jumpstart our business startups (“jobs”) act · pdf filejumpstart our business...

TRANSCRIPT

Jumpstart Our Business Startups (“JOBS”) Act –

An Overview

July 2012

2

Copyright ©2012 Sullivan & Cromwell LLP

2

Copyright ©2012 Sullivan & Cromwell LLP

General

The JOBS Act liberalizes the federal securities laws in a variety of ways discussed in the following slides.

As issuers and market professionals consider new options presented by the JOBS Act, they should:

be mindful of the limits (which may be unclear) of those new options, and the possibility of unintentionally running afoul of other rules or restrictions

carefully weigh potential investor/market reactions

Issuers and professionals should proceed with caution as the SEC and FINRA provide additional guidance and market practices develop.

3

Copyright ©2012 Sullivan & Cromwell LLP

3

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

The Emerging Growth Company (“EGC”) provisions are intended to encourage initial public offerings (“IPOs”) and other capital formation by smaller issuers.

The JOBS Act gives EGCs, on a transitional basis, a grab-bag of new exceptions to the normal procedural and disclosure requirements in registered offerings.

The procedural relief generally relates to the IPO process itself –disclosure relief applies during the issuer’s IPO and for up to 5 years thereafter.

4

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Emerging Growth Company (“EGC”) Definition

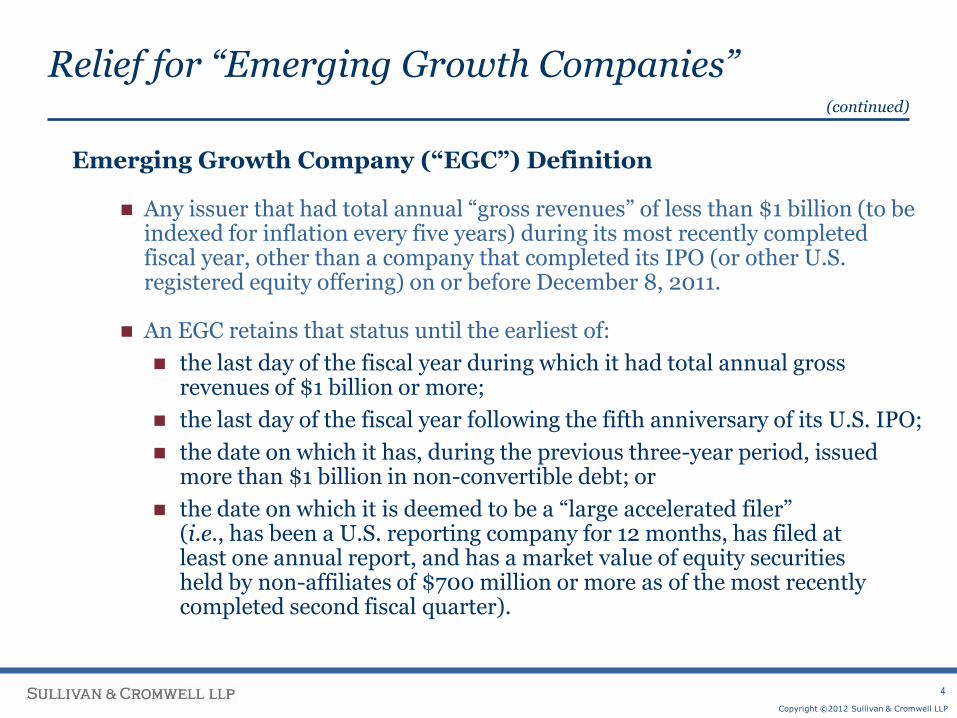

Any issuer that had total annual “gross revenues” of less than $1 billion (to be indexed for inflation every five years) during its most recently completed fiscal year, other than a company that completed its IPO (or other U.S. registered equity offering) on or before December 8, 2011.

An EGC retains that status until the earliest of:

the last day of the fiscal year during which it had total annual gross revenues of $1 billion or more;

the last day of the fiscal year following the fifth anniversary of its U.S. IPO;

the date on which it has, during the previous three-year period, issued more than $1 billion in non-convertible debt; or

the date on which it is deemed to be a “large accelerated filer” (i.e., has been a U.S. reporting company for 12 months, has filed at least one annual report, and has a market value of equity securities held by non-affiliates of $700 million or more as of the most recently completed second fiscal quarter).

(continued)

5

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Notes on Definition

FAQs provide that “gross revenues” means U.S. GAAP (or IFRS as issued by the IASB) revenues.

Not a strict legal-entity approach – FAQs say look to predecessor financial statements where applicable.

FAQs provide different gross revenue test for financial institutions.

Based on approach in SEC’s Financial Reporting Manual with respect to determining “smaller reporting company” status for banks.

Must include all gross revenues from traditional banking activities, including interest on loans and investments, dividends, and any other income from banking or related services.

Do not include gains and losses on dispositions of investment portfolio securities (although may include gains on trading account activity if that is a regular part of the institution’s activities).

(continued)

6

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Disclosure Relief (effective now)

Financial Reporting Periods

An EGC need present no more than two years of audited financial statements in its IPO registration statement and need not present selected financial data for any period prior to the earliest audited period presented in connection with its IPO.

Rules applicable to non-EGCs require three years of audited income statements and five years of selected financial data.

FAQs confirm that financial statements and selected data in follow-on offerings also need not include the omitted year, but would have to include three years when newest year becomes available.

An EGC’s MD&A need cover only the periods for which it files financial statements.

(continued)

7

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Testing the Waters (effective now)

Section 5 of the Securities Act is amended to permit an EGC or any person authorized to act on behalf of an EGC to engage in oral or written communications with potential investors that are QIBs or institutional accredited investors to determine whether those investors might have an interest in a contemplated securities offering, either prior to or following the filing of a registration statement.

Query whether test-the-water statements/materials will be subject to Section 12(a)(2) liability.

Does not appear to preclude contacts by offering participants other than the issuer – but note current debate as to whether an underwriter may take an "indication of interest" in advance of having a complete preliminary prospectus.

Where issuer has outstanding securities (e.g., high-yield), note the potential for material non-public information issues.

SEC Staff routinely requests copies of testing-the-waters materials with a view to comparing those materials with registration statement disclosure.

(continued)

8

Copyright ©2012 Sullivan & Cromwell LLP

8

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Confidential Submissions to SEC (effective now)

EGCs are permitted to confidentially submit to the SEC a draft registration statement for review prior to public filing.

SEC will only review a submission if it is “substantially complete,” consistent with current practice for filed registration statements.

SEC Staff intends to review confidential submissions on the same timeline it reviews filed registration statements.

The EGC must file on EDGAR, 21 days before commencing its “roadshow”, the initial confidential submission and all amendments.

The confidential submission and each amendment (in each case, with all submitted exhibits) will be included as an exhibit to the filed registration statement.

Pre-filing SEC comment letters and issuer responses will also be placed on EDGAR, after completion of the offering.

(continued)

9

Copyright ©2012 Sullivan & Cromwell LLP

9

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Confidential Submissions to SEC (effective now)

FAQs clarify that the confidential submission is not a “filing” for Section 5 purposes.

“Gunjumping” remains a concern, and Rules 134 and 433(f) (the use of which requires a filed registration statement) are not available.

On the interplay between the filing requirement and the test-the-water provisions, the FAQs provide:

“Roadshow” generally means “those meetings traditionally viewed as the road show.”

Compliant test-the-waters communications will not be treated as a “roadshow” triggering the filing requirement.

FAQs provide additional guidance on the confidential submission process and its availability.

(continued)

10

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Research Reports (effective now)

JOBS Act amends Securities Act Section 2(a)(3) (definition of “offer”) to provide that the publication or distribution by a broker-dealer of a research report about an EGC that is the subject of a proposed public offering of its common stock (whether or not a registration statement has been filed or is effective) shall be deemed not to constitute an offer, even if the broker or dealer is or will be participating in the registered offering.

“Research report” means “a written, electronic, or oral communication that includes information, opinions, or recommendations with respect to securities of an issuer or an analysis of a security or an issuer, whether or not it provides information reasonably sufficient upon which to base an investment decision.”

Covers follow-on offerings, as well as IPOs, as long as the issuer is an EGC.

(continued)

11

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Research Reports (effective now) (cont.)

This allows research reports to be published or distributed without violating the registration statement filing requirement of Section 5(c) or the prospectus delivery requirement of Section 5(b)(1).

Prior to the JOBS Act, the Securities Act effectively proscribed the issuance of such research reports in connection with a registered offering, and it still does with respect to non-EGCs.

The change appears to exempt covered research reports from the disclosure liability provisions of Section 12(a)(2) of the Securities Act, but not from other liability provisions such as Section 17 of the Securities Act and Rule 10b-5 under the Exchange Act.

(continued)

12

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Research Reports (effective now) (cont.)

The JOBS Act prohibits the SEC and FINRA from adopting or maintaining any rule prohibiting a broker-dealer from publishing or distributing a research report or making a public appearance with respect to the securities of any EGC either:

within any prescribed period of time following the IPO date of the EGC, or

within any prescribed period of time prior to the expiration date of any lock-up agreement in connection with the IPO.

(continued)

13

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Securities Analyst Communications (effective now)

The JOBS Act also prohibits the SEC and FINRA from adopting or maintaining any rule or regulation in connection with an IPO of the common stock of an EGC:

restricting, based on functional role, which associated persons of a broker-dealer may arrange for communications between a securities analyst and a potential investor, or

restricting a securities analyst from participating in any communications with the management of an EGC that is also attended by any other associated person of a broker-dealer whose functional role is other than as a securities analyst.

It is unclear whether the prohibitions on “maintaining” rules have the effect of immediately nullifying the rules, or whether the rules remain effective until amended.

(continued)

14

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Research Report and Analyst Communications - Notes

The overrides of SEC/FINRA rules apply only with respect to the IPO of an EGC. (The amendment to Section 2(a)(3) applies to any public offering of common stock by an EGC.)

These provisions do not affect the 2003 Global Research Analyst Settlement. Nor would they likely affect other settlements and/or agreements that may include restrictions similar to the global settlement.

Section 3.3 of the May 2011 SIFMA Model Form MAAU prohibits syndicate underwriters from conveying written communications to prospective purchasers in connection with an offering, other than certain writings such as prospectuses and Rule 172, 173 and 134 information.

This appears to prohibit a syndicate member from issuing a research report in connection with the offering, without the managing underwriter’s approval.

We understand that revisions to the model form addressing the JOBS Act are being considered, but we do not expect this prohibition to be removed.

(continued)

15

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Relief from Sarbanes-Oxley Act Section 404(b) (effective now)

EGCs are excluded from Section 404(b) of the Sarbanes-Oxley Act, which requires the auditors of a public company to report on the company’s internal control over financial reporting.

EGCs remain subject to the management report requirements of Sarbanes-Oxley Section 404(a).

A new reporting company is already exempt from both 404(a) and 404(b) until it has been required to file (or did file) a 10-K or 20-F for the prior fiscal year.

Non-“accelerated filers” (i.e., those with less than $75 million float) are already exempt from the 404(b) requirement.

The Sarbanes-Oxley Act is further amended to provide that:

any new rules that may be adopted by the PCAOB requiring mandatory audit firm rotation or changes to the auditor’s report to include auditor discussion and analysis (each of which is currently under consideration by the PCAOB) will not apply to an audit of an EGC, and

any other future rules adopted by the PCAOB will not apply to audits of EGCs unless the SEC determines otherwise.

(continued)

16

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Disclosure Relief (effective now) (cont.)

“Private Company” Accounting Standards

An EGC is not required to comply with any new or revised financial accounting standard until such date as a private company (i.e., a company that is not an “issuer” under the Sarbanes-Oxley Act) is required to comply with such new or revised accounting standard.

This relief relates only to new private company standards, not existing private company standards (such as existing U.S. GAAP private company standards on segments or EPS).

An EGC may irrevocably elect to forego the right to follow new “private company” accounting standards by so stating in its first SEC filing.

In that case, the EGC will be required to comply with all new accounting standards on a “public company” basis.

(continued)

17

Copyright ©2012 Sullivan & Cromwell LLP

Relief for “Emerging Growth Companies”

Disclosure Relief (effective now) (cont.)

Executive Compensation Disclosure

EGCs may comply with Item 402 of Regulation S-K (regarding executive compensation disclosure) by disclosing the more limited information required of a “smaller reporting company”.

EGCs are also exempt from:

advisory “say-on-pay” votes on executive compensation required under Section 14A(a) of the Exchange Act;

Section 14A(b) requirements relating to shareholder advisory votes on golden parachute compensation;

Section 14(i) requirements for disclosure relating to the relationship between executive compensation and financial performance; and

Dodd-Frank Act Section 953(b)(1), which will require disclosure of the relationship between CEO and median employee pay.

(continued)

18

Copyright ©2012 Sullivan & Cromwell LLP

Relief “Emerging Growth Companies” –Other Issues

The Bigger Picture

How will investors react to an EGC’s election to comply with lowered standards?

Especially on number of years of audited statements and 404(b) relief.

Less clear as to executive compensation matters.

Note that earlier publication of research increases practical as well as legal risks.

In U.S. market, research analysts have typically reviewed IPO issuers’ projections, and then develop earnings estimates that are communicated (orally) at time of marketing, but only published 25/40 days after pricing (and commencement of trading)

(continued)

19

Copyright ©2012 Sullivan & Cromwell LLP

General Solicitation Provisions

The JOBS Act provides that the SEC must, by July 4, 2012:

Amend Rule 506 to remove the prohibition against general solicitation or general advertising with respect to offers and sales of securities made pursuant to Rule 506, provided that all purchasers of the securities “are accredited investors.”

Such rules must also require the issuer to take reasonable steps to verify that purchasers are accredited investors, "using such methods as determined by" the SEC.

Amend Rule 144A to provide that securities sold under Rule 144A may be offered to persons other than QIBs, including by means of general solicitation or general advertising, provided that the securities are sold only to persons that the seller and any person acting on behalf of the seller reasonably believe are QIBs.

The SEC will consider such rules at an Aug. 22, 2012 open meeting.

20

Copyright ©2012 Sullivan & Cromwell LLP

General Solicitation Provisions (cont.)

The JOBS Act does not amend the exemption from registration provided by Section 4(2) of the Securities Act itself.

So the new provisions do not, by their terms, apply to private placements conducted in reliance upon Section 4(2) but not in accordance with Rules 506 or 144A as revised.

The JOBS Act does not address Regulation S.

Communications constituting “directed selling efforts” would continue to preclude reliance on that safe harbor.

Under the traditional approach, an issuer could not generally solicit investors in a side-by-side 144A/Regulation S offering, since general solicitation will be indistinguishable from directed selling efforts.

This may be addressed in the proposed rules – commenters have flagged the issue.

21

Copyright ©2012 Sullivan & Cromwell LLP

21

Copyright ©2012 Sullivan & Cromwell LLP

General Solicitation Provisions – Issues

No indication or expectation that these new provisions will affect market practices/perceptions prior to effectiveness of the rule changes. (14 Law Firm Consensus Report)

Will the rule changes affect market practices/perceptions as to “general solicitation” issues in non-safe harbor transactions, particularly in “foot-fault” situations?

We expect the new Rule 506 condition as to purchasers to be based on “reasonable belief.”

The statutory language is unclear, but this seems like the intended outcome; note that the current definition of “accredited investor” itself includes “issuer reasonably believes” qualifier.

22

Copyright ©2012 Sullivan & Cromwell LLP

12(g) Registration Provisions

Effective April 5, 2012:

The record holder threshold for registration (which had been 500 record holders of a non-exempt equity security) was raised:

for most issuers, to either (a) 2,000 persons or (b) 500 persons who are not accredited investors, and

for banks and bank holding companies, to 2,000 persons.

Persons holding securities received pursuant to an employee compensation plan in transactions exempted from the registration requirements of Section 5 of the Securities Act (e.g., because they were issued in a private placement under Regulation D or under Rule 701) are excluded from the record holder count.

SEC Staff indicated, though, that transferees of such securities are included in the record holder count.

23

Copyright ©2012 Sullivan & Cromwell LLP

12(g) Registration Provisions

Section 12(g)(4) (which permits termination of registration of any class of securities held of record by less than 300 persons) and Section 15(d) (which similarly suspends periodic reporting obligations with respect to any class of securities held of record by less than 300 persons) were amended to provide for termination or suspension of reporting obligations with respect to securities of a bank or bank holding company that are held of record by less than 1,200 persons.

A Senate amendment that would have required the SEC to define “held of record” to include beneficial owners was not adopted.

So, consistent with current SEC guidance, the number of record holders of shares held through DTC will continue to be calculated by reference to the number of DTC participants through which shares are held, rather than the number of underlying beneficial owners.

(continued)

24

Copyright ©2012 Sullivan & Cromwell LLP

24

Copyright ©2012 Sullivan & Cromwell LLP

12(g) Registration Provisions – Issues

The registration requirements of Section 12(b), which apply to securities listed on a national securities exchange, were not affected by these JOBS Act provisions.

FAQs provide guidance on registration/deregistration under the new thresholds, particularly regarding BHCs.

Unclear what issuers would be required to do to verify investor status.

25

Copyright ©2012 Sullivan & Cromwell LLP

25

Copyright ©2012 Sullivan & Cromwell LLP

Regulation A Revisions

Section 3(b) of the Securities Act is amended to require the SEC to add a new Regulation A-like exemption for offerings of up to $50 million in any 12-month period. This new exemption is being referred to as "Regulation A Plus."

Basic idea: reduced disclosure format for smaller offerings.

26

Copyright ©2012 Sullivan & Cromwell LLP

26

Copyright ©2012 Sullivan & Cromwell LLP

Crowdfunding Exemption

New Section 4(6) of the Securities Act provides an exemption from Securities Act registration for transactions involving the offer or sale of securities by certain issuers in accordance with new “crowdfunding” statutory provisions and SEC rules.

Available for transactions by an issuer (including all entities controlled by or under common control with the issuer), where:

the aggregate amount sold to all investors during any 12-month period is not more than $1 million;

the aggregate amount sold to any investor during any 12-month period does not exceed:

the greater of $2,000 or 5% of the investor's annual income or net worth, if either annual income or net worth is less than $100,000; and

10% of the investor's annual income or net worth, not to exceed $100,000, if either annual income or net worth is equal to or more than $100,000;

27

Copyright ©2012 Sullivan & Cromwell LLP

27

Copyright ©2012 Sullivan & Cromwell LLP

Crowdfunding Exemption

Other conditions to availability:

the transaction is conducted through a broker or a registered “funding portal” that complies with the requirements of new Section 4A(a); and

the issuer complies with new Section 4A(b) solicitation limitations, disclosure obligations and other requirements and prohibitions.

(continued)

28

Copyright ©2012 Sullivan & Cromwell LLP

28

Copyright ©2012 Sullivan & Cromwell LLP

Required Studies

The SEC is required to conduct studies examining:

the transition to trading and quoting securities in one-penny increments (“decimalization”) and its impact on the number of IPOs and the liquidity for securities of small and mid-cap companies, and

Regulation S-K, to determine how its requirements can be updated to modernize and simplify the registration process and reduce the associated costs and burdens on EGCs.

29

Copyright ©2012 Sullivan & Cromwell LLP

Resources and Information

SEC has posted FAQs on EGC status, confidential registration statement submission, and changes to Exchange Act registration/deregistration:

http://www.sec.gov/divisions/corpfin/guidance/cfjjobsactfaq-title-i-general.htm

http://www.sec.gov/divisions/corpfin/guidance/cfjumpstartfaq.htm

http://www.sec.gov/divisions/corpfin/guidance/cfjjobsactfaq-12g.htm

On several webcasts SEC Division of Corporate Finance Staff has discussed the JOBS Act.

SEC is soliciting comments on all aspects of the JOBS Act, even those that don’t expressly require rule-making:

http://www.sec.gov/spotlight/jobsactcomments.shtml

For those provisions that expressly require rule-making, the SEC is soliciting comments prior to proposing rules.