kimco’s 2020 vision - jefferies.com1).pdf · perception vs. reality: case for kimco 6 mall...

TRANSCRIPT

Jefferies 2017 Global Consumer Conference

KIMCO’S 2020 VISION

The statements in this presentation, including targets and assumptions, state

the Company’s and management’s hopes, intentions, beliefs, expectations or

projections of the future and are forward-looking statements. It is important to

note that the Company’s actual results could differ materially from those

projected in such forward-looking statements. Factors that could cause actual

results to differ materially from current expectations include the key

assumptions contained within this presentation, general economic conditions,

local real estate conditions, increases in interest rates, foreign currency

exchange rates, increases in operating costs and real estate taxes. Additional

information concerning factors that could cause actual results to differ

materially from those forward-looking statements is contained from time to

time in the Company’s SEC filings, including but not limited to the Company’s

Annual Report on Form 10-K. Copies of each filing may be obtained from

http://investors.kimcorealty.com/ or the SEC.

SAFE HARBOR

Suburban Square, Philadelphia, PA Cover: Corsica Square, Miami, FL

10.7%

9.7%

$0.64$0.72 $0.76

$0.84$0.90

$0.96$1.02

1958 – Founded by Milton Cooper & Marty Kimmel

1991 – IPO that launched the “Modern REIT Era”

2006 – Named to the S&P 500 Index

• 517 U.S. properties totaling 84M square feet in 34 states and Puerto Rico

• Total Enterprise Value – $15.5 billion

KIMCO’S HISTORYTSR Since IPO* Dividend Growth

KIM

DJIA

S&P 500

12.0%

11/29/91 – 3/31/17

2010 2011 2012 2013 2014 2015 2016

Information as of 3/31/2017* Source: Bloomberg** Quarterly dividend annualized

4

2017

$1.08*$1.08**

4

KIMCO’S 2020 VISION

High-quality assets, tightly clustered in major metro markets that provide multiple growth levers

Increase net asset value (NAV) through redevelopment, select ground-up development and active investment management

Maintain a strong balance sheet and financial flexibility, on a path to A-/ A3 credit rating

PORTFOLIO QUALITY

NAV CREATION

FINANCIAL STRENGTH

3

Westlake Shopping Center, Daly City, CA

PERCEPTION VS. REALITY: CASE FOR KIMCO

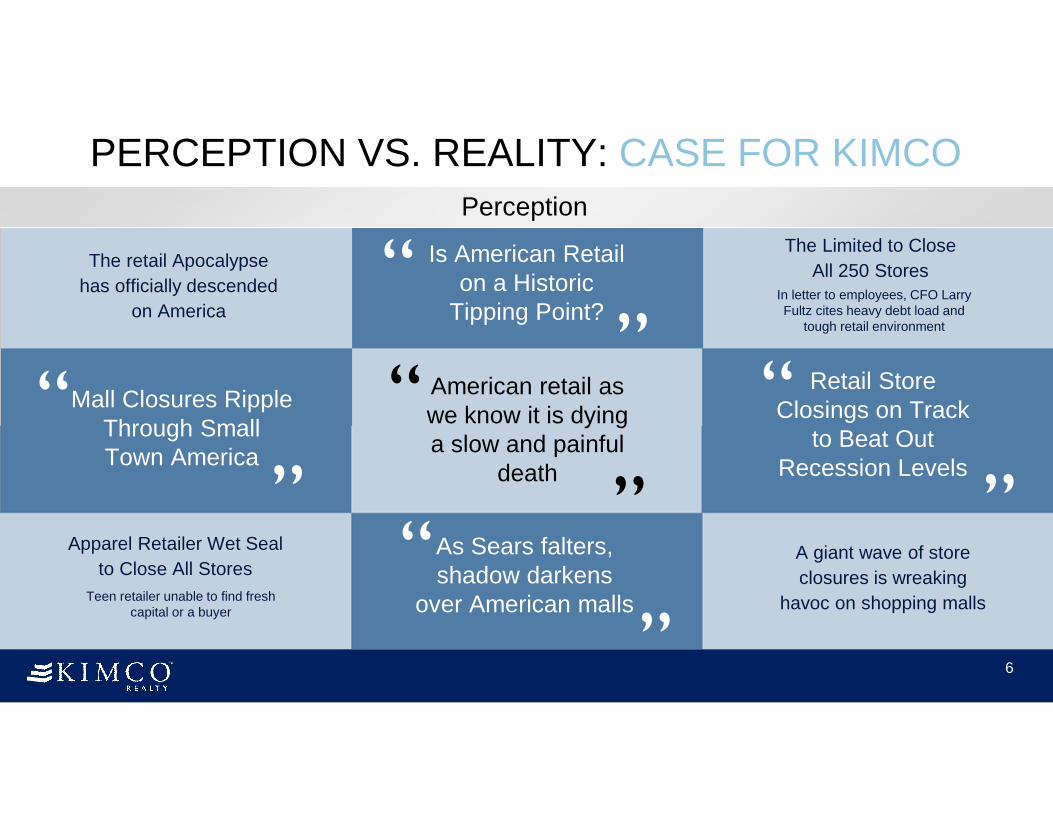

PERCEPTION VS. REALITY: CASE FOR KIMCO

6

Mall Closures Ripple Through Small Town America

“”

Retail Store Closings on Track

to Beat Out Recession Levels

“

”As Sears falters, shadow darkens

over American malls

”“

Is American Retail on a Historic

Tipping Point?“

”

Perception

The Limited to Close

All 250 StoresIn letter to employees, CFO Larry Fultz cites heavy debt load and

tough retail environment

A giant wave of store

closures is wreaking

havoc on shopping malls

Apparel Retailer Wet Seal

to Close All Stores

Teen retailer unable to find fresh capital or a buyer

The retail Apocalypse

has officially descended

on America

American retail as we know it is dying a slow and painful

death

“

”

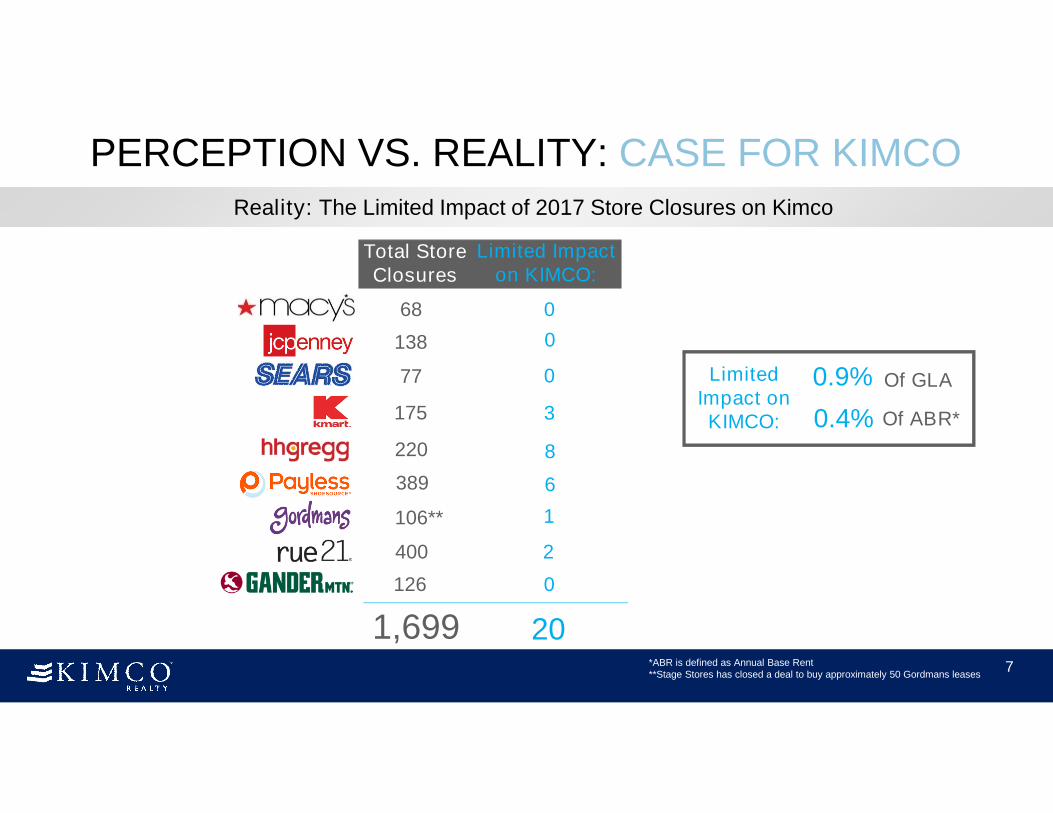

Reality: The Limited Impact of 2017 Store Closures on Kimco

7”1,699

Limited Impact on KIMCO:

20

0.9% Of GLA

0.4% Of ABR*

68 0

138

77

3

8

6

175

220

389

PERCEPTION VS. REALITY: CASE FOR KIMCO

Total Store Closures

0

0 Limited Impact on KIMCO:

*ABR is defined as Annual Base Rent**Stage Stores has closed a deal to buy approximately 50 Gordmans leases

1

2

0126

400

106**

And more…

Reality: Many Retailers are Growing Their Store Count

8

PERCEPTION VS. REALITY: CASE FOR KIMCO

Source: CoStar, Cushman & Wakefield and Peer Reporting

Fitness

Traffic-Drivers

Grocers

Restaurants

Off-Price

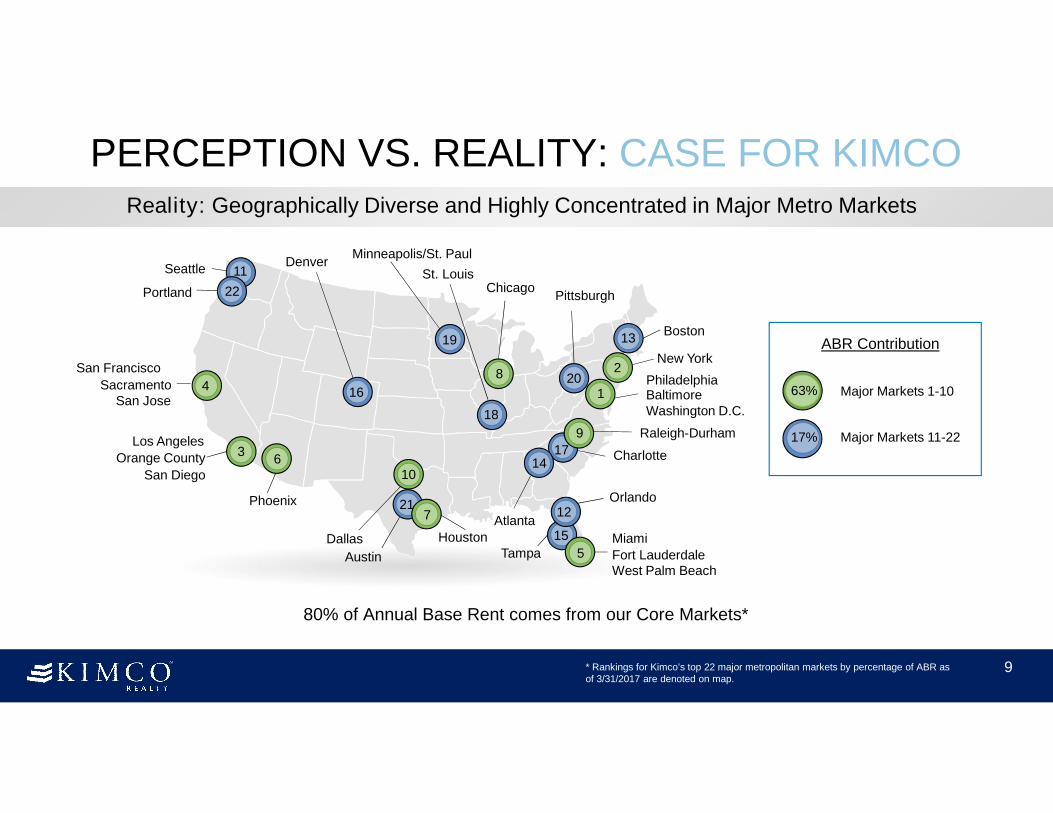

Reality: Geographically Diverse and Highly Concentrated in Major Metro Markets

9* Rankings for Kimco’s top 22 major metropolitan markets by percentage of ABR as of 3/31/2017 are denoted on map.

Seattle

Portland

San Francisco

SacramentoSan Jose

Los Angeles

Orange County

San Diego

Phoenix

DenverMinneapolis/St. Paul

St. LouisChicago

Dallas

Austin

Pittsburgh

HoustonTampa

Atlanta

Miami

Fort LauderdaleWest Palm Beach

Orlando

Charlotte

Boston

New York

PhiladelphiaBaltimoreWashington D.C.

Raleigh-Durham

1

3

5

13

15

202

4

11

12

22

14

16

17

19

21

6

8

7

10

9

80% of Annual Base Rent comes from our Core Markets*

PERCEPTION VS. REALITY: CASE FOR KIMCO

18

Major Markets 11-2217%

63% Major Markets 1-10

ABR Contribution

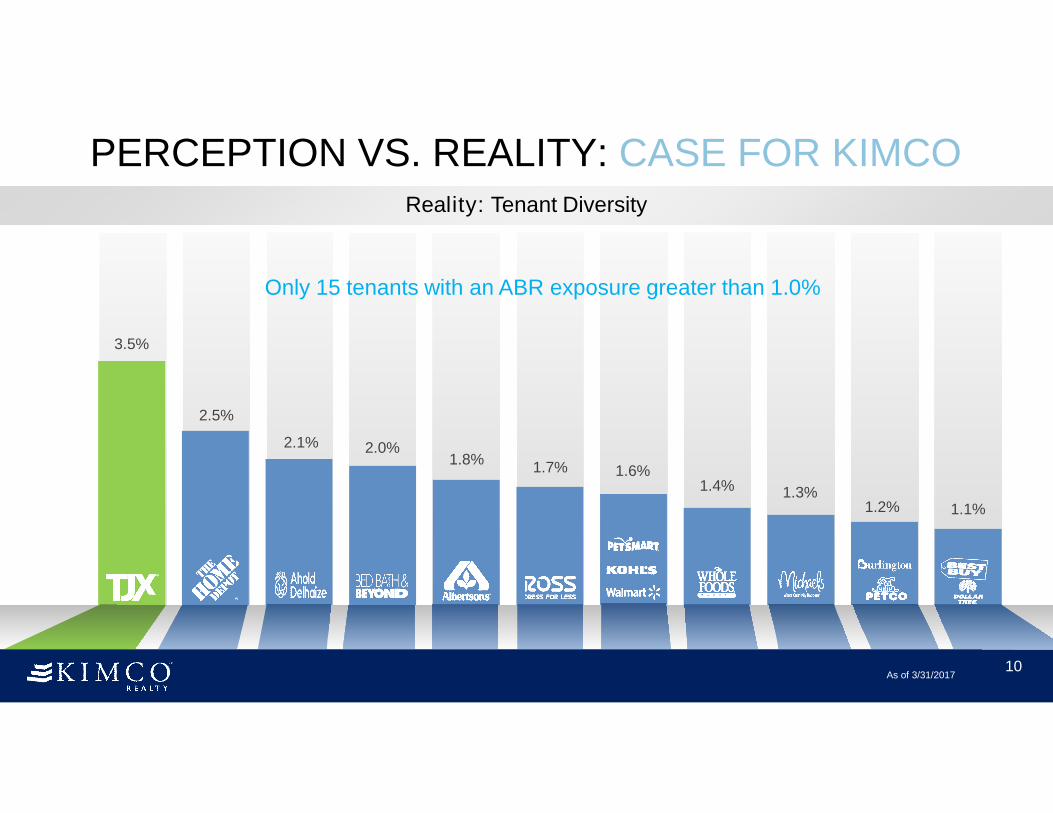

3.5%

2.5%

2.1% 2.0%1.8%

1.7% 1.6%1.4% 1.3%

1.2% 1.1%

As of 3/31/2017

Reality: Tenant Diversity

Only 15 tenants with an ABR exposure greater than 1.0%

10

PERCEPTION VS. REALITY: CASE FOR KIMCO

As of 3/31/2017*excluding options

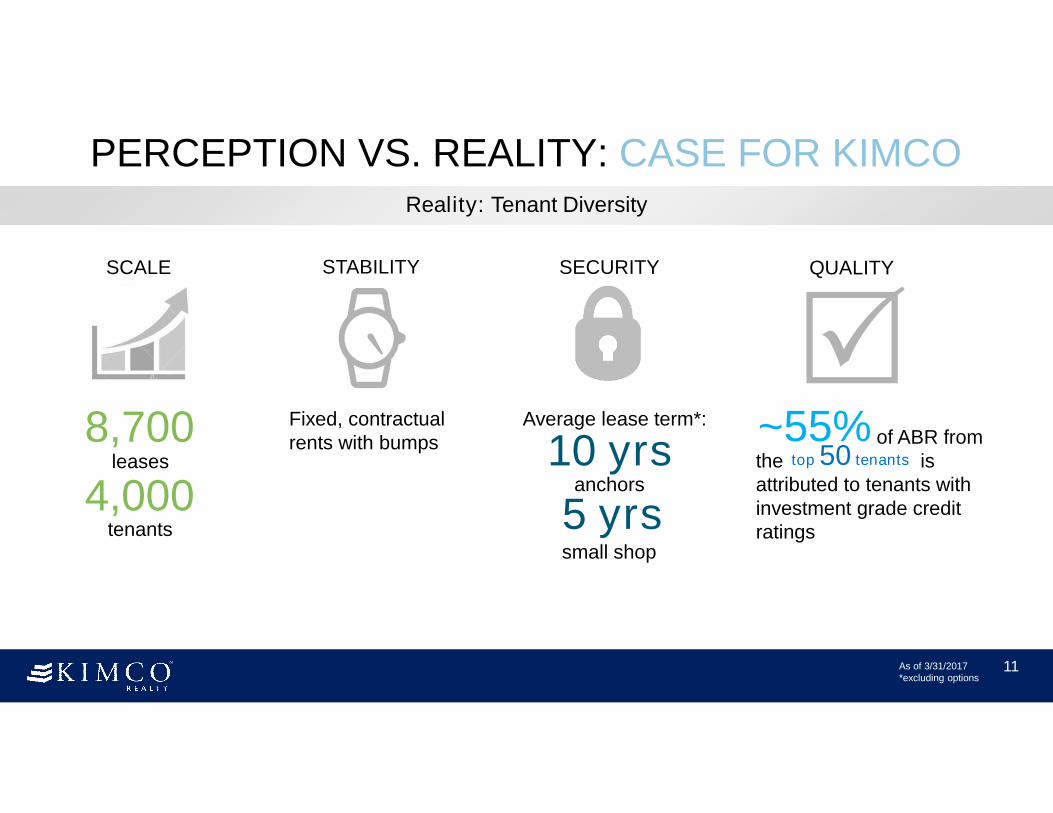

Reality: Tenant Diversity

11

PERCEPTION VS. REALITY: CASE FOR KIMCO

8,700

4,000leases

tenants

SCALE

Average lease term*:

10 yrsanchors

5 yrssmall shop

of ABR from the is attributed to tenants with investment grade credit ratings

QUALITY

top 50 tenants

~55%

STABILITY

Fixed, contractual rents with bumps

SECURITY

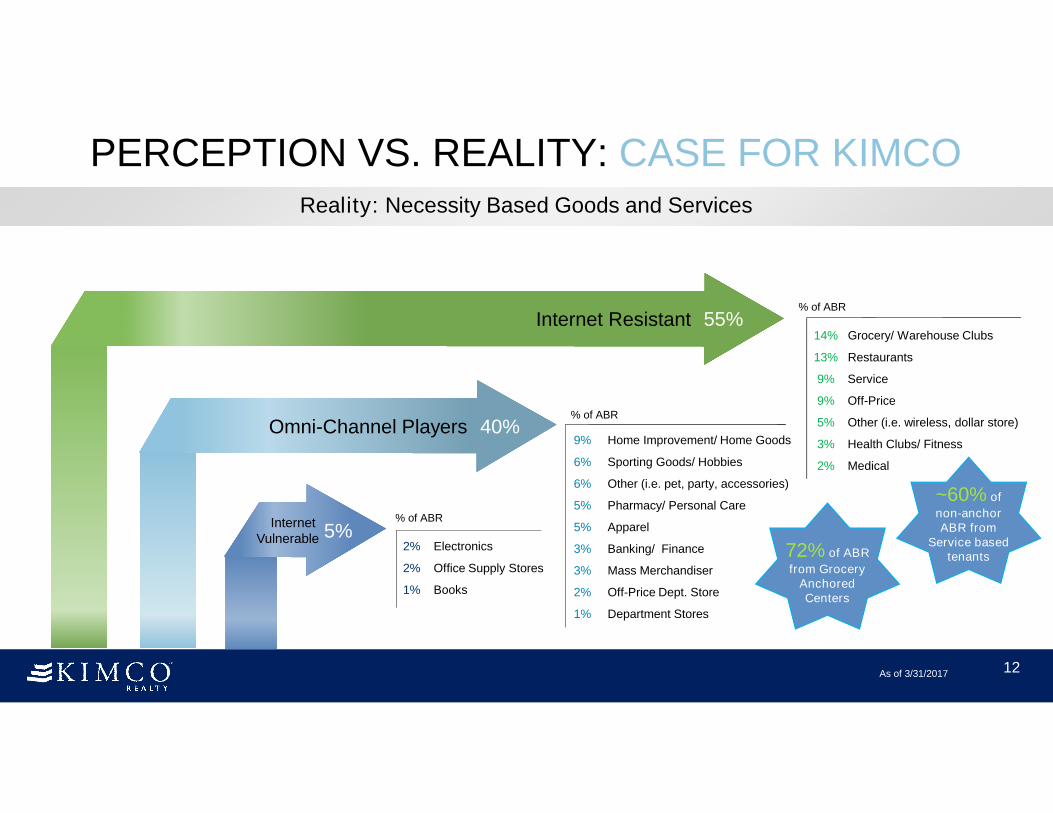

Reality: Necessity Based Goods and Services

12

14% Grocery/ Warehouse Clubs

13% Restaurants

9% Service

9% Off-Price

5% Other (i.e. wireless, dollar store)

3% Health Clubs/ Fitness

2% Medical

Internet Resistant 55%% of ABR

Omni-Channel Players 40%

Internet Vulnerable 5%

9% Home Improvement/ Home Goods

6% Sporting Goods/ Hobbies

6% Other (i.e. pet, party, accessories)

5% Pharmacy/ Personal Care

5% Apparel

3% Banking/ Finance

3% Mass Merchandiser

2% Off-Price Dept. Store

1% Department Stores

2% Electronics

2% Office Supply Stores

1% Books

% of ABR

% of ABR

72% of ABR

from Grocery Anchored Centers

As of 3/31/2017

PERCEPTION VS. REALITY: CASE FOR KIMCO

~60% of

non-anchor ABR from

Service based tenants

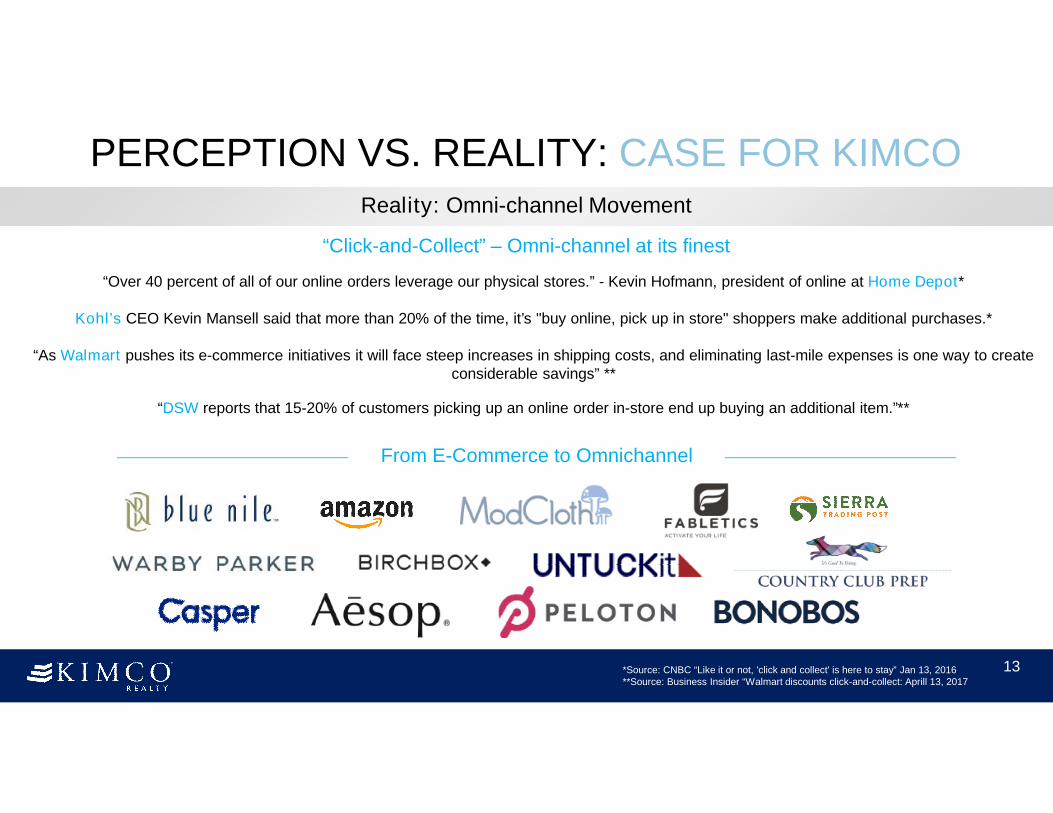

Reality: Omni-channel Movement

13

“Click-and-Collect” – Omni-channel at its finest

From E-Commerce to Omnichannel

“Over 40 percent of all of our online orders leverage our physical stores.” - Kevin Hofmann, president of online at Home Depot*

Kohl’s CEO Kevin Mansell said that more than 20% of the time, it’s "buy online, pick up in store" shoppers make additional purchases.*

“As Walmart pushes its e-commerce initiatives it will face steep increases in shipping costs, and eliminating last-mile expenses is one way to create considerable savings” **

“DSW reports that 15-20% of customers picking up an online order in-store end up buying an additional item.”**

*Source: CNBC “Like it or not, 'click and collect' is here to stay” Jan 13, 2016**Source: Business Insider “Walmart discounts click-and-collect: Aprill 13, 2017

PERCEPTION VS. REALITY: CASE FOR KIMCO

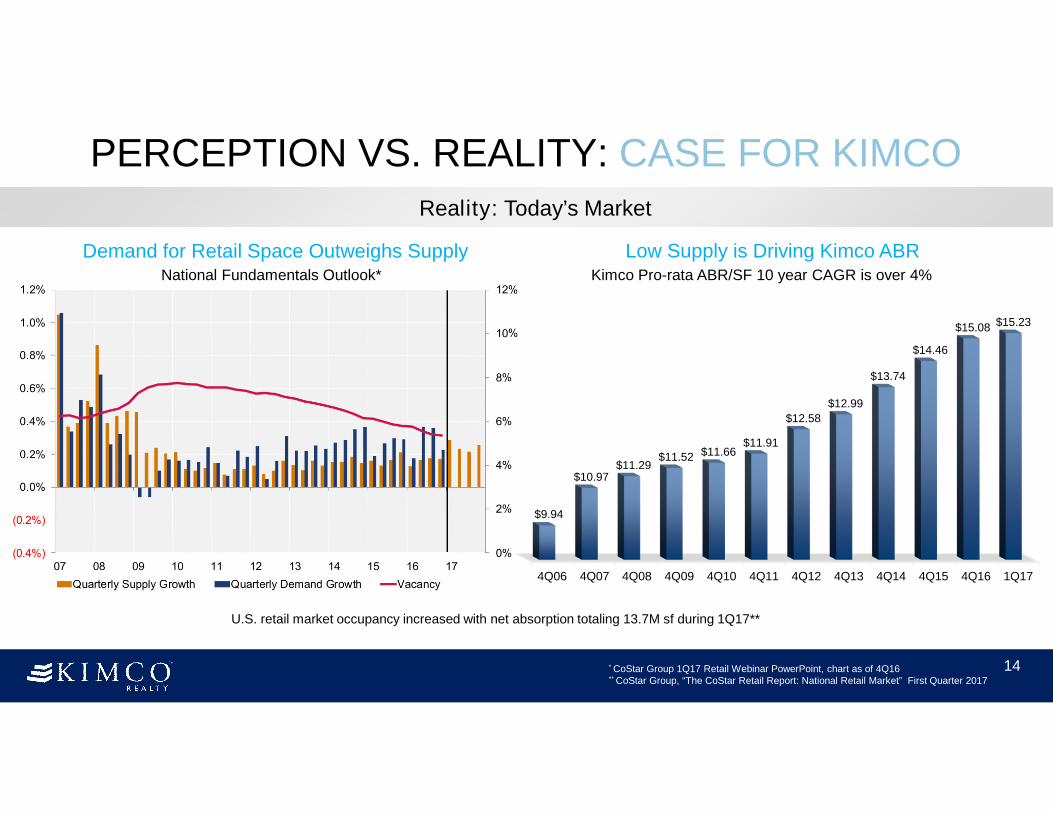

Reality: Today’s Market

* CoStar Group 1Q17 Retail Webinar PowerPoint, chart as of 4Q16** CoStar Group, “The CoStar Retail Report: National Retail Market” First Quarter 2017

Demand for Retail Space Outweighs Supply Low Supply is Driving Kimco ABR

14

Kimco Pro-rata ABR/SF 10 year CAGR is over 4%

4Q06 4Q07 4Q08 4Q09 4Q10 4Q11 4Q12 4Q13 4Q14 4Q15 4Q16 1Q17

$9.94

$10.97 $11.29

$11.52 $11.66 $11.91

$12.58

$12.99

$13.74

$14.46

$15.08 $15.23

National Fundamentals Outlook*

U.S. retail market occupancy increased with net absorption totaling 13.7M sf during 1Q17**

PERCEPTION VS. REALITY: CASE FOR KIMCO

1.1%

2.5%

3.8%

3.3%

3.1%

3.6%

27.8%

15.6%

19.5%

25.0%

Multi-Year Highs and Continued Growth in Operating Metrics

PORTFOLIO QUALITY

16

Annual New Leasing Spreads

2016

2015

2014

2013

2012

2011

2016

2015

2014

2013

2012

2011

29.3%

Annual Same Property NOI Growth

2.8%

All figures are at Kimco’s share

$14.46

$13.74

$12.99

$12.58

$11.91$11.96

$12.66

$13.18

$14.00

$14.67

Rent Per Square Foot

$15.231Q17

1Q16

1Q15

1Q14

1Q13

1Q12

92.8%

93.7%

94.7%

95.7%

95.8%

1Q17

1Q16

1Q15

1Q14

1Q13

1Q12

95.3%Occupancy

PORTFOLIO QUALITYQuality Leads to Multiple Growth Levers

NOI Growth Walk Through 2020

85 -110 bps

100 -150 bps

110 -160 bps

140 -165 bps

435 -585 bps

Ground-Up Development

Targeted Annual Growth

RateRedevelopment

Leasing & Value Creation

Organic Growth(Rent Bumps)

17

$14.12

$15.41 $15.74

$10.14

$10.70

$12.00

$9

$11

$13

$15

$17

2013-2015A 2016A 2016-2020E

PORTFOLIO QUALITYGrowth through Leasing & Value Creation

21

Anchor Lease Spreads/Mark To Market

Mark to Market Spread on Anchor Leases: +62%

118 Naked Leases* expiring through 2020 totaling 2.1M sf

3 Kmart Leases expiring through 2020: 316% market upside

Total Average RPSF up 33% since 2010

New Rent Expiring Rent Projected Rent

$A

BR

/SF

* Naked Leases are defined as leases with no remaining options

+31.1%

+44.0%

+39.3%

Strongest Leasing Volume in the Past 10Years; 497 leases signed in 1Q17

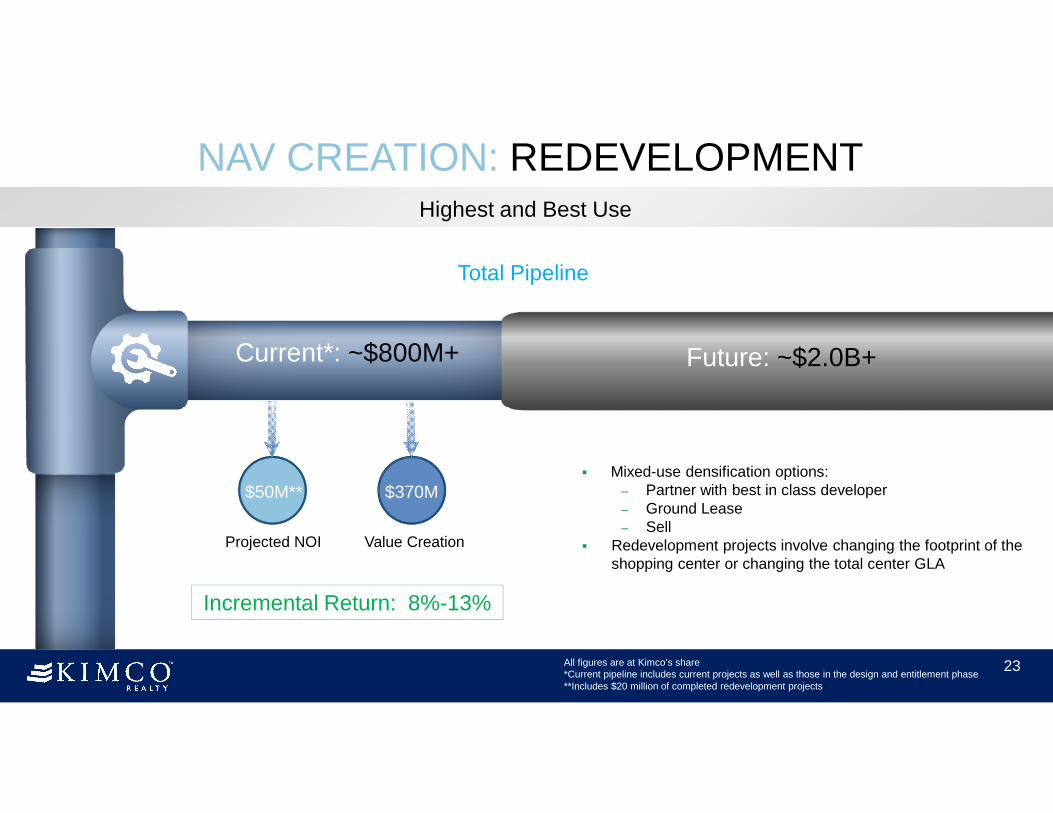

NAV CREATION: REDEVELOPMENTHighest and Best Use

23

Total Pipeline

Future: ~$2.0B+ Current*: ~$800M+

Mixed-use densification options: – Partner with best in class developer– Ground Lease– Sell

Redevelopment projects involve changing the footprint of the shopping center or changing the total center GLA

$370M

Value Creation

$50M**

Projected NOI

All figures are at Kimco’s share*Current pipeline includes current projects as well as those in the design and entitlement phase**Includes $20 million of completed redevelopment projects

Incremental Return: 8%-13%

NAV CREATIONGrowth through Selective Ground-up Development

25

Pipeline

$674MCurrent

Dania Pointe, Dania Beach, FL

Development Approach

Retailer demand-driven

Building additional concentration

Build to own

Risk Management

~75% Pre-leased to build

Phased construction

Experienced team

Projected ROIC 7%-9%

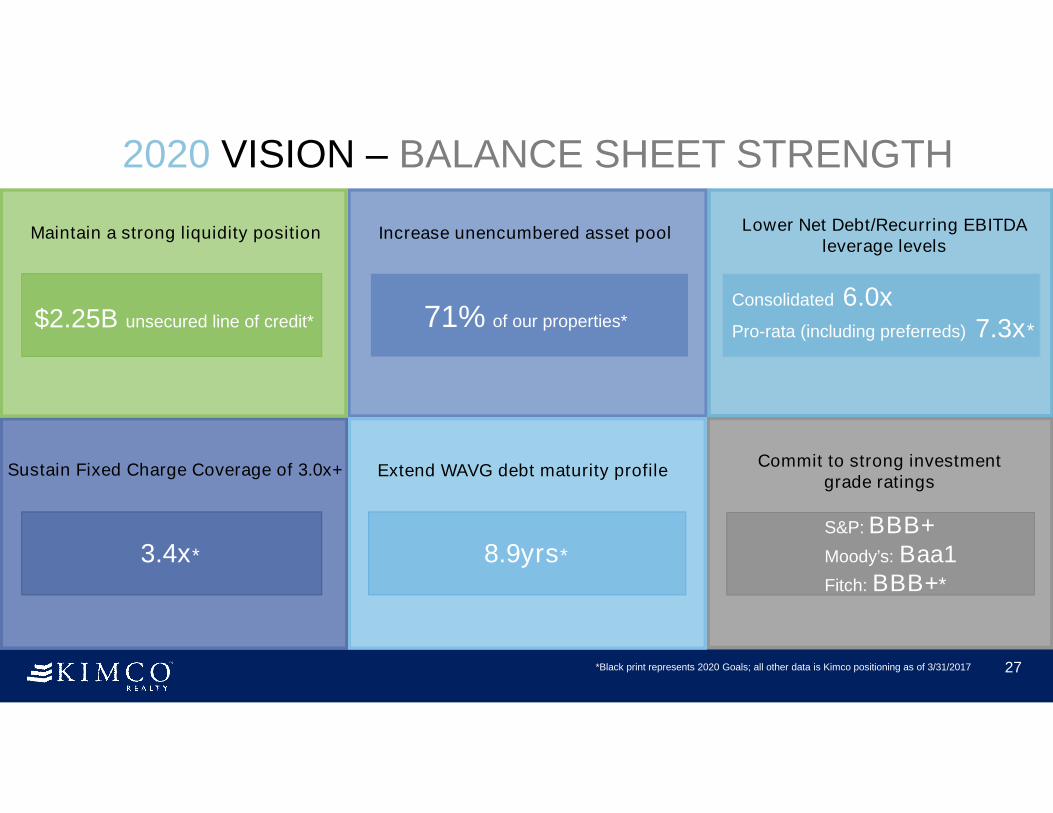

2020 VISION – BALANCE SHEET STRENGTH

Lower Net Debt/Recurring EBITDA leverage levels

Sustain Fixed Charge Coverage of 3.0x+

27

Maintain a strong liquidity position Increase unencumbered asset pool

Extend WAVG debt maturity profileCommit to strong investment

grade ratings

*Black print represents 2020 Goals; all other data is Kimco positioning as of 3/31/2017

$2.25B unsecured line of credit* 71% of our properties*Consolidated 6.0xPro-rata (including preferreds) 7.3x*

3.4x*

S&P: BBB+Moody’s: Baa1 Fitch: BBB+*

8.9yrs*

KIMCO IN SUMMARY2020 VISION

High-quality assets in major metro markets

Solid demographics and operational metrics

Unmatched diversity in geography and tenant base

Growth embedded in portfolio through leasing and redevelopment/ value

creation

Strong balance sheet and related credit ratings with excellent liquidity

50+ years in retail real estate with deep retailer relationships

19

19