key changes in fringe benefit tax australia 2016

TRANSCRIPT

FringeBenefitTax

AndrewLam| 22March2016

What’sNew?

TwilightSeminarSeries

TwilightSeminar|FBT- What'snew?|22March2016| 3

KeyChanges

• FBTratetemporarily increased

• Capping thresholdsalsotemporarily increased

• FBTexemption forentertainmentexpensescutto$5,000(separategrossedupcap)from1April2016.Excessentertainmentexpensescanfallintothegeneralcapsifthereisroom

TwilightSeminar|FBT- What'snew?|22March2016| 4

KeyRatesandThresholds

• 49%FBTrate

• 49%FBTrebate(2016and2017FBTyears)

• Capping threshold$17,667(hospitalsandambulance)and$31,177 (PBIandHPC)(2016and2017FBTyears)

• Type1grossuprate– 2.1463(2.0802in2015)

• Type2grossuprate– 1.9608(1.8868in2015)

KeyDates

TwilightSeminar|FBT- What'snew?|22March2016| 5

• EndofFBTyear– 31March2016

• FBTreturnandpaymentdue– 21May2016

• FBTreturndue– 25June2016(iflodgedbytaxagent)

• FBTpaymentduedate– 28May2016(iflodgedbytaxagent)

ImportantConcepts– SalarySacrificing

• Effectivesalarysacrificearrangements(employeeforgoingfutureentitlement)

• Consequencesofineffectivearrangements– subjecttoincometax

• Cansaveemploymenton-costse.g.,nopayrolltaxonFBTexemptandnoFBTtaxablevalues

• Similarsavingsforworkerscompensationbutcheckeachstateandterritory

• Taxsavingscanbemadeevenforemployeesearningbelow$180,000.Askforananalysis

• Documentation/declarations

TwilightSeminar|FBT- What'snew?|22March2016| 6

PotentialComplianceActivity

TwilightSeminar|FBT- What'snew?|22March2016| 7

• LAFHAclaimsforemployees fromoverseas

• LAFHAclaimslimitedto12months

• Useofoutsourcedsalarypackagingproviders andincorrectinformation

• FailuretolodgenilFBTreturns– anoticeofnon-lodgement doesnotstarttheclock

TwilightSeminar|FBT- What'snew?|22March2016| 8

ReportableFringeBenefits

• Wherethetotalvalueofcertainfringebenefitsprovidedperemployeeexceeds$2,000, theemployer isrequired todisclosethegrossed-up taxablevalueontheemployee’spayment summary

• Usetype-2grossup rateof1.9608

TwilightSeminar|FBT- What'snew?|22March2016| 9

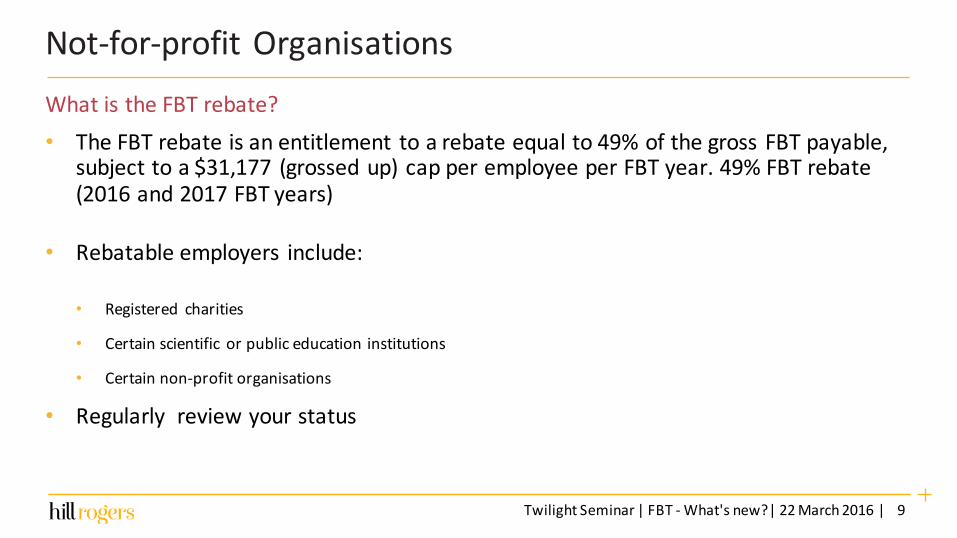

Not-for-profitOrganisations

• TheFBTrebateisanentitlement toarebateequalto49%ofthegrossFBTpayable,subjecttoa$31,177 (grossedup)capperemployeeperFBTyear.49%FBTrebate(2016and2017FBTyears)

• Rebatableemployers include:

• Registered charities

• Certainscientific orpubliceducation institutions

• Certainnon-profitorganisations

• Regularlyreviewyourstatus

WhatistheFBTrebate?

TwilightSeminar|FBT- What'snew?|22March2016| 10

ExamplesofFBTRebateandSalarySacrifice

• Anemployeeofaschoolsalarysacrifices$8,000ofsalaryfor theirchildtoattendtheschool

• ThetaxablevalueofthefeesforFBTpurposes wouldbeasfollows:

TaxableValue $8,000

Grossedupvalue: $8,000 x1.9608 $15,686

FBT: $15,686 x49% $7,686

Less: 49%rebate $(3,766)

FBT Payable $3,920

• $1,000annualreductionabolishedon22October2012

TwilightSeminar|FBT- What'snew?|22March2016| 11

ExamplesofFBTRebateandSalarySacrifice

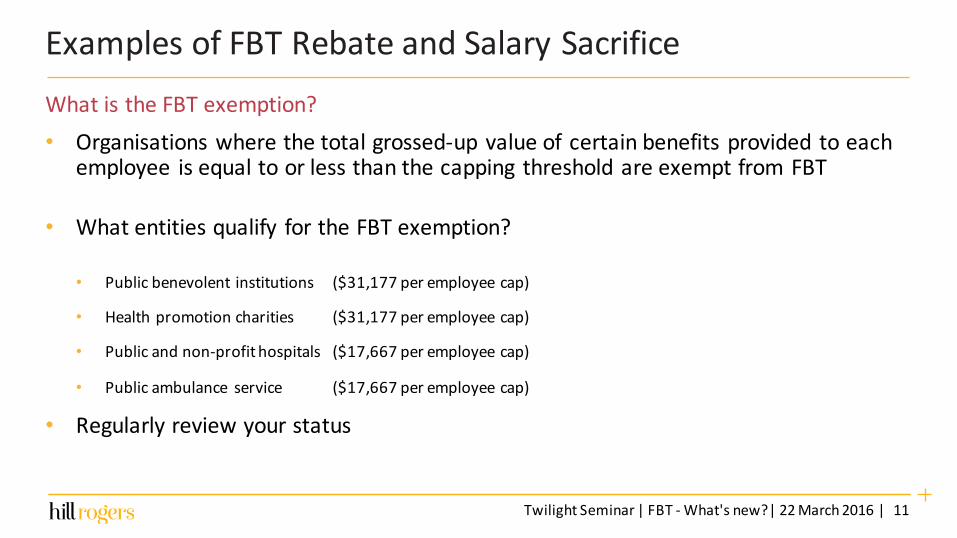

• Organisationswherethetotalgrossed-upvalueofcertainbenefitsprovided toeachemployee isequaltoorlessthanthecapping thresholdareexemptfromFBT

• Whatentitiesqualify fortheFBTexemption?

• Publicbenevolentinstitutions ($31,177peremployeecap)

• Healthpromotioncharities ($31,177peremployeecap)

• Publicandnon-profithospitals ($17,667peremployeecap)

• Publicambulance service ($17,667peremployeecap)

• Regularlyreviewyourstatus

WhatistheFBTexemption?

TwilightSeminar|FBT- What'snew?|22March2016| 12

CommonBenefits

• Cars(statutorymethodoroperatingcostmethod)

• Becarefulwithutilities, panelvansanduteswhenusedforprivatetravelthatisnotminororinfrequent e.g.dropping kidsoffatschool.Policy ofemployerisimportant

• Superannuation contributions (noFBTanddeductible toemployer)

• Exemptbenefits (portableelectronicdevices, toolsoftradeetc.).From1April2016smallbusiness entitieswontbelimitedtooneperyear

• Benefitswithnotaxablevalue, e.g.afterapplication of‘otherwisedeductible rule’

• Minorbenefits ($300)

TwilightSeminar|FBT- What'snew?|22March2016| 13

CommonBenefits

• Mealentertainmentü Restaurantü ChristmasPartyü ClientEntertaining

x Sustenancex Lightmealsx WorkingLunchx Mealswhilsttravelling

• LAFHAalternative• Exemptrelocation

• Removalandstoragecosts

• Incidental costsofsale

• Incidental costsofacquiringnewresidence

• Connectingutilities

• Reasonableaccommodation expenses6– 12months

Questions?

TwilightSeminar|FBT- What'snew?|22March2016|14

Aboutthespeaker

TwilightSeminar|FBT- What'snew?|22March2016| 15

Andrew is both a chartered tax adviser and a solicitor having worked with leading taxationadvisory teams in chartered accounting firms (both big 4 and mid-tier) and a top tier law firm.

Andrew’s expertise lies in

• providing tax advice

• leading tax due diligence assignments

• general tax planning and

• providing tax compliance services.

His clients include family groups, private and public companies (including listed entities) and notfor profit groups.

AndrewLam- Director,BCom,LLM,CTA

Services:Taxation, LargeCorporate,CorporateAdvisory,Not-For-Profit

t:+61292325111d:+61292200381e:[email protected]:www.hillrogers.com.au

t+61292325111 f+61292337950www.hillrogers.com.au| [email protected]

Level5,1ChifleySquare,SydneyNSW2000 AustraliaGPOBox7066,SydneyNSW2001

H.R.P.HPtyLimitedpractisingasHillRogers|ABN12003718 518MemberofMorsion KSi,anassociationofglobal independentaccountingfirms.Liability limitedbyaschemeapprovedunderProfessional StandardsLegislation.

Thankyou