kindly refer to chapter 1 of the …starrygoldservices.com/ican may 2017/know/micoswk1sol.pdfthat...

TRANSCRIPT

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 1

KINDLY REFER TO CHAPTER 1 OF THE COMPREHENSIVE LECTURES

TO READ UP THE TOPIC BEFORE YOU ATTEMPT THE QUESTIONS

BELOW FOR PROPER UNDERSTANDING AS THE TOPIC HAS BEEN

DISCUSSED IN THE SAID VIDEO LECTURES. THANKS

ICAN MI (COSTING)

WEEK 1

TOPICS: INTRODUCTION TO COSTING

SUGGESTED SOLUTIONS

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 2

1. ……………. is the expenditure (actual or notional) incurred on or

attributable to a given thing or described as the resources that have been

sacrificed or must be sacrificed to attain a particular objective.

A. Costing

B. Cost

C. Cost centre

D. Cost unit

THE CORRECT ANSWER IS B

2. The term that is used to classifying, recording, allocation and appropriation

of expenses for the determination of cost of products or services and for the

presentation of suitably arranged data for the purpose of control and

guidance of management.

A. Costing

B. Cost

C. Cost centre

D. Cost unit

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 3

THE CORRECT ANSWER IS A

3. …………… primarily deals with collection, analysis of relevant of cost

data for interpretation and presentation for various problems of

management.

A. Costing

B. Cost accountancy

C. Cost accounting

D. Cost technique

THE CORRECT ANSWER IS C

4. …………… is a broader term and is defined as, ‘the application of costing

and cost accounting principles, methods and techniques to the science and

art and practice of cost control and the ascertainment of profitability as well

as presentation of information for the purpose of managerial decision

making.

A. Costing

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 4

B. Cost accountancy

C. Cost accounting

D. Cost technique

THE CORRECT ANSWER IS B

5. One of the following is a feature of cost control

A. Cost control is a continuous process and involves setting standards and

budgets for deciding targets of different expenses and constant comparison of

actual the budgeted and standards.

B. Cost control involves creation of responsibilities centre with clearly

defined authorities and responsibilities.

C. It also involves, timely cost control reports showing the variances between

standard and actual performance.

D. All of the above

THE CORRECT ANSWER IS D

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 5

6. Which of the following is an objective of cost accounting?

A. To indicate to the management any inefficiencies and the extent of various

forms of waste, whether of materials, time, expenses or in the use of machinery,

equipment and tools. Analysis of the causes of unsatisfactory results may

indicate remedial measures.

B. To provide data for periodical profit and loss accounts and balance sheets at

such intervals, e.g., weekly, monthly or quarterly, as may be desired by the

management during the financial year, not only for the whole business but also

by departments or individual products. Also, to explain in detail the exact

reasons for profit or loss revealed in total, in the profit and loss account.

C. To reveal sources of economies in production having regard to methods,

types of equipment, design, output and layout. Daily, weekly, monthly or

quarterly information may be necessary to ensure prompt and constructive

action.

D. All of the above

THE CORRECT ANSWER IS D

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 6

7. Which of the following best explains the major importance of cost

accounting?

A. Cost accounting helps in channelizing production on right lines - proper

costing information makes it possible for the management to distinguish

between profitable and non-profitable activities. Profits can be maximized by

concentrating on profitable operations and eliminating non-profitable ones.

B. Cost accounting eliminates wastages – As cost accounting is concerned with

detailed break-up of costs, it is possible to check various forms of wastages or

losses.

C. Cost accounting makes comparisons possible – Proper maintenance of

costing records provides various costing data for comparisons which in turn

helps the management in formulation of future lines of action.

D. All of the above

THE CORRECT ANSWER IS D

8. The three broad elements of costs include the following

A. Historical, pre-determined and estimated costs

B. Material, labour and expenses

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 7

C. Total, fixed and variable

D. Material, direct and indirect

THE CORRECT ANSWER IS B

9. The major distinguishing feature of fixed and variable cost is that fixed costs

are those costs that remain constant throughout the production period whereas

variable costs are those costs that vary with the level of output.

A. True

B. False

C. Undecided

D. Ambiguous

THE CORRECT ANSWER IS A

10. …………. are costs that contain fixed and variable elements and because of

the variable element, they fluctuate with volume and because of the fixed

element; they do not change in direct proportion to output.

A. Total cost

B. Average cost

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 8

C. Marginal cost

D. Semi-fixed (semi –variable) costs

THE CORRECT ANSWER IS D

11. Functional costs can be simply classified into which of the following

A. Manufacturing / production Costs

B. Administration Cost

C. Selling and distribution cost

D. All of the above

THE CORRECT ANSWER IS D

12. The cost of replacing an asset at current market values is called …………..

A. Conversion cost

B. Controllable cost

C. Uncontrollable cost

D. Replacement cost

THE CORRECT ANSWER IS D

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 9

13. One of the following is a major principle of costing

A. There must be a close relationship between cost and what is being costed

B. Appropriate cost should be charged to cost unit or cost centre that enjoys the

benefits of the cost

C. The conservative convention should be ignored since it emphasizes the

conservative valuation of assets in order to avoid the risk of paying dividends

out of capital

D. All of the above

THE CORRECT ANSWER IS D

14. Which of the following is not among the techniques of costing?

A. Absorption or total costing

B. Marginal costing

C. Standard costing

D. Contract costing

THE CORRECT ANSWER IS D

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 10

15. Which of the following is a process involved in setting up a sound costing

system?

A. Ascertaining the objective of management in installing the system

B. Ascertaining the information required by the management

C. Ascertaining and understanding the technical features of the class of industry

concerned

D. All of the above

THE CORRECT ANSWER IS D

16. A cost that has already been incurred and that cannot be changed by any

decision made now or in the future is called ………….

A. Differential cost

B. Sunk cost

C. Opportunity cost

D. Product cost

THE CORRECT ANSWER IS B

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 11

17. Because of irregular power supply from Power Holding Company of

Nigeria, Ray Power FM leased a 20KV generator from Holt leasing Nigeria

Limited for electricity supply during power failure. The lease agreement calls

for a flat monthly lease payment of N10,000 plus N300 for each hour that the

generator is in operation. During the month of December, the generator set was

operated for cumulative period of 50 hours. Determine the total cost of operating

the generator set in the month of December by Ray Power FM.

A. N15,000

B. N25,000

C. N35,000

D. N45,000

Total fixed cost = N10,000

Total variable cost = No. of operating hrs. X Rate per hr.

= 50 X 300

= N15,000

Total operating cost for the month of December = FC + VC

= N(10,000 + 15,000)

= N25,000

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 12

THE CORRECT ANSWER IS B

18. The major difference between cost accounting and financial accounting is

that ………..

A. Cost accounting information is meant for the use of internal decision makers

of the business while financial accounting information is meant for both the

management and external users

B. Cost accounting is to aid internal decision making in the organization while

financial accounting is to enable management to render accounts of its

stewardships in terms of the profits generated in relation to the assets invested in

the business

C. The primary emphasis of cost accounting is segment reporting while the

focus of financial accounting is on the totality of the business rather than the

individual parts

D. All of the above

THE CORRECT ANSWER IS D

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 13

19. The major difference that exists between sales and variable cost of the sales

can be termed ……….

A. Profit

B. Revenue

C. Contribution

D. Direct cost

THE CORRECT ANSWER IS C

20. A trader buys an article for N6 and then sells it for N10. What is the profit

and contribution of the trader?

A. N2000 / N2500

B. N4000 / N3000

C. N2500 / N2000

D. N3000 / N4000

From the question,

Selling price = N10

Variable cost = N6

By formula, Contribution = Sales – Variable cost

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 14

= N(10 – 6)

= N4

NOTE:

Contribution is the difference between Sales and Variable cost.

Profit = Contribution – fixed cost

That is, Profit is the difference between contribution and fixed cost.

Since the question does not involve fixed cost, then it would be difficult to

compute the profit.

Therefore, Contribution is N4

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 15

THEORY PART

ATTEMPT ALL QUESTIONS

QUESTION 1

What do you understand by Cost Accounting?

By cost accounting, we simply refer to the process of collecting, summarizing,

analyzing and reporting in monetary terms tailor-made information to

management showing the costs and benefits of pursuing each alternative course

of action open to management.

In other words, cost accounting is a broad term used to explain the principles,

methods, techniques and convention which are employed in business for

planning, control, decision making, analysis and evaluation of utilization of the

business resources that is material, facilities and employees.

Discuss the major principles that underline Cost Accounting

For better understanding and appreciation of cost accounting, there is the need to

be aware of some of the basic principles guiding the subject.

The principles are;

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 16

i. There must be a close relationship between cost and what is being

costed

ii. Appropriate cost should be charged to cost unit or cost centre that

enjoys the benefits of the cost

iii. The conservative convention should be ignored since it emphasizes

the conservative valuation of assets in order to avoid the risk of

paying dividends out of capital

iv. Cost accounting aims to provide information on activity of an

organization to assist managers to perform well

v. Past costs should never be charged to future periods because they

can distort future period results and thus misleading the

management.

Distinguish clearly between Costing methods and costing techniques with

relevant examples

By costing methods, we simply refer to the methods of costing which are

purely designed to suit way goods are produced or the way services are

provided. Therefore, costing methods depend upon the nature of production.

Examples are;

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 17

i. Specific order costing which includes job or batch costing and

contract costing

ii. Operation costing such as process or operation costing, joint and

by-products costing and service operation costing.

On the other hand, costing techniques are those designed to suit the manner in

which it is decided to present the information to management. They largely

depend upon the purpose to which the management requires the information.

Examples of costing techniques are absorption or total costing, marginal costing,

standard costing, budget and budgetary control.

What are the major uses of cost accounting? Highlight the major processes

involved in setting up a sound cost system

The major uses of cost accounting include the following;

i. Cost accounting information assists in identifying areas of

wastages and inefficiencies

ii. It also gives explanation about reasons for increase or decrease

in profit

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 18

iii. It also assists in data collection on actual performance and

presenting them against the background of the budget

iv. The system assists in formulation of cost reduction proposal and

it duly follows it up

v. Installation of costing system would lead to effective cost

control

However, the major processes involved in setting up a sound costing system are;

i.Ascertain the objective of management in installing the system

ii.Ascertain the information required by the management

iii.Ascertain and understand the technical features of the class of industry

concerned

iv.Study the expected individual characteristics of the company

v.Select a suitable costing method

vi.Design suitable forms to collect cost data

vii.Design the cost codes

viii.Prepare a cost manual to guide the costing staff in operating the system

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 19

QUESTION 2

Explain controllable and non-controllable cost with relevant examples.

Controllable costs are those which can be influenced by the action of a specified

member of an undertaking. A business organization is usually divided into a

number of responsibility centres and each such centre is headed by an executive.

Controllable costs incurred in a particular responsibility centre can be influenced

by the action of the executive heading that responsibility centre. Direct costs

comprising direct labour, direct materials, direct expenses and some of the

overhead are generally controllable by the top level management.

Non-controllable costs are those which cannot be influenced by the action of a

specified member of an undertaking. For example, expenditure incurred by the

tool room is controllable by the tool room manager but the share of the tool

room expense which is apportioned to the machine shop cannot be controlled by

the machine shop manager. It is only in relation to a particular individual that a

cost may be specified as controllable or not.

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 20

‘Cost centre’ and ‘Cost unit’ are one and the same. Explain your stand

There are significant differences between cost centre and cost unit, hence they

are not one and the same as they connote different meanings and definitions.

CIMA defines Cost Centre as “a production or service, function, activity or item

of equipment whose costs may be attributed to cost units.

A cost centre is the smallest organizational sub-unit for which separate cost

allocation is attempted”.

A cost centre is an individual activity or group of similar activities for which

costs are accumulated. For example in production departments, a machine or

group of machines within a department or a work group is considered as cost

centre.

Any part of an enterprise to which costs can be charged is called as ‘cost centre’.

A cost centre can be :

(i) Geographical i.e. an area such as production department, stores, sales area.

(ii) An item of equipment e.g. a lathe, forklift, truck or delivery vehicle.

(iii) A person e.g. a sales person.

On the other hand, CIMA defines Cost Unit as “a quantitative unit of product or

service in relation to which costs are ascertained”.

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 21

A ‘cost unit’ is a unit of product or unit of service to which costs are ascertained

by means of allocation, apportionment and absorption.

It is a unit of quantity of product, service or time or a combination of these in

relation to which costs are expressed or ascertained. For example, specific job

Write short notes on the following:

Cost: This is the expenditure (actual or notional) incurred on or attributable to a

given thing or described as the resources that have been sacrificed or must be

sacrificed to attain a particular objective.

Costing: This is the term that is used to classifying, recording, allocation and

appropriation of expenses for the determination of cost of products or services

and for the presentation of suitably arranged data for the purpose of control and

guidance of management.

Profit centre: This is defined as, ‘a segment of the business entity by which

both revenues are received and expenses are incurred or controlled’.

Cost sheet: This is a statement of cost showing the total cost of production and

profit or loss from a particular product or service. A Cost Sheet shows the cost

in a systematic manner and element wise.

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 22

Cost control: It implies various actions taken in order to ensure that the cost do

not rise beyond a particular level while cost reduction means reducing the

existing cost of production. It also means keeping the expenses within limits or

control.

Cost reduction: This refers to attempt to reduce the costs. For example, if the

present costs are #1,500 per unit, attempts can be made to reduce it to bring it

down to #1,000 and below.

QUESTION 3

Explain the major difference between avoidable cost and unavoidable cost

Avoidable costs are those costs which under the present conditions need not

have been incurred. In other words, avoidable costs are those costs that that may

not be incurred but avoided by an organization for some specific reasons.

Example: (a) spoilage in excess of normal limit; (b) Unfavourable cost variances

which could have been controlled

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 23

On the other hand, unavoidable costs are the direct opposite of avoidable costs.

They are those costs which under the present conditions must be incurred

irrespective of the objectives of the organization.

How would you differentiate between direct fixed cost and common fixed

cost?

By definition, direct fixed cost can be seen as cost that can be directly traced to

the production cost. It could also mean the cost that is incurred by and solely for

a given product while common fixed cost is a cost that relates to two or more

segments or it is a cost that supports the operation of more than one segment.

Explain the significant relationship between contribution and profit

There exists significant relationship between contribution and profit which can

be stated below;

Profit = Contribution – Fixed cost

Contribution = Profit + Fixed cost

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 24

By implication, there are two ways of looking at Contribution

i. Contribution = Sales – Variable cost

ii. Contribution = Profit + Fixed cost

QUESTION 4

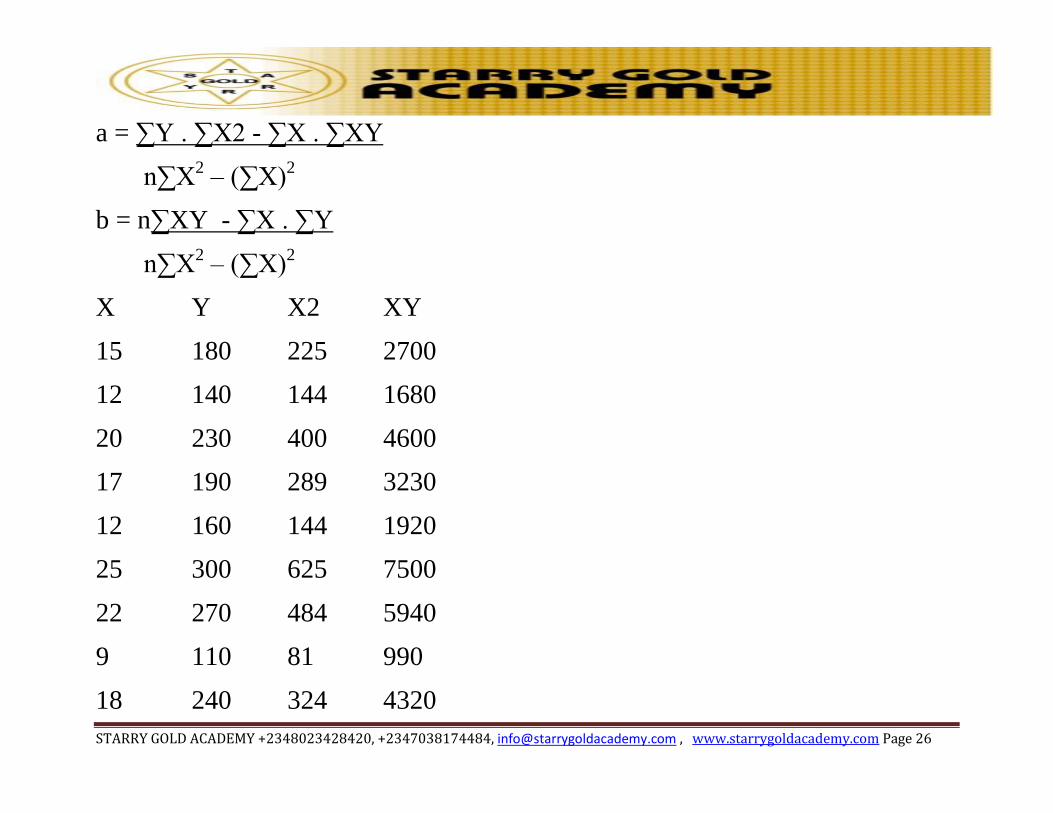

The following cost and activity data were taken from factory records

Activity (Units) Cost incurred (N)

15 180

12 140

20 230

17 190

12 160

25 300

22 270

9 110

18 240

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 25

30 320

Using the least squares method of linear regression, calculate the fixed and

variable elements of cost.

Since the level of Activity is greatly dependent upon the Cost.

Therefore, we can say that Activity is a dependent variable (Y) and Cost is an

independent variable (X)

Given the cost equation;

Y = a + bX

Where;

Y = Activity level

X = Cost incurred

a = fixed cost

b = variable cost

To get fixed cost, a

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 26

a = ∑Y . ∑X2 - ∑X . ∑XY

n∑X2 – (∑X)2

b = n∑XY - ∑X . ∑Y

n∑X2 – (∑X)2

X Y X2 XY

15 180 225 2700

12 140 144 1680

20 230 400 4600

17 190 289 3230

12 160 144 1920

25 300 625 7500

22 270 484 5940

9 110 81 990

18 240 324 4320

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 27

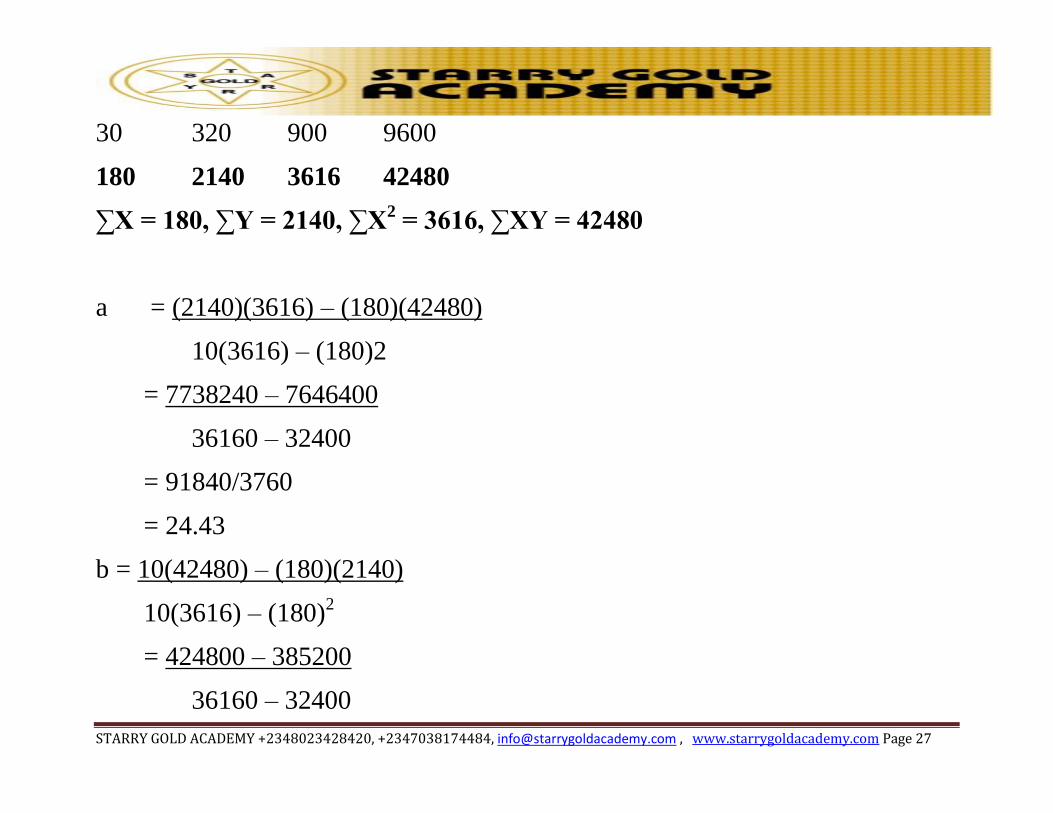

30 320 900 9600

180 2140 3616 42480

∑X = 180, ∑Y = 2140, ∑X2 = 3616, ∑XY = 42480

a = (2140)(3616) – (180)(42480)

10(3616) – (180)2

= 7738240 – 7646400

36160 – 32400

= 91840/3760

= 24.43

b = 10(42480) – (180)(2140)

10(3616) – (180)2

= 424800 – 385200

36160 – 32400

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 28

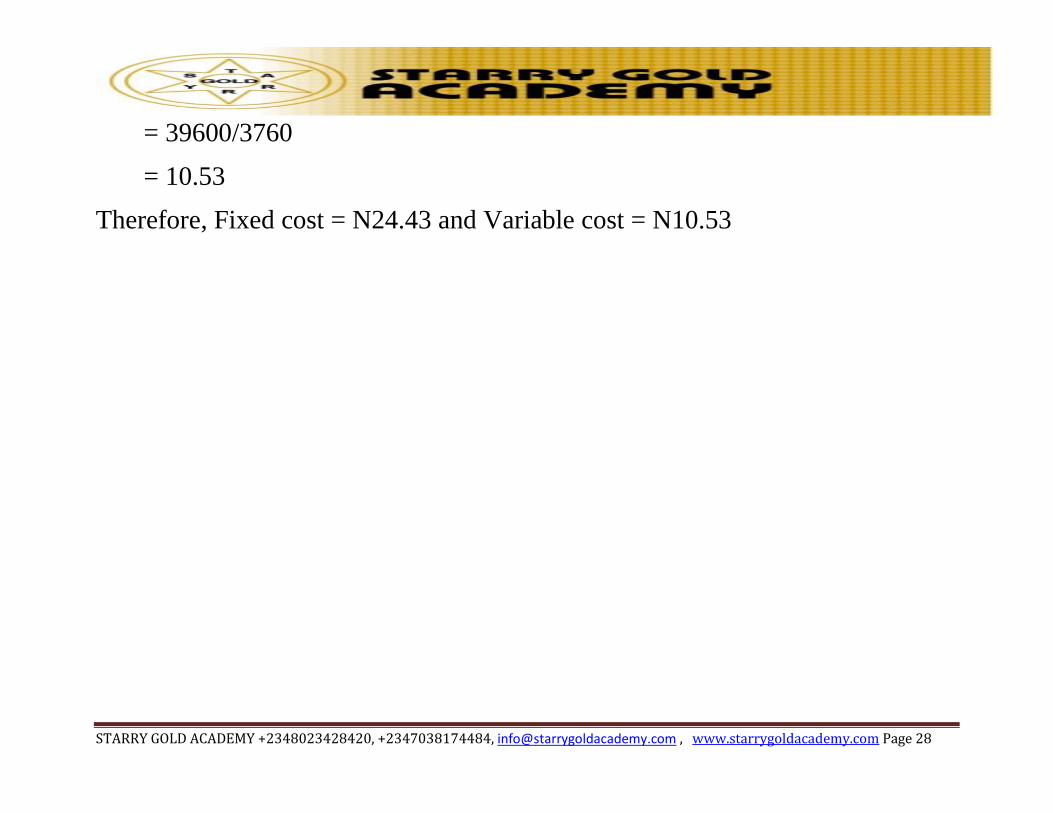

= 39600/3760

= 10.53

Therefore, Fixed cost = N24.43 and Variable cost = N10.53

STARRY GOLD ACADEMY +2348023428420, +2347038174484, [email protected] , www.starrygoldacademy.com Page 29