j.p. morgan iraq and mena trade forum monday 24 september presentation

TRANSCRIPT

Middle East and North Africa Trade Forum

Sunday 23 – Tuesday 25 September, 2012

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

This presentation was prepared exclusively for the benefit and internal use of the J.P. Morgan client to whom it is directly addressed and delivered including such client’s subsidiaries,

(the “Company”) in order to assist the Company in evaluating, on a preliminary basis, certain products or services that may be provided by J.P. Morgan. This presentation is for

discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by J.P. Morgan. It may not be copied,

published or used, in whole or in part, for any purpose other than as expressly authorised by J.P. Morgan.

The statements in this presentation are confidential and proprietary to J.P. Morgan and are not intended to be legally binding. Neither J.P. Morgan nor any of its directors, officers,

employees or agents shall incur any responsibility or liability to the Company or any other party with respect to the contents of this presentation or any matters referred to in, or

discussed as a result of, this document. J.P. Morgan makes no representations as to the legal, regulatory, tax or accounting implications of the matters referred to in this presentation.

IRS Circular 230 Disclosure: JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any

attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone not affiliated with JPMorgan Chase &

Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

J.P. Morgan is a marketing name for the treasury services businesses of JPMorgan Chase Bank, N.A. and its subsidiaries worldwide. In the United Kingdom, JPMorgan Chase Bank,

N.A., London branch and J.P. Morgan Europe Limited are authorised and regulated by the Financial Services Authority

JPMorgan Chase is licensed under US patent numbers 5, 910,988, and 6, 032 and 137

©2012 JPMorgan Chase & Co. All rights reserved.

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Asif Raza

Head of Treasury and Securities Services,

Middle East and North Africa, J.P. Morgan

W E L C O M E R E M A R K S

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Agenda

Monday September 24

09:15 Welcome Refreshments

09:45 Welcome Remarks

Asif Raza, Head of Treasury and Securities Services, Middle East and North Africa, J.P. Morgan

10:00 Changing Paradigms of Trade and Currency Settlement Patterns

Examination of the regional market landscape with identification and analysis of key growth areas and emerging

economies allows capitalization of the trade corridors between MENA and Asia and the growing use of RMB as a

trade settlement currency.

Sonam Kapadia, Global Trade, Middle East and North Africa, J.P. Morgan

11:00 Refreshments

11:30 The Product Landscape in a Growing Trade Environment

To accommodate the growing trade patterns the product landscape is simultaneously increasing it’s range

and scope of offerings. Analyzing the importance of the Cash Conversion Cycle is a vital exercise when choosing

Documentary Credit and Supply Chain.

Amr El Haddad, Global Trade Product, Middle East and North Africa, J.P. Morgan

12:15 Compliance

Evaluating compliance issues specifically encountered in the MENA region and how we can work in this

context to better understand and identify the needs of our clients.

Ian Lyall, Compliance, Europe Middle East and Africa, J.P. Morgan

13:15 Lunch

Al Saraya Restaurant

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Agenda

14:15 Credit Risk Management in a Challenging Environment

Managing credit risk requires in depth analysis of the current challenging environment

Florence Coronel, Risk, Europe, Middle East and Africa, J.P. Morgan

15:15 Panel Discussion: Corporate Perspectives on the State of the Regional Market

How have Corporates adapted their strategies to cope with the unpredictable nature of regional growth and plan to

avoid future liquidity shortages? Examination of opportunities and benefits provided by market diversification in

converged cash and trade finance solutions to help improve working capital.

Moderator: Zeeshan Khan, Global Trade, Middle East and North Africa, J.P. Morgan

Panellists: Azmi Shaban, Shaban Group

Santosh Babu Karkera, A. A. Bin Hindi Group

Guillermo Arias, General Motors

Neeraj Tekchandani, Apparel FZCO

16:30 Close of Day

19:30 Dinner

Meet in Hotel Lobby

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Sonam Kapadia

Global Trade, Middle East and North Africa, J.P. Morgan

C H A N G I N G P A R A D I G M S O F T R A D E A N D

C U R R E N C Y S E T T L E M E N T P A T T E R N S

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Changing face of the world

Trade within Europe accounted for 65% of European trade

More than half of Asia’s exports (54%) remained within Asia

28% of North Americas exports remained in North America

Trade within regions dominates world trade. Europe and Asia remain their own top trading destinations

Slow

Growth Accelerating

Decelerating Fast Growth

<3%

<3% ≥3 %

≥3%

2010 – 2017

GDP growth

2003 –

2007

GD

P g

row

th

Intra/Inter table Origin

Destination NA1 SCA2 Europe CIS Africa MENA APAC Total

North America1 480.3 643.2 405.3 36.6 97.1 68.1 732.0 2,462.5

South & Central America2 415.7 187.3 152.8 7.3 16.6 9.4 329.1 1,118.3

Europe 311.9 152.4 3,513.8 269.3 185.4 147.8 844.8 5,425.3

CIS 15.1 12.6 176.9 100.2 3.6 2.2 99.5 410.1

Africa 34.9 19.5 172.2 9.5 61.4 36.5 128.9 462.9

MENA 51.1 18.0 177.7 10.9 20.9 52.1 171.1 501.8

APAC 419.3 196.4 580.0 94.6 136.2 419.3 2,753.1 4,598.9

Total 1,728.3 1,229.3 5,178.6 528.4 521.2 735.5 5,058.4 14,979.7

Source: UNCTAD database, 2010 international trade data & JPM Analysis 1 excluding Mexico 2 including Mexico

Source: IMF WEO database, JPM Analysis

Country as percentage of Region

US as % of North America1 76.02%

Russia as % of CIS 70.79%

China as % of Asia 39.25%

Mexico as % of SCA2 25.41%

Canada as % of NA1 23.98%

Germany as % of Europe 23.31%

Brazil as % of SCA2 17.94%

India as % of Asia 4.82%

Source: UNCTAD database, JPM Analysis

NA 28%

SCA 24%

Europe 18%

CIS 1%

Africa 2%

MENA 3%

APAC 24%

NA 52%

SCA 15%

Europe 12% CIS

1% Africa

2%

MENA 2%

APAC 16%

NA 14%

SCA 7%

Europe 17% CIS

2% Africa

3% MENA

3%

APAC 54% NA

9%

SCA 1%

Europe 20%

CIS 1%

Africa 5% MENA

7%

APAC 57%

19%

3%

35%

1%

12%

4%

26%

NA 8%

SCA 3%

Europe 68%

CIS 3%

Africa 3%

MENA 4% APAC

11%

7% 1%

51%

19% 2%

2%

18%

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

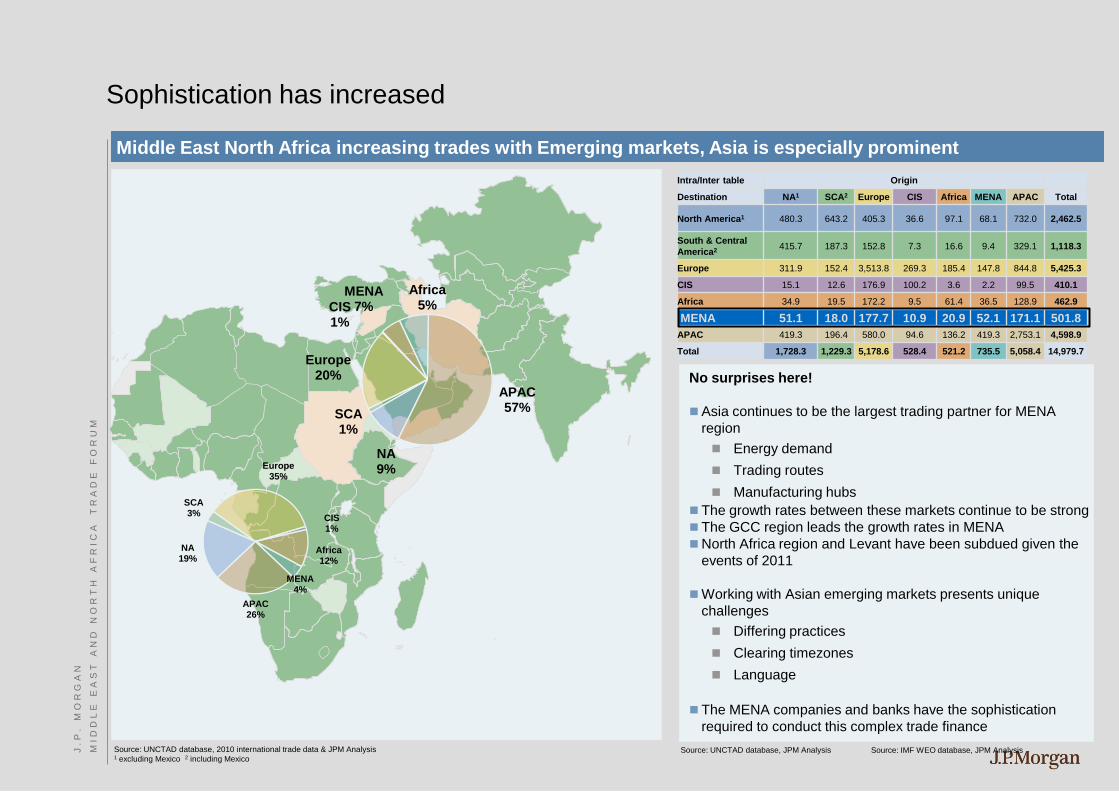

Sophistication has increased

Middle East North Africa increasing trades with Emerging markets, Asia is especially prominent

Intra/Inter table Origin

Destination NA1 SCA2 Europe CIS Africa MENA APAC Total

North America1 480.3 643.2 405.3 36.6 97.1 68.1 732.0 2,462.5

South & Central

America2 415.7 187.3 152.8 7.3 16.6 9.4 329.1 1,118.3

Europe 311.9 152.4 3,513.8 269.3 185.4 147.8 844.8 5,425.3

CIS 15.1 12.6 176.9 100.2 3.6 2.2 99.5 410.1

Africa 34.9 19.5 172.2 9.5 61.4 36.5 128.9 462.9

MENA 51.1 18.0 177.7 10.9 20.9 52.1 171.1 501.8

APAC 419.3 196.4 580.0 94.6 136.2 419.3 2,753.1 4,598.9

Total 1,728.3 1,229.3 5,178.6 528.4 521.2 735.5 5,058.4 14,979.7

Source: UNCTAD database, 2010 international trade data & JPM Analysis 1 excluding Mexico 2 including Mexico

Source: IMF WEO database, JPM Analysis Source: UNCTAD database, JPM Analysis

NA 9%

SCA 1%

Europe 20%

CIS 1%

Africa 5%

MENA 7%

APAC 57%

NA 19%

SCA 3%

Europe 35%

CIS 1%

Africa 12%

MENA 4%

APAC 26%

No surprises here!

Asia continues to be the largest trading partner for MENA

region

Energy demand

Trading routes

Manufacturing hubs

The growth rates between these markets continue to be strong

The GCC region leads the growth rates in MENA

North Africa region and Levant have been subdued given the

events of 2011

Working with Asian emerging markets presents unique

challenges

Differing practices

Clearing timezones

Language

The MENA companies and banks have the sophistication

required to conduct this complex trade finance

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

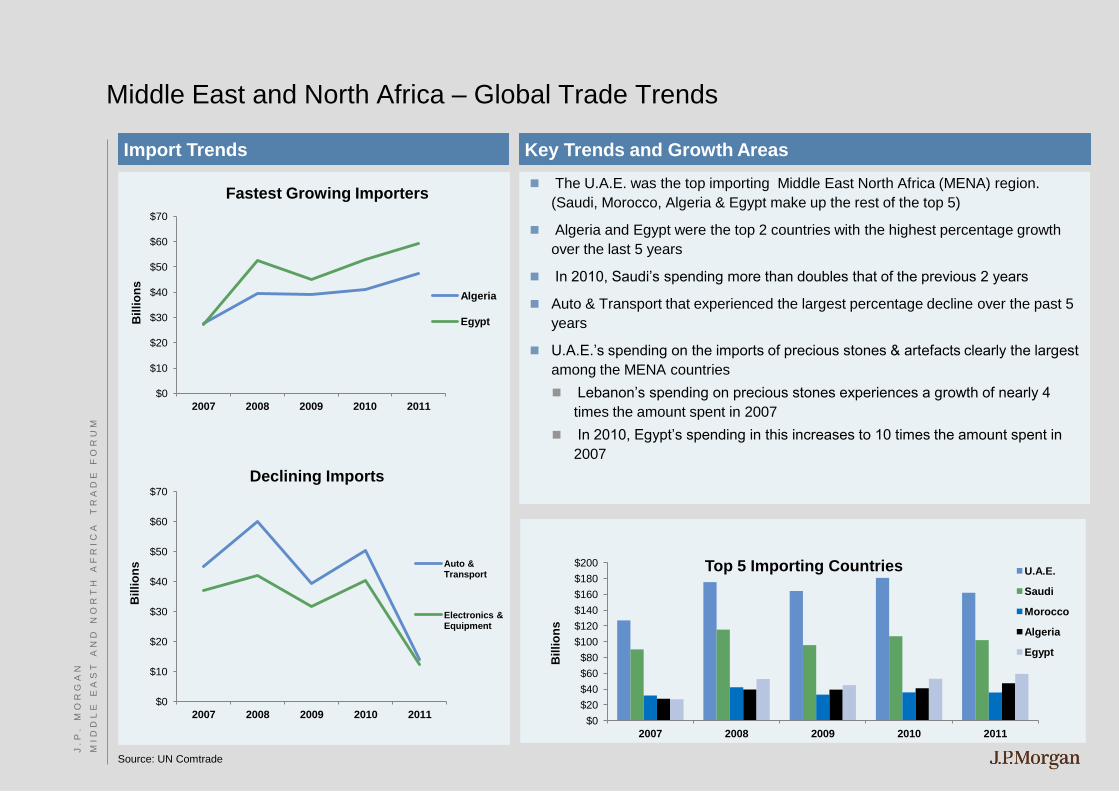

Middle East and North Africa – Global Trade Trends

Import Trends

The U.A.E. was the top importing Middle East North Africa (MENA) region.

(Saudi, Morocco, Algeria & Egypt make up the rest of the top 5)

Algeria and Egypt were the top 2 countries with the highest percentage growth

over the last 5 years

In 2010, Saudi’s spending more than doubles that of the previous 2 years

Auto & Transport that experienced the largest percentage decline over the past 5

years

U.A.E.’s spending on the imports of precious stones & artefacts clearly the largest

among the MENA countries

Lebanon’s spending on precious stones experiences a growth of nearly 4

times the amount spent in 2007

In 2010, Egypt’s spending in this increases to 10 times the amount spent in

2007

Key Trends and Growth Areas

$0

$10

$20

$30

$40

$50

$60

$70

2007 2008 2009 2010 2011

Bil

lio

ns

Fastest Growing Importers

Algeria

Egypt

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2007 2008 2009 2010 2011

Billi

on

s

Top 5 Importing Countries U.A.E.

Saudi

Morocco

Algeria

Egypt

$0

$10

$20

$30

$40

$50

$60

$70

2007 2008 2009 2010 2011

Billi

on

s

Declining Imports

Auto & Transport

Electronics & Equipment

Source: UN Comtrade

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

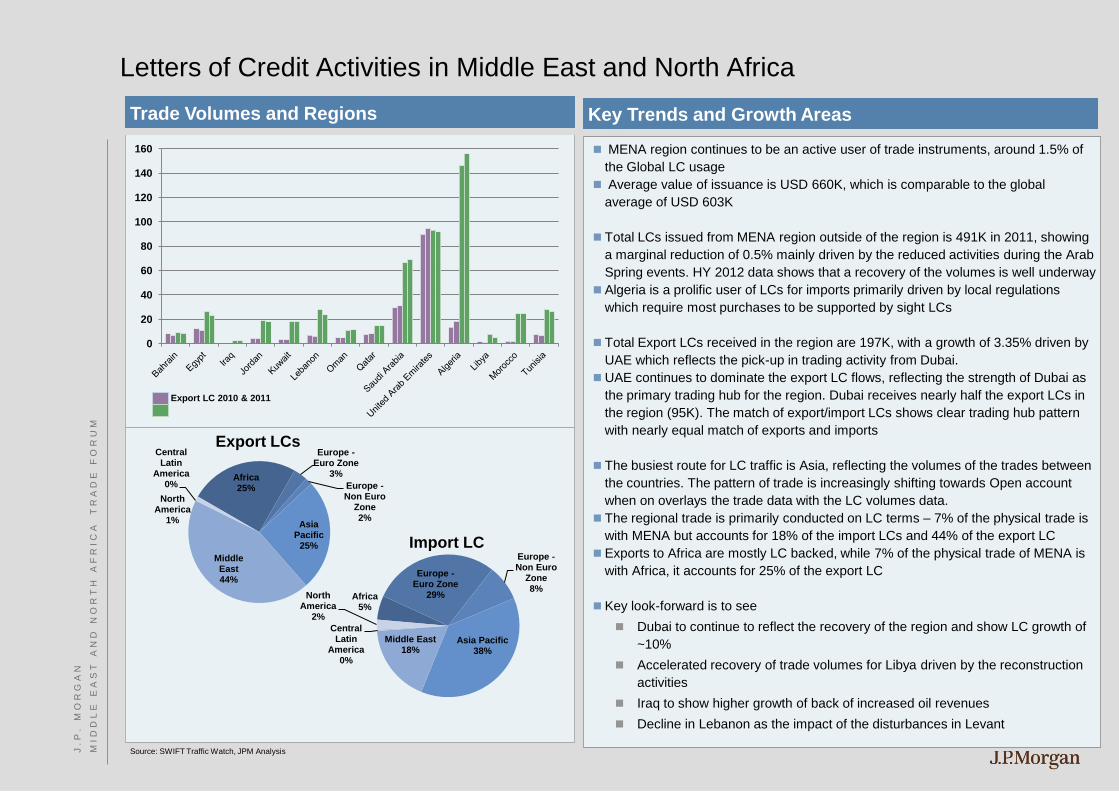

Letters of Credit Activities in Middle East and North Africa

0

20

40

60

80

100

120

140

160

Export LC 2010 & 2011

MENA region continues to be an active user of trade instruments, around 1.5% of

the Global LC usage

Average value of issuance is USD 660K, which is comparable to the global

average of USD 603K

Total LCs issued from MENA region outside of the region is 491K in 2011, showing

a marginal reduction of 0.5% mainly driven by the reduced activities during the Arab

Spring events. HY 2012 data shows that a recovery of the volumes is well underway

Algeria is a prolific user of LCs for imports primarily driven by local regulations

which require most purchases to be supported by sight LCs

Total Export LCs received in the region are 197K, with a growth of 3.35% driven by

UAE which reflects the pick-up in trading activity from Dubai.

UAE continues to dominate the export LC flows, reflecting the strength of Dubai as

the primary trading hub for the region. Dubai receives nearly half the export LCs in

the region (95K). The match of export/import LCs shows clear trading hub pattern

with nearly equal match of exports and imports

The busiest route for LC traffic is Asia, reflecting the volumes of the trades between

the countries. The pattern of trade is increasingly shifting towards Open account

when on overlays the trade data with the LC volumes data.

The regional trade is primarily conducted on LC terms – 7% of the physical trade is

with MENA but accounts for 18% of the import LCs and 44% of the export LC

Exports to Africa are mostly LC backed, while 7% of the physical trade of MENA is

with Africa, it accounts for 25% of the export LC

Key look-forward is to see

Dubai to continue to reflect the recovery of the region and show LC growth of

~10%

Accelerated recovery of trade volumes for Libya driven by the reconstruction

activities

Iraq to show higher growth of back of increased oil revenues

Decline in Lebanon as the impact of the disturbances in Levant

Key Trends and Growth Areas

Africa 25%

Europe - Euro Zone

3%

Europe - Non Euro

Zone 2%

Asia Pacific

25%

Middle East 44%

Central Latin

America 0%

North America

1%

Export LCs

Africa 5%

Europe - Euro Zone

29%

Europe - Non Euro

Zone 8%

Asia Pacific 38%

Middle East 18%

Central Latin

America 0%

North America

2%

Import LC

Source: SWIFT Traffic Watch, JPM Analysis

Trade Volumes and Regions

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

China is the largest trade partner for MENA Region

China is the largest trading partner for the MENA region and has an

accelerated growth path for the trade corridor

The top commodities, that were imported from China and into the MENA

region, from 2007 – 2011 were:

Plant & Machinery (USD 47 billion)

Electronics & Equipment (USD 41 billion)

Clothing & Accessories (USD 21 billion)

Iron & Steel (USD 16 billion)

Auto & Transport (USD 13 billion)

This trend is being witnessed globally and has led to an active increase

in the use of RMB as the trade settlement currency

Banks estimate that 10% China’s trade is now in RMB

The forecast is that in 3-5 years, it will increase to 20% as China’s

share of global trade increases

SWIFT data shows that Renminbi (RMB) is the third largest currency for

Letters of Credit (LCs), after Dollar and the Euro

About 4% of LCs issued were in RMB

Overall it is the 15th largest currency for trade

There are challenges to using RMB which are being actively addressed

Strict documentation requirements

Availability of RMB to the company to pay for purchases

Hedging of RMB exposures

Trade with China is an incentive for RMB settlement

Plant & Machinery

34%

Electronics & Equipment

29%

Clothing & Accessories

15%

Iron & Steel 12%

Auto & Transport

10%

MENA Imports from China

$0

$10

$20

$30

$40

2007 2008 2009 2010 2011

Billio

ns

Import Trends from China 2007-2011

Source: UN Comtrade

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

RMB Settlement has significant tail winds

China’s central bank is increasing the coverage of the Swap agreements that they have with other central banks

Central Banks of key trading markets like Singapore and Dubai are already on-board

London expected to become an off-shore centre for RMB

Liquidity in the Hong Kong market for RMB has increased

Estimates are that the deliverables market in Hong Kong has now increased to USD 3 billion, which provides the ability

to purchase/sell large order without moving the market

RMB based bonds are being issued to provide alternatives for managing RMB liquidity

Faster processing times

Chinese exports estimate that sales based on RMB are cleared in a day as compared to a week or fortnight for USD

Transparency

Typically, Chinese exporters build in a buffer of 3% for currency movements in the sales

RMB invoicing typically shows an improvement of 3%-7% in the cost of goods

Benefits of RMB Trade Settlement Scheme

Enhanced relationships with suppliers in China

A shorter turnaround time processing trade documentation improves the supplier’s cash flow

Exporters settling trades in RMB will be better able to grow their client base in China

Transparency in pricing and better management of foreign exchange risk

Factors providing support

Source: Global Trade Review

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

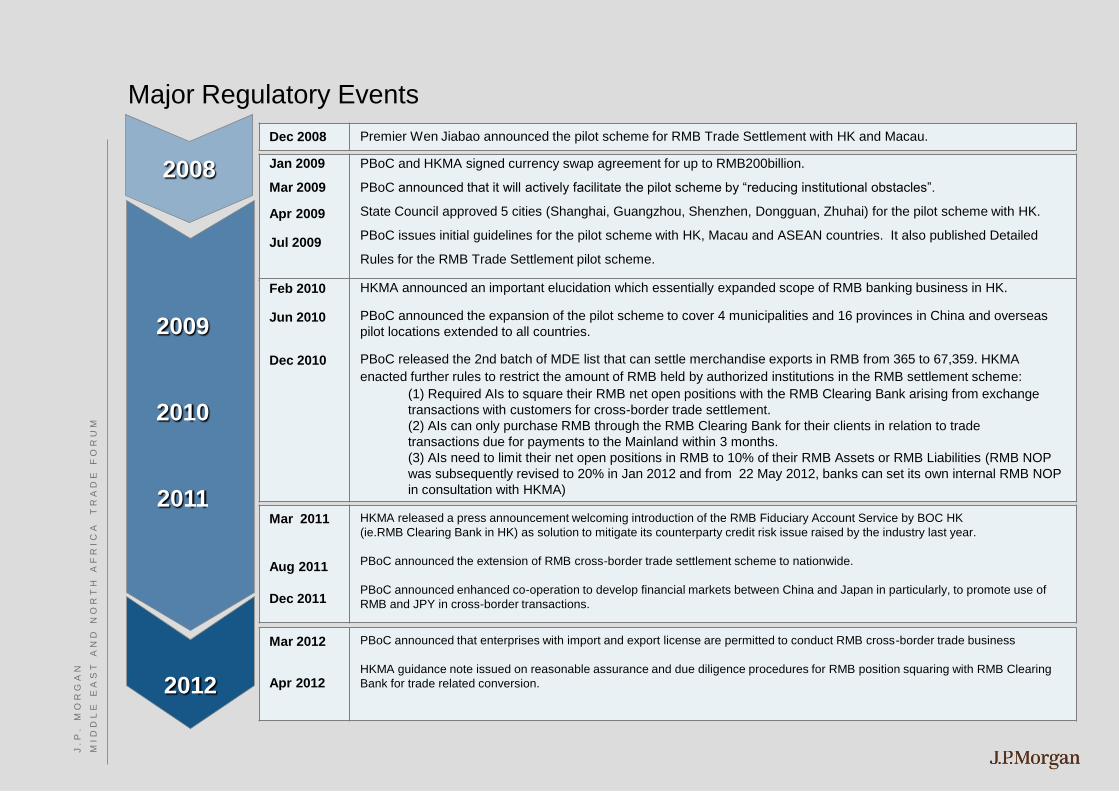

Major Regulatory Events

2008

2009

2010

2011

Jan 2009 Mar 2009 Apr 2009 Jul 2009

PBoC and HKMA signed currency swap agreement for up to RMB200billion. PBoC announced that it will actively facilitate the pilot scheme by “reducing institutional obstacles”. State Council approved 5 cities (Shanghai, Guangzhou, Shenzhen, Dongguan, Zhuhai) for the pilot scheme with HK. PBoC issues initial guidelines for the pilot scheme with HK, Macau and ASEAN countries. It also published Detailed Rules for the RMB Trade Settlement pilot scheme.

Mar 2012

Apr 2012

PBoC announced that enterprises with import and export license are permitted to conduct RMB cross-border trade business

HKMA guidance note issued on reasonable assurance and due diligence procedures for RMB position squaring with RMB Clearing

Bank for trade related conversion.

Dec 2008 Premier Wen Jiabao announced the pilot scheme for RMB Trade Settlement with HK and Macau.

Feb 2010

Jun 2010

Dec 2010

HKMA announced an important elucidation which essentially expanded scope of RMB banking business in HK.

PBoC announced the expansion of the pilot scheme to cover 4 municipalities and 16 provinces in China and overseas

pilot locations extended to all countries.

PBoC released the 2nd batch of MDE list that can settle merchandise exports in RMB from 365 to 67,359. HKMA

enacted further rules to restrict the amount of RMB held by authorized institutions in the RMB settlement scheme:

(1) Required AIs to square their RMB net open positions with the RMB Clearing Bank arising from exchange

transactions with customers for cross-border trade settlement.

(2) AIs can only purchase RMB through the RMB Clearing Bank for their clients in relation to trade

transactions due for payments to the Mainland within 3 months.

(3) AIs need to limit their net open positions in RMB to 10% of their RMB Assets or RMB Liabilities (RMB NOP

was subsequently revised to 20% in Jan 2012 and from 22 May 2012, banks can set its own internal RMB NOP

in consultation with HKMA)

Mar 2011

Aug 2011

Dec 2011

HKMA released a press announcement welcoming introduction of the RMB Fiduciary Account Service by BOC HK

(ie.RMB Clearing Bank in HK) as solution to mitigate its counterparty credit risk issue raised by the industry last year.

PBoC announced the extension of RMB cross-border trade settlement scheme to nationwide.

PBoC announced enhanced co-operation to develop financial markets between China and Japan in particularly, to promote use of

RMB and JPY in cross-border transactions.

2012

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

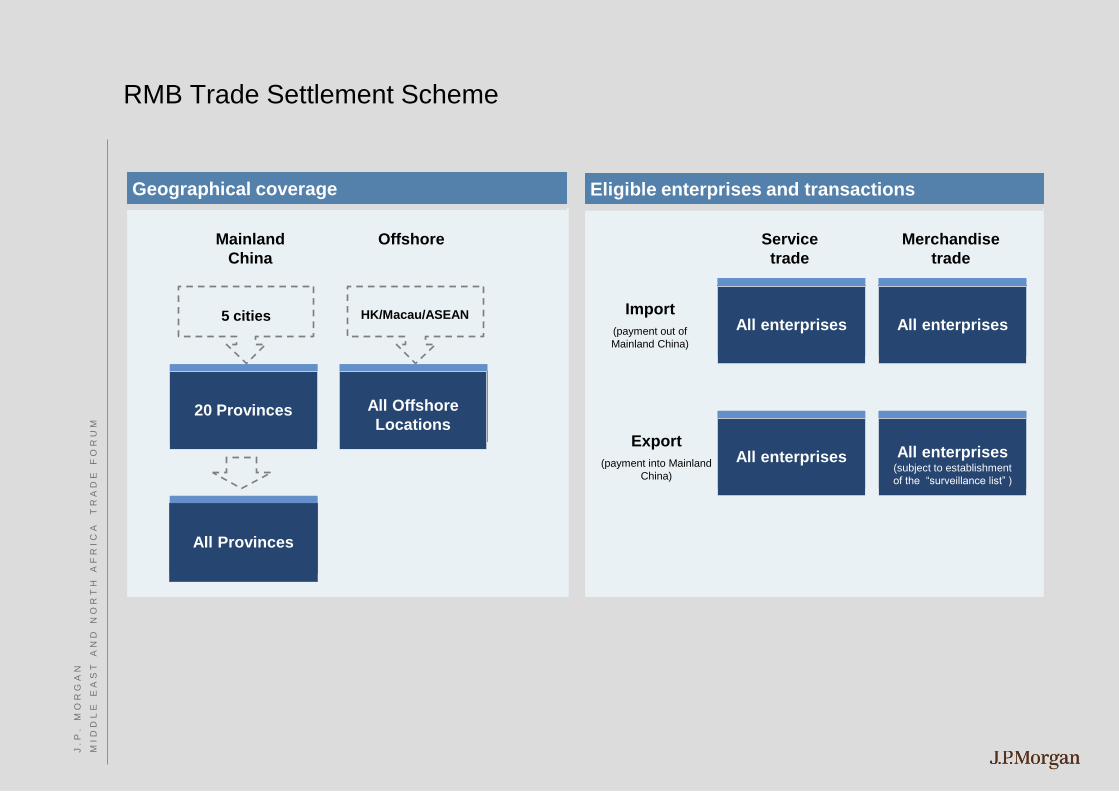

RMB Trade Settlement Scheme

Machinery

and transport

equipment

Geographical coverage Eligible enterprises and transactions

Import

(payment out of

Mainland China)

All enterprises

Merchandise

trade

Service

trade

All enterprises

Export

(payment into Mainland

China)

All enterprises

All enterprises (subject to establishment

of the “surveillance list” )

Offshore Mainland

China

20 Provinces

All Offshore

Locations

HK/Macau/ASEAN

5 cities

All Provinces

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Currency Swap Arrangement

China

Argentina

70Bn

Iceland

3.5Bn

New

Zealand

25Bn

Indonesia

100Bn

Malaysia

180Bn

Singapore

150Bn

Hong Kong

400Bn

Belarus

20Bn

South

Korea

360Bn

Australia

200Bn

Pakistan

10Bn

Mongolia

10Bn

UAE

35Bn Thailand

70Bn

Ukraine

15Bn

Japan

Direct

Swap

China is expanding its bilateral currency swap arrangement

Source: PBoC – Bilateral currency swap arrangement (RMB)

RMB1,648.5 billion

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

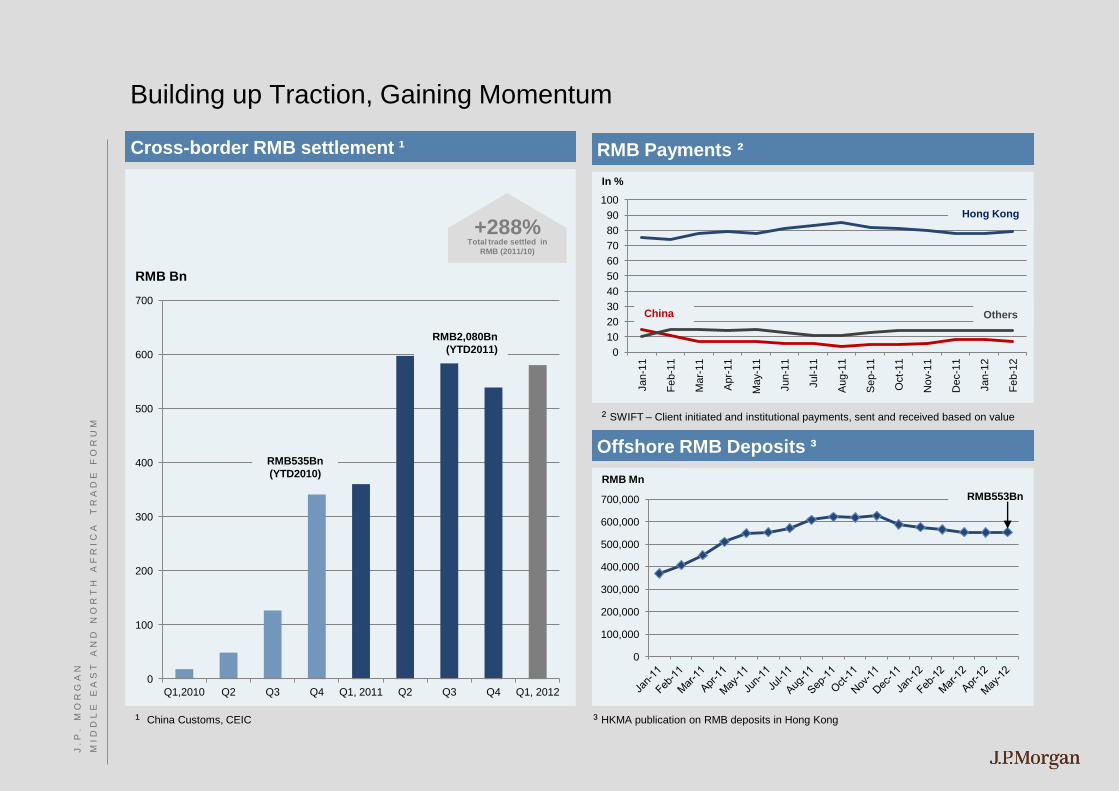

Building up Traction, Gaining Momentum

Cross-border RMB settlement ¹ RMB Payments ²

³ HKMA publication on RMB deposits in Hong Kong

Offshore RMB Deposits ³

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

RMB Mn

RMB553Bn

0

10

20

30

40

50

60

70

80

90

100

Jan-1

1

Fe

b-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-

11

Aug-1

1

Sep-1

1

Oct-

11

Nov-1

1

Dec-1

1

Jan-1

2

Fe

b-1

2

² SWIFT – Client initiated and institutional payments, sent and received based on value

Hong Kong

Others China

In %

0

100

200

300

400

500

600

700

Q1,2010 Q2 Q3 Q4 Q1, 2011 Q2 Q3 Q4 Q1, 2012

RMB Bn

¹ China Customs, CEIC

+288% Total trade settled in

RMB (2011/10)

RMB535Bn

(YTD2010)

RMB2,080Bn

(YTD2011)

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

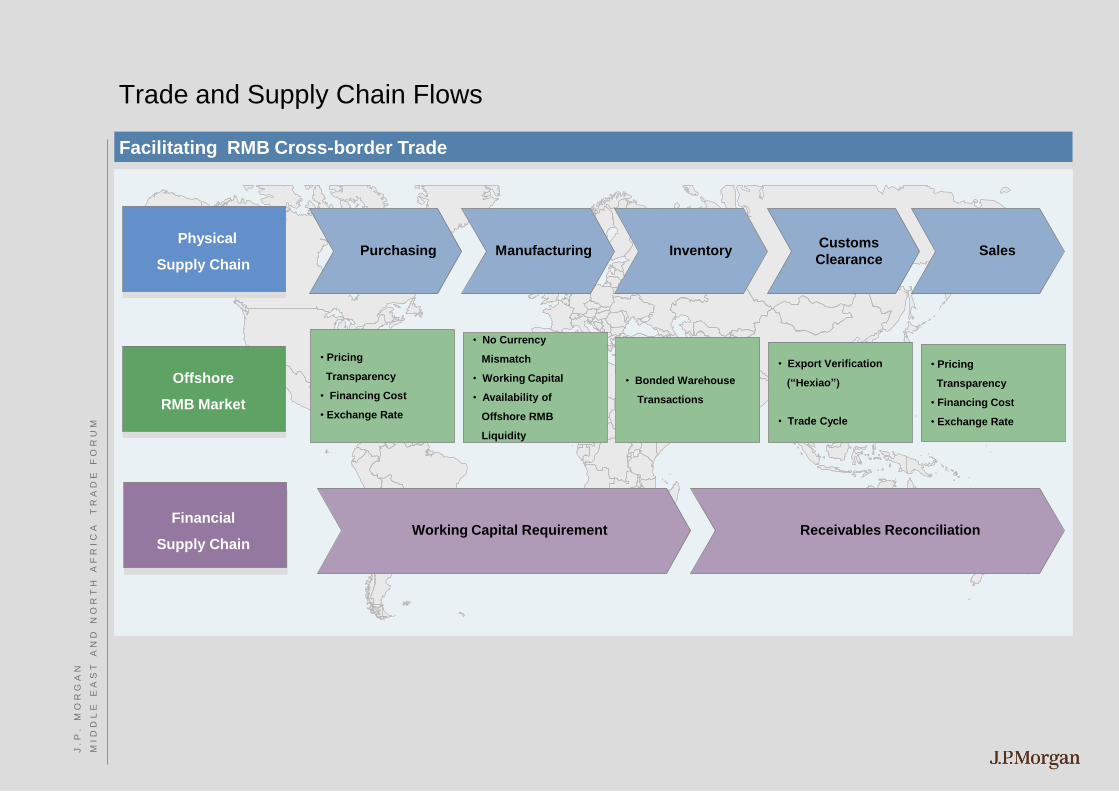

Trade and Supply Chain Flows

Facilitating RMB Cross-border Trade

• Pricing

Transparency

• Financing Cost

• Exchange Rate

• No Currency

Mismatch

• Working Capital

• Availability of

Offshore RMB

Liquidity

• Bonded Warehouse

Transactions

• Export Verification

(“Hexiao”)

• Trade Cycle

• Pricing

Transparency

• Financing Cost

• Exchange Rate

Physical

Supply Chain

Offshore

RMB Market

Financial

Supply Chain

Purchasing Manufacturing Inventory Customs

Clearance Sales

Working Capital Requirement Receivables Reconciliation

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

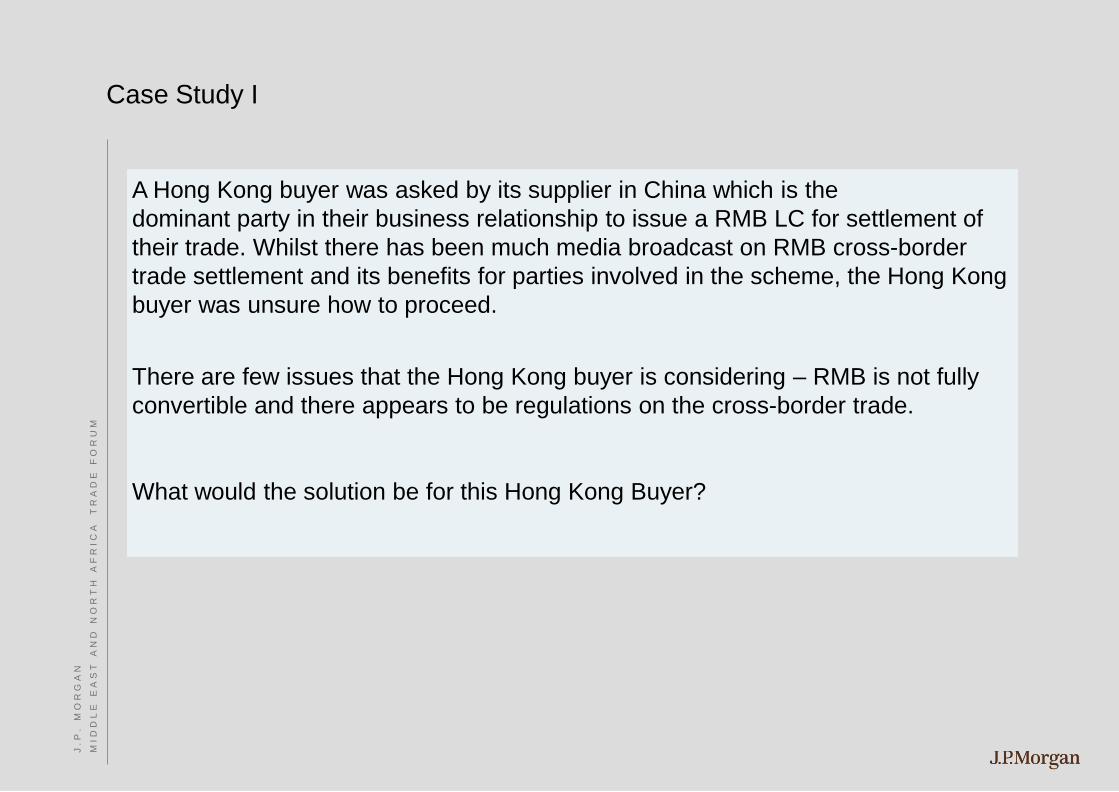

Case Study I

A Hong Kong buyer was asked by its supplier in China which is the

dominant party in their business relationship to issue a RMB LC for settlement of

their trade. Whilst there has been much media broadcast on RMB cross-border

trade settlement and its benefits for parties involved in the scheme, the Hong Kong

buyer was unsure how to proceed.

There are few issues that the Hong Kong buyer is considering – RMB is not fully

convertible and there appears to be regulations on the cross-border trade.

What would the solution be for this Hong Kong Buyer?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

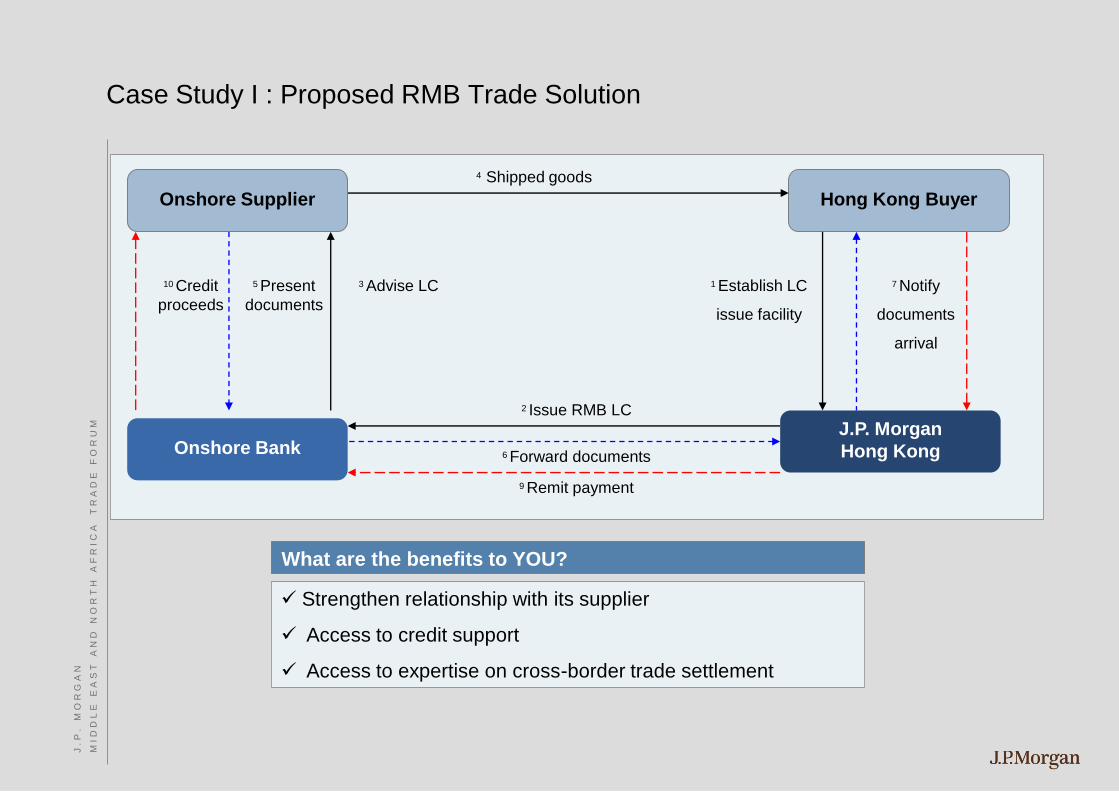

Case Study I : Proposed RMB Trade Solution

9 Remit payment

Hong Kong Buyer

Onshore Bank J.P. Morgan

Hong Kong

Onshore Supplier

2 Issue RMB LC

1 Establish LC

issue facility

3 Advise LC

4 Shipped goods

5 Present

documents

6 Forward documents

7 Notify

documents

arrival

10 Credit

proceeds

Strengthen relationship with its supplier

Access to credit support

Access to expertise on cross-border trade settlement

What are the benefits to YOU?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

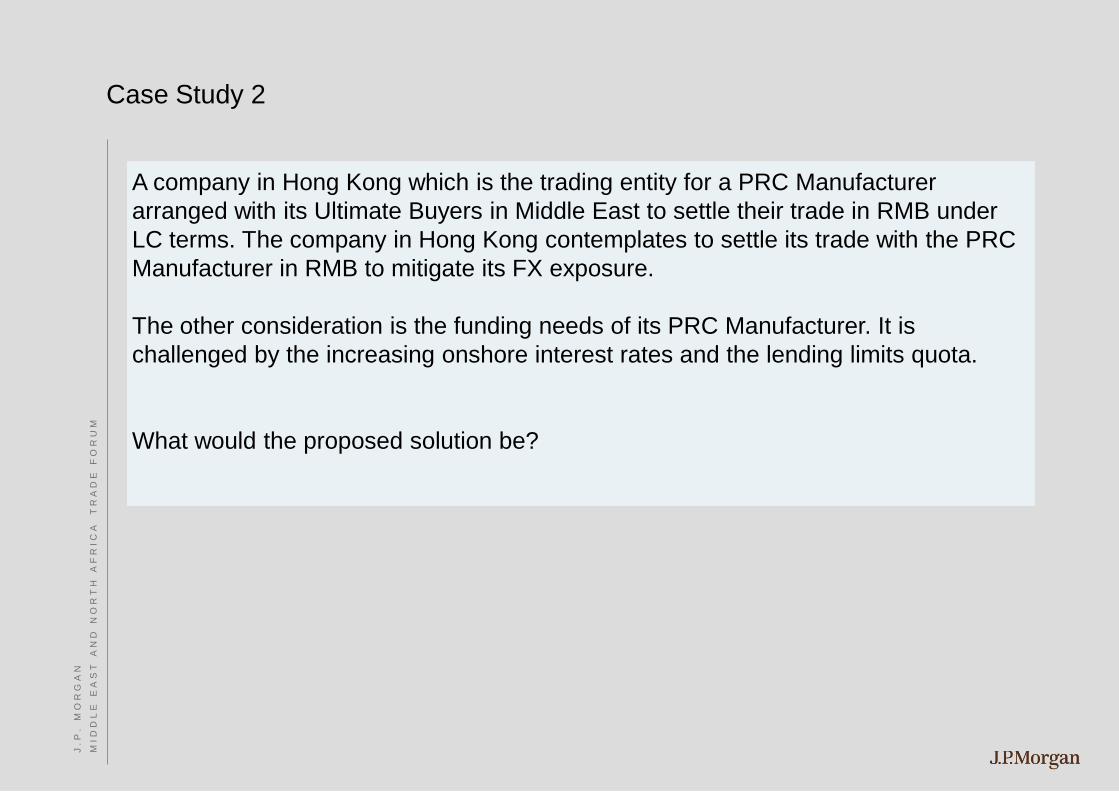

Case Study 2

A company in Hong Kong which is the trading entity for a PRC Manufacturer

arranged with its Ultimate Buyers in Middle East to settle their trade in RMB under

LC terms. The company in Hong Kong contemplates to settle its trade with the PRC

Manufacturer in RMB to mitigate its FX exposure.

The other consideration is the funding needs of its PRC Manufacturer. It is

challenged by the increasing onshore interest rates and the lending limits quota.

What would the proposed solution be?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Case Study 2 : Proposed RMB Trade Solution

PRC

Manufacturer J.P.Morgan China LIB

1) Advise RMB LC

J.P.Morgan Hong Kong Hong Kong

Trading Company

2) Issue RMB LC

3) Provide import LC bills financing

Lower COF offshore

4) Use RMB proceeds received from its Ultimate Buyers to settle loan

Ultimate Buyers

(Middle East)

Enhanced banking relationship

Access to credit support

Increase sales opportunities

Access to credit and funding support

Access to expertise on cross-border trade settlement

What is it for YOU?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

J.P. Morgan locations worldwide (alternate) cities

Argentina Buenos Aires

Bahamas Nassau

Brazil Rio de Janeiro São Paulo

Canada Calgary Montreal Toronto Vancouver

Cayman Islands Georgetown

Chile Santiago

Colombia Bogotá

Mexico Mexico City Monterrey

Peru Lima

United States Chicago Dallas Houston Los Angeles New York San Francisco

Venezuela Caracas

Austria Vienna

Belgium Brussels

Channel Islands Jersey

France Paris

Germany Berlin Frankfurt Munich

Greece Athens

Ireland Dublin

Italy Milan Rome

Luxembourg

Netherlands Amsterdam

Norway Oslo

Poland Warsaw

Portugal Lisbon

Russian Federation Moscow

Spain Madrid

Sweden Stockholm

Switzerland Geneva Zurich

United Kingdom Bournemouth Edinburgh Essex Glasgow Isle of Man London

Egypt Cairo

Nigeria Lagos

South Africa Johannesburg

Australia Melbourne Sydney

Bahrain Manama

China Beijing Hong Kong Shanghai Shenzhen Tianjin

Dubai (UAE)

India Bangalore Mumbai

Indonesia Jakarta Israel Tel Aviv

Sri Lanka Colombo

Thailand Bangkok

Taiwan Kaohsiung Pan Chiao City Taichung Tainan City Taipei Taoyuan

Turkey Istanbul

Uzbekistan Tashkent

Vietnam Hanoi Ho Chi Minh City

Japan Osaka Tokyo

Lebanon Beirut

Malaysia Kuala Lumpur Labuan

Pakistan Karachi

Philippines Manila

Saudi Arabia Riyadh

Singapore

South Korea Seoul

Lagos

Lisbon

Madrid

Rome

Athens Istanbul

Beirut Tel Aviv

Cairo

Riyadh

Manama

Karachi

Mumbai

Bangalore

Colombo

Johannesburg

Edinburgh

Glasgow

Isle of Man

Dublin

Essex

London

Bournemouth

Jersey

Paris

Amsterdam

Brussels

Luxembourg

Zurich

Geneva

Milan

Munich Vienna

Berlin

Frankfurt

Warsaw Moscow

Vancouver Calgary

San Francisco

Los Angeles Dallas Houston

Monterrey

Mexico City Georgetown

Nassau

Caracas

Bogotá

Lima

Rio de Janeiro

São Paulo Santiago

Buenos Aires

Hanoi

Bangkok

Ho Chi Minh City

Kuala Lumpur

Singapore

Labuan

Manila

Hong Kong

Shenzhen

Taoyuan

Taichung

Pan Chiao City

Tainan City

Kaohsiung

Sydney

Melbourne

Taipei

Chicago

Toronto

Montreal

New York

Oslo

Stockholm Beijing

Shanghai

Tianjin

Jakarta

Tokyo

Seoul

Osaka Tashkent

Dubai

Americas Europe Africa Asia Pacific/Middle East

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Amr El Haddad

Global Trade Product, Middle East and North Africa, J.P. Morgan

T H E P R O D U C T L A N D S C A P E I N A

G R O W I N G T R A D E E N V I R O N M E N T

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

In This Presentation

Growth • How have global trade exports grown since the 1950’s?

Action • What did banks do to design the right tools for trade financing?

Re-action

• What’s most suitable for Corporate sector?

Developing trade patterns

Growing product landscape to meet the growth in Trade

Importance of using the Cash Conversion Cycle (CCC) as a criteria to choose the right product

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

Section 1 : How did Global Trade Grow?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

I - Developing trade patterns

Despite a post-crisis dip, the current level of world gross exports is

almost three times that prevailing in the 1950s

Commodity trade accounted for a declining share of this growth (with

some exceptions)

What explains the expansion of global trade?

1) The rise of Emerging Market Economies (EMEs)

2) The growing importance of regional trade

3) The shift of higher technology exports towards dynamic EMEs

Systemic important trading nations are increasing

A chief contributor is the growing role of global supply chains in overall trade, facilitated by lower tariffs

With vertical specialization, production of certain goods is fragmented into several stages

Goods cross borders several times before being transformed into final products, further increasing trade

interconnectedness

Outsourcing of production stages from advanced “upstream” countries to neighbouring EMEs has also

supported a shift in the technology content of exports towards the latter

A. The global trade landscape has witnessed dramatic shifts over the past several decades

B. Trade expansion was further associated with growing trade interconnectedness

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

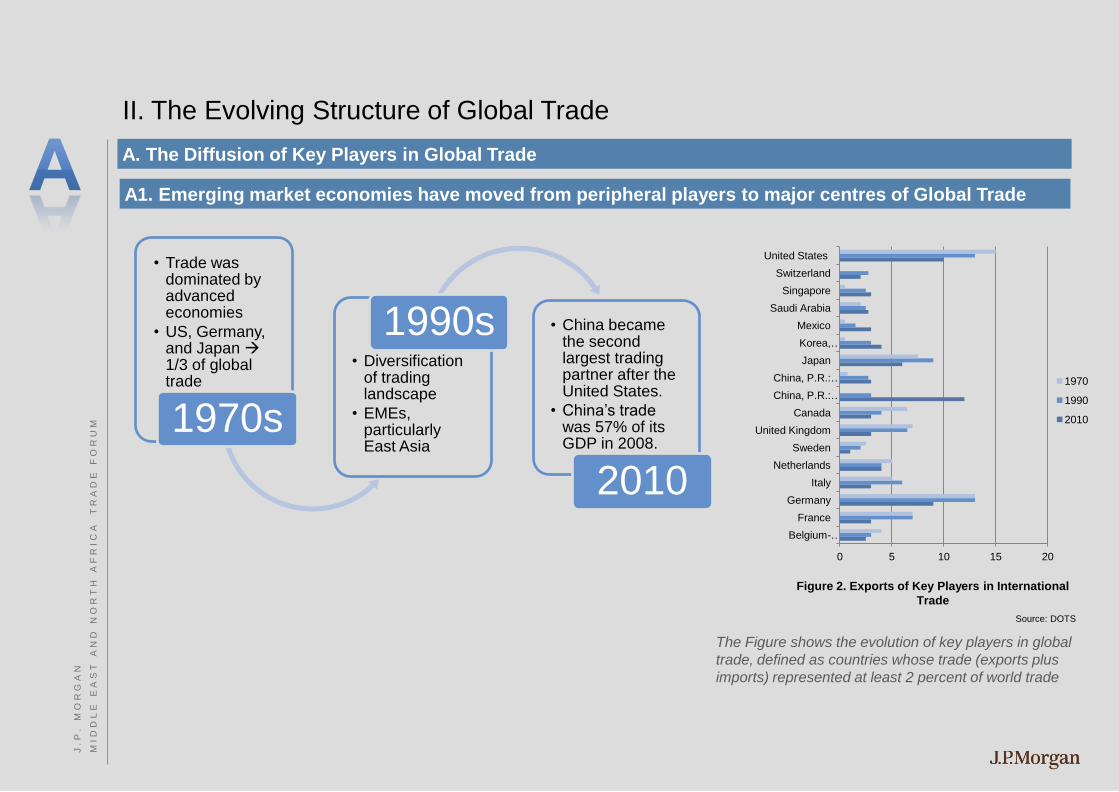

II. The Evolving Structure of Global Trade

• Trade was dominated by advanced economies

• US, Germany, and Japan 1/3 of global trade

1970s

• Diversification of trading landscape

• EMEs, particularly East Asia

1990s • China became the second largest trading partner after the United States.

• China’s trade was 57% of its GDP in 2008.

2010

The Figure shows the evolution of key players in global

trade, defined as countries whose trade (exports plus

imports) represented at least 2 percent of world trade

0 5 10 15 20

Belgium-…

France

Germany

Italy

Netherlands

Sweden

United Kingdom

Canada

China, P.R.: …

China, P.R.: …

Japan

Korea, …

Mexico

Saudi Arabia

Singapore

Switzerland

United States

1970

1990

2010

Figure 2. Exports of Key Players in International

Trade

Source: DOTS

A. The Diffusion of Key Players in Global Trade

A1. Emerging market economies have moved from peripheral players to major centres of Global Trade

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

II. The Evolving Structure of Global Trade

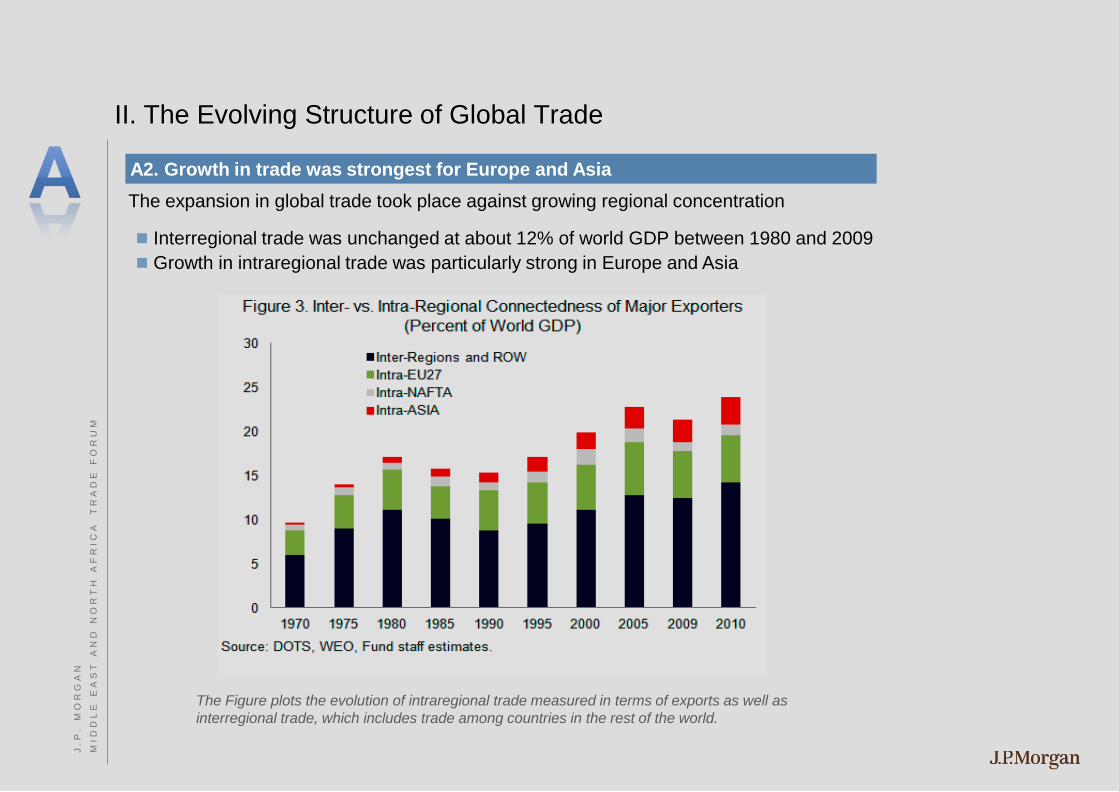

The expansion in global trade took place against growing regional concentration

Interregional trade was unchanged at about 12% of world GDP between 1980 and 2009

Growth in intraregional trade was particularly strong in Europe and Asia

The Figure plots the evolution of intraregional trade measured in terms of exports as well as

interregional trade, which includes trade among countries in the rest of the world.

A2. Growth in trade was strongest for Europe and Asia

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

II. The Evolving Structure of Global Trade

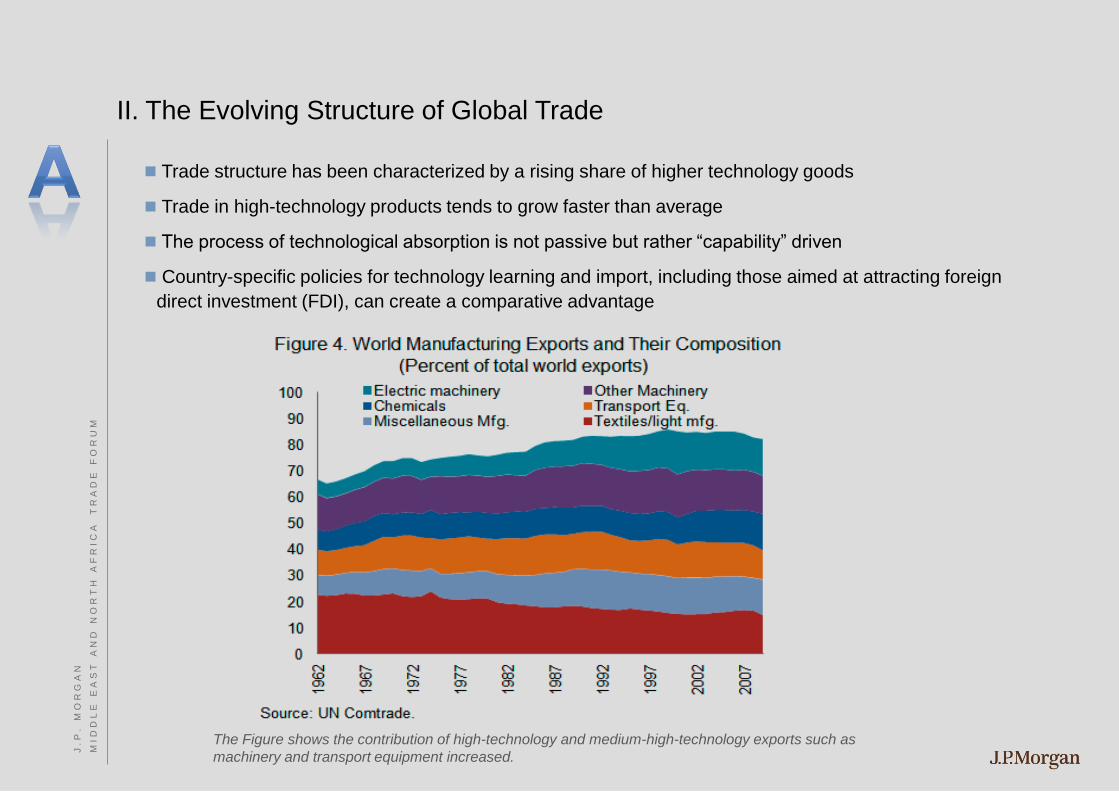

Trade structure has been characterized by a rising share of higher technology goods

Trade in high-technology products tends to grow faster than average

The process of technological absorption is not passive but rather “capability” driven

Country-specific policies for technology learning and import, including those aimed at attracting foreign

direct investment (FDI), can create a comparative advantage

The Figure shows the contribution of high-technology and medium-high-technology exports such as

machinery and transport equipment increased.

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

II. The Evolving Structure of Global Trade

The volume of trade in relation to GDP increased and took the form of intra-industry trade

Intra-industry trade as a share of overall trade has increased steadily

Highest for products such as machinery, chemicals and manufactures

Countries that experienced higher changes in intra-industry trade between 1985 and 2009 are

those integrated in a supply chain, such as China, Thailand, and Mexico (Figure 5B)

Convergence in Income levels

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

II. The Evolving Structure of Global Trade

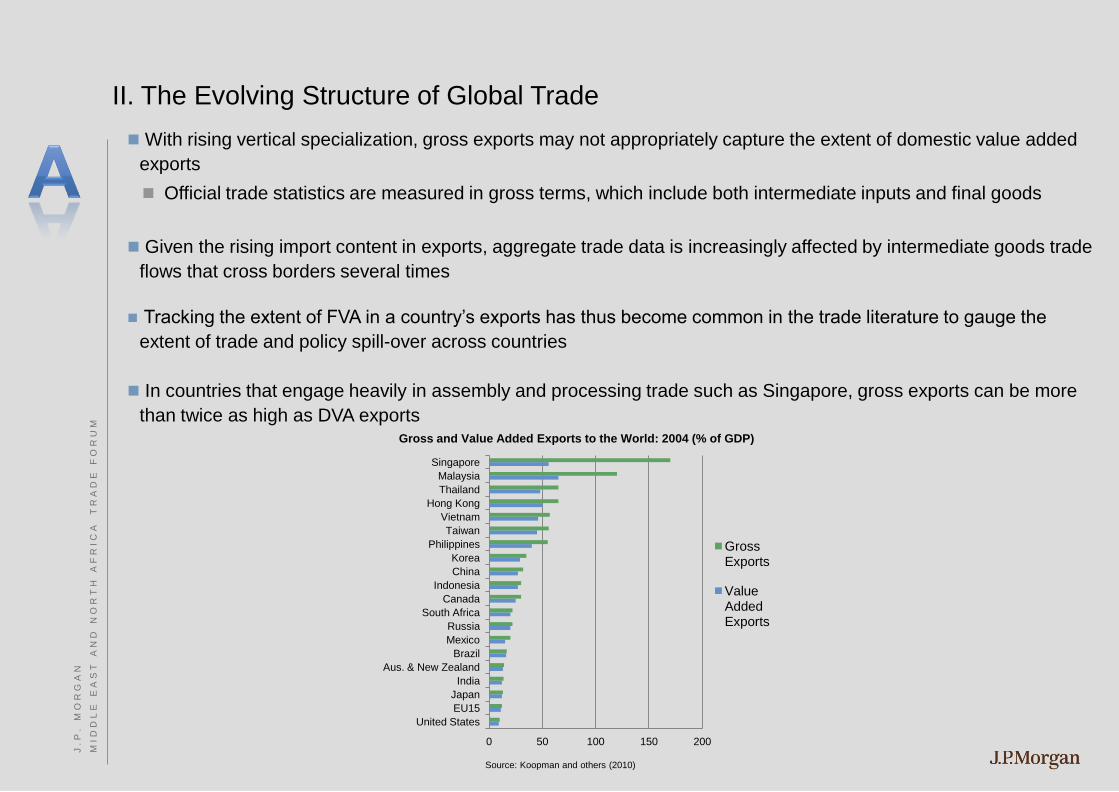

With rising vertical specialization, gross exports may not appropriately capture the extent of domestic value added

exports

Official trade statistics are measured in gross terms, which include both intermediate inputs and final goods

Given the rising import content in exports, aggregate trade data is increasingly affected by intermediate goods trade

flows that cross borders several times

Tracking the extent of FVA in a country’s exports has thus become common in the trade literature to gauge the

extent of trade and policy spill-over across countries

In countries that engage heavily in assembly and processing trade such as Singapore, gross exports can be more

than twice as high as DVA exports

0 50 100 150 200

United States

EU15

Japan

India

Aus. & New Zealand

Brazil

Mexico

Russia

South Africa

Canada

Indonesia

China

Korea

Philippines

Taiwan

Vietnam

Hong Kong

Thailand

Malaysia

Singapore

Gross Exports

Value Added Exports

Gross and Value Added Exports to the World: 2004 (% of GDP)

Source: Koopman and others (2010)

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

Section 2 : What did Banks do?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

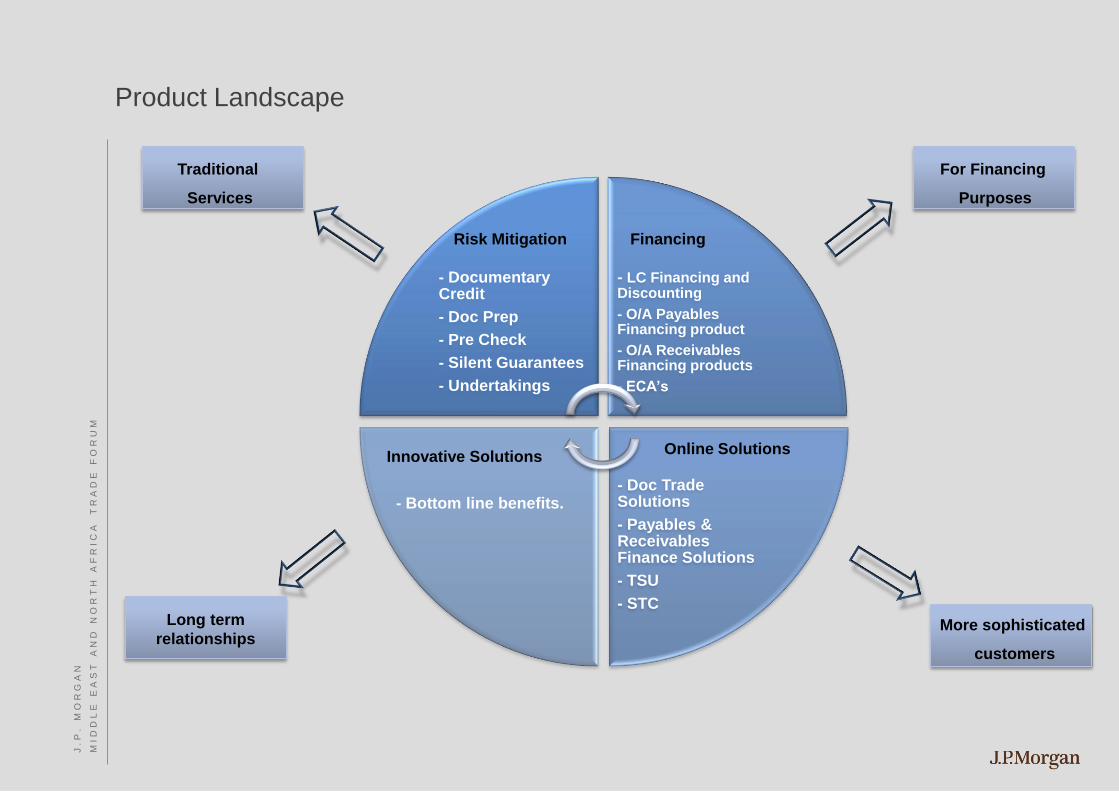

- Documentary Credit

- Doc Prep

- Pre Check

- Silent Guarantees

- Undertakings

- LC Financing and Discounting

- O/A Payables Financing product

- O/A Receivables Financing products

- ECA’s

- Doc Trade Solutions

- Payables & Receivables Finance Solutions

- TSU

- STC

Online Solutions Innovative Solutions

Product Landscape

Financing Risk Mitigation

- Bottom line benefits.

For Financing

Purposes

More sophisticated

customers

Long term

relationships

Traditional

Services

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

Product Landscape

Documentary Trade

Instruments: Letters of Credit – Letters of Guarantees – Documentary Collection - Others

Did they meet the growth?

The more demanding customers?

Today’s technical sophistication?

Were they flexible enough to meet today’s demands?

Silent Guarantees

Undertakings

Services

Document Preperation, Pre Check

Buyer Seller

Bank (s)

Seller

Bank (s)

Buyer

Documentary Credit

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

Product Landscape

LC Financing and Discounting

O/A Payables Financing Product

O/A Receivables Financing Products

Many forms of longer term Financing; ECA’s

Buyer

Seller

Bank (s) Ins. & Others

Finance

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Did they meet the growth?

The more demanding customers?

Today’s technical sophistication?

Were they flexible enough to meet

today’s demands?

Blank slide

Product Landscape

Doc Trade Solutions

Payables & Receivables Finance Solutions

Trade Services Utility

SWIFT Trade for Corporates

Bank (s)

Buyer

Seller

Online Solutions

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Did they meet the growth?

The more demanding customers?

Today’s technical sophistication?

Were they flexible enough to meet today’s

demands?

Blank slide

Product Landscape

Think Bottom Line Benefits

Innovative Solutions

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

Section 3 : How should Corporates re-act?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Factors

Capabilities

Can you do it?

Or not?

Leverage

Who dictates the terms?

Can you financially

benefit from it?

Cost or Benefit?

Thinking of the cost?

Or bottom line?

Factors Affecting Decision Making

Product

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

II. The Evolving Structure of Global Trade

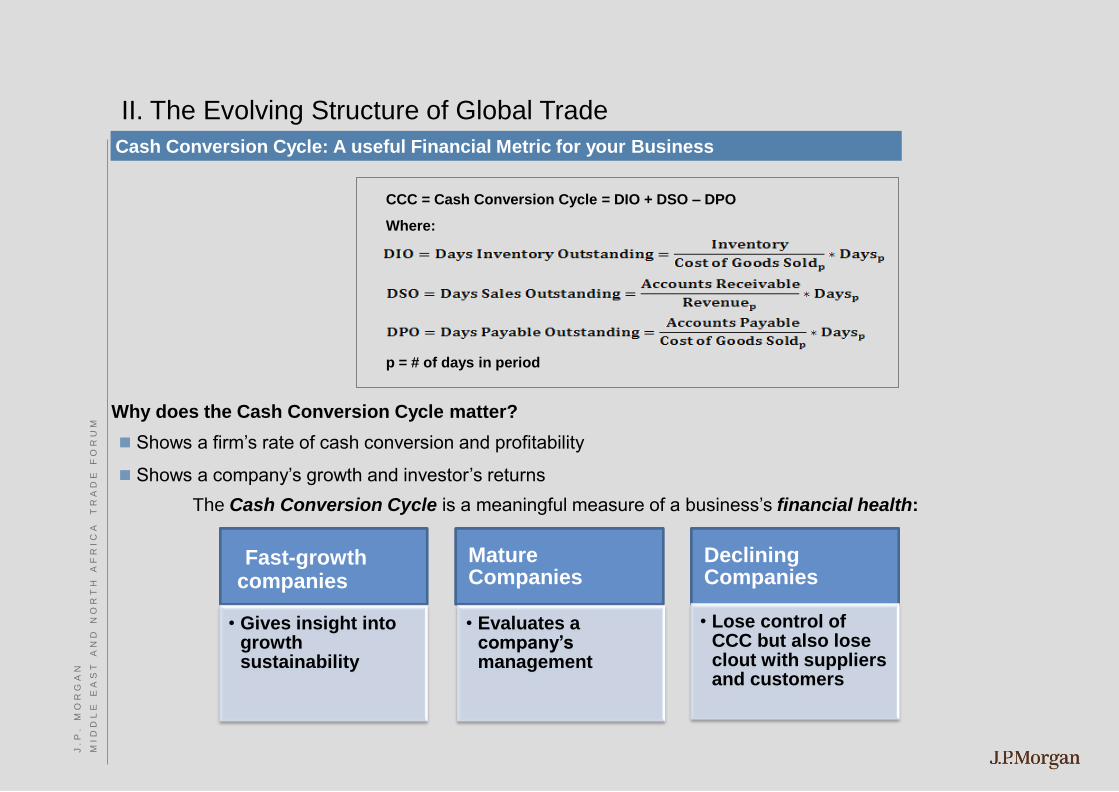

Why does the Cash Conversion Cycle matter?

Shows a firm’s rate of cash conversion and profitability

Shows a company’s growth and investor’s returns

The Cash Conversion Cycle is a meaningful measure of a business’s financial health:

Fast-growth companies

• Gives insight into growth sustainability

Mature Companies

• Evaluates a company’s management

Declining Companies

• Lose control of CCC but also lose clout with suppliers and customers

CCC = Cash Conversion Cycle = DIO + DSO – DPO

Where:

p = # of days in period

Cash Conversion Cycle: A useful Financial Metric for your Business

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Blank slide

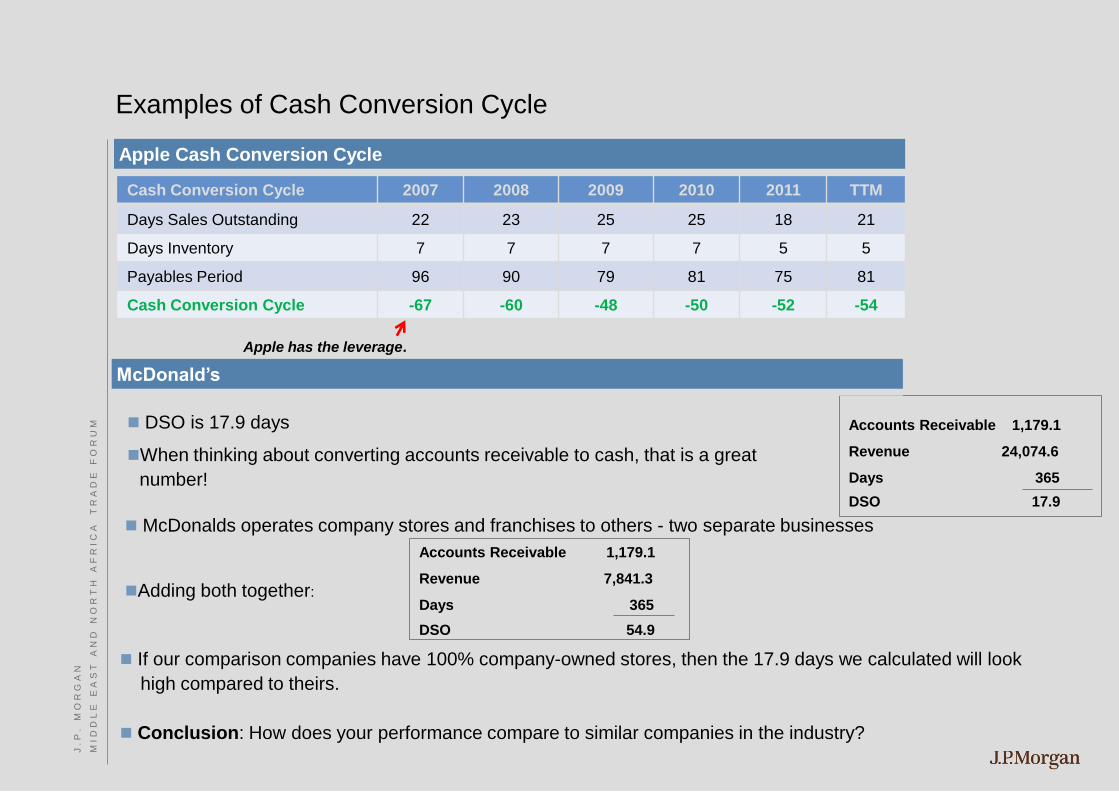

Apple has the leverage.

Examples of Cash Conversion Cycle

DSO is 17.9 days

When thinking about converting accounts receivable to cash, that is a great

number!

McDonalds operates company stores and franchises to others - two separate businesses

Adding both together:

If our comparison companies have 100% company-owned stores, then the 17.9 days we calculated will look

high compared to theirs.

Conclusion: How does your performance compare to similar companies in the industry?

Cash Conversion Cycle 2007 2008 2009 2010 2011 TTM

Days Sales Outstanding 22 23 25 25 18 21

Days Inventory 7 7 7 7 5 5

Payables Period 96 90 79 81 75 81

Cash Conversion Cycle -67 -60 -48 -50 -52 -54

Accounts Receivable 1,179.1

Revenue 24,074.6

Days 365

DSO 17.9

Accounts Receivable 1,179.1

Revenue 7,841.3

Days 365

DSO 54.9

Apple Cash Conversion Cycle

McDonald’s

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Ian Lyall

Compliance, Europe Middle East and Africa, J.P. Morgan

C O M P L I A N C E

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Agenda

Sanctions / Recent US Regulatory Actions and Settlements

Trade and AML / Sanctions

International Sanctions

Bureau of Industry and Security (BIS)

Anti-Corruption Program

Questions

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Sanctions

Recent Regulatory Actions and Settlements

Regulatory Body Financial Institution Fine / Penalty

Department of Justice Dutch Bank (2012) $ 619 Million

Department of Justice UK Bank (2010) $298 Million

Department of Justice

Dutch Bank (2010) $500 Million

Department of Justice

Swiss Bank (2009) $536 Million

Department of Justice

UK Bank (2009) $217 Million

US Treasury Department Australia Bank (2009) $5.75 Million

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Trade and AML/ Sanctions

There is much anecdotal information about trade and its high risk for money laundering

Regulatory interest is high

Few public domain case studies

The FATF paper (June 28, 2008) titled “Best Practices Paper on Trade Based Money Laundering”

characterizes trade as “one of the main methods by which criminal organizations and terrorist

financiers move money for the purpose of disguising its origins and integrating it into the formal

economy” and concludes that “many customs agencies, law enforcement agencies, financial

intelligence units (FIU), tax authorities and banking supervisors appear less capable of identifying

and combating trade-based money laundering than they are in dealing with other forms of money

laundering and terrorist financing.”

The Wolfsberg Group published a paper on Trade Finance Principles in January 2009 setting out

the responsibilities for each of the banks in the documentary credit and collection process.

Usually requires collusion between two or more parties

Over/Under Invoicing

Multiple invoicing

Short shipping

Over shipping

Shipping inferior/substandard goods

Deliberate concealment of the type of goods

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

International Sanctions

TRADE

SANCTIONS2

FLIGHT BANS

RESTRICTIONS

ON ADMISSION

DIPLOMATIC

SANCTIONS1

FINANCIAL

SANCTIONS3

BOYCOTT

SPORTS OR

CULTURAL

EVENTS

SUSPEND

COOPERATION

WITH A THIRD

COUNTRY

Sanctions can range from economic/ trade sanctions to

more targeted measures. J.P. Morgan Chase and

other financial institutions are required to apply

financial/ trade sanctions including those issued by the

Office of Foreign Assets Control, OFAC.

Sanctions may include

1 Diplomatic sanctions such as expulsion of diplomats, severing of diplomatic ties, suspension of official visits 2 Trade sanctions such as general or specific trade sanctions, arms embargoes 3 Financial sanctions such as freezing of funds or economic resources, prohibition on financial transactions, restrictions on export credits or investment

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Definition and purpose of sanctions

Sanctions are the economic arm of foreign policy used to influence countries or individuals:

Violating international laws or human rights

Engaging in unlawful activity such as narcotics trafficking, human trafficking or weapons trafficking

That pose a security threat to other nations through the development and proliferation of weapons

of mass destruction or chemical and biological weapons or acts of terrorism

Purpose of sanctions

The goal of sanctions is to penalize the offending country, entity, or individual for their actions and

persuade the offender to change their actions. Sanctions are normally used by the international

community for one or more of the following reasons

To encourage a change in the behavior of a target country or regime. (e.g. North Korea is subject

to sanctions to encourage the cooperation with the international community and abandon its

nuclear missile program)

To apply pressure on a target country or regime to comply with set objectives. (e.g. Iran is subject

to sanctions aiming to stop the uranium enrichment program)

As an enforcement tool when international peace and security has been threatened and

diplomatic efforts have failed. (e.g. Sierra Leone was subject to sanctions in order to stop the civil

war)

To prevent and suppress the financing of terrorists and terrorist acts. (e.g. Al-Qaida is an

international terrorist organization subject to sanctions in order to stop them perpetrating terrorist

acts)

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

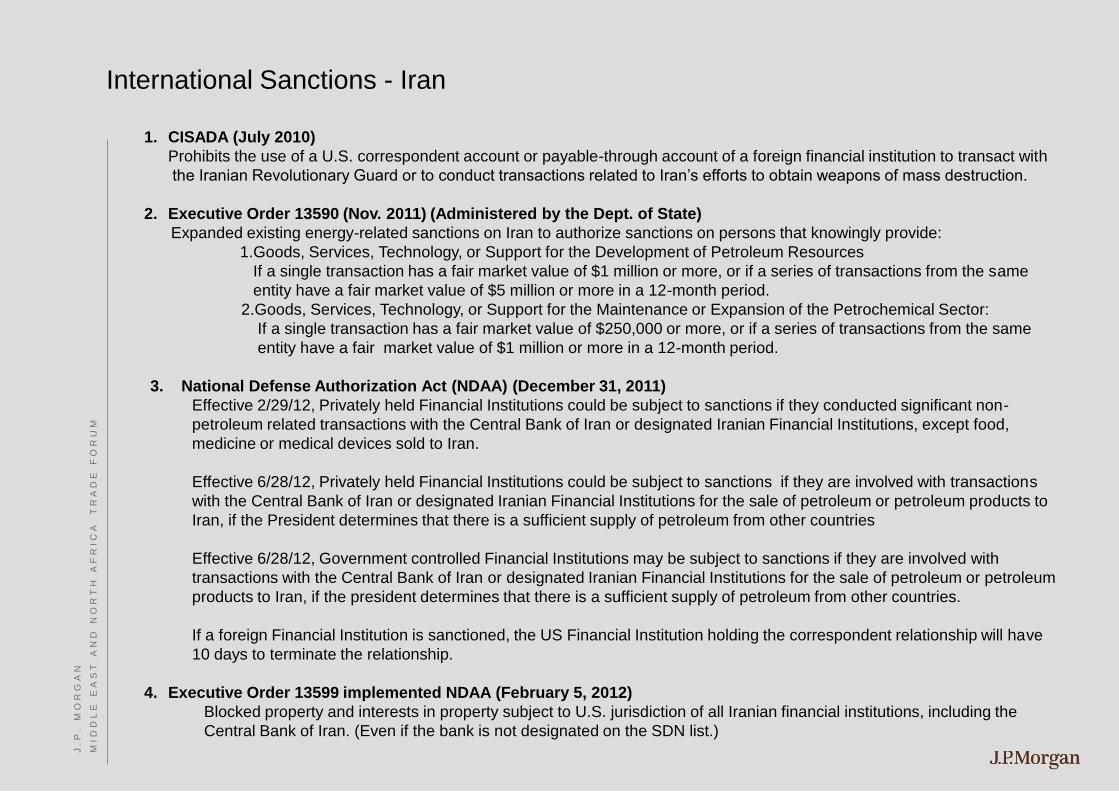

International Sanctions - Iran

1. CISADA (July 2010)

Prohibits the use of a U.S. correspondent account or payable-through account of a foreign financial institution to transact with

the Iranian Revolutionary Guard or to conduct transactions related to Iran’s efforts to obtain weapons of mass destruction.

2. Executive Order 13590 (Nov. 2011) (Administered by the Dept. of State)

Expanded existing energy-related sanctions on Iran to authorize sanctions on persons that knowingly provide:

1.Goods, Services, Technology, or Support for the Development of Petroleum Resources

If a single transaction has a fair market value of $1 million or more, or if a series of transactions from the same

entity have a fair market value of $5 million or more in a 12-month period.

2.Goods, Services, Technology, or Support for the Maintenance or Expansion of the Petrochemical Sector:

If a single transaction has a fair market value of $250,000 or more, or if a series of transactions from the same

entity have a fair market value of $1 million or more in a 12-month period.

3. National Defense Authorization Act (NDAA) (December 31, 2011)

Effective 2/29/12, Privately held Financial Institutions could be subject to sanctions if they conducted significant non-

petroleum related transactions with the Central Bank of Iran or designated Iranian Financial Institutions, except food,

medicine or medical devices sold to Iran.

Effective 6/28/12, Privately held Financial Institutions could be subject to sanctions if they are involved with transactions

with the Central Bank of Iran or designated Iranian Financial Institutions for the sale of petroleum or petroleum products to

Iran, if the President determines that there is a sufficient supply of petroleum from other countries

Effective 6/28/12, Government controlled Financial Institutions may be subject to sanctions if they are involved with

transactions with the Central Bank of Iran or designated Iranian Financial Institutions for the sale of petroleum or petroleum

products to Iran, if the president determines that there is a sufficient supply of petroleum from other countries.

If a foreign Financial Institution is sanctioned, the US Financial Institution holding the correspondent relationship will have

10 days to terminate the relationship.

4. Executive Order 13599 implemented NDAA (February 5, 2012)

Blocked property and interests in property subject to U.S. jurisdiction of all Iranian financial institutions, including the

Central Bank of Iran. (Even if the bank is not designated on the SDN list.)

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

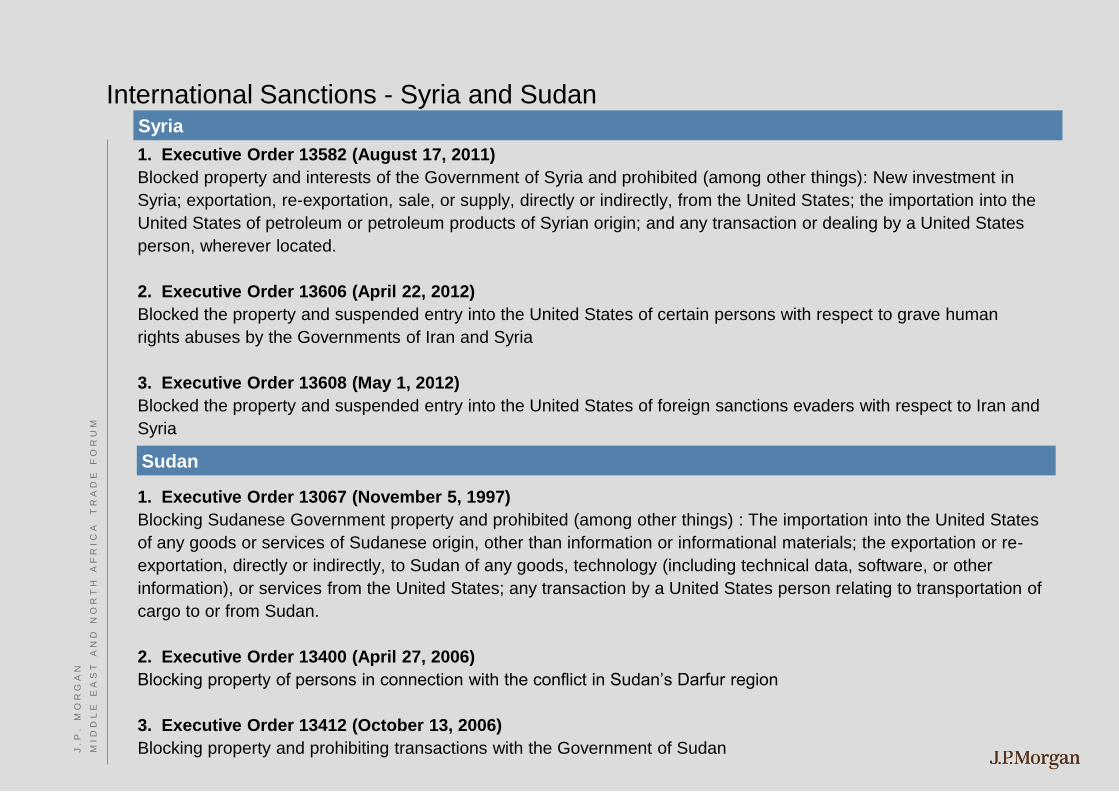

International Sanctions - Syria and Sudan

1. Executive Order 13582 (August 17, 2011)

Blocked property and interests of the Government of Syria and prohibited (among other things): New investment in

Syria; exportation, re-exportation, sale, or supply, directly or indirectly, from the United States; the importation into the

United States of petroleum or petroleum products of Syrian origin; and any transaction or dealing by a United States

person, wherever located.

2. Executive Order 13606 (April 22, 2012)

Blocked the property and suspended entry into the United States of certain persons with respect to grave human

rights abuses by the Governments of Iran and Syria

3. Executive Order 13608 (May 1, 2012)

Blocked the property and suspended entry into the United States of foreign sanctions evaders with respect to Iran and

Syria

1. Executive Order 13067 (November 5, 1997)

Blocking Sudanese Government property and prohibited (among other things) : The importation into the United States

of any goods or services of Sudanese origin, other than information or informational materials; the exportation or re-

exportation, directly or indirectly, to Sudan of any goods, technology (including technical data, software, or other

information), or services from the United States; any transaction by a United States person relating to transportation of

cargo to or from Sudan.

2. Executive Order 13400 (April 27, 2006)

Blocking property of persons in connection with the conflict in Sudan’s Darfur region

3. Executive Order 13412 (October 13, 2006)

Blocking property and prohibiting transactions with the Government of Sudan J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Syria

Sudan

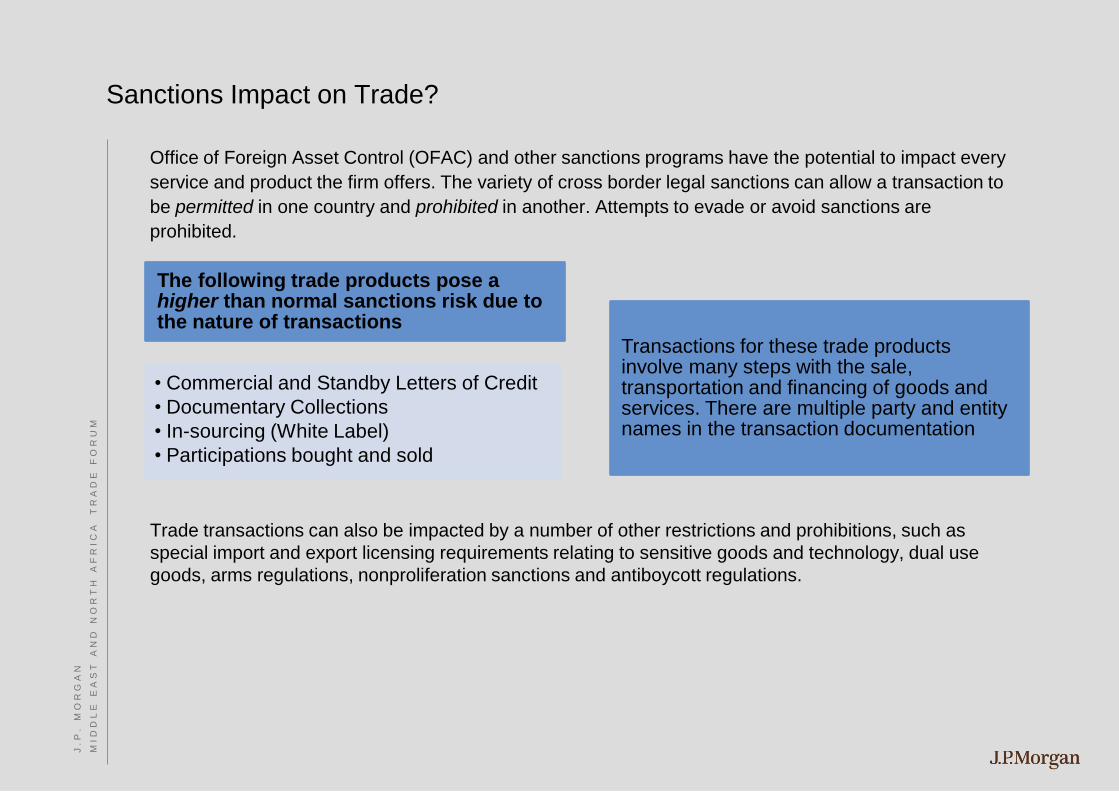

Sanctions Impact on Trade?

Office of Foreign Asset Control (OFAC) and other sanctions programs have the potential to impact every

service and product the firm offers. The variety of cross border legal sanctions can allow a transaction to

be permitted in one country and prohibited in another. Attempts to evade or avoid sanctions are

prohibited.

Trade transactions can also be impacted by a number of other restrictions and prohibitions, such as

special import and export licensing requirements relating to sensitive goods and technology, dual use

goods, arms regulations, nonproliferation sanctions and antiboycott regulations.

The following trade products pose a higher than normal sanctions risk due to the nature of transactions

• Commercial and Standby Letters of Credit

• Documentary Collections

• In-sourcing (White Label)

• Participations bought and sold

Transactions for these trade products involve many steps with the sale, transportation and financing of goods and services. There are multiple party and entity names in the transaction documentation

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Bureau of Industry and Security (BIS) – Dual Use Goods and Boycott Clauses

Bureau of Industry and Security (BIS) – a department within the U.S Department of Commerce charged with the

responsibility for U.S national security, foreign policy and economic interests. All U.S. financial institutions, regardless of

their locations, are required to comply with BIS regulations. Penalties for violations are severe and include the fines of up

to $250,000 per violation or twice the transaction value (whichever is greater) and imprisonment of up to ten years.

BIS Activities include

•Enforcement of antiboycott regulations – the laws are directed generally against foreign boycotts of countries friendly to the U.S.

•Regulation of export of sensitive goods and technology

•Enforcement of export controls, including dual use goods and technology – primarily commercial goods which have potential military applications (proliferation, national security and combating terrorism)

•Assistance of U.S. industry to comply with international arms control agreements

•Requiring compliance with sanctions against imports and exports of goods and cervices to certain Denied / Embargoes Persons

Examples of Dual Use Goods

•Computers;

• Integrated circuits;

•High energy devices;

•Telecommunications;

•Marine acoustic systems and equipment;

•Optical equipment (mirrors, components, cable);

•Chemical mixtures (e.g. ammonium bifluoride, ammonium nitrate, etc.);

•Alloys of metals (e.g. aluminum, lithium, magnesium, metal powder, etc.)

•Chemical compounds (e.g. beryllium, indium, etc.);

•Uranium, helium, hydrogen

BIS Lists

•Denied Persons List (DPL) – A list of entities and individuals that have been exporting privileges. Any dealings with a party on this list that would violate the terms of its denial order are prohibited.

•Unverified List – A list of parties where BIS has been unable to verify the end-user in prior transactions. The presence of a party on this list is a “Red Flag” that should be resolved before proceeding with the transaction.

•Entity List – A list of parties whose presence in a transaction can trigger license requirement under the Export Administration Regulations. The list specifies the license requirements that apply to each listed party, additional to the requirements under the Export Administration Regulations.

Antiboycott Clauses

•Examples of prohibited activities:

•Agreement to refuse or to refuse to do business with or in Israel or with blacklisted companies.

• Implementation of a letter of credit that contains prohibited terms and conditions.

•Agreement to discriminate or actually discriminate against a person, based on race, religion, sex, nationality or national origin.

•Examples of potential antiboycott language:

•Black list:

•Shipment of goods originating from Israel is strictly prohibited.

•Certificate from the manufacturer stating that they are not blacklisted.

•White List:

•Certificate from the steamship company or owner or master or their agents stating that the carrying vessel is allowed/eligible to enter U.A.E. ports.

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Policy/ Program Overview

• A statement of zero tolerance for bribery in all forms

• A strong statement from senior management, setting the tone from the top

• Facilitation payments prohibited

• Pre-clearance required for expenses benefitting government officials

• Strong controls governing the engagement of third parties that help develop business or seek government action

• Mandatory training to all relevant employees; enhanced training for higher risk employees

• Mechanisms provided for employees to self-report issues

Risk Assessment/ Monitoring Training

• Country Corruption Index

• Identification of high risk countries, industries, activities

• Increased attention to local legal requirements

• Monitoring process to enforce pre-clearance requirement

• Generate relevant metrics

• Centralization of due diligence for third party engagements

• Targeted training for high risk employees

• Develop best practices around required due diligence and contractual agreements

Third Party Oversight

• Third parties (that help develop business or seek government action) can create liability for the firm even if not directly paid by the bank

• Most enforcement actions involve third parties that pay bribes for their principals

• Regulatory expectation requiring strong controls

• Engagement of third parties must be treated as a significant event

Governance

• Board level reports

• Senior level accountability

• Increased corporate-level staffing

• Senior governance committee

• Designated legal and compliance officers

Anti-Corruption Program J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Florence Coronel

Risk, Europe Middle East and Africa, J.P. Morgan

C R E D I T R I S K M A N A G E M E N T I N A

C H A L L E N G I N G E N V I R O N M E N T

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Agenda

Risk Management at J.P. Morgan

Pillars of Risk Management

Risk Ratings

Counterparty Credit Risk Analysis

Sovereign Risk

Reputational Risk Management

Market Themes and Risk Management Actions

Eurozone Crisis

Arab Spring

Other issues for risk managers

Q&A

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

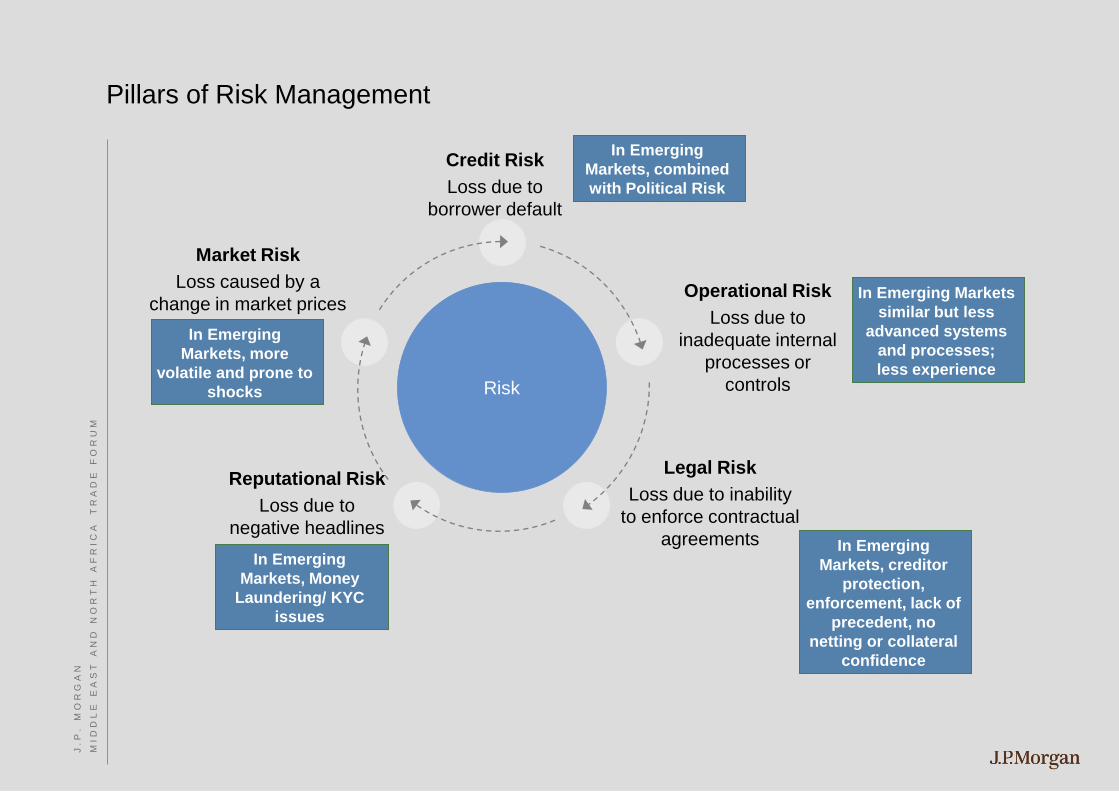

Pillars of Risk Management

Risk

Market Risk

Loss caused by a

change in market prices

or rates

Operational Risk

Loss due to

inadequate internal

processes or

controls

Credit Risk

Loss due to

borrower default

Reputational Risk

Loss due to

negative headlines

Legal Risk

Loss due to inability

to enforce contractual

agreements In Emerging

Markets, Money

Laundering/ KYC

issues

In Emerging

Markets, more

volatile and prone to

shocks

In Emerging

Markets, combined

with Political Risk

In Emerging

Markets, creditor

protection,

enforcement, lack of

precedent, no

netting or collateral

confidence

In Emerging Markets

similar but less

advanced systems

and processes;

less experience

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Risk ratings are used to manage credit exposures

J.P. Morgan risk ratings

Credit risk is the risk of loss from counterparty

default

Risk ratings are assigned to differentiate risk levels

J.P. Morgan risk ratings range from 1+ (low) to 10

(worst)

Corporate Counterparty Ratings

3 step risk grading process:

Stand-alone grade

Obligor grade

Facility grade

Risk Monitoring and Control

Credit risk is monitored at an aggregate portfolio,

industry and individual counterparty level

Risk ratings

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

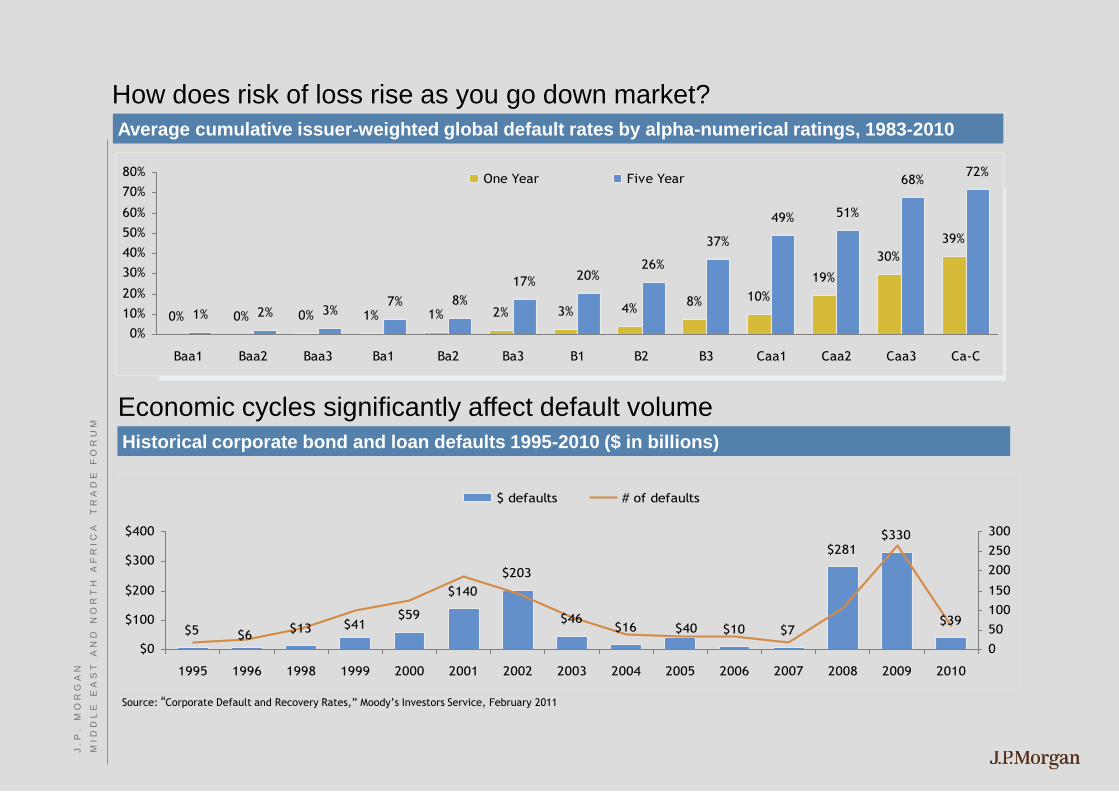

Historical corporate bond and loan defaults 1995-2010 ($ in billions)

How does risk of loss rise as you go down market?

Height: 2.00”

Width: 8.84”

Horizontal: 1.67”

Vertical: 2.00”

Source:

Average cumulative issuer-weighted global default rates by alpha-numerical ratings, 1983-2010

0% 0% 0% 1% 1% 2% 3% 4%8% 10%

19%

30%

39%

1% 2% 3%7% 8%

17% 20%26%

37%

49% 51%

68%72%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Baa1 Baa2 Baa3 Ba1 Ba2 Ba3 B1 B2 B3 Caa1 Caa2 Caa3 Ca-C

One Year Five Year

$5 $13$59

$140

$203

$46$16 $10 $7

$281$330

$39$6

$41 $40

$0

$100

$200

$300

$400

1995 1996 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

0

50

100

150

200

250

300

$ defaults # of defaults

Source: “Corporate Default and Recovery Rates,” Moody’s Investors Service, February 2011

Economic cycles significantly affect default volume

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

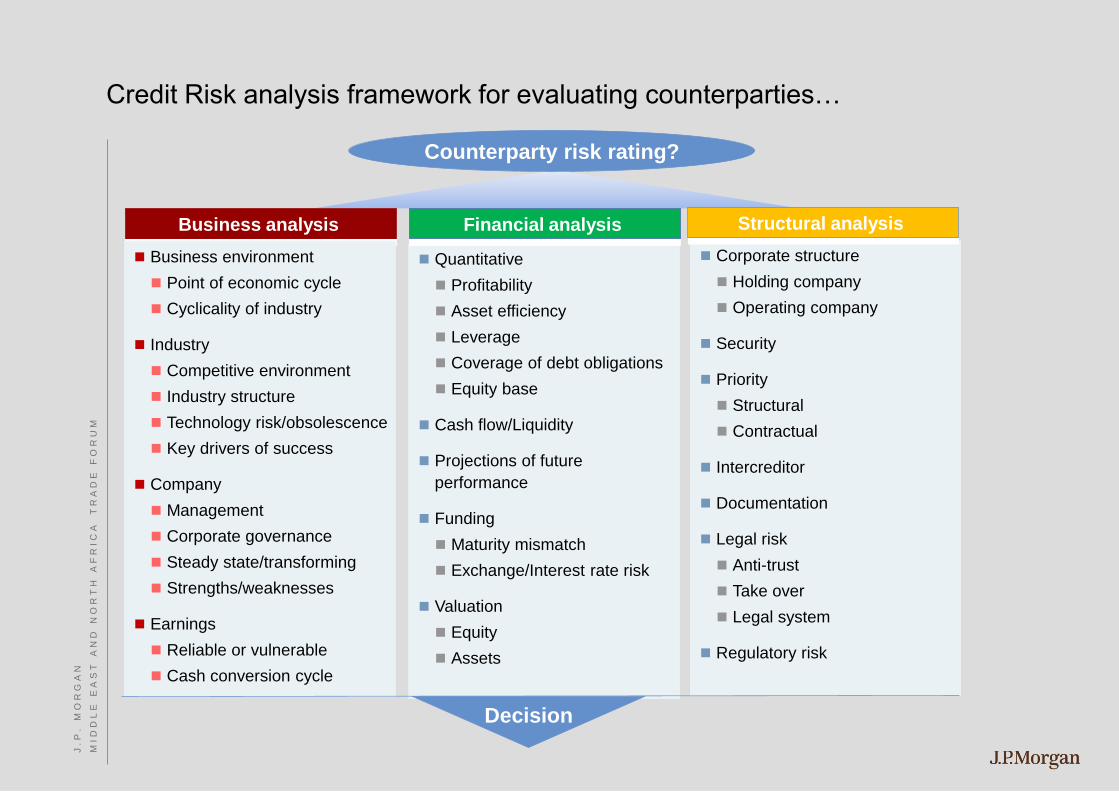

Credit Risk analysis framework for evaluating counterparties…

Quantitative

Profitability

Asset efficiency

Leverage

Coverage of debt obligations

Equity base

Cash flow/Liquidity

Projections of future

performance

Funding

Maturity mismatch

Exchange/Interest rate risk

Valuation

Equity

Assets

Corporate structure

Holding company

Operating company

Security

Priority

Structural

Contractual

Intercreditor

Documentation

Legal risk

Anti-trust

Take over

Legal system

Regulatory risk

Business analysis Financial analysis Structural analysis

Business environment

Point of economic cycle

Cyclicality of industry

Industry

Competitive environment

Industry structure

Technology risk/obsolescence

Key drivers of success

Company

Management

Corporate governance

Steady state/transforming

Strengths/weaknesses

Earnings

Reliable or vulnerable

Cash conversion cycle

Decision

Counterparty risk rating?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

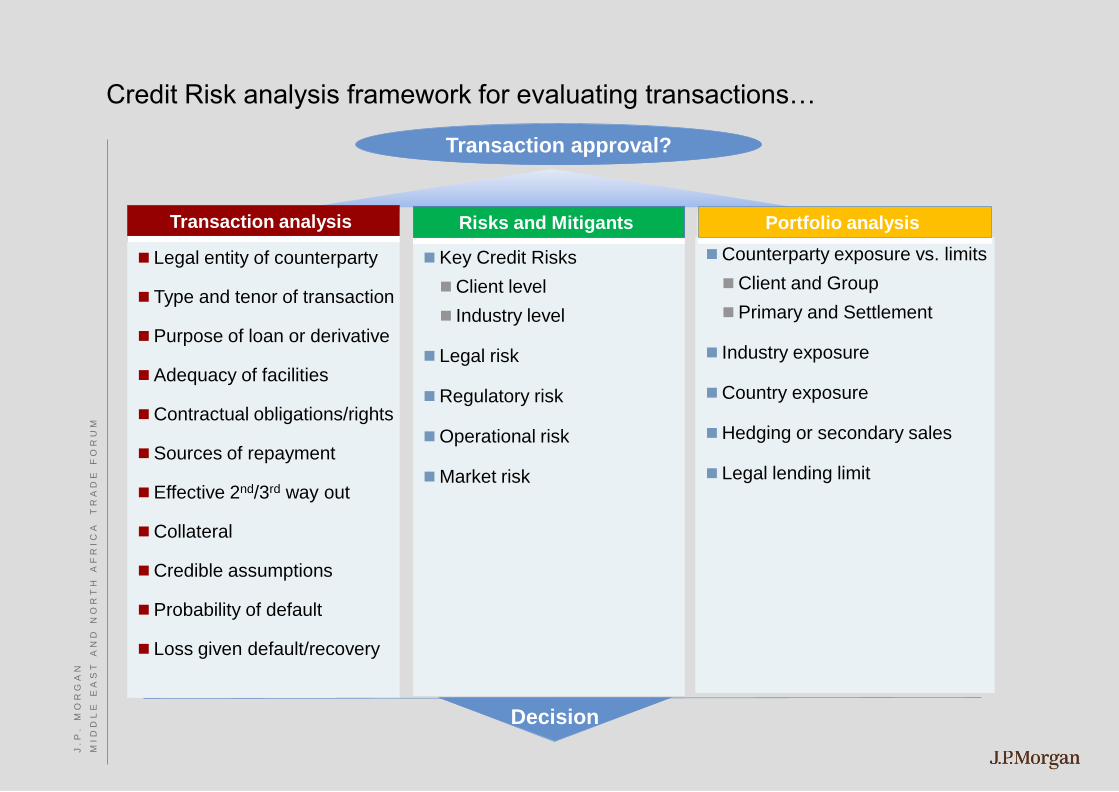

Credit Risk analysis framework for evaluating transactions…

Key Credit Risks

Client level

Industry level

Legal risk

Regulatory risk

Operational risk

Market risk

Counterparty exposure vs. limits

Client and Group

Primary and Settlement

Industry exposure

Country exposure

Hedging or secondary sales

Legal lending limit

Transaction analysis Risks and Mitigants Portfolio analysis

Legal entity of counterparty

Type and tenor of transaction

Purpose of loan or derivative

Adequacy of facilities

Contractual obligations/rights

Sources of repayment

Effective 2nd/3rd way out

Collateral

Credible assumptions

Probability of default

Loss given default/recovery

Decision

Transaction approval?

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

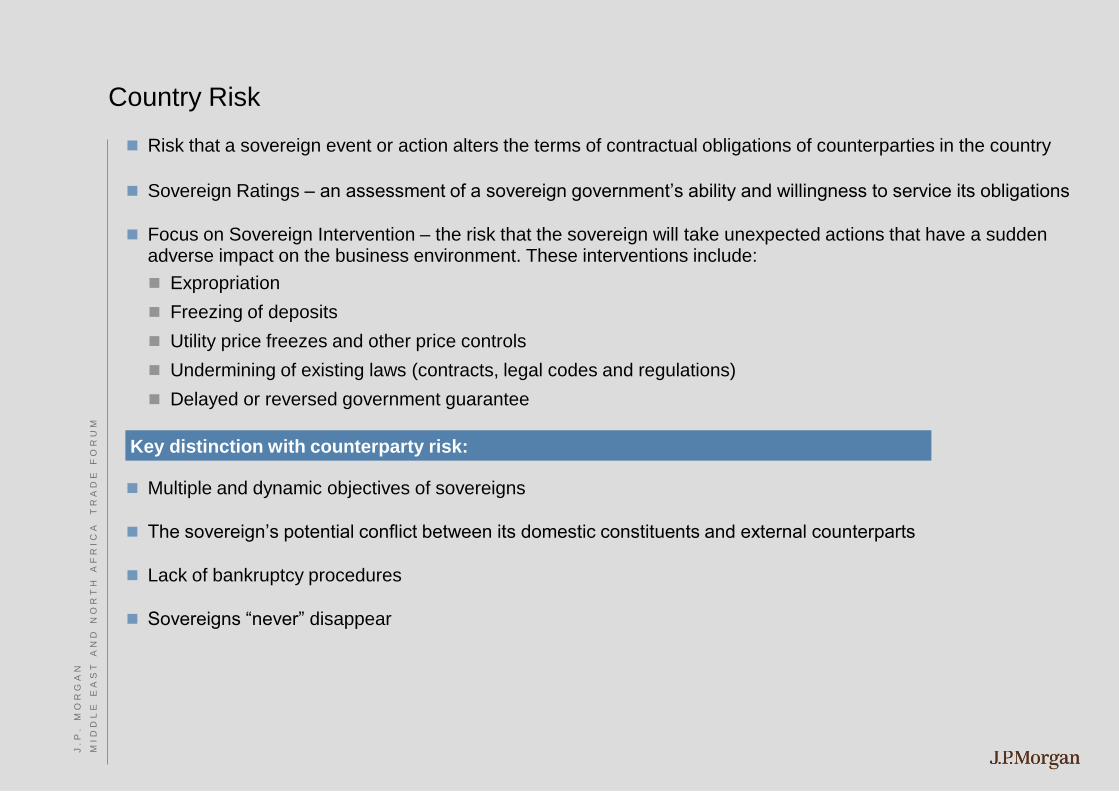

Risk that a sovereign event or action alters the terms of contractual obligations of counterparties in the country

Sovereign Ratings – an assessment of a sovereign government’s ability and willingness to service its obligations

Focus on Sovereign Intervention – the risk that the sovereign will take unexpected actions that have a sudden adverse impact on the business environment. These interventions include:

Expropriation

Freezing of deposits

Utility price freezes and other price controls

Undermining of existing laws (contracts, legal codes and regulations)

Delayed or reversed government guarantee

Multiple and dynamic objectives of sovereigns

The sovereign’s potential conflict between its domestic constituents and external counterparts

Lack of bankruptcy procedures

Sovereigns “never” disappear

Country Risk J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Key distinction with counterparty risk:

Reputation Risk

Exists in virtually every activity, transaction and relationship

Reputation risk is hard to measure and difficult to discern

It can lead to lost business and ultimately a failure of confidence by our clients and counterparties.

Such failure has in the past resulted in failure of financial firms

It can impair our relationship with our regulators

It can affect our ability to attract the best employees

Reputation risk is among the most complex risks facing a financial institution

Definition: The potential for loss of confidence in an institution’s integrity resulting

from adverse publicity – true or not – over its practices and associations

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Managing Reputation Risk

Individual accountability and responsibility for working in a manner consistent with

the highest ethical standard

Vetting clients and transactions

Due diligence

Investigations

Approval process

Internal escalation process

Reputation Risk Committees

LOB Risk Committees

Conflicts Office

Risk Control oversight functions

Compliance

Audit

Policies

While we cannot remove reputation risk, we can make efforts to minimize it

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Slower economic growth in most developed markets

Sovereign debt default concerns in the Eurozone

Political instability in Middle East and North Africa

Regulatory and political scrutiny of the banking industry

Higher capital and liquidity requirements under Basel III

Emerging markets still transforming

J.P. Morgan expansion into new countries in Sub-Saharan Africa

Recent market events are unprecedented and pose tremendous challenges

What are the background issues that J.P. Morgan Risk Management are currently dealing with?

Credit Challenges in 2012 J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

Middle East and North Africa Turmoil J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

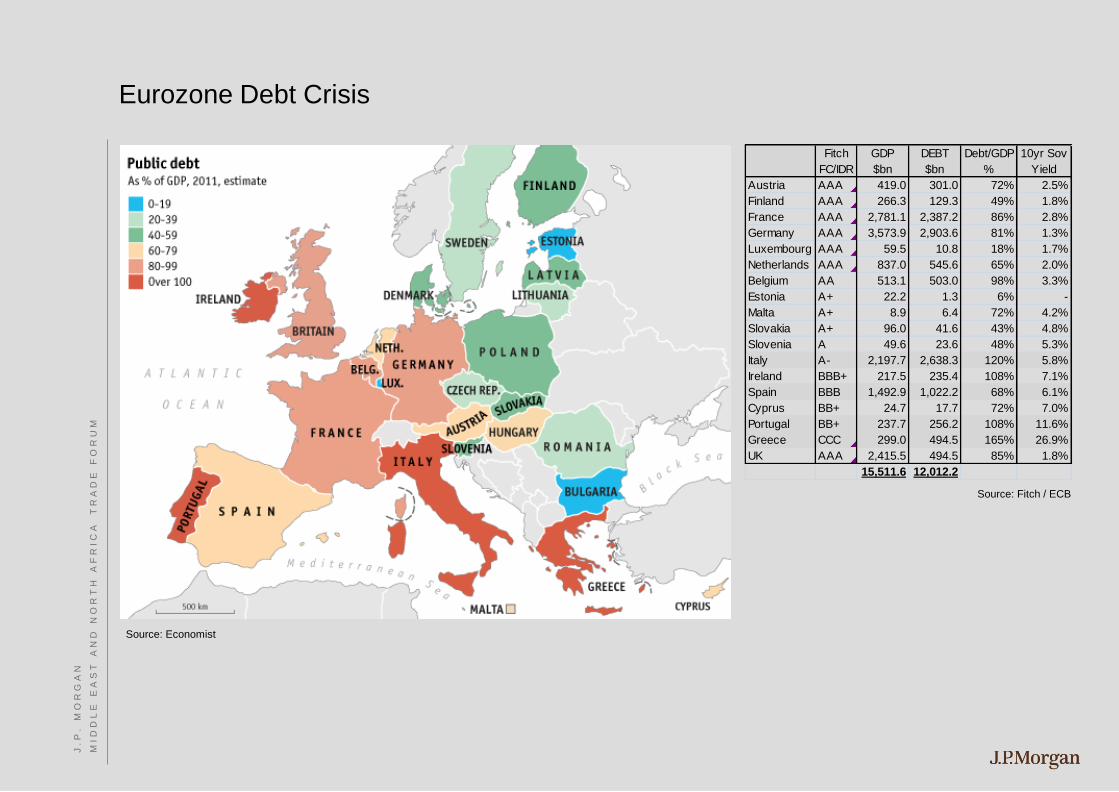

Eurozone Debt Crisis

Source: Economist

Source: Fitch / ECB

Fitch

FC/IDR

GDP

$bn

DEBT

$bn

Debt/GDP

%

10yr Sov

Yield

Austria AAA 419.0 301.0 72% 2.5%

Finland AAA 266.3 129.3 49% 1.8%

France AAA 2,781.1 2,387.2 86% 2.8%

Germany AAA 3,573.9 2,903.6 81% 1.3%

Luxembourg AAA 59.5 10.8 18% 1.7%

Netherlands AAA 837.0 545.6 65% 2.0%

Belgium AA 513.1 503.0 98% 3.3%

Estonia A+ 22.2 1.3 6% -

Malta A+ 8.9 6.4 72% 4.2%

Slovakia A+ 96.0 41.6 43% 4.8%

Slovenia A 49.6 23.6 48% 5.3%

Italy A- 2,197.7 2,638.3 120% 5.8%

Ireland BBB+ 217.5 235.4 108% 7.1%

Spain BBB 1,492.9 1,022.2 68% 6.1%

Cyprus BB+ 24.7 17.7 72% 7.0%

Portugal BB+ 237.7 256.2 108% 11.6%

Greece CCC 299.0 494.5 165% 26.9%

UK AAA 2,415.5 494.5 85% 1.8%

15,511.6 12,012.2

J . P

.

M O

R G

A N

M I

D D

L E

E

A S

T A

N D

N

O R

T H

A

F R

I C

A

T R

A D

E

F O

R U

M

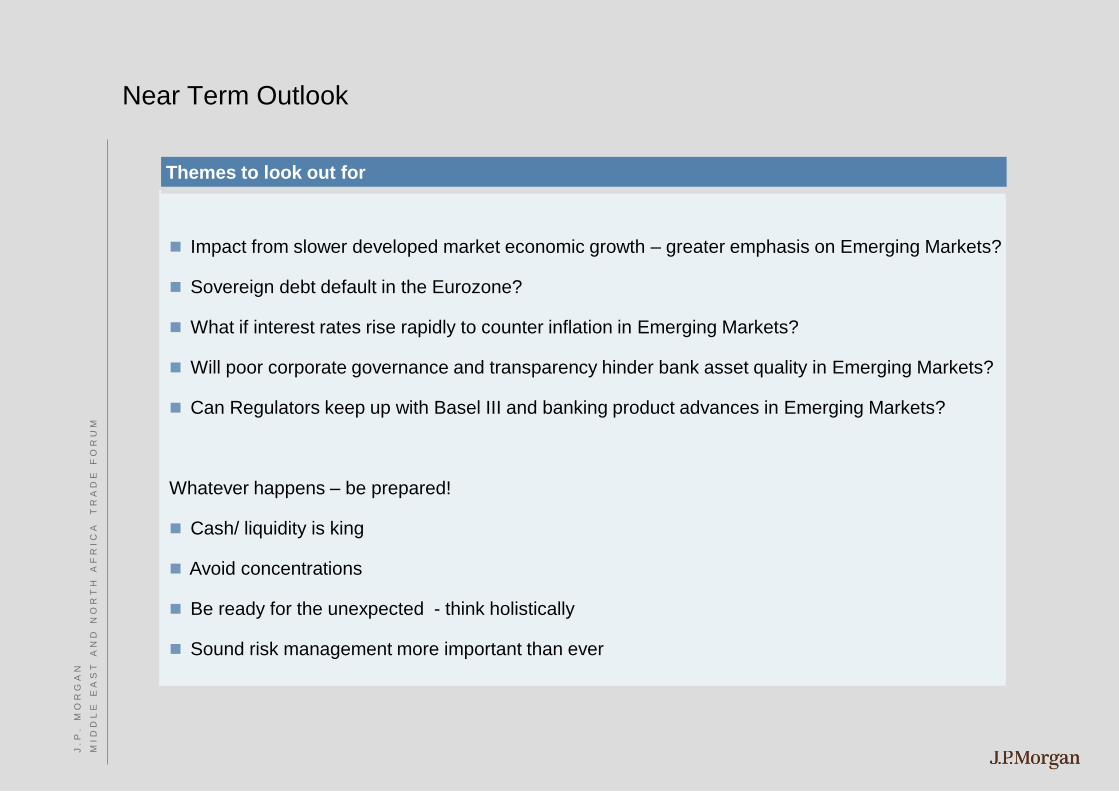

Impact from slower developed market economic growth – greater emphasis on Emerging Markets?

Sovereign debt default in the Eurozone?