key developments and outlook

TRANSCRIPT

1

• Risks to GDP growth and inflation forecast are assessed to be skewed downward, in line with the risks to trading partners’ economies including the impact of Brexit.

• Headline inflation projection remains close to the previous assessment, and is expected to return to the inflation target’s lower bound in H2/16. While, core inflation forecast is revised downward marginally for 2017 in line with slower growth.

• Monetary policy remains conductive to the economic recovery, while preserves the financial stability.

Key developments and outlook

• Thailand’s economic growth projection for 2016 remains close to the previous assessment.Domestic demand and tourism help counteract the revised down merchandise exports, which is owing to weaker trading partners’ growth and structural constraints. Meanwhile, growth projection for 2017 is revised down slightly due to weaker merchandise exports.

2

*Outturn, ( ) March 2016 Monetary Policy Report

2015* 2016 2017

GDP Growth 2.8 3.1 3.2

(3.1) (3.3)

Headline Inflation -0.9 0.6 2.2

(0.6) (2.2)

Core Inflation 1.1 0.8 1.0

(0.8) (1.1)

Forecast Summary as of June 2016

Global economy is to recover at a slower pace than expected, especially Asian economies.

Monetary policy continues to be accommodative in many countries.

3

Asian economies are likely to grow slower due to more pronounced impact from regional trade structural shifting.

US economic growth tends to decelerate following lower-than-expected consumption in Q1/16.

Monetary policy is accommodative longer than expected.

Japan economy in 2017 is likely to expand higher than expected as the sale tax hike is postponed to 2019 (from initially scheduled for 2017).

BOJ continues to conduct accommodative monetary policy

through negative interestrate and QQE.

China economycontinues to slow down as expected.

More downside risks come from financial sector risks.

Euro area is to recover gradually after the terror attacks.

Brexit would be one of the significant risks going forward.

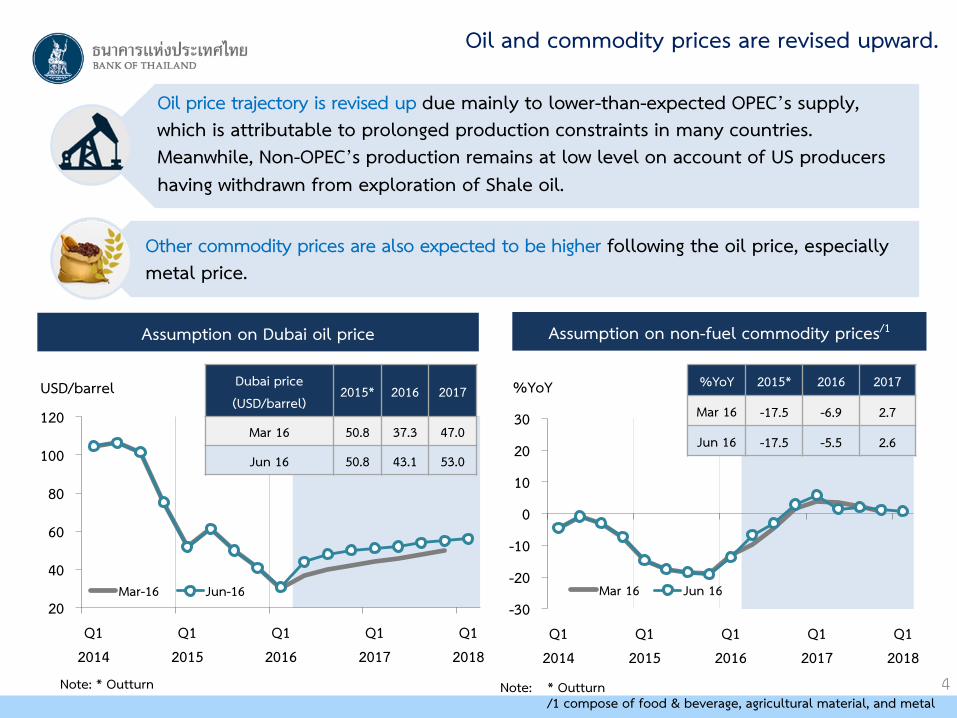

Oil and commodity prices are revised upward.

%YoY

-30

-20

-10

0

10

20

30

Q12014

Q12015

Q12016

Q12017

Q12018

Mar 16 Jun 1620

40

60

80

100

120

Q12014

Q12015

Q12016

Q12017

Q12018

Mar-16 Jun-16

Note: * Outturn

Assumption on Dubai oil price

Dubai price(USD/barrel)

2015* 2016 2017

Mar 16 50.8 37.3 47.0

Jun 16 50.8 43.1 53.0

USD/barrel

Assumption on non-fuel commodity prices/1

%YoY 2015* 2016 2017

Mar 16 -17.5 -6.9 2.7

Jun 16 -17.5 -5.5 2.6

Note: * Outturn/1 compose of food & beverage, agricultural material, and metal

4

Oil price trajectory is revised up due mainly to lower-than-expected OPEC’s supply, which is attributable to prolonged production constraints in many countries. Meanwhile, Non-OPEC’s production remains at low level on account of US producers having withdrawn from exploration of Shale oil.

Other commodity prices are also expected to be higher following the oil price, especially metal price.

5

Asia’s merchandise exports by country (USD term)

%YoY 2015* 2016 2017

As of Mar 16-5.6

-2.0 0.1

As of Jun 16 -2.5 0.0

Projection of merchandise exports value (USD)

• Thai exports face both internal and external structural constraints.- Global trade volume declines continuously due to lower

import dependence in many countries.

- Thailand’s competitiveness in some sectors would take time to improve.

• Slower-than-expected growth of trading partners’ economies

• Export prices are higher following the commodity prices, though the price cannot compensate a declined export quantity.

*Outturn

Index, 3mma sa (Jan 2013=100)

Source : CEICNote : Singapore and Indonesia export value excluded oil

70

80

90

100

110

120

130

Jan2013

Jul Jan2014

Aug Jan2015

Sep Jan2016

CNTH_Exgold

PH

SGMY

ID

TW

May 16

KR

Thai merchandise exports are projected to recover at a slower pace than previously forecasted due to softer trading partners’ economies

and more pronounced shifting global trade structure.

50

100

150

200

250

300

Jan2013

Jul Jan2014

Aug Jan2015

Sep Jan2016

China (27%)Asia excl. China and Malaysia(29%)Europe excl. Russia (16%)Malaysia (12%)Russia (3%)

Tourism has risen more than expected and tends to continue to expand.

Projection of foreign tourist arrivals

6

*Outturn

Million 2015* 2016 2017

As of Mar 1629.8

32.4 34.4

As of Jun 16 34.0 36.7

Number of tourists by origin

The number of Chinese tourists has grown markedly. While, the tourists from other countries showed sign of recovery, especially European and Russia.

Route expansion of low cost airlines is the essential support for Thai tourism.

May 16

Index, 3mma sa (Jan 2013=100)

Note: ( ) Share of tourists in 2015Source: Department of Tourism

29.420.6

30.0 27.7

73.3

49.4

78.8

0

20

40

60

80

100 Remaining Purchase OrderCumulative DisbursementCumulative Purchase Order

Public sector continues to support the economy through investment spending and additional stimulus measures.

7

- Government’s purchase order and disbursement are well on track.

- SOE’s investment remains close to previously forecasted, despite a slight delay of double track railway (Prachuap Khiri Khan-Chumphon) project.

note: *low cost housing scheme (Pracha Rat project) and personal income tax reform

Billion Baht

20152016 2017

Mar 16 Jun 16 ∆ Mar 16 Jun 16 ∆

Consumption 2,334 2,476 2,482 6 2,633 2,637 5

Investment 864 958 955 -3 1,034 1,035 1

Total 3,199 3,434 3,437 3 3,667 3,673 6

Central Government’s obligated contract and disbursement

Projection of public spending, at current prices (calendar year)

Public investment remains close to the previous assessment.

Additional stimulus measures* provide support to domestic expenditure

Note: Excluding transfers to local government and revolving fund Source: Comptroller General’s Department

%

Cumulative Purchase Order in May

FY 2015FY 2014FY 2013 FY 2016FY 2012

70

80

90

100

110

Jan2013

Jul Jan2014

Aug Jan2015

Sep Jan2016

Construction material salesImported capital goods quantity index

Private investment indicators in construction and machinery and equipment

Private spending is likely to grow better than expected.

8

Private consumption is expected to grow at a rate close to the previous forecast thanks to: (1) increased income from the service sector that helps compensate for lower income from the manufacturing sector, (2) improved confidence of households in the agricultural sector, thanks to higher farm prices and reduced concerns regarding the drought due to increased rainfall.

Private investment is expected to grow better than previously anticipated, especially construction related to government projects that grew significantly in Q1/16. Meanwhile, investment in machinery and equipment is projected to remain low due to weak merchandise exports

70

80

90

100

110

120

Jan2013

Jul Jan2014

Aug Jan2015

Sep Jan2016

Real farm income

Real non farm income

Real households’ income

Index, 3mma sa (Jan 2013=100)

May 1686.5

May 16105.9

Source: Office of Agricultural Economics, and calculated by BOT Source : MOC and OIE

May 1681.5

May 16100.3

Index, 3mma sa (Jan 2013=100)

%YoY 2015*2016 2017

Mar 16 Jun 16 Mar 16 Jun 16

Economic Growth 2.8 3.1 3.1 3.3 3.2

- Private Consumption 2.1 1.8 1.8 2.4 2.1

- Private Investment -2.0 2.4 3.1 4.0 2.3

- Government Consumption 2.2 3.3 3.5 2.8 2.8

- Public Investment 29.8 10.7 10.1 4.5 5.2

- Exports of Goods and Services 0.2 1.0 2.2 1.7 0.9

- Imports of Goods and Services -0.4 0.6 -1.9 1.5 2.4

Economic growth projection for 2016 remains close to the previous assessment; however, growth projection for 2017 is revised down slightly due to weaker merchandise exports.

9

Note : *Outturn

Note: The fan chart covers 90% of the probability distribution

GDP growth forecast

10

Risks to growth remain skewed downward.

Annual percentage change

• Downside risks (before Brexit referendum)– A slower growth of trading partners’ economies

due to remaining risks in Chinese financial sector – The impact of Brexit– Fragile confidence of the private sector, which

could affect private spending more than assessed

– Domestic political uncertainty, which could weigh on public spending and tourist arrivals

• Upside risks– Higher-than-expected public spending and

greater-than-expected effects of stimulus measures

– A better-than-expected number of foreign tourists

-4

0

4

8

12

-4

0

4

8

12

Q1 2014 Q1 2015 Q1 2016 Q1 2017 Q1 2018Q12014

Q12015

Q12016

Q12017

Q12018

-3

-2

-1

0

1

2

3

Jan2015

Jul Jan2016

Raw food (15.5%) Electricity fees (3.4%)

Enery price, excl. Electricity (8.0%) Core Infaltion (73.1%)

Headline Infaltion

• Demand-pull inflationary pressure is assessed to be slightly lower than previously forecasted in line with the slower economic growth projection in 2017.

• Inflationary pressure from the cost side is assessed to rise as crude oil and commodity prices increase. However, part of the cost-push pressure is offset by lower electricity fees due to lower costs of electricity purchases from the private sector.

• Headline inflation is expected to rise gradually and return to the inflation target’s lower bound in H2/16.

Projection of core inflation is revised down marginally in 2017, while projection of headline inflation remains close to previously anticipated.

11

2015* 2016 2017

Headline inflation (%YoY) -0.9 0.6 2.2

(0.6) (2.2)

Core inflation (%YoY) 1.1 0.8 1.0

(0.8) (1.1)

Inflation forecastsHeadline inflation contribution

Source: Ministry of commerce calculated by BOT

%YoY

May 16

*Outturn( ) March 2016 Monetary Policy Report

Note: The fan chart covers 90% of the probability distribution

Headline inflation forecast

Annual percentage change

Core inflation forecast

12

Annual percentage change

Risks to inflation forecasts are skewed downwards in tandem with the risks to economic growth.

-2

-1

0

1

2

3

4

-2

-1

0

1

2

3

4

Q1 2014 Q1 2015 Q1 2016 Q1 2017 Q1 2018Q12014

Q12015

Q12016

Q12017

Q12018

Q12014

Q12015

Q12016

Q12017

Q12018

-4

-2

0

2

4

6

8

-4

-2

0

2

4

6

8

Headline inflation target (2.5 + 1.5)

Monetary policy remains conducive to the economic recovery.

13

On May 11 and June 22, 2016, the MPC voted unanimously to maintain the policy rate at 1.50 percent

The committee viewed that monetary policy should remain accommodative. The MPC stands ready to utilize an appropriate mix of available policy tools to provide support to the economic recovery,

while ensuring financial stability.

(1) Economic and inflation projections do not change significantly from the previous assessment.

(2) Monetary conditions, both interest rate and exchange rate, were judged to be accommodative and conducive to economic recovery. While, headline inflation is expected to return to the inflation target’s lower bound in H2/16.

The MPC saw merit in preserving the policy space given risk factors going forwardand also monitored risks to financial stability from search-for-yield behavior.

Key issues monitored by the MPC (before Brexit referendum)

14

(1) Risks to global economic recovery, particularly from China given its domestic financial sector risks and Brexit referendum that could increase the global financial market volatility.

(2) Monetary policy divergence among advanced economies that could impact capital flows.

(3) Shifting global trade structure that could affect export performance of Thailand and Asia.

(4) The risk to financial stability from search-for-yield behavior under a prolonged period of low interest rates.

2015* 2016 2017

GDP Growth 2.8 3.1 3.2

(3.1) (3.3)

Headline Inflation -0.9 0.6 2.2

(0.6) (2.2)

Core Inflation 1.1 0.8 1.0

(0.8) (1.1)

Forecast Summary as of June 2016

*Outturn( ) March 2016 Monetary Policy Report

15

16

Website

https://www.bot.or.th/English/MonetaryPolicy/MonetPolicyComittee/MPR/Pages/default.aspx

(%YoY) 2015* 2016E 2017E

GDP Growth 2.8 3.1 3.2

- Private Consumption 2.1 1.8 2.1

- Private Investment -2.0 3.1 2.3

- Government Consumption 2.2 3.5 2.8

- Public Investment 29.8 10.1 5.2

- Exports of Goods and Services 0.2 2.2 0.9

- Imports of Goods and Services -0.4 -1.9 2.4

Current Account Balance (Billion USD) 32.0 37.8 32.3

- Value of Merchandise Exports -5.6 -2.5 0.0

- Value of Merchandise Imports -11.3 -6.0 5.3

Forecasts in Monetary Policy Report as of June 2016

Attachment

Note: E = projection* Outturn

17

2015*2016 2017

Mar 16 Jun 16 Mar 16 Jun 16

Dubai oil price (USD per barrel) 50.8 37.3 43.1 47.0 53.0

Non-fuel commodity prices (%yoy) -17.5 -6.9 -5.5 2.7 2.6

Fresh food prices (%yoy) -4.4 3.0 3.0 4.0 3.7

Public expenditure (calendar year)

Government Consumption (billion baht)1/ 2,334 2,476 2,482 2,633 2,637

Public investment (billion baht)1/ 864 958 955 1,034 1,035

Fed funds rate (% year end) 0.38 0.88 0.63 1.63 1.38

Trading partners’ GDP growth (%yoy) 3.2 3.1 3.0 3.3 3.3Regional currencies per USD (excl RMB)** 150.7 160.6 154.4 161.4 157.2

18

Attachment

Forecast Assumptions

Note: * Outturn** Higher values indicate currency depreciation against the US dollar1/ Including spending on the Water Management and Infrastructure Investment plans

(% YoY)Weight

(%)2015*

2016 2017

Mar 16 Jun 16 Mar 16 Jun 16

US 14.9 2.4 2.2 1.9 2.4 2.3

Euro area 10.0 1.6 1.4 1.7 1.6 1.6

Japan 13.6 0.6 0.8 0.6 0.4 1.0

China 15.7 6.9 6.5 6.5 6.4 6.4

Asia** 37.4 3.5 3.5 3.2 3.9 3.7

Total*** 100 3.2 3.1 3.0 3.3 3.3

Assumption on trading partners’ GDP growth

19

Attachment

Note: * Outturn** Weighted by export shares of Thailand’s major trading partners in 2014 (7 Asian countries including Singapore (6.5%),

Hong Kong (7.9%), Malaysia (8.0%), Taiwan (2.5%), Indonesia (5.9%), South Korea (2.8%), and Philippines (3.7%))*** Weighted by export shares of Thailand’s major trading partners in 2014 (13 countries)