key financial metrics and ratios - north carolina world

TRANSCRIPT

1

Export Department Management

Key Financial Metrics and Ratios

NASBITE Annual Conference, Savannah, Georgia, April 10-11, 2019

2

Financial metrics and ratios

The common language of business

Guide managerial actions byproviding targets and standards

Enable comparisons of performance

Alert management to issues thatrequire immediate attention

3

Financial metrics

Quantify business performance

Obtained from financial statements

Example: sales revenues, profits, costs,assets, liabilities, etc.

Metrics do not tell the whole story andcan be misleading:o Rising sales but declining profitso Profits but lack of liquidity

SALES

PROFIT

4

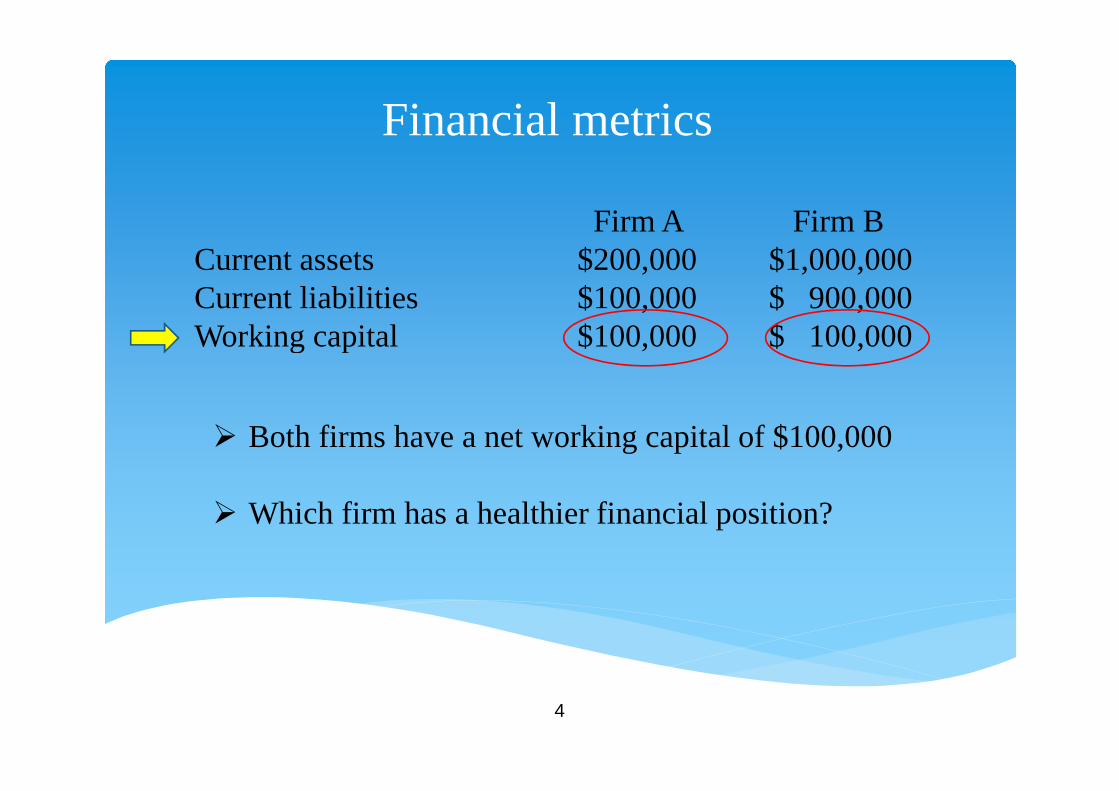

Financial metrics

Firm A Firm BCurrent assets $200,000 $1,000,000Current liabilities $100,000 $ 900,000Working capital $100,000 $ 100,000

Both firms have a net working capital of $100,000

Which firm has a healthier financial position?

5

Financial metrics

Profit is the bottom line of any businessactivity

No other goals can be achieved withoutprofits

Looking at profits is not sufficient toevaluate performance – Is $100,000 inprofits a good performance?

Management must understand theunderlying drivers

6

Financial ratios

Express the relationship between twoselected metrics

Allow relative comparisons of financialmetrics and offer greater insights

Give insights into profitability, efficiency,liquidity and solvency

A critical tool for financial analysis andmanagerial decision making

7

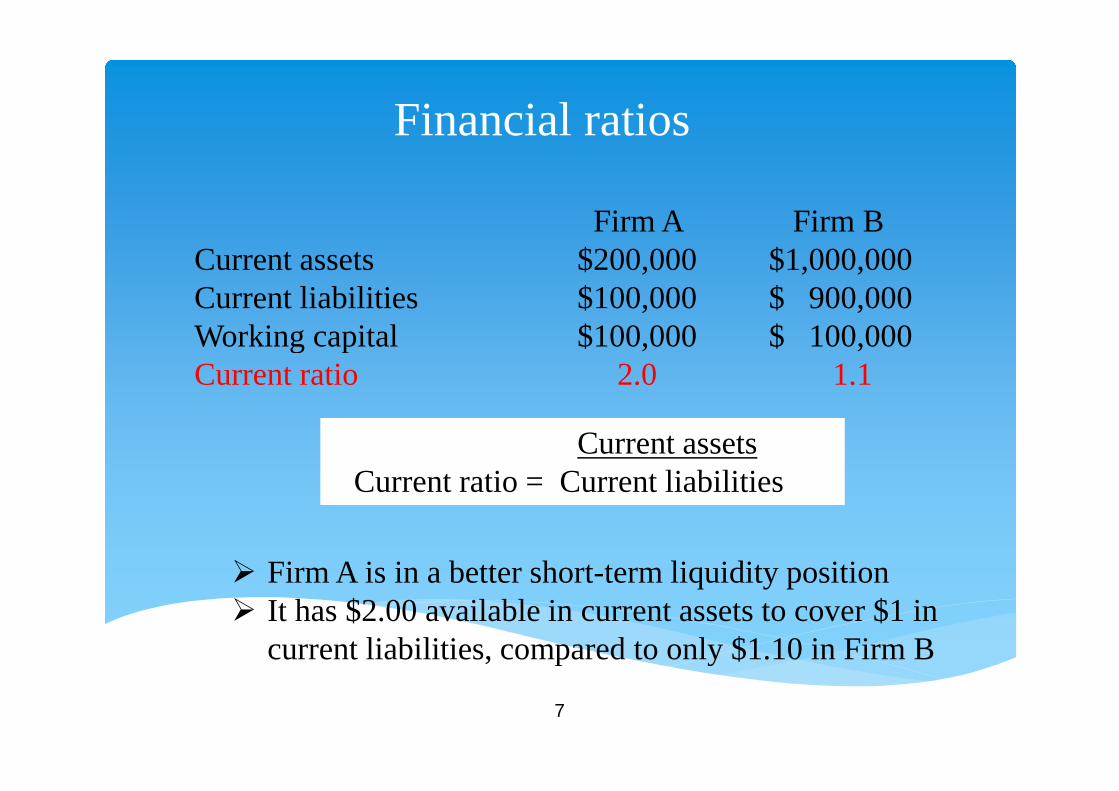

Financial ratios

Firm A Firm BCurrent assets $200,000 $1,000,000Current liabilities $100,000 $ 900,000Working capital $100,000 $ 100,000Current ratio 2.0 1.1

Current assetsCurrent ratio = Current liabilities

Firm A is in a better short-term liquidity position It has $2.00 available in current assets to cover $1 in

current liabilities, compared to only $1.10 in Firm B

8

Return on equity

The ultimate financial ratio

Reflects the earnings power of the business

Indicator of the overall businessperformance – how efficiently the businessmanages all of its resources

9

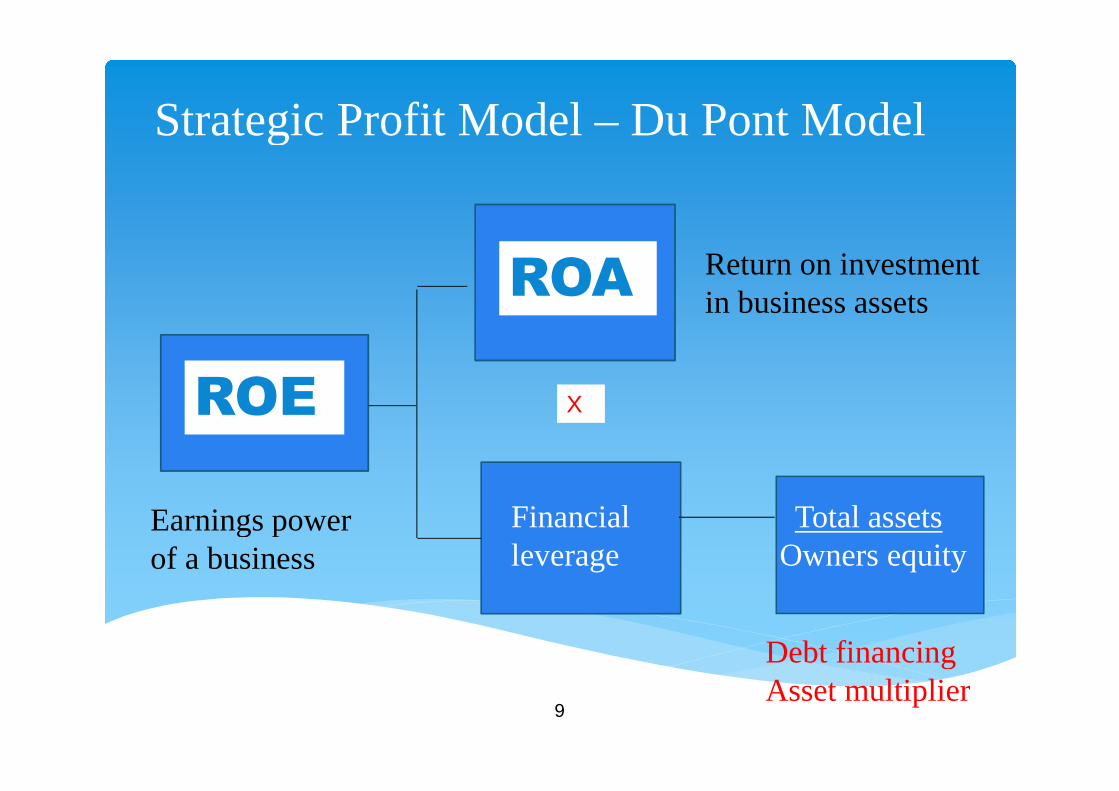

Strategic Profit Model – Du Pont Model

Financialleverage

X

Total assetsOwners equity

Debt financingAsset multiplier

Earnings powerof a business

Return on investmentin business assets

ROA

ROE

10

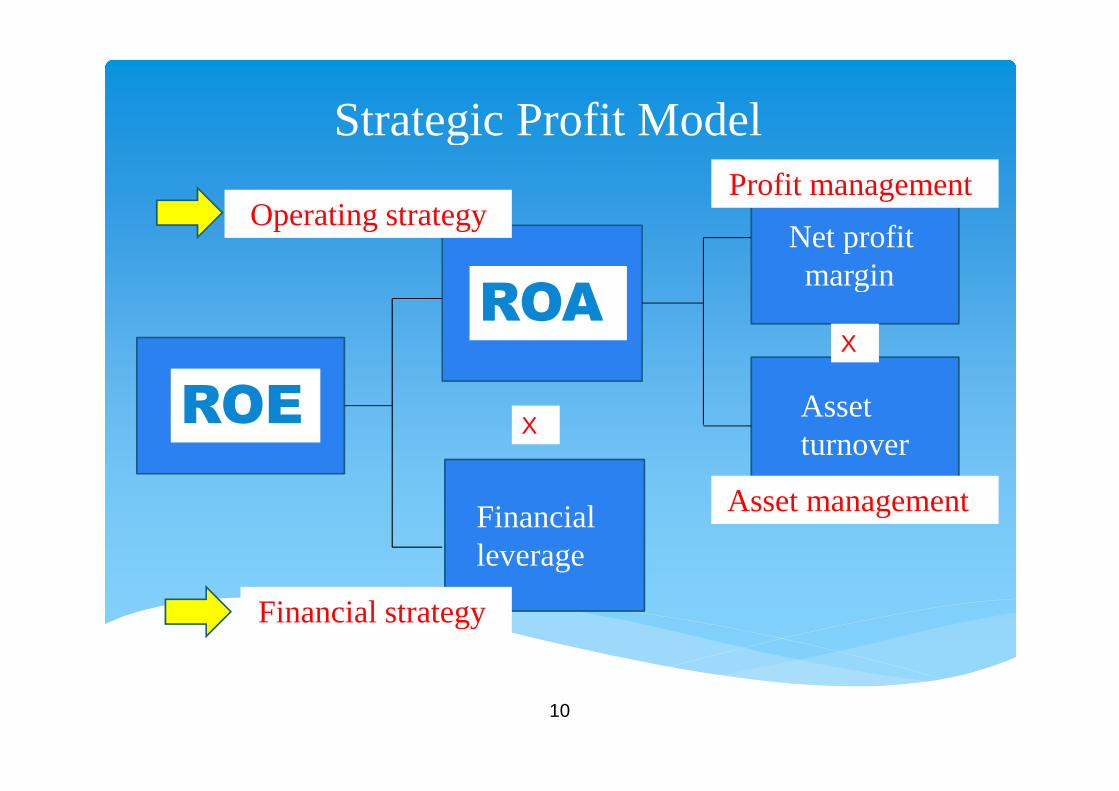

Strategic Profit Model

Financialleverage

Assetturnover

Net profitmargin

Profit management

Asset management

X

X

Financial strategy

Operating strategy

ROE

ROA

11

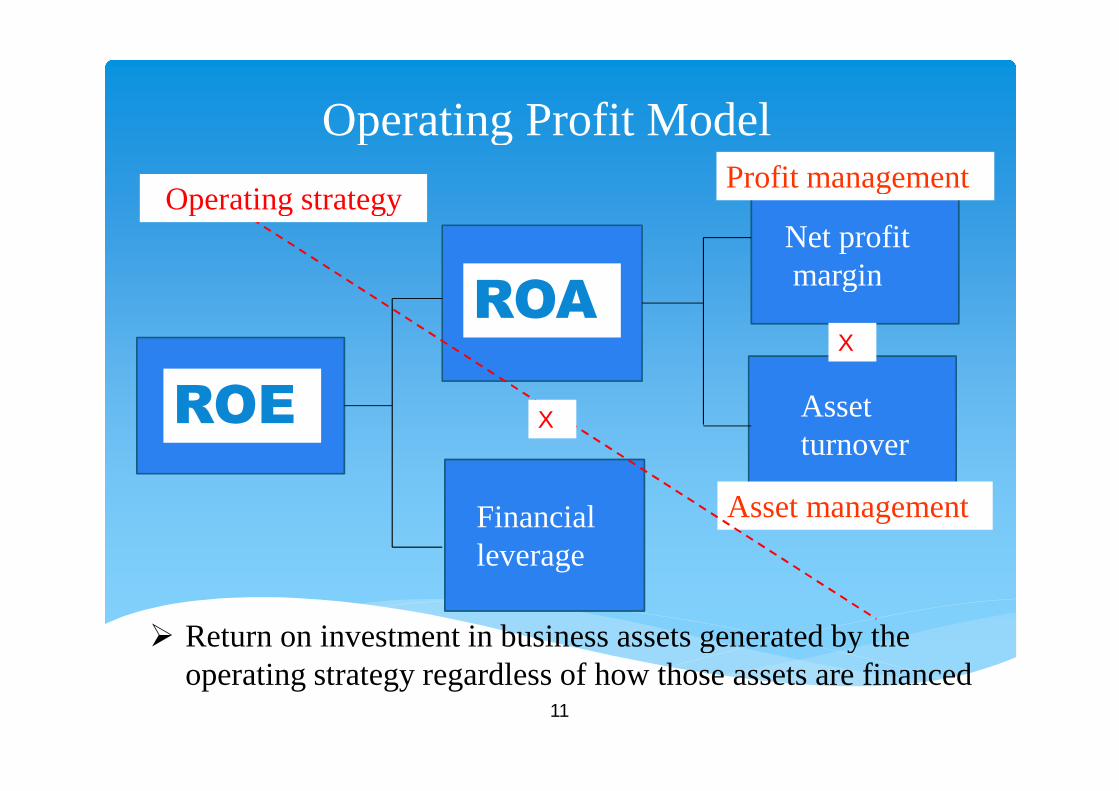

Operating Profit Model

Financialleverage

Assetturnover

Net profitmargin

Profit management

Asset management

X

X

Operating strategy

Return on investment in business assets generated by theoperating strategy regardless of how those assets are financed

ROE

ROA

12

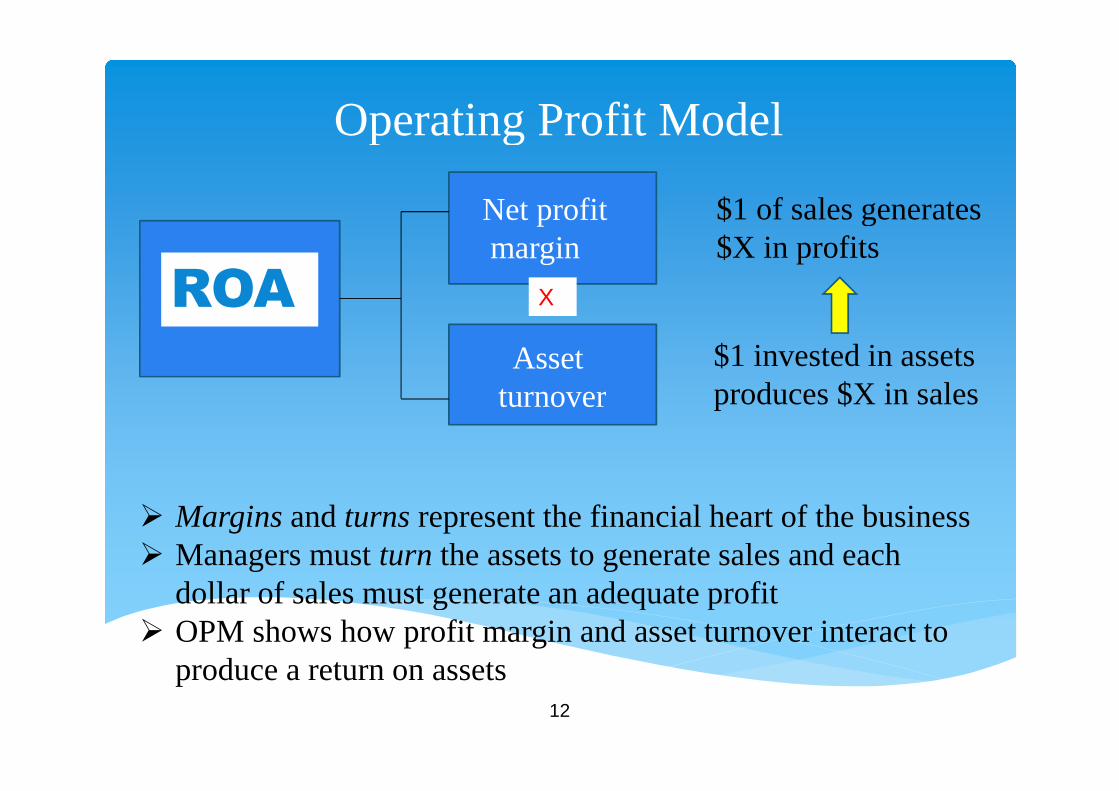

Operating Profit Model

Assetturnover

Net profitmargin

X

Margins and turns represent the financial heart of the business Managers must turn the assets to generate sales and each

dollar of sales must generate an adequate profit OPM shows how profit margin and asset turnover interact to

produce a return on assets

$1 invested in assetsproduces $X in sales

$1 of sales generates$X in profits

ROA

13

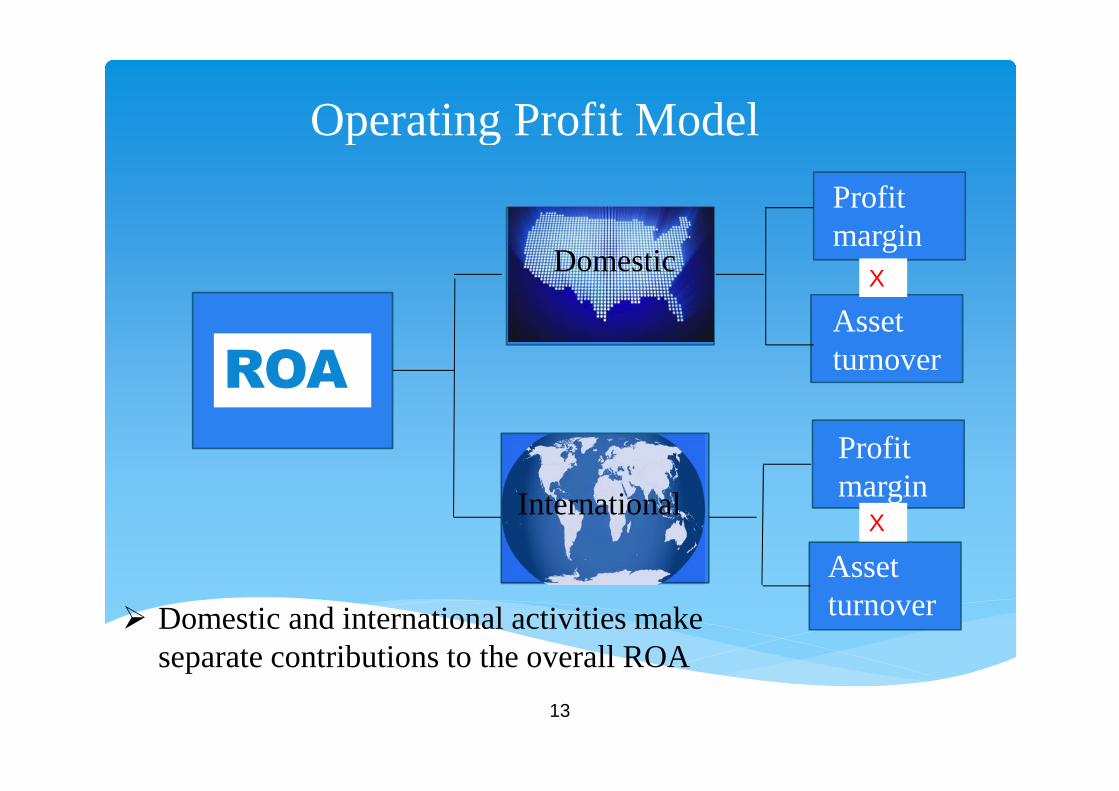

Operating Profit Model

Domestic

International

Profitmargin

Profitmargin

Assetturnover

Assetturnover

X

X

Domestic and international activities makeseparate contributions to the overall ROA

ROA

14

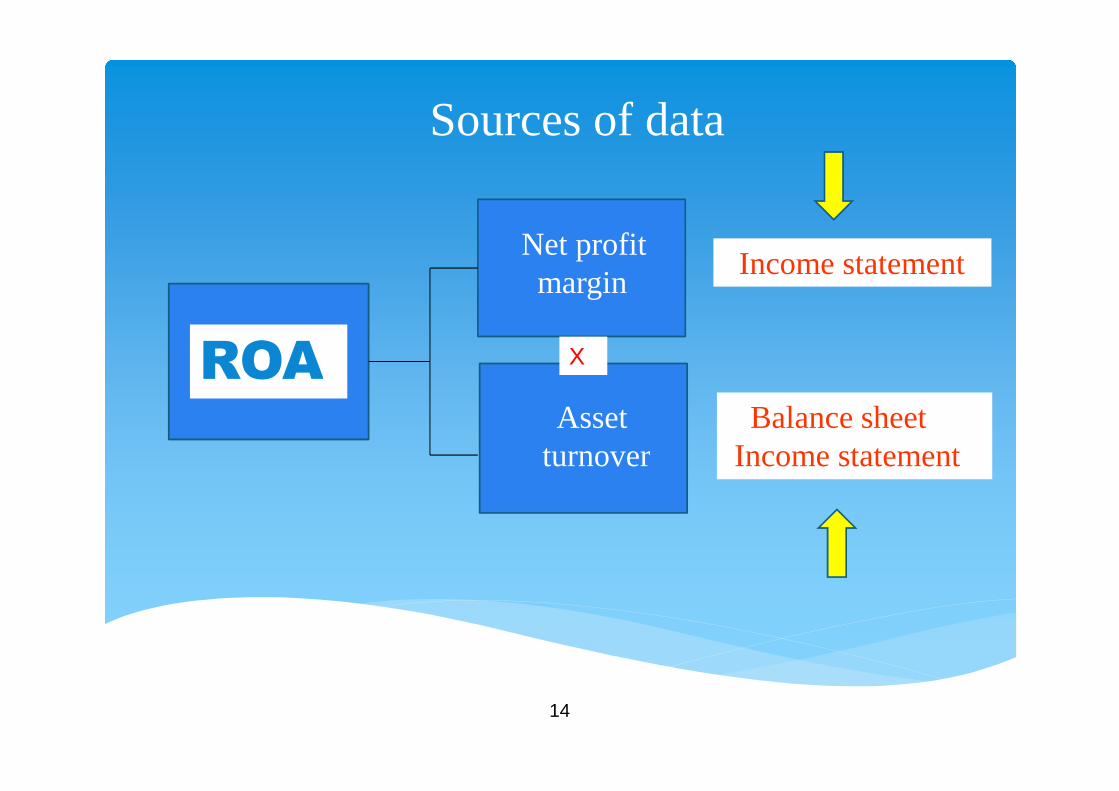

Sources of data

Assetturnover

Net profitmargin

Income statement

Balance sheetIncome statement

XROA

15

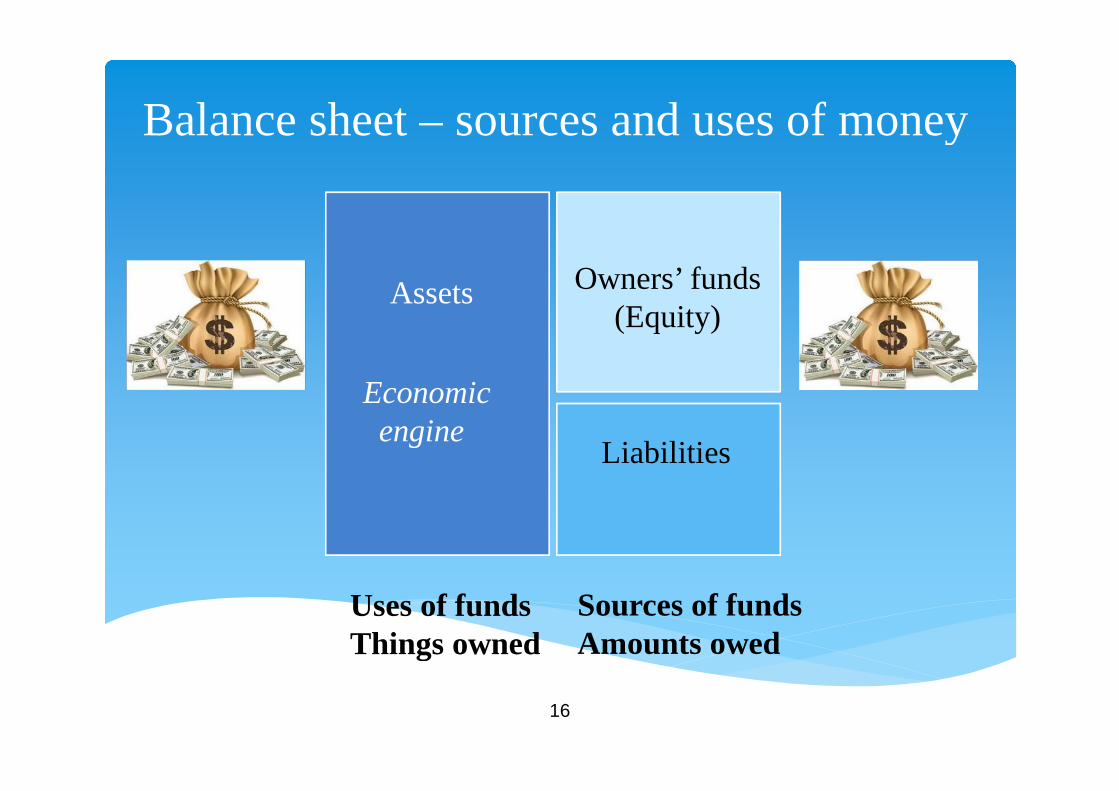

Balance sheet

Presents all the assets, liabilities and shareholders’ funds ata given point in time

16

Balance sheet – sources and uses of money

Assets Owners’ funds(Equity)

Liabilities

Sources of fundsAmounts owed

Uses of fundsThings owned

Economicengine

17

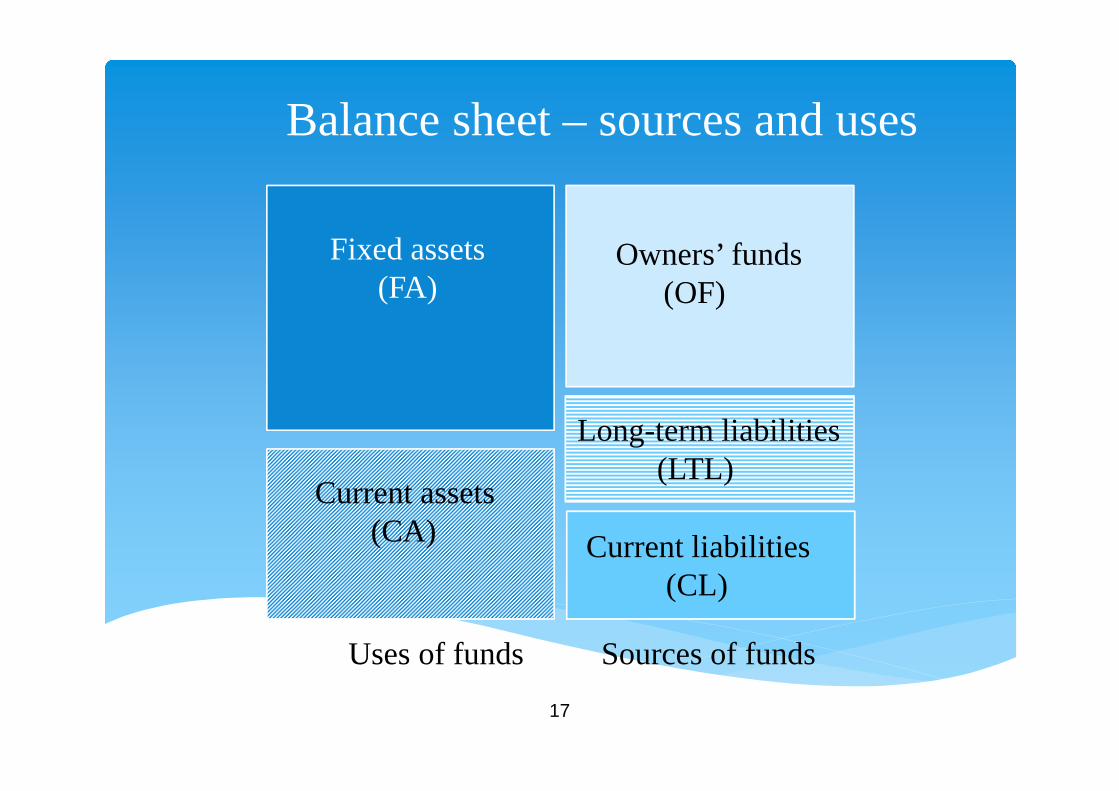

Balance sheet – sources and uses

Fixed assets(FA)

Owners’ funds(OF)

Long-term liabilities(LTL)

Sources of fundsUses of funds

Current liabilities(CL)

Current assets(CA)

18

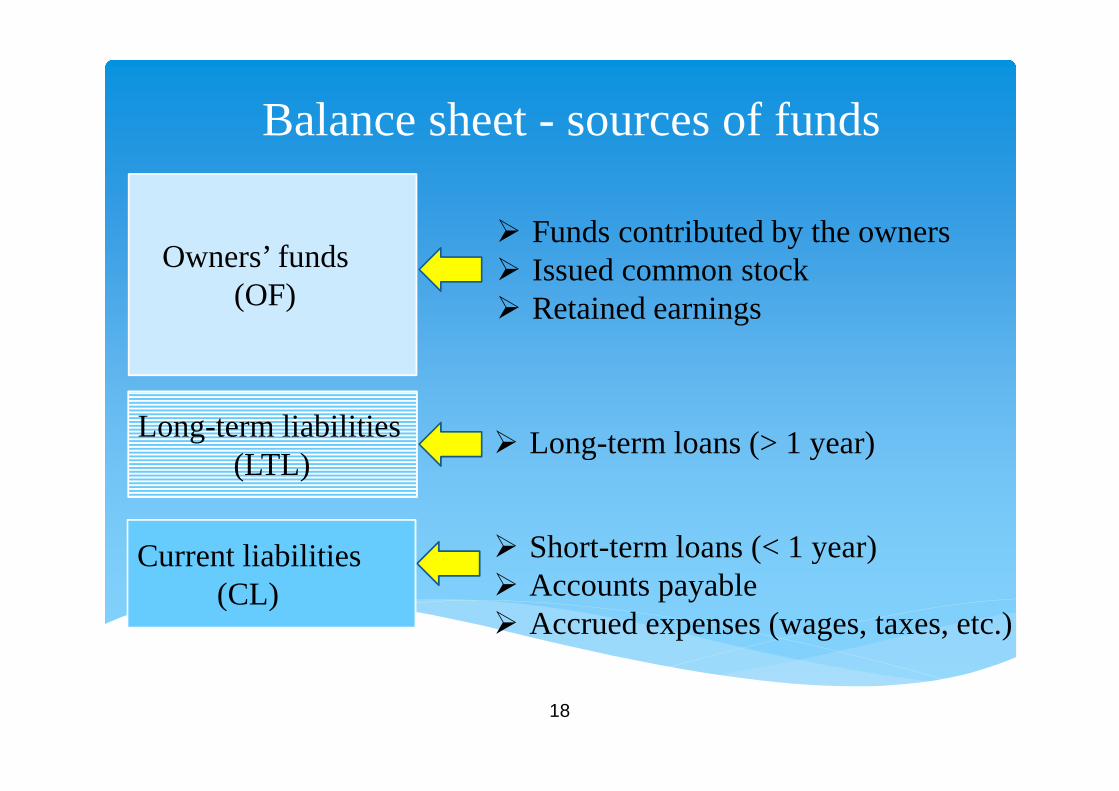

Balance sheet - sources of funds

Funds contributed by the owners Issued common stock Retained earnings

Long-term loans (> 1 year)

Short-term loans (< 1 year) Accounts payable Accrued expenses (wages, taxes, etc.)

Owners’ funds(OF)

Long-term liabilities(LTL)

Current liabilities(CL)

19

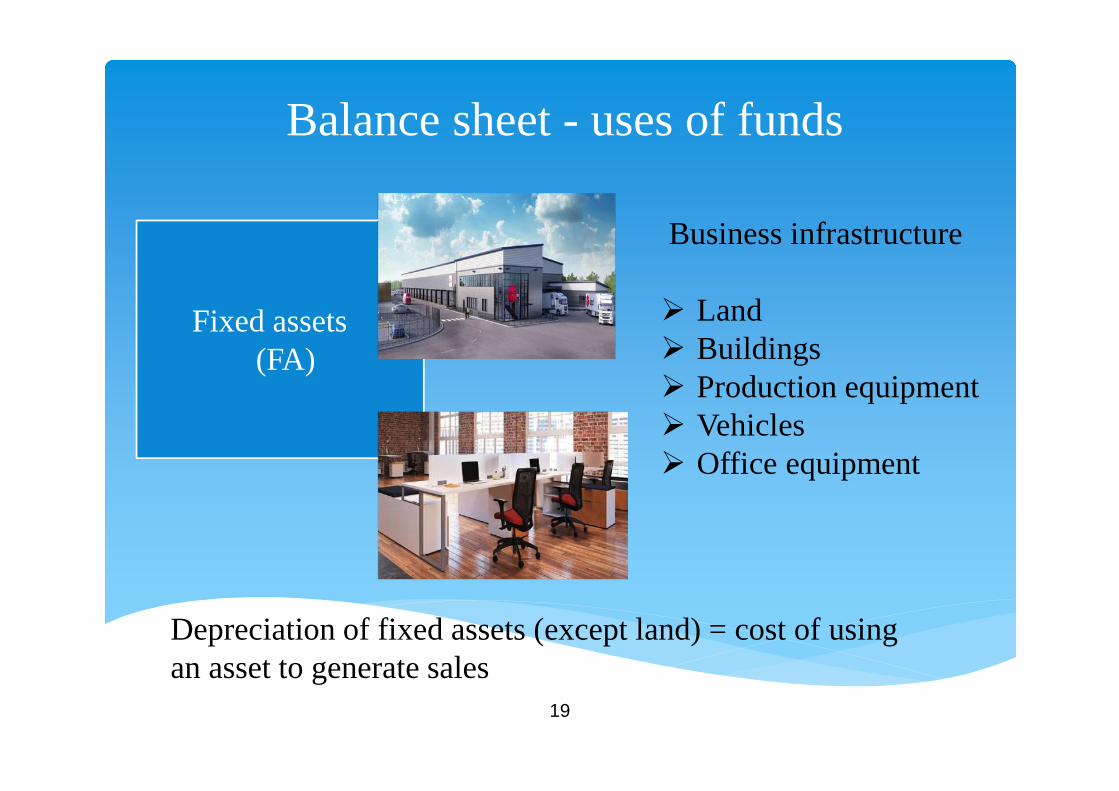

Balance sheet - uses of funds

Fixed assets(FA)

Business infrastructure

Land Buildings Production equipment Vehicles Office equipment

Depreciation of fixed assets (except land) = cost of usingan asset to generate sales

20

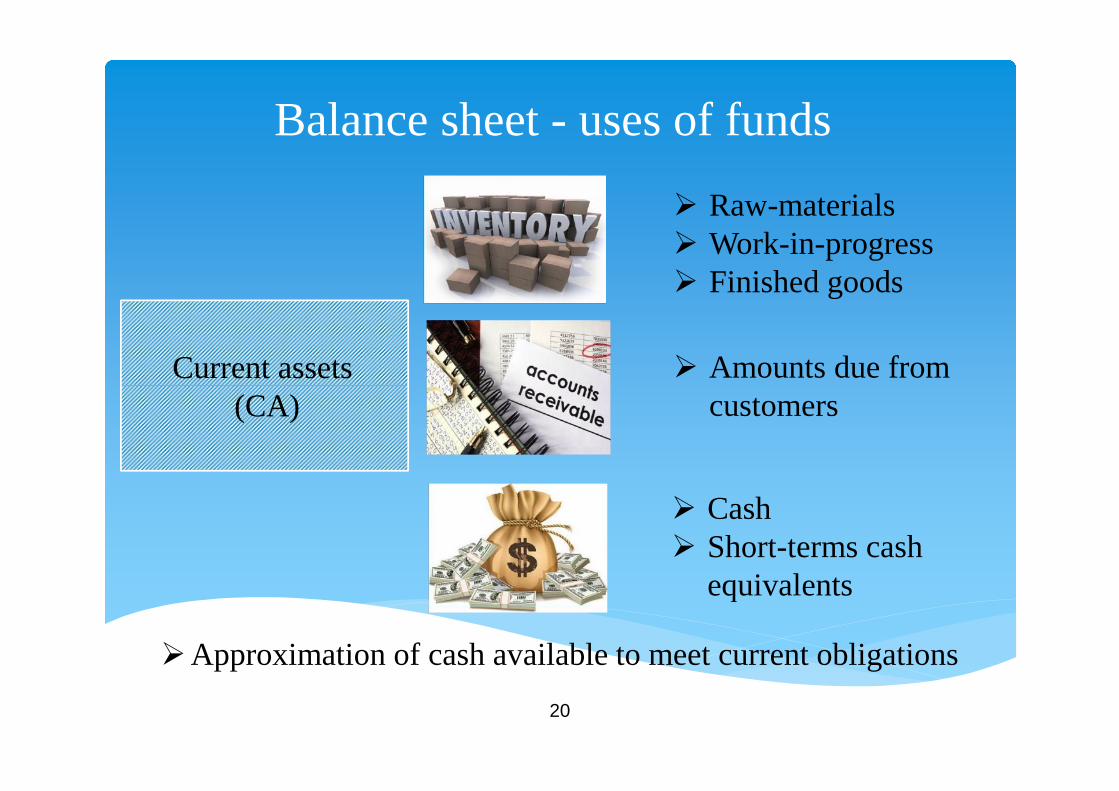

Balance sheet - uses of funds

Current assets(CA)

Raw-materials Work-in-progress Finished goods

Amounts due fromcustomers

Cash Short-terms cash

equivalents

Approximation of cash available to meet current obligations

21

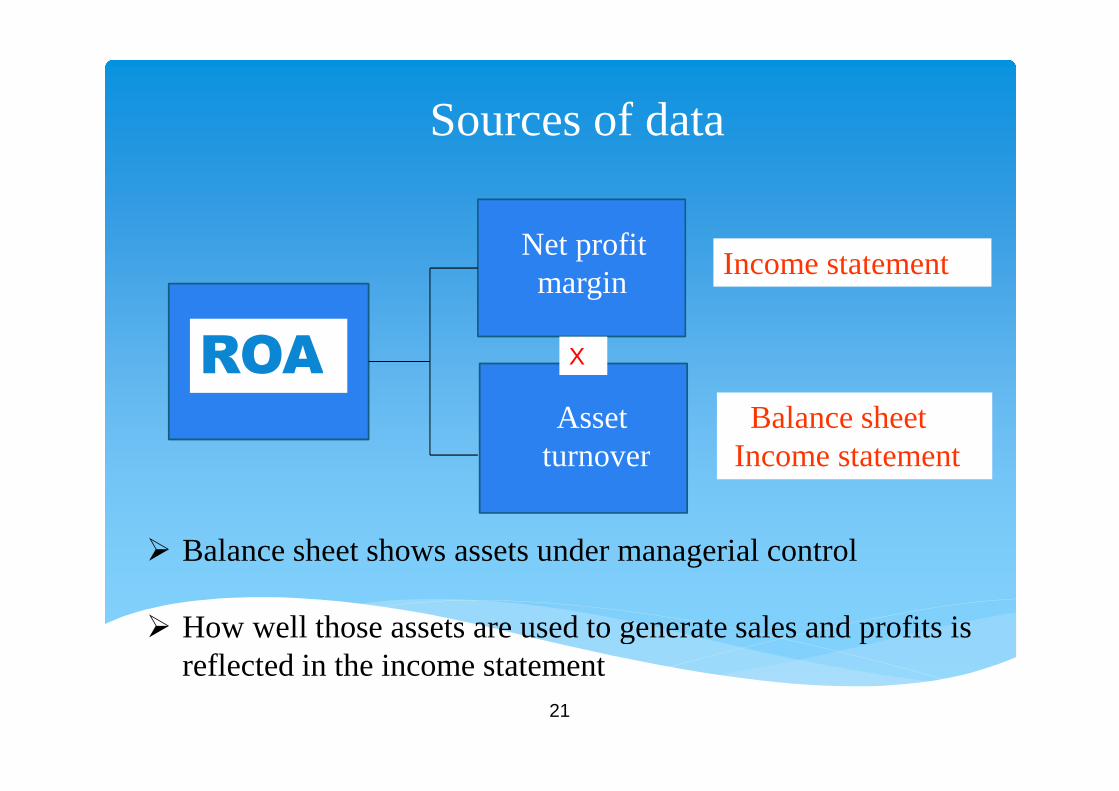

Sources of data

Assetturnover

Net profitmargin

Income statement

Balance sheetIncome statement

X

Balance sheet shows assets under managerial control

How well those assets are used to generate sales and profits isreflected in the income statement

ROA

22

Income statement

Matches the sales revenues and expenses for a given period Sales and profits can be compared to the asset base to

evaluate performance, reflected in the ROA

23

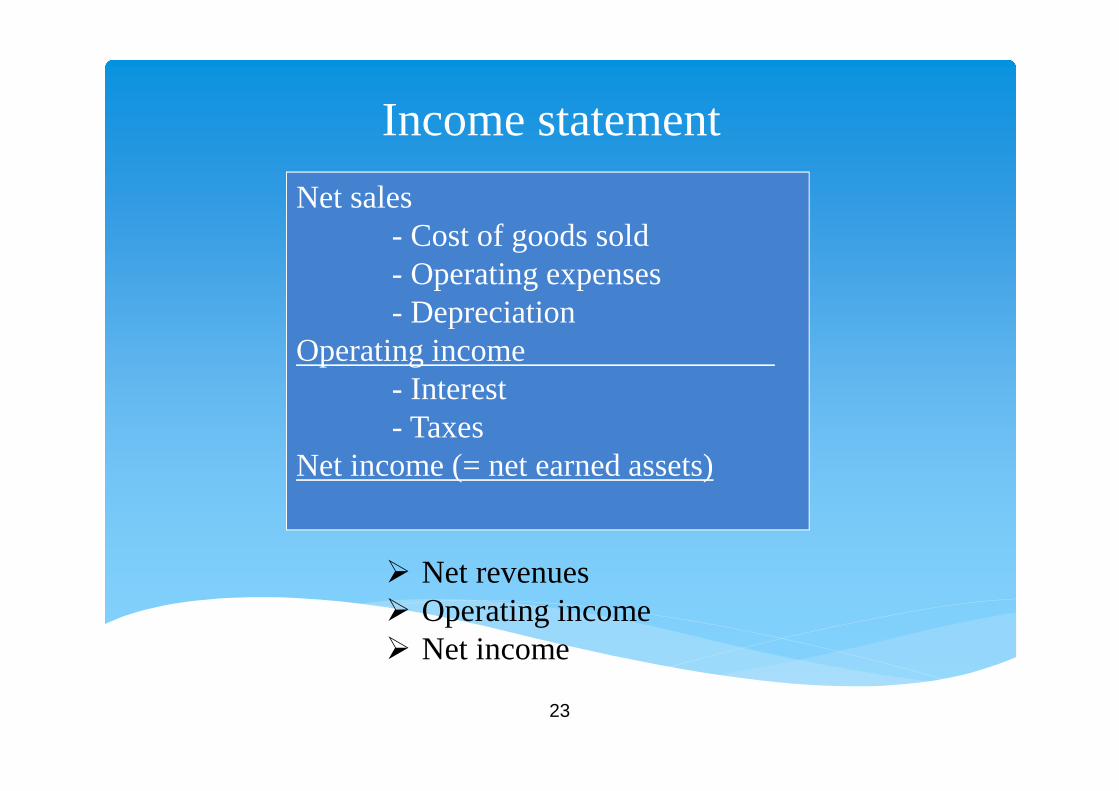

Income statement

Net sales- Cost of goods sold- Operating expenses- Depreciation

Operating income- Interest- Taxes

Net income (= net earned assets)

Net revenues Operating income Net income

24

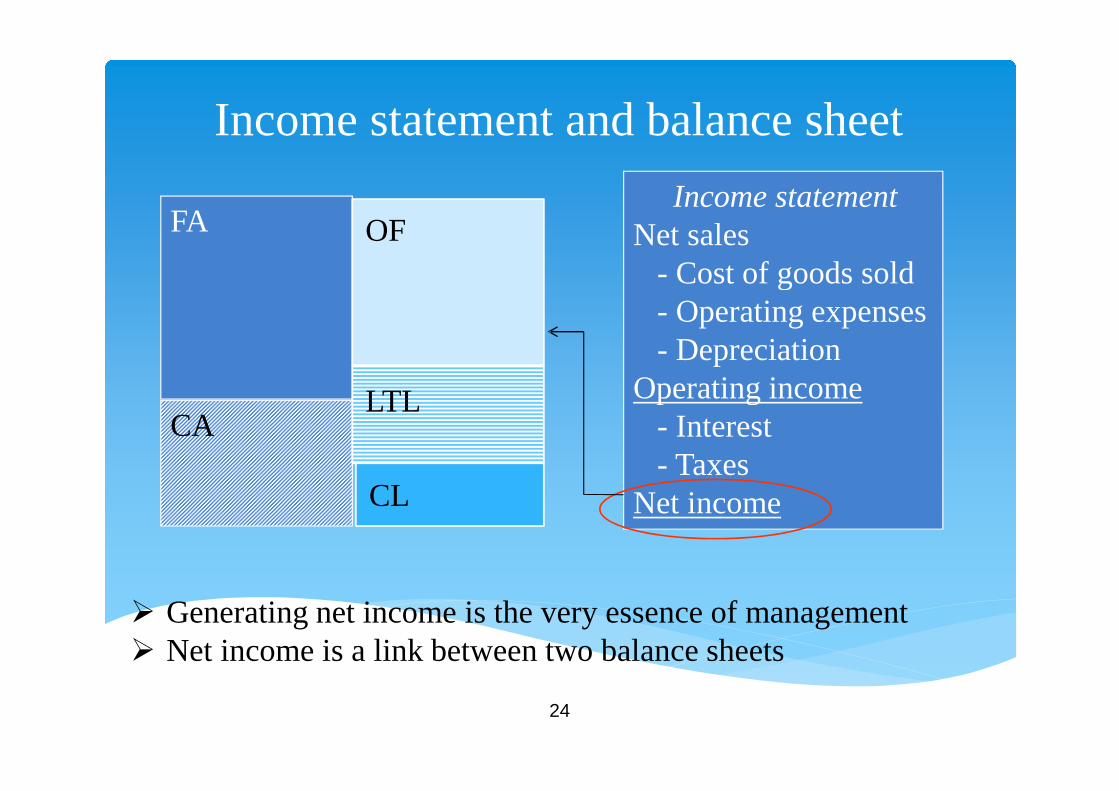

Income statement and balance sheet

Income statementNet sales

- Cost of goods sold- Operating expenses- Depreciation

Operating income- Interest- Taxes

Net income

FA

CA

OF

LTL

CL

Generating net income is the very essence of management Net income is a link between two balance sheets

25

Financial accounting

General purpose balance sheet and income statement

Main purpose – financial information for external users

Too aggregated for the day-to-day management ofbusiness divisions, market segments or products

26

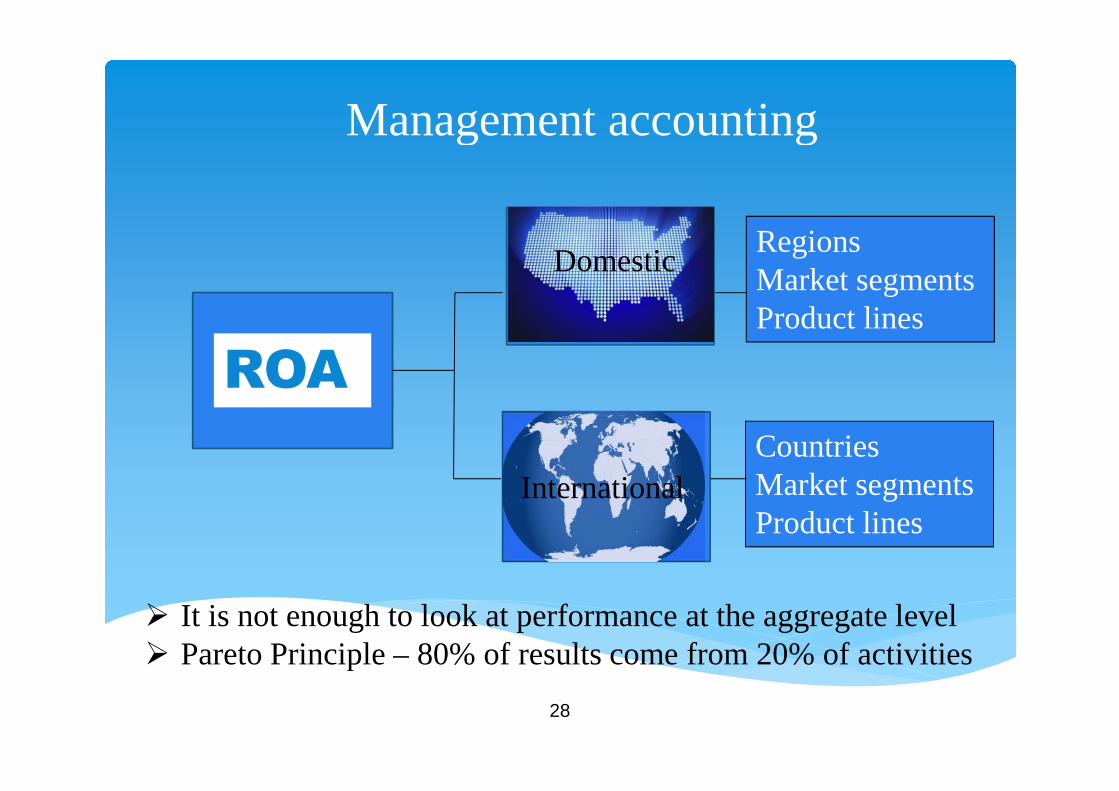

Management accounting

Domestic

International

Management accounting is used to implement the OperatingProfit Model at a sub-corporate level

ROA

27

Management accounting

Main purpose – information for internal users Relevant for managerial decision making Financial information disaggregated by divisions,

departments, countries, market segments and products

28

Management accounting

Domestic

International

It is not enough to look at performance at the aggregate level Pareto Principle – 80% of results come from 20% of activities

CountriesMarket segmentsProduct lines

RegionsMarket segmentsProduct lines

ROA

29

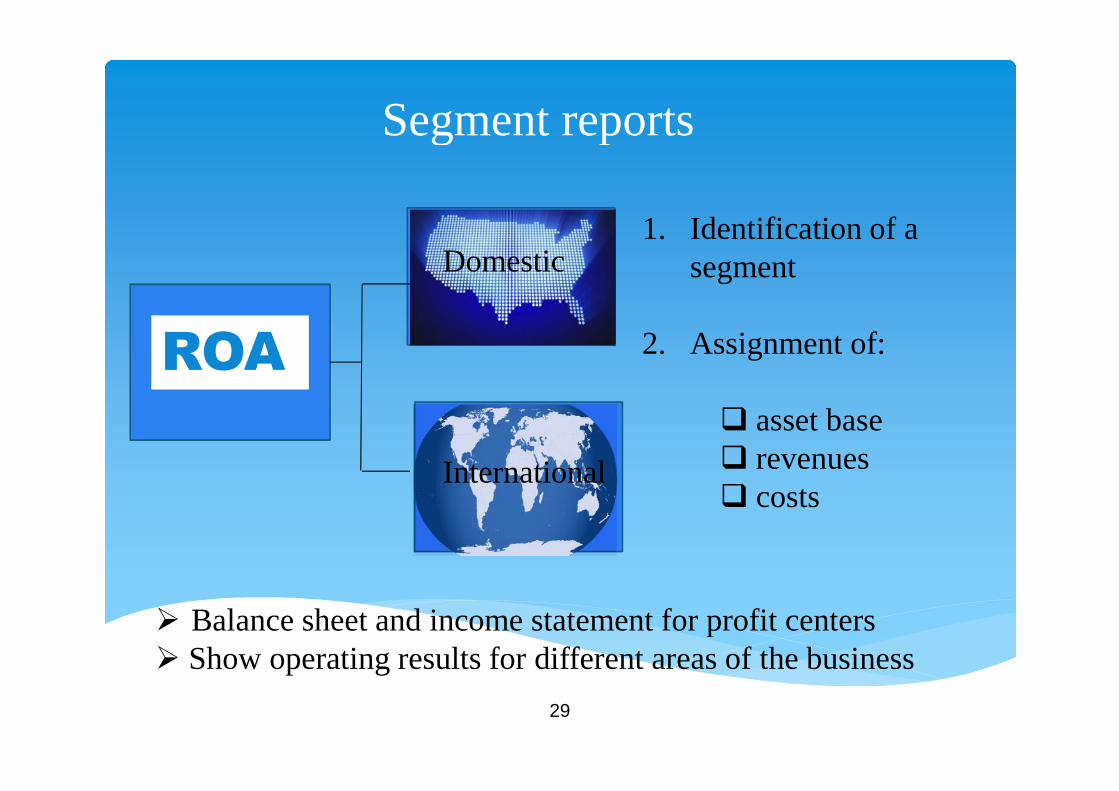

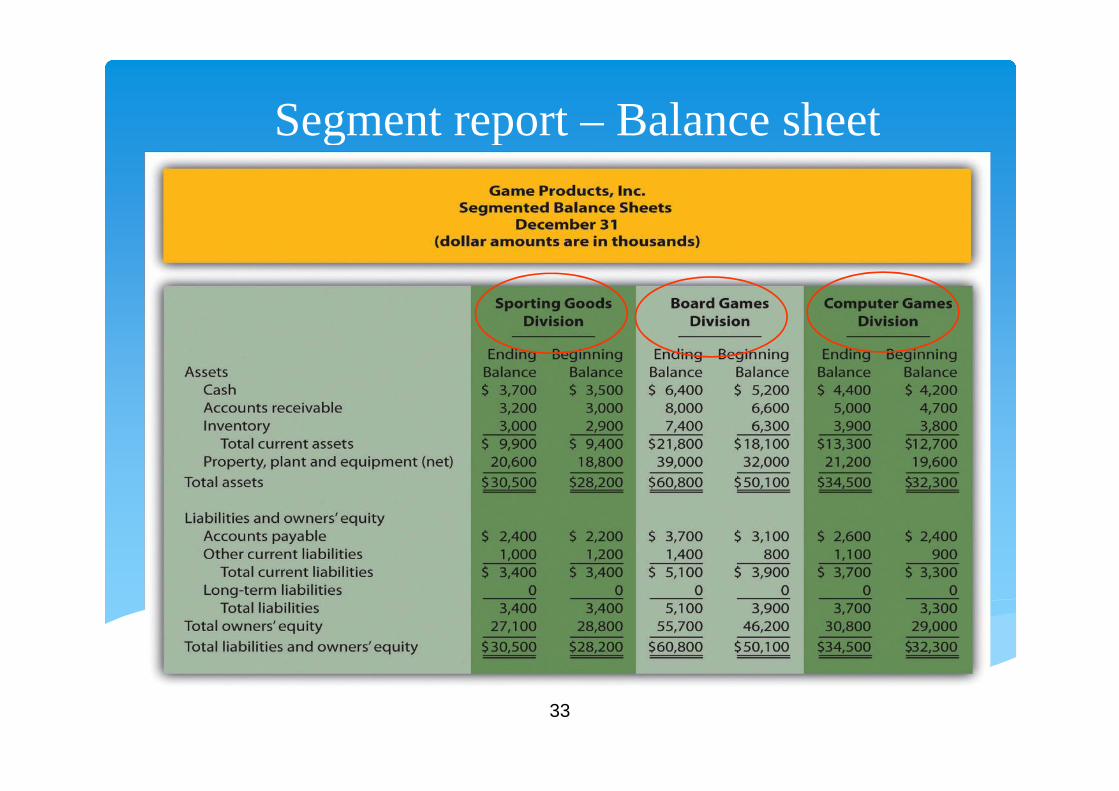

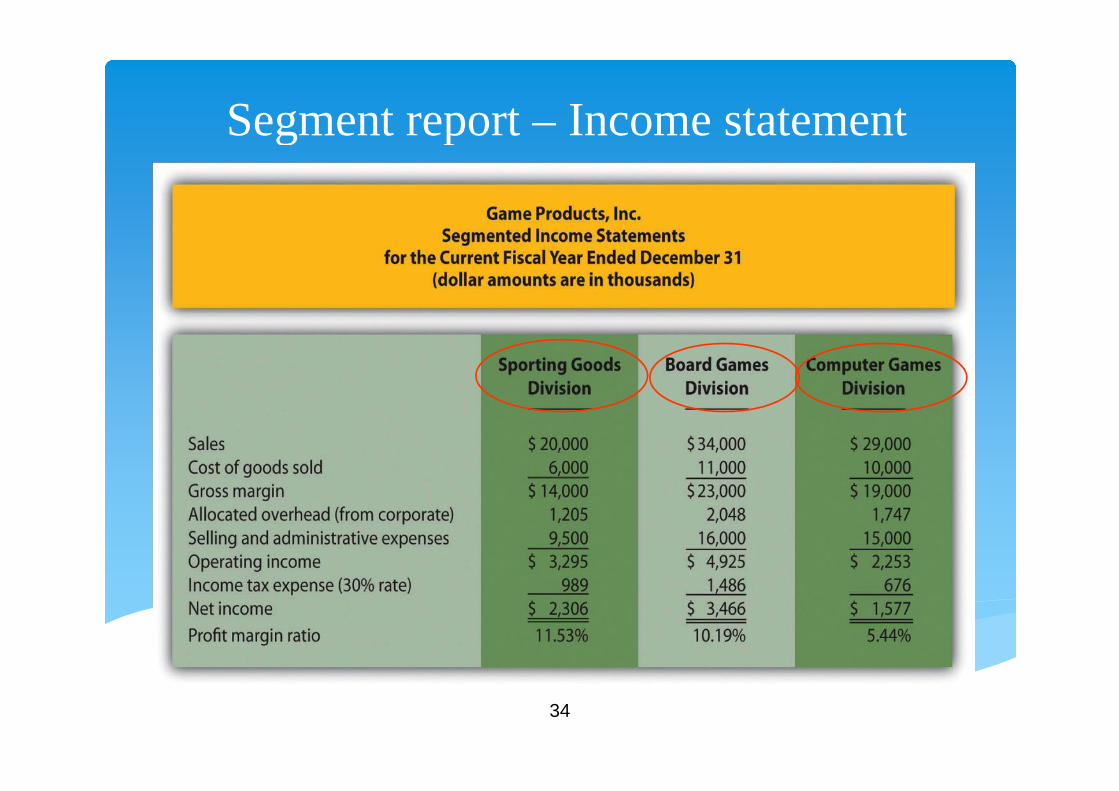

Segment reports

Domestic

International

Balance sheet and income statement for profit centers Show operating results for different areas of the business

1. Identification of asegment

2. Assignment of:

asset base revenues costs

ROA

30

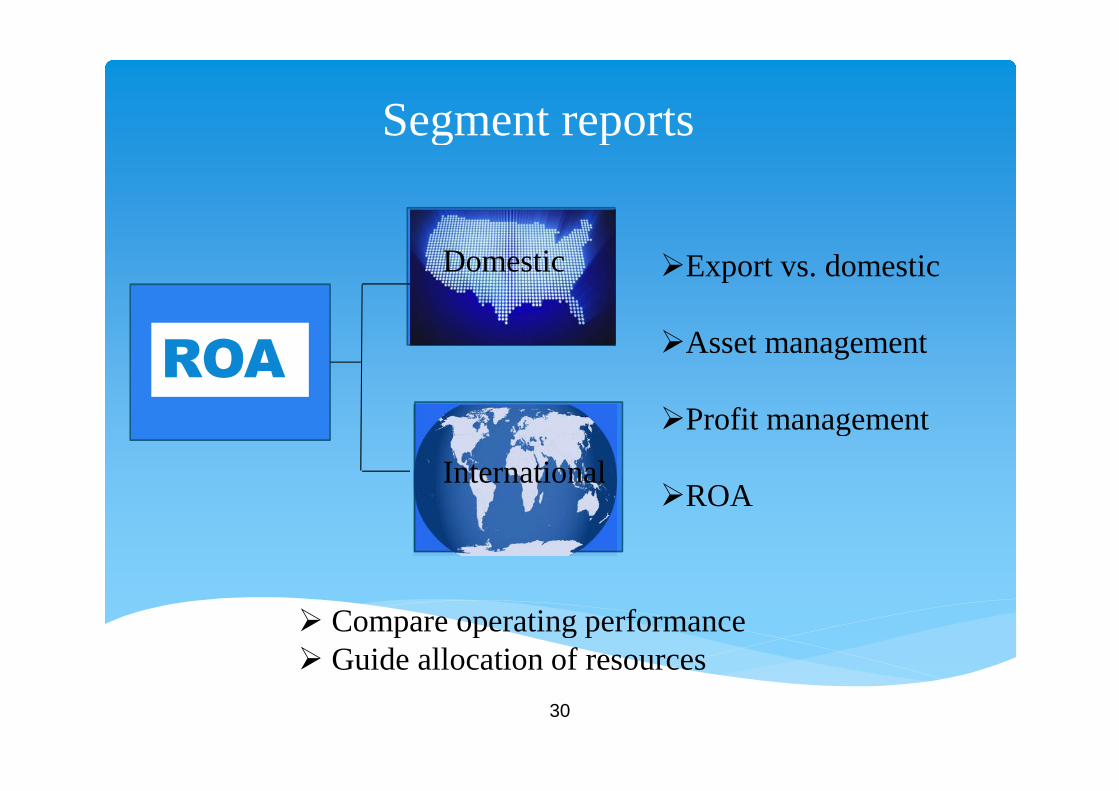

Segment reports

Domestic

International

Compare operating performance Guide allocation of resources

Export vs. domestic

Asset management

Profit management

ROA

ROA

31

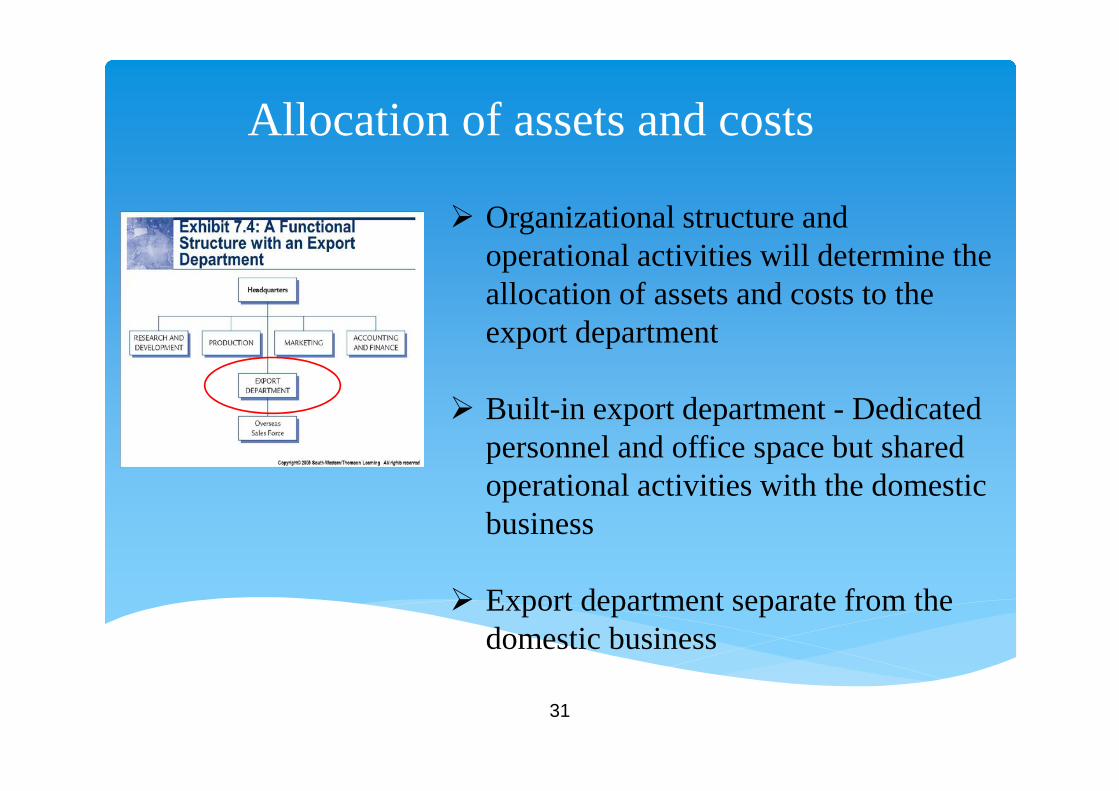

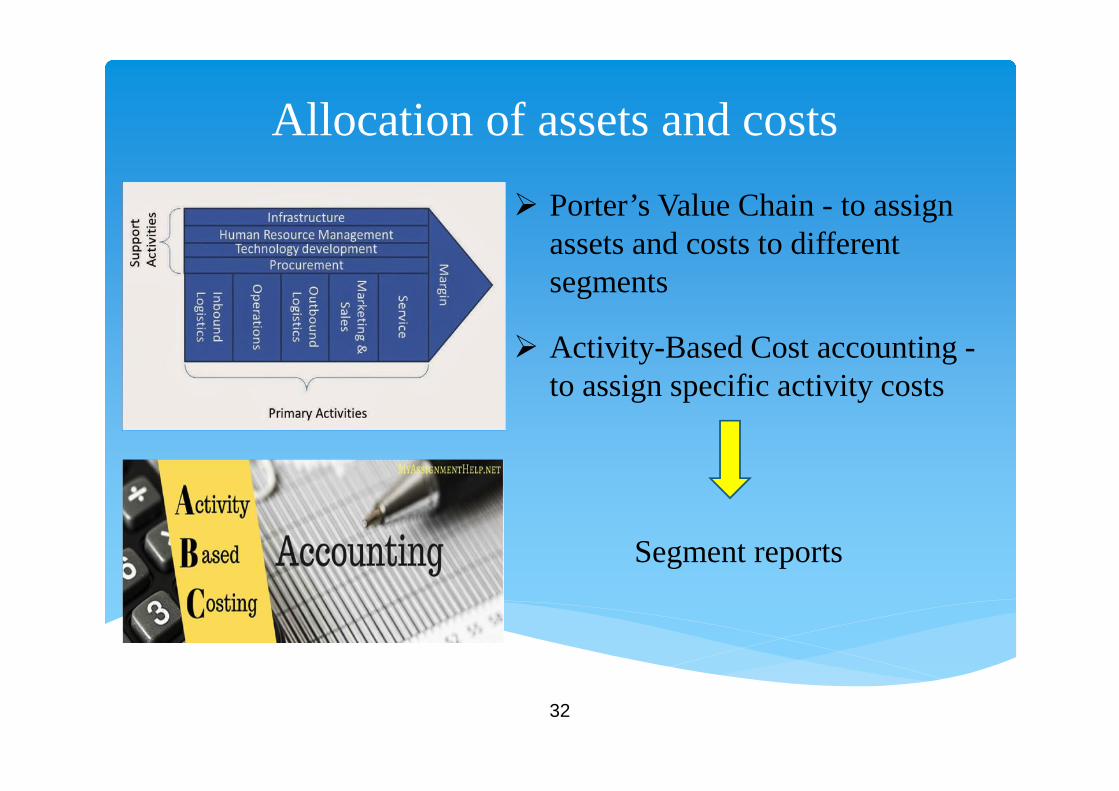

Allocation of assets and costs

Organizational structure andoperational activities will determine theallocation of assets and costs to theexport department

Built-in export department - Dedicatedpersonnel and office space but sharedoperational activities with the domesticbusiness

Export department separate from thedomestic business

32

Allocation of assets and costs

Porter’s Value Chain - to assignassets and costs to differentsegments

Activity-Based Cost accounting -to assign specific activity costs

Segment reports

33

Segment report – Balance sheet

34

Segment report – Income statement

35

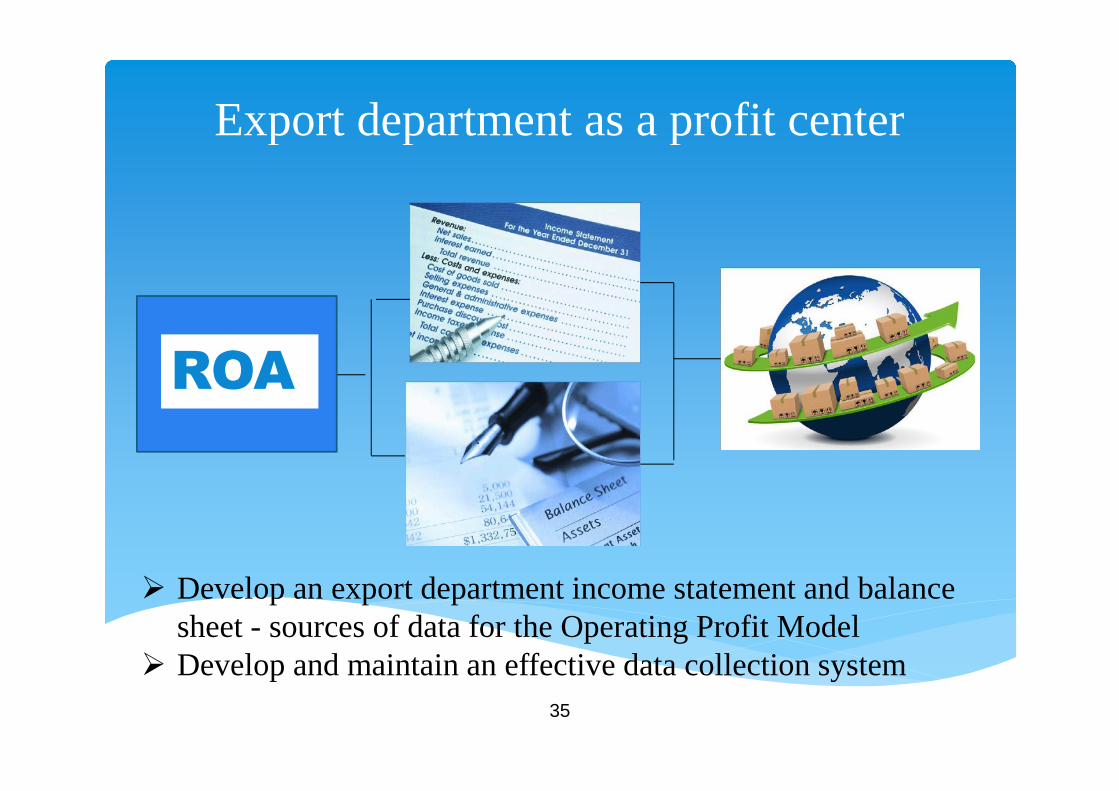

Export department as a profit center

Develop an export department income statement and balancesheet - sources of data for the Operating Profit Model

Develop and maintain an effective data collection system

ROA

36

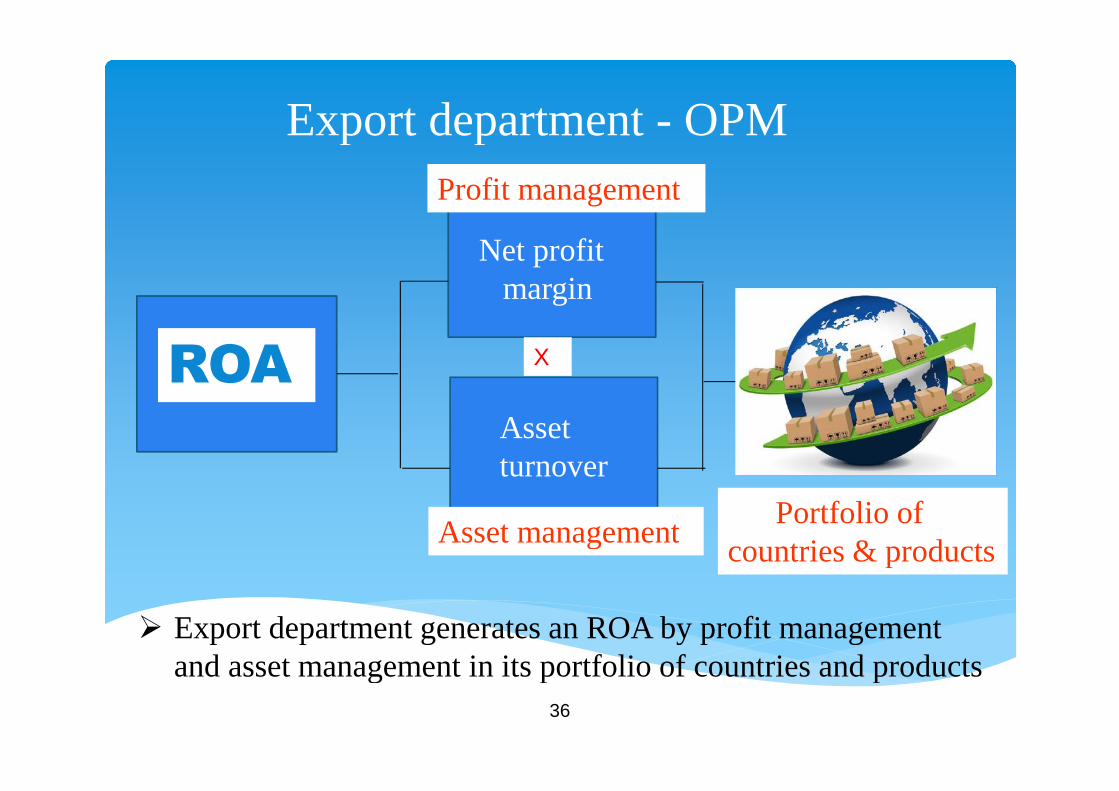

Export department - OPM

Assetturnover

X

Portfolio ofcountries & products

Profit management

Asset management

Net profitmargin

Export department generates an ROA by profit managementand asset management in its portfolio of countries and products

ROA

37

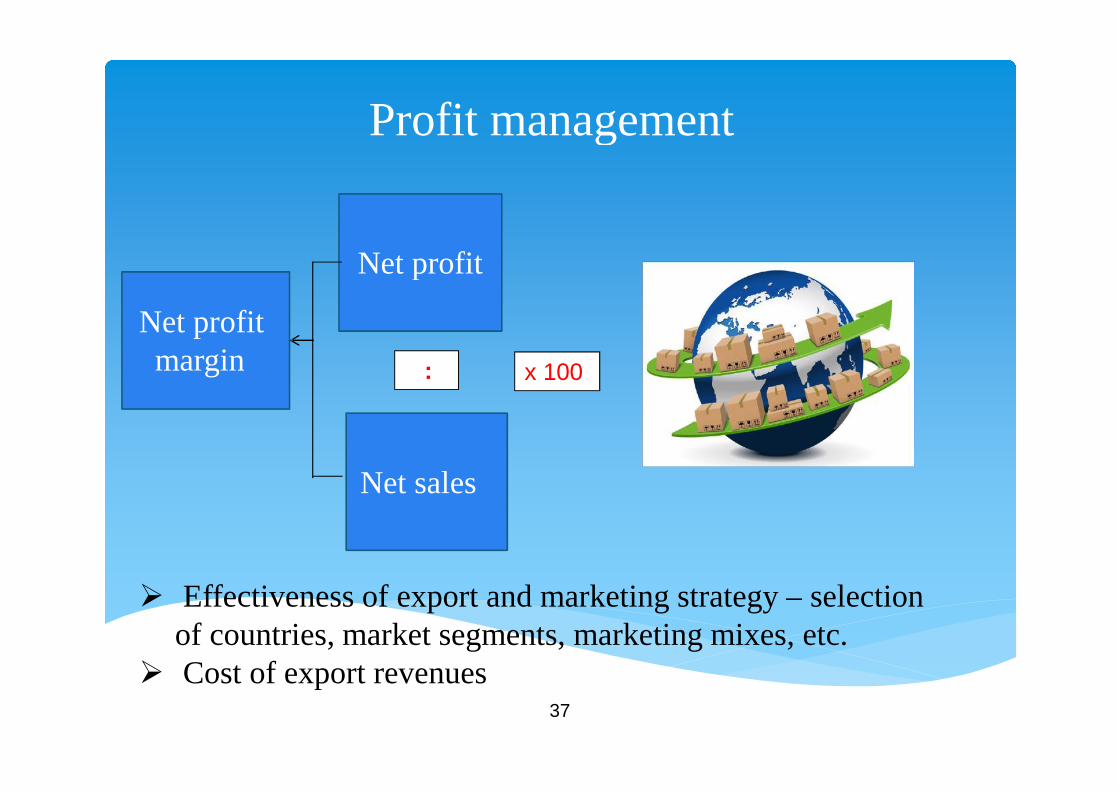

Profit management

Net sales

Net profit

:

Net profitmargin

Effectiveness of export and marketing strategy – selectionof countries, market segments, marketing mixes, etc.

Cost of export revenues

x 100

38

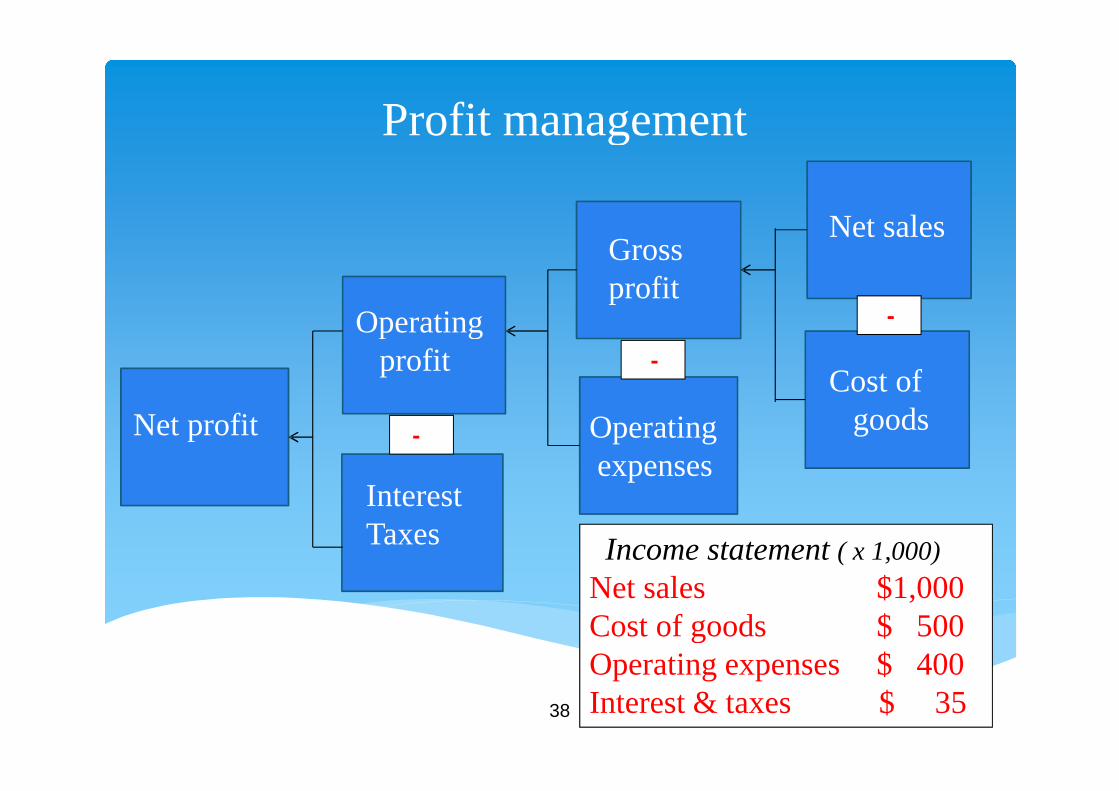

Profit management

InterestTaxes

Operatingprofit

Operatingexpenses

Grossprofit

Net sales

Cost ofgoods

-

-

-

Net profit

Income statement ( x 1,000)

Net sales $1,000Cost of goods $ 500Operating expenses $ 400Interest & taxes $ 35

39

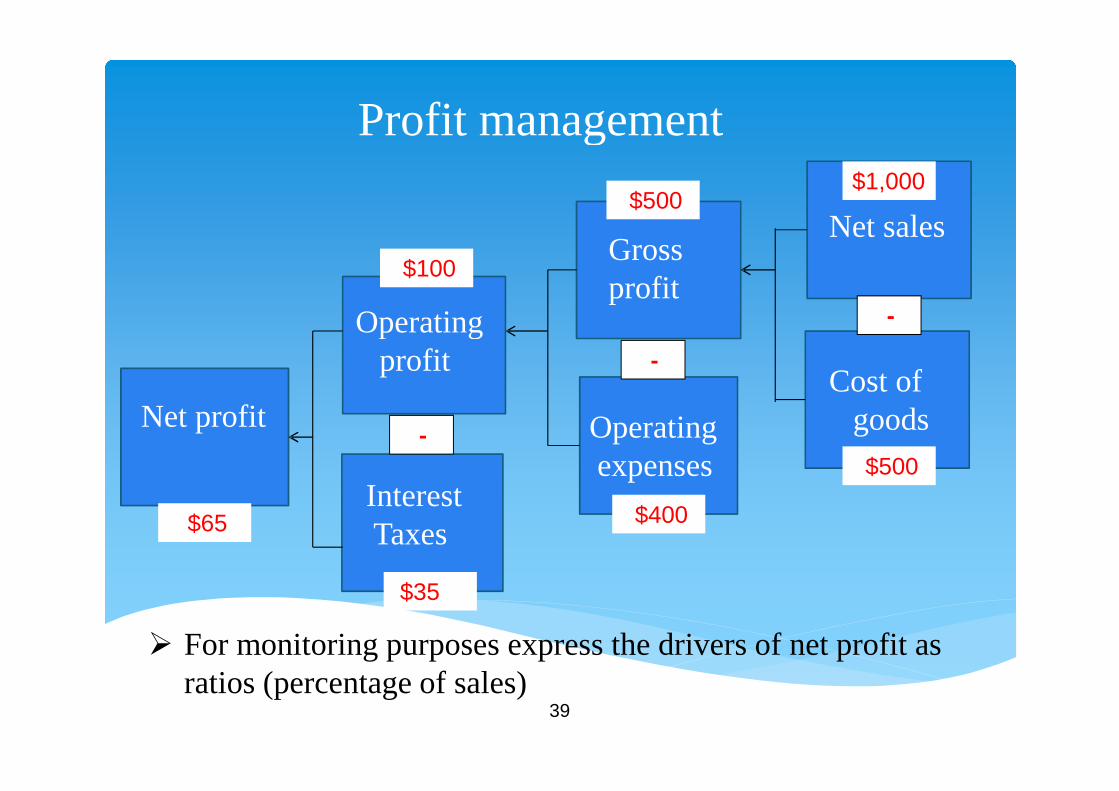

Profit management

Operatingprofit

Operatingexpenses

Grossprofit

Net sales

Cost ofgoods

-

-

-

$1,000

$500

$500

$400

$100

$35

$65

Net profit

InterestTaxes

For monitoring purposes express the drivers of net profit asratios (percentage of sales)

40

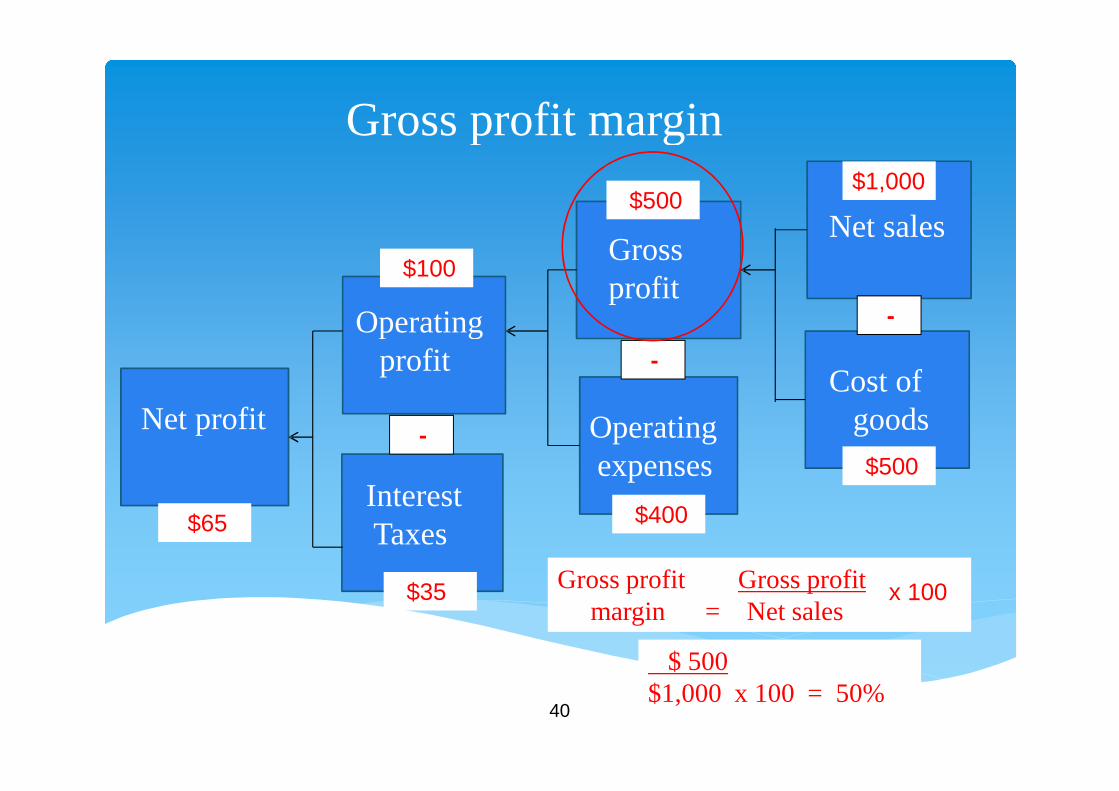

Gross profit margin

Operatingprofit

Operatingexpenses

Grossprofit

Net sales

Cost ofgoods

-

-

-

$1,000

$500

$500

$400

$100

$35

$65

Gross profit Gross profitmargin = Net sales

$ 500$1,000 x 100 = 50%

Net profit

x 100

InterestTaxes

41

Gross profit margin

An important indicator of export strategy

First indication of the marketing strategy(net sales) and production efficiency (costof goods sold)

Indication of a competitive advantage(differentiation or low cost)

Affected by a mix of products and markets

Reflects pricing strategy, cost of materials,product modification, etc.

42

Gross profit margin

There may be growing internationalsales but declining gross margins, and adeclining return on export investment

Great importance of relevant financialdata, at the lowest possible level

Very small changes in prices or the costof goods sold lead to big changes inprofits

43

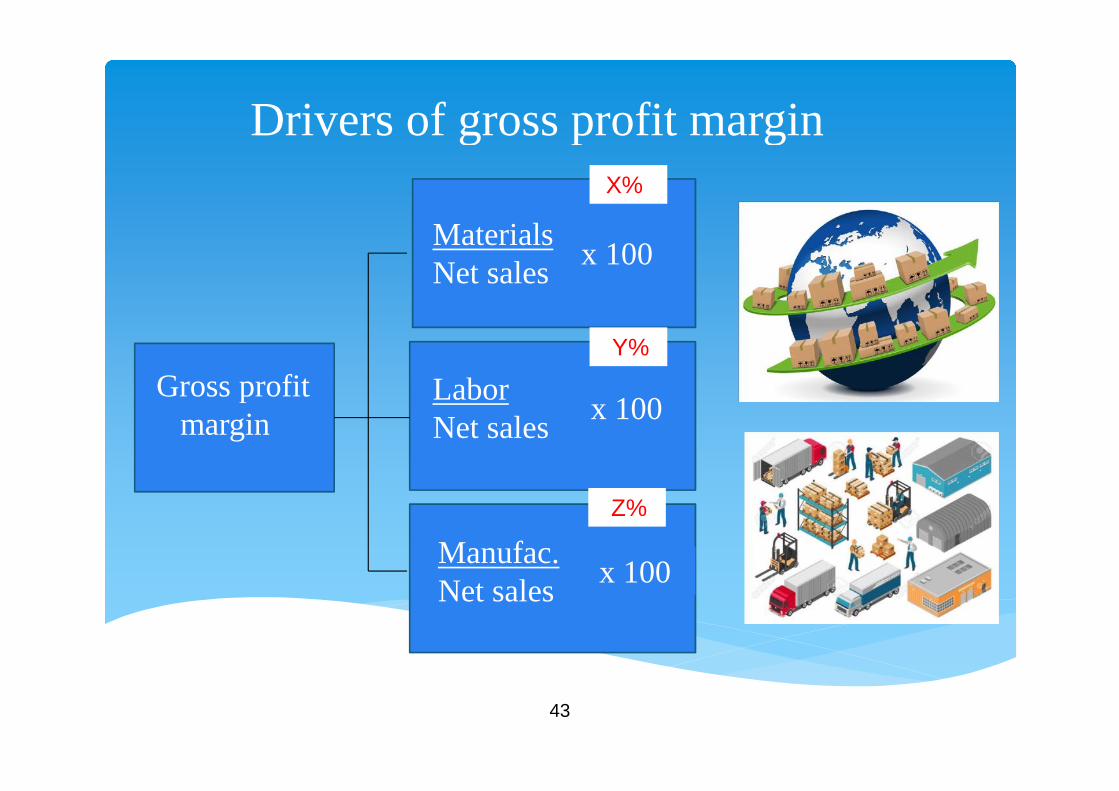

Drivers of gross profit margin

MaterialsNet sales

Gross profitmargin

LaborNet sales

X%

Y%

Z%

Manufac.Net sales

x 100

x 100

x 100

44

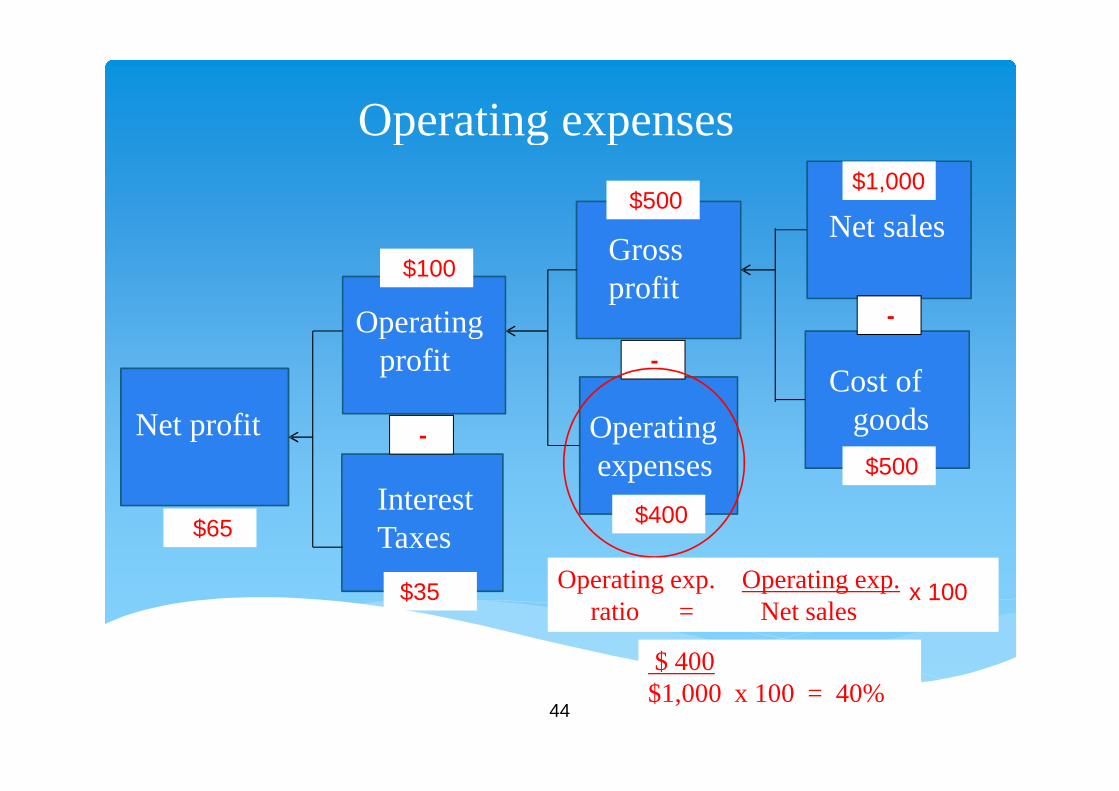

Operating expenses

Net profit

InterestTaxes

Operatingprofit

Operatingexpenses

Grossprofit

Net sales

Cost ofgoods

-

-

-

$1,000

$500

$500

$400

$100

$35

$65

Operating exp. Operating exp.ratio = Net sales

$ 400$1,000 x 100 = 40%

x 100

45

Operating expenses

Sales and administration salaries Office and travel expenses Marketing expenses Market development (market research,

travel, trade shows, samples, etc.) Product development, product

modifications General overhead: utilities, repairs,

insurance Depreciation

46

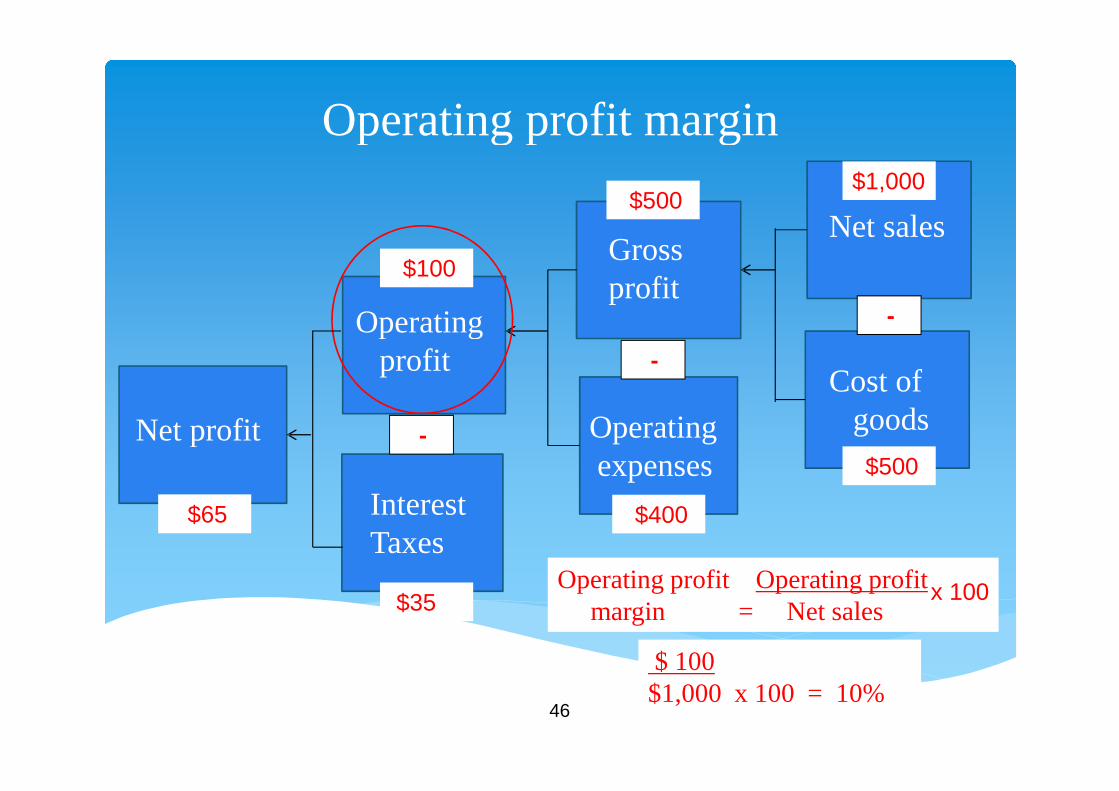

Operating profit margin

Net profit

InterestTaxes

Operatingprofit

Operatingexpenses

Grossprofit

Net sales

Cost ofgoods

-

-

-

$1,000

$500

$500

$400

$100

$35

$65

Operating profit Operating profitmargin = Net sales

$ 100$1,000 x 100 = 10%

x 100

47

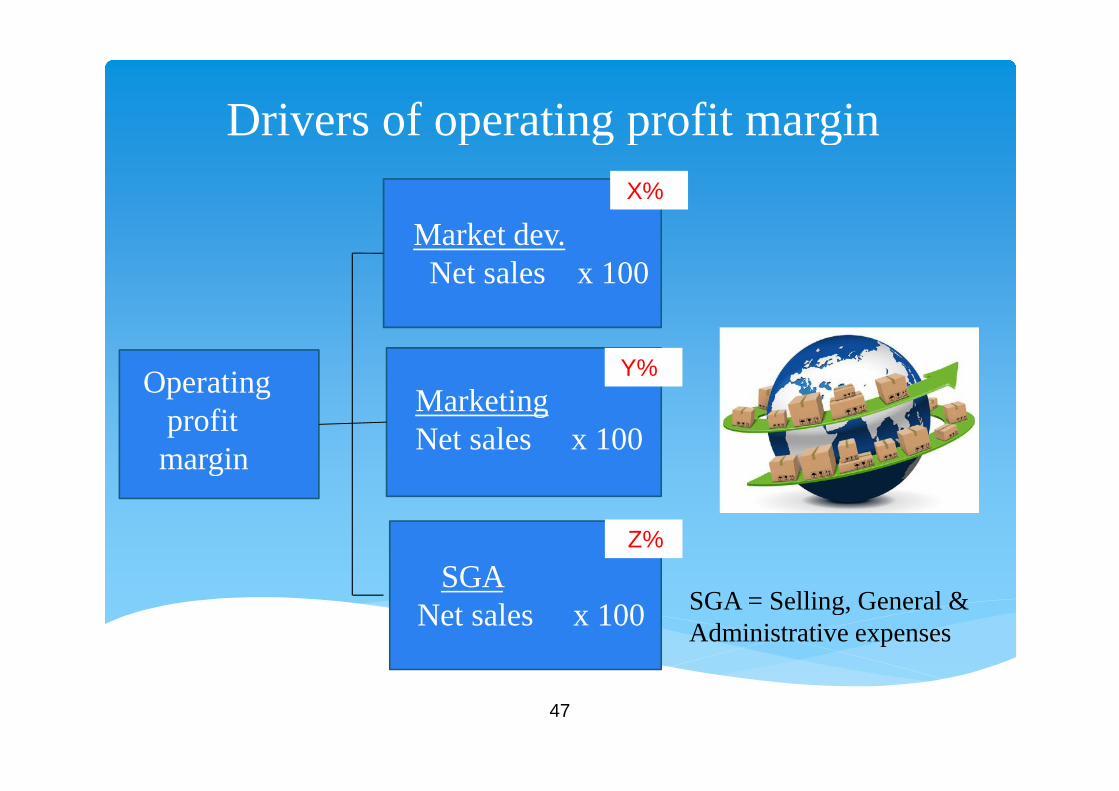

Drivers of operating profit margin

MarketingNet sales x 100

Operatingprofitmargin

SGANet sales x 100

Market dev.Net sales x 100

X%

Y%

Z%

SGA = Selling, General &Administrative expenses

48

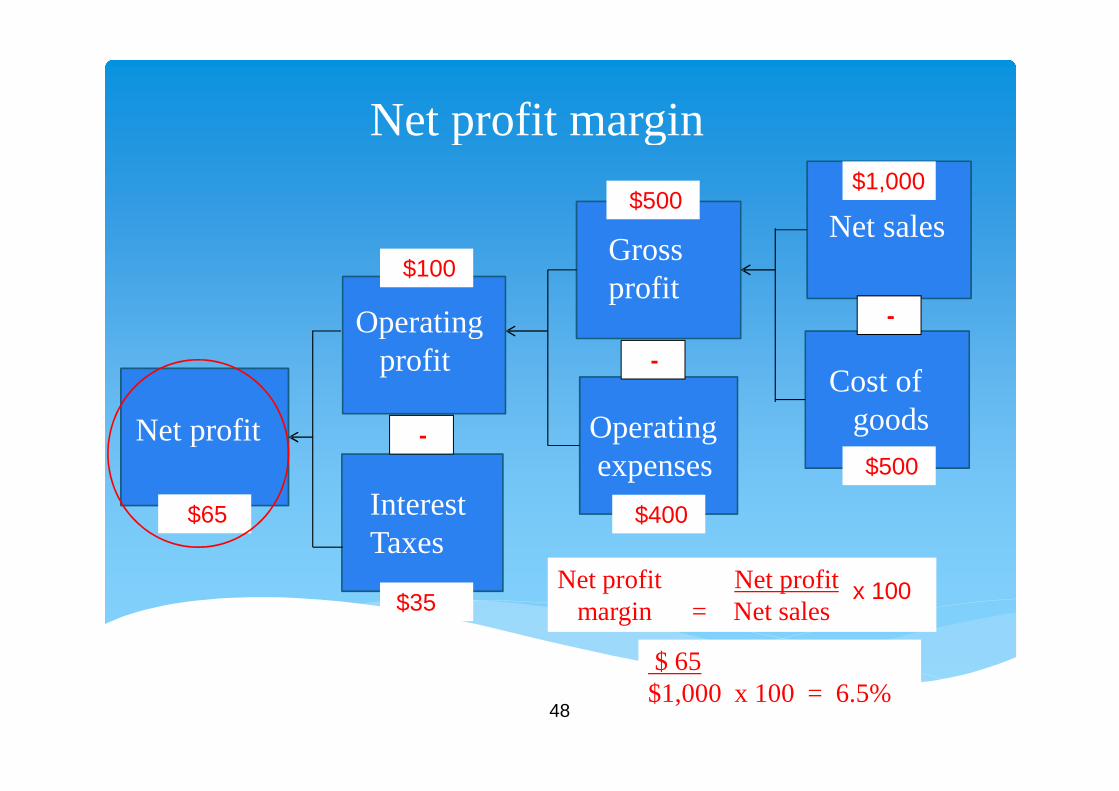

Net profit margin

Net profit

InterestTaxes

Operatingprofit

Operatingexpenses

Grossprofit

Net sales

Cost ofgoods

-

-

-

$1,000

$500

$500

$400

$100

$35

$65

Net profit Net profitmargin = Net sales

$ 65$1,000 x 100 = 6.5%

x 100

49

Profitability ratios

Operatingprofitmargin

Grossprofitmargin

Reflection of the operating strategy (costs)and marketing strategy (sales revenues)

Should be actively monitored and managed

Netprofitmargin

50

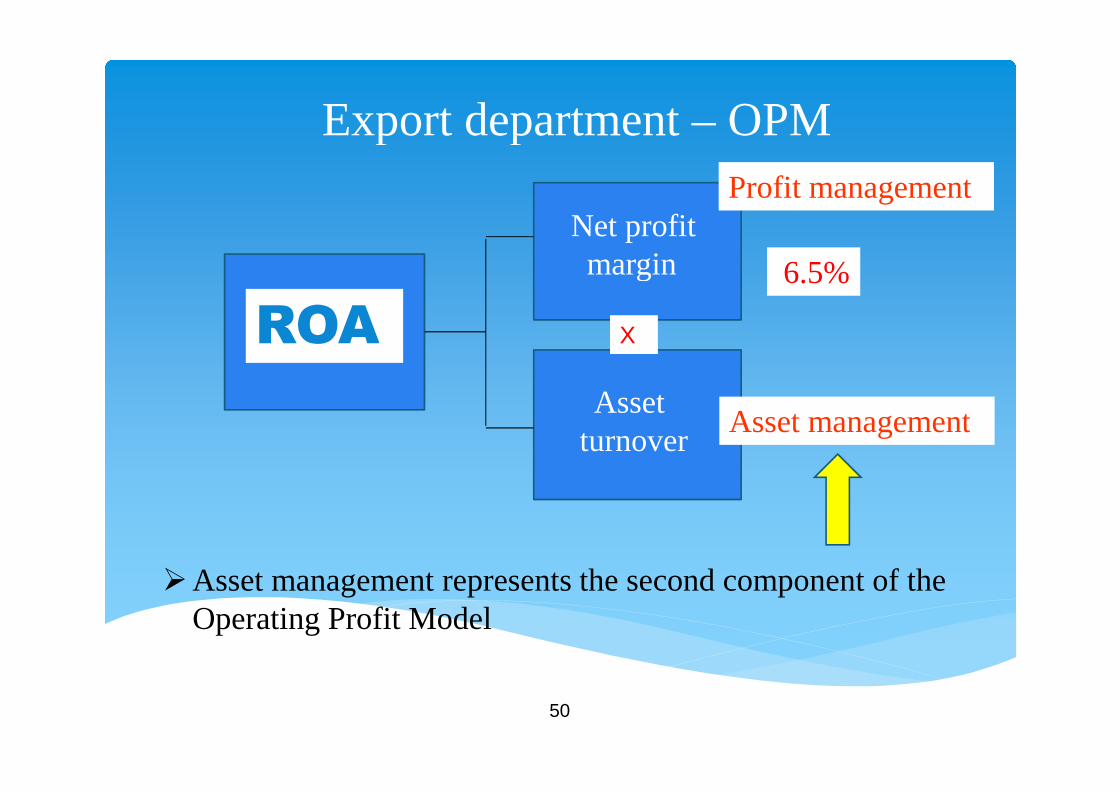

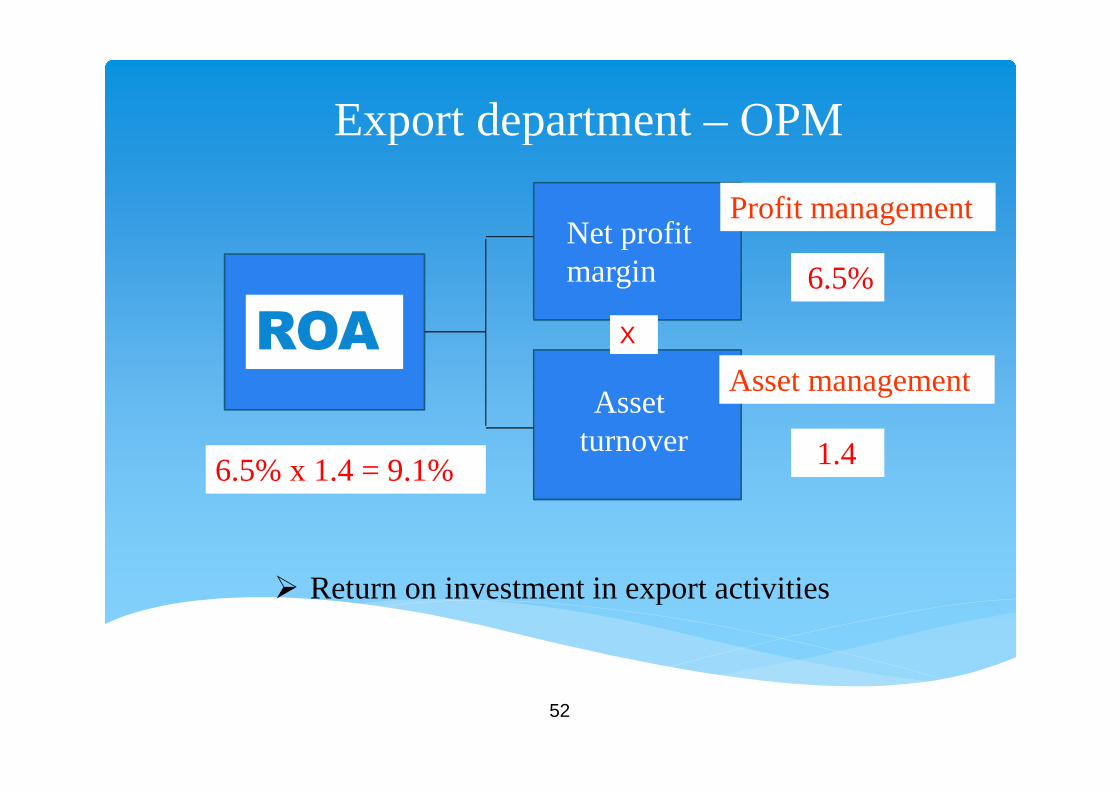

Export department – OPM

Assetturnover

Asset management

X

Profit management

6.5%

Net profitmargin

Asset management represents the second component of theOperating Profit Model

ROA

51

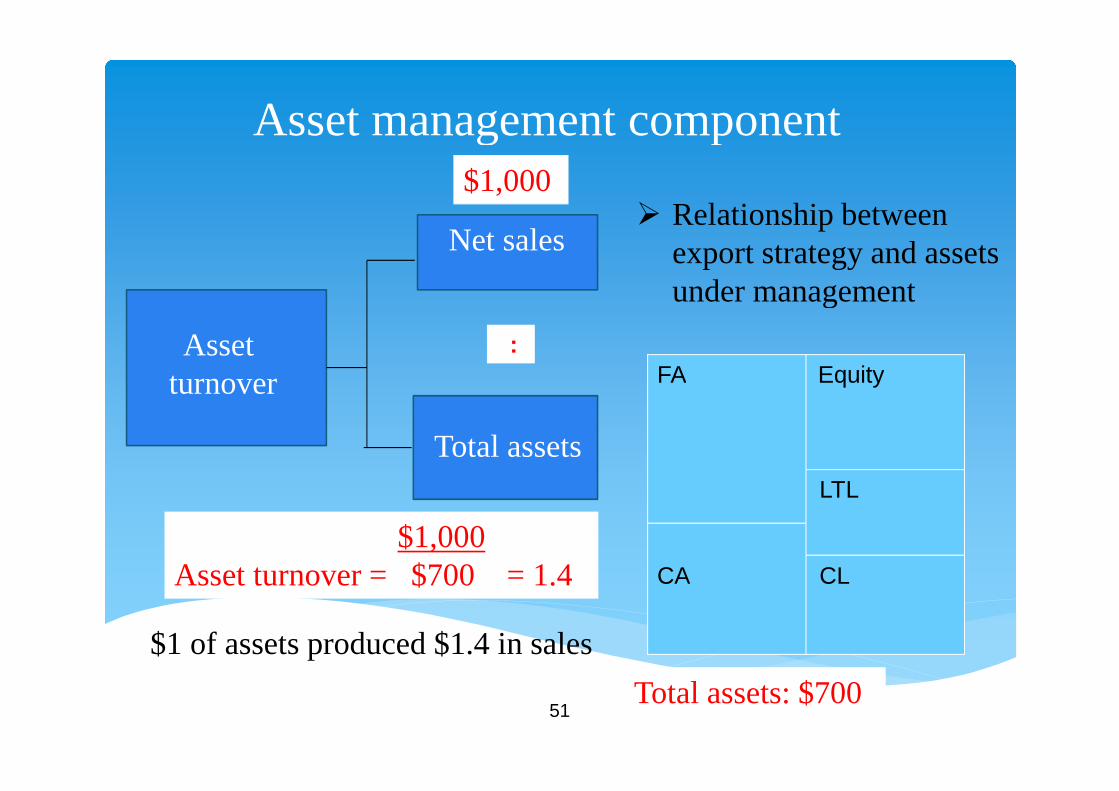

Asset management component

Assetturnover

Total assets

Net sales

:

$1,000

FA Equity

LTL

CA CL

Total assets: $700

$1,000Asset turnover = $700 = 1.4

$1 of assets produced $1.4 in sales

Relationship betweenexport strategy and assetsunder management

52

Export department – OPM

Assetturnover

Net profitmargin

Asset management

X

Return on investment in export activities

Profit management

6.5%

1.46.5% x 1.4 = 9.1%

ROA

53

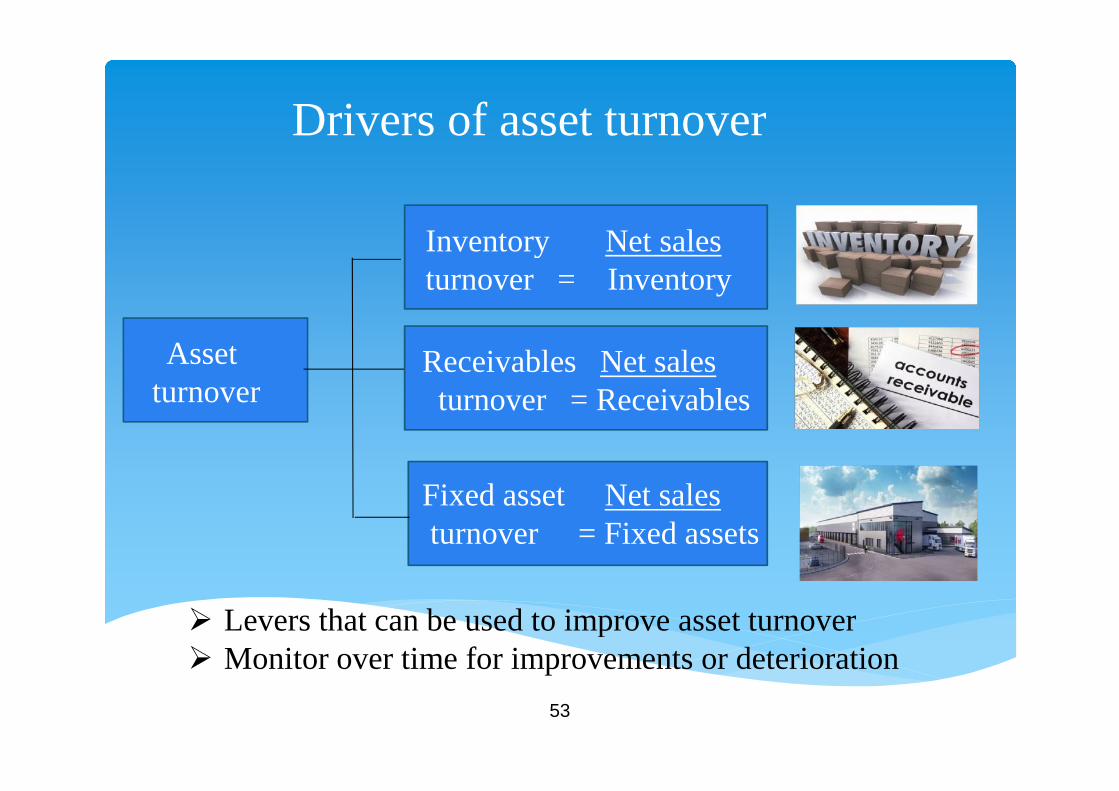

Drivers of asset turnover

Assetturnover

Fixed asset Net salesturnover = Fixed assets

Inventory Net salesturnover = Inventory

Receivables Net salesturnover = Receivables

Levers that can be used to improve asset turnover Monitor over time for improvements or deterioration

54

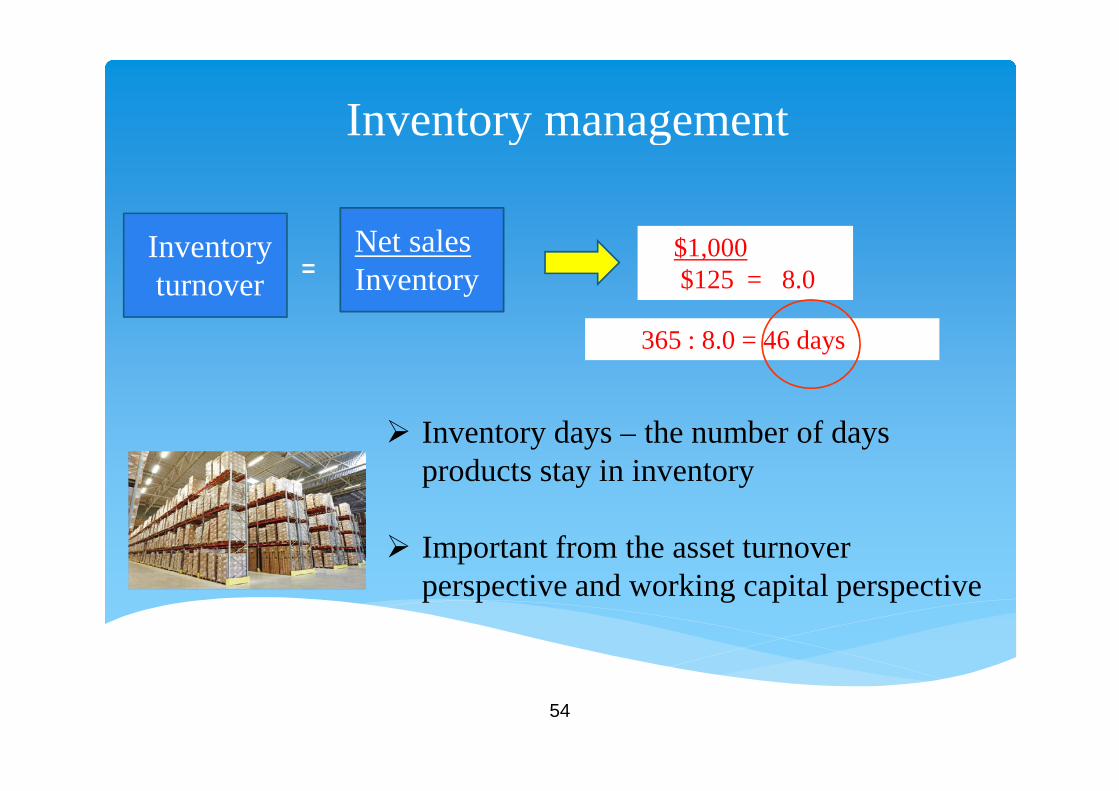

Inventory management

Net salesInventory

$1,000$125 = 8.0

Inventory days – the number of daysproducts stay in inventory

Important from the asset turnoverperspective and working capital perspective

365 : 8.0 = 46 days

Inventoryturnover

=

55

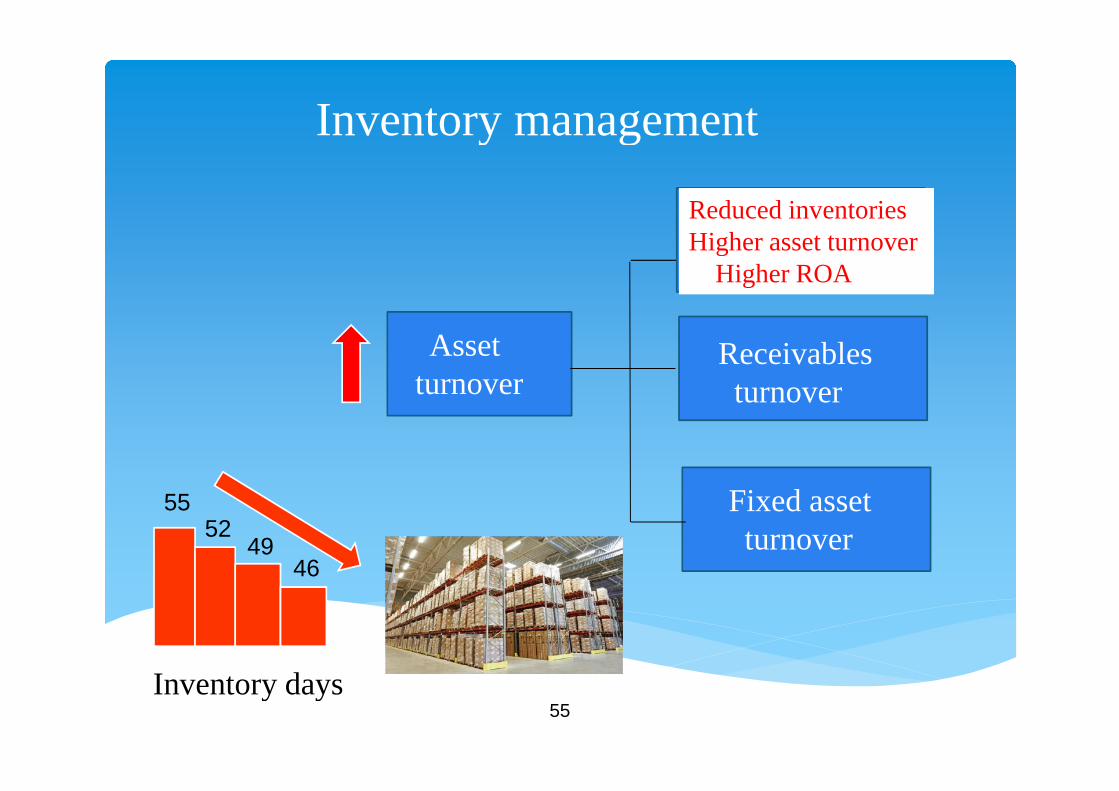

Inventory management

Assetturnover

5552

4946

Inventory days

Reduced inventoriesHigher asset turnover

Higher ROA

Receivablesturnover

Fixed assetturnover

56

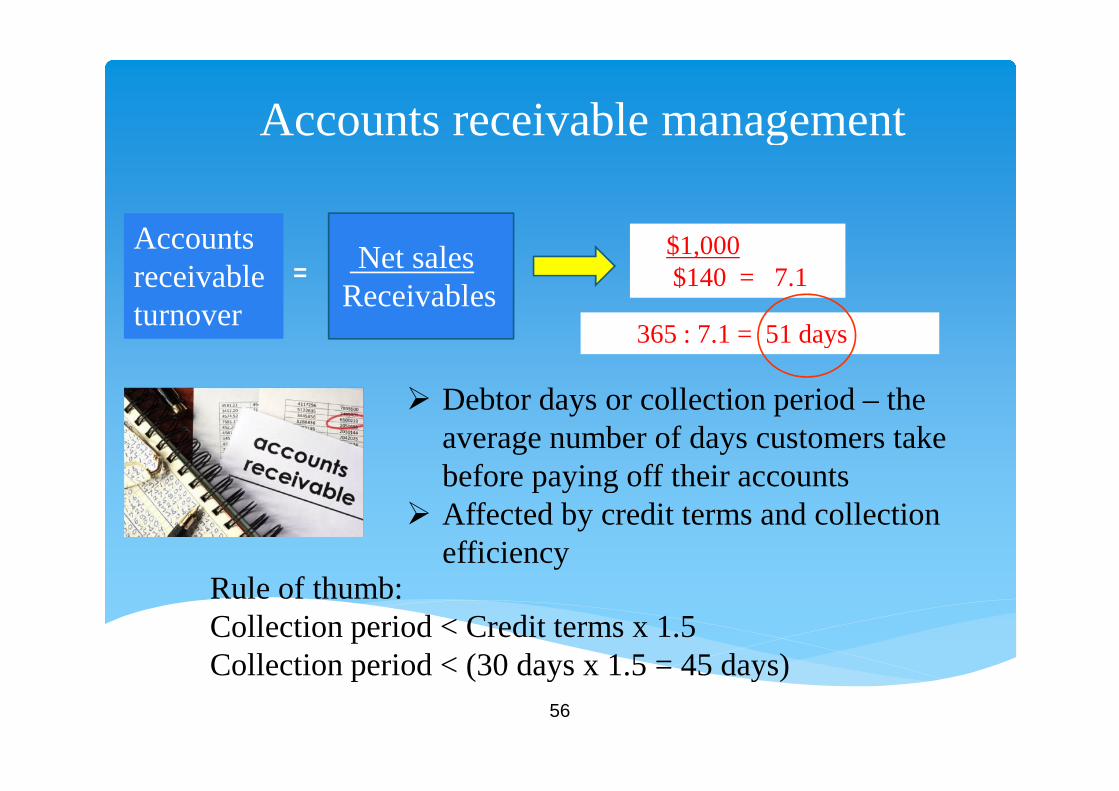

Accounts receivable management

Net salesReceivables

$1,000$140 = 7.1

Debtor days or collection period – theaverage number of days customers takebefore paying off their accounts

Affected by credit terms and collectionefficiency

365 : 7.1 = 51 days

Accountsreceivableturnover

=

Rule of thumb:Collection period < Credit terms x 1.5Collection period < (30 days x 1.5 = 45 days)

57

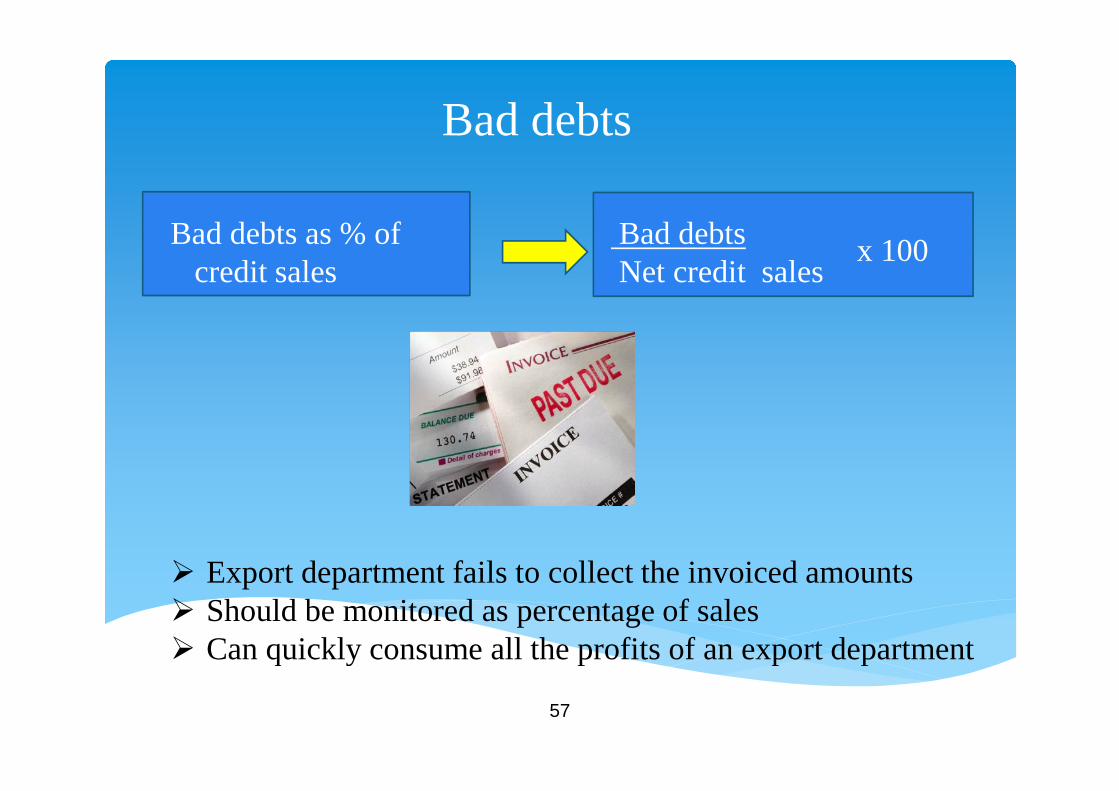

Bad debts

Bad debtsNet credit sales

Bad debts as % ofcredit sales

Export department fails to collect the invoiced amounts Should be monitored as percentage of sales Can quickly consume all the profits of an export department

x 100

58

Accounts receivable management tools

Collection time

Non-paymentprotection

Lower non-payment risk

Faster collectionNon-payment protection

59

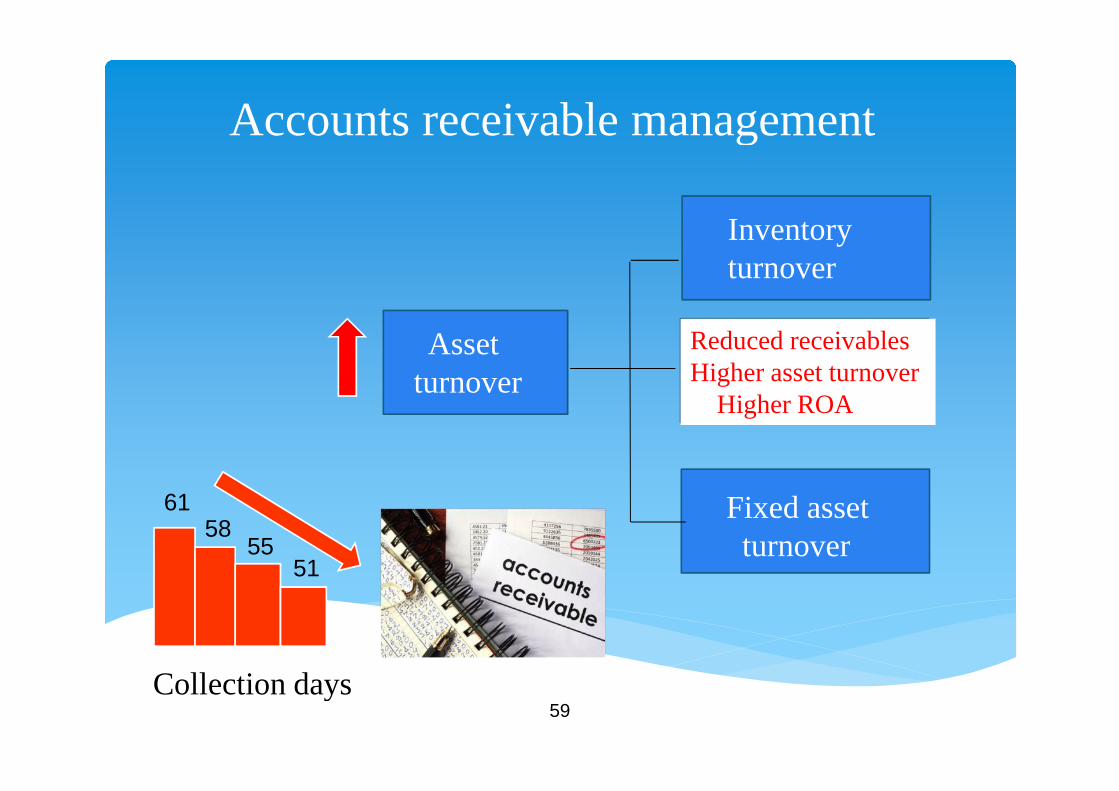

Accounts receivable management

Assetturnover

Reduced receivablesHigher asset turnover

Higher ROA

6158

5551

Collection days

Fixed assetturnover

Inventoryturnover

60

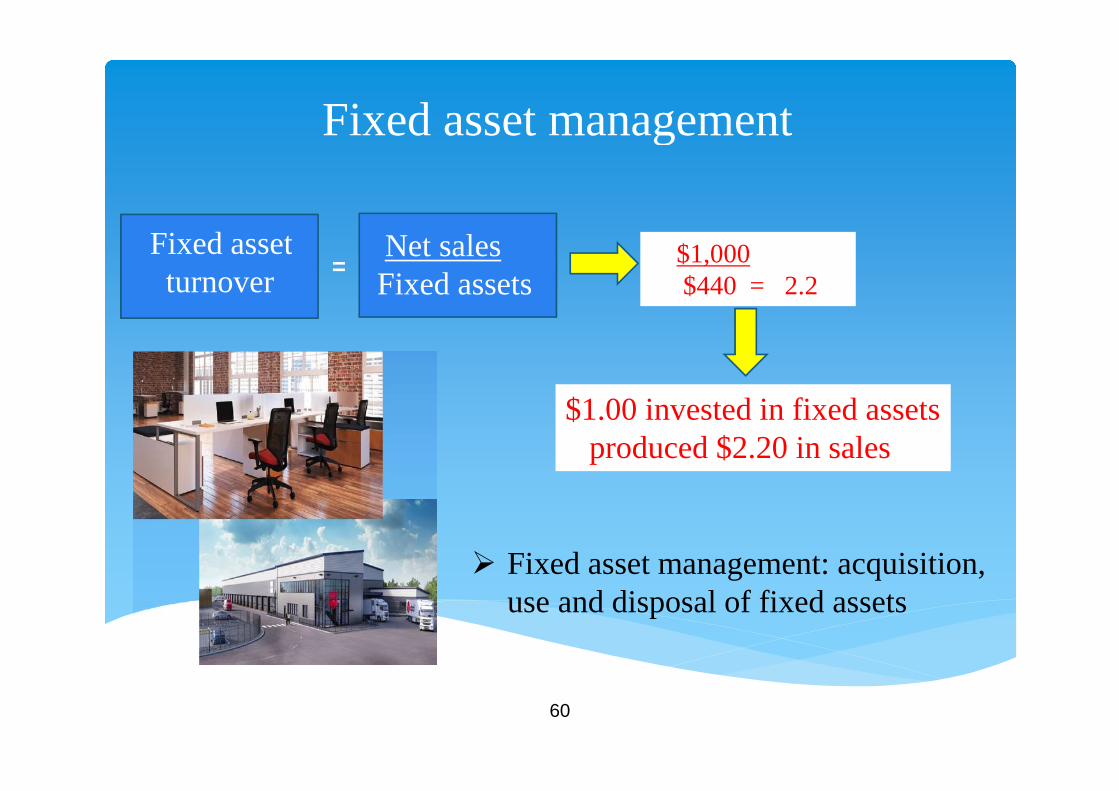

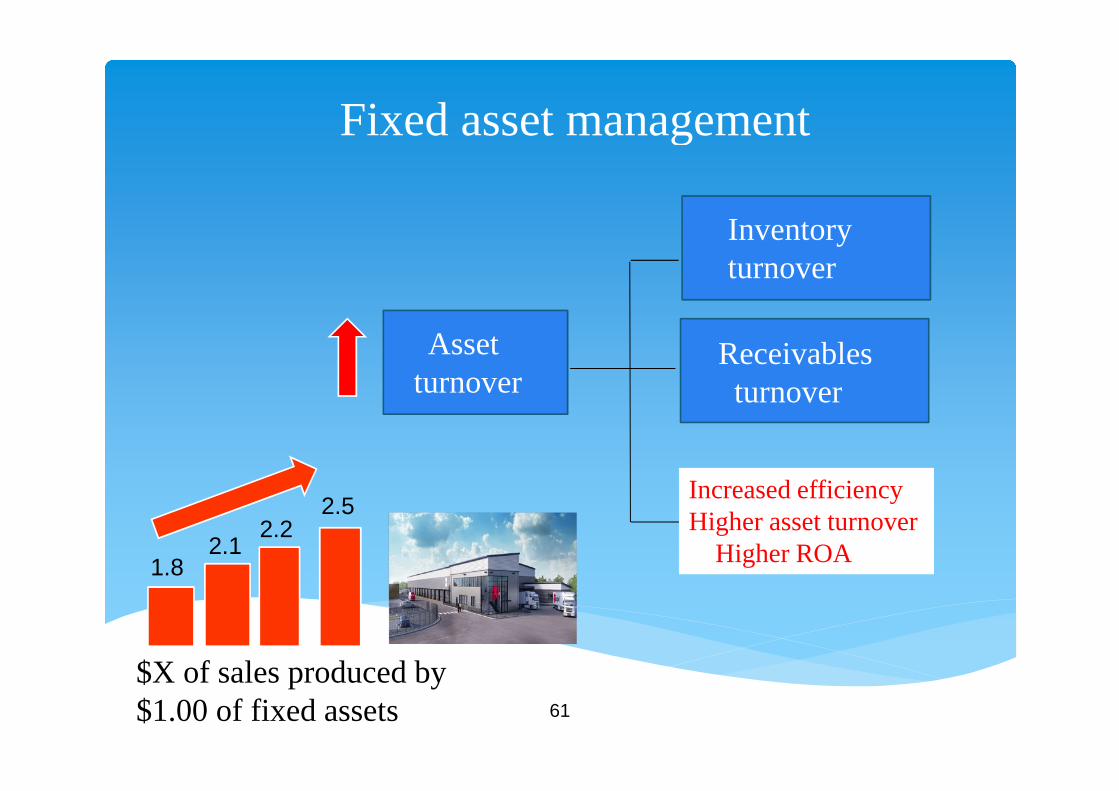

Fixed asset management

Net salesFixed assets

$1,000$440 = 2.2

$1.00 invested in fixed assetsproduced $2.20 in sales

Fixed assetturnover

=

Fixed asset management: acquisition,use and disposal of fixed assets

61

Fixed asset management

Assetturnover

Increased efficiencyHigher asset turnover

Higher ROA2.1

$X of sales produced by$1.00 of fixed assets

Inventoryturnover

2.22.5

1.8

Receivablesturnover

62

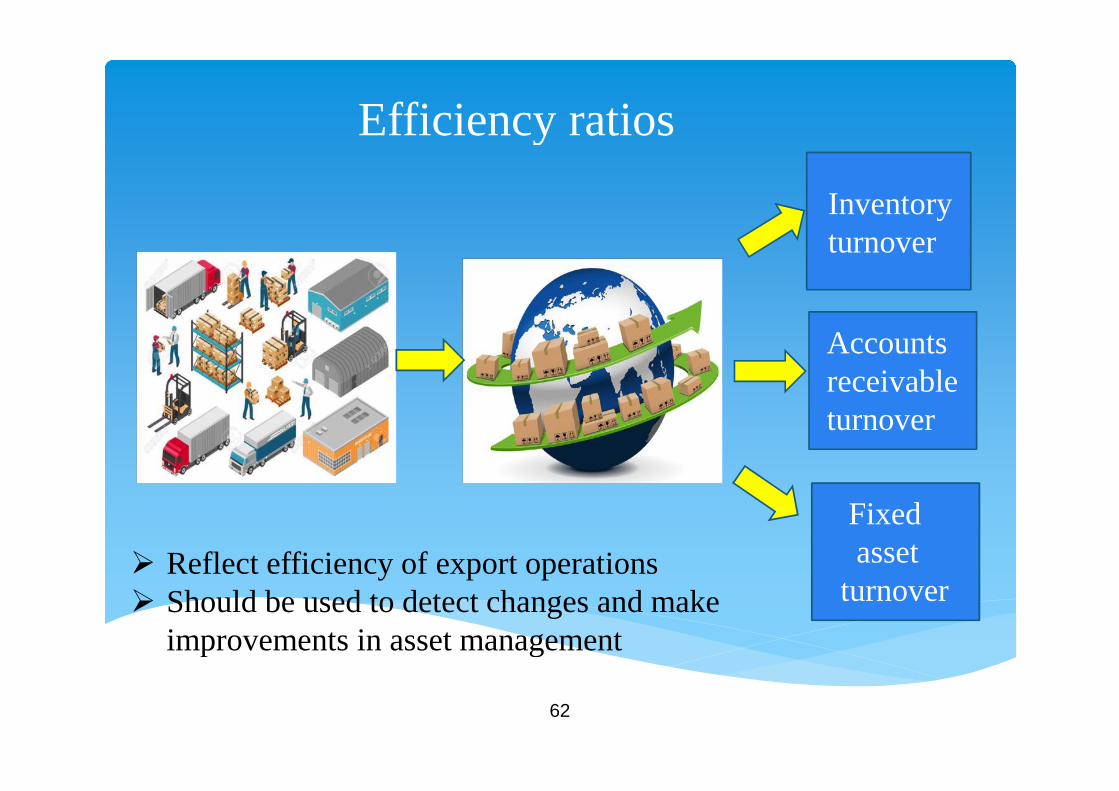

Efficiency ratios

Accountsreceivableturnover

Inventoryturnover

Fixedasset

turnover Reflect efficiency of export operations Should be used to detect changes and make

improvements in asset management

63

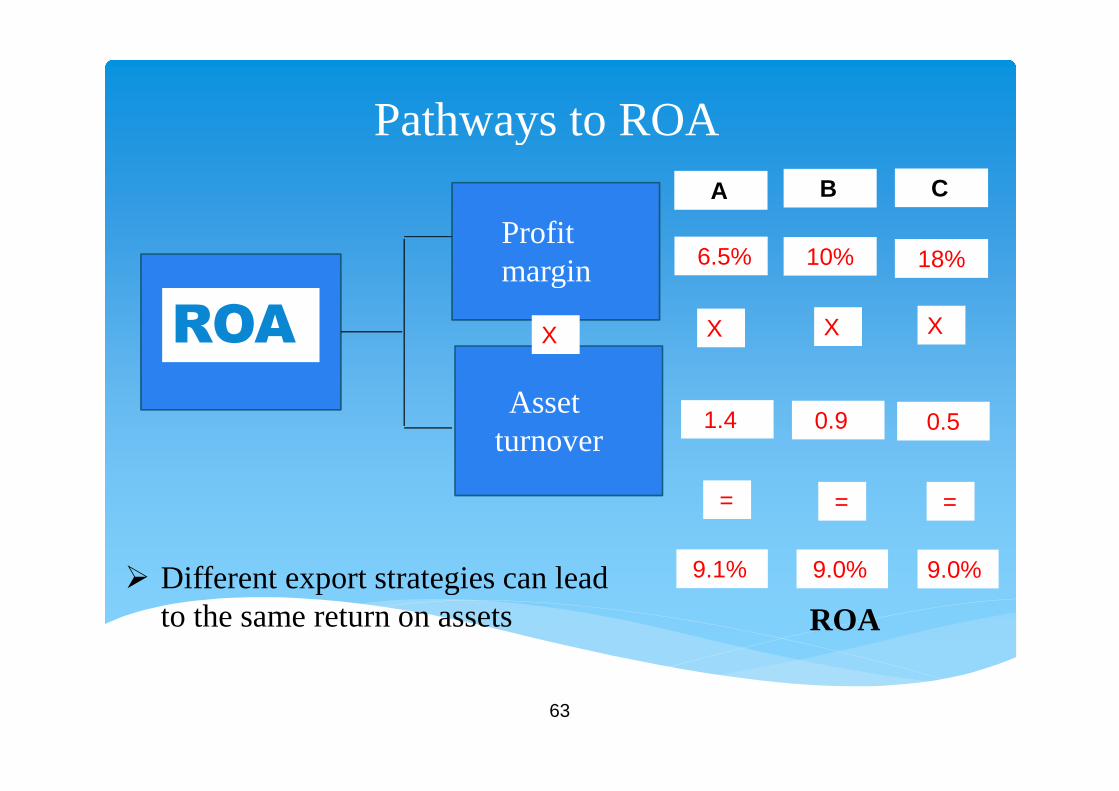

Pathways to ROA

Assetturnover

Profitmargin

X

6.5%

1.4

9.1%

10% 18%

X X X

0.9 0.5

= = =

9.0% 9.0%

A B C

Different export strategies can leadto the same return on assets ROA

ROA

64

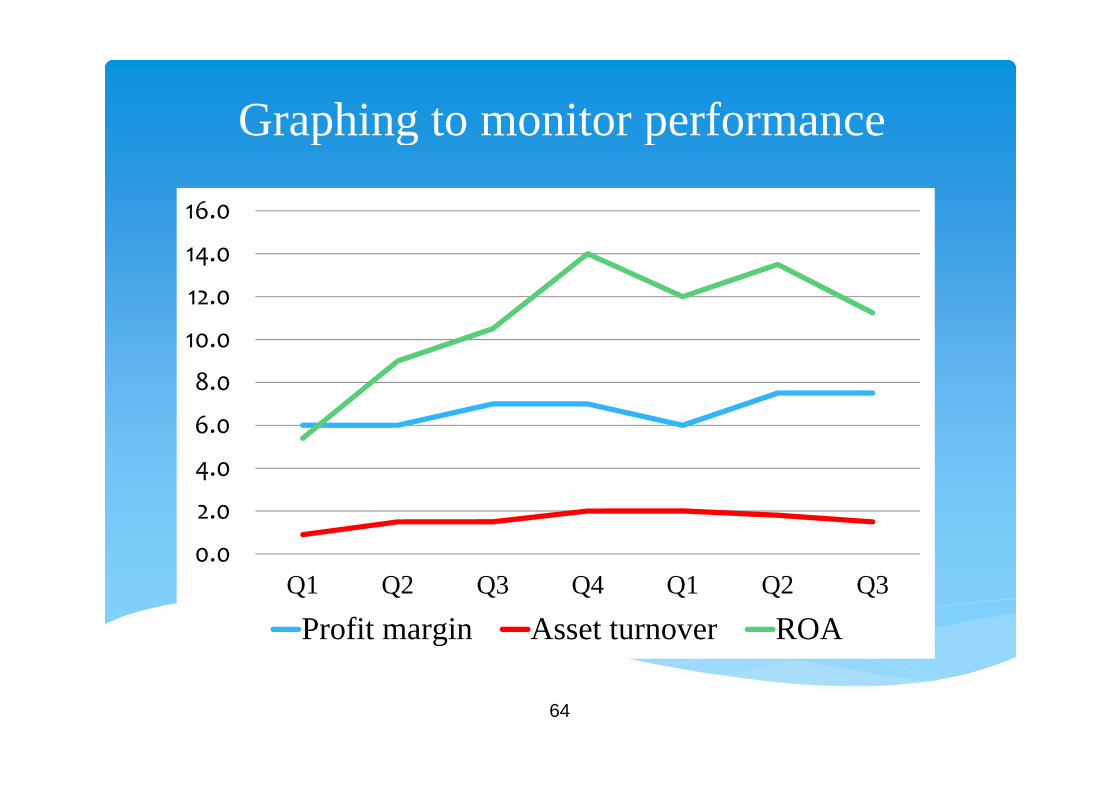

Graphing to monitor performance

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Profit margin Asset turnover ROA

65

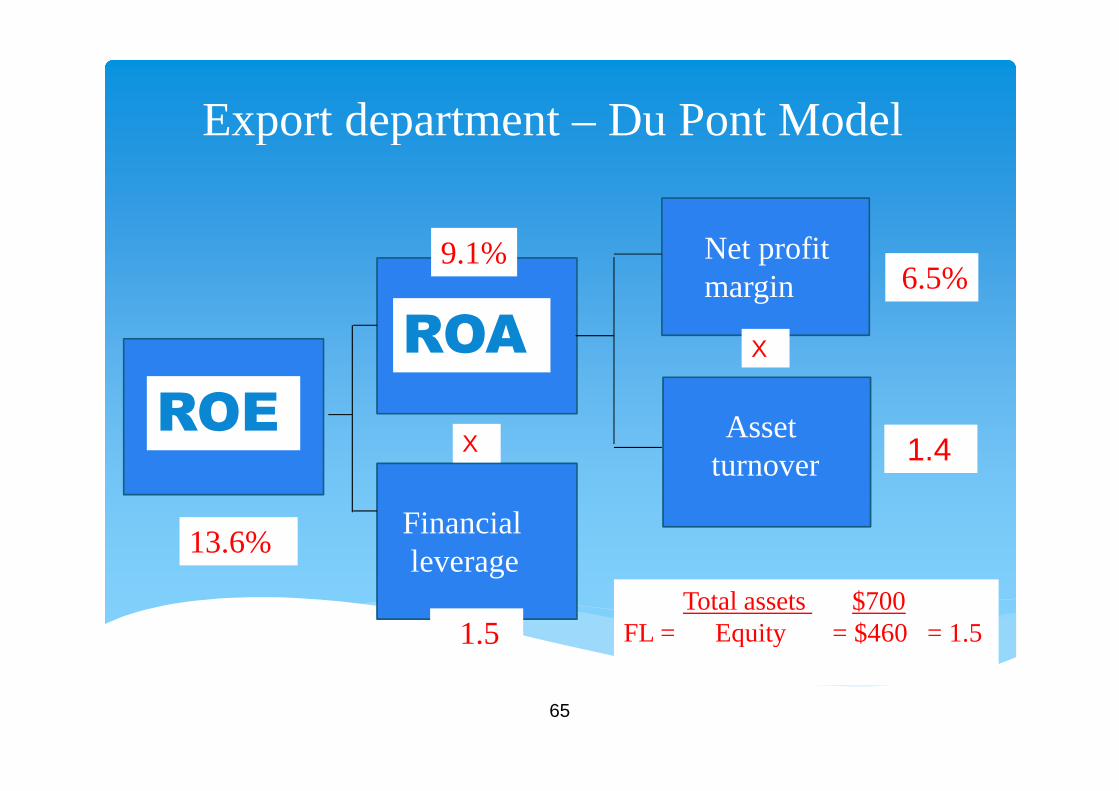

Export department – Du Pont Model

Assetturnover

Net profitmargin

X

6.5%

1.4

9.1%

Financialleverage

X

Total assets $700FL = Equity = $460 = 1.51.5

13.6%

ROE

ROA

66

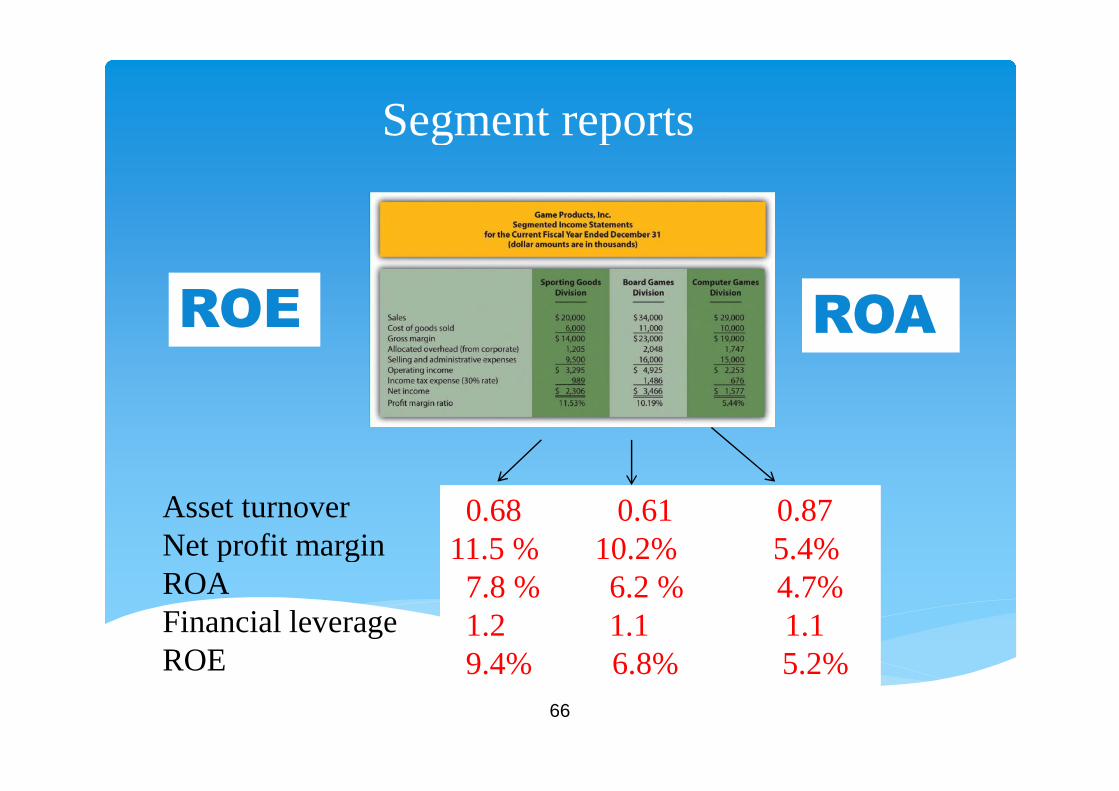

Segment reports

0.68 0.61 0.8711.5 % 10.2% 5.4%7.8 % 6.2 % 4.7%1.2 1.1 1.19.4% 6.8% 5.2%

Asset turnoverNet profit marginROAFinancial leverageROE

ROE ROA

67

Export department liquidity

Cash for continuedoperations

Cash for bills thatcome due

Without liquidity, business operations cannot continue

68

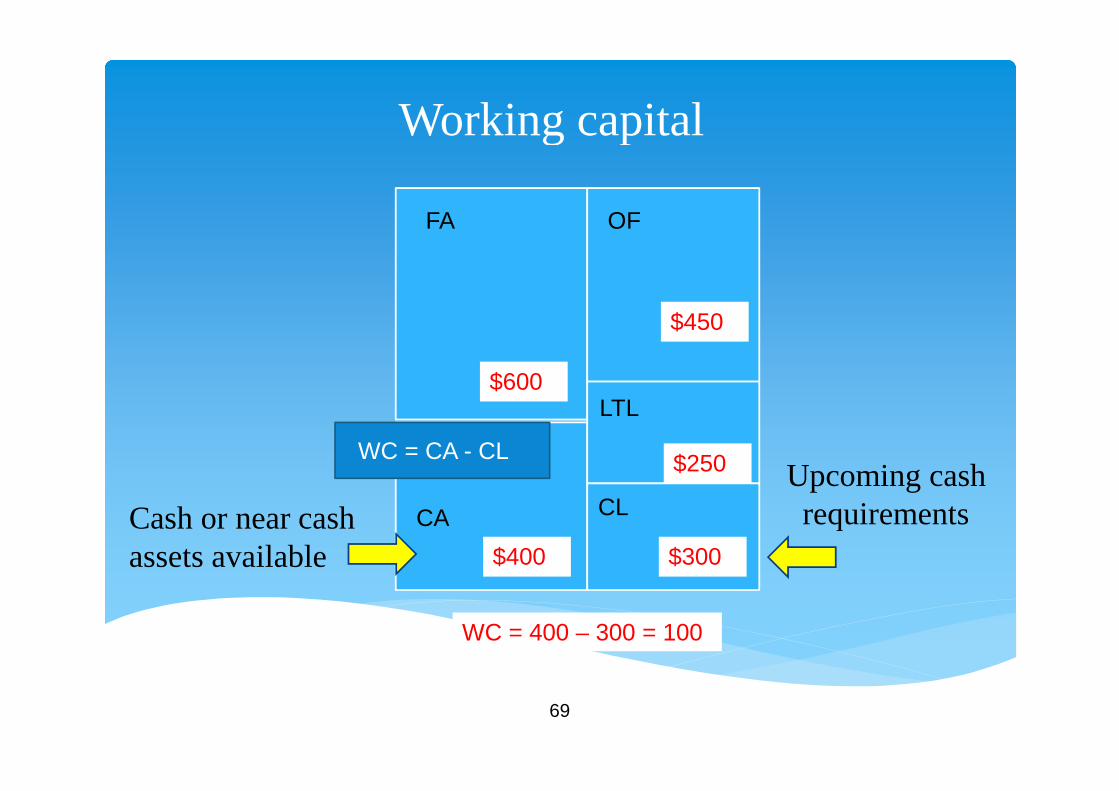

Working capital

Working capital – metric of liquidity Indicator of cash available to sustain operations Cash is in constant movement flowing through inventories,

collections and payments

69

Working capital

FA

CA

LTL

OF

CL

$600

$400

$450

$250

$300

WC = CA - CL

WC = 400 – 300 = 100

Cash or near cashassets available

Upcoming cashrequirements

70

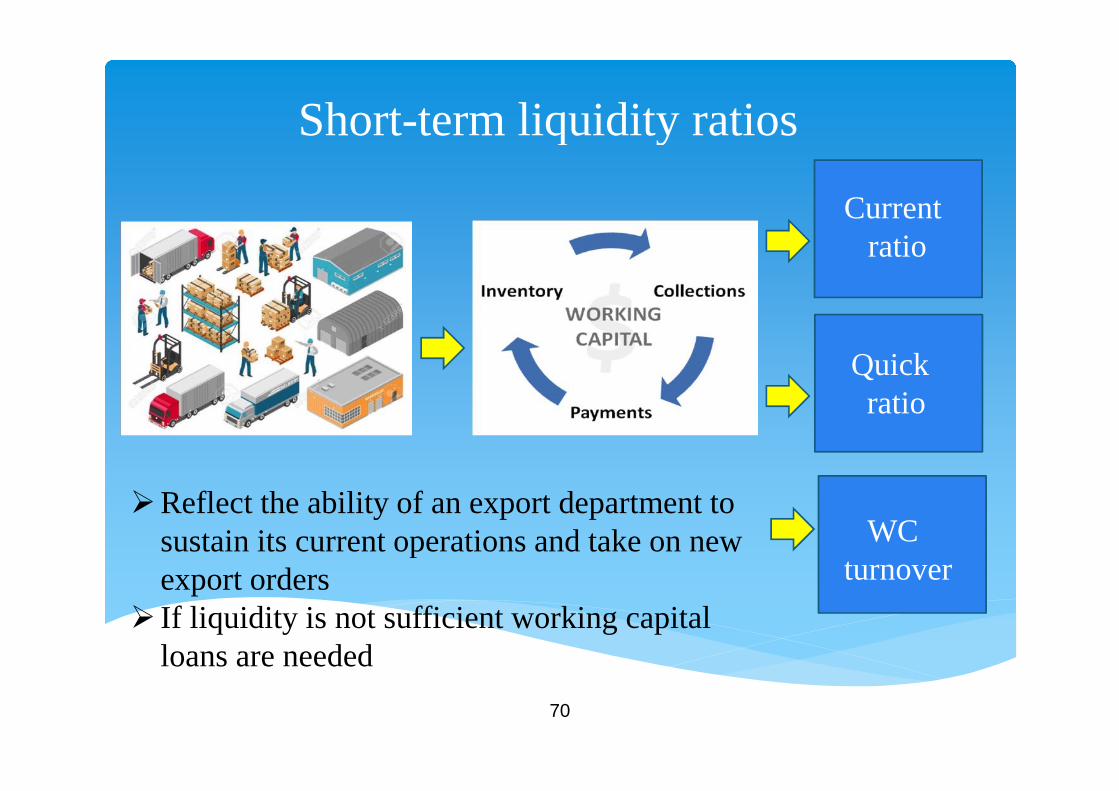

Short-term liquidity ratios

Currentratio

Quickratio

WCturnover

Reflect the ability of an export department tosustain its current operations and take on newexport orders

If liquidity is not sufficient working capitalloans are needed

71

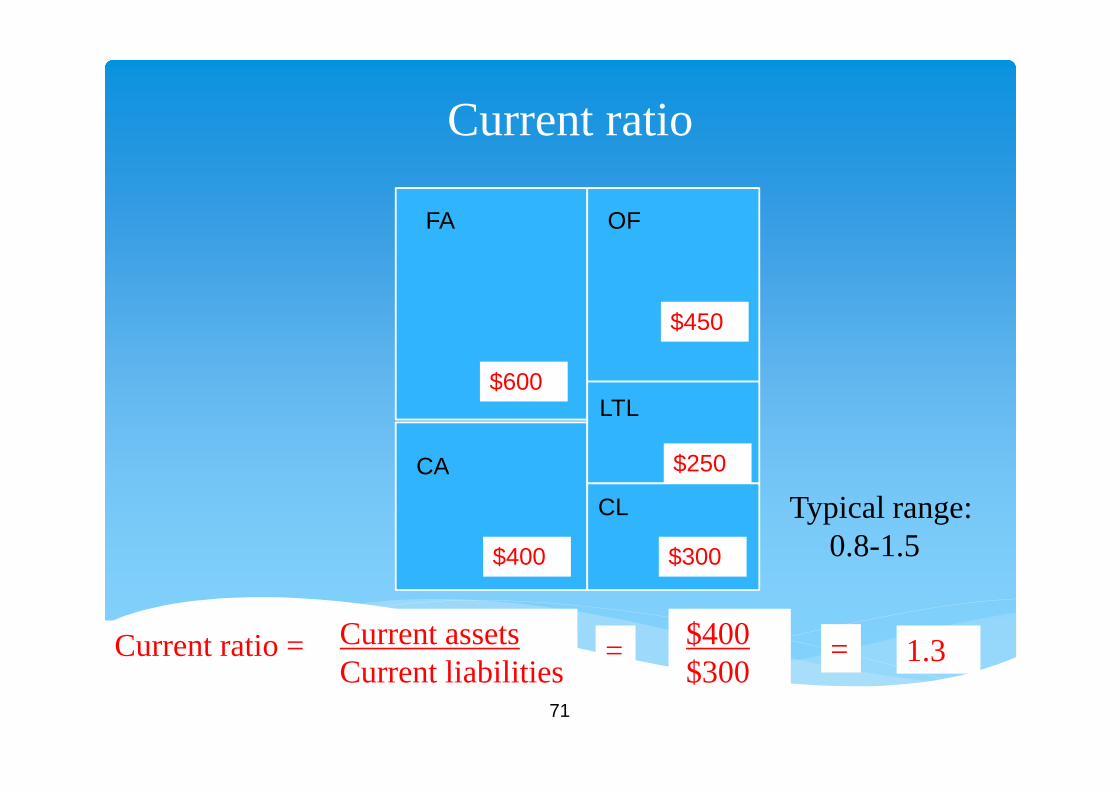

Current ratio

FA

CA

LTL

OF

CL

$600

$400

$450

$250

$300

Current assetsCurrent liabilities

$400$300

Current ratio = = = 1.3

Typical range:0.8-1.5

72

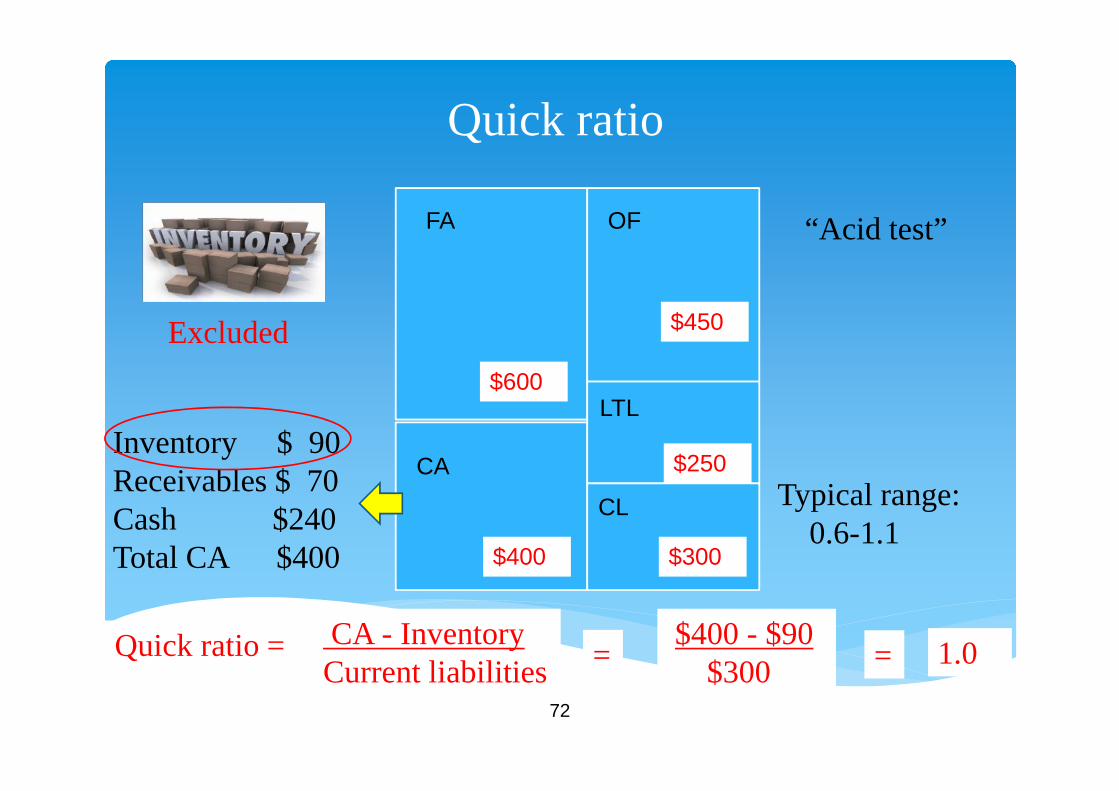

Quick ratio

FA

CA

LTL

OF

CL

$600

$400

$450

$250

$300

CA - InventoryCurrent liabilities

$400 - $90$300

Quick ratio = = = 1.0

Inventory $ 90Receivables $ 70Cash $240Total CA $400

Excluded

“Acid test”

Typical range:0.6-1.1

73

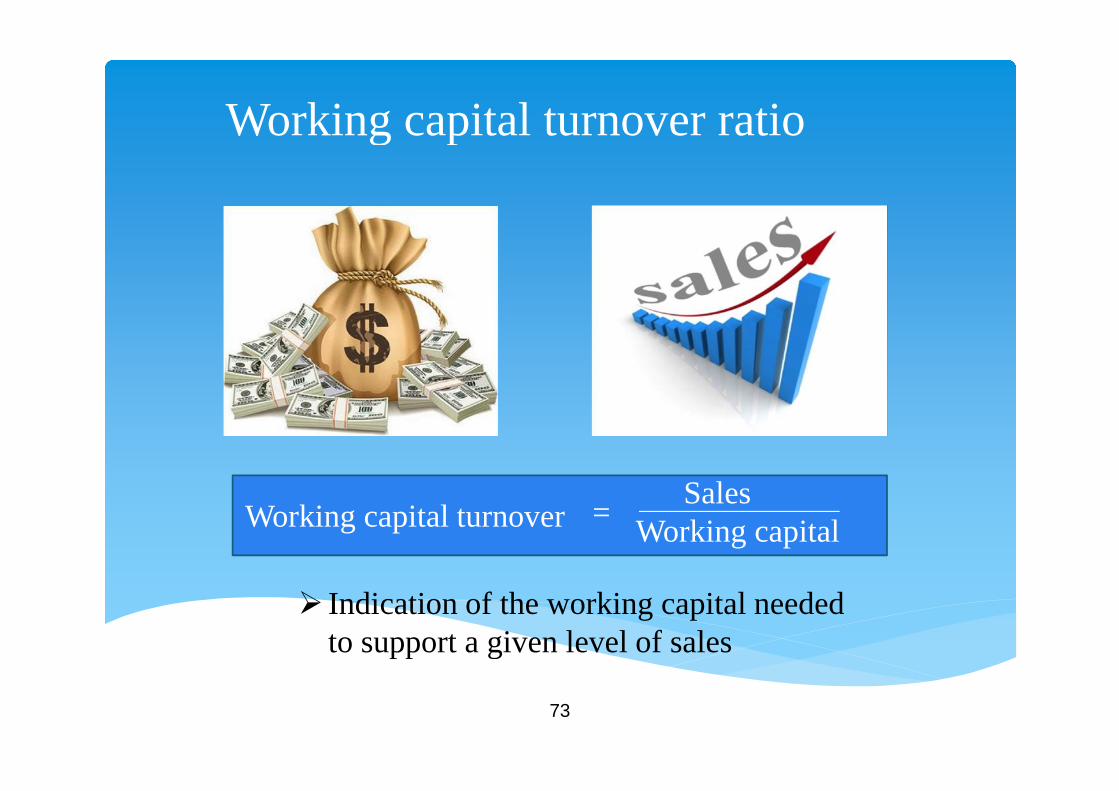

Working capital turnover ratio

Indication of the working capital neededto support a given level of sales

Working capital turnoverSales

Working capital=

74

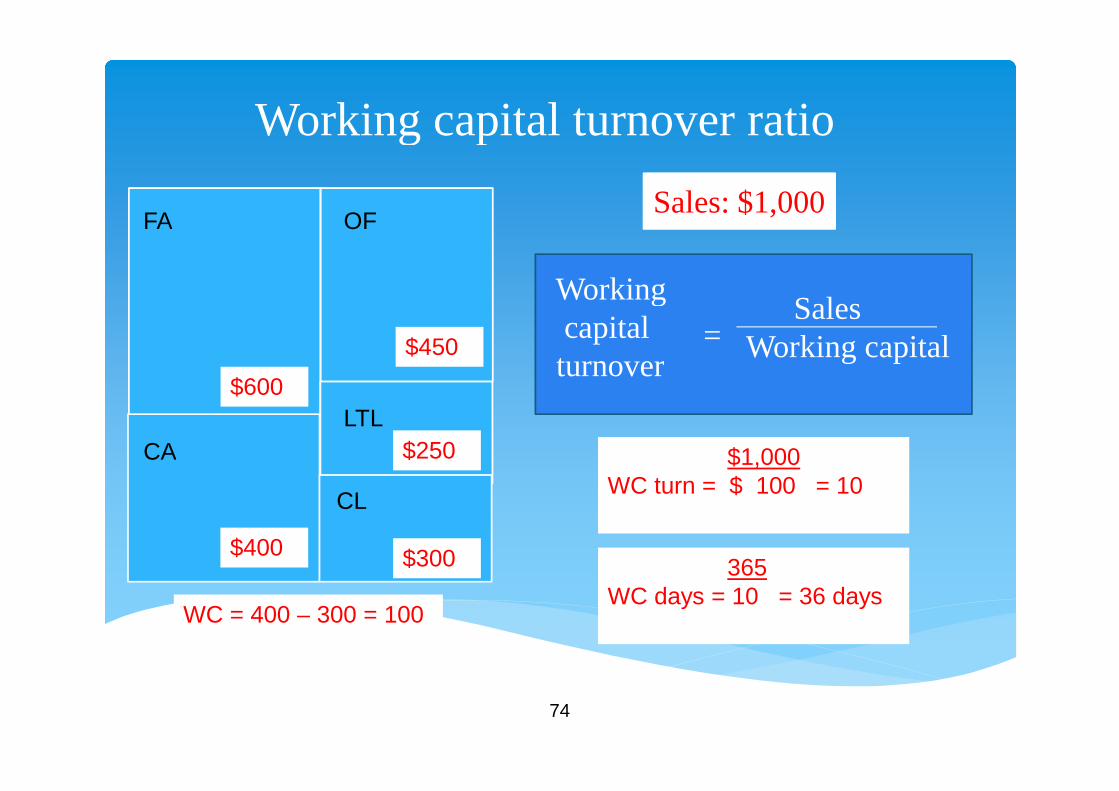

Working capital turnover ratio

FA

CA

LTL

OF

CL

$600

$400

$450

$250

$300

WC = 400 – 300 = 100

Sales: $1,000

Workingcapitalturnover

SalesWorking capital=

$1,000WC turn = $ 100 = 10

365WC days = 10 = 36 days

75

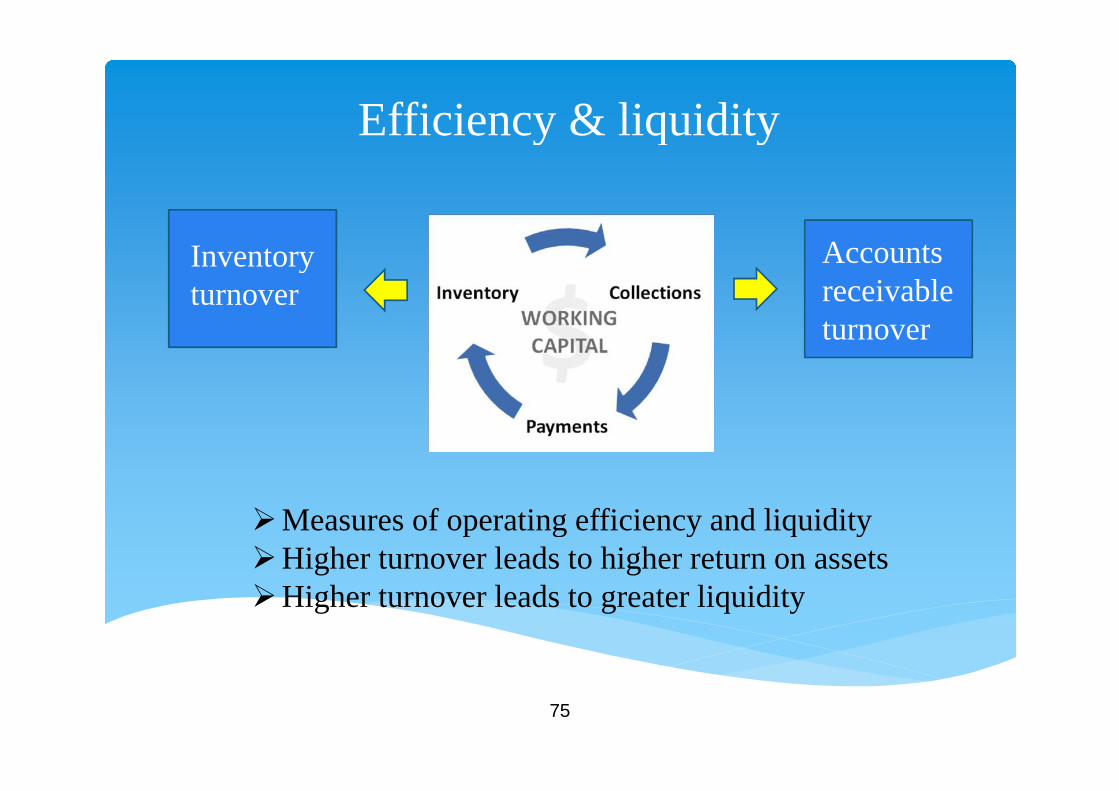

Efficiency & liquidity

Accountsreceivableturnover

Inventoryturnover

Measures of operating efficiency and liquidityHigher turnover leads to higher return on assetsHigher turnover leads to greater liquidity

76

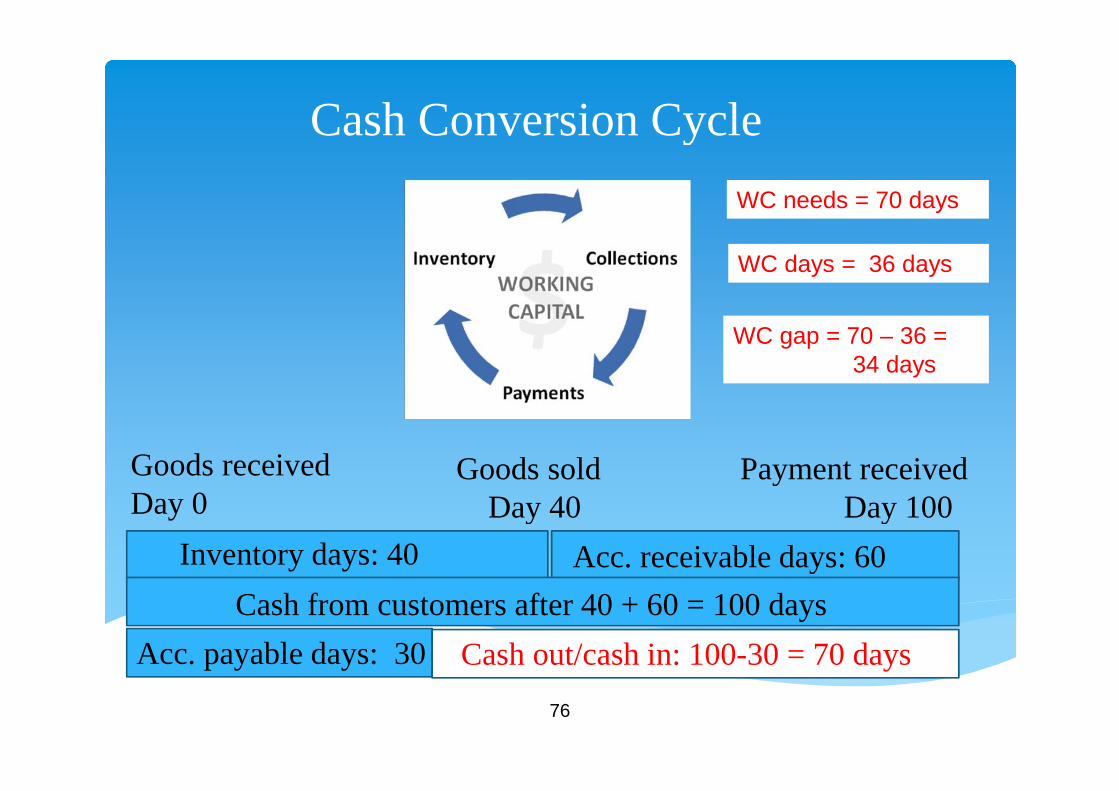

Cash Conversion Cycle

Goods receivedDay 0

Goods soldDay 40

Payment receivedDay 100

Inventory days: 40 Acc. receivable days: 60

Acc. payable days: 30

Cash from customers after 40 + 60 = 100 days

Cash out/cash in: 100-30 = 70 days

WC days = 36 days

WC gap = 70 – 36 =34 days

WC needs = 70 days

77

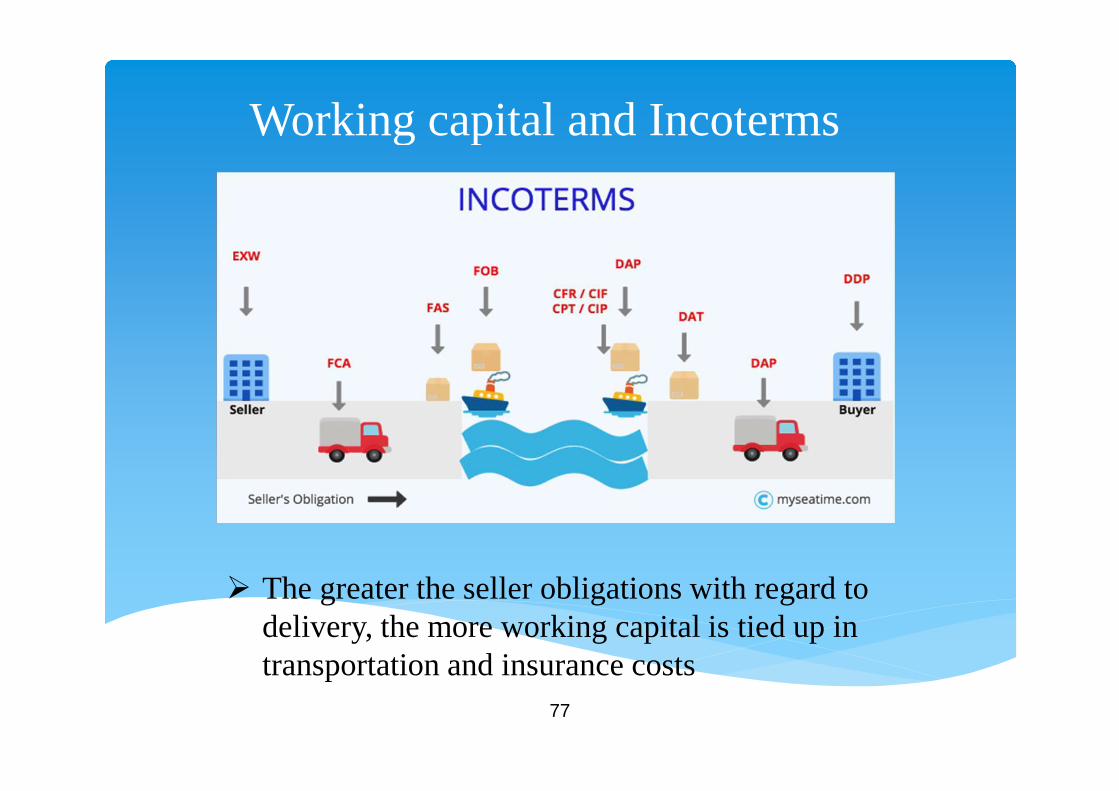

Working capital and Incoterms

The greater the seller obligations with regard todelivery, the more working capital is tied up intransportation and insurance costs

78

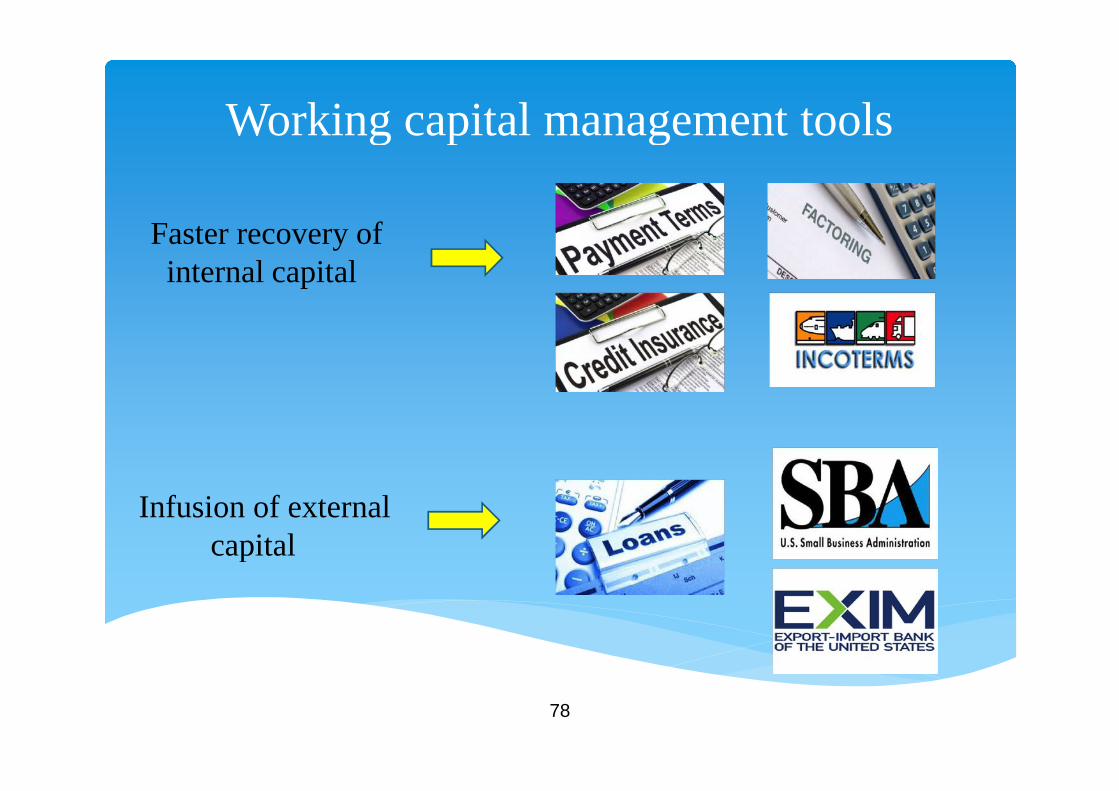

Working capital management tools

Faster recovery ofinternal capital

Infusion of externalcapital

79

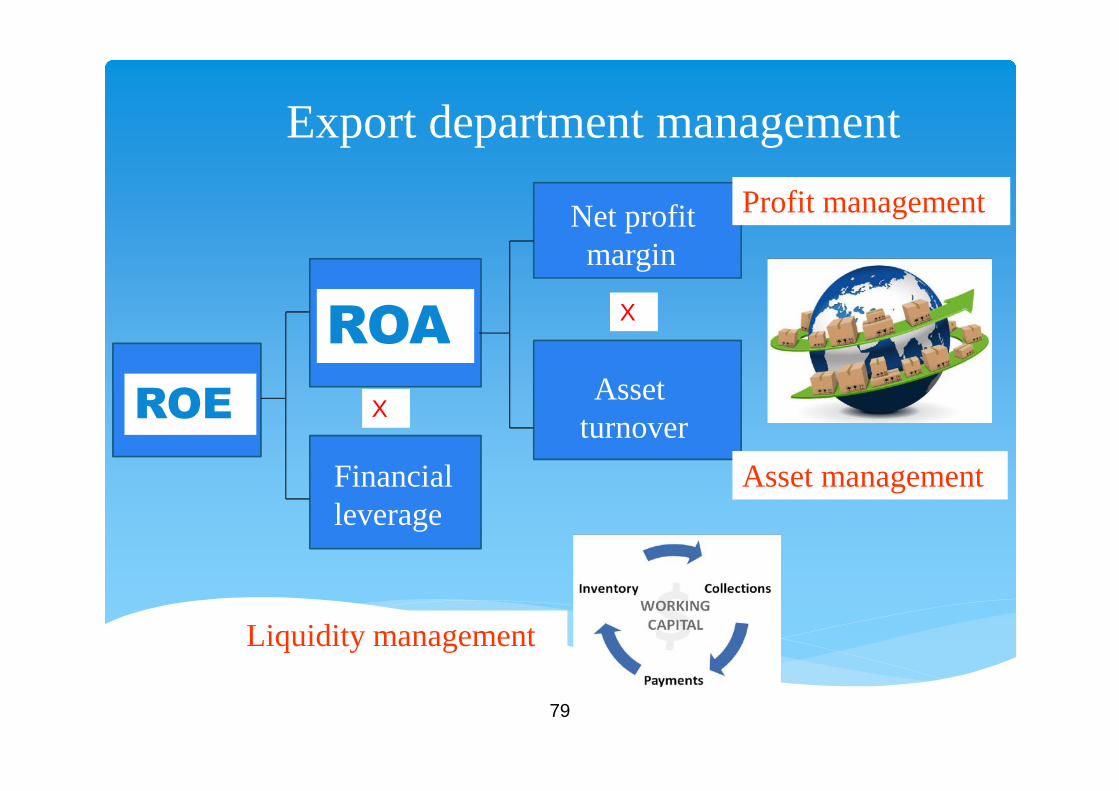

Export department management

Assetturnover

Net profitmargin

Profit management

Asset management

X

Liquidity management

X

Financialleverage

ROE

ROA

80

Export department management

Develop, monitor and manage key metrics and ratios toachieve a high return on export investment