kbb final paper - university of california, berkeley

TRANSCRIPT

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

1

Introduction

Fabio is currently developing a start-up, SGZ, that will operate in Brazil as the first

online car insurance broker in which the consumer compares several options of car insurance

plans from different insurance companies and acquires the one that best fits his/her criteria (e.g.

price, coverage). Revenues come from commissions paid by the insurance company for each

policy sale.

Although common in other markets, this business model faces a unique legal context in

Brazil, which empowers incumbents to apply a mix of market and non-market strategies to fight

SGZ’s entry.

Car Insurance Market – History, Structure and Stakeholders

In Brazil, an individual or a company cannot buy an insurance plan directly from an

insurance company due to a law that was implemented by a populist government in the 1970’s.

According to the legislation, insurance must be purchased through a broker. The rationale

behind this law is very controversial: it was created to avoid the formation of a cartel by the

insurance companies and to provide a small part of the population with a way to make a living by

creating an artificial market for car insurance brokers.

To stop insurance companies from forming a cartel, the government allowed the

formation of a smaller, yet powerful cartel of insurance brokers. This action created an anomaly

in the market in which the brokers operate in a pocket of artificial demand. Every new player in

the insurance brokerage business needs to earn an authorization by the national insurance

brokers’ association under a very intense selection process creating high barriers to entry. In

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

2

addition, this artificial market provides low incentives to modernize and compete with other

brokers. There is also tacit coordination on advertising expenditures and targeting. As a result,

the industry is heavily fragmented and old-fashioned. With all these conditions, brokers earn an

average of 16%1 commission from insurance companies on every sale, including policy

renewals. The Brazilian car insurance brokerage business is a $1BB/year1 industry, only

considering individual car policies.

An increase in the Brazilian population’s purchase power, the emergence of a middle

class and increasing competition among car manufacturers has enabled the Brazilian car

insurance market to grow at a strong and steady pace. In the midst of the financial crisis in the

beginning of 2009, car sales in 1H2009 increased by 4.1%2 when compared to the same semester

in 2008 (before the crisis was fully in place). The estimated growth in the industry for 2010 is

over 10%2. In addition, insurance is an increasingly important product for many Brazilians, not

only due to the chaotic traffic in cities, but also due to the high car theft rate.

To enter the car insurance market, SGZ needs to be incorporated as a brokerage company

to be eligible to sell insurance policies from insurance companies directly to the consumer.

Since SGZ is bringing a disruptive business model to Brazil – current insurance agents only sell

through phone – the Company must make sure to consider the reactions and strategies of all

stakeholders involved, including insurance brokers, insurance companies, consumers and the

1 Source: Superintendência de Seguros Privados (SUSEP): Brazilian Government’s Agency, which regulates the car insurance industry -‐ http://www.susep.gov.br/menuestatistica/ses/principal.aspx 2 Source: Associação Nacional de Fabricantes de Veículos Automotores (ANFAVEA): Brazilian Association of Car Manufacturers and Importers -‐ http://www.anfavea.com.br/tabelas.html

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

3

government. SGZ must analyze the decisions and best responses each party may utilize in the

event of SGZ entering the market.

Repeal of legislation?

The car insurance brokerage business relies on current laws to sustain its market.

Without this law, insurance companies would no longer need to use middlemen and would

immediately start selling insurance directly to the end-user. In this case, the car insurance

market would resemble that in the United States, decimating the demand for car insurance

brokers.

SGZ will attempt to profit on the current inefficiencies and inconvenience of current

brokerage practices by introducing an efficient and transparent means for consumers to directly

pick the best policy for them, without having the need for a traditional broker. While there

certainly is a tremendous opportunity to capitalize on a market that has been allowed to wallow

in inefficiency, SGZ, like the current brokerage industry, also relies on the artificial market that

Brazilian law has created. The repeal of this law would eliminate the opportunity.

Since SGZ relies on this law, the Company must determine whether the law will be

repealed (eliminating the current entrepreneurial opportunity) in the near future before deciding

to enter the market. To do this, SGZ must analyze the mental models of the stakeholders that

would be involved and affected by this decision. The players in this game are the government,

consumers (voters), insurance companies and the brokers.

Local insurance companies, who make up the majority of market share, are on the fence

regarding the repeal of the law. Although it might seem obvious that they would want to get rid

of a step in the value chain and be able to sell directly to consumers, the brokers’ law gives these

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

4

insurance companies the opportunity to lock in brokers and protect markets from the

international insurance companies, which have always struggled to grow in Brazil due to the

channel protection by the local companies. International insurance companies, on the other

hand, would definitely want to have the opportunity to sell their own products direct to

consumers. This would help them overcome the lack of channels and use the knowledge of

online sales they have developed in other countries in North America and Europe.

All in all, the domestic insurance companies, which have more political power than the

international companies, would likely want to keep the law to inhibit transparent competition

amongst each other and from the middle-market international insurance companies, keeping the

status quo.

For SGZ, the analysis should revolve around the politicians, brokers and consumers, as

these groups will likely have the most influence on the decisions regarding the law. Lawmakers

are the only group that has the final say on the status of legislation and these politicians are held

accountable by their constituents. Therefore, the decision of whether to repeal the law will come

down to the costs and benefits to the brokers and consumers and the subsequent change in

approval ratings, and thereby votes, that any change would bring for the politician.

With the hopes of getting re-elected, politicians will choose to repeal the law if they feel

that doing so will increase the overall number of voters who will support them in the next

election. To analyze this situation, SGZ must calculate the approximate amount of voters

politicians would lose due to the broker community losing jobs and compare this amount to the

number of voters gained from consumers based upon the insurance savings they would gain if

they no longer had to transact through a broker (note that the only gains in votes from consumers

would be from those who do not already support the current government.)

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

5

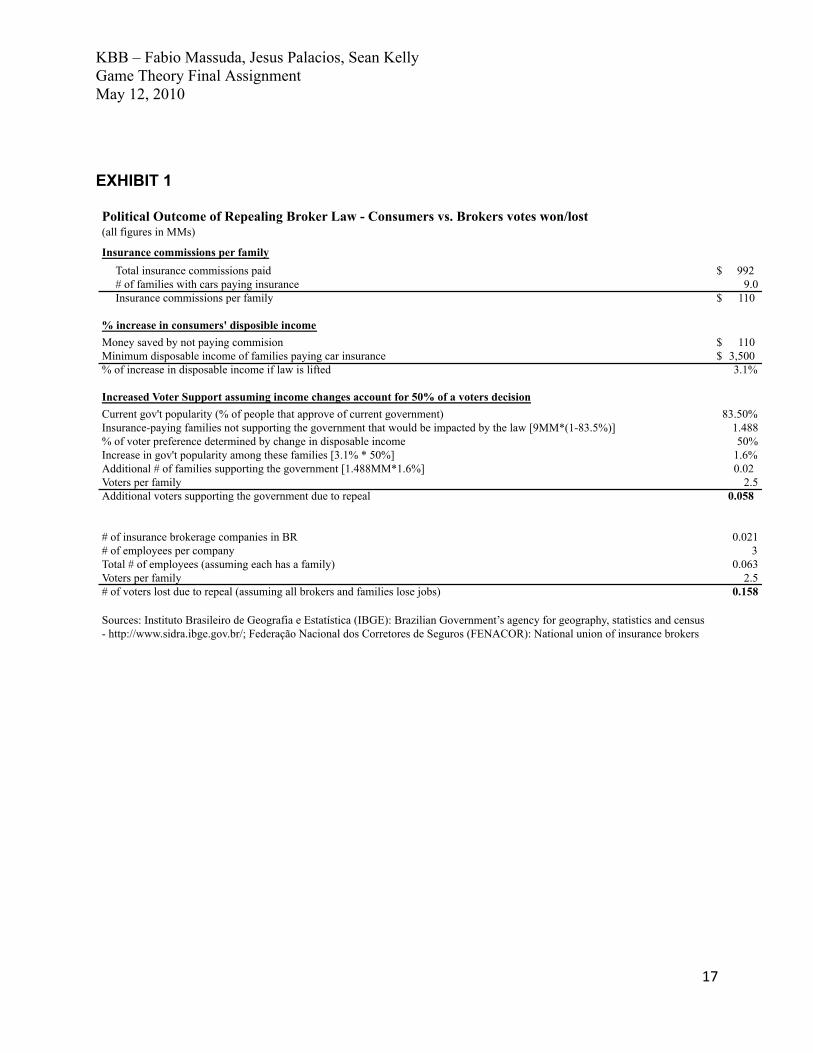

Exhibit 1 outlines the analysis of gained and lost votes. In terms of the consumers’ votes

gained from the repeal of the broker law, SGZ must first see how much money each family with

car insurance would save and then how much this savings relates to their disposable income. In

2009, $992.2MM was paid in commissions to insurance brokers. Approximately 9MM families

currently pay for car insurance, paying an average of $110/per family. If brokers were

eliminated from the value chain, each of these families would save approximately $110, which

amounts to a 3.1% change in disposable income for a family making $3,500/year (this is low end

of the range of family incomes, but is used to be conservative.)

We estimate that the total change in votes received by a politician due to the savings

brought by the elimination of brokers would be approximately 58K based on current government

support levels and assuming that the change in a family’s disposable income has a 50% effect on

political sentiment.

On the other side of a decision to repeal the current broker law is the brokers and their

families. Currently there are approximately 21K brokerage companies, with an average of three

employees per company, in Brazil. Assuming that each of these 63K employees has a family

and that each family contains 2.5 voters3, a repeal of the broker law would most certainly cause

the loss of approximately 158K voters who will have been put out of work.

Given these approximations about votes won and lost given a repeal of the broker law, it

is in the best interest for politicians to keep the current law in place for now. Given this

assessment, SGZ can go forward with plans to enter the market without fear of the government

repealing the law under the current circumstances.

3 Source: Instituto Brasileiro de Geografia e Estatística (IBGE): Brazilian Government’s agency for geography, statistics and census -‐ http://www.sidra.ibge.gov.br/

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

6

Market Entry

The structure of the insurance market can impose several barriers to entry. Due to the

disruption SGZ is bringing to the market, insurance companies might be afraid of triggering a

price war. This price war could be caused by the easier approach to comparing benefits and

prices caused by a service like SGZ. Although in markets dominated by this sales approach (e.g.

UK, Switzerland, Spain) the evidence shows that insurance companies sustained a 5%

profitability average4 – the current average in Brazil. The fear of a price war is justified and

might provide insurance companies enough arguments to not allow SGZ to sell their policies.

The strategy to overcome this resistance is to take advantage of the current distribution of

firms in the market. Currently 15 companies own 98% of the market with the top 4 having a 60%

share5. The top 4 companies are naturally more averse to a disruption in the market, especially

one that could expose them to increased transparency and therefore more fierce competition that

would harm profitability. Hence it is very unlikely that these companies, wanting to keep the

status quo, would allow SGZ to sell their policies initially.

A few of the bottom 11 companies though are large international insurance companies

that are struggling to grow in the Brazilian market mainly due to the fact that the big domestic

insurance companies have locked up most of the brokers. This means that a lock up of the

distribution channel is preventing these companies to grow more rapidly. For these big

international companies – which are the middle market in Brazil – the creation of a new channel

with a potentially strong reach could be very valuable. These companies have the decision of

4 Source: Yahoo! Finance 5 Source: Superintendência de Seguros Privados (SUSEP): Brazilian Government’s Agency, which regulates the car insurance industry -‐ http://www.susep.gov.br/menuestatistica/ses/principal.aspx

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

7

whether or not to allow SGZ to sell their policies, facing the risk of a price war or a more clear

exposure of flaws in their value proposition, but having the benefit of having access to an

innovative sales channel.

To outline this game SGZ needs to also understand the structure of the car insurance

consumer market. There are 3 main types of consumers: those loyal to insurance companies,

those loyal to brokers and those that are free agents.

The first group (15% market share) is comprised of those consumers that are loyal to a

specific insurance company. Even if SGZ presents itself as a more convenient way of signing up

for a policy, these consumers would not use it unless the insurance company they are loyal to

offers its product through SGZ.

The second group (10% market share) is comprised of those consumers that are loyal to a

specific broker. They are highly influenced by those brokers and the advent of a new channel is

unlikely to affect their behavior.

The third group (75% market share) is comprised of those clients that usually compare

multiple insurance policies. They are not loyal to any specific insurance company or broker, but

are looking for value for their money. This value can be translated in terms of benefits and

convenience.

Consider an entry into the market in which SGZ targets the middle-size companies. To

assess whether or not the international insurance companies will accept SGZ as a sales channel,

let’s design a game. For example we can take two large international insurance companies that

are among the mid-size in Brazil: Liberty Mutual – one of the top 5 insurance companies in the

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

8

US, but with a 5.1% market share in Brazil6 – and Allianz – the 2nd largest insurance

organization in the World, but also with a 5.1% market share in Brazil2.

The decision Liberty faces is whether or not to have SGZ as a sales channel, especially

considering that a competitor – Allianz in this case – also faces the same decision.

Consider that SGZ might achieve a market share of 10% in the first year, which is a

conservative penetration estimate based on penetration rates observed by similar companies in

other markets7. If none of the companies accept SGZ as a channel, they stop the company from

entering and they keep their 5.1% market share each. If only one of the companies accepts SGZ,

we can project that the penetration SGZ achieves is only 5%, which is fully taken by that one

company. Hence that company has its original 5.1% market share plus 5% from SGZ less a

potential loss in market share due to increased exposure to product comparison by consumers.

Due to the current size of Liberty and Allianz, the probability of them losing market share by

deciding to sell through SGZ too is small, as their current market share is composed of either

loyal clients or those that find a better value-to cost ratio with them, hence it does not depend

much on the increasing exposure they might gain from starting to use SGZ as a channel. We

assumed the loss to be one-tenth of their current market share, i.e. 0.5%. If both companies enter

then SGZ achieves 10% and due to the current market share of the companies, we assumed that

they will evenly share the 10% penetration of SGZ, achieving 10% penetration market share

each less the loss in market share from increased exposure, which in this case we assumed to be

6 Source: Superintendência de Seguros Privados – Brazilian Government’s regulatory board for insurance companies 7 Source: Admiral Group: Owner of similar service websites in Spain, France and the UK.

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

9

1%. As outlined in the diagram in Exhibit 2, it is in these middle-size insurance companies’ best

interest to start selling through SGZ, enabling the company to enter the market.

By continuing with the strategy of going after the mid-size insurance companies, SGZ

offers an interesting value proposition for them: access to a powerful sales channel and the

possibility of growth by overcoming the current lock-up of brokers by the big insurance

companies. Hence, the upside for mid-size companies to join – especially after a critical mass of

them has signed up with SGZ – is higher than the potential downsides as they will already be

losing market share when a critical mass is with SGZ. The next step then for SGZ is signing up

with the big insurance companies.

Fight with Big Insurance Companies

The secret when dealing with big insurance companies is scale. Once SGZ achieves

enough scale, the benefits for big insurance companies to use this channel increase for three main

reasons. First, they might be losing market share already if customers start using more and more

of the SGZ service due to its convenience and unparallel customer service. Second, similarly to

the above game, the first mover among the big companies might enjoy access to this increasingly

important channel, thus having the opportunity to offer its products in a competition only with

mid-size companies in the beginning. Third, once a big company has moved in, all other big

companies would want to follow to avoid an acceleration of market share loss to this first mover.

In overall terms, once SGZ achieves scale, there is pressure for big companies to sign up with it.

Empirical evidence from other markets show that similar players to SGZ managed to sign up

with the insurance industry leaders in less than 1.5 years of market entry.8

8 Source: Admiral Group: Owner of similar service websites in Spain, France and the UK

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

10

However let’s suppose that, due to the threat to their current channel lock-up, big

companies would try to kill SGZ instead of joining it. There are two ways they might engage in

this war. The first way is politically and the second way is market-based through a price war.

The political option is to lobby with the Brazilian government to change the legislation

and lift the brokers’ exclusivity as a sales channel to consumers. Due to reasons outlined before,

several barriers exist against that. Being labeled as a company that pushed for the repeal of

legislation that would extinguish the livelihood of brokers and related members for the sake of

increasing profits would sound bad among the public and likely have an adverse effect on

business. Also, SGZ would still be the only relevant channel for mid-size insurance companies

if the government decided not to lift the law, keeping the big companies’ lock-up over brokers.

Finally, if the legislation is lifted, insurance companies will start using the Internet as a direct

sales channel and SGZ would not need the companies’ authorization to compare benefits and

price anymore. SGZ would adapt its business to the new environment and create a service like

Kayak, which simply has automatic systems to check companies’ websites. Hence it seems that

the political tactic is unlikely at this point.

The market-based tactic, however, might seem relevant. Basically, the insurance

companies, using their deep pockets, could try to cut prices to a point where all policies being

offered by SGZ are more expensive. It is unlikely that small brokers would contribute financially

to this war by lowering their commission rates due to their short cash position. In addition, since

mid-size companies might not have enough cash to fund a price war, the only way for SGZ to

compete is to cut the amount of its commissions. Hence, to simulate such a war we designed a

game dynamic with 2 players: big insurance companies, who will lower the cost to consumers

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

11

through premium cost cuts (in collusion) and SGZ, who will lower the cost to consumers through

a reduction of its commission rates.

In this game, both players have 2 options: engage or don’t engage in a price war. This

game only makes sense to big insurance companies if they see SGZ as a credible threat. In this

sense, we assumed that a trigger to a price war is when SGZ achieves 10% market share.

If both players choose not to start a price war, SGZ would gain market share reaching

30% in Year 5 and benefit from a 3% profit margin over policy prices. On the other hand, big

insurance companies would keep their 5% profitability and lose market share due to SGZ.

If SGZ engages in a price cut strategy and big insurance companies do not, the former

would reach 40% market share by Year 5, sacrificing profits until then; and the latter would lose

more market share, but keeping the profitability percentage.

If big insurance companies engage in a price war and SGZ does not, we estimated that

SGZ might go bankrupt in 4 years, losing 2.5% market share per year. On the other hand, big

insurance companies would give up their 5% profitability for those 4 years and be back to their

current market share level after that, benefiting from the standard profitability.

If both engage in a price war, SGZ would go bankrupt in 3 years as insurance companies

have deeper pockets and big insurance companies would have not only to give up profits but

have losses in those 3 years to be able to undercut SGZ in terms of pricing.

The calculations of outcomes can be seen in Exhibit 4. The game diagram in Exhibit 5

shows the outcomes, proving that the dominant strategies for both players are not to engage in a

price war due to the razor-thin profitability of the industry.

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

12

Fight with Brokers

As mentioned before, due to shallow pockets, it is very unlikely that brokers could start a

price war with SGZ. In that sense, the most likely way they might fight SGZ is through politics

by claiming that although being incorporated as a brokerage company, SGZ cannot be

considered a valid player under the broker law, and therefore SGZ could not operate in the

market. This strategy is very powerful and would immediately hurt SGZ. Applying game theory

concepts, a counter-strategy is to position SGZ as a ‘friend’ of customers – by bringing

transparency to the market – and threat that, if it is stopped from operating, it will engage

customers to campaign against the brokers’ monopoly, eventually leading to the lifting of the

law. In regards to the aforementioned decision that the government faces – whether or not to lift

the law – this threat means to make the general population more aware of the issue and more

willing to have the law lifted, making it more beneficial for the government to cut the monopoly

of the brokers as a sales channel. Though SGZ would be hurting its own business prospects by

helping to repeal the law, the threat is still highly credible because SGZ would stand to lose very

little (except for the opportunity to take advantage of the artificial market) and the brokers have

so much to lose (their entire livelihood.) Given the risk of this threat being credible, brokers

would likely be apprehensive about pursuing this political strategy. To demonstrate the decision

that brokers face, we designed the decision tree pictured in Exhibit 4. It is easy to see that, if the

brokers engage in this fight, SGZ’s best response is to fight to have the law lifted. Therefore, the

decision for the brokers depends on whether:

($992MM-X)*(1-MS1) < ($992MM)*(1-MS3), where $992MM is the total revenues of

the car insurance brokerage business.

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

13

In a free market without the protection to brokers it is more likely that SGZ has a higher market

share than with the protection, because its value proposition is a better match to the situation

where insurance companies sell their products online directly to clients. Thus, since X>0, then

insurance companies are better off by not engaging into a political war.

Applications of game theory to foster competition

In a later stage, once SGZ has reached a critical scale –measured perhaps by market share

or traffic volume milestones to be defined – an auction mechanism for brokerage fees will be put

in place in order for SGZ to extract the highest value from attracting customers that insurance

companies may consider either the most profitable or strategic for market expansion goals.

Today, the brokerage fees structure is flat, meaning that brokers have no incentives to

attract the best customers to an insurance company. An auction system will allows insurance

companies to bid higher brokerage fees in exchange for being featured in SGZ’s website as a

‘Featured Offer’ if they match the lowest price available to each customer from other

competitors within SGZ’s network, providing a higher commission than it would pay originally.

How will this work?

A customer will enter SGZ website to request a quote for car insurance. The system will

require policy specific information (car making, model, etc) as well as socio-demographic

information (age, sex, years driving, etc) that insurance companies will use to provide their best

base price (as illustrated in Exhibit 6). The base price list is immediately shared with all

insurance companies’ systems. In a second step, each company’s system will decide whether or

not to match the best price available and will place a bid for brokerage fee applicable to that

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

14

specific policy (the bid cannot yield a lower absolute commission than that under the standard

flat rate). As per Exhibit 6, you can see that Company B and Company C decided to match the

lowest price and offered the minimum commission to be higher than their initial offers. Finally,

the highest bid wins the auction and its offer is featured as a recommendation in SGZ’s website.

If the company is chosen as a provider, it pays SGZ the second best commission offer – to

stimulate the insurance companies to bid their willingness to pay. Naturally, all insurance options

will have to be equivalent in terms of policy characteristics (deductible, co-pay, coverage, etc).

By the end of this process, it is the consumer obviously that decides which company he / she will

have as a provider, however we increase our potential profits. In Exhibit 6, Company C is the

winner, being promoted as a ‘Featured Offer’ in. It is important to mention that the auction is

voluntary, hence those not participating (e.g. Company D in Exhibit 6) still are shown as options

to the client on their regular pricing.

Once, the offer is presented, the customer would chose whether to take the featured offer

or choose another insurance company, that is, being featured as the best alternative will not mean

that the customer is locked in with that option as this would be counterintuitive to the business

model.

It is important to note that this process will be performed in real time through the

insurance companies’ pricing algorithms and SGZ systems; so swift processing is a key success

factor. For this reason, the choice of auction mechanism would have to take into consideration

systems processing capabilities.

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

15

Of course, two elements ought to be present to have insurance companies willing to

accept this auction: SGZ’s scale – meaning that the service is relevant enough to be ignored by

insurance companies – and SGZ’s data capability which should be able to segment the market.

We consider systems processing capabilities as the main driver of choice as we know that

revenues will be maximized based on the revenue equivalence principle.

In summary, SGZ’s ‘featured insurance option’ proposal will add value to insurance

companies as they will be able to differentiate themselves from the competition in an ‘opt in’

basis. SGZ will be able to price this added value on a case-by-case basis through an auction

process and will be able to solve the single bidder problem by defining a minimum entry price.

Conclusion

The applications of game theory concepts on SGZ adds valuable insights for analyzing

the feasibility of entering a highly regulated insurance market as well as for determining the

appropriate strategies to be implemented based on competitors responses. In this complex

setting, it’s important to frame the analysis into the competitive landscape of the industry in

addition to understanding the behavioral aspects of every player including government

regulators, insurance companies, brokers and end customers. This is particularly interesting

given that the competitive landscape is highly determined by non-market strategies and

incentives; thus, getting a sense of non-market reactions is the key to assessing the actions that

SGZ has to undertake in order to be successful.

Finally, SGZ can leverage other game theoretic approaches to foster competition and

attract the highest value possible. In this case, we addressed the possibility of launching an

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

16

auction mechanism to set the basis for a more competitive market, shifting from a passive

intermediation system to a more active one where “shelf space” – a concept take from the retail

industry - plays a significant role in the pricing for brokerage commissions. In this case, game

theory contributes not only in the decision making process on whether and how to enter this

market, but also helps implement a competitive mechanism in line with the spirit of SGZ.

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

17

EXHIBIT 1

Political Outcome of Repealing Broker Law - Consumers vs. Brokers votes won/lost(all figures in MMs)

Insurance commissions per familyTotal insurance commissions paid 992$ # of families with cars paying insurance 9.0Insurance commissions per family 110$

% increase in consumers' disposible incomeMoney saved by not paying commision 110$ Minimum disposable income of families paying car insurance 3,500$ % of increase in disposable income if law is lifted 3.1%

Increased Voter Support assuming income changes account for 50% of a voters decisionCurrent gov't popularity (% of people that approve of current government) 83.50%Insurance-paying families not supporting the government that would be impacted by the law [9MM*(1-83.5%)] 1.488% of voter preference determined by change in disposable income 50%Increase in gov't popularity among these families [3.1% * 50%] 1.6%Additional # of families supporting the government [1.488MM*1.6%] 0.02 Voters per family 2.5Additional voters supporting the government due to repeal 0.058

# of insurance brokerage companies in BR 0.021# of employees per company 3Total # of employees (assuming each has a family) 0.063Voters per family 2.5# of voters lost due to repeal (assuming all brokers and families lose jobs) 0.158

Sources: Instituto Brasileiro de Geografia e Estatística (IBGE): Brazilian Government’s agency for geography, statistics and census - http://www.sidra.ibge.gov.br/; Federação Nacional dos Corretores de Seguros (FENACOR): National union of insurance brokers

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

18

EXHIBIT 2

EXHIBIT 3

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

19

EXHIBIT 4

KBB – Fabio Massuda, Jesus Palacios, Sean Kelly Game Theory Final Assignment May 12, 2010

20

EXHIBIT 5

EXHIBIT 6

Base pricingPrice to consumer Standard comission (%) SGZ's potential revenues

Company A 1000 15.0% 150.00$ Company B 1010 17.0% 171.70$ Company C 1100 16.0% 176.00$ Company D 1250 15.0% 187.50$

After biddingPrice to consumer Offered comission (%) SGZ's potential revenues

Company A 1000 15.0% 150.00$ Company B 1000 17.2% 171.80$ Company C 1000 17.7% 177.00$ Company D 1250 15.0% 187.50$

Company C is the winner, so it is presented as a 'Featured Offer'