full-year

2015 (+0%-5%) compared to 2014 levels. The biggest uplift is forecast for Asia Pacific (+15%-20%), while volumes in

the U.S. and Europe are anticipated to remain in line with 2014 levels. The focus will be on CBD space, notably markets

that have amenity, density and a diverse mix of office inventory to create dynamic environments, albeit that supply

shortages in these locations will constrain leasing activity.

A shift towards expansion demand

Expansion demand is now firmly on the agenda of many corporate occupiers, with projections of a 15%-20% increase in

global net absorption for the full-year 2015. Occupancy growth in the U.S. is expected to be sustained at its current

robust level, and also has the potential to accelerate in Europe and Asia Pacific.

Technology still dominates demand

While there is now a much broader diversity of demand in terms of industry sectors, technology continues to have a

significant impact on leasing markets across the globe as it expands into new business areas, such as financial,

healthcare and personal services. As the sector becomes more ubiquitous within business in general, a greater variety

of office markets, beyond the more established global technology hubs, are benefiting from technology’s expansion.

A more robust U.S. economy boosts office demand

Leasing activity during the second quarter in the U.S. reached its highest level in two years, following a disappointing

first quarter:

Leasing activity was led by Boston, Chicago, Los Angeles and Washington DC, where demand has

intensified as scientific and technical industries have expanded out beyond the supply-constrained Northern

California (San Francisco, Silicon Valley), Pacific Northwest (Seattle, Portland) and New York.

Absorption gains were more evenly spread across markets, with Washington DC and New York making a

significant comeback. Dallas topped the U.S. rankings in terms of net absorption, reflecting its rapid ascent as

a powerhouse economy. Silicon Valley, Atlanta, Boston and Raleigh-Durham also performed well.

Many suburban markets continued to struggle with weak demand as they compete for tenants who are looking

for amenity-rich locations and also using such locations as a recruitment and retention tool.

Growth slowed substantially in energy-dependent Houston as occupiers consolidate their space

requirements.

Pre-leasing was strong with companies like Apple, Box, Google and Salesforce leasing full buildings in the

San Francisco Bay Area and Austin.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 18

Global Market Perspective, Third Quarter 2015

In Canada, positive absorption was registered in Vancouver and Toronto, while Calgary is feeling the

negative effects of depressed oil prices.

Looking southwards, demand was among the most resilient in Mexico City, where the market is successfully

absorbing significant new supply.

Europe records strongest Q2 take-up volumes since 2008

European office leasing activity totalled just over 2.9 million square metres in Q2, up 25% quarter-on-quarter and the

strongest second quarter since 2008. While most markets recorded positive growth, Europe continues to be a multi-

speed environment with cities also moving in different directions:

Corporate occupier activity in London shows no signs of weakening with take-up increasing by 41% year-on-

year in Q2, representing the strongest quarter in almost 10 years.

In Spain, Barcelona experienced a strong quarter, with leasing volumes up by 87% year-on-year. In Madrid,

transaction volumes are being increasingly held back by the lack of good-quality supply in central locations.

German offices have gone from strength to strength. The five largest office markets recorded a year-on-year

increase in take-up of 12% in the second quarter. Berlin and Hamburg put in particularly robust performances

as the willingness of occupiers to expand has increased substantially in recent quarters, as signified by a jump

in occupied stock and increases in take-up of 22% and 15% in the respective cities in H1 2015 versus H1 2014.

Central and Eastern Europe (CEE) also performed strongly in Q2. Prague saw a year-on-year increase in

take-up of around 55%, while Budapest and Warsaw recorded their best quarters in over 15 years.

By contrast, two of the largest office markets in Europe - Paris and Moscow - underperformed in H1 2015

compared with their long-term averages. Excluding Paris and Moscow, overall take-up for Europe was up 15%

on the Q2 2014 numbers.

Strong improvement in Asia Pacific leasing activity

Office leasing activity in Asia Pacific surged in Q2, with gross and net leasing up by 41% and 76% year-on-year

respectively. India and Greater China were the outperformers, with India contributing 40% of total regional gross

absorption and its volumes nearly double their Q2 2014 level:

The strongest activity was recorded in Delhi and Bangalore on the back of large deals signed by finance,

professional services and IT firms.

Shanghai saw a rising number of enquiries from domestic financial services companies as well as MNCs.

A few large occupiers and Chinese mainland companies drove take-up in Hong Kong.

Singapore saw weak activity, with many tenants holding off in expectation of lower rents due to the large

volume of impending supply.

Tokyo continued to see business consolidation to new high-quality buildings and persisting demand from the IT

sector.

Leasing activity maintained its recovery in Australia, particularly in Sydney where the CBD recorded its most

robust quarter of net absorption since Q4 2005.

JLL is optimistic that office leasing volumes in Asia Pacific will continue to improve in 2015, and has upgraded its

forecast of growth of 15%-20% for the full-year 2015. Domestic financial firms and technology should remain active

demand drivers.

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 19

Global Office Demand – Net Absorption Trends, 2004-2015

24 markets in Europe; 25 markets in Asia Pacific; 44 markets in the U.S. Asia relates to Grade A only. Source: JLL, July 2015

Global Office Completions, 2000-2017

24 markets in Europe; 25 markets in Asia Pacific; 44 markets in the U.S. Asia relates to Grade A only. Source: JLL, July 2015

-5

0

5

10

15

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

mill

ions

sq

m

Pro

ject

ion

0

5

10

15

20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015(F)

2016(F)

2017(F)

U.S. Europe Asia Pacific

mill

ions

sq

m

Average

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 20

Global Market Perspective, Third Quarter 2015

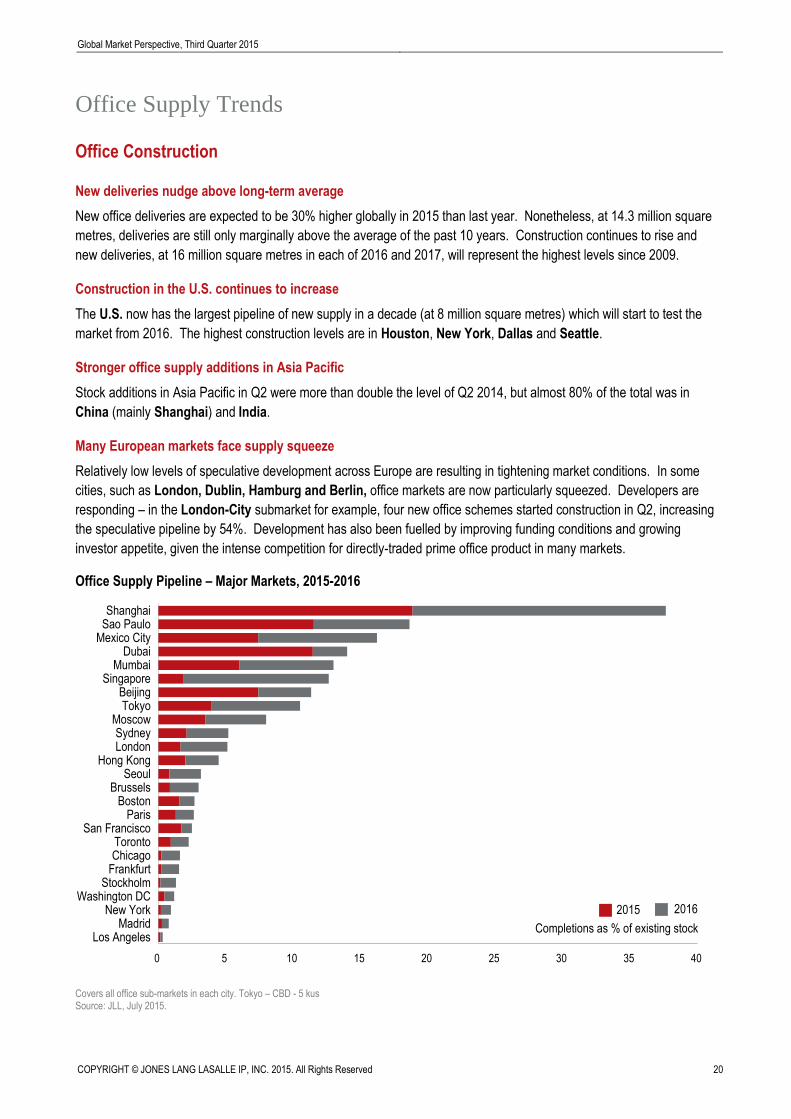

Office Supply Trends

Office Construction

New deliveries nudge above long-term average

New office deliveries are expected to be 30% higher globally in 2015 than last year. Nonetheless, at 14.3 million square

metres, deliveries are still only marginally above the average of the past 10 years. Construction continues to rise and

new deliveries, at 16 million square metres in each of 2016 and 2017, will represent the highest levels since 2009.

Construction in the U.S. continues to increase

The U.S. now has the largest pipeline of new supply in a decade (at 8 million square metres) which will start to test the

market from 2016. The highest construction levels are in Houston, New York, Dallas and Seattle.

Stronger office supply additions in Asia Pacific

Stock additions in Asia Pacific in Q2 were more than double the level of Q2 2014, but almost 80% of the total was in

China (mainly Shanghai) and India.

Many European markets face supply squeeze

Relatively low levels of speculative development across Europe are resulting in tightening market conditions. In some

cities, such as London, Dublin, Hamburg and Berlin, office markets are now particularly squeezed. Developers are

responding – in the London-City submarket for example, four new office schemes started construction in Q2, increasing

the speculative pipeline by 54%. Development has also been fuelled by improving funding conditions and growing

investor appetite, given the intense competition for directly-traded prime office product in many markets.

Office Supply Pipeline – Major Markets, 2015-2016

Covers all office sub-markets in each city. Tokyo – CBD - 5 kus Source: JLL, July 2015.

0 5 10 15 20 25 30 35 40

Los AngelesMadrid

New YorkWashington DC

StockholmFrankfurtChicagoToronto

San FranciscoParis

BostonBrussels

SeoulHong Kong

LondonSydney

MoscowTokyo

BeijingSingapore

MumbaiDubai

Mexico CitySao PauloShanghai

Completions as % of existing stock

2015 2016

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 21

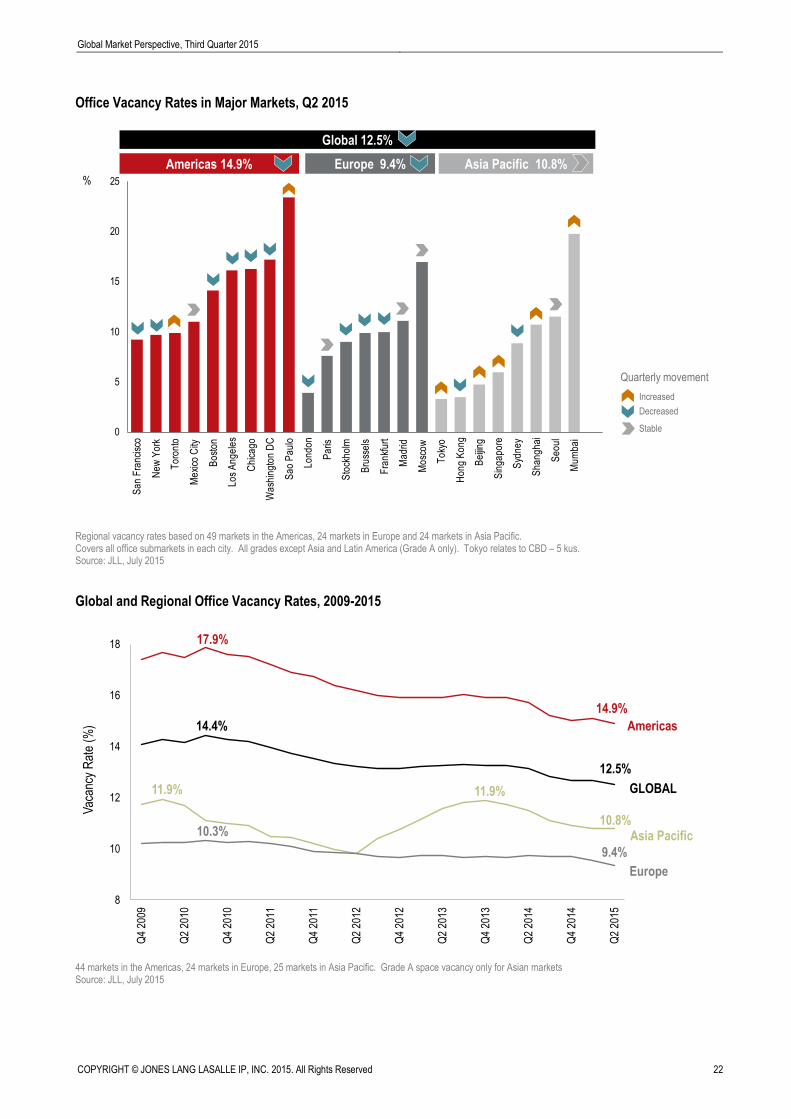

Office Vacancy

Vacancy rates fall steadily

The global office vacancy rate (across 98 markets) fell to 12.5% in Q2 and is projected to decline further, driven primarily

by a drop in U.S. vacancy rates. A shortage of space in many CBD markets is forcing higher occupier mobility, with

some companies now targeting a much wider range of submarkets to satisfy space requirements.

U.S. vacancy below 15% by year-end

U.S vacancy decreased to 15.3% in Q2, and rates are projected to fall below 15% by year-end. Stronger leasing activity

has led to vacancy declines across most U.S. cities. Single-digit direct vacancy is a feature of Salt Lake City, Portland,

San Francisco and New York, where low vacancy rates are forcing tenants to explore new markets.

Development surge in Canada pushes up vacancy

Despite positive absorption in the second quarter, Canada’s total office vacancy rate increased 30 bps during the

quarter to 10.3%. This was a result of new construction added to the inventory.

Large office development pipeline in Latin America

Upcoming new supply is still posing challenges for landlords across several office markets in Latin America, but is

introducing new space options for tenants at the same time. In Brazil, the market continues to become yet more tenant-

favourable. The total vacancy rate in Sao Paulo increased again in the second quarter, to 23.4%, up nearly 300 bps

from the level a year ago.

Europe’s vacancy falls again

The overall office vacancy rate in Europe has fallen for the second consecutive quarter (to 9.4% from 9.5% in Q1). In

many markets, the strengthening of occupier demand and a lack of speculative completions has resulted in a sharp drop

in supply. In Dublin, this effect has been most extreme with the vacancy rate plummeting from 16.6% to 8.6% over the

last 12 months. Meanwhile, in London, the vacancy rate has decreased to 3.9%. Strong occupier demand in Germany

has pushed vacancy rates to their lowest levels in over five years across the five largest markets.

New supply in Dubai

Much of the currently vacant office space in Dubai is in secondary-quality buildings, many of which are in strata-title

ownership and of little interest to major corporate occupiers. The lack of high-quality space will result in the delivery of a

number of new office projects during 2015.

Asia Pacific regional vacancy rate stable

Healthy demand led to lower vacancy in most Asian cities in the second quarter and the regional vacancy rate held

steady at 10.8%. However, vacancy rose in Beijing, Tokyo, Jakarta, Manila and Kuala Lumpur on the back of new

completions. The vacancy rate in Sydney’s CBD continued to fall, tightening to 7.5% from last quarter’s 9.9%.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 22

Global Market Perspective, Third Quarter 2015

Office Vacancy Rates in Major Markets, Q2 2015

Regional vacancy rates based on 49 markets in the Americas, 24 markets in Europe and 24 markets in Asia Pacific. Covers all office submarkets in each city. All grades except Asia and Latin America (Grade A only). Tokyo relates to CBD – 5 kus. Source: JLL, July 2015

Global and Regional Office Vacancy Rates, 2009-2015

44 markets in the Americas, 24 markets in Europe, 25 markets in Asia Pacific. Grade A space vacancy only for Asian markets Source: JLL, July 2015

0

5

10

15

20

25

Sa

n F

ran

cisc

o

Ne

w Y

ork

To

ron

to

Me

xico

City

Bo

sto

n

Lo

s A

ng

ele

s

Ch

ica

go

Wa

shin

gto

n D

C

Sa

o P

au

lo

Lo

nd

on

Pa

ris

Sto

ckh

olm

Bru

sse

ls

Fra

nkf

urt

Ma

drid

Mo

sco

w

To

kyo

Ho

ng

Ko

ng

Be

ijin

g

Sin

ga

po

re

Syd

ne

y

Sh

an

gh

ai

Se

ou

l

Mu

mb

ai

Europe 9.4% Asia Pacific 10.8%Americas 14.9%%

Quarterly movement

Increased

Decreased

Stable

Global 12.5%

8

10

12

14

16

18

Q4

2009

Q2

2010

Q4

2010

Q2

2011

Q4

2011

Q2

2012

Q4

2012

Q2

2013

Q4

2013

Q2

2014

Q4

2014

Q2

2015

Vac

ancy

Rat

e (%

) Americas

Asia Pacific

Europe

GLOBAL

17.9%

14.9%

14.4%

12.5%

11.9%

10.8%

11.9%

10.3%

9.4%

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 23

Office Rental Trends

Rental growth moves at a steady pace

Tightening fundamentals are fuelling landlord confidence. Rental growth continues to move at a steady pace, with the

annual rate of growth on prime office assets across 24 markets standing at circa 3%.1 Nonetheless, momentum is

building in several markets.

Landlord confidence builds in the U.S.

In the U.S., asking rents have increased by 2.5% since the start of the year, with rental growth strengthening in the vast

majority of markets. San Francisco (+10.3% year-on-year) and Boston (+8.4%) continue to lead, but landlords in Los

Angeles (+5.9%) and Chicago (+4.1%) are also benefiting from expanded demand.

As supply-demand becomes more unbalanced in favour of landlords, we should see further rental uplifts in U.S. markets

over the next 12 months. However, rental growth should decelerate by the end of 2016 as supply comes on tap.

Increased optimism selectively boosts rents across Asia Pacific

Net effective rents have increased in about three-quarters of Asia Pacific markets. Hong Kong recorded the most

robust growth (+7.9% year-on-year) in Q2, the best result in four years, supported by improved occupancy levels at the

mid-range of the market. Solid annual growth was also seen in Tokyo (+6.8%) and Shanghai (+5.3%). Of the major

Asia Pacific markets, the biggest quarterly fall was in Singapore (-5.2%), where landlords have started to drop rents as

tenants delay decisions due to large upcoming supply in 2016. Sydney’s rental levels have moved higher over the year

(+2.4%).

Single-digit rental growth across the region is generally expected for the full-year 2015, although Singapore and a few

Australian cities are projected to see further declines. Rental growth has picked up in Hong Kong and Tokyo which,

among the major markets, are likely to be the top global performers in 2015.

Positive momentum across Europe

The European Office Index increased by 0.5% quarter-on-quarter, indicating positive momentum across most of Europe.

London was the top performer (+11.9% year-on-year) where prime rents have moved ahead of the previous peak. The

robust recovery in Spain translated into further prime rental growth in Q2, with Barcelona (+8.6%) and Madrid (+6.1%)

outperforming most of the rest of Europe. In Germany, the rise in office-related employment continued to feed rental

growth, with Berlin (+4.5%) recording the strongest uplift.

In Paris, prime CBD rents have dropped by 4.1% over the past year. While there is a risk of further minor corrections in

the short term, prime rents in Paris have recently fluctuated between quarters without a strong uptrend. The most

significant correction in prime rents was recorded in Warsaw (-2.1% year-on-year).

In general, the outlook for European offices is upbeat and H2 2015 should see positive rental growth in most European

office markets. The intensifying supply squeeze in markets such as London, Dublin, Berlin, Hamburg and Munich will

add to this momentum. Many Southern European office markets offer further potential for growth as prime rents are still

well below their previous peaks, including Madrid (-38%), Barcelona (-30%) and Milan (-18%). At the other end of the

spectrum, oversupplied markets such as Warsaw and The Hague might experience some further downward corrections.

1 Excludes Moscow which, due to sharp falls in rents, is distorting the average

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 24

Global Market Perspective, Third Quarter 2015

Prime Offices – Rental Change, Q2 2014-Q2 2015

Based on rents for Grade A space in CBD or equivalent. In local currency. Source: JLL, July 2015

Prime Offices – Rental Change, 2010-2015

Prime office rental growth: unweighted average of 25 major markets. * 2015 forecast excludes Moscow Source: JLL, July 2015

-25 -20 -15 -10 -5 0 5 10 15

Moscow

Sao Paulo

Mumbai

Paris

Brussels

Seoul

Stockholm

Singapore

Frankfurt

Washington DC

Mexico City

Dubai

Sydney

New York

Toronto

Beijing

Chicago

Shanghai

Los Angeles

Madrid

Tokyo

Hong Kong

Boston

San Francisco

London

0

1

2

3

4

5

6

7

8

9

10

2010 2011 2012 2013 2014 2015

8.9%

7.9%

1.9%1.2%

Ren

tal c

hang

e (y

-o-y

%)

4%*

3.6%

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 25

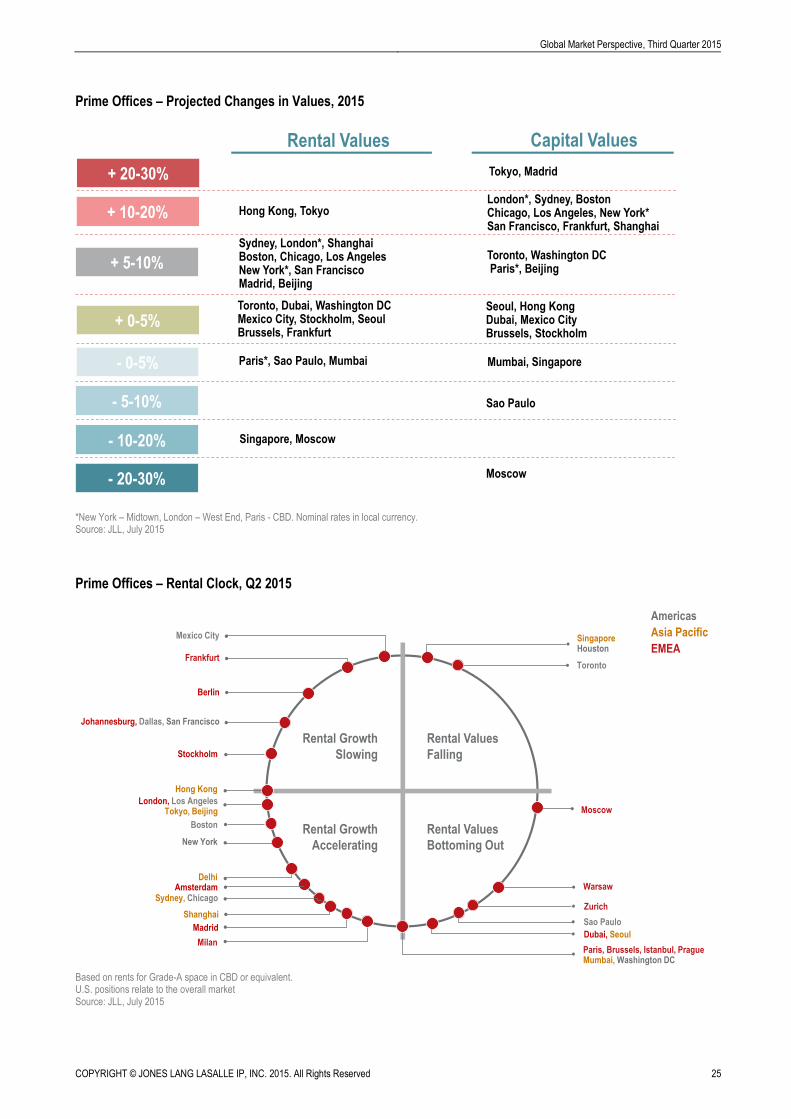

Prime Offices – Projected Changes in Values, 2015

*New York – Midtown, London – West End, Paris - CBD. Nominal rates in local currency. Source: JLL, July 2015

Prime Offices – Rental Clock, Q2 2015

Based on rents for Grade-A space in CBD or equivalent. U.S. positions relate to the overall market Source: JLL, July 2015

+ 10-20%

+ 5-10%

+ 0-5%

- 0-5%

- 5-10%

Sydney, London*, Shanghai Boston, Chicago, Los Angeles New York*, San FranciscoMadrid, Beijing

Hong Kong, Tokyo

Capital ValuesRental Values

Toronto, Dubai, Washington DCMexico City, Stockholm, Seoul Brussels, Frankfurt

Paris*, Sao Paulo, Mumbai

London*, Sydney, BostonChicago, Los Angeles, New York*San Francisco, Frankfurt, Shanghai

Toronto, Washington DCParis*, Beijing

Seoul, Hong Kong Dubai, Mexico CityBrussels, Stockholm

Mumbai, Singapore

Sao Paulo

- 10-20% Singapore, Moscow

Moscow

+ 20-30% Tokyo, Madrid

- 20-30%

Rental Values

Bottoming Out

Rental Growth

Slowing

Rental Values

Falling

Rental Growth

Accelerating

Americas

Asia Pacific

EMEA

New York

Moscow

Johannesburg, Dallas, San Francisco

Hong Kong

MilanParis, Brussels, Istanbul, Prague Mumbai, Washington DC

Sao Paulo

Delhi

Sydney, Chicago

Boston

London, Los AngelesTokyo, Beijing

WarsawAmsterdam

Madrid

Frankfurt

Mexico City

Toronto

Berlin

Singapore Houston

Shanghai

Stockholm

Zurich

Dubai, Seoul

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 26

Global Market Perspective, Third Quarter 2015

Retail Markets

Slow pace of improvement continues in the United States

The U.S. retail market’s pace of improvement is much more gradual than in the country’s other property sectors – but it

continues to strengthen nonetheless. Retailer demand has comfortably exceeded supply for the past four quarters,

resulting not only in consistent vacancy compression to 5.9% in Q2, but also rising rents across most major markets.

Rents rose 0.5% from the first quarter, and grew 1.2% year-on-year in the quarter. Among U.S. shopping centre types,

power centres are still experiencing the tightest overall market conditions, with total vacancy of 4.7%. Several standout

markets, such as Miami, New York, Houston, Dallas, Fort Lauderdale, Boston and San Francisco, are maintaining

the healthiest growth conditions, as rents see assertive growth and vacancy continues to compress.

Increased consumer confidence as optimism boosts retail sales across Europe

Improved consumer confidence across Europe during the second quarter has fuelled optimism in the retail sector.

Reduced fuel and energy prices, decreasing unemployment and lower interest rates are boosting disposable incomes.

European retail sales are forecast to grow by 2.9% in 2015 and 2.0% in 2016. Up to 2017, this growth is expected to

remain especially robust in the UK, Turkey and Norway, as well as the CEE region.

Northern European cities record robust rental uplift

The strongest increases in high street rents in the second quarter were recorded in Birmingham (+8.8% quarter-on-

quarter), Brussels (+8.1%), Antwerp (+8.1%), Frankfurt (+3.3%) and Stockholm (+2.1%), although rents softened in

the main Dutch cities – Rotterdam (-2.8%) and Amsterdam (-1.7%). For the full-year 2015, London and Birmingham

as well as Dublin and the German cities of Frankfurt, Hamburg and Munich are anticipated to outperform.

Varied retailer demand picture in Asia Pacific

China witnessed steady demand for retail space in the second quarter, underpinned by mid-tier fashion brands and

F&B, whereas luxury brands remained cautious. At the same time, weaker retail trading conditions in Hong Kong have

seen retailers adopt a more wary stance. Several new brands entered Singapore in Q2, while some landlords have

readjusted their tenant mix amidst a challenging operating environment. Some foreigner retailers are exploring

decentralised locations and/or second-tier cities in emerging Southeast Asia for new store openings. Retail growth in

Australia continues to be driven by the F&B sector.

New-to-market foreign retailers and Chinese tourists support growth

Rents rose in around half of all Asian markets in the second quarter, with the biggest gains in Bangkok and Jakarta

(around 2% quarter-on-quarter). In contrast, falls in rents were seen in the Hong Kong ‘high street’ and Singapore

markets. For the next 12 months, new-to-market foreign retailers and the growth of inbound tourism (particularly

Chinese) should continue to support many markets around the region.

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 27

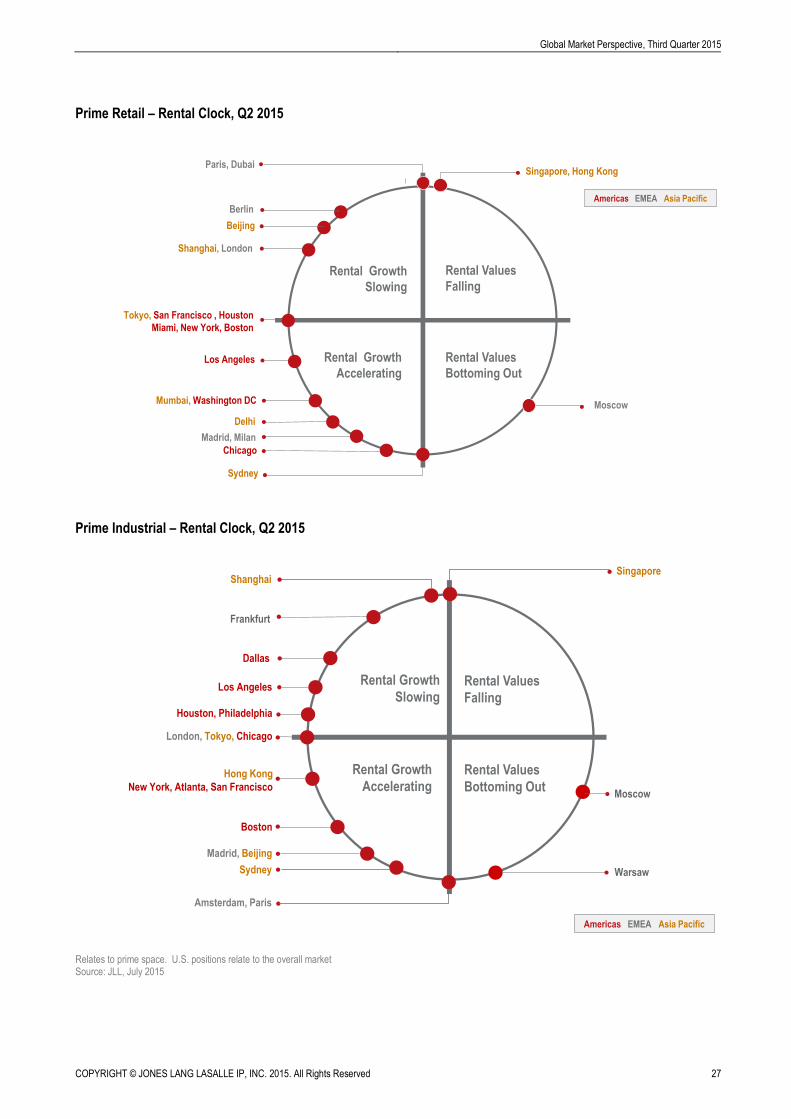

Prime Retail – Rental Clock, Q2 2015

Prime Industrial – Rental Clock, Q2 2015

Relates to prime space. U.S. positions relate to the overall market Source: JLL, July 2015

Rental Growth

Slowing

Rental Values

Falling

Rental Growth

Accelerating

Rental Values

Bottoming Out

Americas EMEA Asia Pacific

Delhi

Madrid, Milan

Mumbai, Washington DC

Singapore, Hong Kong

Los Angeles

Paris, Dubai

Beijing

Berlin

Sydney

Tokyo, San Francisco , Houston

Miami, New York, Boston

Moscow

Shanghai, London

Chicago

Rental Growth

SlowingRental Values

Falling

Rental Values

Bottoming Out

Warsaw

Americas EMEA Asia Pacific

Rental Growth

Accelerating

Amsterdam, Paris

Boston

Frankfurt

London, Tokyo, Chicago

Los Angeles

Singapore

Dallas

Shanghai

Hong Kong

New York, Atlanta, San Francisco

Sydney

Madrid, Beijing

Houston, Philadelphia

Moscow

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 28

Global Market Perspective, Third Quarter 2015

Industrial Warehousing Markets

Absorption trumps completions in most major U.S. markets

Approximately 40% of the industrial stock in the U.S. is currently concentrated in seven major logistics corridors – Los

Angeles, the Inland Empire, Dallas/Fort Worth, Chicago, Philadelphia/Harrisburg, New Jersey and Atlanta – and

fundamentals have been strong in these trend-driving, population-centric markets. Their respective construction

deliveries have lagged their absorption totals, which, in turn, have caused vacancies to tighten and rents to increase.

Consequently, landlords have gained more leverage to push up rents.

U.S. vacancy at 10-year low

Based on active tenant requirements, nearly all U.S. markets have scenarios where their construction pipelines will be

unable to keep up with space needs during 2015. This suggests that national net absorption will continue to outpace

completions (as it did from 2010-2014) for its sixth consecutive year. Market conditions remain bullish, with national

vacancy finishing the quarter at 6.7% – a 10-year low. Average asking rents for warehouse space in Q2 were up 5%

year-on-year.

While absorption has exceeded completions in most U.S. cities, the spotlight fell on two major markets in Q2 –

Dallas/Fort Worth and Chicago – where vacancy rates have risen to 6.3% and 7.6% respectively on the back of

increasing speculative completions.

Industrial vacancy rates remain low over the rest of North America

In Canada, despite strong positive absorption in Q2, vacancy remained unchanged at 4.2%, mainly as a result of

speculative construction being added to the total inventory. Latest data for Mexico’s industrial market point to positive

trends – the national vacancy declined to 5.6% in the quarter, led by a particularly robust showing by the North Region.

European demand maintains momentum, but increasingly selective

The European logistics occupational market remains sturdy. Continued innovation in order-fulfilment and delivery is

driving further adaptation of logistics networks. Implementation of new strategies will support modest growth in annual

take-up this year. In addition, occupational demand has been further boosted by a strengthening manufacturing sector

across CEE (excluding Russia) and a recovery that is gaining momentum in Southern Europe. As a result, 2015 is likely

to see a new record in European take-up. Nonetheless, occupier demand is becoming increasingly selective, with a

rising focus on multimodal locations, automated facilities and facilities supporting efficient urban logistics.

Build-to-suit dominates in Europe

Speculative development in Europe remains thin overall, although speculative development starts in the UK have risen

markedly in recent months. This trend is expected to extend into the major Western European markets and, more

selectively, Central Europe. However, speculative development will continue to be limited overall and nowhere near pre-

GFC levels, supporting ongoing low vacancy over the medium term.

There is heavy pressure on the occupier side to maintain/reduce supply chain costs; a pressure that, in combination with

relative easy access to finance and low interest rates, is pushing more occupiers into owner-occupier development, if it

offers a cost premium on rental levels.

Third-party logistics companies and retailers support warehouse rents in Asia

Healthy leasing levels of logistics space in Asia were driven by third-party logistics companies and retailers in the second

quarter. Rents were stable or higher in most monitored markets apart from Singapore, where rising supply pressures

nudged rents down. Tokyo achieved the highest rental uplift (2.8% quarter-on-quarter), driven by strong tenant demand

and increasing construction costs.

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 29

Hotel Markets

Global hotel investment going from strength to strength

Continuing the robust growth from Q1 2015, global hotel transaction volumes have gone from strength to strength,

reaching a new high of US$42 billion in H1 2015, up 55% from the same period last year. Of the three regions, the

Americas takes top position with volumes at US$24 billion. It has also achieved the highest year-on-year growth at 73%,

followed by EMEA, up 55%. Conversely, Asia Pacific has seen a slight decline in investment volumes, down 6% to

US$4 billion.

Hotel Investment Volumes, 2014-2015

US$ billions

H1 2014 H1 2015 % change

Americas 13.7 23.6 73%

Asia Pacific 3.9 3.7 -6%

EMEA 9.4 14.6 55%

Total 27.0 42.0 55%

Source: JLL, July 2015

Cross-border investors remain active. EMEA is still a magnet for foreign investment, attracting the largest amount of

capital of all the regions, worth US$9 billion. Meanwhile, North America and Asia Pacific received US$4 billion and

US$2 billion respectively. Investors from the Middle East and mainland China have been the major exporters of capital.

Hotel Transactions: Capital Flows, H1 2015

Source: JLL, July 2015

($1.3)

($3.5)

($3.8)

($6.0)

$0.3

$8.7

$1.3

$4.2

Australasia

Europe

Asia

North America

Mainland China

Middle East

Outflows Inflows US$ billions

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 30

Global Market Perspective, Third Quarter 2015

Chinese investors highly active

Mainland Chinese investors continue to play a major role in global hotel transactions. Their volumes rose from US$1

billion in 2014 to US$4 billion in the first half of 2015, equating to 80% of our 2015 forecast, and they are showing strong

interest in luxury properties in both North America and Europe. Australia is also seeing inflows from Chinese investors,

with the Hilton Sydney changing hands at the beginning of July.

China’s insurance companies have been the most dominant buyer, snapping up a total of US$2 billion of properties in

H1 2015 and accounting for 58% of all hotel transactions completed by Chinese investors. Investment volumes are

expected to grow, due to the Chinese government relaxing the investment threshold towards foreign investment. In

addition, only two out of the ten largest Chinese insurance companies have currently invested in hotels globally,

representing big opportunities ahead.

The Americas – private equity in the spotlight

For the first half of 2015, the Americas region witnessed a 73% year-on-year increase in deal volumes to US$24 billion

with 96% of transactions occurring in the United States. New York and San Francisco were the top two cities in terms

of volumes, at US$4 billion and US$1 billion respectively.

On the buy side, investment funds and private equity firms were the most dominant players in H1 2015, accounting for

42% of transaction volumes. Their primary focus was portfolio deals, which made up 65% of purchases.

Investment funds and private equity firms demonstrated an equally strong appetite in the seller market, representing

60% of total activity in the first half of the year, a big jump from the 44% share in the same period last year. This is their

strategy to make profit by recycling capital.

Investors from mainland China and the Middle East were the most prominent foreign investors into the U.S. market with

investment volumes in H1 2015 totalling US$4 billion, a staggering 308% uplift from H1 2014.

EMEA – UK steals the show

EMEA transaction volumes rose 55% or US$5 billion to US$15 billion in H1 2015, with the UK securing 54% of total deal

volumes, up 200% year-on-year. While London remains attractive, there were a high number of deals in UK regional

cities such as Edinburgh, Liverpool and Manchester. Trading performance (RevPAR) for hotels in the UK’s regions

has been stronger than London, making properties more desirable for potential investors.

Germany posted the second highest growth in hotel transactions in EMEA, up 29% to US$2 billion in H1 2015

compared to H1 2014, followed by Spain, increasing by 17% to US$1 billion.

Portfolio sales in the first half of 2015 accounted for 65% of total deals in the region, a significant increase from the 39%

in H1 2014. The largest portfolio deal in Q2 2015 was the sale of the Maybourne portfolio in London to a Middle Eastern

investor for c. US$2 billion. In addition, Accor disposed a number of properties in the UK and Germany as part of the

company’s asset-recycling strategy.

Investment funds and private equity firms were the most active buyers in H1, representing 30% of transactions, followed

by hotel operators (22%) and REITs (8%).

Global Market Perspective, Third Quarter 2015

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015. All Rights Reserved 31

Asia Pacific – focus on single-asset deals

Investment volumes in Asia Pacific totalled US$4 billion in H1, a slight decline of 6% or US$0.2 billion from the same

period last year. Single-asset transactions dominated the Asia Pacific market, accounting for 82% (US$3 billion) of total

deal volumes.

Sovereign wealth funds were the most active buyers in Q2, thanks to the 50% sale to ADIA of three hotels in Hong