keynes's general theory and structural...

TRANSCRIPT

It

jt1{

IIT

I

fvar Jonsson:

Keynes's GeneralTheory and Structural

Competitiveness

r kjolfar efnahagskreppunnar 6 Vesturlondum. sem h6fst 66ttunda aratugnum scetf keynesisminn og kenningar John

Maynard Keynes har5ri gagnrYni. pa5 voru einkum ny-klassfskirog rnonetorfsklr hagfrcebingar, sern gagnrYndu Keynes. r pessorl

grein er sett fram strukturollsk gagnrYni 6 kenningar Keynes umatvinnustig og vexti , auk pess sern kenningar hans eru prooocr

6fram. Pab er geit meb tillitl til mikilvcegis tceknlprouncr ogstofnanagrunns llagkerfa fyrir ouomcqnsupphleoslu. atvinnustig

og pjobatekjur. Jafnframt er sett fram likan af ,formgerbarlegrisamkeppnishcefni' sem byggir a pessorl gagnrYni 6 kenningar

Keynes.

T:e main subjec~ of this article isacritique of). M. Keynes's theories ofemployment and output. The limited problematic and inadequate solutions of his

'general theory' are criticized and the discussion results in a model of the deter-mirumts of 'structural competitiveness' and hence output and employment. With

this model, we will present the main elements of a general theory or generalizedtheory that incorporates structural arul institutional determinants of capital

accumuwtion, i.e. a theory of Keynes's 'given factors' that he fails to analyse.Economic theories tend to be based on models characterized by ideal

types on high level of abstraction. As a consequence the validity of economictheoretical discourse tends to be biased towards big economies. It is one of ourbasic postulate that there is a fundamental difference between small economies

and bigeconomies, in the sense that the possibility of the rule of market rationality (or

~6am(jj12. 1991. s. 87-117.

I

'real abstractions' in the marxist sense') in a capitalist socio-economic formation,is the more limited the smaller the economy is. As a consequence, from thepoint of view of a metacritique of the object of economic analysis, formalist andrationalist approaches to the dynamics of the development of small socio-economic formations loose much of their validity and explanatory power inthis context. It follows that a 'critical' approach to economic analysis thatattempts to overcome the sizebias of economic theories and cover characteristicsof small economies and microstates, emphasizes historical specificity andhence ismore realist than a rationalist approach (for further discussion see {varJonsson 19(1).

What is at stake is therefore the realism of approaches and theoriesof socio-economic phenomena, i.e. realism which is determined by the natureofthe object of analysis. In view of recent history of economic thought, onecan analyse Keynes's critique of neo-classical economics as being a realistcritique of the rationalism of neo-classical economics just as one can analyseneo-schumpeterian and regulation-school critique of Keynesian ism as well asneo-classical theories as being fundamentally a quest for extending the objectof analyses to the dynamics of social and technological change (see IvarJonsson 1991). We would argue that for the sake of realist approach, thedefinition of the object has to take into account as wen the size factor of theeconomy which determines the ontology/existence of market rationality and'real abstractions'.

Let's start by discussing Keynes's critique of neo-classical theory.

a) Keynes's critique of neo-closslcol theoryKeynes critique of neo-classical economics' was at the same time a pragmatistand a realist (although limited) critique of the orthodox theories of his day andeconomic policies based on them. In his General Theory he claims that:

Our criticism of the accepted classical theory of economics (i.e. neo-classicaltheory - LJ.) has consisted not so much in finding logical flaws in its analysisas in pointing out that its tacit assumptions are seldom or never satisfied, withthe result that it cannot solve the economic problems of the actual world.(J.M. Keynes 1983,378).

And he states:

Our present object is to discover what determines at any time the nationalincome of a given economic system and (which is almost the same thing) theamount of its employment ...Our final task might be to select those variableswhich can be deliberately controlled or managed by central authority in thekind of system in which we actually live. (ibid., 247).

Keynes's main object of analysis is the conditions ofoptimal equilibriumwith fun employment in his contemporary capitalism. He criticizes the neo-classical theory for its notion of equilibrium which is only valid, according toKeynes, in particular circumstances and claims therefore that it isnot generallyvalid. As a consequence, Keynes opposes the neo-classical notion of'stationaryequilibrium' with his own notion of'shitting equilibrium'. The former presumesthat price formation is determined by demand and supply and relative pricesare constantly reproduced, given pure market dearing and no externaldisturbing force. Shifting equilibrium on the other hand refers to:

...theory of a system in which changing views about the future are capable ofinfluencing the present situation ... We can consider what distribution ofresources between different uses will be consistent with equilibrium underthe influence of normal economic motives in a world in which our viewsconcerning the future are fixed and reliable mall respects ...were all things areforeseen from the beginning. Or we can pass from this simplified propaedeuticto the problems of the real world in which our previous expectations are liableto disappointment and expectations concerning the future affect of what wedo to-day. [ibid., 293).

It goes that Keynes's approach, unlike the neo-clsssical one, emphasizes theopenness or shifting nature of the object of analysis and is based on anevolutionary world view stressing the need of flexibility in theory as wen aspolicy:

The object of our analysis is, not to provide a machine, or method of blindmanipulation, which will furnish an infallible answer, but to provide ourselveswith an organized and orderly method of thinking out particular problems;and, after we have reached a provisional conclusion by isolating thecomplicating factors one by one, we then have to go back on ourselves andallow, as well as we can, for the probable interactions of the factors amongthemselves. This is the nature of economic thinking. Any other way ofapplying our formal principles of thought (without which, however, we shanbe lost in the wood) will lead us into error. It is the great fault of symbolicpseudo-mathematical methods of formalizing a system of economicanalysis ... that they expressly assume strict independence between the factorsinvolved and lose all their cogency and authority if this hypothesis isdisallowed ...Too large a proportion of recent 'mathematical' economics aremerely concoctions, as imprecise as the initial assumptions they rest on,which allow the author to lose sight of the complexities and interdependenceof the real world in a maze of pretentious and unhelpful symbols. (ibld., 297 -8).

88··-89

It is this 'evolutionary' approach, if you like, of 'shifting equilibrium'on which Keynes's critique of the neo-classical theory isbased. To put it briefly,he claims that the kind of equilibrium presumed by the Say's law, in whichproduction creates its own demand, is not established as shifting expectationsdo affect confidence in the different markets so that markets do not clear in anoptimizing way concerning output. In the last analysis it is, according toKeynes, the level of aggregate demand that determines investment and output!employment through the level of confidence.

b) Keynes's critique of the neo-closstcol theoryof employment

In his General Theory Keynes develops a theory of the formation of confidence,which is, we will argue, only partial and inadequate. It is partial as heconcentrates only on the neo-classical theory of wages and employment andthe orthodox theory of interests (what he cans the 'classical theory ofinterests'), and it is inadequate as his theory of interests is not fully developed.But the greatest shortcoming of Keynes's approach is that it is based on adualism of the spiritual and physical worlds which obscures the role and thedynamics of the formation of techno-economic paradigms, i.e, the missingmoment in his theory of the formation of confidence in capitalist economies.As goes for neo-classical theory, Keynes view of technology is based on themarginalist view of the malleability offactors ofproduction, and asa consequencethe factor of technical change is never problematized. Let's have a closer lookat his critique of neo-classical theory and his model.

Keynes reduces the neo-classical theory of employment {and henceoutput according to Keynes} to two taken for granted postulates:

1) The wage is equal to the marginal product of labour and;2) the utility of the wage when a given volume of labour is employed

is equal to the marginal disutiliry of that amount of employment (ibid., 5).The first one refers to the willingness of capital to invest in labour in

relation to the marginal efficiency of capital, while the second refers to thewillingness of labour to work in relation to wages offered. These postulates arebased on the assumption that wages are formed in bargaining betweenindividual entrepreneurs and labourers. It follows from these simplisticpresumptions that unemployment can only have two reasons, i.e. frictions inthe markets, the labour market included and the 'pricing out of labour' aslabourers claim to high wages. As a consequence the neo-classical theoryacknowledges only two kinds of unemployment, i.e. 'frictional' and 'voluntary'.Keynes claims that the third kind of unemployment, namely 'involuntaryunemployment' has to be taken into account and that the neo-classical theory

is incapable of analysing that kind of unemployment (ibtd., 6), Involuntaryemployment, according to Keynes, is a situation in which demand for labourdoes not increase although demand for the output of labour increases (ibid.,26) or in other words, the demand for labour is inelastic to demand for output.Or as Keynes puts his formal definition:

Men are involuntarily unemployed if, in the event of a small rise in the pricewage-goods relatively to money-wage, both the aggregate supply of labourwilling to work for the current money-wage and the aggregate demand for itat that wage would be greater than the existing volume of employment. (ibid.,15).

The question is then, what is it that prevents individual capital or firms fromemploying labour although demand is even increasing, as the neo-classicaltheory presumes? Keynes attempts to answer this question with his generaltheory of employment.

In Keynes theory, aggregate demand consists of total consumptionand total investment in a given community. On the other side aggregate supplyis determined by the expected aggregate supply price of the output fromemploying N men and the expected profits. Effective demand is the point ofintersection between the aggregate demand function and the aggregate supplyfunction and it is that point that determines the expected proceeds oraggregate income (factor cost plus profits) resulting from entrepreneursemplovrnent ofN men (ibid., p. 23-5). Obviously one of the main factors thataffect this point ofintersection iswages as wages determine both consumptionand expected proceeds (and hence investment, employment and output). Theprocess of wage formation is consequently one of the crucial factors thatdetermine effective demand.

Keynes theory is a rejection of the neo-classical theory (cf. Pigou)which presumes fluidity of money-wages and a self-adjusting character of theeconomic system and blames rigidity in wages for maladjustment in the system.Resting on these assumptions the neo-classical theory, or 'classical theory' asKeynes calls it, presumes that demand will be stimulated by simply reducingmoney-wages as it will diminish prices of finished products and will thereforeincrease output and employment until the level of reduced wages intersectswith the diminishing marginal efficiency oflabour as output is increased (Ibid.,257).

Keynes argues that this is an unrealistic picture of reality and that thisdoes not happen because of political and economic reasons that determineconfidence, expectations and the marginal efficiency of capital. Roughly wecan summarize Keynes's theory in this respect by saying that expectations and

90...91

the marginal efficiency of capital {and hence investment} is affected by wagereductions through, on the one side, the reactions of capital and on the otherthrough the reactions of labour.

In terms of the reactions of capital, reductions of money-wages willhave negative effects on investment as 1) reduced prices, which it leads to, willinvolve some redistribution of real income from wage-earners to other factorsentering into marginal prime cost whose remuneration has not been reducedand from entrepreneurs to rentiers to whom a certain fixed income in terms ofmoney has been guaranteed. Reduction in wages will diminish the propensityto consume of wage-earners and it will not increase insofar as rentiers are onthe whole the richer section of the community. Price reductions will alsoincrease the debt burden of entrepreneurs and may offset any cheerful reactionsfrom the wage reductions;2) if the reductions lead to the expectation or serious possibility of furtherwage-reductions, investment will diminish as the propensity to consume islikely to diminish even further. If the reduction is expected to be a reductionrelative to money-wages in the future, then investment will increase.

In terms of reactions of labour, the effects on investment may benegative as class struggle or "labour troubles" as Keynes cans it, may offsetfavorable conditions of capital accumulation because, as a rule, there are nomeans of securing a simultaneous and equal reduction of money-wages in allindustries, and therefore it is in the interest of all workers to resist a reductionin their own particular case. A popular discontent may furthermore cause adisturbance in political confidence which would lead to increase in liquidity-preference' which may offset the release of cash from the active circulation andwhich would lead to increase in the rate of interest and hence diminishingmarginal efficiency of capital.

In terms of effects of money-wage reductions on the economy as awhole, Keynes highlights that in an open system such actions, althoughfavorable to the balance of trade, will worsen the terms of trade and thus areduction in real income and hence the propensity to consume.

It is only in the cases when reductions in money-wages are relative tomoney-wages in the future, i.e. when increased future demand is expected, andwhen liquidity -preference is reduced, given that there are no "labour troubles",that Keynes presumes that these wage reductions may lead to increasedinvestment and hence employment (ibid., 262-5). Keynes does not, however,analyse this point in detail, as such a discussion would lead him out of hisnarrow, pragmatic quaesitum into analysis of the 'given factors' of his model,namely techno-structural determination of cost-structures of production. Wewill analyse and criticize his model in this respect below.

But his most important contribution concerning wage-reductions isprobably his comparison of reducing money-wages and increasing the quantityof money. Both actions lead to the same result but while the former may leadto "labour troubles" the latter will not, it may shatter confidence. As Keynesputs it:

... if the quantity of money is virtually fixed, it is evident that its quantity interms of wage-units can be indefinitely increased by a sufficient reduction inmoney-wages; and that its quantity in proportion to incomes generally canbe largely increased, the limit to this increase depending on the proportionof wage-cost to marginal prime cost and on the response of other elements ofmarginal prime cost to the falling wage-unit.

We can, therefore, theoretically at least, produce precisely thesame effects on the rate of interest by reducing wages, whilst leaving thequantity of money unchanged, that we can produce by increasing thequantity of money whilst leaving the level of wages unchanged. It follows thatwage reductions, as a method of securing fun employment, are also subject tothe same limitations as the method of increasing the quantity of money. Thesame reasons as those mentioned above, which limit the efficacy of increasesin the quantity of money as a means of increasing investment to the optimumfigure, apply mutatis mutandis to wage reductions. Just as a moderate increasein the quantity of money may exert an inadequate influence over the long-term rate of interest, whilst an immoderate increase may offset its otheradvantages by its disturbing effect on confidence; so a moderate reduction inmoney-wages may prove inadequate, whilst an immoderate reduction mightshatter confidence even if it were practicable.

There is, therefore, no ground for the belief that a flexible wagepolicy is capable of maintaining a state of continuous full ememployment; -any more than for the belief that an open-market monetary policy is capable,unaided, of achieving this result. The economic system cannot be made self-adjusting along these lines (ibid., 266-7).

As a consequence, in a real-political manner, Keynes advocatesflexible money policy rather than flexible wage policy. It prevents wasteful anddisastrous struggle on the labour market and, Keynes believes, stable money-wages win secure the greatest practicable fairness in the system as prices willmainly correspond to the diminishing marginal productivity of the existingtechnology as output is increased [i.e. apart from 'administered' or monopolyprices which are not purely determined by marginal cost). Furthermore,increased quantity of money decreases the burden of debt and finally flexiblewage policy is likely to diminish propensity to consume and therefore investmentand might thus postpone recovery (ibid., 267-9).

92...93

c) Keynes's critique of the neo-closslcol theory of interestsKeynes rejects the traditional, neo-classical view of interests that on the oneside reduces the role of money to two functions only, i.e. as a mere medium intransactions in current business and as a store of wealth, and on the other sidepresumes that the rate of interest depends on the interaction of the scheduleof the marginal efficiency of capital with the psychological propensity to save.

Unlike this view, Keynes theory of money and interest presumes anindependent role ofinterest in the relationship between the quantity of moneyand the marginal efficiency of capital. He argues that it is impossible, astraditional theory does, to deduce the rate of interest from on the one side theschedule of marginal efficiency of capital and on the other side the psychologicalpropensity to save. So, while the schedule of the marginal efficiency of capitalgoverns the terms on which loanable funds are demanded for new investmentand the rate of interest governs the supply offunds, what needs to be explainedis what governs the rate of interest (Ibid., 165).

The answer to this question is what Keynes considered to be thenovelty of the General Theory. He claimed that:

1) Individuals decide how much they are going to save or invest inrelation to how much of their given income they are going to spend onconsumption. Their 'liqidity preference', i.e. how much of their income theywant to keep in the form of cash, is in the first instance determined by their'propensity to consume'.

2) Having decided how much they will spend on consumption theywill have to decide in what form they will keep the rest. Their decision will beaffected by three motives; a) the transaction-motive, i.e. the amount of cashneeded for current transactions of personal and business exchange; b) theprecautionary-motive, i.e, the desire for security as to the future cash equivalentofa certain proportion of total resources; and c) the speculative motive, i.e. theobject of earning profit from knowing better than the market what the futurewill bring forth (the first to motives of liquidity preference are presumed to benot very sensitive to changes in the rate of interest, but the speculative motiveis sensitive to such changesjtibid., 169-70);

3) Now the quantity of money enters the theory as the amount ofmoney available for hoarding and the amount available for yielding throughlending or buying assets which is determined, Keynes claims, by, on the oneside the quantity of money in the economy and on the other side the amountrequired for transactions of current businesses. Furthermore, the amount ofmoney available for hoarding and/or yielding determine the rate of interest andprospective yields on assets {which in equilibrium are equally desirablealternatives for the marginal investor}:

4) As the rate of interest and opinions of the prospective yields ofassets fluctuate, the prices of assets consequently fluctuate; and

5) Finally, if opinions of prospective yields are positive and the pricesof assets increase, investment in assets will increase, or the other way around,if the schedule of the marginal efficiency of capital is thought to be uncertainor low the propensi ty to hoard money will increase (and ifpeople hoard moneyrather than buy assets, interests will have to increase which further lowers theschedule of the marginal efficiency of capital, which counter-affects theincreases in interest, but only at the later stages in the process);

6) As a consequence Keynes concludes that investment depends ona) the propensity to hoard and b) opinions of future yields on capital assets[ibid., 116-17).

In so far as Keynes has captured the framework within which interestsare determined in the short run, he does not adequately deal with the

. relationship between the determination of short run and long run interests,although he emphasizes the importance of the long run.

If we hold wages, the quantity of money and the propensity to

the initial novelty lies in my maintaining that it is not the rate of interest, butthe level of incomes which ensures equality between saving and investment.The arguments which lead up to this initial conclusion are independent ofmy subsequent theory of the rate of interest, and in fact I reached it before Ihad reached the latter theory. But the result of it was to leave the rate ofinterest in the air. If the rate of interest is not determined by saving andinvestment in the same way in which price is determined by supply anddemand, how is it determined? '" It was only when (attempts in otherdirections failed) ... that! hit on what! now think to be true explanation. (InEconomic Joumal193 7, quoted in Garegnani, 50).

According to Keynes, interests are to be defined as "the 'price' whichequilibrates the desire to hold wealth in the form of cash with the availablequantity of cash" (]. M. Keynes, 1983, 167). This idea is fundamental to histheory of interests as this desire to hold wealth in the form of cash, or 'liquiditypreference', rests on the interaction between the level of income (which hasan overdetermining role d. the quotation above) and the propensity toconsume." His theory of interest has to be analysed on the one side in termsof the short term economic context and on the other in terms of the long run.It is in this context that the weaknesses of his theory of interests become dear,as he did only develop a short term theory and his long term theory "leaves therate of interest in the air".

Keynes's short term theory of interests can be summarized as follows:

94..95

consume constant, we can isolate those two factors that Keynes considersfundamental in determining investment, i.e.Iiqidity preference and expectedmarginal efficiency of capital. The latter determines how much investors areprepared to pay for interests of their turnover, while the former determines therate of interest at which suppliers of funds are willing to provide loans. Thesupplier of funds chooses between, on the one hand, to invest in assetsaccording to expected marginal efficiency of the investment, and on the otherhand, to lend his or her wealth on current rate of interests or wait if the currentrate of interest is lower than the expected 'natural' rates of interests in thefuture, or if it is lower than rates of interest of long term loans (it is possible thata supplier of funds prefers to lend on lower current interests than the higherexisting rates of long term loans if he/she expects that the marginal efficiencyof capital or assets will be higher in the future). By 'natural' rate of interestKeynes does not mean the neo-classical idea of a rate of interest at funemployment, as Keynes presumes that the rate of interest is different fordifferent equilibriums ofdifferent levels of employment. It refers to conventionalrates of interest depending on the aggregate status of the economy (ibid., 242-4).

In the above mentioned situation, ideas concerning 'natural' rate ofinterest are crucial concerning supply offunds. Keynes does not provide us withany theory of the relationship between short term and long term rates ofinterests [i.e. expected 'natural' rates in the future). He is content withreferring to his obscure concept of "confidence" and says:

Th,e relation between Lj and Y is relatively constant in Keynes'smodel, but the same does not go for the relations between L, and r, Because ofuncertainty concerning future development of the rate of int~rests one can notassume a constant relation between M] and r; Lz fluctuates:

... what matters is not the absolute level of r but the degree of its divergencefrom what is considered a fairly safe level of r, having regard to thosecalculations of probability which are being relied on. (ibid., 201).

The rate of interest, consequently, is thought to be determined byconvention, but not supply and demand of investment funds, as orthodoxtheories would have it:

It might be more accurate, perhaps to say that the rate of interest is a highlyconventional, rather than a highly psychological, phenomenon. For itsactual value is largely governed by the prevailing view as to what its value isexpected to be. Any level of interest which is accepted with sufficientconviction as likely to be durable wi!! be durable; subject of course, in achanging society to fluctuations for all kinds of reasons round the expectednormal. (ibid., 203)

M=Ml +M2=L1(Y) +L2(r)

The rate of interest as an independent variable because of thesereasons, is the reason why fun employment equilibrium is not a necessaryoutcome of the market forces according to Keynes. Following this conclusionhe advocates interest rate policy that is a logical result of his theory of the rateof interest. The aim of governments should be twofold, i.e. on the one side theyshould determine the rate of interest so that the general public will haveconfidence in its stability (ibid., 203). On the other side the aim should be tokeep the rate ofinterest near the 'neutral' level offull employment equilibrium,because lower rates will create a situation of true inflation where MJ requiresincreasingly more quantity of liquid cash.

To sum up his theory of interests, we can briefly say that Keynes'scritique of the orthodox theory of interest is twofold:

1) On the one side he claims that it is inaccurate. As was highlightedabove, the level of real income differentiates depending on the level ofrealization of the output capacity of the economy in question and therefore thesupply of saving differentiates. If the schedule of the marginal efficiency ofcapital is given, possible rates of interest, in which investment and saving isinequilibrium, are therefore many and;

2) On the other side Keynes's critique consists of his hypothesis thatinterests are not the price of saving, but the necessary price to get individuals

Just as we found that the marginal efficiency of capital is fixed, not by the'best' opinion, but by the market valuation as determined by mass psychology,so also expectations as to the future of the rate of interest as fixed by masspsychology have their reactions on liquidity-preference. (ibid., 170).

As he goes to analyse the relationship between rates of interest andspeculation, we find also here that the solution is "left in the air". Hedistinguishes between two kinds of liquidity preference, LJ and L2, where LJ

refers to liquidity-preference because of the transaction and precautionarymotives, while L2 refers to liquidity-preference due to the speculation motive.He also distinguishes the quantity of money in the economy (M ) into thequantity that L

Jrequires (M1 ) and the quantity that L2 requires (M2)· LJ is

determines by the income (Y) of individuals and firms, while L2 is determinedby the rate of interest (r ), so that:

d) A critique of Keynes's critique of neo-classical theoryKeynes's point of departure and 'territory of analysis' is the macro economicproblem of equilibrium between supply and demand and this problem reflectsthe obvious paradox of the capitalist system in economic crisis, i.e. vacantimmense capacity to produce over-against low levels of demand andemployment. In his attack on orthodox economic theory, he criticized itstheories of economic equilibrium and claimed that these theories are onlyvalid for one special kind of equilibrium, i.e, equilibrium characterized by fullemployment under the conditions of prefect competition on flex-price markets.His own contribution was supposed to be a general theory of equilibriumformation not just under the conditions of neo-classical flex-price markets

The main characteristic of the dynamics of Keynes's economic modelis that it concentrates on the 'subjective' side of the short term dynamics ofexpectations and motives of entrepreneurs to invest (see figures 4.1 and 4.2).As a consequence the' objective' side isneglected, i.e. the structural developmentof capital accumulation; uneven long term development between sectors ofthe economy, regions and countries; the dynamics of monopoly andmultinational capital and the structural development of competition on

inte~nationaI markets; and technological determination of the developmentof profitability are external, 'given' factors in hilsmodel,

His emphasis on the subjective side is understandable in the contextof the economic crisis of the 19305 in which lack of investment on behalf ofentrepreneurs and/or companies was permanent. But the shortcomings ofKeynes is that he does neither adequately analyse the long term objectivedetermination of short term business behaviournor the short term historicaldetermination of long term economic development.

The main theme of Keynes's theories is to show that fun employmentis not only ideologically desirable, but necessary and logical in terms of thelogic of the capitalist system itself. It was indeed one of the striking novelty ofhis doctrine to show that {abstracting from effects on foreign trade} an all-round reduction in wages would not reduce unemployment and would actuallybe likely to increase it O. Robinson, 131), i.e. that reduction in all-round wageswould lead to reduction in aggregate demand which would lead to reductionin incentives to invest which would lead to increase in unemployment etc. Asa consequence, by increasing aggregate demand, Keynes believed it possible toapproach "fun employment". But the gap between to low level of aggregatedemand and full employment is wide and Keynes attempted to build thetheoretical construction, a model, that would do to bridge that gap.

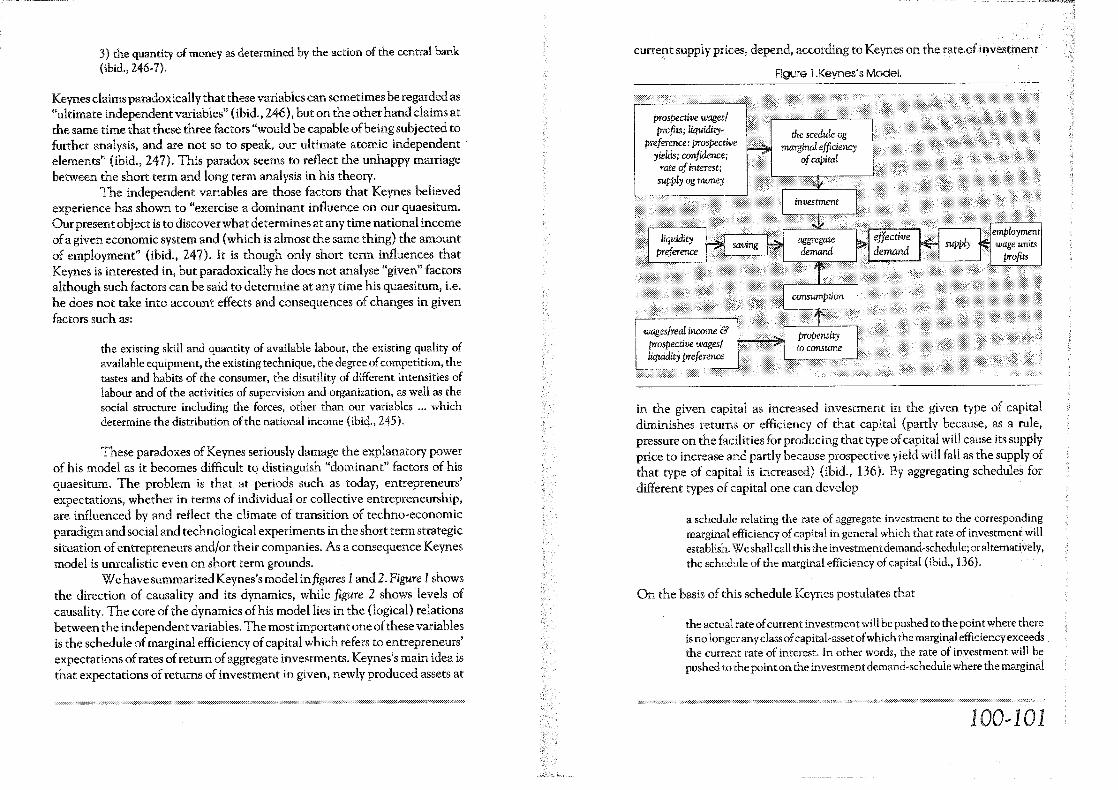

Keynes's model is based on relatively few interrelated variables themain of which are: the propensity to consume and the multiplier; theinducement to invest and the marginal efficiency of capital, long termexpectations and incentives to liquidity; and finally the employment function.He abstracts carefully his variables from technological and societal factors andtheir development and defines a matrix of independent and dependentvariables that particularly suit short term analysis.

According to his summary of his model in General Theory he definesas independent variables "in the first instance, the propensity to consume, theschedule of the marginal efficiency of capital and the rate of interest ..." Hisdependent variables "are the volume of employment and national income (ornational dividend) measured in wage units" (Ibid., 245).

But interestingly enough, there is more to Keynes's causality. Histheory is based on a notion of overdetermination in which the independentvariables are determined by:

to keep their wealth in other form than cash. Keynes claimed that demand formoney depends on the quantity of money in the economy (decided by themonetary authorities), the quantity of money needed for transactions in theeconomy and the rate of interest. Keynes's theory presumes that it is not supplyand demand that determine the rate of interest, but the rate of interest affectsthe demand and that it depends on ideas of 'conventional' rate of futureinterests and the confidence in the monetary policy of the authorities.

This theory is very inadequate as it does not explain the long termdetermination of interests and the formation of expectations of long terminterests. This is indeed a problematic that his narrow pragmatic, short termproblematic does not allow. "fie will therefore have to go into the domain ofthe 'given factors', namely technological development and its relation to thedevelopment of expected marginal efficiency of capital. As P. Garegnani haspointed at, as Keynes leaves the theory of interests in the air, his theory wasbound to lead either to a conversion to the neo-classical theory or a moreradical rejection of it than Keynes developed himself (P. Garegnani, 54). Wewould argue that it is the qualitative nature of technical change that determinesthe schedule of marginal efficiency of capital and through it ideas of 'natural'future interest rates as it is the establishment of stable regimes of capitalaccumulation and techno-economic paradigms that are the preconditions oflong term speculation.

1) the three fundamental psychological factors, namely, the psychologicalpropensity to consume, the psychological attitude to liquidity and thepsychologicalexpectation offuture yieldfromcapital assets,2) the wage-unitasdetermined bythe bargainsreached between employersand employed,and

98...99

3) the quantity of money as determined by the action of the central bank(ibid., 246-7).

current supply prices, depend, according to Keynes on the rate of investment

Figure 1.Keynes's Model.

Keynes claims paradoxically that these variables can sometimes be regarded as"ultimate independent variables" [ibid., 246), but on the other hand claims atthe same time that these three factors "would be capable of being subjected tofurther analysis, and are not so to speak, our ultimate atomic independentelements" (Ibid., 247). This paradox seems to reflect the unhappy marriagebetween the short term and long term analysis in his theory.

The independent variables are those factors that Keynes believedexperience has shown to "exercise a dominant influence on our quaesitum.Our present object is to discover what determines at any time national incomeof a given economic system and (which is almost the same thing) the amountof employment" (ibid., 247). It is though only short term influences thatKeynes is interested in, but paradoxically he does not analyse "given" factorsalthough such factors can be said to determine at any time his quaesitum, i.e,he does not take into account effects and consequences of changes in givenfactors such as:

prospective wages!profits; liquidity·

preference: prospectiveyields; confidence;

rate of interest;supply og money

the existing skill and quantity of available labour, the existing quality ofavailable equipment, the existing technique, the degree ofcompetition, thetastes and habits of the consumer, the disutility of different intensities oflabour and of the activities of supervision and organization, as well as thesocial structure including the forces, other than our variables ... whichdetermine the distribution of the national income (ibid., 245).

wages/real income &prospective wages!liquidity preference

These paradoxes of Keynes seriously damage the explanatory powerof his model as it becomes difficult to distinguish "dominant" factors of hisquaesitum. The problem is that at periods such as today, entrepreneurs'expectations, whether in terms of individual or collective entrepreneurship,are influenced by and reflect the climate of transition of techno-economicparadigm and social and technological experiments in the short term strategicsituation of entrepreneurs and/or their companies. As a consequence Keynesmodel is unrealistic even on short term grounds.

We have summarized Keynes's model in figures 1and 2. Figure 1showsthe direction of causality and its dynamics, while figure 2 shows levels ofcausality. The core of the dynamics of his model lies in the (logical) relationsbetween the independent variables. The most important one of these variablesis the schedule of marginal efficiency of capital which refers to entrepreneurs'expectations of rates of return of aggregate investments. Keynes's main idea isthat expectations of returns of investment in given, newly produced assets at

in the given capital as increased investment in the given type of capitaldiminishes returns or efficiency of that capital (partly because, as a rule,pressure on the facilities for producing that type of capital will cause its supplyprice to increase and partly because prospective yield will fall as the supply ofthat type of capital is increased) (ibid., 136). By aggregating schedules fordifferent types of capital one can develop

a schedule relating the rate of aggregate investment to the correspondingmarginal efficiency of capital in general which that rate of investment willestablish.We shallcan this the investment demand-schedule;oralternatively,the schedule of the marginal efficiency of capital (ibid., 136).

On the basis of this schedule Keynes postulates that

the actual rate ofcurrent investment willbe pushed to the point where thereisno longer anyclassofcapital-asset ofwhich the marginalefficiencyexceedsthe current rate of interest. In other words, the rate of investment will bepushed to [he painton the investment demand-schedule where the marginal

100., 101

Figure 2. Causal Factors in Keynes's Model.

forces of quantity & qual- the psvchologi-production/ ity of labour & cal: propensityorganic equipment & to consume; propensity tocomposition technique & attitude towards comsurneof capital intesity of liquidity;

labour expectations of volume offuture yields employment

structure/ degree of wage-units the schedulerelations of competition determined in the marginal nationaldiffernet bargains efficiency incomecapitals of capital

structure of tastes &reproduction habits of theof labour of the consumer

quantity ofmoney determinedby the centralbank

the rate ofinterest

classstruggle andbalance ofpower ofsocial andpoliticalforces

degree oflabour troubles

But, interestingly enough, Keynes emphasises that it is first andforemost the prospective yield of capital that is important for investment andnot merely the current. yield as it is the prospective yield that determinesexpectations. What is important for our discussion here is that he distinguishesbetween three main factors that influence prospective yields, i.e, changes inprospective cost of production referring to changes in labour cost, inventionsand new technique and expectations of a fan in the value of money (ibid., 141).It is interesting indeed that Keynes paradoxically introduces expectations ofchanges in labour costs and technique as determining factors of prospectiveyield as he carefully defines these factors as "given" factors in his model.

Having in mind these striking paradoxes in Keynes's problematic, itseems reasonable to criticize his problematic with reference on the one side toshort term analysis of capital accumulation and on the other side to long term

analysis. The main shortcoming of his theory can be summarized as beingincapable of analysing how long term factors have a crucial influence on shortterm uncertainty in markets at different times.

e) Keynes and the short termThe shortcomings of his short term analysis is best seen through the strategicsituation of the entrepreneur or company. His/her or their situation is threefold,i.e. 1) he/she or they have to work on micro short term strategy; 2) short termstructural factors and; 3) macro economic context and long term structuraldevelopmental trends.

Besides dealing with the factors in Keynes's model that determine theschedule of the marginal efficiency of capital in the short run, and the turnoverand flow quantities on day-to-day, month or year basis and reproducingrelations with customers and suppliers, demand etc. - he/she or they have todeal with renewing depreciated capital stock and fixed capital. It is here thatstrategic decisions concerning technological innovation come into question.The entrepreneur or company has to choose between renewing old stocks,working on incremental innovations or, at times when technical change israpid and fundamental, investing in new technology. At this point he/she orthey have to consider long term prospects of the technology, such as, is thistechnology based on standards that will be the rule in the future or are thereany signs that it will be obsolete in the near future! Furthermore, they will haveto consider and decide on levels of risk in their in vestment. It is indeed at thispoint that the company's risk taking ability may result in technological muddle(d. e.g, J. Hirsch) and it is at this pointthat Keynes's distinction between shortterm variables and "given" factors proves to be nonsense.

Here they will also have to take into account structural aspects, suchas 'social' risks of investment determined by the nature of the industrialrelations, chances of strikes, retraining possibilities etc. They will also have totake into account chances ofinvesting elsewhere or abroad, taking part in jointventures and takeovers on the stock market. They will also have to take intoaccount the degree of stability of political regimes. Keynes does not addressthese problems of strategic decision making, which though determine theframework within which short term decisions are taken.

Although Keynes did develop a consistent model of aggregate demandand the inducement to invest on the basis of his short term problematic, hisdistinction between the short term and given factors is seriously fallacious interms of the strategic situation of the investor. He fails in this respect as he doesnot take into account aspects that are of important qualitative nature, i.e.factors that are crucial for the strategic situation in certain periods. The factors

102;103

we have in mind are:a) the system of industrial relations tends to brake down at the end of boomsand the consequence is that it becomes more difficult for investors to forecastthe development or state of the rate of exploitation and policies of governments.It is easier for labour, capital and governments to forecast and form long-termexpectations in periods of steady growth as the "rules of the game" are betterknown. Keynes does not understand the importance of this historical factor ascan be seen from the fact that class struggle or "labour troubles" as he calls it,is treated as an dependent variable determined by the flexibility of wagepolicies; b) as the rates of profits of ruling technological systems have beenincreasingly competed away as booms change into crises, the search for best-practice-technolgy becomes more difficult and investment more risky (see e.g.]. Hirsch), especially as the development of capitalism has led to ever morecapital-intensive technology and higher organic composition of capital. It maytake many years before new technological systems spread and meanwhile risksin long-term investment are high (depending on countries and cultures, factora may exaggerate the role of b) as is discussed in Ivar Jonsson 1991 on'conjunctural uneven development'); c) the level of internationalization offinancial capital complicates further the strategic situation of the investor, asit has become easier to speculate on international markets in the present eraof deregulation, speculation rather than 'enterprise' (in the keynesian sense)becomes more reasonable in the crisis. The lack of incentives to invest in'enterprise' has to be analysed in historical and structural way by analysingshifts of techno-economic paradigms, and not as a question of waves ofoptimism and/or pessimism or in the mystical terms of the 'animal spirit ofcapitalism' as Keynes is satisfied to do and we will discuss below as we criticizehis theory of trade cycles.

1)Keynes and the long termAs we tum to long term analysis of capital accumulation Keynes's theory is tobe criticized for the following:

a) it is a serious fallacy in Keynes's theory of employment that he doesnot take into account qualitative differences in technical change. The phaseof automatization based on information technology that we are experiencingtoday, releases labour from production to much greater extent and much morerapidly than we have experienced in previous technological revolutions in thehistory of capitalism. As a consequence increased aggregate demand does notincrease national income to the same extent as before unless global division oflabour allows technological frontier countries to use the technology gap tocreate more employment in their, and only their, own countries and/or new

markets are produced; the relationship between investment and employmentis not a~ simple as Keynes's model presumes;

b) if investment and expectations are to be steady then markets andpatterns of consumption and industrial relations (both in terms of distributionofremuneration and technological innovations) have to be already established.These factors are given in Keynes's model and he does not present any theoryof the dynamics of the production of markets and social relations. The reasonishis reified theory of science, according to which such analysis belong to othersciences than economics;

c) the long term development of capital accumulation and the growthof multinational corporations and international trade (Y. Droucopoulos andP. Teague) has come to a stage where the "national" role and power of thecapitalist state has been greatly diminished. As a consequence, out of lack ofanalysis of these matters in Keynes's theory, his assumption of steady growthbased on status quo in patterns of distribution of total remuneration in theeconomy turns out to be seriously defective. Furthermore his liberalist ideologyprevents that he realizes that the state is not an abstract, neutral agent incapitalist society, but is a battlefield of national and multinationals' antagonistinterests and therefore not capable of realizing a permanent pattern of suchdistribution of renurneration (one has to keep in mind that Keynes was anactive member of the British Liberal Party most of his life. We will discuss hisnaivety concerning the state as we discuss his theory of trade cycles below);d) Keynes liberalist view of the capitalist state and reified view of scienceprevents him in his theory from seeing the importance of working on activeformation of state structures of class collaboration and tripartite nee-corporatismfor capital accumulation. As can be seen from the W -German experience (d.H. Mattfeldt), in Late-Capitalism, tripartite structures have been moreimportant than keynesian policies in economic policy making as such politicalstructures of redistribution existed long before keynesian policies whereseriously implemented in the BRD. The same goes for the post-war frencheconomic history as R. Boyer has argued (R. Boyer 1985) and scandinaviancountries Sweden and especially Norway (where nee-corporatist structures ofredistribution where established already in 1930 (D.S. Schwerin). As aConsequence, the post-war boom in these countries has to be explained byother means than anti-cyclical keynesian policies, although Keynesian policiesdid diminish trade cycle effects in the boom era where they were realized. Thefactors that determined the class collaboration and neo-corporatist scenario inEurope after W orld War 2, has to be explained by the experience of the war-economy, the struggle against fascism and nazism, the fascist and nazi persecutionand weakening of the communist movement outside and inside the labour

................................. ;.:.;.:.:.~;.:.;.: ...•......... :.:.;.:.:.;.:.:.:.:.:.;.;.:.:.;.:.:.:.:.:~.:.:.:.;.;.:........... . ...•.•.•.•.• ;.;.:-:.;.;.<:.;.;-:.:.:.;.:.; ••.•.•••........ ,'

104--105

movement, that altogether strengthened the power position of the social-democratic movement after the war. Stalin's class collaborationist strategy andcontrol of the european communist movements after the war is also importantin this scenario, and finally the renewal of the technological base of thesecountries in the post-war era (see e.g. L. Panitch 1979 and 1981 and I. [onsson1984). These neo-corporatist structures have survived despite the monetaristpolicy attempts in the present crisis of capitalism;

e) it is only a problematic of capital accumulation that considers thesocio-historical nature and development of the process of capital accumulationwhich presumes ever increasing internationalization and socialization of thisprocess, and theories of the necessity of increasing rate of accumulation (cf. H.Grossmann) that are capable of analysing capital accumulation and supersedingKeynes's dichotomy of short term as opposed to long term analysis;

f) it seems that all the basic shortcoming of Keynes's theory is, on theone side, concentrated in his theory of trade cycles and crises - i.e. his naivenotion of the capitalist state, his marginalist notion of technology and shortterm vis-a-vis long term dichotomy and the mystical dualism of his idea ofhuman nature, on the other side, the objective situation of the investor on theother - as he "explains" the upper turning point when trade cycles change intocrises.

Fundamentally, trade cycles are to be explained by fluctuations in themarginal efficiency of capital. according to Keynes, and he takes it that suchfluctuations are complicated and often aggravated by associated changes in theother significant short-period variables of the economic system. A trade-cycleischaracterized by three main elements, i.e. a cyclical movement ischaracterizedby upward and downward tendencies and secondly by a recognizable degree ofregularity in the time-sequence and duration of the upward and downwardmovements and finally cycles are characterized by the phenomenon of crisis,i.e.:

of capital which depends on the existing abundance or scarcity of oapitalgocdsand the current cost of production of capital goods, and furthermore, on thecurrent expectations of the future yield of capital goods. But expectations aresubject to sudden and violent changes and these changes cause crises. Keynesis especially interested in what happens at the upper turning-point from aboom to a crisis.

Keynes argues that the crises should not be explained as usual, as hesays, by the rising rate of interest influenced by the increased demand formoney in the boom for trade and speculative motives, but instead he suggests:"a more typical, and often the predominant explanation ... not primarily a risein the rate of interest, but a sudden collapse in the marginal efficiency ofcapital" (ibtd., 314), i.e. a collapse in the schedule (i.e. expectations) of themarginal efficiency ofcapital, Keynes explanation assumes unrealistic optimismand speculation in the later stages of the boom and panic in investmentmarkets as the causes of the crises. As he puts it (note that he is talking aboutthe schedule of the marginal efficiency of capital when writes "the marginalefficiency of capital", cf. ibid., 315):

the fact that the substitution of a downward for an upward tendency oftentakes suddenly and violently, whereas there is, as a rule, no such sharpturning-point when an upward is substituted for a downward tendency (]. M.Keynes 1983,314).

The later stages of the boom are characterized by optimistic expectations asto the future yield of capital-goods sufficiently strong to offset their growingabundance and their rising costs of production and, probably, a rise in the rateof interest also. It is the nature of organised investment markets, under theinfluence of purchasers largely ignorant of what they are buying and ofspeculators who are more concerned with fore-casting the next shift ofmarket sentiment than with a reasonable estimate of the future yield ofcapital-assets, then, when disillusion falls upon an over-optimistic and over-bought market, it should fan with sudden and even catastrophic force.Moreover, the dismay and uncertainty as to the future which accompanies acollapse in the marginal efficiency of capital naturally precipitates a sharpincrease in liquidity-preference - and hence a rise in the rate of interest. Thusthe fact that a collapse in the marginal efficiency of capital tends. to beassociated with a rise in the rate of interest may seriously aggravate thedecline in investment. But the essence of the situation is to befound nevertheless,in the collapse in the marginal efficiency of capital, particularly in the case of thOsetypes of capital which have been contributing most to the previous phase of heavynew investment. Liquidity-preference, except those manifestations ofitwhichare associated with increasing trade and speculation, does not increase untilafter the collapse in the marginal efficiency of capital.

It is this, indeed, which renders the slump so intractable. Later on,a decline in the rate of interest will be a great aid to recovery and, probably,a necessary condition of it. But for the moment, the collapse in the marginalefficiency of capital may be so complete that no practicable reduction in the

He explains the time-element or the fact that cycles last regularlybetween three and five years, on the one side by the length of life of durableassets in relation to the normal rate of growth in a given epoch, and on theother by the carrying-costs of surplus stocks. Or in other words, the mismatchbetween the level of growth in the given epoch and the degree of abundanceof capital goods. Investment depends on the schedule of the marginal efficiency

rate of interest will be enough ... It is the return of confidence, to speak inindividualistic capitalism (ibld., 315-17. underlines: 1.J.).

tendencies. Keynes's main idea is that slumps caninvestment is prevented, so the crucial question is,defined? He defines it as:

So it is unrealistic optimism vis-a-vis a collapse in the marginalefficiency of capital that is supposed to explain the upper turning-point. Butgiven the history of capitalism and the fact that economic crises are differentin terms of duration and rhythm (d.Kondratieff waves compared with businesscycles), one has to answer these fundamental questions: Why is optimismrelatively more unrealistic in some periods? How is the different duration of thecrises to be explained? Why is it more difficult to establish confidence in someperiods relative to others?

Incapable of analysing qualitative technological change and periodsof technological transition from one regime of accumulation to another as animportant part of explaining the upper turning-point, Keynes has no answerto these questions. One can only refer to his dualist and mystical idea of the'animal spirit' in search of an answer in the General Theory where he says:

a state of affairs where every kind of capital-goods is so ab\Indarit tnat.tnere

to earn in the course of its life more than its replacementinvestment would be a sheer waste of resources. Moreover,

would not lie in clapping on a high rate of interest whichdeter some useful investments and might further diminish the pr<)pensiitytoconsume, but in taking drastic steps, by redistributing incomes or otherwise,to stimulate the propensity to consume (Ibid., 320-20.

Once again Keynes presents the idea that steady growth is possible ifthe prices of the factors of production are held constant relative to each otherand in balance with effective demand. But this conclusion seems to be veryunrealistic to us as it presumes static equilibrium and negates some fundamentalcharacteristics of capital accumulation, namely the fact that there is no suchindependent institution in capitalist society that is capablewealth in a "neutral" way and per definition to secure full employmentstate is not an abstract independent institution in such societies,battlefield of objective, antagonistic interests and social and politicaland cast in the process of 'hegemonic politics' (see {val' Jonsson

Even apart from the instability due to speculation, there is the instability dueto the characteristic of human nature that a large proportion of our positiveactivities depend on spontaneous optimism rather than on a mathematicalexpectation ... But individual initiative will only be adequate when reasonablecalculation is supplemented and supported by animal spirits ... This means,unfortunately, not only that slumps and depressions are exaggerated indegree, but that economic prosperity is excessively dependent on a politicaland social atmosphere which is congenial to the average business man ... Inestimating the prospects of investment, we must have regard, therefore, tothe nerves and hysteria and even the digestions and reactions to the weatherof those upon whose spontaneous activity it largely depends ... We should notconclude from this that everything depends on waves ofirrational psychology.On the contrary, the state oflong-term expectation is often steady, and, evenwhen it is not, the other factors exert their compensating effects (ibid., 161-2).

historically and institutionally determined process that disturbs,eq\ii.libraltitl~tendencies and can not simply be dealt with in the framework ofmatgirialli.$t,keynesian reduction of technology to the problem of 'pr'Oduct:ioIl-fllI'!.<:tic)fis'with itsnotion of malleability of'factors of production'B.-A. Lundvall 1988 and }, A. Schumpeter 1981, partcapitalism is the competition between different capitalspresumes uneven development in which technological deve],oprnf:ntcrucial part. The structural aspects of uneven ~SI~~Ci:lllVimportant when the particular problems of small economiesis argued in lvar Jonsson 1991, especially the analysis Of'C01:ljunC!turahln~:y!!ndevelopment'). Keynes's approach is quite hollow in

Leaving aside the technological dimension and the role of industrialrelations, it is true that Keynes, because of his pragmatic problematic, isespecially interested in the interest rate part of the schedule of the marginalefficiency of capital. But even here his theory of trade cycles is unrealistconcerning the chances of preventing booms to tum into crises.

It is over-investment, according to Keynes, which leads to thediminishing schedule of the marginal efficiency of capital, which is the basicsource of slumps in his theory of crises and the remedy against crisis is nothigher rate of interest as such development would only aggravate the crisis-

and the process of Inrernaionalization of capital accumulatiott COl[l1p,lieatefurther the strategic context of the investor, be it fimlncialorin(i!1s:tI.'ian:ap,ital,and hence the qualitative differences in the tormationKeynes's analysis of uncertainty in the process of

therefore not adequate at the same time as his short term analysis are to narrowand methodologically inadequate even in terms of his own field of analysiswhich is supposed to concentrate especially on the causality of short termeconomic development.

is,,consiciered to be in equilibrium when all markets are characterized by sets ofmarket-dearing prices, with associated commodities and 'factors ofproduction' .

As it is presumed that all markets dear in equilibrium, it goes that itis presumed that equilibrium prices and equilibrium quantities are determinedsimultaneously; the theory of value is one and the same thing as the theory ofoutput. Having defined equilibrium in this rationalist way as a pure thoughtcreation, an 'ideal type', orthodox theory deduces aUdeviations from equilibriumas disturbances of market-dearing, as 'frictions' or 'rigidities' .To mention butfew of such disturbances out oflegion in the orthodox literature, J. Eatwell andM. Mulgate have highlighted the most usual ones:

g) Extending Keynes's problematic - the critique put into abroader theoretical perspective

We have highlighted Keynes's critique of neo-classical theory which basicallyconcentrates on the concept of equilibrium and the idea that the rate interestcan not have the equilibrating function that neo-classical theory presumes. Asa consequence the neo-classical theory is incapable of analysing the realconditions and formation offull employment in contemporary capitalism. We

, have highlighted thatthe role of technological development as an independentvariable is missing in Keynes's theory and that it does not deal with thequalitative changes in technology. These shortcomings both undermine hisidea of a direct, linear relationship between employment and investment onthe macro level and his theory of the strategic situation of the investor on themicro level, as he does not deal seriously with the problem of technologicaldevelopment. We have also highlighted his naive view of the capitalist stateand lack of analysis of monopoly and multinationals as well as the growth ofinternational trade which seriously undermines keynesian policies," We willnow develop this critique further.

In short we can summarize much of economic debate as the disputewhether full employment and optimum output will be created by the mediatingrole of price formation in markets, so that relative changes in values will betransformed by the market mechanisms of price formation, into optimumoutput and full employment (in the sense that at the going wages all workerswilling to offer labour would be able to find employment). To tackle thisproblem one needs both a theory of value and a theory of price formation aswell as a theory of the relationship between these and employment and output.

Neo-classicists attempt to solve the problem by basing their theoryon a threefold ground, i.e.: on a subjectivist theory of prices that rejects theRicardian and Marxian labour theory of value; the rnarginalist theory off actorsand functions of production and; its theory of equilibrium. In the mostelementary orthodox neo-classical economics the dynamics of economic lifeis reduced to the relationship between supply and demand (see J. Eatwell/M.Milgare, 1-17). According to this reduction, 'equilibrium' is determined at thepoint of intersection of a function relating price to quantity demanded andanother relating price to quantity supplied, i.e. what is caned 'market clearing'.This idea of market dearing is generalized to the economy as a whole which

'sticky' prices (particularly 'sticky' or even rigidly fixed wages and/or 'sticky'interest rates):

institutional barriers to the efficacy of the price mechanism, such as monopolypricing (by firms or individual groups of workers);

inefficiencies introduced into the working of the 'real' economy by theoperations of the monetary system;

the failure of individual agents to respond appropriately to price signalsbecause ofdisbelief in those signals, the disbeliefbeing derived from uncertaintyabout the current or future state of the market, or from incorrect expectationsconcerning future movements in relative prices, or from false 'conjectures'about the actual state of the market.

Indeed, examples of 'frictions' and rigidities' can be multiplied at will- anyfactor which causes the market to work imperfectly will do. It will beconvenient, therefore, to group all the authors of the myriad of arguments ofthis kind together under the general heading of''imperfecnonists'. (Ibid., 3).

It is a common idea of such 'imperfectionist' authors that if theparticular factors causing frictions or rigidities would not exist, then supply anddemand would create the neo-classical equilibrium (ibtd., 3).

Opposed to this neo-classical thinking are theories that reject theidea that full employment equilibrium will be created by market dearingprices. Keynes rejected it on the bases of his theory of the dynamics ofexpectations and the independent role of the rate of interest. J. A. Schumpetercriticized it as it is not valid in terms of the economic history of capitalism:"it is quite clear that perfect competition has at no time been more of a realitythan it is at present". J.A. Schumpeter, 81). For Schumpeter, even the shortterm, neo-classical idea of fun employment equilibrium is somewhat misleading,as he puts it:

11O~111

A system - any system, economic or other - that at every given point of timefully utilizes its possibilities to the best advantage may yet in the long run beinferior to a system that does so at no given point of time, because the latter'sfailure to do so may be a condition for the level or speed of long-runperformance. (tbid., 83).

It is indeed the nature of the organic process of capital accumulation, 'theprocess of creative destruction' to find new ways of production to create extraprofits. As a consequence the neo-classical reduction of competition to pricecompetition is also misleading:

The first thing to go is the traditional conception of the modus operandi ofcompetition. Economists are at long last emerging from the stage in whichprice competition was all they saw. As soon as quality competition and saleseffort are admitted into the sacred precincts of theory, the price variable isousted from its dominant position. However, it is still competition within arigid pattern of invariant conditions, methods of production and forms ofindustrial organization in particular, that practically monopolizes attention.But in capitalist reality as distinguished from its textbook picture, it is not thatkind of competition which counts but the competition from the newcommodity, the new technology, the new source of supply, the new type oforganization (the largest-scale unit of control for instance) - competitionwhich commands a decisive cost or quality advantage and which strikes notat the margins of profits and the outputs of the existing firms but at theirfoundations and their very lives ... a theoretical construction which neglectsthis essential element ... is like Hamlet without the Danish prince. (tbid., 84-86).

Left wing Keynesian such as M. Kalecki, N. Kaldor, L. Klein, J.Robinson and J. Strachey, have emphasized the intrinsic tendency towardmonopoly and oligopoly in capitalism. Disequilibrium is caused by a lack ofaggregate demand relative to production capacity and supply, according to thisschool, and this lack of demand is explained by to low real wages. But left wingKeynesianism emphasizes as well that increasing monopolization of markets incontemporary capitalism prevents prices of products to lower as productivityoflabour increases. The context of the low level of real wages and price rigidityin monopolized markets, leads to under-consumption crisis in contemporarycapitalism (c. Deutschmann, 11-12).

Neo-keynesians (cf. J. Cornwall) have criticized the idea of pricecompetition and emphasized the importance of 'stickyness' of prices inreproducing producer-user and firm-customer relations as an important factor

of long run competitiveness of companies. But it is especially what we wouldlike to can 'the social construction' of the present restructuring of capitalaccumulation that they have advocated. The idea here is that industrialrelations and especially the power of the labour movement has to be taken intoaccount in restructuring capitalism as antagonist industrial relations, typicallyin the anglo-saxon countries, delay necessary technological change. Classcollaboration is thought to be one of the main precondition of capitalistrestructuring.

But it is especially neo-schumpeterlans that have worked on the long-run impact of technical change on macro economic performance andcompetitiveness ofindividual capital. Neo-classical theory is rejected as it doesnot have an adequate theory of the diffusion of technological innovations andtechno-economic paradigms that, according to the neo-schumpeterians. Theregulation-school criticizes as wen the neo-classical theory for its lack of atheory of the phases of capitalist development, but emphasizes strongly the roleof socio-economic structures and balance of power of soda-political forces inthe timing of the introduction of new regimes of capital accumulation. It isespecially the concept of hegemony that differs these two schools, but, thetheory of the capitalist state and hegemony in the regulation-theory, as wen asin neo-schumpeterian theories, is inadequate (see Ivar Jonsson 1991).

We have argued elsewhere that the capitalist state, industrial relationsand the specific character of small economies has to be analysed as independentfactors alongside Keynes's rate ofinterests (ibid.). Furthermore, the qualitativenature of technical change and regimes of capital accumulation as analysed inthe neo-schumpeterian and regulation theories have to be taken into account.These are the independent variables that determine the 'structuralcompetitiveness' of individual capital through which the level of output andemployment is determined.

As a consequence, Keynes's model of the determinants of output andemployment needs to be extended on the grounds of the variables which wehave just mentioned. We have developed a model based on an extendedproblematic as shown in figure 3. There are three main sets of independentvariables in the model. The independent variables in the model range fromstructural variables to collective variables and individual variables, while thedependent variables are structural competitiveness, level of employment andoutput.

The causality in this model is dialectical in the sense that, on the oneside, the structural variables are historical conditions, both in the sense on theone side of the phases of capitalist development and the conjunctural conditionsspecific to the location of capital accumulation of individual capital. and on

Figure 3. The Determinants of 'structural Competitiveness'.

position in theinternationaldivision oflabour

size of theeconomy

stages oftechnological,development

technical andorganic compo-sition of capital& structure ofthe labourmarket

forms ofreproductionof labour

organizedbargainingof wages andtraining andand natureof skills andforms ofcontracts

forms ofhouseholds,civil societyrelations,organizedconsumerinterests andstandards ofconsumption

Monopolization; price de-centralization terminationand concentrat-ion of capital

power relationsbetween labourand capital andsocial and pol-itical forces

hegemonicpolitics:nature ofpower bloc,strategies oforgainzedeconomic,social andpolitical

labourprocessesof individualcapital andbargainingof wages andforms ofcontracts

nature ofdemand andmarketspecializationof firms

price de-termination

level of rankand fileacceptance ofthe policiesof organizedinterests andindividualactivities

strategic structuralsituation of competi-the investor tiveness

employmentand output

intereststowards eachother andthe state

industrialrelations

organizedina. rel.statistic ornon-statistic

intra-finnstrategiesof ind, rel.

the state accumulational strategies:monetary,fiscal, indust-rial, science!

tech, policy,strategies ofinterestmediation

policy nuxof differentgovernments

the other side in the sense that the 'actions' of collective and individualvariables to some extent and in a non- determinist way, do affect the structuralvariables in the long run. But the structural variables determine the frameworkwithin which short term actions of the actors of the model move and thepotential forms they take; i.e. it is a question of the dialectics of the'structurization' of the material conditions of conjunctural capital accumulation ..

h) ConclusionIn this article we have analysed Keynes's critique of neo-classical theory ofemployment and output. Instead ofrejecting his general theory of employment,interest and money, we have argued that it is incomplete and indeed not as'general' a theory of employment and output as he presumes. AlthoughKeynesis right in that output and employment can be increased by affecting theschedule of marginal efficiency of capital through interests and monetarymeasures, he fails in his analysis of the long term determination of the scheduleof marginal efficiency of capital and strategic situation of investors and/oreconomic actors. His theory fails in terms of being a general theory ofemployment, interest and money as it does not explain the different role of thegiven factors in determining the schedule of marginal efficiency of capital indifferent periods - and hence the different effectiveness of his interest andmonetary based policies in different periods.

Finally we have sketched the main factors needed for a general theoryin the above sense in our mode! of the determinants ofstructuralcompetitiveness

114~115

and hence output and employment (see Ivar Jonsson 1991 for further analysisof structural development, especially with reference to small states andmicrostates) .

capital in the post-war era. See ego E. A. Brett: The World Economy since theWar.

Notes:1 Marx describes the emergence of real abstract social and economic relations in

the Introduction to his Grundrisse according to which real abstract socialrelations develop as a consequence of the emergence of the purest forms ofmarket relations. Marx takes labour as an example of real abstract socialrelation: "As a rule, the most general abstractions arise only in the midst of therichest possible concrete development, where one thing appears as common tomany, to all. Then it ceases to be thinkable in a particular form alone. On theother side, this abstraction of labour as such is not merely the mental product ofa concrete totality oflabours, Indifference towards specific labours correspondsto a form of society in which individuals can with ease transfer from one labourto another, and where the specific kind is a matter of chance for them, hence ofindifference. Not only the category, labour, but labour in reality has herebecome the means of creating wealth in general, and has ceased to beorganically linked with particular individuals in any specific form. Such a stateof affairs is at its most developed in the most modem form of existence ofbourgeois society - in the United States. Here, then, for the first time, the pointof departure of modern economics, namely the abstraction of the category'labour', 'labour as such', labour pure and simple, becomes true in practice. Thesimplest abstraction, then, which modern economics places at the head of itsdiscussions, and which expresses an immeasurably ancient relation valid in allforms of society, nevertheless achieves practical truth as an abstraction only as acategory of the most modem society." K. Marx 1974, 104-5.

2 P. Garegnani has shown that Keynes's 'classical school' refers to the neo-classical economists Marshall, Edgeworth and Pigiou and that Keynes wronglypresumed that Ricardo based his theory on the notion of price elasticity offactors. While such a theory was developed by the neo-classical school, Ricardodid not develop such a theory. P. Garegnani: Notes on Consumption ... p. 24-28.

3 i.e. the desire to hold wealth in the form of cash.<4 Keynes based his theory of the relationship between the level of income and the

propensity to consume on a mysticism of "human nature" which he presumedwas so constituted that it prevented people from consuming more/less as theirincome increased/decreased; i.e, he based it on his own protestant ethic cf MaxWeber.

5 Keynes did deal with problems of uneven exchange in international trade in thepost second world war em, but there his naive view of the state was transformedinto a even more naive idea of a possibility of a supra-international-state thatwould equalize international trade. But his dreams of a progressive role of theIMP and the World Bank never came true because of the superior power of US

BibliographyE. S. Andersen/ B.-A. Lundvall: 'Small National Systems of Innovation facing

Tecchnological Revolutions: An Analytical Framework' in C. Freeman/B.A.1988.

R. Boyer: 'The Influence of Keynes on French Economic Policy: Past and Present'Wattel1985.

E. A. Brett: The WOi"IdEconomy since the War; Macmillan; London 1985.J. Cornwall: The Conditions far Economic Recovery; Oxford 1983.C. Deutschmann: Venstrekeynesianismen; Modtrvk; Aarhus 1976.V. Droucopoulos: 'The Non American Challenge' ... in Capital and Class 14{1981J. Eatwell and M. Milgate (ed.): Keynes's Economics and the Theory of Value and Distribution;

Distribution; Duckworth London X 983.C. Freeman/Be-A. Lundvall: Small Countries Facing the TechnologicalRe'volu!ion; FrancesPinter; London 1988.

P. Garegnani: 'Notes on consumption, investment and effective demand' in J. Eatwell andM. Milgate (ed.) 1983.

H. Grossmann: Marx. den klassiske nationalokonomi og dynamikken; Forlaget Rhodos;Copenhagen 1975.

J. Hirsch: 'Auf dem 'lXlege zum Post-Fordismus' in Das Argument 1985.Ivar jonsson: Contemporary Theories of Neo-Carparatism; A Thematic Discussion of Paradigms;

M.A.-Dissertation; University of Essex 1984.Ivar J6nsson: 'Hegemonic Politics and Capitalist Restructuring' in Pj6lJm41; National

Institute of Social and Economic Research; Reykjavik 1989.Ivar [onsson: 'Hegemonic Politics and Accumulation Strategies in iceland 1945-

1990'; Long Waves in the WarldEconomy, Regimes of Accumulation and UnevenDevelopment. Small States, MicrosUltes and Problems ofV?orld Market Adjustment; Ph.D.-disseration; University of Sussex 1991.

J. M. Keynes: The General Theory of Employment, Interest and Money; Macmillan; London1983.

K. Marx: Grundrisse; Penguin; Harmondsworth 1974.H. Mattfeldt:' Kevnestanismus, Monetarismus un Demokraue' in Das Argument 151/1985.L. Panitch: 'The Develeopment of Corporatism in Liberal Democracies' in P.c. Schmitter/