jm associates federal credit union annual report 09 annual report.pdf · • managing the...

TRANSCRIPT

JM Associates Federal Credit Union

Annual Report09

2

Mission Statement

• Building customer-friendly relationships…

• Managing the membership’s collective resources for the benefit of all…

• Providing a wide range of competitively priced products, and…

• Leveraging technology to maximize efficiency, while always protecting and maintaining member confidentiality.

JM Associates Federal Credit Union is a financial institution whose primary purpose is to provide the highest quality services to our members. In support of this mission, we are committed to:

Building Better Relationships

We’re here for you!

3

JM Associates Federal Credit Union Annual Meeting

March 18, 2010Southeast Toyota Distributors

Westlake Tech Center Jacksonville, Florida

Table of Contents

Chairman’s Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

President’s Letter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Navigating the Waters of Change. . . . . . . . . . . . . . . . . . . . . . 7

Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Independent Auditor’s Report. . . . . . . . . . . . . . . . . . . . . . . .28

Supervisory Committee Report . . . . . . . . . . . . . . . . . . . . . . .30

Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

4

Chairman’s ReportMarch 2010

Dear Members,

On behalf of the Board of Directors, “Thank-You” for allowing us the privilege to serve our fellow members. We believe in the Credit Union philosophy and work assiduously to uphold our mission statement of “managing the memberships’ collective resources for the benefit of all.” In support of this mission I am proud to report, that despite an increase in loan loss reserves, we had another profitable year. Even with a profitable year, the Credit Union has never before seen such turmoil in the financial markets. I have witnessed first-hand the financial hardship families have endured as they dealt with diminished incomes, rising unemployment and a decline in their most cherished asset, their home.

During these tough economic times I fully appreciate how different we are from the big “banks” and I am in awe of Mr. Moran and the founding members’ for their foresight in creating JMAFCU, a cooperatively run financial institution that exists for the sole purpose of bringing value to its member-owners. It is the support of JM Family Enterprise and Executive Management that allows us to continue carrying out the original goal of “people helping people.”

Looking back on the challenges of 2009 I commend the JMAFCU management and staff for “going the extra mile” and realize the unique position and tremendous responsibility we, as a Credit Union, have in truly making a difference in the lives of our members.

As we move forward into a new decade, we will be serving our members with improved technology through our SAFE system of internet banking, bill pay and audio response. In addition, we will be upgrading all our ATM’s to provide a better member experience.

In closing, I want to reassure our members that JMAFCU is well-positioned to continue being the safe, secure, and trusted financial cooperative that we have always been for the past 30 years.

Best Regards,

Pamela Rower, MBA, CPA, CAPMChairman, Board of DirectorsJM Associates Federal Credit Union

Pam Rower

5

President’s Letter

Jim Ryan

Dear Member,

“Into each life some rain must fall.” Henry Wadsworth Longfellow

We all saw our share of “rain” in 2009. It was a true test of the cooperative nature of credit unions and our members’ fortitude. JMAFCU was pulled between the desire to assist members in trouble and protecting the assets of all members.

JMAFCU had a challenging but successful year. Our deposit base grew by over 27% in the 12 months ending September 2009. Over the same period, loans outstanding had no growth. These are a sign that many of our members were growing more conservative (fewer loans) and wanted to be safe and liquid (growth in deposits). Members were also being challenged by salary reductions, layoffs and other financial strains. In anticipation of additional loan defaults, extra reserves were placed in the allowance for loan losses through the provision expense. Despite this added expense and a continued erosion of interest income (lower interest rates), JMAFCU had a positive bottom line and the enclosed financial statements should be a testament to JMAFCU’s efforts to protect members’ assets.

What is not apparent in the enclosed reports are the efforts to work with members in need. JMAFCU has always worked with members to provide loans for their financial needs but in 2009 members also needed special payment arrangements, interest only payments and loan modifications to help them get through their various difficulties. Helping members is not something new for a not-for-profit financial cooperative nor is it new for JMAFCU

Sincerely,

Jim Ryan, CCUEPresident

6

7

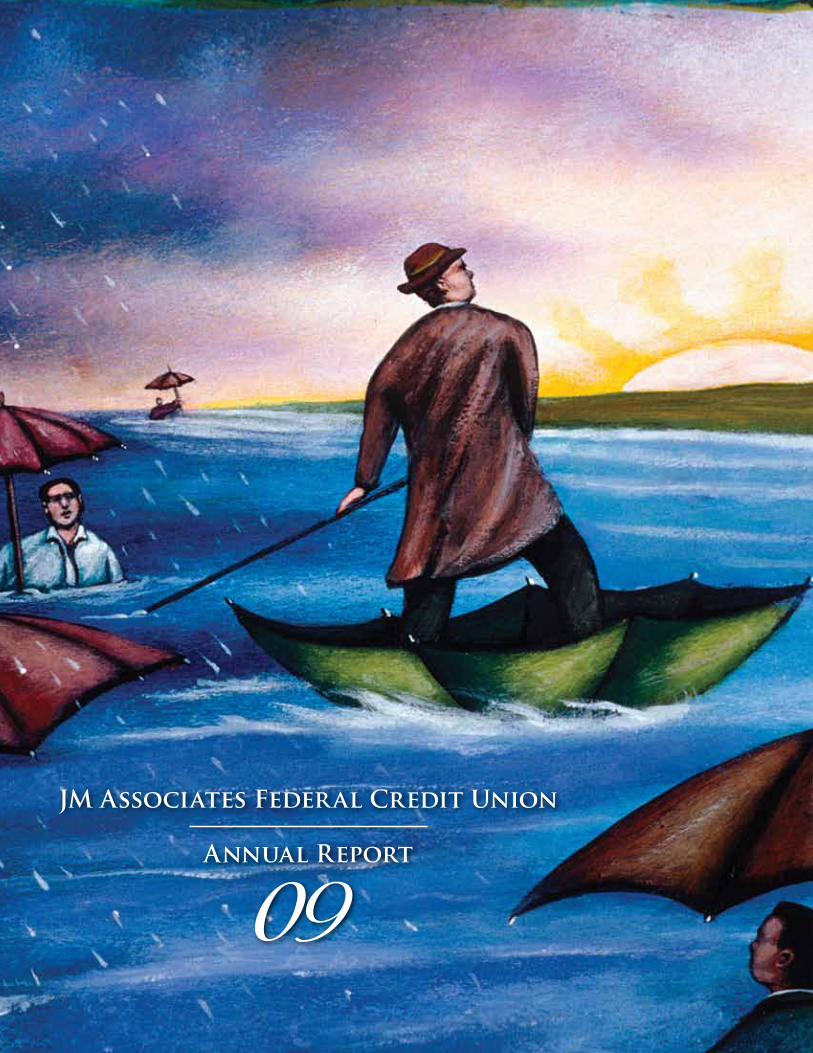

Last year’s annual report portrayed the Little Man, a long standing symbol of the credit union movement;

he is besieged by the cares of the world, but protected by his strong and safe credit union umbrella. JMAFCU’s

2009 Annual Report depicts a different “little man”. On our cover, we find our little man ingenuously using his

umbrella as a makeshift boat. Even though others around him appear to be washed out by the rain, he has used

his umbrella to navigate through the storms and is headed toward the sunshine on the horizon.

Throughout this year’s report, we see the little man navigating the often times troubled and shark infested waters

of the present financial environment and even enduring the rough rapids of change all around. He is able to

endure and be at peace because he has placed his trust in his credit union, JM Associates Federal Credit Union.

Experience has taught him that even in the midst of a storm; JM Associates Federal Credit Union is working

diligently on his behalf and making decisions with his best interest in mind.

While some financial institutions have been forced to make changes in the way they “serve” their customers,

JMAFCU has not had to change the way we calculate interest or our fee structure. We have always treated our

members like family, keeping their needs in mind. The same umbrella that has served as protection from the

storms of life and as a navigational vessel through treacherous currents and rip tides has helped our members

rise far above the chaos we see in today’s economy.

The rains have come, and the river has risen, however JM Associates Federal Credit Union is well prepared!

The enclosed financial reports attest that there is strength in the numbers and in the sound wisdom that will

take JMAFCU and its members to the safety of higher, drier ground.

Navigating the Waters of Change

8

jm associates federal credit unionStatement of Financial Condition

2009 2008 Cash and cash equivalents 834,500$ 973,239$ Investments: Available-for-sale 20,511,704 15,684,241 Held-to-maturity 4,192,662 1,280,113 Other 22,005,935 10,212,606 Loans held for sale 252,278 1,938,925 Loans receivable, net of allowance for loan losses 30,586,040 31,818,067 Accrued interest receivable: Loans 116,588 249,048 Investments 164,993 102,905 Premises and equipment, net 35,628 110,113 NCUSIF deposit 473,484 438,634 Other assets 51,144 62,379 Total assets 79,224,956$ 62,870,270$

September 30,

LIABILITIES AND MEMBERS' EQUITY

ASSETS

JM ASSOCIATES FEDERAL CREDIT UNIONSTATEMENTS OF FINANCIAL CONDITION

Read the accompanying notes to these financial statements.

2009 2008LIABILITIES: Members' share and savings accounts 70,201,013$ 55,060,594$ Accounts payable and other liabilities 849,889 613,501 Total liabilities 71,050,902 55,674,095

Commitments and contingent liabilities

MEMBERS' EQUITY: Regular reserve 716,460 716,460 Undivided earnings 7,114,355 6,827,005 Accumulated other comprehensive income (loss) 343,239 (347,290) Total members' equity 8,174,054 7,196,175 Total liabilities and members' equity 79,224,956$ 62,870,270$

September 30,

Read the accompanying notes to these financial statements.

9

jm associates federal credit unionStatement of Financial Income

2009 2008INTEREST INCOME: Loans receivable 2,290,263$ 2,439,748$ Investments 1,107,737 1,115,210 Total interest income 3,398,000 3,554,958

INTEREST EXPENSE: Members' share and savings accounts 1,185,832 1,275,627 Borrowed funds 40 - Total interest expense 1,185,872 1,275,627 Net interest income 2,212,128 2,279,331

PROVISION FOR LOAN LOSSES 1,121,000 922,000 Net interest income after provision for loan losses 1,091,128 1,357,331

NON-INTEREST INCOME: Interchange income 1,637,456 1,315,812 NCUSIF recapitalization 326,704 -

N ffi i f d f 144 371 123 738

September 30,

JM ASSOCIATES FEDREAL CREDIT UNIONSTATEMENTS OF INCOME

Non-sufficient funds fees 144,371 123,738 Other fees and service charges 97,852 136,379 Late charge fees 81,933 59,770 Gain on sale of VISA stock - 141,426 Total non-interest income 2,288,316 1,777,125

NON-INTEREST EXPENSE: Compensation and employee benefits 1,263,510 1,314,134 Other operation expense 507,346 564,392 NCUSIF impairment and assessment 417,974 - Professional and outside services 341,776 378,610 Miscellaneous expense 283,918 66,466 Loan servicing expense 277,570 252,521 Loss on sale of investments - 12,718 Total non-interest expense 3,092,094 2,588,841 Net income 287,350$ 545,615$

JM ASSOCIATES FEDREAL CREDIT UNIONSTATEMENTS OF INCOME

Read the accompanying notes to these financial statements.

10

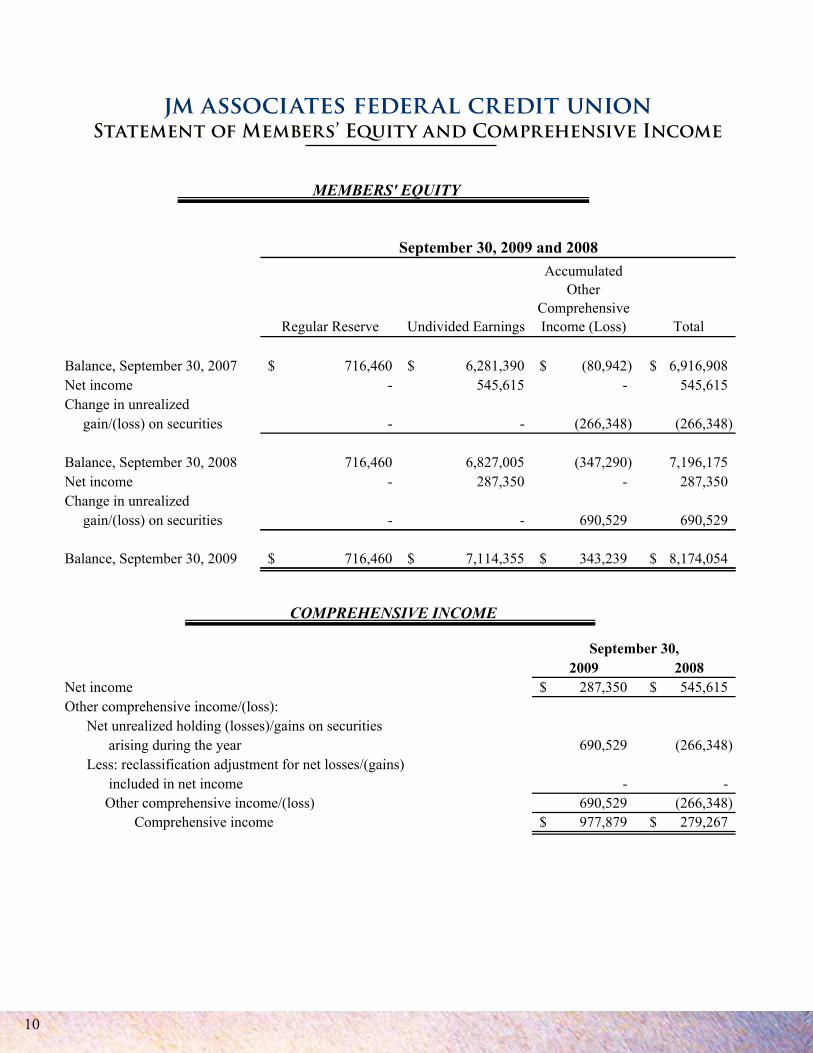

jm associates federal credit unionStatement of Members’ Equity and Comprehensive Income

Regular Reserve Undivided Earnings

AccumulatedOther

ComprehensiveIncome (Loss) Total

Balance, September 30, 2007 716,460$ 6,281,390$ (80,942)$ 6,916,908$Net income - 545,615 - 545,615Change in unrealized gain/(loss) on securities - - (266,348) (266,348)

Balance, September 30, 2008 716,460 6,827,005 (347,290) 7,196,175Net income - 287,350 - 287,350Change in unrealized gain/(loss) on securities - - 690,529 690,529

September 30, 2009 and 2008

JM ASSOCIATES FEDERAL CREDIT UNIONSTATEMENTS OF MEMBERS' EQUITY AND

COMPREHENSIVE INCOME

MEMBERS' EQUITY

Read the accompanying notes to these financial statements.

Balance, September 30, 2009 716,460$ 7,114,355$ 343,239$ 8,174,054$

2009 2008Net income 287,350$ 545,615$Other comprehensive income/(loss): Net unrealized holding (losses)/gains on securities arising during the year 690,529 (266,348) Less: reclassification adjustment for net losses/(gains) included in net income - -

690,529 (266,348)977,879$ 279,267$ Comprehensive income

September 30,

Other comprehensive income/(loss)

JM ASSOCIATES FEDERAL CREDIT UNIONSTATEMENTS OF MEMBERS' EQUITY AND

COMPREHENSIVE INCOME

MEMBERS' EQUITY

COMPREHENSIVE INCOME

Read the accompanying notes to these financial statements.

11

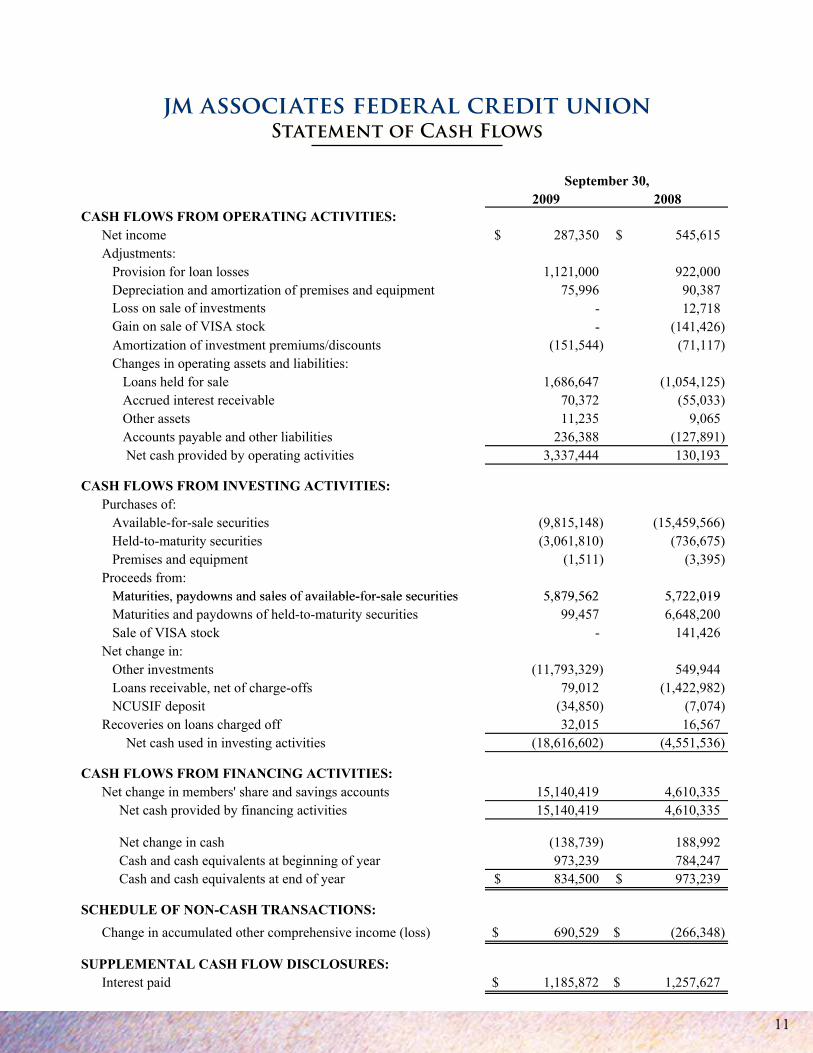

jm associates federal credit unionStatement of Cash Flows

2009 2008CASH FLOWS FROM OPERATING ACTIVITIES: Net income 287,350$ 545,615$ Adjustments: Provision for loan losses 1,121,000 922,000 Depreciation and amortization of premises and equipment 75,996 90,387 Loss on sale of investments - 12,718 Gain on sale of VISA stock - (141,426) Amortization of investment premiums/discounts (151,544) (71,117) Changes in operating assets and liabilities: Loans held for sale 1,686,647 (1,054,125) Accrued interest receivable 70,372 (55,033) Other assets 11,235 9,065 Accounts payable and other liabilities 236,388 (127,891) Net cash provided by operating activities 3,337,444 130,193

CASH FLOWS FROM INVESTING ACTIVITIES: Purchases of: Available-for-sale securities (9,815,148) (15,459,566) Held-to-maturity securities (3,061,810) (736,675) Premises and equipment (1,511) (3,395) Proceeds from:

Maturities paydowns and sales of available-for-sale securities 5 879 562 5 722 019

September 30,

JM ASSOCIATES FEDERAL CREDIT UNIONSTATEMENTS OF CASH FLOWS

Read the accompanying notes to these financial statements.

Maturities, paydowns and sales of available-for-sale securities 5,879,562 5,722,019 Maturities and paydowns of held-to-maturity securities 99,457 6,648,200 Sale of VISA stock - 141,426 Net change in: Other investments (11,793,329) 549,944 Loans receivable, net of charge-offs 79,012 (1,422,982) NCUSIF deposit (34,850) (7,074) Recoveries on loans charged off 32,015 16,567 Net cash used in investing activities (18,616,602) (4,551,536)

CASH FLOWS FROM FINANCING ACTIVITIES: Net change in members' share and savings accounts 15,140,419 4,610,335 Net cash provided by financing activities 15,140,419 4,610,335

Net change in cash (138,739) 188,992 Cash and cash equivalents at beginning of year 973,239 784,247 Cash and cash equivalents at end of year 834,500$ 973,239$

SCHEDULE OF NON-CASH TRANSACTIONS: Change in accumulated other comprehensive income (loss) 690,529$ (266,348)$

SUPPLEMENTAL CASH FLOW DISCLOSURES: Interest paid 1,185,872$ 1,257,627$

Read the accompanying notes to these financial statements.

12

jm associates federal credit unionNOTES TO THE FINANCIAL STATEMENTS

Organization

Use of Estimates

Cash and Cash Equivalents

Investments

The preparation of financial statements in conformity with generally accepted accounting principles in the UnitedStates (GAAP) requires Management to make estimates and assumptions that affect the reported amounts of assetsand liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and thereported amounts of revenues and expense during the reporting period. Specifically, Management has madeestimates based on assumptions for fair value of financial instruments and the assessment of other than temporaryimpairment on investments. Actual results could differ from these estimates.

For purposes of the statement of financial condition and the statement of cash flows, cash and cash equivalentsincludes cash on hand, amounts due from financial institutions, and highly liquid debt instruments classified ascash which were purchased with maturities of three months or less. Amounts due from financial institutions may,at times, exceed federally insured limits.

JM Associates Federal Credit Union (the "Credit Union") is a cooperative association organized in accordance withthe provisions of the Federal Credit Union Act for the purposes of promoting thrift among, and creating a source ofcredit for its members. Participation in the Credit Union is limited to those individuals that qualify formembership. The field of membership is defined in the Credit Union's Charter and Bylaws.

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

NOTE 1: SIGNIFICANT ACCOUNTING POLICIES

Other Investments: Investments in this category do not meet the definition of a debt or equity security underaccounting pronouncements. Other investments may include certain cash equivalents that Management has electedto classify as investments. Other investments are stated at the lower of cost or market.

The Credit Union's investments are classified and accounted for as follows:

Held-to-Maturity : Investments which the Credit Union has the positive intent and ability to hold to maturity arereported at cost, adjusted for amortization of premiums and accretion of discounts.

Cost of investments sold are recognized using the specific identification method. The amortization of premiumsand the accretion of discounts are recognized over the term of the related investment by a method that approximatesthe interest method.

Available-for-Sale: Investments are classified available-for-sale when Management anticipates that the securitiescould be sold in response to rate changes, prepayment risk, liquidity, availability of and the yield on alternativeinvestments and other market and economic factors. These securities are reported at fair value. Unrealized gainsand losses on securities available for sale are recognized as direct increases or decreases in members' equity andcomprehensive income. Cost of investments sold are recognized using the specific identification method. Theamortization of premiums and the accretion of discounts are recognized over the term of the related investment by amethod that approximates the interest method.

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

NOTE 1: SIGNIFICANT ACCOUNTING POLICIES

13

jm associates federal credit unionnotes to the financial statements

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Visa Inc. Stock

Loans Held for Sale

Loans Receivable

Loans originated and intended for sale in the secondary market are carried at the lower of aggregate cost orestimated market value in the aggregate. Net unrealized losses are recognized in a valuation allowance by chargesto income. All sales are made without recourse.

During 2008, the Credit Union received notice of the restructuring of Visa Inc. As part of the restructuring, theCredit Union was issued shares of Class B Common Stock in Visa Inc. The shares represented by this issuance arefully paid and non-assessable. During the first quarter of 2008, there was a partial redemption of the Credit Union'sClass B Common Stock in Visa Inc. leaving a balance of 5,245 shares. Currently, there is no readily available fairmarket value of the stock and therefore, the stock is not reflected in the Credit Union’s financial statements. Oncea readily available fair market value of the stock is available, the value of the stock will be reflected in the CreditUnion's financial statements.

The Credit Union grants mortgage, commercial, and consumer loans to members. The ability of the members tohonor their contract is dependent upon the real estate and general economic conditions of the area.

Management periodically performs analyses to test for impairment of various assets. A significant impairmentanalysis relates to the other than temporary declines in the value of the securities. Management conducts periodicreviews and evaluations of the securities portfolio to determine if the value of any security has declined below itscarrying value and whether such a decline is other than temporary. If such decline is deemed other than temporary,Management would adjust the amount of the security by writing it down to fair market value through a charge tocurrent period operations.

Allowance for Loan Losses

Loans that the Credit Union has the intent and ability to hold for the foreseeable future or until maturity or payoffare reported at principal balance outstanding, net of an allowance for loan losses and net deferred loan originationfees and costs. Interest income is recognized over the term of the loan and is calculated using the specific loaninterest rate and the number of days outstanding during the period.

The allowance for loan losses is a valuation allowance for probable incurred credit losses, increased by theprovision for loan losses and decreased by charge-offs less recoveries. Management estimates the allowancebalance required using past loan loss experience, known and inherent risks in the nature and volume of theportfolio, information about specific borrower situations and estimated collateral values, economic conditions, andother factors. Allocations of the allowance may be made for specific loans, but the entire allowance is available forany loan that, in Management's judgment, should be charged-off. Loan losses are charged against the allowance forloan losses when Management believes the uncollectibility of a loan balance is confirmed.

Interest income is not reported when full loan repayment is in doubt, typically when the loan is impaired orpayments are past due over 90 days. All interest accrued but not received for loans placed on nonaccrual isreversed against interest income. Interest received on such loans is accounted for on the cash basis or cost-recoverymethod, until qualifying for return to accrual. Loans are returned to accrual status when all the principal andinterest amounts contractually due are brought current and future payments are reasonably assured.

The allowance consists of specific and general components. The specific component relates to loans that areindividually classified as impaired or loans otherwise classified as substandard or doubtful. The generalcomponent covers non-classified loans and is based on historical loss experience adjusted for current factors.

14

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Premises and Equipment

NCUSIF Deposit

Furniture and equipment, and leasehold improvements are carried at cost, less accumulated depreciation andamortization. Furniture, and equipment are depreciated using the straight-line method over the estimated usefullives of the assets. The cost of leasehold improvements is amortized using the straight-line method over the termsof the related leases. Maintenance and repairs are expensed, and major improvements are capitalized.Management reviews premises and equipment for impairment whenever events or changes in circumstancesindicate that the carrying value may not be recoverable. Gains and losses on disposals are included in currentoperations.

The deposit in the National Credit Union Share Insurance Fund (NCUSIF) is in accordance with National CreditUnion Administration (NCUA) regulations, which require the maintenance of a deposit by each insured creditunion in an amount equal to one percent of its insurable shares, less any reportable impairment. The deposit wouldbe refunded to the Credit Union if its insurance coverage is terminated, it converts to insurance coverage fromanother source, or the operations of the fund are transferred from the NCUA Board.

On January 28, 2009, the NCUA approved a corporate stabilization effort designed to enhance and support acorporate credit union system facing unprecedented strains on liquidity and capital due to extraordinary marketdi ti d th t i li t Th t bili ti ff t i l d d th i f $1 billi it l

A loan is impaired when full payment under the loan terms is not expected. Impairment is generally evaluated intotal for smaller-balance loans of similar nature such as residential mortgage, consumer, and credit card loans, butmay be evaluated on an individual loan basis if deemed necessary. If a loan is impaired, a portion of the allowanceis allocated so that the loan is reported, net, at the present value of estimated future cash flows using the loan'sexisting rate or at the fair value of collateral if repayment is expected solely from the collateral.

NCUSIF Insurance Premium

On May 20, 2009, the President of the United States of America signed into law the NCUA’s CorporateStabilization Fund. The new law gave the NCUA a variety of tools to ease the burden of the estimated $6 billioncost of the corporate bailout of credit unions, including the ability to spread out the costs for as long as seven years.On September 18, 2009, the NCUA Board approved the Stabilization Fund to pay the NCUSIF $1 billion forassignment of the full right, title and interest in the outstanding capital note extended to U.S. Central Federal CreditUnion executed on January 28, 2009. This action recapitalizes the NCUSIF to the point that the fund is no longerimpaired. As a result of the recapitalization of the NCUSIF, the Credit Union recognized non-interest income ofapproximately $327,000. Additionally, the NCUA Board revised their special assessment to 0.15 percent of acredit union’s insured shares up to $250,000 which resulted in a $92,000 reduction of the original special premiumassessment recorded by the Credit Union.

A credit union is required to pay an annual insurance premium equal to one-twelfth of one percent of its totalinsured shares, unless the payment is waived or reduced by the NCUA Board.

disruptions and the current economic climate. The stabilization effort included the issuance of a $1 billion capitalnote to U.S. Central Corporate Federal Credit Union and a declaration of a premium assessment to restore theNCUSIF equity ratio to 1.30 percent, to be collected from all federally-insured credit unions in 2009. Eachfederally-insured credit union was required to record a write-down of their NCUSIF deposit as well as record aspecial premium assessment. As a result of these actions, the Credit Union's NCUSIF deposit was impaired byapproximately 69% of its value. This impairment approximated $327,000 and was reflected in the incomestatement in operating expenses. The Credit Union's special premium assessment to restore the NCUSIF equityratio to 1.30 percent approximated $183,000 which was also reflected in the income statement in operatingexpenses.

15

jm associates federal credit unionnotes to the financial statements

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Premises and Equipment

NCUSIF Deposit

Furniture and equipment, and leasehold improvements are carried at cost, less accumulated depreciation andamortization. Furniture, and equipment are depreciated using the straight-line method over the estimated usefullives of the assets. The cost of leasehold improvements is amortized using the straight-line method over the termsof the related leases. Maintenance and repairs are expensed, and major improvements are capitalized.Management reviews premises and equipment for impairment whenever events or changes in circumstancesindicate that the carrying value may not be recoverable. Gains and losses on disposals are included in currentoperations.

The deposit in the National Credit Union Share Insurance Fund (NCUSIF) is in accordance with National CreditUnion Administration (NCUA) regulations, which require the maintenance of a deposit by each insured creditunion in an amount equal to one percent of its insurable shares, less any reportable impairment. The deposit wouldbe refunded to the Credit Union if its insurance coverage is terminated, it converts to insurance coverage fromanother source, or the operations of the fund are transferred from the NCUA Board.

On January 28, 2009, the NCUA approved a corporate stabilization effort designed to enhance and support acorporate credit union system facing unprecedented strains on liquidity and capital due to extraordinary marketdi ti d th t i li t Th t bili ti ff t i l d d th i f $1 billi it l

A loan is impaired when full payment under the loan terms is not expected. Impairment is generally evaluated intotal for smaller-balance loans of similar nature such as residential mortgage, consumer, and credit card loans, butmay be evaluated on an individual loan basis if deemed necessary. If a loan is impaired, a portion of the allowanceis allocated so that the loan is reported, net, at the present value of estimated future cash flows using the loan'sexisting rate or at the fair value of collateral if repayment is expected solely from the collateral.

NCUSIF Insurance Premium

On May 20, 2009, the President of the United States of America signed into law the NCUA’s CorporateStabilization Fund. The new law gave the NCUA a variety of tools to ease the burden of the estimated $6 billioncost of the corporate bailout of credit unions, including the ability to spread out the costs for as long as seven years.On September 18, 2009, the NCUA Board approved the Stabilization Fund to pay the NCUSIF $1 billion forassignment of the full right, title and interest in the outstanding capital note extended to U.S. Central Federal CreditUnion executed on January 28, 2009. This action recapitalizes the NCUSIF to the point that the fund is no longerimpaired. As a result of the recapitalization of the NCUSIF, the Credit Union recognized non-interest income ofapproximately $327,000. Additionally, the NCUA Board revised their special assessment to 0.15 percent of acredit union’s insured shares up to $250,000 which resulted in a $92,000 reduction of the original special premiumassessment recorded by the Credit Union.

A credit union is required to pay an annual insurance premium equal to one-twelfth of one percent of its totalinsured shares, unless the payment is waived or reduced by the NCUA Board.

disruptions and the current economic climate. The stabilization effort included the issuance of a $1 billion capitalnote to U.S. Central Corporate Federal Credit Union and a declaration of a premium assessment to restore theNCUSIF equity ratio to 1.30 percent, to be collected from all federally-insured credit unions in 2009. Eachfederally-insured credit union was required to record a write-down of their NCUSIF deposit as well as record aspecial premium assessment. As a result of these actions, the Credit Union's NCUSIF deposit was impaired byapproximately 69% of its value. This impairment approximated $327,000 and was reflected in the incomestatement in operating expenses. The Credit Union's special premium assessment to restore the NCUSIF equityratio to 1.30 percent approximated $183,000 which was also reflected in the income statement in operatingexpenses.

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Members' Share and Savings Accounts

Regular Reserve

Members' shares are the savings deposit accounts of the owners of the Credit Union. Share ownership entitles themembers to vote in annual elections of the Board of Directors and on other corporate matters. Irrespective of theamount of shares owned, no member has more than one vote. Members' shares are subordinated to all otherliabilities of the Credit Union upon liquidation. Interest on members' share and savings accounts is based onavailable earnings at the end of an interest period and is not guaranteed by the Credit Union. Interest rates onmembers' share accounts are set by the Board of Directors, based on an evaluation of current and future marketconditions.

The Credit Union is required by regulation to maintain a statutory reserve. This reserve, which represents aregulatory restriction of undivided earnings, is not available for the payment of dividends.

Recent Accounting PronouncementsThe Financial Accounting Standards Board (FASB) issued Statement #168, The FASB Accounting StandardsCodification and the Hierarchy of Generally Accepted Accounting Principles, which is codified at FASB ASC 105.FASB ASC 105 establishes FASB ASC as the source of authoritative GAAP recognized by FASB to be applied bynongovernmental entities. Rules and interpretive releases of the SEC under authority of federal securities laws arealso sources of authoritative GAAP for SEC registrants. FASB ASC supersedes all existing non-SEC accountingand reporting standards. All other nongrandfathered, non-SEC accounting literature not included in FASB ASC hasbecome nonauthoritative. FASB will no longer issue new standards in the form of Statements, FASB StaffPositions (FSPs) or Emerging Issues Task Force Abstracts. Instead, it will issue Accounting Standards Updates,which will serve to update FASB ASC, provide background information about the guidance and provide the basisfor conclusions on the changes to FASB ASC FASB ASC is not intended to change U S GAAP or any

In April 2009, the FASB issued FSP FAS 115-2 and FAS 124- 2, Recognition and Presentation of Other-Than-Temporary Impairments (OTTI), which is primarily, codified FASB ASC 320-10. This recent guidance amends therecognition guidance for other-than-temporary impairments of debt securities and expands the financial statementdisclosures for OTTI on debt and equity securities. This FSP replaced the “intent and ability” indication in currentguidance by specifying that (a) if a company does not have the intent to sell a debt security prior to recovery and(b) it is more likely than not that it will not have to sell the debt security prior to recovery, the security would notbe considered other-than-temporarily impaired unless there is a credit loss. When an entity does not intend to sellthe security and it is more likely than not, the entity will not have to sell the security before recovery of its costbasis, it will recognize the credit component of an OTTI of a debt security in earnings and the remaining portion inother comprehensive income. For held-to-maturity (HTM) debt securities, the amount of OTTI recorded in othercomprehensive income for the non-credit portion of a previous OTTI should be amortized prospectively over theremaining life of the security on the basis of the timing of future estimated cash flows of the security.

In December 2007, the FASB FAS #141r which is codified at FASB ASC 805. This Statement replaces FAS #141,Business Combinations, but retains the fundamental requirements in Statement 141 that the acquisition method ofaccounting be used for all business combinations. This Statement’s scope is broader than that of Statement 141,which applied only to business combinations in which control was obtained by transferring consideration. Theapplication of FAS 141r to a merger between two credit unions will generally result in the recognition of eithergoodwill or a bargain purchase gain. Goodwill is added to the acquirer’s balance sheet and reviewed forimpairment, while the bargain purchase gain is recorded to the income statement in the period of the merger.

for conclusions on the changes to FASB ASC. FASB ASC is not intended to change U.S. GAAP or anyrequirements of the SEC. This statement is effective for financial statements issued for interim and annual periodsending after September 15, 2009.

16

jm associates federal credit unionnotes to the financial statements

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Federal and State Tax Exemption

Comprehensive Income

Advertising Costs

Reclassifications

Beginning with audit periods ending December 31, 2008, fair value estimates must follow the requirement set forthin FAS #157 “Fair Value Measurements” which is codified at FASB ASC 820. FAS #157, establishes a frameworkfor measuring fair value in generally accepted accounting principles (GAAP), and expands disclosures about fairvalue measurements. This Statement applies under other accounting pronouncements that require or permit fairvalue measurements, the Board having previously concluded in those accounting pronouncements that fair value isthe relevant measurement attribute. Accordingly, this Statement does not require any new fair value measurements.However, for some entities, the application of this Statement will change current practice.

This Statement applies prospectively to business combinations for which the acquisition date is on or after thebeginning of the first annual reporting period beginning on or after December 15, 2008. An entity may not apply itbefore that date.

The Credit Union is exempt from federal and most state and local taxes under the provisions of the Federal CreditUnion Act, the Internal Revenue Code, and state tax laws.

Accounting principles generally require that recognized revenue, expenses, gains, and losses be included in netincome. Certain changes in assets, liabilities, such as unrealized gains and losses on available-for-sale securities,are reported as a separate component of the member equity section of the statements of financial condition.

Advertising costs are expensed as incurred.

Certain 2008 financial statement amounts have been reclassified to conform with classifications adopted in theCertain 2008 financial statement amounts have been reclassified to conform with classifications adopted in thecurrent year.

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Members' Share and Savings Accounts

Regular Reserve

Members' shares are the savings deposit accounts of the owners of the Credit Union. Share ownership entitles themembers to vote in annual elections of the Board of Directors and on other corporate matters. Irrespective of theamount of shares owned, no member has more than one vote. Members' shares are subordinated to all otherliabilities of the Credit Union upon liquidation. Interest on members' share and savings accounts is based onavailable earnings at the end of an interest period and is not guaranteed by the Credit Union. Interest rates onmembers' share accounts are set by the Board of Directors, based on an evaluation of current and future marketconditions.

The Credit Union is required by regulation to maintain a statutory reserve. This reserve, which represents aregulatory restriction of undivided earnings, is not available for the payment of dividends.

Recent Accounting PronouncementsThe Financial Accounting Standards Board (FASB) issued Statement #168, The FASB Accounting StandardsCodification and the Hierarchy of Generally Accepted Accounting Principles, which is codified at FASB ASC 105.FASB ASC 105 establishes FASB ASC as the source of authoritative GAAP recognized by FASB to be applied bynongovernmental entities. Rules and interpretive releases of the SEC under authority of federal securities laws arealso sources of authoritative GAAP for SEC registrants. FASB ASC supersedes all existing non-SEC accountingand reporting standards. All other nongrandfathered, non-SEC accounting literature not included in FASB ASC hasbecome nonauthoritative. FASB will no longer issue new standards in the form of Statements, FASB StaffPositions (FSPs) or Emerging Issues Task Force Abstracts. Instead, it will issue Accounting Standards Updates,which will serve to update FASB ASC, provide background information about the guidance and provide the basisfor conclusions on the changes to FASB ASC FASB ASC is not intended to change U S GAAP or any

In April 2009, the FASB issued FSP FAS 115-2 and FAS 124- 2, Recognition and Presentation of Other-Than-Temporary Impairments (OTTI), which is primarily, codified FASB ASC 320-10. This recent guidance amends therecognition guidance for other-than-temporary impairments of debt securities and expands the financial statementdisclosures for OTTI on debt and equity securities. This FSP replaced the “intent and ability” indication in currentguidance by specifying that (a) if a company does not have the intent to sell a debt security prior to recovery and(b) it is more likely than not that it will not have to sell the debt security prior to recovery, the security would notbe considered other-than-temporarily impaired unless there is a credit loss. When an entity does not intend to sellthe security and it is more likely than not, the entity will not have to sell the security before recovery of its costbasis, it will recognize the credit component of an OTTI of a debt security in earnings and the remaining portion inother comprehensive income. For held-to-maturity (HTM) debt securities, the amount of OTTI recorded in othercomprehensive income for the non-credit portion of a previous OTTI should be amortized prospectively over theremaining life of the security on the basis of the timing of future estimated cash flows of the security.

In December 2007, the FASB FAS #141r which is codified at FASB ASC 805. This Statement replaces FAS #141,Business Combinations, but retains the fundamental requirements in Statement 141 that the acquisition method ofaccounting be used for all business combinations. This Statement’s scope is broader than that of Statement 141,which applied only to business combinations in which control was obtained by transferring consideration. Theapplication of FAS 141r to a merger between two credit unions will generally result in the recognition of eithergoodwill or a bargain purchase gain. Goodwill is added to the acquirer’s balance sheet and reviewed forimpairment, while the bargain purchase gain is recorded to the income statement in the period of the merger.

for conclusions on the changes to FASB ASC. FASB ASC is not intended to change U.S. GAAP or anyrequirements of the SEC. This statement is effective for financial statements issued for interim and annual periodsending after September 15, 2009.

17

jm associates federal credit unionnotes to the financial statements

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Gross GrossAmortized Unrealized Unrealized Fair

Cost Gains Losses ValueFederal agency securities 16,219,704$ 351,795$ (28,657)$ 16,542,842$Bank notes and certificates 3,948,761 59,313 (39,212) 3,968,862 Total 20,168,465$ 411,108$ (67,869)$ 20,511,704$

Gross GrossAmortized Unrealized Unrealized Fair

Cost Gains Losses ValueFederal agency securities 13,537,105$ 22,356$ (234,968)$ 13,324,493$Bank notes and certificates 2,494,426 9,259 (143,937) 2,359,748

Total 16 031 531$ 31 615$ (378 905)$ 15 684 241$

September 30, 2009

Investments classified as available-for-sale securities consist of the following:Available-for-Sale

September 30, 2008

NOTE 2: INVESTMENTS

Total 16,031,531$ 31,615$ (378,905)$ 15,684,241$

FairValue

Unrealized Losses

FairValue

Unrealized Losses

Federal agency securities 16,542,842$ (28,657)$ -$ -$Bank notes and certificates 1,245,836 (2,792) 2,723,026 (36,420)

17,788,678$ (31,449)$ 2,723,026$ (36,420)$

FairValue

Unrealized Losses

FairValue

Unrealized Losses

Federal agency securities 7,438,678$ (135,478)$ 1,863,872$ (99,493)$Bank notes and certificates 1,622,265 (143,934) - -

9,060,943$ (279,412)$ 1,863,872$ (99,493)$

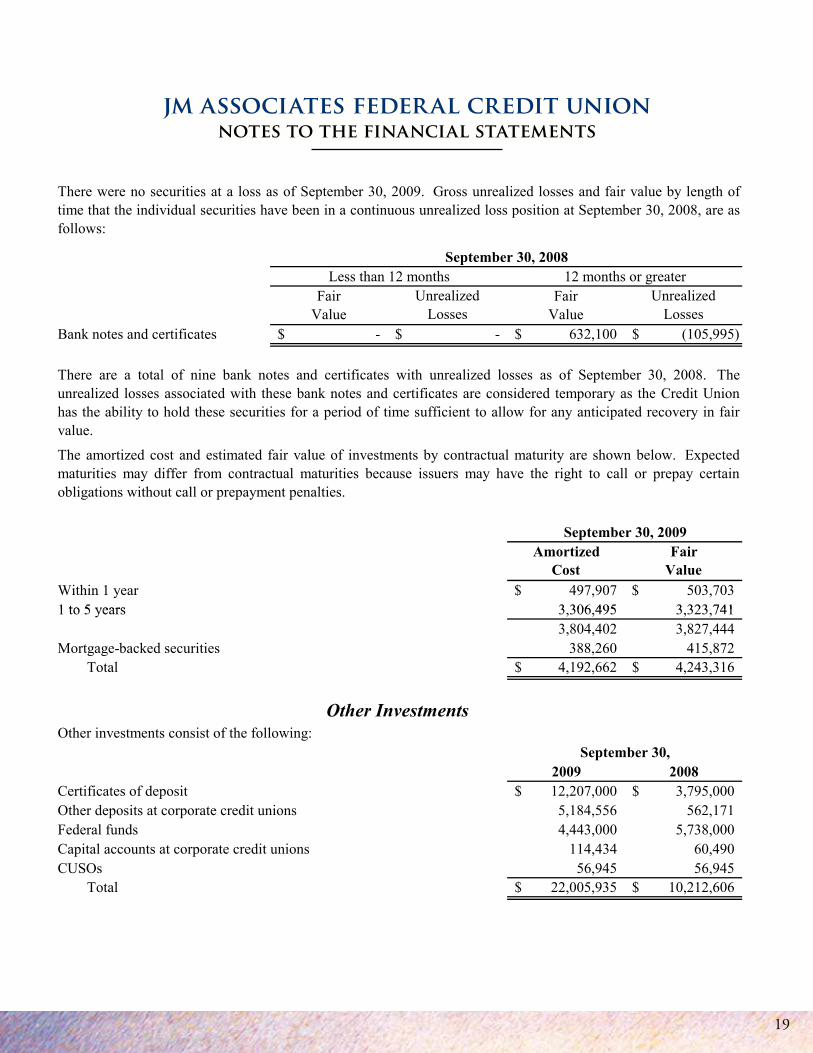

Gross unrealized losses and fair value by length of time that the individual securities have been in a continuousunrealized loss position at September 30, 2009 and 2008, are as follows:

September 30, 2009

Less than 12 months

Less than 12 months

September 30, 200812 months or greater

12 months or greater

18

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNION

NOTES TO THE FINANCIAL STATEMENTS

Amortized FairCost Value

Within 1 year 746,793$ 759,026$1 to 5 years 3,701,968 3,711,1505 to 10 years 1,032,337 1,008,417

5,481,098 5,478,593Mortgage-backed securities 14,687,367 15,033,111 Total 20,168,465$ 20,511,704$

September 30 2009

There are a total of 11 and 27 debt securities with unrealized losses as of September 30, 2009 and 2008,respectively. The unrealized losses associated with these securities are considered temporary as the Credit Unionhas the ability to hold these securities for a period of time sufficient to allow for any anticipated recovery in fairvalue.

September 30, 2009

The amortized cost and estimated fair value of investments by contractual maturity are shown below. Expectedmaturities may differ from contractual maturities because issuers may have the right to call or prepay certainobligations without call or prepayment penalties.

Investments classified as held-to maturity securities consist of the following:Held-to-Maturity

Gross GrossAmortized Unrealized Unrealized Fair

Cost Gains Losses ValueFederal agency securities 3,444,755$ 35,891$ -$ 3,480,646$Bank notes and certificates 747,907 14,763 - 762,670 Total 4,192,662$ 50,654$ -$ 4,243,316$

Gross GrossAmortized Unrealized Unrealized Fair

Cost Gains Losses ValueFederal agency securities 542,018$ 12,825$ -$ 554,843$Bank notes and certificates 738,095 - (105,995) 632,100 Total 1,280,113$ 12,825$ (105,995)$ 1,186,943$

September 30, 2009

September 30, 2008

19

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNION

NOTES TO THE FINANCIAL STATEMENTS

FairValue

Unrealized Losses

FairValue

Unrealized Losses

Bank notes and certificates -$ -$ 632,100$ (105,995)$

Amortized FairCost Value

Within 1 year 497,907$ 503,703$1 to 5 years 3 306 495 3 323 741

September 30, 2009

September 30, 2008

The amortized cost and estimated fair value of investments by contractual maturity are shown below. Expectedmaturities may differ from contractual maturities because issuers may have the right to call or prepay certainobligations without call or prepayment penalties.

There are a total of nine bank notes and certificates with unrealized losses as of September 30, 2008. Theunrealized losses associated with these bank notes and certificates are considered temporary as the Credit Unionhas the ability to hold these securities for a period of time sufficient to allow for any anticipated recovery in fairvalue.

12 months or greater

There were no securities at a loss as of September 30, 2009. Gross unrealized losses and fair value by length oftime that the individual securities have been in a continuous unrealized loss position at September 30, 2008, are asfollows:

Less than 12 months

1 to 5 years 3,306,495 3,323,7413,804,402 3,827,444

Mortgage-backed securities 388,260 415,872 Total 4,192,662$ 4,243,316$

2009 2008Certificates of deposit 12,207,000$ 3,795,000$Other deposits at corporate credit unions 5,184,556 562,171Federal funds 4,443,000 5,738,000Capital accounts at corporate credit unions 114,434 60,490CUSOs 56,945 56,945 Total 22,005,935$ 10,212,606$

September 30,Other investments consist of the following:

Other Investments

20

jm associates federal credit unionnotes to the financial statements

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

The Credit Union maintains share accounts at Southeast Corporate Federal Credit Union, that exceed federallyinsured limits. On January 28, 2009, the NCUA Board announced the Temporary Corporate Credit Union ShareGuarantee Program. The program is part of the Board's plan to stabilize the corporate credit union system inrelation to the strains on its liquidity and capital due to credit market disruptions and the current economic climate.One of the provisions of the plan is to offer a temporary NCUSIF guarantee of member shares in corporate creditunions. The guarantee would cover all shares, except paid-in-capital and membership capital accounts, throughDecember 31, 2011.

The amount of impairment of the Credit Union’s membership capital accounts held by Southeast Corporate FederalCredit Union is not material at this time. Additionally, if there is any additional impairment, it will be writtendown when the asset is deemed impaired.

As a requirement of membership, the Credit Union is required to maintain a membership capital account atSoutheast Corporate Federal Credit Union. A membership capital share account is a restricted share base that issubject to depletion based on the financial health of the corporate credit union. Therefore, membership capitalshare account balances could become impaired. Included in the deposit at Southeast Corporate Federal CreditUnion is the restricted membership capital share base which approximated $114,000 and $60,000 as of September30, 2009 and 2008, respectively.

NOTE 3: LOANS RECEIVABLE AND ALLOWANCE FOR LOAN LOSSES

Loans receivable consist of the following:

2009 2008Real estate loans: Fixed rate 4,949,201$ 4,204,320$ Variable rate 4,105,967 4,503,766

9,055,168 8,708,086

Vehicle loans 12,775,678 14,004,752Unsecured loans 8,629,262 8,760,824Other consumer loans 1,298,053 1,033,771

31,758,161 32,507,433Allowance for loan losses (1,172,121) (689,366) Loans receivable, net 30,586,040$ 31,818,067$

Loans on which the accrual of interest has been discontinued or reduced approximated $467,000 and $22,000 as ofSeptember 30, 2009 and 2008, respectively. If interest on these loans had been accrued, such income would haveapproximated $32,000 and $5,000 as of September 30, 2009 and 2008, respectively.

September 30,

21

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNION

NOTES TO THE FINANCIAL STATEMENTS

The following summarizes the activity in the allowance for loan losses account:

2009 2008Balance, beginning of year 689,366$ 238,433$Provision for loan losses 1,121,000 922,000Recoveries 32,015 16,567Loans charged off (670,260) (487,634)Balance, end of year 1,172,121$ 689,366$

Premises and equipment consist of the following:

2009 2008Furniture and equipment 531,690$ 530,179$Leasehold improvements 10,449 10,449

542,139 540,628 Less accumulated depreciation and amortization (506,511) (430,515) Premises and equipment, net 35,628$ 110,113$

September 30,

September 30,

NOTE 4: PREMISES AND EQUIPMENT

NOTE 5 MEMBERS' SHARE AND SAVINGS ACCOUNTS

Members' share and savings accounts consist of the following:

2009 2008Share draft accounts 10,121,781$ 9,005,387$Money market accounts 30,833,434 19,942,651Share accounts 8,243,781 7,907,490IRA share accounts 3,324,456 2,818,721Certificate accounts 17,677,561 15,386,345 Total share and savings accounts 70,201,013$ 55,060,594$

September 30,

NOTE 5: MEMBERS' SHARE AND SAVINGS ACCOUNTS

22

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNION

NOTES TO THE FINANCIAL STATEMENTS

2009 20080.25% - 1.00% 10,748$ 56,279$1.01% - 2.00% 5,376,164 5,753,8652.01% - 3.00% 4,658,689 3,977,3343.01% - 4.00% 4,710,314 4,317,7814.01% - 5.00% 1,731,469 1,281,0865.01% - 5.10% 1,190,177 -

17,677,561$ 15,386,345$

Year ending September 30, Amount2010 14,867,987$2011 1,184,1032012 540,3102013 721,3172014 363,844

17 677 561$

Scheduled rates of certificate accounts are as follows:

The aggregate amount of certificate accounts in denominations of $100,000 or more were approximately$5,110,000 and $1,286,000 as of September 30, 2009 and 2008, respectively.

As of September 30, 2009, scheduled maturities of certificate accounts are as follows:

September 30,

17,677,561$

401(k) Plan & Trust

The Helping Families Save Their Homes Act of 2009, signed into law May 20, 2009, includes a provisionextending $250,000 share insurance coverage provided by the NCUSIF through December 31, 2013. Previously,this level of coverage was set to expire December 31, 2009. The new law also requires NCUA to use the higher$250,000 standard maximum share insurance amount when making decisions about premiums and administeringinsurance deposit adjustments. This includes all account types, such as savings, checking, money market, andcertificates of deposit. Individual Retirement Account coverage remains at the previously established level of$250,000.

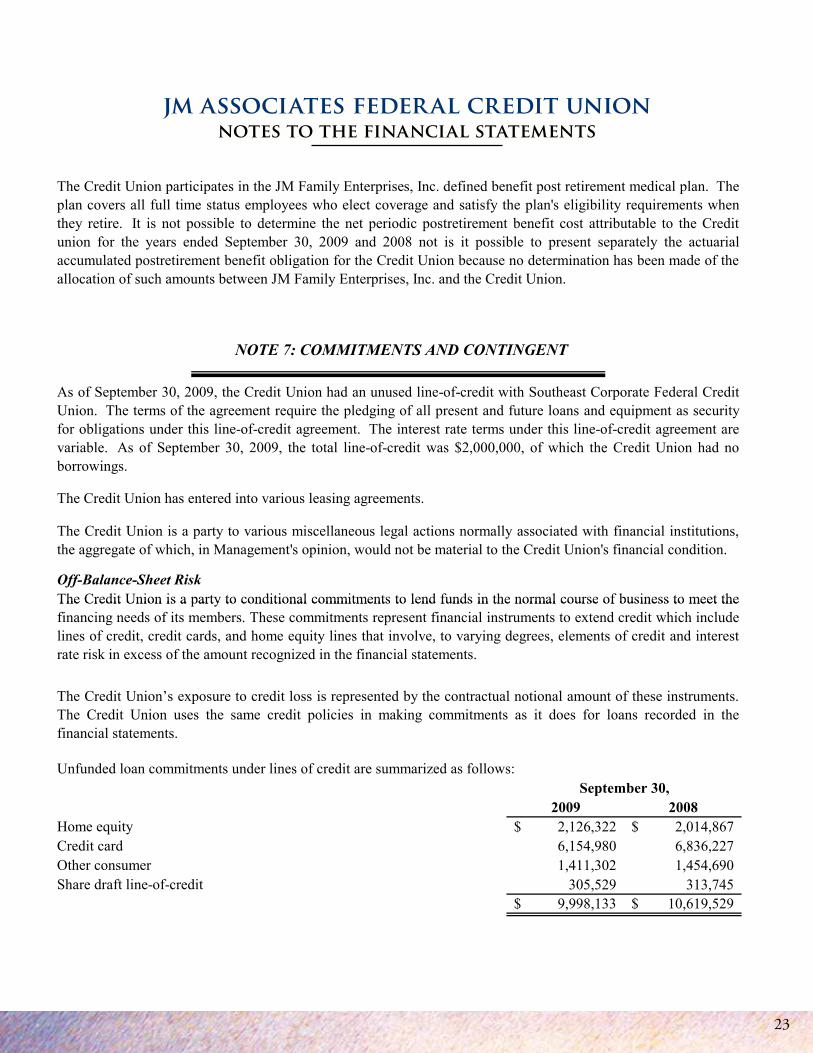

Employees of the Credit Union are participants in the JM Family Enterprises, Inc. pension plans. The plans include a contributory defined contribution pension plan, a noncontributory defined benefit pension plan, and anoncontributory profit sharing plan. It is not possible to determine the net pension expense for the Credit Union forthe years ended September 30, 2009 and 2008 or to present separately the actuarial present value of benefitobligations or the net assets available for benefits of the Credit Union because no determination has been made ofthe allocation of such amounts between JM Family Enterprises, Inc. and the Credit Union.

NOTE 6: EMPLOYEE BENEFITS

23

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNION

NOTES TO THE FINANCIAL STATEMENTS

Off-Balance-Sheet Risk

As of September 30, 2009, the Credit Union had an unused line-of-credit with Southeast Corporate Federal CreditUnion. The terms of the agreement require the pledging of all present and future loans and equipment as securityfor obligations under this line-of-credit agreement. The interest rate terms under this line-of-credit agreement arevariable. As of September 30, 2009, the total line-of-credit was $2,000,000, of which the Credit Union had noborrowings.

The Credit Union is a party to various miscellaneous legal actions normally associated with financial institutions,the aggregate of which, in Management's opinion, would not be material to the Credit Union's financial condition.

The Credit Union is a party to conditional commitments to lend funds in the normal course of business to meet the

The Credit Union has entered into various leasing agreements.

The Credit Union participates in the JM Family Enterprises, Inc. defined benefit post retirement medical plan. Theplan covers all full time status employees who elect coverage and satisfy the plan's eligibility requirements whenthey retire. It is not possible to determine the net periodic postretirement benefit cost attributable to the Creditunion for the years ended September 30, 2009 and 2008 not is it possible to present separately the actuarialaccumulated postretirement benefit obligation for the Credit Union because no determination has been made of theallocation of such amounts between JM Family Enterprises, Inc. and the Credit Union.

NOTE 7: COMMITMENTS AND CONTINGENT

2009 2008Home equity 2,126,322$ 2,014,867$Credit card 6,154,980 6,836,227Other consumer 1,411,302 1,454,690Share draft line-of-credit 305,529 313,745

9,998,133$ 10,619,529$

September 30,

The Credit Union’s exposure to credit loss is represented by the contractual notional amount of these instruments.The Credit Union uses the same credit policies in making commitments as it does for loans recorded in thefinancial statements.

The Credit Union is a party to conditional commitments to lend funds in the normal course of business to meet thefinancing needs of its members. These commitments represent financial instruments to extend credit which includelines of credit, credit cards, and home equity lines that involve, to varying degrees, elements of credit and interestrate risk in excess of the amount recognized in the financial statements.

Unfunded loan commitments under lines of credit are summarized as follows:

24

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNION

NOTES TO THE FINANCIAL STATEMENTS

Concentrations of Credit Risk

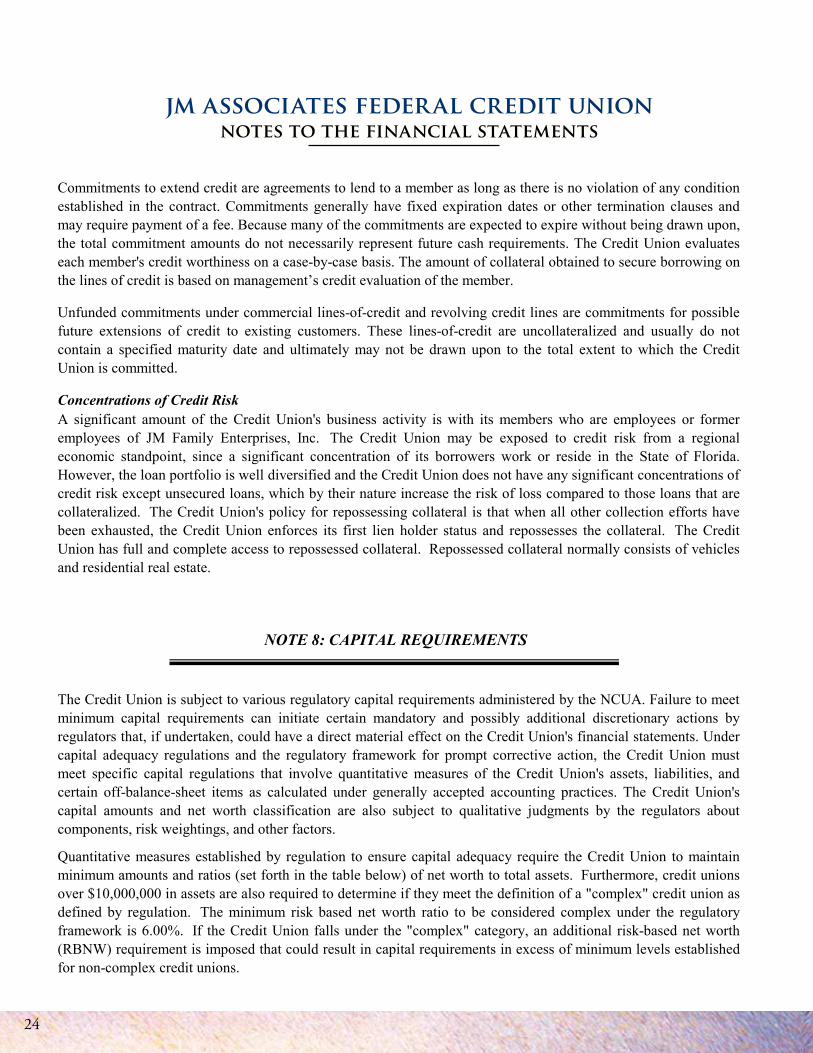

Unfunded commitments under commercial lines-of-credit and revolving credit lines are commitments for possiblefuture extensions of credit to existing customers. These lines-of-credit are uncollateralized and usually do notcontain a specified maturity date and ultimately may not be drawn upon to the total extent to which the CreditUnion is committed.

Commitments to extend credit are agreements to lend to a member as long as there is no violation of any conditionestablished in the contract. Commitments generally have fixed expiration dates or other termination clauses andmay require payment of a fee. Because many of the commitments are expected to expire without being drawn upon,the total commitment amounts do not necessarily represent future cash requirements. The Credit Union evaluateseach member's credit worthiness on a case-by-case basis. The amount of collateral obtained to secure borrowing onthe lines of credit is based on management’s credit evaluation of the member.

A significant amount of the Credit Union's business activity is with its members who are employees or formeremployees of JM Family Enterprises, Inc. The Credit Union may be exposed to credit risk from a regionaleconomic standpoint, since a significant concentration of its borrowers work or reside in the State of Florida.However, the loan portfolio is well diversified and the Credit Union does not have any significant concentrations ofcredit risk except unsecured loans, which by their nature increase the risk of loss compared to those loans that arecollateralized. The Credit Union's policy for repossessing collateral is that when all other collection efforts havebeen exhausted, the Credit Union enforces its first lien holder status and repossesses the collateral. The CreditUnion has full and complete access to repossessed collateral. Repossessed collateral normally consists of vehiclesand residential real estate.

The Credit Union is subject to various regulatory capital requirements administered by the NCUA. Failure to meetminimum capital requirements can initiate certain mandatory and possibly additional discretionary actions byregulators that, if undertaken, could have a direct material effect on the Credit Union's financial statements. Undercapital adequacy regulations and the regulatory framework for prompt corrective action, the Credit Union mustmeet specific capital regulations that involve quantitative measures of the Credit Union's assets, liabilities, andcertain off-balance-sheet items as calculated under generally accepted accounting practices. The Credit Union'scapital amounts and net worth classification are also subject to qualitative judgments by the regulators aboutcomponents, risk weightings, and other factors.

Quantitative measures established by regulation to ensure capital adequacy require the Credit Union to maintainminimum amounts and ratios (set forth in the table below) of net worth to total assets. Furthermore, credit unionsover $10,000,000 in assets are also required to determine if they meet the definition of a "complex" credit union asdefined by regulation. The minimum risk based net worth ratio to be considered complex under the regulatoryframework is 6.00%. If the Credit Union falls under the "complex" category, an additional risk-based net worth(RBNW) requirement is imposed that could result in capital requirements in excess of minimum levels establishedfor non-complex credit unions.

NOTE 8: CAPITAL REQUIREMENTS

25

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Risk Based Net Worth Ratio

Is the Credit Union considered complex?

Ratio/ Ratio/Amount Requirement Amount Requirement

Amount needed to beclassified as "well capitalized" 5,545,747$ 7.00% 4,400,919$ 7.00%

Actual net worth 7,830,815$ 9.88% 7,543,465$ 12.00%

No

Key aspects of the Credit Union's minimum capital amounts and ratios are summarized as follows:

September 30, 2008

Yes

Risk Based Net Worth RatioSeptember 30, 2008

General Capital Requirements

5.25%

September 30, 2009

September 30, 20096.49%

NOTE 9: RELATED PARTY TRANSACTIONS

Effective January 1, 2008, the Credit Union adopted the provisions of FASB's Codification for "Fair ValueMeasurements" for assets and liabilities measured and reported at fair value. The Codification defines fair value,establishes a framework for measuring fair value and expands disclosures about fair value measurements.

The fair value of financial instruments represents the fair value in terms of the price in an orderly transactionbetween market participants to sell an asset or transfer a liability in the principal (or most advantageous) market forthe asset or liability. The transaction to sell the asset or transfer the liability is a hypothetical transaction at themeasurement date, considered from the perspective of a market participant that holds the asset or owes the liability.Therefore, the objective of a fair value measurement is to determine the price that would be received to sell theasset or paid to transfer the liability at the measurement date (an exit price).

In the normal course of business, the Credit Union extends credit to Directors, Supervisory Committee membersand executive officers. The aggregate loans to related parties at September 30, 2009 and 2008 are approximately$757,000 and $576,000, respectively. Shares from related parties at September 30, 2009 and 2008 amounted toapproximately $1,979,000 and $1,286,000, respectively.

NOTE 10: FAIR VALUE MEASUREMENTS

26

jm associates federal credit unionnotes to the financial statementsJM ASSOCIATES FEDERAL CREDIT UNION

NOTES TO THE FINANCIAL STATEMENTS

Level 2 inputs are inputs other than quoted prices included within Level 1 that are observable for the asset orliability, either directly or indirectly through corroboration with observable market data (market-corroboratedinputs). If the asset or liability has a specified (contractual) term, a Level 2 input must be observable forsubstantially the full term of the asset or liability. An adjustment to a level 2 input that is significant to the fair

To increase consistency and comparability in fair value measurements and related disclosures, the fair valuehierarchy prioritizes the inputs to valuation techniques used to measure fair value into three broad levels. The fairvalue hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets orliabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). In some cases, the inputs used tomeasure fair value might fall into different levels of the fair value hierarchy. The level in the fair value hierarchywithin which the fair value measurement in its entirety falls shall be determined based on the lowest level input thatis significant to the fair value measurement in its entirety. Assessing the significance of a particular input to the fairvalue measurement in its entirety requires judgment, considering factors specific to the asset or liability.

The availability of inputs relevant to the asset or liability and the relative reliability of the inputs might affect theselection of appropriate valuation techniques.

Level 1 InputsLevel 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that the reportingentity has the ability to access at the measurement date. An active market for the asset or liability is a market inwhich transactions for the asset or liability occur with sufficient frequency and volume to provide pricinginformation on an ongoing basis. In general, a quoted price in an active market provides the most reliable evidenceof fair value and shall be used to measure fair value whenever available.

Level 2 Inputs

Available-for-Sale Securities: Fair values for securities are based on quoted market prices, where available. Ifquoted market prices are not available, fair values are based on quoted market prices of comparable instruments, oron discounted cash flow models based on the expected payment characteristics of the underlying instruments.

y y j p gvalue measurement in its entirety might render the measurement a Level 3 measurement, depending on the level inthe fair value hierarchy within which the inputs used to determine the adjustment fall.

Level 3 InputsLevel 3 inputs are unobservable inputs for the asset or liability. Unobservable inputs shall be used to measure fairvalue to the extent that observable inputs are not available, thereby allowing for situations in which there is little, ifany, market activity for the asset or liability at the measurement date. Therefore, unobservable inputs shall reflectthe reporting Credit Union's own assumptions about the assumptions that market participants would use in pricingthe asset or liability (including assumptions about risk). Unobservable inputs shall be developed based on the bestinformation available in the circumstances, which might include the Credit Union's own data. However, theunobservable inputs shall not ignore information about market participant assumptions that is reasonably availablewithout undue cost and effort.

The asset’s or liability’s fair value measurement level within the fair value hierarchy is based on the lowest level ofany input that is significant to the fair value measurement. Valuation techniques used need to maximize the use ofobservable inputs and minimize the use of unobservable inputs.

Following is a description of the valuation methodologies used for assets measured at fair value. There have beenno changes in the methodologies used at September 30, 2009.

27

jm associates federal credit unionnotes to the financial statements

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Level 2 inputs are inputs other than quoted prices included within Level 1 that are observable for the asset orliability, either directly or indirectly through corroboration with observable market data (market-corroboratedinputs). If the asset or liability has a specified (contractual) term, a Level 2 input must be observable forsubstantially the full term of the asset or liability. An adjustment to a level 2 input that is significant to the fair

To increase consistency and comparability in fair value measurements and related disclosures, the fair valuehierarchy prioritizes the inputs to valuation techniques used to measure fair value into three broad levels. The fairvalue hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets orliabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). In some cases, the inputs used tomeasure fair value might fall into different levels of the fair value hierarchy. The level in the fair value hierarchywithin which the fair value measurement in its entirety falls shall be determined based on the lowest level input thatis significant to the fair value measurement in its entirety. Assessing the significance of a particular input to the fairvalue measurement in its entirety requires judgment, considering factors specific to the asset or liability.

The availability of inputs relevant to the asset or liability and the relative reliability of the inputs might affect theselection of appropriate valuation techniques.

Level 1 InputsLevel 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that the reportingentity has the ability to access at the measurement date. An active market for the asset or liability is a market inwhich transactions for the asset or liability occur with sufficient frequency and volume to provide pricinginformation on an ongoing basis. In general, a quoted price in an active market provides the most reliable evidenceof fair value and shall be used to measure fair value whenever available.

Level 2 Inputs

Available-for-Sale Securities: Fair values for securities are based on quoted market prices, where available. Ifquoted market prices are not available, fair values are based on quoted market prices of comparable instruments, oron discounted cash flow models based on the expected payment characteristics of the underlying instruments.

y y j p gvalue measurement in its entirety might render the measurement a Level 3 measurement, depending on the level inthe fair value hierarchy within which the inputs used to determine the adjustment fall.

Level 3 InputsLevel 3 inputs are unobservable inputs for the asset or liability. Unobservable inputs shall be used to measure fairvalue to the extent that observable inputs are not available, thereby allowing for situations in which there is little, ifany, market activity for the asset or liability at the measurement date. Therefore, unobservable inputs shall reflectthe reporting Credit Union's own assumptions about the assumptions that market participants would use in pricingthe asset or liability (including assumptions about risk). Unobservable inputs shall be developed based on the bestinformation available in the circumstances, which might include the Credit Union's own data. However, theunobservable inputs shall not ignore information about market participant assumptions that is reasonably availablewithout undue cost and effort.

The asset’s or liability’s fair value measurement level within the fair value hierarchy is based on the lowest level ofany input that is significant to the fair value measurement. Valuation techniques used need to maximize the use ofobservable inputs and minimize the use of unobservable inputs.

Following is a description of the valuation methodologies used for assets measured at fair value. There have beenno changes in the methodologies used at September 30, 2009.

JM ASSOCIATES FEDERAL CREDIT UNIONNOTES TO THE FINANCIAL STATEMENTS

Level 1 Level 2 Level 3 TotalAvailable-for-sale securities * 20,511,704$ -$ -$ 20,511,704$Held-to-maturity securities 4,243,316$ -$ -$ 4,243,316$

* - financial instrument measured on a recurring basis.

Held-to-Maturity Securities: Fair values for securities are based on quoted market prices, where available. Ifquoted market prices are not available, fair values are based on quoted market prices of comparable instruments, oron discounted cash flow models based on the expected payment characteristics of the underlying instruments.

Assets at Fair Values as of September 30, 2009

Unless indicated the financial instruments are measured on a non-recurring basis. The fair value of financialinstruments are as follows:

28

INDEPENDENT AUDITOR’S REPORT

December 21, 2009

Supervisory Committee JM Associates Federal Credit Union Jacksonville, Florida

We have audited the accompanying statements of financial condition of JM Associates Federal Credit Union as of September 30, 2009 and 2008, and the related statements of income, members' equity, comprehensive income, and cash flows for the years then ended. These financial statements are the responsibility of the Credit Union's Management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by Management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of JM Associates Federal Credit Union as of September 30, 2009 and 2008, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Nearman, Maynard, Vallez, CPAs Nearman, Maynard, Vallez, CPAs

INDEPENDENT AUDITOR’S REPORT

December 21, 2009

Supervisory Committee JM Associates Federal Credit Union Jacksonville, Florida

We have audited the accompanying statements of financial condition of JM Associates Federal Credit Union as of September 30, 2009 and 2008, and the related statements of income, members' equity, comprehensive income, and cash flows for the years then ended. These financial statements are the responsibility of the Credit Union's Management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by Management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of JM Associates Federal Credit Union as of September 30, 2009 and 2008, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Nearman, Maynard, Vallez, CPAs Nearman, Maynard, Vallez, CPAs

29

30

Dear Members,

Your Supervisory Committee is pleased to provide the following report to you for 2009.

Our independent auditor, Nearman, Maynard, & Vallez (Nearman), Certified Public Accountants, performed the annual audit of JM Associates Federal Credit Union (JMAFCU). The audit for the 12-month period ending September 30, 2009 is complete and resulted in an unqualified opinion. The auditor’s report consisting of the financial statements, corresponding notes to the financial statements and the auditor’s opinion letter are included in the Annual Report booklet.

In addition to the annual audit, Nearman personnel performed internal audit work in the operational areas of: Vendor Risk Assessments, Consumer Loans, Investment Review, Bank Secrecy Act (BSA) and Office of Foreign Assets Control (OFAC) compliance, and Automated Clearing House (ACH) compliance. Additionally, Nearman provided an independent review of the Allowance for Loan and Lease Loss (ALLL) methodology. There were no significant findings resulting from these audits and/or reviews.

An independent auditor, Croysdale Technology Consulting Inc., conducted a review of JMAFCU systems with no significant findings. Members of the Supervisory Committee conducted regular closed account surveys, loan file maintenance and dormant account reviews, and random cash counts at credit union locations, with no significant findings.

The National Credit Union Administration (NCUA) examines the credit union on a regular basis. The last NCUA examination of JMAFCU occurred in March 2009 and resulted in a favorable report with no significant action requirements. The Supervisory Committee believes that all audits and examinations, with their related reports, have shown that the financial statements present a fair and reliable report of the financial condition of JMAFCU.

Respectfully submitted,

Vicki McCombChairman, Supervisory Committee

Supervisory Committee ReportMarch 18, 2010

Vicki McComb

31

Board of Directors

Pam RowerChairman

Maryann SilerSecretary

Skip MurrayDirector

Art MirandiVice Chairman

Jerry CookDirector

Ralph O’DayDirector

Larry JaffeTreasurer

Chuck FowlerDirector

Marty OsborneDirector

8019 Bayberry Road, Jacksonville, FL 32256www.jmafcu.org

Building Better Relationships

We’re here for you!