kansas insurance department medicare supplement · kansas insurance department. medicare...

TRANSCRIPT

Kansas Insurance Department

Medicare supplement

insurance shopper’s guideeffective March 1, 2015

Commissioner of InsuranceKen Selzer, CPA

March 2015

Dear Kansas consumer,

If you have picked up this guide, chances are you are somewhat familiar with Medicare — a federally-funded health insurance program for people with disabilities and people age 65 and older. Although Medicare may pay a large part of your health care expenses, it doesn’t cover every service or medical supply. Medicare recipients are responsible for paying coinsurance and deductibles.

This guide will help you evaluate your health care insurance needs. It will also help you gather accurate information concerning Medicare, Medicare supplement and other health insurance options so you can make decisions that will prevent serious, costly problems.

Toward the middle of this book, you’ll find rate comparisons of companies selling various Medicare supplement insurance plans. These rates were accurate as of March 2015. For the most up-to-date rate comparisons, visit our website, www.ksinsurance.org.

If you have questions or need assistance understanding insurance issues, don’t hesitate to contact the Kansas Insurance Department’s Consumer Assistance Hotline toll-free at 800-432-2484. Our trained staff is dedicated to helping answer your insurance questions and finding solutions to your problems.

Sincerely,

Ken Selzer, CPA Commissioner of Insurance

Medicare supplementinsurance shopper’s guide

Section I: About Medicare Supplement and Medicare SELECT Insurance 2

Overview of Medicare Parts A & B 6 Your Medicare coverage choices at a glance 7 Details of Plans A - N 8 Medicare supplement insurance at a glance 28

Section II: Medicare Supplement andMedicare SELECT Rates 29

Appendix I: About Medicare and Medicare Advantage Plans 41

How is Medicare divided? 42

Appendix II: Consumer Protections and Other Resources 49 Protections when you lose coverage 49 Tips & Warnings 52 Glossary of Terms 54 What you need to know in 2015 56 Customer service phone numbers inside back cover

Table of Contents

Section I: About Medicare Supplement and Medicare SELECT Insurance

What is Medicare supplement insurance?

Medicare supplement insurance can help cover the expenses that come with the gaps in Original Medicare (described in further detail in Appendix 1). This supplemental insurance is also often called “Medigap” because it helps pay for these gaps. Medicare supplement policies can only be pur-chased with Original Medicare - you may not have a Medicare supplement policy if you have a Medicare Advantage plan. The Kansas Insurance Department is responsible for regulating Medicare supplement insurance in the state of Kansas.

Costs that you must pay, like coinsurance, copay-ments and deductibles, are examples of some of the gaps in Original Medicare coverage. You might want to consider buying a Medicare supplement policy to cover these expenses. Some Medicare supple-ment policies also cover benefits that the Original Medicare plan doesn’t cover, like emergency health care while traveling outside the United States. A Medicare supplement policy may help you save on out-of-pocket costs.

How does Medicare supplement insurance work?

Medicare supplement insurance is broken down into plans identified by letters - A, B, C, D, F, G, K, L, M & N. These plans are standardized and must fol-low federal and state laws, which have been created to protect you, the consumer. (Details about each of these plans is available later in this booklet.) These plans are sold by private insurance companies, but all plans identified by the same letter have the same benefits. That is, plans identified as “Plan A” in the state of Kansas are identical, regardless of the company that is selling it. However, the cost of the plan will vary depending on the company that provides it.

All companies in the state of Kansas that wish to sell Medicare supplement insurance must make Plan A available to their customers. If they want to offer additional Medicare supplement plans, they must also offer either Plan C or Plan F. Plan A features the core benefits of a Medicare supplement policy. All other plans build upon this.

How are premium rates determined?

Premium rates for Medicare supplement insurance policies are determined in one of two ways:

Issue age - The company will not raise your premi-um just because you are getting older. Your premi-um will always be based on your age when you pur-chased the policy, but it will be adjusted for other factors, like inflation. If you buy a plan at age 65, you will always pay the current premiums charged to 65-year old customers, regardless of your current age. Issue age policies can be more costly up front but also can save money in the long run.

2015 Medicare Supplement Shopper’s Guide02

Attained age - For rates determined by attained age, the premium will increase as you get older. If you buy a plan at age 65, you may have a premium increase each year.

Enrollment Periods

Medicare supplement enrollment periods differ from other Medicare enrollment periods. Insurers must offer a six-month open enrollment period to all Medicare beneficiaries. This six-month period begins with the first month in which the beneficiary first enrolled for benefits under Medicare Part B (for many people, this is age 65; for others, it be-gins when you lose employer- or group-sponsored health care). During this six-month period, insur-ers are required to offer any Medicare supplement policy to all enrollees, regardless of their health sta-tus. During this time, the same amount is charged to both healthy individuals and those with medical conditions. After this six-month period ends, in-surers are allowed to use medical underwriting to determine whether or not you are accepted into the plan and, if so, how much you will be charged, so it is important to evaluate your options carefully during your first enrollment period. Should you decide to switch to a different Medicare supplement policy after this open enrollment period, you may be subject to medical underwriting.

The six-month open enrollment period for Medicare supplement insurance starts on the same day your Part B Medicare starts. This date is shown on your Medicare card.

Medicare SELECT insurance

Medicare SELECT is another option available to some Kansas Medicare beneficiaries. Medicare SELECT policies are just like standardized Medi-care supplement policies. However, each Medicare SELECT policy has specific hospitals and, in some cases, doctors that you must use in order to be eli-gible for full benefits (except in the case of medical emergencies).

Because the insurers negotiate directly with specific providers (sometimes called “preferred providers”), premium costs for Medicare SELECT plans are gen-erally lower than a standard Medicare supplement policy. When you choose to use a preferred provid-er, Medicare pays its share of the approved charges and the Medicare SELECT policy pays for the full supplemental benefits provided for in the policy.

Beneficiaries with disabilitiesDisabled Medicare beneficiaries under age 65 have equal access to all Medicare supplement policies sold in Kansas.

• Upon enrolling in Medicare Part B, a disabled ben-eficiary has a 6-month open-enrollment period to buy supplement coverage. That period begins the day Part B coverage becomes effective.

• Supplement policies must be sold at the same rate as for seniors who turn 65 and are eligible for Medicare.

• Disabled Medicare beneficiaries cannot be turned down for any Medicare supplement plan being sold in Kansas during the initial 6-month open-enrollment period.

• Coverage will be guaranteed issue, but the same pre-existing condition limitation as applies to age 65 beneficiaries may apply. A second open-enrollment period will apply when the disabled Medicare benefi-ciary turns 65.

2015 Medicare Supplement Shopper’s Guide 03

If you do not want to use the preferred provider, Medicare will still pay its share of approved charges. However, the Medicare SELECT policy would not be required to pay any benefits.

A comparison shopper’s guide for both Medicare supplement policies and Medicare SELECT policies for premium rates is available in Section II of this book.

Services provided under Medicare supplement policies

The following services are provided under Medi-care. Medicare supplement plans help pay for portions of these services not covered by Medicare. The following details, from www.Medicare.gov, will help you determine whether or not you will need a supplement policy.

Hospitalization - Medicare covers a semiprivate room, meals, general nursing, and other hospital services and supplies. This includes care in criti-cal access hospitals and inpatient mental health care. This does not include private duty nursing or a television or telephone in your room. It does not include a private room, unless medically necessary. Medicare does not cover Part A deductible, coin-surance, or coverage after your allotted number of days have been used each benefit period.

Skilled Nursing Facility Care - Medicare covers a semiprivate room, meals, skilled nursing and reha-bilitative services, and other services and supplies (after a related 3-day hospital stay). You must have been admitted to the Medicare-approved nursing

facility within 30 days of leaving the hospital. Medi-care does not cover coinsurance or coverage after 100 days per benefit period.

Blood - Medicare covers pints of blood you get at a hospital or skilled nursing facility during a covered stay after the first three pints. You are responsible for the cost of the first three pints and the Part B deductible.

Hospice Care - Medicare covers medical and sup-port services from a Medicare-approved hospice for people with a terminal illness, drugs for symptom control and pain relief. Hospice care is given in your home. However, short-term hospital and inpatient respite care (care given to a hospice patient by an-other caregiver so that the usual caregiver can rest) are covered when needed. You must have a doctor’s certification of a terminal illness. Medicare does not cover the copayment or coinsurance.

Medical Expenses - Medicare covers doctor ser-vices, outpatient medical and surgical services and supplies, diagnostic tests, ambulatory surgery center facility fees for approved procedures, and durable medical equipment (such as wheelchairs, hospital beds, oxygen, and walkers). It also covers second surgical opinions, outpatient mental health care, outpatient physical and occupational therapy, including speech-language therapy. Medicare does not cover the Part B deductible or coinsurance.

Clinical Laboratory Services - Medicare covers blood tests, urinalysis and other tests for diagnostic services.

2015 Medicare Supplement Shopper’s Guide04

2015 Medicare Supplement Shopper’s Guide 05

Home Health Care - Medicare covers part-time skilled nursing care, physical therapy, occupational therapy, speech-language therapy, home health aide services, medical social services, durable medi-cal equipment (such as wheelchairs, hospital beds, oxygen, and walkers) and medical supplies, and other services. Medicare does not cover the Part B deductible.

The following services are not covered under Medicare, but may be covered by some Medicare supplement plans:

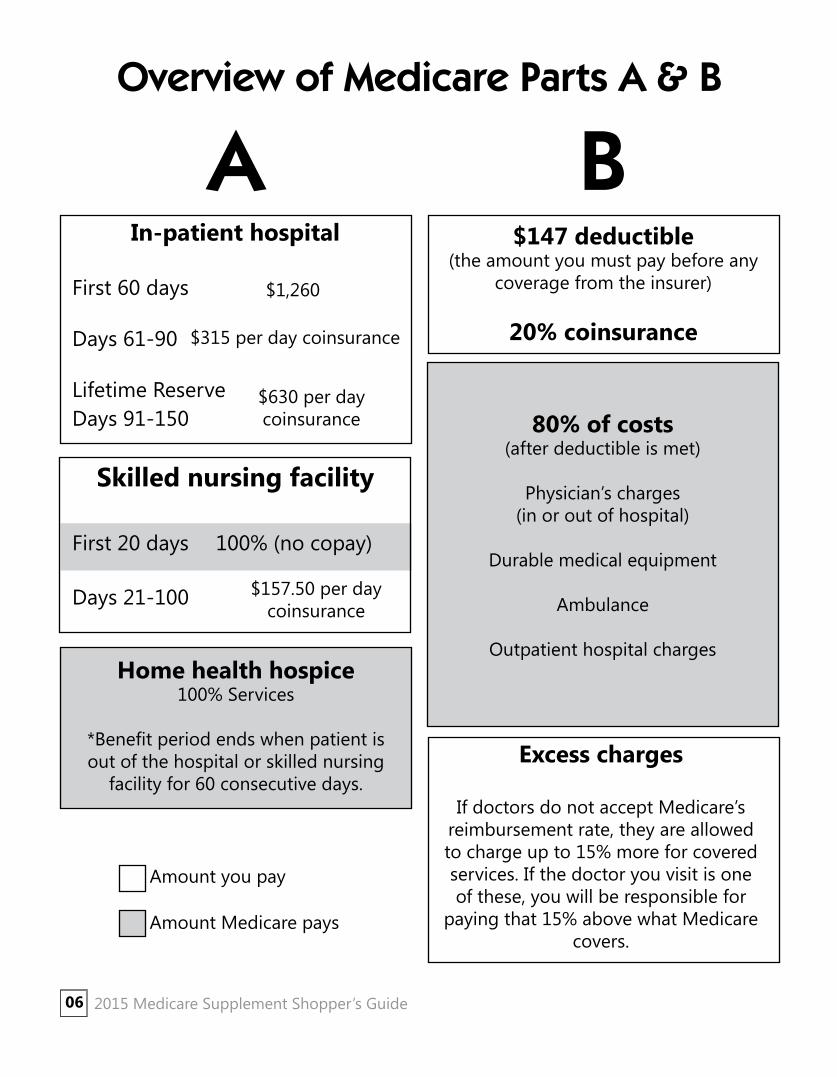

Part B Excess charges - “Excess charges” are not covered under Medicare. If doctors decide not to accept the reimbursement rate they receive from Medicare for providing certain services, they are al-lowed to charge up to 15% more for those covered services. If the doctor you visit is one of these, you will be responsible for paying that 15% above what Medicare covers. The Medicare supplement policy may cover some or all of your expenses above the Medicare approved amounts.

Foreign Travel - Some Medicare supplement poli-cies will cover some of your expenses related to emergency care while traveling outside the United States.

Benefit time frames

Part A of Medicare is based on a “per-benefit pe-riod” timeline. According to Medicare, a “benefit period” begins the day you go into a hospital or skilled nursing facility (SNF). The benefit period ends when you haven’t received any hospital care (or skilled care in a SNF) for 60 days in a row. If you return to the hospital or SNF before the end of that 60 day period, it will be considered part of the same benefit period. If you go into a hospital or a SNF after one benefit period has ended, a new benefit period begins. You must pay the inpatient hospital deductible for each benefit period. There is no limit to the number of benefit periods an enrollee may have.

Part B benefits are based on the calendar year, which begins January 1 of each year and ends De-cember 31.

Overview of Medicare Parts A & B

A B

$157.50 per day coinsurance

$630 per day coinsurance

$315 per day coinsurance

$1,260

Home health hospice100% Services

*Benefit period ends when patient is out of the hospital or skilled nursing

facility for 60 consecutive days.

$147 deductible(the amount you must pay before any

coverage from the insurer)

20% coinsurance

80% of costs(after deductible is met)

Physician’s charges(in or out of hospital)

Durable medical equipment

Ambulance

Outpatient hospital charges

Excess charges

If doctors do not accept Medicare’s reimbursement rate, they are allowed to charge up to 15% more for covered services. If the doctor you visit is one of these, you will be responsible for

paying that 15% above what Medicare covers.

Amount you pay

Amount Medicare pays

2015 Medicare Supplement Shopper’s Guide06

In-patient hospital

First 60 days

Days 61-90

Lifetime ReserveDays 91-150

Skilled nursing facility

First 20 days 100% (no copay)

Days 21-100

Your Medicare Coverage Choices at a GlanceThere are two main ways to get your Medicare coverage: Original Medicare (Parts A and B) or a Medicare Advantage Plan (Part C). Use these steps to help you decide which way to get your coverage.

StartStep 1: Decide how you want to get your coverage

orMEDICARE ADVANTAGE

PLAN(like an HMO or PPO)

Part CCombines Part A, Part B and

usually Part D

Step 2: Decide if you need to add drug coverage

Part DPrescription drug coverage

Part DPrescription drug coverage

(if not already included)

END

MedigapMedicare supplement insurance

NOTE: If you join a Medicare Advan-tage Plan, you don’t need a Medicare supplement policy. If you already have a Medicare supplement policy, you can’t use it to pay for out-of-pocket costs you have under a Medicare Advantage Plan. If you already have a Medicare Advan-tage Plan, you can’t be sold a Medicare supplement policy.

ORIGINAL MEDICARE

Part A Hospital insurance

Part B

Medical insurance

Step 3: Decide if you need to add supplemental coverage

Step 2: Decide if you need to add drug coverage

END

2015 Medicare Supplement Shopper’s Guide 07

For more information on Original Medicare and Medicare Advantage plans, see

Appendix I.

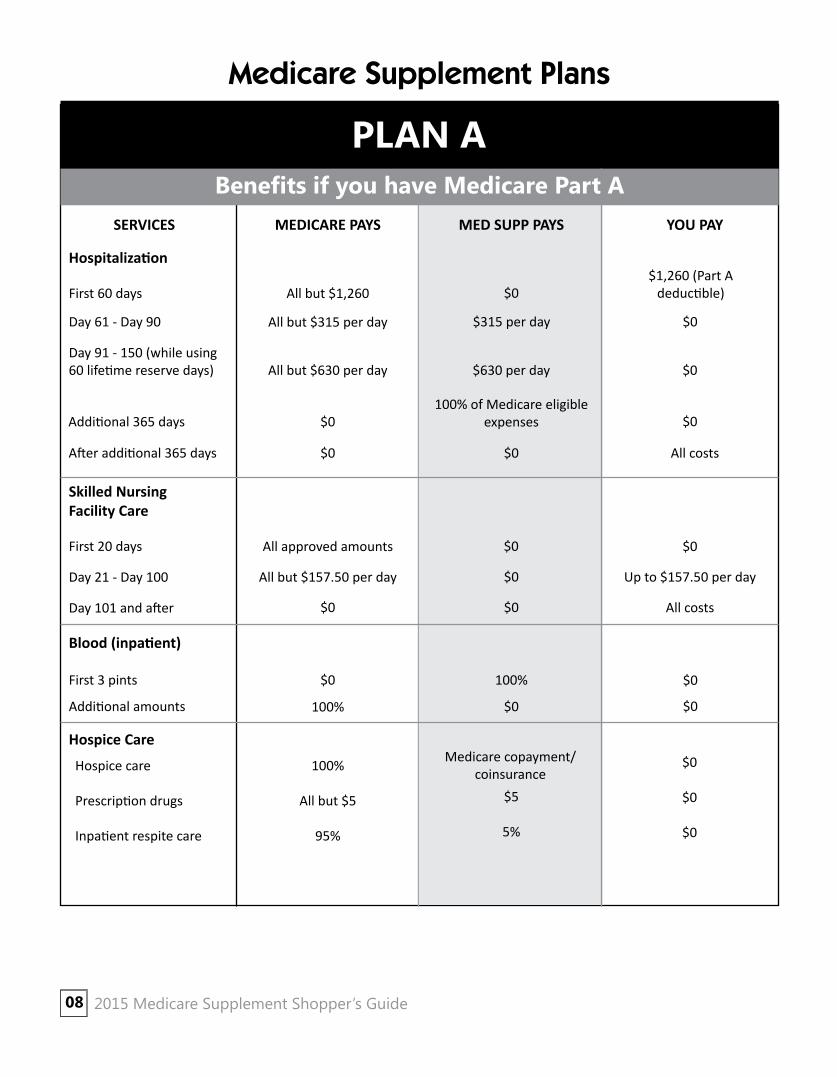

PLAN A

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Hospitalization

First 60 days All but $1,260 $0$1,260 (Part A

deductible)

Day 61 - Day 90 All but $315 per day $315 per day $0

Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Skilled Nursing Facility Care

First 20 days All approved amounts $0 $0

Day 21 - Day 100 All but $157.50 per day $0 Up to $157.50 per day

Day 101 and after $0 $0 All costs

Blood (inpatient)

First 3 pints $0 100% $0

Additional amounts 100% $0 $0

Hospice Care

100%

All but $5

95%

Medicare copayment/coinsurance

$0

$0

$0

Medicare Supplement Plans

2015 Medicare Supplement Shopper’s Guide08

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

Benefits if you have Medicare Part A

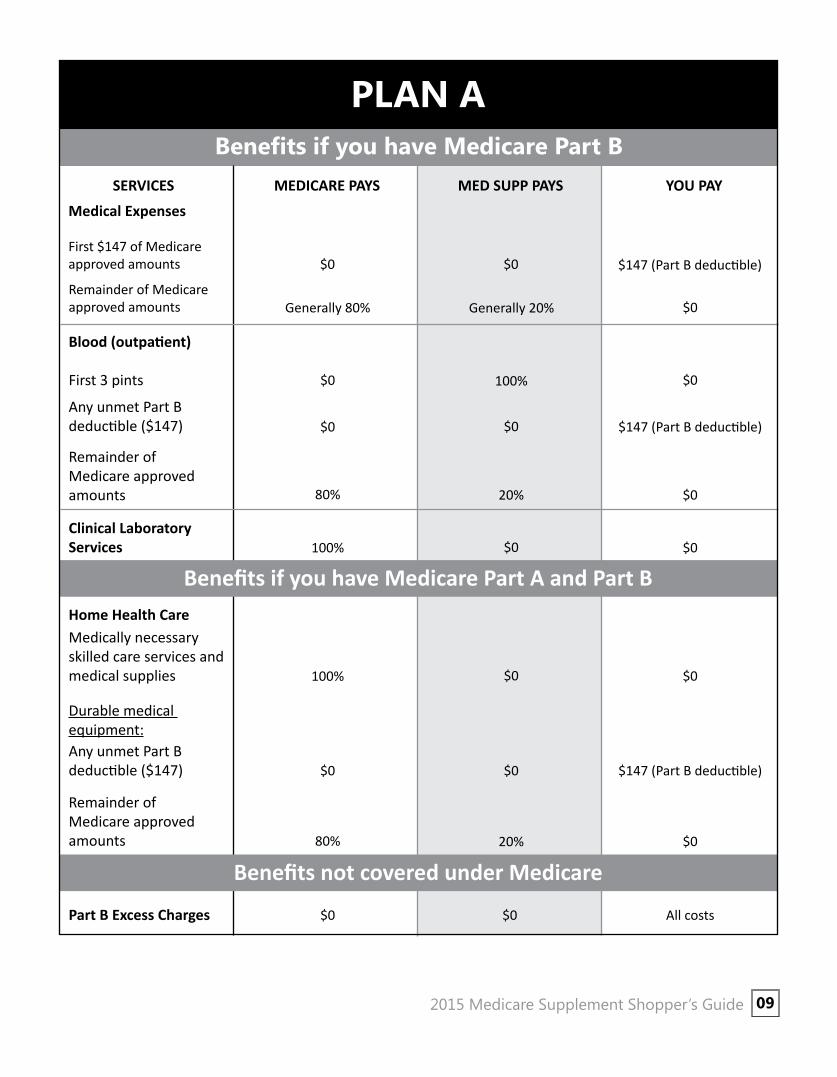

PLAN ABenefits if you have Medicare Part B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Remainder of Medicare approved amounts Generally 80% Generally 20% $0

Part B Excess Charges $0 All costs$0

Blood (outpatient)

First 3 pints $0 100% $0

Any unmet Part B deductible ($147) $0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Clinical Laboratory Services 100% $0 $0

Home Health CareMedically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Benefits not covered under Medicare

2015 Medicare Supplement Shopper’s Guide 09

Medical Expenses

First $147 of Medicare approved amounts $0 $0 $147 (Part B deductible)

Benefits if you have Medicare Part A and Part B

PLAN B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Hospitalization

First 60 days All but $1,260 $1,260 (Part A deductible) $0

Day 61 - Day 90 All but $315 per day $315 per day $0

Skilled Nursing Facility Care

First 20 days All approved amounts $0 $0

Day 101 and after $0

Blood (inpatient)

First 3 pints

Additional amounts 100% $0 $0

$0 100% $0

Day 91 - 150 (while using 60 lifetime reserve days)

Additional 365 days

After additional 365 days $0 $0 All costs

$0100% of Medicare eligible

expenses $0

All but $630 per day $630 per day $0

Hospice Care

100%

All but $5

95%

Medicare copayment/coinsurance $0

$0

$0

$0 All costs

Day 21 - Day 100 All but $157.50 per day $0 Up to $157.50 per day

2015 Medicare Supplement Shopper’s Guide10

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

Benefits if you have Medicare Part A

PLAN B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Part B Excess Charges $0 All costs$0

Blood (outpatient)

First 3 pints $0 100% $0

Any unmet Part Bdeductible ($147) $0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Clinical Laboratory Services 100% $0 $0

Home Health Care

Medically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

2015 Medicare Supplement Shopper’s Guide 11

Remainder of Medicare approved amounts Generally 80% Generally 20% $0

Medical Expenses

First $147 of Medicare approved amounts $0 $0 $147 (Part B deductible)

Benefits if you have Medicare Part B

Benefits if you have Medicare Part A and Part B

Benefits not covered under Medicare

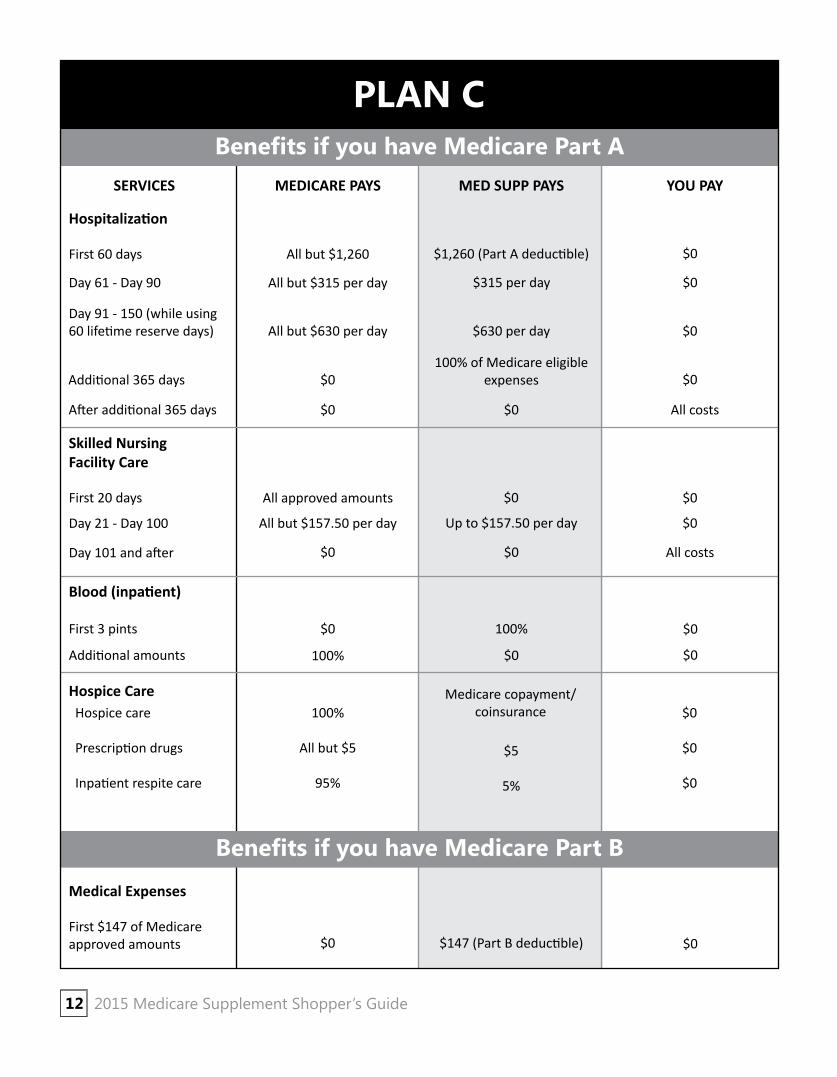

PLAN C

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Hospitalization

First 60 days

Day 61 - Day 90

Day 91 - 150 (while using 60 lifetime reserve days)

Additional 365 days

After additional 365 days $0

Skilled Nursing Facility Care

First 20 days

Day 21 - Day 100

Day 101 and after $0

Blood (inpatient)

First 3 pints

Additional amounts 100% $0 $0

$0 100% $0

Hospice Care

Medical Expenses

First $147 of Medicare approved amounts $0 $147 (Part B deductible) $0

100%

All but $5

95%

Medicare copayment/coinsurance $0

$0

$0

$0 All costs

All but $157.50 per day Up to $157.50 per day $0

All approved amounts $0 $0

$0 All costs

$0100% of Medicare eligible

expenses $0

All but $630 per day $630 per day $0

All but $315 per day $315 per day $0

All but $1,260 $1,260 (Part A deductible) $0

2015 Medicare Supplement Shopper’s Guide12

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

Benefits if you have Medicare Part A

Benefits if you have Medicare Part B

PLAN CBenefits if you have Medicare Part B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Benefits if you have Medicare Part A and Part B

Part B Excess Charges $0 All costs$0

Blood (outpatient)First 3 pints $0 100% $0

Any unmet Part Bdeductible ($147) $0 $147 (Part B deductible) $0Remainder of Medicare approved amounts 80% 20% $0

Clinical Laboratory Services 100% $0 $0

Home Health CareMedically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $147 (Part B deductible) $0

Remainder of Medicare approved amounts 80% 20% $0

Foreign TravelFirst $250 per calendar year $0 $0 $250

Remainder of charges $0 80% to a lifetime maximum benefit of $50,000

20% and amounts over the $50,000 lifetime

maximum

Benefits not covered under Medicare

2015 Medicare Supplement Shopper’s Guide 13

Medical ExpensesRemainder of Medicare approved amounts Generally 80% Generally 20% $0

PLAN DBenefits if you have Medicare Part A

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Hospitalization

First 60 days All but $1,260 $1,260 (Part A deductible) $0

Day 61 - Day 90 All but $315 per day $315 per day $0

Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Skilled Nursing Facility Care

First 20 days All approved amounts $0 $0

Day 21 - Day 100 All but $157.50 per day Up to $157.50 per day $0

Day 101 and after $0 $0 All costs

Blood (inpatient)

First 3 pints $0 100% $0

Additional amounts 100% $0 $0

Hospice Care

100%

All but $5

95%

Medicare copayment/coinsurance $0

$0

$0

Benefits if you have Medicare Part BMedical Expenses

First $147 of Medicare approved amounts $0 $0 $147 (Part B deductible)

2015 Medicare Supplement Shopper’s Guide14

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

PLAN DBenefits if you have Medicare Part B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Benefits if you have Medicare Part A and Part B

Part B Excess Charges $0 All costs$0

Blood (outpatient)First 3 pints $0 100% $0

Any unmet Part Bdeductible ($147) $0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Clinical Laboratory Services 100% $0 $0

Home Health CareMedically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Foreign TravelFirst $250 per calendar year $0 $0 $250

Remainder of charges $0 80% to a lifetime maximum benefit of $50,000

20% and amounts over the $50,000 lifetime

maximum

Benefits not covered under Medicare

2015 Medicare Supplement Shopper’s Guide 15

Medical ExpensesRemainder of Medicare approved amounts Generally 80% Generally 20% $0

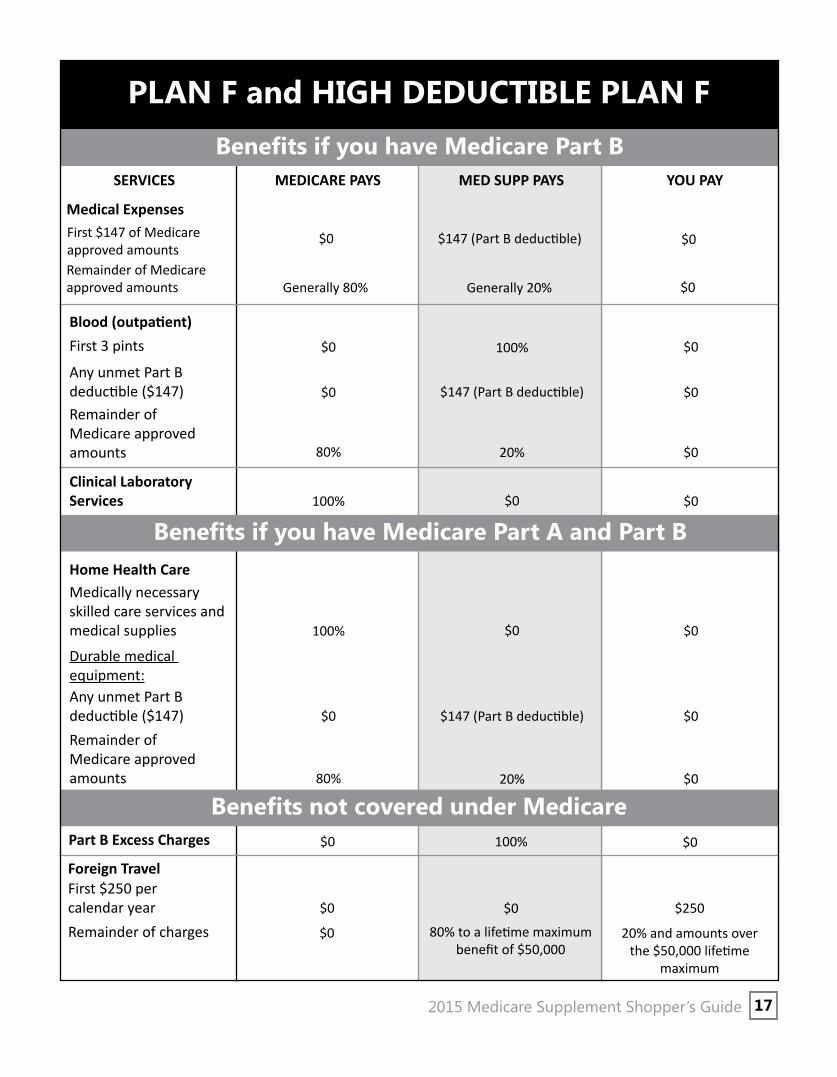

PLAN F and HIGH DEDUCTIBLE PLAN F

Benefits if you have Medicare Part ASERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Hospitalization

First 60 days All but $1,260 $1,260 (Part A deductible) $0

Day 61 - Day 90 All but $315 per day $315 per day $0

Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Skilled Nursing Facility Care

First 20 days All approved amounts $0 $0

Day 21 - Day 100 All but $157.50 per day Up to $157.50 per day $0

Day 101 and after $0 $0 All costs

Additional amounts 100% $0 $0

Hospice Care

100%

All but $5

95%

Medicare copayment/coinsurance $0

$0

$0

The high deductible Plan F pays the same benefits as Plan F after one has paid a calendar year $2,140 deduct-ible. Benefits from the high deductible Plan F will not begin until out-of-pocket expenses are $2,140. Out-of-pocket expenses for this deductible are expenses that would ordinarily be paid by the policy. This includes the Medicare deductibles for Part A and Part B, but does not include the plan’s separate foreign travel emergency deductible.

First 3 pints $0 100% $0Blood (inpatient)

2015 Medicare Supplement Shopper’s Guide16

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

PLAN F and HIGH DEDUCTIBLE PLAN F

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Benefits if you have Medicare Part A and Part B

Part B Excess Charges $0 $0100%

Blood (outpatient)First 3 pints $0 100% $0

Any unmet Part Bdeductible ($147) $0 $147 (Part B deductible) $0Remainder of Medicare approved amounts 80% 20% $0

Clinical Laboratory Services 100% $0 $0

Home Health CareMedically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $147 (Part B deductible) $0

Remainder of Medicare approved amounts 80% 20% $0

Foreign TravelFirst $250 per calendar year $0 $0 $250

Remainder of charges $0 80% to a lifetime maximum benefit of $50,000

20% and amounts over the $50,000 lifetime

maximum

Benefits not covered under Medicare

Benefits if you have Medicare Part B

2015 Medicare Supplement Shopper’s Guide 17

Remainder of Medicare approved amounts Generally 80% Generally 20% $0

First $147 of Medicare approved amounts

$0 $147 (Part B deductible) $0

Medical Expenses

PLAN GBenefits if you have Medicare Part A

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Hospitalization

First 60 days All but $1,260 $1,260 (Part A deductible) $0

Day 61 - Day 90 All but $315 per day $315 per day $0

Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Skilled Nursing Facility Care

First 20 days All approved amounts $0 $0

Day 21 - Day 100 All but $157.50 per day Up to $157.50 per day $0

Day 101 and after $0 $0 All costs

Blood (inpatient)

First 3 pints $0 100% $0

Additional amounts 100% $0 $0

Hospice Care

100%

All but $5

95%

Medicare copayment/coinsurance $0

$0

$0

Benefits if you have Medicare Part BMedical Expenses

First $147 of Medicareapproved amounts $0 $0 $147 (Part B deductible)

2015 Medicare Supplement Shopper’s Guide18

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

PLAN GBenefits if you have Medicare Part B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Benefits if you have Medicare Part A and Part B

Part B Excess Charges $0 $0100%

Blood (outpatient)First 3 pints $0 100% $0

Any unmet Part Bdeductible ($147) $0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Clinical Laboratory Services 100% $0 $0

Home Health Care

Medically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Foreign Travel

First $250 per calendar year $0 $0 $250

Remainder of charges $0 80% to a lifetime maximum benefit of $50,000

20% and amounts over the $50,000 lifetime

maximum

Benefits not covered under Medicare

2015 Medicare Supplement Shopper’s Guide 19

Medical Expenses Remainder of Medicare approved amounts Generally 80% Generally 20% $0

PLAN K

Benefits if you have Medicare Part ASERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Day 61 - Day 90 All but $315 per day $315 per day $0Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Skilled Nursing Facility Care

First 20 days All approved amounts $0 $0

Day 21 - Day 100 All but $157.50 per dayUp to $78.75 per day (50%

of Part A coinsurance)Up to $78.75 per day (50%

of Part A coinsurance)•

Day 101 and after $0 $0 All costs

First 3 pints $0 50% 50%•

Additional amounts 100% $0 $0

You will pay half the cost-sharing of some covered services until you reach the annual out-of-pocket limit of $4,940 each calendar year. The amounts that count toward your annual limit are noted with circles (•) in the chart. Once you reach the annual limit, the plan pays 100% of your Medicare copayment and coinsurance for the rest of the calen-dar year. However, this limit does NOT include charges from your provider that exceed Medicare-approved amounts (these are called “Excess Charges”) and you will be responsible for paying this difference in the amount charged by your provider and the amount paid by Medicare for the item or service. Once you have been billed $147 of Medicare-approved amounts for covered services, your Part B deductible will have been met for the calendar year.

Hospitalization

First 60 days All but $1,260$630 (50% of Part A

deductible)$630 (50% of Part A

deductible)•

Blood (inpatient)

2015 Medicare Supplement Shopper’s Guide20

Hospice Care

100%

All but $5

95%

50% of copayment/coinsurance

50% of Medicare copayment/coinsurance•

Hospice care

Prescription drugs

Inpatient respite care

PLAN KBenefits if you have Medicare Part B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Remainder of Medicare approved amounts Generally 80% Generally 10% Generally 10%•

Remainder of Medicare approved amounts Generally 80% Generally 10% Generally 10%•

Any unmet Part Bdeductible ($147) $0 $0 $147 (Part B deductible)•

Clinical Laboratory Services 100% $0 $0

Home Health Care

Medically necessary skilled care services and medical supplies 100% $0 $0

Benefits if you have Medicare Part A and Part B

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible)•

Remainder of Medicare approved amounts 80% 10% 10%•

Medical Expenses

Part B Excess Charges $0 All costs (and they do not count toward annual out-of-pocket limit of $4,940)

$0

Benefits not covered under Medicare

First 3 pints $0 50% 50%•

Blood (outpatient)

2015 Medicare Supplement Shopper’s Guide 21

First $147 of Medicare approved amounts

$0 $0 $147 (Part B deductible)•

PLAN L

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Day 61 - Day 90 All but $315 per day $315 per day $0

Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Skilled Nursing Facility Care

Day 21 - Day 100 All but $157.50 per dayUp to $118.13 per day (75%

of Part A coinsurance)Up to $39.37 per day (25% of Part A coinsurance) n

Day 101 and after $0 $0 All costs

Additional amounts 100% $0 $0

Hospice Care

100%

All but $5

95%

75% of copayment/coinsurance

25% of Medicare copyament/

coinsurance n

You will pay one-fourth of the cost-sharing of some covered services until you reach the annual out-of-pocket limit of $2,470 each calendar year. The amounts that count toward your annual limit are noted with a square (n) in the chart. Once you reach the annual limit, the plan pays 100% of your Medicare copayment and coinsurance for the rest of the calendar year. However, this limit does NOT include charges from your provider that exceed Medicare-approved amounts (these are called “Excess Charges”) and you will be responsible for paying this difference in the amount charged by your provider and the amount paid by Medicare for the item or service. Once you have been billed $147 of Medicare-approved amounts for covered services, your Part B deductible will have been met for the calendar year.

First 60 days All but $1,260$945 (75% of Part A

deductible)$315 (25% of Part A

deductible) n

Hospitalization

All approved amounts $0 $0First 20 days

First 3 pints $0 75% 25% n

Blood (inpatient)

2015 Medicare Supplement Shopper’s Guide22

Hospice care

Prescription drugs

Inpatient respite care

Benefits if you have Medicare Part A

PLAN LBenefits if you have Medicare Part B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Remainder of Medicare approved amounts Generally 80% Generally 15% Generally 5% n

Remainder of Medicare Approved Amounts Generally 80% Generally 15% Generally 5% n

Any unmet Part Bdeductible ($147) $0 $0

$147 (Part B deductible) n

Clinical Laboratory Services 100% $0 $0

Medical Expenses

First 3 pints $0 75% 25% nBlood (outpatient)

Benefits if you have Medicare Part A and Part BHome Health Care

Medically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible) n

Remainder of Medicare approved amounts 80% 15% 5% n

Part B Excess Charges $0 All costs (and they do not count toward annual out-of-pocket limit of $2,470)

$0

Benefits not covered under Medicare

2015 Medicare Supplement Shopper’s Guide 23

First $147 of Medicare approved amounts $0 $0

$147 (Part B deductible) n

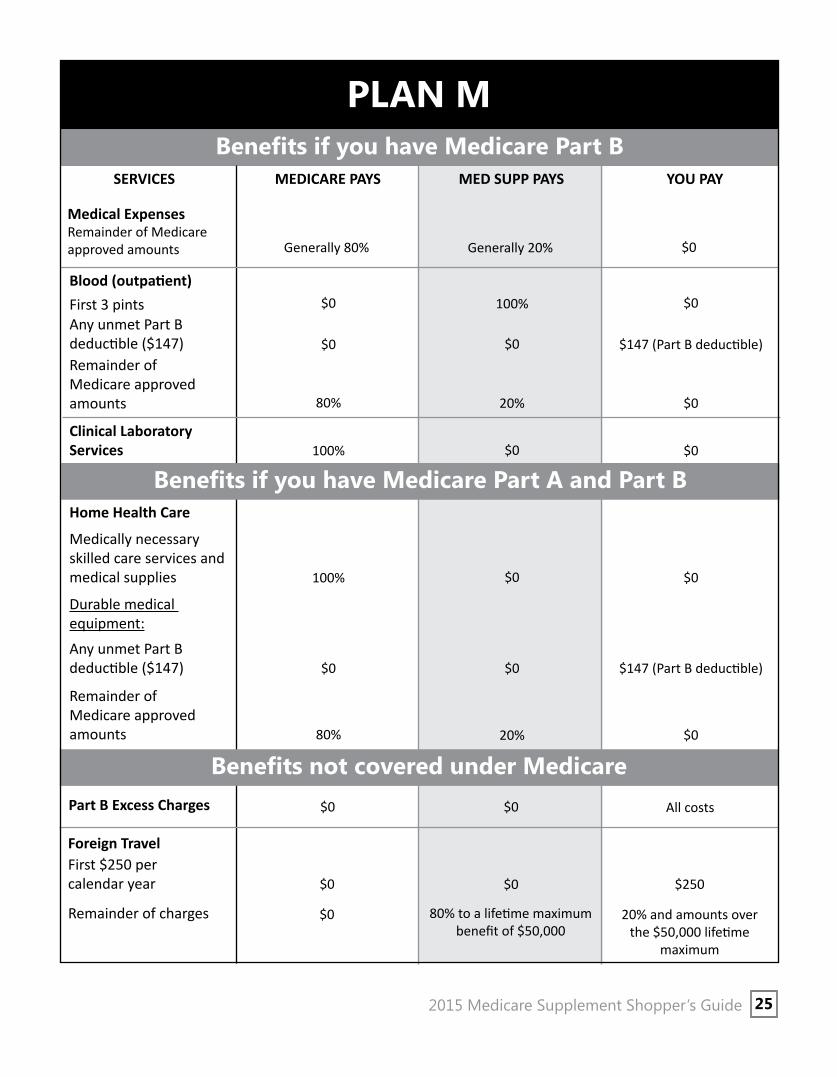

PLAN MBenefits if you have Medicare Part A

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Hospitalization

First 60 days All but $1,260$630 (50% of Part A

deductible)$630 (50% of Part A

deductible)

Day 61 - Day 90 All but $315 per day $315 per day $0

Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Skilled Nursing Facility Care

First 20 days All approved amounts $0 $0

Day 21 - Day 100 All but $157.50 per day Up to $157.50 per day $0

Day 101 and after $0 $0 All costs

Blood (inpatient)

First 3 pints $0 100% $0

Additional amounts 100% $0 $0

Hospice Care

100%

All but $5

95%

Medicare copayment/coinsurance $0

$0

$0

Benefits if you have Medicare Part BMedical Expenses

First $147 of Medicare approved amounts $0 $0 $147 (Part B deductible)

2015 Medicare Supplement Shopper’s Guide24

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

PLAN MBenefits if you have Medicare Part B

Benefits if you have Medicare Part A and Part B

Part B Excess Charges $0 All costs$0

Blood (outpatient)First 3 pints $0 100% $0Any unmet Part Bdeductible ($147) $0 $0 $147 (Part B deductible)Remainder of Medicare approved amounts 80% 20% $0

Clinical Laboratory Services 100% $0 $0

Home Health Care

Medically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Foreign TravelFirst $250 per calendar year $0 $0 $250

Remainder of charges $0 80% to a lifetime maximum benefit of $50,000

20% and amounts over the $50,000 lifetime

maximum

Benefits not covered under Medicare

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

2015 Medicare Supplement Shopper’s Guide 25

Medical ExpensesRemainder of Medicare approved amounts Generally 80% Generally 20% $0

PLAN NBenefits if you have Medicare Part A

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Day 61 - Day 90 All but $315 per day $315 per day $0

Day 91 - 150 (while using 60 lifetime reserve days) All but $630 per day $630 per day $0

Additional 365 days $0100% of Medicare eligible

expenses $0

After additional 365 days $0 $0 All costs

Day 21 - Day 100 All but $157.50 per day Up to $157.50 per day $0

Day 101 and after $0 $0 All costs

Additional amounts 100% $0 $0

Hospice Care

100%

All but $5

95%

Medicare copayment/coinsurance $0

$0

$0

Benefits if you have Medicare Part B

First 60 days All but $1,260 $1,260 (Part A deductible) $0

Hospitalization

First 20 days All approved amounts $0 $0

Skilled Nursing Facility Care

Blood (inpatient)$0 100% $0First 3 pints

2015 Medicare Supplement Shopper’s Guide26

Hospice care

Prescription drugs

Inpatient respite care

$5

5%

Any unmet Part Bdeductible ($147) $0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Blood (outpatient)$0 100% $0First 3 pints

PLAN NBenefits if you have Medicare Part B

SERVICES MEDICARE PAYS MED SUPP PAYS YOU PAY

Benefits if you have Medicare Part A and Part BHome Health Care

Medically necessary skilled care services and medical supplies 100% $0 $0

Any unmet Part Bdeductible ($147)

Durable medical equipment:

$0 $0 $147 (Part B deductible)

Remainder of Medicare approved amounts 80% 20% $0

Part B Excess Charges $0 All costs$0

Foreign Travel

First $250 per calendar year $0 $0 $250

Remainder of charges $080% to a lifetime maximum

benefit of $50,00020% and amounts over the $50,000 lifetime maximum

Other benefits not covered under Medicare

2015 Medicare Supplement Shopper’s Guide 27

Remainder of Medicare approved amounts

Generally 80% Generally 20% of the balance, other than up to $20 per office visit and up to $50 per emer-gency room visit. The copay-ment of up to $50 is waived if the insured is admitted to any hospital and the emergency visit is covered as a Medicare Part A expense.

Up to $20 per office visit and up to $50 per emergency room visit. The copayment of up to $50 is waived if the insured is admitted to any hospital and the emergency visit is covered as a Medicare Part A expense.

Medical Expenses

$0 $0 $147 (Part B deductible)First $147 of Medicare approved amounts

Clinical Laboratory Services 100% $0 $0

If an

X a

ppea

rs in

the

char

t, th

e M

edic

are

supp

lem

ent p

olic

y co

vers

100

% o

f the

des

crib

ed b

enefi

t. If

a ro

w li

sts

a pe

rcen

tage

, the

pol

icy

cove

rs th

at p

erce

ntag

e of

the

desc

ribed

ben

efit.

If a

row

is b

lank

, the

pol

icy

does

n’t c

over

that

ben

efit.

NO

TE: T

he M

edic

are

supp

lem

ent

polic

y co

vers

coi

nsur

ance

onl

y af

ter y

ou h

ave

paid

the

dedu

ctib

le (u

nles

s th

e su

pple

men

t pol

icy

also

cov

ers

the

dedu

ctib

le).

*Pla

n F

also

offe

rs a

hig

h-de

duct

ible

pla

n. If

you

cho

ose

this

opt

ion,

this

mea

ns y

ou m

ust p

ay fo

r Med

icar

e-co

vere

d co

sts

up to

the

dedu

ctib

le a

mou

nt o

f $2,

180

in 2

015

befo

re y

our M

edic

are

supp

lem

ent p

lan

pays

an

ythi

ng.

**Af

ter y

ou m

eet y

our o

ut-o

f-po

cket

yea

rly li

mit

and

your

yea

rly P

art B

ded

uctib

le ($

147

in 2

015)

, the

Med

i-ca

re s

uppl

emen

t pla

n pa

ys 1

00%

of c

over

ed s

ervi

ces

for t

he re

st o

f the

cal

enda

r yea

r.**

*Pla

n N

pay

s 10

0% o

f the

Par

t B c

oins

uran

ce, e

xcep

t for

a c

opay

men

t of u

p to

$20

for s

ome

offic

e vi

sits

an

d up

to a

$50

cop

aym

ent f

or e

mer

genc

y ro

om v

isits

that

don

’t re

sult

in a

n in

patie

nt a

dmis

sion

.

Med

icar

e su

pp

lem

ent

insu

ranc

e at

a g

lanc

e

Bene

fits

AB

CD

F*G

KL

MN

Part

A c

oins

uran

ce a

nd h

os-

pita

l cos

ts u

p to

an

addi

tiona

l 36

5 da

ys a

fter

Med

icar

e be

n-efi

ts a

re u

sed

upX X X X

X X X X X

X X X X X X X

X X X X X X X

X X X X X X X

X X X X X X X

X 50%

50%

50%

50%

50%

X 75%

75%

75%

75%

75%

X X X X X 50% X

X X*** X X X X X

Out

-of-

Pock

et

Lim

it**

$4,9

40$2

,470

Part

B c

oins

uran

ce o

r co

paym

ent

Bloo

d (fi

rst 3

pin

ts)

Part

A H

ospi

ce c

are

coin

sura

nce

or c

opay

men

t

Skill

ed N

ursi

ng F

acili

ty C

are

coin

sura

nce

Med

icar

e Pa

rt A

ded

uctib

le

Part

B d

educ

tible

Part

B e

xces

s ch

arge

s

Fore

ign

Trav

el E

mer

genc

y ca

re

(up

to p

lan

limits

)

XX

XX

2015 Medicare Supplement Shopper’s Guide28

Plan AIssue age policies - annual premium

Section II: Medicare Supplement and Medicare SELECT Insurance Rates

A note about these ratesPremium quotes listed here are for a nonsmoking man living in the 66612 ZIP code and are broken into four age categories. Premiums may vary according to your age or the area in which you live. Additionally, these rates may have changed since March 2015, when these rates were compiled. An-nual costs may be higher if premiums are paid in installments. Contact the insurance company to find out exact premiums.

DisclaimerThis shopper’s guide does not recommend or endorse any insurance company or policy. It is de-signed to help you comparison shop for coverage to supplement your Medicare benefits. Contact the Kansas Insurance Department’s Consumer Assistance Hotline if you have any questions about how to use this guide: 800-432-2484.

2015 Medicare Supplement Shopper’s Guide 29

Company Age 65 Age 70 Age 75 Age 80Bankers Fidelity Life Insurance Company $1,344 $1,500 $1,680 $1,812 Everence Association Inc. $1,575 $1,703 $1,786 $1,894

Old Surety Life Insurance Company $1,114 $1,376 $1,620 $1,822 Transamerica Life Insurance Company $1,169 $1,495 $1,862 $2,207

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

Aetna Health and Life Insurance Company $1,312 $1,414 $1,563 $1,669Aetna Life Insurance Company $1,521 $1,816 $2,093 $2,262 American Continental Insurance Company $1,544 $1,750 $2,045 $2,252

American Family Life Assurance Co. of Columbus $1,738 $2,058 $2,276 $2,389 American Republic Corp Insurance Company $1,896 $2,124 $2,531 $2,844 American Republic Insurance Company $1,424 $1,485 $1,800 $2,109American Retirement Life Insurance Company $1,403 $1,650 $1,898 $2,133Blue Cross & Blue Shield of Kansas City $1,356 $1,860 $2,256 $2,688 Blue Cross and Blue Shield of Kansas, Inc. $1,286 $1,501 $1,752 $2,047 Central States Indemnity Company of Omaha $1,277 $1,449 $1,721 $1,956 Christian Fidelity Life Insurance Company $1,392 $1,648 $1,959 $2,135 Colonial Penn Life Insurance Company $1,892 $2,311 $2,813 $3,288 Combined Insurance Company of America $1,470 $1,736 $1,922 $2,037

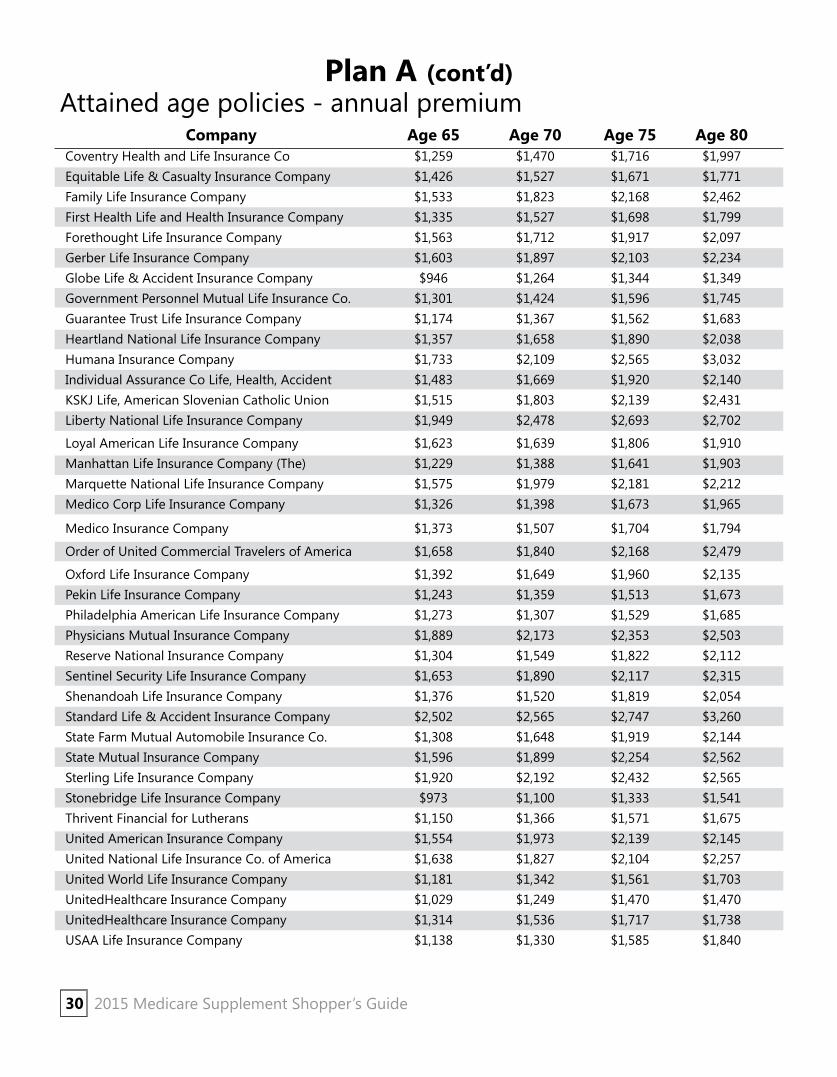

Attained age policies - annual premiumPlan A (cont’d)

2015 Medicare Supplement Shopper’s Guide30

Company Age 65 Age 70 Age 75 Age 80Coventry Health and Life Insurance Co $1,259 $1,470 $1,716 $1,997Equitable Life & Casualty Insurance Company $1,426 $1,527 $1,671 $1,771Family Life Insurance Company $1,533 $1,823 $2,168 $2,462 First Health Life and Health Insurance Company $1,335 $1,527 $1,698 $1,799Forethought Life Insurance Company $1,563 $1,712 $1,917 $2,097Gerber Life Insurance Company $1,603 $1,897 $2,103 $2,234Globe Life & Accident Insurance Company $946 $1,264 $1,344 $1,349Government Personnel Mutual Life Insurance Co. $1,301 $1,424 $1,596 $1,745Guarantee Trust Life Insurance Company $1,174 $1,367 $1,562 $1,683Heartland National Life Insurance Company $1,357 $1,658 $1,890 $2,038Humana Insurance Company $1,733 $2,109 $2,565 $3,032Individual Assurance Co Life, Health, Accident $1,483 $1,669 $1,920 $2,140KSKJ Life, American Slovenian Catholic Union $1,515 $1,803 $2,139 $2,431Liberty National Life Insurance Company $1,949 $2,478 $2,693 $2,702

Loyal American Life Insurance Company $1,623 $1,639 $1,806 $1,910Manhattan Life Insurance Company (The) $1,229 $1,388 $1,641 $1,903Marquette National Life Insurance Company $1,575 $1,979 $2,181 $2,212Medico Corp Life Insurance Company $1,326 $1,398 $1,673 $1,965

Medico Insurance Company $1,373 $1,507 $1,704 $1,794

Order of United Commercial Travelers of America $1,658 $1,840 $2,168 $2,479

Oxford Life Insurance Company $1,392 $1,649 $1,960 $2,135Pekin Life Insurance Company $1,243 $1,359 $1,513 $1,673Philadelphia American Life Insurance Company $1,273 $1,307 $1,529 $1,685Physicians Mutual Insurance Company $1,889 $2,173 $2,353 $2,503Reserve National Insurance Company $1,304 $1,549 $1,822 $2,112Sentinel Security Life Insurance Company $1,653 $1,890 $2,117 $2,315Shenandoah Life Insurance Company $1,376 $1,520 $1,819 $2,054Standard Life & Accident Insurance Company $2,502 $2,565 $2,747 $3,260State Farm Mutual Automobile Insurance Co. $1,308 $1,648 $1,919 $2,144State Mutual Insurance Company $1,596 $1,899 $2,254 $2,562Sterling Life Insurance Company $1,920 $2,192 $2,432 $2,565Stonebridge Life Insurance Company $973 $1,100 $1,333 $1,541Thrivent Financial for Lutherans $1,150 $1,366 $1,571 $1,675United American Insurance Company $1,554 $1,973 $2,139 $2,145United National Life Insurance Co. of America $1,638 $1,827 $2,104 $2,257United World Life Insurance Company $1,181 $1,342 $1,561 $1,703UnitedHealthcare Insurance Company $1,029 $1,249 $1,470 $1,470UnitedHealthcare Insurance Company $1,314 $1,536 $1,717 $1,738USAA Life Insurance Company $1,138 $1,330 $1,585 $1,840

2015 Medicare Supplement Shopper’s Guide 31

Plan BIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Transamerica Life Insurance Company $1,544 $1,974 $2,458 $2,914

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

Aetna Health and Life Insurance Company $1,485 $1,617 $1,827 $2,024Aetna Life Insurance Company $1,684 $2,065 $2,455 $2,790American Continental Insurance Company $1,948 $2,206 $2,575 $2,835Central States Indemnity Company of Omaha $1,491 $1,692 $2,009 $2,284Colonial Penn Life Insurance Company $1,994 $2,427 $2,937 $3,435Family Life Insurance Company $1,865 $2,220 $2,634 $2,993First Health Life and Health Insurance Company $1,522 $1,775 $2,022 $2,226Globe Life & Accident Insurance Company $1,445 $1,794 $2,075 $2,098Humana Insurance Company $1,886 $2,295 $2,792 $3,300KSKJ Life, American Slovenian Catholic Union $1,843 $2,192 $2,602 $2,957

Liberty National Life Insurance Company $2,709 $3,498 $3,907 $3,972Order of United Commercial Travelers of America $1,934 $2,147 $2,531 $2,893Sentinel Security Life Insurance Company $1,829 $2,093 $2,372 $2,636

Standard Life & Accident Insurance Company $2,849 $2,920 $3,128 $3,711

State Mutual Insurance Company $1,863 $2,214 $3,953 $2,989Sterling Life Insurance Company $2,241 $2,617 $2,980 $3,240Thrivent Financial for Lutherans $1,289 $1,548 $1,826 $2,026

United American Insurance Company $2,500 $3,225 $3,590 $3,643

United World Life Insurance Company $1,858 $2,112 $2,457 $2,680

UnitedHealthcare Insurance Company $1,483 $1,800 $2,118 $2,118

Plan CIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Transamerica Life Insurance Company $1,827 $2,336 $2,908 $3,447

Attained age policies - annual premium Company Age 65 Age 70 Age 75 Age 80

American Family Life Assurance Co of Columbus $2,097 $2,528 $2,909 $3,271Blue Cross & Blue Shield of Kansas City $2,016 $2,772 $3,372 $4,008Blue Cross and Blue Shield of Kansas, Inc. $1,667 $1,963 $2,371 $2,911Central States Indemnity Company of Omaha $1,784 $2,027 $2,438 $2,771Coventry Health and Life Insurance Co. $2,032 $2,391 $2,889 $3,616

2015 Medicare Supplement Shopper’s Guide32

Plan C (cont’d)

Company Age 65 Age 70 Age 75 Age 80Everence Association, Inc. $2,315 $2,739 $3,079 $3,325Family Life Insurance Company $2,139 $2,552 $3,071 $3,492Forethought Life Insurance Company $2,060 $2,265 $2,579 $2,879

Government Personnel Mutual Life Ins. Co. $1,763 $1,939 $2,210 $2,469Guarantee Trust Life Insurance Company $1,689 $1,962 $2,264 $2,515Humana Insurance Company $2,216 $2,696 $3,281 $3,877KSKJ Life, American Slovenian Catholic Union $2,093 $2,497 $3,005 $3,415

Manhattan Life Insurance Company (The) $1,648 $1,861 $2,201 $2,552

Order of United Commercial Travelers of America $2,314 $2,572 $3,072 $3,511

Reserve National Insurance Company $1,937 $2,301 $2,706 $3,136

Sentinel Security Life Insurance Company $2,242 $2,573 $2,933 $3,280Standard Life & Accident Insurance Company $3,239 $3,320 $3,556 $4,220

State Farm Mutual Automobile Insurance Co. $1,972 $2,485 $2,879 $3,234

State Mutual Insurance Company $2,230 $2,653 $3,191 $3,629

Sterling Life Insurance Company $2,571 $2,979 $3,379 $3,671

Thrivent Financial for Lutherans $1,523 $1,805 $2,143 $2,512

United American Insurance Company $2,796 $3,635 $4,156 $4,522

United World Life Insurance Company $2,210 $2,512 $2,922 $3,187

UnitedHealthcare Insurance Company $1,793 $2,178 $2,562 $2,562

Plan DIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Transamerica Life Insurance Company $1,689 $2,159 $2,689 $3,187

Attained age policies - annual premium

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

American Family Life Assurance Co of Columbus $1,889 $2,278 $2,635 $2,982Family Life Insurance Company $1,958 $2,328 $2,763 $3,141Heartland National Life Insurance Company $1,707 $2,121 $2,486 $2,793KSKJ Life, American Slovenian Catholic Union $1,711 $2,034 $2,416 $2,747Marquette National Life Insurance Company $1,771 $2,268 $2,671 $2,996Order of United Commercial Travelers of America $2,027 $2,251 $2,653 $3,034Sentinel Security Life Insurance Company $1,693 $1,944 $2,221 $2,491Standard Life & Accident Insurance Company $1,952 $2,001 $2,143 $2,543State Mutual Insurance Company $1,953 $2,322 $2,756 $3,133

2015 Medicare Supplement Shopper’s Guide 33

Plan D (cont’d)Attained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Thrivent Financial for Lutherans $1,311 $1,586 $1,917 $2,275

United American Insurance Company $2,602 $3,444 $3,966 $4,332

United National Life Insurance Co. of America $1,939 $2,191 $2,589 $2,882

United World Life Insurance Company $1,409 $1,602 $1,863 $2,032

Plan FIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Bankers Fidelity Life Insurance Company $1,872 $2,076 $2,316 $2,520Everence Association Inc. $2,671 $2,897 $3,071 $3,324Old Surety Life Insurance Company $1,611 $1,887 $2,100 $2,300Transamerica Life Insurance Company $1,837 $2,350 $2,992 $3,467

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

Aetna Health and Life Insurance Company $1,732 $1,892 $2,154 $2,412Aetna Life Insurance Company $1,950 $2,404 $2,880 $3,307American Continental Insurance Company $2,261 $2,537 $2,916 $3,153American Family Life Assurance Co. of Columbus $2,142 $2,589 $2,980 $3,355American Republic Corp Insurance Company $2,606 $2,919 $3,478 $3,909American Republic Insurance Company $2,034 $2,121 $2,571 $3,012American Retirement Life Insurance Company $1,730 $2,019 $2,352 $2,726Blue Cross & Blue Shield of Kansas City $2,028 $2,772 $3,384 $4,020

Blue Cross and Blue Shield of Kansas, Inc. $1,733 $2,040 $2,463 $3,025

Central States Indemnity Company of Omaha $1,850 $2,080 $2,490 $2,811

Christian Fidelity Life Insurance Company $1,567 $1,865 $2,175 $2,513Colonial Penn Life Insurance Company $2,329 $2,822 $3,425 $4,086Combined Insurance Company of America $1,712 $2,021 $2,447 $2,776Coventry Health and Life Insurance Company $2,057 $2,421 $2,923 $3,646Equitable Life & Casualty Insurance Company $1,902 $2,050 $2,253 $2,401Family Life Insurance Company $2,045 $2,402 $2,877 $3,248

Colonial Penn Life Insurance Company $2,469 $2,992 $3,631 $4,442Combined Insurance Company of America $1,764 $2,081 $2,521 $2,859Coventry Health and Life Insurance Company $2,201 $2,590 $3,128 $3,616Equitable Life & Casualty Insurance Company $2,131 $2,297 $2,524 $2,690Family Life Insurance Company $2,229 $2,619 $3,135 $3,541First Health Life and Health Insurance Company $1,775 $2,082 $2,389 $2,658

2015 Medicare Supplement Shopper’s Guide34

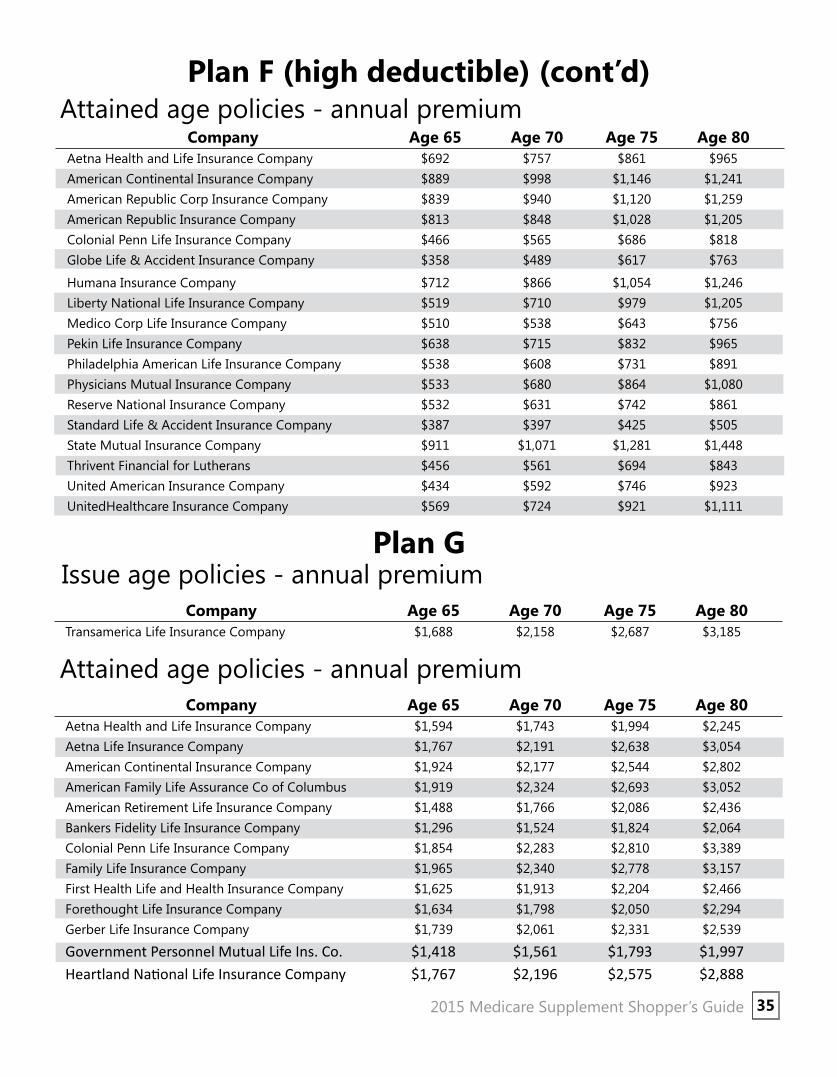

Plan F (cont’d)Attained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Forethought Life Insurance Company $2,110 $2,321 $2,642 $2,949Gerber Life Insurance Company $2,263 $2,682 $3,027 $3,286

Globe Life & Accident Insurance Company $1,697 $2,061 $2,422 $2,595

Government Personnel Mutual Life Ins. Co. $1,805 $1,986 $2,262 $2,529

Heartland National Life Insurance Company $1,994 $2,415 $2,792 $3,100Humana Insurance Company $2,261 $2,751 $3,348 $3,956Individual Assurance Co Life, Health, Accident $1,749 $1,956 $2,278 $2,621KSKJ Life, American Slovenian Catholic Union $2,181 $2,562 $3,068 $3,463Liberty National Life Insurance Company $2,820 $3,666 $4,201 $4,587Loyal American Life Insurance Company $1,996 $2,096 $2,368 $2,655Manhattan Life Insurance Company (The) $1,640 $1,854 $2,190 $2,540Marquette National Life Insurance Company $2,078 $2,597 $3,015 $3,355Medico Corp Life Insurance Company $1,700 $1,793 $2,145 $2,519Medico Insurance Company $1,860 $2,068 $2,432 $2,777Order of United Commercial Travelers of America $2,398 $2,640 $3,138 $3,564Oxford Life Insurance Company $1,568 $1,865 $2,176 $2,514Pekin Life Insurance Company $1,557 $1,740 $2,027 $2,349Philadelphia American Life Insurance Company $1,827 $1,944 $2,225 $2,435Physicians Mutual Insurance Company $2,858 $3,346 $4,011 $4,650Reserve National Insurance Company $1,691 $2,009 $2,362 $2,738Sentinel Security Life Insurance Company $2,097 $2,407 $2,743 $3,067Shenandoah Life Insurance Company $1,759 $1,943 $2,326 $2,626Standard Life & Accident Insurance Company $2,664 $2,730 $2,925 $3,470State Farm Mutual Automobile Insurance Co. $1,992 $2,510 $2,908 $3,267State Mutual Insurance Company $2,318 $2,724 $3,259 $3,681Sterling Life Insurance Company $2,453 $2,843 $3,224 $3,502Stonebridge Life Insurance Company $1,644 $1,858 $2,253 $2,604Thrivent Financial for Lutherans $1,531 $1,813 $2,154 $2,524United American Insurance Company $2,758 $3,578 $4,091 $4,449United National Life Insurance Co. of America $2,362 $2,642 $3,087 $3,410United World Life Insurance Company $2,268 $2,578 $2,999 $3,271UnitedHealthcare Insurance Company $1,804 $2,190 $2,577 $2,577UnitedHealthcare Insurance Company $1,767 $2,128 $2,561 $2,932USAA Life Insurance Company $1,734 $2,032 $2,424 $2,807

Plan F (high deductible)Issue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Bankers Fidelity Life Insurance Company $552 $624 $696 $756

2015 Medicare Supplement Shopper’s Guide 35

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

Aetna Health and Life Insurance Company $692 $757 $861 $965American Continental Insurance Company $889 $998 $1,146 $1,241American Republic Corp Insurance Company $839 $940 $1,120 $1,259American Republic Insurance Company $813 $848 $1,028 $1,205Colonial Penn Life Insurance Company $466 $565 $686 $818Globe Life & Accident Insurance Company $358 $489 $617 $763

Humana Insurance Company $712 $866 $1,054 $1,246Liberty National Life Insurance Company $519 $710 $979 $1,205Medico Corp Life Insurance Company $510 $538 $643 $756Pekin Life Insurance Company $638 $715 $832 $965Philadelphia American Life Insurance Company $538 $608 $731 $891Physicians Mutual Insurance Company $533 $680 $864 $1,080Reserve National Insurance Company $532 $631 $742 $861Standard Life & Accident Insurance Company $387 $397 $425 $505State Mutual Insurance Company $911 $1,071 $1,281 $1,448Thrivent Financial for Lutherans $456 $561 $694 $843United American Insurance Company $434 $592 $746 $923UnitedHealthcare Insurance Company $569 $724 $921 $1,111

Plan GIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Transamerica Life Insurance Company $1,688 $2,158 $2,687 $3,185

Plan F (high deductible) (cont’d)

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

Aetna Health and Life Insurance Company $1,594 $1,743 $1,994 $2,245Aetna Life Insurance Company $1,767 $2,191 $2,638 $3,054American Continental Insurance Company $1,924 $2,177 $2,544 $2,802American Family Life Assurance Co of Columbus $1,919 $2,324 $2,693 $3,052American Retirement Life Insurance Company $1,488 $1,766 $2,086 $2,436Bankers Fidelity Life Insurance Company $1,296 $1,524 $1,824 $2,064Colonial Penn Life Insurance Company $1,854 $2,283 $2,810 $3,389Family Life Insurance Company $1,965 $2,340 $2,778 $3,157First Health Life and Health Insurance Company $1,625 $1,913 $2,204 $2,466Forethought Life Insurance Company $1,634 $1,798 $2,050 $2,294Gerber Life Insurance Company $1,739 $2,061 $2,331 $2,539

Government Personnel Mutual Life Ins. Co. $1,418 $1,561 $1,793 $1,997Heartland National Life Insurance Company $1,767 $2,196 $2,575 $2,888

2015 Medicare Supplement Shopper’s Guide36

Plan G (cont’d)

Company Age 65 Age 70 Age 75 Age 80Individual Assurance Co Life, Health, Accident $1,429 $1,618 $1,911 $2,216KSKJ Life, American Slovenian Catholic Union $1,462 $1,739 $2,066 $2,347Loyal American Life Insurance Company $1,742 $1,855 $2,116 $2,393Manhattan Life Insurance Company (The) $1,358 $1,537 $1,817 $2,114Marquette National Life Insurance Co. $1,874 $2,399 $2,823 $3,169Medico Corp Life Insurance Company $1,582 $1,675 $2,029 $2,399Order of United Commercial Travelers of America $2,038 $2,263 $2,668 $3,050Pekin Life Insurance Company $1,357 $1,519 $1,776 $2,070Philadelphia American Life Insurance Co. $1,533 $1,692 $1,977 $2,194Physicians Mutual Insurance Company $1,906 $2,231 $2,676 $3,102Reserve National Insurance Company $1,476 $1,753 $2,062 $2,390Shenandoah Life Insurance Company $1,421 $1,567 $1,876 $2,119Standard Life & Accident Insurance Company $1,967 $2,016 $2,159 $2,562State Mutual Insurance Company $1,961 $2,336 $2,773 $3,150Sterling Life Insurance Company $2,236 $2,599 $2,957 $3,225

Stonebridge Life Insurance Company $1,516 $1,714 $2,077 $2,401Thrivent Financial for Lutherans $1,319 $1,595 $1,927 $2,290United American Insurance Company $2,515 $3,456 $3,979 $4,347United National Life Insurance Co. of America $1,819 $2,053 $2,427 $2,698United World Life Insurance Company $1,952 $2,219 $2,582 $2,816UnitedHealthcare Insurance Company $1,592 $1,945 $2,362 $2,722

Attained age policies - annual premium

Plan KIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Transamerica Life Insurance Company $841 $1,076 $1,340 $1,588

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

American Republic Corp Insurance Company $1,133 $1,269 $1,512 $1,700Bankers Fidelity Life Insurance Company $768 $900 $1,080 $1,200Blue Cross and Blue Shield of Kansas, Inc. $886 $1,043 $1,260 $1,548Colonial Penn Life Insurance Company $753 $918 $1,154 $1,425Humana Insurance Company $1,016 $1,237 $1,504 $1,778Sterling Life Insurance Company $962 $1,121 $1,280 $1,401UnitedHealthcare Insurance Company $580 $704 $828 $828UnitedHealthcare Insurance Company $837 $988 $1,147 $1,199

2015 Medicare Supplement Shopper’s Guide 37

Plan LIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Everence Association Inc. $1,437 $1,573 $1,678 $1,823Transamerica Life Insurance Company $1,249 $1,597 $1,988 $2,357

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

American Republic Corp Insurance Company $1,561 $1,748 $2,083 $2,341Colonial Penn Life Insurance Company $1,453 $1,742 $2,128 $2,559Humana Insurance Company $1,445 $1,757 $2,138 $2,527Thrivent Financial for Lutherans $939 $1,137 $1,375 $1,635UnitedHealthcare Insurance Company $1,077 $1,308 $1,539 $1,539UnitedHealthcare Insurance Company $1,151 $1,388 $1,678 $1,932

Plan MIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Transamerica Life Insurance Company $1,538 $1,966 $2,448 $2,902

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

Colonial Penn Life Insurance Company $1,823 $2,260 $2,795 $3,344Coventry Health and Life Insurance Company $1,621 $1,909 $2,306 $2,886

Family Life Insurance Company $1,761 $2,095 $2,487 $2,827Heartland National Life Insurance Company $1,597 $1,983 $2,321 $2,592KSKJ Life, American Slovenian Catholic Union $1,539 $1,831 $2,174 $2,471State Mutual Insurance Company $1,756 $2,092 $2,481 $2,821Thrivent Financial for Lutherans $1,239 $1,493 $1,793 $2,106United World Life Insurance Company $1,595 $1,812 $2,109 $2,300

Plan NIssue age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Transamerica Life Insurance Company $1,446 $1,849 $2,302 $2,729

2015 Medicare Supplement Shopper’s Guide38

Attained age policies - annual premiumCompany Age 65 Age 70 Age 75 Age 80

Aetna Health and Life Insurance Company $1,250 $1,371 $1,573 $1,784Aetna Life Insurance Company $1,405 $1,748 $2,117 $2,471American Continental Insurance Company $1,528 $1,729 $2,023 $2,227

American Family Life Assurance Co of Columbus $1,472 $1,784 $2,080 $2,372American Retirement Life Insurance Company $1,185 $1,399 $1,656 $1,949Blue Cross & Blue Shield of Kansas City $1,680 $2,268 $2,796 $3,300Blue Cross and Blue Shield of Kansas, Inc. $1,288 $1,516 $1,830 $2,248Central States Indemnity Company of Omaha $1,295 $1,456 $1,743 $1,967Christian Fidelity Life Insurance Company $1,135 $1,338 $1,594 $1,838Colonial Penn Life Insurance Company $1,254 $1,597 $2,045 $2,536Combined Insurance Company of America $1,507 $1,786 $2,028 $2,218Coventry Health and Life Insurance Company $1,587 $1,868 $2,257 $2,825Equitable Life & Casualty Insurance Company $1,340 $1,447 $1,587 $1,693Everence Association Inc. $1,323 $1,587 $1,799 $1,965Family Life Insurance Company $1,431 $1,682 $2,012 $2,273First Health Life and Health Insurance Company $1,253 $1,481 $1,715 $1,934Forethought Life Insurance Company $1,374 $1,514 $1,731 $1,944Government Personnel Mutual Life Ins. Co. $1,239 $1,365 $1,563 $1,758Guarantee Trust Life Insurance Company $1,166 $1,375 $1,620 $1,832Heartland National Life Insurance Company $1,376 $1,698 $2,000 $2,260Humana Insurance Company $1,334 $1,623 $1,975 $2,334Individual Assurance Co Life, Health, Accident $1,208 $1,363 $1,614 $1,885KSKJ Life, American Slovenian Catholic Union $1,193 $1,402 $1,678 $1,894Liberty National Life Insurance Company $2,326 $3,092 $3,598 $3,993Loyal American Life Insurance Company $1,616 $1,692 $1,926 $2,191Manhattan Life Insurance Company (The) $1,101 $1,270 $1,536 $1,812Marquette National Life Insurance Company $1,408 $1,836 $2,213 $2,555Medico Corp Life Insurance Company $1,204 $1,275 $1,544 $1,826

Medico Insurance Company $1,315 $1,476 $1,756 $2,040Order of United Commercial Travelers of America $1,679 $1,848 $2,196 $2,495Oxford Life Insurance Company $1,135 $1,338 $1,595 $1,838Pekin Life Insurance Company $1,100 $1,241 $1,469 $1,725Philadelphia American Life Insurance Co. $1,279 $1,361 $1,558 $1,704Physicians Mutual Insurance Company $1,649 $2,010 $2,470 $2,927Reserve National Insurance Company $1,336 $1,587 $1,866 $2,164Sentinel Security Life Insurance Company $1,219 $1,399 $1,602 $1,802Shenandoah Life Insurance Company $1,164 $1,284 $1,537 $1,736Standard Life & Accident Insurance Company $1,285 $1,317 $1,411 $1,674State Mutual Insurance Company $1,621 $1,906 $2,281 $2,578Sterling Life Insurance Company $1,272 $1,482 $1,690 $1,848

Plan N (cont’d)

2015 Medicare Supplement Shopper’s Guide 39

Attained age policies - annual premium (cont’d)

SELECT Plan AAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Sterling Life Insurance Company $1,636 $1,860 $2,055 $2,155

Company Age 65 Age 70 Age 75 Age 80Stonebridge Life Insurance Company $1,267 $1,432 $1,736 $2,006United American Insurance Company $2,108 $2,805 $3,254 $3,601United National Life Insurance Co of America $1,252 $1,411 $1,659 $1,878United World Life Insurance Company $1,785 $2,029 $2,361 $2,575UnitedHealthcare Insurance Company $1,233 $1,497 $1,761 $1,761UnitedHealthcare Insurance Company $1,184 $1,491 $1,851 $2,164USAA Life Insurance Company $1,248 $1,463 $1,744 $2,020

SELECT Plan BAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Blue Cross & Blue Shield of Kansas City $1,368 $1,872 $2,280 $2,712Sterling Life Insurance Company $1,778 $2,040 $2,278 $2,420

SELECT Plan CAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Blue Cross & Blue Shield of Kansas City $1,716 $2,352 $2,868 $3,396Blue Cross and Blue Shield of Kansas, Inc. $1,186 $1,396 $1,677 $2,053Sentinel Security Life Insurance Company $1,794 $2,059 $2,346 $2,624Sterling Life Insurance Company $2,074 $2,369 $2,643 $2,818UnitedHealthcare Insurance Company $1,487 $1,805 $2,124 $2,124

SELECT Plan DAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Sentinel Security Life Insurance Company $1,355 $1,555 $1,776 $1,993

2015 Medicare Supplement Shopper’s Guide40

SELECT Plan FAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Blue Cross & Blue Shield of Kansas City $1,728 $2,364 $2,880 $3,408Blue Cross and Blue Shield of Kansas, Inc. $1,260 $1,483 $1,783 $2,182Sentinel Security Life Insurance Company $1,837 $2,108 $2,403 $2,686Sterling Life Insurance Company $1,825 $2,084 $2,325 $2,480UnitedHealthcare Insurance Company $1,495 $1,816 $2,136 $2,136

SELECT Plan GAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Sterling Life Insurance Company $1,645 $1,883 $2,105 $2,251

SELECT Plan KAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Blue Cross and Blue Shield of Kansas, Inc. $701 $825 $996 $1,224Sterling Life Insurance Company $745 $854 $956 $1,024

SELECT Plan NAttained age policies - annual premium

Company Age 65 Age 70 Age 75 Age 80Blue Cross & Blue Shield of Kansas City $1,368 $1,872 $2,280 $2,712Sentinel Security Life Insurance Company $1,164 $1,120 $1,282 $1,442Sterling Life Insurance Company $1,219 $1,397 $1,564 $1,676

2015 Medicare Supplement Shopper’s Guide 41

Appendix I: About Medicare and Medicare Advantage Plans

What is Medicare?Medicare is a federally-run health insurance pro-gram administered by the Centers for Medicare and Medicaid Services (CMS). In order to be eligible to receive Medicare, you must meet at least one of the following criteria: • be age 65 or older • have permanent kidney failure • have a Medicare-qualified disability

The Kansas Insurance Department has no direct regulatory authority over Medicare.

How does Medicare work?

There are four separate parts to Medicare: Part A (Hospital Insurance), Part B (Medical Insurance), Part C (Medicare Advantage plans) and Part D (Prescrip-tion Drug Coverage). Each of these parts covers specific services (see graph on next page).

When you near your 65th birthday, you should contact Medicare to see about enrolling in Part A coverage. You will also have the option to enroll in Part B and Part D at this time. For most people, en-rollment in Part A is automatic and comes without cost - the Medicare taxes you’ve paid while you’ve worked take care of this premium. However, most people will need to pay a monthly premium for Part B, Part C and Part D.

Medicare enrollment

Some people qualify for automatic enrollment in Medicare, while others must apply for enrollment.

Applied enrollment - If you are not receiving Social Security or Railroad Retirement Board (RRB) benefits (for example, if you are still working), you will need to apply to receive Part A and Part B. You can contact the Social Security office 3 months

before your 65th birthday to receive this coverage. Individuals with End-Stage Renal Disease (ESRD) should also contact their local Social Security office to sign up for Parts A and B. If you want Part C and/or Part D, you must apply for it - there is no auto-matic enrollment.

Automatic enrollment - Automatic enrollment in Part A and Part B occurs if you are already receiving benefits from Social Security or the RRB. This cover-age begins the first day of the month that you turn 65 years old. If your birthday falls on the first day of the month, your coverage will begin the first day of the month before you turn 65. Individuals under age 65 and disabled will automatically be enrolled in Part A and Part B after receiving disability benefits from Social Security (or some other limited sources) for 24 months. NOTE: Three months before your 65th birthday you will receive your red, white and blue Medicare card. Keeping this card automatically enrolls you in Parts A and B. If you do not want to receive Part B, follow the instructions that are included with the card.

Enrollment periods for Parts A, B, C and D vary. The following are guidelines to help you figure out when your enrollment period is. There are several different enrollment periods that you should be aware of when signing up for Medicare.

Initial enrollment period: Your initial enrollment period lasts 7 months, beginning three months before your 65th birthday (or, if you are still covered under a group health plan, when you first become eligible for Part B coverage). During this time, you will enroll in Part A (and, if you choose, Part B) or a Medicare Advantage Plan (Part C). You will also de-cide if you want Part D prescription drug coverage. Your initial enrollment period is the only time that you can enroll in all Parts of Medicare penalty-free. Make sure to weigh your options carefully during this time so that you don’t have to pay late enroll-ment fees for Part B or Part D later on.

2015 Medicare Supplement Shopper’s Guide42

**Some information taken from CMS’s “Medicare Basics.”

How is Medicare divided?

Medicare has four parts:

• Helps cover doctor services and outpatient care.

• Helps cover some preventive services to help maintain a person’s health and to keep certain illnesses from getting worse.

• Helps cover durable medical equipment.

Medicare Part B (Medical Insurance)

• A way to get Medicare benefits through private insurance companies approved by and under contract with Medicare.

• Includes Part A, Part B, and usually other benefits Medicare doesn’t cover. Some plans also provide prescription drug coverage for an additional cost.

• Part C takes the place of Parts A and B.

Medicare Part C (Medicare Advantage Plans)

• Run by private companies approved by Medicare.

• Helps cover the cost of prescription drugs.

• Each plan can vary in cost and drugs covered.

Medicare Part D (Prescription Coverage)

• Helps cover inpatient care in hospitals (includes critical access hospitals, inpatient rehabilitation facilities, and long-term care hospitals).

• Helps cover skilled nursing facility (not custodial or long-term care), hospice, and home health care services.

Medicare Part A (Hospital Insurance)

General enrollment - Those who did not enroll in Part A or Part B during their initial enrollment period may do so between January 1 and March 31 each year. Those who enroll during this time will begin receiving this coverage on July 1 of the same year. You may have to pay a late enrollment fee if you sign up during this time.

Special enrollment - Special enrollment periods occur for those who chose not to enroll in Part A and/or B because they were still covered under employer or other group plan coverage when they turned 65. Generally this special enrollment period occurs during the 8-month period following the end of employment or the end of group health plan coverage, whichever comes first (for example, retirement). If you have been continuously covered under employer or group-sponsored health cover-

age since your 65th birthday, and enroll in Part A and/or Part B during this special enrollment period, you will not have to pay a late enrollment penalty.

Late enrollment penalties - Should you choose not to enroll in Part B or Part D during your initial enrollment period, then change your mind later, you may be charged a late enrollment penalty. To avoid this extra cost, make sure you weigh your options carefully during the 7-month initial enrollment period around your 65th birthday.

Gaps in MedicareMedicare was never intended to pay 100% of medi-cal bills. It forms the foundation for beneficiaries’ protection against heavy medical expenses. There

2015 Medicare Supplement Shopper’s Guide 43

are gaps in Medicare coverage where the benefi-ciary must pay a portion of expenses. Medicare supplement insurance, also called Medigap, can help cover some of these expenses. The Kansas Insurance Department is charged with regulating Medicare supplement insurance (see Section I).

Items and services not covered under Medicare include: • Acupuncture • Deductibles, coinsurance or copayments when you obtain certain health care services • Dental care and dentures • Cosmetic surgery • Long-term care, like custodial care (help with bathing, dressing, using the bathroom and eating) at home or in a nursing home • Eye care (routine exam), eye refractions • Hearing aids and hearing exams • Orthopedic shoes (with a few exceptions) • Outpatient prescription drugs (with a few exceptions) • Routine foot care, such as cutting of corns or calluses (with a few exceptions) • Diabetic supplies (like syringes or insulin, unless the insulin is used with a pump or it may be covered by Medicare Part D) • Chiropractic services except to correct a subluxation (when bones in your spine move out of position) using manipulation of the spine. You are responsible for co- insurance, and the Part B deductible applies

To find out if Medicare will cover a service, visit www.medicare.gov/coverage or call 800-Medicare (800-633-4227).

Medicare supplement insurance was created to help cover some of these gaps in coverage. See Section I for more information on what Medicare supplement insurance covers to help you decide whether it is right for you.

What is Part A?Part A of Medicare was created to cover inpatient care in hospitals, skilled nursing facilities, hospice

and some home health care. Many people do not have to pay for this portion of Medicare because they have paid Medicare taxes while working (re-ferred to as “premium-free Part A”). You will not have to pay a monthly premium for Part A if: • You already receive retirement benefits from Social Security or Railroad Retirement Board benefits. • You are eligible for Social Security or Rail- road Retirement Board benefits but haven’t filed for them yet. • You or your spouse worked in Medicare- covered employment for at least 10 years.

If you do not qualify for premium-free Part A, you may still be able to purchase Part A coverage, as long as you meet one of the following require-ments: • Are 65 or older, are eligible to purchase Part B coverage, and meet residency or citizenship requirements. • Are under 65, disabled, and your premium- free Part A ended because you returned to work.

What is included in Part A?Generally, the following services are covered under Part A:

• Inpatient care in hospitals (such as critical access hospitals, inpatient rehabilitation facilities, and long-term care hospitals). • Inpatient care in a skilled nursing facility (not custodial or long-term care).• Hospice care services.• Home health care services.• Inpatient care in a Religious Nonmedical Health Care Institution.