kdi-imf-world bank conference on strengthening the

TRANSCRIPT

KDI-IMF-World Bank Conference on Strengthening the Management of Public Investment: Korean and International Experiences

Seoul, October 30-31, 2014 Dr. Murray Petrie Director, Economics and Strategy Group. [email protected]

Distinctive challenges of PIM

Fiscal risks and PIM

International transparency standards

Public participation in PIM

Core PIM transparency indicators

Some special cases

Concluding remarks

2

3

Focus here is on government capital expenditures v broader and less well-defined, concept of investment expenditures.

Acquisition of fixed capital assets, including own-account capital formation and also major renovations, reconstructions, or enlargements of existing fixed assets

Investment cycle v project cycle

4

Modalities: Central govt. MDAs EBFs Donors On-lending and guarantees PPPs, RFIs SOEs Sub-national govternments

5

6

7

Projects are discretionary, location-specific risk of politicized decisions. Multiple modalities.

Dual budgeting – gaps and overlaps. Distinctive processes and capacity required: ◦ Multi-year planning, budgeting, project management,

accounting, reporting. ◦ Project appraisal. ◦ Complex procurement. ◦ Service delivery and the investment cycle

8

9

Optimism bias in ex-ante appraisal

Poor project selection

Lack of appraisal, procurement and project management skills

Inadequate accounting, reporting, and monitoring systems

Chronic under-execution of capital projects

Cost over-runs and time delays

Failure to operate and maintain created assets

Lack of data on PIM system performance

Case for ‘investing in capacity to invest’

10

International standards increasingly moving beyond disclosure to recognize importance of direct public participation to improve policy design and implementation, reduce fiscal risks: ◦ The GIFT High Level Principles of FTPA (HLP10).

◦ The new IMF Fiscal Transparency Code

◦ The new OECD Principles of Budgetary Governance

◦ The Open Budget Survey

◦ A new draft norm on public participation in fiscal policy, including public investment projects

11

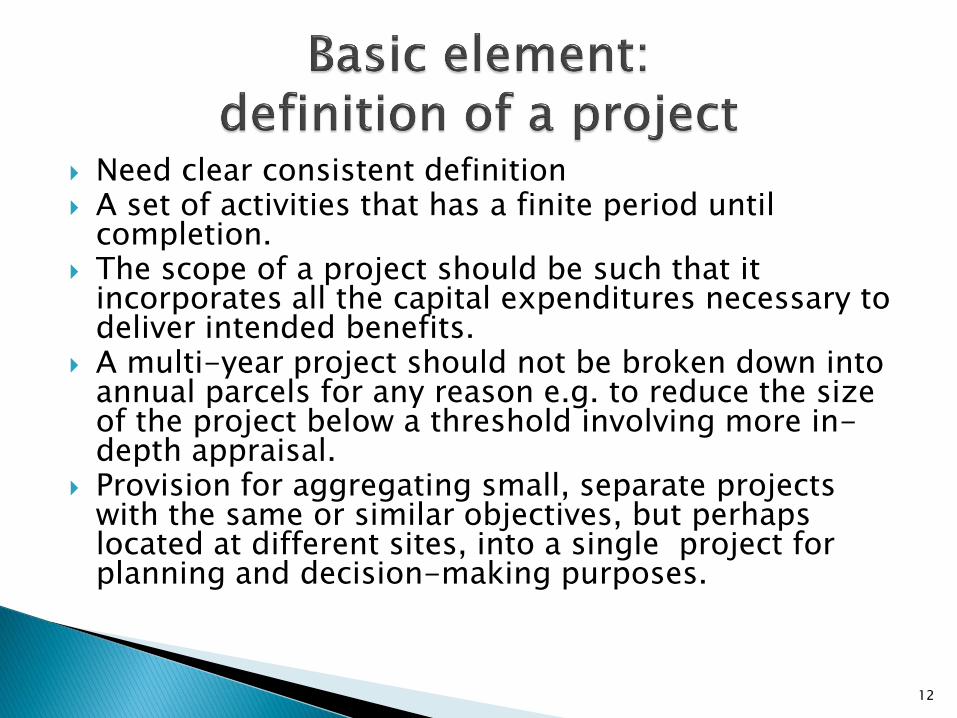

Need clear consistent definition A set of activities that has a finite period until

completion. The scope of a project should be such that it

incorporates all the capital expenditures necessary to deliver intended benefits.

A multi-year project should not be broken down into annual parcels for any reason e.g. to reduce the size of the project below a threshold involving more in-depth appraisal.

Provision for aggregating small, separate projects with the same or similar objectives, but perhaps located at different sites, into a single project for planning and decision-making purposes.

12

2.1.4 Investment Projects: the government regularly discloses its financial obligations under multi-annual investment projects, and subjects all major projects to CBA and open and competitive tender.

Basic practice Good practice

Advanced practice

One of the following applies: i) Regular disclosure of value of

total obligations ii) All major projects subject to

CBA iii) All major projects contracted

via open and competitive tender

Two of the three apply

All three apply.

13

Principle 3.2.4 in IMF Code:

Obligations under PPPs are regularly disclosed and actively managed.

Advanced practice:

The government at least annually publishes its total rights, obligations, and other exposures under PPP contracts and the expected annual receipts and payments over the life of the contracts. A legal limit is also placed on accumulated obligations.

14

Information on each capital project (total cost, cost to date, expenditure in T-2, T-1, budget year, T+1, T+2, any remaining balance)

Details of central government PPPs

Details of new capital spending being introduced in budget.

Details of any capital grants, on-lending to or guarantees of borrowing by SOEs and local governments for capital spending.

Estimates of any capital spending QFAs and tax expenditures.

15

Public Investment Management (PI-PIM): ◦ Projects appraised according to objective economic

analysis

◦ Integrated budgeting over the project life cycle

◦ Project data base, monitoring and reporting

Public Asset Management: ◦ Quality of non-financial asset monitoring (asset

registers and reports)

◦ Transparency in sale of non-financial assets

16

Coverage and content of sector strategies: PI-12(i)

Procurement: PI-19: four dimensions covering legal framework, use of competitive methods; public access to information; and independent complaints system.

17

Principle 3: Capital budgeting framework should be designed to meet national development needs in a cost-effective and coherent manner: ◦ Objective analysis of investment needs, project

costs and benefits, VFM.

◦ Projects analysed irrespective of financing method.

◦ Requires adequate institutional capacity, legal framework, coordination across levels of government, and integration with MTFF.

18

Different approaches to managing key risks in the PIM cycle in countries with advanced PIM systems: • In Ireland and the UK project proposals are subject to

independent review by the central finance agency. UK also uses Gateway system across whole project cycle.

• In Chile project appraisal is conducted by the planning ministry rather than by the sponsoring ministry, and subjected to independent review by a separate unit within MIDEPLAN.

• In Korea the CPIM in KDI, a semi-autonomous agency, conducts appraisals at arms-length from sponsoring ministries.

• Effective preliminary screening of proposed projects. • Mechanism to trigger review of a project’s continued justification

if there are material changes to project costs, schedule, or expected benefits during implementation.

• Major efforts to build capacity for project appraisal.

19

IMF FTC Principle 2.3.3

The government provides citizens with an accessible summary of the implications of budget policies and an opportunity to participate in budget deliberations.

The new OECD Principles of Budgetary Governance: …citizens should be able to engage with and influence the discussion about budgetary policy options…

20

OBS 2012 introduced detailed questions on public engagement by the executive, legislature and SAI across the whole budget cycle (Section 5 of the OBS).

Most countries provide few opportunities (average score 19/100).

Strongest performers include Korea, Brazil and Philippines.

21

The Global Initiative for Fiscal Transparency is a multi-stakeholder action network aimed at progressive increase in FTPA.

GIFT Lead Stewards are the IMF, the World Bank, the International Budget Partnership, and the governments of Brazil and the Philippines.

GIFT High Level Principles endorsed by UNGA in 2012.

22

Citizens and non-state actors should have the right and effective opportunities to participate directly in public debate over the design and implementation of fiscal policies.

23

GIFT has concluded there is a gap in the normative architecture, and is undertaking work on case studies, research, and development of a possible new norm on public participation.

24

Public consultation over national and sector planning, and over new infrastructure projects.

Public testimony at Legislature Select Committees.

Citizen membership of tender committees.

Procurement complaints mechanisms.

Judicial review of planning decisions.

Citizen monitoring of project implementation.

Citizen audits of projects.

Construction Sector Transparency Initiative (CoST)

25

Public authorities designing and implementing large physical investment projects should involve direct stakeholders (‘the affected public’), and the general public as appropriate, at each of the following stages:

i. National and regional planning. ii. Planning and design of each project, including option creation and analysis. iii. Feasibility studies, and environmental and social impact assessments. iv. Any decisions about displacement, resettlement and compensation. v. Construction. vi. Operations monitoring and evaluation. vii. Relicensing and eventual decommissioning as relevant.

26

Public authorities should publish a policy on the criteria they use to determine the scale and scope of public consultation and engagement over investment projects in particular instances.

The affected public and the general public should have access to low-cost administrative review of planning and implementation decisions, and the ability to seek judicial review of process.

27

a. Each public authority should document its overall approach to public participation, including the scope for deeper forms of participation such as involving citizens in decisions over the allocation of public resources, and the institutionalization of consultative processes through standing bodies… Public authorities should devote resources sufficient to achieve their objectives. b. Each public authority should define the knowledge, skills, behaviours and attitudes that relevant staff need to meet the authority’s objectives with respect to public participation, and take measures to ensure that staff possess the required attributes. c. Each public authority should define and document processes to learn effectively from the public participation exercises it conducts, including from monitoring, evaluation, surveys and complaints.

28

PIM in resource-dependent settings: ◦ Full information in budget on finances of Natural

Resource Fund, regular reporting on activities including any spending on public infrastructure.

◦ Details of any ‘resources for infrastructure’ projects.

◦ Information on any ‘infrastructure quasi-fiscal activities’ i.e. requirements for natural resource companies to finance public infrastructure.

29

PIM in post-disaster reconstruction: Unusually high level of uncertainty over damage and of

cost of replacement contracting difficult

Need rapid implementation, and major upsurge in activity capacity constraints.

Multiple co-located projects coordination costs

Use of the alliance model of procurement rather than competitive tender: variant of target cost approach with sharing of risks.

30

Need clarity of roles in budget-making between the executive and legislature.

Legislature should play active role in holding the executive to account for the budget, for in-year reporting, and for the Final Accounts and performance reporting

Where the legislature amends the budget significantly, need full transparency on amendments so public can hold each branch to account

Undesirable for projects to be added to budget that have not been subject to appraisal.

Legislature should play active role in ensuring public availability and integrity of fiscal information; and facilitating civil society input

31

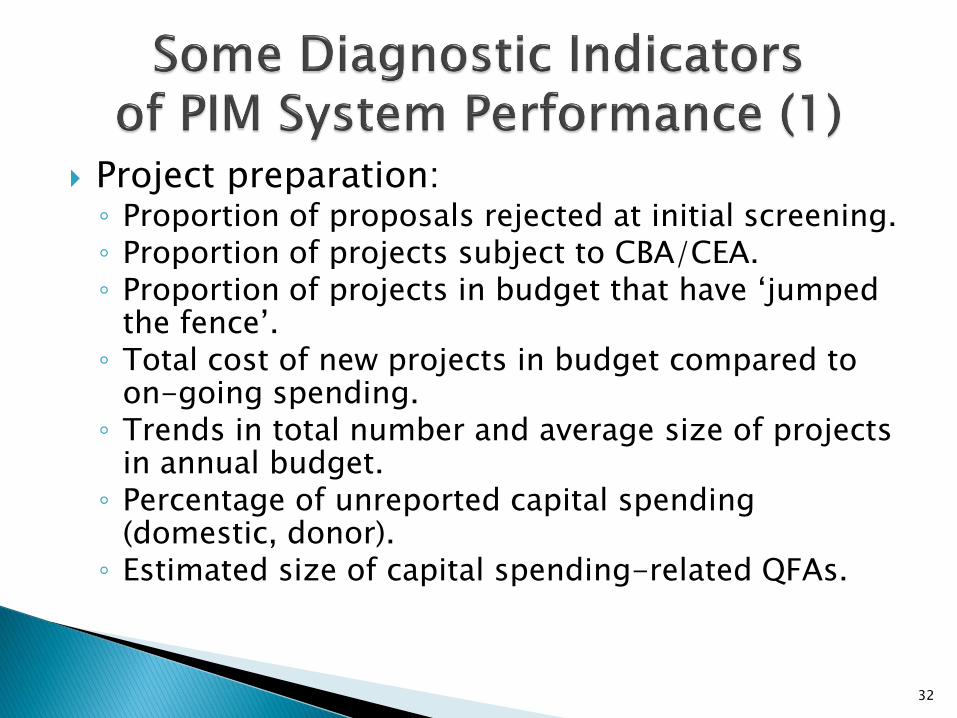

Project preparation: ◦ Proportion of proposals rejected at initial screening. ◦ Proportion of projects subject to CBA/CEA. ◦ Proportion of projects in budget that have ‘jumped

the fence’. ◦ Total cost of new projects in budget compared to

on-going spending. ◦ Trends in total number and average size of projects

in annual budget. ◦ Percentage of unreported capital spending

(domestic, donor). ◦ Estimated size of capital spending-related QFAs.

32

Project implementation: ◦ Capital budget execution rate (by month/quarter; by

MDA; domestic/donor). ◦ Frequency and coverage of in-year reporting (domestic

and donor). ◦ Proportion of project financing managed through

national systems (by donor). ◦ Proportion of projects cancelled/re-designed during

implementation. ◦ Completion rate of the public investment program. ◦ Proportion of open procurements. ◦ Average project cost and time over-runs (by MDA,

domestic/donor). ◦ Coverage of non-financial asset registers. ◦ Estimated rates of return of completed projects.

33

PIM a very demanding element of PFM, requires specific capacities.

Key risks related to project selection, cost/time overruns, and poor service delivery.

Transparency (disclosure) an important cross-cutting component of risk management.

Public participation at all stages of investment cycle increasingly recognized as important for quality, accountability, and risk management.

More attention to generating and reporting diagnostic indicators of PIM system performance.

34

35

36