jurnal auditing

DESCRIPTION

jurnal akuntansi tentang masalah auditTRANSCRIPT

Performance of Auditing Procedures by Governmental Auditors: Some Preliminary EvidenceAuthor(s): Leonard Eugene Berry, Gordon B. Harwood and Joseph L. KatzReviewed work(s):Source: The Accounting Review, Vol. 62, No. 1 (Jan., 1987), pp. 14-28Published by: American Accounting AssociationStable URL: http://www.jstor.org/stable/248043 .

Accessed: 14/11/2012 12:46

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

American Accounting Association is collaborating with JSTOR to digitize, preserve and extend access to TheAccounting Review.

http://www.jstor.org

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

THE A CCOUNTING RE VIEW Vol. LXII, No. 1 January 1987

Performance of Auditing Procedures

by Governmental Auditors: Some

Preliminary Evidence

Leonard Eugene Berry, Gordon B. Harwood, and Joseph L. Katz

ABSTRACT: The evaluation of the quality of governmental auditors' work is of keen interest among governmental audit policy-makers. However, as there is little published evidence on which to base such evaluations at this time, this paper discusses the results of an exploratory study on the subject. The study assumes that the extent to which an auditor actually per- forms the audit procedures prescribed by a given audit program is an important indicator of the quality of the auditor's work. Accordingly, responses were sought from governmental auditors at all levels of government as to their failure to perform prescribed procedures, even though they affirmed performance through sign-offs on their working papers. To offer anonymity to the respondents and to encourage truthful responses, the survey was based on the randomized response technique. The findings indicate that a number of false sign-offs have occurred among governmental auditors as a group. Within the governmental group, the study found that false sign-off rates were slightly higher among auditors at the state level than those at the federal level. Also, rates were slightly higher among auditors not working under a civil service system than those who were, and higher among those who were not certified compared to those who were. It also found that independence of the audit function was not helpful in explaining positive false sign-off rates. However, the significance of these differ- ences as a way of describing the false sign-off rates of governmental auditors was not strong.

T HE requirement that the perfor- mance of governmental auditing procedures be reviewed to deter-

mine whether they have been performed satisfactorily is inherent in the profes- sional auditing standards of the United States General Accounting Office [GAO, 1981]. In most audit organiza- tions this requirement is usually incorpo- rated into a quality control program. In the public accounting profession and pri- vate enterprise internal auditing, an important dimension of quality control has been the regular practice of quality- assurance reviews (also called peer

The authors express their appreciation to the Georgia State University, College of Business Administration Research Committee and the Association of Government Accountants' National Research Board for providing resources to help conduct this research. Also, they appre- ciate the helpful comments of two anonymous reviewers.

Leonard Eugene Berry and Gordon B. Harwood are Professors of Accounting, and Joseph L. Katz isAssociate Professor of Decision Science, all at Georgia State University.

Manuscript received January 1984. Revisions received December 1984, February 1986,

and May 1986. Accepted June 1986.

14

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

Berry, Harwood, and Katz 15

reviews), which assess the quality of audit work of the audit organization as a whole [Pearce and Thornhill, 1985].

During the past five years federal gov- ernment officials have become con- vinced of the need to evaluate the quality of governmental audit work as well. For example, the Office of Management and Budget (OMB) issued Circular A-102 in 1979 requiring a single, organization- wide audit of each governmental unit receiving a grant from the federal gov- ernment in lieu of an audit of the grant alone. The Circular also required that a quality-assurance review be performed on the audit work. The requirements of the OMB Circular have now been enacted into law by the U.S. Congress in the Single Audit Act of 1984.

In prior research related to quality- assessment reviews in governmental auditing, Ferber [1976] discussed a GAO investigation of the internal audit func- tion within the U.S. Department of Transportation. Berry [1978] presented evidence on the nature of the quantita- tive criteria that selected experts in gov- ernmental auditing considered important in evaluating a governmental audit orga- nization. Garner [1980] offered evidence that the low level of funding provided to various federal audit organizations in relation to higher levels of funding pro- vided to many auditee organizations may lead to low audit quality in the federal sector.

An interview with U.S. General Accounting officials by the authors revealed that they have recently com- menced quality-assurance reviews of 20 major audit agencies at the federal level. Also, within the last three years the National Intergovernmental Audit Forum has attempted to establish a vol- untary, national quality-assurance program at the state and local levels, although no research findings appear in

the literature on the extent to which this program has been implemented.

The preceding discussion suggests that there is little research in the literature on the performance of auditing procedures by governmental auditors and the use of quality-assurance reviews for control of audit work. The purpose of this study is to explore (1) whether governmental auditors have failed to perform required auditing procedures and then concealed this omission (hereafter referred to as false sign-offs), (2) the extent to which these false sign-offs exist, and (3) differ- ences in the extent of false sign-offs across certain characteristics of govern- mental auditors and their environment.

A THEORETICAL DEVELOPMENT OF THE ISSUES RESEARCHED

The following discussion outlines some characteristics of governmental auditors and their environment that may explain false sign-off rates.

Governmental Auditors Compared to Private Enterprise Auditors

Previous research has shown that false sign-off rates existed among private enterprise auditors. Rhode [1977, p. 179] found that a large proportion of his par- ticipants (all CPAs and 74 percent in public accounting) indicated that they sometimes engaged in false sign-offs. Time pressures and client-imposed deadlines were the main reasons given for the false sign-offs. Buchman and Tracy [1982] compared the effectiveness of different questionnaire designs in elic- iting sensitive responses from auditors who were CPAs engaged in public ac- counting practice. In the process they also found evidence of false sign-offs. Alderman and Deitrick [1982] found evi- dence of false sign-offs among public accountants due to time budget pressures and Buchman [1983], studying the reli-

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

16 The Accounting Review, January 1987

ability of internal auditors' working papers, found some evidence of false sign-offs within that group as well.

These prior studies on false sign-offs cannot be directly extrapolated to gov- ernmental auditors, as they either expressly excluded governmental audi- tors or only included them in an inci- dental way. Furthermore, notable dif- ferences exist between the scope and environment of governmental auditing and the scope and environment of pri- vate enterprise auditing. Zimmerman [1977] modeled governmental officials as agents of citizens of their governmental entity and posited that these officials will tend to shirk or use their office for politi- cal gain, i.e., to be re-elected or reap- pointed. In turn, citizens and other interested parties (creditors, public inter- est groups, the media, etc.) will create or cause the creation of monitoring activi- ties, such as fund accounting, financial reports, and internal and external audits, to control the behavior of politicians [Baber, 1983; Berry and Wallace, 1986; Ingram, 1984; Ingram and Copeland, 1981; Wallace, 1980; Wallace, 1986].

We suggest that politicians or bureau- crats may circumvent these monitoring activities and induce the audit function to make false sign-offs to suppress the "bad news" effect of negative audit reports. (Wells [1985] presented a case of such an occurrence in state government.) Our rationale is that expanded scope audits are more widely employed in gov- ernmental units than in private enter- prise organizations [Berry and Wallace, 1986]. This results in a broader review of management and decision-making activi- ties than attest and financial audits, with the potential for more negative findings that reflect on the leadership and man- agement abilities of the politician. Fur- ther, since governmental audit reports are usually public information, more fre-

quent media disclosure of negative find- ings tends to occur from these reports. These disclosures could have a negative effect on a politician's chances for re- election or a bureaucrat's chances for reappointment. This type of political environment is not faced by private enterprise auditors.

Another difference between govern- mental auditors and private enterprise auditors is the concern that independent CPAs have with firm reputations [De- Angelo, 1981]. Disclosure of false sign- off rates would have a more negative impact on a public accounting firm's reputation and its ability to hold and obtain new clients. Therefore, public accounting firms would likely have more controls to prevent false sign-offs, so one would expect higher false sign-off rates among governmental auditors.

A final factor that distinguishes the CPA from governmental auditors in our view relates to the CPA's license to prac- tice. If practicing CPAs do not follow generally accepted auditing standards, they stand to lose their licenses to prac- tice. While some governmental auditors may be CPAs, government auditors do not rely on this license to practice gov- ernmental auditing. They are regulated by the governmental unit's policies, and most come under the protection of a civil service system (discussed later). This sug- gests that the penalties for false sign-offs are more severe for practicing CPAs. Thus, we believe the difference in licens- ing requirements to practice would also contribute to higher false sign-off rates among governmental auditors in general compared to practicing independent CPAs.

In summary, previous research in pri- vate enterprise auditing on false sign-offs cannot be extrapolated to the govern- mental audit case. Therefore, the major purpose of this study is to explore

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

Berry, Harwood, and Katz 17

whether false sign-off rates do exist among governmental auditors in general and to what extent. In addition, we identified some intuitively appealing fac- tors that might explain the differences among different classes of governmental auditors. These factors are briefly dis- cussed in the next four sections.

Level of Government

We speculate that the level of govern- ment will affect the pattern of false sign- off rates among governmental auditors for two reasons. First, governmental auditors at the federal level are required by law to follow the GAO auditing stan- dards, but governmental auditors at the state level cannot be legally required by the GAO to follow these standards. Although state and local auditors are strongly encouraged to do so, surveys have reported that state and local gov- ernments have not widely accepted the GAO auditing standards [Dykes and Liao, 1984/85]. The failure to adopt a formal set of auditing standards imposes fewer constraints to guide and control (1) the influence of management over the audit function and (2) the performance of the individual auditor. We believe that this environment would contribute to a higher false sign-off rate at the state level compared to the federal level.

A second reason to expect the level of government to affect the false sign-off rate relates to the establishment of qual- ity controls and sanctions. We believe that politicians have an incentive to resist the establishment of outside quality- assurance reviews over the audit func- tion because this type of review would weaken the politician's influence on the audit function. As reported earlier, although federal auditors are now sub- ject to quality-assurance reviews, there is no evidence that these reviews have been implemented to any appreciable extent in

state audit organizations. This creates an environment at the state level that may facilitate the politician's influence over the audit function. Based on the failure of all state governments to establish mandatory quality assurance reviews and their failure to adopt the GAO auditing standards, we expected to find the false sign-off rate higher at that level.

Independence

We expected that audit independence would also have an effect on the pattern of false sign-off rates among govern- mental auditors. Auditors' independence can be affected by their place within the organizational structure of the govern- mental entity to which they are assigned and also by whether they are auditing internally or externally. Internal audi- tors1 have a higher probability of being placed within the organizational struc- ture where they can be influenced by the management process they are auditing. External auditors, on the other hand, are presumed to be independent of the audited entity, assuming there are no personal or external impairments [GAO, 1981, pp. 19-20].

We believe that governmental internal auditors are less likely to be independent of higher government officials than gov- ernmental external auditors because they are more likely to have external impair- ments to the formation of independent and objective opinions and conclusions. The GAO Auditing Standards define external impairments as the ability of officials external to the audit organiza-

' Governmental internal auditors are defined as gov- ernmental employees reporting to a head auditor who is appointed and is primarily responsible to an official of an executive body at the level of government in which appointed. Governmental external auditors are defined as governmental employees reporting to a head auditor who is appointed or elected and is primarily responsible to a legislative body at the level of government in which appointed [GAO, 1981, pp. 19-21].

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

18 The Accounting Review, January 1987

tion to influence the: (1) assignment of audit personnel, (2) allocation of resources to the audit organization, (3) auditor's judgment as to the appropriate content of an audit report or selection of what is to be audited, and (4) con- tinued employment of the auditor for reasons other than competency [GAO, 1981, p. 19]. Based on this rationale, we expected to find higher false sign-off rates among governmental internal audi- tors than among governmental external auditors.

Civil Service Protection

Whenever feasible, governmental auditors should be employed under a personnel system where compensation, training, job tenure, and advancement are based solely on merit [GAO, 1981, p. 20]. Generally, a civil service system is designed to meet this objective by pro- viding employment protection from poli- ticians who, after an election, may fire employees and appoint political cronies to an audit position without regard to qualifications, and who could also influ- ence the independent judgment of the auditor through other personnel actions as discussed in the previous section. Thus, we expected to find false sign-off rates higher among those governmental auditors who were not protected by a civil service system.

Certification

To be certified, a CPA or CIA must meet a minimum set of educational, experience, and ethical standards, and the penalty for not maintaining these standards could be the loss of certifi- cation. The penalty is more severe for CPAs in public accounting than those in governmental auditing because CPAs in public accounting convicted of violating the AICPA code of ethics can lose their license to practice accounting, whereas

governmental auditors have no single profession-wide certification program. Although some governmental auditors are certified from previous practice in industry or are certified to enhance their professional credentials, there is no requirement that they be certified. The behavior of governmental auditors is controlled primarily by governmental policies and regulations and not by the standards of certification bodies. Thus, we expected that certification would have little effect on the false sign-off rates between categories of governmental auditors.

RESEARCH METHOD

A questionnaire was mailed to a sam- ple of 1,600 auditors selected randomly from the membership list of the Asso- ciation of Government Accountants (AGA). (Part of the questionnaire appears in Appendix A.) The list was stratified into federal, state, and local members to test the level-of-government effect. The size of the sample within each stratum was based on the percentage relationship of that stratum, as reflected in the membership list, to the overall number of AGA members in all three categories. Those members of the AGA whose job category was other than gov- ernmental auditing were excluded from the sampling procedures. The AGA membership was selected as the sampling frame because that organization has more governmental auditors than any other professional organization. The first questionnaire item qualified the respondent as to performance of work as a governmental auditor in the last five years. The respondents answering no were excluded from the overall sample and were asked to mail the questionnaire back without completing it.

Two weeks after the first question- naire, a follow-up questionnaire was

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

Berry, Harwood, and Katz 19

TABLE 1

PROFILE OF RESPONDENTS

Demographic Variable Number Percent

Level of Government at which Employed Federal 495 55.6

State 295 33.1

Local 101 11.3

Total 897 100.0

Number of Years Employed as a Governmentl A editor 0-2 years 7.9*

2-5 years 21.1

6-10 years 23.8

11 and above 47.2

Total 100.0

Type of Certification Certified Public Accountant 13.2**

Certified Internal Auditor 30.4**

Position of Head Auditor Elected 13.3*

Appointed, reporting to legislature 26.2

Appointed, reporting to executive branch 60.5

Working Under a Civil Service System? Yes 75.6*

No 24.4

* Percentages have been adjusted for missing values and nonresponses. ** Some respondents indicated that they were both a CPA and a CIA.

mailed to all sample members who had not responded. A test for nonresponse bias yielded no statistical difference between responses received before and after the follow-up. A total of 1,042 usable responses were received, repre- senting a response rate of 65.1 percent. Of this total, 897 individuals (86.1 per- cent) affirmed working in governmental auditing at some time during the pre- ceding five years. A more detailed demo- graphic profile of the respondents is displayed in Table 1.

In addition to demographic questions, each respondent was asked to answer ten questions that would indicate a false sign-off if answered affirmatively (see Appendix A). The first nine questions asked if the respondent had ever, whether because of time pressure or for another reason, indicated on working papers that a specific audit procedure had been performed, when in fact it had not. The tenth question asked directly whether the respondent had ever accepted a bribe. The first nine questions

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

20 The Accounting Review, January 1987

addressed key audit procedures in a financial and compliance type audit, the most common types of audits conducted at all levels of government. The ques- tions were selected because of their commonality to all groups of govern- mental auditors. Failure to perform or truthfully document any of these pro- cedures would seriously compromise the responsibility of the auditor and seri- ously weaken the value of the audit report to the users. The acceptance of a bribe would constitute one of the most serious instances of fraud that could be committed by a governmental official of any rank or position.

Because the failure to perform any of the procedures or the acceptance of a bribe could provide the basis for dis- missal proceedings against the respon- dent, respondents could be expected to conceal such misdeeds. To offer ano- nymity to individual respondents and encourage truthful responses, a random- ized-response (RR) questionnaire (see Warner [1965], for example) was used. This technique has been used in account- ing research by Buchman and Tracy [1982] and Buchman [1983] in their stud- ies mentioned above, and the validity of the RR method in eliciting responses to sensitive questions was demonstrated by Tracy and Fox [1981].

A questionnaire based on the RR tech- nique presents each sensitive question in tandem with an innocuous question. The respondent is asked to select and answer one question in each pair based on the outcome of a random process. In this study, the random process was the occur- rence of specified digits in the serial number of a currency bill drawn from the respondent's own wallet. Although the random process prevents the experi- menter from ascertaining which question in each pair an individual respondent selects, the expected proportion of all

respondents answering the sensitive ques- tion can be computed. The mathematical procedure for these calculations has been demonstrated by Greenberg et al. [1969], and a summary is presented in Appendix B.

ANALYSIS AND FINDINGS

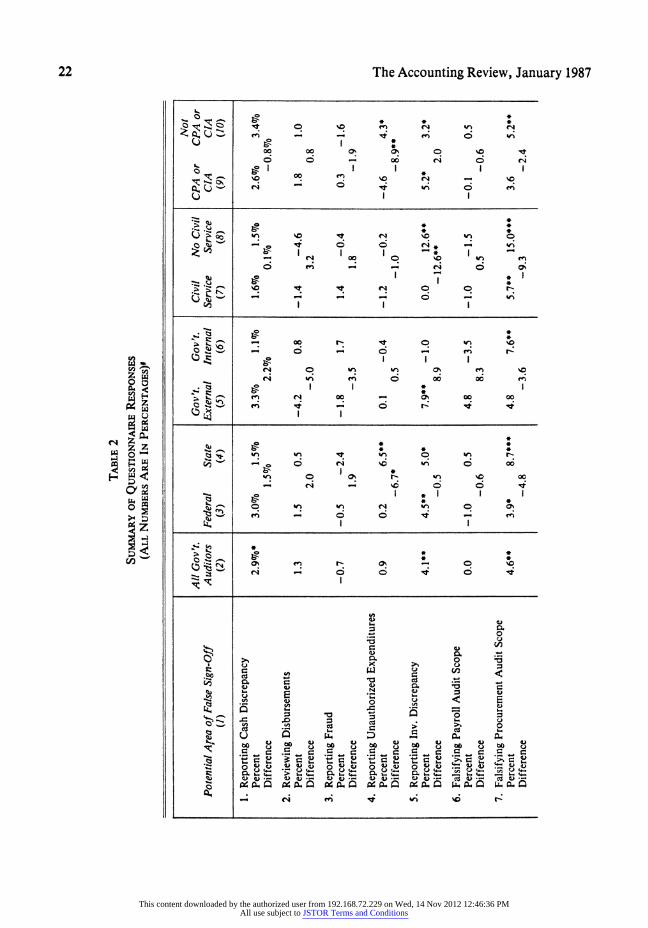

Table 2 displays a summary of the responses to each of the ten sensitive questions. Column 2 gives the estimated percentage of false sign-offs by all gov- ernmental auditors to each of the ten questions. Negative rates can arise because of the adjustment to account for expected responses to the innocuous questions. Of the seven items in column 2 with positive false sign-off rates, four are significantly greater than zero at the .01 level. This suggests that a statistically significant, though small, percentage of governmental auditors have failed to apply proper auditing procedures in four of ten key areas of a financial or com- pliance audit. The following discussion breaks down the findings in Table 2 with respect to the characteristics of govern- mental auditors and their environment.

Level of Government

We postulated that the false sign-off rates of state auditors would be higher than those of federal auditors.2 The data on this point are shown in columns 3 and 4 of Table 2. The sign-off rate for state auditors was higher than for federal auditors for seven questions, and these differences were significantly greater on

2 We originally intended to compare the false sign-off rates of local auditors to those of federal auditors and then to those of state auditors. However, the number of local auditors responding (101) was too low for the RR method to (1) provide meaningful comparisons and (2) to assess significance of individual false sign-off rates when compared to zero. Therefore, these tests were not made with respect to local auditors. Further research that includes a larger sample of local auditors will be required.

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

Berry, Harwood, and Katz 21

questions 4 and 9. The federal auditors were higher on only three questions, and none of these differences was significant. For questions 3 and 10, the two most sensitive questions asked, both groups had a zero or negative false sign-off rate. This result suggests that neither federal nor state governmental auditors are likely to accept a bribe or fail to carry out their responsibility to report fraud.

Because some of the differences are very large (questions 4, 7, and 9), there is the suggestion that the state group may have a higher incidence of false sign- offs. However, the sensitivity of the test as well as the RR technique preclude a strong assertion to this effect.

Independence

We also postulated that governmental internal auditors and governmental external auditors would have different false sign-off rates because of the orga- nizational independence factor. Spe- cifically, we thought internal auditors would be more likely to experience exter- nal impairments to independence and therefore would have a higher false sign- off rate. However, the results in columns 5 and 6 of Table 2 do not suggest that this is so. On six of the ten questions, external auditors had higher false sign- off rates, though none tested significantly higher.

We analyzed state internal and exter- nal auditors and federal internal and external auditors separately and found essentially the same results. We were somewhat puzzled at these findings and can only speculate on the reasons. Per- haps governmental external auditors are not as independent as we had theorized, or perhaps internal auditors are more independent. This could be particularly true at the federal level where the agency head may supervise several management levels and where the internal audit head

could be relatively independent from the lower operating levels.

Civil Service Protection

We predicted that civil service protec- tion would tend to insulate the audit function from the influence of politi- cians. Columns 7 and 8 of Table 2 show that auditors not under a civil service system had higher false sign-off rates on six out of ten questions. The rates were significantly higher on question 5. Four questions had higher false sign-off rates for auditors who were under a civil ser- vice system, but none was significant. These results suggest that lower false sign-off rates tend to be weakly associ- ated with a civil service system. Finding significant differences on only one out of ten questions, and given the sensitivity of the test and the nature of the RR tech- nique, precludes a stronger assertion to this effect.

Certification

Finally, we postulated that profes- sional certification as a CPA or CIA would have little association with inci- dence of false sign-offs between federal auditors and state and local auditors. Our reasoning was that neither group is required to be certified, and there are no sanctions against a governmental auditor per se for violating the code of ethics governing CPAs and CIAs. Columns 9 and 10 of Table 2 show that auditors who were not certified had a higher false sign-off rate on eight questions. The dif- ferences on questions 4 and 10 were sig- nificant. On the other two questions, those who were certified had higher rates than those who were not certified. None of these was significant. These findings suggest-contrary to our expectations- that certification may have some effect on false sign-offs among governmental auditors.

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

22 The Accounting Review, January 1987

6 6 _ x00 f-i 0

;C--s v0 db t N O O e4 W

o t 4 _ X F t _ bC14 0

X x Oo 1 I I |

O~~~ %0w N 00 *0r

FZ - 006

CO)

0~~~~~~ 04 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

e-4 00 '0 -0

4C4

eq Z3

o~~~~' m ei 0 0 r uo

z~~~~~~~~~

00 _1<, _ o o C 0

00 '| ' eX 0 ~ vC t- I '0

~~ r'~~~~~ 6 c45 00 1

) -L' z ei 00 0% 00 00 o

0 WI 1 IO C;| > cO _

Cd Cn6 C C: Cd:

U "4 :D 3 - a

0 0 %0 bo I0 bo to

u_ oul D ou U 0 6Q, 6 O

* ,a *. 4. > S.. 4. 1. C6. S. to. +,S.. 4 .. 4 .g 0E o 0 a .- 0 0 Co 0 0 C%

o 044m9 W;

t a; :2; aX X1v*

4) 4) 4) 0

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

Berry, Harwood, and Katz 23

An~~~~~~~~~~~~~~~~dd

bat 0fi 0 N 0

* 0

0 *~~~~~~~

0 0

04 -f 0

, 3

i ) I ^1 i .)v !ce !_ ;2 55

0

*n a

0o or 0

I 4)

0 ~ ~ I *

0o

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

24 The Accounting Review, January 1987

Finally, we compared false sign-off rates for similar questions used in studies of private enterprise internal auditing to those in our study. Studies of indepen- dent CPAs did not contain similar ques- tions. Of those questions that were simi- lar, governmental auditors had a higher false sign-off rate on three, while private enterprise internal auditors had a higher rate on the remaining two. When both sets of ten questions were considered, regardless of similarity, private enter- prise internal auditors only had a false sign-off rate significantly greater than zero at the .10 level on two of their ten questions while governmental auditors had a significantly higher rate on four of their ten (as this study previously indicates). This weakly supports our assumption that the false sign-off rates are different between private enterprise and governmental auditors.

SUMMARY AND CONCLUSIONS

This exploratory study gathered infor- mation about false sign-offs in selected key areas of governmental audit. We were aware at the outset that prior studies have reported false sign-off rates among certain classes of auditors, but these studies either excluded govern- mental auditors or included them only in a minor way. Also, we argued that the nature and practice of governmental auditing is considerably different from private enterprise auditing. In addition, the study attempted to identify differ- ences in the extent of any false sign-offs across certain characteristics of govern- mental auditors and their environment. These characteristics were the level of government at which an auditor works, the organizational independence of an auditor, the existence of civil service pro- tection, and an auditor's certification as a CPA or CIA.

The results indicate that there were

significant sign-offs in four out of nine auditing procedures relating to a finan- cial or compliance-type audit among the 897 responding governmental auditors taken as a whole. No group had a signif- icant positive result on the question of having ever taken a bribe. State auditors had significantly higher false sign-off rates than federal auditors on two of the ten questions.

Governmental external auditors indi- cated slightly more false sign-offs than governmental internal auditors. We had expected the opposite effect, but since none of the differences was significant, we concluded that independence was not useful in explaining differences in false sign-off rates among governmental audi- tors.

Governmental auditors under a civil service system indicated significantly higher false sign-off rates on one of the ten questions. Governmental auditors who were certified as a CPA or CIA had significantly higher false sign-off rates than those who were not certified on two of the ten questions. We had expected that certification would have little effect on the false sign-off rates of govern- mental auditors.

On the basis of the survey we conclude that there were significant false sign-off rates among governmental auditors as a whole. The results suggest that level of government, civil service protection, and certification might be useful in attempt- ing to identify some differences in these false sign-off rates across certain char- acteristics of governmental auditors and their environment. However, these points should be interpreted in light of the fact that of 40 different tests, only five tests found significant differences and in light of the sensitivity and nature of the RR technique. Although there are indications that some governmental audi- tors have falsely signed off on auditing

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

Berry, Harwood, and Katz 25

procedures, information about the num- ber of times they have done so and how long ago is not available. Furthermore, the data for this study were drawn from a representative sample of governmental auditors who belong to the Association of Government Accountants. Although a large percentage of federal and state auditors belong to this organization, they may not be representative of all governmental auditors at these levels of

government. Future studies should investigate the

incidence of false sign-offs in other areas of governmental audit work. Also, why certain audit procedures have a higher false sign-off rate than others should be investigated to identify incentives that might be helpful in explaining the occur- rence of false sign-off rates. An agency theoretic framework might be helpful in this regard.

APPENDIX A

A STUDY OF THE CONDUCT OF GOVERNMENT AUDITORS IN PERFORMING AUDITING PROCEDURES

(Note: Please DESTROY this page after entering your answers on the ANSWER SHEET.)

II. Instructions. The following questions ask you to provide some information that may be sensitive, so we are using an unusual technique to neutralize your answers. Specifically, an innocuous masking question is paired with every potentially sensitive question below. You will be asked to answer only one question in each pair, and only you will know whether the question you answered was the potentially sensitive question or the innocuous masking question.

To accomplish this, you will be asked to use the serial number on a currency bill taken from your wallet to determine which question in each pair to answer. Only you will know the bill's serial number. Statistically we know the number of respondents answering each question in total, so we can estimate the aggregate answer to each. At this point, please take a currency bill from your wallet. You will need only the last three digits of the bill's serial number. As noted at the top of this page, you DESTROY this page after entering your answers on the ANSWER SHEET so you may record the last three digits of your bill's serial number in the space below for easy reference:

Now, please record your answer to the question you select from each of the following pairs of questions, on the ANSWER SHEET.

1. If the LAST digit of your bill's serial number is 4, 5, or 6 answer question IA; otherwise answer question lB.

IA. Is the LAST digit of your bill's serial number even?

1 B. Have you ever, whether because of time pres- sure or other reasons, failed to indicate on audit working papers a discrepancy between the amount of cash that you physically

counted and the cash account balance (regard- less of the amount involved)?

2. If the NEXT TO LAST digit of your bill's serial number is 4, 5, or 6 answer question 2A; otherwise answer question 2B.

2A. Is the NEXT TO LAST digit of your bill even?

2B. Have you ever, whether because of time pres- sure or other reasons, indicated in any way on the audit working papers that you have carried out an audit procedure regarding the review of an audited organization's internal control over approvals of cash disbursements, when in fact you did not?

3. If the THIRD TO LAST digit of your bill's serial number is 4, 5, or 6 answer question 3A; otherwise answer question 3B.

3A. Is the THIRD TO LAST digit of your bill's serial number even?

3B. Have you ever, whether because of time pres- sure or the extra paperwork involved or any other reason, failed to report the occurrence of fraud (regardless of amount involved)?

4. If the LAST digit of your bill's serial number is 7, 8, or 9 answer question 4A; otherwise answer question 4B.

4A. Is the LAST digit of your bill's serial number odd?

4B. Have you ever, whether because of time pres- sure or other reasons, failed to report the expenditure of government funds for pur- poses other than those authorized by govern- ment regulation or appropriations?

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

26 The Accounting Review, January 1987

APPENDIX A-Continued

5. If the NEXT TO LAST digit of your bill's serial number is 7, 8, or 9 answer question 5A; otherwise answer question 5B.

5A. Is the NEXT TO LAST digit of your bill's serial number odd?

5B. Have you ever, whether because of time pres- sure or other reasons, failed to indicate on audit working papers a discrepancy between the quantity of inventory that you physically counted and the inventory account balance (regardless of the quantity involved)?

6. If the THIRD TO LAST digit of your bill's serial number is 7, 8, or 9 answer question 6A; otherwise answer question 6B.

6A. Is the THIRD TO LAST digit of your bill's serial number odd?

6B. Have you ever, whether because of time pres- sure or other reasons, indicated in any way on the audit working papers that you examined more payroll transactions than you actually did?

7. If the LAST digit of your bill's serial number is 1, 2, or 3, answer question 7A; otherwise answer question 7B.

7A. Is the LAST digit of your bill's serial number odd?

7B. Have you ever, whether because of time pres- sure or other reasons, indicated in any way on the audit working papers that you carried out an audit procedure regarding reviewing and testing internal control of purchase orders and procurement, when in fact you did not?

8. If the NEXT TO LAST digit of your bill's serial number is 1, 2, or 3 answer question 8A; otherwise answer 8B.

8A. Is the NEXT TO LAST digit of your bill's serial number odd?

8B. Have you ever, whether because of time pres- sure or other reasons, indicated in any way on the audit working papers that you examined more supply (logistics) transactions (e.g., shipments, receipts, issues and turn-ins) than you actually did?

9. If the THIRD TO LAST digit of your bill's serial number is 1, 2, or 3 answer question 9A; otherwise answer question 9B.

9A. Is the THIRD TO LAST digit of your bill's serial number odd?

9B. Have you ever, whether because of time pres- sure or other reasons, indicated in any way on the audit working papers that you carried out an audit procedure regarding review and testing of internal control of an EDP system, when in fact you did not?

10. If the LAST digit of your bill's serial number is 4, 5, or 6 answer question lOA; otherwise answer question lOB.

lOA. Is the LAST digit of your bill odd?

lOB. Have you ever accepted a bribe (regardless of the amount)?

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

Berry, Harwood, and Katz 27

APPENDIX B

STATISTICS OF THE RANDOMIZED RESPONSE TECHNIQUE

Let N=the total number of responses to the pair of questions, n =the number of yes responses to the pair of questions, p =the probability of answering the sensitive question in the pair,

1-p =the probability of answering the innocuous question in the pair, 0 =the probability of a yes response given the innocuous question, and -r=the probability of a yes response given the sensitive question.

Then,

P(yes response) =P(yes response sensitive question)P(sensitive question) +P(yes response | innocuous question)P(innocuous question).

Mathematically, this is equivalent to:

n/N= rp + 0(1 -p). (1)

Solving equation (1) for ir yields

'r = [n/N-(1 -p)0]/p. (2)

It follows [see Greenberg et al., 1969] that

VAR( 7r) = [n/N(1 - n/N)]/Np2, (3)

and (7r-O)/V Varl(r) follows a standard normal distribution.

REFERENCES

Alderman, C. W., and J. W. Deitrick, "Auditors' Perceptions of Time Budget Pressures and Premature Sign-offs: A Replication and Extension," Auditing: A Journal of Practice and Theory (Winter 1982), pp. 54-68.

Baber, W. R., "Toward Understanding the Role of Auditing in the Public Sector," Journal ofAccounting and Economics (1983), pp. 214-227.

Berry, L. E., "Quantitative Criteria for Evaluating Overall Performance of a Government Audit Organi- zation: An Empirical Study," The Government Accountants Journal (Summer 1978), pp. 43-52.

, and W. A. Wallace, "Governmental Auditing Research: An Analytic Framework, Assessment of Past Work, and Future Directions," Research in Governmental and Non-Profit Accounting (JAI Press, 1986), pp. 89-115.

Buchman, T. A., "The Reliability of Internal Auditors' Working Papers," Auditing: A Journal of Prac- tice and Theory (Fall 1983), pp. 92-103.

, and J. A. Tracy, "Obtaining Responses to Sensitive Questions: Conventional Questionnaire ver- sus Randomized Response Technique," Journal of Accounting Research (Spring 1982), pp. 263-271.

DeAngelo, L. E., The Auditor-Client Contractual Relationship: An Economic Analysis (UMI Research Press), 1981.

Dykes, J. M., and S. S. Liao, "Internal Auditing in Local Governmental Units," The Government Accountants Journal (Winter 1984/85, pp. 23-29).

Ferber, M. M., "Evaluating Internal Audit," GAO Review (Summer 1976), pp. 56-60. GAO, Standards for Audit of Governmental Organizations, Programs, Activities and Functions (United

States Printing Office, 1981). Garner, D. E., "A Comparison of Audit Costs in the Federal and Private Sectors," The Government

Accountants Journal (Summer 1980), pp. 37-46.

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions

28 The Accounting Review, January 1987

Greenberg, B. G., A. A. Ela, W. R. Simons, and D. G. Horvitz, "The Unrelated Question Randomized Response Model: Theoretical Framework," Journal of the American Statistical Association (June 1969), pp. 520-539.

Ingram, R. W., "Economic Incentives and the Choice of State Government Accounting Practices," Jour- nal of Accounting Research (Spring 1984), pp. 126-144.

, and Ronald M. Copeland, "Municipal Accounting Information and Voting Behavior," THE ACCOUNTING REvIEw (October 1981), pp. 830-843.

Lansing, J., "Local Government Auditing," Public Sector News (American Accounting Association, 1983), pp. 1-3.

Pearce, P. A., and W. T. Thornhill, "What Are the Lessons of Quality-Assurance Reviews?", The Inter- nal Auditor (February 1985), pp. 34-37.

Rhode, J. G., Survey on the Influence of Selected Aspects of the Auditor's Work Environment on Pro- fessional Performance of Certified Public Accountants: A Study and Report for the Commission on Auditors'Responsibilities (AICPA, 1977).

Tracy, P. E., and J. A. Fox, "The Validity of Randomized Response for Sensitive Measurements," American Sociological Review (April 1981), pp. 187-200.

Wallace, W. A., The Economic Role of the Audit in Free and Regulated Markets (Touche Ross Founda- tion, 1980).

, "The Timing of Initial Audits of Municipalities: An Empirical Test," Research in Governmental and Non-Profit Accounting (JAI Press, 1986), pp. 3-51.

Warner, S. L., "Randomized Response: A Survey Technique for Eliminating Evasive Answer Bias," Jour- nal of the American Statistical Association (March 1965), pp. 63-69.

Wells, S. F., "Ethics in Practice-A Personal Challenge," The InternalAuditor (February 1985), pp. 58- 62.

Zimmerman, J., "The Municipal Accounting Maze: An Analysis of Political Incentives," Supplement to Journal of Accounting Research (Supplement 1977), pp. 117-127.

This content downloaded by the authorized user from 192.168.72.229 on Wed, 14 Nov 2012 12:46:36 PMAll use subject to JSTOR Terms and Conditions