key takeaways - asiawealth.co.th takeaways 2 please see ... 1,289 1,342 1,379 1,535 1,678 sg&a...

TRANSCRIPT

3 February 2015

Key Takeaways

1

Please see disclaimer on last page

VGI Global Media PCL (VGI)

► Analyst meeting on 2 February 2015

► Ongoing good news from increased advertising space.

► 4QFY15 earnings to be neutral but bright earnings outlook

for FY16.

Good news from increased advertising space

VGI and Chulalongkorn University are in the process of negotiating

a contract that would allow the company to use space inside and

outside of Chamchuri Square, a high-rise complex located in a CBD

area. After it signs the contract, VGI expects to begin generating

revenue around June 2015 onward with minimum rent as fixed cost.

Management expects this to contribute around Bt75mn per year

from selling space on two of the mega LEDs and a total of 127

panels of digital & static media. In addition, VGI has been appointed

as the exclusive agent to manage four mega digital billboards at

Victory Monument, which is one of the busiest intersections in

Bangkok with more than 350,000 vehicles driving past every day.

VGI has also installed one mega digital billboard outside Empire

Tower. These mega billboards are expected to contribute around

Bt130mn in revenue per year. The new developments would not

only drive revenue going forward, but also diversify VGI’s business

risk as it diversifies the advertising space in its portfolio.

Don’t expect good 4QFY15 earnings (Jan-Mar 15), but FY16

should be bright

We expect VGI’s 4QFY15 earnings to decline QoQ as it is normally

a low quarter for the company with the country’s low season for

consumption and advertising spending together with the loss of the

sales floor contract at Tesco Lotus from Feb 2015 onward. We

expect VGI’s FY15 net profit to drop 6% YoY to Bt1.07bn.

However, with many good deals to boost revenue, we see bright

earnings for FY16 and good prospects in the medium term. We

expect VGI’s FY16 net profit to increase 19% YoY to Bt1.3bn. We

maintain our earnings forecast for FY15-17 and recommend BUY

with a target price of Bt16.30.

Note: VGI announced a cash dividend payment for its 3QFY15

operations of Bt0.011/share and a stock dividend payment at a

ratio of 1 existing share : 1 stock dividend, XD date 17 Mar 2015.

After XD our target price should drop to Bt8.15/share to reflect the

increase in the number of shares.

BUY

TP: Bt16.30 Upside/downside +32%

Sector Media & Publishing

Paid-up shares (shares mn) 3,432

Market capitalization (Bt mn) 43,243

Free float (%) 36.40

12-mth daily avg. turnover (Bt mn) 189

12-mth trading range (Bt) 14.60/8.35

Major shareholders (%)

BTSC 51.0

BTS Group Holding PCL 11.2

Thai NVDR 2.9

Financial highlights (Year-end Mar)

Source: SET, AWS

Thailand Research Department

Mr. Warut Siwasariyanon,

License, No. 17923

Tel: 02 680 5041

Ms. Sukanya Leelarwerachai, (Assistant Analyst)

Unit: Btmn FY2013 FY2014 FY2015E FY2016E

Revenue 2,838 3,149 3,040 3,551

Normalized Profit 902 1,146 1,040 1,285

Extra items - - 38 -

Net Profit 902 1,146 1,078 1,285

EPS (Bt) 0.26 0.33 0.31 0.37

EPS Growth (%) n.m. 27% -5% 19%

P/E (x) 48.5 38.2 40.1 33.7

P/BV(x) 23.7 22.1 21.0 19.7

DPS (Bt) 0.26 0.31 0.28 0.34

Div. Yield (%) 2% 2% 2% 3%

3 February 2015

Key Takeaways

2

Please see disclaimer on last page

Key Financial Ratios FY2013 FY2014 FY2015E FY2016E FY2017E

Operating Revenue Growth (%) 44% 11% -3.5% 17% 13%

Net Profit Growth (%) 224% 27% -6% 19% 16%

EPS Growth (%) 0% 27% -5% 19% 16%

Gross Profit Margin (%) 55% 57% 55% 57% 58%

Operating Profit Margin (%) 41% 44% 41% 43% 44%

EBITDA Margin (%) 45% 48% 49% 50% 51%

Net Profit Margin (%) 32% 36% 35% 36% 37%

Effective tax rate (%) 24% 19% 19% 20% 20%

ROA (%) 35% 42% 36% 40% 43%

ROE (%) 50% 59% 52% 59% 64%

Net Debt to Equity (x) 0.00 0.00 0.10 0.09 0.09

EPS (Bt) 0.26 0.33 0.31 0.37 0.43

BVPS (Bt) 0.53 0.57 0.60 0.64 0.68

DPS (Bt) 0.26 0.31 0.28 0.34 0.39

Dividend Payout Ratio 100% 94% 90% 90% 90%

P/E (x) 48.5 38.2 40.1 33.7 29.1

P/BV (x) 23.7 22.1 21.0 19.7 18.5

EV/EBITDA (x) 15.9 13.6 13.6 63.8 55.2

Div. Yield (%) 2% 2% 2% 3% 3%

Income Statement

Unit: Btmn FY2013 FY2014 FY2015E FY2016E FY2017E

Operating Revenue 2,838 3,149 3,040 3,551 4,006

COGS 1,289 1,342 1,379 1,535 1,678

SG&A 390 426 420 490 553

Gross Profit 1,548 1,807 1,662 2,016 2,328

Operating Profit 1,158 1,381 1,242 1,526 1,776

EBITDA 1,289 1,510 1,503 1,785 2,059

Tax 285 273 257 321 371

Interest Expenses 2.2 0.7 8.0 4.0 4.0

Normalized Profit 902 1,146 1,040 1,285 1,486

One-off items - - 38 - -

Net Profit 902 1,146 1,078 1,285 1,486

EPS (Bt) 0.26 0.33 0.31 0.37 0.43

Statement of Financial Position

Unit: Btmn FY2013 FY2014 FY2015E FY2016E FY2017E

Cash & Short-term investments 1,254 1,009 859 822 992

Account Receivable 673 607 586 685 772

Total Current Assets 1,995 1,630 1,459 1,520 1,778

Net Equipment 473 923 1,367 1,497 1,453

Total Non-Current Assets 584 1,111 1,555 1,685 1,641

Total Assets 2,579 2,741 3,014 3,205 3,420

Short-Term Borrowings - - 200 200 200

Account Payable 178 151 155 172 188

Total Current Liabilities 737 762 924 984 1,047

Provision for LT employee 22 26 28 31 34

Total Liabilities 758 788 953 1,015 1,082

Paid-up Capital 300 343 343 343 343

Capital Surplus 863 863 863 863 863

Retained Earnings 623 749 857 985 1,134

Total Equity 1,821 1,953 2,061 2,190 2,338

Total Liabilities and Equity 2,579 2,741 3,014 3,205 3,420

Key Assumptions FY2013 FY2014 FY2015E FY2016E FY2017E

Revenue Breakdown (%)

BTS Media 50 53 62 62 64

Modern Trade Media 44 41 30 24 23

Office Building & Others 6 6 8 14 14

Gross margin (%)

BTS Media 78% 81% 76% 75% 75%

Modern Trade Media 26% 25% 15% 25% 25%

Office Building & Others 72% 69% 65% 70% 70%

Source: SET, AWS estimates

3 February 2015

CG Report

3

Please see disclaimer on last page

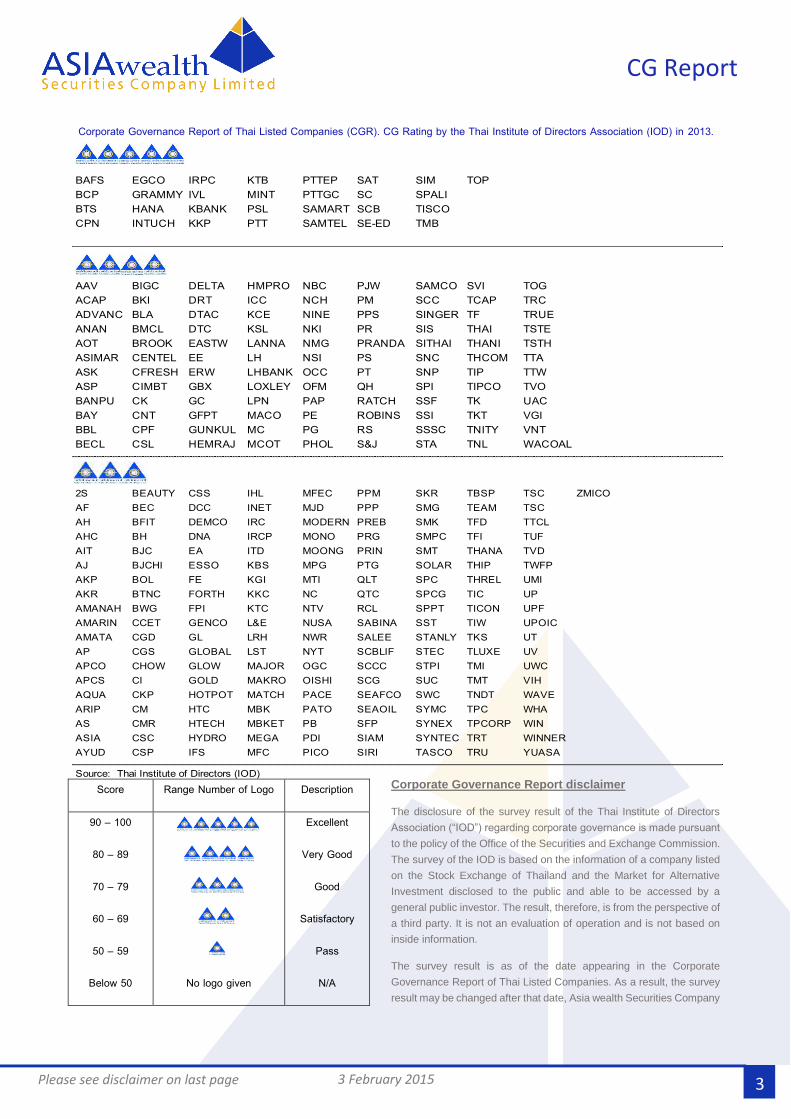

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (IOD) in 2013.

Corporate Governance Report disclaimer

The disclosure of the survey result of the Thai Institute of Directors

Association (“IOD”) regarding corporate governance is made pursuant

to the policy of the Office of the Securities and Exchange Commission.

The survey of the IOD is based on the information of a company listed

on the Stock Exchange of Thailand and the Market for Alternative

Investment disclosed to the public and able to be accessed by a

general public investor. The result, therefore, is from the perspective of

a third party. It is not an evaluation of operation and is not based on

inside information.

The survey result is as of the date appearing in the Corporate

Governance Report of Thai Listed Companies. As a result, the survey

result may be changed after that date, Asia wealth Securities Company

Limited does not conform nor certify the accuracy of such survey result.

Score Range Number of Logo Description

90 – 100

80 – 89

70 – 79

60 – 69

50 – 59

Below 50

No logo given

Excellent

Very Good

Good

Satisfactory

Pass

N/A

BAFS EGCO IRPC KTB PTTEP SAT SIM TOPBCP GRAMMY IVL MINT PTTGC SC SPALIBTS HANA KBANK PSL SAMART SCB TISCOCPN INTUCH KKP PTT SAMTEL SE-ED TMB

AAV BIGC DELTA HMPRO NBC PJW SAMCO SVI TOGACAP BKI DRT ICC NCH PM SCC TCAP TRCADVANC BLA DTAC KCE NINE PPS SINGER TF TRUEANAN BMCL DTC KSL NKI PR SIS THAI TSTEAOT BROOK EASTW LANNA NMG PRANDA SITHAI THANI TSTHASIMAR CENTEL EE LH NSI PS SNC THCOM TTAASK CFRESH ERW LHBANK OCC PT SNP TIP TTWASP CIMBT GBX LOXLEY OFM QH SPI TIPCO TVOBANPU CK GC LPN PAP RATCH SSF TK UACBAY CNT GFPT MACO PE ROBINS SSI TKT VGIBBL CPF GUNKUL MC PG RS SSSC TNITY VNTBECL CSL HEMRAJ MCOT PHOL S&J STA TNL WACOAL

2S BEAUTY CSS IHL MFEC PPM SKR TBSP TSC ZMICOAF BEC DCC INET MJD PPP SMG TEAM TSCAH BFIT DEMCO IRC MODERN PREB SMK TFD TTCLAHC BH DNA IRCP MONO PRG SMPC TFI TUFAIT BJC EA ITD MOONG PRIN SMT THANA TVDAJ BJCHI ESSO KBS MPG PTG SOLAR THIP TWFPAKP BOL FE KGI MTI QLT SPC THREL UMIAKR BTNC FORTH KKC NC QTC SPCG TIC UPAMANAH BWG FPI KTC NTV RCL SPPT TICON UPFAMARIN CCET GENCO L&E NUSA SABINA SST TIW UPOICAMATA CGD GL LRH NWR SALEE STANLY TKS UTAP CGS GLOBAL LST NYT SCBLIF STEC TLUXE UVAPCO CHOW GLOW MAJOR OGC SCCC STPI TMI UWCAPCS CI GOLD MAKRO OISHI SCG SUC TMT VIHAQUA CKP HOTPOT MATCH PACE SEAFCO SWC TNDT WAVEARIP CM HTC MBK PATO SEAOIL SYMC TPC WHAAS CMR HTECH MBKET PB SFP SYNEX TPCORP WINASIA CSC HYDRO MEGA PDI SIAM SYNTEC TRT WINNERAYUD CSP IFS MFC PICO SIRI TASCO TRU YUASA

Source: Thai Institute of Directors (IOD)

3 February 2015

Contact

4

Please see disclaimer on last page

This report has been prepared by Asia Wealth Securities Company Limited (“AWS”). The information herein has been obtained from sources believed to be reliable and accurate, but AWS makes no representation as to the accuracy and completeness of such information. AWS does not accept any liability for any loss or damage of any kind arising out of the use of such information or opinions in this report. Before making your own independent decision to invest or enter into transaction, investors should study this report carefully and should review information relating. All rights are reserved. This report may not be reproduced, distributed or published by any person in any manner for any purpose without permission of AWS. Investment in securities has risks. Investors are advised to consider carefully before making decisions.

Branch Address Phone Fax

Head Office 540 Floor 7,14,17 , Mercury Tower, Ploenchit Road, Lumphini,

Pathumwan Bangkok 10330

02-680-5000 02-680-5111

Silom 191 Silom Complex Building,21st Floor Room 2,3-1 Silom Rd.,

Silom, Bangrak, Bangkok, 10500 Thailand

02-630-3500 02-630-3530-1

Asok 159 Sermmitr Tower, 17th FL. Room No.1703, Sukhumvit 21

Road, Klong Toey Nua, Wattana, Bangkok 10110

02-261-1314-21 02-261-1328

Pinklao

7/3 Central Plaza Pinklao Office Building Tower B, 16th Flr., Room

No.1605-1606 Baromrajachonnanee Road, Arunamarin,

Bangkoknoi, Bangkok 10700

02-884-7333 02-884-7357,

02-884-7367

Chaengwattana

99/99 Moo 2 Central Plaza Chaengwattana Office Tower, 22nd Flr.,

Room 2204 Chaengwattana Road, Bang Talad, Pakkred,

Nonthaburi 11120

02-119-2300 02-8353014

Chaengwattana 2

9/99 Moo 2 Central Plaza Chaengwattana Office Tower, 22nd Flr.,

Room 2203 Chaengwattana Road, Bang Talad, Pakkred,

Nonthaburi 11120

02-119-2388 02-119-2399

Mega Bangna 39 Moo6 Megabangna, 1st Flr., Room 1632/7 Bangna-Trad Road,

Bangkaew Bangplee, Samutprakarn 10540

02-106-7345 02-105-2070

Rayong 356/18 Sukhumvit Road, Nuen-Phra Sub District, Muang District,

Rayong Province 21000

038-808200 038-807200

Khonkaen 26/9 Srijanmai Road, Tamboonnaimuang, Khon Khaen

40000

043-334-700 043-334-799

Chonburi 44 Vachiraprakarn Road, Bangplasoi, Muang Chonburi, Chonburi

20000

038-274-533 038-275-168

Chaseongsao 233-233/2 Moo2 1st Flr., Sukprayoon Road, Na Meung Sub-

District, Meung District, Chachoengsao 24000

038-981-587 038-981-591