jollibee foods corporation · 2019-07-01 · jollibee 3,202 jws 312 freemont 842 mang inasal 347...

TRANSCRIPT

Jollibee Foods Corporation Employees’ Multi- Purpose Cooperative

COOPERATIVE From the word: COOPERATION

adjective

1.working or acting together willingly for a common purpose or benefit.

2. demonstrating a willingness to cooperate.

noun

a jointly owned enterprise engaging in the production or distribution of goods or the supplying of services, operated by its members for their mutual benefit, typically organized by consumers or farmers.

COOPERATIVE Cooperative is an autonomous and duly registered association of persons, with a common bond of interest, who have voluntarily joined together to achieve their social, economic, and cultural needs and aspirations by making equitable contributions to the capital required, patronizing their products and services and accepting a fair share of risks and benefits of undertaking in accordance with universally accepted cooperative principles.

HISTORY OF COOPERATIVE Industrial Revolution - Robert Owen of England, the Father of Cooperation

28 Weavers in Rochdale, England established the first successful consumer cooperative

Frederick Wilhelm Raiffeisen set up the First Rural Credit Association

Dr. Jose Rizal organized Marketing Farmers Cooperative during his exile in Dapitan In February 5, the Rural Credit Law was enacted in the Philippine Republic

March 10,1990 Under Aquino Admin, Signing of RA 6939, Creating CDA & RA 6938, the Coop Code of the Philippines

Types of Cooperatives • Credit: savings & lending

• Consumers: procure & distribute

• Producers: undertakes production

• Marketing: markets the products

• Service: medical, dental care, hospitalization & etc services

• Multi-purpose: combination of 2 or more business activities.

• Advocacy:promotes & advocates cooperativism

• Agrarian reform

• Cooperative bank

• Financial Service

• Fishermen

• Health Service

• Housing Cooperative

• Insurance Coop

• Transport Coop

• Water Service Coop

• Workers Coop

• Dairy cooperative

• Education cooperative

• Electric

Principles

1. Open and Voluntary Membership

2. Democratic Member Control

3. Member Economic Participation

4. Autonomy & Independence

5. Education, Training & Information

6. Cooperation Among Cooperatives

7. Concern For Community

Values

Are attitudes about the worth of people, concepts, or things

Influence a person’s behavior in weighing the importance of alternatives

Self-help

Self-responsibility

Democracy

Equality

Equity

Solidarity

Honesty

Openness

Social responsibility

Caring for others

HOW IT ALL STARTED?

• April 19, 1988 • Registered as JFC Employees’

Consumers Cooperative,Inc.

• Founded by 15 incorporators • (15 Jollibee Employees)

HOW IT ALL STARTED?

1991 Registered as Jollibee Foods Corporation Employees’ Multi Purpose Cooperative 1992 Php5M total assets Php836K total contribution Area of Operation: Metro Manila

FIRST LOGO

The JFC COOP

Today!

& Features the human chain. This represents STRENGTH & POWER of our UNITED membership.

Human chain is circle, represents INFINITY.

Blue Color – TRUST & RESPONSIBILITY

Gold Color – PROSPERITY & WEALTH CURRENT LOGO

MISSION

· To be the best provider of relevant and reliable financial services to our members.

• To grow the assets and wealth of the cooperative, to continually improve the benefits of its members.

VISION

•We will be a significant contributor to the welfare and development of the JFC Community and become a real source of pride to our members.

•We will be one of the most admired and emulated cooperatives in the country.

By 2020

1988 2001 2002

2007 2003

2008

2011 2012

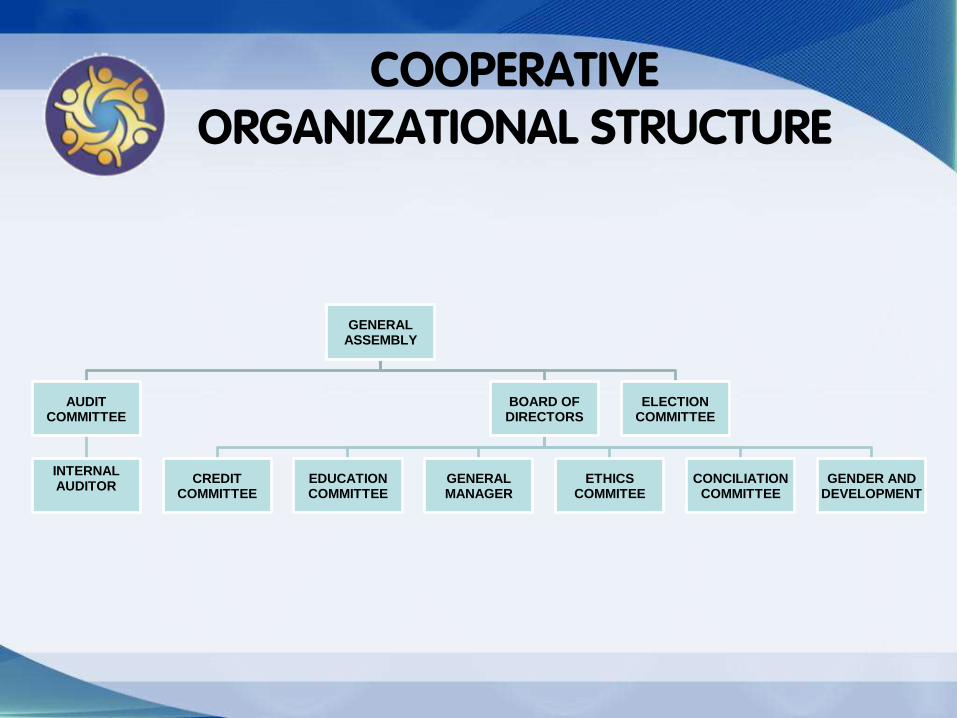

COOPERATIVE ORGANIZATIONAL STRUCTURE

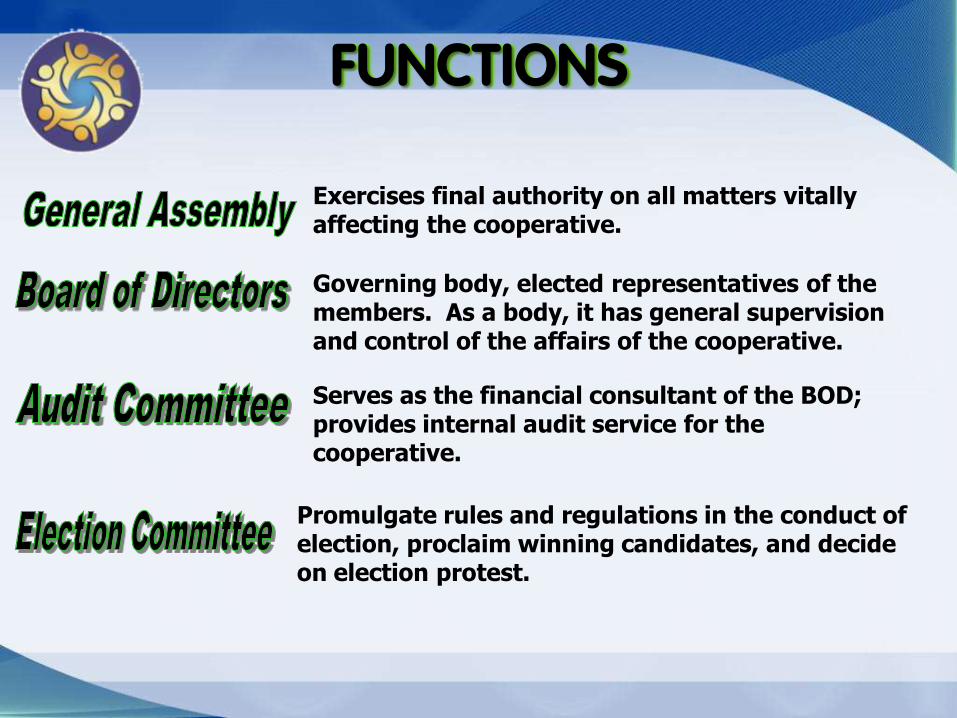

GENERAL ASSEMBLY

AUDIT COMMITTEE

INTERNAL AUDITOR

BOARD OF DIRECTORS

CREDIT COMMITTEE

EDUCATION COMMITTEE

GENERAL MANAGER

ETHICS COMMITEE

CONCILIATION COMMITTEE

GENDER AND DEVELOPMENT

ELECTION COMMITTEE

Exercises final authority on all matters vitally affecting the cooperative.

Governing body, elected representatives of the members. As a body, it has general supervision and control of the affairs of the cooperative.

Serves as the financial consultant of the BOD; provides internal audit service for the cooperative.

FUNCTIONS

Promulgate rules and regulations in the conduct of election, proclaim winning candidates, and decide on election protest.

Conciliate, hear and decide all intra-cooperative Disputes between and/or among members, officers, directors and the community.

Develops, plans, and implements educational and information activities of the cooperative.

FUNCTIONS

Develop, formulate and recommend the rules under the Code of Governance and the Ethical standard of the members, officers and employees of the cooperative.

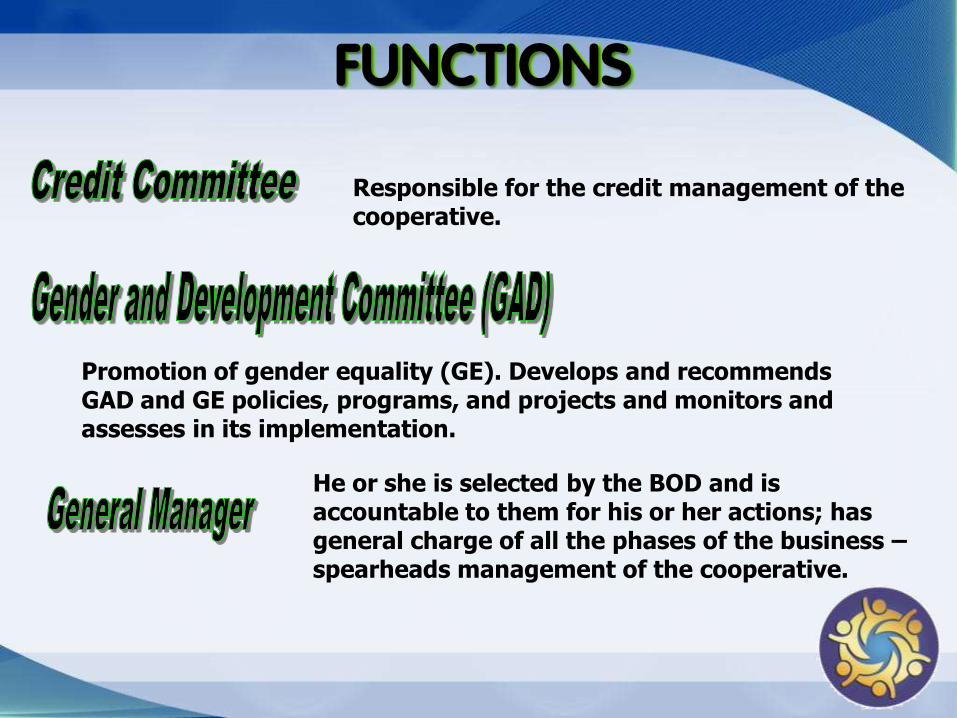

Promotion of gender equality (GE). Develops and recommends GAD and GE policies, programs, and projects and monitors and assesses in its implementation.

FUNCTIONS

He or she is selected by the BOD and is accountable to them for his or her actions; has general charge of all the phases of the business – spearheads management of the cooperative.

Responsible for the credit management of the cooperative.

JFC Coop Achievements

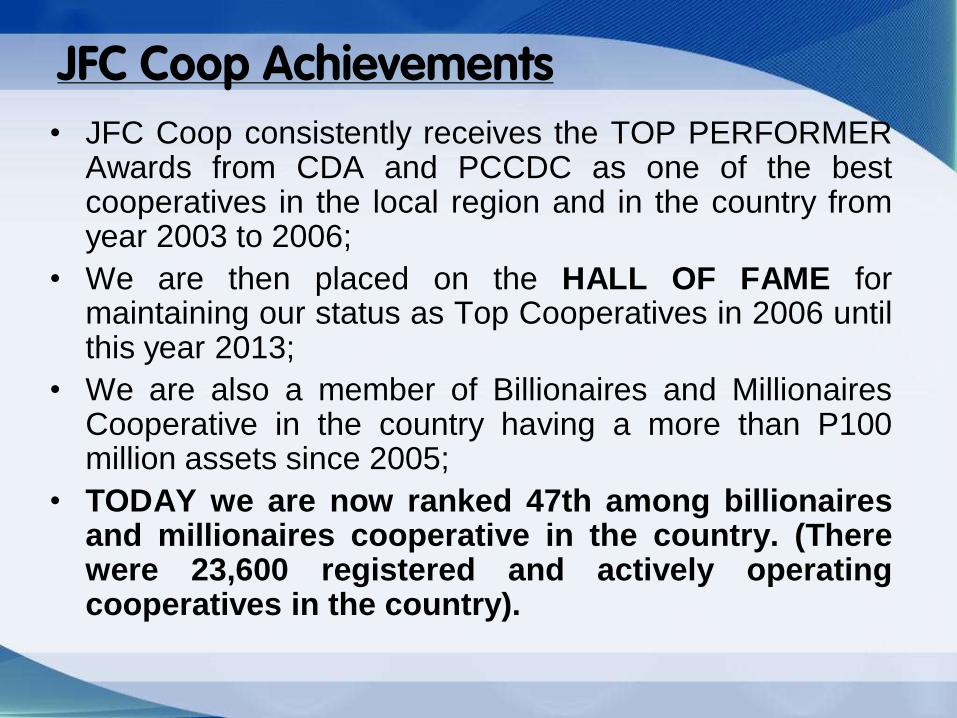

• JFC Coop consistently receives the TOP PERFORMER Awards from CDA and PCCDC as one of the best cooperatives in the local region and in the country from year 2003 to 2006;

• We are then placed on the HALL OF FAME for maintaining our status as Top Cooperatives in 2006 until this year 2013;

• We are also a member of Billionaires and Millionaires Cooperative in the country having a more than P100 million assets since 2005;

• TODAY we are now ranked 47th among billionaires and millionaires cooperative in the country. (There were 23,600 registered and actively operating cooperatives in the country).

MEMBERSHIP

Total of 8,898 members

As of December 31, 2017 SBU / BRAND No. of Members

BURGER KING 203

CHOWKING 1,102

GREENWICH 709

JOLLIBEE 3,202

JWS 312

FREEMONT 842

MANG INASAL 347

ZENITH

FRANCHISE / Associate

277

1,904

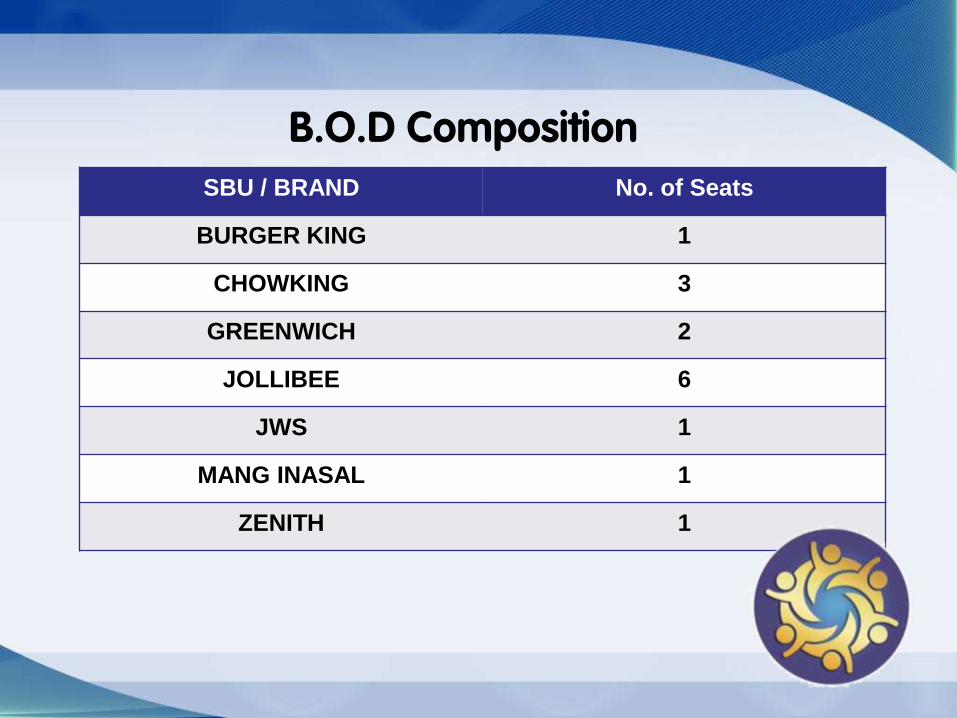

B.O.D Composition

SBU / BRAND No. of Seats

BURGER KING 1

CHOWKING 3

GREENWICH 2

JOLLIBEE 6

JWS 1

MANG INASAL 1

ZENITH 1

BOARD OF DIRECTORS

Chairman S’ Dags Tan, Vice-Chairman M’ CS Siason

BOD Member S’ Alex Mendoza

BOARD OF DIRECTORS

BOD Members M’ Sheila Martinez, S’ Mario Malalis

S’ Art Laureta, M’ Jenny Benedicto

BOARD OF DIRECTORS

BOD Members S’ Julius Ceazar Greralda

M’ Cherry Obmasca, M’ Emie Barajas

BOARD OF DIRECTORS

BOD Members S’ Rico Baldo

Secretary S’ Vic Tolosa, Treasurer S’ Jerome Pinugu

BOARD OF DIRECTORS

BOD Members S’ Jojo Subido, S’ Allan Constantino,

M’ Arcy Edombingo, M’ Barbara Jane Regalado

BOARD OF DIRECTORS

BOD Members M’ Cherry Obmasca, M’ Emie Barajas

Secretary S’ Vic Tolosa, Treasurer S’ Jerome Pinugu

MANAGEMENT TEAM

General Manager

M’ Oma Guhiting

Support Head

M’ Cherry Gonzales

MANAGEMENT TEAM

M’ Marlene Meneses (Accounting)

M’ Marissa Fernandez (Loans)

MANAGEMENT TEAM

S’ Ricky Sing (Member Relations & Marketing)

M’ Malou Dumlao (Sales)

How do I become a member?

• YOU must be a REGULAR and a good standing employee of JFC or its subsidiaries, affiliates or franchise.

• Fill-out the Membership

Application Form

• Pay one time membership fee of

P200.00

• Contribute a continuous minimum share capital of P100.00 per payday up to the extent of subscribed capital

• Excess of subscribed capital will be deposited in your Fixed Savings account

• Open a PSF ,CPF, or SPF s w/ a minimum contribution of P100 per payday.

(Through salary deduction)

How do I become a member?

TYPES OF MEMBERSHIP

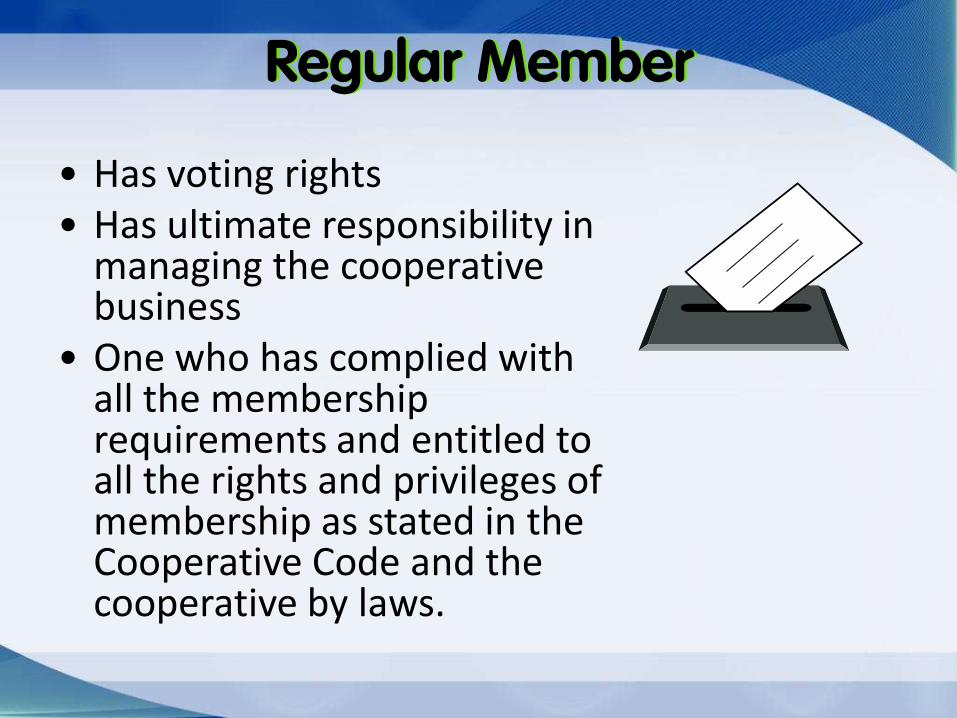

Regular Member

• Has voting rights • Has ultimate responsibility in

managing the cooperative business

• One who has complied with all the membership requirements and entitled to all the rights and privileges of membership as stated in the Cooperative Code and the cooperative by laws.

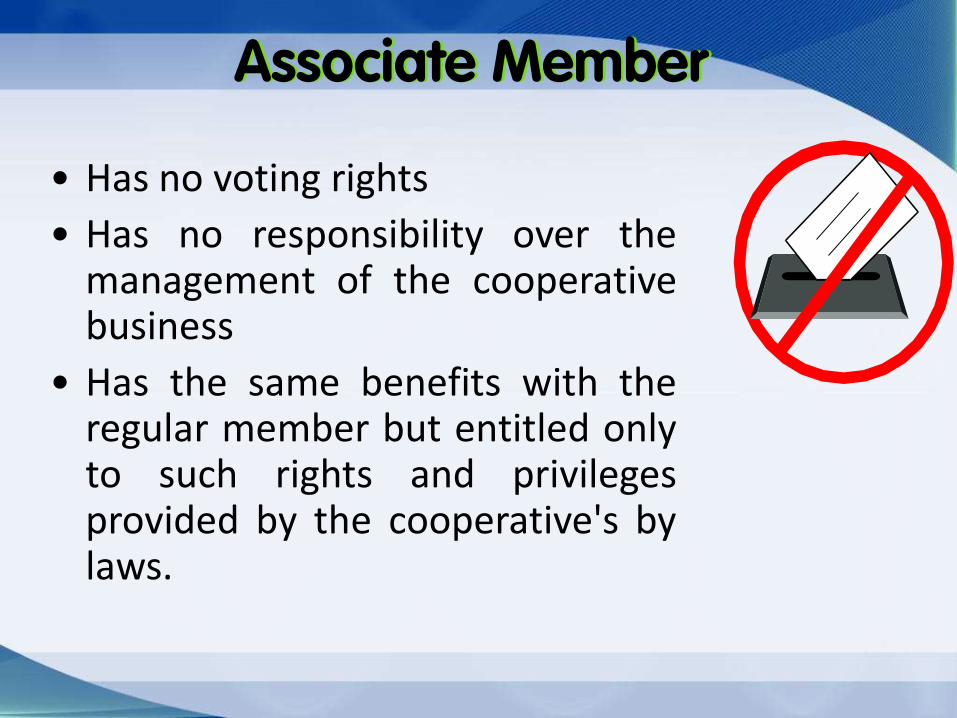

Associate Member

• Has no voting rights

• Has no responsibility over the management of the cooperative business

• Has the same benefits with the regular member but entitled only to such rights and privileges provided by the cooperative's by laws.

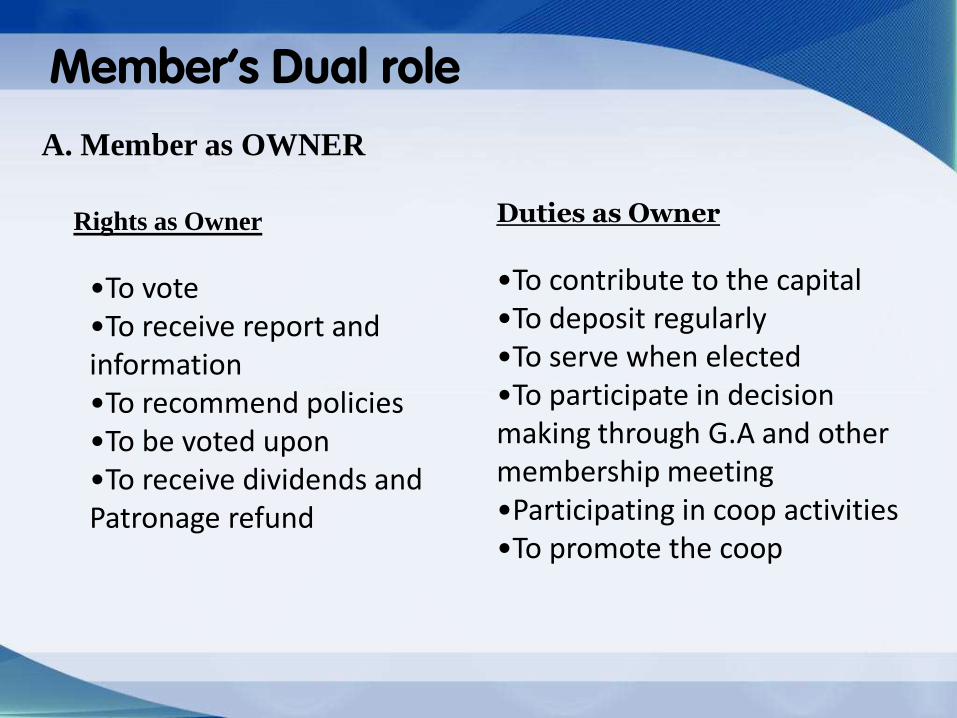

MEMBER’S Dual Role

Duties as Owner

•To contribute to the capital •To deposit regularly •To serve when elected •To participate in decision making through G.A and other membership meeting •Participating in coop activities •To promote the coop

Member’s Dual role A. Member as OWNER

Rights as Owner

•To vote

•To receive report and information •To recommend policies •To be voted upon •To receive dividends and Patronage refund

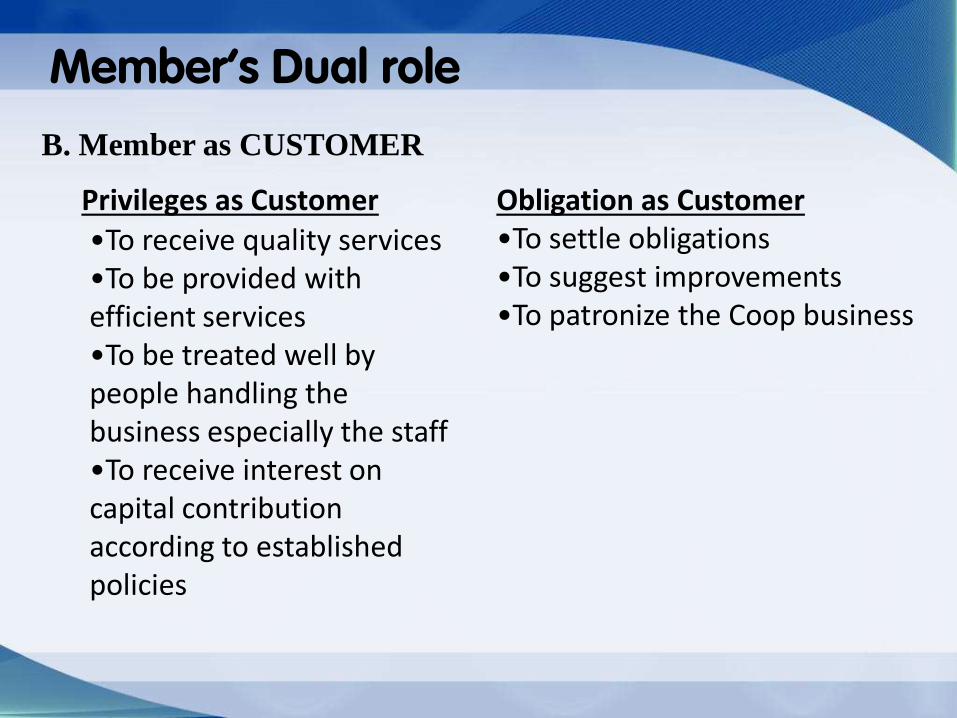

Obligation as Customer •To settle obligations •To suggest improvements •To patronize the Coop business

Member’s Dual role B. Member as CUSTOMER

Privileges as Customer

•To receive quality services •To be provided with efficient services •To be treated well by people handling the business especially the staff •To receive interest on capital contribution according to established policies

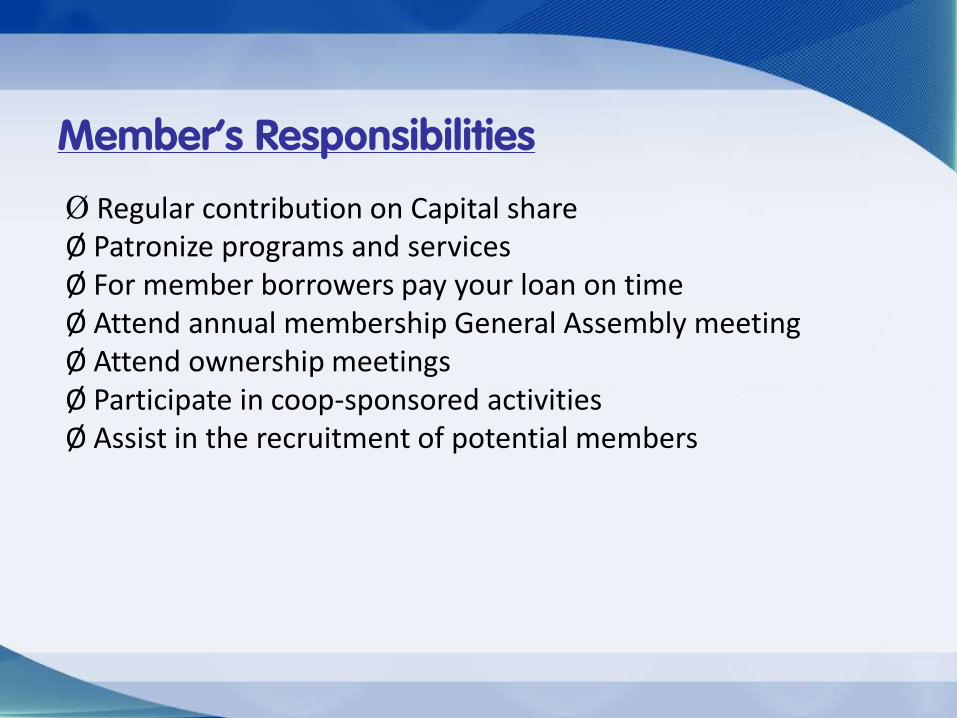

Ø Regular contribution on Capital share Ø Patronize programs and services Ø For member borrowers pay your loan on time Ø Attend annual membership General Assembly meeting Ø Attend ownership meetings Ø Participate in coop-sponsored activities Ø Assist in the recruitment of potential members

Member’s Responsibilities

SHARE CAPITAL, FIXED SAVINGS, &

PATRONAGE REFUND

Share Capital - The Share capital of cooperative is the money paid or required to be paid for the conducts of its operation. (Article 76 of Chapter VIII, Cooperative Code 9520.)

- The total amount of your capital share will also be the baring for the computation of your dividend. - This is also being use as your collateral for your future loan.

FIXED SAVINGS

Features

• Contributions in excess of subscribed capital

• Withdrawal upon resignation from the Coop or from the company

• Tax free

Benefit

• 3% interest per annum

Dividends Refers to the cooperative practice of distributing annual earnings to their members

Patronage Refund Refers to the cooperative practice of distributing interest payment from the products they purchase and loan availment

You can enjoy any of the following benefits and privileges:

1. Savings and time deposits at very competitive rates

2. Loan and other credit facilities

3. Purchase privileges with payment on installments through salary deductions

4. Christmas and BIRTHDAY Cash gifts

5. Attend FREE livelihood / enterprise and skills enhancement trainings and programs.

6. Opportunity to avail Scholarship Assistance.

7. Damayan Fund – death assistance for members only

8. Opportunity to attend special activities e.g. trade fair / caravan and Cooperative Month Celebration, Compulsory Raffle and etc.

9. Patronage refunds on loan and purchases

10. Annual Profit sharing in the form of interest on share capital and

11. Guaranteed earnings on fixed deposits

Products and Services

Cooperative’s Savings Facilities

No matter where you’re looking to go, a savings account from JFC COOP can help you get there. Plan for health expenses, holiday expenses, and unexpected expenses with our

Savings Facilities.

For a seriously great rate of return.

HOW DO WE DEFINE SAVINGS?

SAVINGS IS AN EXPENSE THAT BUYS YOUR FUTURE

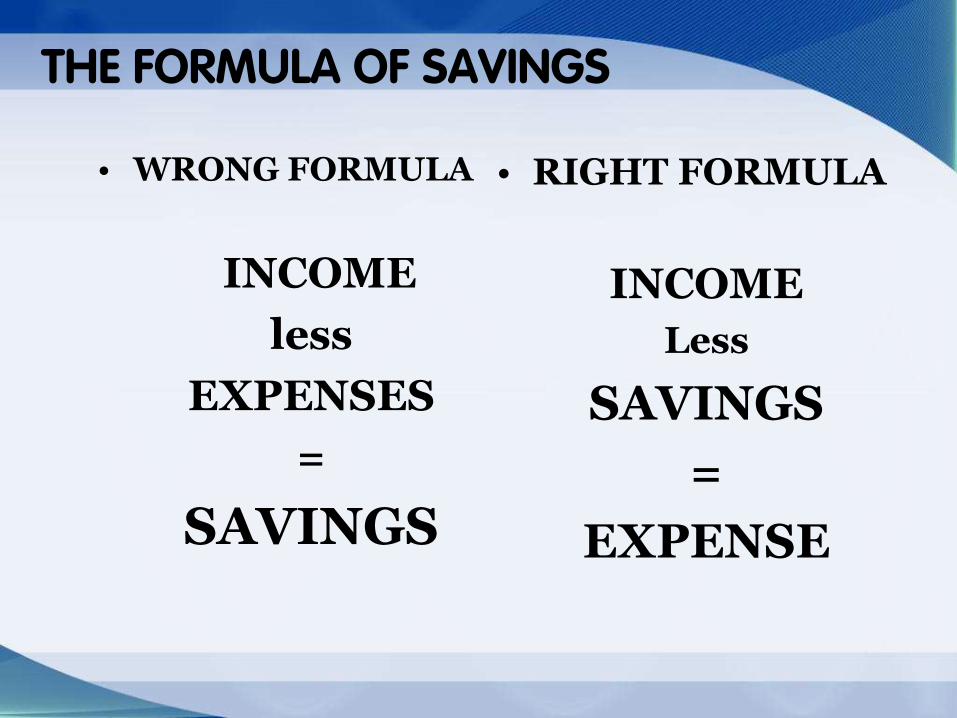

THE FORMULA OF SAVINGS

• WRONG FORMULA

INCOME

less

EXPENSES

=

SAVINGS

• RIGHT FORMULA

INCOME

Less

SAVINGS

=

EXPENSE

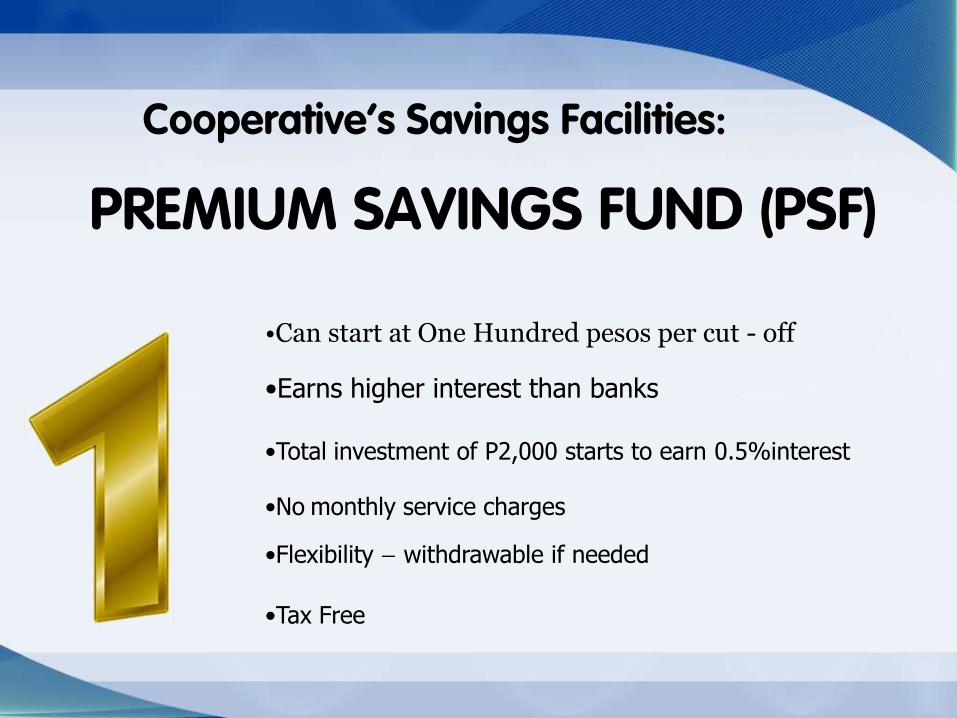

Cooperative’s Savings Facilities:

PREMIUM SAVINGS FUND (PSF)

•Tax Free

•Can start at One Hundred pesos per cut - off

•Earns higher interest than banks

•Total investment of P2,000 starts to earn 0.5%interest

•No monthly service charges

•Flexibility – withdrawable if needed

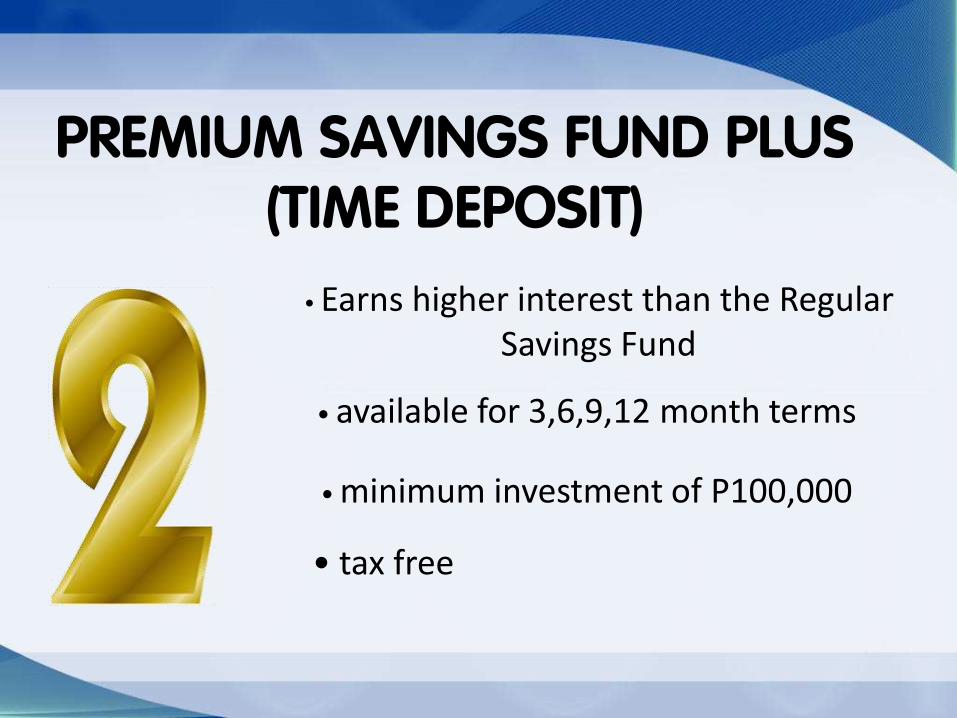

PREMIUM SAVINGS FUND PLUS (TIME DEPOSIT)

• available for 3,6,9,12 month terms

• minimum investment of P100,000

• Earns higher interest than the Regular Savings Fund

• tax free

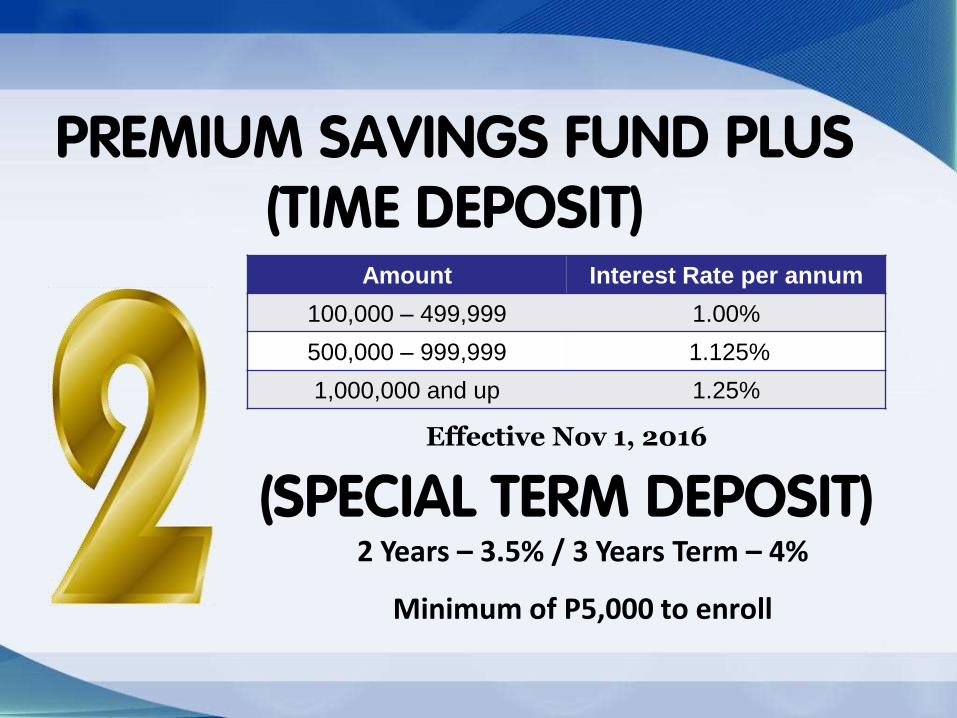

PREMIUM SAVINGS FUND PLUS (TIME DEPOSIT)

Amount Interest Rate per annum

100,000 – 499,999 1.00%

500,000 – 999,999 1.125%

1,000,000 and up 1.25%

Effective Nov 1, 2016

(SPECIAL TERM DEPOSIT) 2 Years – 3.5% / 3 Years Term – 4%

Minimum of P5,000 to enroll

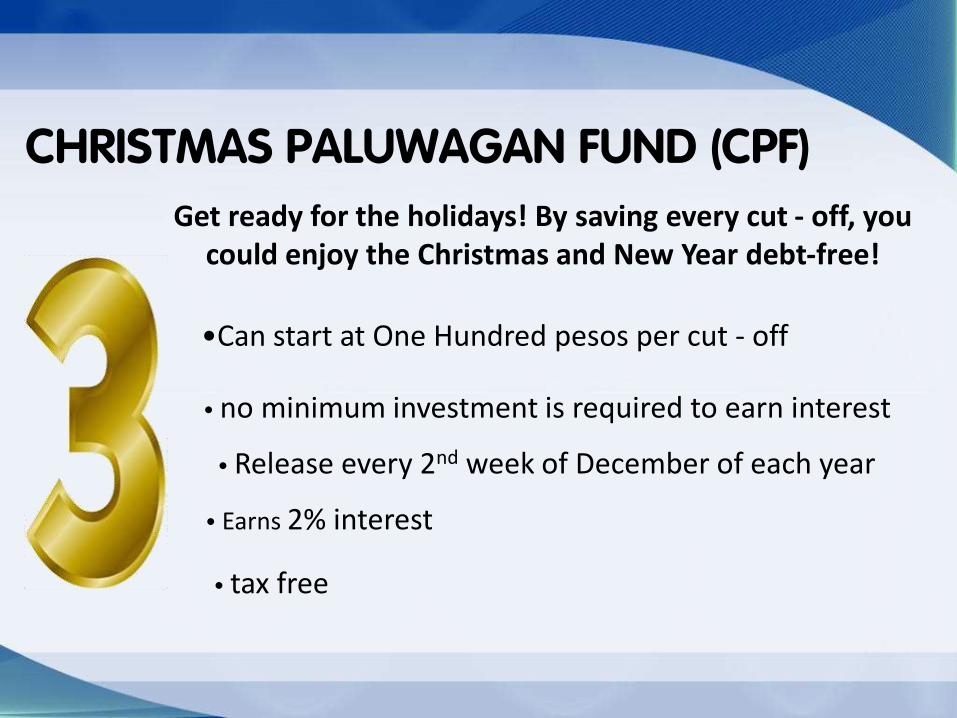

CHRISTMAS PALUWAGAN FUND (CPF)

• no minimum investment is required to earn interest

• Release every 2nd week of December of each year

• tax free

• Earns 2% interest

Get ready for the holidays! By saving every cut - off, you could enjoy the Christmas and New Year debt-free!

•Can start at One Hundred pesos per cut - off

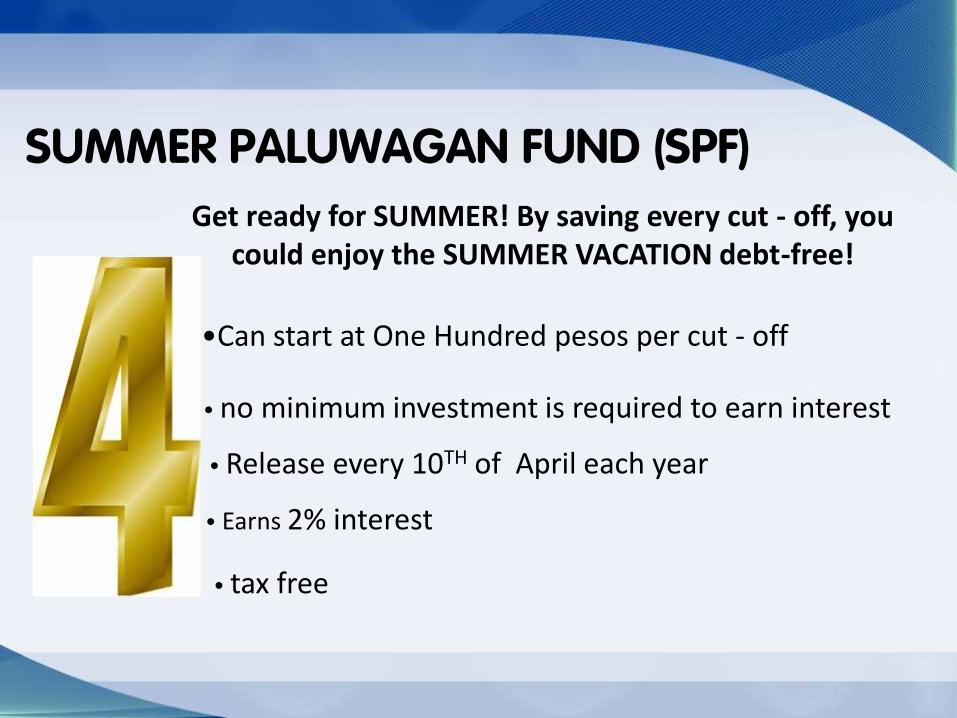

• no minimum investment is required to earn interest

• tax free

• Earns 2% interest

•Can start at One Hundred pesos per cut - off

SUMMER PALUWAGAN FUND (SPF)

Get ready for SUMMER! By saving every cut - off, you could enjoy the SUMMER VACATION debt-free!

• Release every 10TH of April each year

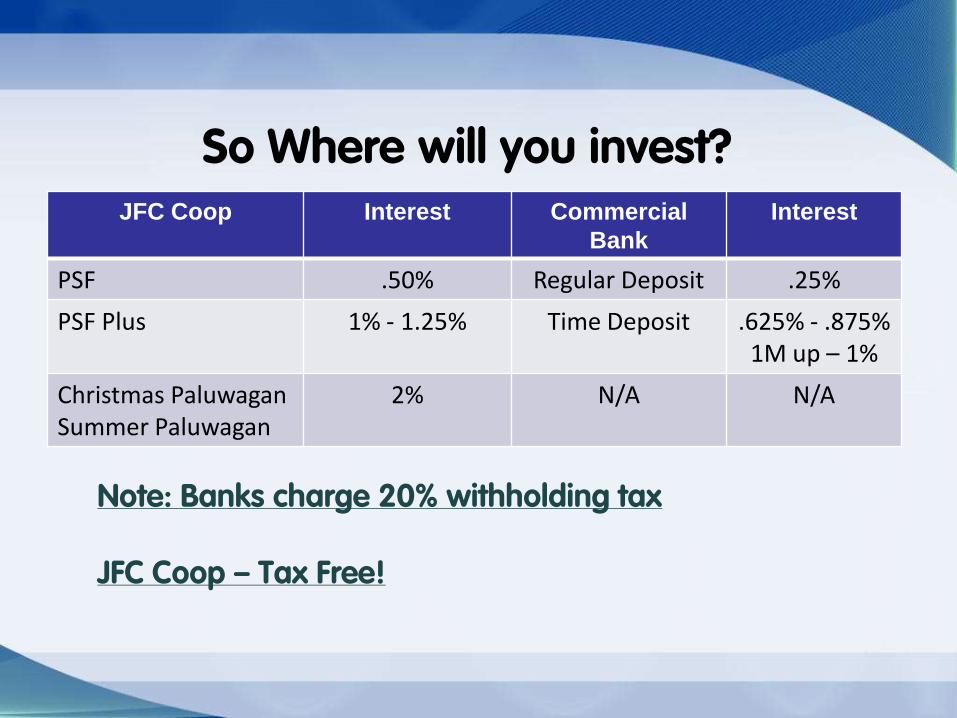

So Where will you invest? JFC Coop Interest

Commercial

Bank

Interest

PSF .50% Regular Deposit .25%

PSF Plus 1% - 1.25% Time Deposit .625% - .875% 1M up – 1%

Christmas Paluwagan Summer Paluwagan

2% N/A N/A

Note: Banks charge 20% withholding tax JFC Coop – Tax Free!

LOAN PRODUCTS

One of your privileges as a member is to avail loan products offered by JFC Coop JFC Coop Offers Low Interest + Patronage Refund

Who are entitled to loan?

Qualified members of JFC-Coop:

– Contributed a minimum share capital of P2,500.00

– Tenure of membership should be at least 6 months

– And with a 45% allowable deduction / Capacity to pay

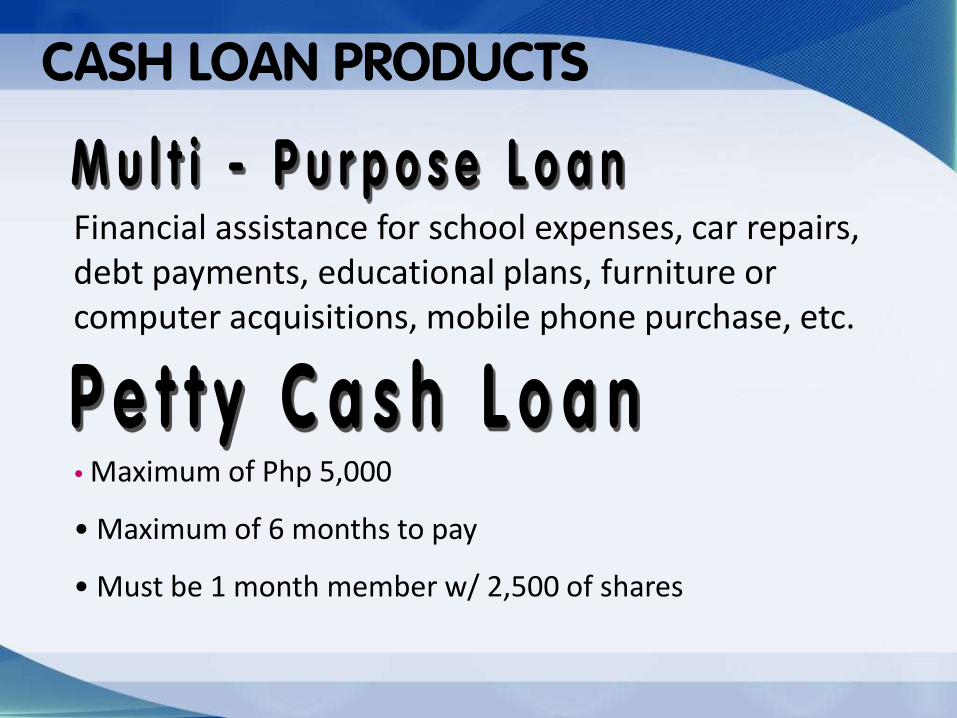

CASH LOAN PRODUCTS

Financial assistance for school expenses, car repairs, debt payments, educational plans, furniture or computer acquisitions, mobile phone purchase, etc.

• Maximum of Php 5,000

• Maximum of 6 months to pay

• Must be 1 month member w/ 2,500 of shares

Financial assistance during untimely events like sickness and death

CASH LOAN PRODUCTS

Natural Calamities like storm surge, typhoon, earthquake etc.

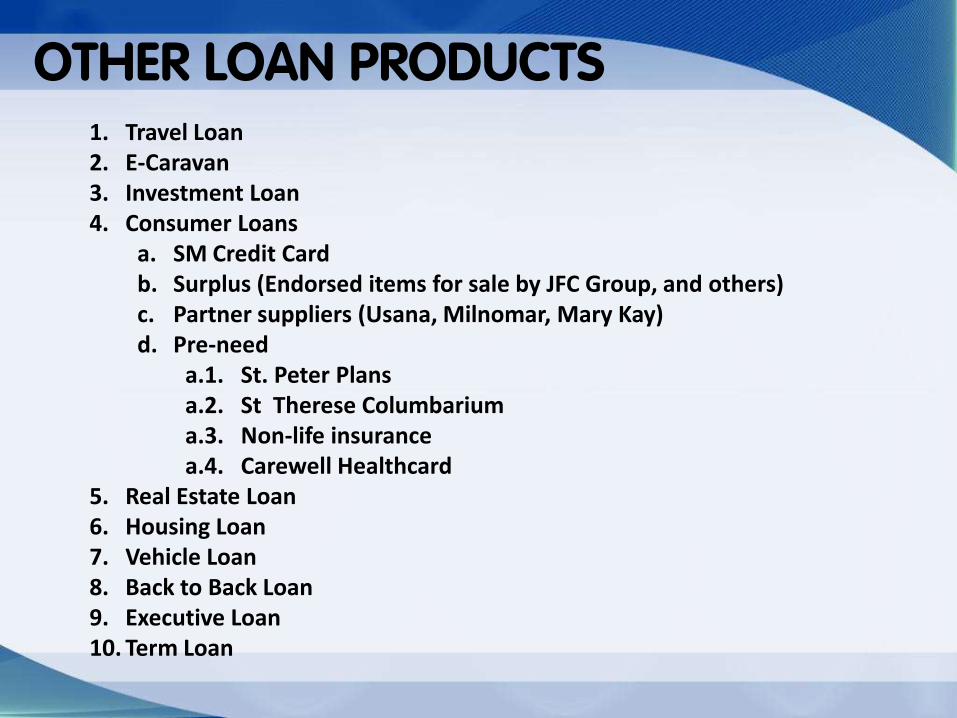

OTHER LOAN PRODUCTS 1. Travel Loan 2. E-Caravan 3. Investment Loan 4. Consumer Loans

a. SM Credit Card b. Surplus (Endorsed items for sale by JFC Group, and others) c. Partner suppliers (Usana, Milnomar, Mary Kay) d. Pre-need

a.1. St. Peter Plans a.2. St Therese Columbarium a.3. Non-life insurance a.4. Carewell Healthcard

5. Real Estate Loan 6. Housing Loan 7. Vehicle Loan 8. Back to Back Loan 9. Executive Loan 10. Term Loan

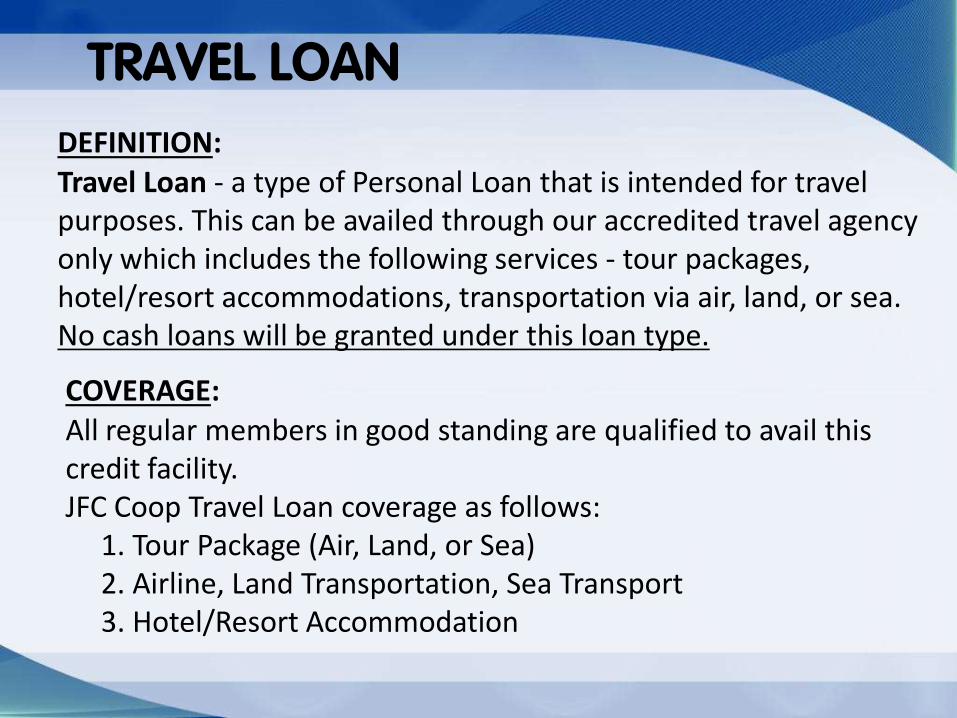

TRAVEL LOAN

DEFINITION: Travel Loan - a type of Personal Loan that is intended for travel purposes. This can be availed through our accredited travel agency only which includes the following services - tour packages, hotel/resort accommodations, transportation via air, land, or sea. No cash loans will be granted under this loan type.

COVERAGE: All regular members in good standing are qualified to avail this credit facility. JFC Coop Travel Loan coverage as follows: 1. Tour Package (Air, Land, or Sea) 2. Airline, Land Transportation, Sea Transport 3. Hotel/Resort Accommodation

TRAVEL LOAN

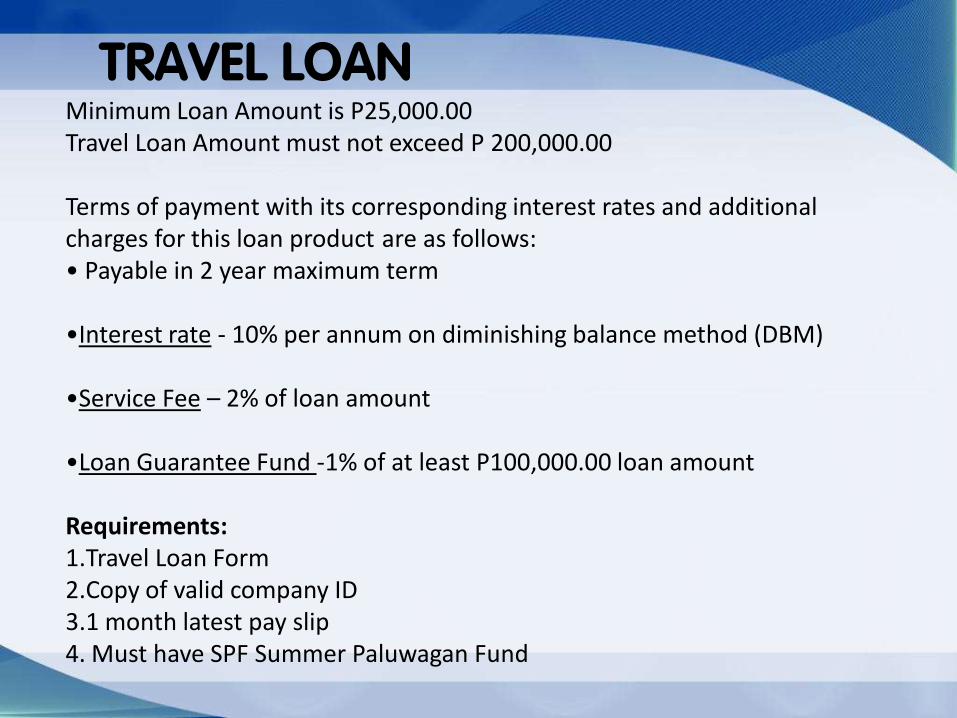

TRAVEL LOAN Minimum Loan Amount is P25,000.00 Travel Loan Amount must not exceed P 200,000.00 Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows: • Payable in 2 year maximum term •Interest rate - 10% per annum on diminishing balance method (DBM)

•Service Fee – 2% of loan amount

•Loan Guarantee Fund -1% of at least P100,000.00 loan amount Requirements: 1.Travel Loan Form 2.Copy of valid company ID 3.1 month latest pay slip 4. Must have SPF Summer Paluwagan Fund

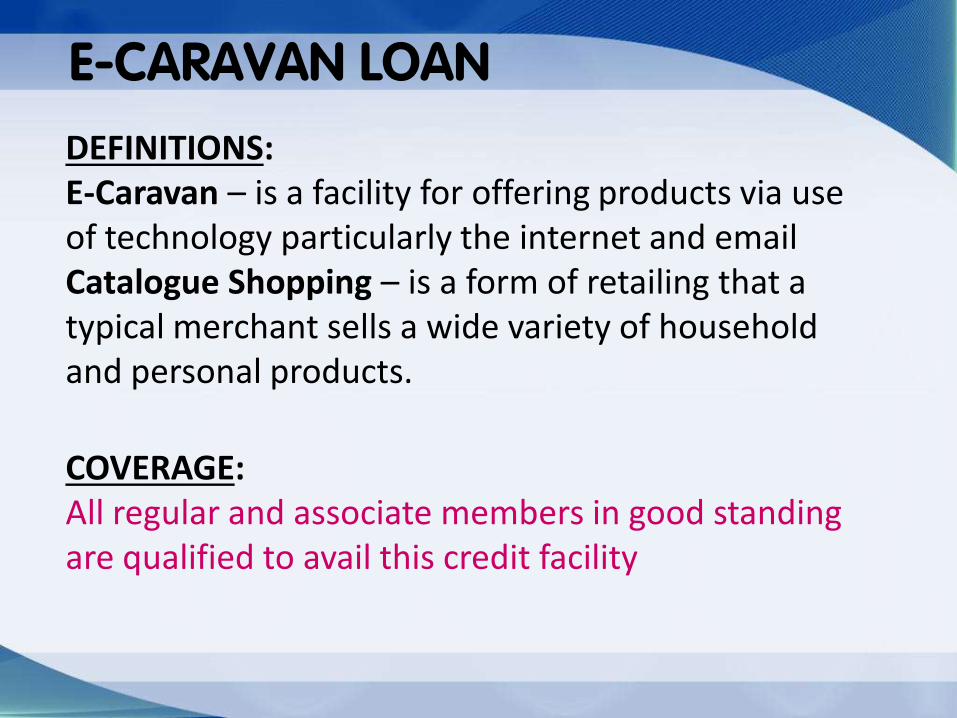

E-CARAVAN LOAN

DEFINITIONS: E-Caravan – is a facility for offering products via use of technology particularly the internet and email Catalogue Shopping – is a form of retailing that a typical merchant sells a wide variety of household and personal products.

COVERAGE: All regular and associate members in good standing are qualified to avail this credit facility

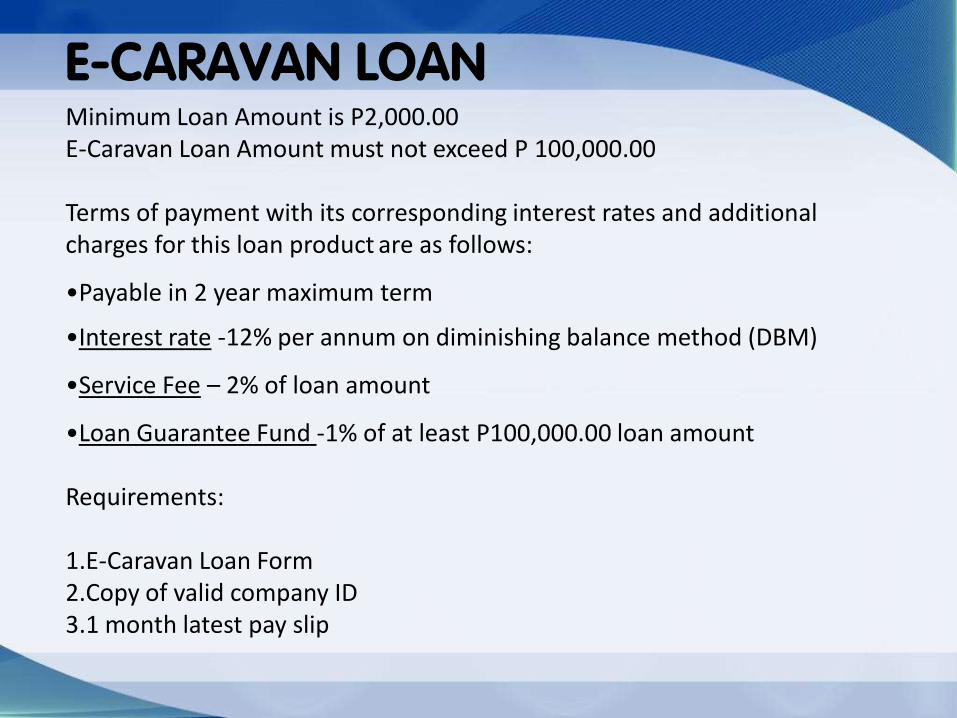

E-CARAVAN LOAN

E-CARAVAN LOAN Minimum Loan Amount is P2,000.00 E-Caravan Loan Amount must not exceed P 100,000.00 Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows:

•Payable in 2 year maximum term

•Interest rate -12% per annum on diminishing balance method (DBM)

•Service Fee – 2% of loan amount

•Loan Guarantee Fund -1% of at least P100,000.00 loan amount Requirements: 1.E-Caravan Loan Form 2.Copy of valid company ID 3.1 month latest pay slip

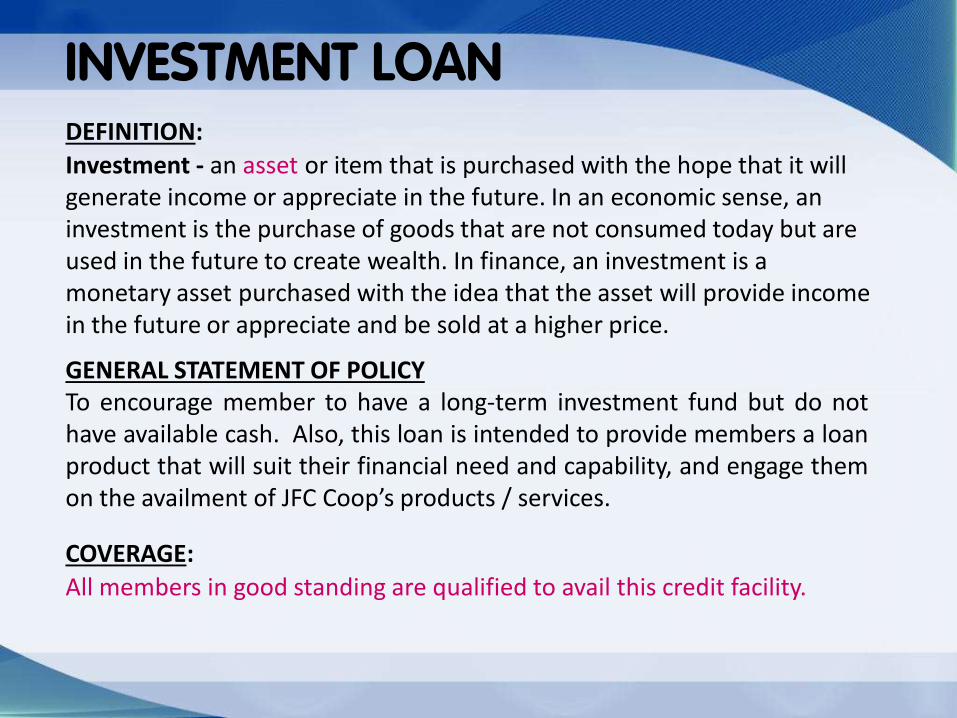

INVESTMENT LOAN DEFINITION: Investment - an asset or item that is purchased with the hope that it will generate income or appreciate in the future. In an economic sense, an investment is the purchase of goods that are not consumed today but are used in the future to create wealth. In finance, an investment is a monetary asset purchased with the idea that the asset will provide income in the future or appreciate and be sold at a higher price.

GENERAL STATEMENT OF POLICY To encourage member to have a long-term investment fund but do not have available cash. Also, this loan is intended to provide members a loan product that will suit their financial need and capability, and engage them on the availment of JFC Coop’s products / services.

COVERAGE: All members in good standing are qualified to avail this credit facility.

INVESTMENT LOAN

*JOLLIBEE/ DOUBLE DRAGON

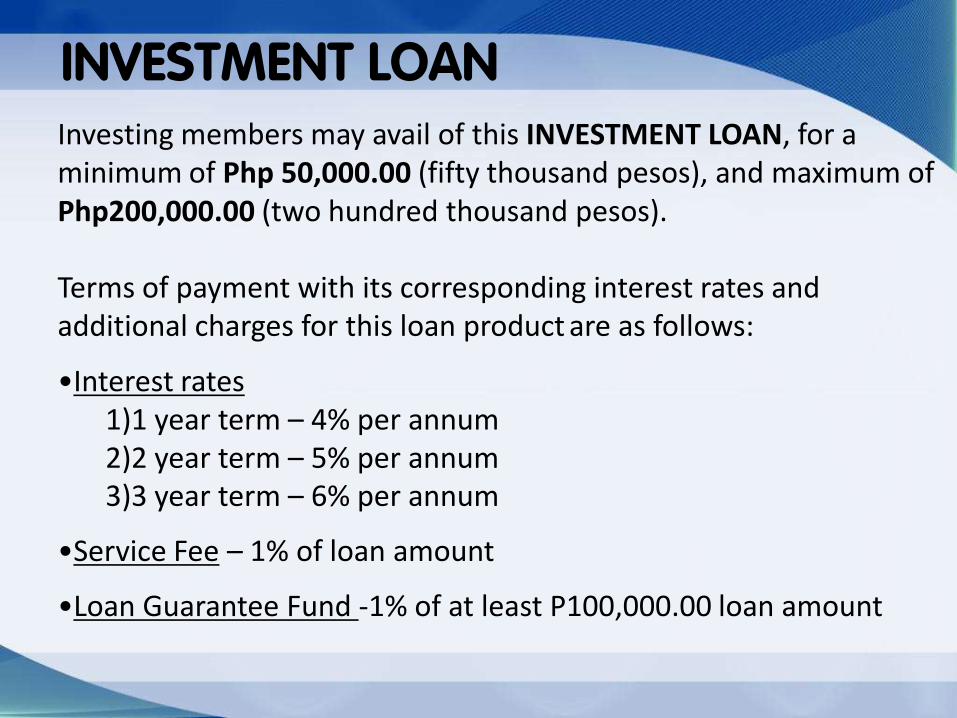

INVESTMENT LOAN Investing members may avail of this INVESTMENT LOAN, for a minimum of Php 50,000.00 (fifty thousand pesos), and maximum of Php200,000.00 (two hundred thousand pesos). Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows:

•Interest rates 1)1 year term – 4% per annum

2)2 year term – 5% per annum

3)3 year term – 6% per annum

•Service Fee – 1% of loan amount

•Loan Guarantee Fund -1% of at least P100,000.00 loan amount

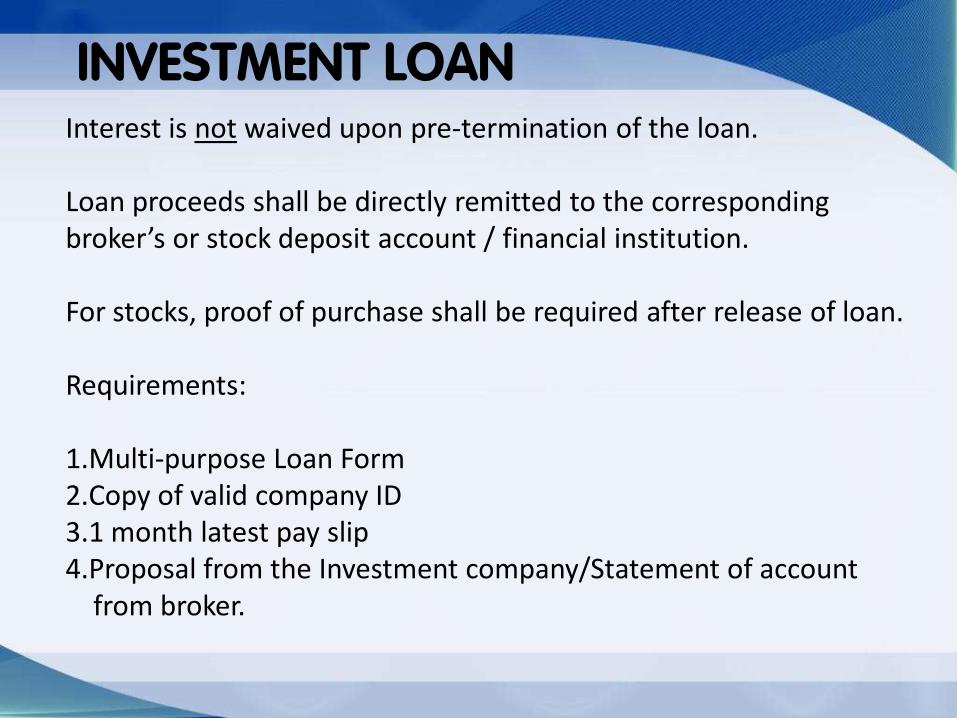

INVESTMENT LOAN Interest is not waived upon pre-termination of the loan. Loan proceeds shall be directly remitted to the corresponding broker’s or stock deposit account / financial institution. For stocks, proof of purchase shall be required after release of loan. Requirements: 1.Multi-purpose Loan Form 2.Copy of valid company ID 3.1 month latest pay slip 4.Proposal from the Investment company/Statement of account from broker.

CONSUMER LOAN

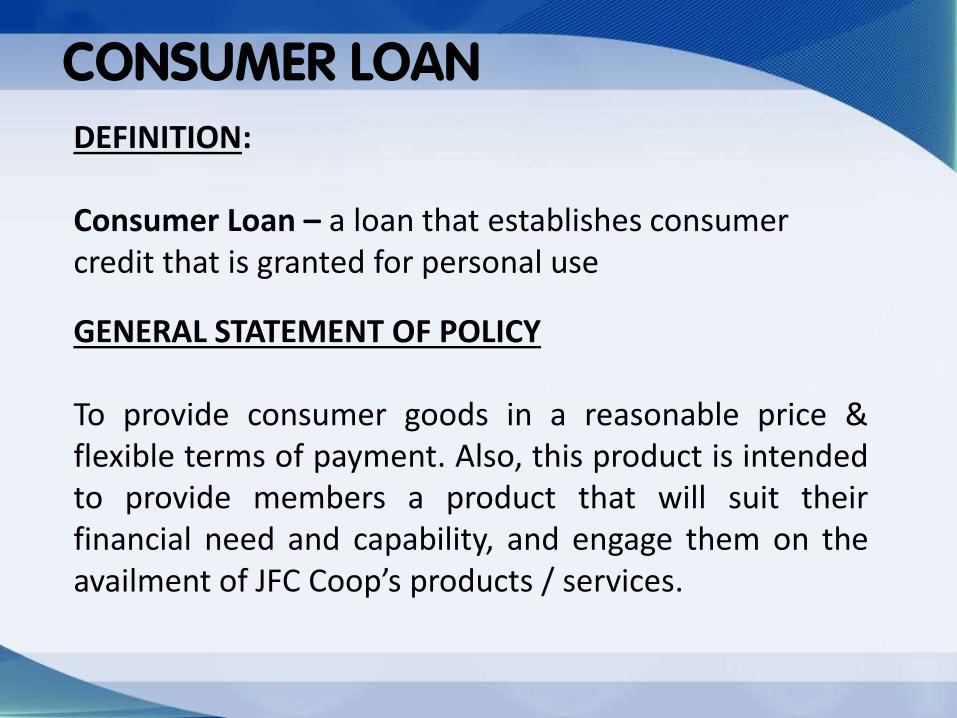

DEFINITION: Consumer Loan – a loan that establishes consumer credit that is granted for personal use

GENERAL STATEMENT OF POLICY To provide consumer goods in a reasonable price & flexible terms of payment. Also, this product is intended to provide members a product that will suit their financial need and capability, and engage them on the availment of JFC Coop’s products / services.

CONSUMER LOAN

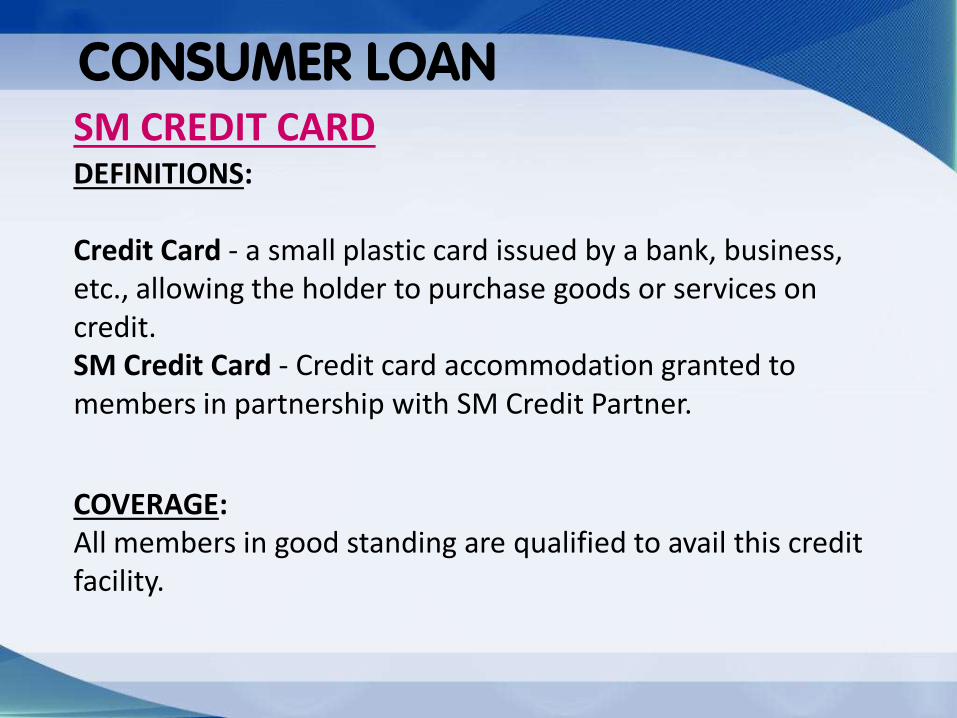

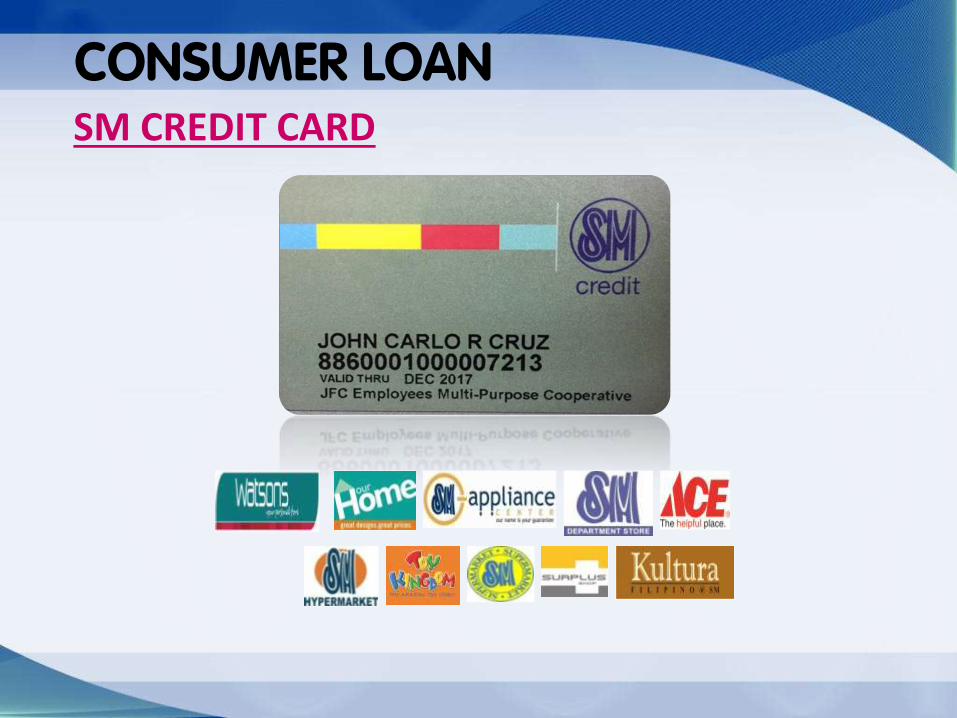

DEFINITIONS: Credit Card - a small plastic card issued by a bank, business, etc., allowing the holder to purchase goods or services on credit. SM Credit Card - Credit card accommodation granted to members in partnership with SM Credit Partner.

COVERAGE: All members in good standing are qualified to avail this credit facility.

SM CREDIT CARD

CONSUMER LOAN

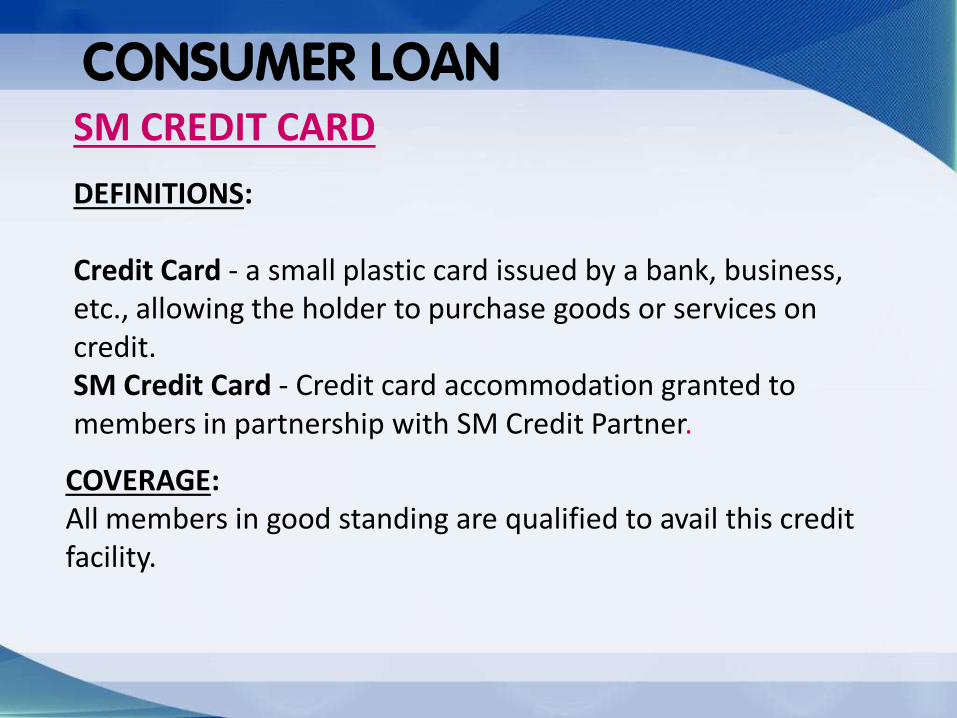

DEFINITIONS: Credit Card - a small plastic card issued by a bank, business, etc., allowing the holder to purchase goods or services on credit. SM Credit Card - Credit card accommodation granted to members in partnership with SM Credit Partner.

COVERAGE: All members in good standing are qualified to avail this credit facility.

SM CREDIT CARD

CONSUMER LOAN SM CREDIT CARD

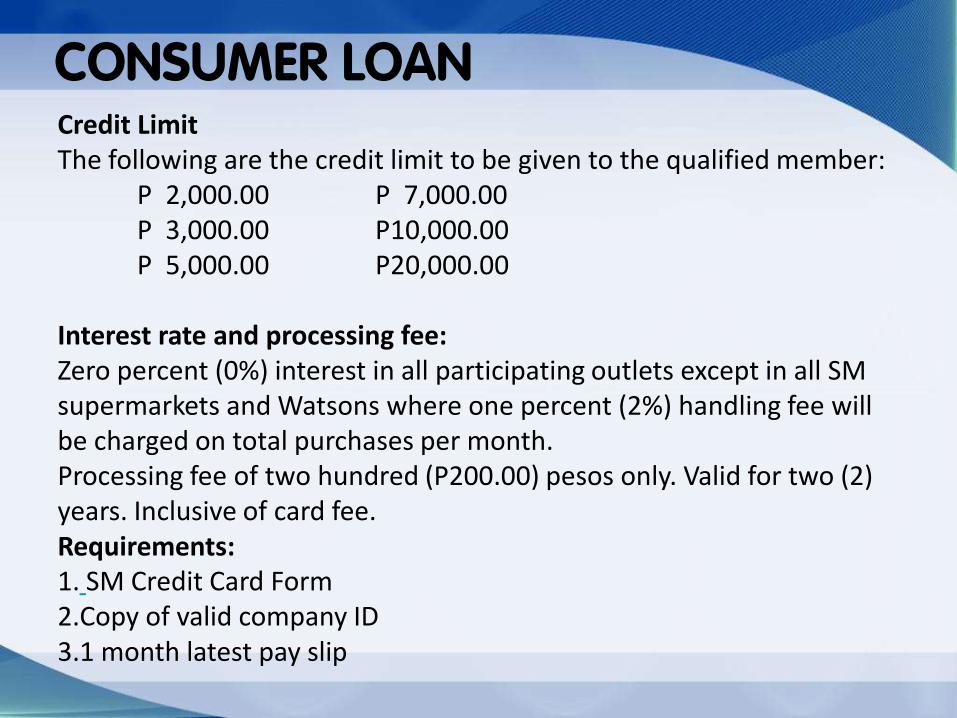

CONSUMER LOAN Credit Limit The following are the credit limit to be given to the qualified member: P 2,000.00 P 7,000.00 P 3,000.00 P10,000.00 P 5,000.00 P20,000.00 Interest rate and processing fee: Zero percent (0%) interest in all participating outlets except in all SM supermarkets and Watsons where one percent (2%) handling fee will be charged on total purchases per month. Processing fee of two hundred (P200.00) pesos only. Valid for two (2) years. Inclusive of card fee. Requirements: 1. SM Credit Card Form 2.Copy of valid company ID 3.1 month latest pay slip

CONSUMER LOAN

DEFINITIONS:

Surplus Sale – Selling activity of excess goods from Jollibee Foods Corporation Strategic Business Unit (SBU), Regional Business Unit (RBU) or Commissaries Surplus Items – Excess goods / items or some are near expiry or extended consume until but still fit for human consumption.

SURPLUS

COVERAGE: All members in good standing are qualified to purchase.

CONSUMER LOAN

CHRISTMAS HAM SALE

CONSUMER LOAN

Purchases Terms of payment

P99.00 below 1 time

P100.00 – P999.00 1 month

P1,000.00 above 2 months

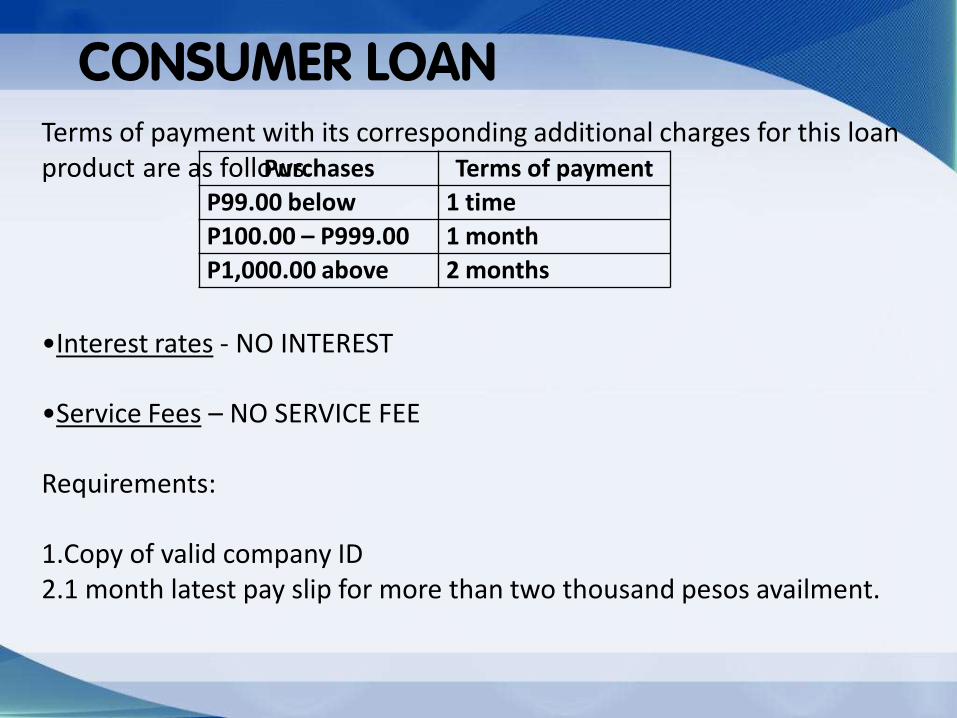

Terms of payment with its corresponding additional charges for this loan product are as follows:

•Interest rates - NO INTEREST

•Service Fees – NO SERVICE FEE Requirements: 1.Copy of valid company ID 2.1 month latest pay slip for more than two thousand pesos availment.

CONSUMER LOAN

MILNOMAR

PARTNER SUPPLIERS

PRE-NEED PRODUCTS DEFINITION: Pre-need – denoting a scheme in which one pays in advance for a service or facility.

GENERAL STATEMENT OF POLICY To cater the needs of members in preparation for the inevitable events. Also, this product is intended to provide members a product that will suit their financial need and capability, and engage them on the availment of JFC Coop’s products / services.

COVERAGE: All members in good standing are qualified to avail this pre-need product through cash or credit facility subject to certain conditions, provisions, and revisions as included in this manual.

PRE-NEED PRODUCTS

St. Peter Life Plan Inc. is a Pre-Need Death Care Company that offers affordable traditional memorial life plans to all segments of society. Since 1970, it has maintained its leadership and excelled in its role as Death Care Experts in the Death Care Services Industry through the continuous development of its wide range of memorial products and services attuned to the changing needs of Philippine society.

PRE-NEED PRODUCTS Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows: •Payable in five year term maximum •Interest rate - gain over terms. (Terms - contract price less total loan amount) •Service Fee – NO Service Fee

Requirements: 1. Fully filled out Life Plan and Insurance Loan Application Form 2. Fully filled out St. Peter Life Plan Application Form 3. Photocopy of valid company ID ( back to back ) 4. One-month latest pay slips

PRE-NEED PRODUCTS

St. Therese Columbarium – the first of its kind in the Philippines, a fully air conditioned columbarium, is a breath of fresh air to those who seek peace and privacy in the comfort of family and friends. The Columbarium is an elegant, practical and most ideal sanctuary for the interment of the ashes or bones of departed loved ones. It has a total of 36,000 vaults as a repository for the ashes of our departed loved ones. The vaults are a milestone in itself, made of imported aluminum, a first in the country.

PRE-NEED PRODUCTS

Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows: •Payable in two year term maximum •Interest rate - NO Interest •Service Fee – NO Service Fee

Requirements: 1. Fully filled out St. Therese Application Form 2. Fully filled out St. Therese Vault Changes Form 3. Photocopy of valid company ID ( back to back ) 4. One-month latest pay slips

ST. THERESE COLUMBARIUM

PRE-NEED PRODUCTS

Fire insurance - is a specialized form of insurance beyond property insurance, and is designed to cover the cost of replacement, reconstruction or repair beyond what is covered by the property insurance policy. Car insurance - is a policy purchased by vehicle owners to mitigate costs associated with getting into a car accident. Instead of paying out of pocket for auto accidents, people pay annual premiums to a car insurance company; the company then pays all or most of the costs associated with the car accident or other vehicle damage

PRE-NEED PRODUCTS

Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows: •Payable in six months term maximum •Interest rate - NO Interest •Service Fees – NO Service Fee

Requirements: 1. Car Insurance Application Form ( for quotation ) 2. Life Plan Insurance Form 3. Photocopy of valid company ID ( back to back ) 4. One-month latest pay slips 5. Photocopy of OR/CR

CAR INSURANCE

PRE-NEED PRODUCTS

Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows: •Payable in six months term maximum •Interest rate - NO Interest •Service Fee – NO Service Fee

Requirements: 1. Fire Insurance Application Form ( for quotation ) 2. Life Plan Insurance Form 3. Photocopy of valid company ID ( back to back ) 4. One-month latest pay slips

FIRE INSURANCE

PRE-NEED PRODUCTS

Health Maintenance Organization (HMO) is an organization that provides health coverage for a monthly or annual fee. A Health Maintenance Organization (HMO) is a group of medical insurance providers that limit coverage to medical aid provided from doctors that are under the contract of HMO.

HEALTH CARD

PRE-NEED PRODUCTS HEALTH CARD

PREVENTIVE EMERGENCY DENTAL

OUT - PATIENT CONFINEMENT FINANCIAL ASSISTANCE

PRE-NEED PRODUCTS HEALTH CARD

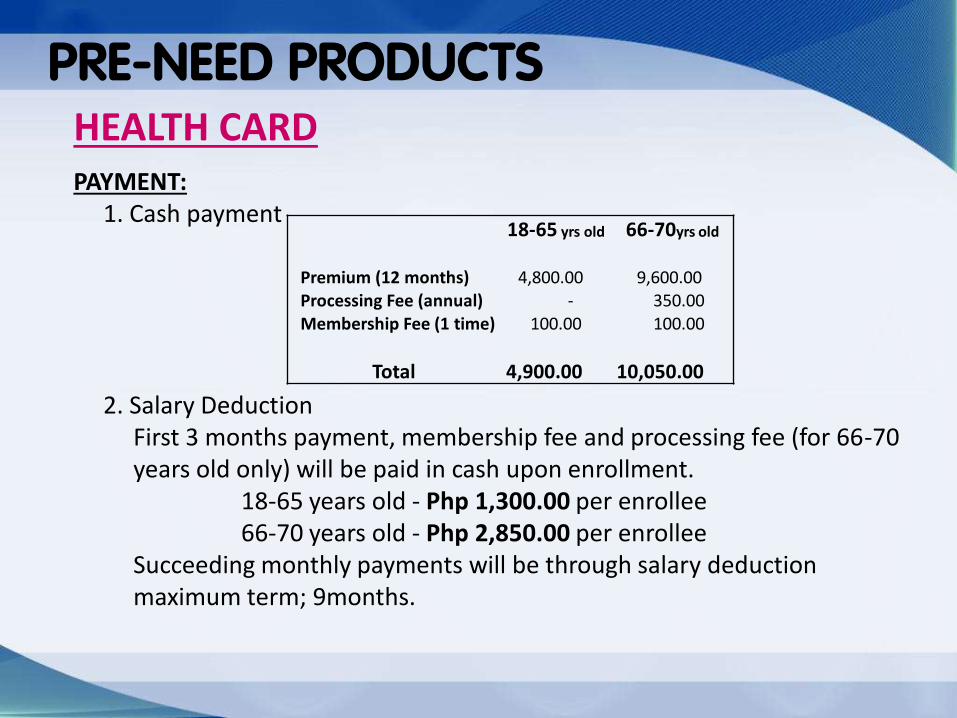

18-65 yrs old 66-70yrs old

Premium (12 months) 4,800.00 9,600.00 Processing Fee (annual) - 350.00 Membership Fee (1 time) 100.00 100.00

Total 4,900.00 10,050.00

PAYMENT: 1. Cash payment 2. Salary Deduction First 3 months payment, membership fee and processing fee (for 66-70 years old only) will be paid in cash upon enrollment. 18-65 years old - Php 1,300.00 per enrollee 66-70 years old - Php 2,850.00 per enrollee Succeeding monthly payments will be through salary deduction maximum term; 9months.

PRE-NEED PRODUCTS HEALTH CARD Payment can be made through:

1. Over the counter at JFC Coop office or 2. Direct deposit at Metrobank, account details as follows; Account Name: JFC COOP

Account Number: 630-363005396-0 *Payment verification: Validated deposit slip or copy of online transfer Requirements: 1. Carewell Application Form (filled-out and sign by the dependent) 2. Carewell Membership Form (filled-out and sign by the dependent and Coop member) 3. Copy of valid company ID (Coop Member) 4. Copy of any valid ID (Dependent)

REAL ESTATE LOAN DEFINITION: Real Estate - is property consisting of land and the buildings on it, along with its natural resources such as crops, minerals or water; immovable property of this nature; an interest vested in this (also) an item of real property; (more generally) buildings or housing in general. Also: the business of real estate; the profession of buying, selling, or renting land, buildings or housing.

COVERAGE: All members in good standing who intend to purchase of lot, house & Lot, condominium including parking slot owned by JFC Coop are qualified to avail this credit facility

REAL ESTATE LOAN

REAL ESTATE LOAN

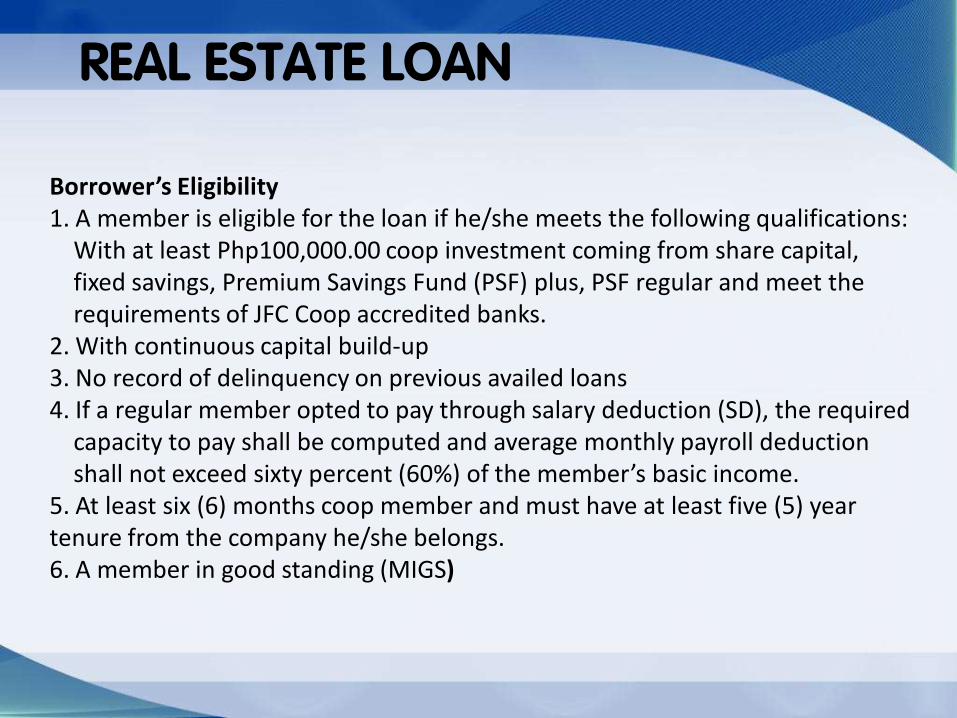

Borrower’s Eligibility 1. A member is eligible for the loan if he/she meets the following qualifications: With at least Php100,000.00 coop investment coming from share capital, fixed savings, Premium Savings Fund (PSF) plus, PSF regular and meet the requirements of JFC Coop accredited banks. 2. With continuous capital build-up 3. No record of delinquency on previous availed loans 4. If a regular member opted to pay through salary deduction (SD), the required capacity to pay shall be computed and average monthly payroll deduction shall not exceed sixty percent (60%) of the member’s basic income. 5. At least six (6) months coop member and must have at least five (5) year tenure from the company he/she belongs. 6. A member in good standing (MIGS)

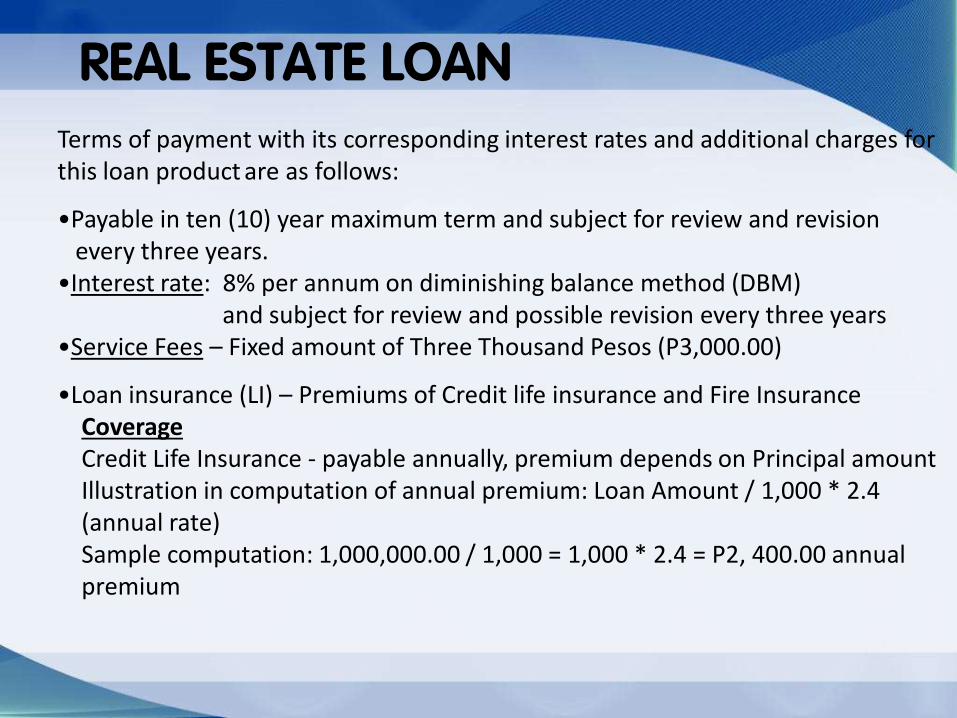

REAL ESTATE LOAN Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows:

•Payable in ten (10) year maximum term and subject for review and revision every three years. •Interest rate: 8% per annum on diminishing balance method (DBM)

and subject for review and possible revision every three years

•Service Fees – Fixed amount of Three Thousand Pesos (P3,000.00)

•Loan insurance (LI) – Premiums of Credit life insurance and Fire Insurance Coverage Credit Life Insurance - payable annually, premium depends on Principal amount Illustration in computation of annual premium: Loan Amount / 1,000 * 2.4 (annual rate) Sample computation: 1,000,000.00 / 1,000 = 1,000 * 2.4 = P2, 400.00 annual premium

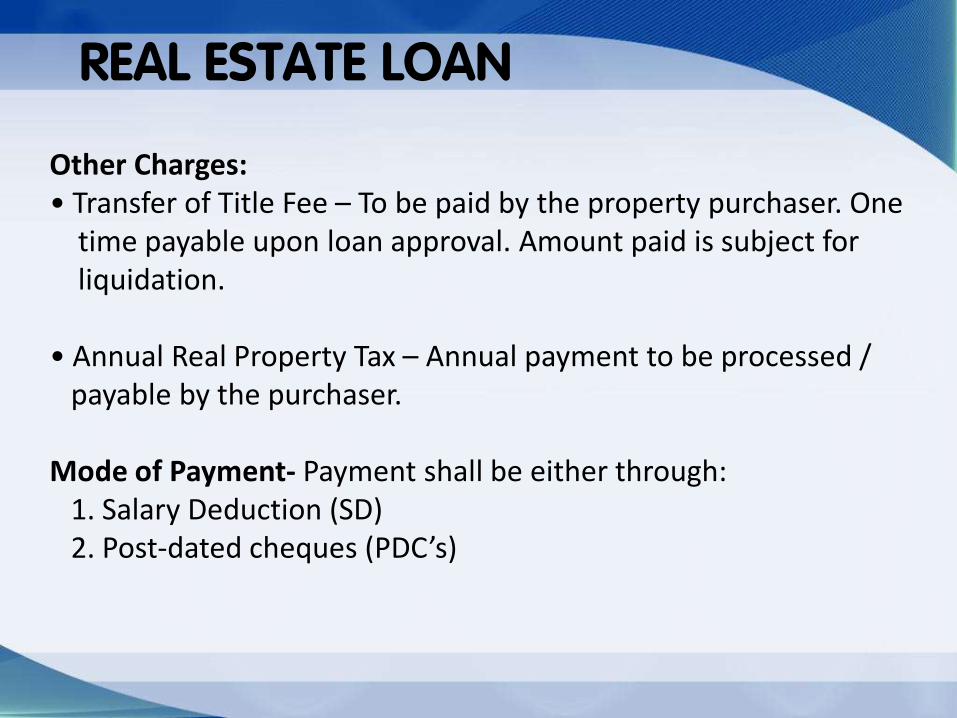

REAL ESTATE LOAN Other Charges: • Transfer of Title Fee – To be paid by the property purchaser. One time payable upon loan approval. Amount paid is subject for liquidation.

• Annual Real Property Tax – Annual payment to be processed / payable by the purchaser. Mode of Payment- Payment shall be either through: 1. Salary Deduction (SD) 2. Post-dated cheques (PDC’s)

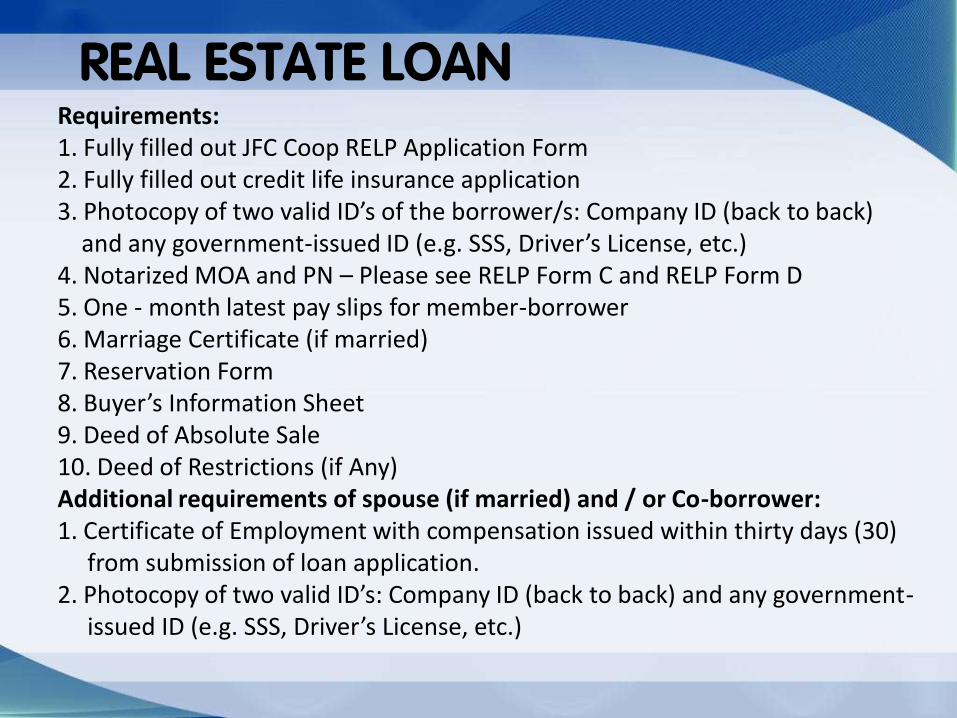

REAL ESTATE LOAN Requirements: 1. Fully filled out JFC Coop RELP Application Form 2. Fully filled out credit life insurance application 3. Photocopy of two valid ID’s of the borrower/s: Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.) 4. Notarized MOA and PN – Please see RELP Form C and RELP Form D 5. One - month latest pay slips for member-borrower 6. Marriage Certificate (if married) 7. Reservation Form 8. Buyer’s Information Sheet 9. Deed of Absolute Sale 10. Deed of Restrictions (if Any) Additional requirements of spouse (if married) and / or Co-borrower: 1. Certificate of Employment with compensation issued within thirty days (30) from submission of loan application. 2. Photocopy of two valid ID’s: Company ID (back to back) and any government- issued ID (e.g. SSS, Driver’s License, etc.)

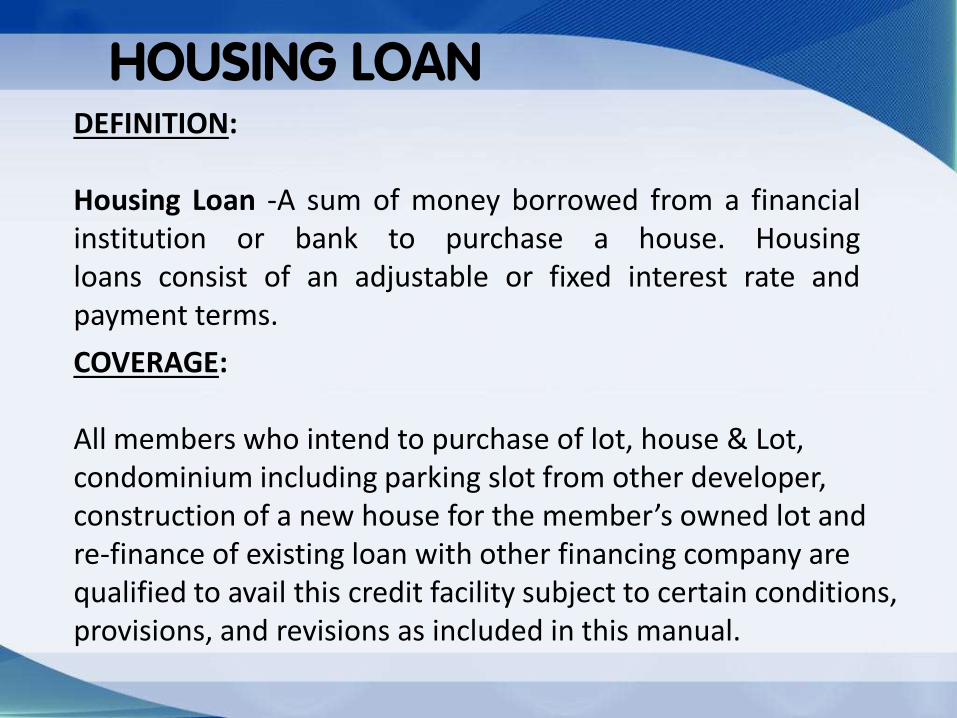

HOUSING LOAN DEFINITION: Housing Loan -A sum of money borrowed from a financial institution or bank to purchase a house. Housing loans consist of an adjustable or fixed interest rate and payment terms.

COVERAGE: All members who intend to purchase of lot, house & Lot, condominium including parking slot from other developer, construction of a new house for the member’s owned lot and re-finance of existing loan with other financing company are qualified to avail this credit facility subject to certain conditions, provisions, and revisions as included in this manual.

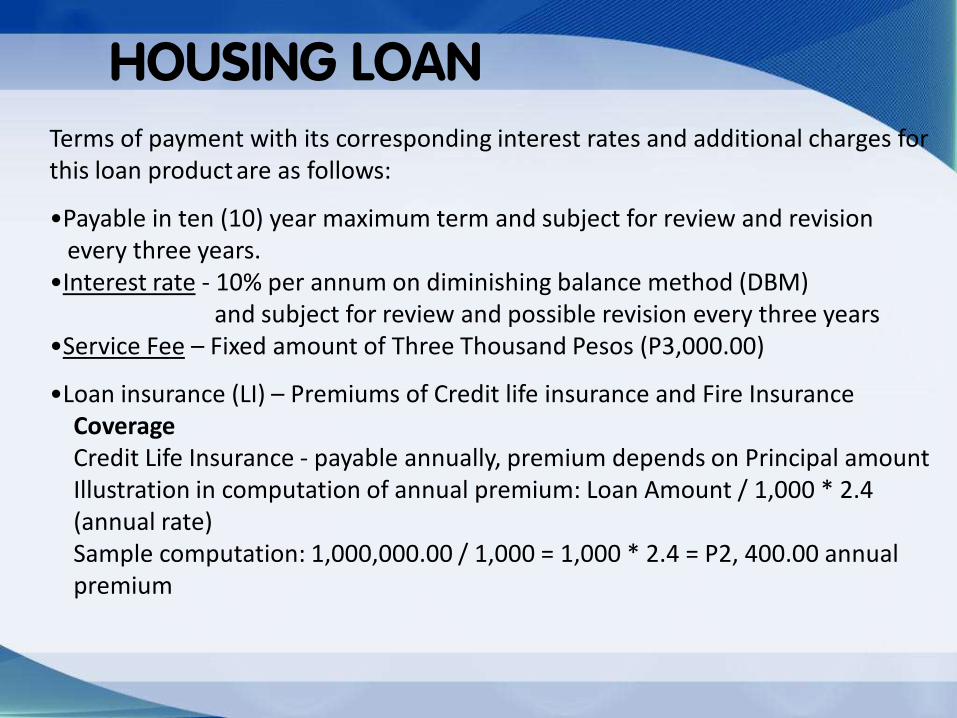

HOUSING LOAN Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows:

•Payable in ten (10) year maximum term and subject for review and revision every three years. •Interest rate - 10% per annum on diminishing balance method (DBM)

and subject for review and possible revision every three years •Service Fee – Fixed amount of Three Thousand Pesos (P3,000.00)

•Loan insurance (LI) – Premiums of Credit life insurance and Fire Insurance Coverage Credit Life Insurance - payable annually, premium depends on Principal amount Illustration in computation of annual premium: Loan Amount / 1,000 * 2.4 (annual rate) Sample computation: 1,000,000.00 / 1,000 = 1,000 * 2.4 = P2, 400.00 annual premium

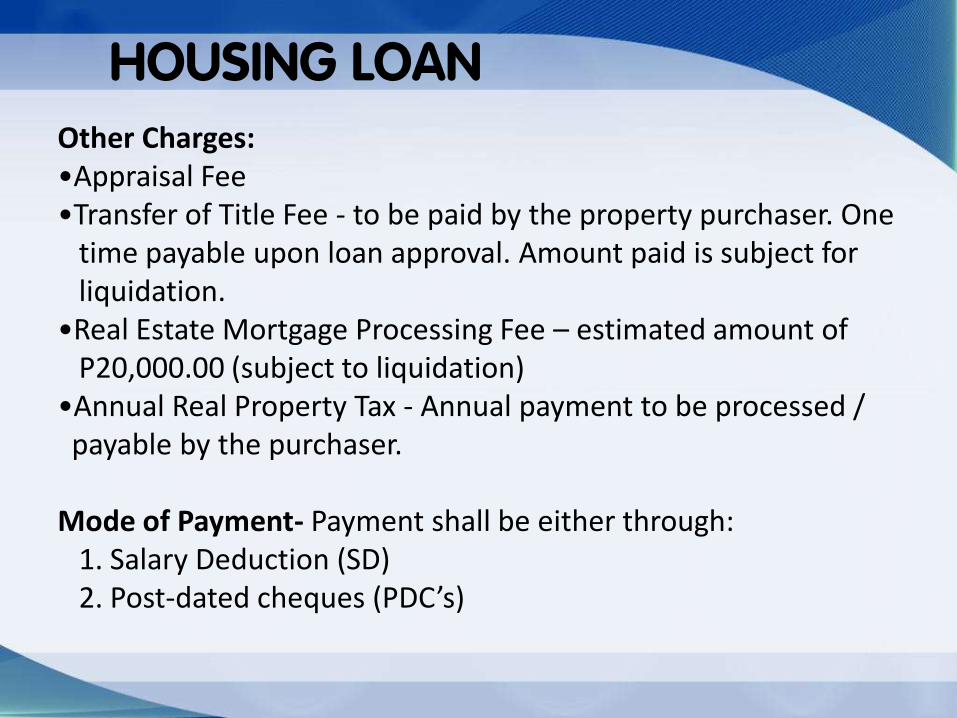

HOUSING LOAN Other Charges: •Appraisal Fee •Transfer of Title Fee - to be paid by the property purchaser. One time payable upon loan approval. Amount paid is subject for liquidation. •Real Estate Mortgage Processing Fee – estimated amount of P20,000.00 (subject to liquidation) •Annual Real Property Tax - Annual payment to be processed / payable by the purchaser. Mode of Payment- Payment shall be either through: 1. Salary Deduction (SD) 2. Post-dated cheques (PDC’s)

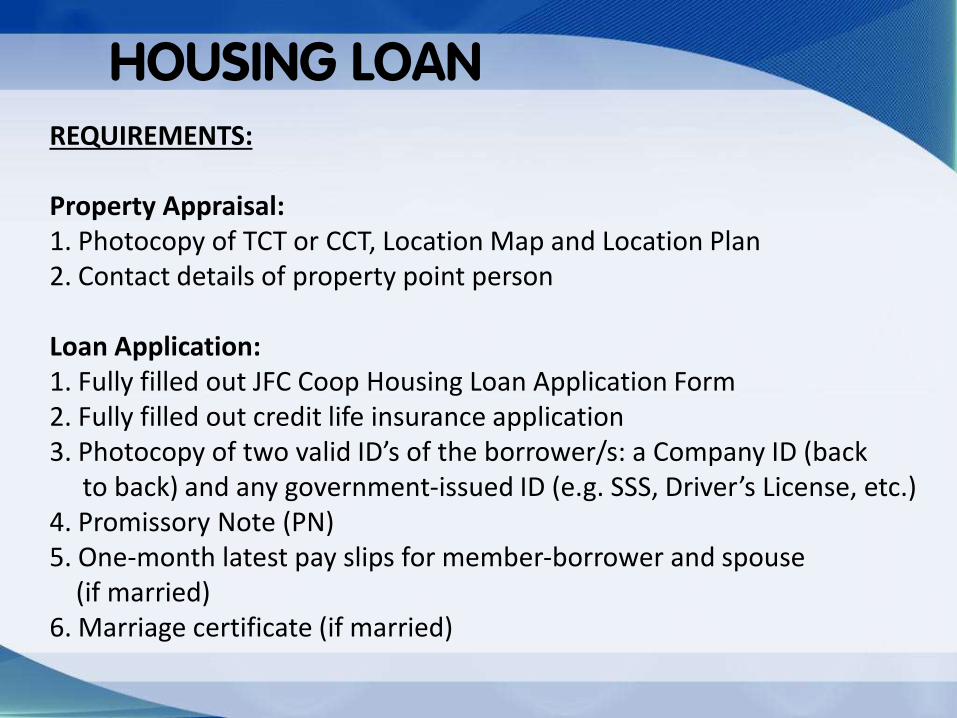

HOUSING LOAN REQUIREMENTS: Property Appraisal: 1. Photocopy of TCT or CCT, Location Map and Location Plan 2. Contact details of property point person Loan Application: 1. Fully filled out JFC Coop Housing Loan Application Form 2. Fully filled out credit life insurance application 3. Photocopy of two valid ID’s of the borrower/s: a Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.) 4. Promissory Note (PN) 5. One-month latest pay slips for member-borrower and spouse (if married) 6. Marriage certificate (if married)

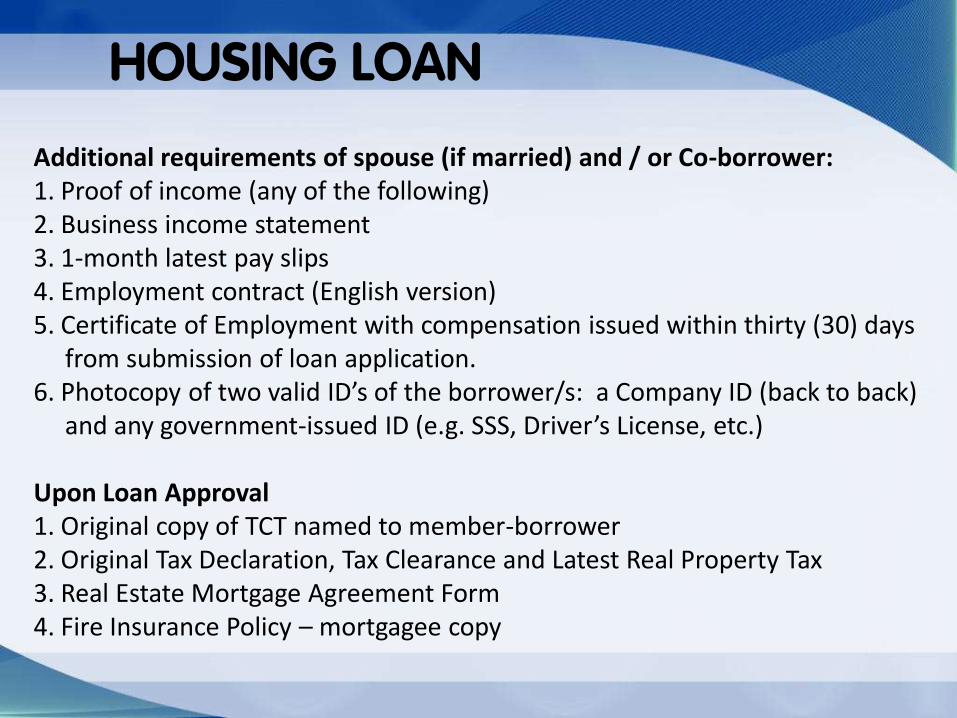

HOUSING LOAN Additional requirements of spouse (if married) and / or Co-borrower: 1. Proof of income (any of the following) 2. Business income statement 3. 1-month latest pay slips 4. Employment contract (English version) 5. Certificate of Employment with compensation issued within thirty (30) days from submission of loan application. 6. Photocopy of two valid ID’s of the borrower/s: a Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.) Upon Loan Approval 1. Original copy of TCT named to member-borrower 2. Original Tax Declaration, Tax Clearance and Latest Real Property Tax 3. Real Estate Mortgage Agreement Form 4. Fire Insurance Policy – mortgagee copy

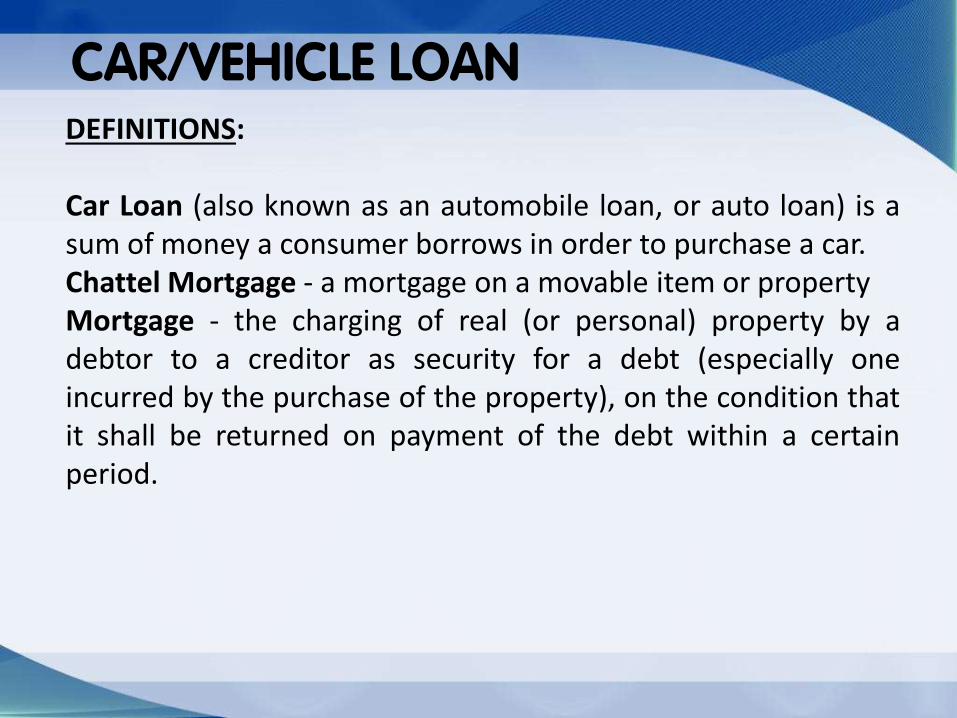

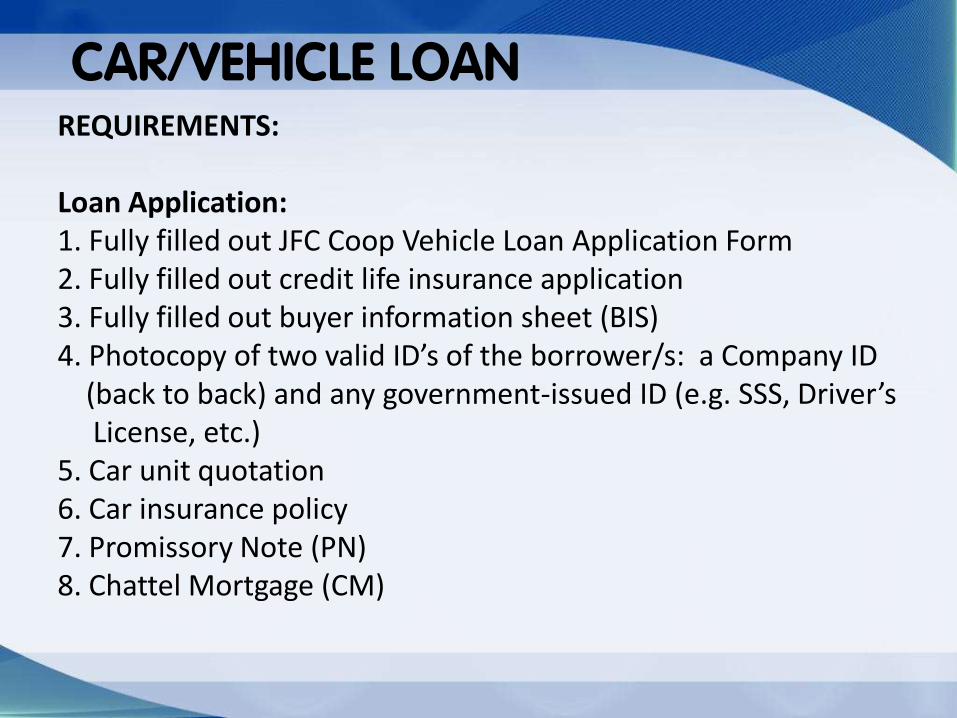

CAR/VEHICLE LOAN DEFINITIONS: Car Loan (also known as an automobile loan, or auto loan) is a sum of money a consumer borrows in order to purchase a car. Chattel Mortgage - a mortgage on a movable item or property Mortgage - the charging of real (or personal) property by a debtor to a creditor as security for a debt (especially one incurred by the purchase of the property), on the condition that it shall be returned on payment of the debt within a certain period.

CAR/VEHICLE LOAN

CAR/VEHICLE LOAN

Service Fee rate Loan amount bracket

P3,000.00 500,000.00 – 999,999.00

P4,000.00 1,000,000.00 – 1,999,999.00

P5,000.00 2,000,000.00 – 3,000,000.00

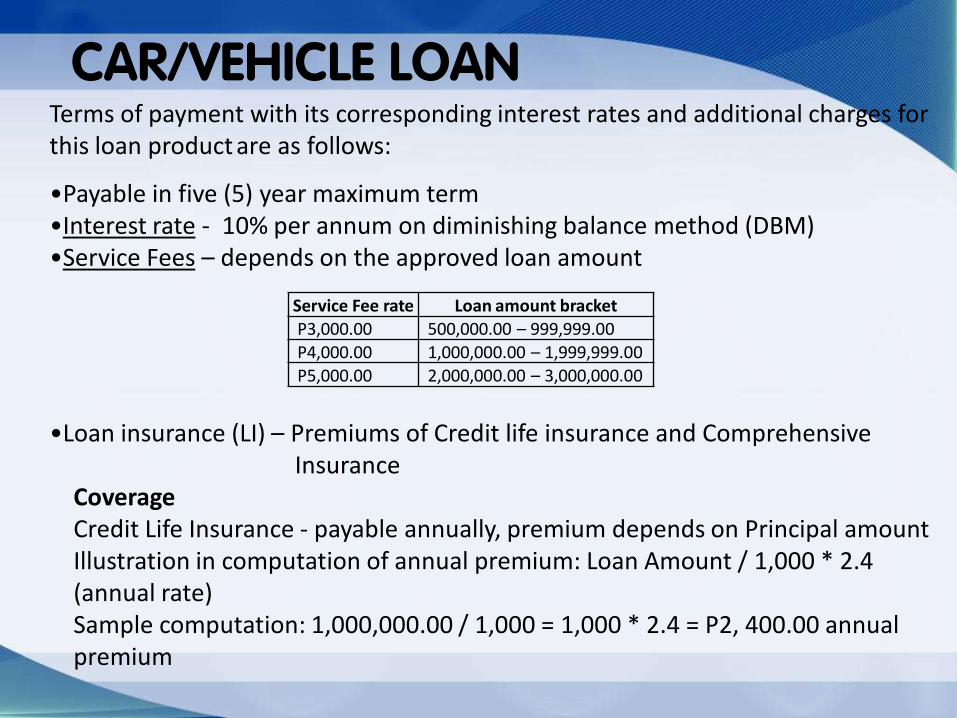

Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows:

•Payable in five (5) year maximum term •Interest rate - 10% per annum on diminishing balance method (DBM) •Service Fees – depends on the approved loan amount

•Loan insurance (LI) – Premiums of Credit life insurance and Comprehensive Insurance Coverage Credit Life Insurance - payable annually, premium depends on Principal amount Illustration in computation of annual premium: Loan Amount / 1,000 * 2.4 (annual rate) Sample computation: 1,000,000.00 / 1,000 = 1,000 * 2.4 = P2, 400.00 annual premium

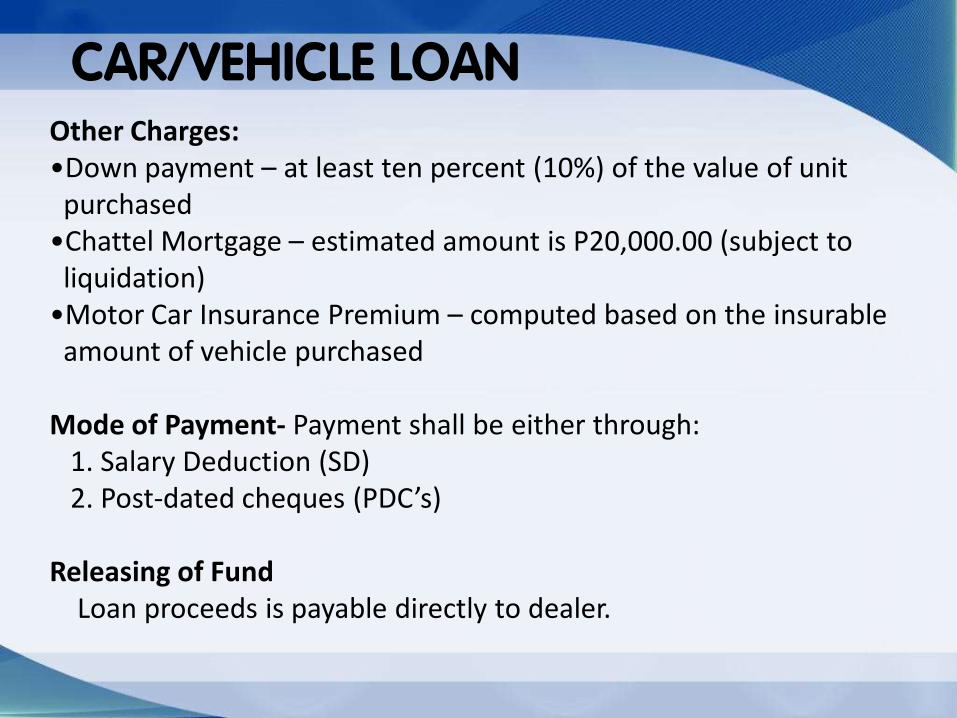

CAR/VEHICLE LOAN Other Charges: •Down payment – at least ten percent (10%) of the value of unit purchased •Chattel Mortgage – estimated amount is P20,000.00 (subject to liquidation) •Motor Car Insurance Premium – computed based on the insurable amount of vehicle purchased Mode of Payment- Payment shall be either through: 1. Salary Deduction (SD) 2. Post-dated cheques (PDC’s) Releasing of Fund Loan proceeds is payable directly to dealer.

CAR/VEHICLE LOAN REQUIREMENTS: Loan Application: 1. Fully filled out JFC Coop Vehicle Loan Application Form 2. Fully filled out credit life insurance application 3. Fully filled out buyer information sheet (BIS) 4. Photocopy of two valid ID’s of the borrower/s: a Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.) 5. Car unit quotation 6. Car insurance policy 7. Promissory Note (PN) 8. Chattel Mortgage (CM)

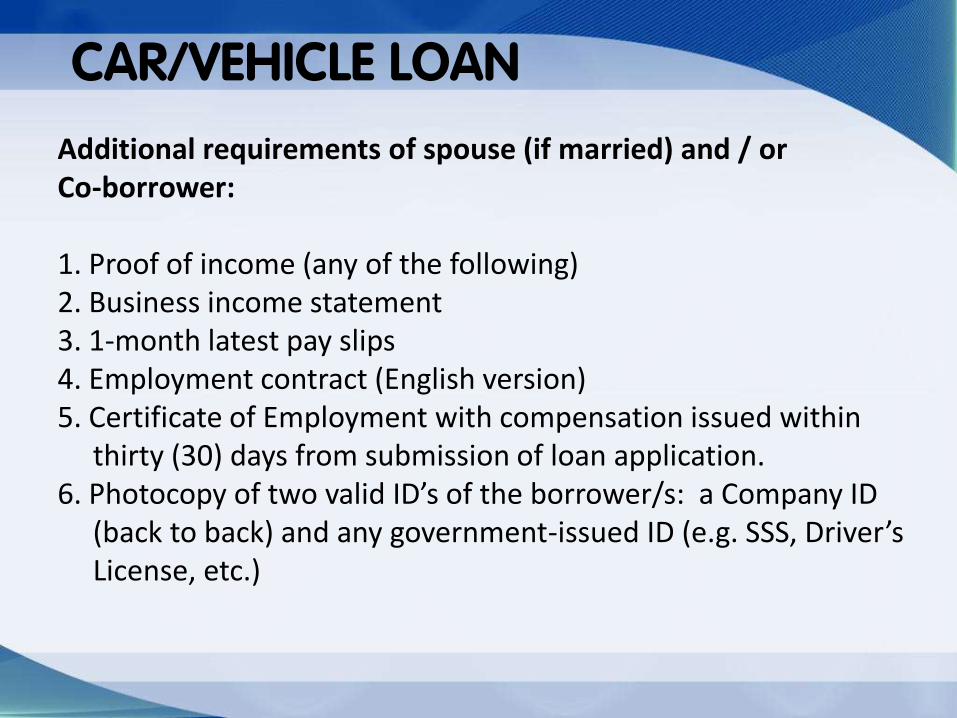

CAR/VEHICLE LOAN Additional requirements of spouse (if married) and / or Co-borrower: 1. Proof of income (any of the following) 2. Business income statement 3. 1-month latest pay slips 4. Employment contract (English version) 5. Certificate of Employment with compensation issued within thirty (30) days from submission of loan application. 6. Photocopy of two valid ID’s of the borrower/s: a Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.)

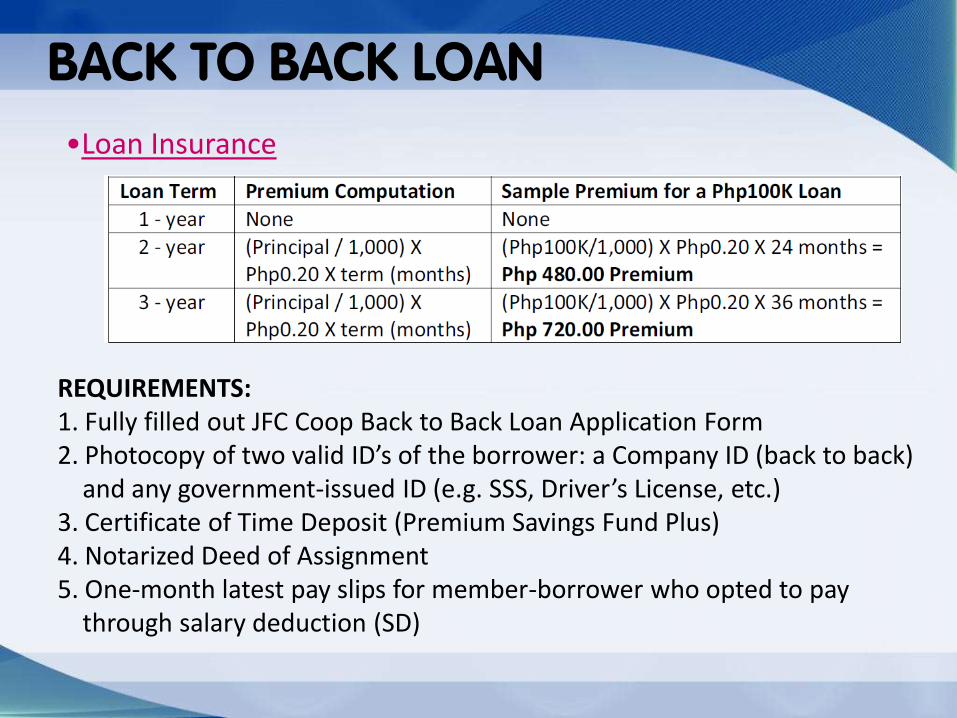

BACK TO BACK LOAN

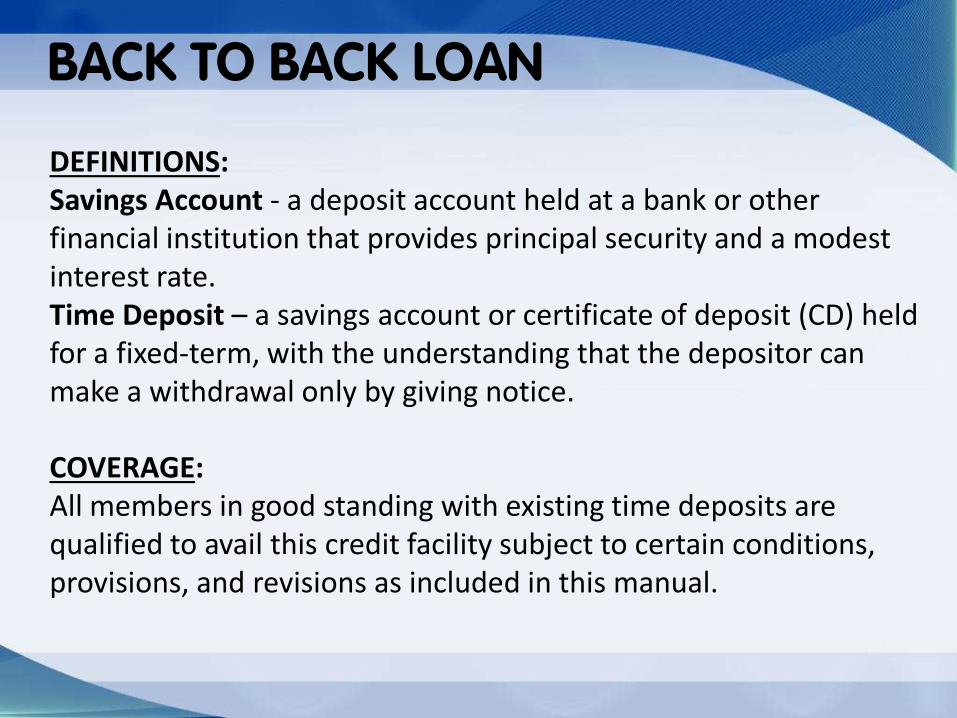

DEFINITIONS: Savings Account - a deposit account held at a bank or other financial institution that provides principal security and a modest interest rate. Time Deposit – a savings account or certificate of deposit (CD) held for a fixed-term, with the understanding that the depositor can make a withdrawal only by giving notice.

COVERAGE: All members in good standing with existing time deposits are qualified to avail this credit facility subject to certain conditions, provisions, and revisions as included in this manual.

BACK TO BACK LOAN

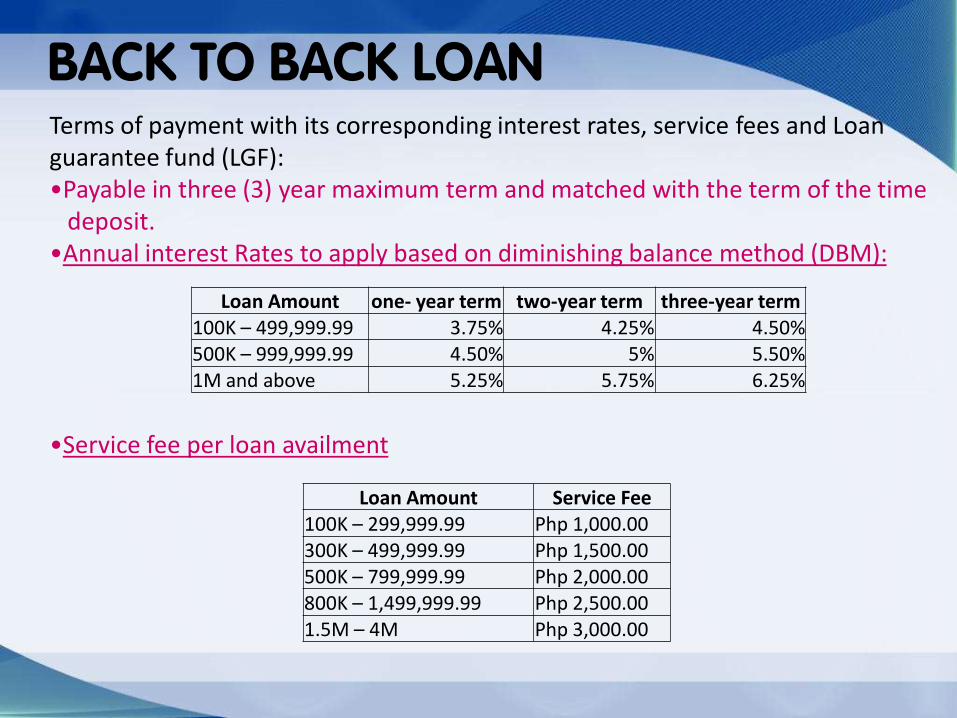

Loan Amount one- year term two-year term three-year term 100K – 499,999.99 3.75% 4.25% 4.50% 500K – 999,999.99 4.50% 5% 5.50% 1M and above 5.25% 5.75% 6.25%

Loan Amount Service Fee 100K – 299,999.99 Php 1,000.00 300K – 499,999.99 Php 1,500.00 500K – 799,999.99 Php 2,000.00 800K – 1,499,999.99 Php 2,500.00 1.5M – 4M Php 3,000.00

Terms of payment with its corresponding interest rates, service fees and Loan guarantee fund (LGF): •Payable in three (3) year maximum term and matched with the term of the time deposit. •Annual interest Rates to apply based on diminishing balance method (DBM):

•Service fee per loan availment

BACK TO BACK LOAN

•Loan Insurance

REQUIREMENTS: 1. Fully filled out JFC Coop Back to Back Loan Application Form 2. Photocopy of two valid ID’s of the borrower: a Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.) 3. Certificate of Time Deposit (Premium Savings Fund Plus) 4. Notarized Deed of Assignment 5. One-month latest pay slips for member-borrower who opted to pay through salary deduction (SD)

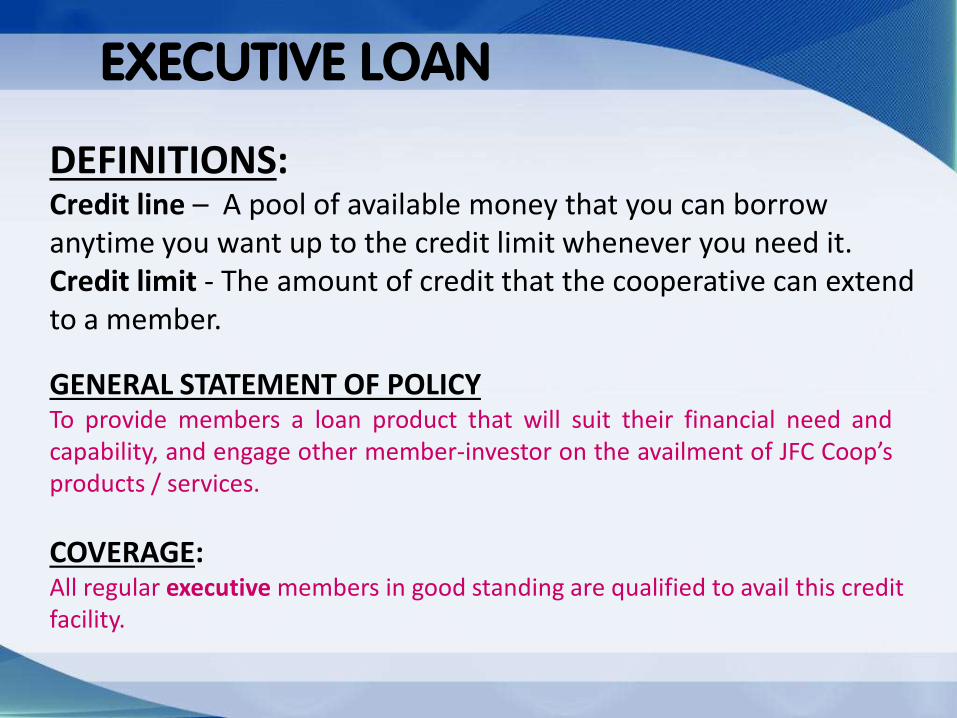

EXECUTIVE LOAN

DEFINITIONS: Credit line – A pool of available money that you can borrow anytime you want up to the credit limit whenever you need it. Credit limit - The amount of credit that the cooperative can extend to a member.

GENERAL STATEMENT OF POLICY To provide members a loan product that will suit their financial need and capability, and engage other member-investor on the availment of JFC Coop’s products / services.

COVERAGE: All regular executive members in good standing are qualified to avail this credit facility.

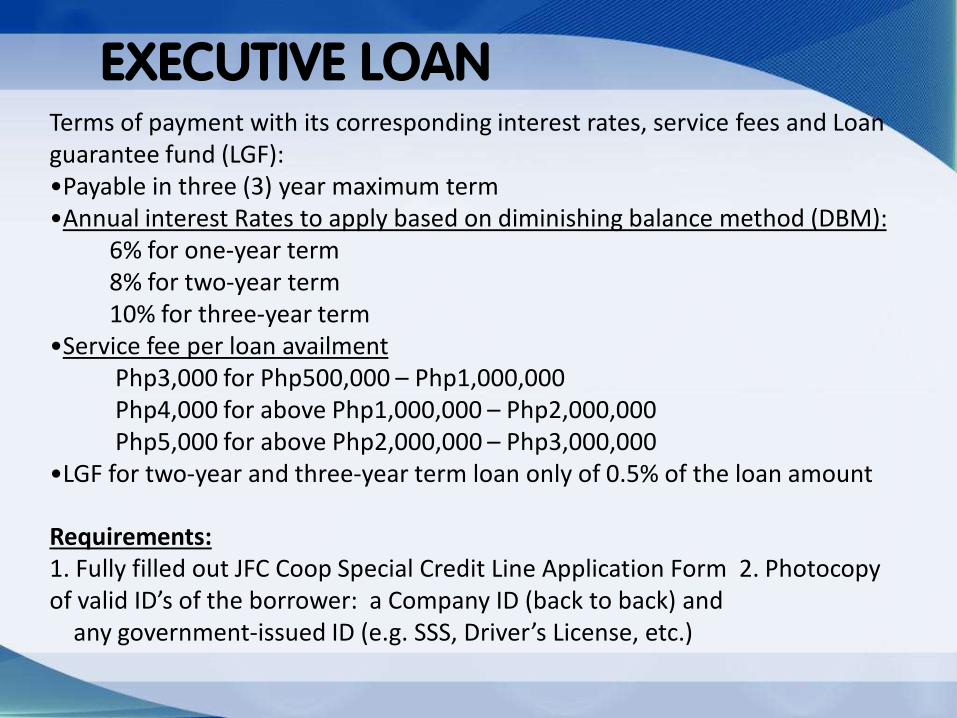

EXECUTIVE LOAN Terms of payment with its corresponding interest rates, service fees and Loan guarantee fund (LGF): •Payable in three (3) year maximum term •Annual interest Rates to apply based on diminishing balance method (DBM):

6% for one-year term 8% for two-year term 10% for three-year term

•Service fee per loan availment Php3,000 for Php500,000 – Php1,000,000 Php4,000 for above Php1,000,000 – Php2,000,000 Php5,000 for above Php2,000,000 – Php3,000,000

•LGF for two-year and three-year term loan only of 0.5% of the loan amount Requirements: 1. Fully filled out JFC Coop Special Credit Line Application Form 2. Photocopy of valid ID’s of the borrower: a Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.)

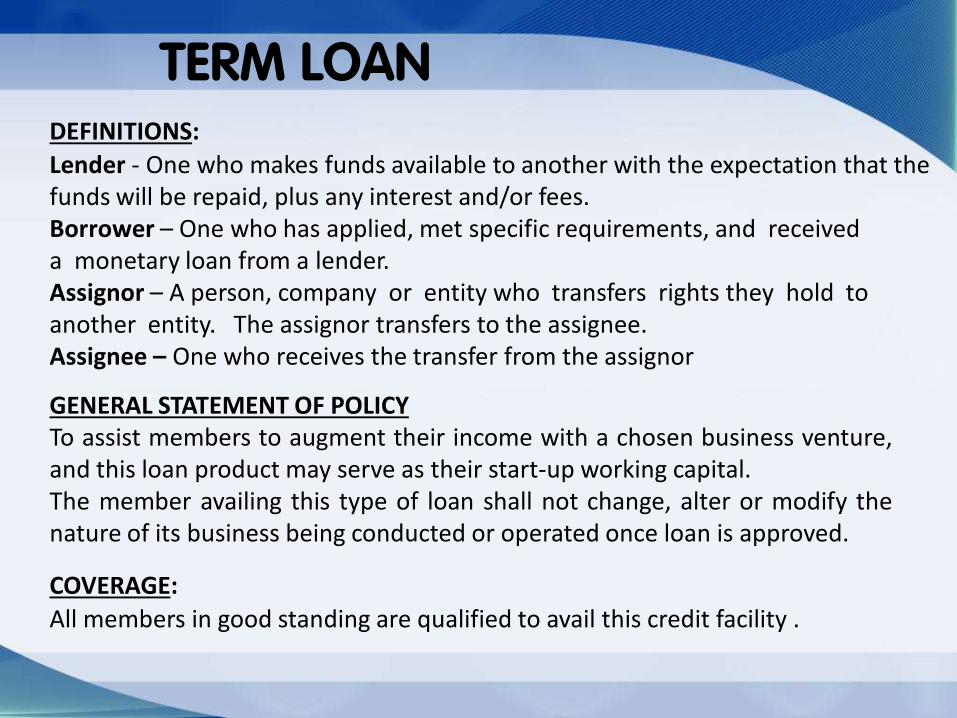

TERM LOAN DEFINITIONS: Lender - One who makes funds available to another with the expectation that the funds will be repaid, plus any interest and/or fees. Borrower – One who has applied, met specific requirements, and received a monetary loan from a lender. Assignor – A person, company or entity who transfers rights they hold to another entity. The assignor transfers to the assignee. Assignee – One who receives the transfer from the assignor

GENERAL STATEMENT OF POLICY To assist members to augment their income with a chosen business venture, and this loan product may serve as their start-up working capital. The member availing this type of loan shall not change, alter or modify the nature of its business being conducted or operated once loan is approved.

COVERAGE: All members in good standing are qualified to avail this credit facility .

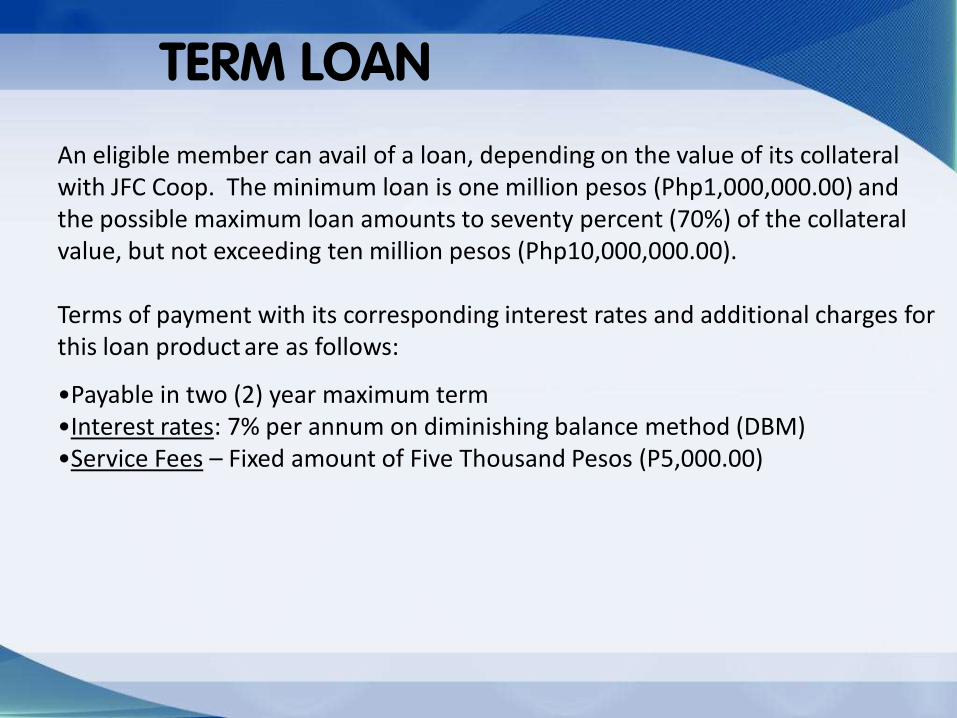

TERM LOAN

An eligible member can avail of a loan, depending on the value of its collateral with JFC Coop. The minimum loan is one million pesos (Php1,000,000.00) and the possible maximum loan amounts to seventy percent (70%) of the collateral value, but not exceeding ten million pesos (Php10,000,000.00). Terms of payment with its corresponding interest rates and additional charges for this loan product are as follows:

•Payable in two (2) year maximum term •Interest rates: 7% per annum on diminishing balance method (DBM) •Service Fees – Fixed amount of Five Thousand Pesos (P5,000.00)

TERM LOAN REQUIREMENTS: 1. Fully filled out JFC Coop Term Loan Application 2. Photocopy of two valid ID’s of the borrower: a Company ID (back to back) and any government-issued ID (e.g. SSS, Driver’s License, etc.) 3. Latest income tax return (ITR) 4. Latest bank statement/s 5. Notarized Promissory Note with Assignment of Receivables 6. For businesses entered in partnership or connected with Jollibee Group SBU, a photocopy of Contract with the SBU 7. For Member-Borrower applying as the owner, a copy of the registration of the company, and other related documents (e.g. business permits, etc.). 8. In case Member-Borrower is an authorized representative of a business entity, a copy of the notarized Board Resolution shall submitted together with the copy of the registration of the company, and other related documents (e.g. business permits, etc.)

MEMBER IN GOOD

STANDING

(MIGS)

The membership of JFC COOP is

open to all natural born Filipino citizen,

of legal age, employees of JFC or its

subsidiaries, affiliates or franchise, with

capacity to go into contract within the

common bond and field of

membership.

JFC COOP MEMBERSHIP

version 2.0: change in rating

scale

TYPES OF MEMBERSHIP

version 2.0: change in rating

scale

There are two (2) types of membership in the

Cooperative and are as follows:

• Regular Member – one who has complied with all

the membership requirements and entitled to all the

rights and privileges of membership.

•Associate Member – one who has no right to vote

or to be voted upon and shall only be entitled only to

such right and privileges as the

by-laws may provide.

IMPORTANCE OF MIGS

As written in our by-laws, under

ARTICLE 2, SECTION 7

It is primarily part of our DUTIES

and RESPONSIBILITIES as

Member / Owner of the

Cooperative.

version 2.0: change in rating

scale

DUTIES & REPONSIBILITIES

version 2.0: change in rating

scale

1. Pay the installment of his share capital as it falls

due and to participate in the capital build-up and

savings mobilization activities of the Cooperative.

2. Patronize Coop’s businesses and services.

3. Participate in the membership education

programs.

4. Attend and participate in the deliberation of all

matters taken during general assembly meetings.

5. Observe and obey all lawful orders,

discussions, rules and regulations adopted by

the BOD & the General Assembly.

6. Promote the purposes and goals of the

Cooperative, the success of its business, the

welfare of its members and the cooperative

movement in general.

version 2.0: change in rating

scale

DUTIES & REPONSIBILITIES

As a rule, all members must be

classified as MIGS or member in

good standing to be able to enjoy

the rights and privileges of being a

JFC Coop member – regardless of

membership type.

MEMBER IN GOOD STANDING

version 2.0: change in rating

scale

MIGS : REQUIREMENTS TO

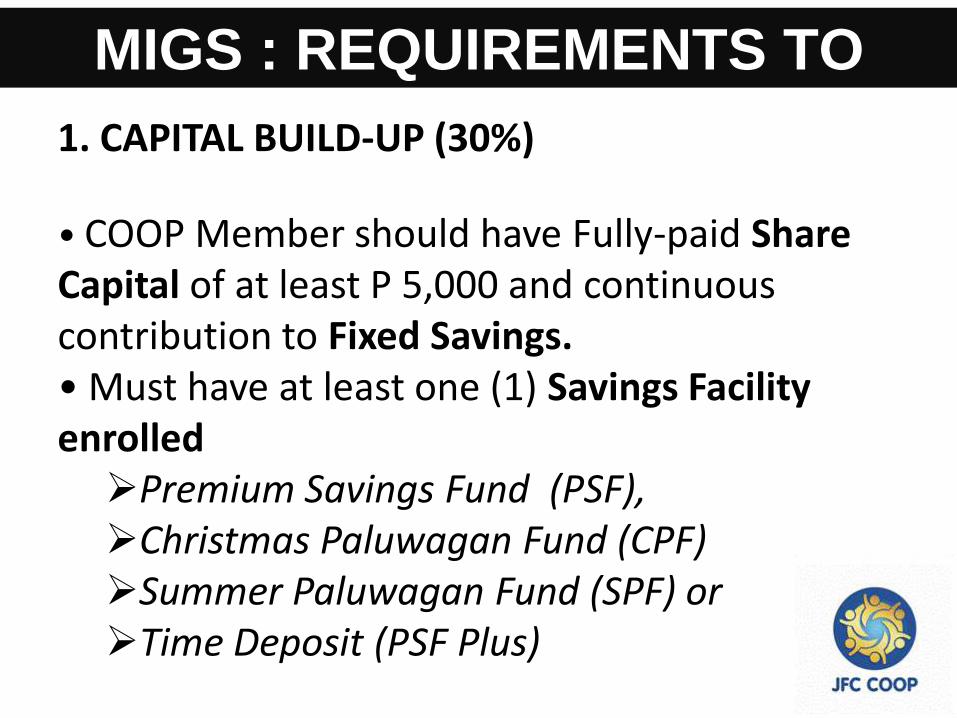

QUALIFY 1. CAPITAL BUILD-UP (30%)

• COOP Member should have Fully-paid Share Capital of at least P 5,000 and continuous contribution to Fixed Savings. • Must have at least one (1) Savings Facility enrolled Premium Savings Fund (PSF), Christmas Paluwagan Fund (CPF) Summer Paluwagan Fund (SPF) or Time Deposit (PSF Plus)

MIGS : REQUIREMENTS TO

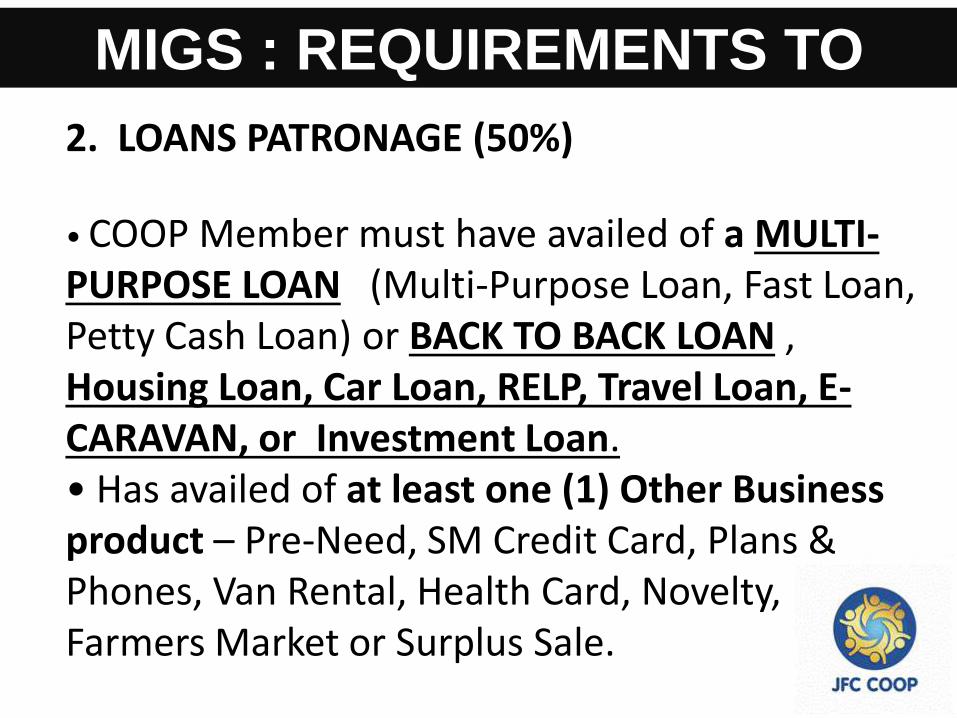

QUALIFY 2. LOANS PATRONAGE (50%)

• COOP Member must have availed of a MULTI-PURPOSE LOAN (Multi-Purpose Loan, Fast Loan, Petty Cash Loan) or BACK TO BACK LOAN , Housing Loan, Car Loan, RELP, Travel Loan, E-CARAVAN, or Investment Loan. • Has availed of at least one (1) Other Business product – Pre-Need, SM Credit Card, Plans & Phones, Van Rental, Health Card, Novelty, Farmers Market or Surplus Sale.

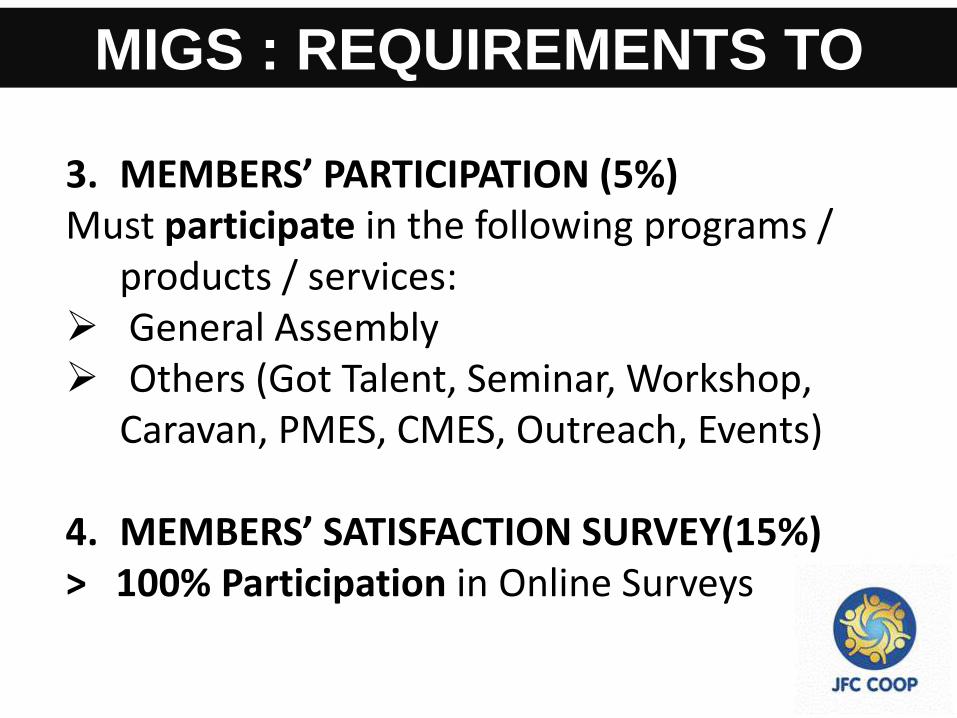

MIGS : REQUIREMENTS TO

QUALIFY 3. MEMBERS’ PARTICIPATION (5%) Must participate in the following programs /

products / services: General Assembly Others (Got Talent, Seminar, Workshop,

Caravan, PMES, CMES, Outreach, Events) 4. MEMBERS’ SATISFACTION SURVEY(15%) > 100% Participation in Online Surveys

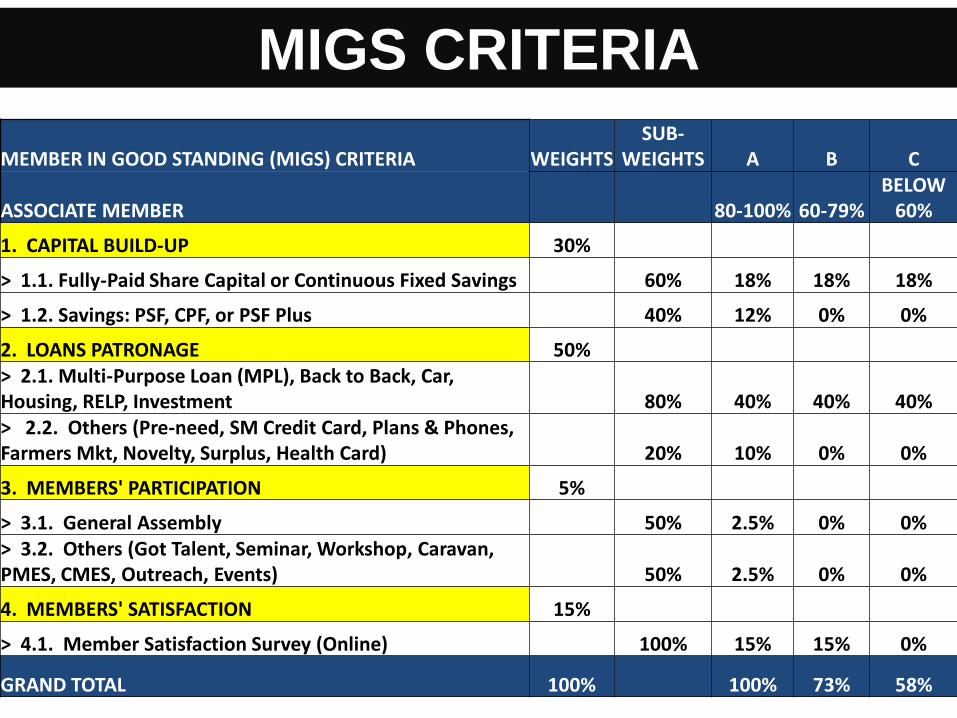

MEMBER IN GOOD STANDING (MIGS) CRITERIA WEIGHTS SUB-

WEIGHTS A B C

ASSOCIATE MEMBER 80-100% 60-79% BELOW

60%

1. CAPITAL BUILD-UP 30%

> 1.1. Fully-Paid Share Capital or Continuous Fixed Savings 60% 18% 18% 18%

> 1.2. Savings: PSF, CPF, or PSF Plus 40% 12% 0% 0%

2. LOANS PATRONAGE 50% > 2.1. Multi-Purpose Loan (MPL), Back to Back, Car, Housing, RELP, Investment 80% 40% 40% 40% > 2.2. Others (Pre-need, SM Credit Card, Plans & Phones, Farmers Mkt, Novelty, Surplus, Health Card) 20% 10% 0% 0%

3. MEMBERS' PARTICIPATION 5%

> 3.1. General Assembly 50% 2.5% 0% 0% > 3.2. Others (Got Talent, Seminar, Workshop, Caravan, PMES, CMES, Outreach, Events) 50% 2.5% 0% 0%

4. MEMBERS' SATISFACTION 15%

> 4.1. Member Satisfaction Survey (Online) 100% 15% 15% 0%

GRAND TOTAL 100% 100% 73% 58%

MIGS CRITERIA

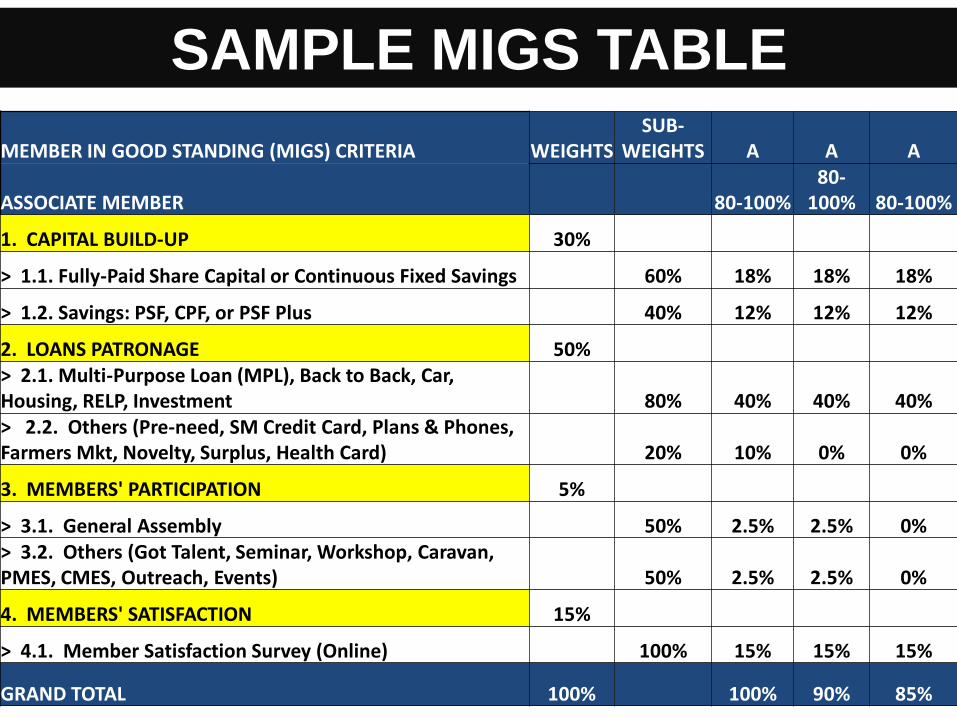

SAMPLE MIGS TABLE

MEMBER IN GOOD STANDING (MIGS) CRITERIA WEIGHTS SUB-

WEIGHTS A A A

ASSOCIATE MEMBER 80-100% 80-

100% 80-100%

1. CAPITAL BUILD-UP 30%

> 1.1. Fully-Paid Share Capital or Continuous Fixed Savings 60% 18% 18% 18%

> 1.2. Savings: PSF, CPF, or PSF Plus 40% 12% 12% 12%

2. LOANS PATRONAGE 50% > 2.1. Multi-Purpose Loan (MPL), Back to Back, Car, Housing, RELP, Investment 80% 40% 40% 40% > 2.2. Others (Pre-need, SM Credit Card, Plans & Phones, Farmers Mkt, Novelty, Surplus, Health Card) 20% 10% 0% 0%

3. MEMBERS' PARTICIPATION 5%

> 3.1. General Assembly 50% 2.5% 2.5% 0% > 3.2. Others (Got Talent, Seminar, Workshop, Caravan, PMES, CMES, Outreach, Events) 50% 2.5% 2.5% 0%

4. MEMBERS' SATISFACTION 15%

> 4.1. Member Satisfaction Survey (Online) 100% 15% 15% 15%

GRAND TOTAL 100% 100% 90% 85%

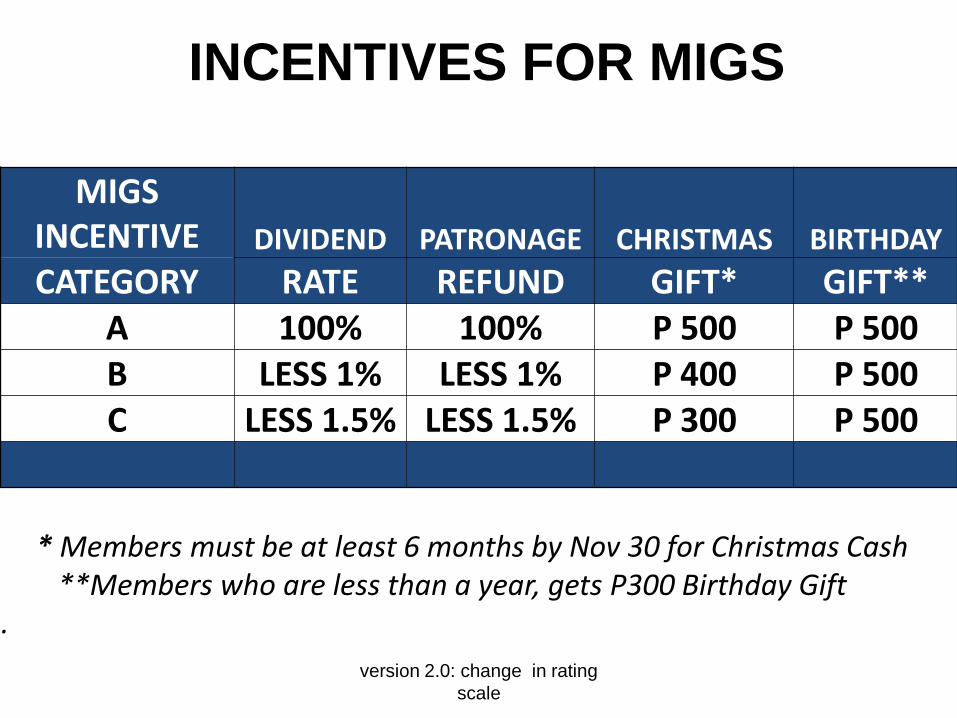

INCENTIVES FOR MIGS

MIGS INCENTIVE DIVIDEND PATRONAGE CHRISTMAS BIRTHDAY

CATEGORY RATE REFUND GIFT* GIFT** A 100% 100% P 500 P 500 B LESS 1% LESS 1% P 400 P 500 C LESS 1.5% LESS 1.5% P 300 P 500

* Members must be at least 6 months by Nov 30 for Christmas Cash **Members who are less than a year, gets P300 Birthday Gift .

version 2.0: change in rating

scale

Credit and Collection

Submission of remittance summary and copy of validated deposit slip : Every 07th and 22nd of the month Thru:

• Fax # 638-5962 •E-mail to : [email protected] cc: [email protected]

•HRD & Membership •Admin •Finance

•Loans & marketing • New Business • Surplus / Sales

THANK YOU

version 2.0: change in rating

scale