key metrics genzyme corporation rating: buy - morgan … · · 2009-04-06renvela, a...

TRANSCRIPT

The Disclosure section may be found on pages 20 - 22 of this report.The Valuation section may be found on page 20 of this report.

January 6, 2009

Key MetricsGENZ - NASDAQ $67.70

Pricing Date 01/05/2009

Price Target $81.00

52-Week Range $83.97-$57.61

Shares Outstanding (mm) 270.5

Market Capitalization ($mm) $18,312.8

3-Mo Average Daily Volume 3,721,360

Institutional Ownership 92%

Debt/Total Capital 1.3%

ROE 14.0%

Book Value/Share $26.75

Price/Book 2.5x

Dividend Yield 0.0%

LTM EBITDA Margin 16.00%

EPS($) FY: DecemberPrior Curr. Prior Curr.

2007A 2008E 2008E 2009E 2009E1Q-Mar 0.78 -- 0.95A -- --

2Q-Jun 0.88 -- 0.98A -- --

3Q-Sep 0.90 -- 1.04A -- --

4Q-Dec 0.91 -- 1.01E -- --

FY 3.47 -- 3.98E -- 4.75E

P/E 19.5x 17.0x 14.3x

Revenue($mm)Prior Curr. Prior Curr.

2007A 2008E 2008E 2009E 2009E1Q-Mar 883.2 -- 1,100.0A -- --

2Q-Jun 933.4 -- 1,171.2A -- --

3Q-Sep 960.3 -- 1,160.4A -- --

4Q-Dec 1,036.8 -- 1,221.1E -- --

FY 3,813.5 -- 4,632.6E -- 5,301.2E

Q1 Q1 Q2 Q348

56

64

72

80

88

2009

1 Year Price History for GENZ

Created by BlueMatrix

Company Description: Founded in 1981, Genzyme is a largebiotechnology company headquartered in Cambridge, Massachusetts.Genzyme has a diversified product portfolio focused in five areas:Renal, Therapeutics, Transplant, Oncology, and Biosurgery.

Genzyme Corporation

Rating: Buy

Drivers in Place for Strong Growth; Initiating

Coverage at BUY, $81PT

Investment Highlights:■ We are initiating coverage on Genzyme with a BUY rating and an

$81 price target. We like Genzyme because we believe the companyhas the growth drivers in place to grow the company 20% over the nexttwo years. Additionally, we believe Genzyme's new drugs and strongpipeline have the ability to sustain the company's strong growth wellinto the next decade.

■ Drivers in place for strong growth. Mostly based on growth fromexisting products, we expect Genzyme to grow earnings 21% between2008 and 2011. Myozyme, which has already become Genzyme'sfastest penetrating rare-disease drug since its approval in 2006, shouldgrow strongly with additional manufacturing capacity this year. Withthe approval of Synvisc-One and Mozobil, those concerns are nowbehind the company. Some investors have been concerned about theeffect of foreign exchange; in our opinion, due to Genzyme'sconsiderable manufacturing outside of the US, risks to the bottom-lineare minimized. We also believe there is considerable room for thecompany to gain operational efficiencies, especially with growth drivenby high margin drugs like Myozyme.

■ Strong pipeline ensures sustainable growth. There are some maturingdrugs in Genzyme's portfolio, competition for which may negativelyimpact growth beyond 2011. Growth detractors include newcompetition for Cerezyme by the end of 2010, and generics for Renagelin 2014. However we anticipate drugs launched between 2006 and 2012to more than offset any related slowing growth. We expect longer-termgrowth to be led by Myozyme (approved in 2006), Mozobil (recentlylaunched), mipomersin (possible launch in 2011), and Campath for MS(possible launch in 2012). We believe three of these four drugs haveblockbuster potential. There could be upside to our and the Street'sview of Genzyme's prospects if we see positive clinical data fromProchymal, PTC-124, and Clorar in adult AML, which are inlate-to-mid-stage clinical trials.

■ Key catalysts this quarter. We expect the approval of a 2000-literplant to help Genzyme significantly step-up sales of Myozyme as soonas February. We expect Genzyme to affirm strong guidance for growthin the next three years later this month at various conferences.

■ Attractive valuation. In our view, Genzyme is trading at an attractivevaluation of 14.3x 2009 estimated EPS given the company's projectedlonger-term 20% bottom line growth rate. We derive our price target of$81 using our 2009 EPS estimate of $4.75 and a P/E multiple of 17x.

BIOTECHNOLOGYShiv Kapoor

(917) [email protected]

Initiating Coverage

2 MORGAN JOSEPH & CO. INC.

Executive Summary

Company

• Founded in 1981, Genzyme is a large biotechnology company headquartered in Cambridge, Massachusetts.Genzyme has a diversified product portfolio focused in five areas: Renal, Therapeutics, Transplant,Oncology, and Biosurgery.

• There are three reasons why we believe Genzyme is well positioned to benefit from acquisitions andin-licensing in the current macroeconomic environment: one, it has global infrastructure; two, it hasexpertise in a wide array of technologies; and three, in our opinion, management has shown financialprudence with its past acquisitions.

• Genzyme's key partnerships include three recent in-licensing deals with Isis, Osiris, and PTC therapeutics,and an ongoing partnership with BioMarin. These partnerships involve either late-stage or approved drugsfor niche disease areas, and should generate significant late-stage data in 2009 and 2010.

Products

• Cerezyme: Genzyme's enzyme replacement therapy (ERT) for Gaucher's disease accounted forapproximately 30% of total product revenues in 2007. By the end of 2010, there could be competition forCerezyme from two enzyme replacement therapies: Shire's Velaglucerase alfa and Protalix Biotherapeutic'sprGCD. Both companies expect Phase III data starting in mid-09 and expect to attain approval by the end of2010. In our opinion, these two competitive drugs may have similar efficacy compared to Cerezyme and willhave to clear higher regulatory and marketing hurdles. Further, we expect Cerezyme to account for around20% of sales in 2011, the first full year that either prGCD or Velaglucerase alfa could be on the market.

• Renagel, a phosphate binder, indicated for the control of serum phosphorus in kidney disease patients,generated sales of $602.7 million in 2007, or around 17% of total product sales. Renvela, a next-generationsevelamer drug, contains carbonate and offers better gastrointestinal tolerability compared to Renagel. In thenear term, we expect double-digit growth from the Renagel franchise as the launch of Renvela in the USshould expand the overall market. The composition-of-matter patent related to Renagel expires in 2014,following which we expect generic competition.

• Fabrazyme, an ERT for Fabry's disease, recorded sales of $424 million in 2007, representing approximately11% of Genzyme's total product sales. Shire and Amicus are in discussion with the FDA and the EMEA todesign a registration program for Amigal, a possible competitor of Fabrazyme, and begin Phase III trials in2009. It is not clear whether Amicus' technology works, and we believe only a subset of patients can likelybe treated with such an approach.

• Myozyme, an ERT for Pompe's disease, was approved in 2006 and contributed 2007 sales of $200.7 million,accounting for approximately 5% of total sales. When compared to the launches of Cerezyme, or even therecently launched Fabrazyme and Aldurazyme, Myozyme has enjoyed a speedy launch. Genzyme isawaiting regulatory action on two plants: a 2000-liter plant in the United States, and a 4000-liter plant inEurope (Belgium). We believe the manufacturing shortage is temporary and expect that, in time, the 2000Land 4000L plants will be approved to supply the drug in the US and Europe in 2009.

• Mozobil is an inhibitor of the CXCR4 chemokine receptor that induces rapid mobilization of stem cellsfrom the bone marrow into the peripheral blood system. We believe Mozobil will have a slow launch, buteventually attain peak sales over $300 million based on a 45% penetration in the autologous transplantmarket and strong pricing because of limited competition.

• Clolar is a small molecule indicated for the treatment of children (ages 1-21) with relapsed or refractoryacute lymphoblastic leukemia (ALL). The market opportunity for Clorar should increase with a possibleapproval in the untreated adult elderly AML population based on overall remission (45%) data from a PhaseII study (CLASSIC II). Although Genzyme estimates that the peak sales for Clorar would be close to $600million, we believe positive survival data is needed to gain significant market share and we don't anticipate a

Genzyme Corporation January 6, 2009

3 MORGAN JOSEPH & CO. INC.

significant step-up in sales based on an approval in this indication.• Synvisc is a biomaterial used to help reduce or eliminate pain resulting from osteoarthritis of the knee.

Synvisc sales of $242.3 million represents approximately 6% of 2007 total product sales. Synvisc competesin a competitive market, and initially gained market share because of the lower number of injections pertreatment compared to existing products. We think the approval of Synvisc-One in December 2008 willlikely help Genzyme retain market share. We believe the key patent on Synvisc will expire in August 2011;chondrogen (in-licensed from Osiris) could possibly be the next-generation osteoporosis drug for Genzyme.

• Other products: Genzyme markets several other products including Aldurazyme formucopolysaccharidosis I (MPS I), Hectorol for the treatment of secondary hyperparathyroidism, Campathfor the treatment of B-cell chronic lymphocytic leukemia (B-CLL), Thyrogen as an alternative diagnostictool used to monitor well-differentiated thyroid cancer patients who have had their thyroid glands removed,and Thymoglobulin for the treatment of acute rejection in renal transplant patients. Genzyme has abiosurgery division selling Sepra, Carticel, and Epicel and a diagnostic division that sells diagnostic toolsand services for oncology, pathology, reproductive and genetic areas.

Pipeline

Mipomersin in Phase III. In January 2008, Genzyme entered into a collaboration with Isis Pharmaceuticalsfor rights to its lead antisense drug candidate, mipomersin. Mipomersin has shown in Phase II studies todramatically lower cholesterol, specifically LDL (the 'bad' cholesterol) and all other atherogenic lipids.Genzyme will share a portion of mipomersin profit, starting at 70% and decreasing to 50% as annual salesgrow to $2 billion. Phase II data from several drug doses showed a speedy, statistically significant reduction inLDL with a strong dose response curve. Isis and Genzyme have a comprehensive Phase III program includinga pivotal Phase III trial evaluating homozygous FH patients, from which we believe there should be positivedata by mid-2009.

CAMPATH in Phase III. CAMPATH is a humanized monoclonal antibody against the cell surfaceglycoprotein, CD52. It is currently approved for the treatment of B-cell chronic lymphocytic leukemia(B-CLL). Genzyme is studying CAMPATH as a treatment of Multiple Sclerosis (MS). Genzyme is developingCAMPATH in collaboration with Bayer. This drug showed compelling efficacy in Phase II studies in MultipleSclerosis. It is is currently being studied in two pivotal studies looking at first-line and relapsed patients. Thestudies were initiated in 2007 and enrollment is likely to be completed in 2009 with results from trialsexpected in 2011.

Prochymal in Phase III. In November 2008, Genzyme entered into a collaboration with Osiris for ex-USrights to Prochymal with an option to rights on Chondrogen. Prochymal is an intravenously administered formof mesenchymal adult stem cells (MSC). Phase III data from Prochymal are expected from two Graft vs. HostDisease (GvHD) trials and one Crohn's disease trial in 2009. If these trials are positive, European approvalcould come in 2010. Genzyme has the right to make a go/no-go decision on ex-US rights for Chondrogen,based on a Phase II/III study in patients with osteoarthritis of the knee.

PTC-124 in Phase IIb. In July 2008, Genzyme entered into a collaboration with PTC Therapeutics (PTC), forex-US rights to PTC-124. PTC-124 is a novel, orally administered, small-molecule new drug candidate for thetreatment of genetic disorders resulting from nonsense mutations. Data from the Phase IIa clinical trials ofPTC-124 in pediatric patients with nonsense mutation Duchenne muscular dystrophy (nmDMD) showedproduction of full-length dystrophin and statistically significant reductions in the leakage of muscle-derivedcreatine kinase into the blood implying decreases in muscle fragility. PTC-124 is currently being evaluated ina phase IIb trial for nmDMD, which is expected to enroll 165 patients, and in a phase IIb trial in cystic fibrosis

Genzyme Corporation January 6, 2009

4 MORGAN JOSEPH & CO. INC.

(CF) patients planned to begin by YE08.

Other pipeline drugs include Genzyme 112638, a small molecule for Gaucher disease currently in Phase IIstudies; a next generation treatment of Pompe's disease using a highly potent version of GAA; and GEN-644470, a next generation phosphate binder in research.

Financials and Valuation

• Guidance indicates confidence in growth. Genzyme has provided long-term guidance for 20% growthbetween 2006 and 2011. Based on this guidance, Genzyme expects EPS of $7.00 by 2011. Managementrecently confirmed both its 2009 and 2011 guidance. We believe Genzyme is in a good position to gainoperational efficiencies during this period because we see no strategic new initiatives to increase SG&A orR&D. Genzyme has established 2009 EPS guidance of $4.70; we believe Genzyme has the potential to beatthat number.

• Attractive valuation. Compared to the current average large cap peer P/E of 17.9x 2009 estimated EPS,Genzyme is trading attractively at 14.3x 2009E EPS. We believe this is especially attractive becauseGenzyme's growth rate is one of the best among its large cap peers. We derive our price target of $81 usingour 2009 EPS estimate of $4.75 and a P/E multiple of 17x.

Company Background

Founded in 1981, Genzyme is a large biotechnology company headquartered in Cambridge, Massachusetts,and it's listed on the NASDAQ stock market under the symbol GENZ. For much of its history, Genzyme'sprimary business was enzyme replacement therapies for patients with rare inherited diseases. But morerecently, it has emerged as a diversified company with products and a pipeline focused in five areas: Renal,Therapeutics, Transplant, Oncology, and Biosurgery. Genzyme recently combined its Transplant andOncology divisions and has global infrastructure. Its products are sold in over 90 countries.

Figure 1: Key Events in Genzyme's History

Year Key Events

1981 Genzyme is founded. Employees: 21. Revenue: $2.2 million.

1983 Henri Termeer is named president.

1985 Ceredase receives orphan drug status. Henri Termeer is named CEO.

1986 Genzyme IPO.

1991 FDA approves Ceredase in the U.S. for the treatment of Gaucher disease.

Employees: 800. Revenue: $121 million.

1994 FDA approves Cerezyme, a second-generation recombinant product for Gaucher

disease.

1998 FDA approves Renagel for chronic kidney disease and Thyrogen for thyroid

cancer.

2001 Genzyme launches Fabrazyme in the E.U. Employees: 5,212. Revenue: $981 million.

2003 FDA approves Fabrazyme for patients with Fabry disease. Genzyme and its

partner BioMarin receive FDA approval for Aldurazyme for patients with MPS I.

2006 Myozyme approved in the U.S. and Europe. Employees: 9,000. Revenue: $3.2

billion.

2007 Genzyme awarded the National Medal of Technology

Source: Company reports and Morgan Joseph & Co. Inc.

Genzyme Corporation January 6, 2009

5 MORGAN JOSEPH & CO. INC.

We Believe Genzyme is Well Suited for In-Licensing and Acquisitions Because:

Genzyme has historically grown through internal R&D as well as acquisitions. There are three reasons why webelieve Genzyme is well positioned to benefit from current macroeconomic conditions: first, it has globalinfrastructure; second, it has expertise in a wide array of technologies; and third, in our opinion, managementshould continue to show financial prudence with regard to future acquisitions, as it has in the past.

First, Genzyme has a Global Development and Sales Infrastructure

One of Genzyme's core competences, in our opinion, is its global infrastructure. Since very early on,acquisitions have been key to Genzyme's growth. Genzyme Corporation began in 1981 with the acquisition ofWhatman Biochemicals fermentation, extraction, and purification facilities in Maidstone, England. Genzymesells several of its drugs in over 50 countries. It has developed specialized sales forces and regulatoryknow-how in the US, Europe, Japan, and Brazil. Genzyme has manufacturing plants in Ireland, Belgium, theUnited Kingdom, and the United States. More recently, Genzyme established a direct presence in China andIndia. The following map shows Genzyme's worldwide presence in 2006.

Figure 2: Worldwide Presence of Genzyme

Source: Company reports

In our opinion, Genzyme has the unique ability to add value to acquire and in-license products fromcompanies with limited sales capabilities. Worldwide infrastructure helps Genzyme extract synergies fromacquisitions. While internally developed drugs like Cerezyme, Fabrazyme, and Myozyme have helpedGenzyme build and use this infrastructure, Genzyme has been able to rapidly grow acquired products likeRenagel and Thymoglubulin through it. Using the renal infrastructure built for Renagel, Genzyme is nowmarketing Hectorol, which was more recently acquired through the acquisition of Bone Care International. Weare excited by the prospect of the addition of Mozobil to Genzyme's sales force for thymoglobulin. Late-stagedrug candidates from the ongoing partnership with Osiris have the potential to leverage Genzyme's transplant

Genzyme Corporation January 6, 2009

6 MORGAN JOSEPH & CO. INC.

and biosurgery sales forces.

Second, Genzyme has Expertise in Various Technologies

Current revenues come from protein therapeutics, polymer therapeutics, small molecules, and biomaterials.Genzyme is also involved in cutting-edge research in antisense, cell therapy, and gene therapy technologies.

• Genzyme commercialized the first stem-cell product, Carticel, and has enhanced its pipeline via acollaboration with Osiris.

• Genzyme signed a partnership with Isis, the pioneer in antisense technology, to in-license its lead drugcandidate, mipomersin, which we believe has the potential to be the first antisense blockbuster drugcandidate.

• Genzyme has been doing research in gene therapy since 1991. In 2009, we expect Phase II data from twogene therapy product candidates: HIF-1a for peripheral arterial disease and CERE-120 (in collaboration withCeregene) for Parkinson's disease. The HIF-1a Phase II study enrolled nearly 300 patients at approximately40 medical centers in the United States and Europe and evaluated growth of new blood vessels andcirculation in patients' limbs. Ceregene has announced that the CERE-120 Phase II trial did not meetprimary endpoints; results are expected to be reported at a medical conference in early 2009.

Figure 3: Life Science Technologies and Genzyme's Exposure

Technology Clinical Risk Market Reward Examples Genzyme

Small molecule, proven mechanism Low Low Morphine None

Simple Protein therapeutics Low Medium Insulin Cerezyme

Combination therapeutics Medium Medium Vytorin None

Antibodies Medium High Rituxan Campath

Antisense/RNAi Medium High Mipomersin Mipomersin

Small molecule, new mechanisms High High HSP-90 inhibitors Renagel

Gene therapy Very High High Oncorine Ad2/HIF-1a

Stem cell therapy Very High Unknown Prochymal Prochymal

Source: Morgan Joseph & Co. Inc.

With Genzyme's history and deep expertise in many of these technologies, we believe the company is betterequipped than many of its competitors to make prudent acquisition-related decisions across the industry. Likeits revenue stream, Genzyme enjoys a diversified technology focus with leading franchises for enzymereplacement therapies and small molecules with novel mechanisms.

Third, Genzyme has an Experienced Management Team

Genzyme benefits from having a highly experienced management team, including several senior memberswho have been at Genzyme for more than a decade. In our opinion, Henri Termeer is a visionary leader whohas taken this company from a fledgling institution to one of the few profitable biotechnology companies inthe 1990s, and since 2000, he has helped the company diversify away from its two largest products, Cerezymeand Renagel.

Genzyme Corporation January 6, 2009

7 MORGAN JOSEPH & CO. INC.

Figure 4: Genzyme's Management Team

Name Position Background

Henri A. Termeer President, Chairman and

Chief Executive Officer

With Genzyme for 25 years.

Earl M. Collier,€Jr. Executive Vice President,

Cardiovascular, Oncology

and Genetics

With Genzyme for 11 years. Served as a Genzyme

outside lawyer since 1990.

With Genzyme for 10 years. Previously CFO of

Sovereign Hill Software Inc.

Peter Wirth Executive Vice President,

Secretary

With Genzyme for 11 years. Served as outside

general counsel since 1982.

Richard A. Moscicki, M.D. Senior Vice President, Chief

Medical Officer

Michael S. Wyzga Executive Vice President,

Chief Financial Officer

David Meeker, M.D. Executive Vice President,

Therapeutics, Transplant

With Genzyme for 14 years. Previously a director at

Cleveland Clinical Foundation.

Alan E. Smith, Ph.D. Senior Vice President, Chief

Scientific Officer

With Genzyme for 19 years.

With Genzyme for 16 years.

Sandford D. Smith President, International

Group

With Genzyme for 12 years. Previously President

and CEO of Repligen Corp.

Thomas J. DesRosier Senior Vice President; Chief

Legal Officer

With Genzyme for 9 years. Previously with

American Home Products

Richard H. Douglas, Ph.D. Senior Vice President,

Corporate Development

With Genzyme for 19 years.

Source: Company reports and Morgan Joseph & Co. Inc.

Product-Based Acquisitions, Limited Dilution

Genzyme has used a variety of methods to limit dilution to current shareholders. Firstly, Genzyme has focusedprimarily on product-based acquisitions rather than technology-based acquisitions, limiting the premium paidfor acquisitions. The size of these acquisitions has become increasingly small compared to Genzyme's marketcapitalization. Most of the acquisitions have been made using internally-generated cash. Genzyme has beenable to strongly grow sales of drugs obtained through acquisitions, while eliminating related overheadexpenses, thus expanding product margins.

Figure 5: Key Acquisitions Since 2000

Announced Completed

Acquired

Company

Key Product/s

Acquired

Acquisition

Price

Method of

acquisition

As a % of

Market Cap

Prior Cash

($ million)

May-07 Oct-07 Bioenvision Clorar $345 million Cash 1.8% $850.5 million

Aug-06 Nov-06 Anormed Mozobil $600 million Cash 3.4% $663.5 million

May-05 Jul-05 Bone Care Int. Hectorol $600 million Cash 3.9% $481.9 million

Mar-04 May-04 IMPATH Oncology

diagnostics

$215 million Cash 2.2% $551.2 million

Feb-04 Dec-04 ILEX Oncology Campath, Clorar $1.05 billion Stock 8.0% $551.2 million

Aug-03 Sep-03 SangStat Thymoglobulin $640 million Cash 5.9% $588.8 million

Sep-00 Dec-00 GelTex Renagel, Welchol 8M shares

+ $515 million

Cash + Stock 16.6% $361.7 million

Source: Company reports and Morgan Joseph & Co. Inc.

Maturing Strategy for Growth from Partnerships and Acquisitions

In 2008, Genzyme returned to in-licensing drugs from companies rather than adding them via acquisitions.This year, Genzyme signed several partnerships including ones with Isis, Osiris, and PTC therapeutics, whichlimit Genzyme's upfront expenses for acquiring technologies and products. At the same time, Genzyme hasremained disciplined in its approach to acquiring products, not technologies, which have generally paid off inthe long-term. Drugs in-licensed from these companies focus on Genzyme's strengths in niche areas andleverage Genzyme's global infrastructure.

Genzyme Corporation January 6, 2009

8 MORGAN JOSEPH & CO. INC.

ProductsCerezyme

Cerezyme (imiglucerase for injection) is Genzyme's enzyme replacement therapy for patients with Type 1Gaucher disease. Cerezyme, Genzyme's largest selling drug, accounted for approximately 30% of total productrevenues in 2007 with $1.133 billion in sales.

Gaucher disease is a genetic disorder where the body fails to produce enough glucocerebrosidase, an enzymewhich breaks down a certain type of fat molecule (glucocerebroside). As a result, fatty deposits build up incertain organs and bones of Gaucher patients. There are less than 10,000 cases of Gaucher worldwide—mostcommon type is lysosomal storage disease.

Competition on the horizon ...

Cerezyme does not compete with any enzyme replacement therapies currently. By 2010, there could becompetition for Cerezyme from two enzyme replacement therapies: Shire's Velaglucerase alfa and ProtalixBiotherapeutic's prGCD. Both companies expect Phase III data starting in mid-09 and expect to attain approvalby the end of 2010. Shire is expected to have results from three Phase III studies in mid-09, with a possiblefiling in 2H09. Of the three studies, two of them enrolled naive patients. Protalix completed enrollment of itsPhase III trial in December 2008, and we expect Phase III results in Q309, with a possible filing in Q409.

...but we are not too concerned

In our opinion, these two competitive drugs may have similar efficacy compared to Cerezyme and will have toclear higher regulatory and marketing hurdles. Especially because of the plant-based technology, we believethere will be higher scrutiny on prGCD patients. Additionally, it is not clear at this point if both of thesecompetitors will have sufficient data to convince the FDA that patients can be safely switched from Cerezymeto these new drugs. Since Genzyme is already penetrated in this large market, we expect sales from these newdrugs to come mainly from new patients, implying a very small dent, if any, in Cerezyme's current marketpenetration. Furthermore, the risk of Cerezyme competition to Genzyme is significantly lower than it used tobe historically; Cerezyme currently accounts for 30% of total sales, down from 70% in 2000; we expectCerezyme to account for around 20% of sales in 2011, the first full year that either prGCD or Velaglucerasealfa could be on the market.

Figure 6: Genzyme's Lowered Dependence on Cerezyme

Source: Company reports

Genzyme Corporation January 6, 2009

9 MORGAN JOSEPH & CO. INC.

Fabrazyme

Fabrazyme (agalsidase beta) is Genzyme's enzyme replacement therapy for patients with Fabry's disease.Fabrazyme sales of $424 million in 2007 represented approximately 11% of Genzyme's total product sales.

Fabry disease is a genetic disorder where the body fails to produce enough alpha-galactosidase, an enzymewhich breaks down globotriosylceramide (GL-3). The most serious symptoms of the disease are kidneyfailure, heart disease, and stroke. Fabry disease only affects a few thousand people worldwide.

Shire markets competitive drug Replagal ex-US, however, Fabrazyme is the market leader. Shire, incollaboration with Amicus therapeutics, is developing Amigal (migalastat HCL), an oral chaperone for Fabrydisease. Shire and Amicus are in discussion with the FDA and the EMEA to design a registration program forAmigal and begin Phase III trials in 2009. It is not clear whether Amicus' technology works, and we believeonly a subset of patients can likely be treated with such an approach.

Myozyme

Myozyme (alglucosidase alfa) is Genzyme's enzyme replacement therapy for infantile-onset Pompe disease.Myozyme was approved in the European Union in March 2006 and in the U.S. in April 2006. Myozyme 2007sales of $200.7 million accounted for approximately 5% of total sales.

Pompe's disease is a genetic disorder where the body failed to produce enough acid alpha-glucosidase, anenzyme which normally breaks down glycogen, a compound used by the body to store sugar. Accumulation ofglycogen in lysosomes leads to muscle weakness, particularly in heart and skeletal muscles.

Fast penetration exemplifies high need

Myozyme's penetration into the Pompe's disease market has been quite fast, despite shortage of supply.Especially when compared to the launches of Cerezyme, or even the recently launched Fabrazyme andAldurazyme, Myozyme has had a speedy launch. For instance, 1000 patients were on Fabrazyme in the fourthyear after approval; in Myozyme's case, it has taken only two years to cross 1000 patients in therapy. Webelieve the faster penetration confirms the fundamental strength of the Pompe's market.

Figure 7: Myozyme Sales Projection

Myozyme Sales Projection 2007 2008E 2009E 2010E 2011E

Patient Market (US and EU) 9,300 9,486 9,676 9,869 10,067

Drug cost ($/year) 275,000 275,000 275,000 275,000 275,000

Annual $ market ($ million) 2,558 2,609 2,661 2,714 2,768

Penetration 8% 11% 14% 18% 22%

Sales ($ million) 200.7 296.2 372.5 488.5 609.0

Drug Inflation 0% 0% 0% 0% 0%

Patient market growth 2% 2% 2% 2% 2%

Source: Company reports and Morgan Joseph & Co. Inc.

Manufacturing woes are short-lived

Genzyme is awaiting regulatory action on two plants: a 2000-liter plant in the United States, and a 4000-literplant in Europe (Belgium). We believe the manufacturing shortage is temporary and expect that, in time, the2000L and 4000L plants will be approved to supply drugs in the US and Europe in the near term. We believethe positive advisory panel meeting earlier this year bodes well for the approval of the 2000-liter facility in theUS. In the advisory panel meeting, FDA's panelists agreed, by a vote of 16 to 1, that the LOTS trial haddemonstrated the effectiveness of the 2000-liter product in the late onset of Pompe's disease. The FDA hasagreed to an accelerated decision regarding the 2000-liter facility with a PDUFA date of Feb. 28, 2009. Before

Genzyme Corporation January 6, 2009

10 MORGAN JOSEPH & CO. INC.

February, the FDA and Genzyme need to agree upon a post-approval verification study and a risk evaluationstrategy for the 2000-liter drug. The European filing will likely be made in early 2009, with an approvalexpected by mid-09. We believe the approval of large-scale manufacturing facilities for Myozyme, especiallythe 4000-liter facility, will satisfy global demand for the drug.

There are currently no competitive drugs treating Pompe's disease. Amicus is developing AT2220(1-deoxynojirimcyin HCL), an oral chaperone drug candidate in phase ll studies. Additionally, BioMarin hasBMN-103, an enzyme replacement prospective therapy for Pompe's in preclinical development.

Renagel/Renvela

Renagel (sevelamer hydrochloride) is a calcium-free, metal-free phosphate binder indicated for the control ofserum phosphorus in patients with chronic kidney disease (CKD) on hemodialysis. Renagel 2007 sales of$602.7 million accounted for approximately 17% of total product sales. Renvela, a next-generation sevelamerdrug, contains carbonate and offers better gastrointestinal tolerability compared to Renagel.

In the near term, we expect growth of the Renagel franchise in healthy double-digits as the launch of Renvelain the US is growing the market. In a short time after approval, Renvela has gained around 10% share ofsevelamer scripts. Patients on Renvela are taking a higher dosage of sevelamer because of switching from acombination regimen of Renagel and Phos-Lo to Renvela.

Approval in pre-dialysis CKD patients could offer upside to the Renagel/Renvela franchise, however, we donot include revenue from pre-dialysis patients in our model. In October 2007, An FDA-advisory panel voted8-4 in favor of the usage of phosphate binders for pre-dialysis patients. Since then, Genzyme and FDA havebeen discussing data that would be needed to gain approval in this patient population. Genzyme currentlybelieves it will file an sNDA in mid-09.

Renagel's key competitors include Shire's Fosrenol, a non-calcium based phosphate binder and Fresenius'Phos-Lo. Fosrenol was approved by the FDA in October 2004 and had sales in 2007 of $102 million. Renagelhas maintained its market share close to 50% despite the addition of Fosrenol. Longer-term, Amgen's AMG223 may pose a threat. Amgen added AMG 223 to its pipeline via the Ilypsa acquisition. In earlier trials, AMG223 has demonstrated more efficient binding to phosphate, which could lead to lower doses and thereforebetter GI tolerability. We expect Phase II data from AMG 223 in January 2009; if these data are positive,Amgen may decide to initiate a Phase III study next year. The composition-of-matter patent related to Renagelexpires in 2014, following which we expect generic competition.

Mozobil

Mozobil is an inhibitor of the CXCR4 chemokine receptor, which is present on white blood cells and has beenshown to play a key regulatory role in the trafficking and homing of human CD34+ stem cells in the bonemarrow. Mozobil induces rapid mobilization of stem cells from the bone marrow into the peripheral bloodsystem. We think Mozobil should get FDA approval towards the end of this year based on strong Phase IIIdata. Based on our model, Mozobil's peak revenues will likely be greater than $500 million, much higher thanStreet estimates of $200 - $300 million. Genzyme recently set the pricing for Mozobil at $6,250 per vial. Webelieve most patients will use more than one vial for mobilization.

Genzyme Corporation January 6, 2009

11 MORGAN JOSEPH & CO. INC.

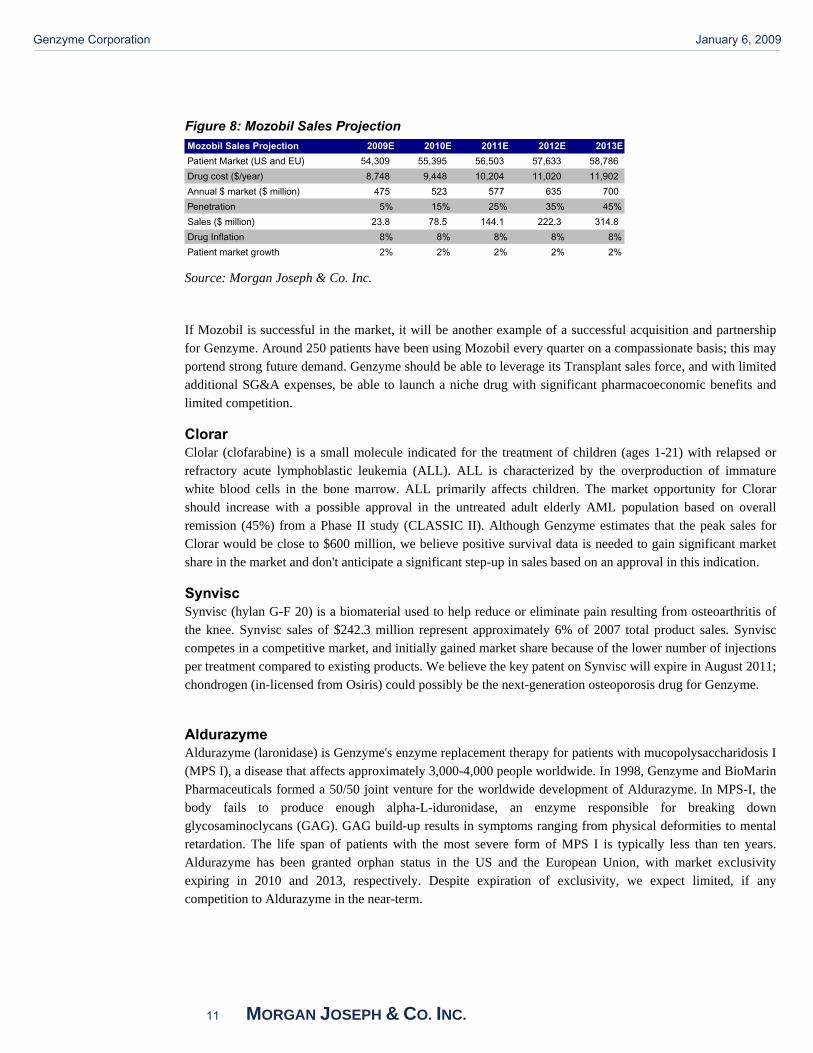

Figure 8: Mozobil Sales Projection

Mozobil Sales Projection 2009E 2010E 2011E 2012E 2013E

Patient Market (US and EU) 54,309 55,395 56,503 57,633 58,786

Drug cost ($/year) 8,748 9,448 10,204 11,020 11,902

Annual $ market ($ million) 475 523 577 635 700

Penetration 5% 15% 25% 35% 45%

Sales ($ million) 23.8 78.5 144.1 222.3 314.8

Drug Inflation 8% 8% 8% 8% 8%

Patient market growth 2% 2% 2% 2% 2%

Source: Morgan Joseph & Co. Inc.

If Mozobil is successful in the market, it will be another example of a successful acquisition and partnershipfor Genzyme. Around 250 patients have been using Mozobil every quarter on a compassionate basis; this mayportend strong future demand. Genzyme should be able to leverage its Transplant sales force, and with limitedadditional SG&A expenses, be able to launch a niche drug with significant pharmacoeconomic benefits andlimited competition.

Clorar

Clolar (clofarabine) is a small molecule indicated for the treatment of children (ages 1-21) with relapsed orrefractory acute lymphoblastic leukemia (ALL). ALL is characterized by the overproduction of immaturewhite blood cells in the bone marrow. ALL primarily affects children. The market opportunity for Clorarshould increase with a possible approval in the untreated adult elderly AML population based on overallremission (45%) from a Phase II study (CLASSIC II). Although Genzyme estimates that the peak sales forClorar would be close to $600 million, we believe positive survival data is needed to gain significant marketshare in the market and don't anticipate a significant step-up in sales based on an approval in this indication.

Synvisc

Synvisc (hylan G-F 20) is a biomaterial used to help reduce or eliminate pain resulting from osteoarthritis ofthe knee. Synvisc sales of $242.3 million represent approximately 6% of 2007 total product sales. Synvisccompetes in a competitive market, and initially gained market share because of the lower number of injectionsper treatment compared to existing products. We believe the key patent on Synvisc will expire in August 2011;chondrogen (in-licensed from Osiris) could possibly be the next-generation osteoporosis drug for Genzyme.

Aldurazyme

Aldurazyme (laronidase) is Genzyme's enzyme replacement therapy for patients with mucopolysaccharidosis I(MPS I), a disease that affects approximately 3,000-4,000 people worldwide. In 1998, Genzyme and BioMarinPharmaceuticals formed a 50/50 joint venture for the worldwide development of Aldurazyme. In MPS-I, thebody fails to produce enough alpha-L-iduronidase, an enzyme responsible for breaking downglycosaminoclycans (GAG). GAG build-up results in symptoms ranging from physical deformities to mentalretardation. The life span of patients with the most severe form of MPS I is typically less than ten years.Aldurazyme has been granted orphan status in the US and the European Union, with market exclusivityexpiring in 2010 and 2013, respectively. Despite expiration of exclusivity, we expect limited, if anycompetition to Aldurazyme in the near-term.

Genzyme Corporation January 6, 2009

12 MORGAN JOSEPH & CO. INC.

Other Products

• Hectorol (doxercalciferol) is a vitamin D prohormone indicated for the treatment of secondaryhyperparathyroidism in patients with CKD. Hectorol sales in 2007 totaled $93 million.

• Campath (alemtuzumab for injection) is a humanized monoclonal antibody indicated for the treatment ofB-cell chronic lymphocytic leukemia (B-CLL) in patients who have been treated with alkylating agents andhave failed fludarabine therapy.

• Thyrogen (thyrotropin alfa for injection) is an alternative diagnostic tool used to monitor well-differentiatedthyroid cancer patients who have had their thyroid glands removed. Sales for Thyrogen in 2007 totaled $114million.

• Thymoglobulin (Anti-thymocyte Globulin (Rabbit)) is a polyclonal antibody indicated for the treatment ofacute rejection in renal transplant patients that is used in conjunction with concomitant immunosuppression.2007 sales for Thymoglobulin were $166 million.

• The Sepra family of products are designed to prevent or reduce adhesions in patients undergoing abdominalor pelvic laparotomy.

• Carticel (autologous cultured chondrocytes) is a biologic product indicated for the repair of knee cartilagedamaged by acute or repetitive trauma.

• Epicel (cultured epidermal autografts) is a permanent skin replacement product for patients who haveexperienced severe burns.

• Genzyme sells diagnostic tools and provides diagnostic services focused primarily in theoncology/pathology and reproductive/genetic areas.

Pipeline

Figure 9: Genzyme's Late Stage Pipeline

Drug Candidate Partner NDA

Mipomersin Isis

Prochymal Osiris

Clorar None

CAMPATH Bayer

GENZ-112638 None

PTC-124 PTC

NG Myozyme None Pompe's disease

Adult acute myeloid leukemia

Multiple Sclerosis

Phase III

Duchenne muscular dystrophy (ex-US rights)

Research/Pre-clinical

Graft vs. Host Disease (ex-US)

Phase I Phase II

Hypercholesterolemia

Gaucher's disease

Source: Company reports and Morgan Joseph & Co. Inc.

Mipomersin

In January 2008, Genzyme entered into a collaboration with Isis Pharmaceuticals for rights to its lead antisensedrug candidate, mipomersin. Mipomersin is a novel, antisense drug candidate that interacts with Apo-B, amolecule that is difficult to target with small molecules. Mipomersin has shown in Phase II studies todramatically lower cholesterol, specifically LDL (the 'bad' cholesterol) and all other atherogenic lipids.

Genzyme provided an upfront payment of $325 million for rights to mipomersin and agreed to up to $1.575billion in milestone payments, including $825 million for development and regulatory milestones, and $750million for commercial milestones. Of the $825 million in milestones for development and regulatoryachievements, $50 million and $150 million are related to the homozygous and heterozygous FH indications.The balance is related to approval in high-cholesterol patients ($375 million) and the approval of follow-onproducts ($250 million). Following approval of mipomersin, Isis will share a portion of mipomersin profit,

Genzyme Corporation January 6, 2009

13 MORGAN JOSEPH & CO. INC.

starting at 30% and up to 50%, as annual sales grow to $2 billion.

Isis' Phase II program evaluated mipomersin in both familial and polygenic hypercholesterolemia patients.Phase II data from several drug doses showed fast, statistically significant reduction in LDL with a strong doseresponse curve. The drug was also shown to have a prolonged effect in all atherogenic lipids including LDLand triglycerides, as shown in the figure below.

Figure 10: Data from Mipomersin First-in Human Trial

Source: Company reports

Since mipomersin has shown to be highly potent, the regulatory focus is on "very high need" diseases such asfamilial hypercholesterolemia (FH) and LDL-apheresis eligible patients. Familial hypercholesterolemia (FH)is a genetic disorder characterized by extremely high cholesterol levels, specifically very high low-densitylipoprotein (LDL or 'bad cholesterol') levels.

Competitive advantages of Mipomersin

Due to proven benefits of having lower cholesterol to one's cardiovascular health, the cholesterol loweringmarket is the largest pharmaceutical market, with drug sales of over $20 billion. Unlike any other drugapproved to lower cholesterol, mipomersin lowers all atherogenic lipids. The JUPITER trial showed thatmipomersin can have potent activity (lowering LDL more than 70%) with very good safety. Mipomersin doesnot have the usual side-effects of statins and can be combined with statins to increase efficacy. Instead of dailypills, mipomersin will likely be injected once-a-week subcutaneously.

Expect Phase III data by mid-2009

Isis and Genzyme have a comprehensive Phase III program, of which one study has been initiated and fourothers are planned to begin shortly:

• Isis and Genzyme are conducting one pivotal Phase III trial evaluating homozygous FH patients.Registration trials are evaluating weekly subcutaneous injections of mipomersin. Genzyme expects

Genzyme Corporation January 6, 2009

14 MORGAN JOSEPH & CO. INC.

enrollment in this phase III trial to be completed by year-end. Genzyme expects data from this trial bymid-2009.

• Genzyme initiated a Phase III trial in August 2008 evaluating mipomersin in around 100 heterozygous FHpatients. Genzyme expects data from this trial in 2010; although we believe results could be seen by the endof 2009 if enrollment happens faster.

• Genzyme plans to initiate three additional trials by the end of this year: one in apheresis-eligible patients,and two in high-risk, high cholesterol patients. These trials will have a 2:1 randomization ratio and utilize a200 mg dose of mipomersin weekly for 26 weeks. We believe enrollment for these trials could happen muchfaster than the homozygous FH trials, and results could come as early as Q409.

Expect homozygous FH filing by 2H10

For severely high risk patients, the FDA has agreed to using LDL-lowering as the primary endpoint. Outcomestudies might be needed for lesser risk patients. It is unclear how the FDA will demarcate risk. At this point,there is the least doubt about the homozygous program, for which there should be adequate data to file forapproval in 2H10. Although there will be LDL-lowering data from the apheresis and heterozygous FH studies,we are not sure that will be enough for approval in those indications in the US. Genzyme has also helddiscussions with the regulatory authorities in Europe. European registration requirements may be more laxthan the FDA; as a result, a faster approval process is expected ex-US.

CAMPATH

CAMPATH (alemtuzumab for injection) is a humanized monoclonal antibody against the cell surfaceglycoprotein, CD52. It is currently approved for the treatment of B-cell chronic lymphocytic leukemia(B-CLL). Genzyme is studying CAMPATH as a treatment of Multiple Sclerosis (MS). Genzyme is developingCAMPATH in collaboration with Bayer.

CAMPATH has shown compelling efficacy in Phase II studies in Multiple Sclerosis. In the Phase II trial, 334patients with active relapsing-remitting Multiple Sclerosis were randomized to treatment with CAMPATH orRebif. CAMPATH was dosed at either 12 or 24 mg per day intravenously for five days followed by a threeday treatment after 12 months and Rebif was dosed at 44 mcg three times per week. The mean disability scoreof patients after CAMPATH improved by 0.39 EDSS points, indicating a recovery of neurologic functions.The median disability score improved to a similar extent after alemtuzumab. In contrast, mean disabilityworsened in the Rebif group by 0.38 EDSS points. The resulting difference at three years between the twotherapies was nearly a 0.77 EDSS with a highly significant p value, p<0.0001.

CAMPATH is currently being studied in two pivotal studies, CARE-MS I and CARE-MS II, looking atfirst-line and relapsed patients, respectively. Time to sustained accumulation of disability and annualizedrelapse rate are the primary endpoints in both pivotal studies. CARE-MS I is a randomized rater-blinded525-patient study comparing CAMPATH to Rebif at the 12mg dosage. CARE-MS II is a randomized trialinvolving 1200 patients who have relapsed on current therapies, randomized to receive one of two doses ofCampath (12mg or 24mg) and placebo. The studies were initiated in 2007 and enrollment is likely to becompleted in 2009, while results from the trials are expected in 2011.

In CARE-MS I, patients are dosed with 12 mg of CAMPATH or placebo for 5 days, followed by a 1 year gapbefore re-treatment. In CARE-MS I, patients are dosed with 12 mg of CAMPATH or 24 mg of CAMPATH orplacebo for 5 days, followed by a 1 year gap before re-treatment. Rebif is dosed 3 times a week.

Genzyme Corporation January 6, 2009

15 MORGAN JOSEPH & CO. INC.

Based on our estimates, the MS market is currently greater than $6 billion, with the top-5 drugs accounting fora majority of the sales. Despite several available treatments, current treatments have suboptimal efficacy(interferon betas and copaxone) or severe safety issues (tysabri). Based on the need in the MS market, and theefficacy shown by CAMPATH, and the convenience of infrequent injections (less than one week per year), webelieve this could be a blockbuster indication for Genzyme. Since the efficacy in Phase II studies was quitecompelling, we believe the key attribute to evaluate in the Phase III trials will be the safety profile ofCAMPATH .

Procymal and Chondrogen

In November 2008, Genzyme entered into a collaboration with Osiris for ex-US rights to Prochymal with anoption to rights to Chondrogen. According to the agreement, Genzyme paid $130 million upfront and couldpay up to $1.25 billion in milestones. A significant portion of the milestones are related to sales, and arepayable only if drug sales cross very large milestones. Genzyme will be responsible for 40% of Phase III trialcosts related to Prochymal and Chondrogen (for studies starting beyond November 2008).

Prochymal is an intravenously administered form of mesenchymal adult stem cells (MSC); these stem cells areextracted from human bone marrow. Phase III data from Prochymal are expected from two Graft vs. HostDisease (GvHD) trials and one Crohn's disease trial in 2009. If these trials are positive, European approvalcould come in 2010. Genzyme has the right to make a go/no-go decision on ex-US rights for Chondrogen,based on a Phase II/III study in patients with osteoarthritis of the knee.

Graft vs. Host Disease (GvHD) occurs in around half of all allogeneic hematopoietic stem cell transplants.Steroids are generally used to treat these patients, and around one-third generally respond to steroid therapy.Patients refractory to steroid therapy have a very high mortality rate. In a small study (31 patients), Prochymalattained a complete response of 74%; by day 28, 94% of the patients responded to therapy. Although werecognize that this was an open-label study, we are encouraged about the mechanism of action and possiblepotent efficacy.

Prochymal's usage can extend to several inflammatory and transplant indications including Crohn's disease,myocardial infarction, COPD, and Type-1 diabetes.

PTC-124

In July 2008, Genzyme entered into a collaboration with PTC Therapeutics (PTC) for ex-US rights toPTC-124. PTC-124 is a novel, orally administered, small-molecule new drug candidate for the treatment ofgenetic disorders resulting from nonsense mutations. According to the agreement, Genzyme paid $100 millionupfront and could pay up to $337 million in milestones, of which $165 million are development and approvalmilestones, mostly related to approvals in Genzyme's territories, and the balance includes sales milestones.PTC expects to receive tiered double-digit royalties from sales in Genzyme territories beginning with sales of$300 million, and increasing in increments through revenues of $2.4 billion. PTC is responsible for two PhaseIIb trials and two additional proof-of-concept trials, following which research expenses are to be sharedequally between Genzyme and PTC.

Genzyme Corporation January 6, 2009

16 MORGAN JOSEPH & CO. INC.

Data from Phase IIa clinical trials of PTC-124 in pediatric patients with nonsense mutation Duchennemuscular dystrophy (nmDMD) showed production of full-length dystrophin and statistically significantreductions in the leakage of muscle-derived creatine kinase into the blood implying decreases in musclefragility. Based on these data, PTC-124 could potentially have broad applicability in several genetic disordersinvolving nonsense mutations.

PTC-124 is currently being evaluated in a phase IIb trial for nmDMD, which is expected to enroll 165 patients;a phase IIb trial in cystic fibrosis (CF) patients planned to begin by YE08.

Other Pipeline Drugs

• Genzyme 112638 is a small molecule for Gaucher disease currently in Phase II studies. We expect finalPhase II data in 1H09, followed by an end of Phase II meeting with the FDA in Q109, and the initiation of aPhase III trial in Q209. Based on positive interim Phase II results, we are excited about this drug's efficacy,which could be similar to Cerezyme. In our opinion, the key risk for this program is longer-term safety,which will not be known until longer-term Phase III studies are run.

• Next Generation Myozyme. Genzyme is also working on a next generation treatment of Pompe's disease.A highly potent version of GAA is currently in preclinical development with an IND on this candidate in1H10. According to Genzyme, this molecule is 5 times more potent than Myozyme.

• GEN-644470. Genzyme expects to file an IND for its next generation phosphate binder, GEN-644470, soon.We believe this could be a next-generation drug to replace Renagel and Renvela. It is not clear whetherGenzyme will be able to get this drug candidate through all clinical and regulatory hurdles before the patentexpires on Renagel.

Valuation

Compared to the current average large cap peer P/E of 17.9x 2009 EPS, Genzyme is trading at an attractiveP/E ratio of 14.3x 2009 EPS. Since Genzyme's growth trajectory is far superior to its peers, we expectGenzyme to trade at a premium to its peers. We derive our price target of $81 using our 2009 EPS estimate of$4.75 and a P/E multiple of 17x.

Figure 11: Current Large-Cap Biotech P/E and P/S Multiples

Ticker Share Shr. Out. 2008E 2009E 2008E 2009E 2008E 2009E 2008E 2009E

Symbol Price (million)

AMGN $59.65 1,060 $15,041 $15,448 $4.52 $4.73 13.2x 12.6x 4.2x 4.1x

BIIB $47.44 292 3,630 3,950 3.64 3.95 13.0x 12.0x 3.8x 3.5x

CELG $54.36 458 2,240 2,960 1.55 2.31 35.1x 23.5x 11.1x 8.4x

DNA $83.00 1,050 13,360 14,490 3.43 3.93 24.2x 21.1x 6.5x 6.0x

GILD $51.00 966 5,340 6,320 2.07 2.51 24.6x 20.3x 9.2x 7.8x

Average: 22.0x 17.9x 7.0x 6.0x

GENZ $67.70 271 4,633 5,301 3.98 4.75 17.0x 14.3x 4.0x 3.5x

Sales ($ million) EPS ($) P/E P/S

Source: Company reports, First Call, and Morgan Joseph & Co. Inc.

Morgan Joseph currently rates the shares of AMGN a Buy and GILD a Hold.

Genzyme Corporation January 6, 2009

17 MORGAN JOSEPH & CO. INC.

Public companies mentioned in this report:

Amicus (FOLD - $8.00 - NASDAQ)

Bayer (BAY.DE - 42.84 - XETRA)

Biomarin (BMRN- $19.00 - NASDAQ)

Isis (ISIS - $14.41 - NASDAQ)

Osiris (OSIR - $20.00 - NASDAQ)

Genzyme Corporation January 6, 2009

18 MORGAN JOSEPH & CO. INC.

Genzyme Income Sheet 2006A Q107A Q207A Q307A Q407A 2007A Q108A Q208A Q308A Q408E 2008E 2009E 2010E 2011E

Revenues

Renal:

Renagel/Renvela 515.1 137.4 145.0 154.2 166.2 602.7 168.7 168.6 171.0 175.0 683.3 765.3 857.1 960.0

Hectorol 93.4 28.3 27.3 30.3 29.9 115.7 29.1 30.9 33.8 32.6 126.4 139.1 153.0 168.3

Total Renal 608.5 165.7 172.3 184.5 196.1 718.4 197.8 199.5 204.8 226.3 809.7 904.4 1,010.1 1,128.3

Therapeutics:

Cerezyme 1,007.0 263.8 283.0 286.1 300.3 1,133.2 304.3 319.4 309.3 315.3 1,248.3 1,323.2 1,402.6 1,332.5

Fabrazyme 359.3 100.7 104.3 104.6 114.7 424.3 116.5 126.6 125.6 137.6 506.3 597.5 705.0 831.9

Thyrogen 93.7 26.3 29.5 26.8 30.9 113.6 33.8 39.4 38.2 41.7 153.1 191.4 229.7 271.0

Myozyme 59.2 37.9 46.7 53.6 62.5 200.7 67.3 77.2 76.7 75.0 296.2 414.7 580.6 772.1

Aldurazyme - - - - - - 37.0 38.8 38.2 40.0 154.0 192.5 231.0 277.2

Mipomersin 44.6 143.4

Other 1.5 0.8 1.1 0.3 7.3 9.5 9.8 10.5 11.4 11.2 42.9 47.2 51.9 57.1

Total Therapeutics 1,520.7 429.5 464.6 471.4 515.7 1,881.3 568.7 611.9 599.4 620.9 2,400.9 2,766.5 3,245.4 3,685.3

Transplant:

Thymoglobulin/Lymphoglobuline 149.5 39.4 41.4 41.0 44.0 165.9 43.7 45.6 45.5 46.5 181.3 199.4 223.4 250.2

Mozobil - - - - - - - - - - - 23.8 78.5 144.1

Other 6.4 1.8 2.0 1.8 3.4 9.1 2.3 2.3 2.4 2.5 9.5 9.9 10.3 10.7

Total Transplant 155.9 41.2 43.4 42.8 47.4 175.0 46.0 47.9 47.9 49.0 190.8 233.1 312.1 405.0

Biosurgery:

Synvisc 233.9 53.6 64.9 61.2 62.7 242.3 56.1 70.9 67.5 69.0 263.5 279.3 290.5 302.1

Sepra 85.3 23.1 25.1 26.4 29.7 104.3 30.6 34.8 33.0 35.6 134.0 167.5 201.0 241.2

Other 68.4 21.7 18.0 18.6 21.8 80.0 24.9 25.5 22.4 25.3 98.1 112.8 129.7 149.2

Total Biosurgery 387.6 98.4 108.0 106.2 114.2 426.6 111.6 131.2 122.9 129.9 495.6 559.6 621.2 692.5

Genetics:

Total Genetics 240.9 66.2 73.7 73.1 72.2 285.1 74.3 78.5 82.1 85.6 318.9 360.4 407.2 460.1

Other:

Diagnostics 115.0 30.8 29.5 - - 60.3 - - - - - - - -

Oncology 59.4 22.4 17.4 22.7 26.0 88.5 29.0 33.3 34.0 36.0 132.4 158.9 190.7 228.8

Other 99.0 29.0 24.5 59.6 65.2 178.3 72.6 68.9 69.3 73.5 284.3 318.4 356.6 399.4

Total Other 273.4 82.2 71.4 82.3 91.2 327.1 101.6 102.2 103.3 109.5 416.7 477.3 547.3 628.2

Total Revenues 3,187.0 883.2 933.4 960.3 1,036.8 3,813.5 1,100.0 1,171.2 1,160.4 1,221.1 4,632.6 5,301.2 6,143.4 6,999.4

Operating expenses

COGS 714.2 196.6 210.7 227.1 246.4 880.7 265.8 294.0 278.3 293.1 1,131.2 1,272.3 1,413.0 1,609.9

SG&A 879.3 246.3 240.2 245.2 284.3 1,016.1 295.5 315.4 306.9 329.7 1,247.5 1,378.3 1,535.8 1,679.9

R&D 565.4 146.3 154.3 162.3 178.5 641.4 180.3 190.8 190.6 195.4 757.1 848.2 921.5 979.9

Total Operating expenses 2,158.9 589.2 605.2 634.6 709.2 2,538.2 741.6 800.2 775.8 818.2 3,135.8 3,498.8 3,870.3 4,269.6

Operating Income 1,028.1 294.0 328.2 325.7 327.6 1,275.3 358.4 371.0 384.6 403.0 1,496.9 1,802.4 2,273.1 2,729.8

Other Income

Equity in income(loss) 5.4 1.8 5.9 6.5 9.3 23.5 0.2 - - - (0.8) (0.9) (1.0) (1.1)

Minority interest 0.1 0.1 - - - 0.1 0.5 0.6 0.6 0.5 1.7 1.0 1.0 1.0

Gain on investment (1.2) 1.9 0.1 1.1 (1.0) 2.2 0.8 0.1 0.1 0.1 1.1 0.5 0.7 1.0

Other 5.9 (0.5) (0.3) 0.9 (1.5) (1.4) (0.2) - (0.7) - 0.2 0.2 0.3 0.1

Investment income 56.0 16.2 17.2 18.2 18.5 70.2 14.9 13.4 11.8 9.0 53.5 32.0 35.0 37.0

Interest income (expense) (15.5) (4.2) (3.6) (1.5) (2.9) (12.1) (1.7) (1.1) (0.8) (3.0) (6.6) (15.5) (15.5) (15.5)

Total Other Income 50.7 15.3 19.3 25.2 22.4 82.5 14.5 13.0 11.0 6.6 49.1 17.3 20.5 22.5

Earnings (loss) before taxes 1,078.8 309.3 347.5 350.9 350.0 1,357.8 372.9 384.0 395.6 409.6 1,546.0 1,819.7 2,293.6 2,752.3

Income taxes (336.1) (98.5) (108.9) (109.6) (100.9) (417.9) (112.0) (115.3) (105.7) (118.8) (448.3) (509.5) (665.1) (798.2)

Net Income 742.7 210.8 238.6 241.3 249.1 939.9 260.9 268.7 289.9 290.8 1,097.7 1,310.2 1,628.4 1,954.1

Earnings per share 2.77 0.78 0.88 0.90 0.91 3.47 0.95 0.98 1.04 1.01 3.98 4.75 5.86 7.03

Outstanding shares (basic) 261.1 263.5 263.9 262.8 265.4 263.9 267.3 266.9 269.2 268.9 268.1 267.4 267.9 268.4

Outstanding shares (diluted) 268.0 270.2 270.9 269.5 273.7 271.1 275.5 274.6 278.5 287.5 279.0 276.0 278.0 278.0

Source: Company Reports and Morgan Joseph & Co. Inc. estimates

Genzyme Corporation January 6, 2009

19 MORGAN JOSEPH & CO. INC.

Genzyme Balance Sheet as of: Dec 07A Mar 08A Jun 08A Sep 08A

Assets

Current Assets

Cash And Cash Equivalents 867.01 882.80 693.69 918.74

Short Term Investments 80.45 79.05 67.69 76.57

Net Receivables 1,068.44 1,189.69 1,225.21 1,171.24

Inventory 439.12 468.82 472.54 442.90

Other Current Assets 154.18 160.03 170.71 200.67

Total Current Assets 2,609.20 2,780.39 2,629.83 2,810.11

Long Term Investments 602.12 654.44 656.05 647.62

Property Plant and Equipment 1,968.40 2,118.96 2,212.04 2,268.85

Goodwill 1,403.83 1,403.72 1,404.07 1,403.57

Intangible Assets 1,555.65 1,982.74 1,990.16 1,935.03

Accumulated Amortization - - - -

Other Assets 66.88 22.11 19.95 19.03

Deferred Long Term Asset Charges 95.66 120.71 270.75 331.37

Total Assets 8,301.74 9,083.05 9,182.85 9,415.59

Liabilities

Current Liabilities

Accounts Payable 792.50 757.35 776.55 760.75

Short/Current Long Term Debt 696.63 696.74 696.86 697.43

Other Current Liabilities 13.28 21.57 18.73 17.85

Total Current Liabilities 1,502.41 1,475.66 1,492.14 1,476.03

Long Term Debt 113.75 111.14 109.16 125.35

Other Liabilities 55.99 532.72 525.37 564.01

Deferred Long Term Liability Charges 16.66 15.54 14.78 14.31

Minority Interest - - - -

Negative Goodwill - - - -

Total Liabilities 1,688.80 2,135.06 2,141.45 2,179.70

Stockholders' Equity

Misc Stocks Options Warrants - - - -

Redeemable Preferred Stock - - - -

Preferred Stock - - - -

Common Stock 2.66 2.67 2.67 2.70

Retained Earnings 826.72 971.99 1,041.55 1,161.15

Treasury Stock - - - -

Capital Surplus 5,385.15 5,461.71 5,491.73 5,736.68

Other Stockholder Equity 398.41 511.62 505.46 335.36

Total Stockholder Equity 6,612.94 6,947.99 7,041.40 7,235.88

Liabilities and Equity 8,301.74 9,083.05 9,182.85 9,415.59

Source: Company Reports and Morgan Joseph & Co. Inc. estimates

Genzyme Corporation January 6, 2009

20 MORGAN JOSEPH & CO. INC.

Required Disclosures

Q1 Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q340

50

60

70

80

90

2007 2008 2009

Rating and Price Target History for: Genzyme Corporation (GENZ) as of 01-05-2009

Created by BlueMatrix

Price TargetOur price target is $81.

Valuation MethodologyWe derive our price target of $81 using a 17x multiple on our 2009 EPS estimate of $4.75.

Risk FactorsThe key risks of investing in Genzyme shares include, in our view, clinical, regulatory, competitive, and reimbursement risks:

■ Regulatory risks. Drugs may not gain approval from regulatory agencies such as the FDA or EMEA. Genzyme could faceregulatory risks with mipomersin, clorar, Campath, Prochymal, and PTC 124, among other drugs.

■ Patent risks. The company will likely loose market share to generic drugs, due to aggressive pricing, once its patents expire. Keypatent risks associated with Genzyme relate to Synvisc and Renagel. Synvisc patents expire in 2011, while key Renagel patentsexpire in 2014.

■ Clinical risks. Drugs in clinical trials may not advance because of inadequate safety, efficacy, or because a determination ofefficacy or safety cannot be made. Key clinical risks associated with Genzyme relate to mipomersin, clorar, Campath, Prochymal,and PTC 124, among other drugs.

■ Competition. We expect competition for the company's drugs from many public and private companies developingpharmaceuticals: Especially devastating can be any success of a disruptive technology that treats genetic diseases.

■ Reimbursement risk. Sales of the company's drugs should be highly dependent on reimbursement from private insurers as well asgovernment agencies. Success of an approved drug will depend on reimbursement, which can depend on the strength of clinicaldata.

Genzyme Corporation January 6, 2009

21 MORGAN JOSEPH & CO. INC.

Q1 Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q330

40

50

60

70

80

2007 2008 2009

07/28/08I:Buy:$77

08/25/08Buy:$80

Rating and Price Target History for: Amgen, Inc. (AMGN) as of 01-05-2009

Created by BlueMatrix

Q1 Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q320

30

40

50

60

2007 2008 2009

12/09/08I:Hold:NA

Rating and Price Target History for: Gilead Sciences, Inc. (GILD) as of 01-05-2009

Created by BlueMatrix

I, Shiv Kapoor, the author of this research report, certify that the views expressed in this report accurately reflect my personal viewsabout the subject securities and issuers, and no part of my compensation was, is, or will be directly or indirectly tied to the specificrecommendations or views contained in this research report.

Research analyst compensation is dependent, in part, upon investment banking revenues received by Morgan Joseph & Co. Inc.

Morgan Joseph & Co. Inc. intends to seek or expects to receive compensation for investment banking services from the subjectcompany within the next three months.

Genzyme Corporation January 6, 2009

22 MORGAN JOSEPH & CO. INC.

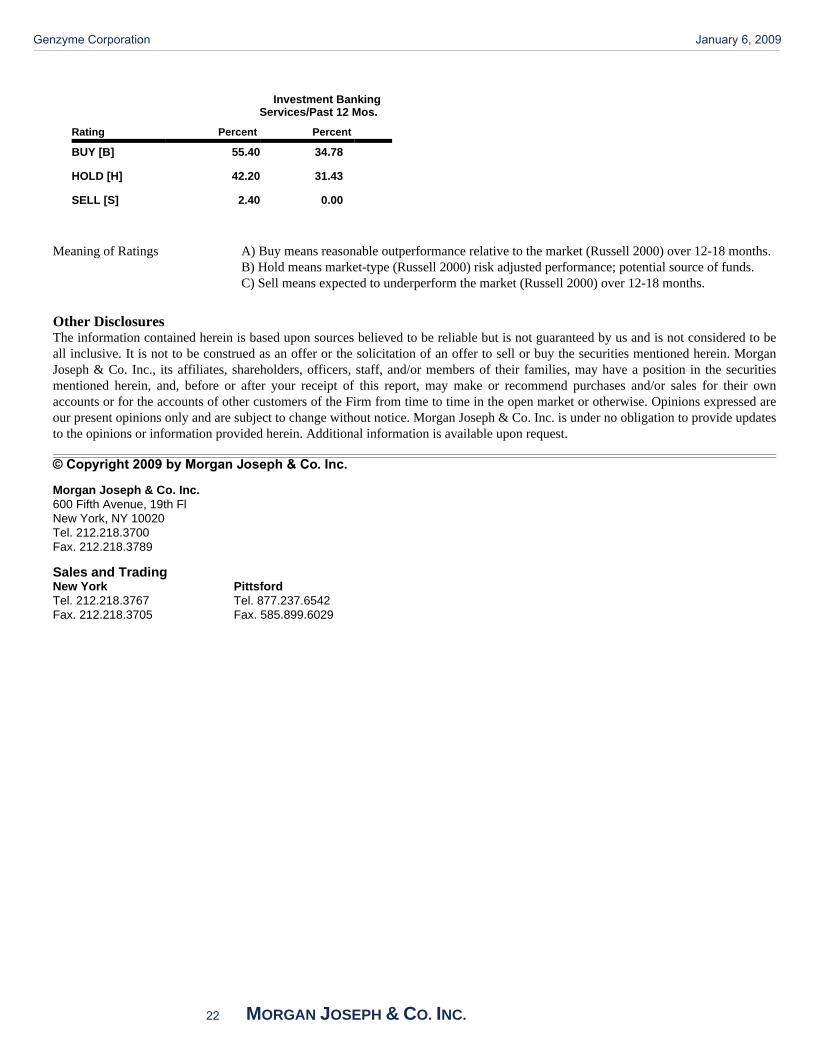

Investment BankingServices/Past 12 Mos.

Rating Percent Percent

BUY [B] 55.40 34.78

HOLD [H] 42.20 31.43

SELL [S] 2.40 0.00

Meaning of Ratings A) Buy means reasonable outperformance relative to the market (Russell 2000) over 12-18 months.B) Hold means market-type (Russell 2000) risk adjusted performance; potential source of funds.C) Sell means expected to underperform the market (Russell 2000) over 12-18 months.

Other DisclosuresThe information contained herein is based upon sources believed to be reliable but is not guaranteed by us and is not considered to beall inclusive. It is not to be construed as an offer or the solicitation of an offer to sell or buy the securities mentioned herein. MorganJoseph & Co. Inc., its affiliates, shareholders, officers, staff, and/or members of their families, may have a position in the securitiesmentioned herein, and, before or after your receipt of this report, may make or recommend purchases and/or sales for their ownaccounts or for the accounts of other customers of the Firm from time to time in the open market or otherwise. Opinions expressed areour present opinions only and are subject to change without notice. Morgan Joseph & Co. Inc. is under no obligation to provide updatesto the opinions or information provided herein. Additional information is available upon request.

© Copyright 2009 by Morgan Joseph & Co. Inc.

Morgan Joseph & Co. Inc.600 Fifth Avenue, 19th FlNew York, NY 10020Tel. 212.218.3700Fax. 212.218.3789

Sales and TradingNew YorkTel. 212.218.3767Fax. 212.218.3705

PittsfordTel. 877.237.6542Fax. 585.899.6029

Genzyme Corporation January 6, 2009