july 20, 2018 abb india (abb) -...

TRANSCRIPT

Initiating Coverage

ICICI Securities Ltd | Retail Equity Research

July 20, 2018

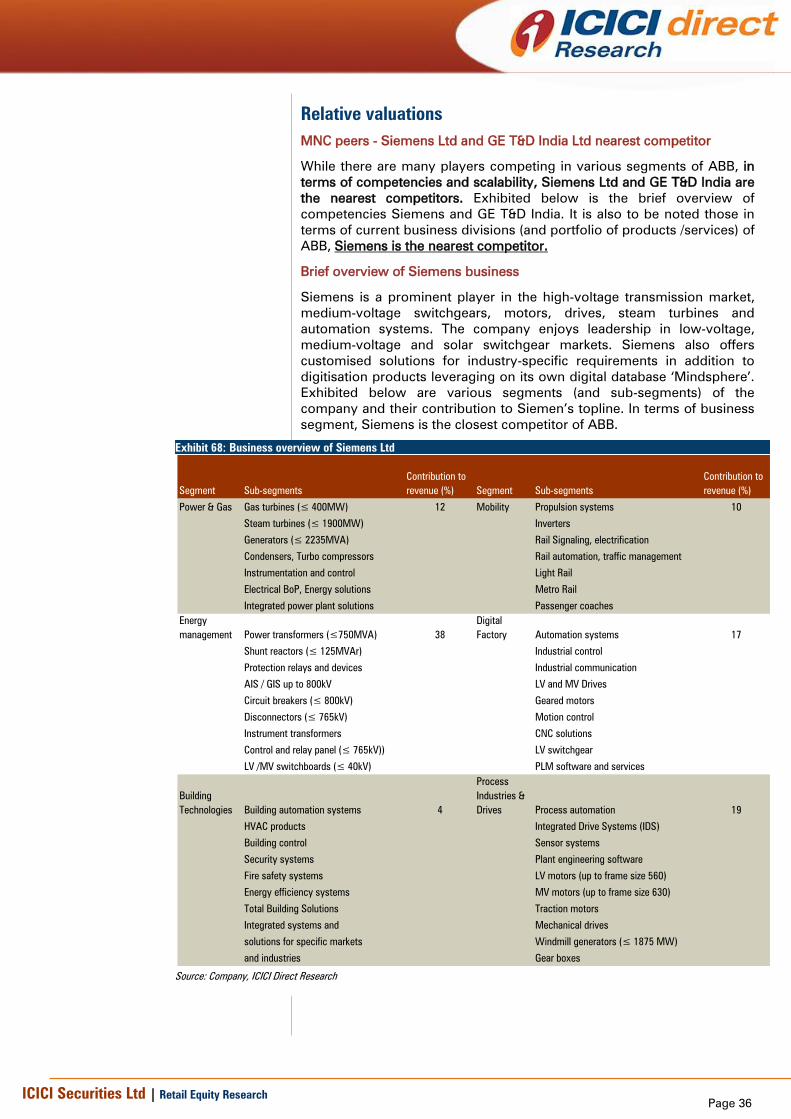

Leader in automation technology…

ABB India (ABB) is an Indian subsidiary (75%) of Swedish-Swiss based

global company ABB Ltd. With over 69 years of domestic operations,

ABB’s key business segment includes power grids (transformers, sub-

stations, HVDC, grid stabilisation/automation systems), electrification

products (switchgears, solar inverters, EV chargers), robotics and motion

(industrial robots, drives, motors, generators) and industrial automation

(process automation, enterprise solutions) serving customers in utilities,

industry and transport & infrastructure. With strong competencies and

technology leadership in most of the above segments, proven expertise

in execution, healthy b/s and large anticipated spends in these segments,

we believe ABB will deliver a healthy performance, going forward.

Capex in power T&D, smart grid solutions, railways gives strong visibility

We believe ABB will be a key beneficiary of planned capex spends of

| 2,60,000 crore in FY17-22E in the T&D segment. Under-investment in the

T&D segment, upgradation to high voltage network and 'Power for all'

initiative of current governments is likely to help ABB keep its order book

ticking. ABB, a pioneer in smart grid solutions, is also likely to benefit

from improved allocation in smart-grid programmes (| 980 crore in

Twelfth Plan) due to accelerated pace of addition in renewables (175 GW

by FY22E). Electrification of railways, 30,000 ckm by FY22E by spending

~| 35,000 crore, introduction of electric locomotives (~| 10,000 crore

opportunity), spends on network expansion/ de-congestion and slew of

metro projects across the country are likely to open up opportunities for

ABB’s best-in-class electrification and power solutions (transformers,

turbochargers, etc.) Thus, we expect these key segments, i.e. power grids

and electrification to grow at 9.5% and 13.9%, respectively, in CY17-19E.

Industry solutions, renewables, E-cars to bring new growth opportunities

ABB's industrial solutions segment is also poised to grow at 9.5% CAGR

with a pick-up of industrial capex and high value-added propositions like

ABB AbilityTM. On the renewables front, ABB's leadership in solar

inverters, step-up transformers and grid stabilisation systems is likely to

open opportunities of over | 8500 crore in FY19-22E. In the E-mobility

segment, ABB's technical prowess in charging infrastructure space is also

to augur well for the company. With all cylinders firing and robust existing

order book of | 11,628 crore, we believe ABB will clock revenue, EBITDA

and PAT growth of 14%, 20.5% and 21.3% CAGR, respectively, in CY17-

19E. ABB has always traded at premium multiples due to its strong

technical capabilities (15-year average P/E at 58x). We value the company

at 48x CY19E earnings (20% discount to average P/E) to arrive at a target

price of | 1400. We initiate coverage with a BUY recommendation.

Exhibit 1: Valuation Metrics

(| crore) CY15 CY16 CY17 CY18E CY19E

Revenues 8,140 8,648 9,087 10,378 11,819

EBITDA 713 747 736 880 1,068

Net Profit 300 376 420 505 619.3

EPS (|) 14.2 17.8 19.8 23.9 29.2

P/E (x) 80.6 64.2 57.5 47.8 39.0

Price / Book (x) 8.0 7.4 6.7 6.1 5.4

EV/EBITDA (x) 33.9 31.6 30.8 25.8 21.0

RoCE (%) 11.9 17.5 23.2 24.8 25.5

RoE (%) 10.0 11.4 11.6 12.7 13.9

Source: Company, ICICI Direct Research

ABB India (ABB) | 1140

| 1200

Rating Matrix

Rating Matrix

Rating : Buy

Target : | 1400

Target Period : 12 - 15 months

Potential Upside : 23%

Key Financials

| Crore CY16 CY17 CY18E CY19E

Revenue 8,648 9,087 10,378 11,819

EBITDA 747 736 880 1,068

EBITDA margin 8.6% 8.1% 8.5% 9.0%

Net Profit 376 420 505 619

EPS (|) 17.8 19.8 23.9 29.2

Valuation Summary

(x) CY16 CY17 CY18E CY19E

P/E 64.2 57.5 47.8 39.0

Target P/E 78.8 70.6 58.7 47.9

EV / EBITDA 31.6 30.8 25.8 21.0

P/BV 7.4 6.7 6.1 5.4

RoNW (%) 11 11.6 12.7 13.9

RoCE (%) 17.5 23.2 24.8 25.5

Stock Data

Stock Data

Average Volumes (shares) 55031

Market Capitalization | 24158 Crore

Total Debt (CY17) | 8 Crore

Cash and Investments (CY17) | 1491.6 crore

EV (CY17) | 22673.9 Crore

52 week H/L (BSE) (|) 1744 / 1123

Equity capital | 42.4 Crore

Face value | 2

MF Holding (%) 5.8

FII Holding (%) 3.1

Promoter Holding (%) 75

Price Performance

Return (%) 1M 3M 6M 12M

ABB India Ltd (4.2) (7.4) (27.0) (20.4)

Siemens Ltd (5.3) (11.3) (27.4) (30.4)

GE T&D India Ltd (6.6) (25.9) (32.6) (10.6)

Price Movement

6,000

7,000

8,000

9,000

10,000

11,000

12,000

0

300

600

900

1,200

1,500

1,800

Jul-18Jan-

18

Aug-

17

Feb-

17

Aug-

16

Feb-

16

Aug-

15

ABB (R.H.S) Nifty (L.H.S)

Research Analyst

Chirag J Shah

Sagar K Gandhi

Page 2 ICICI Securities Ltd | Retail Equity Research

Company background

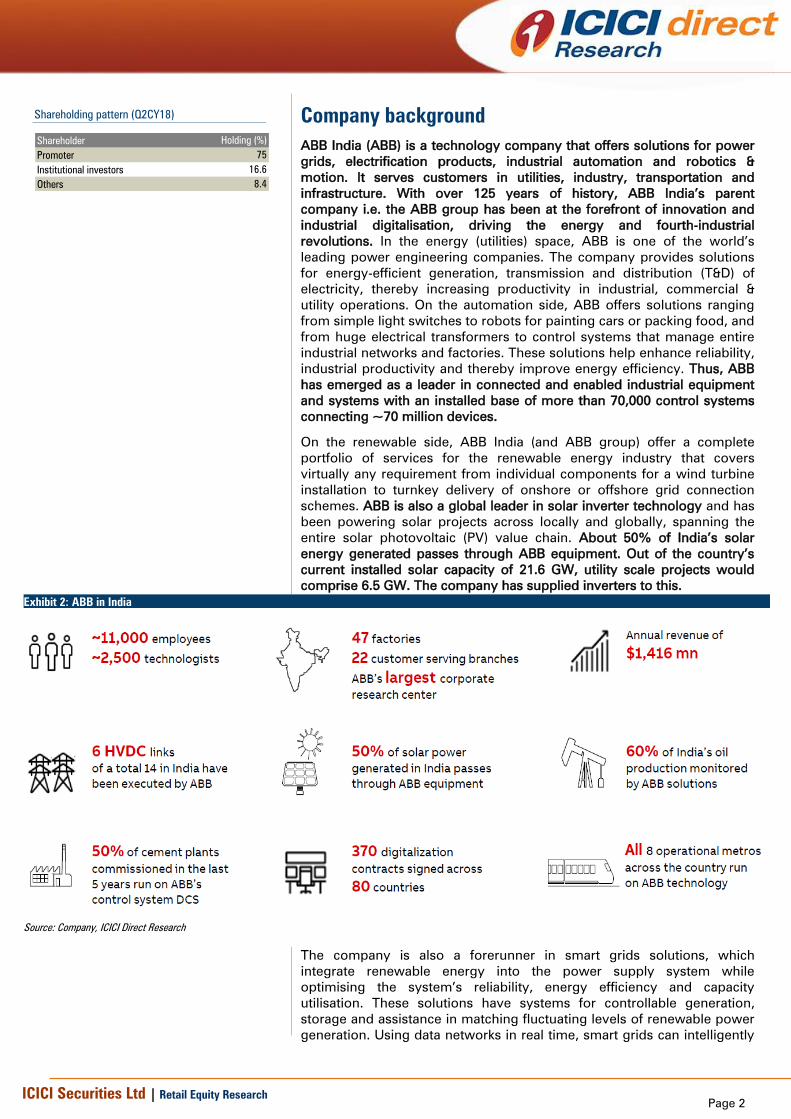

ABB India (ABB) is a technology company that offers solutions for power

grids, electrification products, industrial automation and robotics &

motion. It serves customers in utilities, industry, transportation and

infrastructure. With over 125 years of history, ABB India’s parent

company i.e. the ABB group has been at the forefront of innovation and

industrial digitalisation, driving the energy and fourth-industrial

revolutions. In the energy (utilities) space, ABB is one of the world’s

leading power engineering companies. The company provides solutions

for energy-efficient generation, transmission and distribution (T&D) of

electricity, thereby increasing productivity in industrial, commercial &

utility operations. On the automation side, ABB offers solutions ranging

from simple light switches to robots for painting cars or packing food, and

from huge electrical transformers to control systems that manage entire

industrial networks and factories. These solutions help enhance reliability,

industrial productivity and thereby improve energy efficiency. Thus, ABB

has emerged as a leader in connected and enabled industrial equipment

and systems with an installed base of more than 70,000 control systems

connecting ~70 million devices.

On the renewable side, ABB India (and ABB group) offer a complete

portfolio of services for the renewable energy industry that covers

virtually any requirement from individual components for a wind turbine

installation to turnkey delivery of onshore or offshore grid connection

schemes. ABB is also a global leader in solar inverter technology and has

been powering solar projects across locally and globally, spanning the

entire solar photovoltaic (PV) value chain. About 50% of India’s solar

energy generated passes through ABB equipment. Out of the country’s

current installed solar capacity of 21.6 GW, utility scale projects would

comprise 6.5 GW. The company has supplied inverters to this.

Exhibit 2: ABB in India

Source: Company, ICICI Direct Research

The company is also a forerunner in smart grids solutions, which

integrate renewable energy into the power supply system while

optimising the system’s reliability, energy efficiency and capacity

utilisation. These solutions have systems for controllable generation,

storage and assistance in matching fluctuating levels of renewable power

generation. Using data networks in real time, smart grids can intelligently

Shareholding pattern (Q2CY18)

Shareholder Holding (%)

Promoter 75

Institutional investors 16.6

Others 8.4

Page 3 ICICI Securities Ltd | Retail Equity Research

and automatically control these increasingly complex power systems. The

ABB group is a pioneer in micro grid technology with more than 30 global

installations across a diverse range of applications serving remote

communities, islanded grids, utility grid support and industrial campuses.

Brief history of ABB India

ABB’s origins in India go back several decades when Asea was set up as

an agency in 1928. The company was incorporated in 1949 as the

Hindustan Electric Company and later became Hindustan Brown Boveri

(HBB) in 1965. Following the amalgamation with Asea Ltd in 1989 it

became Asea Brown Boveri. The name was changed to ABB Ltd in 2003.

Today, ABB has a local presence with 47 factories across nine

manufacturing locations and 22 sales & marketing offices across India.

The company’s major plants are at Bangalore, Faridabad, Haridwar,

Mumbai, Nashik and Vadodara. ABB India also exports to over 100

countries and has employee strength of 5590 (permanent) employees.

Exhibit 3: Brief history and key milestones of ABB India

2013-17

2001- 12

1949-881989- 2000

• Co. renamed as Asea Brown Boveri Ltd in

1989 after merger of Asea, Sweden & BBC

Brown Boveri, Switzerland

• Commissioned first high voltage direct

current transmission link for connecting

Northern & Western power grids

• Commissioned process control system for

petrochemical complex for RIL Ltd

• Launched new 400 KV transformers

• Wins order for power products, automaton

systems for Delhi International Airport

Terminal (T3)

• Sets up state-of-the-art manufacturing

facility near Bangalore

• Inaugurates global wind power generator

factory in India

• Inaugurates new facility for miniature

circuit breakers, residual current circuit

breakers and surge protection devices

• Incorporated as Hindustan Electric Co. Ltd in

1949 to manufacture power products

(transformers, electric motors, conductors,

furnaces, etc)

• Name changed to Hindustan Brown Boveri

after collaboration with Switzerland's Brown

Boveri in 1965

• Pioneered manufacture of industrial steam

engines, switch gears, relays and signals for

railways, etc.

• Receives order from PGCIL to construct

switchgear substation to boost transmission

capacity in the southern region. Name

changed to ABB India Ltd

• Introduced first 800kV converter transformer.

Integrates power from world’s largest solar

plants to national transmission grid

• Doubles solar inverter manufacturing

capacity. Wins order to supply 1600

transformers to railways

Source: Company, ICICI Direct Research

The parent company was started by Charles Brown and

Walter Boveri in Switzerland in 1891.

Page 4 ICICI Securities Ltd | Retail Equity Research

ABB’s business segments, revenue break-up & clientele

ABB’s business segments

ABB’s business can be broadly classified into four main segments, ‘power

grids’, ‘electrification products’, ‘robotics and motion’ and ‘industrial

automation’. The company’s business segments are organised around

products and (system) solutions provided to its customers, including

utilities, industries, channel partners & original equipment manufacturers.

Exhibit 4: ABB’s offerings for customers

Source: Company, ICICI Direct Research

Exhibit 5: ABB’s key business segments

Power Grids

ABB's key business segments

Electrification Products

Industrial Automation

Robotics & Motion

Source: Company, ICICI Direct Research

ABB’s revenue segmentation/break-up

Over the last three fiscals (CY15-17), the break-down of ABB’s average

operating revenues is as follows: As seen in the above exhibit, ABB earns

majority of its revenue from the power grids segment (~41%) followed by

electrification products (~24%), robotics & motions (~22%) and industrial

automation (~16%).

Exhibit 6: Revenue segmentation

Revenue break-up CY15 CY16 CY17 CY15-17

Power Grids 3533 3691 3832 11056

As % of total 43.4 40.2 40.9 41.4

Robotics and Motion 2062 1936 1936 5934

As % of total 25.3 21.1 20.6 22.2

Electrification Products 1651 2390 2439 6480

As % of total 20.3 26.0 26.0 24.3

Industrial Automation 1337 1485 1409 4231

As % of total 16.4 16.2 15.0 15.8

Total 8140 9184 9375 26699

Source: Company, ICICI Direct Research

Exhibit 7: ABB’s key business segments

Revenue break-up CY15-17

Power Grids

41%

Robotics and

Motion

21%

Electrification

Products

23%

Industrial

Automation

15%

`

Source: Company, ICICI Direct Research

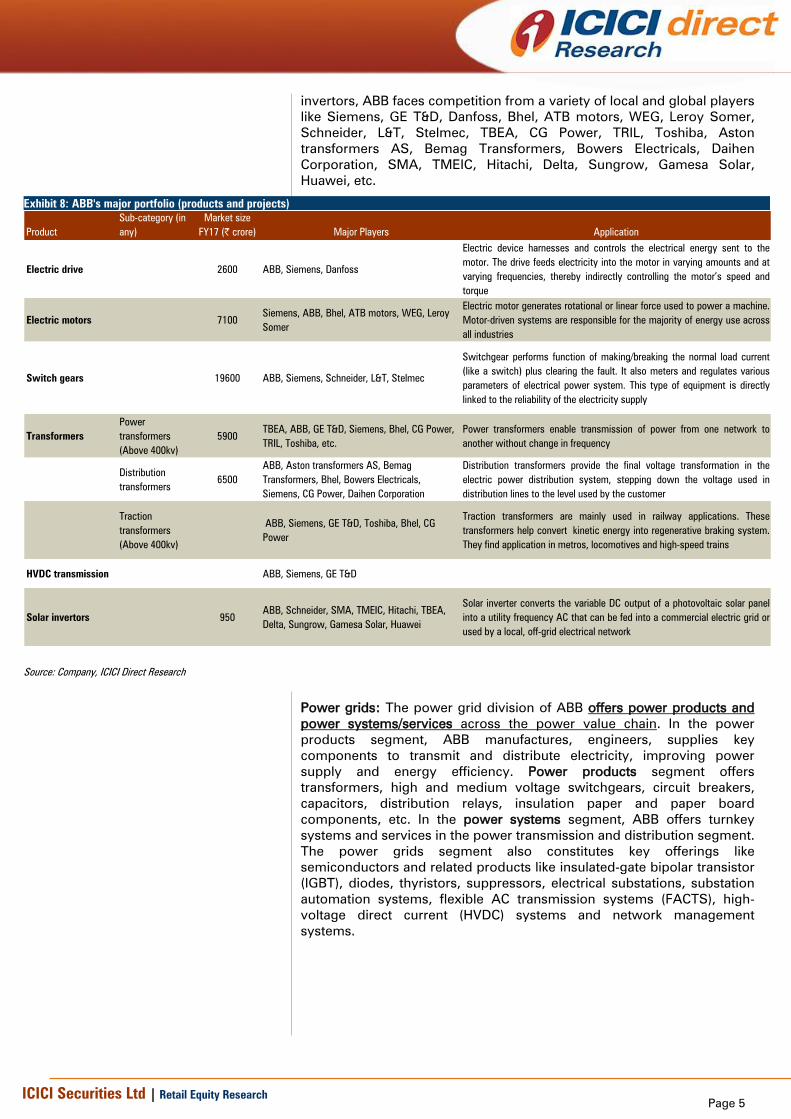

ABB derives its revenues from three major segments – products, projects

and services. The first two segments together contribute ~93% of

revenues while services contribute the remaining ~7%. In the products

and projects segments, the major products and projects that ABB offers is

exhibited below. In each category such as electric drives, electric motors,

switch gears, transformers (power transformers, distribution

transformers, traction transformers), HVDC transmission projects, solar

Page 5 ICICI Securities Ltd | Retail Equity Research

invertors, ABB faces competition from a variety of local and global players

like Siemens, GE T&D, Danfoss, Bhel, ATB motors, WEG, Leroy Somer,

Schneider, L&T, Stelmec, TBEA, CG Power, TRIL, Toshiba, Aston

transformers AS, Bemag Transformers, Bowers Electricals, Daihen

Corporation, SMA, TMEIC, Hitachi, Delta, Sungrow, Gamesa Solar,

Huawei, etc.

Exhibit 8: ABB's major portfolio (products and projects)

Product

Sub-category (in

any)

Market size

FY17 (| crore) Major Players Application

Electric drive 2600 ABB, Siemens, Danfoss

Electric device harnesses and controls the electrical energy sent to the

motor. The drive feeds electricity into the motor in varying amounts and at

varying frequencies, thereby indirectly controlling the motor’s speed and

torque

Electric motors 7100

Siemens, ABB, Bhel, ATB motors, WEG, Leroy

Somer

Electric motor generates rotational or linear force used to power a machine.

Motor-driven systems are responsible for the majority of energy use across

all industries

Switch gears 19600 ABB, Siemens, Schneider, L&T, Stelmec

Switchgear performs function of making/breaking the normal load current

(like a switch) plus clearing the fault. It also meters and regulates various

parameters of electrical power system. This type of equipment is directly

linked to the reliability of the electricity supply

Transformers

Power

transformers

(Above 400kv)

5900

TBEA, ABB, GE T&D, Siemens, Bhel, CG Power,

TRIL, Toshiba, etc.

Power transformers enable transmission of power from one network to

another without change in frequency

Distribution

transformers

6500

ABB, Aston transformers AS, Bemag

Transformers, Bhel, Bowers Electricals,

Siemens, CG Power, Daihen Corporation

Distribution transformers provide the final voltage transformation in the

electric power distribution system, stepping down the voltage used in

distribution lines to the level used by the customer

Traction

transformers

(Above 400kv)

ABB, Siemens, GE T&D, Toshiba, Bhel, CG

Power

Traction transformers are mainly used in railway applications. These

transformers help convert kinetic energy into regenerative braking system.

They find application in metros, locomotives and high-speed trains

HVDC transmission ABB, Siemens, GE T&D

Solar invertors 950

ABB, Schneider, SMA, TMEIC, Hitachi, TBEA,

Delta, Sungrow, Gamesa Solar, Huawei

Solar inverter converts the variable DC output of a photovoltaic solar panel

into a utility frequency AC that can be fed into a commercial electric grid or

used by a local, off-grid electrical network

Source: Company, ICICI Direct Research

Power grids: The power grid division of ABB offers power products and

power systems/services across the power value chain. In the power

products segment, ABB manufactures, engineers, supplies key

components to transmit and distribute electricity, improving power

supply and energy efficiency. Power products segment offers

transformers, high and medium voltage switchgears, circuit breakers,

capacitors, distribution relays, insulation paper and paper board

components, etc. In the power systems segment, ABB offers turnkey

systems and services in the power transmission and distribution segment.

The power grids segment also constitutes key offerings like

semiconductors and related products like insulated-gate bipolar transistor

(IGBT), diodes, thyristors, suppressors, electrical substations, substation

automation systems, flexible AC transmission systems (FACTS), high-

voltage direct current (HVDC) systems and network management

systems.

Page 6 ICICI Securities Ltd | Retail Equity Research

Exhibit 9: Power grids – Offerings

Power Grids

• Control Systems

• Power Converters &

Inverters

• Power Plant

Automation &

Optimisation

• Turbine Control

• Turnkey Power Plant

Solutions

• FACTS

• HVDC

• Microgrids

Substations and

Electrification

• AIS Substations

• GIS Substations

• Hybrid Substations

• Mobile Substations

• Containerised&

Prefabricated

Substations

• Energy Storage

Solutions

Semiconductors

• IGBT & Diode

Modules

• Press-pack IGBT

Modules

• Insulated gate-

commutated

thyristors (IGCT)

• Thyristors

• Diodes

• Gate turn-off

thyristors (GTO)

• Silicon surge voltage

Substations Automation

Protection & Control

• Substation Automation

Systems

• Substation Automation

Products

• Distribution

Automation Systems

• Distribution

Automation Products

Source: Company, ICICI Direct Research

Electrification products: Electrification products segment (EP) includes

medium voltage and low voltage products like circuit breakers, switches,

control products, wiring accessories, enclosures and cable systems to

protect people, installations and electronic equipment from electrical

overload. The division further makes KNX systems that integrate and

automate a building’s electrical installations, ventilation systems and

security & data communication networks. KNX systems are standardised

OSI-based network communications protocols for building automation

systems. Electrification products also incorporate an electrification

solutions unit that manufactures low voltage switchgear and motor

control centres. Customers for electrification product include a wide

range of industry and utility operations, plus commercial and residential

buildings. Over the last couple of years, the electrification products

division has seen portfolio expansion with the inclusion of

Solar business (solar inverters, micro grid solutions, energy

storage solutions, etc),

Power quality businesses (UPS, switches, etc) and

Electric vehicle charging (standard chargers, fast chargers)

ABB group (parent co of ABB India) acquired GE Industrial

Solutions to gain a foothold in the electrification product

space in the US and Europe. The acquisition process is

underway and is likely to be over by H2CY18…

Page 7 ICICI Securities Ltd | Retail Equity Research

Exhibit 10: Electrification Products –Offerings

Medium voltage

products

• Modular systems

• Switchgears

• Apparatus

• Distribution

automation &

protection

• Services

Low voltage

products/systems

• Electrical

installation

• Electrical

distribution

• Automation

control &

protection

• Building

technologies

Solar inverters

• String inverters

• Turnkey stations

• Software tools

• Central inverters

• Energy storage

Solutions

• Microgrid solutions

• Legacy inverters

• Monitoring &

communication

EV charging

infrastructure

• Multi-standard

fast chargers

• Single-standard

fast chargers

• Highway & en

route fast

chargers

• Chargers for EV

dealers &

commercial

locations

UPS & power

conditioning

• UPS systems

• Power & voltage

conditioners

• Static switches

• Power distribution

• DC chargers

Source: Company, ICICI Direct Research

Industrial automation: The main focus in this business segment is on

providing customers with integrated solutions for better control of

industrial systems and/or plant optimisation. Products offered in this

segment include control systems, measurement products, turbo-

chargers, programmable logic controllers, etc. The industries serviced

here include oil & gas, power, chemicals, pharmaceuticals, pulp & paper,

metals & minerals, marine, etc. The idea behind offering industrial

automation solutions to clients is to improve their asset productivity and

reduce cost via energy savings.

Exhibit 11: Industrial automation –Offerings

Control systems

• Control room

Consolidation

• Safety systems

• Compact product

suite

• ABB ability Symphony

plus

• ABB ability system

800xA

Turbochargers

• Turbochargers for low,

medium & high speed

engines in marine, oil &

gas, power generation,

earthmoving & mining

equipment & rail

• Efficiency enhancement

technologies such as

high-pressure tuning,

valve control

management, variable

turbine geometry &

waste heat recovery

systems

Measurement products

• Actuators

• Diesel engine

monitoring

• Web tension

measurement

• Thickness gauging

• positioners

• Level measurement

products

• Roll force

measurement

Programmable logic

controllers

• PLCs

• Automation builder

• ZenonIoTSoftware

• Control panels

• Legacy products

Source: Company, ICICI Direct Research

Page 8 ICICI Securities Ltd | Retail Equity Research

To fill some gaps in the company’s portfolio, the ABB group acquired

B&R, an Austrian company for offerings in factory automation and

machine automation.

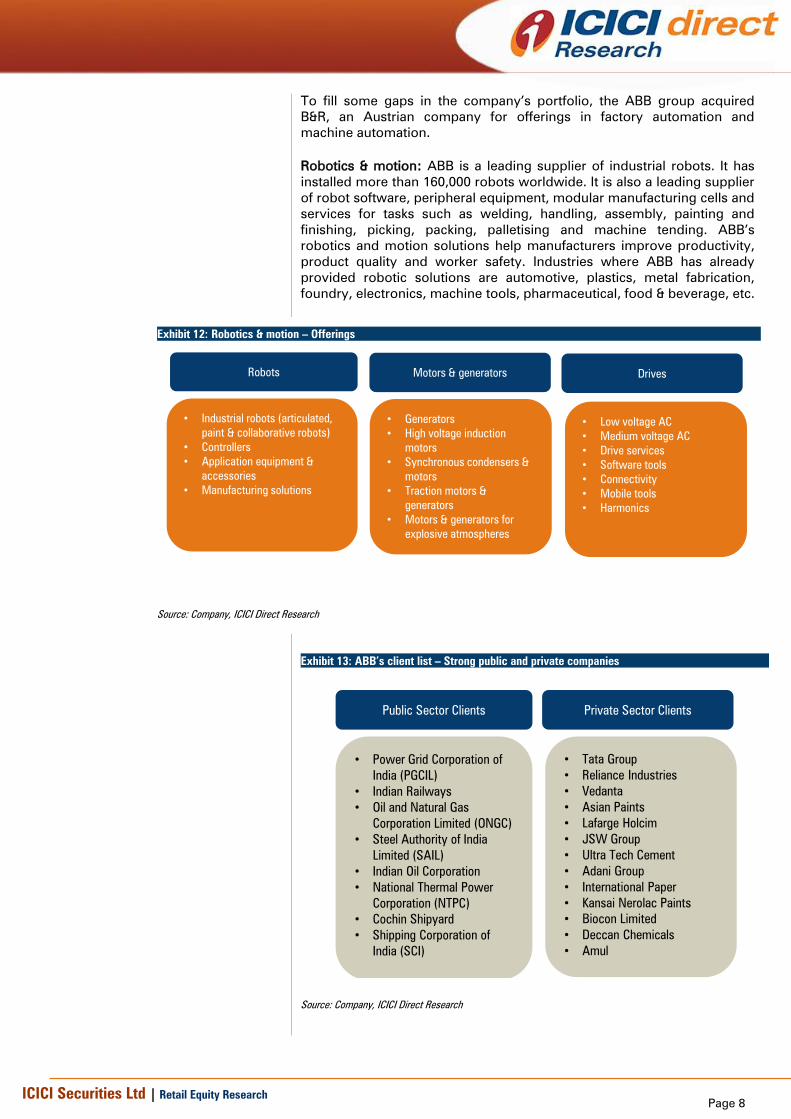

Robotics & motion: ABB is a leading supplier of industrial robots. It has

installed more than 160,000 robots worldwide. It is also a leading supplier

of robot software, peripheral equipment, modular manufacturing cells and

services for tasks such as welding, handling, assembly, painting and

finishing, picking, packing, palletising and machine tending. ABB’s

robotics and motion solutions help manufacturers improve productivity,

product quality and worker safety. Industries where ABB has already

provided robotic solutions are automotive, plastics, metal fabrication,

foundry, electronics, machine tools, pharmaceutical, food & beverage, etc.

Exhibit 12: Robotics & motion – Offerings

Robots

• Industrial robots (articulated,

paint & collaborative robots)

• Controllers

• Application equipment &

accessories

• Manufacturing solutions

Motors & generators

• Generators

• High voltage induction

motors

• Synchronous condensers &

motors

• Traction motors &

generators

• Motors & generators for

explosive atmospheres

Drives

• Low voltage AC

• Medium voltage AC

• Drive services

• Software tools

• Connectivity

• Mobile tools

• Harmonics

Source: Company, ICICI Direct Research

Exhibit 13: ABB’s client list – Strong public and private companies

Public Sector Clients

• Power Grid Corporation of

India (PGCIL)

• Indian Railways

• Oil and Natural Gas

Corporation Limited (ONGC)

• Steel Authority of India

Limited (SAIL)

• Indian Oil Corporation

• National Thermal Power

Corporation (NTPC)

• Cochin Shipyard

• Shipping Corporation of

India (SCI)

Private Sector Clients

• Tata Group

• Reliance Industries

• Vedanta

• Asian Paints

• Lafarge Holcim

• JSW Group

• Ultra Tech Cement

• Adani Group

• International Paper

• Kansai Nerolac Paints

• Biocon Limited

• Deccan Chemicals

• Amul

Source: Company, ICICI Direct Research

Page 9 ICICI Securities Ltd | Retail Equity Research

Investment Rationale

Leveraging upcoming capex spend in T&D segment

The Indian power sector has significantly evolved over the past 10-15

years with successive governments moving steadily on a ‘Power for all’

initiative. Towards this, subsequent governments have formulated a

number of policies and spent huge sums building capacities in the power

value chain (generation, transmission & distribution). While capacities in

the ‘generation’ segment have been built at a significant pace,

transmission and distribution (T&D) capacities have lagged in pace over

the last decade. As exhibited in the table below, capacities in the

generation segment have grown at 8.9% CAGR in FY08-18. In the same

period, capacities in the T&D segment have grown at only 6.3% and

8.5%, respectively. For a fully strengthened network, additions in the T&D

segment should outpace generation segment growth.

Exhibit 14: Capacity addition across generation, transmission and distribution over FY08-18

FY07 FY12 May-18

Capacity addtions 10th Plan 11th Plan CAGR

Generation / Transmission

Achieved as on

March 2007

Achieved as on

March 2012

Achieved as on

May 2018 FY08-18

Power Generation (MW) 132329 199877 343898 8.9%

AC transmission lines capacity (ckm) 198407 257481 393076 6.3%

Substations transformation capacity (AC)

(220 / 440 MVA) 249439 374801 617878 8.5%

Source: Central Electricity Authority, Power Sector May 2018, Company, ICICI Direct Research

From the end of the Eleventh Plan (FY12), the generation segment has

seen 70% capacity addition. Making this power available to the

population and industries at large, wherein lies the opportunity for the

transmission and distribution (T&D) segment, is important. Over the last

five to six years, inter-region transmission capex has significantly picked

up, primarily due to efforts of Power Grid Corporation of India (PGCIL).

Investments have considerably lagged on the intra-state T&D front. Going

forward, we believe generation capex will be subdued (except additions

on the renewables side) but T&D capex will ensure last-mile connectivity

will pick-up significantly. Thus, capex spends towards building

transmission lines and substations (1,05,580 ckm of transmission line, 292

MVA substations) in the Thirteenth Plan are likely to open up

opportunities for players like ABB.

Exhibit 15: Addition in power generation capacities

199877

343898

0

50000

100000

150000

200000

250000

300000

350000

400000

FY12 May-18

in M

W

Power Generation (MW)

Source: Central Electricity Authority, Power Sector May 2018, Company, ICICI Direct

Research

Exhibit 16: PGCIL accelerating inter-regional networks

27750

86450

0

20000

40000

60000

80000

100000

FY12 May-18

in M

W

Inter-regional transmission Capacity (MW)

Source: Central Electricity Authority, Power Sector May 2018, Company, ICICI Direct

Research

In fully strengthened power networks, for every MW of

generation capacity, 7 MVA of power transformation

capacity has been seen – which in India is at ~2 MVA

Page 10 ICICI Securities Ltd | Retail Equity Research

Exhibit 17: Addition in transmission capacities

257481

393076

0

100000

200000

300000

400000

500000

FY12 May-18

in M

W

AC transmission lines capacity (ckm)

1.5x

Source: Central Electricity Authority, Power Sector May 2018, Company, ICICI Direct

Research

Exhibit 18: Addition in substation trans capacities

374801

617878

0

100000

200000

300000

400000

500000

600000

700000

FY12 May-18

in M

W

Substations transformation capacity (AC) (220 / 440

MVA)

Source: Central Electricity Authority, Power Sector May 2018, Company, ICICI Direct

Research

Exhibit 19: Expected transmission systems addition during Thirteenth Plan

Expected % Growth

10th Plan

till FY07

11th Plan

till FY12

12th Plan

till FY17 Additon in 13th Plan

13th Plan

Till FY22E

In 13th plan over

12th

TRANSMISSION LINES

(a) HVDC ± 500kV/800 kV Bipole Ckm 5872 9432 15535 4280 19815 27.6%

(b) 765 kV Ckm 2184 5250 29431 27300 56731 92.8%

(c) 400 kV Ckm 75722 106819 157644 46000 203644 29.2%

(d) 230/220kV Ckm 114629 135980 162325 28000 190325 17.2%

Total–Transmission Lines Ckm 198407 257481 364935 105580 470515 28.9%

SUBSTATIONS

(a) 765 kV MVA 0 25000 155000 114000 269000 73.5%

(b) 400 kV MVA 92942 151027 234372 103000 337372 43.9%

(c) 230/220 kV MVA 156497 223774 298265 75000 373265 25.1%

Total – Substations MVA 249439 399801 687637 292000 979637 42.5%

HVDC

(a)Bi-pole link capacity MW 5000 6750 13500 14000 27500 103.7%

(b) Back-to back capacity MW 3000 3000 3000 0 3000 0.0%

Total - HVDC MW 8000 9750 16500 14000 30500 84.8%

Achieved

Source: Central Electricity Authority, National Electricity Plan Vol-II (Transmission), Central Electricity Authority, Power Sector April-2018, Company, ICICI Direct Research

Graduation to higher voltage networks entail additional spends

India is steadily moving towards a higher voltage line in its transmission

network. This is primarily to reduce losses while transmitting power over

long distances on low voltage networks. Reduction in losses is also very

important as India is planning a substantial increase in capacity inter-

regionally i.e. power transmission over long distance transmission lines.

Capacity in this segment is likely to grow from the current ~86 GW to 127

GW in FY22E.

Page 11 ICICI Securities Ltd | Retail Equity Research

Exhibit 20: Capacity addition in inter-regional networks in FY18-22E

FY12 May-18 Mar-22

Capacity addtions 11th Plan CAGR

Generation / Transmission

Achieved as on

March 2012

Achieved as on

May 2018

Targetted

achievement FY18-22E

Inter-regional transmission Capacity (MW) 27750 86450 127000 10.1%

Source: Central Electricity Authority, Power Sector May 2018, Company, ICICI Direct Research

In terms of the current transmission line network, the country has

3,93,076 circuit kilometre (ckm) of transmission lines, including both

alternating current (AC) and direct current (DC) as on May 2018. Of the

total transmission network, 220 ckm and 400 ckm transmission lines

constitute 90.6% of the total network (refer exhibit below). Similarly, the

total substation transformation capacity is at 8,34,878 MVA, of which 220

MVA and 400 MVA substations comprise 76.1% of total capacity. To

improve the efficiency of the entire power value chain, this necessitates

spends on graduating lower networks to higher ones with corresponding

spends on transformation capacity.

Exhibit 21: Graduation to higher voltage networks entails additional spends

FY07 FY12 May-18

Voltage 6th Plan 7th Plan 8th Plan 9th Plan 10th Plan 11th Plan

Transmission system Type (KV) level Unit

Achieved as on

March 2007

Achieved as on

March 2012

Achieved as on

May 2018

765 ckm 0 0 0 1160 2184 5250 35301

400 ckm 6029 19824 36142 49378 75722 106819 172263

220 ckm 46005 59631 79600 96993 114629 135980 169956

Total ckm 52034 79455 115742 147531 192535 248049 377520

(220 ckm+400 ckm) as % of total

transmission lines90.6%

HVDC ckm 0 0 1634 4738 5872 9432 15556

Total (AC+HVDC) ckm 52034 79455 117376 152269 198407 257481 393076

765 MVA 0 0 0 0 0 25000 194500

400 MVA 9330 21580 40865 60380 92942 151027 284197

220 MVA 37291 53742 84177 116363 156497 223774 333681

Total AC MVA 46621 75322 125042 176743 249439 399801 812378

(220 MVA+400 MVA) as % of total

substation transformation capacity76.1%

HVDC MW 0 0 0 5200 8200 9750 22500

AC+HVDC 46621 75322 125042 181943 257639 409551 834878

Inter-regional transmission Capacity MW 14050 27750 86450

AC Transmission lines

AC Substations Transformation Capacity

Source: Central Electricity Authority, National Electricity Plan Vol-II (Transmission), Central Electricity Authority, Power Sector April-2018, Company, ICICI Direct Research

Focus on loss reduction by state electricity boards (SEBs) to benefit ABB

Going forward, SEB’s efforts towards increasing network efficiency by

reducing AT&C losses would entail significant spends. This is likely to

open up opportunities for players like ABB given its strong portfolio in

network management systems and grid stabilisation systems such as

flexible AC systems (FACTS) and static compensators (STATCOM). Intra-

state and distribution segment capex had not picked up over the past

many years due the weak state of SEB finances. However, with

government policies and incentives in place, like launch of Ujjwal Discom

Assurance Yojana (UDAY) in November, 2015, we believe we should see

gradual progress over the next two to three years. The same is also

visible in the aggregate performance of discoms over the last two to three

years. The AT&C loss (aggregate technical and commercial loss) was at

Page 12 ICICI Securities Ltd | Retail Equity Research

21.8% in 2015-16. With the implementation of Uday over the last two and

a half years, the current AT & C losses were at 18.7%.

Going forward, as projected by Central Electricity Authority, National

Electricity Plan, the T&D segment is likely to see spends of ~ | 2,60,000

crore in 2017-22E. Of the total amount, around | 1, 60,000 crore is likely to

be spent by states and the rest by PGCIL. Considering ABB’s strong

product portfolio and long-standing presence in this segment, we believe

its power grids are likely to do well over the coming few years.

High voltage direct current (HVDC) transmission – ABB a pioneer

HVDC has emerged as the key technology for inter-connecting regions

and countries for electricity transfer as it helps transmit more power with

fewer infrastructure. The network also helps in synchronising electricity

generated from different sources. HVDC also helps connect power plants

to distant load dispatch centres and facilitates development of energy

highways to transfer large amounts of power over long distances.

In FY16-17, ABB won a mega HVDC project worth over | 4350 crore to

deliver a transmission link that will have the capacity to bring electricity to

~8 crore people. The Raigarh-Pugalur 800 kilovolt (kV) ultrahigh-voltage

direct current (UHVDC) system will connect Raigarh in Central India to

Pugalur in Tamil Nadu.

The 1,830 km link is among the longest in the world. With a capacity of

6,000 MW – the equivalent of more than six large power plants – it will be

enough to meet the electricity needs of over 8 crore people in India. The

two-way link will integrate thermal and wind energy for transmission of

power to high consumption centres located thousands of kilometre away,

supporting electricity demand in the south, when wind strength is low,

and transmitting clean energy to the north, when there is excess wind

power. This mega project is expected to be completed in 2019. The

turnkey project encompasses design, engineering, supply, installation &

commissioning while major equipment supplies include the complete

UHVDC stations, including transformers, converter valves, cooling

systems, as well as control and protection technology.

ABB has an impressive HVDC track-record in India, where it introduced

the technology over 25 years ago with the Vindhyachal project in 1989.

Raigarh-Pugalur is ABB’s sixth HVDC project in India and the second

UHVDC installation, following the multi-terminal North-East Agra link. The

1,728 km long North-East Agra UHVDC link is the world’s highest HVDC

transmission system as well as the first to have three converter stations.

The UHVDC link transmits ~6,000 MW of clean hydroelectric power from

the north east region of the country to Agra, Uttar Pradesh.

Going forward, while there are no major domestic HVDC orders in the

pipeline, some orders in the form of inter-country projects may be

finalised. They include,

Katihar (India)-Parbatipur (Bangladesh)-Bornagar (India) 765kv DC line

along with 500 MW HVDC back-to-back terminal at Parbatipur. The

total project is likely to be $ 700 million or ~| 5000 crore

500 MW HVDC bipole lines between Madurai (India) and New

Anuradhapura (Sri Lanka). The HVDC link would measure ~285 km,

including 50 km of submarine cables. The project cost is likely to be

~| 5500 crore

Overall, we estimate ABB’s ‘power grids’ division to grow at a CAGR of

9.5% in CY17-19E.

ABB India is the only Indian manufacturer to successfully

test 765 kV generator step up and tie transformers at

KEMA. The company achieved another milestone of

releasing the first batch of locally manufactured 400 kV gas

insulated switchgear (GIS) bays for the largest

transmission network in the country

Page 13 ICICI Securities Ltd | Retail Equity Research

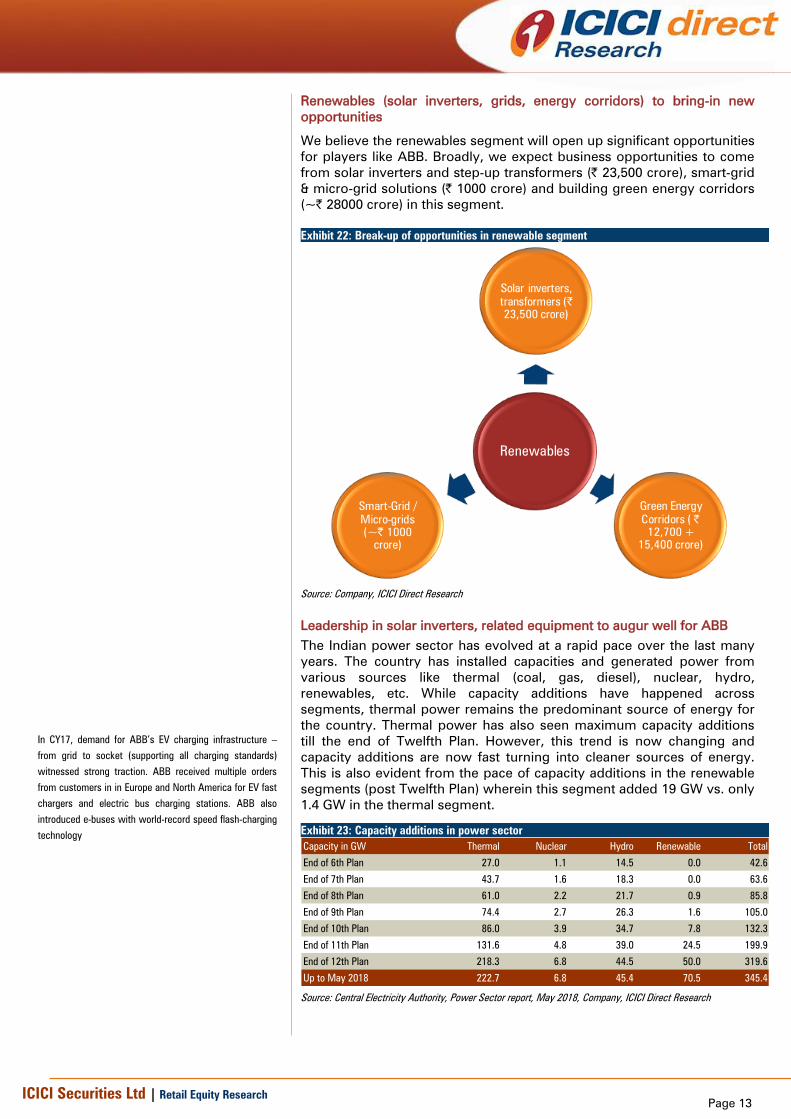

Renewables (solar inverters, grids, energy corridors) to bring-in new

opportunities

We believe the renewables segment will open up significant opportunities

for players like ABB. Broadly, we expect business opportunities to come

from solar inverters and step-up transformers (| 23,500 crore), smart-grid

& micro-grid solutions (| 1000 crore) and building green energy corridors

(~| 28000 crore) in this segment.

Exhibit 22: Break-up of opportunities in renewable segment

Renewables

Solar inverters,

transformers (|

23,500 crore)

Green Energy

Corridors ( |

12,700 +

15,400 crore)

Smart-Grid /

Micro-grids

(~| 1000

crore)

Source: Company, ICICI Direct Research

Leadership in solar inverters, related equipment to augur well for ABB

The Indian power sector has evolved at a rapid pace over the last many

years. The country has installed capacities and generated power from

various sources like thermal (coal, gas, diesel), nuclear, hydro,

renewables, etc. While capacity additions have happened across

segments, thermal power remains the predominant source of energy for

the country. Thermal power has also seen maximum capacity additions

till the end of Twelfth Plan. However, this trend is now changing and

capacity additions are now fast turning into cleaner sources of energy.

This is also evident from the pace of capacity additions in the renewable

segments (post Twelfth Plan) wherein this segment added 19 GW vs. only

1.4 GW in the thermal segment.

Exhibit 23: Capacity additions in power sector

Capacity in GW Thermal Nuclear Hydro Renewable Total

End of 6th Plan 27.0 1.1 14.5 0.0 42.6

End of 7th Plan 43.7 1.6 18.3 0.0 63.6

End of 8th Plan 61.0 2.2 21.7 0.9 85.8

End of 9th Plan 74.4 2.7 26.3 1.6 105.0

End of 10th Plan 86.0 3.9 34.7 7.8 132.3

End of 11th Plan 131.6 4.8 39.0 24.5 199.9

End of 12th Plan 218.3 6.8 44.5 50.0 319.6

Up to May 2018 222.7 6.8 45.4 70.5 345.4

Source: Central Electricity Authority, Power Sector report, May 2018, Company, ICICI Direct Research

In CY17, demand for ABB’s EV charging infrastructure –

from grid to socket (supporting all charging standards)

witnessed strong traction. ABB received multiple orders

from customers in in Europe and North America for EV fast

chargers and electric bus charging stations. ABB also

introduced e-buses with world-record speed flash-charging

technology

Page 14 ICICI Securities Ltd | Retail Equity Research

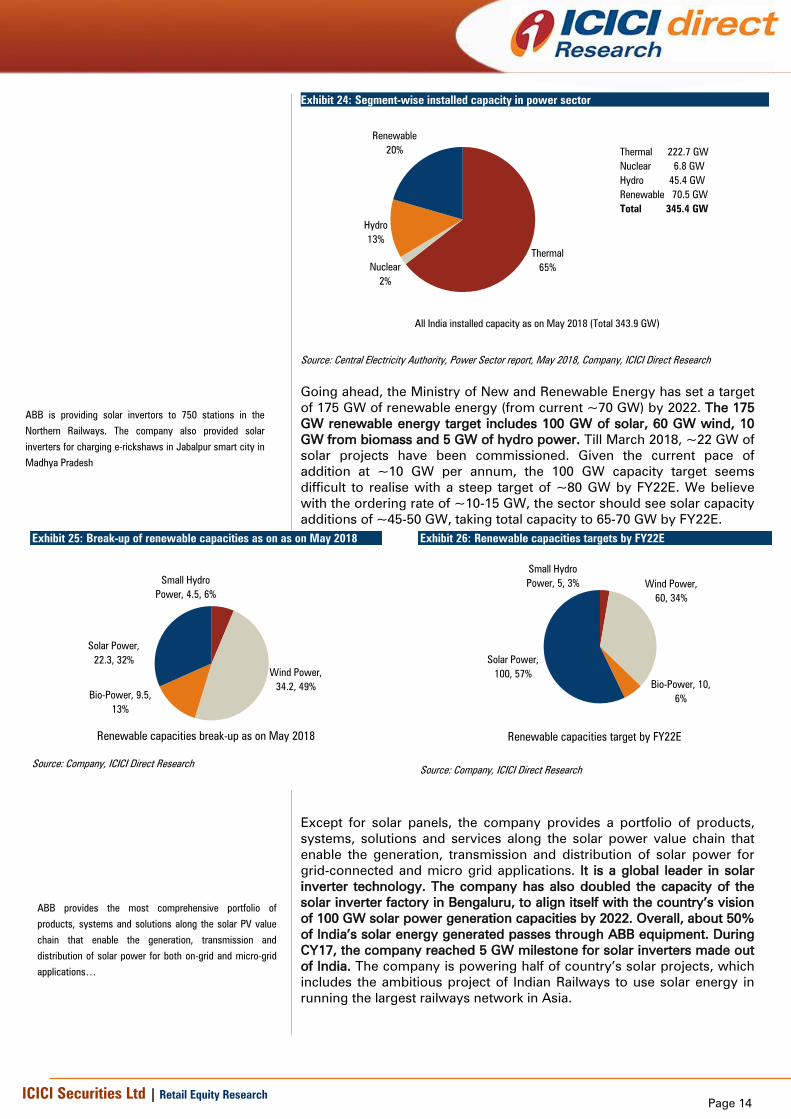

Exhibit 24: Segment-wise installed capacity in power sector

All India installed capacity as on May 2018 (Total 343.9 GW)

Thermal

65%Nuclear

2%

Hydro

13%

Renewable

20% Thermal 222.7 GW

Nuclear 6.8 GW

Hydro 45.4 GW

Renewable 70.5 GW

Total 345.4 GW

Source: Central Electricity Authority, Power Sector report, May 2018, Company, ICICI Direct Research

Going ahead, the Ministry of New and Renewable Energy has set a target

of 175 GW of renewable energy (from current ~70 GW) by 2022. The 175

GW renewable energy target includes 100 GW of solar, 60 GW wind, 10

GW from biomass and 5 GW of hydro power. Till March 2018, ~22 GW of

solar projects have been commissioned. Given the current pace of

addition at ~10 GW per annum, the 100 GW capacity target seems

difficult to realise with a steep target of ~80 GW by FY22E. We believe

with the ordering rate of ~10-15 GW, the sector should see solar capacity

additions of ~45-50 GW, taking total capacity to 65-70 GW by FY22E.

Exhibit 25: Break-up of renewable capacities as on as on May 2018

Renewable capacities break-up as on May 2018

Solar Power,

22.3, 32%

Bio-Power, 9.5,

13%

Wind Power,

34.2, 49%

Small Hydro

Power, 4.5, 6%

Source: Company, ICICI Direct Research

Exhibit 26: Renewable capacities targets by FY22E

Renewable capacities target by FY22E

Small Hydro

Power, 5, 3% Wind Power,

60, 34%

Bio-Power, 10,

6%

Solar Power,

100, 57%

Source: Company, ICICI Direct Research

Except for solar panels, the company provides a portfolio of products,

systems, solutions and services along the solar power value chain that

enable the generation, transmission and distribution of solar power for

grid-connected and micro grid applications. It is a global leader in solar

inverter technology. The company has also doubled the capacity of the

solar inverter factory in Bengaluru, to align itself with the country’s vision

of 100 GW solar power generation capacities by 2022. Overall, about 50%

of India’s solar energy generated passes through ABB equipment. During

CY17, the company reached 5 GW milestone for solar inverters made out

of India. The company is powering half of country’s solar projects, which

includes the ambitious project of Indian Railways to use solar energy in

running the largest railways network in Asia.

ABB is providing solar invertors to 750 stations in the

Northern Railways. The company also provided solar

inverters for charging e-rickshaws in Jabalpur smart city in

Madhya Pradesh

ABB provides the most comprehensive portfolio of

products, systems and solutions along the solar PV value

chain that enable the generation, transmission and

distribution of solar power for both on-grid and micro-grid

applications…

Page 15 ICICI Securities Ltd | Retail Equity Research

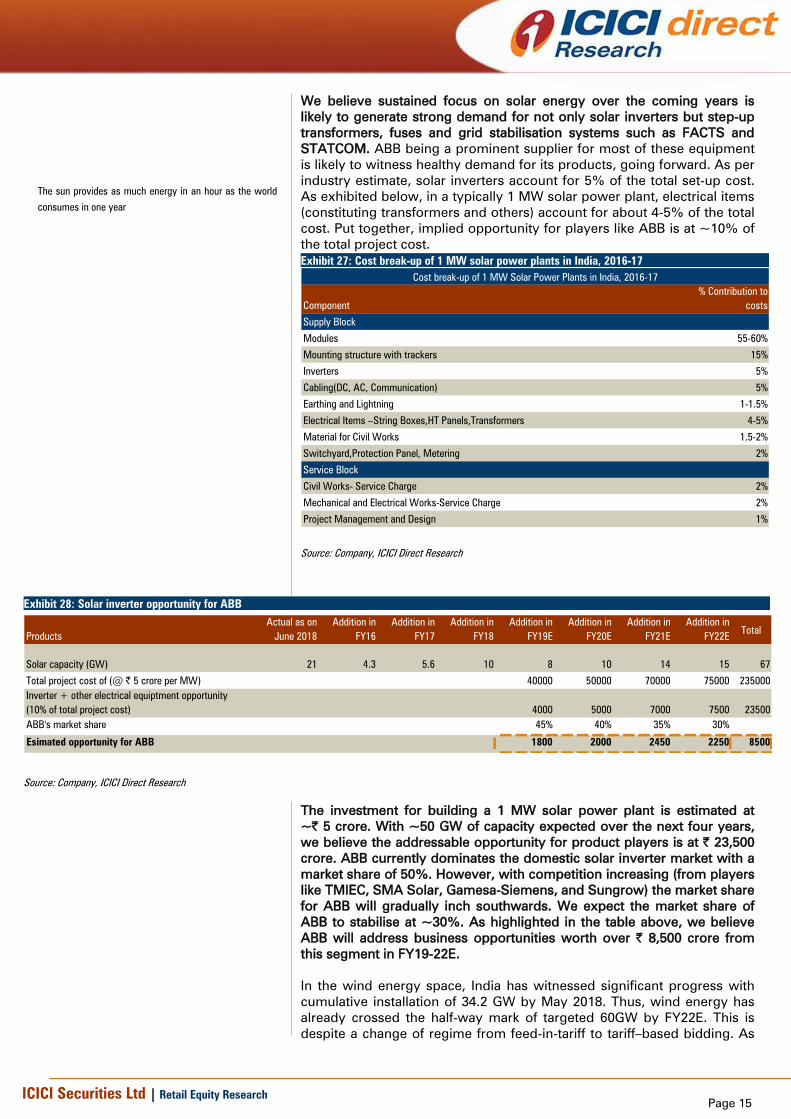

We believe sustained focus on solar energy over the coming years is

likely to generate strong demand for not only solar inverters but step-up

transformers, fuses and grid stabilisation systems such as FACTS and

STATCOM. ABB being a prominent supplier for most of these equipment

is likely to witness healthy demand for its products, going forward. As per

industry estimate, solar inverters account for 5% of the total set-up cost.

As exhibited below, in a typically 1 MW solar power plant, electrical items

(constituting transformers and others) account for about 4-5% of the total

cost. Put together, implied opportunity for players like ABB is at ~10% of

the total project cost.

Exhibit 27: Cost break-up of 1 MW solar power plants in India, 2016-17

Component

% Contribution to

costs

Supply Block

Modules 55-60%

Mounting structure with trackers 15%

Inverters 5%

Cabling(DC, AC, Communication) 5%

Earthing and Lightning 1-1.5%

Electrical Items –String Boxes,HT Panels,Transformers 4-5%

Material for Civil Works 1.5-2%

Switchyard,Protection Panel, Metering 2%

Service Block

Civil Works- Service Charge 2%

Mechanical and Electrical Works-Service Charge 2%

Project Management and Design 1%

Cost break-up of 1 MW Solar Power Plants in India, 2016-17

Source: Company, ICICI Direct Research

Exhibit 28: Solar inverter opportunity for ABB

Products

Actual as on

June 2018

Addition in

FY16

Addition in

FY17

Addition in

FY18

Addition in

FY19E

Addition in

FY20E

Addition in

FY21E

Addition in

FY22ETotal

Solar capacity (GW) 21 4.3 5.6 10 8 10 14 15 67

Total project cost of (@ | 5 crore per MW) 40000 50000 70000 75000 235000

Inverter + other electrical equiptment opportunity

(10% of total project cost) 4000 5000 7000 7500 23500

ABB's market share 45% 40% 35% 30%

Esimated opportunity for ABB 1800 2000 2450 2250 8500

Source: Company, ICICI Direct Research

The investment for building a 1 MW solar power plant is estimated at

~| 5 crore. With ~50 GW of capacity expected over the next four years,

we believe the addressable opportunity for product players is at | 23,500

crore. ABB currently dominates the domestic solar inverter market with a

market share of 50%. However, with competition increasing (from players

like TMIEC, SMA Solar, Gamesa-Siemens, and Sungrow) the market share

for ABB will gradually inch southwards. We expect the market share of

ABB to stabilise at ~30%. As highlighted in the table above, we believe

ABB will address business opportunities worth over | 8,500 crore from

this segment in FY19-22E.

In the wind energy space, India has witnessed significant progress with

cumulative installation of 34.2 GW by May 2018. Thus, wind energy has

already crossed the half-way mark of targeted 60GW by FY22E. This is

despite a change of regime from feed-in-tariff to tariff–based bidding. As

The sun provides as much energy in an hour as the world

consumes in one year

Page 16 ICICI Securities Ltd | Retail Equity Research

wind energy has now emerged as very competitive with respect to other

energy sources, we believe it is now quickly likely to move into

industrialisation phase. Volumes are set to grow with 8-10 GW auctions

each year. While ABB has not made any significant strides in this area in

India, the company possesses strong capabilities across the value chain.

Parent ABB offers the complete portfolio of offerings, from individual

components for a wind turbine installation to the turnkey delivery of

onshore or offshore grid connection schemes.

Additionally, newer areas like wind-solar hybrid, offshore wind farms and

power evacuation corridors are also areas that ABB can significantly

capitalise on given competencies in its global portfolio. The Centre has

planned such energy corridors for building large scale capacities on the

renewable side. The cost estimate for these green energy corridors -

intrastate and interstate transmission systems are pegged at | 12,700

crore and | 15,400 crore, respectively.

ABB’s smart-grid and micro-grid solutions

The company is a forerunner in smart grids solutions, which integrates

renewable energy into the power supply system while optimising the

system’s reliability, energy efficiency and capacity utilisation. These

solutions have systems for controllable generation and storage and assist

in matching fluctuating levels of renewable power generation. Using data

networks in real time, smart grids can intelligently and automatically

control these increasingly complex power systems. The ABB Group is a

pioneer in micro grid technology with more than 30 global installations

across a diverse range of applications serving remote communities,

islanded grids, utility grid support and industrial campuses. This

innovative micro grid solution has now been extended for community use

by ABB. This has been done in a way such that it aids communities to

enjoy stable and cost-effective continuity of power while minimising the

environmental impact. We believe these smart-grid and micro-grid

solutions will provide additional lever of growth for ABB, going forward.

With improving allocations every year (~| 980 crore in the Twelfth Plan

for NSGM activities), we see an improving outlook for this segment in

coming years.

What is a Micro-grid?

Micro-grid is a localised group of electricity sources and

loads that normally operate connected to and synchronous

with the traditional centralised electrical grid (macro-grid),

but can also disconnect to ‘island mode’ and function

autonomously as physical and/or economic conditions

dictate

In this way, a micro-grid can effectively integrate various

sources of distributed generation; especially renewable

energy sources, and can supply emergency power,

changing between island and connected modes

What is a smart-grid?

A smart grid is an electrical grid, which allows a variety of

operational and energy measures like smart meters, smart

appliances, renewable energy resources and energy

efficient resources

Page 17 ICICI Securities Ltd | Retail Equity Research

Capitalising on railway electrification/modernisation programmes

ABB has been a key partner of Indian Railways over the past many years

with a suite of traction solutions. For example, 52% of diesel locomotives

of India run on ABB turbochargers. ABB’s technology offerings in this

segment have helped Indian Railways evolve in various areas like

electrification, clean energy, safety, speed, robustness, etc. ABB group’s

global leadership in railway and transportation technologies ensure that

ABB (India) continue to develop and deploy the latest in the future of

transportation technologies in the fourth largest railway network in the

world. For ABB, opportunities from Indian railways stem from the huge

capex and opex programmes planned over the next few years. Broadly,

we expect the opportunity to come from three segments – Electrification

of rail networks (~| 35,000 crore, continued addition of electric

locomotives (~| 9,000 crore) and opportunities arising of (rail) network

decongestion and metros.

Exhibit 29: ABB’s opportunities in railway electrification/ modernisation programmes

Railways

Electrifying

railway

networks (|

35,000 crore)

Network de-

congestion,

Metros

Electric

Locomotives (|

9000 crore)

Source: Company, ICICI Direct Research

For example, the Indian rail network is electrified to the tune of 45% (as

on April 2017). Indian Railways has a goal to electrify most its rail network

over the next three to five years as an electric rail network can play a vital

role in improving operating ratio for the railways. As per the study

conducted by Tata Energy and Research Institute, electric rail networks

are ~3x more energy efficient than diesel networks. The pace of

electrification has also substantially improved in the past two to three

years. As highlighted in exhibit below, electrification grew substantially in

2015-16 and 2016-17, growing over 25.5% and 16.4%, respectively.

Indian Railways plans to fully electrify its rail network by 2021-22.

Accordingly, we envisage huge capex spends in this segment over the

next two to three years. Indian Railways has already earmarked | 35,000

for execution of the same. This move is also likely to help Indian Railways

save | 10,500–11,000 crore a year in fuel bill. The budgeted sum of

| 35,000 crore is based on railways’ internal estimates of ~| 1 crore for

every km of railway-line to be electrified. For players like ABB, this is likely

to open up huge opportunities as it is a leading supplier of power

transmission and electrification products like transformers, turbochargers,

low and medium voltage products, switchgears, etc.

In rail, ABB won orders worth $70 million from Swiss train

manufacturer Stadler Rail to supply traction and on board

power equipment to three European rail operators

Total 52% of diesel locomotives of India run on ABB

turbochargers

ABB and Siemens have a dominant market share in the

domestic drive and transformer segment

Page 18 ICICI Securities Ltd | Retail Equity Research

Exhibit 30: Electrification of Indian railways

Plan Period 1948-2012 2012-13 2013-14 2014-15 2015-16 2016-17

R.km. Electrified 21836 1317 1350 1378 1730 2013

Growth YoY (%) 2.5% 2.1% 25.5% 16.4%

R.km. Cumulative 22224 23541 24891 26269 27999 30012

Total R.km.: 66,687, Total electrified: 45%

Source: Central organisation for railway electrification, Company, ICICI Direct Research

For ABB, the next big area of opportunity is electric locomotives. Over the

next five years, Indian Railways needs ~5,000 more electric locomotives

to move all trains on electric traction. It has ~5,399 electric locomotives at

present and is able to add ~250 every year. Together for locos, coaches

and wagons, Indian Railways has already allocated ~| 1 lakh crore for

FY17-22E. Indian Railways has already awarded a large contract to

procure 1000 electric locomotives over the next 10 years to Alstom India

(now taken over by GE). Indian railways is also planning to convert

existing diesel locos into electric ones and ramp-up the existing electric-

loco production by doubling facilities at Varanasi and Chittaranjan

Locomotive Works (CLW) in West Bengal. ABB is already supplying

traction equipment to CLW for several years. The company has also

received order to supply 1600 traction transformers installation in

Alstom’s electric locomotives. As exhibited below, an electric locomotive

houses several critical electrical equipment like motors, transformers,

rectifiers, inverters, etc. The cost of electronic devices in a modern

locomotive is ~50% of the cost of the vehicle. ABB is already a major

supplier of these systems to rolling stock manufacturers around the

world. With Indian railways moving swiftly towards procurement of

electric locomotives, we believe companies like ABB are likely to see

sustained business momentum over the next three to five years. We peg

this opportunity at | 9000 crore over CY18-22E.

Exhibit 31: Electrical equipment in electric locomotive

Source: Indian railways document – Story of growth and modernisation, Company, ICICI Direct Research

More than half the world’s electrical locomotives and train

sets are powered by ABB transformers

Page 19 ICICI Securities Ltd | Retail Equity Research

Exhibit 32: Electric locomotive opportunity for ABB for CY18-22E

Opportunity Ordering rate per annum (qty) Cost per locomotive (| crore)

Electric locomotive 250 25

Share of electronic components @

50% 12

Opportunity for ABB over the next 3

year CY18-21E (| crore) (250 X 12 X 3) 9000

Source: Company, ICICI Direct Research

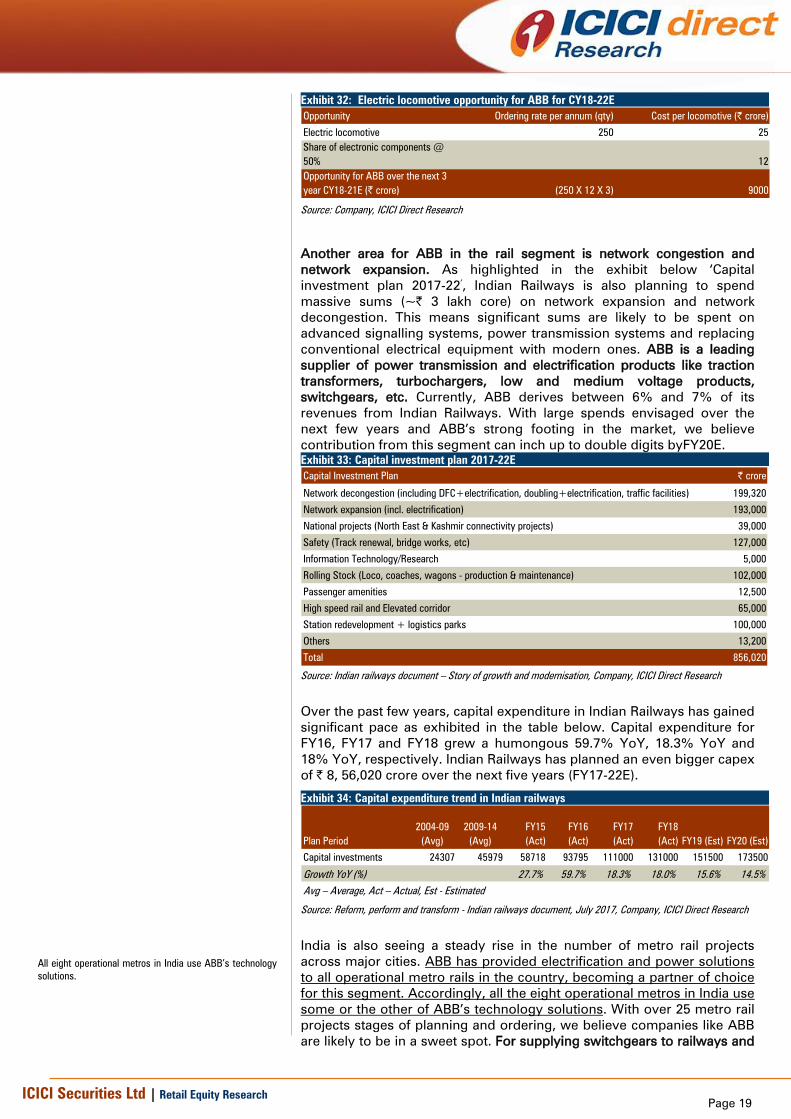

Another area for ABB in the rail segment is network congestion and

network expansion. As highlighted in the exhibit below ‘Capital

investment plan 2017-22’, Indian Railways is also planning to spend

massive sums (~| 3 lakh core) on network expansion and network

decongestion. This means significant sums are likely to be spent on

advanced signalling systems, power transmission systems and replacing

conventional electrical equipment with modern ones. ABB is a leading

supplier of power transmission and electrification products like traction

transformers, turbochargers, low and medium voltage products,

switchgears, etc. Currently, ABB derives between 6% and 7% of its

revenues from Indian Railways. With large spends envisaged over the

next few years and ABB’s strong footing in the market, we believe

contribution from this segment can inch up to double digits byFY20E.

Exhibit 33: Capital investment plan 2017-22E

Capital Investment Plan | crore

Network decongestion (including DFC+electrification, doubling+electrification, traffic facilities) 199,320

Network expansion (incl. electrification) 193,000

National projects (North East & Kashmir connectivity projects) 39,000

Safety (Track renewal, bridge works, etc) 127,000

Information Technology/Research 5,000

Rolling Stock (Loco, coaches, wagons - production & maintenance) 102,000

Passenger amenities 12,500

High speed rail and Elevated corridor 65,000

Station redevelopment + logistics parks 100,000

Others 13,200

Total 856,020

Source: Indian railways document – Story of growth and modernisation, Company, ICICI Direct Research

Over the past few years, capital expenditure in Indian Railways has gained

significant pace as exhibited in the table below. Capital expenditure for

FY16, FY17 and FY18 grew a humongous 59.7% YoY, 18.3% YoY and

18% YoY, respectively. Indian Railways has planned an even bigger capex

of | 8, 56,020 crore over the next five years (FY17-22E).

Exhibit 34: Capital expenditure trend in Indian railways

Plan Period

2004-09

(Avg)

2009-14

(Avg)

FY15

(Act)

FY16

(Act)

FY17

(Act)

FY18

(Act) FY19 (Est) FY20 (Est)

Capital investments 24307 45979 58718 93795 111000 131000 151500 173500

Growth YoY (%) 27.7% 59.7% 18.3% 18.0% 15.6% 14.5%

Avg – Average, Act – Actual, Est - Estimated

Source: Reform, perform and transform - Indian railways document, July 2017, Company, ICICI Direct Research

India is also seeing a steady rise in the number of metro rail projects

across major cities. ABB has provided electrification and power solutions

to all operational metro rails in the country, becoming a partner of choice

for this segment. Accordingly, all the eight operational metros in India use

some or the other of ABB’s technology solutions. With over 25 metro rail

projects stages of planning and ordering, we believe companies like ABB

are likely to be in a sweet spot. For supplying switchgears to railways and

All eight operational metros in India use ABB’s technology

solutions.

Page 20 ICICI Securities Ltd | Retail Equity Research

metros, ABB has set up a state-of-the-art green field manufacturing facility

(in India in 2013) to manufacture gas insulated switchgear (GIS) from

72.5kV to 420kV as per common global design platform. This facility is

also likely be used to supply 800kV GIS.

ABB - At the forefront of ‘Fourth Industrial Revolution’

The first Industrial Revolution was driven by the steam engine and

mechanisation, the second by Henry Ford’s assembly line and the third in

the 1970s, when computers revolutionised the workplace. Now, the three

have amalgamated, putting technology companies like ABB at the cusp of

Industry 4.0, an age where ‘smart devices’ really are smart enough to

assume major control over the machines of manufacturing and

distribution. ABB’s industrial automation division offers ‘cyber-physical

production systems’ in which sensor-laden ‘smart products’ tell machines

how they should be processed. Processes, thus now govern themselves

in a decentralised, modular system. Smart embedded devices start

working together wirelessly either directly or via the Internet ‘cloud’ – the

Internet of Things (IoT) – to revolutionise production. ABB provides

products, systems and services that increase industrial productivity and

energy efficiency for a wide range of industrial applications. ABB’s robots,

drives and servo motors provide a high level of flexible and reliable

automation solutions. ABB’s automation solutions help its clients improve

uptime, product quality and workplace safety while reducing energy

consumption and waste.

Digital ABB to cater to industrial/process automation opportunities

ABB expects huge opportunities to come from the digitisation space,

going forward. This is on account of the value proposition the company is

likely to offer in this space. The management statements indicate this is

going to be the most value-add space in coming years. Traditionally, ABB

has been supplying assets to the customer installed base to improve

efficiencies and productivity. However, with digitisation at the forefront of

new industrial revolution, this is likely to change, going forward. ABB

plans to offer (or is already offering) digitisation solutions like internet of

things (IoT), machine learning (ML) and artificial intelligence (AI). These

three put together form the critical layers of the digitisation process.

Together, or in parts, these layers help increase operational efficiency,

reliability, predictability and overall productivity of the system.

Accordingly, ABB has launched a digital platform ABB Ability. It is an

open platform that allows ABB to work with its industrial customers to co-

create solutions. For ABB Ability, a leading cement producer of India has

already engaged ABB for improving its productivity and efficiency.

Creating digital opportunities by staying ahead of curve – ABB Ability™

ABB Ability™ is an open, globally available, digital-industrial ecosystem

with cloud infrastructure for customers, partners, suppliers and

developers. It is a unified, cross-industry capable enterprise solution

(launched in March 2017). Leveraging its large installed base of connected

systems and devices, ABB has launched more than 210 ABB Ability™

solutions. These have a secure, open-architecture system, ranging from

edge to cloud. Going forward, ABB Ability™ is likely to be central to ABB’s

strategy to drive growth through expansion of high value-added solutions

and services.

ABB has implemented automations solutions in Asia’s

third largest paint company, Asian Paints. ABB executed

design, engineering, project management, installation,

commissioning and service of the integrated manufacturing

execution systems (MES) and distributed control system

(DCS) of this new plant. This greenfield facility has

production capacity of 225,000 kilo litre per annum (kl/a)

water based paint, 70,000 kl/a of solvent based paint and

5,000 kl/a of machine colorants. Having around 42,000

input-output points (I/Os), ABB implemented end-to-end

solution that controls and integrates plant processes from

raw material receipt, storage and transportation to paint

manufacture and packing

ABB Ability™ - A cloud-based operating system for the

industrial internet of things (IIOT)

Page 21 ICICI Securities Ltd | Retail Equity Research

Exhibit 35: ABB has over 210+ ABB Ability™ solutions

Source: Company, ICICI Direct Research

Exhibit 36: ABB Ability™: Industry-leading digital solution

Source: Company, ICICI Direct Research

To build a leading/ world-class platform, ABB has announced a

partnership with Microsoft to build a platform for digitalisation and act as

partners for driving futuristic industrial solutions. ABB Ability, thus, brings

together digital capabilities as one unified offer.

Industrial automation, Robotics & Motion to grow at ~10% CAGR in

CY17-19E

Industry estimates suggest India’s factory and industrial automation

market has grown at 10-11% CAGR in FY17-22E. With automation

systems with advanced features being deployed in all major sectors such

as automotive, chemicals, manufacturing, mining, etc, to perform a

number of complex tasks and consistently provide customers with

superior quality products, this market is poised to grow at an accelerated

rate, going forward. Further, growing adoption of energy saving control

equipment such as energy efficient motor systems is also expected to

propel the adoption of factory automation in India in coming years. This

industry in India is worth ~| 12,000 crore and has the potential to grow

15-20% given the existing capacity addition in infrastructure, energy and

other sectors. Accordingly, we estimate ABB’s ‘industrial automation’ and

‘robotics and motion’ segment to also grow at least ~10% CAGR in the

next few years (industrial automation 9.5% CAGR, robotics and

automation 10.8% CAGR).

Exhibit 37: Industrial automation market size FY12-17

7250

12000

0

2000

4000

6000

8000

10000

12000

14000

FY12 FY13 FY14 FY15 FY16 FY17

| c

rore

Market Size FY12-17 (| crore)

10.6% CAGR

Source: Confederation of Indian Industry, Factory automation document 2017,

Company, ICICI Direct Research

Exhibit 38: Estimated industrial automation market size FY17-22E

12000

26500

0

5000

10000

15000

20000

25000

30000

FY17 FY18 FY19 FY20 FY21 FY22

| c

rore

Market Size FY17-22E (| crore)

17.2% CAGR

Source: Confederation of Indian Industry, Factory automation document 2017,

Company, ICICI Direct Research

Page 22 ICICI Securities Ltd | Retail Equity Research

E-cars to bring accelerated growth opportunities

To facilitate quick adoption of electric vehicles and encourage large scale

electric mobility, the Government of India has formulated two national-

level programmes;

National Electric Mobility Mission Plan (NEMMP) &

Faster Adoption & Manufacturing of (Hybrid) & Electric Vehicles in

India (FAME)

These programmes, designed in a way that help in realising the

governments vision of 100% electrification of vehicles by 2030 are likely

to open accelerated opportunities for technology companies like ABB.

ABB is one of the world’s leading suppliers of EV charging stations with a

range of products from flash chargers to standard chargers. As a global

player in EV fast-charging solutions, ABB has more than 6,000 units

installed across more than 55 countries. Also, ABB’s fast chargers are

used by all Indian, global OEMS to test their vehicles. Given that charging

infrastructure is vital to realising government’s vision. This area is likely to

witness accelerated spends, going forward. ABB has already proven its

competencies in this segment in developed geographies like US and

Europe, with large orders inflow and execution in both countries.

To walk the talk, the Government of India, through its state-run enterprise

Energy Efficiency Services Ltd (EESL), has also awarded a contract to

procure 10,000 electric vehicles for various government departments. It

has also invited bids for 4500 electric vehicle charging stations (for which

ABB has also bid). With most domestic and international auto majors

announcing new launches in this segment, we believe strong charging

infrastructure will be the need of the hour, going ahead. ABB’s technical

prowess and heads-up start in this segment, we believe, will significantly

benefit the company in CY18E-22E.

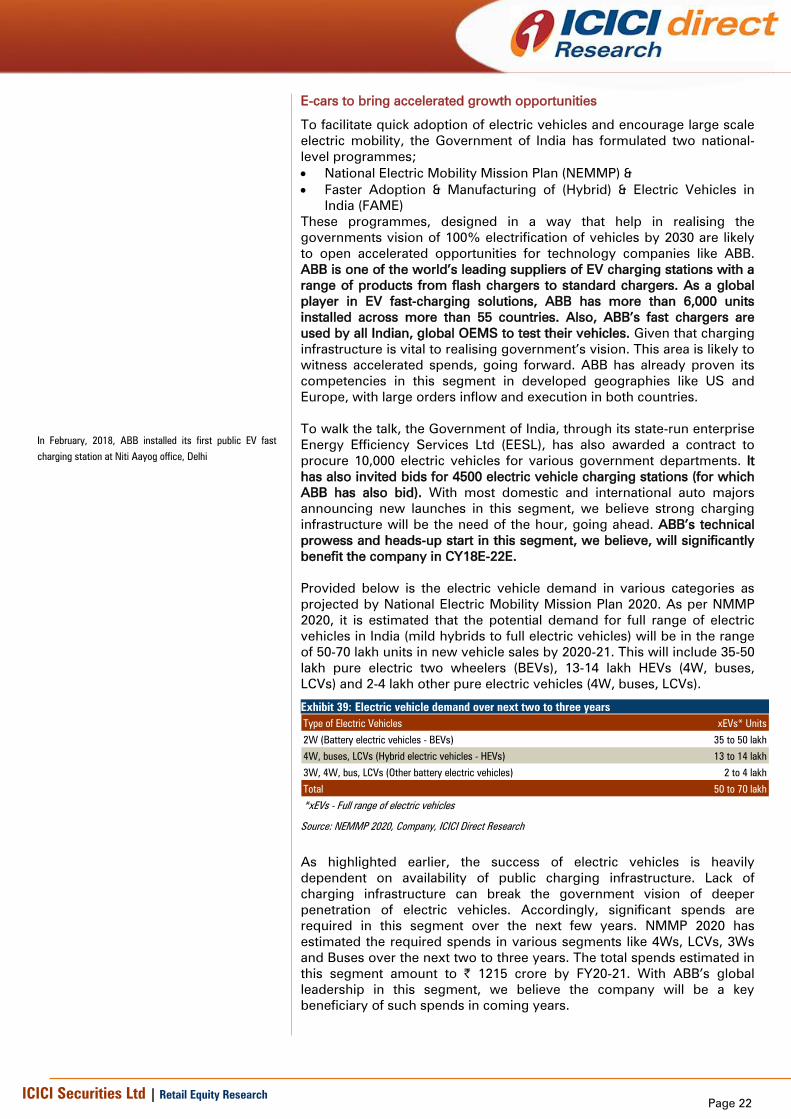

Provided below is the electric vehicle demand in various categories as

projected by National Electric Mobility Mission Plan 2020. As per NMMP

2020, it is estimated that the potential demand for full range of electric

vehicles in India (mild hybrids to full electric vehicles) will be in the range

of 50-70 lakh units in new vehicle sales by 2020-21. This will include 35-50

lakh pure electric two wheelers (BEVs), 13-14 lakh HEVs (4W, buses,

LCVs) and 2-4 lakh other pure electric vehicles (4W, buses, LCVs).

Exhibit 39: Electric vehicle demand over next two to three years

Type of Electric Vehicles xEVs* Units

2W (Battery electric vehicles - BEVs) 35 to 50 lakh

4W, buses, LCVs (Hybrid electric vehicles - HEVs) 13 to 14 lakh

3W, 4W, bus, LCVs (Other battery electric vehicles) 2 to 4 lakh

Total 50 to 70 lakh

*xEVs - Full range of electric vehicles

Source: NEMMP 2020, Company, ICICI Direct Research

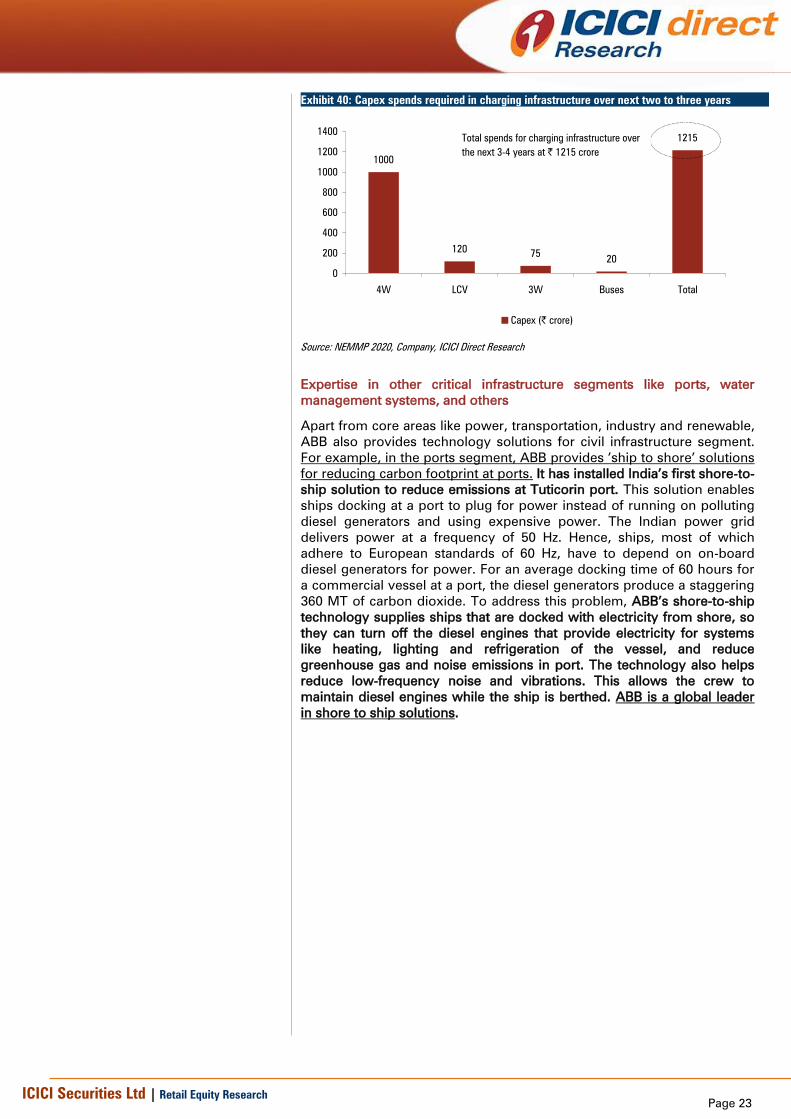

As highlighted earlier, the success of electric vehicles is heavily

dependent on availability of public charging infrastructure. Lack of

charging infrastructure can break the government vision of deeper

penetration of electric vehicles. Accordingly, significant spends are

required in this segment over the next few years. NMMP 2020 has

estimated the required spends in various segments like 4Ws, LCVs, 3Ws

and Buses over the next two to three years. The total spends estimated in

this segment amount to | 1215 crore by FY20-21. With ABB’s global

leadership in this segment, we believe the company will be a key

beneficiary of such spends in coming years.

In February, 2018, ABB installed its first public EV fast

charging station at Niti Aayog office, Delhi

Page 23 ICICI Securities Ltd | Retail Equity Research

Exhibit 40: Capex spends required in charging infrastructure over next two to three years

1000

12075

20

1215

0

200

400

600

800

1000

1200

1400

4W LCV 3W Buses Total

Capex (| crore)

Total spends for charging infrastructure over

the next 3-4 years at | 1215 crore

Source: NEMMP 2020, Company, ICICI Direct Research

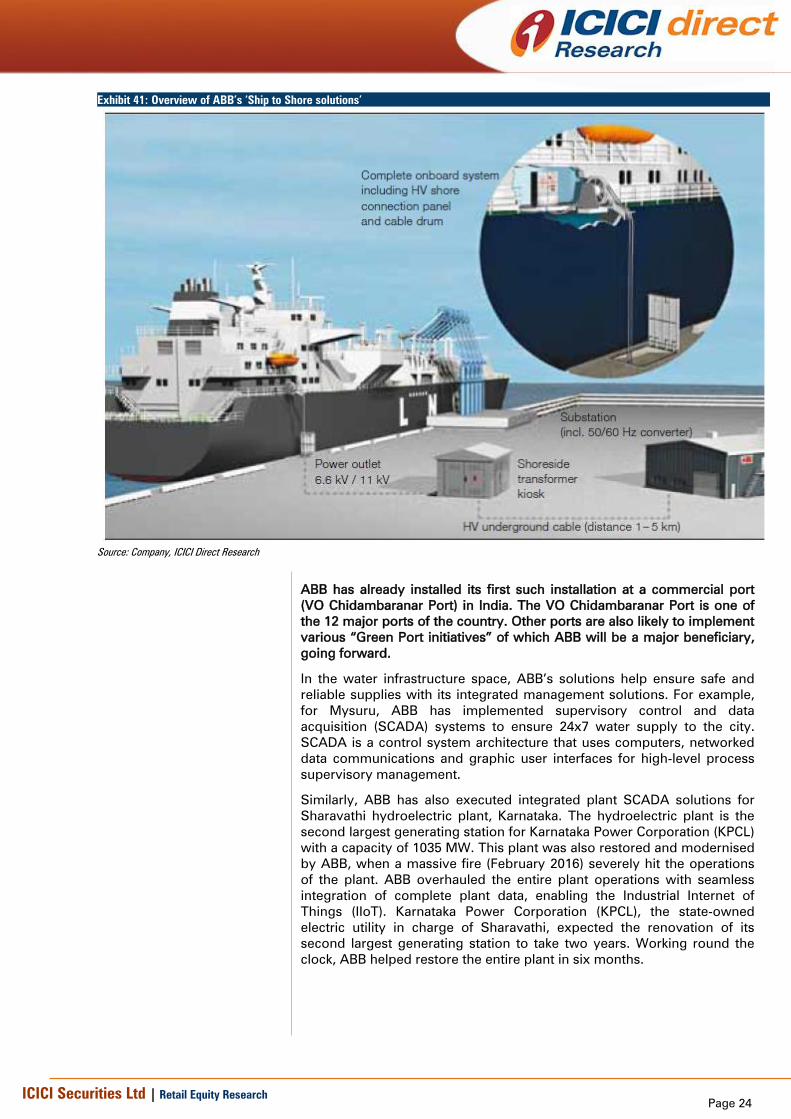

Expertise in other critical infrastructure segments like ports, water

management systems, and others

Apart from core areas like power, transportation, industry and renewable,

ABB also provides technology solutions for civil infrastructure segment.

For example, in the ports segment, ABB provides ’ship to shore’ solutions

for reducing carbon footprint at ports. It has installed India’s first shore-to-

ship solution to reduce emissions at Tuticorin port. This solution enables

ships docking at a port to plug for power instead of running on polluting

diesel generators and using expensive power. The Indian power grid

delivers power at a frequency of 50 Hz. Hence, ships, most of which

adhere to European standards of 60 Hz, have to depend on on-board

diesel generators for power. For an average docking time of 60 hours for

a commercial vessel at a port, the diesel generators produce a staggering

360 MT of carbon dioxide. To address this problem, ABB’s shore-to-ship

technology supplies ships that are docked with electricity from shore, so

they can turn off the diesel engines that provide electricity for systems

like heating, lighting and refrigeration of the vessel, and reduce

greenhouse gas and noise emissions in port. The technology also helps

reduce low-frequency noise and vibrations. This allows the crew to

maintain diesel engines while the ship is berthed. ABB is a global leader

in shore to ship solutions.

Page 24 ICICI Securities Ltd | Retail Equity Research

Exhibit 41: Overview of ABB’s ‘Ship to Shore solutions’

Source: Company, ICICI Direct Research

ABB has already installed its first such installation at a commercial port

(VO Chidambaranar Port) in India. The VO Chidambaranar Port is one of

the 12 major ports of the country. Other ports are also likely to implement

various “Green Port initiatives” of which ABB will be a major beneficiary,

going forward.

In the water infrastructure space, ABB’s solutions help ensure safe and

reliable supplies with its integrated management solutions. For example,

for Mysuru, ABB has implemented supervisory control and data

acquisition (SCADA) systems to ensure 24x7 water supply to the city.

SCADA is a control system architecture that uses computers, networked

data communications and graphic user interfaces for high-level process

supervisory management.

Similarly, ABB has also executed integrated plant SCADA solutions for

Sharavathi hydroelectric plant, Karnataka. The hydroelectric plant is the

second largest generating station for Karnataka Power Corporation (KPCL)

with a capacity of 1035 MW. This plant was also restored and modernised

by ABB, when a massive fire (February 2016) severely hit the operations

of the plant. ABB overhauled the entire plant operations with seamless

integration of complete plant data, enabling the Industrial Internet of

Things (IIoT). Karnataka Power Corporation (KPCL), the state-owned

electric utility in charge of Sharavathi, expected the renovation of its

second largest generating station to take two years. Working round the

clock, ABB helped restore the entire plant in six months.

Page 25 ICICI Securities Ltd | Retail Equity Research

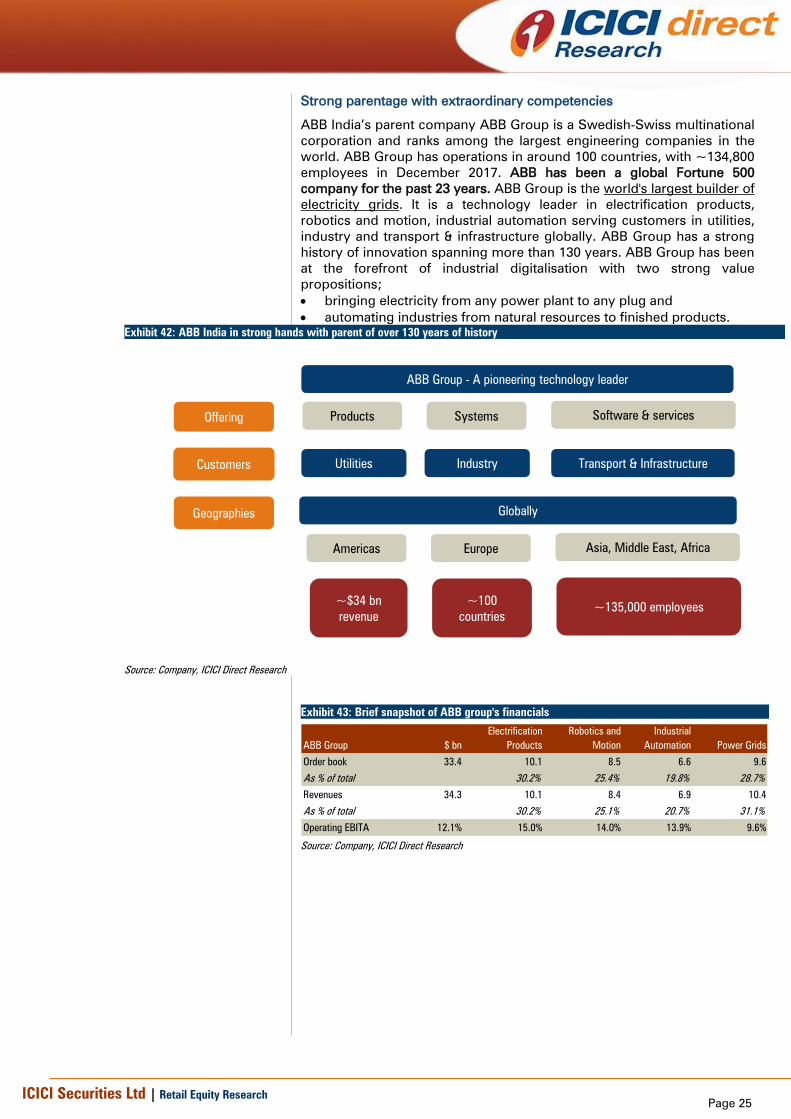

Strong parentage with extraordinary competencies

ABB India’s parent company ABB Group is a Swedish-Swiss multinational

corporation and ranks among the largest engineering companies in the

world. ABB Group has operations in around 100 countries, with ~134,800

employees in December 2017. ABB has been a global Fortune 500

company for the past 23 years. ABB Group is the world's largest builder of

electricity grids. It is a technology leader in electrification products,

robotics and motion, industrial automation serving customers in utilities,

industry and transport & infrastructure globally. ABB Group has a strong

history of innovation spanning more than 130 years. ABB Group has been

at the forefront of industrial digitalisation with two strong value

propositions;

bringing electricity from any power plant to any plug and

automating industries from natural resources to finished products.

Exhibit 42: ABB India in strong hands with parent of over 130 years of history

ProductsOffering

Customers

Geographies

ABB Group - A pioneering technology leader

Utilities

Globally

Industry Transport & Infrastructure

Systems Software & services

Americas Europe Asia, Middle East, Africa

~$34 bn

revenue

~100

countries

~135,000 employees

Source: Company, ICICI Direct Research

Exhibit 43: Brief snapshot of ABB group's financials

ABB Group $ bn

Electrification

Products

Robotics and

Motion

Industrial

Automation Power Grids

Order book 33.4 10.1 8.5 6.6 9.6

As % of total 30.2% 25.4% 19.8% 28.7%

Revenues 34.3 10.1 8.4 6.9 10.4

As % of total 30.2% 25.1% 20.7% 31.1%

Operating EBITA 12.1% 15.0% 14.0% 13.9% 9.6%

Source: Company, ICICI Direct Research

Page 26 ICICI Securities Ltd | Retail Equity Research

Financials

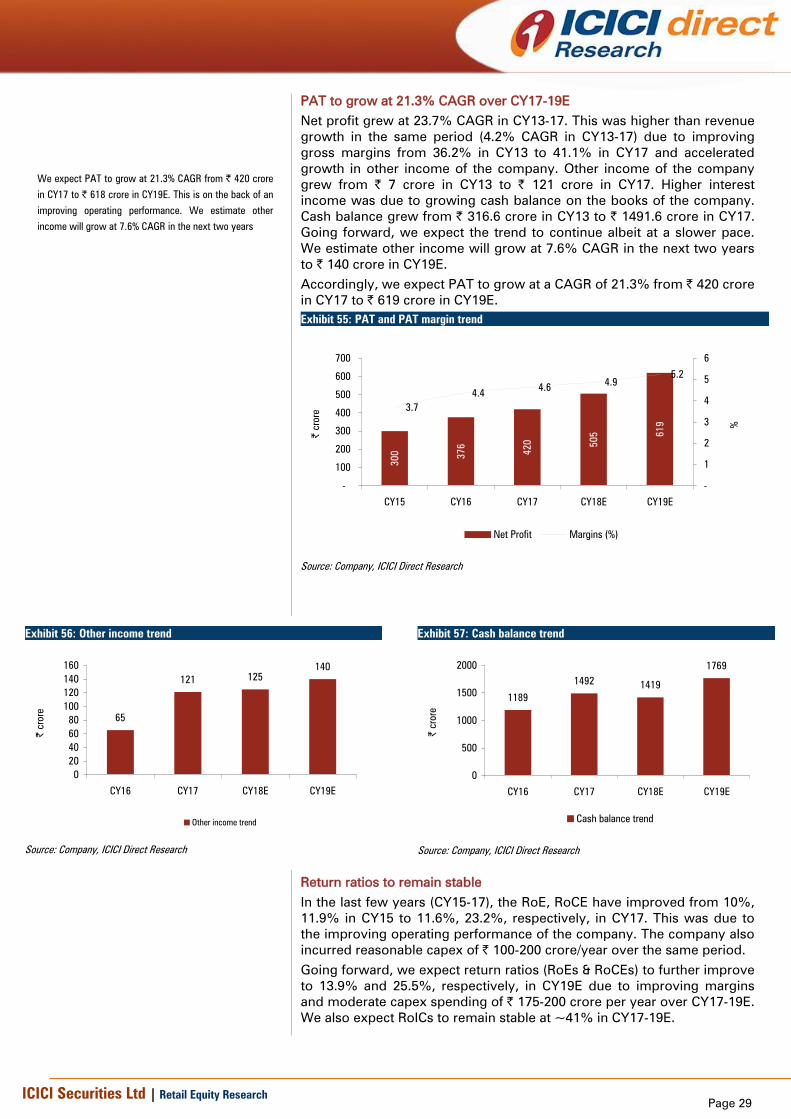

Revenues to grow at 14% CAGR in CY17-19E

We expect revenues to increase from | 9,087 crore in CY17 to | 11,819

crore in CY19E at 14% CAGR in CY17-19E. We expect revenue growth on

the back of improved execution from all key segments, viz. power grids,

electrification products, robotics and motion and industrial automation.

We expect these segments to grow at a CAGR of 9.5%, 13.9%, 10.8% and

9.5%, respectively. Order inflows in these segments are also expected to