key findings from the ey global consumer insurance survey 2014 · the ey global consumer insurance...

TRANSCRIPT

Reimagining customer relationshipsKey findings from the EY Global Consumer Insurance Survey 2014

Americas

Reimagining customer relationshipsKey findings from the EY Global Consumer Insurance Survey 2014Americas

01 Executive summary

02 Aboutthisreport|Keyfindings

04 Keyfinding1: High turnover and low trust signal serious relationship issues.

10 Keyfinding2: Just because they leave you doesn’t mean they don’t love you.

14 Keyfinding3: Insurers have so few interactions with their customers that each one becomes a critical moment of truth.

20 Keyfinding4: Consumers want more frequent, meaningful and personalized

communications.

24 Keyfinding5: As consumers embrace digital, insurers must rethink their

distribution strategies and partner relationships.

28 Conclusion | Key contacts in the Americas

Contents

4

30

countries

24,000

people

1

Executive summary

Two years after EY’s inaugural Global Consumer Insurance Survey, results from the 2014 survey confirm that the insurance industry is facing the same type of digital-driven and consumer-led disruption that retail, banking, media and entertainment, and other sectors have experienced in recent years. Indeed, insurers have much work to do in delivering the customized experiences, intuitive toolsets and easy information access that today’s informed and empowered customers require.

The following key findings, as well as the details and analysis in this report, outline the breadth, depth and urgency of the customer-facing challenges:

1. High turnover and low trust signal serious relationship issues.

2. Just because they leave you doesn’t mean they don’t love you.

3. Insurers have so few interactions with their customers that each one becomes a critical moment of truth.

4. Consumers want more frequent, meaningful and personalized communications.

5. As consumers embrace digital, insurers must rethink their distribution strategies and partner relationships.

DavidP.Hollander Global and Americas Insurance Advisory Leader

KaenanHertz US Insurance Customer Leader

Looking deeply at the results highlights some of the unique issues insurers face. For instance, more insurance consumers switch providers than express an intent to switch (an almost unprecedented finding in consumer research). Similarly, turnover is high even among “advocates” and large percentages of customers have essentially no interactions with their insurers over long periods of time. All of these issues have direct — and potentially severe — impacts on the bottom line.

It’s clear that the time has come for insurers to rethink their approach to customer relationships. For one thing, they must assume responsibility for the overall health of all customer relationships. For another, they must greatly improve their customer intelligence by embracing advanced analytics. Tomorrow’s top performers will be notable for having accurate and actionable insights into shifting consumer needs. Further, they will gain the ability to act predictively, precisely and nimbly in advance of key decision points and to offer relevant and timely solutions, independent of channel, during critical interactions.

Achieving customer centricity and stronger customer relationships will be a long-term journey for insurers — but it’s one that must begin now. The findings and analysis on the following pages will help insurers navigate the most formidable obstacles and seize the highest-value opportunities along that journey, beginning with immediate-term steps.

2

About this report

This regional overview complements the EY Global Consumer Insurance Survey 2014 report and provides a snapshot of detailed findings and data for the Americas region.

The report compares some of our global findings with survey data for the four countries in this region, using the following groupings:

• Mature markets in North America: the US and Canada

• Developing markets in Latin America: Brazil and Mexico

Definingourterms

The following definitions are used in the report, most notably in key finding 3.

Moment of truth = an interaction or experience that positively or negatively changed customer perceptions of their insurer or broker

Positiveoutcomes = coverage increases, the opening of new policies or higher favorability ratings from the consumer

Negative outcomes = coverage reductions, policy closures or lower favorability ratings

The EY Global Consumer Insurance Survey 2014 confirms that strengthening customer relationships and achieving customer centricity in core operations have become strategic imperatives for the insurance industry across product classifications, geographies and the full range of operating models.

EY Global Consumer Insurance Survey 2014

Keyfindings

High turnover and low trust signal serious relationship issues.

1.

Just because they leave you doesn’t mean they don’t love you.

2.

Insurers have so few interactions with their customers that each one becomes a critical moment of truth.

3.

Consumers want more frequent, meaningful and personalized communications.

4.

As consumers embrace digital, insurers must rethink their distribution strategies and partner relationships.

5.

3

4

Keyfinding1:

High turnover and low trust signal serious relationship issues. For life and auto insurance, customers within the Americas place a much stronger emphasis on the role of cost and terms.

5

If there is consensus about anything in the insurance industry, it is that turnover rates are too high. Findings from the Global Consumer Insurance Survey report indicate several of the underlying drivers. For instance, insurance companies register lower levels of trust compared to other industries. In the Americas, insurance companies rank toward the bottom of the list — though not quite as low as in the global rankings.

Respondents from both mature and developing markets within the Americas report higher levels of trust than their global counterparts (Figure 1). Latin American consumers in particular show a much higher relative trust than consumers in other developing markets around the world. This is consistent with the global findings, where consumers in developing markets report higher levels of trust than those in mature markets.

Just as troubling as the low level of trust is that far more insurance consumers actually switch insurers than express an intention to switch — an exceedingly rare phenomenon. In market research encompassing other industries, the vast majority of consumer studies find that anticipated switching or intent to switch almost always surpasses actual switching rates.

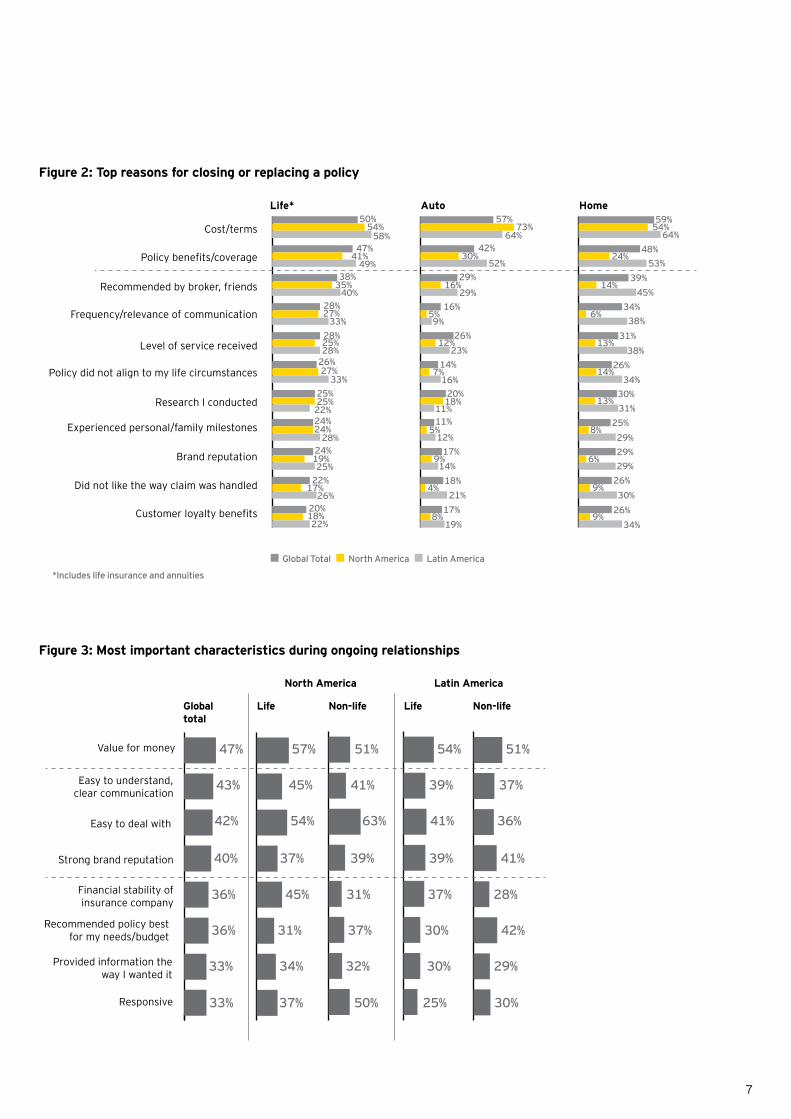

SignificantfocusoncostandtermsGenerally speaking, customers from the Americas close or replace policies for the same reasons as global consumers. Cost and policy benefits rank as the top two reasons for policy closure across life, auto and home policies (Figure 2). However, there are differences within the region compared to global results.

For life and especially auto insurance, customers in the Americas place a much stronger emphasis on the role of cost and terms. More than 7 in 10 auto auto insurance customers in North America, for example, leave because of cost — a far higher percentage than among all global consumers. For Latin American consumers, policy benefits and coverage and recommendations of brokers and friends play a more important role in policy closures across all product types. North America bucks the global trend quite dramatically in non-life, where communications and service levels are not reported as significant factors, reflecting this market’s dominant focus on cost.

Figure1:Percentageofconsumersciting“completetrust”and“moderatetrust”bytypeofbusiness

70%Insurance companies

84%

78%

82%

80%

68%

62%

86%

77%

69%

74%

62%

75%

84%

79%

90%

84%

72%

65%

89%

78%

73%

64%

55%

Supermarkets

Online shopping

sites

Banks

Car manufacturers

Pharmaceutical companies

81%

87%

77%

80%

90%

83%

Latin America

North America

Global Developing Markets

Global Mature Markets

Global Total

Americas:Reimagining customer relationships

6

HighercustomerserviceexpectationsintheAmericasIn terms of what matters most to consumers during their relationship with insurers, “value for money” is important, which is consistent with global findings. However, customers in North America place much stronger emphasis on client service characteristics than global customers (Figure 3). In particular, being “easy to deal with” is more important than “value for money” (60% vs. 53%, respectively) in North America. Being responsive is also viewed as a more important relationship characteristic in North America than globally, especially for non-life products.

These higher customer service expectations do not appear to be limited to a particular sales channel: compared to global results, being “easy to deal with” is viewed as more important across all channels. Responsiveness is considered more important among those buying their insurance from brokers or agents. Interestingly, consumers in the Americas who buy directly from an insurance company are far more likely than their global counterparts to emphasize “value for money” (65% in Americas vs. 54% globally).

For direct writers, many of whom differentiate themselves based on price, this presents clear challenges, given that 70% of North American auto customers who leave do so because of price. Direct-to-consumer insurers may believe they have mastered service, but the findings show that independent brokers are more effective in recommending the best product and dedicated agents are viewed as highly responsive.

The bottom line is that direct-writing insurers are clearly falling short in critical areas and can apply lessons learned from intermediaries in these areas. However, it is important to note that no distribution channel is performing at peak levels. When it comes to satisfying customers, every sales channel has room for improvement.

PositivebrokerandagentrelationshipexperiencesMany global insights regarding consumer satisfaction with the most important characteristics also apply to the Americas. Those using an independent agent or broker report positive experiences on most key relationship characteristics; however, a notable exception is the vulnerability that exists around perceived “value for money.” (Vulnerabilities are defined as areas rated as highly important, but with relatively low satisfaction levels.)

While our analysis did not highlight clear vulnerabilities among dedicated agent channels in the region, “understanding customers’ needs and preferences” and “value for money” look dangerously close to becoming vulnerabilities. Furthermore, customers buying directly from insurers indicate that communication-related aspects of their relationship with their insurer are “at or nearing” vulnerable levels. The two most cited examples are “easy to understand, clear communication” and “provided information the way I want it.” The role of communications seems to play a critical role across multiple dimensions of the relationships and all channels, a point explored in more detail in several other sections of this report.

7

Figure2:Topreasonsforclosingorreplacingapolicy

50%

47%41%

49%38%

28%27%

33%28%25%28%

26%27%

33%25%25%22%24%24%

28%24%19%25%

22%

20%18%22%

17%26%

35%40%

54%58%

Cost/terms

Life*57%

42%30%

52%29%

29%16%

5%9%

26%12%

23%14%

7%16%

20%18%

11%11%

5%12%

17%9%

14%18%

4%21%

17%8%

19%

16%

73%64%

59%54%

64%48%

24%53%

39%14%

13%

14%

38%26%

34%30%

13%31%

25%29%29%

26%

26%

29%

30%

34%

8%

6%

9%

9%

6%

45%34%38%

31%

Policy benefits/coverage

Recommended by broker, friends

Frequency/relevance of communication

Level of service received

Policy did not align to my life circumstances

Research I conducted

Experienced personal/family milestones

Brand reputation

Did not like the way claim was handled

Customer loyalty benefits

Auto Home

North America Latin AmericaGlobal Total

*Includes life insurance and annuities

Figure3:Mostimportantcharacteristicsduringongoingrelationships

47%Value for money

Globaltotal

Easy to understand, clear communication

Easy to deal with

Strong brand reputation

Financial stability of insurance company

Recommended policy best for my needs/budget

Provided information the way I wanted it

Responsive

43%

42%

40%

36%

36%

33%

33%

57%

45%

54%

37%

45%

31%

34%

37%

51%

41%

63%

39%

31%

37%

32%

50%

54%

39%

41%

39%

37%

30%

30%

25%

51%

37%

36%

41%

28%

42%

29%

30%

Life

North America Latin America

Non-life Life Non-life

Americas:Reimagining customer relationships

8

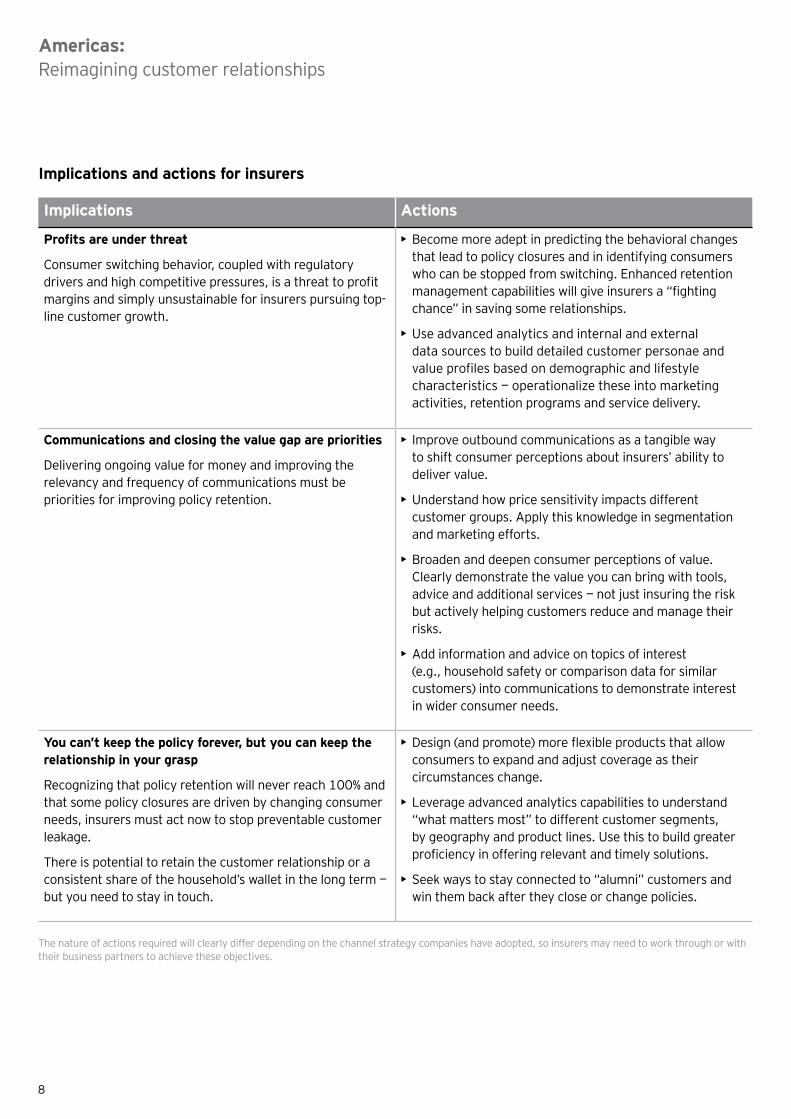

Implicationsandactionsforinsurers

Implications Actions

Profitsareunderthreat

Consumer switching behavior, coupled with regulatory drivers and high competitive pressures, is a threat to profit margins and simply unsustainable for insurers pursuing top-line customer growth.

• Become more adept in predicting the behavioral changes that lead to policy closures and in identifying consumers who can be stopped from switching. Enhanced retention management capabilities will give insurers a “fighting chance” in saving some relationships.

• Use advanced analytics and internal and external data sources to build detailed customer personae and value profiles based on demographic and lifestyle characteristics — operationalize these into marketing activities, retention programs and service delivery.

Communicationsandclosingthevaluegaparepriorities

Delivering ongoing value for money and improving the relevancy and frequency of communications must be priorities for improving policy retention.

• Improve outbound communications as a tangible way to shift consumer perceptions about insurers’ ability to deliver value.

• Understand how price sensitivity impacts different customer groups. Apply this knowledge in segmentation and marketing efforts.

• Broaden and deepen consumer perceptions of value. Clearly demonstrate the value you can bring with tools, advice and additional services — not just insuring the risk but actively helping customers reduce and manage their risks.

• Add information and advice on topics of interest (e.g., household safety or comparison data for similar customers) into communications to demonstrate interest in wider consumer needs.

Youcan’tkeepthepolicyforever,butyoucankeeptherelationship in your grasp

Recognizing that policy retention will never reach 100% and that some policy closures are driven by changing consumer needs, insurers must act now to stop preventable customer leakage.

There is potential to retain the customer relationship or a consistent share of the household’s wallet in the long term — but you need to stay in touch.

• Design (and promote) more flexible products that allow consumers to expand and adjust coverage as their circumstances change.

• Leverage advanced analytics capabilities to understand “what matters most” to different customer segments, by geography and product lines. Use this to build greater proficiency in offering relevant and timely solutions.

• Seek ways to stay connected to “alumni” customers and win them back after they close or change policies.

The nature of actions required will clearly differ depending on the channel strategy companies have adopted, so insurers may need to work through or with their business partners to achieve these objectives.

9

10

Keyfinding2:

Just because they leave you doesn’t mean they don’t love you.The likelihood to recommend and other measures of consumer advocacy have become common proxies of overall brand health. In some industries, they are the dominant means by which executives assess the strength of customer relationships. The survey results demonstrate that traditional loyalty measures may not be strong indicators of actual behavior in the global insurance marketplace.

11

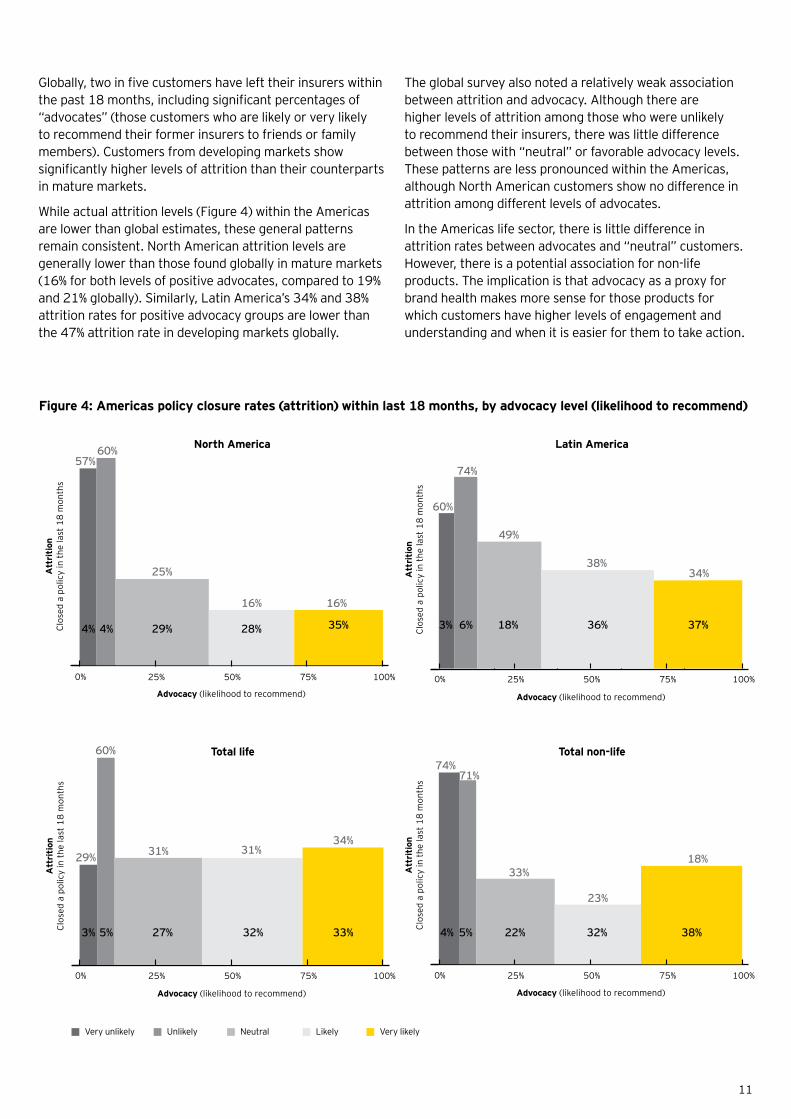

Globally, two in five customers have left their insurers within the past 18 months, including significant percentages of “advocates” (those customers who are likely or very likely to recommend their former insurers to friends or family members). Customers from developing markets show significantly higher levels of attrition than their counterparts in mature markets.

While actual attrition levels (Figure 4) within the Americas are lower than global estimates, these general patterns remain consistent. North American attrition levels are generally lower than those found globally in mature markets (16% for both levels of positive advocates, compared to 19% and 21% globally). Similarly, Latin America’s 34% and 38% attrition rates for positive advocacy groups are lower than the 47% attrition rate in developing markets globally.

The global survey also noted a relatively weak association between attrition and advocacy. Although there are higher levels of attrition among those who were unlikely to recommend their insurers, there was little difference between those with “neutral” or favorable advocacy levels. These patterns are less pronounced within the Americas, although North American customers show no difference in attrition among different levels of advocates.

In the Americas life sector, there is little difference in attrition rates between advocates and “neutral” customers. However, there is a potential association for non-life products. The implication is that advocacy as a proxy for brand health makes more sense for those products for which customers have higher levels of engagement and understanding and when it is easier for them to take action.

Figure4:Americaspolicyclosurerates(attrition)withinlast18months,byadvocacylevel(likelihoodtorecommend)

Total non-life

Advocacy (likelihood to recommend)

North America

16%

25%

60%

16%

0

10

20

30

40

50

60

0% 25% 50% 75% 100%

57%

29% 28% 35%4%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

Total life60%

0

10

20

30

40

50

60

29% 31% 31%34%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

27% 32% 33%5%3%

Latin America

Advocacy (likelihood to recommend)

49%

38%

74%

34%

0

10

20

30

40

50

60

70

80

60%

18% 36% 37%6%3%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

23%

33%

71%

18%

0

10

20

30

40

50

60

70

80 74%

22% 32% 38%5%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

Very likelyLikelyNeutralUnlikelyVery unlikely

Total non-life

Advocacy (likelihood to recommend)

North America

16%

25%

60%

16%

0

10

20

30

40

50

60

0% 25% 50% 75% 100%

57%

29% 28% 35%4%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

Total life60%

0

10

20

30

40

50

60

29% 31% 31%34%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

27% 32% 33%5%3%

Latin America

Advocacy (likelihood to recommend)

49%

38%

74%

34%

0

10

20

30

40

50

60

70

80

60%

18% 36% 37%6%3%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

23%

33%

71%

18%

0

10

20

30

40

50

60

70

80 74%

22% 32% 38%5%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

Very likelyLikelyNeutralUnlikelyVery unlikely

Total non-life

Advocacy (likelihood to recommend)

North America

16%

25%

60%

16%

0

10

20

30

40

50

60

0% 25% 50% 75% 100%

57%

29% 28% 35%4%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

Total life60%

0

10

20

30

40

50

60

29% 31% 31%34%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

27% 32% 33%5%3%

Latin America

Advocacy (likelihood to recommend)

49%

38%

74%

34%

0

10

20

30

40

50

60

70

80

60%

18% 36% 37%6%3%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

23%

33%

71%

18%

0

10

20

30

40

50

60

70

80 74%

22% 32% 38%5%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

Very likelyLikelyNeutralUnlikelyVery unlikely

Total non-life

Advocacy (likelihood to recommend)

North America

16%

25%

60%

16%

0

10

20

30

40

50

60

0% 25% 50% 75% 100%

57%

29% 28% 35%4%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

Total life60%

0

10

20

30

40

50

60

29% 31% 31%34%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

27% 32% 33%5%3%

Latin America

Advocacy (likelihood to recommend)

49%

38%

74%

34%

0

10

20

30

40

50

60

70

80

60%

18% 36% 37%6%3%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

23%

33%

71%

18%

0

10

20

30

40

50

60

70

80 74%

22% 32% 38%5%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

Very likelyLikelyNeutralUnlikelyVery unlikely

Total non-life

Advocacy (likelihood to recommend)

North America

16%

25%

60%

16%

0

10

20

30

40

50

60

0% 25% 50% 75% 100%

57%

29% 28% 35%4%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

Total life60%

0

10

20

30

40

50

60

29% 31% 31%34%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

27% 32% 33%5%3%

Latin America

Advocacy (likelihood to recommend)

49%

38%

74%

34%

0

10

20

30

40

50

60

70

80

60%

18% 36% 37%6%3%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

Advocacy (likelihood to recommend)

23%

33%

71%

18%

0

10

20

30

40

50

60

70

80 74%

22% 32% 38%5%4%

Att

riti

onCl

osed

a p

olic

y in

the

last

18

mon

ths

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

0% 25% 50% 75% 100%

Very likelyLikelyNeutralUnlikelyVery unlikely

Americas:Reimagining customer relationships

12

Implicationsandactionsforinsurers

Implications Actions

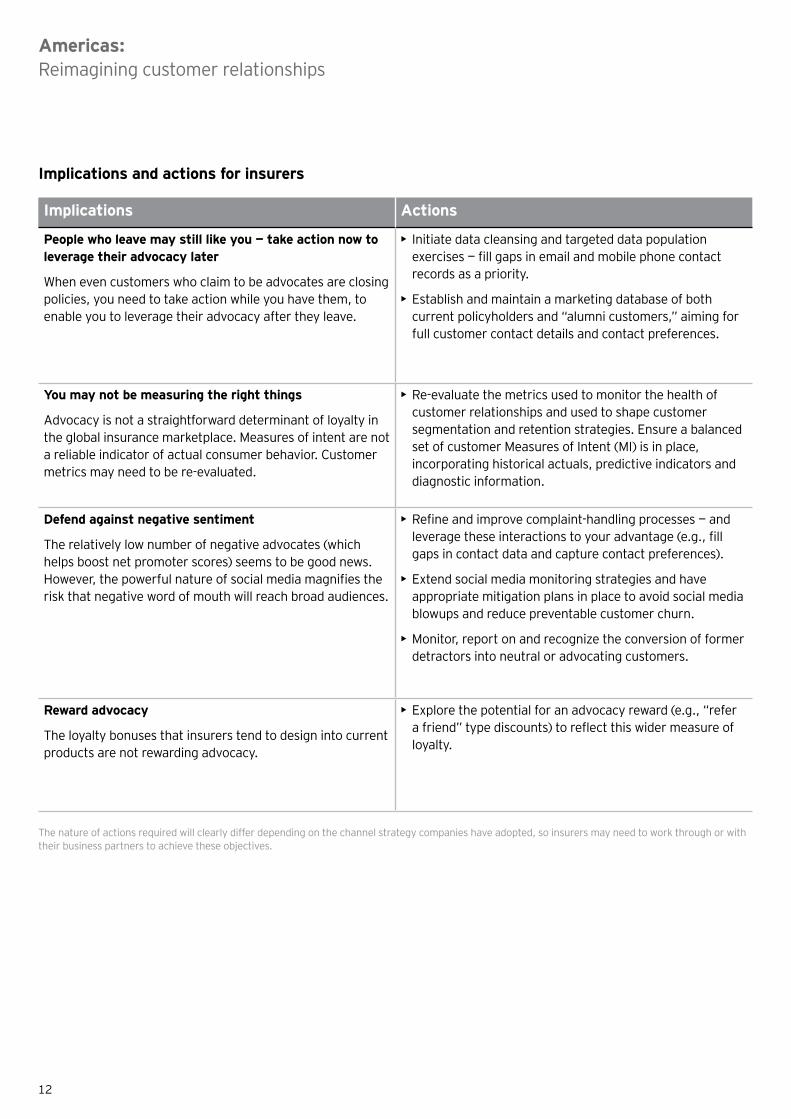

Peoplewholeavemaystilllikeyou—takeactionnowtoleveragetheiradvocacylater

When even customers who claim to be advocates are closing policies, you need to take action while you have them, to enable you to leverage their advocacy after they leave.

• Initiate data cleansing and targeted data population exercises — fill gaps in email and mobile phone contact records as a priority.

• Establish and maintain a marketing database of both current policyholders and “alumni customers,” aiming for full customer contact details and contact preferences.

You may not be measuring the right things

Advocacy is not a straightforward determinant of loyalty in the global insurance marketplace. Measures of intent are not a reliable indicator of actual consumer behavior. Customer metrics may need to be re-evaluated.

• Re-evaluate the metrics used to monitor the health of customer relationships and used to shape customer segmentation and retention strategies. Ensure a balanced set of customer Measures of Intent (MI) is in place, incorporating historical actuals, predictive indicators and diagnostic information.

Defendagainstnegativesentiment

The relatively low number of negative advocates (which helps boost net promoter scores) seems to be good news. However, the powerful nature of social media magnifies the risk that negative word of mouth will reach broad audiences.

• Refine and improve complaint-handling processes — and leverage these interactions to your advantage (e.g., fill gaps in contact data and capture contact preferences).

• Extend social media monitoring strategies and have appropriate mitigation plans in place to avoid social media blowups and reduce preventable customer churn.

• Monitor, report on and recognize the conversion of former detractors into neutral or advocating customers.

Rewardadvocacy

The loyalty bonuses that insurers tend to design into current products are not rewarding advocacy.

• Explore the potential for an advocacy reward (e.g., “refer a friend” type discounts) to reflect this wider measure of loyalty.

The nature of actions required will clearly differ depending on the channel strategy companies have adopted, so insurers may need to work through or with their business partners to achieve these objectives.

13

14

Keyfinding3:

Insurers have so few interactions with their customers that each one becomes a critical moment of truth. Far fewer insurance customers in the Americas experience a moment of truth than reported globally.

15

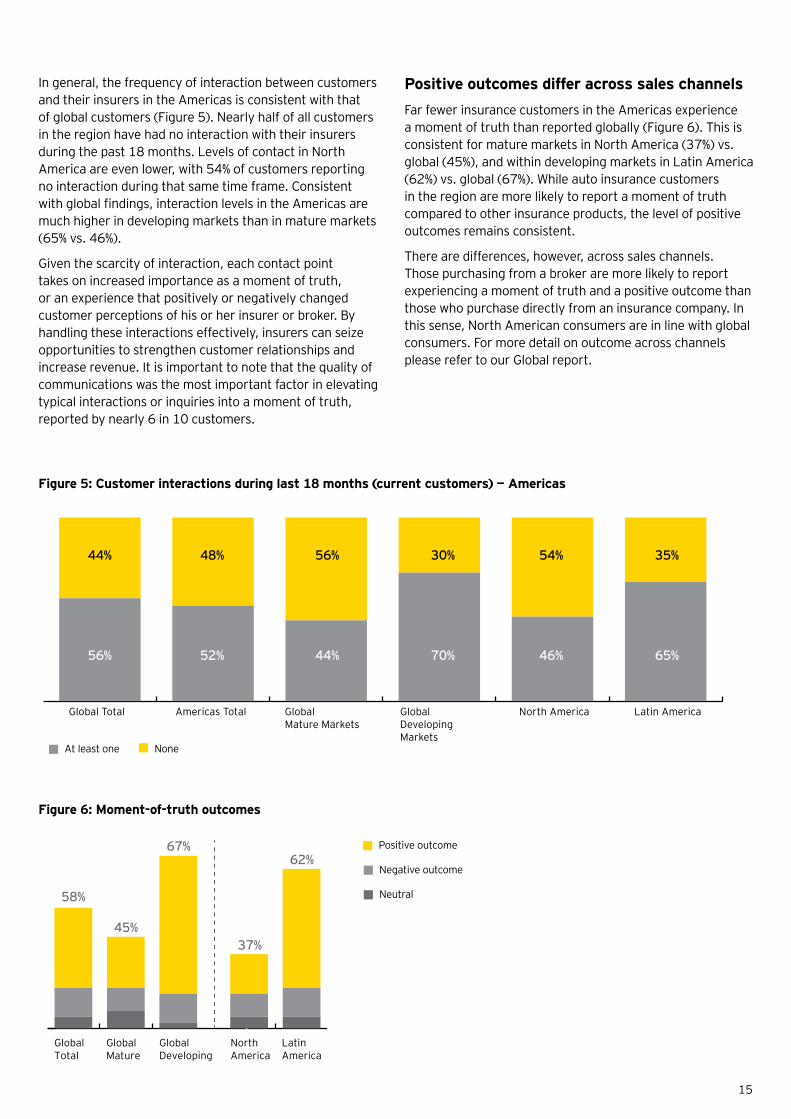

In general, the frequency of interaction between customers and their insurers in the Americas is consistent with that of global customers (Figure 5). Nearly half of all customers in the region have had no interaction with their insurers during the past 18 months. Levels of contact in North America are even lower, with 54% of customers reporting no interaction during that same time frame. Consistent with global findings, interaction levels in the Americas are much higher in developing markets than in mature markets (65% vs. 46%).

Given the scarcity of interaction, each contact point takes on increased importance as a moment of truth, or an experience that positively or negatively changed customer perceptions of his or her insurer or broker. By handling these interactions effectively, insurers can seize opportunities to strengthen customer relationships and increase revenue. It is important to note that the quality of communications was the most important factor in elevating typical interactions or inquiries into a moment of truth, reported by nearly 6 in 10 customers.

PositiveoutcomesdifferacrosssaleschannelsFar fewer insurance customers in the Americas experience a moment of truth than reported globally (Figure 6). This is consistent for mature markets in North America (37%) vs. global (45%), and within developing markets in Latin America (62%) vs. global (67%). While auto insurance customers in the region are more likely to report a moment of truth compared to other insurance products, the level of positive outcomes remains consistent.

There are differences, however, across sales channels. Those purchasing from a broker are more likely to report experiencing a moment of truth and a positive outcome than those who purchase directly from an insurance company. In this sense, North American consumers are in line with global consumers. For more detail on outcome across channels please refer to our Global report.

Figure5:Customerinteractionsduringlast18months(currentcustomers)—Americas

Global Total Global Mature Markets

GlobalDeveloping Markets

Americas Total North America Latin America

NoneAt least one

56%

44%

52%

48%

44%

56%

70%

30%

46%

54%

65%

35%

Figure6:Moment-of-truthoutcomes

0

5

10

15

20

2530

35

58%

45%

67%

37%

62%Positive outcome

Negative outcome

Neutral

Global Total

Global Mature

Global Developing

NorthAmerica

LatinAmerica

Americas:Reimagining customer relationships

16

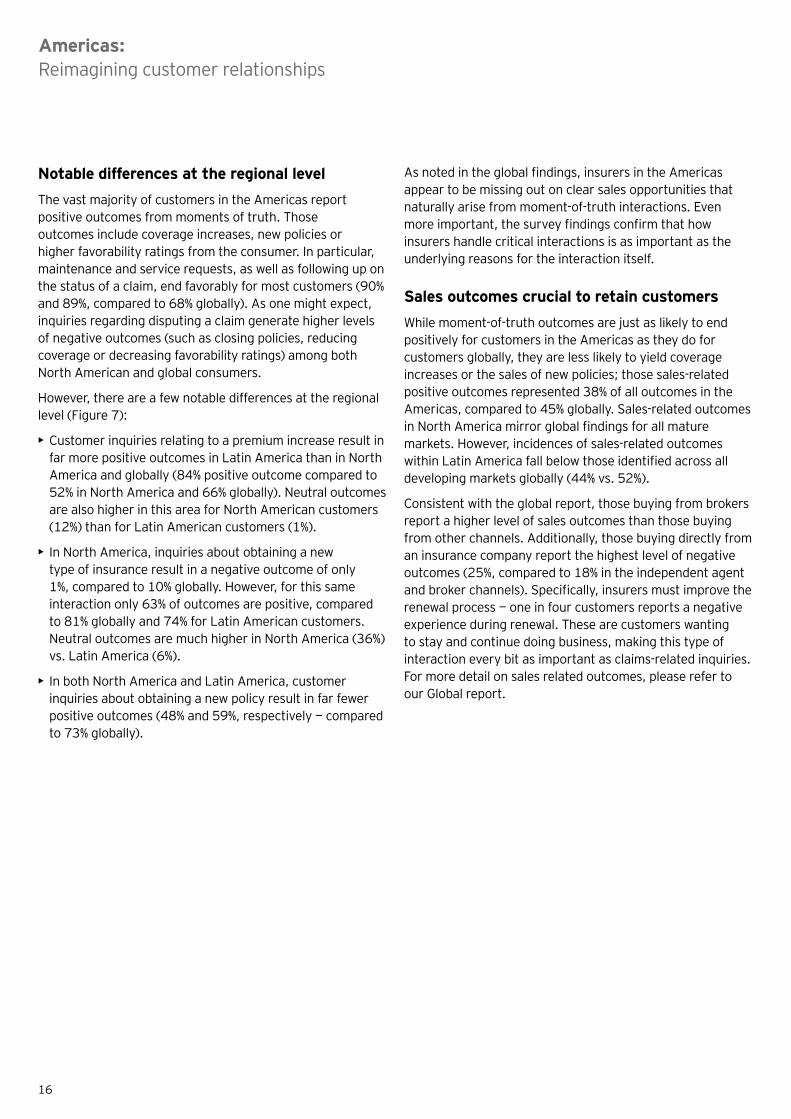

NotabledifferencesattheregionallevelThe vast majority of customers in the Americas report positive outcomes from moments of truth. Those outcomes include coverage increases, new policies or higher favorability ratings from the consumer. In particular, maintenance and service requests, as well as following up on the status of a claim, end favorably for most customers (90% and 89%, compared to 68% globally). As one might expect, inquiries regarding disputing a claim generate higher levels of negative outcomes (such as closing policies, reducing coverage or decreasing favorability ratings) among both North American and global consumers.

However, there are a few notable differences at the regional level (Figure 7):

• Customer inquiries relating to a premium increase result in far more positive outcomes in Latin America than in North America and globally (84% positive outcome compared to 52% in North America and 66% globally). Neutral outcomes are also higher in this area for North American customers (12%) than for Latin American customers (1%).

• In North America, inquiries about obtaining a new type of insurance result in a negative outcome of only 1%, compared to 10% globally. However, for this same interaction only 63% of outcomes are positive, compared to 81% globally and 74% for Latin American customers. Neutral outcomes are much higher in North America (36%) vs. Latin America (6%).

• In both North America and Latin America, customer inquiries about obtaining a new policy result in far fewer positive outcomes (48% and 59%, respectively — compared to 73% globally).

As noted in the global findings, insurers in the Americas appear to be missing out on clear sales opportunities that naturally arise from moment-of-truth interactions. Even more important, the survey findings confirm that how insurers handle critical interactions is as important as the underlying reasons for the interaction itself.

Sales outcomes crucial to retain customersWhile moment-of-truth outcomes are just as likely to end positively for customers in the Americas as they do for customers globally, they are less likely to yield coverage increases or the sales of new policies; those sales-related positive outcomes represented 38% of all outcomes in the Americas, compared to 45% globally. Sales-related outcomes in North America mirror global findings for all mature markets. However, incidences of sales-related outcomes within Latin America fall below those identified across all developing markets globally (44% vs. 52%).

Consistent with the global report, those buying from brokers report a higher level of sales outcomes than those buying from other channels. Additionally, those buying directly from an insurance company report the highest level of negative outcomes (25%, compared to 18% in the independent agent and broker channels). Specifically, insurers must improve the renewal process — one in four customers reports a negative experience during renewal. These are customers wanting to stay and continue doing business, making this type of interaction every bit as important as claims-related inquiries. For more detail on sales related outcomes, please refer to our Global report.

17

Neutral outcome Negative outcomePositive outcome

Inquire about obtaining a new type of insurance

Inquire about switching a policy from another provider

Obtain a new policy

Obtain information about the policy

Update information, such as your address

Follow up on the status of an existing claim

Dispute the resolution of a claim

Inquire about replacing an existing policy

Questions about a premium increase

North America

Inquire about obtaining a new type of insurance

Inquire about switching a policy from another provider

Obtain a new policy

Obtain information about the policy

Update information, such as your address

Follow up on the status of an existing claim

Dispute the resolution of a claim

Inquire about replacing an existing policy

Questions about a premium increase

Latin America

63% 74%6%

20%61%

12%27%

59%11%

30%75%

10%15%

88%7%

5%89%

3%8%

46%0%

54%75%

1%24%

84%1%

15%

36%1%

61%10%

29%48%

15%37%

81%12%

7%77%

19%4%

90%10%

0%32%

21%47%51%

11%38%

52%12%

37%

Figure7:Reasonsforcontactandoutcomesacrossdifferentphasesofthecustomerlifecyclerelationship:totalAmericas

Americas:Reimagining customer relationships

18

Implicationsandactionsforinsurers

Implications Actions

All the little interactions count

Empowered consumers have increasingly high expectations for every interaction they have with their insurers, even if those touch points are infrequent. Given the potential impact on satisfaction, even interactions that seem minor must be viewed in a competitive context. It is possible to win long-term loyalty by seizing small opportunities in the here and now.

• Develop the processes and system triggers to differentiate and automatically route customer inquiries to the right treatment, between inquiries that merit a “high touch” approach, such as questions about increasing coverage, versus those that can be routed to self-service channels.

• Develop effective front-end systems between the customer’s experience and legacy technology. For example, self-serve functionality eliminates the need for customers to duplicate processes or re-key data (e.g., common logon, one change of address for multiple policies).

Whencustomersdoengage,insurerscanrespondwell—buttherearetoofewengagements

It seems that insurers are very capable of succeeding when consumers engage them or have a specific problem to solve or task to handle. But since the engagement level is so low, insurers have relatively few opportunities to shine.

• Create more and better points of interaction through more frequent, proactive and meaningful communications, aligned to shifting consumer needs.

• Broaden the value proposition to create frequent and two-way opportunities to connect — for example, establishing affinity groups, customer clubs or rewards programs for specific communities and segments can boost engagement.

• Offer supplemental information on topics of interest (like household safety or safe driving tips, or comparison data for similar customers) to standard communications (like policy statements) to demonstrate interest in wider consumer needs.

Allinboundinquiriessignalanopportunityandapotential threat

There are obvious opportunities regarding inbound inquiries from consumers concerning increasing coverage or purchasing new products. These signal a clear intent to buy or move, a signal insurers must be prepared to heed and act upon. When those interactions end without a closed sale, the likelihood of attrition increases significantly.

But also recognize that any kind of inbound inquiry indicates a potentially dormant customer has “awakened.”

• Treat those customer inquiries (coverage or option related) as priority “flight risks.” Focus retention programs on improving handling of these highest-priority inquiries, and monitor up-selling performance in those instances.

• When customers actively reach out to you, this often indicates a life event or circumstance change. Leverage this opportunity to understand and capture these changes in customer records — and use this to deliver a positive moment of truth, including follow-up contact and offerings.

19

Implicationsandactionsforinsurers

Implications Actions

Timelinessandpersonalizationdrivesuccessfuloutcomes,butthismustbecost-effective

Successful moments of truth are about communicating in a timely fashion, in preferred formats, with relevant content.There is a demand for personalization, but insurers cannot afford to meet everyone’s demands all the time.

A balance must be struck between the need to drive positive outcomes with the need to standardize and industrialize sales and service interactions. Insurers that can correctly strike the right balance will be the future winners.

• Develop and deploy a clear customer value-based segmentation model to drive customer treatment, in terms of marketing campaigns, contact channels offered and routing of inbound customer inquiries.

• Optimize the consumer experience in digital channels through easy-to-use, intuitive self-service tools.

• Identify where personal interaction creates the most value in the relationship — and operationalize this. Make the hard decisions, based on costs and return on investment, regarding what you are prepared to offer and to whom. The decision will differ by customer segment, product and market, but the criteria must be consistent.

The nature of actions required will clearly differ depending on the channel strategy companies have adopted, so insurers may need to work through or with their business partners to achieve these objectives.

20

Keyfinding4:

Consumers want more frequent, meaningful and personalized communications. About one in six customers (17%) across the Americas is very satisfied with the communications he or she receives.

21

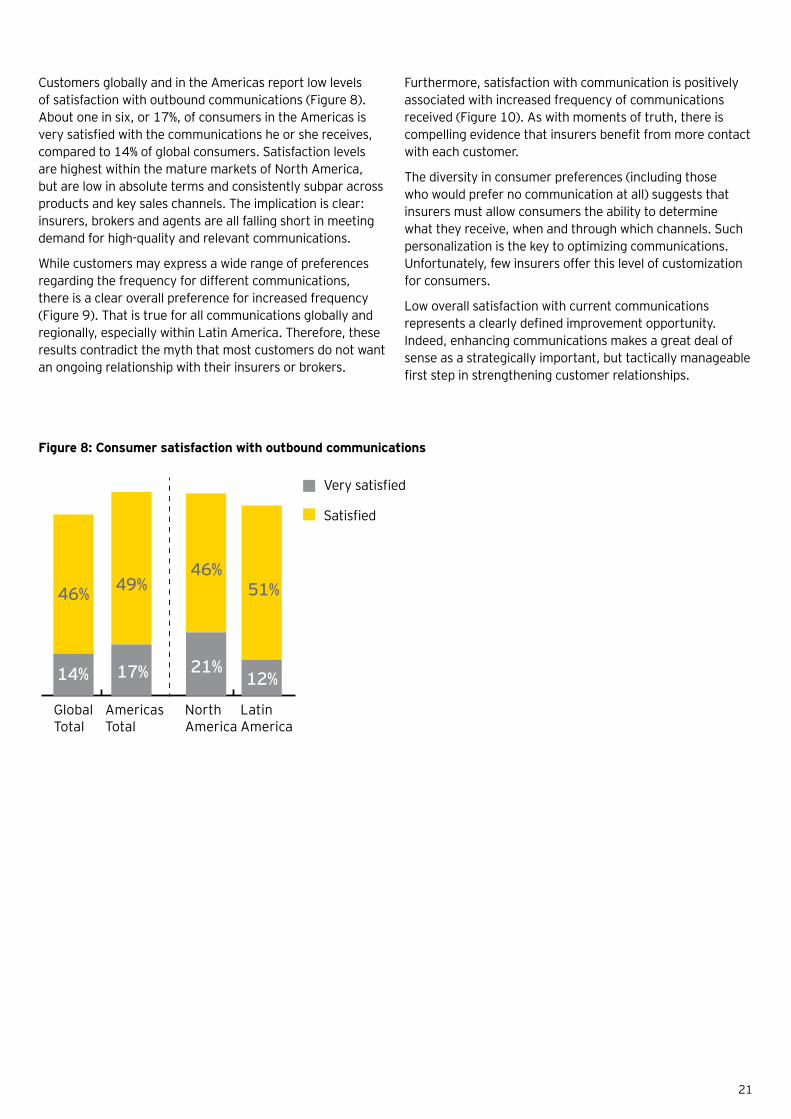

Customers globally and in the Americas report low levels of satisfaction with outbound communications (Figure 8). About one in six, or 17%, of consumers in the Americas is very satisfied with the communications he or she receives, compared to 14% of global consumers. Satisfaction levels are highest within the mature markets of North America, but are low in absolute terms and consistently subpar across products and key sales channels. The implication is clear: insurers, brokers and agents are all falling short in meeting demand for high-quality and relevant communications.

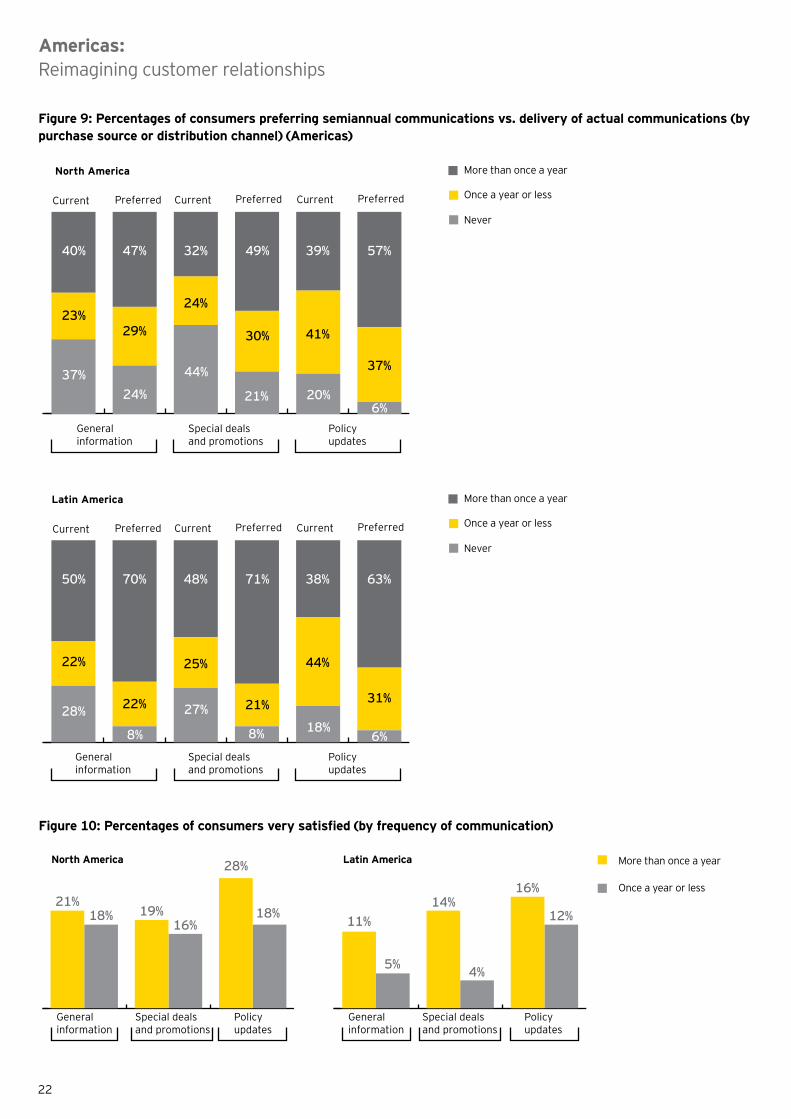

While customers may express a wide range of preferences regarding the frequency for different communications, there is a clear overall preference for increased frequency (Figure 9). That is true for all communications globally and regionally, especially within Latin America. Therefore, these results contradict the myth that most customers do not want an ongoing relationship with their insurers or brokers.

Furthermore, satisfaction with communication is positively associated with increased frequency of communications received (Figure 10). As with moments of truth, there is compelling evidence that insurers benefit from more contact with each customer.

The diversity in consumer preferences (including those who would prefer no communication at all) suggests that insurers must allow consumers the ability to determine what they receive, when and through which channels. Such personalization is the key to optimizing communications. Unfortunately, few insurers offer this level of customization for consumers.

Low overall satisfaction with current communications represents a clearly defined improvement opportunity. Indeed, enhancing communications makes a great deal of sense as a strategically important, but tactically manageable first step in strengthening customer relationships.

Figure8:Consumersatisfactionwithoutboundcommunications

46%

GlobalTotal

46%51%49%

North America

LatinAmerica

AmericasTotal

14% 21%12%17%

Satisfied

Very satisfied

Americas:Reimagining customer relationships

22

Figure10:Percentagesofconsumersverysatisfied(byfrequencyofcommunication)

General information

Special dealsand promotions

Policyupdates

More than once a year

Once a year or less

North America

General information

Special dealsand promotions

Policyupdates

Latin America

21%18% 19%

28%

18%16%

16%

12%11%

5%

14%

4%

Figure9:Percentagesofconsumerspreferringsemiannualcommunicationsvs.deliveryofactualcommunications(bypurchasesourceordistributionchannel)(Americas)

0

20

40

60

80

100

40% 47% 32% 49% 39% 57%

23%29%

24%

30% 41%

37%

20%6%

21%

44%

24%37%

Generalinformation

Special dealsand promotions

Policyupdates

More than once a year

Once a year or less

Never

Current Preferred Current Preferred Current Preferred

0

20

40

60

80

100

50% 70% 48% 71% 38% 63%

22%

22%

25%

21%

44%

31%

18%6%8%

27%

8%

28%

Generalinformation

Special dealsand promotions

Policyupdates

Current Preferred Current Preferred Current Preferred

North America Latin America

0

20

40

60

80

100

40% 47% 32% 49% 39% 57%

23%29%

24%

30% 41%

37%

20%6%

21%

44%

24%37%

Generalinformation

Special dealsand promotions

Policyupdates

More than once a year

Once a year or less

Never

Current Preferred Current Preferred Current Preferred

0

20

40

60

80

100

50% 70% 48% 71% 38% 63%

22%

22%

25%

21%

44%

31%

18%6%8%

27%

8%

28%

Generalinformation

Special dealsand promotions

Policyupdates

Current Preferred Current Preferred Current Preferred

North America Latin America

0

20

40

60

80

100

40% 47% 32% 49% 39% 57%

23%29%

24%

30% 41%

37%

20%6%

21%

44%

24%37%

Generalinformation

Special dealsand promotions

Policyupdates

More than once a year

Once a year or less

Never

Current Preferred Current Preferred Current Preferred

0

20

40

60

80

100

50% 70% 48% 71% 38% 63%

22%

22%

25%

21%

44%

31%

18%6%8%

27%

8%

28%

Generalinformation

Special dealsand promotions

Policyupdates

Current Preferred Current Preferred Current Preferred

North America Latin America

0

20

40

60

80

100

40% 47% 32% 49% 39% 57%

23%29%

24%

30% 41%

37%

20%6%

21%

44%

24%37%

Generalinformation

Special dealsand promotions

Policyupdates

More than once a year

Once a year or less

Never

Current Preferred Current Preferred Current Preferred

0

20

40

60

80

100

50% 70% 48% 71% 38% 63%

22%

22%

25%

21%

44%

31%

18%6%8%

27%

8%

28%

Generalinformation

Special dealsand promotions

Policyupdates

Current Preferred Current Preferred Current Preferred

North America Latin America

23

Implicationsandactionsforinsurers

Implications Actions

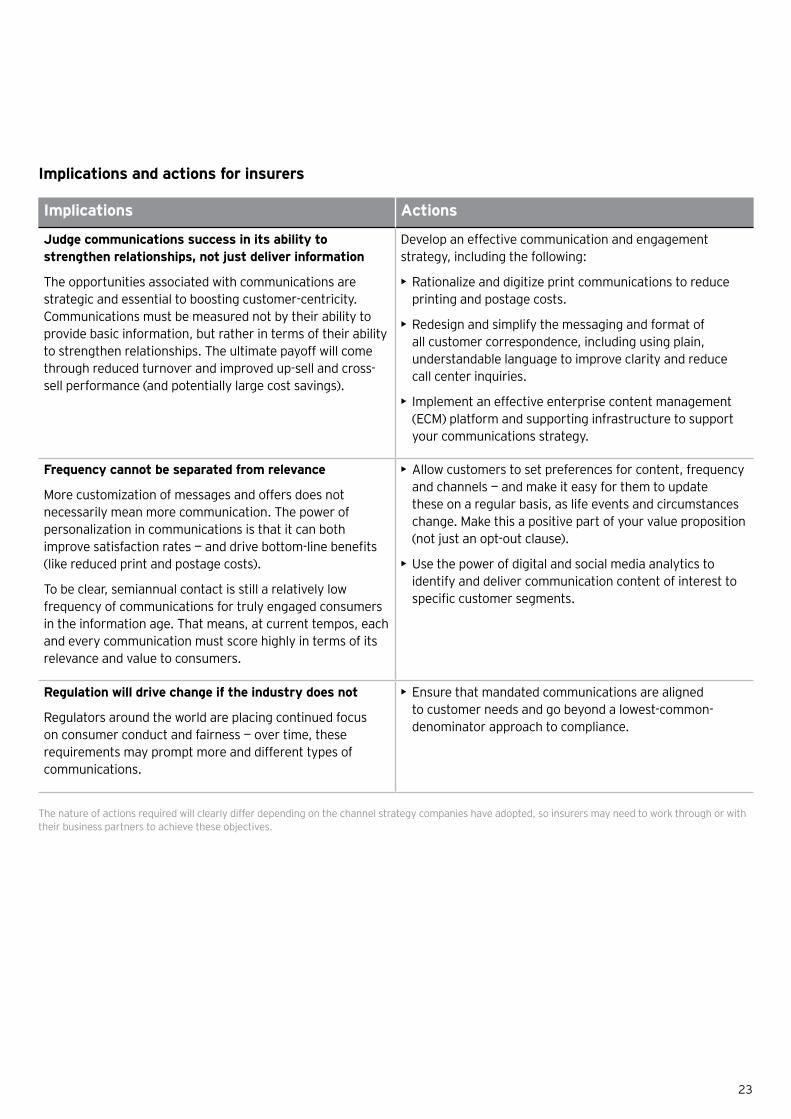

Judgecommunicationssuccessinitsabilitytostrengthenrelationships,notjustdeliverinformation

The opportunities associated with communications are strategic and essential to boosting customer-centricity. Communications must be measured not by their ability to provide basic information, but rather in terms of their ability to strengthen relationships. The ultimate payoff will come through reduced turnover and improved up-sell and cross-sell performance (and potentially large cost savings).

Develop an effective communication and engagement strategy, including the following:

• Rationalize and digitize print communications to reduce printing and postage costs.

• Redesign and simplify the messaging and format of all customer correspondence, including using plain, understandable language to improve clarity and reduce call center inquiries.

• Implement an effective enterprise content management (ECM) platform and supporting infrastructure to support your communications strategy.

Frequencycannotbeseparatedfromrelevance

More customization of messages and offers does not necessarily mean more communication. The power of personalization in communications is that it can both improve satisfaction rates — and drive bottom-line benefits (like reduced print and postage costs).

To be clear, semiannual contact is still a relatively low frequency of communications for truly engaged consumers in the information age. That means, at current tempos, each and every communication must score highly in terms of its relevance and value to consumers.

• Allow customers to set preferences for content, frequency and channels — and make it easy for them to update these on a regular basis, as life events and circumstances change. Make this a positive part of your value proposition (not just an opt-out clause).

• Use the power of digital and social media analytics to identify and deliver communication content of interest to specific customer segments.

Regulationwilldrivechangeiftheindustrydoesnot

Regulators around the world are placing continued focus on consumer conduct and fairness — over time, these requirements may prompt more and different types of communications.

• Ensure that mandated communications are aligned to customer needs and go beyond a lowest-common-denominator approach to compliance.

The nature of actions required will clearly differ depending on the channel strategy companies have adopted, so insurers may need to work through or with their business partners to achieve these objectives.

24

Keyfinding5:

As consumers embrace digital, insurers must rethink their distribution strategies and partner relationships. Most customers express a willingness to consider remote and electronic contact channels as an alternative to in-person communication.

25

Shifting consumer preferences and increased willingness to use remote and digital channels are driving significant change in the distribution landscape. Insurers must manage these changes thoughtfully and learn to master a range of communication and contact channels for different types of inquiries and transactions.

Adding to the urgency are the large numbers of policyholders who appear to receive little or no contact from their insurers, agents or brokers. The sense of “orphaned customers” was clear in the aftermath of Hurricane Sandy when some US-based insurers were unable to contact all of their impacted insureds; because agents or brokers “owned” those customers, insurers had no access to contact information, such as mobile phone numbers. No customer, under any circumstances, should be overlooked in this way, especially not in the wake of a natural disaster.

Among those customers initiating a transaction or inquiry, most rely on a limited number of communication channels (Figures 11 and 11a). The type of inquiry can have a

significant impact on the channels used. In the Americas, customers show a clear preference for in-person channels when they seek advice or make changes to their portfolios. The telephone is preferred for filing a claim or managing or obtaining information about a current policy, such as changing vehicles, reducing premiums or requesting general policy information. Websites represent the preferred channel to obtain information about replacing a current policy.

Most customers express a willingness to consider remote and electronic contact channels as an alternative to in-person communication. In this context, web chat, email and call center access would likely be sufficient to serve the majority of customers. In the eyes of consumers, remote and digital channels seem most appropriate for questions about an existing policy, general policy management and filing a claim. Those seeking financial advice or canceling a policy would be least amenable to conducting these engagements via remote or digital channels.

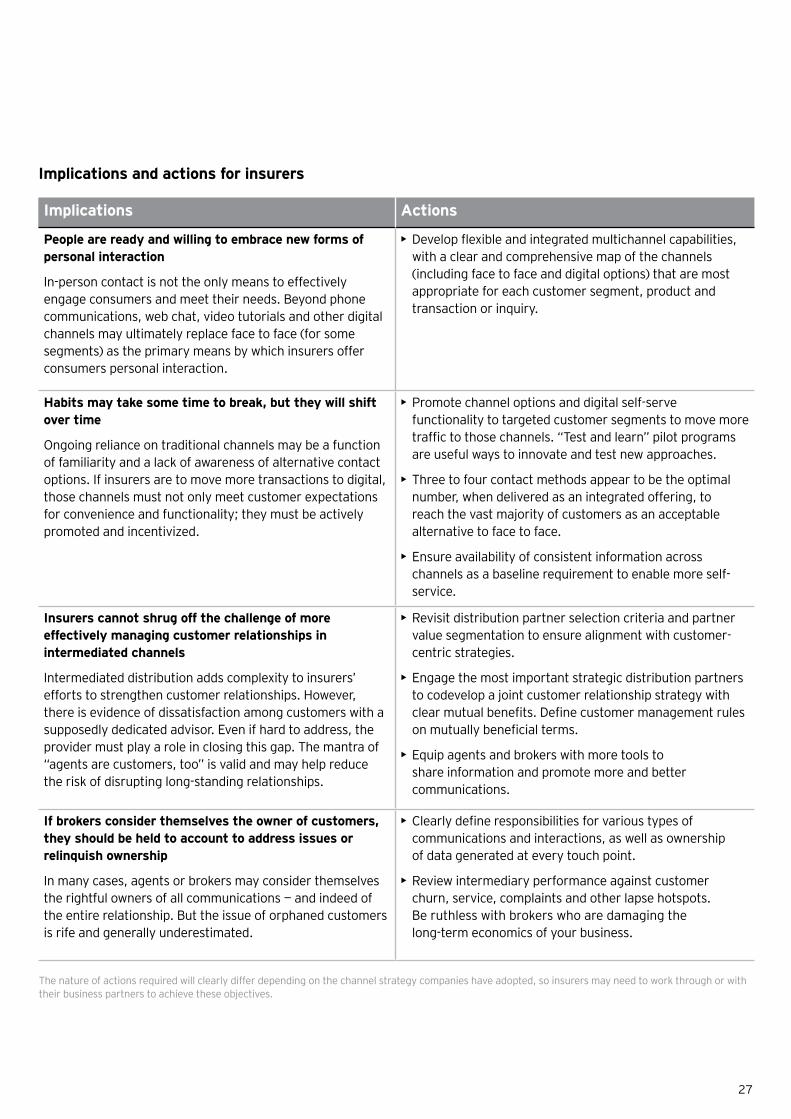

Figure11:Percentagesofconsumerswhowouldconsiderusingthesecontactmethods(assumingtheywereavailable)wheninteractingwiththeirinsurancecompanies

Inquireaboutnewinsurance policy

Questions about an existing policy

Seekingfinancialadvice

Assistance withaclaim

Researching differenttypes of insurance

Managing your current policy

Renewingyour policy

Cancel my policy

Web chat 26% 34% 14% 27% 18% 23% 17% 14%

Email 40% 51% 27% 36% 35% 49% 41% 29%

24-hour telephone hotline

33% 47% 25% 57% 28% 42% 36% 37%

Mobile app 17% 20% 11% 17% 18% 20% 15% 11%

Interactive support

18% 20% 13% 19% 19% 22% 14% 11%

Video tutorials and guides

18% 17% 16% 14% 28% 14% 10% 6%

None of the above

30% 18% 46% 20% 32% 23% 30% 39%

Note: Interactive support is defined as combined phone and remote control of a customer’s computer screen to assist with navigating online materials.

North America

Americas:Reimagining customer relationships

26

Latin America

Inquireaboutnewinsurance policy

Questions about an existing policy

Seekingfinancialadvice

Assistance withaclaim

Researching differenttypes of insurance

Managing your current policy

Renewingyour policy

Cancel my policy

Web chat 48% 50% 37% 34% 39% 30% 27% 20%

Email 43% 42% 41% 32% 39% 38% 38% 27%

24-hour telephone hotline

38% 47% 39% 53% 31% 41% 36% 41%

Mobile app 33% 37% 29% 34% 37% 30% 25% 18%

Interactive support

31% 35% 29% 31% 35% 30% 22% 15%

Video tutorials and guides

24% 31% 32% 24% 35% 22% 16% 12%

None of the above

11% 9% 11% 10% 10% 12% 17% 22%

Note: Interactive support is defined as combined phone and remote control of a customer’s computer screen to assist with navigating online materials.

Figure11a:Percentagesofconsumerswhowouldconsiderusingthesecontactmethods(assumingtheywereavailable)wheninteractingwiththeirinsurancecompanies

There are major differences in consumer receptivity to these channels across mature North American markets and developing Latin American countries. For example:

• Approximately half of all Latin American consumers would consider web chat to inquire about a new policy or resolve questions on an existing policy, compared to 26% and 34% in North America, respectively.

• In Latin America, 32% of consumers would consider using video tutorials to seek financial advice, compared to only 16% in North America; for renewals, 25% of Latin American consumers would use a mobile app, compared to only 15% in North America.

This gap between mature and developing markets is consistent with the global findings.

Insurers seeking to improve the effectiveness of existing contact channels, as well as establish more digital options for consumers, must invest time and resources to identify which channels customers want to use and how they want to use them. It is not a matter of simply adding more channels. Pilot programs for specific product lines or regions can help build the business case for updating and optimizing distribution channels and service models.

27

Implicationsandactionsforinsurers

Implications Actions

Peoplearereadyandwillingtoembracenewformsofpersonal interaction

In-person contact is not the only means to effectively engage consumers and meet their needs. Beyond phone communications, web chat, video tutorials and other digital channels may ultimately replace face to face (for some segments) as the primary means by which insurers offer consumers personal interaction.

• Develop flexible and integrated multichannel capabilities, with a clear and comprehensive map of the channels (including face to face and digital options) that are most appropriate for each customer segment, product and transaction or inquiry.

Habitsmaytakesometimetobreak,buttheywillshiftover time

Ongoing reliance on traditional channels may be a function of familiarity and a lack of awareness of alternative contact options. If insurers are to move more transactions to digital, those channels must not only meet customer expectations for convenience and functionality; they must be actively promoted and incentivized.

• Promote channel options and digital self-serve functionality to targeted customer segments to move more traffic to those channels. “Test and learn” pilot programs are useful ways to innovate and test new approaches.

• Three to four contact methods appear to be the optimal number, when delivered as an integrated offering, to reach the vast majority of customers as an acceptable alternative to face to face.

• Ensure availability of consistent information across channels as a baseline requirement to enable more self-service.

Insurers cannot shrug off the challenge of more effectively managing customer relationships in intermediatedchannels

Intermediated distribution adds complexity to insurers’ efforts to strengthen customer relationships. However, there is evidence of dissatisfaction among customers with a supposedly dedicated advisor. Even if hard to address, the provider must play a role in closing this gap. The mantra of “agents are customers, too” is valid and may help reduce the risk of disrupting long-standing relationships.

• Revisit distribution partner selection criteria and partner value segmentation to ensure alignment with customer-centric strategies.

• Engage the most important strategic distribution partners to codevelop a joint customer relationship strategy with clear mutual benefits. Define customer management rules on mutually beneficial terms.

• Equip agents and brokers with more tools to share information and promote more and better communications.

Ifbrokersconsiderthemselvestheownerofcustomers,theyshouldbeheldtoaccounttoaddressissuesorrelinquishownership

In many cases, agents or brokers may consider themselves the rightful owners of all communications — and indeed of the entire relationship. But the issue of orphaned customers is rife and generally underestimated.

• Clearly define responsibilities for various types of communications and interactions, as well as ownership of data generated at every touch point.

• Review intermediary performance against customer churn, service, complaints and other lapse hotspots. Be ruthless with brokers who are damaging the long-term economics of your business.

The nature of actions required will clearly differ depending on the channel strategy companies have adopted, so insurers may need to work through or with their business partners to achieve these objectives.

28

Conclusion:

A new era dictates new value propositions. Insurers must rethink and take control of customer relationships with new offerings, new capabilities and optimized channels.

29

The findings of the report confirm the clear and actionable opportunities for insurers seeking market advantage through better customer engagement. The way forward will require more than just trying to solve problems or ticking the boxes in those areas where customer satisfaction levels are dangerously low. Rather, a broad-based and strategic rethink regarding the core value proposition insurers offer customers must take place.

The first step is to understand current capabilities, as well as where the organization is on its journey to strong customer relationships. Among the key questions to ask include the following:

• How effectively do we serve and satisfy customers?

• Why do we lose customers today?

• Whom do we want as customers tomorrow?

• Which products and services do our customers want from us?

• Which channels work best?

• Which tools and technology do we need to understand what customers really want?

The answers to these questions will uncover transformation opportunities at multiple dimensions of the organization. Improvements will be needed in many areas and functions, including technology; product design; underwriting; customer service; and, critically, the challenging area of organizational culture. Indeed, the outward-facing work of customer engagement will likely necessitate an unprecedented level of internal change.

As the fallout from the financial crisis recedes, we believe that stronger customer relationships hold the key to future success. Insurers must find ways to offer more value across the relationship life cycle. Engineering mutually beneficial, two-way relationships is not just about boosting the industry’s poor brand perception and trust levels, but also about adopting new, partner-like roles in customers’ lives. Insurers must overcome their unique challenge of their products typically being “out of sight and out of mind.”

That grand aspiration, along with the many demographic, technological and competitive factors at play, is likely to drive insurers to develop next-generation products. Insurers simply cannot reach such symbiotic, win-win customer relationships with current product sets. Telematics, wearable technology and other advancements are redefining the “art of the possible” in terms of what we know about how people live and behave (and when we can know it).

For insurers, that means the time is now to start designing products and offerings that break the industry mold. Inevitably, they will look outside of traditional risk-based insurance products to find new profit pools, new business models, new partners and new forms of growth.

Whatever exact shape the future takes, there can be no doubt that reimagining insurance customer relationships will be the key to future success.

Key contacts in the Americas

North America (USandCanada) KaenanHertzUS Insurance Customer Leader [email protected] +1 212 773 5988

Canada WalterRondinaSenior Manager Performance Improvement [email protected] +1 514 879 2765

Latin America (BrazilandMexico) JamesLittlewood Latin America Insurance Leader [email protected] +1 305 415 1849

Brazil Duarte S CarvalhoPartner/Principal Performance Improvement [email protected] +55 11 2573 3243

Mexico GustavoABohorquezGarcia Executive Director Performance Improvement [email protected]+52 1 55 4091 1471

For additional information about this survey, go to www.ey.com/us/insurance

Achieving customer-centricity and stronger customer relationships will be a long-term journey for insurers — but it’s one that must begin now.

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisoryservices. The insights and quality services we deliver help build trust andconfidence in the capital markets and in economies the world over. Wedevelop outstanding leaders who team to deliver on our promises to allof our stakeholders. In so doing, we play a critical role in building a betterworking world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, ofthe member firms of Ernst & Young Global Limited, each of which is aseparate legal entity. Ernst & Young Global Limited, a UK company limitedby guarantee, does not provide services to clients. For more informationabout our organization, please visit ey.com.

EY is a leader in serving the global financial services marketplaceNearly 43,000 EY financial services professionals around the world provide integrated assurance, tax, transaction and advisory services to our asset management, banking, capital markets and insurance clients. In the Americas, EY is the only public accounting organization with a separate business unit dedicated to the financial services marketplace. Created in 2000, the Americas Financial Services Office today includes more than 6,900 professionals at member firms in over 50 locations throughout the US, the Caribbean and Latin America.

EY professionals in our financial services practices worldwide align with key global industry groups, including EY’s Global Wealth & Asset Management Center, Global Banking & Capital Markets Center, Global Insurance Center and Global Private Equity Center, which act as hubs for sharing industry-focused knowledge on current and emerging trends and regulations in order to help our clients address key issues. Our practitioners span many disciplines and provide a well-rounded understanding of business issues and challenges, as well as integrated services to our clients.

With a global presence and industry-focused advice, EY’s financial services professionals provide high-quality assurance, tax, transaction and advisory services, including operations, process improvement, risk and technology, to financial services companies worldwide.

© 2014 EYGM Limited. All Rights Reserved.

EYG No. EG02161410-1345707 NYED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com