joint expert opinion - man group · in case of any inconsistencies between the german and english...

TRANSCRIPT

Joint Expert Opinion

on the Equity Value

of MAN SE,

Munich,

as well as on an appropriate recurring compensation payment and an appro-

priate cash compensation in accordance with § 304 AktG, § 305 AktG as at

6 June 2013 in connection with the intended domination and profit and loss

transfer agreement according to § 291.1 AktG between Truck & Bus GmbH,

Wolfsburg and MAN SE, Munich

This English version serves only as an explanatory note and shall not be signed by us.

In case of any inconsistencies between the German and English version of our joint expert opinion,

the German version shall prevail.

PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsgesellschaft

is one of the autonomous and

legally independent member companies of the international PricewaterhouseCoopers network cooperating under PricewaterhouseCoopers International Limited.

-

KPMG AG Wirtschaftsprüfungsgesellschaft,

a subsidiary of KPMG Europe LLP and

a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity.

KPMG PwC

3

Xx

Table of Contents Page

A. Engagement and scope of work ......................................................................................................... 12

B. Principles and methods of valuation .................................................................................................. 15

I. Basics of the valuation ............................................................................................................. 15

II. Appropriate cash compensation according to § 305 AktG ...................................................... 18

III. Appropriate recurring compensation payment according to § 304 AktG ............................... 18

C. Description of the valuation object .................................................................................................... 19

I. Legal and tax situation ............................................................................................................. 19

II. Economic fundamentals .......................................................................................................... 24

1. Business activity .............................................................................................................. 24

a) General information .................................................................................................. 24

b) MAN Truck & Bus division ......................................................................................... 24

c) MAN Latin America division ...................................................................................... 25

d) MAN Diesel & Turbo division ..................................................................................... 26

e) Renk division .............................................................................................................. 28

2. Market and competition ................................................................................................. 30

a) Preliminary remark and economic indicators in comparison.................................... 30

b) Market positioning and competitive environment in the MAN Truck & Bus

division ....................................................................................................................... 31

c) Market positioning and competitive environment in the MAN Latin America

division ....................................................................................................................... 46

d) Market positioning and competitive environment in the MAN Diesel and

Turbo division ............................................................................................................ 49

e) Market positioning and competitive environment in the Renk division ................... 58

3. Net assets, financial position and results of operations ................................................. 63

a) Net assets and financial position ............................................................................... 63

b) Results of operations ................................................................................................. 67

c) Adjustment of the results of operations ................................................................... 73

4. Major success factors of the MAN Group’s business model .......................................... 74

D. Determination of equity value ........................................................................................................... 77

I. Basis for valuation .................................................................................................................... 77

1. Valuation approach and assumptions ............................................................................ 77

KPMG PwC

4

Xx

Table of Contents Page

2. Forecasting procedure and accuracy .............................................................................. 79

II. Financial projections ................................................................................................................ 82

1. Financial planning of earnings before interest and taxes (EBIT) .................................... 82

a) Financial planning of the MAN group ........................................................................ 82

b) Financial planning of MAN Truck & Bus .................................................................... 83

c) Financial planning of MAN Latin America ................................................................. 90

d) Financial planning of MAN Diesel & Turbo ................................................................ 94

e) Financial planning of Renk ....................................................................................... 100

f) Financial planning of the Corporate Center and consolidation .............................. 103

2. Earnings before interest and tax (EBIT) in the terminal value ...................................... 104

3. Net dividends after personal income tax ..................................................................... 108

III. Determination of the discount rate ....................................................................................... 112

1. Risk-free rate ................................................................................................................ 112

2. Risk premium ................................................................................................................ 113

3. Growth rate .................................................................................................................. 118

4. Derivation of the discount rate .................................................................................... 119

IV. Value of operating assets ....................................................................................................... 120

V. Value of the separately valued assets ................................................................................... 120

1. Properties and buildings ............................................................................................... 120

2. Corporate tax credit ...................................................................................................... 121

VI. Equity value ............................................................................................................................ 121

VII. Liquidation value .................................................................................................................... 121

E. Plausibility assessment of the equity value on the basis of multiples ............................................. 123

I. General approach .................................................................................................................. 123

II. Derivation of the multiples .................................................................................................... 124

III. Multiple valuation .................................................................................................................. 125

F. Determination of appropriate cash compensation pursuant to § 305 AktG and the recurring

compensation payment pursuant to § 304 AktG ............................................................................. 127

I. Share price ............................................................................................................................. 127

II. Determination of the appropriate compensation ................................................................. 130

KPMG PwC

5

Xx

Table of Contents Page

III. Determination of the appropriate recurring compensation payment .................................. 131

G. Summary of results .......................................................................................................................... 136

Appendix

General Engagement Terms for Wirtschaftsprüfer and Wirtschaftsprüfungsgesellschaften (German Pub-

lic Auditors and Public Audit Firms) as at January 1, 2002

For computational reasons, there can be rounding differences in the tables

amounting to ± one unit (€, % etc.).

KPMG PwC

6

Xx

List of abbreviations

% Percent

§ Article

€ Euro

AB Aktiebolag (limited company in Sweden)

AG Aktiengesellschaft (German public limited company)

Agrale Agrale S.A., Caxias do Sul/Brazil

AktE Aktenzeichen OLG (File number of OLG)

AktG Aktiengesetz (German stock corporation act)

AMI International, 2010 "20-Year global naval market forecast: number of ships", Bob Nugent, AMI

International, July 2010

AMI International, 2011 "Changing threats, changing markets – A consideration of the naval future",

AMI International, 2011

Analyse & Prognose Analyse & Prognose GmbH, Wilhelmsfeld

Analyse & Prognose, 2012 "European bus survey report", Analyse & Prognose, August 2012

AO Abgabenordnung (General Tax Code)

Ashok Leyland Ashok Leyland Limited, Chennai/India

BaFin Bundesanstalt für Finanzdienstleistungsaufsicht (Federal Financial Supervi-

sory Authority)

BCG, 2012 "Winning the BRIC truck battle", The Boston Consulting Group, February

2012

BGAV Beherrschungs- und Gewinnabführungsvertrag (domination and profit and

loss transfer agreement)

BGH Bundesgerichtshof (Federal High Court)

bn. billion

BP, 2012 "BP statistical review of world energy 2012", BP p.l.c, London/United King-

dom, June 2012

BRIC Brazil, Russia, India, China

BS Balance sheet

Btu British thermal unit (unit of measurement for energy)

BVerfG Bundesverfassungsgericht (Federal Constitutional Court of Germany)

BvR Aktenzeichen für Verfassungsbeschwerden (File number of an appeal to the

Federal Constitutional Court on a constitutional issue)

CAGR Compound annual growth rate

CAPM Capital asset pricing model

Caterpillar Caterpillar Inc., Peoria/USA

KPMG PwC

7

Xx

CDAX Performance Index Composite DAX

CIQ S&P Capital IQ Inc., a business of the McGraw-Hill Companies, New York

City/USA

CLA Cargo Line A

Clarkson, 2012 "Offshore forecast club report, Spring 2012", Clarkson Research Services

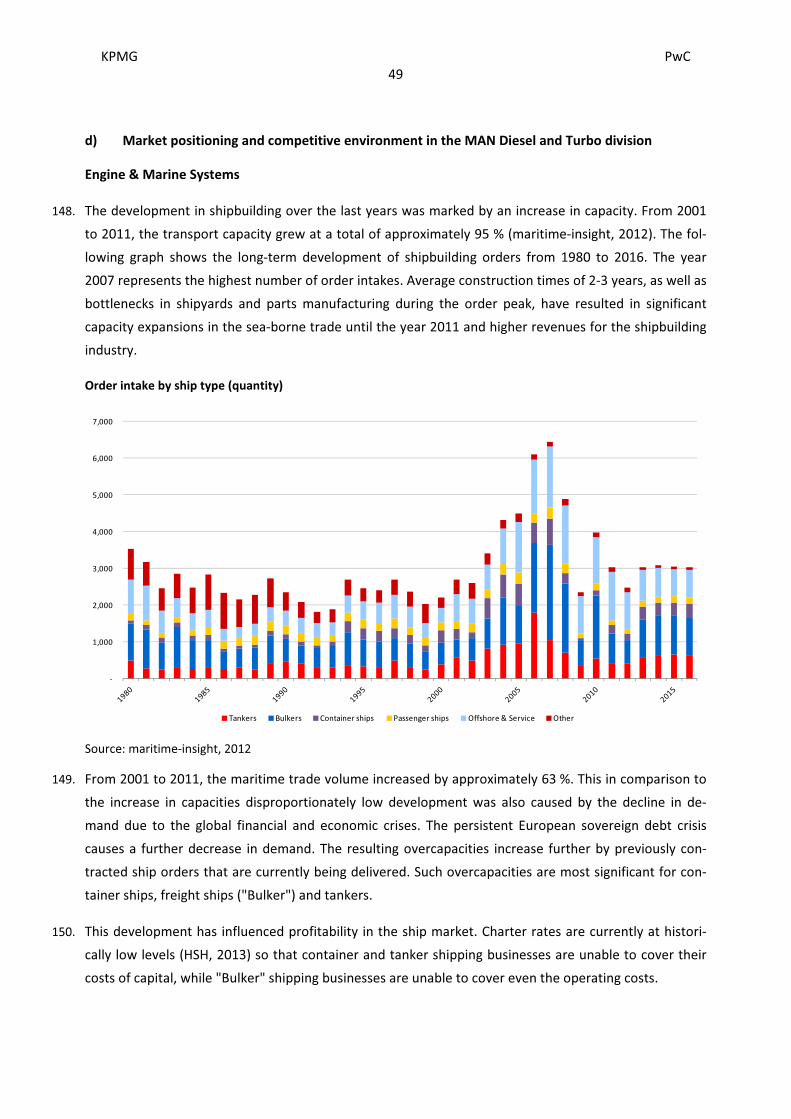

Limited, London/United Kingdom, 2012

CNHDTC China National Heavy Duty Truck Group Company Limited, Jinan/China

Co. Company

Corporate Center Central area consisting of the group holding MAN SE and other companies

Daimler Daimler AG, Stuttgart

DAF DAF Trucks N.V., Eindhoven/Netherlands, a brand of PACCAR

DAX Deutscher Aktienindex (German Stock Index)

DCF Discounted cash flow

Defenceweb.co.za, 2012 "Armoured vehicles MRO market grows while overall market shrinking",

www.defenceweb.co.za, 2012

dena, 2012 dena market analysis 2012: Status and outlook for the worldwide develop-

ment of renewable energies, Deutsche Energie-Agentur GmbH, Berlin, 2012

Deutsche Bank, 2012 "Cement outlook 2013", Deutsche Bank AG, Frankfurt am Main, December

2012

Deutsche Börse AG Deutsche Börse AG (German Stock Exchange), Frankfurt am Main

Dongfeng Dongfeng Motor Corporation, Wuhan/China

E Expected (estimation)

EBIT Earnings before interest and tax

EBITDA Earnings before interest, taxes, depreciation and amortisation

e.g. For example

Eicher Motors Eicher Motors Limited, Delhi/India

EIU Economist Intelligence Unit Limited, London/United Kingdom

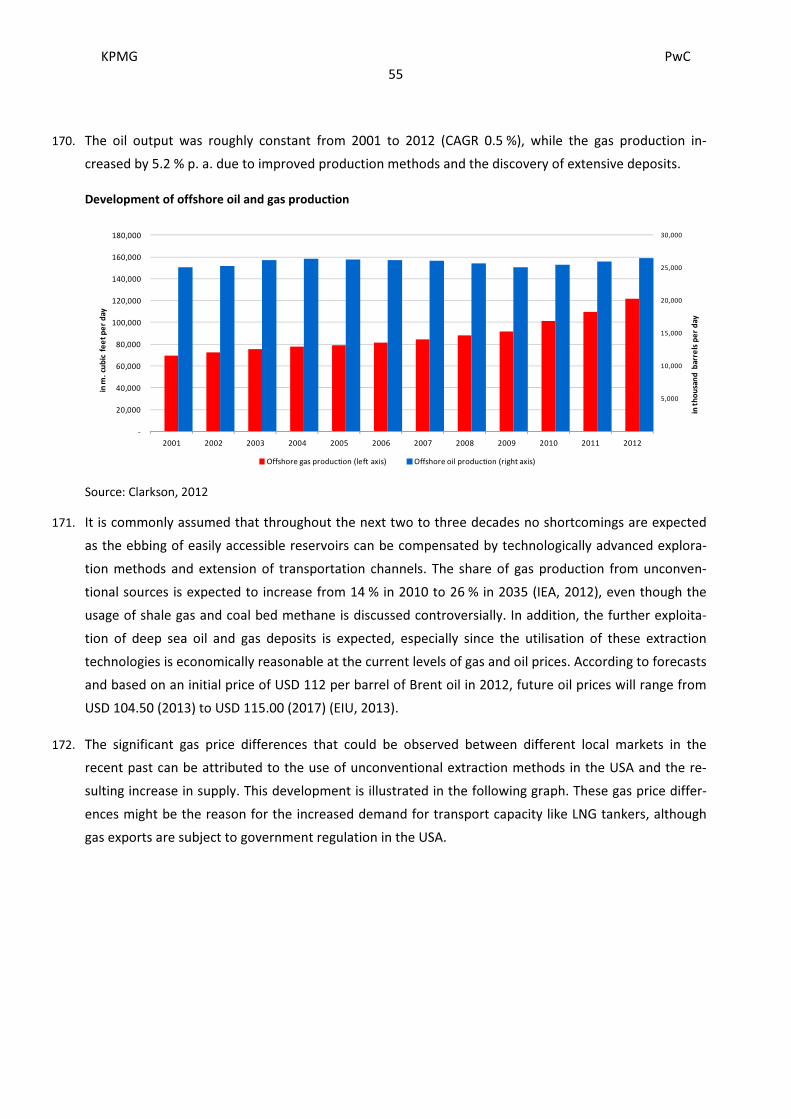

et. seq. and the following

EU European Union

EUGH Europäischer Gerichtshof (Court of Justice of the European Union)

EURO-Leasing EURO-Leasing GmbH, Sittensen

EV Enterprise value

e.V. Eingetragener Verein (incorporated association)

EvoBus EvoBus GmbH, Kirchheim unter Teck

Ferrostaal Ferrostaal Aktiengesellschaft, Essen

First Automotive Works First Automotive Works Co., Ltd., Changchun/China

KPMG PwC

8

Xx

FY Fiscal year(s)

GAZ OAO GAZ, Nizhny Novgorod/Russia

GE General Electric Company, Fairfield/USA

GDP Gross domestic product

GmbH Gesellschaft mit beschränkter Haftung (German company with limited liabi-

lity)

GVW Gross vehicle weight

GW Gigawatt

HGB Handelsgesetzbuch (German commercial code)

HHI Hyundai Heavy Industries Co., Ltd., Ulsan/South Korea

hp Horsepower

HR B Handelsregister Abteilung B (trade register section B)

HSH, 2013 "Shipping quarterly 1-2013", HSH Nordbank, February 2013

Hyundai Hyundai Motor Company, Seoul/South Korea

IAS International accounting standard

IDC, 2011 Statement by IDC Research, Framingham/USA, 2011

IDW Institut der Wirtschaftsprüfer in Deutschland e.V. (Institute of Public Audi-

tors in Germany, Incorporated Association), Dusseldorf

IDW S 1 IDW Standard: Grundsätze zur Durchführung von Unternehmensbewertun-

gen (Principles for the performance of business valuations), as at

2 April 2008

i.e. Id est

IEA International Energy Agency, Paris/France

IEA, 2012 IEA – World Energy Outlook 2012

IFRS International Financial Reporting Standard

IHS, 2012 ”Automotive Medium and Heavy Commercial Vehicle Industry Forecast”,

IHS Global Insight, 2012

Inc. Incorporated

IPIC International Petroleum Investment Company, Abu Dhabi/UAE

ISIN International Security Identification Number

Isuzu Motors Isuzu Motors Ltd., Tokyo/Japan

IT Information Technology

Iveco Iveco S.p.A., Turin/Italy ("Iveco")

KAMAZ OAO KAMAZ, Kazan/Russia

KPMG KPMG AG Wirtschaftsprüfungsgesellschaft, Berlin

KPMG, 2011 "Competing in the global truck industry", KPMG, September 2011

KPMG PwC

9

Xx

kW Kilowatt

LMC Automotive Information service provider in the automobile sector, division of LMC In-

ternational Ltd, Oxford/United Kingdom

LMC, 2012 LMC Automotive, Q4 2012

LNG Liquefied natural gas

Ltd. Limited

Ltda. Sociedade Limitada (limited company in Brazil and Portugal)

Mahindra Mahindra & Mahindra Ltd., Mumbai/India

MAN FORCE TRUCKS MAN FORCE TRUCKS Private Limited, Akurdi/India

MAN Group Consolidated MAN SE and its direct and indirect affiliates

MAN SE MAN SE, Munich

MAN Trucks India MAN Trucks India Private Limited, Akurdi/India ("MAN Trucks India")

Management Engineers &

AutoValue, 2010

"How to Move in Moving Markets? The Global Perspective of the Truck

Industry", Management Engineers and AutoValue, 2010

manroland manroland AG, Offenbach

maritime-insight,

2012

"maritime-insight Shipbuilding Outlook Club, October 2012", mari-

time-insight, Västra Frölunda/Sweden

MarketLine, 2012 "Global cement", MarketLine (a division of Datamonitor Ltd, Lon-

don/UK), October 2012

M toe million tonnes of oil equivalent (energy unit measure)

MAZ OAO MAZ, Minsk/Belarus

mbH Mit beschränkter Haftung (with limited liability)

MDT MAN Diesel & Turbo division

MDT SE MAN Diesel & Turbo SE, Augsburg

Mercosur Mercado Común del Sur (joint domestic market in South America)

MFI MAN Finance division

MFI GmbH MAN Finance International GmbH, Munich

Mitsubishi Mitsubishi Motor Corporation, Tokyo/Japan

ML MAN Latin America division

Moody’s Moody’s Investors Service, New York/USA

MPC MPC Industries GmbH, Hamburg

MTB MAN Truck & Bus division

MTB AG MAN Truck & Bus AG, Munich

MW Megawatt

KPMG PwC

10

Xx

Navistar Navistar International Corporation, Warrenville/USA

NAFTA North American Free Trade Agreement

No. Number

N.V. Naamloze Vennootschap (public limited liability company in the Nether-

lands)

OAO Otkrytoje Akzionernoje Obschtschestwo (russian public company)

OECD Organisation for Economic Co-operation and Development

OLG Oberlandesgericht (Higher Regional Court)

OPV Offshore patrol vessel

p.a. per annum

PACCAR PACCAR Inc., Bellevue/US

P&L Profit and loss statement

P/E Price-earnings ratio

PPA Purchase price allocation

PR61 Planning round 61

PROCONVE Programa de Controle da Poluição do Ar por Veículos Automotores

(emission standard in Brazil)

PwC PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsge-

sellschaft, Frankfurt am Main

R&D Research and development

Region West B.V. MAN Region west B.V., Vianen/The Netherlands

Renault Trucks Renault Trucks SAS, Saint-Priest/France

Renk Renk division

Renk AG Renk Aktiengesellschaft, Augsburg

RFC Rolling forecast

RMMV Rheinmetall MAN Military Vehicles GmbH, Munich

ROS Return on Sales

S. Page or clause

S.A. Société Anonyme (limited company in France, Luxembourg, Spain and Bel-

gium)

SAS Société par actions simplifiée (simplified public company in France)

SBU Strategic business unit

Scania Scania AB, Södertälje/Sweden

SE Societas Europaea

KPMG PwC

11

Xx

SG&A Selling, general & administrative

Siemens Siemens AG, Munich

Sinotruk Sinotruk (Hong Kong) Ltd., Hong Kong/China

SIPRI Stockholm International Peace Research Institute (www.sipri.org)

SKD Semi Knocked Down

S.p.A. Società per Azioni (public limited liability company in Italy)

S&P Standard & Poor's, a division of The McGraw-Hill Companies, Inc., New

York/USA

t ton(s)

Tata Motors Tata Motors Limited, Mumbai/India

TGA Trucknology generation A

Triade Western Europe, North America and Japan

Truck & Bus GmbH Truck & Bus GmbH, Wolfsburg

UAE United Arab Emirates

UPL Corporate planning

UralAZ OAO Ural AZ, Oblast Tscheljabinsk/Russia

USA United States of America

USD United States Dollar

VAT Value added tax

VCI, 2013 "Die deutsche chemische Industrie 2030 - VCI-Prognose-Studie", Verband

der chemischen Industrie e. V., January 2013

Volkswagen AG Volkswagen Aktiengesellschaft, Wolfsburg

Volvo Volvo AB, Gothenburg/Sweden

WKN Wertpapierkennummer (security identification number)

WpÜG Wertpapiererwerbs- und Übernahmegesetz (securities acquisition and ta-

keover act)

WTO World Trade Organization

XETRA Exchange Electronic Trading

KPMG PwC

12

Xx

A. Engagement and scope of work

1. The management board of Truck & Bus GmbH (formerly: Volkswagen Coaching Gesellschaft mbH),

Wolfsburg ("Truck & Bus GmbH") has appointed PricewaterhouseCoopers Aktiengesellschaft

Wirtschaftsprüfungsgesellschaft, Frankfurt am Main ("PwC"), with engagement letter dated 9 Janu-

ary 2013 and the executive board of MAN SE, Munich ("MAN SE") has appointed KPMG AG

Wirtschaftsprüfungsgesellschaft, Berlin ("KPMG"), (PwC and KPMG hereinafter together referred to as

"we") with engagement letter dated 18 January 2013 to prepare a joint expert opinion on the equity

value of MAN SE as well as on an appropriate recurring compensation payment and cash compensation

in accordance with §304 AktG, § 305 AktG ("joint expert opinion").

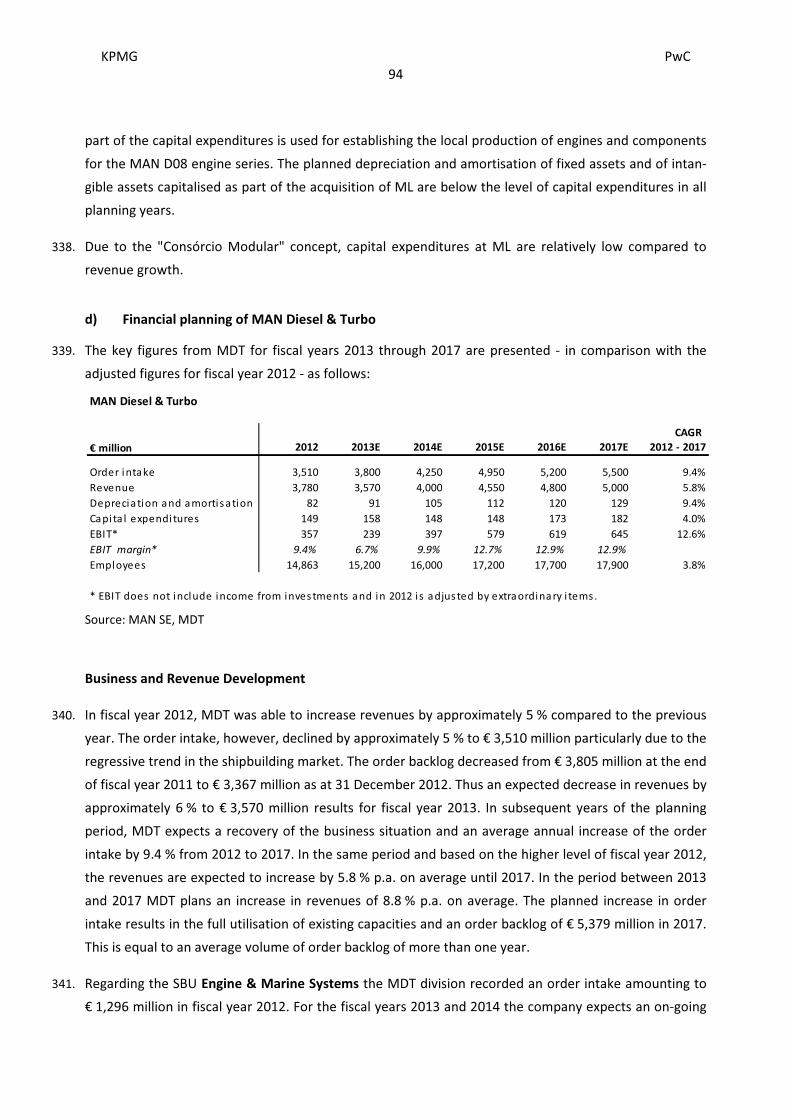

2. The reason for this valuation is the intended domination and profit and loss transfer agreement in

accordance with § 291.1 AktG between Truck & Bus GmbH, a 100 % direct affiliate of Volkswagen AG,

Wolfsburg ("Volkswagen AG") and MAN SE. The joint expert opinion on the equity value of MAN SE will

serve to determine the appropriate cash compensation pursuant to § 305 AktG as well as to determine

the appropriate recurring compensation payments pursuant to § 304 AktG for the outside shareholders

of MAN SE.

3. In accordance with § 293.1 AktG, the domination and profit and loss transfer agreement is subject to

approval by the general shareholders’ meeting of MAN SE. The valuation date is the date of the general

shareholders’ meeting of MAN SE at which the resolution is adopted and which has been scheduled for

6 June 2013.

4. We performed our valuation in accordance with the German valuation guideline established by the

Institute of Public Auditors in Germany, Incorporated Association (Institut der Wirtschaftsprüfer in

Deutschland e.V.): IDW S 1 ‘Principles for the Performance of Business Valuations’ as at 2 April 2008

(IDW S 1). In accordance with this standard, we acted as an independent expert and determined an ob-

jectified equity value.

5. The joint expert opinion has been prepared exclusively for internal use by Truck & Bus GmbH, Volks-

wagen AG and MAN SE for the purpose of the joint report on the domination and profit and loss transfer

agreement ("contract report") to be prepared by the parties to the agreement. Internal use also includes

written and verbal reports to shareholders of MAN SE as well as disclosure pursuant to § 293f.3 AktG

and the shareholder's option of inspection of the joint expert opinion in connection with the general

shareholders’ meeting of MAN SE. The management board of Truck & Bus GmbH and the executive

board of MAN SE may attach this expert opinion to their contract report according to § 293a AktG. Fur-

thermore, the joint expert opinion can be used in connection with a possible subsequent legal proce-

dure as well as the reference required by the court appointed auditor within the scope of the verifica-

tion of appropriateness of the compensation and recurring compensation payments according to

KPMG PwC

13

Xx

§ 293b.1 AktG. The joint expert opinion may not be published, duplicated or used for any purpose other

than those mentioned above. Without our prior written consent, this may not be forwarded to third

parties for any purposes other than those mentioned above. Consent will not be denied for undue rea-

sons.

6. This valuation and our responsibilities, including responsibilities towards third parties, are governed by

the "General Engagement Terms" as at 1 January 2002, which are attached to this joint expert opinion.

7. We conducted our work from January 2013 to April 2013 in the business premises of MAN SE as well as

individual affiliates of MAN SE in Munich and Augsburg, of Volkswagen AG in Wolfsburg and in the of-

fices of PwC and KPMG at various locations. Our valuation is primarily based on the following documents

made available to us:

• Audited consolidated financial statements of MAN SE as well as of Renk Aktiengesellschaft, Augs-

burg ("Renk AG") in accordance with International Financial Reporting Standards ("IFRS") for the fi-

nancial years 2010 to 2012, each issued with an unqualified audit opinion by PwC,

• Audited consolidated financials of the subgroups Truck & Bus AG, Munich ("MTB AG"), MAN Diesel

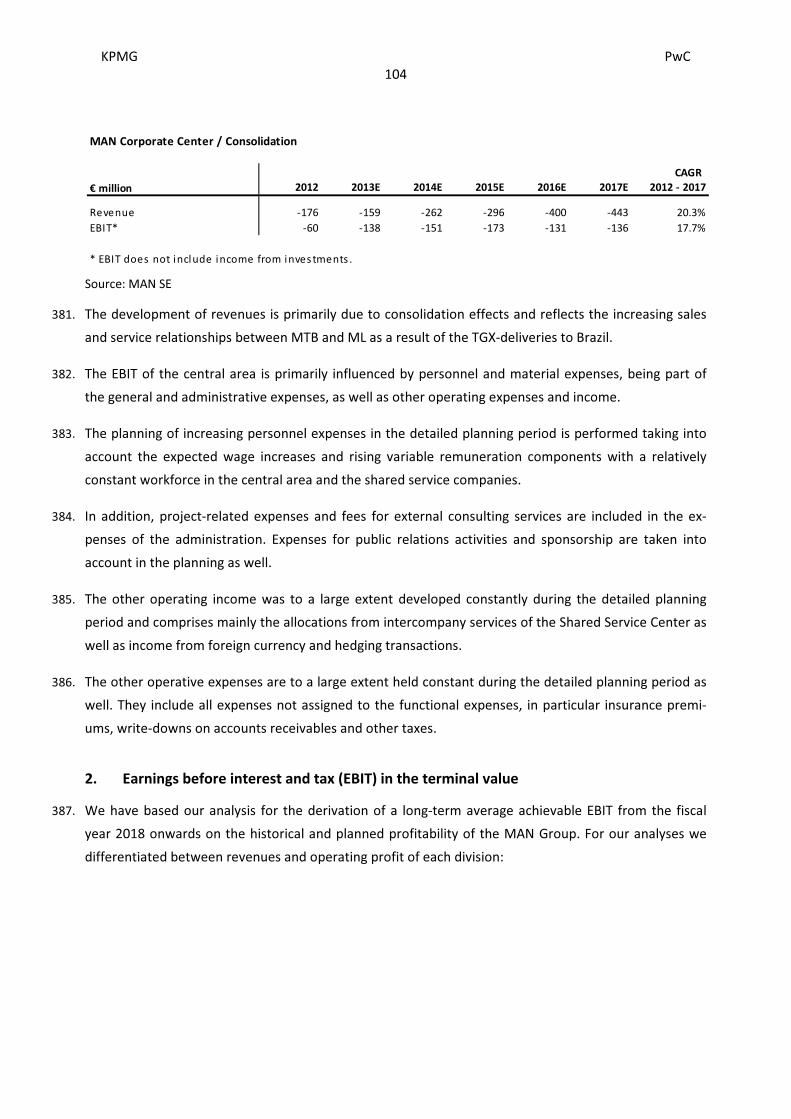

& Turbo SE, Augsburg ("MDT SE"), MAN Finance International GmbH, Munich ("MFI GmbH") in ac-

cordance with IFRS for the financial years 2010 to 2012, each issued with an unqualified audit opin-

ion by PwC,

• Audited annual financial statements of MAN SE, MTB AG, MDT SE, Renk AG and MFI GmbH in accor-

dance with German GAAP for the financial years 2010 to 2012, each issued with an unqualified audit

opinion by PwC,

• Consolidated financial planning figures of MAN SE comprising profit and loss statements, balance

sheets as well as cash flow statements including relevant explanations, for the years 2013 to 2017,

• Financial planning for the divisions MAN Truck & Bus ("MTB"), MAN Finance ("MFI"), MAN Latin

America ("ML"), MAN Diesel & Turbo ("MDT"), Renk as well as the Corporate Center,

• Documents and information relating to the mandatory offer of Volkswagen AG to all external share-

holders of MAN SE for the acquisition of their shares pursuant to § 35.2 WpÜG as at 31 May 2011,

• Articles of Association and excerpts from the Commercial Register of MAN SE and of important af-

filiates in the respective latest versions,

• Final draft of the domination and profit and loss transfer agreement between Truck & Bus GmbH

and MAN SE in the version dated 18 April 2013 ("draft of the domination and profit and loss transfer

agreement") as well as preliminary drafts,

• Final draft of the Letter of Affiliation and Comfort of Volkswagen AG to MAN SE dated 18 April 2013,

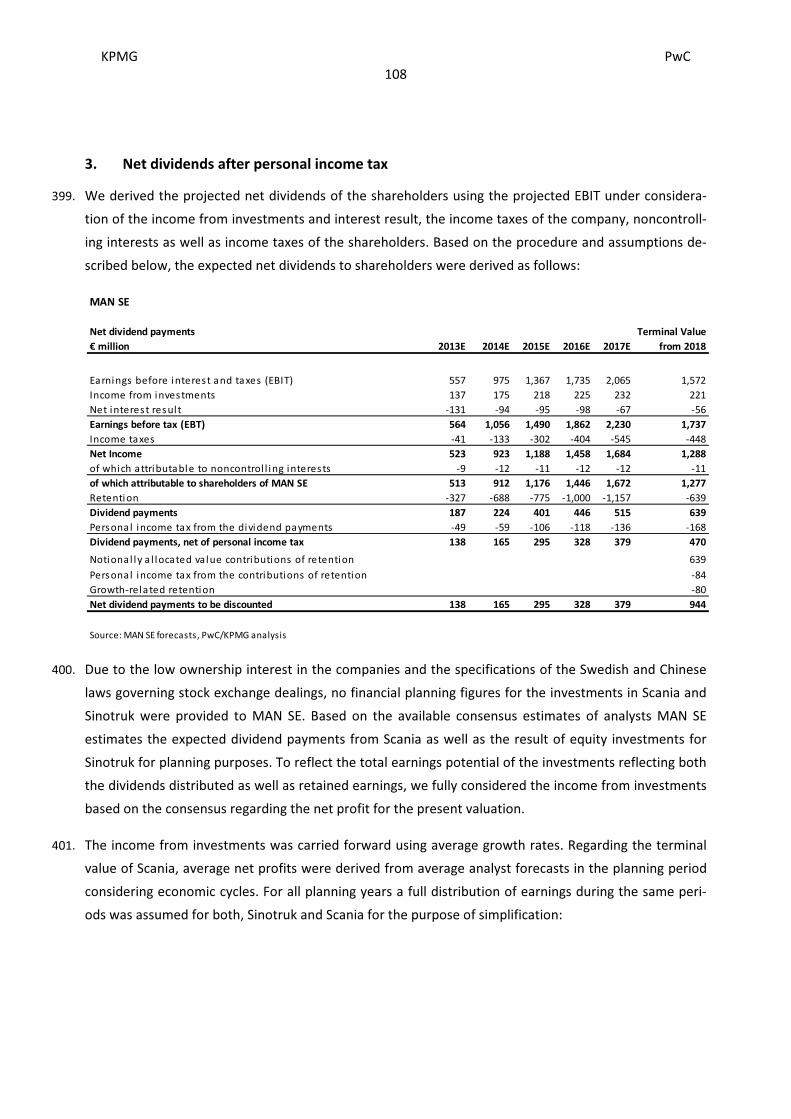

• Final draft of the contract report in the version dated 18 April 2013 as well as preliminary drafts,

• Other documents and information relevant for the valuation.

KPMG PwC

14

Xx

8. Further information was provided to us by the executive board of MAN SE and managers and employees

named by the board (together "management of MAN SE" or "management"). The executive board of

MAN SE, the executive board of Volkswagen AG and the management board of Truck & Bus GmbH have

provided us with a written statement to the effect that all material information and explanations given

to us in connection with the preparation of our joint expert opinion are both complete and correct.

9. Our valuation is based on the documents provided for the purpose of this valuation. We have assessed

these critically, but have not verified them with reference to an annual audit. We have verified the plau-

sibility of the financial planning figures based on the historical financial development, the current legal

and economic conditions as well as through market studies, analyst reports and industry reports and

have discussed the same with the management of MAN SE. We have not conducted individual audits

with reference to §§ 316 et. seq. HGB. These were not part of our engagement.

10. Please note that the calculations specified in this report have been rounded. Since the calculations were

in fact made with exact values, addition or subtraction of table values may lead to subtotals and totals

that deviate from those presented in these tables.

11. In the context of the valuation, no particular difficulties as defined in § 293e.1, sentence 2, no.3 AktG

have occurred.

KPMG PwC

15

Xx

B. Principles and methods of valuation

I. Basics of the valuation

12. The principles and valuation procedures described below embody standards which are generally ac-

cepted in current business valuation theory and practice and are recognised in jurisdiction.

13. According to IDW S 1 as amended in 2008, the value of a business is determined by the future benefits

the business will generate on the basis of the key success factors inherent to the business at the time of

valuation. The key success factors comprise factors such as the products, market position, organisation,

management, employees as well as the innovative capacity of the business. Assumed that merely finan-

cial objectives are pursued, the value of a business is determined by the capacity of the business to gen-

erate financial surpluses for the shareholders through the combination of all factors which influence the

earnings potential.

14. The value of a business may be determined by either the dividend discount method or the discounted

cash flow method ("DCF"). Both methods are basically equivalent since they share the same theoretical

basis (capitalisation of future benefits) and, when using the same financing assumptions, lead to identi-

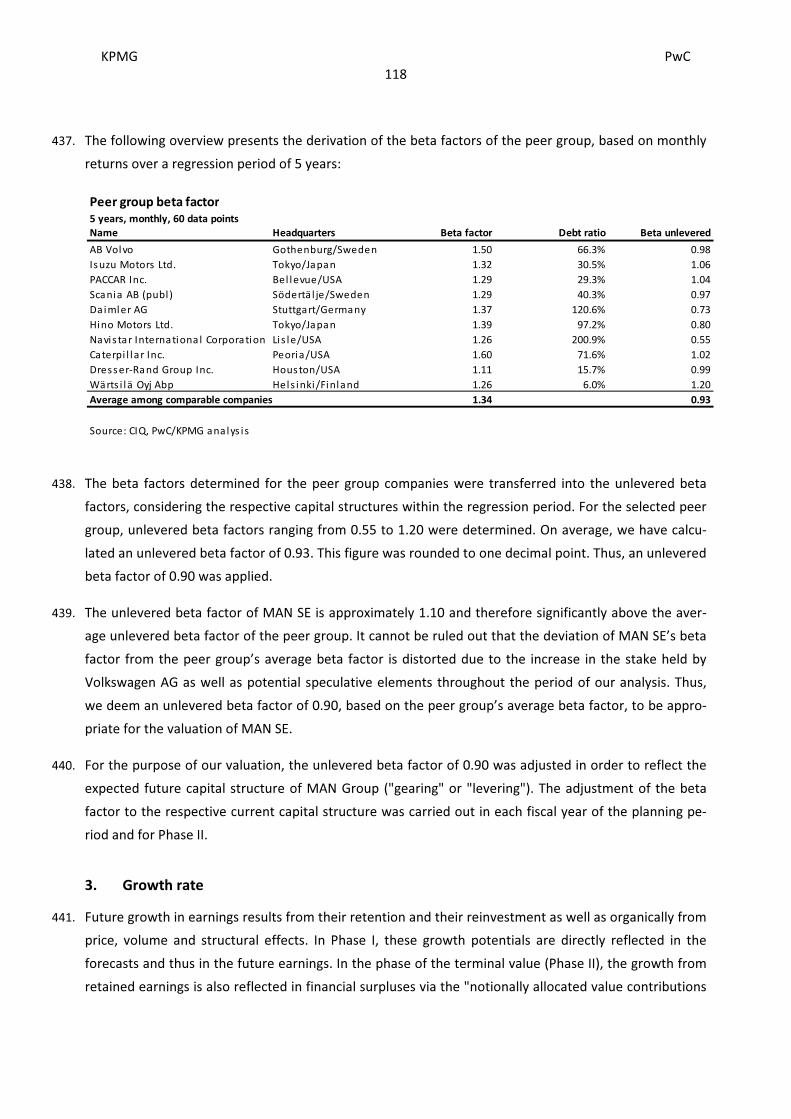

cal results. In our joint expert opinion, the dividend discount method was applied.

15. Both methods first determine the present value of the financial surpluses generated by the assets es-

sential for the business (operating assets). Assets (including liabilities) that could be separated from the

business and sold without affecting the actual purpose of the business are classified as non-operating

assets and valued separately. Therefore, the value of a business generally equals the sum of the present

values of financial surpluses that can be derived from the operating and non-operating assets.

16. According to the dividend discount method, the equity value is derived directly from the net income to

shareholders. The discounted net income to the company owners subject to the derivation of the equity

value results mainly from the financial surpluses generated by the company. Financial planning figures

are generally prepared based on historical profitability. In the context of a valuation, only those financial

surpluses should be considered that result from specific measures that have already been initiated, or

that originate from a sufficiently documented and substantiated business concept as at the valuation

date.

17. The principles of the IDW S 1 as amended in 2008 distinguish between real and pseudo synergy effects.

Real synergy effects are surpluses that can only be materialised through the domination and profit and

loss transfer agreement between Truck & Bus GmbH and MAN SE. Pseudo synergy effects can be im-

plemented without the execution of this measure. Real synergies would thus include measures, which

would not be executable without concluding the domination and profit and loss transfer agreement. On

KPMG PwC

16

Xx

the other hand, pseudo synergy effects include the synergies expected from measures that can be exe-

cuted even without the contract between the companies. These pseudo synergy effects should be con-

sidered in the valuation if they are allotted to the valuation object.

18. In determining the value of a business, it is generally assumed that all available financial surpluses

resulting from a documented business concept as at the valuation date will be distributed, subject to

any applicable legal restrictions. Retained earnings as well as their use must be taken into account when

determining the net earnings to shareholders.

19. In order to value a business, the projected future financial surpluses need to be discounted to the valua-

tion date using an appropriate interest rate (discount rate). The discount rate serves to measure the

series of expected financial surpluses against an alternative investment different to the investment in

MAN SE shares.

20. Due to the relevance of personal income taxes to the business value, it is necessary to characterise the

tax situation of shareholders in the framework of objectified business valuations. In case of legally and

contractually motivated valuations within the meaning of IDW S 1 as amended in 2008, the standardisa-

tion is based, in accordance with long-standing legal practice and valuation experience, on the tax situa-

tion of a domestic taxpayer, subject to full taxation ("direct standardisation"). To this end, appropriate

assumptions regarding the personal tax charge on net earnings generated by the company to be valued

and the alternative investment must be made.

21. If it is beneficial to sell the operating and non-operating assets rather than continue the business opera-

tions, the valuation must be based on the liquidation value of the business as well unless this is not pos-

sible on account of legal or factual limitations. This applies at least, if the company has no operating

business and consists only of non-operating assets and liabilities (OLG Düsseldorf 4 October 2006- I-26

W7/06 AktE). This condition does not apply to MAN SE. However, in order to verify whether the liquida-

tion value exceeds the equity value, the liquidation value of MAN SE was roughly determined as at the

valuation date and compared with the equity value determined by us according to the dividend discount

method.

22. The net asset value resulting from an asset-based approach has no independent informative value as

part of a business valuation. The net asset value is the reconstruction cost or replacement value of all

existing intangible and tangible assets (and liabilities) present in the business. Since the market value of

equity of a business as a going concern is determined on the basis of its future earnings potential and

since the net asset value is neither based on future projections nor represents an enterprise value, the

latter was not determined.

23. Since the shares of MAN SE have been admitted to various stock exchanges for trading, it would be

possible to determine the cash compensation using observable share prices of MAN SE. However, there

KPMG PwC

17

Xx

can be strong arguments opposing a cash compensation derived exclusively from the share price, since

share prices depend on numerous special factors such as the size and constriction of the market, on

random trading turnovers as well as on speculative influences and influences that are not related to the

value and can thus be subject to unpredictable variations and developments.

24. The application of share prices (market capitalisation) cannot replace a business valuation according to

the described principles if this valuation uses a more detailed base compared to information available to

the capital market and integrates the capital market considerations into the valuation methodology. The

valuation described in this joint expert opinion is based on an analysis of historical data and on long-

term corporate planning, which is not publicly accessible in this level of detail and scope.

25. The Federal Constitutional Court (Bundesverfassungsgericht or "BVerfG") and the Federal Court of

Justice (Bundesgerichtshof or "BGH") have ruled in multiple cases that the share price should be gener-

ally considered as minimum value when determining a cash compensation for outside shareholders in

connection with some special purpose business valuations (e.g. recurring compensation payment and

compensation in accordance with §§ 304, 305 AktG) (compare e.g. BVerfG, decision dated 27 April 1999,

1 BvR 1613/94, BGH, decision dated 12 March 2001, II ZB 15/00; BGH, decision dated 19 July 2010, II ZB

18/09). However according to the Federal Constitutional Court, the requirement to determine the ap-

propriate compensation based on the share price does not mean that it should always be the only deci-

sive factor. Exceeding the share price is acceptable under constitutional law.

26. Refer to section F.I for the development and relevance of the share prices of MAN SE.

KPMG PwC

18

Xx

II. Appropriate cash compensation according to § 305 AktG

27. A domination and profit and loss transfer agreement must amongst others include the obligation of the

other party to the contract to - on demand of a outside shareholder - acquire the shares in return for an

appropriate cash compensation defined in the agreement (§ 305.1 AktG). In the present case, the draft

of the domination and profit and loss transfer agreement proposes a cash compensation (§ 305.2 no.

3 AktG).

28. According to the knowledge of financial studies, jurisdiction (compare BVerfG decision dated 27 April

1999 – 1 BvR 1613/94; DB 1999, page 1695) and the valuation practice, the equity value is the correct

basis for determining the compensation as per § 305 AktG. Thus, the value of a company as a whole

needs to be considered. This will therefore correspond to the postulate of compensation at full value of

shares developed by the jurisdiction. Therefore, the equity value of MAN SE has to be determined in-

cluding all affiliated companies and the compensation per share has to be derived from this value.

III. Appropriate recurring compensation payment according to § 304 AktG

29. According to § 304.1 sentence 1 AktG, a domination and profit and loss transfer agreement must ar-

range for an appropriate recurring compensation payment for the outside shareholders with a recurring

payment (compensation payment) related to the shares in the share capital. According to § 304.2 sen-

tence 1 AktG, at least the annual payment per share, which could probably be distributed as an average

profit per share according to the previous earnings situation of the company and its future earnings

prospects under consideration of appropriate depreciations and fair value adjustments, however with-

out a retention of other profits, should be assured as compensation payment. According to § 304.1 sen-

tence 2 AktG a domination agreement without profit and loss transfer must guarantee a reasonable

minimum compensation of the earnings of the dominated company to the outside shareholders.

30. The discounted dividend value based on the corporate financial planning figures considers - with regard

to interest effects - the expected payments (dividends and retention of earnings) between company and

shareholders. With respect to a normalised annual compensation payment, the legislative body does

not relate the payment obligation to the expected earnings that vary year by year, but refers to the av-

erage amount per share that could probably be distributed under consideration of appropriate depre-

ciations and fair value adjustments, however without retention of other earnings. The determination of

an average amount per share should thus consider the volatility of profits or losses, but be converted

into a uniform average amount per share.

KPMG PwC

19

Xx

C. Description of the valuation object

I. Legal and tax situation

31. MAN SE was founded through a change in legal form from MAN Aktiengesellschaft to a Societas Eu-

ropaea ("SE") and has been registered in the Commercial Register at the district court of Munich since

2009 under HR B 179426 and under the name MAN SE with its headquarters in Munich. The latest entry

in the Commercial Register is dated 14 March 2013.

32. The fiscal year corresponds to the calendar year.

33. Purpose of the company according to § 2 of the Articles of Association in the version dated 1 April 2010

is

• the investment in companies of all kinds, in particular companies engaging in mechanical engi-

neering, plant engineering, vehicle manufacturing and engine production as well as trade,

• manufacturing of such products as well as the processing of materials of all kinds.

The company is authorised to conduct all business and take all measures deemed necessary or useful for

attaining the company's objectives.

34. The registered share capital of MAN SE as at the date of this joint expert opinion is € 376,422,400. It is

composed of 147,040,000 no-par value bearer shares, which are subdivided into

140,974,350 common shares and

6,065,650 non-voting preferred shares.

According to § 4.2 sentence 2 of the Articles of Association of MAN SE, shareholders may not claim de-

livery of physical share certificates.

35. In accordance with § 17.1 of the company’s Articles of Association, every common share grants one vote

in the general shareholders’ meeting. The general shareholders’ meeting especially decides on the

shareholder representatives of the supervisory board, the appropriation of net profits, on the formal

discharge of the executive board and the supervisory board as well as on the appointment of the exter-

nal auditor.

36. Holders of preferred shares do not have voting rights at the general shareholders’ meeting, except for

cases prescribed by law. However, according to § 24.3 of the Articles of Association of MAN SE, holders

of preferred shares are entitled to a preferred dividend of € 0.11 per preferred share. This preferred

dividend of € 0.11 is payable in advance but is not an additional dividend.

KPMG PwC

20

Xx

37. The executive board is authorised to increase the share capital, with the consent of the supervisory

board, by up to € 188,211,200 by issuing common bearer shares on one or more occasions against cash

contributions and/or noncash contributions in the period up to 31 March 2015.

38. Moreover, the general shareholders’ meeting on 1 April 2010, resolved to contingently increase the

share capital by up to € 76,800,000. The contingent capital increase will only be implemented to the

extent that the holders of convertible bonds or bonds with warrants or with conversion obligations is-

sued for cash consideration by MAN SE or its Group companies by virtue of the authorising resolution of

the general shareholders’ meeting on 1 April 2010, exercise their conversion rights or options or settle

their conversion obligations, and provided that other forms of settlement are not used. We have been

informed that no convertible bonds or bonds with warrants or with conversion obligations have been

issued up to the end of our valuation work.

39. The common and preferred shares of MAN SE are traded on the German electronic stock exchange

trading platform Xetra, as well as on all seven German stock exchanges (Berlin, Düsseldorf, Frankfurt am

Main, Hamburg, Hanover, Munich and Stuttgart).

40. The common shares have been assigned the German security identification number ("WKN") 593700 as

well as the international security identification number ("ISIN") DE0005937007. The preferred shares of

the company have been assigned the German WKN 593703 and the ISIN DE0005937031.

41. Until 24 September 2012, the common shares of the company were listed in the German stock index

"DAX" of Deutsche Börse AG, Frankfurt am Main ("Deutsche Börse AG"). Deutsche Börse AG decided on

a change in composition of the DAX as part of its annual review in September 2012. Due to the low free

float of the common shares of MAN SE, the common shares of the company no longer fulfilled the crite-

rion of Deutsche Börse AG to be retained in the DAX. Accordingly, the common shares of MAN SE were

transferred to the Mid-Cap-DAX ("MDAX"), effective 24 September 2012. The common shares of MAN

SE are listed in further stock exchange indices, including HDAX, CDAX, Euro Stoxx®, Stoxx® Europe 600

and Euro Stoxx® TMI Industrial. The preferred shares of MAN SE are listed in the CDAX.

42. On 3 October 2006, Volkswagen AG announced its acquisition of a 15.06 % share in MAN SE. On

26 February 2007, Volkswagen AG increased its voting rights to 29.9 %. With the acquisition of further

shares in MAN SE, Volkswagen AG exceeded the threshold of 30 % of the voting rights on 9 May 2011

and was, according to the German Takeover Act, obligated to submit a mandatory offer to all external

shareholders of MAN SE to acquire the remaining shares. The takeover price fixed within the scope of

the mandatory offer was € 95.00 per common share of MAN SE and € 59.90 per preferred share. By the

end of the acceptance period, 29 June 2011, the offer for 35,857,607 common shares and 164,613 pre-

ferred shares was accepted. After the approval from all necessary regulatory authorities was granted,

the transaction was completed on 9 November 2011 and the share of Volkswagen AG increased to a

total of 55.90 % of the voting rights and 53.71 % of the share capital in MAN SE.

KPMG PwC

21

Xx

43. The takeover price fixed within the scope of the mandatory offer is not relevant with respect to the

determination of the recurring compensation payment and cash compensation in connection with the

domination and profit and loss transfer agreement. First, the consideration of prior takeover prices with

respect to the determination of the recurring compensation payment and cash compensation is not

envisaged by law. Second, overall economic as well as company-specific conditions have changed signifi-

cantly after the mandatory offer was submitted. Earnings before interest and taxes decreased from

€ 1,256 million in 2011 - the financial year which ended shortly after the completion of the mandatory

offer - by 50.4 % to € 623 million (compare note 238). In addition, as at the time the statement on the

mandatory offer was prepared by the executive and supervisory board, financial planning figures for

2012 were significantly higher than the actual earnings before interest and taxes in 2012. Moreover, at

that time a more positive economic outlook, as indicated for example based on the GDP of MAN’s cen-

tral markets, was generally anticipated. Consequently expectations for the fiscal year 2013 and the years

to follow were more optimistic as compared to the present valuation of the company. This is reflected in

the low price of MAN common shares prior to the announcement of the planned domination and profit

and loss transfer agreement.

44. Volkswagen AG increased its share in MAN SE through further acquisitions and exceeded the threshold

of 75 % of the voting rights in MAN SE with a voting interest of 75.03 % and an interest in the share capi-

tal of MAN SE of 73.41 % on 6 June 2012.

45. On 9 January 2013, Volkswagen AG informed MAN SE about the intention to conclude a domination and

profit and loss transfer agreement with MAN SE as a dominated company, in order to establish an inte-

grated commercial vehicle group. At that date, Volkswagen AG held 105,769,788 common shares and

2,626,244 preferred shares in MAN SE at that time, which corresponds to 75.03 % of the voting rights,

and 73.72 % of the share capital of MAN SE.

46. MAN SE is an indirect affiliate of Volkswagen AG and is fully consolidated in the group financial state-

ments of Volkswagen AG since 9 November 2011.

47. Based on the approval by the general shareholders’ meeting of Truck & Bus GmbH on 16 April 2013, all

shares of MAN SE held by Volkswagen AG, consisting of 105,769,788 common shares and 2,626,244

preferred shares, were contributed to the capital reserve of Truck & Bus GmbH. In addition, according to

§ 272.2 no.4 HGB, a cash contribution amounting to € 3.25 billion will be paid into the capital reserve of

Truck & Bus GmbH on 25 April 2013. Volkswagen AG is the sole shareholder of Truck & Bus GmbH with a

nominal share capital of € 10 million.

48. The shareholder structure of MAN SE for common and preferred shares as at the date of this joint

expert opinion is as follows:

KPMG PwC

22

Xx

Shareholders of MAN SE Number of common

shares

in %

of common shares

Truck & Bus GmbH 105,769,788 75.03

Free float 35,204,562 24.97

Total 140,974,350 100.00

Shareholders of MAN SE Number of preferred

shares

in %

of preferred shares

Truck & Bus GmbH 2,626,244 43.30

Free float 3,439,406 56.70

Total 6,065,650 100.00

Source: Volkswagen AG

49. The organisational structure of the company as well as the capital shares in major individual companies

on the valuation date, which are in some cases held indirectly by MAN SE, are as shown below:

Source: MAN SE

50. On 31 December 2012, the consolidation group included 135 affiliated companies and MAN SE. Fur-

thermore 9 investments were recognised applying the equity method, 11 investments are recognised at

MAN SE

Munich

Renk AG

Augsburg

MAN Diesel & Turbo

SE

Augsburg

MAN Truck & Bus AG

Munich

MAN Latin America

Indústria e Comércio

de Veículos Ltda.

Sao Paulo/Brazil

Sinotruk Ltd.

Hong Kong/China

Scania AB

Södertälje/

Sweden

100.00% 100.00%100.00% 76.00%

MAN Finance

International GmbH

Munich

100.00%

13.35%

(17.37% of the voting rights)25.00% + 1 share

KPMG PwC

23

Xx

amortised cost, and additional 60 investments were not included in the consolidated financial state-

ments (MAN Group).

Tax situation

51. Based on domination and profit and loss transfer agreements, a fiscal unity for corporate and trade tax

purposes exists between MAN SE and the following MAN Group companies in Germany:

• MAN Truck & Bus AG, Munich,

• MAN Diesel & Turbo SE, Augsburg,

• MAN Ferrostaal Beteiligungs GmbH, Munich,

• MAN GHH Immobilien GmbH, Oberhausen,

• MAN Grundstücksgesellschaft mbH, Oberhausen,

• MAN HR Services GmbH, Munich,

• MAN Finance International GmbH, Munich,

• MAN Versicherungsvermittlung GmbH, Munich,

• MAN IT Services GmbH, Munich,

• MAN Beteiligungs GmbH, Munich.

52. Due to further subsidiaries of these companies, with which domination and profit and loss transfer

agreements have been concluded, further indirect fiscal unities for income tax purposes exist between

MAN SE and companies of the MAN Group. There are also fiscal unities for value added tax ("VAT") pur-

poses between MAN SE and these as well as other companies.

53. According to management information, MAN SE's corporate income tax loss carryforwards amounted to

approximately € 639 million and the trade tax loss carryforwards amounted to approxi-

mately € 521 million as at 31 December 2012. Moreover, several domestic and international affiliates of

MAN SE had corporate income tax loss carryforwards amounting to a total of € 633 million, of which

approximately € 334 million are usable. Non-usable loss carryforwards relate to companies in countries

where loss carryforwards may only be utilised for a limited time period and to companies with insuffi-

cient earnings prospects for the utilisation of loss carryforwards.

54. As at 31 December 2012, the corporate tax credit of MAN SE amounted to approximately € 7.76 million.

KPMG PwC

24

Xx

55. The tax assessment of MAN SE, including 2008, has been closed and is subject to subsequent audit as

per § 164.1 AO. Tax returns for subsequent financial years are currently being prepared.

56. An external tax audit for the assessment periods 2002 to 2005 has largely been completed and covered

the audit fields of corporate income tax, trade tax and VAT. The respective tax assessment notices is-

sued in 2012 are subject to subsequent audit. The external tax audit for the financial years 2006 to 2010

for corporate tax, trade tax and VAT had already started in 2012 and was completed for smaller compa-

nies of the fiscal unity.

II. Economic fundamentals

1. Business activity

a) General information

57. The MAN Group is one of the leading players in commercial vehicles and mechanical engineering in

Europe. It mainly supplies trucks, buses, diesel engines, turbomachinery as well as special gear units.

58. The MAN Group focuses on the business areas Commercial Vehicles and Power Engineering.

59. With regard to the business area Commercial Vehicles, the MTB division is one of Europe’s leading

manufacturers of trucks and buses and the ML division represents the largest truck manufacturer in

Brazil. In addition, MAN SE holds an interest of 25 % plus one share in the capital of Sinotruk (Hong

Kong) Ltd., Hong Kong/China ("Sinotruk").

60. In the business area Power Engineering, the MDT division is a globally leading developer and manufac-

turer of large-bore diesel engines for use in ships and power plants and also specialises in the develop-

ment and production of turbo compressors, industrial turbines as well as chemical reactor systems. This

business area is supplemented with a majority holding in Renk, a global manufacturer of gear units, pro-

pulsion components and testing systems.

b) MAN Truck & Bus division

61. The core market of the MTB division, whose leading entity is MTB AG, is the European commercial

vehicle market. MTB also serves markets outside Europe, especially the Russian, Asia-Pacific and Arabian

as well as the African market. MTB has production facilities in four European countries as well as in

South Africa and India. Its products range from general-purpose trucks with a gross vehicle weight

("GVW") of 7.5 t to 44 t and special-purpose vehicles with a gross train weight of up to 250 t, through

buses and coaches, to diesel and gas engines for on- and off-road uses. Operations are supplemented

with an extensive range of services and the sale of used vehicles.

KPMG PwC

25

Xx

62. To support its commercial vehicle business MTB also offers financing solutions (loans and leases) as well

as supplementary services, particularly insurance solutions, through MFI. In addition, MFI’s subsidiary

Euro-Leasing GmbH, Sittensen ("EURO-Leasing") offers short- and long-term rental solutions for com-

mercial vehicles. The predominant function of MFI and its subsidiaries within the MTB division is how-

ever to promote sales of new vehicles. Due to the close linkage of MFI and MTB’s commercial vehicle

business MFI will be presented as part of the MTB division in the following.

63. MTB uses the brand MAN as a product brand in the truck as well as in the bus business. With the series

TGX and TGS (heavy trucks), TGM (medium trucks) and TGL (light trucks), MTB is a full range manufac-

turer producing trucks in a range from 7.5 t to 44 t and offering solutions for the national and interna-

tional heavy duty long-haul transport, the heavy-duty and building site traffic as well as the short-haul

and distribution transport. With the series Cargo Line A ("CLA"), MAN Trucks India Private Limited,

Akurdi/India ("MAN Trucks India") offers a truck for the Indian market as well as selected markets in

Africa and Asia. In the bus segment, MTB offers coaches (MAN Lion’s Coach), intercity buses (MAN Lion’s

Regio), city buses (MAN Lion’s City series) as well as chassis. Coaches are also sold using the premium

brand NEOPLAN.

64. The diesel and gas engines from MTB cover a range from 37 kW (50 hp) to 1,324 kW (1,800 hp) and are

offered as 4- and 6-cylinder in-line units and as 8- and 12-cylinder V engines. Besides the use in the

group’s own trucks and buses, the engines are also offered to third-parties, for power generation in

cogeneration plants and as drive units in agricultural machinery, rail vehicles, ships and boats and spe-

cial-purpose vehicles.

65. In the fiscal year 2012, MTB sold 74,680 trucks and 5,286 buses, achieving revenues of € 8,822 million.

This equals a sales decrease in volumes of 4.1 % compared to the previous year. Including subcontracted

employees, 34,879 employees were employed at the end of the financial year 2012.

c) MAN Latin America division

66. The ML division, whose leading entity is MAN Latin America Indústria e Comércio de Veículos Ltda., São

Paulo/Brazil, concentrates on the production and sale of commercial vehicles and buses (mainly bus

chassis) in Latin America and the southern part of Africa.

67. The product range covers trucks with a GVW of 5 t to 74 t, which are mainly marketed under the Volks-

wagen brand. ML offers the following Volkswagen branded truck series: "Delivery" from 5 t to 10 t,

"Worker" from 13 t to 31 t and "Constellation" from 13 t to 63 t. Moreover, the MAN branded TGX se-

ries was launched in the Brazilian market in 2012. In addition, the Volkswagen branded ADVANTECH

series sold in South America is equipped with MAN engines.

KPMG PwC

26

Xx

68. In 1993, ML launched its first bus chassis (model VW 16.180 CO) and has, since then, been active in the

bus market. ML offers in total eight different chassis for city and intercity buses.

69. All ML vehicles produced for the Brazilian market and delivered in March 2012 or later fulfil the Brazilian

standard PROCONVE P-7 (comparable to the Euro V standard).

70. The main production facility of ML is located in Resende/Brazil. Light trucks and buses are also manufac-

tured at the production facility in Querétaro/Mexico in SKD assembly.

71. ML has developed the concept "Consórcio Modular" for the facility in Resende, in which the actual

manufacturing of the vehicles is done by partner companies. ML employees are only involved in the

product development and quality assurance as well as for sales and customer service. "Consórcio Modu-

lar" is characterised by low capital employed and low investment requirements.

72. At the end of fiscal year 2012, ML employed a total of 1,937 employees, while approxi-

mately 3,800 employees worked in the "Consórcio Modular" production network.

73. In fiscal year 2012, ML sold 45,829 trucks and 10,476 buses, generating revenues of € 2,870 million. This

equals a sales decrease in volumes of 21.9 % compared to the previous year.

74. ML uses an extensive dealer network in Brazil and the other countries served. In Brazil, vehicle manufac-

turers can sell their products to end customers only through dealers. Overall, ML cooperates with ap-

proximately 265 authorised dealers in Latin America, of which approximately 150 are in Brazil.

d) MAN Diesel & Turbo division

75. The MDT division, whose leading entity is MDT SE, is one of the globally leading developers and manu-

facturers of large-bore diesel engines, turbo compressors and industrial turbines for maritime and sta-

tionary applications as well as of chemical reactor systems. With revenues of € 3,780 million in the fiscal

year 2012, the division contributed 23.9 % of the company’s total revenues. As at 31 December 2012,

MDT employed 14,863 employees.

76. MDT consists of three strategic business units (SBUs): Engines & Marine Systems, Power Plants, and

Turbomachinery. The revenue split for these three SBUs is illustrated in the following graph:

KPMG PwC

27

Xx

MAN Diesel & Turbo – Revenues according to SBUs

Source: MAN SE

77. The SBU Engines & Marine Systems develops two-stroke diesel engines for propulsion systems in large

vessels and develops and manufactures four-stroke diesel engines that are used for propulsion systems

for smaller vessels and as auxiliary engines. The engines cover a power range from 450 kW to 87,000

kW. Moreover, the SBU Engines & Marine Systems delivers turbochargers for large-bore diesel engines

as well as propellers and complete ship propulsion systems. After-sales services are offered worldwide

under the brand MAN PrimeServ.

78. MDT is the global market leader for large-bore two-stroke diesel engines with capacities of 2,000 kW to

87,000 kW. Due to their enormous sizes, these engines that are used for large bulk carriers, tankers and

container vessels are manufactured by licensees in the surrounding of shipyards, especially in South

Korea, Japan, and China. The four-stroke engines cover an output range from 450 kW to 21,600 kW and

can run with both liquid and gaseous fuels. The four-stroke engines are mainly used in all types of cargo

vessels, passenger ships, cruise vessels, towboats, dredgers, cable-laying ships, fast ferries and marine

ships. Additionally, the engines can also be used as on-board power gensets. These generator sets have

a power range from 450 kW to 11,200 kW. MDT manufactures the four-stroke engines in its facilities in

Germany, France and India. In fiscal year 2012, the SBU Engines & Marine Systems was the largest of the

three SBUs with revenues of € 1,552 million (2011: € 1,670 million). The order intake amounted to

€ 1,296 million in fiscal year 2012 (2011: € 1,605 million).

79. The SBU Power Plants manufactures and sells stationary diesel and gas engines for power generation,

ranging from small emergency generators up to turnkey power plants with capacities of up to 400 MW.

41.8% 46.3% 41.0%

22.3% 17.9% 20.5%

35.9%35.8%

38.5%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2010 2011 2012

€million

Engines & Marine Systems Power Plants Turbomachinery

3,6103,7803,766

KPMG PwC

28

Xx

The four-stroke diesel and gas engines offer capacities of 450 kW to 18,900 kW, the two-stroke engines

of up to 80 MW amongst others. The MDT engines can be powered with diesel, heavy foil, bio-fuels or

gas as well as with a combination of diesel and gas. The SBU Power Plants also offers systems for com-

bined heat and power generation, diesel combined cycle and expandable, modular concepts. The busi-

ness activities also include the operation and maintenance of power plants.

80. In 2012, the order intake in the power plant business increased by 4 % to € 668 million (2011:

€ 640 million). This was mainly due to large orders from emerging and developing countries, where de-

mand for MDT power plant solutions is high, in order to bridge the energy supply gap quickly. Diesel and

gas engine power plants are primarily used as temporary decentralised solutions to cover the base load.

In addition to order intakes, revenues could also be increased in fiscal year 2012. With € 773 million

(2011: € 647 million), revenues were approximately 20 % higher than in the previous year.

81. The SBU Turbomachinery offers a wide range of turbomachinery products. Among others, the product

range includes compressors as well as gas and steam turbines for the oil and gas industry, the processing

industry and for the power generation. This SBU also offers turnkey machine lines including power tur-

bines and auxiliary units, reactors for the chemical and petrochemical industry as well as special devices

for research facilities.

82. Contrary to the general market development, the SBU Turbomachinery increased its order intake in

fiscal year 2012 by approximately 7 % to € 1,546 million (2011: € 1,447 million). Although the orders of

new compressors and turbines declined due to the economic contraction in the overall market, there is

still a considerable need for capital spending at a number of industrial facilities. These requirements

result from the global population growth and the expanding middle class in emerging countries and the

resulting demand for energy and primary materials. Emerging and developing countries, especially Brazil

and China, were the key regions in 2012. The SBU also offers after-sales services for turbomachinery

using the brand MAN PrimeServ. In comparison to the previous year, revenues of the SBU could be in-

creased considerably by approximately 13 % to € 1,455 million mainly due to the business activities in

China (2011: € 1,293 million).

e) Renk division

83. Renk AG is a publicly listed subsidiary of MAN SE and a global manufacturer of special gear units, propul-

sion components and testing systems. MAN SE holds 76.0 % of the company’s share capital. The com-

pany is a leading manufacturer in tracked vehicle transmissions of different sizes as well as in slide bear-

ings for electrical machinery. Renk also has a leading position in the market for special gear units used

for marine and industrial purposes. The product portfolio also includes different types and performance

categories of couplings. In addition, Renk manufactures testing systems used in development, produc-

tion and quality assurance mainly in the automotive, rail and aviation industries.

KPMG PwC

29

Xx

84. In 2012, order intakes increased by approximately 15 % from € 456 million (2011) to € 525 million. In

addition, Renk generated revenues of € 476 million (2011: € 389 million). This corresponds to approxi-

mately 3 % of the total revenues of MAN SE in 2012.

85. In addition to production facilities in Augsburg, Rheine, Hanover and Berlin, Renk operates production

facilities and sales companies all over the world. The company employed 2,245 people (2011:

2,013 employees) as at 31 December 2012.

86. Renk’s business is divided into four SBUs: Vehicle transmissions, slide bearings, special gear units and

standard gear units.

87. In the SBU vehicle transmissions Renk is a leading manufacturer of fully-automatic transmissions for

medium and heavy tracked vehicles and also offers a wide range of high-performance test beds for vari-

ous sectors.

88. Renk’s automatic power-shift transmissions are designed for all modern diesel engines, for rear and

front installation. The transmissions are controlled and monitored electronically. They are predomi-

nantly manufactured at the production site in Augsburg.

89. Renk’s test beds activities are associated with the SBU vehicle transmissions. Renk designs and manufac-

tures customised test beds for the development, production and quality assurance of motor vehicles,

helicopters, rail car components, tracked vehicles and wind turbines.

90. Located in Hanover/Germany, the SBU slide bearings together with ADMOS-Gleitlager Produktions- und

Vertriebsgesellschaft mbH, Berlin, as well as the American sales company Renk Corporation, Dun-

can/USA, supply hydrodynamic lubricated slide bearings. These slide bearings are used in electric mo-

tors, generators, pumps, fans, water turbines, production plants and marine applications.

91. The SBU special gear units comprises the production of large-scale gear units at the Augsburg site of

Renk AG and at Renk-MAAG GmbH, Winterthur/Switzerland. The product range covers stationary

transmissions for various industrial applications, amongst others for the cement industry, through turbo

transmissions with high transmission applications of up to 140 MW to complex transmissions for fast

ships and marine applications with transmission capacities of up to 80 MW.

92. The SBU standard gear units includes the production of large-scale gear units at the Rheine facility of

Renk AG. One of the core areas are vessel gear units for merchant shipping, ferries, LNG tankers and

supply vessels. The SBU also manufactures transmissions for turbine systems and couplings for industrial

applications. In 2011, Renk’s offshore wind power gear unit business was relocated from Augsburg to

Rheine.

KPMG PwC

30

Xx

2. Market and competition

a) Preliminary remark and economic indicators in comparison

93. Our market and competition analysis focuses on the markets and areas of activities that are significant

for the MAN Group. Therefore, we analysed and described the underlying markets of the divisions MTB,

ML, MDT and Renk in more detail.

94. In the past years, the world economy had to face the effects of the financial and sovereign debt crisis

and was thus characterised by volatile and partly reduced growth rates. This difficult economic envi-

ronment strained the development of the Gross Domestic Products ("GDPs") of the markets that are

relevant for the MAN Group. In the EU-countries and in Brazil, the two most important markets of the

MAN Group especially in 2009, the real GDP decreased significantly. Based on the data of The Economist

Intelligence Unit Ltd., London/United Kingdom ("EIU"), the GDP in Germany, the most important market

for the MAN Group within the EU, decreased by 5.1 %, the Brazilian GDP by 0.3 %. After a worldwide

economic recovery in 2010, with considerably positive GDP growth rates, especially in China with

10.4 %, the growth rates have again been declining since 2011 and have again been negative in the EU (-

0.3 % in 2012). A recovery of the world economy with moderately increasing GDP growth rates is again

expected from 2013 onwards. In individual countries of the EU, low growth rates of less than 1.0 % are

expected for 2013. Up to 2017, slightly higher growth rates of the respective GDP as compared to 2012

are forecast for all the markets under consideration, except for China.

95. The development of inflation rates also faced the effects of the financial and sovereign debt crisis. After

a worldwide low inflation level in 2009, the inflation rates in all relevant markets increased up to 2011.

In 2012, the inflation rates were marginally below the level of 2011. For the EU countries, EIU forecasts

a decline in the inflation rate from 2.5 % in 2012 to 2.1 % in 2017. For Germany, nearly stable inflation

rates of approximately 2.0 % are expected (2.1 % in 2012, 2.0 % in 2017). For Brazil, a slightly declining

inflation development from 5.4 % (2012) to 4.9 % (2017) is assumed. On the other hand, increasing infla-

tion rates have been forecast for China and South Korea, the main markets of the MAN Group in Asia. In

2012, the inflation rate for China amounted to 2.6 %, while the South Korean inflation rate amounted to

2.2 %; according to the EIU forecasts, the inflation rate in China will increase to 4.0 % in 2017 and to

3.1 % in South Korea.

KPMG PwC

31

Xx

96. The GDP growth rates as well as the inflation rates over time in the most important markets for the

MAN Group are illustrated in the following overview:

b) Market positioning and competitive environment in the MAN Truck & Bus division

Truck

Global truck market

97. The global truck and commercial vehicle market depends considerably on the general economic devel-

opment and the resulting demand for transport services. The commercial vehicle market is divided into

several categories according to the GVW.1

1 The consideration thus focuses on the vehicle market with a gross vehicle weight of over 6 t that is relevant for

MTB.

GDP growth rate

Difference, % 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Germany -5.1% 4.0% 3.1% 0.9% 0.7% 1.6% 1.3% 1.3% 1.4%

Brazil -0.3% 7.5% 2.7% 1.0% 3.5% 3.8% 3.5% 3.7% 3.5%

China 9.2% 10.4% 9.3% 7.8% 8.5% 7.8% 7.7% 7.3% 6.4%

South Korea 0.3% 6.3% 3.6% 2.1% 2.9% 3.8% 3.9% 4.0% 4.0%

Russia -7.8% 4.5% 4.3% 3.4% 3.3% 3.7% 4.1% 4.1% 4.0%

India 8.2% 9.6% 6.9% 5.2% 6.5% 7.3% 7.3% 7.5% 7.5%

European Union -4.3% 2.1% 1.6% -0.3% 0.0% 1.2% 1.5% 1.6% 1.5%

…

World -2.3% 3.9% 2.6% 2.1% 2.3% 2.9% 2.9% 2.9% 3.0%

Inflation

Difference, % 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Germany 0.2% 1.2% 2.5% 2.1% 1.8% 1.9% 2.1% 1.9% 2.0%

Brazil 4.9% 5.0% 6.6% 5.4% 6.1% 5.7% 5.4% 5.1% 4.9%

China -0.7% 3.2% 5.5% 2.6% 4.3% 4.1% 3.9% 4.2% 4.0%

South Korea 2.8% 2.9% 4.0% 2.2% 2.6% 2.8% 2.9% 3.1% 3.1%

Russia 11.7% 6.9% 8.4% 5.1% 6.3% 6.2% 5.7% 5.1% 5.0%

India 10.8% 12.0% 8.9% 9.3% 8.8% 8.0% 7.0% 6.6% 7.1%

European Union 0.7% 1.9% 2.7% 2.5% 2.2% 2.1% 2.3% 2.1% 2.1%

…

World 1.5% 3.0% 4.1% 3.4% 3.4% 3.5% 3.4% 3.3% 3.3%

Source: EIU, February/March 2013

KPMG PwC

32

Xx

98. The following chart gives an overview of the expected development of global truck sales with a GVW

over 6 t according to regions:

Global truck sales (in thousand units)

Source: LMC, 20122

99. Two developments can be observed when considering the development of the truck market. On the one

hand, the significant dependency of the truck market on the overall economic development is reflected

especially in the financial market crisis around the year 2009 (refer to e. g. KPMG, 2011). On the other

hand, it becomes apparent that the market growth mainly results from the growth of the emerging

markets, especially from the BRIC countries (Brazil, Russia, India and China), while the fully developed

and mature markets of the triad (West Europe, North America and Japan) only show marginal growth.

100. Beyond the development of sales volumes, other trends can also be observed in the commercial vehicle

market. The most important trends are given below:

• Development of a noticeably increasing middle class segment,

• The customers’ focus on the total cost of ownership,

• Increasing significance of environmental protection ("Green Fleet"),

• Increasing significance of Asian manufacturers to the disadvantage of European and American

manufacturers.

2 LMC Automotive is one of the leading data providers in the automobile sector and offers turnover and produc-

tion forecasts for passenger cars and trucks as well as forecasts for the supply and demand of engines and

transmissions.

2,231

2,340 2,206

1,811

2,495

2,626

2,321 2,455

2,729 2,885

2,986 3,166

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Europe North America Asia Mercosur Africa and Australia Other

CAGR 2012-17: 6.4 %

KPMG PwC

33

Xx

Cyclicality of the truck market

101. The commercial vehicle industry is subject to a noticeable cyclicality. In comparison with other indus-

tries, the commercial vehicle industry reacts heavily to cyclical changes with respect to both the speed

of adjustments as well as volatility. As a result, fluctuating sales volumes and revenues of truck manu-

facturers can regularly be observed in the course of an economic cycle.

102. The central driver of this development is the real Gross Domestic Product with the input factors private

consumption, gross investments, public expenditures as well as export surplus. When these factors and

thus the overall economic environment improve, this usually has a positive effect on truck sales. Other

relevant macroeconomic drivers are the interest level and the development of the producer price indi-

ces. Besides these macroeconomic indicators, the development of industries that are relevant for the

truck market is also important. These include, for instance, the logistics as well as the building industry.

Changes in these industries often have direct effects on the truck market. In addition to quantitative

factors, there are also qualitative aspects that are important for the development of truck sales. These

include regulatory and legislative initiatives such as the harmonisation of the truck toll in Europe, modi-

fications in emission standards, safety regulations as well as conditions for driving permits in inner-city

environmental zones.

Emerging markets

103. In the last two decades, the significance of various regional truck markets in the global market has

considerably changed in favour of the emerging countries. Especially the BRIC countries have strength-

ened their importance in the truck market at the expense of the triad countries. An analysis by the Bos-

ton Consulting Group (BCG, 2012) shows that the world market share of the triad countries has reduced

from 56 % in 2000 to 17 % in 2010. In the same period, the BRIC countries have increased their share of

worldwide truck sales from 33 % to 74 %. The authors of the study also expect that the truck markets in

the BRIC countries will offer attractive opportunities in future, even though the high growth rates from

the past can probably no longer be attained in future. In the long term, infrastructure problems will

probably brake Russia’s growth. For China, a market slow-down is expected due to expiry of the gov-

ernmental economic stimulus packages that drove the truck market in the past. Yet the European truck

market will also offer opportunities for growth in the coming years due to the catch-up effect from the

financial and sovereign debt crisis. However, growth forecasts for the European market depend on

when the financial and sovereign debt crisis has finally been overcome.

104. Overall, the outlook for the development of the global truck market is positive. The expected average

annual growth in sales for the period from 2012 to 2017 is 6.4 %. The highest level of growth is expected

in Asia, with an average growth rate of 7.7 % p.a. for the period from 2012 to 2017 followed by Europe,

as well as Africa and Australia with average growth rates of 6.3 % and 6.1 % p. a. in the same period.

KPMG PwC

34

Xx

Trends

105. One of the most important trends in the truck market is the shift from the low price segment to the